Embed Size (px)

Citation preview

Building the Pearl of the GulfReal estate, hospitality and construction outlook

2 | Building the Pearl of the Gulf

Contents03 Executive summary

04 Qatar’s economy continues to grow and become more diverse, backed by sector diversification

05 Qatar’s government initiatives are driving growth

08 Implication and opportunities for Qatar’s RHC sector

13 In summary

3Building the Pearl of the Gulf |

Executive summaryRobust economic growth, strong market fundamentals and well thought-out national visions and strategies have helped set the stage for increased investment and development in an effort to propel Qatar forward. Qatar’s renewed focus has helped them win the competition to host the 2022 World Cup, which has accelerated the rate of construction and inflow of investments into infrastructure, healthcare, social housing and education — helping Qatar to accommodate future population growth.

As a result, a wide range of infrastructure projects — including rail and metro works, ports and airports are being planned or already underway. These projects will undoubtedly have a positive spill-over effect on the real estate, hospitality and construction (RHC)industry — helping to build a healthy pipeline for many years to come and enhance Qatar’s competitive position on both a regional and international level.

The primary purpose of the report is to provide the reader with a deeper understanding of some of Qatar’s visions and strategies, their potential impact on the RHC sector and the prominent role the RHC sector will play in helping make Qatar’s visions a reality.

We hope you enjoy the report and please direct any questions to the contacts at the back of the publication.

Sincerely,

Yousef Wahbah

MENA Real Estate, Hospitality and Construction Sector Leader

4 | Building the Pearl of the Gulf

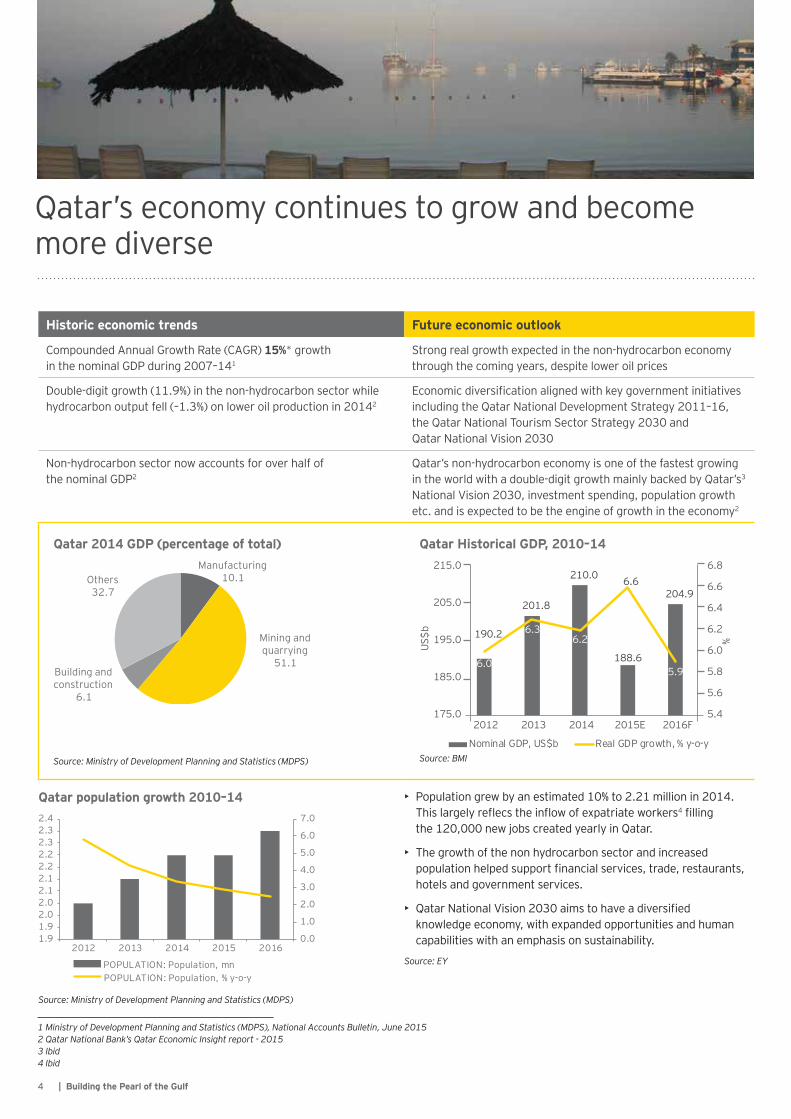

Qatar’s economy continues to grow and become more diverse

H is toric ec onom ic trends F uture ec onom ic outlook

Compounded Annual Growth Rate (CAGR) 1 5 % * growth in the nominal GDP during 2007–141

Strong real growth expected in the non-hydrocarbon economy through the coming years, despite lower oil prices

Double-digit growth (11.9%) in the non-hydrocarbon sector while hydrocarbon output fell (–1.3%) on lower oil production in 20142

Economic diversification aligned with key government initiatives including the Qatar National Development Strategy 2011–16, the Qatar National Tourism Sector Strategy 2030 and Qatar National Vision 2030

