Embed Size (px)

Citation preview

Bus 225D – Individuals and Foreign Corps

Instructor:

Carol Rutlen, CPA

650-321-3999

2

• Other expat issues– Moving expenses– Principal residence– State rules– Expatriation rules

• Extended business trips– Benefits of extended business trips– What is an extended business trip– Requirements to meet extended business trip

status– Reporting requirements– Practical issues

Agenda for Class 4 - Overview

3

Moving Expenses – General Rules

• Deduct certain moving costs – Change in principal place of employment– Distance test: new job site at least 50 miles from

farther from old principal residence than old job site– Time test: 39/78 weeks

• Deduct reasonable expenses of– Moving household goods and personal effects

(includes lodging, excludes meals)– Traveling from old residence to new residence– Storage

• If employer reimburses or pays directly, may exclude amounts from income if paid from accountable plan

4

Moving Expenses - Sourcing

• §1.911-3(e)(5)(i) reimbursement compensation for future services– Moving to foreign country → foreign sourced– Moving to US → US sourced– Written policy of reimbursing to and from → both

foreign sourced

• §911(d)(6) – denies deductions allocable to excluded income

• Moving expenses allocable to foreign earnings if taxpayer qualifies for §911 for at least 120 days in that year

[§911-3(c)(5)(ii)(A)]

5

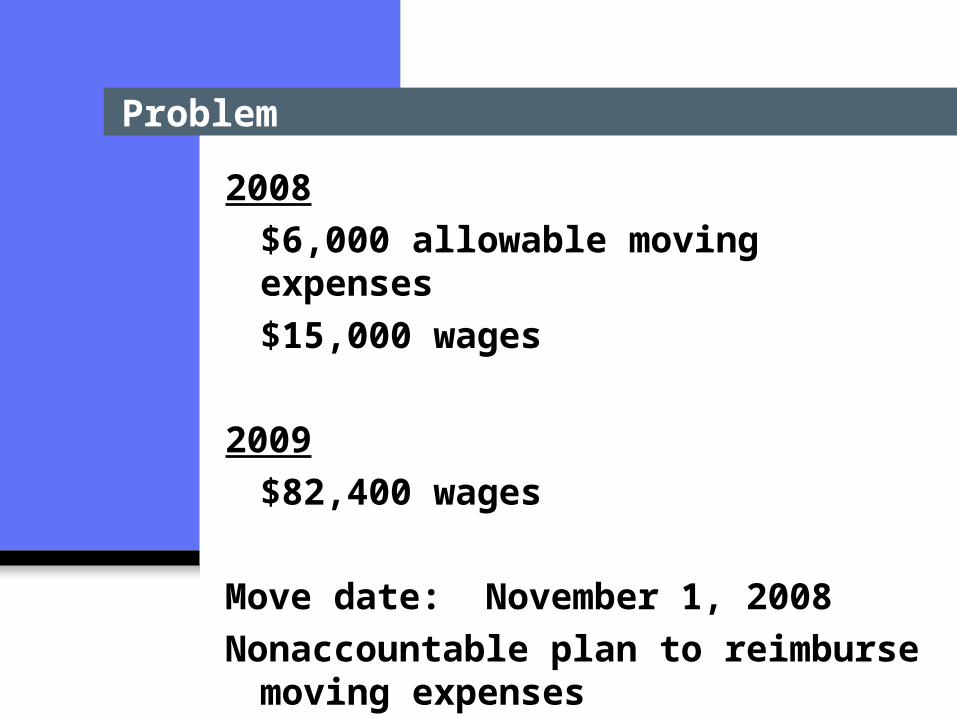

Problem

2008

$6,000 allowable moving expenses

$15,000 wages

2009

$82,400 wages

Move date: November 1, 2008

Nonaccountable plan to reimburse moving expenses

6

Impact on Principal Residence

• Section 469(j)(7)– Rental of principal residence while on assignment– Passive activity rules

• Passive losses can’t be deducted from nonpassive income

• Except active participation in rental real estate activity

• $25,000 passive losses from rental real estate can be deducted from nonpassive income

– 469(j)(7) “The passive activity loss of a taxpayer shall be computed without regard to qualified residence interest (within the meaning of section 163(h)(3).”

