Embed Size (px)

Citation preview

BUILDING THE RISK BASED AUDIT PLANSPEAKERS:CAROLYN SAINT, VICE PRESIDENT, INTERNAL AUDIT, 7-ELEVENPATRICK POTTER, GRC STRATEGIST, RSAMELISSA BAYER, PROCESS & STRATEGIC EXCELLENCE AND GOVERNANCE, RISK MANAGEMENT & ASSURANCE LEADER, BANK OF AMERICACAROLE SWITZER, PRESIDENT, OCEG

OCEG WEBINAR SERIESSeptember 18, 2014

Discussion Participants

Patrick Potter, GRC Strategist,

RSA

Carolyn Saint, Vice President,

Internal Audit, 7-Eleven

Carole Switzer, President,

OCEG

Melissa Bayer, Process

& Strategic Excellence and Governance,

Risk Management &

Assurance Leader, Bank of

America

Housekeeping

Download slides at http://www.oceg.org/event/building-the-risk-based-audit-plan/

Answer all 3 polls Certificates of completion (only for OCEG

Premium/Enterprise members and All-Access Pass holders)

Evaluation survey at the close of the webinar

Archive at Recorded Events on OCEG site

Learning Objectives

Define how to use risk and compliance capabilities to improve and define audit plans and processes

Identify example key risk indicators (KRIs) and key compliance indicators (KCIs) that may impact audit priorities or timing

Develop a maturity lifecycle for risk based audit planning

The role of internal audit, especially in large, geographically diverse organizations has become more complex. What are the greatest challenges in developing a meaningful entity-wide audit plan today?

Panelist Question #1

Carole SwitzerCarolyn SaintPatrick PotterMelissa Bayer

POLL #1

How do you go about defining and prioritizing the auditable entities in your organization?

Panelist Question #2

Carole SwitzerCarolyn SaintPatrick PotterMelissa Bayer

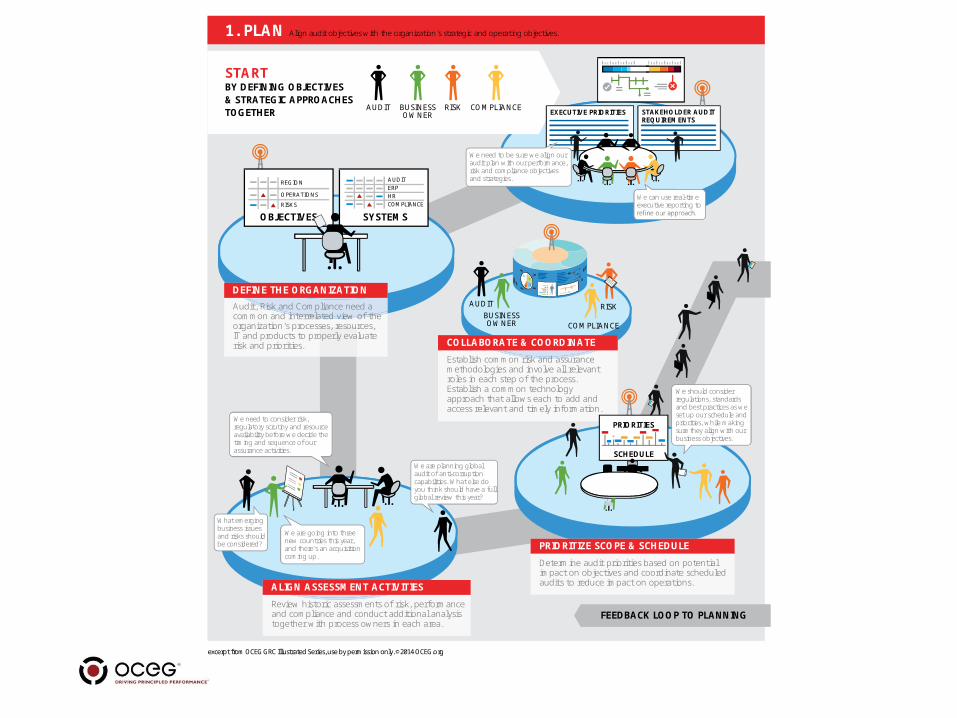

1. PLAN Align audit objectives with the organization's strategic and operating objectives.

STAKEHOLDER AUDITREQUIREMENTS

We can use real-timeexecutive reporting to

We need to consider risk,regulatory scrutiny and resourceavailability before we decide thetiming and sequence of ourassurance activities.