Non-hydrocarbon sector now accounts for over half of the nominal GDP2

Qatar’s non-hydrocarbon economy is one of the fastest growing in the world with a double-digit growth mainly backed by Qatar’s3 National Vision 2030, investment spending, population growth etc. and is expected to be the engine of growth in the economy2

Q atar 2 0 1 4 GD P ( p erc entage of total)Manufacturing

10.1

Mining and quarrying

51.1Building and construction

6.1

Others32.7

Source: Ministry of Development Planning and Statistics (MDPS)

Q atar H is toric al GD P, 2 0 1 0 – 1 4

190.2

201.8

210.0

188.6

204.9

6.0

6.36.2

6.6

5.9

5.4

5.6

5.8

6.0

6.2

6.4

6.6

6.8

175.0

185.0

195.0

205.0

215.0

2012 2013 2014 2015E 2016F%US

$b

Nominal GDP, US$b Real GDP growth, % y-o-ySource: BMI

Q atar p op ulation grow th 2 0 1 0 – 1 4

POPULATION: Population, mnPOPULATION: Population, % y-o-y

2012 2013 2014 2015 20160.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

1.91.92.02.02.12.12.22.22.32.32.4

Source: Ministry of Development Planning and Statistics (MDPS)

• Population grew by an estimated 10% to 2.21 million in 2014. This largely reflecs the inflow of expatriate workers4 filling the 120,000 new jobs created yearly in Qatar.

• The growth of the non hydrocarbon sector and increased population helped support financial services, trade, restaurants, hotels and government services.

• Qatar National Vision 2030 aims to have a diversified knowledge economy, with expanded opportunities and human capabilities with an emphasis on sustainability.

Source: EY

1 Ministry of Development Planning and Statistics (MDPS), National Accounts Bulletin, June 2015 2 Qatar National Bank’s Qatar Economic Insight report - 2015 3 Ibid 4 Ibid

5Building the Pearl of the Gulf |

Qatar’s government initiatives are driving growth

Q a t a r G o v e r n m e n t i n i t i a t i v e s

• Defines national values and long-term goals

• Defines national initiatives toward achievingQatar National Vision 2030 goals

• Defines sectoral priorities to be integrated into the QNDS 2011–16

• Defines ministerial plans to support implementationof sectoral strategiesMinistry and agency strategies

Sector strategies2011–16

QatarNational

Vision 2030

Qatar NationalDevelopment Strategy

2011–16

Sources: MDPS, General Secretariat for Development Planning (GSDP)

• The Qatar National Development Strategy 2011-2016 was prepared to set a path towards achieving the goals of Qatar National Vision 2030. Qatar’s National Vision helps build a bridge from the present to the future. This should help transform Qatar into an advanced country, sustaining its development, and providing a high standard of living for its people.

• The broad Qatar National Development Strategy integrates a number of sector-specific strategies aligned to Qatar National Vision 2030, outlined below.