– Mortgage interest in excess of $25,000 limitation on loss can be itemized deduction

7

Rental of Principal Residence

Description Amount

Income (2,000 x 12) 24,000

Property Tax -7,500

Mortgage Interest -36,000

Other Expenses -5,000

Depreciation -10,000

Loss -31,500

8

Impact on Principal Residence

• Section 121- exclusion of gain from sale of principal residence– “Gross income shall not include gain from the sale

or exchange of property if, during the 5-year period ending on the date of the sale or exchange, such property has been owned and used by the taxpayer as the taxpayer's principal residence for periods aggregating 2 years or more.”

– Gain excluded $250,000 ($500,000 joint returns)– Applies to only 1 sale or exchange every 2 years

9

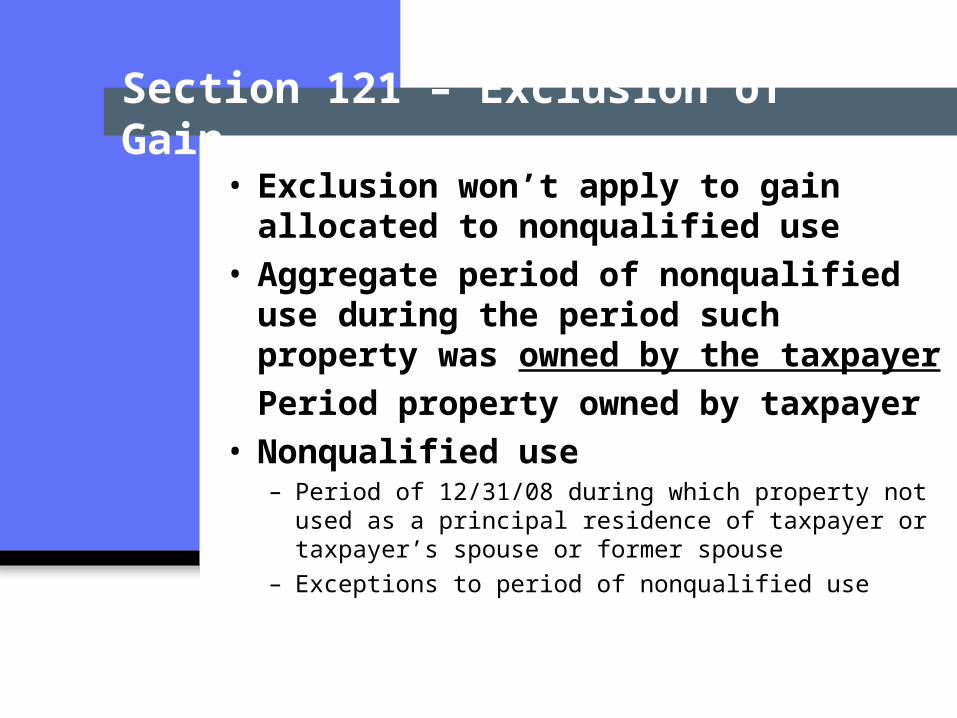

Section 121 – Exclusion of Gain

• Exclusion won’t apply to gain allocated to nonqualified use

• Aggregate period of nonqualified use during the period such property was owned by the taxpayer

Period property owned by taxpayer• Nonqualified use

– Period of 12/31/08 during which property not used as a principal residence of taxpayer or taxpayer’s spouse or former spouse

– Exceptions to period of nonqualified use

10

Exceptions to Nonqualified Use

• 5-year period which is after the last date property is used as the principal residence

• Period (not to exceed aggregate of 10 years) is serving in military, etc.

