-

8/6/2019 Brazil 2011 Mining - BMI

1/37

www.datamonitor.comDatamonitor USA

245 Fifth Avenue

4th Floor

New York, NY 10016USA

t: +1 212 686 7400

f: +1 212 686 2626

e: [email protected]

Datamonitor Europe

119 Farringdon Road

London EC1R 3DA

United Kingdom

t: +44 20 7551 9000

f: +44 20 7675 7500

e: [email protected]

Datamonitor Middle East

and North America

Datamonitor

PO Box 24893Dubai, UAE

t: +49 69 9754 4517

f: +49 69 9754 4900

e: datamonitormena@

datamonitor.com

Datamonitor Asia Pacific

Level 46, 2 Park Street

Sydney, NSW 2000

Australia

t: +61 2 8705 6900

f: +61 2 8705 6901

e: [email protected]

Brazil - Metals & Mining 0076 - 2106 - 2009

Datamonitor. This profile is a licensed product and is not to be

photocopied Page 1

INDUSTRY PROFILE

Metals & Mining in

Brazil

Reference Code: 0076-2106

Publication Date: August 2010

-

8/6/2019 Brazil 2011 Mining - BMI

2/37

EXECUTIVE SUMMARY

Brazil - Metals & Mining 0076 - 2106 - 2009

Datamonitor. This profile is a licensed product and is not to be

photocopied Page 2

EXECUTIVE SUMMARY

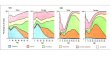

Market value

The Brazilian metals & mining industry shrank by 39.7% in

2009 to reach a value of $36,800.7 million.

Market value forecast

In 2014, the Brazilian metals & mining industry is forecast

to have a value of $60,459.2 million, an

increase of 64.3% since 2009.

Market segmentation I

Iron & Steel is the largest segment of the metals &

mining industry in Brazil, accounting for 77.1% of the

industry's total value.

Market segmentation II

Brazil accounts for 13.8% of the Americas metals & mining

industry value.

Market rivalry

The metals and mining industry was greatly affected by a global

drop in commodity prices in 2009 which

caused a sharp decline in many markets.

-

8/6/2019 Brazil 2011 Mining - BMI

3/37

CONTENTS

Brazil - Metals & Mining 0076 - 2106 - 2009

Datamonitor. This profile is a licensed product and is not to be

photocopied Page 3

TABLE OF CONTENTS

EXECUTIVE SUMMARY 2

MARKET OVERVIEW 6

Market definition 6

Research highlights 7

Market analysis 8

MARKET VALUE 9

MARKET SEGMENTATION I 10

MARKET SEGMENTATION II 11

COMPETITIVE LANDSCAPE 12

LEADING COMPANIES 15

BHP Billiton Group 15

Gerdau S.A. 20

Vale S.A. 25

MARKET FORECASTS 31

Market value forecast 31

MACROECONOMIC INDICATORS 32

APPENDIX 34

Methodology 34

Industry associations 35

Related Datamonitor research 35

Disclaimer 36

ABOUT DATAMONITOR 37

Premium Reports 37

Summary Reports 37

Datamonitor consulting 37

-

8/6/2019 Brazil 2011 Mining - BMI

4/37

CONTENTS

Brazil - Metals & Mining 0076 - 2106 - 2009

Datamonitor. This profile is a licensed product and is not to be

photocopied Page 4

LIST OF TABLES

Table 1: Brazil metals & mining industry value: $ million,

200509 9

Table 2: Brazil metals & mining industry segmentation I:%

share, by value, 2009 10

Table 3: Brazil metals & mining industry segmentation II: %

share, by value, 2009 11

Table 4: BHP Billiton Group: key facts 15

Table 5: BHP Billiton Group: key financials ($) 17

Table 6: BHP Billiton Group: key financial ratios 18

Table 7: Gerdau S.A.: key facts 20

Table 8: Gerdau S.A.: key financials ($) 23

Table 9: Gerdau S.A.: key financials (BRL) 23

Table 10:

Gerdau S.A.: key financial ratios 23

Table 11: Vale S.A.: key facts 25

Table 12: Vale S.A.: key financials ($) 28

Table 13: Vale S.A.: key financials (BRL) 28

Table 14: Vale S.A.: key financial ratios 29

Table 15: Brazil metals & mining industry value forecast: $

million, 200914 31

Table 16: Brazil size of population (million), 200509 32

Table 17: Brazil GDP (constant 2000 prices, $ billion), 200509

32

Table 18: Brazil GDP (current prices, $ billion), 200509 32

Table 19: Brazil inflation, 200509 33

Table 20: Brazil consumer price index (absolute), 200509 33

Table 21: Brazil exchange rate, 200509 33

-

8/6/2019 Brazil 2011 Mining - BMI

5/37

CONTENTS

Brazil - Metals & Mining 0076 - 2106 - 2009

Datamonitor. This profile is a licensed product and is not to be

photocopied Page 5

LIST OF FIGURES

Figure 1: Brazil metals & mining industry value: $ million,

200509 9

Figure 2: Brazil metals & mining industry segmentation I:%

share, by value, 2009 10

Figure 3: Brazil metals & mining industry segmentation II: %

share, by value, 2009 11

Figure 4: BHP Billiton Group: revenues & profitability

18

Figure 5: BHP Billiton Group: assets & liabilities 19

Figure 6: Gerdau S.A.: revenues & profitability 24

Figure 7: Gerdau S.A.: assets & liabilities 24

Figure 8: Vale S.A.: revenues & profitability 29

Figure 9: Vale S.A.: assets & liabilities 30

Figure 10:

Brazil metals & mining industry value forecast: $ million,

200914 31

-

8/6/2019 Brazil 2011 Mining - BMI

6/37

MARKET OVERVIEW

Brazil - Metals & Mining 0076 - 2106 - 2009

Datamonitor. This profile is a licensed product and is not to be

photocopied Page 6

MARKET OVERVIEW

Market definition

The metals & mining industry consists of the aluminum, iron

& steel, precious metals & minerals, coal andbase metal

markets.

In the aluminum market, only production of primary aluminum is

considered. Recycled aluminum is not

included within this report. The market is valued at

manufacturer's selling price (MSP).

The base metals market consists of lead, zinc, copper, nickel

and tin. The market has been valued as

total primary metal production at annual average prices.

The coal market consists of just primary coal (anthracite,

bituminous and lignite). Secondary coal

(metallurgical coke, anthracite and bituminous briquets, and

lignite briquets) is not included in this report.

The market has been valued as total mine production at annual

average minemouth prices and does not

include any transportation costs.

The iron & steel market consists of the production of crude

steel, blast furnace (pig) iron and direct

reduced iron. Market values have been calculated using annual

average steel and iron prices.

The precious metals & minerals market includes gold, silver,

platinum, palladium, rhodium and industrial

and gem-quality diamonds. The market is valued using total

annual mining production volumes and

annual average prices.

For the purposes of this report, the Americas consists of North

America and South America.

North America consists of Canada, Mexico, and the United

States.

South America comprises Argentina, Brazil, Chile, Colombia, and

Venezuela.

