Embed Size (px)

Citation preview

Case study

September 2014

Business Property Relief: An Essential Financial Planning Solution

or call 0808 1000 804 for an immediate free trial

www.defaqto.com/adviser/engage

Defaqto EngageDefaqto Engage provides integrated product, platform and fund research all in one place.Saving you time, reducing your compliance risk and cost, and helping you evidence research and demonstrate value to clients.

Supports both independent and restricted advice with comprehensive data and research

Integrated three-way research across products, platforms and funds

Easily fi lter our market-leading data to a shortlist and recommendation – with a clear and robust audit trail to help you meet regulatory requirements

Clear and professional output for clients

Creation, management and distribution of panels

Our unique quality scoring of each product and platform feature (DNA benchmarking) enables you to graph, compare and undertake detailed feature-based analysis

Over 60,000 share classes across more than 15,000 funds, integrating Morningstar data with our own, including:

• Investment trusts• Insured funds• ETFs• O� shore funds

More than 2,700 LPI products (including banks’ and direct products) across more than 100 product types including:

• DFMs• Structured products• SIPPs

Over 40 platforms across 30 providers

www.defaqto.com/adviser/engage Find out more now at www.defaqto.com/advisers/solutions/engage

Defaqto Case Study Business Property Relief: An Essential Financial Planning Solution

www.defaqto.com/advisers

About Defaqto

Defaqto is an independent researcher of financial products, focused on providing intelligence to support better decision-making.

For further information please contact us on 0808 1000 804

At our heart is the UK's largest retail financial product and fund database - we maintain it by collecting data from across the whole market, and using our expertise and insight to analyse this data and make it comparable.

From this, we create a range of products and services ˛ ratings, software solutions, consultancy services, data services, and publications and events ˛ to deliver this information in a meaningful way.

Our intelligence facilitates better financial decisions and greater effectiveness in the creation, management and distribution of financial products.

1

About Defaqto EngageDefaqto Engage is the leading financial product, fund and platform research analysis system

available to financial advisers.

Defaqto Engage can sift through thousands of options, produce results in a matter of minutes and even keep track of how it did it, so users get a full audit trail to satisfy compliance. The reporting, analysis, recommendation and review process saves users time and effort.

Defaqto Engage is completely web-based, offering the flexibility to search for products whenever and wherever necessary. It integrates with the advice process to ensure advisers deliver nothing less than best practice.

For more information, or to arrange a 14 day free trial, visit www.defaqto.com/advisers/solutions/engage

About Defaqto ConsultancyThorough research of products, funds and investments suitable to clients can be time consuming, shifting the adviser's focus away from the essential services they offer. Our consultancy services can support advisers to maximise the time spent with their clients.

Defaqto's experienced consultants can undertake research and data analysis, saving time and money. From researching new products and markets to finding the perfect discretionary management solution, we can provide all the professional support financial advisers may require, allowing them to focus their efforts on growing their business.

For more information visit www.defaqto.com/advisers/solutions/panel-support/

Defaqto Case Study Business Property Relief: An Essential Financial Planning Solution

www.defaqto.com/advisers

Defaqto has seen steadily increasing interest from advisers in tax shelter investing over the last few years. More of our clients are requesting information on these very specialist solutions and our panel clients are encouraging us to add Venture Capital Trusts (VCTs), Enterprise Investment Schemes (EIS) and Business Property Relief (BPR) panels to the more mainstream product solutions.

Introduction

The focus of this publication is on Business Property Relief (BPR).

Tax shelter specialists Allenbridge, who have contributed significantly to this publication, also advise that not only do they see increasing interest in BPR from advisers, but this is being met with the launch of a growing number of solutions.

Just to underline the interest, we are also beginning to see some innovation in the market, with solutions being tailored to answering specific financial planning needs ˛ a sure sign of growing demand.

2

Fraser Donaldson

Insight Analyst ˛ Wealth Management

[email protected] 01844 295 432

IO We are beginning to see some innovation in the market, with solutions being tailored to answering specific financial planning needs. OI

Defaqto Case Study Business Property Relief: An Essential Financial Planning Solution

www.defaqto.com/advisers 3

Why the interest?

From a financial planning point of view, the purpose of BPR is to remove assets from the client's estate for inheritance tax (IHT) purposes. The nil rate band - the point at which IHT becomes payable on an estate - has been frozen at £325,000 since 6 April 2009 and the value of properties, which usually form the largest portion of an estate, have been increasing over this period, which means that a smaller proportion of the nil rate band is free for other assets.