Q atar N ational D ev elop m ent S trategy 2 0 1 1 – 1 6

Human development

Social development

Healthy and capable population

and Caring cohesive society

Environmental development

Well-managed and sustainableenvironment

Economic development

Strong and resilient economy

Institutional development and modernization

Modern and citizen-centric government

Development pillars Sector strategies

Health Employment Education andtraining

Culture Social protection

Family cohesionand women empowerment

Security and public safety

Sports

Healthy and capable population

Economicmanagement

Economic infrastructure

Natural resources

Economic diversification and private sector growth

Modern government institutions Efficient government services

Sources: MDPS, GSDP

6 | Building the Pearl of the Gulf

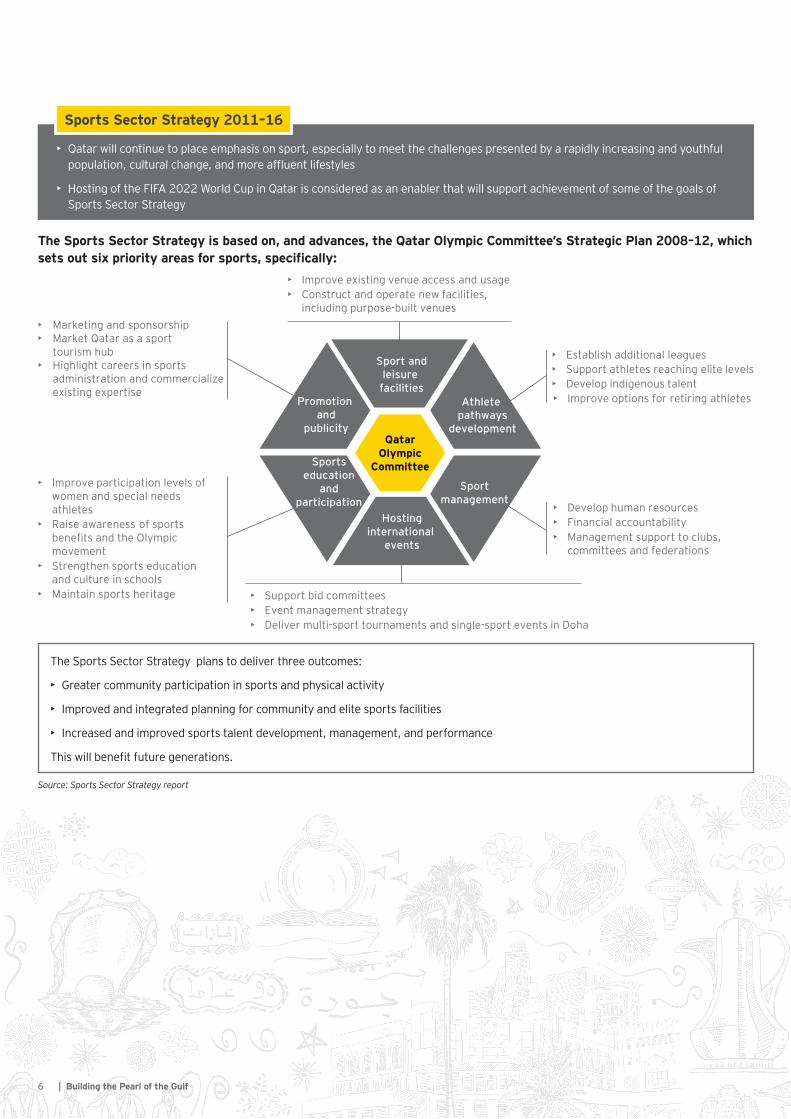

• Qatar will continue to place emphasis on sport, especially to meet the challenges presented by a rapidly increasing and youthful population, cultural change, and more affluent lifestyles

• Hosting of the FIFA 2022 World Cup in Qatar is considered as an enabler that will support achievement of some of the goals of Sports Sector Strategy

S p orts S ec tor S trategy 2 0 1 1 – 1 6

T he S p orts S ec tor S trategy is b as ed on, and adv anc es , the Q atar O ly m p ic C om m ittee’ s S trategic Plan 2 0 0 8 – 1 2 , w hic h sets out six priority areas for sports, specifically:

• Improve participation levels of women and special needs athletes

• Raise awareness of sports benefits and the Olympic movement

• Strengthen sports education and culture in schools

• Maintain sports heritage • Support bid committees• Event management strategy• Deliver multi-sport tournaments and single-sport events in Doha

• Develop human resources• Financial accountability• Management support to clubs,

committees and federations

• Establish additional leagues• Support athletes reaching elite levels• Develop indigenous talent• Improve options for retiring athletes

• Improve existing venue access and usage• Construct and operate new facilities,

including purpose-built venues• Marketing and sponsorship• Market Qatar as a sport

tourism hub• Highlight careers in sports

administration and commercialize existing expertise

Sport andleisure

facilities

Hostinginternational

events

Promotion and

publicity

Athlete pathways

development

Sports education

andparticipation

Sportmanagement

QatarOlympic

Committee

The Sports Sector Strategy plans to deliver three outcomes:

• Greater community participation in sports and physical activity

• Improved and integrated planning for community and elite sports facilities

• Increased and improved sports talent development, management, and performance

This will benefit future generations.