-

8/6/2019 Brazil 2011 Mining - BMI

7/37

MARKET OVERVIEW

Brazil - Metals & Mining 0076 - 2106 - 2009

Datamonitor. This profile is a licensed product and is not to be

photocopied Page 7

Research highlights

The Brazilian metals & mining market had total revenue of

$36.8 billion in 2009, representing a compound

annual rate of change (CARC) of -0.8% for the period spanning

2005-2009.

Iron & steel sales proved the most lucrative for the

Brazilian metals & mining market in 2009, with total

revenues of $28.4 billion, equivalent to 77.1% of the market's

overall value.

The performance of the market is forecast to accelerate, with an

anticipated compound annual growth

rate (CAGR) of 10.4% for the five-year period 2009-2014, which

is expected to drive the market to a value

of $60.5 billion by the end of 2014.

-

8/6/2019 Brazil 2011 Mining - BMI

8/37

MARKET OVERVIEW

Brazil - Metals & Mining 0076 - 2106 - 2009

Datamonitor. This profile is a licensed product and is not to be

photocopied Page 8

Market analysis

The Brazilian metals & mining market experienced strong

growth until 2009 when it fell into a steep

decline. Recovery to very strong growth is expected in 2010. The

market is then expected decelerate

throughout the forecast period, experiencing only moderate

growth from 2013.

The Brazilian metals & mining market had total revenue of

$36.8 billion in 2009, representing a compound

annual rate of change (CARC) of -0.8% for the period spanning

2005-2009. In comparison, the US and

Canadian markets declined with CARCs of -2.4% and -0.3%

respectively, over the same period, to reach

respective values of $124.3 billion and $30.6 billion in

2009.

Iron & steel sales proved the most lucrative for the

Brazilian metals & mining market in 2009, with total

revenues of $28.4 billion, equivalent to 77.1% of the market's

overall value. In comparison, sales of

aluminum generated revenues of $3.6 billion in 2009, equating to

9.7% of the market's aggregate

revenues.

The performance of the market is forecast to accelerate, with an

anticipated compound annual growthrate (CAGR) of 10.4% for the

five-year period 2009-2014, which is expected to drive the market

to a value

of $60.5 billion by the end of 2014. Comparatively, the US and

Canadian markets will grow with CAGRs

of 8% and 12.3% respectively, over the same period, to reach

respective values of $182.5 billion and

$54.6 billion in 2014.

-

8/6/2019 Brazil 2011 Mining - BMI

9/37

MARKET VALUE

Brazil - Metals & Mining 0076 - 2106 - 2009

Datamonitor. This profile is a licensed product and is not to be

photocopied Page 9

MARKET VALUE

The Brazilian metals & mining industry shrank by 39.7% in

2009 to reach a value of $36,800.7 million.

The compound annual rate of change of the industry in the period

200509 was -0.8%.

Table 1: Brazil metals & mining industry value: $ million,

200509

Year $ million BRL million million % Growth

2005 37,970.0 76,261.5 27,306.5

2006 37,632.6 75,584.0 27,063.9 (0.9%)

2007 45,354.6 91,093.3 32,617.2 20.5%

2008 61,016.5 122,549.8 43,880.6 34.5%

2009 36,800.7 73,913.2 26,465.6 (39.7%)

CAGR: 200509 (0.8%)

Source: Datamonitor D A T A M O N I T O R

Figure 1: Brazil metals & mining industry value: $ million,

200509

Source: Datamonitor D A T A M O N I T O R

-

8/6/2019 Brazil 2011 Mining - BMI

10/37

MARKET SEGMENTATION I

Brazil - Metals & Mining 0076 - 2106 - 2009

Datamonitor. This profile is a licensed product and is not to be

photocopied Page 10

MARKET SEGMENTATION I

Iron & Steel is the largest segment of the metals &

mining industry in Brazil, accounting for 77.1% of the

industry's total value.

The aluminum segment accounts for a further 9.7% of the

industry.

Table 2: Brazil metals & mining industry segmentation I:%

share, by value, 2009

Category % Share

Iron & Steel 77.1%

Aluminum 9.7%

Base metals 7.3%

Precious metals & minerals 4.7%

Coal 1.2%

Total 100%

Source: Datamonitor D A T A M O N I T O R

Figure 2: Brazil metals & mining industry segmentation I:%

share, by value, 2009

Source: Datamonitor D A T A M O N I T O R

-

8/6/2019 Brazil 2011 Mining - BMI

11/37

MARKET SEGMENTATION II

Brazil - Metals & Mining 0076 - 2106 - 2009

Datamonitor. This profile is a licensed product and is not to be

photocopied Page 11

MARKET SEGMENTATION II

Brazil accounts for 13.8% of the Americas metals & mining

industry value.

The United States accounts for a further 46.6% of the Americas

industry.

Table 3: Brazil metals & mining industry segmentation II: %

share, by value, 2009

Category % Share

United States 46.6%

Brazil 13.8%

Canada 11.5%

Mexico 7.9%

Rest of the Americas 20.2%

Total 100%

Source: Datamonitor D A T A M O N I T O R

Figure 3: Brazil metals & mining industry segmentation II: %

share, by value, 2009

Source: Datamonitor D A T A M O N I T O R

-

8/6/2019 Brazil 2011 Mining - BMI

12/37

COMPETITIVE LANDSCAPE

Brazil - Metals & Mining 0076 - 2106 - 2009

Datamonitor. This profile is a licensed product and is not to be

photocopied Page 12

COMPETITIVE LANDSCAPE

The metals & mining market will be analyzed by taking

companies engaged in primary metal production

and mining as the key players. The key buyers will be taken as

industrial consumers, and producers of

equipment, with suppliers of raw materials being the key

suppliers.

The metals and mining industry was greatly affected by a global

drop in commodity prices in 2009 which

caused a sharp decline in many markets.

Given the centrality of scale economies within the metals and

mining industry there is a continuing

tendency towards concentration. The leading players are large

multinationals who dominate the market.

Buyers come from numerous industries and the industry players

can rely on a relatively large number of

customers. The need to defend margins against rising raw

material prices serves as a driver of vertical

integration, evident in the fact that major steel and aluminum

companies often own their own iron ore and

bauxite mines. Whilst it is possible to enter the industry it

does require a significant outlay as it is essential

to build production facilities. This constitutes a strong entry

barrier and raises exit costs, which tends toincrease rivalry in

the industry. However, large-scale production and high fixed costs,

especially energy,

block many potential new players from entering the industry.

This analysis will centre on steel production, a core component

of the industry. Therefore, industry players

will be taken as steel makers. These companies make products

such as steel rod, wire, and sheets. End

users include companies involved in industries such as the

automotive and construction industries, as

well as stockholders and service centers. In some countries,

there is a tendency for high-volume end-

users to purchase direct, while low-volume customers buy from

stockholders and service centers. This

leads to the typical size of buyers being quite large. However,

steel is so widely used that industry players

can rely on a relatively large number of customers overall,

which reduces buyer power. On the other

hand, steel is commoditized with little to distinguish between

the products of competitors in this industry,boosting buyer power

to an extent. However, players in developed economies - mindful of

the surge in

Chinese capacity - are seeking to differentiate themselves by

focusing on added-value specialty products,

especially when selling in the more mature markets. Most buyers

are unlikely to integrate backwards into

steel making, whereas steel makers are prone to integrate

forwards into certain buyers' businesses, such

as engineered products. Steel manufacturers, for instance, may

sell fabricated items as well as simple

sheets, rods, wire etc. This, as well as the necessity of these

products to the success of the buyers'

business, tends to dilute the power of buyers, which is assessed

as moderate overall.