Many properties now exceed the nil rate band, which also means that all other assets are subject to IHT. These dynamics, coupled with the tightening of allowances within the more mainstream tax-efficient investments (in particular pensions), mean that investors are looking elsewhere for tax-efficient investing.

As such, we feel it is the ideal time to introduce the subject to help our adviser colleagues navigate their way through the recommendation process.

Purpose of this publication

The purpose of this publication, therefore, is twofold. Focussing on the subject of BPR, the first section will be a general introductory guide to BPR.

The second section will look at a real world proposition from Ingenious and see how this fits with and answers the issues that advisers face from the point of view tax planning, investment and administration.

We believe that the second section, looking at a real proposition, will bring the subject to life and help advisers benchmark the kind of research, due diligence and client suitability issues that need to be considered.

By the time readers have completed this case study, they will have learned about the following aspects of Business Property Relief:

What Business Property Relief is and how it can be applied currently

Business Property Relief both as an investment and a tax planning vehicle

Good due diligence to undertake in this specialist area

Fraser DonaldsonInsight Analyst ˛ Wealth Management

The annual pension cap has actually fallen in recent years from £225,000 all the way down to £40,000 for 2014/2015.

The lifetime pension cap has also continued to fall over recent years from a high of £1.8m all the way down to £1.25m currently.

For adviser firms, there has also been a regulatory push, in that the Retail Distribution Review (RDR) has reminded advisers that "independence" means whole of market. Even restricted advisers need to know enough about markets they would not normally use in order to be in a position to judge whether BPR, for instance, would be the most suitable solution and whether they should refer a client on to another adviser.

Even though this is still undoubtedly a specialist area of investment, factors such as the market and the current regulatory and tax regimes, have created a perfect storm driving advisers towards these propositions.

Defaqto Case Study Business Property Relief: An Essential Financial Planning Solution

www.defaqto.com/advisers 4

Introductions

They describe themselves and their relevant experience as follows:

Allenbridge

The Allenbridge Tax Shelter Report offers the widest range of independent product reviews available in the market today ˛ across EIS, Seed EIS, VCT and IHT products, and has been available since 1984. Our team of analysts reviews the majority of all such products in the market, including new entrants.

Allenbridge is made up of a team of experts including an internal investment committee that has over 50 years of financial knowledge and expertise.

Allenbridge is all about delivering outstanding research and giving clients the confidence that independent experts have given an impartial and detailed appraisal of the merits of the products.

Ingenious

For more than 15 years, investors have chosen Ingenious to manage their funds. In that time, Ingenious has raised and deployed more than £9 billion.

Since 2005, Ingenious has raised and deployed more than £800 million in BPR- qualifying investments, including over £70m in the Ingenious Estate Planning service launched in 2011 and over £450m in Ingenious Broadcasting (which preceded that service).

There will be two significant contributors to this publication. Firstly Allenbridge, who have provided significant technical detail around BPR and also independently analysed the Ingenious proposition. Secondly Ingenious, who have opened their doors to us and allowed us to use their proposition as a proof of concept for BPR.

Defaqto Case Study

www.defaqto.com/advisers

Business Property Relief: An Essential Financial Planning Solution

5

3

4

A Guide to Business Property Relief (BPR)

A client's estate valued above the current nil rate band (NRB) of £325,000 is liable to IHT on death. However, assets that qualify for BPR will pass to beneficiaries free of IHT, making those investment schemes that are able to claim BPR potentially useful and powerful financial planning tools.

Background to BPR

BPR was introduced in the 1976 Finance Act and is established under law. BPR was designed to stimulate investment in unquoted businesses by allowing a family-owned company to be bequeathed free of IHT. This will help ensure an unquoted company's survival as a trading entity on the death of its owner by protecting the businesses from being broken up to pay death duties.

BPR provides a potential 100% reduction in the value chargeable to IHT, where that value is attributable to "relevant business property", as stipulated under BPR legislation. BPR, therefore, also provides an incentive to invest in unquoted companies, which it is hoped may stimulate the grass roots of the UK economy.

Examples of relevant business property include, but are not limited to:

The first section of this publication will deal with BPR as a financial planning solution. It is a guide to the technical details, structure and background.