Source: Sports Sector Strategy report

7Building the Pearl of the Gulf |

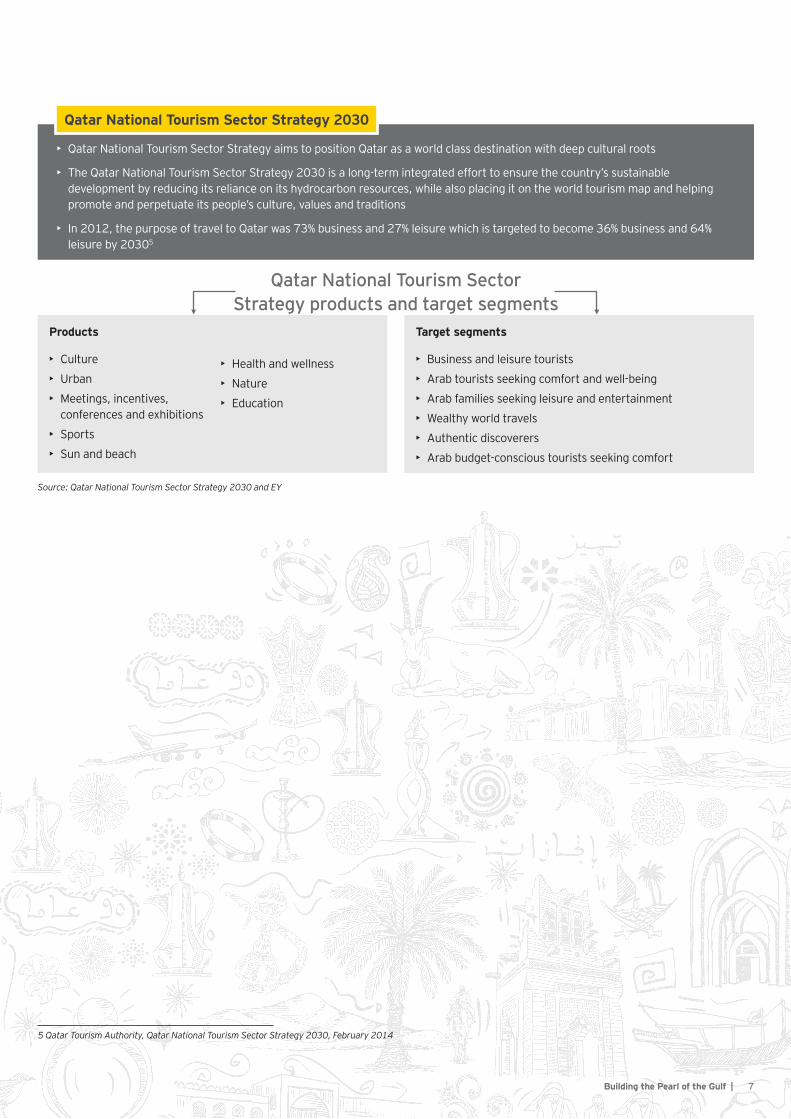

• Qatar National Tourism Sector Strategy aims to position Qatar as a world class destination with deep cultural roots

• The Qatar National Tourism Sector Strategy 2030 is a long-term integrated effort to ensure the country’s sustainable development by reducing its reliance on its hydrocarbon resources, while also placing it on the world tourism map and helping promote and perpetuate its people’s culture, values and traditions

• In 2012, the purpose of travel to Qatar was 73% business and 27% leisure which is targeted to become 36% business and 64% leisure by 20305

Q atar N ational T ouris m S ec tor S trategy 2 0 3 0

Produc ts

• Culture

• Urban

• Meetings, incentives, conferences and exhibitions

• Sports

• Sun and beach

• Health and wellness

• Nature

• Education

T arget s egm ents

• Business and leisure tourists

• Arab tourists seeking comfort and well-being

• Arab families seeking leisure and entertainment

• Wealthy world travels

• Authentic discoverers

• Arab budget-conscious tourists seeking comfort

Q a t a r N a t i o n a l T o u r i s m S e c t o r S t r a t e g y p r o d u c t s a n d t a r g e t s e g m e n t s

Source: Qatar National Tourism Sector Strategy 2030 and EY

5 Qatar Tourism Authority, Qatar National Tourism Sector Strategy 2030, February 2014

8 | Building the Pearl of the Gulf

Q a t a r ’ s R H C s e c t o r o v e r v i e wKey government initiatives and Qatar’s hosting of the 2020 World Cup should bode well for the RHC sector

Qatar’s real estate prices are expected to continue to grow, although at a more moderate pace

Sector open to international private sector involvement Large-scale infrastructure projects are being planned or are underway — US$200b expected investment in infrastructure, tourism and sports projects6

Source: MEED

Q a t a r c o n s t r u c t i o n / i n f r a s t r u c t u r e m a r k e t• Qatar’s construction industry is performing above predictions, helping to alleviate concerns about the country’s ability to host the FIFA

World Cup in 2022.

• Government spending and public sector firms are supporting Qatar’s infrastructure investments. The National Development Strategy has allotted 40% of the state budget for backing infrastructure projects for 2011–16.

• Qatar is on the expansion mode with sufficient budgets allocated for stadiums for the FIFA 2022 World Cup, medical centers and Qatar’s extensive roads program. The Government is keen to speed up its large infrastructure investment program, following a large number of project delays and poor execution.

C ons truc tion indus try v alue ( 2 0 1 2 – 1 6 f)

CAGR 14% during 2012–16f

8.59.7

11.914.0

16.4

4.4 4.85.7

7.4

8.0

0.01.02.03.04.05.06.07.08.09.0

0.02.04.06.08.0

10.012.014.016.018.0

2012 2013 2014 2015E 2016F

%US$b

Construction industry value, US$bConstruction Industry Value, % of GDP

Source: BMI

K ey infras truc ture p roj ec ts

1 Q atar’ s national rail netw ork

3 5 0 k m U S $ 9 . 1 b

• Qatar’s main industrial and residential hubs will be connected via high-speed passenger rail and freight services through this link.

• This project isn’t scheduled to be completed until 2029.

2 Three tree-shaded corridors free of car traffic — D oha a greener c ity

• Two green infrastructure plans — a new residential area and a commercial zone.

• A third parcel for mixed use which is expected to be completed by 2016.

Source: EY

Implication and opportunities for Qatar’s RHC sector

6 MEED 2014, http://www.meedconferences.com/qatar/

9Building the Pearl of the Gulf |

Q a t a r r e s i d e n t i a l m a r k e t • It’s been a dynamic year for the Qatar real estate market.

The overall Qatari market felt inflationary pressures in addition to the volume of transactions and increased land values.

• The Qatar Statistics Authority stated that the population grew by 9.5% during the period from March 2014 to March 2015.

• Growth in population created a lot of jobs in the non-hydrocarbon sectors, which also resulted in an increase in demand for family accommodation, especially four and five bedroom villas. Currently occupancy rates are high according to DTZ’s Q1 2015 report.