Suppliers in this industry include producers of mining and

production equipment, IT providers and also

suppliers of raw materials such as the iron ore, coal and coke

needed for the production of steel. Although

some players rely on raw material producers, many are highly

vertically integrated and provide their own

raw material. This strategy helps to decrease a company's

dependence on third-party suppliers and offers

additional revenue stream if raw materials can be sold to other

companies. This potential for backward

integration also weakens supplier power however it does require

significant investment.

-

8/6/2019 Brazil 2011 Mining - BMI

13/37

COMPETITIVE LANDSCAPE

Brazil - Metals & Mining 0076 - 2106 - 2009

Datamonitor. This profile is a licensed product and is not to be

photocopied Page 13

Companies involved only in mining have suppliers in terms of

equipment, IT, labor, and so on, as they are

the providers of raw materials only. However, they must ensure

adequate reserves, as coal and metal

ores are non-renewable. This means that major landowners,

governments, and similar bodies can be

viewed as suppliers, and exert strong power. In general,

supplier power is weakened by the fact that the

metals and mining industry is integral to supplier revenues.

Mining equipment, for example, is so

specialized that manufacturers would find it difficult to sell

to any customer outside the industry. Similarly,

the quality and availability of the raw materials is essential

to the efficient running of the metals and

mining industry. Consequently, concerns about the future

availability and cost of inputs in steel production

could affect the industry dramatically, placing more power in

the hands of suppliers. Overall supplier

power in this industry is moderate.

There is a strong tendency towards integration in the metals and

mining industry. Cross-border mergers

have been taking place for several years with the focus being on

technological improvements and new

products. Through integration, companies tend to strengthen

their position, lower production costs, and

expand towards new markets. To enter the industry and make

ground against incumbents that arecushioned by scale economies it

is necessary to integrate. This trend puts smaller and weaker

companies

out of the industry and lowers the risk of newcomers. The metals

and mining industry faces increasingly

stringent environmental regulations, and companies are under

pressure to develop cleaner and more

efficient technologies. Recent years have seen the punitive

costs for violations of environmental

regulations increase, threatening margins. In fact, they now

include criminal penalties in some

jurisdictions. Governments use a variety of strategies, e.g.

tariffs, subsidies, loans and import restrictions

to ensure that the industry remains competitive domestically. In

many cases, this has allowed the local

industry to continue operations even where better quality,

cheaper commodities could be imported from

another country. Fixed costs in this industry are high as the

main outgoings are transportation and energy

which have both faced increased prices. The Brazilian metals and

mining industry saw a steep decline in

2009 as commodity prices crashed but strong growth is projected

towards 2014. As a result, new entrants

may still be attracted to the market. Overall the threat of new

entrants is assessed as weak.

There are potential substitutes for metal available. Stone or

brick can be used in building construction,

carbon fiber materials may be substitutes for aluminum in

aerospace applications, less common materials

like fiberglass (glass-reinforced plastic) can be especially

advantageous in the automotive industry, where

manufacturers are looking to use lighter materials. The benefits

of this include an improvement in fuel

consumption, there can sometimes be a reduction in manufacturing

costs, and some plastics are as

recyclable as steel. Furthermore, metals such as steel can

corrode whereas reinforced plastic is more

durable. However, not all buyers will replace metals with these

alternatives as they do not provide all of

the same properties and are hardly 'drop-in replacements'. Using

them would require substantial re-

tooling of an assembly line. Thus, although the price of the

alternatives may be favorable in some market

conditions, switching costs are likely to be very high.

Similarly, coal has several substitutes in the power

generation market: oil, gas, nuclear fuels, etc.

-

8/6/2019 Brazil 2011 Mining - BMI

14/37

COMPETITIVE LANDSCAPE

Brazil - Metals & Mining 0076 - 2106 - 2009

Datamonitor. This profile is a licensed product and is not to be

photocopied Page 14

However, while power companies can alter their primary energy

mix to a small extent without incurring

many costs, a thoroughgoing transition to these substitutes

would require investment in different

generation facilities, which constitutes a very high switching

cost. The threat of substitutes overall is

viewed as weak.

The metals and mining industry is concentrated and is

represented by a limited number of large,

multinational players offering similar products and services

within each segment. Metal is a commodity

difficult to diversify strongly, however different customers may

require different specifications (e.g.

consistency in physical properties, variations in strength and

rigidity etc) and producers may tend to

specialize, thereby reducing competition but also limiting the

size of their potential market. Although some

of the players have other businesses and are often

geographically diversified, insulating them from

fluctuations in particular markets, their relative lack of

diversification increases rivalry. The centrality of

scale economies in the metal and coal industry favors larger

companies, which means that deeper

consolidation through mergers and acquisitions is to be

expected, especially in the more fragmented

markets. Exit barriers are high, because many of the major

tangible assets are highly specific to theirindustry, and thus

harder to divest. In this situation, players are strongly motivated

to remain in the

industry even when conditions are difficult, boosting rivalry.

However, this is a cyclical industry, in which

growth cannot always be sustained. Industry margins are

susceptible to changes in raw material and

energy prices. Overall, rivalry is assessed as strong.

-

8/6/2019 Brazil 2011 Mining - BMI

15/37

LEADING COMPANIES

Brazil - Metals & Mining 0076 - 2106 - 2009

Datamonitor. This profile is a licensed product and is not to be

photocopied Page 15

LEADING COMPANIES

BHP Billiton Group

Table 4: BHP Billiton Group: key facts

Head office: 180 Lonsdale Street, Melbourne, Victoria 3000,

AUS

Telephone: 61 1300 554 757

Fax: 61 3 9609 3015

Website: www.bhpbiliton.com

Financial year-end: June

Ticker: BLT, BHP

Stock exchange: London, New York

Source: company website D A T A M O N I T O R

BHP Billiton Group comprises two entities: BHP Billiton Limited

and BHP Billiton Plc. The two entities

exist as separate companies, but operate as a combined company

known as BHP Billiton Group (BHP

Billiton).

BHP Billiton is a diversified natural resources group. The group

exports metallurgical coal for the steel

industry and energy coal. BHP Billiton is engaged in the

production of iron ore, copper, nickel,

manganese ore, primary aluminums, and manganese and chrome

ferroalloys. Furthermore, BHP Billiton

also has substantial interests in oil, gas, liquefied natural

gas (LNG), diamonds, silver, and titanium

minerals. The group has a global presence with more than 100

operations in 25 countries.

BHP Billiton operates nine customer sector groups (CSGs) aligned

with the commodities which it extracts

and markets. They are base metals, petroleum, iron ore, energy

coal, aluminum, stainless steel materials,

metallurgical coal, manganese, and diamonds and specialty

products.

