Embed Size (px)

Citation preview

Outlook 2012: Outlook 2012: What to Expect inDirect & Digital MarketingDirect & Digital Marketing

Bruce BiegelManaging Director

October 1, 2012Boston, MA

Winterberry Group & Petsky Prunier LLC: Maximizing Shareholder Value of Companies in the Marketing Sector

• Market Intelligence

Strategic Consulting

Sell-Side Representation

•• Strategic Consulting

• Transaction/Diligence Support

p

Corporate Divestitures

•g pp

• Market/Competitive Landscape Analysis

Capital Raising & Private Placements

B id M&A

•

• Industry Insight:Publishing andTactical Execution

Buy side M&A Advisory

Fairness Opinions

••

Fairness Opinions

Agenda

Outlook 2012

What happened in 2011?

2012 Channel Check: The evolution of direct and digital

Changing Data Landscape

9for12: What You Should 9for12: What You Should Consider for 2012

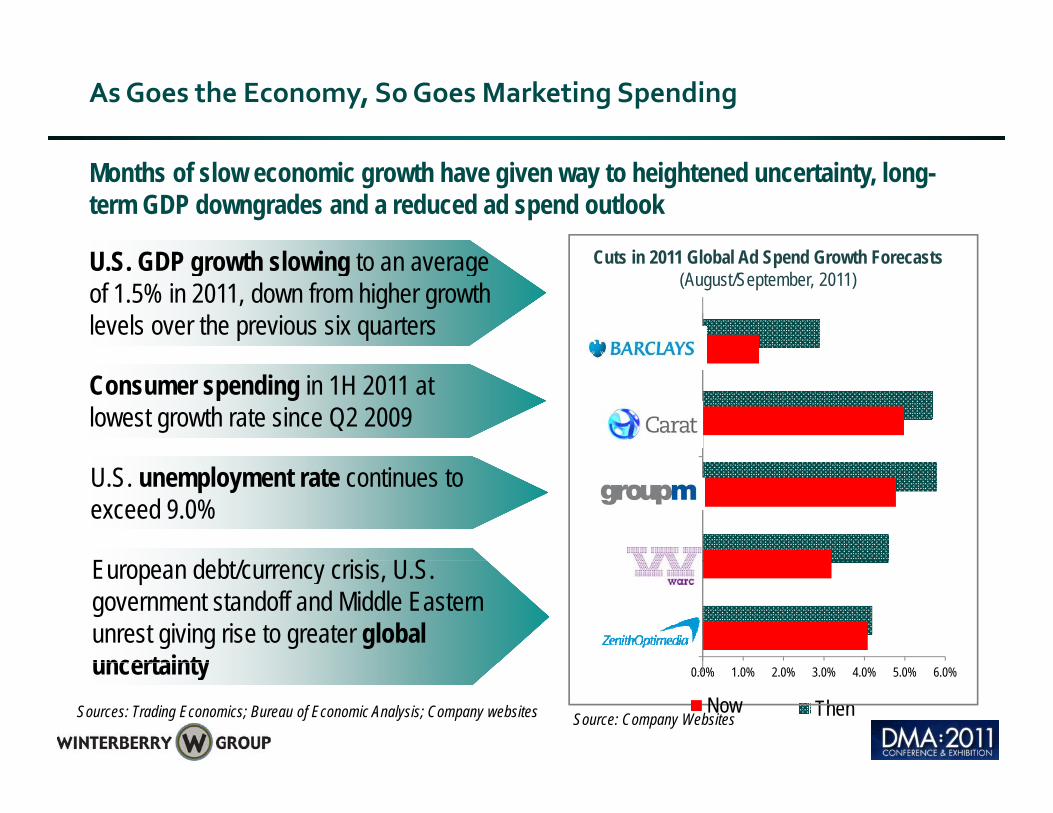

As Goes the Economy, So Goes Marketing Spending

U S GDP th l i t

Months of slow economic growth have given way to heightened uncertainty, long-term GDP downgrades and a reduced ad spend outlook

C t i 2011 Gl b l Ad S d G th F t U.S. GDP growth slowing to an average of 1.5% in 2011, down from higher growth levels over the previous six quarters

Cuts in 2011 Global Ad Spend Growth Forecasts (August/September, 2011)

Consumer spending in 1H 2011 at lowest growth rate since Q2 2009

U.S. unemployment rate continues to exceed 9.0%

E d bt/ i i U S European debt/currency crisis, U.S. government standoff and Middle Eastern unrest giving rise to greater global uncertainty 0.0% 1.0% 2.0% 3.0% 4.0% 5.0% 6.0%

ThenSources: Trading Economics; Bureau of Economic Analysis; Company websites

uncertaintyNow

Source: Company Websites

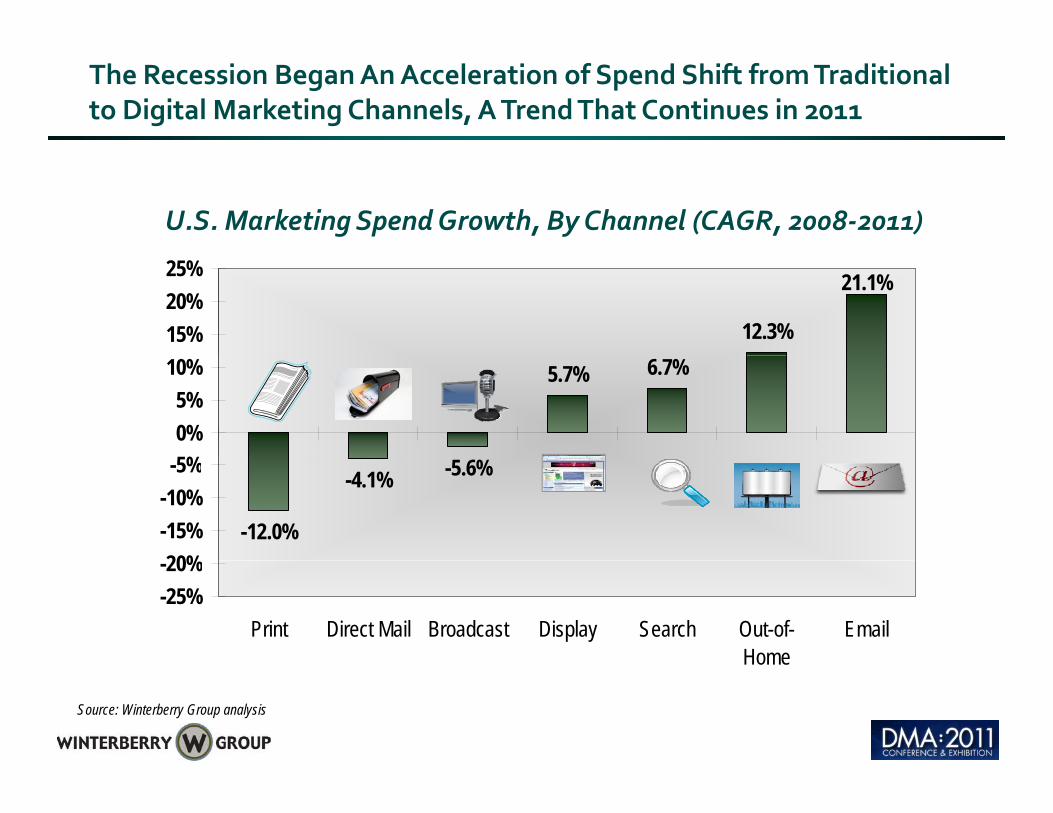

The Recession Began An Acceleration of Spend Shift from Traditional to Digital Marketing Channels, A Trend That Continues in 2011

U.S. Marketing Spend Growth, By Channel (CAGR, 2008‐2011)

12.3%

21.1%

15%20%25%

5.7% 6.7%

5%0%5%

10%

-12.0%

-4.1% -5.6%

20%-15%-10%-5%

-25%-20%

Print Direct Mail Broadcast Display Search Out-of-Home

EmailHome

Source: Winterberry Group analysis

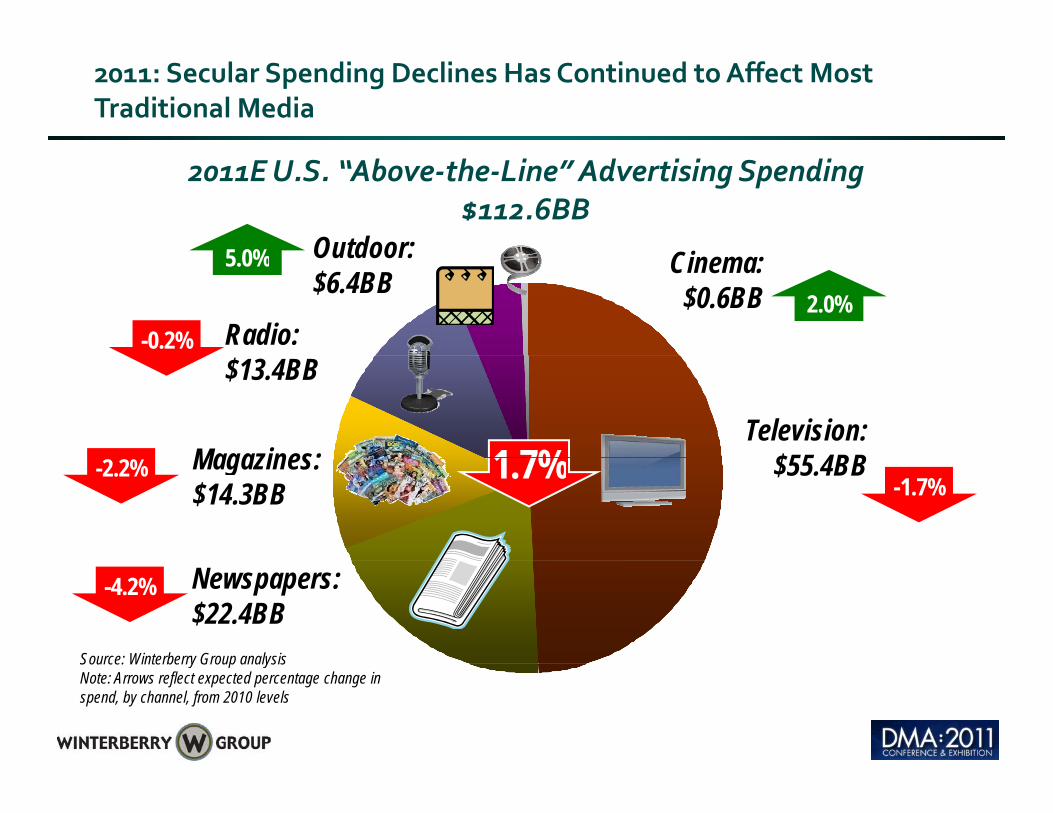

2011: Secular Spending Declines Has Continued to Affect Most Traditional Media

2011E U.S. “Above‐the‐Line” Advertising Spending $112.6BB

Outdoor: Ci5 0%

Radio:

Outdoor:$6.4BB Cinema:

$0.6BB-0.2%

5.0%

2.0%

Television:$55 4BBMagazines:

$13.4BB

1 7% $55.4BBMagazines:$14.3BB

-2.2%-1.7%1.7%

Newspapers:$22.4BB

-4.2%

Source: Winterberry Group analysisSource: Winterberry Group analysisNote: Arrows reflect expected percentage change in spend, by channel, from 2010 levels

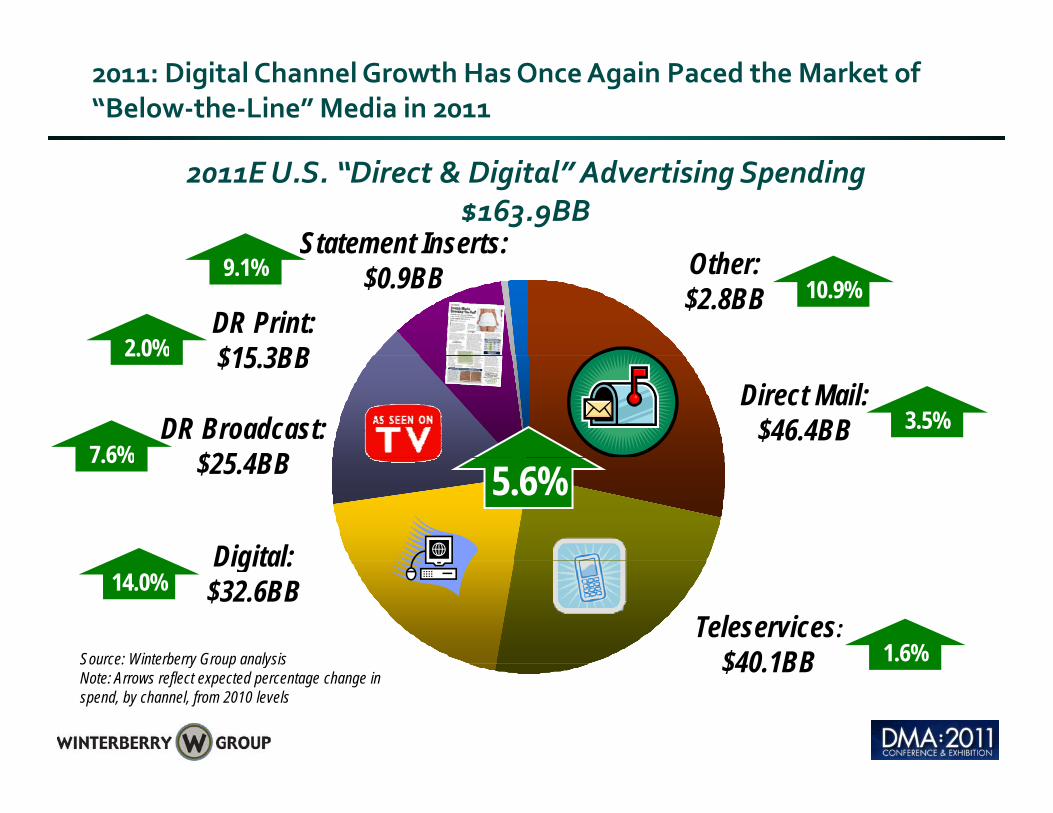

2011: Digital Channel Growth Has Once Again Paced the Market of“Below‐the‐Line” Media in 2011

2011E U.S. “Direct & Digital” Advertising Spending $163.9BB

OStatement Inserts:

DR Print:$15 3BB

Other:$2.8BB

Statement Inserts:$0.9BB9.1%

10.9%

2.0%

Direct Mail:$46.4BBDR Broadcast:

$25 4BB

$15.3BB

7 6%

2.0%

3.5%

$25.4BB

Digital:

7.6%5.6%

Teleservices:$40 1BB

Digital:$32.6BB14.0%

1.6%Source: Winterberry Group analysis $40.1BBSource: Winterberry Group analysisNote: Arrows reflect expected percentage change in spend, by channel, from 2010 levels

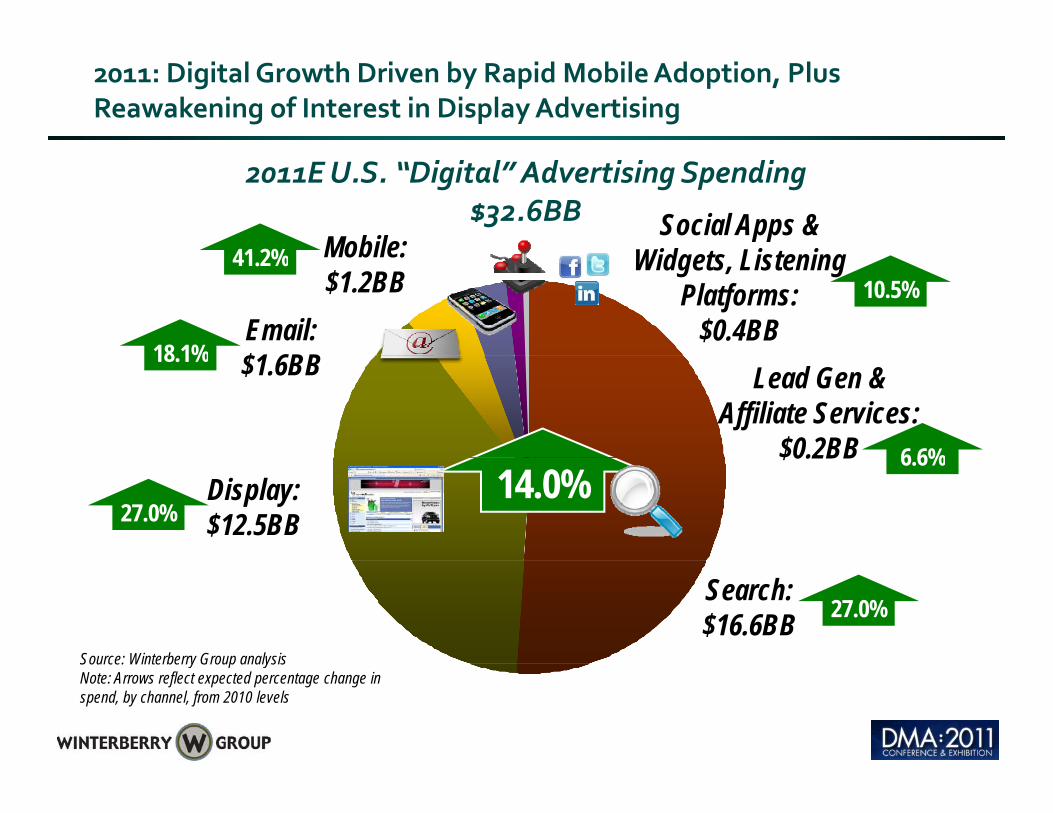

2011: Digital Growth Driven by Rapid Mobile Adoption, Plus Reawakening of Interest in Display Advertising

2011E U.S. “Digital” Advertising Spending $32.6BB

Mobile:Social Apps &

Wid t Li t i 41 2% Mobile:$1.2BB

Email:$1 6BB

Widgets, Listening Platforms:

$0.4BB

41.2%

18 1%

10.5%

$1.6BB18.1%Lead Gen &

Affiliate Services:$0.2BB 6 6%

Display:$12.5BB27.0%

14.0%$0.2BB 6.6%

Search:$16.6BB 27.0%

Source: Winterberry Group analysisSource: Winterberry Group analysisNote: Arrows reflect expected percentage change in spend, by channel, from 2010 levels

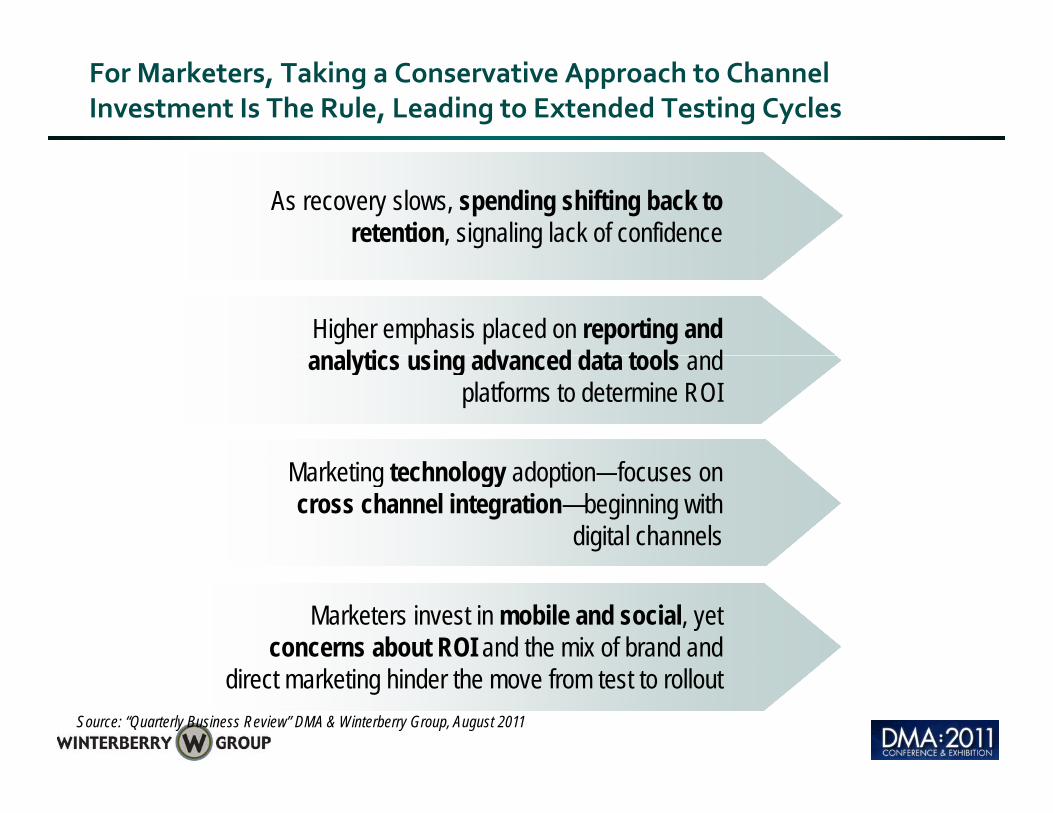

For Marketers, Taking a Conservative Approach to Channel Investment Is The Rule, Leading to Extended Testing Cycles

As recovery slows, spending shifting back to retention, signaling lack of confidence

Higher emphasis placed on reporting and l ti i d d d t t l d analytics using advanced data tools and

platforms to determine ROI

Marketing technology adoption—focuses oncross channel integration—beginning with

digital channels

Marketers invest in mobile and social, yet concerns about ROI and the mix of brand and

direct marketing hinder the move from test to rolloutSource: “Quarterly Business Review” DMA & Winterberry Group, August 2011