• Colliers International estimated that the number of housing units will exceed 129,200 by the end of 2014 and an additional 8,200 units were expected to enter the market between 2015–2018. Despite annual increases in supply, high population growth rates are expected to result in an undersupplied market. Supply scarcity in Doha’s housing market offers a strong foundation.

• Average rental rates in Doha increased over the last three years, increasing by 14% in 2014 according to Colliers International.

• Housing affordability is becoming an issue.

• The real estate sector was robust following heavy investment in infrastructure and property development. The new metro in Doha is one of the major infrastructure projects and some of the real estate development projects include Musheireb and Lusail City.

D oha R es idential D em and and S up p ly

0

50,000

100,000

150,000

200,000

250,000

300,000

2010 2011 2012 2013 2014 2015 2016 2017 2018

No.

of U

nits

Under Supply DemandSource: Colliers International

A v erage A p artm ent R ental R ates ac ros s D oha

875

745634 614 639

700799

-15.0%-15.0%

-3.0%

4.0%10.0%

14.0%

-20.00%

-15.00%

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

20.00%

0100200300400500600700800900

1000

2008 2009 2010 2011 2012 2013 2014

YO

Y%

Gro

wth

QA

R p

er m

2 p.a

.

YOY Growth QAR per m2 p.a.Source: Colliers International

Key highlights: Government initiatives, vision and strategies positively affecting the Qatar residential market

• Barwa and Qatari Diar made around US$274b investments in residential and business construction projects during 2011–16

• Plans to have a program of permanent residency for expatriates meeting predetermined criteria

• To establish a tribunal for resolving labor disputes

1

2

Qatarcompanies'investments

Permanentresidency

1 0 | Building the Pearl of the Gulf

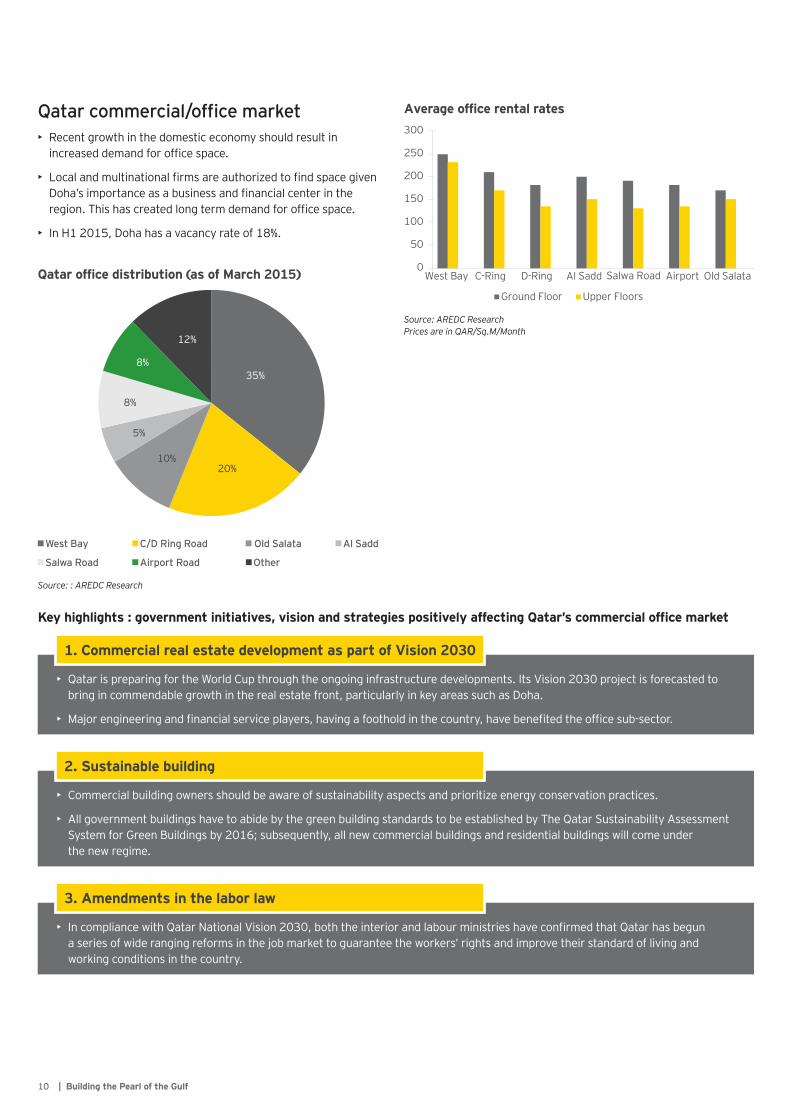

Qatar commercial/office market• Recent growth in the domestic economy should result in

increased demand for office space.

• Local and multinational firms are authorized to find space given Doha’s importance as a business and financial center in the region. This has created long term demand for office space.

• In H1 2015, Doha has a vacancy rate of 18%.