The base metals CSG produces copper, silver, lead, uranium, and

zinc. It provides copper, lead, and zinc

concentrates to smelters worldwide. It sells copper cathodes to

rod and brass mills and casting plants and

uranium oxide to electricity generating utilities, primarily in

Western Europe, North America, and North

Asia. BHP Billiton's key base metals assets include Escondida

copper mine in northern Chile, the Cerro

Colorado copper mine in northern Chile, Spence copper mine in

Chile, Antamina copper mine in Peru, theCannington mine (with

silver, lead, and zinc ores) in Australia, Olympic Dam in South

Australia, and Pinto

Valley in Arizona. In FY2009, BHP Billiton produced 1.2 million

tones of copper.

The petroleum CSG comprises oil and natural gas exploration,

production, and development in Australia,

the US, Algeria, Trinidad and Tobago, Pakistan, and the Gulf of

Mexico.

-

8/6/2019 Brazil 2011 Mining - BMI

16/37

LEADING COMPANIES

Brazil - Metals & Mining 0076 - 2106 - 2009

Datamonitor. This profile is a licensed product and is not to be

photocopied Page 16

It also conducts an international exploration and development

program as well as marketing crude oil,

condensate, liquefied petroleum gases, natural gas, and

liquefied natural gas to customers globally. BHP

Billiton produced 137.19 million barrels of oil equivalent in

FY2009.

The iron ore CSG is one of the leading suppliers of seaborne

iron ore globally. Its operations comprise

Western Australia Iron Ore (WAIO) business and a 50% interest in

the Samarco joint venture with Vale in

Brazil. WAIO's operations involve a complex integrated system of

seven mines and more than 1,000

kilometers of rail and port facilities, all located in the

Pilbara region of northern Western Australia.

BHP Billiton's energy coal CSG produces, markets, and exports

thermal coal (steaming coal). The group

operates three sets of assets: a group of mines and associated

infrastructure collectively known as BHP

Billiton Energy Coal South Africa (BECSA), New Mexico Coal

operations in the US, and Hunter Valley

Energy Coal operations in New South Wales, Australia. BHP

Billiton also owns a one-third share of the

Cerrejon Coal Company, which operates a coal mine in

Colombia.

The aluminum CSG is engaged in the production of aluminum,

bauxite, and alumina. It has four aluminum

smelters in South Africa, Mozambique, and Brazil; and three

alumina refineries and three bauxite mining

operations in Australia, Suriname, and Brazil. BHP Billiton is

one of the largest producers of primary

aluminum. In FY2009, it produced approximately 1.2 million tons

of aluminum, approximately 15 million

tons of bauxite, and 4.4 million tons of alumina.

The stainless steel materials CSG supplies a variety of nickel

products to the global steel industry. In

addition, it also supplies nickel and cobalt to other markets

including the specialty alloy, foundry,

chemicals, and refractory material industries. The segment

produces nickel and cobalt at Yabulu and

Nickle West in Australia and Cerro Matoso in Columbia.

BHP Billiton metallurgical coal CSG is one of the largest global

suppliers of seaborne metallurgical coal. It

primarily produces and markets hard coking coals for the global

steel industry. In addition, it also supplies

a range of other coal qualities. The group owns production

assets in two major resource basins, the

Bowen Basin in Central Queensland, Australia and the Illawarra

region of New South Wales, Australia.

BHP Billiton's manganese operations produce a combination of

ores, alloys, and metal from sites in South

Africa and Australia. The group owns and manages all of its

manganese mining assets and alloy plants

through 60-40 joint ventures with an Anglo-American joint

venture known as Samancor Manganese. The

Samancor Manganese joint venture owns Hotazel Manganese Mines

(HMM) and Metalloys, both situated

in South Africa and the Groote Eylandt Mining Company (GEMCO)

and Tasmanian Electro MetallurgicalCompany (TEMCO) located in

Australia. In July 2009, Samancor sold 26% of HMM in a series

of

transactions designed to comply with South Africa's Black

Economic Empowerment requirements. The

joint venture also owns 51% of the Manganese Metal Company,

which operates a manganese metal plant

in South Africa.

-

8/6/2019 Brazil 2011 Mining - BMI

17/37

LEADING COMPANIES

Brazil - Metals & Mining 0076 - 2106 - 2009

Datamonitor. This profile is a licensed product and is not to be

photocopied Page 17

The diamonds and specialty products CSG comprises the businesses

of diamonds and titanium minerals,

and the exploration and development of a potash business. The

group's Ekati Diamond Mine, of which it

owns 80%, is located in the Canadian Northwest Territories and

produces over 3 million carats of rough

diamonds annually. It sells polished diamonds, manufactured

through contract polishing arrangements,

through its CanadaMark and AURIAS brands. BHP Billiton owns 50%

of Richards Bay Minerals (RBM), a

heavy mineral sands mine and smelter situated in northern

KwaZulu-Natal, South Africa. RBM is a major

producer of titania slag, high purity pig iron, rutile, and

zircon. It has a titania slag project at Corridor

Sands in Mozambique.

In July 2008, the group acquired the remaining 25% of interest

in a joint venture with Anglo Potash

formed for a large land position in Saskatchewan, Canada. BHP

Billiton currently controls 100% of the

land position. The company's permit positions for potash extend

over 7,338 square kilometers of highly

prospective exploration ground within Saskatchewan and Manitoba.

It is currently undertaking a pre-

feasibility study for the Jansen project in Saskatchewan.

Key Metrics

The company recorded revenues of $50,211 million in the fiscal

year ending June 2009, a decrease of

15.6% compared to fiscal 2008. Its net income was $6,338 million

in fiscal 2009, compared to a net

income of $15,962 million in the preceding year.

Table 5: BHP Billiton Group: key financials ($)

$ million 2005 2006 2007 2008 2009Revenues 31,150.0 39,099.0

47,473.0 59,473.0 50,211.0

Net income (loss) 6,628.0 10,450.0 13,496.0 15,962.0 6,338.0

Total assets 45,077.0 51,343.0 61,404.0 76,008.0 78,770.0

Total liabilities 23,927.0 24,283.0 31,737.0 37,673.0

38,816.0

Employees 36,468 33,184 33,861 41,732 40,990

Source: company filings D A T A M O N I T O R

-

8/6/2019 Brazil 2011 Mining - BMI

18/37

LEADING COMPANIES

Brazil - Metals & Mining 0076 - 2106 - 2009

Datamonitor. This profile is a licensed product and is not to be

photocopied Page 18

Table 6: BHP Billiton Group: key financial ratios

Ratio 2005 2006 2007 2008 2009

Profit margin 21.3% 26.7% 28.4% 26.8% 12.6%Revenue growth 24.9%

25.5% 21.4% 25.3% (15.6%)

Asset growth 44.6% 13.9% 19.6% 23.8% 3.6%

Liabilities growth 55.1% 1.5% 30.7% 18.7% 3.0%

Debt/asset ratio 53.1% 47.3% 51.7% 49.6% 49.3%

Return on assets 17.4% 21.7% 23.9% 23.2% 8.2%

Revenue per employee $854,174 $1,178,249 $1,401,996 $1,425,117

$1,224,957

Profit per employee $181,748 $314,911 $398,571 $382,488

$154,623

Source: company filings D A T A M O N I T O R

Figure 4: BHP Billiton Group: revenues & profitability

Source: company filings D A T A M O N I T O R

-

8/6/2019 Brazil 2011 Mining - BMI

19/37

LEADING COMPANIES

Brazil - Metals & Mining 0076 - 2106 - 2009

Datamonitor. This profile is a licensed product and is not to be

photocopied Page 19

Figure 5: BHP Billiton Group: assets & liabilities

Source: company filings D A T A M O N I T O R

-

8/6/2019 Brazil 2011 Mining - BMI

20/37

LEADING COMPANIES

Brazil - Metals & Mining 0076 - 2106 - 2009

Datamonitor. This profile is a licensed product and is not to be

photocopied Page 20

Gerdau S.A.

