Embed Size (px)

Citation preview

Academy of American and International Law

BUSINESS ORGANIZATION

AND REGULATORY

LEGISLATION

Prof. Stanley Siegel New York University Law School

© 2015, Stanley Siegel

I. The Major Forms of

Organization A. The forms of business organization

B. The character of the business and the relative

importance of each form in the United States

C. Sources of law applicable to business organizations

D. Criteria for choice of form

A. The forms of business organization

(1) Proprietorship. (2) General partnership. (3) Partnerships with limited liability: (a) Limited partnership (“LP”). (b) Limited liability limited partnership (“LLLP”). (c) Limited liability partnership (“LLP”). (4) Joint venture. (5) Business trust. (6) Corporation. (7) Limited liability company (“LLC”).

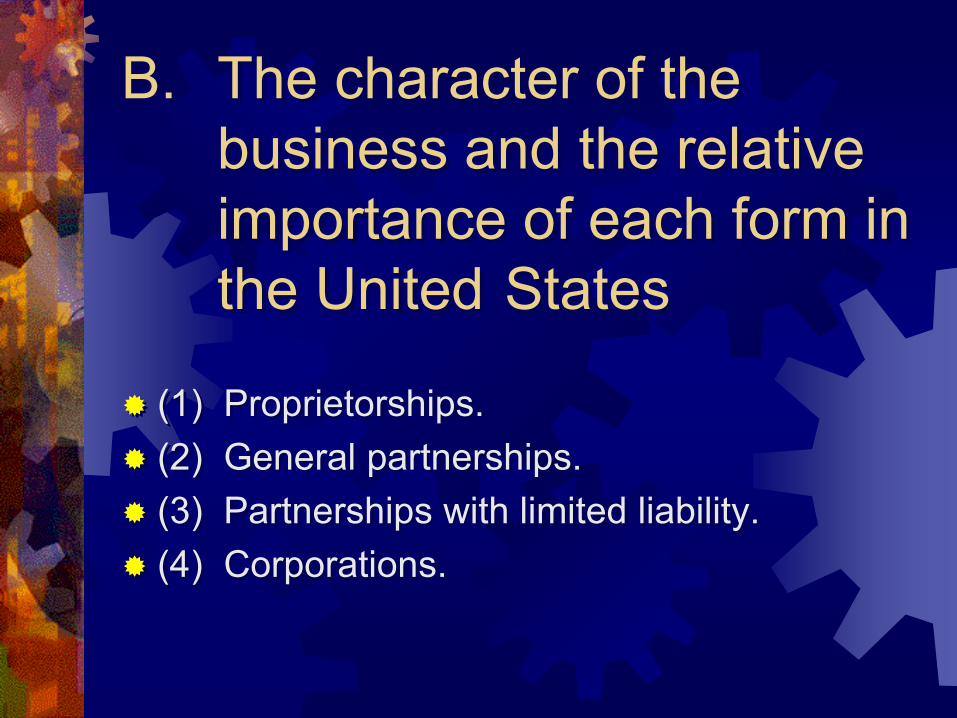

B. The character of the business and the relative importance of each form in the United States

(1) Proprietorships. (2) General partnerships. (3) Partnerships with limited liability. (4) Corporations.

C. Sources of law applicable to business organizations

(1) Business entities generally:

(a) State licensing and registration statutes.

(b) Federal and state decisional law and regulations.

C. Sources of law applicable to business organizations

(2) General partnerships:

(a) Uniform Partnership Act (1914) (the “UPA”): originally adopted by all states except Louisiana. Remains in effect in 20 states.

(b) Revised Uniform Partnership Act (1997)(the “RUPA”): adopted by 38 states.