• Shares in an unquoted trading company (which qualify for BPR at 100%)

• Land, buildings, plant or machinery used by a partnership of which the individual is a member (which qualify for BPR at 50%)

• Forests, agricultural land, and suitably qualified companies listed on AIM

• An Enterprise Investment Scheme (EIS) may also qualify for BPR, which is not limited to domestic business interests; international interests would also qualify for BPR

Defaqto Case Study Business Property Relief: An Essential Financial Planning Solution

www.defaqto.com/advisers 6

BPR Qualification

To qualify for BPR, the relevant holding must have been held for at least two years and the business itself must meet certain trading criteria. BPR qualification, as invariably with many tax-based products, is defined more by HMRC restrictions than permissions; HMRC restrictions can be summarised as follows:

• The business must be trading on a commercial basis for profit

• The business must not be subject to a contract for sale or being wound up

• The activity, wholly or mainly, of dealing in securities, stocks or shares, land or buildings, or in the making or holding of investments, is strictly prohibited

• Businesses that generate solely income will not attract BPR, thereby excluding the following activities:

o Residential or commercial property letting

o Property dealing

o Serviced offices

While HMRC may provide written advice on a BPR-qualifying investment if requested, it is only on a case by case basis, and generally at the time that BPR is claimed. That is to say, only when there is the potential for an immediate IHT charge will HMRC rule under the law as to whether an asset qualifies for BPR or not.

Once HMRC has assessed an application for BPR, investments that qualify for BPR (assuming they have been held for two years) can be passed to the deceased's beneficiaries free of IHT.

To obtain BPR, the executors of an estate must submit probate return form IHT 412 to HMRC.

The following link provides more information on HMRC requirements: http://www.hmrc.gov.uk/cto/customerguide/page16.html

Defaqto Case Study Business Property Relief: An Essential Financial Planning Solution

www.defaqto.com/advisers 7

Market development

Historically, clients seeking investments in BPR-qualifying companies (single company options being excluded for their high risk) generally preferred AIM-listed companies to unquoted companies, because a listed company should, in theory, have a lower risk profile than an unquoted one. Under a discretionary management contract with an asset manager, clients would buy an AIM portfolio to be held long-term.

Since 2007, the range of BPR products widened with the launch of the first IHT Service, which provided investors with carefully chosen low risk trades operating within special purpose vehicles (SPVs), which were created explicitly to run BPR qualifying projects. This service was run under a discretionary contract, which gave the manager power to choose, on behalf of investors, companies that fitted its general mandate of seeking to preserve and maintain capital.

More recently, several other product providers have entered the market with similar mandates of investing in only perceived low risk trades. Many of these providers were already running EIS and/or VCT, and saw BPR as an offshoot of their existing investment activities, which may have invested in similar sectors (renewable energy or pubs being two good examples).

New BPR vehicles, as demand increases for the product, appear to be becoming more refined and their structures more robust, with improved governance and clearer liquidity options.

Type of solutions

The type of solutions now being offered in the current market have varying degrees of associated risks, features and benefits.

From a financial planning perspective, there are several ways to invest in opportunities that can benefit from BPR, which, to aid understanding, we categorise as follows:

• Enterprise Investment Schemes (EIS)

• AIM portfolios

• Special Purpose Vehicles (SPVs)

IO New BPR vehicles, as demand increases for the product, appear to be becoming more refined and their structures more robust, with improved governance and clearer liquidity options. IO

Defaqto Case Study

www.defaqto.com/advisers

Business Property Relief: An Essential Financial Planning Solution

8

Enterprise Investment Schemes

The Enterprise Investment Scheme (EIS) was designed to encourage investment in small and growing businesses (i.e. companies with gross assets of less than £15 million). Shares in an EIS should also be exempt from IHT under BPR. The investor would gain the relief after holding the EIS investment for at least two years, provided the company meets the BPR trading criteria.

As a single unquoted company, an EIS is considered a high-risk investment, though the tax benefits available to EIS investors - income tax relief, capital gains tax reliefs, loss relief and tax-free growth - mitigate the risk somewhat. A portfolio of EIS may help reduce risk through a degree of diversification.

The advantage of investing in EIS to obtain BPR is the securing of additional tax benefits as stated above. The disadvantage is that the directors of an EIS company will invariably seek to secure an exit for its shareholders after the obligatory three-year holding period, and will generally state such an intention from the start.

Hence, BPR investors who are hoping to use EIS for IHT planning may have to find a new BPR investment elsewhere at any given time. This could result in the two-year obligatory BPR holding period having to restart, putting at risk their IHT planning. Furthermore, EIS, having no defined secondary market, can be highly illiquid, making withdrawals fraught with problems.