Table 7: Gerdau S.A.: key facts

Head office: Av. Farrapos, 1811 Floresta, Porto Alegra, Rio

Grande do Sul90220005, BRA

Telephone: 55 51 3323 2000

Fax: 55 51 3323 2222

Website: www.gerdau.com.br

Financial year-end: December

Ticker: GGB, GGBR4

Stock exchange: New York, Sao Paulo

Source: company website D A T A M O N I T O R

Gerdau is a Brazil-based long steel producer, ranking as the

largest steel producer in Brazil and the

Americas. The company operates steel mills that produce steel by

direct iron-ore reduction (DRI) in blast

furnaces and in electric arc furnaces. In Brazil, it operates

three blast furnace steel mills, including its

largest mill, Gerdau Acominas, an integrated steel mill. The

company has 60 steel producing units

globally, including joint ventures and associated companies. The

joint ventures include a unit located in

the US for the production of flat rolled steel, and another unit

in India. The associated companies are

Aceros Corsa in Mexico; Corporacion Centroamericana del Acero in

Guatemala; and INCA in the

Dominican Republic.

The company operates in Brazil, Argentina, Chile, Colombia,

Peru, Uruguay, Mexico, Dominican

Republic, Venezuela, Guatemala, the US, Canada, Spain and India.

The company has an installed

capacity of 26 million tons of crude steel and 22 million tons

of rolled steel products annually. The

company also has presence in North America, Latin America and

Europe.

The company offers a range of steel products. Its product mix

includes crude steel (slabs, blooms and

billets) sold to rolling mills, finished products for the

construction industry, such as rods and structural

bars, finished products for industry such as commercial rolled

steel bars and machine wire and products

for farming and agriculture, such as poles, smooth wire and

barbed wire. It also produces specialty steel

products for the manufacture of tools and machinery, chains,

locks and springs, mainly for the automotive

and mechanical industries.

-

8/6/2019 Brazil 2011 Mining - BMI

21/37

LEADING COMPANIES

Brazil - Metals & Mining 0076 - 2106 - 2009

Datamonitor. This profile is a licensed product and is not to be

photocopied Page 21

Gerdau is a non-operational holding company controlled by a

Metalurgica Gerdau. The company

operates through following subsidiaries: Gerdau Acos Longos

(Brazil), Gerdau Comercial de Acos

(Brazil), Gerdau Aominas (Brazil), Gerdau Ameristeel

(US/Canada), Gerdau Acos Especiais (Brazil),

Corporacion Sidenor (Spain), Gerdau MacSteel (US), Gerdau Laisa

(Uruguay), Gerdau Chile Inversiones

(Chile), Sipar Gerdau Inversiones and Diaco (Colombia), Empresa

Siderurgica del Peru, Gerdau GTL

Mexico (Mexico), Siderurgica Zuliana (Venezuela) and Seiva

(Brazil).

The company operates through five business segments: North

America includes all North American

operations, except for the Mexican operations and specialty

products (MacSteel); long steel Brazil;

specialty steel includes the specialty steel operations in

Brazil, Europe and the US; Acominas Ouro

Branco and Latin America include all Latin American operations,

except for the Brazil operations.

The company's North America segment is operated through its

Gerdau Ameristeel subsidiary. Gerdau

Ameristeel is the second largest mini-mill steel producer in

North America with annual manufacturing

capacity of over 10.3 million tons of mill finished steel

products. It has a vertically integrated network of 18steel units

and one 50%-owned joint venture for the operation of a mini-mill,

22 scrap recycling facilities,

14 downstream operations (including three 50%-owned joint

ventures), and 56 fab shops. Gerdau

Ameristeel primarily serves customers in the eastern parts of

the US and Canada. Its products are

generally sold to steel service centers and steel fabricators,

or directly to original equipment

manufacturers, for use in a variety of industries, including

construction, automotive, mining, cellular and

electrical transmission, metal construction fabrication and

equipment.

Gerdau Ameristeel is organized into two business segments: mills

and downstream. The mills segment

manufactures and markets a range of steel products, including

steel reinforcement bars (rebar), merchant

bars, structural shapes, beams, special sections and coiled wire

rod. The mills segment also produces

rebar, merchant bars, rod and special bar quality products used

by the downstream segment. The

downstream segment comprises secondary value-added steel

businesses and consists of fabrication of

rebars, railroad spikes, cold drawn products, super light beam

processing, elevator guide rails, grinding

balls, wire mesh and collated nails.

The long steel Brazil segment is the largest distribution

channel with 68 stores throughout Brazil, 14

fabricated reinforcing steel facilities (Prontofer) and four

flat steel service centers, which serviced more

than 120,000 customers in 2008.

The specialty steel segment includes the operations in Brazil

(Piratini and Acos Villares), the US

(MacSteel) and Spain (Corporacion Sidenor). These operations

produce engineering steel, tool steel,special bar quality and

stainless steel. Gerdau's main specialty steel operation is located

in Brazil through

Acos Villares (Sao Paulo) and Piratini (Rio Grande do Sul), with

combined annual capacity of 1.4 million

tons of crude steel and 1.5 million tons of rolled steel, which

is sold in the domestic and export markets.

-

8/6/2019 Brazil 2011 Mining - BMI

22/37

LEADING COMPANIES

Brazil - Metals & Mining 0076 - 2106 - 2009

Datamonitor. This profile is a licensed product and is not to be

photocopied Page 22

Gerdau maintains a presence in North America through MacSteel,

the second largest producer of

specialty steel (Special Bar Quality - SBQ) in the US. MacSteel

operates three mini-mills, located in

Jackson, Michigan; Monroe, Michigan; and Fort Smith, Arkansas.

The company also operates six

downstream operations located in the states of Michigan (two),

Ohio, Indiana (two) and Wisconsin.

MacSteel has annual installed capacity of 1.2 million tons of

crude steel and 1.1 million tons of rolled

products. Corporacion Sidenor sells specialty steel to the

entire Europe continent with more than 450

clients located across Spain, France, Germany and Italy. It has

annual installed capacity of 1.2 million

tons of crude steel and rolled products.

The Acominas Ouro Branco segment's products are sold to rolling

mills and to companies that use slabs,

billets, blooms and ingots as raw material for their finishing

lines such as shipbuilding, forging and

mechanical. The segment also produces its own finished products

such as high quality wire rod and

sections.