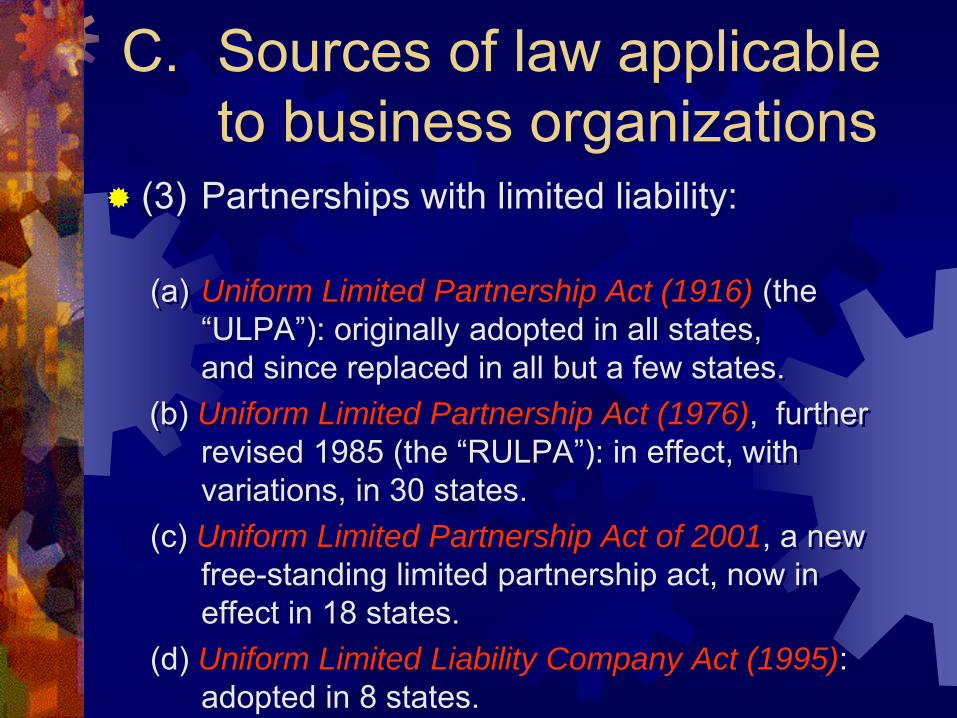

C. Sources of law applicable to business organizations (3) Partnerships with limited liability: (a) Uniform Limited Partnership Act (1916) (the

“ULPA”): originally adopted in all states, and since replaced in all but a few states.

(b) Uniform Limited Partnership Act (1976), further revised 1985 (the “RULPA”): in effect, with variations, in 30 states.

(c) Uniform Limited Partnership Act of 2001, a new free-standing limited partnership act, now in effect in 18 states.

(d) Uniform Limited Liability Company Act (1995): adopted in 8 states.

C. Sources of law applicable to business organizations (4) Corporations:

(a) Model Business Corporation Act (1969, revised

through 1981) (ALI/ABA) (the “MBCA”); Revised Model Business Corporation Act (1985, with later revisions) (the “RMBCA”) adopted, with variations, by 24 states.

(b) State corporation laws of important commercial states: Delaware, New York, New Jersey, California.

(c) State securities (blue sky) laws; Uniform Securities Act.

C. Sources of law applicable to business organizations (4) Corporations:

(d) United States Securities Act of 1933, as

amended. (e) United States Securities Exchange Act of

1934, as amended. (f) United States Internal Revenue Code of

1986 and Treasury Regulations. (g) State tax laws.

D. Criteria for choice of form (1) Ability to raise capital. (2) Transferability of ownership interests. (3) Liability of owners for enterprise debts. (4) Economic planning potential. (5) Tax implications for enterprise and

owners. (6) Flexibility of control and financial

structure.

II. Principles Applicable to

All Forms of Organization --

Employment, Licensing and

Agency A. The licensing phenomenon B. The basic agency principle of respondeat

superior C. The basic agency principle that the

principal is liable on actually or apparently authorized contracts of the agent

D. The fiduciary principle

B. The basic agency principle of respondeat superior: the employer is liable for the torts of employees

(1) The nature of the relationship - control. (2) Scope of the employment - covered acts. (3) Incidental acts. (4) Joint control. (5) No-fault liability: worker's compensation.

C. The principal is liable on actually or apparently authorized contracts entered into by the agent (1) Actual and implied authority; formal

authority. (2) Requirement of a writing: the statute of frauds

and the parol evidence rule. (3) Apparent authority by representation, trade

practice or position. (4) Special problems of representational liability:

the fraudulent agent. Authority to represent; apparent authority to misrepresent.

C. The principal is liable on actually or apparently authorized contracts entered into by the agent

(5) Unauthorized contracts -- the agent's warranty of authority.

(6) Unauthorized contracts -- ratification. (7) The undisclosed principal. (8) Termination of agency power.

D. The fiduciary principle (1) The duty of loyalty: (a) Good faith -- the negative obligation

not to act contrary to the interests of the principal.

(b) Accounting -- the affirmative obligation to account for profits or benefits.

(2) The duty of due care, or business judgment.