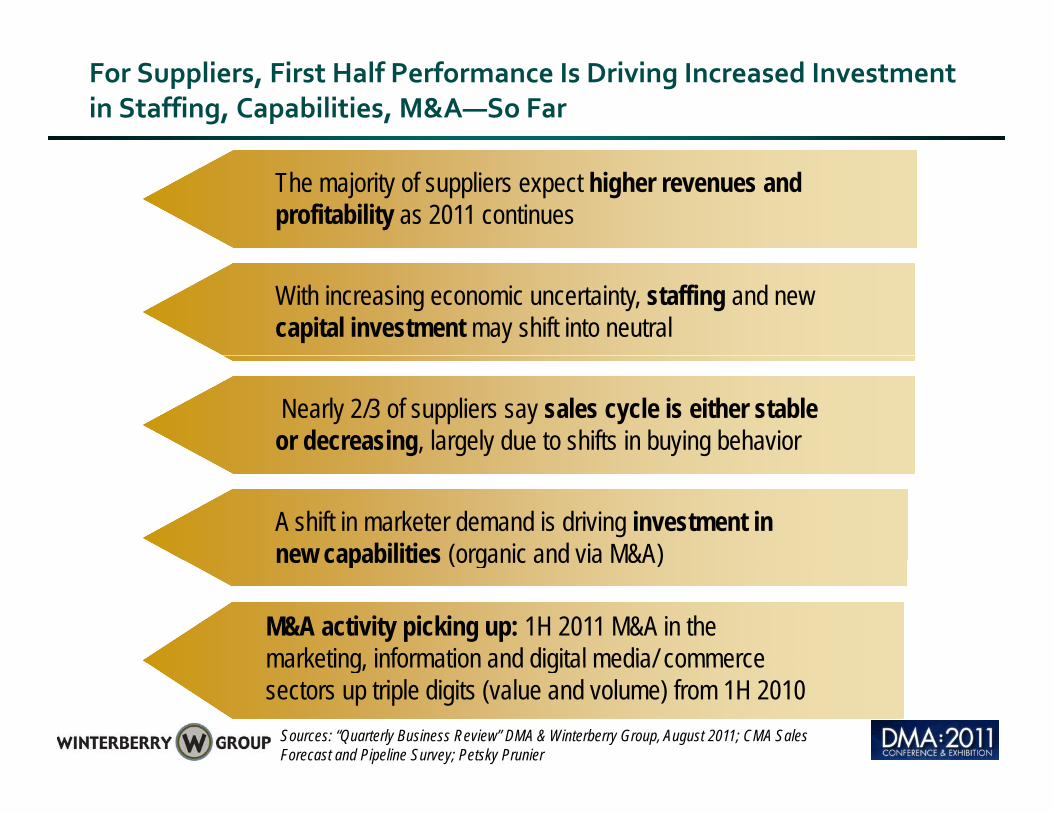

For Suppliers, First Half Performance Is Driving Increased Investment in Staffing, Capabilities, M&A—So Far

The majority of suppliers expect higher revenues and profitability as 2011 continues

With increasing economic uncertainty, staffing and new capital investment may shift into neutral

Nearly 2/3 of suppliers say sales cycle is either stable or decreasing, largely due to shifts in buying behavior

A shift in marketer demand is driving investment in new capabilities (organic and via M&A)new capabilities (organic and via M&A)

M&A activity picking up: 1H 2011 M&A in the marketing information and digital media/ commerce marketing, information and digital media/ commerce sectors up triple digits (value and volume) from 1H 2010

Sources: “Quarterly Business Review” DMA & Winterberry Group, August 2011; CMA Sales Forecast and Pipeline Survey; Petsky Prunier

Agenda

Outlook 2012

What happened in 2011?

2012 Channel Check: The evolution of direct and digital

Changing Data Landscape

9for12: What You Should 9for12: What You Should Consider for 2012

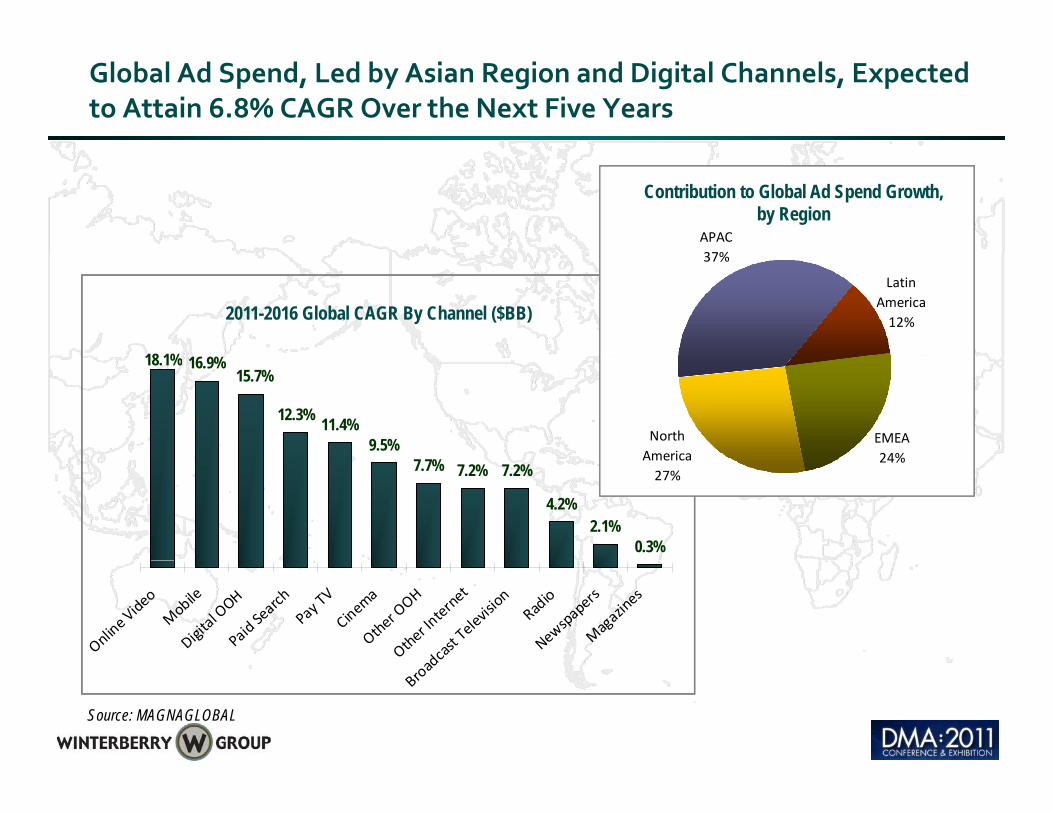

Global Ad Spend, Led by Asian Region and Digital Channels, Expected to Attain 6.8% CAGR Over the Next Five Years

APAC37%

Contribution to Global Ad Spend Growth, by Region

18 1%

2011-2016 Global CAGR By Channel ($BB)

37%

Latin America12%

11.4%9.5%

18.1% 16.9%15.7%

12.3%EMEA24%

North America7.7% 7.2% 7.2%

4.2%2.1%

0.3%

24%America27%

Online Video

Mobile

Digital OOH

Paid Search

Pay TV

Cinema

Other OOH

Other Internet

adcast Television

Radio

Newspapers

Magazines

Broad

Source: MAGNAGLOBAL

2012: A Challenging Economic Outlook

Slow U.S. GDP growth continues: forecasts predict 2% for the year¹ • U.S. unemployment rate likely to stay above 9% • Gas prices, fiscal tightening, and European

sovereign debt weigh down the 2012 outlook²sovereign debt weigh down the 2012 outlook• Odds of a renewed recession put at 1 in 2³• Reduced confidence in U.S. economy as S&P

downgrades U.S. credit rating and Moody’s lowers U.S. economic outlook through 2012

Sources: [1] “World Economic Outlook” IMF [2] Goldman Sachs [3] Business Cycle Dating Committee of the National Bureau of Economic Research

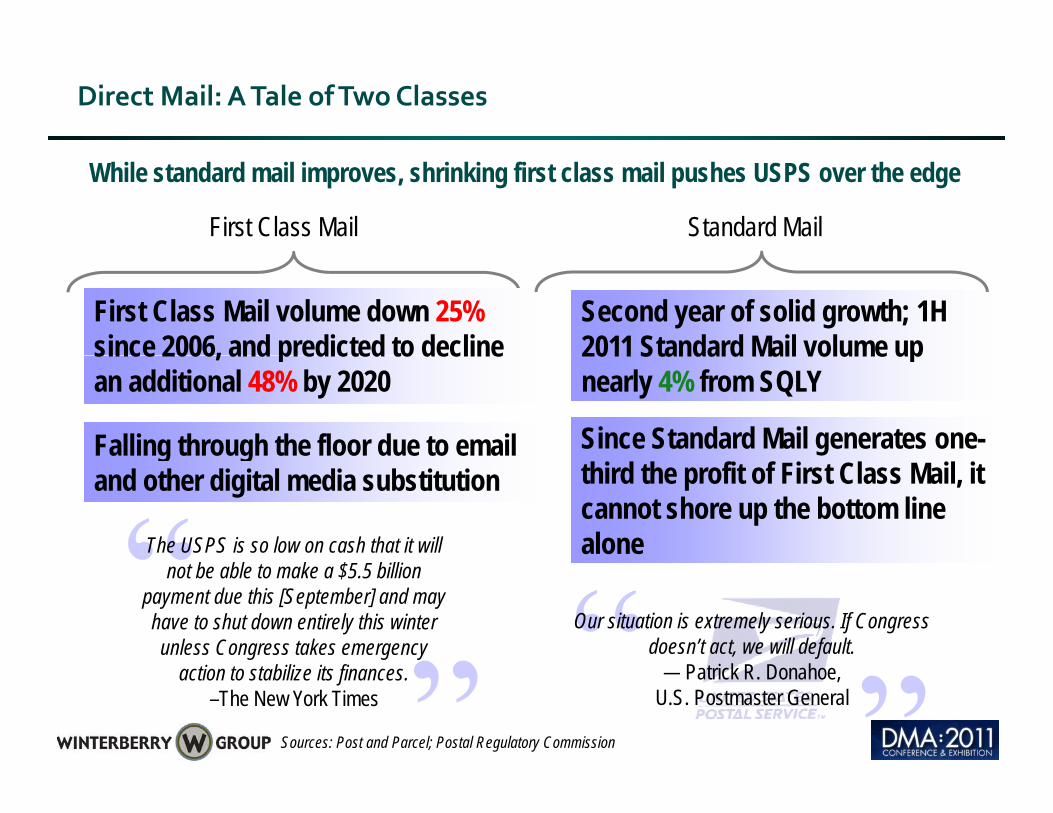

Direct Mail: A Tale of Two Classes

First Class Mail Standard Mail

While standard mail improves, shrinking first class mail pushes USPS over the edge

First Class Mail volume down 25%since 2006, and predicted to decline

Second year of solid growth; 1H 2011 Standard Mail volume up

Falling through the floor due to email

since 2006, and predicted to decline an additional 48% by 2020

2011 Standard Mail volume up nearly 4% from SQLY

Since Standard Mail generates one-g gand other digital media substitution third the profit of First Class Mail, it

cannot shore up the bottom line aloneThe USPS is so low on cash that it will

Our situation is extremely serious. If Congress doesn’t act, we will default.

not be able to make a $5.5 billion payment due this [September] and may have to shut down entirely this winter unless Congress takes emergency

— Patrick R. Donahoe, U.S. Postmaster General

action to stabilize its finances. –The New York Times

Sources: Post and Parcel; Postal Regulatory Commission

Direct Mail’s Place in the Marketing Mix Has Changed

Th f di t il h hift d

Direct mail moving from a direct-response-only approach to key player in the multichannel world

The purpose of direct mail has shifted… …from direct order….