Defaqto Case Study Business Property Relief: An Essential Financial Planning Solution

www.defaqto.com/advisers 9

AIM Portfolios

As mentioned, AIM portfolios were the traditionally preferred method of obtaining BPR through a portfolio of diversified holdings. Many asset managers still offer such a service.

Normally, a specialist investment manager would put together a portfolio of qualifying AIM stocks under a long-term, conservative investment strategy. The underlying companies must be deemed to qualify for BPR, and the portfolio held for two years in order to qualify.

In order to reduce risk, the underlying companies are often selected for their mature business models, established market share, profitability, and strong financials. The skill and expertise of the investment manager in this market is clearly a primary consideration.

Advantages

The advantages of investing in AIM stocks may include:

• The potential profits that can come from investing in companies with exciting growth opportunities

• The investor retaining control of their investment

• A high degree of liquidity, allowing it to be accessed quickly and easily to meet unexpected needs for capital

Disadvantages

Disadvantages of investing in AIM stocks may include:

• AIM-listed companies can be volatile due to their size and market sensitivity.

• A yield may not be available, if required, because it is up to the discretion of each company whether or not to pay a dividend. The investor, therefore, cannot rely on any firm dividend policy.

• Furthermore, investing in AIM stocks, as with investment in all listed companies, requires patience, and an understanding of the risk of equity investment, in particular at the smaller company end of the market.

IO The skill and expertise of the investment manager in this marketis clearly a primary consideration. IO

Defaqto Case Study Business Property Relief: An Essential Financial Planning Solution

www.defaqto.com/advisers 10

Special Purpose Vehicles (SPVs)

Increasingly, newly-launched BPR investment services involve a specialised manager capitalising one or more SPVs, which will undertake qualifying trades in what are considered to be relatively low risk opportunities. In some cases, the single investor can own the entire shareholding, giving ultimate control.

Capital preservation is usually the priority and, as such, growth prospects may be modest. The following trades, among others, commonly feature in such schemes:

Advantages

These may include:

• The investor owns a real asset with a known and quantifiable value

• Usually a relatively low risk investment strategy

• A tangible method of withdrawals

• A transparent cost structure

• Enjoying the expertise of a proven specialist in BPR (although due diligence should confirm this to the adviser's satisfaction)

Disadvantages

• The priority given to capital preservation is likely to be at the cost of growth, meaning that the assets (after fees and charges) may see their real value, in extremis, eroded by time and the opportunity cost of not investing in traditional investment classes (perhaps with less favourable tax treatment).

• Investment in this type of structure may also lead to a lack of diversification, since the investor is likely to hold shares in one or perhaps two companies, but not usually more.

• Governance can also be key, since managers tend to populate the board of the SPV with their own executives, thus having the potential to create conflicts of interest and requiring robust conflict policies.

Construction services for residential or commercial properties

Collaterised lending

Asset leasing

Pubs (asset-backed)

TV/film production, where the earnings are identified and secured against a third party

Renewable energy assets, where the income may be secured against government-backed subsidies

Defaqto Case Study

www.defaqto.com/advisers

Business Property Relief: An Essential Financial Planning Solution

11

The use of BPR in financial planning

If we can answer this question we can then apply good client segmentation to identify, at an early stage, individual clients for whom BPR may be suitable - whether now or at some point in the future.

Why should advisers consider using the BPR solution?

Under UK legislation, an individual's estate worth more than £325,000 (the nil rate band) is subject to 40% IHT, payable on death, and the nil rate band is expected to be frozen until at least 2018.

The value of an estate includes assets such as property and investments, as well as a proportion of any gifts made in the seven years prior to death, life assurance policies and pension plans not held in a trust.

Since individuals are increasingly being affected by IHT thanks to rising house prices and growth in value of other asset classes, the emphasis on IHT planning is becoming ever more important.

Investing in a BPR vehicle can have certain advantages over other types of financial planning opportunities for the following reasons.

• Whereas traditional forms of inheritance tax planning (such as gifts or simple trusts) take seven years to reach full exemption, BPR can be obtained in just two.

• Unlike some estate planning strategies, there are no complex legal structures, no expensive underwriting and medical reports.

• Assets in a BPR qualifying investment service can be withdrawn in part or in whole, helping a client to deal with changing life circumstances, such as the need for long-term health care.

• The client can continue to enjoy growth or a yield on his assets, which can be taken or re-invested depending on his wishes and the terms of the underlying investment.