III. The General Partnership A. Partnership formation B. The statute imposes presumptive rules of

partnership structure C. The importance of careful drafting of the

partnership agreement D. Liability of present and former partners E. Application of the fiduciary principle among

partners F. Dissolution and winding up G. The joint venture is a variant of the partnership

A. Partnership formation UPA §§ 6, 7 RUPA §§ 101(6), 202

(1) Partnership defined as co-ownership of a business for profit.

(2) No formal agreement required: the general partnership as a residuary entity.

(3) Presumptions as to existence of partnership based on division of net profits.

B. Presumptive rules of structure absent an agree- ment among the partners UPA §18; RUPA § 401

(1) Control is equally divided among partners. (2) Each partner is an agent of the

partnership for carrying on the apparent partnership affairs.

(3) Profits and losses are divided equally.

B. Presumptive rules of structure absent an agree- ment among the partners UPA §18; RUPA § 401

(4) No salaries are paid to partners. (5) Interest is paid on contributions in excess

of the agreed amounts. (6) Property is held as tenants in partnership:

all partners may possess property for partnership purposes but no partner may possess partnership property for non-partnership purposes.

C. The importance of careful drafting of the partnership agreement (1) Division of profits and losses: typical

formulas and typical disputes. (2) Payment of a partner's interest upon

death or retirement; problems of valuation.

(3) Insurance and installment payment provisions.

(4) Deadlock among partners.

D. Present and former partners are personally liable if partnership assets are inadequate to pay partnership debts.

E. Application of the fiduciary principle among partners; the action for an "accounting"

F. Dissolution and winding up UPA §§ 35, 37 Dissociation and dissolution RUPA §§ 601-603, 701-705, 801-807

(1) Events of dissolution / dissociation. (2) Rightful and wrongful dissolution /

dissociation. (3) The right to continue the business. (4) The right to a "winding up," and the

inherent equity jurisdiction of the courts.

G. The joint venture is a variant of the partnership

(1) Real estate, motion picture and natural resources joint ventures.

(2) Joint ventures of corporations.

IV. Partnerships With Limited Liability A. Formation and operation under the

Revised Limited Partnership Act. B. Limitation of liability. C. Formation and operation under the

Uniform Limited Partnership Act (2001).

A. Formation and operation under the Revised Uniform Limited Partnership Act (1) Filing requirements; effects of defective

formation. RULPA §§ 201, 304 (2) The partnership name must not include

the name of a limited partner. RULPA § 102(2)

(3) A limited partner who participates in control may become liable to creditors as a general partner; but permissible participation has been considerably liberalized under RULPA § 303(b).

B. Limitation of liability

(1) Extension of limited liability: the corporate general partner.

(2) Limited liability by contract: nonrecourse debt, subordinated debt, and insurance.

B. Limitation of liability (3) Permissible participation in control has

been expanded by RULPA § 303(b): (a) Voting by limited partners. (b) Acting as contractor, agent or

employee of the limited partnership. (c) Consultation with the general

partner on business matters. (d) Approval of amendments to the

partnership agreement.

C. Formation and operation under the ULPA (2001) (1) A free-standing, new law, with different

numbering, language and substance. (2) Adoption, to date, by a minority of

jurisdictions. (3) Substantively closer to the corporate

model: unlimited life, no limitations on name or on control by limited partners.

(4) Refashioning of the limited partnership to achieve favored tax status without compromise of corporate attributes.

D. Public offering of limited partnership interests

(1) Qualified investors. (2) Multi-tier limited partnerships. (3) Alternative use of the limited liability

company.

V. The Corporation -- Basic

Aspects of State Law A. Formation and choice of state of

incorporation. B. Registration, recognition and taxation of

“foreign corporations.” C. Drafting of articles of incorporation and

bylaws. D. The statutory control model.

V. The Corporation -- Basic

Aspects of State Law

E. Special problems of control and operation of “close corporations.”

F. Capital and financial structure. G. Corporate fiduciary duties and their

enforcement.

A. Formation and choice of state of incorporation

(1) Delaware continues to be desirable as the jurisdiction of incorporation:

(a) Liberality and thoroughness of the statute. (b) The Delaware Revision Commission. (c) Sophistication and efficiency of the

Delaware Chancery Court. (2) Changes in other corporate laws: California and

the Revised Model Business Corporation Act.

B. Registration, recognition and taxation of "foreign corporations"

(1) Full faith and credit: recognition of foreign corporations and general application of foreign law to matters of internal affairs.

(2) Registration requirement: "doing business."

(3) Consequences of failure to file: inability to enforce contracts; tax and other penalties.

(4) State corporate taxation: the three-fold formula -- assets, payroll, receipts.