…to driving sales online or in-storeThe catalog is great driver for sales online and in stores. We’re not publishing with the idea of p gcreating an [independent] direct marketing

business. It’s the idea of driving traffic into stores and giving the sense of a brand.

-Ellen Smolyar, ySenior Manager of Sales and Circulation

at Crate & Barrel

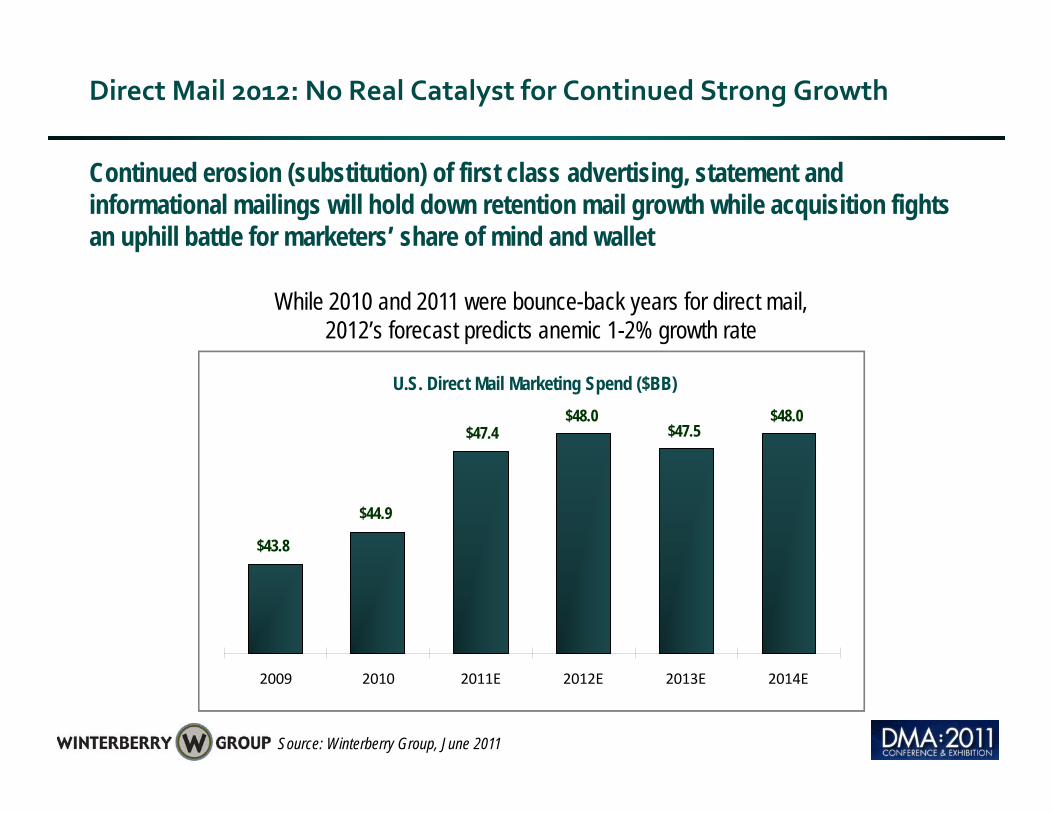

Direct Mail 2012: No Real Catalyst for Continued Strong Growth

Continued erosion (substitution) of first class advertising, statement and informational mailings will hold down retention mail growth while acquisition fights an uphill battle for marketers’ share of mind and wallet

While 2010 and 2011 were bounce-back years for direct mail, 2012’s forecast predicts anemic 1-2% growth rate

$47.5$48.0

$47.4$48.0

U.S. Direct Mail Marketing Spend ($BB)

$43.8

$44.9

2009 2010 2011E 2012E 2013E 2014E

Source: Winterberry Group, June 2011

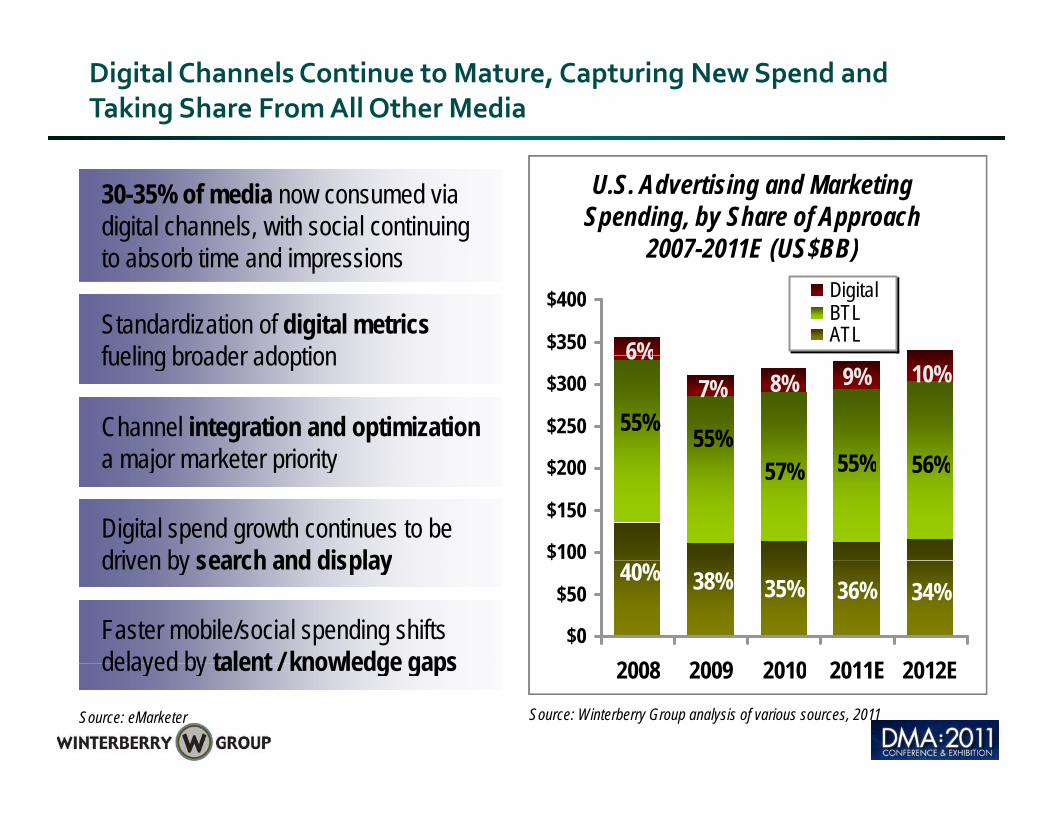

Digital Channels Continue to Mature, Capturing New Spend and Taking Share From All Other Media

U.S. Advertising and Marketing Spending, by Share of Approach

2007-2011E (US$BB)

30-35% of media now consumed via digital channels, with social continuing t b b ti d i i

$350

$400 DigitalBTLATL

2007 2011E (US$BB)

6%

to absorb time and impressions

Standardization of digital metricsfueling broader adoption

$250

$3006%

7% 8% 9% 10%

55% 55%55% 56%

Channel integration and optimizationa major marketer priority

fueling broader adoption

$100

$150

$200 57% 55% 56%a major marketer priority

Digital spend growth continues to be driven by search and display

$0

$50

$

2008 2009 2010 2011E 2012E

40% 38% 35% 36% 34%driven by search and display

Faster mobile/social spending shifts delayed by talent / knowledge gaps 2008 2009 2010 2011E 2012E

Source: Winterberry Group analysis of various sources, 2011

delayed by talent / knowledge gaps

Source: eMarketer

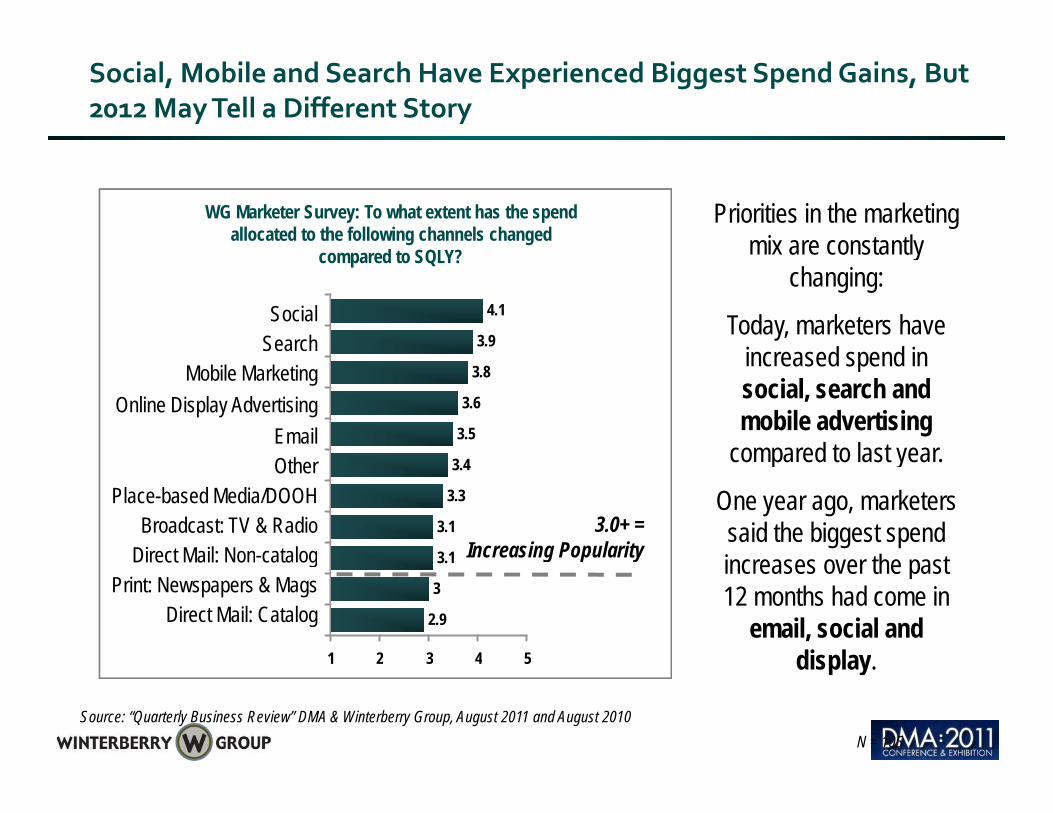

Social, Mobile and Search Have Experienced Biggest Spend Gains, But 2012 May Tell a Different Story

WG Marketer Survey: To what extent has the spend allocated to the following channels changed

d t SQLY?