• Any other period of temporary absence (not to exceed an aggregate of 2 years) due to change of employment, health conditions, or unforeseen circumstances

11

Foreign Mortgage

• Sale of residence and payoff of mortgage treated as two transactions

• A principal residence is valued at the gross value

• A mortgage is not netted against the value of a residence

• A foreign denominated mortgage carries foreign exchange gains/losses

12

Impact on Principal Residence

1/1/02 1 € = $ 1Buy home 110,000 € $110,000

Mortgage 100,000 € $100,000

1/1/10 1 € = $ .75Sell home 140,000 € $105,000

Mortgage 100,000 € 75,000

Gain(loss) from sale

Gain from mtg

30,000 €

-0-

($5,000)

25,000

13

Impact on Principal Residence

1/1/02 1 € = $ 1Buy home 110,000 € $110,000

Mortgage 100,000 € $100,000

1/1/10 1 € = $ 1.25Sell home 140,000 € $175,000

Mortgage 100,000 € 125,000

Gain(loss) from sale

Gain(loss) from mtg

Personal/nondeductible

30,000 €

-0-

$65,000

($25,000)

14

State Rules

• Each state has specific residency rules

• May allow Sec 911 and FTC• May honor tax treaties• California residency test

– Out of state 18 months (546 days) under an employment related contract

– No more than 45 days in CA during taxable year– Intangible income can’t exceed $200,000 in taxable

year

• CA doesn’t allow 911, FTC, or treaties

15

Other States

• Pennsylvania: generally follows Federal but see REV-625

• Virginia: Follows Federal• Maryland: Follows Federal• NY: Follows Federal• Minnesota: Follows Federal

16

History of Expatriation Rules

• IRC Sec 877 – expatriating individuals continue to be taxed as US citizens

• Pre 1996 IRS must prove expatriation tax motivated + US citizen

• 2004 revisions• New rules effective for

expatriations after June 16, 2008

17

New Expatriation Rules

• Applies to US citizens • Applies to green card holders for 8

years or more during the 15 preceding tax years

• Threshold for applicability – §877(a)(2)– Average annual income tax liability over 5-year period

greater than $145,000 or– Net worth ≥ $2 million or– Taxpayer fails to certify compliance with US tax laws

for prior 5 years

18

Expatriation Rules

• If meet threshold test, all property is deemed sold on day before expatriation date for FMV – If property owned when became a US resident, basis

at least = FMV on date residency established– Losses may not be recognized until property disposed

• $627,000 exclusion for 2010• Special rules

– Deferred compensation: 30% tax withheld on payment

– Nongrantor trusts– Tax deferred accounts

19

Expatriation Rules

• Additional tax may be deferred until property sold– Election irrevocable– Property-by-property election– Tax triggered when property sold– Deferral terminates upon death– Must provide security to IRS– Interest is charged on amount deferred

20

EBT Status

• Business trip vs. short-term assignment vs. long-term assignment

• Taxation of travel expenses on business trip– § 162(a)(2)– Reg. § 162.2

• Business trip vs. EBT• Use

– Don’t meet 911 qualifications– Foreign nationals in US

21

§ 162 Trade or Business Expenses

(a) In general. There shall be allowed as a deduction all the ordinary and necessary expenses paid or incurred during the taxable year in carrying on any trade or business, including— (1) a reasonable allowance for salaries or other

compensation for personal services actually rendered;

(2) traveling expenses (including amounts expended for meals and lodging other than amounts which are lavish or extravagant under the circumstances) while away from home in the pursuit of a trade or business;

22

Ordinary and Necessary Expenses

• What types of expenses?• Meet substantiation requirements

of §274(d)– Adequate record– Amount of expense– Time and place of expense– Business purpose

23

While Away From Home

• Tax home– Regular place of abode in a real and substantial

sense §301.7701(b)-(2)(c)(1)– Rosenspan v. US

• §162 expenses vs. moving expenses

• Temporary vs. indefinite

24

Rev. Rul. 72-529

• Used prior to current job and work contacts maintained in that area

• Living expenses duplicated• Family members residing in abode

or taxpayer continues to use for lodging

25

Examples (Rev. Rul. 93-86)

Example 1:Expected to last 10 monthsLasts 10 months

Example 2:Expected to last 18 monthsLasts 10 months

Example 3:Expected to last 10 monthAfter 8 months, extended 7 additional months

26

Other Issues

• Break in service (CCA 200026025)– 3 weeks or less not significant– 7 month break significant