The Latin America business segment operations include 20 steel

units 25 retail facilities, 12 fab shops(including joint ventures

and associated companies) and six scrap processing facilities

located in nine

countries. It operates mini-mills facilities with annual

manufacturing capacity of 2.9 million tons of finished

steel products. In Chile, the company operates under the name

Gerdau AZA. The company operates a

business unit known as AZAonLine, which services customers in

Chile through the internet. The company

sells its products to more than 150 clients, which are both

distributors and end-users. The company

operates through Diaco in Colombia, Siderperu in Peru, and

Sidertul in Mexico.

Gerdau's production processes are mainly based on the mini-mill

concept, with mills equipped with

electric arc furnaces that can melt steel scrap and produce the

steel product with the required

specifications. The main metallic input used by the company's

mills in the US is steel scrap. The

company's Brazilian mills use scrap and pig iron purchased from

local suppliers. The division Gerdau

Metalicos collects and supplies scrap to the industrial units;

and also recycles the steel scrap.

Key Metrics

The company recorded revenues of $13,214 million in the fiscal

year ending December 2009, a decrease

of 37.2% compared to fiscal 2008. Its net income was $559

million in fiscal 2009, compared to a net

income of $1,962 million in the preceding year.

-

8/6/2019 Brazil 2011 Mining - BMI

23/37

LEADING COMPANIES

Brazil - Metals & Mining 0076 - 2106 - 2009

Datamonitor. This profile is a licensed product and is not to be

photocopied Page 23

Table 8: Gerdau S.A.: key financials ($)

$ million 2005 2006 2007 2008 2009

Revenues 10,643.4 11,723.8 15,301.2 21,028.9 13,214.1Net income

(loss) 1,384.6 1,766.0 1,767.5 1,961.9 558.6

Total assets 10,893.4 13,408.2 20,651.5 29,401.0 22,197.7

Total liabilities 6,889.3 10,438.3 14,326.3 19,360.0

12,982.9

Employees 0 0 0 0 0

Source: company filings D A T A M O N I T O R

Table 9: Gerdau S.A.: key financials (BRL)

BRL million 2005 2006 2007 2008 2009Revenues 21,377.0 23,547.0

30,732.0 42,236.0 26,540.0

Net income (loss) 2,781.0 3,546.9 3,549.9 3,940.5 1,122.0

Total assets 21,879.0 26,930.0 41,478.0 59,051.0 44,583.3

Total liabilities 13,837.0 20,965.0 28,773.9 38,884.0

26,075.8

Source: company filings D A T A M O N I T O R

Table 10: Gerdau S.A.: key financial ratios

Ratio 2005 2006 2007 2008 2009

Profit margin 13.0% 15.1% 11.6% 9.3% 4.2%

Revenue growth 8.0% 10.2% 30.5% 37.4% (37.2%)

Asset growth 17.2% 23.1% 54.0% 42.4% (24.5%)

Liabilities growth 9.9% 51.5% 37.2% 35.1% (32.9%)

Debt/asset ratio 63.2% 77.8% 69.4% 65.8% 58.5%

Return on assets 13.7% 14.5% 10.4% 7.8% 2.2%

Source: company filings D A T A M O N I T O R

-

8/6/2019 Brazil 2011 Mining - BMI

24/37

LEADING COMPANIES

Brazil - Metals & Mining 0076 - 2106 - 2009

Datamonitor. This profile is a licensed product and is not to be

photocopied Page 24

Figure 6: Gerdau S.A.: revenues & profitability

Source: company filings D A T A M O N I T O R

Figure 7: Gerdau S.A.: assets & liabilities

Source: company filings D A T A M O N I T O R

-

8/6/2019 Brazil 2011 Mining - BMI

25/37

LEADING COMPANIES

Brazil - Metals & Mining 0076 - 2106 - 2009

Datamonitor. This profile is a licensed product and is not to be

photocopied Page 25

Vale S.A.

Table 11: Vale S.A.: key facts

Head office: Avenida Graca Aranha, No. 26, Rio de Janeiro 20030

900, BRA

Telephone: 55 21 3814 4477

Fax: 55 21 3814 4040

Website: www.vale.com

Financial year-end: New York, , Madrid, Madrid, BM&F

Bovespa, BM&F Bovespa

Ticker: VALE,XVALP, XVALO VALE 3, VALE 5

Stock exchange: December

Source: company website D A T A M O N I T O R

Vale is engaged in the production and export of iron ore and

pellets. It also produces nickel, copper,

manganese, ferroalloys, bauxite, precious metals, cobalt,

kaolin, potash, and other products. The

company is actively engaged in mineral exploration efforts in 22

countries globally. It operates in America,

Europe, Middle East, Asia, Africa, and Oceania.

The company operates through four business divisions: ferrous

minerals, non-ferrous minerals, logistics

services, and others.

Through its ferrous minerals division, Vale is engaged in the

business of iron ore mining, iron ore pellet

production, manganese ore mining, and ferroalloy production.

Vale conducts its iron ore business in Brazil, primarily at the

parent-company level and through its

subsidiary Urucum Mineracao (Urucum). The company operates its

iron ore mining and related

operations through three integrated systems, the Southeastern

System, the Southern System, and the

Northern System.

The Southeastern System mines are located in the Iron Quadrangle

region of the state of Minas Gerais,

where they are divided into three mining complexes, Itabira,

Minas Centrais, and Mariana. These mines

are also in the state of Mato Grosso do Sul, where the Urucum

mine is located. Vale conducts open-pit

mining operations in the Southeastern System. In FY2008, the

company produced 99.4% of the electric

energy consumed in the Southeastern System at its hydroelectric

power plants (Igarapava, Porto Estrela,Funil, Candonga, Aimores,

Capim Branco I, and Capim Branco II). The company owns and

operates

integrated railroad and terminal networks in the three mining

complexes of the Southeastern System.

The Southern System mines are located in the Iron Quadrangle

region of the state of Minas Gerais in

Brazil. It consists of the mines of Mineracoes Brasileiras

Reunidas (MBR), a subsidiary of Vale.

-

8/6/2019 Brazil 2011 Mining - BMI

26/37

-

8/6/2019 Brazil 2011 Mining - BMI

27/37

LEADING COMPANIES

Brazil - Metals & Mining 0076 - 2106 - 2009

Datamonitor. This profile is a licensed product and is not to be

photocopied Page 27

Under its aluminum business, Vale is engaged in bauxite mining,

alumina refining, and aluminum metal

smelting. In Brazil, Vale owns a bauxite mine, an alumina

refinery, and two aluminum smelters. The

company has a 40% interest in Mineracao Rio do Norte (MRN), a

bauxite producer, operations of which

are also located in Brazil.

Under its copper business, Vale has copper mining operations in

Brazil and Canada. In Brazil, Vale

produces copper concentrates at Sossego in Carajas, in the state

of Para. In Canada, Vale produces

copper concentrate, copper anode, and copper cathode in

conjunction with its nickel mining operations at

Sudbury, Thompson, and Voisey's Bay.