Priorities in the marketing mix are constantly

3.9

4.1Search

SocialSocialSearch

compared to SQLY? mix are constantly changing:

Today, marketers have increased spend in

3.5

3.6

3.8

Oth

E–Mail

Online Display Advertising

Mobile MarketingMobile MarketingOnline Display Advertising

EmailO h

increased spend in social, search and mobile advertising

compared to last year

3 1

3.1

3.3

3.4

Broadcast: TV & Radio

Direct Mail: Non-catalog

Out-of-Home / Outdoor

OtherOtherPlace-based Media/DOOH

Broadcast: TV & RadioDirect Mail: Non-catalog

3.0+ =Increasing Popularity

compared to last year.

One year ago, marketers said the biggest spend increases over the past

2.9

3

3.1

1 2 3 4 5

Direct Mail: Catalog

Print: Newspaper & Magazine

Direct Mail: Non catalogPrint: Newspapers & Mags

Direct Mail: Catalog

g p y increases over the past 12 months had come in

email, social and display 1 2 3 4 5

N = 105Source: “Quarterly Business Review” DMA & Winterberry Group, August 2011 and August 2010

display.

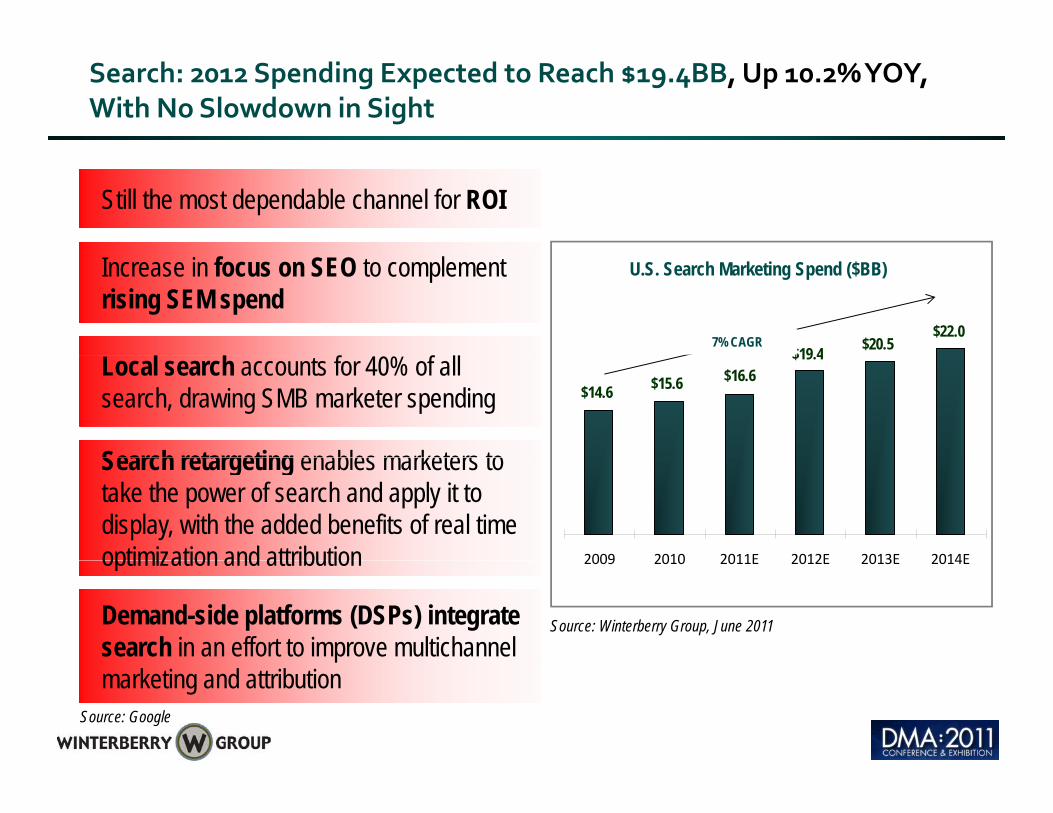

Search: 2012 Spending Expected to Reach $19.4BB, Up 10.2% YOY, With No Slowdown in Sight

Still the most dependable channel for ROI

Increase in focus on SEO to complement rising SEM spend

$20.5$22.0

$19 4

U.S. Search Marketing Spend ($BB)

7% CAGR

Local search accounts for 40% of all search, drawing SMB marketer spending

Search retargeting enables marketers to

$19.4$16.6$15.6$14.6

46% 44% 43% 44% 44%

Search retargeting enables marketers to take the power of search and apply it to display, with the added benefits of real time optimization and attribution 2009 2010 2011E 2012E 2013E 2014E46% 43%

Demand-side platforms (DSPs) integrate search in an effort to improve multichannel

optimization and attribution 2009 2010 2011E 2012E 2013E 2014E

Source: Winterberry Group, June 2011

marketing and attributionSource: Google

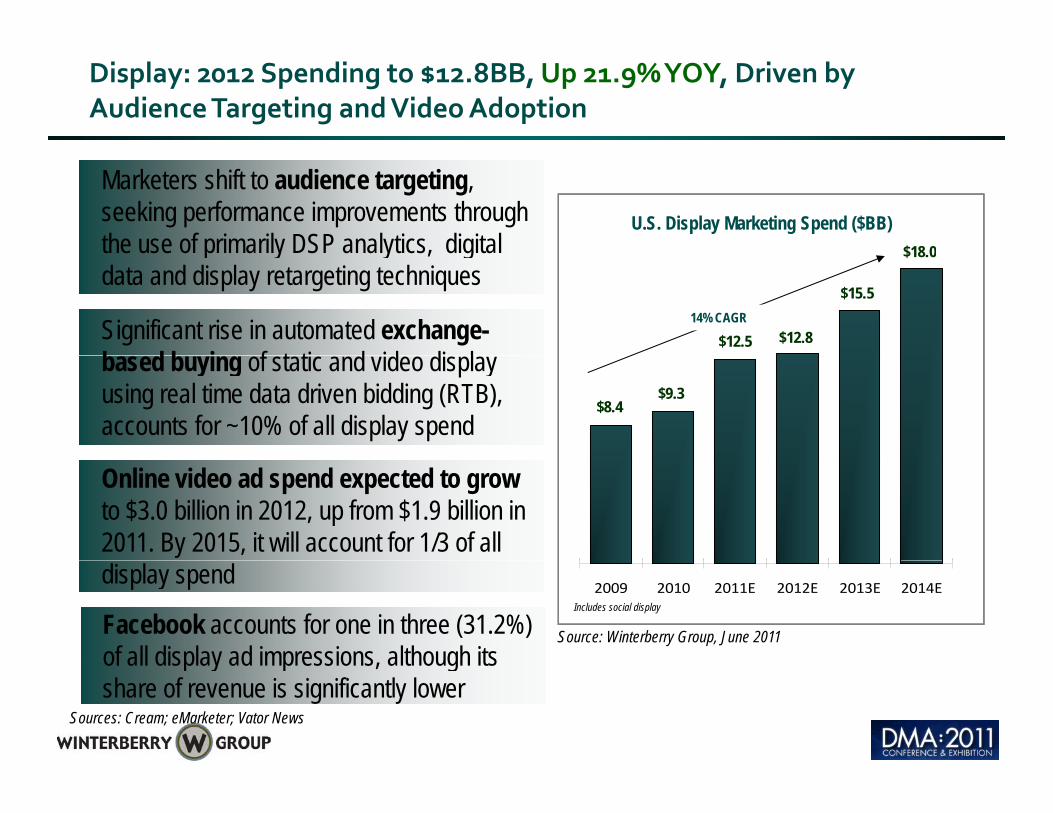

Display: 2012 Spending to $12.8BB, Up 21.9% YOY, Driven by Audience Targeting and Video Adoption

Marketers shift to audience targeting, seeking performance improvements through the use of primarily DSP analytics, digital $18 0

U.S. Display Marketing Spend ($BB)

Significant rise in automated exchange-b d b i f t ti d id di l

the use of primarily DSP analytics, digital data and display retargeting techniques

$15.5

$18.0

$12.5 $12.814% CAGR

based buying of static and video display using real time data driven bidding (RTB), accounts for ~10% of all display spend

$8.4$9.3

Online video ad spend expected to growto $3.0 billion in 2012, up from $1.9 billion in 2011. By 2015, it will account for 1/3 of all display spend

Facebook accounts for one in three (31.2%) of all display ad impressions, although its

Source: Winterberry Group, June 2011

2009 2010 2011E 2012E 2013E 2014EIncludes social display

Sources: Cream; eMarketer; Vator News

of all display ad impressions, although its share of revenue is significantly lower

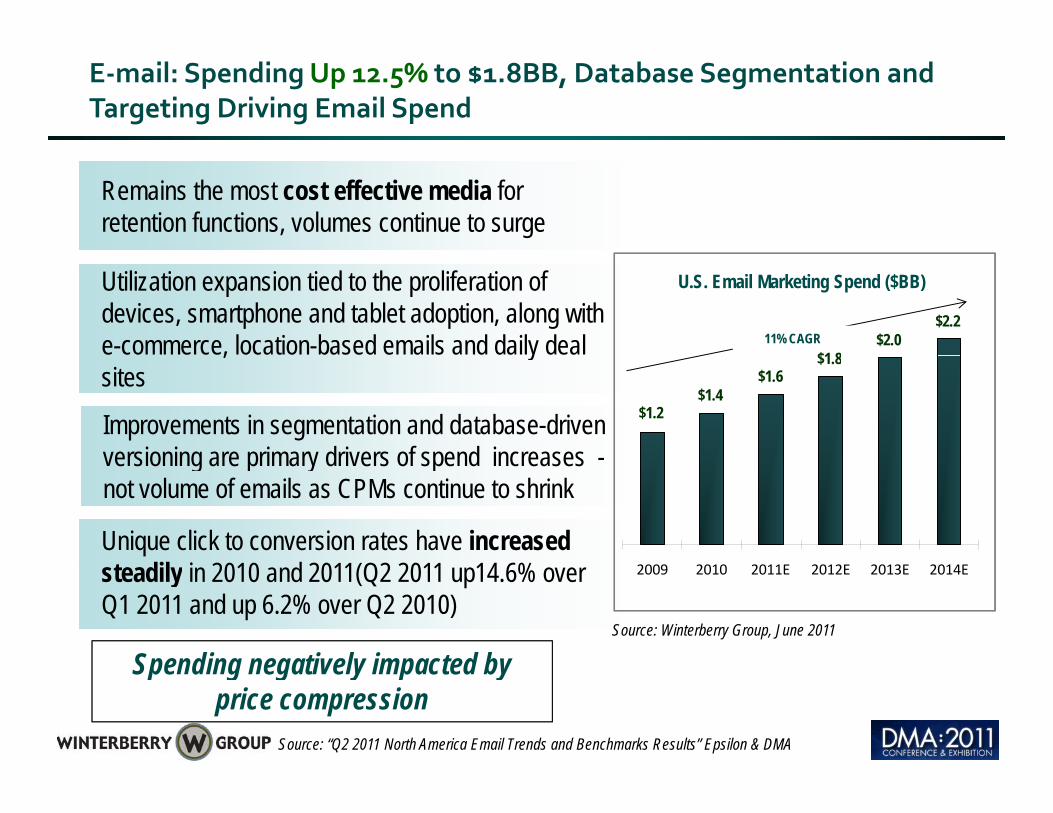

E‐mail: Spending Up 12.5% to $1.8BB, Database Segmentation and Targeting Driving Email Spend