Q atar offic e dis trib ution ( as of M arc h 2 0 1 5 )

West Bay C/D Ring Road Old Salata Al Sadd

Salwa Road Airport Road Other

35%

20%10%

5%

8%

8%

12%

Source: : AREDC Research

A v erage offic e rental rates

0

50

100

150

200

250

300

West Bay C-Ring D-Ring Al Sadd Salwa Road Airport Old Salata

Ground Floor Upper Floors

Source: AREDC ResearchPrices are in QAR/Sq.M/Month

Key highlights : government initiatives, vision and strategies positively affecting Qatar’s commercial office market

• Qatar is preparing for the World Cup through the ongoing infrastructure developments. Its Vision 2030 project is forecasted to bring in commendable growth in the real estate front, particularly in key areas such as Doha.

• Major engineering and financial service players, having a foothold in the country, have benefited the office sub-sector.

1 . C om m erc ial real es tate dev elop m ent as p art of V is ion 2 0 3 0

• Commercial building owners should be aware of sustainability aspects and prioritize energy conservation practices.

• All government buildings have to abide by the green building standards to be established by The Qatar Sustainability Assessment System for Green Buildings by 2016; subsequently, all new commercial buildings and residential buildings will come under the new regime.

2 . S us tainab le b uilding

• In compliance with Qatar National Vision 2030, both the interior and labour ministries have confirmed that Qatar has begun a series of wide ranging reforms in the job market to guarantee the workers’ rights and improve their standard of living and working conditions in the country.

3 . A m endm ents in the lab or law

1 1Building the Pearl of the Gulf |

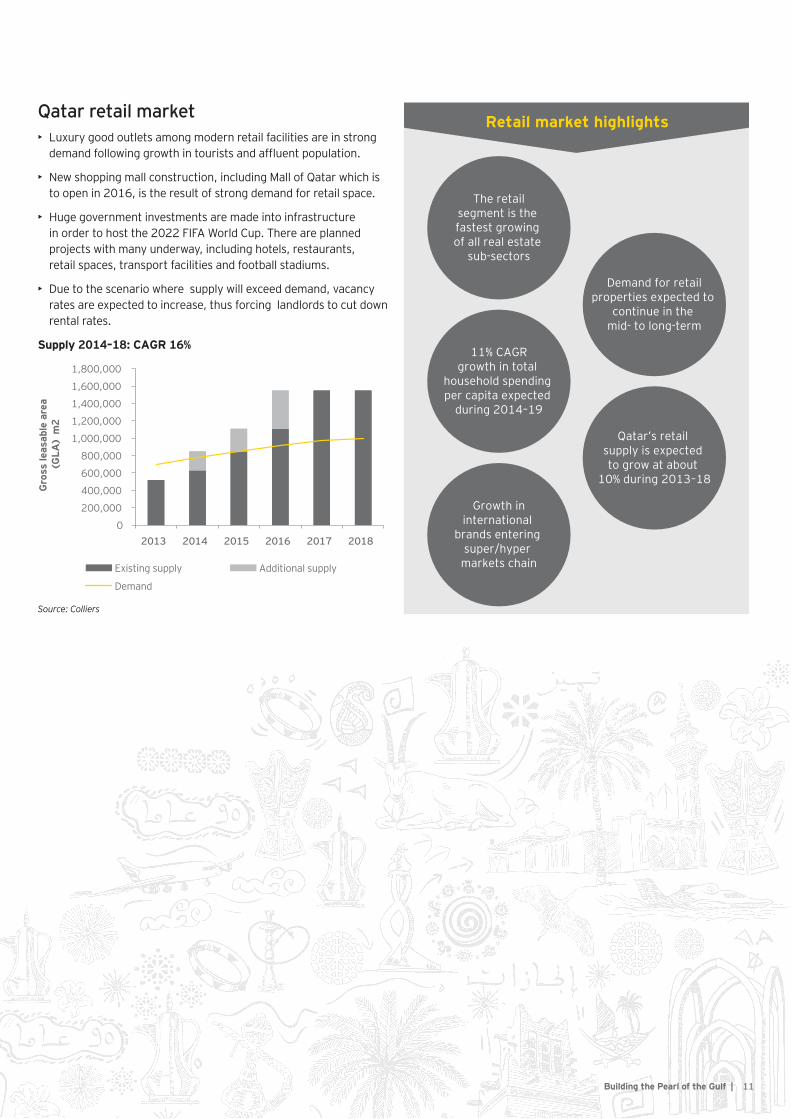

Q a t a r r e t a i l m a r k e t• Luxury good outlets among modern retail facilities are in strong

demand following growth in tourists and affluent population.

• New shopping mall construction, including Mall of Qatar which is to open in 2016, is the result of strong demand for retail space.

• Huge government investments are made into infrastructure in order to host the 2022 FIFA World Cup. There are planned projects with many underway, including hotels, restaurants, retail spaces, transport facilities and football stadiums.

• Due to the scenario where supply will exceed demand, vacancy rates are expected to increase, thus forcing landlords to cut down rental rates.