C. Drafting of articles of incorporation and bylaws (1) Mandatory provisions in the articles:

name, office, agent for process service, authorized capital.

(2) Optional provisions: financial and control structure.

(3) The role of the bylaws: general rules with respect to meetings, notices, officers, directors, indemnification.

C. Drafting of articles of incorporation and bylaws

(4) Planning the corporate control structure: which provisions belong in the articles and which in the bylaws?

(5) The role of other documents: shareholder agreements, employment agreements, transfer restrictions.

D. The statutory control model

(1) Actions by the shareholders: (a) The shareholders meeting. (b) Action by unanimous consent. (c) Non-unanimous consent. (2) The board of directors, meetings,

quorums and votes.

D. The statutory control model

(3) The structure of the board of directors: (a) The unitary, non-constituent board (United

States). (b) The two-level board -- supervisory and

management (e.g., Germany: Aufsichtsrat and Vorstand)

(c) Representation of labor and other elements on the board -- codetermination.

(4) Board committees: the executive committee, audit committee and litigation committee.

E. Special problems of control and operation of "close corporations"

(1) The "incorporated partnership." (2) The contrast between United States law

and laws of other nations with respect to private companies.

E. Special problems of control and operation of "close corporations" (3) Voting and control agreements at common law

and under special close-corporation acts: (a) Board control by cumulative voting. (b) Voting trusts, voting agreements and

irrevocable proxies. (c) Unanimity voting requirements and other

limitations in the articles and bylaws. (d) Voting agreements; "sterilization" of the

board of directors. (e) The statutory close corporation.

E. Special problems of control and operation of "close corporations"

(4) Share transfer restrictions and buy-sell agreements:

(a) Forms of restraint: consent, first option, buy-sell agreement.

(b) Problems of timing, valuation and payment.

(5) Problems of deadlock, shareholder oppression, and judicial dissolution.

F. Capital and financial structure (1) Equity capital: (a) Minimum capital, par value, and

watered stock. (b) Common and preferred stock:

leveraging with senior securities. (c) Preferred stock terms: cumulation,

participation, conversion and contingent voting rights.

(d) Open-ended capital structure: series preferred, unlimited authorized shares.

(e) Warrants and options.

F. Capital and financial structure (2) Debt: (a) The advantages of debt: leverage

and tax aspects. (b) Debt instrument terms: security,

interest, conversion. (c) The trust indenture: control by

contract. (d) Corporate risk implications.

F. Capital and financial structure (3) Corporate distributions: (a) Dividends and redemptions at the

board’s discretion. (b) Absence of protection for stated

capital. (c) Financing by earnings retention.

Tax implications and excess earnings retention.

G. Corporate fiduciary duties and their enforcement (1) Loans and other transactions with "interested

directors." (2) Statutory liability of directors and the common

law "business judgment rule": (a) Statutory "safe harbors" in recent

legislation: reliance on accountants and experts.

(b) Leading cases clarifying the extent of the duty of care: Smith v. Van Gorkom, 488 A.2d 858 (Delaware 1985); Francis v. United Jersey Bank, 87 N.J. 15, 432 A.2d 814 (1981).

G. Corporate fiduciary duties and their enforcement (2) Statutory liability of directors and the common

law "business judgment rule" (cont’d): (c) The costs of defending litigation against

directors. (d) Delaware's legislative response: Del. Gen.

Corp. L. § 102(b)(7). (e) What remains of the standard of care: In

re Walt Disney Co. Derivative Litigation, 906 A.2d 814 (Del.Sup.Ct. 2006).

(3) Derivative suits: dismissal and settlement. (4) Indemnification and insurance of directors and

officers.

VI. The Corporation -- Federal

and State Securities Laws

A. An introduction to securities marketing and distribution in the United States.

B. The Securities Act of 1933 – marketing of securities.

C. The Securities Exchange Act of 1934 – registration of securities following initial distribution.

D. State regulation of securities: the “Blue Sky Laws”

E. The effects of contemporary financial theory on the regulation of corporations and securities markets.

A. An introduction to securities marketing and distribution in the United States 1) Sources of corporate capital: equity, debt,

retention of earnings. (2) Underwriting: firm commitment, best

efforts, and standby. (3) Market makers: national securities

exchanges, NASDAQ, and the over-the-counter market. Listing and delisting of securities; criteria of the major exchanges.

A. An introduction to securities marketing and distribution in the United States (4) Other markets: options, commodities

futures. (5) The costs of public distribution of

securities: accounting, legal, underwriting, registration.