We are going into threenew countries this year,and there's an acquisitioncoming up.

We are planning globalaudit of anti-corruptioncapabilities. What else doyou think should have a fullglobal review this year?

OBJECTIVES

REGION

OPERATIONS

RISKS

SYSTEMS

AUDITERPHRCOMPLIANCE

STARTBY DEFINING OBJECTIVES&STRATEGIC APPROACHESTOGETHER EXECUTIVE PRIORITIES

What emergingbusiness issuesand risks shouldbe considered?

FEEDBACK LOOPTO PLANNING

We need to be sure we align ouraudit plan with our performance,risk and compliance objectivesand strategies.

We should considerregulations, standardsand best practices as weset up our schedule andpriorities, while makingsure they align with ourbusiness objectives.

excerpt from OCEG GRCIllustratedSeries, useby permission only. ©2014 OCEG.org

Audit, Risk and Compliance need acommon and interrelated view of theorganization's processes, resources,IT and products to properly evaluaterisk and priorities.

DEFINE THE ORGANIZATION

ALIGN ASSESSMENT ACTIVITIES

Review historic assessments of risk, performanceand compliance and conduct additional analysistogether with process owners in each area.

PRIORITIZE SCOPE & SCHEDULE

Determine audit priorities based on potentialimpact on objectives and coordinate scheduledaudits to reduce impact on operations.

AUDIT RISKBUSINESSOWNER COMPLIANCE

COLLABORATE & COORDINATE

Establish common risk and assurancemethodologies and involve all relevantroles in each step of the process.Establish a common technologyapproach that allows each to add andaccess relevant and timely information.

AUDIT RISK COMPLIANCEBUSINESSOWNER

PRIORITIES

SCHEDULE

How do you coordinate activities to reduce audit burden on the business but still get the best results?

Panelist Question #3

Carole SwitzerCarolyn SaintPatrick PotterMelissa Bayer

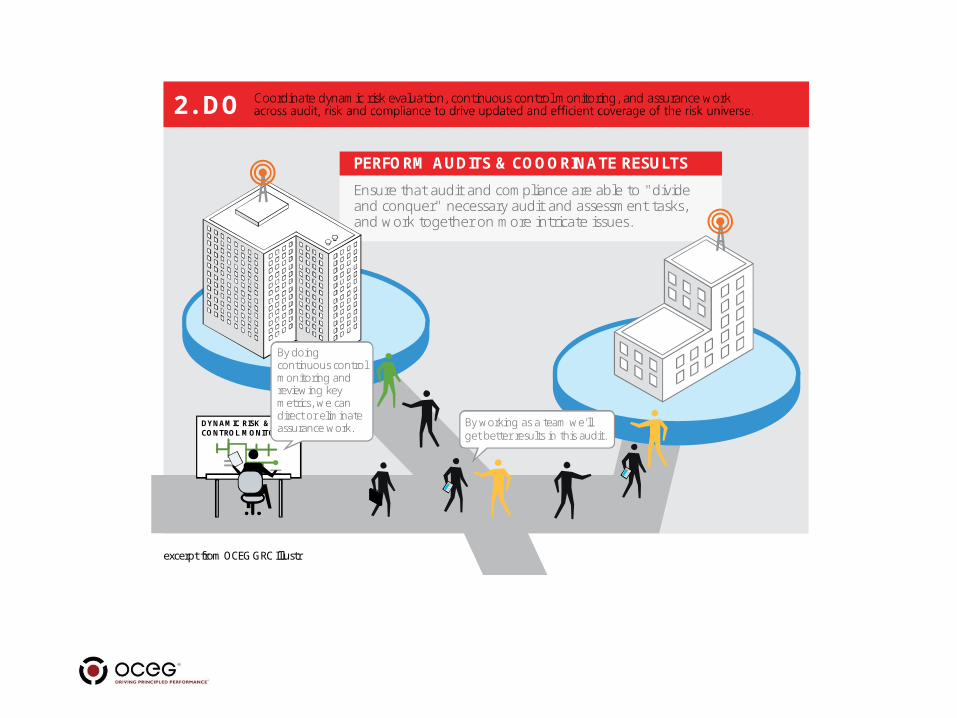

2. DO Coordinate dynamic risk evaluation, continuous control monitoring, and assurance work

By working as a team we'llget better results in this audit.