Supply 2014–18: CAGR 16%

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1,800,000

2013 2014 2015 2016 2017 2018

Gro

ss le

asab

le a

rea

(GLA

) m

2

Existing supply Additional supply

Demand

Source: Colliers

The retailsegment is the fastest growing of all real estate

sub-sectors

Demand for retailproperties expected to

continue in the mid- to long-term

11% CAGRgrowth in total

household spending per capita expected

during 2014–19

Qatar’s retail supply is expected to grow at about

10% during 2013–18

Growth ininternational

brands entering super/hyper

markets chain

Retail market highlights

1 2 | Building the Pearl of the Gulf

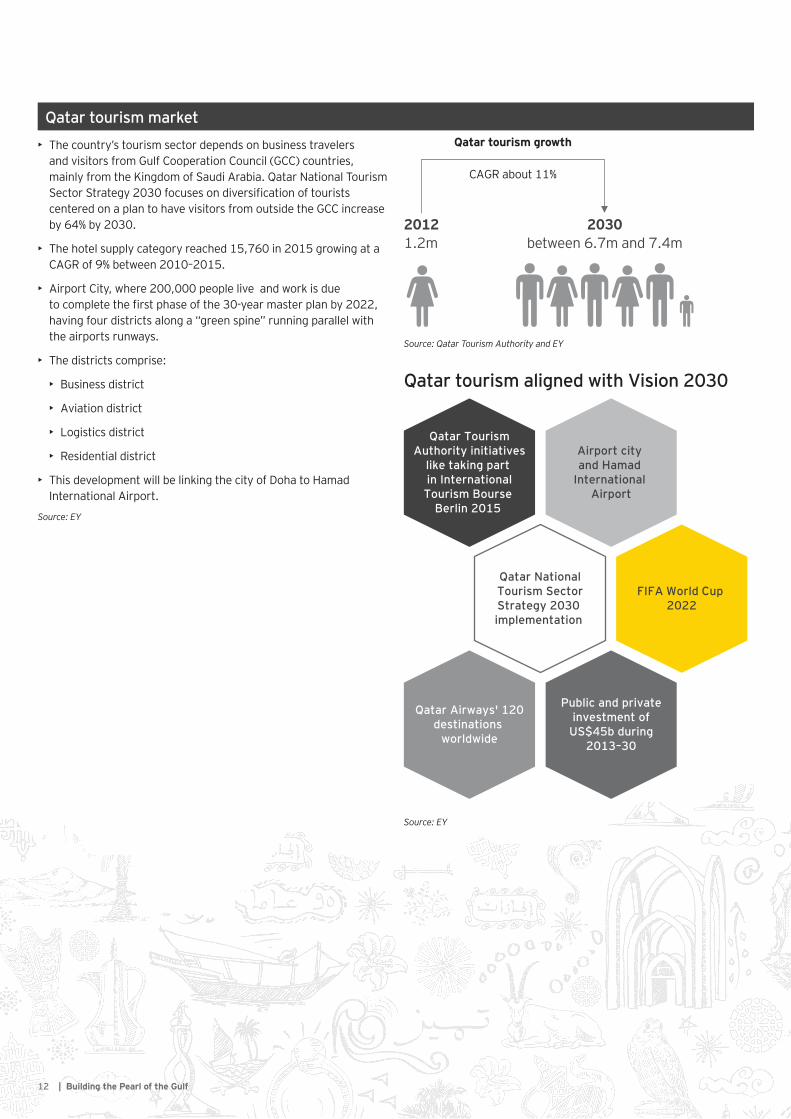

Q a t a r t o u r i s m m a r k e t

• The country’s tourism sector depends on business travelers and visitors from Gulf Cooperation Council (GCC) countries, mainly from the Kingdom of Saudi Arabia. Qatar National Tourism Sector Strategy 2030 focuses on diversification of tourists centered on a plan to have visitors from outside the GCC increase by 64% by 2030.

• The hotel supply category reached 15,760 in 2015 growing at a CAGR of 9% between 2010–2015.

• Airport City, where 200,000 people live and work is due to complete the first phase of the 30-year master plan by 2022, having four districts along a “green spine” running parallel with the airports runways.

• The districts comprise:

• Business district

• Aviation district

• Logistics district

• Residential district

• This development will be linking the city of Doha to Hamad International Airport.

Source: EY

2 0 1 2 2 0 3 01.2m between 6.7m and 7.4m

Q atar touris m grow th

CAGR about 11%

Source: Qatar Tourism Authority and EY

Q a t a r t o u r i s m a l i g n e d w i t h V i s i o n 2 0 3 0

Airport city and Hamad

International Airport

FIFA World Cup 2022

Public and privateinvestment of

US$45b during2013–30

Qatar Airways' 120destinations

worldwide

Qatar NationalTourism SectorStrategy 2030 implementation

Qatar TourismAuthority initiatives

like taking part in InternationalTourism Bourse

Berlin 2015

Source: EY

1 3Building the Pearl of the Gulf |

With Qatar being one of the fastest-growing economies in the world and having a population that earns some of the world’s largest disposable income, investors have focused on Qatar. The country is determined to embark on its National Vision 2030, to help diversify its economy from oil and gas dependency. Efforts would be made to route its rich gas surplus into investments to expand and diversify its key sectors, upgrade its infrastructure and thus place the country on the world map as a leading destination for tourists and investors.