• The investor does not want to lose control of their assets, which is the case with other IHT planning solutions, although they reside in a tax-benign structure.

The most fundamental question for an adviser to answer is "at what point and in what circumstances should I be considering BPR solutions for my clients?"

Defaqto Case Study Business Property Relief: An Essential Financial Planning Solution

www.defaqto.com/advisers 12

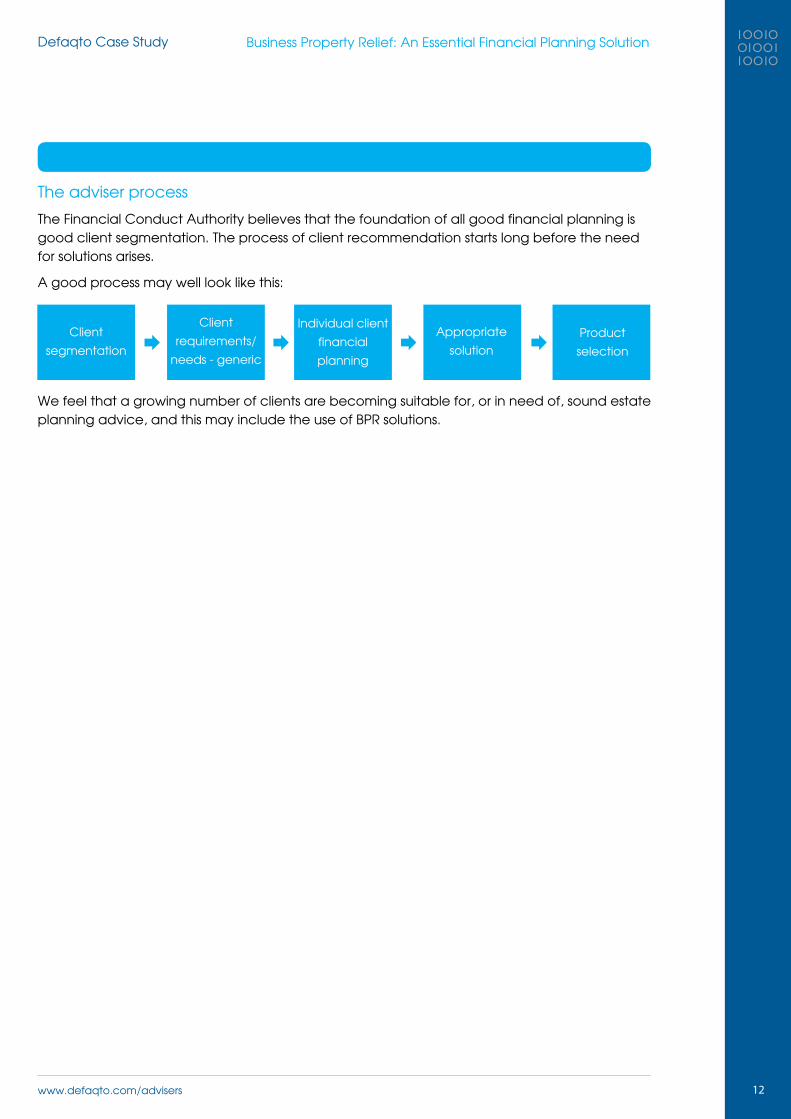

The adviser process

The Financial Conduct Authority believes that the foundation of all good financial planning is good client segmentation. The process of client recommendation starts long before the need for solutions arises.

A good process may well look like this:

Client

segmentation

Client

requirements/

needs - generic

Individual client

financial

planning

Appropriate

solutionProduct

selection

We feel that a growing number of clients are becoming suitable for, or in need of, sound estate planning advice, and this may include the use of BPR solutions.

Defaqto Case Study Business Property Relief: An Essential Financial Planning Solution

www.defaqto.com/advisers 13

Client segmentation

In relation to BPR, the indicators that this may be required at some stage would include:

• Existing assets well in excess of the IHT threshold of £325K (nil rate band)

• Maximum contributions already being invested into other tax-efficient solutions such as ISAs or pensions

• Owning a family business that has land, buildings and/or machinery of value

• Ill health - the likelihood of not surviving the seven years that would normally exempt gifts or transfers of assets (although this is more likely to crop up at client review than through client segmentation)

• Old age, for the same reasons

Defaqto Case Study Business Property Relief: An Essential Financial Planning Solution

www.defaqto.com/advisers 14

BPR selection

A process of due diligence needs to take place linking the circumstances and investment attitudes of the client to the available solutions in the market.