DYNAMIC RISK &CONTROL MONITORING

PERFORM AUDITS & COOORINATE RESULTS

Ensure that audit and compliance are able to "divideand conquer" necessary audit and assessment tasks,and work together on more intricate issues.

By doingcontinuous controlmonitoring andreviewing keymetrics, we candirect or eliminateassurance work.

excerpt from OCEG GRCIllustr

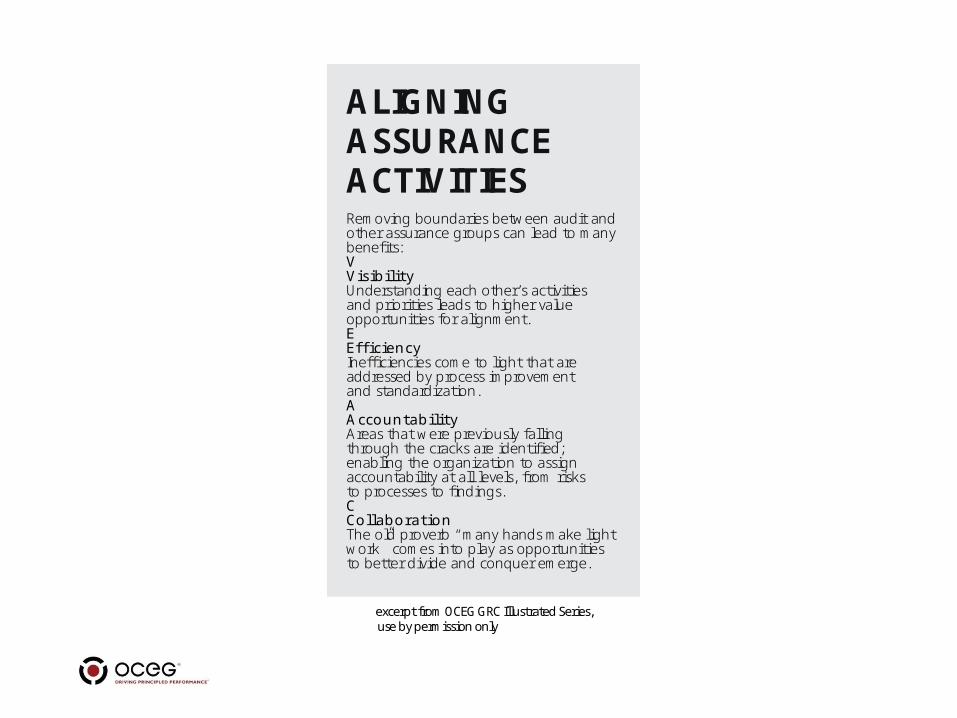

ALIGNINGASSURANCEACTIVITIESRemoving boundaries between audit andother assurance groups can lead to manybenefits:VVisibilityUnderstanding each other’s activitiesand priorities leads to higher valueopportunities for alignment.EEffi ciencyInefficiencies come to light that areaddressed by process improvement and standardization.AAccountabilityAreas that were previously fallingthrough the cracks are identified;enabling the organization to assignaccountability at all levels, from risksto processes to findings.CCollaborationThe old proverb “many hands make lightwork” comes into play as opportunitiesto better divide and conquer emerge.

excerpt from OCEG GRCIllustratedSeries,useby permission only

How does technology enable the best audit performance and use of the audit results?

Panelist Question #4

Carole SwitzerCarolyn SaintPatrick PotterMelissa Bayer

Here's the reportfor your meeting withthe audit committee.