This has created significant opportunities for the RHC sector. Construction of required infrastructure to accommodate the future population growth has been carefully planned to provide necessary residential, commercial, hotel and retail buildings with necessary power and energy framework. This ensures projects are completed without any bottlenecks or shortages.

This, combined with Qatar’s commitment to implementing its key government visions and strategies, should positively impact the RHC sector going forward.

In summary

T o u r i s m a n d H o s p i t a l i t y :Tourism product diversification is a primary consideration for the QTA which is also looking to expand the hospitality and tourism offering outside of Doha. Current hotel supply remains skewed towards the five-star segment despite recent price sensitivity witnessed among regional travelers. Five-star hotels have experienced rate pressure over the past two-year period as the macro-economic environment shifted consumer preferences making it difficult for 5-star hotels to command a significant premium over their 4-star counterparts. Over the short to medium-term, the demand for business, budget and economy hotels is expected to continue to out pace supply.

Concerns remain in regards to oversupply of hotel accommodation post FIFA 2022 prompting the QTA to explore temporary accommodation models. However, practical challenges remain in implementing such models particularly within the legal and time frame constraints present.

Office:Despite the expectation that infrastructure and tourism investment would drive demand for office space within Qatar, the office market performance remains subdued. The primary cause is ostensibly related to rental rates sought by landlords and a lack of well-priced quality office space resulting in tenants delaying the decision to move. The current office pipeline is heavily skewed towards Grade A office space which is expected to place price pressure on landlords and induce a flight to quality by tenants bringing the office market in Doha towards equilibrium. Despite a tendency among key developers to delay new supply in order to retain pricing power, the inevitable delivery pressures from lenders, government authorities, and investors will likely mean that all current supply under development will be completed in the short- to medium-term.

R e t a i l :Historically, Doha was a significantly under-supplied retail market leading to significant investment in organized retail over the last decade. Traditionally residential focused developers benefited from diversification while meeting the needs of a rapidly rising population. Looking ahead, the retail sector is expected to see significant supply additions in the medium to long term far out-pacing population growth leading to risks of oversupply. With the threat of new supply, current landlords are looking at capital improvement plans to mitigate the competitive risk and maintain market share. By 2020 when the last of the current proposed supply is expected to enter the market Doha’s GLA per capita will rival that of established tourism destinations such as Manhattan and Dubai.

R e s i d e n t i a l :Traditionally considered a safe bet thanks to a rapidly growing population base and chronic under-supply developers have historically favored quantity over quality. Going forward, tapering population growth, reduced affordability and a larger share of the population identifying towards the upper tier income strata is expected to drive a shift towards quality. Layered within this dynamic is the anticipated delivery of significant residential supply to market over the next three years placing added pressure on landlords and reducing their pricing power whilst also driving tenants towards better quality housing.

Future outlook

A b o u t E Y ’ s G l o b a l R e a l E s t a t e S e c t o r

Today’s real estate sector must adopt new approaches to address regulatory requirements and financial risks while meeting the challenges of expanding globally and achieving sustainable growth. EY’s Global Real Estate Sector brings together a worldwide team of professionals to help you succeed — a team with deep technical experience in providing assurance, tax, transaction and advisory services. The Sector team works to anticipate market trends, identify their implications and develop points of view on relevant sector issues. Ultimately, this team enables us to help you meet your goals and compete more effectively.

E Y r o l e

EY’s real estate, hospitality and construction sector has been helping clients with development advisory services for the last two decades, including the development of West Bay in the early 2000’s and Lusail at present. Owners, developers, investors and lenders have sought our services for highest-and-best-use studies, master plan reviews, valuations, operator search and selection and strategic support around transactions or internal restructurings. In addition, EY’s real estate, hospitality and construction sector added project management to its services offering across MENA to ensure we can support you throughout your development life cycle.

E Y | Assurance | Tax | Transactions | Advisory

A b o u t E YEY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

The MENA practice of EY has been operating in the region since 1923. For over 90 years, we have grown to over 5,000 people united across 20 offices and 15 countries, sharing the same values and an unwavering commitment to quality. As an organization, we continue to develop outstanding leaders who deliver exceptional services to our clients and who contribute to our communities. We are proud of our accomplishments over the years, reaffirming our position as the largest and most established professional services organization in the region.

© 2016 EYGM Limited. All Rights Reserved.

EYG no. DF0238

ED NoneThis material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax or other professional advice. Please refer to your advisors for specific advice.

e y . c o m / m e n a

K e y c o n t a c tY ous ef W ahb ahMENA Real Estate, Hospitality and Construction Sector Leader T: +971 4 312 9113 E: [email protected]

F adi M aroufMENA Real Estate, Hospitality and Construction Advisory Leader T: +971 4 701 0952 E: [email protected]

Z iad N aderAssurance Partner T: +974 4 457 4130 E: [email protected]

M arc el K erk v lietTax Partner T: +974 4 457 4201 E: [email protected]