Remains the most cost effective media for retention functions, volumes continue to surge

Utilization expansion tied to the proliferation of devices, smartphone and tablet adoption, along with e-commerce, location-based emails and daily deal $2.0

$2.2

$1 811% CAGR

U.S. Email Marketing Spend ($BB)

Improvements in segmentation and database-driven versioning are primary drivers of spend increases -

, ysites

$1.2$1.4

$1.6$1.8

versioning are primary drivers of spend increases -not volume of emails as CPMs continue to shrink

Unique click to conversion rates have increased steadily in 2010 and 2011(Q2 2011 up14.6% over Q1 2011 and up 6.2% over Q2 2010)

Spending negatively impacted by

2009 2010 2011E 2012E 2013E 2014E

Source: Winterberry Group, June 2011

Spending negatively impacted by price compression

Source: “Q2 2011 North America Email Trends and Benchmarks Results” Epsilon & DMA

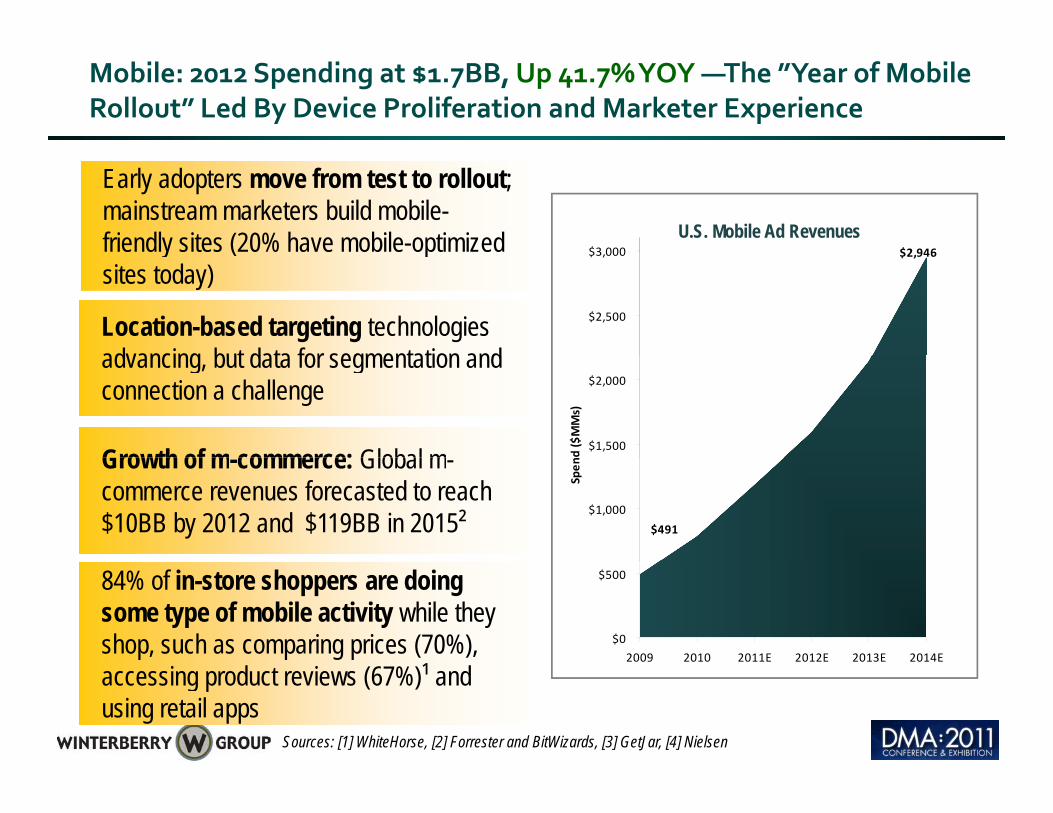

Mobile: 2012 Spending at $1.7BB, Up 41.7% YOY —The ”Year of Mobile Rollout” Led By Device Proliferation and Marketer Experience

$2 946$3 000U.S. Mobile Ad Revenues

Early adopters move from test to rollout; mainstream marketers build mobile-friendly sites (20% have mobile-optimized

Location-based targeting technologies advancing but data for segmentation and

$2,946

$2,500

$3,000y ( psites today)

advancing, but data for segmentation and connection a challenge

Growth of m commerce: Global m$1,500

$2,000

d ($MMs)

Growth of m-commerce: Global m-commerce revenues forecasted to reach $10BB by 2012 and $119BB in 2015² $491

$1,000

Spen

84% of in-store shoppers are doing some type of mobile activity while they shop, such as comparing prices (70%), $0

$500

2009 2010 2011E 2012E 2013E 2014E

accessing product reviews (67%)¹ and using retail apps

Sources: [1] WhiteHorse, [2] Forrester and BitWizards, [3] GetJar, [4] Nielsen

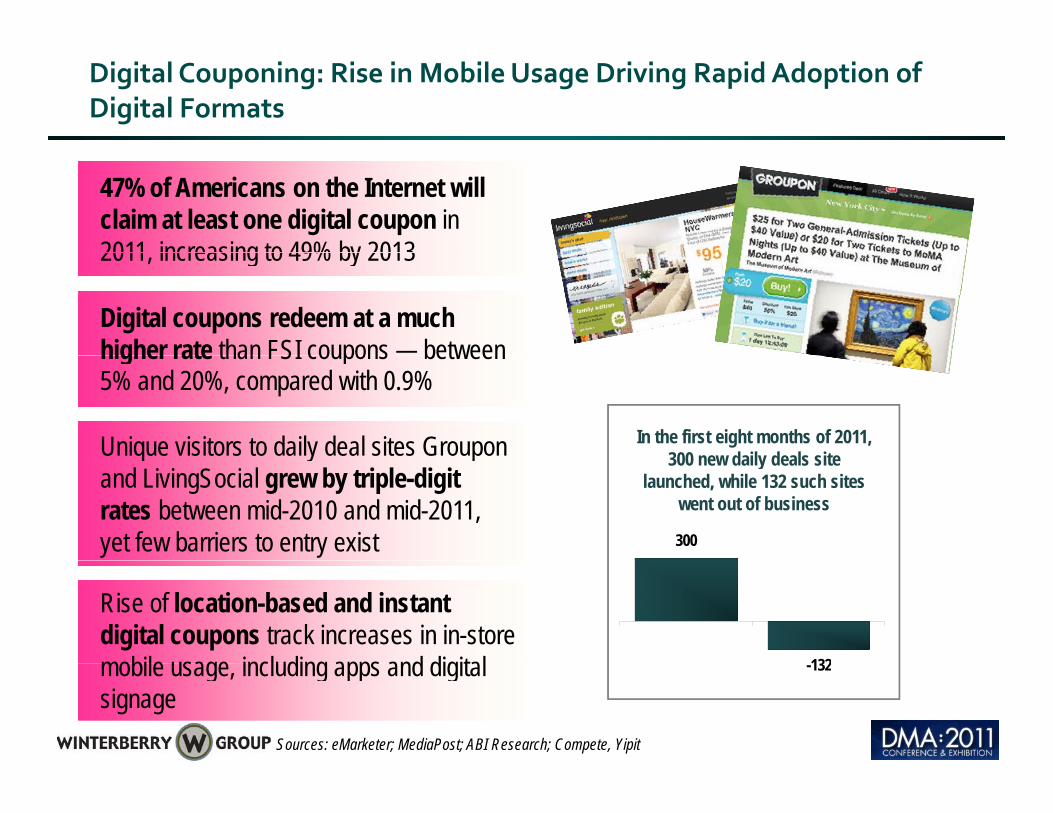

Digital Couponing: Rise in Mobile Usage Driving Rapid Adoption of Digital Formats

47% of Americans on the Internet will claim at least one digital coupon in 2011 increasing to 49% by 20132011, increasing to 49% by 2013

Digital coupons redeem at a much higher rate than FSI coupons — between

Unique visitors to daily deal sites Groupon

higher rate than FSI coupons between 5% and 20%, compared with 0.9%

In the first eight months of 2011, 300 new daily deals site q y p

and LivingSocial grew by triple-digit rates between mid-2010 and mid-2011, yet few barriers to entry exist 300

300 new daily deals site launched, while 132 such sites

went out of business

Rise of location-based and instant digital coupons track increases in in-store mobile usage including apps and digital 132

Sources: eMarketer; MediaPost; ABI Research; Compete, Yipit

mobile usage, including apps and digital signage

-132

Social Media: 2012 U.S. Ad Revenues Up 27.7% YOY to $3.9BB, Growth Slows But Brand Dollars Accelerate

Social media revenue ramps (31.6% forecast CAGR through 2015) from multiple streams:

Coming Soon?

Social adoption and time spent slows:i l di f ti t i l

subscription, social currency and advertising

social media fatigue sets in among some early adopters, leading to fewer unique visitors and less time spent on social network sitesHigh valuations are likely to come down as advertisers decide where to place their social dollars. Facebook and LinkedIn may catch up t th i ito their revenue promise

Marketers increasing investment focus in social media analytics to address concerns yover ROI and measurability

Sources: BIA/Kelsey; eMarketer; Nielsen Wire; Bizo

65% of Marketers Say Social is The Channel They Will Focus On Most in the Next 12 Months: Are They Asking the Right Questions?

As social media matures and becomes part of the fabric of everyday life, marketers must ask themselves marketers must ask themselves fundamental questions….

Wh I i i l di ?•Why am I using social media?•How do I increase engagement?•How do I increase modernization? Social Media for

M k ti P •How do I measure social media? •Should I focus on branding or direct response?