AUDITMANAGEMENTPORTAL

AUDIT PLAN PERFORMANCE

AUDIT PLAN DETAILS

AUDIT ENTITY MAPS

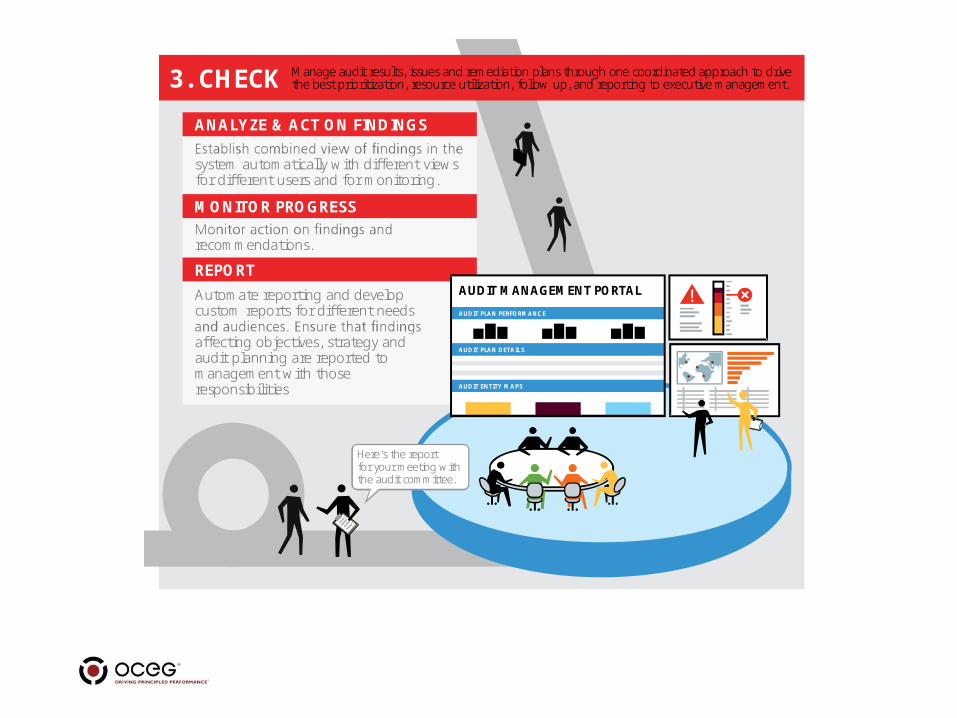

3. CHECK Manageaudit results, issuesand remediation plans through one coordinated approach to drivethebest prioritization, resource utilization, follow up, and reporting to executive management.

ANALYZE & ACT ON FINDINGS

system automatically with different viewsfor different users and for monitoring.

MONITOR PROGRESS

recommendations.

REPORT

Automate reporting and developcustom reports for different needs

affecting objectives, strategy andaudit planning are reported tomanagement with thoseresponsibilities