This section examines the kind of questions that advisers should ask, both in general and also specific to each client. We are using the Ingenious Estate Planning (IEP) solutions as the proof of concept. These solutions come in three variations.

• IEP Classic, which is a simple and flexible investment service designed to help investors maximise the value of their estate on death by protecting the value of the investment from IHT after two years.

• IEP Care, an investment service that provides the benefits of IEP Classic, but is specifically designed to help investors plan for potential care costs by giving them access to their investment should they need to fund care, while protecting whatever isn't withdrawn from IHT. In addition, the solution provides free access to independent care guidance at no additional cost.

• IEP Private, a tailored investment service that provides the benefits of IEP Classic, but also offers investors the flexibility to build and adjust their investment allocation to suit their personal goals.

Unless stated otherwise, the IEP Care service is the one used as the proof of concept throughout the rest of this report.

The due diligence process

Advisers should be armed with a list of due diligence questions that they need to apply to all potential BPR solutions under consideration. Some will be generic, and some will be client specific.

The investment firm

One of the fundamental issues that advisers need to satisfy themselves with before making a recommendation to a client, is whether they are comfortable with the firm managing their client's money. There would be three basic questions to ask here, which revolve around financial stability, experience in this area of investing and success of BPR claims.

Once it is accepted that some clients may be suitable for BPR solutions, the next stage is establishing which of those solutions are appropriate.

Allenbridge Analysis

Since being founded in 1998, Ingenious has raised and deployed more than £9 billion for private clients, institutional and corporate investors, including over £800 million in BPR-qualifying investments. All known BPR claims have been successfully upheld, the Manager states.

In this instance Defaqto would suggest that Ingenious are likely to meet any criteria set (£800m in BPR-qualifying investments is amongst the highest in the industry).

Defaqto Case Study Business Property Relief: An Essential Financial Planning Solution

www.defaqto.com/advisers 15

The investment strategy

This is clearly a very important aspect. We would suggest that BPR for financial planning is most likely to require a conservative approach with a good diversification of investments. This is not always the case, but where the solution is being used for estate value protection it seems to make sense.

It is also important that both adviser and client understand and buy in to the strategy adopted.

While IEP Care is a new product, the media and clean energy strategies which it employs are closely based on the media and clean energy strategies used in the existing Ingenious Estate Planning service.

There is clearly diversity of theme here, but it may be wise to look a little further into each strategy.

Allenbridge Analysis

The Manager has chosen three conservative, asset-backed trading strategies (each of which is adopted from the Manager's broader business activities), which should provide a range of return and liquidity profiles, each supported by a team of sector specialists. The three strategies are Media, Renewable Energy, and Real Estate.

Allenbridge Analysis

The media strategy is designed to preserve capital, and to deliver conservative but predictable growth and maximise liquidity. Through asset-backed lending on media projects, the Manager's aim is to ensure that transactions entered into provide a regular turnover of capital (to provide strong liquidity) while mitigating risk through diversification and secured income streams.

The clean energy strategy is designed to preserve capital, with investments characterised by low levels of volatility and minimal correlation to traditional investment markets. The clean energy strategy focuses on acquisition, operation and lending to a portfolio of renewable energy assets that are backed by strong cash flows and index-linked returns.

The real estate strategy is designed to preserve capital with investments that show low levels of correlation with movements in interest rates or inflation expectations. Through lending on residential development projects backed by full security over the properties, the Manager's aim is to ensure that transactions entered into provide a regular turnover of capital while mitigating risk through diversification and secured income streams.

Further detail of these strategies can be found in the appendix.

Defaqto Case Study Business Property Relief: An Essential Financial Planning Solution

www.defaqto.com/advisers 16

Specific solutions ˛ Long-Term Care

There may be clients who have the twin needs of estate planning and potentially the prospects of considering long-term care. Retaining control of the assets, even if run under a Power of Attorney, is clearly important here. BPR should be a consideration and more specifically a solution tailored to the specific circumstances.

There may even be clients who at this stage are only considering the estate planning aspect but potentially feel it is worthwhile addressing the possibility of the need for long-term care. There is always the risk of the need for long-term care, which if ignored, may ultimately lead to a higher than necessary erosion of the client's estate.

Ingenious has produced a variation of their standard Estate Planning solution IEP Classic, which has been tailored to the needs of those who are also considering long-term care.