Marketing Purposes is About…

Source: Bizo

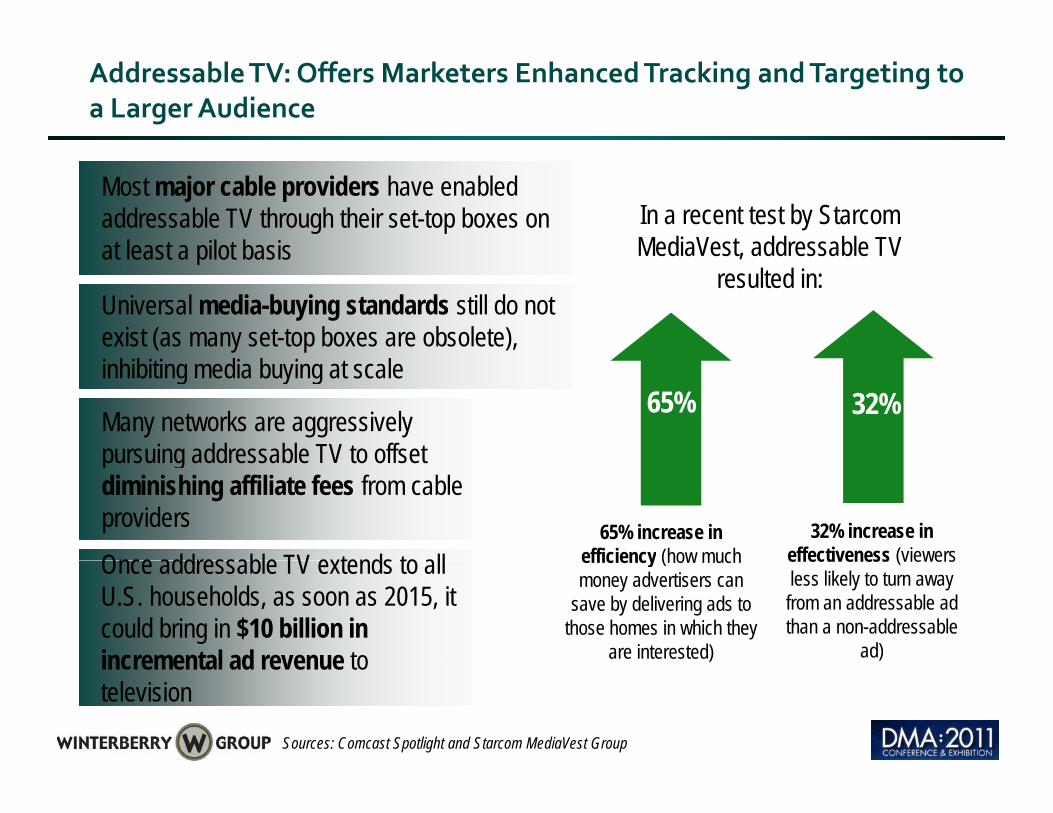

Addressable TV: Offers Marketers Enhanced Tracking and Targeting to a Larger Audience

Most major cable providers have enabled addressable TV through their set-top boxes on at least a pilot basis

In a recent test by Starcom MediaVest addressable TV at least a pilot basis MediaVest, addressable TV

resulted in: Universal media-buying standards still do not exist (as many set-top boxes are obsolete),

Many networks are aggressively pursuing addressable TV to offset

inhibiting media buying at scale65% 32%

pursuing addressable TV to offset diminishing affiliate fees from cable providers

Once addressable TV extends to all 65% increase in

efficiency (how much 32% increase in

effectiveness (viewers Once addressable TV extends to all U.S. households, as soon as 2015, it could bring in $10 billion in incremental ad revenue to

efficiency (how much money advertisers can

save by delivering ads to those homes in which they

are interested)

effectiveness (viewers less likely to turn away from an addressable ad than a non-addressable

ad)

Sources: Comcast Spotlight and Starcom MediaVest Group

incremental ad revenue to television

Agenda

Outlook 2012

What happened in 2011?

2012 Channel Check: The evolution of direct and digital

Changing Data Landscape

9for12: What You Should 9for12: What You Should Consider for 2012

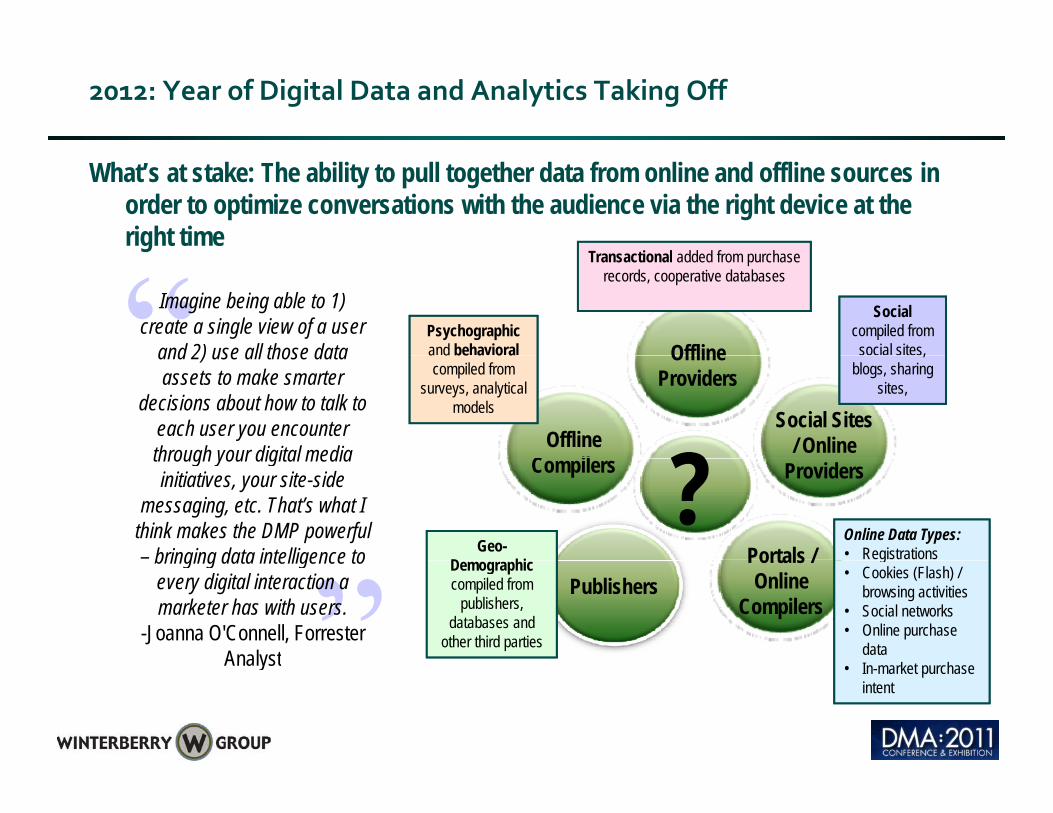

2012: Year of Digital Data and Analytics Taking Off

What’s at stake: The ability to pull together data from online and offline sources in order to optimize conversations with the audience via the right device at the right time

T ti l dd d f h

Offline

Imagine being able to 1) create a single view of a user

and 2) use all those data Psychographicand behavioral

Socialcompiled from

social sites,

Transactional added from purchase records, cooperative databases

Offline Providers

Offline C il

Social Sites / Online

and 2) use all those data assets to make smarter

decisions about how to talk to each user you encounter through your digital media

a d be a o acompiled from

surveys, analytical models

,blogs, sharing

sites,

?Compilers Providers

Portals /

through your digital media initiatives, your site-side

messaging, etc. That’s what I think makes the DMP powerful – bringing data intelligence to Geo-

D hi

Online Data Types:• Registrations

?Publishers

Portals / Online

Compilers

bringing data intelligence to every digital interaction a marketer has with users.

-Joanna O'Connell, Forrester Analyst

Demographiccompiled from

publishers, databases and

other third parties

g• Cookies (Flash) /

browsing activities• Social networks• Online purchase

dataI k t h Analyst • In-market purchase intent

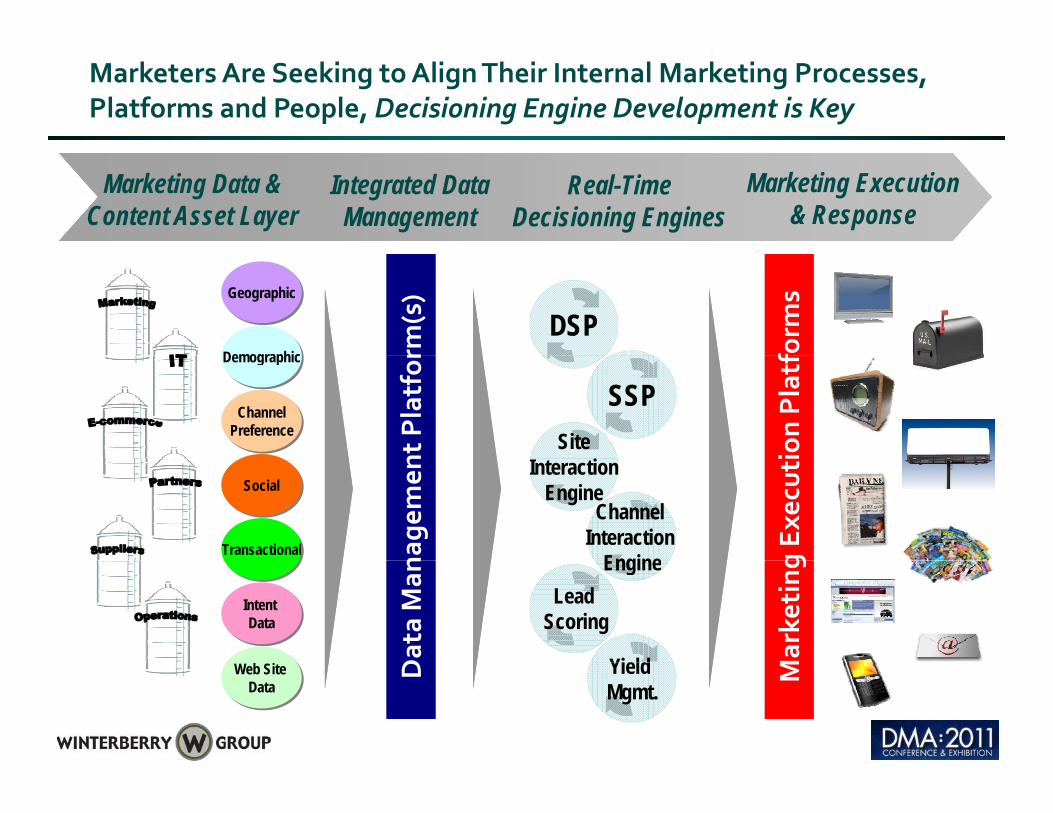

Marketers Are Seeking to Align Their Internal Marketing Processes, Platforms and People,Decisioning Engine Development is Key

Marketing Data & Content Asset Layer

Real-Time Decisioning Engines

Integrated Data Management

Marketing Execution & Response

DSP

form

s

rm(s)GeographicGeographic

D hiDemographic

Site

SSP

ion Platf

nt PlatforDemographicDemographic

ChannelPreferenceChannel

Preference

Interaction Engine

Channel Interaction

Engine g Ex

ecuti

nage

menSocialSocial

TransactionalTransactional

LeadScoring

Engine

Yield Marke

ting

Data Man

Intent Data

Intent Data

Yield Mgmt.