Vale produces PGMs as by-products of its nickel mining and

processing operations in Canada. The

PGMs are concentrated at its Port Colborne facilities, in the

Province of Ontario, Canada, and refined at

its precious metals refinery in Acton, England.

Vale also produces gold and silver as by-products of its nickel

mining and processing operations inCanada. Some of these precious

metals are upgraded at its facilities in Port Colborne, Ontario,

and all are

refined by unrelated parties in Canada.

Vale also produces other non-ferrous minerals. Vale is the

world's fourth largest producer of kaolin for the

paper industry and Brazil's sole producer of potash. Vale

produces cobalt as a by-product of its nickel

mining and processing operations in Canada and refines it at its

Port Colborne facilities.

The logistics services division of Vale consists of the

company's transportation systems that pertain to the

operation of its ships, ports, and railroads for third-party

cargos. It provides logistics services in Brazil,

with railroad, coastal shipping, and port handling operations.

Two of the company's three iron ore systems

incorporate an integrated railroad network linked to automated

port and terminal facilities. These

complexes provide rail transportation for the company's mining

products, general cargo and passengers,

bulk terminal storage, and ship loading services for its mining

operations. The company also has a 31.3%

interest in Log-In Logistica Intermodal (Log-In), which provides

container-based logistics services in

Brazil, and a 41.5% interest in MRS Logistica (MRS), which

transports Vale's iron ore products from the

Southern System mines to its Guaiba Island and Itaguai maritime

terminals, in the state of Rio de Janeiro.

Under its others business division, the company produces

metallurgical and thermal coal through Vale

Australia Holdings (Vale Australia), which operates coal assets

in Australia through wholly-owned

subsidiaries and unincorporated joint ventures. Vale also has

minority interests in Chinese coal and coke

producers. Vale also has ownership interest in California Steel

Industries (CSI), a flat-rolled steelproducer in the US. CSI

produces approximately 1.8 million metric tons of flat steel per

year. Vale has

investments in several steel projects in order to create

additional demand for its iron ore and iron ore

pellets.

-

8/6/2019 Brazil 2011 Mining - BMI

28/37

LEADING COMPANIES

Brazil - Metals & Mining 0076 - 2106 - 2009

Datamonitor. This profile is a licensed product and is not to be

photocopied Page 28

Key Metrics

The company recorded revenues of $19,915 million in the fiscal

year ending 2009, a decrease of 43.4%

compared to fiscal 2008. Its net income was $5,277 million in

fiscal 2009, compared to a net income of

$10,595.

Table 12: Vale S.A.: key financials ($)

$ million 2005 2006 2007 2008 2009

Revenues 17,165.3 22,735.2 32,970.9 35,191.0 19,915.3

Net income (loss) 5,199.5 6,687.2 9,960.8 10,595.1 5,276.8

Total assets 26,684.0 61,245.1 66,168.8 92,497.8 102,280.5

Total liabilities 14,708.7 41,778.1 37,774.0 44,563.3

41,782.8

Employees 38,560 52,646 0 0 57,043

Source: company filings D A T A M O N I T O R

Table 13: Vale S.A.: key financials (BRL)

BRL million 2005 2006 2007 2008 2009

Revenues 34,476.0 45,663.0 66,221.0 70,680.0 39,999.3

Net income (loss) 10,443.0 13,431.0 20,006.0 21,280.0

10,598.4

Total assets 53,594.0 123,009.0 132,898.0 185,779.0

205,427.4

Total liabilities 29,542.0 83,910.0 75,868.0 89,504.0

83,919.5

Source: company filings D A T A M O N I T O R

-

8/6/2019 Brazil 2011 Mining - BMI

29/37

LEADING COMPANIES

Brazil - Metals & Mining 0076 - 2106 - 2009

Datamonitor. This profile is a licensed product and is not to be

photocopied Page 29

Table 14: Vale S.A.: key financial ratios

Ratio 2005 2006 2007 2008 2009

Profit margin 30.3% 29.4% 30.2% 30.1% 26.5%Revenue growth 16.2%

32.4% 45.0% 6.7% (43.4%)

Asset growth 23.3% 129.5% 8.0% 39.8% 10.6%

Liabilities growth 24.7% 184.0% (9.6%) 18.0% (6.2%)

Debt/asset ratio 55.1% 68.2% 57.1% 48.2% 40.9%

Return on assets 21.5% 15.2% 15.6% 13.4% 5.4%

Source: company filings D A T A M O N I T O R

Figure 8: Vale S.A.: revenues & profitability

Source: company filings D A T A M O N I T O R

-

8/6/2019 Brazil 2011 Mining - BMI

30/37

LEADING COMPANIES

Brazil - Metals & Mining 0076 - 2106 - 2009

Datamonitor. This profile is a licensed product and is not to be

photocopied Page 30

Figure 9: Vale S.A.: assets & liabilities

Source: company filings D A T A M O N I T O R

-

8/6/2019 Brazil 2011 Mining - BMI

31/37

MARKET FORECASTS

Brazil - Metals & Mining 0076 - 2106 - 2009

Datamonitor. This profile is a licensed product and is not to be

photocopied Page 31

MARKET FORECASTS

Market value forecast

In 2014, the Brazilian metals & mining industry is forecast

to have a value of $60,459.2 million, anincrease of 64.3% since

2009.

The compound annual growth rate of the industry in the period

200914 is predicted to be 10.4%.

Table 15: Brazil metals & mining industry value forecast: $

million, 200914

Year $ million BRL million million % Growth

2009 36,800.7 73,913.2 26,465.6 (39.7%)

2010 50,026.2 100,476.1 35,976.8 35.9%

2011 53,859.6 108,175.3 38,733.7 7.7%

2012 56,179.5 112,834.8 40,402.0 4.3%

2013 58,353.5 117,201.4 41,965.5 3.9%

2014 60,459.2 121,430.6 43,479.9 3.6%

CAGR: 200914 10.4%

Source: Datamonitor D A T A M O N I T O R

Figure 10: Brazil metals & mining industry value forecast: $

million, 200914

Source: Datamonitor D A T A M O N I T O R

-

8/6/2019 Brazil 2011 Mining - BMI

32/37

MACROECONOMIC INDICATORS

Brazil - Metals & Mining 0076 - 2106 - 2009

Datamonitor. This profile is a licensed product and is not to be

photocopied Page 32

MACROECONOMIC INDICATORS

Table 16: Brazil size of population (million), 200509

Year Population (million) % Growth

2005 189.0 1.3%

2006 191.5 1.3%

2007 193.9 1.3%

2008 196.3 1.2%

2009 198.7 1.2%

Source: Datamonitor D A T A M O N I T O R

Table 17: Brazil GDP (constant 2000 prices, $ billion),

200509

Year Constant 2000 Prices, $ billion % Growth

2005 738.6 3.1%

2006 767.4 3.9%

2007 810.4 5.6%

2008 851.9 5.1%

2009 850.3 (0.2%)

Source: Datamonitor D A T A M O N I T O R

Table 18: Brazil GDP (current prices, $ billion), 200509

Year Current Prices, $ billion % Growth

2005 840.8 32.4%

2006 1,018.7 21.2%

2007 1,245.3 22.2%

2008 1,467.0 17.8%

2009 1,374.4 (6.3%)