(6) Stock and securities ownership in the United States: individuals, institutional investors, mutual funds.

B. The Securities Act of 1933 -- marketing of securities (1) The broad definition of a "security." (2) All-inclusive coverage of SA § 5 in the

absence of a demonstrated exemption. (3) Liabilities for failure to register when

required. SA § 12 (4) The nature of a 1933 Act prospectus; form

S-1 and simplified filing requirements under forms S-2 and S-3.

B. The Securities Act of 1933 -- marketing of securities

(5) The filing process. (6) Extensive statutory liabilities based on

filed documents. SA § 11 (7) The desirability (and complexity) of

obtaining an exemption. SA § 4 (8) Secondary distributions.

C. The Securities Exchange Act of 1934 -- regulation after initial distribution (1) The registration requirement. SEA § 12(g) (2) Filing requirements under SEA §§ 13 and 14.

Periodic filings on forms 10-K, 10-Q and 8-K. The nature and utility of the filed information. Annual reports.

(3) The proxy rules, proxy statements, and the development of private civil-damage remedies for dissemination of erroneous information. Standards of liability: materiality as defined by the Supreme Court.

(4) Short-swing profit recovery under SEA § 16(b).

C. The Securities Exchange Act of 1934 -- regulation after initial distribution (5) Rule 10b-5, a "rule for all seasons";

expansion and contraction of the implied civil damage remedy.

(6) Tender offers and the Williams Act. (7) The Foreign Corrupt Practices Act:

prohibitions and reporting requirements. (8) The Sarbanes-Oxley Act: accounting

standards, oversight, certifications and liabilities.

D. The information regime of the SEC (1) Public access to filings; the early history

of paper filing. (2) Electronic filing and the EDGAR system

(Electronic Data Gathering, Analysis and Retrieval).

(3) Some recent developments: international data access and the effects of data formatting and security. HTML, PDF and XBRL.

E. State regulation of Securities: the "Blue Sky Laws"

(1) Disclosure compared with merit regulation.

(2) The process of "blue skying" an offering.

VII. The Structure of

Enterprise Taxation

A. Individual taxation. B. Partnership taxation. C. Corporate taxation. D. Taxation of corporate reorganizations.

A. Individual taxation

(1) Direct taxation of taxable income. Varying rates for ordinary income, capital gains, and dividends received.

(2) Alternate minimum tax. (3) Direct deductibility of operating losses,

and use of carry-forward losses.

B. Partnership taxation

(1) Partnership as a reporting entity only; no payment of taxes by partnership.

(2) Pass-through of items of income, expense, gain, loss and credit to individual partners.

(3) Similar results obtainable in corporate form through election as an "S corporation."

C. Corporate taxation

(1) Corporation is a separate taxable entity, liable for tax at maximum rate of 35% on taxable income.

(2) The nature of the so-called "double tax": recipients of corporate dividends pay ordinary income tax thereon. Effects of legislation substantially reducing tax rates on dividends.

(3) Avoidance of the double tax through capital structure, compensation, and other benefits.

(4) Problems raised by excess retention of earnings.

D. Taxation of corporate reorganizations

(1) The basic structure of reorganization taxation under Subchapter C: (a) Nonrecognition of gain or loss by corporations or shareholders. IRC §§ 354, 356, 361

(b) Carryover basis by corporations and shareholders. IRC §§ 358, 362

(c) Carryover of tax attributes. IRC §§ 381, 382

D. Taxation of corporate reorganizations

(2) The definition of "reorganization" IRC § 368: (a) Corporate combinations: the "A", "B" and

"C" reorganizations and their variations. (b) Divisive reorganizations: the "D"

reorganization and IRC § 355. (c) Recapitalizations and rearrangements:

the "E" and "F" reorganizations. (d) Bankruptcy reorganizations: "G"

D. Taxation of corporate reorganizations

(3) Tax doctrines of general application: (a) Business purpose doctrine. (b) Step transaction. (c) Continuity of business enterprise. (d) Continuity of proprietary interest.

D. Taxation of corporate reorganizations

(4) An introduction to reorganization planning; tax and corporate structuring designed to achieve disparate objectives:

(a) Minimize corporate formalities and costs, and avoid dissenters' or other remedies.

(b) Preserve desirable contract, franchise and other arrangements.

(c) Avoid taxation of gain; obtain recognition of losses. (d) Obtain step-up in basis in certain circumstances. (e) Preserve desirable tax characteristics; e.g., tax

loss carry-forwards.