In investment terms the strategies are the same. However, the IEP Care service includes access, at no additional cost, to long-term care specialists Grace Consulting. In addition, the product is administered so it can cope with the settling of regular invoices. This is quite important as liquidity with some BPR-qualifying companies can sometimes be an issue.

Allenbridge Analysis

IEP Care offers individuals a product that aims to provide (a) steady capital growth and access to the investment to help meet care costs, should they arise, during life and (b) protection of the remaining value of the investment from IHT on death. It should be noted that any value withdrawn from the investment during life will no longer qualify for BPR on death and may give rise to tax charges. An added benefit is elderly care guidance at no additional cost to investors.

The conservative investment strategy should appeal to low-risk investors seeking to protect their assets from IHT through BPR, investors seeking steady growth from an IHT protected portfolio, and those concerned with planning for long-term care costs. As the Manager is a leader in the field of BPR and EIS deal flow should be ample, thanks to the company's strong public profile.

To help with long-term care issues, Ingenious has engaged Grace Consulting to provide IEP Care investors with a comprehensive care guidance and support package for investors, need of care, at no additional cost. We understand that Grace Consulting is a leading independent provider of information, guidance and support regarding the options for care services in the UK.

Defaqto Case Study Business Property Relief: An Essential Financial Planning Solution

www.defaqto.com/advisers 17

Performance

It is obviously important that the solutions under consideration deliver to their mandate ˛ generally capital protection provided by a low growth, low-risk strategy. Requesting evidence of previous schemes and how they have performed to mandate is reasonable. For the Classic and Care versions, growth after fees of between 3% & 5% per annum is the target.

Ingenious Response

IEP Classic and IEP Care are new products. However, the media and clean energy strategies they undertake are closely based on the media and clean energy strategies for the existing Ingenious Estate Planning service and the relevant performance details are as follows.

• The media strategy within the existing Ingenious Estate Planning service has a mandate to deliver target annual growth of 1%-2% above the Bank of England base rate (after deduction of initial charges). Published performance since inception is fully in line with the mandate, with the latest 12-month NAV growth at 2.3%.

• The clean energy strategy of the existing Ingenious Estate Planning service has a mandate to deliver target annual growth of in excess of 5% per annum. Published NAV performance since inception is also fully in line with the mandate, with the latest 12-month NAV growth at 6.5%. Of the three strategies of investment (media, clean energy and real estate), the Manager can show a long record of successfully meeting mandate aims in media and is well on its way to establishing a similar record of success in relation to its clean energy mandates.

• The real estate strategy is a new addition and it is too early in the investment cycle to have an established track record, although Ingenious has demonstrated its commitment to the strategy by making a seed investment of £9.9m to commence the trading activities of the Real Estate division.

Defaqto Case Study Business Property Relief: An Essential Financial Planning Solution

www.defaqto.com/advisers

Cost

There are no hard and fast definitive rules here. If the solution is precisely what the investor needs and is the most suitable in the market, generally speaking it may be worth paying a little more for. A good example is the Ingenious Care product. Fees are a little more than the standard variation of IEP Classic, but there is the inclusion of access to Grace Consulting and built-in enhanced liquidity to help with care invoice payments; potentially worth paying a little extra for to solve two financial planning needs in one.

Of course this is something only the client can judge with help from their financial adviser.

18

Defaqto Analysis

The standard offering from Ingenious, IEP Classic, with initial fees of 1.5%, dealing fees of 1% and annual management fee of 1% which is only payable if the minimum growth target of 3% is achieved plus additional 0.25% administration fee, is in line with the market for these specialist solutions. The IEP Care version has similar charges although the initial investment fee is 2%. This seems reasonable for the enhanced liquidity and Grace Consulting access when needed.

Defaqto Case Study Business Property Relief: An Essential Financial Planning Solution

www.defaqto.com/advisers 19

Summary

The key advantages are that the investor retains control of the assets. BPR applies after a qualifying period of only two years, whereas other solutions, such as gifting under trust, require surviving seven years to receive full exemption and there is a loss of beneficial ownership. The latter not usually a problem but there could be potential problems if the assets are no longer owned by the client.

The balance is that investment will only be in very small companies, which by their nature carry more risk.