• No duplicate living expenses• Allocation between employee and

family– § 274(m)(3) no deduction with respect to spouse

or dependent accompanying taxpayer – Incremental cost (e.g., housing)– Directly attributable cost (e.g., airfare)

27

Reporting

• § 31.3306(b)-2 – Not wages if paid under accountable plan– Otherwise wages – subject to withholding and

reporting

• Accountable plan– Business connection– Substantiation– Returning amounts in excess of expenses

28

Per Diem – Rev. Proc. 2009-47

• Domestic: http://www.gsa.gov/portal/content/104877

• International: http://aoprals.state.gov/content.asp?content_id=184&menu_id=78

• Amount of expense deemed substantiated is per diem allowance

• Only amounts paid in excess of per diem rates must be accounted for as wages

• COLA vs. per diem

29

Short-Term Converting to Long-Term

• What happens when assignment gets extended?– Basic incompatibility of EBT and 911– Where is the tax home?– What was management’s intent?– Examine the facts and circumstances

• Convert to long-term when intent changes– Different reporting requirements, e.g., treatment

of per diems and housing– Host country taxability may change

30

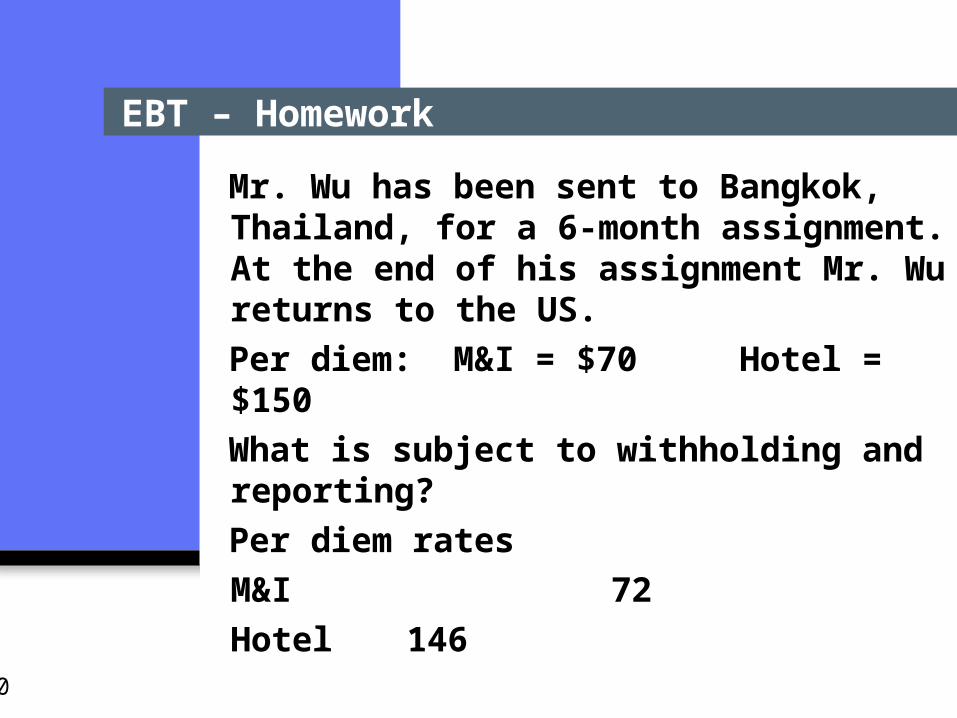

EBT – Homework

Mr. Wu has been sent to Bangkok, Thailand, for a 6-month assignment. At the end of his assignment Mr. Wu returns to the US.

Per diem: M&I = $70 Hotel = $150

What is subject to withholding and reporting?

Per diem rates

M&I 72

Hotel 146

31

• Other expat issues– Moving expenses– Principal residence– State rules– Expatriation rules

• Benefits of extended business trips• What is an extended business trip• Requirements to meet extended

business trip status• Reporting requirements• Practical issues

Agenda for Class - Overview