MDWeb Site Data

Web Site Data

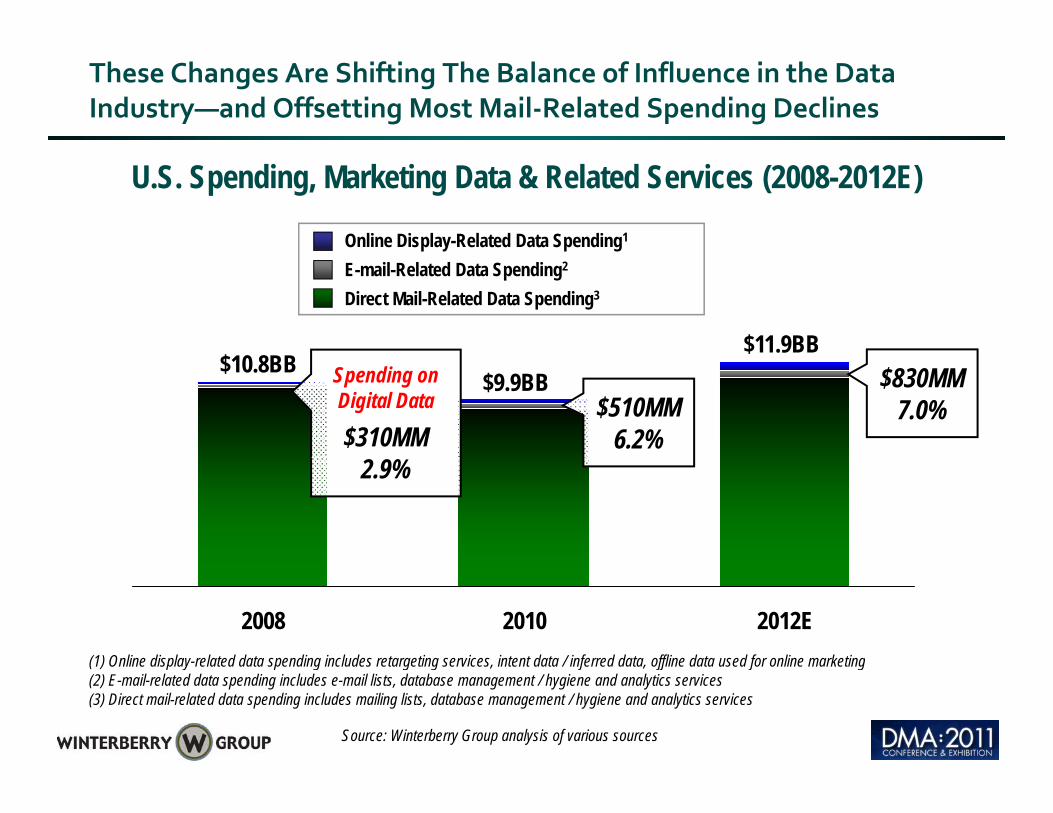

These Changes Are Shifting The Balance of Influence in the Data Industry—and Offsetting Most Mail‐Related Spending Declines

U.S. Spending, Marketing Data & Related Services (2008-2012E)

Online Display-Related Data Spending1

$10 8BB

E-mail-Related Data Spending2

Direct Mail-Related Data Spending3

$11.9BB$10.8BB

$9.9BBSpending on Digital Data

$310MM

$830MM7.0%$510MM

6.2%2.9%

2008 2010 2012E(1) Online display-related data spending includes retargeting services intent data / inferred data offline data used for online marketing(1) Online display-related data spending includes retargeting services, intent data / inferred data, offline data used for online marketing(2) E-mail-related data spending includes e-mail lists, database management / hygiene and analytics services(3) Direct mail-related data spending includes mailing lists, database management / hygiene and analytics services

Source: Winterberry Group analysis of various sources

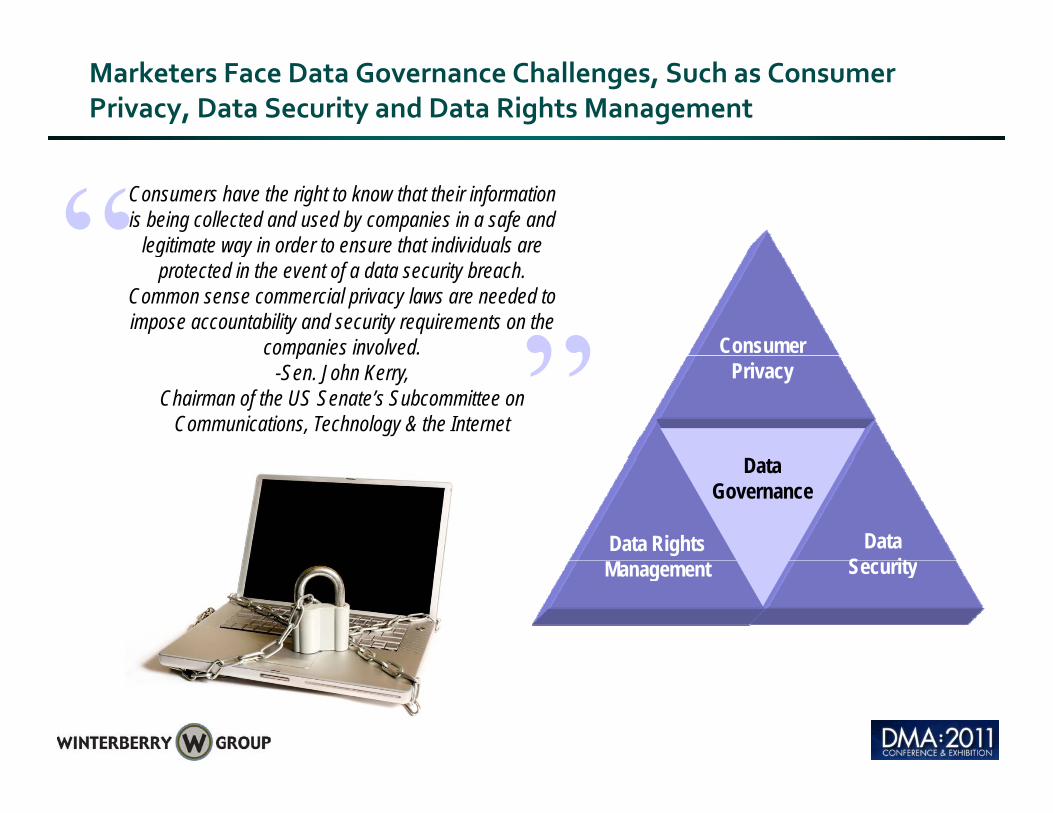

Marketers Face Data Governance Challenges, Such as Consumer Privacy, Data Security and Data Rights Management

Consumers have the right to know that their information is being collected and used by companies in a safe and

legitimate way in order to ensure that individuals are g yprotected in the event of a data security breach.

Common sense commercial privacy laws are needed to impose accountability and security requirements on the

companies involved. Consumer p-Sen. John Kerry,

Chairman of the US Senate’s Subcommittee on Communications, Technology & the Internet

Privacy

D

Data S it

Data Rights

Data Governance

SecurityManagement

Agenda

Outlook 2012

What happened in 2011?

2012 Channel Check: The evolution of direct and digital

Changing Data Landscape

9for12: What You Should 9for12: What You Should Consider for 2012

9for12

It is the (another) Year of Data: Marketers will begin to approach the growing Big Data problem, developing plans on how to manage and activate data across channels Early adopters begin

1

manage and activate data across channels. Early adopters begin to implement solutions including integrating online DMPs with offline prospect and CRM data sets to manage the conversation with disparate audiences across devices

Content is the new black: Content, recognized as the primary 2driver of engagement (along with the data that informs it), marketers and their agencies begin to wrap their arms around content marketing, including the continual creation, curation

2

content marketing, including the continual creation, curation (finding, organizing, sharing), editing and active management – in order to organize content across channels and devices – and content is just another “unstructured” form of big data to deal with content is just another unstructured form of big data to deal with

9for12

Mobile: recognizing that mobile is about devices (tablets, 3 g g ( ,smartphones, computers), location and intent, marketers accelerate the transformation of web sites from PC design (currently 80% of sites are PC only) to device specific sites tablet sites smartphone sites

3

are PC only) to device specific sites – tablet sites, smartphone sites and PC sites.

Cross digital media buying search display and email) driven by first Cross digital media buying search, display and email), driven by first, second and third party data experiences significant performance improvements as attribution solutions mature and are better able to

4

identify the impact (engagement relationships) across channels…driving more digital spend

9for12

Improved marketing technology stacks, assembled via acquisition in 2010-2011 by large tech players (IBM, Adobe, Google) release the

5in 2010 2011 by large tech players (IBM, Adobe, Google) release the first sets of integrated products, primarily for enterprise marketers, that can automate the marketing process from campaign planning through execution and attribution through execution and attribution.

USPS postal crisis is put to rest as the administration and congress accept a portion of the recommendations put forth by the postmaster general including a reduction in post offices and SCFs though the 6

6

general including a reduction in post offices and SCFs, though the 6 day week is more likely to remain in place. Force reductions will complemented by an agreement on a partial pension reform

9for12

The pace of M&A accelerates in the ad tech (digital display) sector along with continued agency consolidation of those with mobile/social

7along with continued agency consolidation of those with mobile/social specialties. Emerging attribution providers and data companies see renewed interest to complement the push towards digital cross-channel integration Smaller ad tech firms that have not gained channel integration. Smaller ad tech firms that have not gained traction experience reduced funding forcing asset sales and closures.

Privacy regulation, mostly quiet in 2011, moves back into the Washington conversation as legislators continue to examine the impact of EU privacy laws enacted this year Probable outcomes

8

impact of EU privacy laws enacted this year. Probable outcomes include data (breach) security legislation and some form of baseline privacy rules around sensitive information – though not a Do Not Track (DNT) bill.

9for12

And finally – the economy. If the US goes into a recesssion it will negatively impact all measured media channels along with direct mail

9negatively impact all measured media channels along with direct mail spend while slowing (not stopping) the rate of growth in the digital sector. Marketers will stick to longer test periods as spend tilts back towards retention marketing againtowards retention marketing again.

A neutral of low level of growth should result in the forecast i i d i thi t ti A hi h th t ill b fit envisioned in this presentation. Any higher growth rate will benefit

TV, direct mail (in addition to the bump they get with the election) and the digital media channels – while stabilizing magazine and g g gnewspaper ad spend..

Questions? Copy of the Deck?

60 Broad Street, 38th Floor60 Broad Street, 38 FloorNew York, NY 10004

www.winterberrygroup.com

Bruce BiegelManaging Director

@[email protected](212) 842-6030