Source: Datamonitor D A T A M O N I T O R

-

8/6/2019 Brazil 2011 Mining - BMI

33/37

MACROECONOMIC INDICATORS

Brazil - Metals & Mining 0076 - 2106 - 2009

Datamonitor. This profile is a licensed product and is not to be

photocopied Page 33

Table 19: Brazil inflation, 200509

Year Inflation Rate (%)

2005 6.9%2006 4.2%

2007 3.6%

2008 5.7%

2009 4.3%

Source: Datamonitor D A T A M O N I T O R

Table 20: Brazil consumer price index (absolute), 200509

Year Consumer Price Index (2000 =100)

% Growth

2005 151.4 6.9%

2006 157.8 4.2%

2007 163.5 3.6%

2008 172.8 5.7%

2009 180.2 4.3%

Source: Datamonitor D A T A M O N I T O R

Table 21: Brazil exchange rate, 200509

Year Exchange rate ($/BRL) Exchange rate (/BRL)

2005 2.4348 3.0264

2006 2.1800 2.7351

2007 1.9516 2.6704

2008 1.8402 2.6927

2009 2.0085 2.7928

Source: Datamonitor D A T A M O N I T O R

-

8/6/2019 Brazil 2011 Mining - BMI

34/37

APPENDIX

Brazil - Metals & Mining 0076 - 2106 - 2009

Datamonitor. This profile is a licensed product and is not to be

photocopied Page 34

APPENDIX

Methodology

Datamonitor Industry Profiles draw on extensive primary and

secondary research, all aggregated,analyzed, cross-checked and

presented in a consistent and accessible style.

Review of in-house databases Created using 250,000+ industry

interviews and consumer surveys

and supported by analysis from industry experts using highly

complex modeling & forecasting tools,

Datamonitors in-house databases provide the foundation for all

related industry profiles

Preparatory research We also maintain extensive in-house

databases of news, analyst

commentary, company profiles and macroeconomic & demographic

information, which enable our

researchers to build an accurate market overview

Definitions Market definitions are standardized to allow

comparison from country to country. The

parameters of each definition are carefully reviewed at the

start of the research process to ensure they

match the requirements of both the market and our clients

Extensive secondary research activities ensure we are always

fully up-to-date with the latest

industry events and trends

Datamonitor aggregates and analyzes a number of secondary

information sources, including:

- National/Governmental statistics

- International data (official international sources)

- National and International trade associations

- Broker and analyst reports

- Company Annual Reports

- Business information libraries and databases

Modeling & forecasting tools Datamonitor has developed

powerful tools that allow quantitative

and qualitative data to be combined with related macroeconomic

and demographic drivers to create

market models and forecasts, which can then be refined according

to specific competitive, regulatory

and demand-related factors

Continuous quality control ensures that our processes and

profiles remain focused, accurate and

up-to-date

-

8/6/2019 Brazil 2011 Mining - BMI

35/37

APPENDIX

Brazil - Metals & Mining 0076 - 2106 - 2009

Datamonitor. This profile is a licensed product and is not to be

photocopied Page 35

Industry associations

International Iron and Steel Institute

Rue Colonel Bourg, 120, B-1140 Brussels, Belgium

Tel.: 322 702 89 00Fax: 322 702 88 99

www.worldsteel.org

International Aluminium Institute

New Zealand House, Haymarket, London, SW1Y 4TE, UK

Tel.: 44 20 7930 0528

Fax: 44 20 7321 0183

www.world-aluminium.org

World Coal Institute5th Floor, Heddon House, 149 - 151 Regent

Street, London, W1B 4JD, UK

Tel.: 44 20 7851 0052

Fax: 44 20 7851 0061

www.wci-coal.com

MEPS

www.meps.co.uk

World Gold Council

55 Old Broad Street, London EC2M 1RX, United Kingdom

Tel.: 0044 20 7826 4700

Fax: 0044 20 7826 4799

www.gold.org

Related Datamonitor research

Industry Profile

Metals & Mining in France

Metals & Mining in Germany

Metals & Mining in the United Kingdom

Metals & Mining in Belgium

-

8/6/2019 Brazil 2011 Mining - BMI

36/37

APPENDIX

Brazil - Metals & Mining 0076 - 2106 - 2009

Datamonitor. This profile is a licensed product and is not to be

photocopied Page 36

Disclaimer

All Rights Reserved.

No part of this publication may be reproduced, stored in a

retrieval system or transmitted in any form

by any means, electronic, mechanical, photocopying, recording or

otherwise, without the prior

permission of the publisher, Datamonitor plc.

The facts of this report are believed to be correct at the time

of publication but cannot be guaranteed.

Please note that the findings, conclusions and recommendations

that Datamonitor delivers will be

based on information gathered in good faith from both primary

and secondary sources, whose

accuracy we are not always in a position to guarantee. As such

Datamonitor can accept no liability

whatever for actions taken based on any information that may

subsequently prove to be incorrect.

-

8/6/2019 Brazil 2011 Mining - BMI

37/37

ABOUT DATAMONITOR

B il M t l & Mi i 0076 2106 2009

ABOUT DATAMONITOR

The Datamonitor Group is a world-leading provider of premium

global business information, delivering

independent data, analysis and opinion across the Automotive,

Consumer Markets, Energy & Utilities,

Financial Services, Logistics & Express, Pharmaceutical

& Healthcare, Retail, Technology and

Telecoms industries.

Combining our industry knowledge and experience, we assist over

6,000 of the worlds leading

companies in making better strategic and operational

decisions.

Delivered online via our user-friendly web platforms, our market

intelligence products and services

ensure that you will achieve your desired commercial goals by

giving you the insight you need to best

respond to your competitive environment.

Premium Reports

Datamonitor's premium reports are based on primary research with

industry panels and consumers.We gather information on market

segmentation, market growth and pricing, competitors and

products.

Our experts then interpret this data to produce detailed

forecasts and actionable recommendations,

helping you create new business opportunities and ideas.

Summary Reports

Our series of company, industry and country profiles complements

our premium products, providing

top-level information on 30,000 companies, 3,000 industries and

100 countries. While they do not

contain the highly detailed breakdowns found in premium reports,

profiles give you the most important

qualitative and quantitative summary information you need -

including predictions and forecasts.

Datamonitor consulting

We hope that the data and analysis in this profile will help you

make informed and imaginative business

decisions. If you have further requirements, Datamonitors

consulting team may be able to help you. For

more information about Datamonitors consulting capabilities,

please contact us directly at

[email protected].

![BM1弾 カードチェックリスト · 2020-06-17 · 1.89 d bmi-scp4[cp1 c] bmi-scp8[cp] bmi-hcpi bmi-scps[cpi a bmi cl bmi-scpi c] bmi-scp5[cp] c] bmi-cpi [cpi 12 bmi-cp2tcp]](https://img.pdfslide.net/doc/110x75/5f0d11867e708231d43885ac/bm1-fffffff-2020-06-17-189-d-bmi-scp4cp1-c-bmi-scp8cp.jpg)