POLL #2

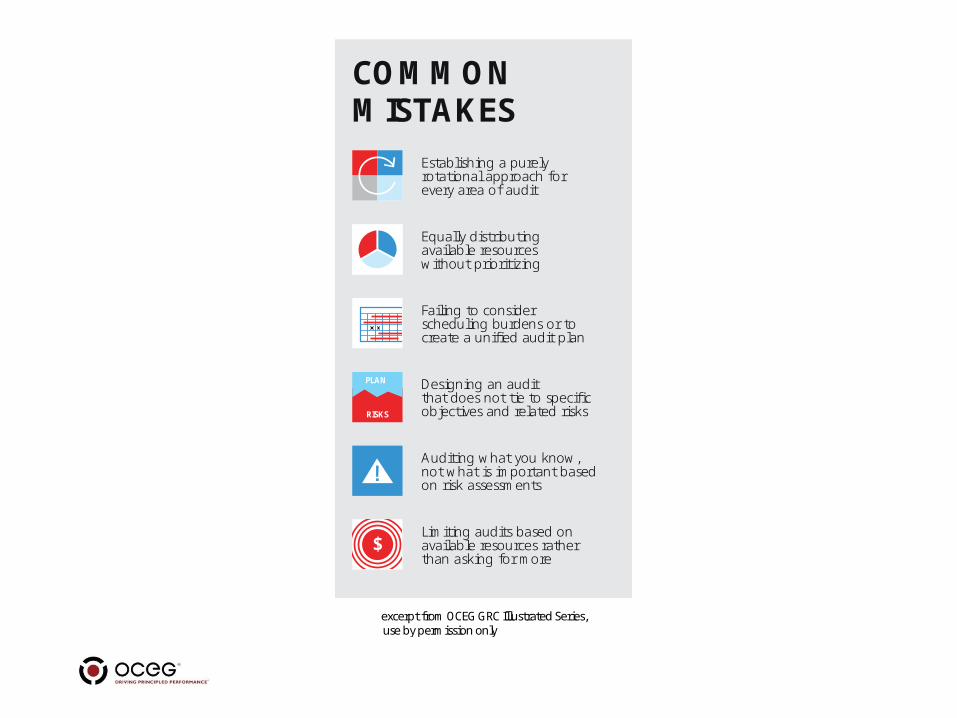

What are some common mistakes to address in your planning?

Panelist Question #5

Carole SwitzerCarolyn SaintPatrick PotterMelissa Bayer

COMMONMISTAKES

Establishing a purelyrotational approach forevery area of audit

Equally distributingavailable resourceswithout prioritizing

Failing to consider scheduling burdens or to create a unified audit plan

Designing an audit that does not tie to specificobjectives and related risks

Auditing what you know, not what is important basedon risk assessments

Limiting audits based onavailable resources ratherthan asking for more

$

PLAN

RISKS

excerpt from OCEG GRCIllustratedSeries,useby permission only

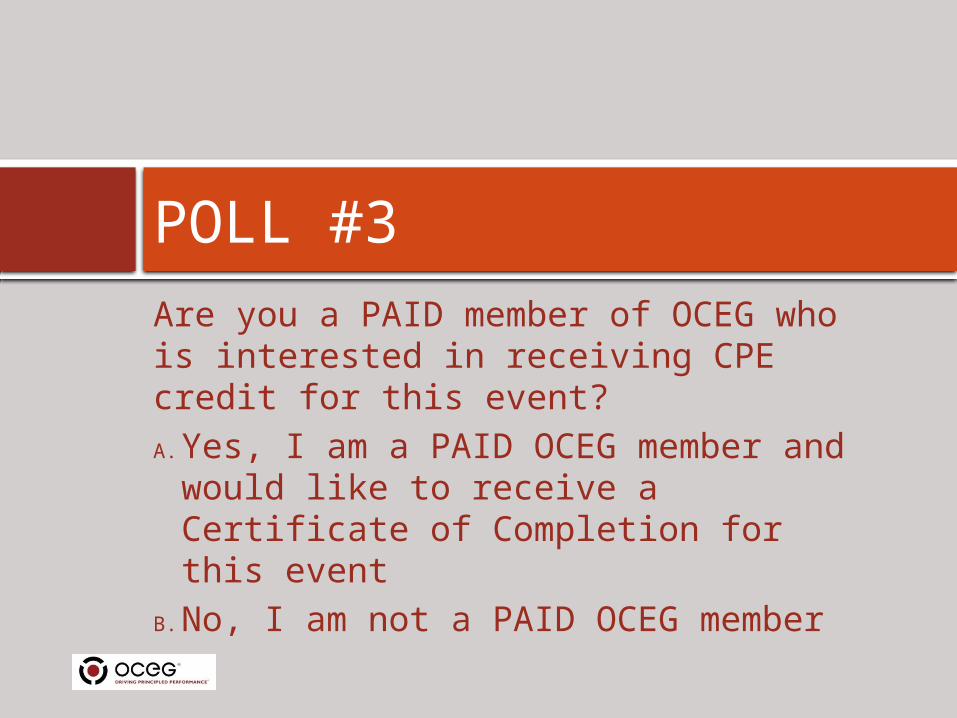

Are you a PAID member of OCEG who is interested in receiving CPE credit for this event? A. Yes, I am a PAID OCEG member and

would like to receive a Certificate of Completion for this event

B. No, I am not a PAID OCEG member

POLL #3

Questions?