There are essentially six elements that should be fundamental to the due diligence carried out on any proposition. Without satisfactory answers to any of these, given the specialist nature of the product, investment should not go ahead:

• The firm itself ˛ history of success including a record of BPR-qualifying failures; research resource

• Experience of the investment team in the relevant market

• Performance history (in terms of following the mandate rather than absolute, as many have low growth expectations in return for lower risk). This would include payment of, and level of, income if this is important

• Diversification ˛ sector, themes, number of stocks

• Structure of solution (SPV, EIS or AIM portfolio)

• Cost

There may well be other essential ingredients that are client specific. For example, in the context of Ingenious IEP CARE offering, access to Grace Consulting and the enhanced liquidity available for paying of care invoices will appeal to clients using BPR as a long-term care solution, for instance. If relevant these should be factored in on a case by case basis.

Perhaps still not a mainstream financial planning solution BPR should now be considered as potential solution for a growing number of clients.

Finally, much of the due diligence required is well within the capabilities of most advisers. However, there is certainly some specialist knowledge required of this market and its product providers. If help is required there are certainly firms out there, such as Defaqto and Allenbridge, that can assist with all or some of the due diligence.

The use of BPR is essentially a function of investment risk assessment, tax planning and client need, and as such can only really be decided upon following an in-depth client fact find.

Defaqto Case Study Business Property Relief: An Essential Financial Planning Solution

www.defaqto.com/advisers 20

Appendix - More details on the Ingenious Investment Strategy

Media strategy

An example of trading activities targeted by the Manager includes providing asset-backed loans to finance film and TV productions; an area in which the Manager has long experience. Since 2005, Ingenious Broadcasting has produced over 530 hours of programming across over 135 television projects and has made c. 85 loans worth c. £80m, either through Ingenious Estate Planning or the Ingenious Broadcasting Partnerships.

Under a typical transaction, the BPR Company would advance funds to the producer of a television programme or film secured against certain identified assets, which may include broadcaster licence fees, pre-sale contracts, distribution advances and state subsidies.

In assessing a prospective loan, full due diligence is undertaken, with consideration given to a broad range of factors including term, counterparty(ies) involved, asset security, insurance package/production cost/budget/schedule (if applicable). Loans would include penalties for late payment.

Clean energy strategy

An example of trading activities targeted by the Manager include renewables energy projects with stable pricing backed by strong counterparties and, where applicable, government guaranteed subsidies.

Ingenious has a dedicated clean energy team, comprising 12 industry experts with strong experience across the sector. To date, Ingenious has over £180m of capital under management in this, or similar strategies.

Transactions may include buying renewable energy assets, particularly solar photovoltaic (PV), although other technologies can also fall within the investment remit, as long as they are proven and well tested (e.g. onshore wind, biomass etc.)

Real estate strategy

An example of trading activities targeted by the Manager includes providing fully- secured development and bridging loans to experienced developers on wholly or mainly residential development and redevelopment projects, predominantly in London and its commuter belt.

The real estate strategy has been designed to take advantage of the widely reported, restricted supply of credit from banks to residential property developers, who may struggle to access sufficient finance on acceptable terms to fund developments that already have full planning.

The body of the publication has given a high level view of the Ingenious investment strategy undertaken by the BPR companies in IEP Care. Further analysis by Allenbridge of each strategy follows.

Defaqto Case Study Business Property Relief: An Essential Financial Planning Solution

www.defaqto.com/advisers

Test yourself

In order to assess your knowledge following completion of this publication, why not work your way through the following questions? All the answers can be found within the content of this publication.

1 What are four assets that may qualify for BPR?

2 What was the main reason for bringing in BPR, in the 1976 Finance Act?

3 For how long does an asset need to be held to qualify for BPR?

4 Other than the period of qualification, what other advantage does BPR have over trust-based IHT planning?

5 What are three reasons why you may consider BPR for a client?

6 What are five key areas of due diligence when considering a solution?

Send Us Your Feedback

Your feedback is extremley important to us and we would be grateful if, after completing this publication, you could take a few minutes to complete a short survey. Your answers will be treated in the strictest confidence and the results of this will help the development of future publications.

The survey can be accessed at:

http://surveys.defaqto.com/surveys/businesspropertyrelief2014/businesspropertyrelief2014.htm

21

Defaqto Case Study Business Property Relief: An Essential Financial Planning Solution

www.defaqto.com/advisers

Notes

Defaqto Case Study Business Property Relief: An Essential Financial Planning Solution

www.defaqto.com/advisers

Notes

Defaqto Case Study Business Property Relief: An Essential Financial Planning Solution

www.defaqto.com/advisers

Notes

Defaqto Case Study Business Property Relief: An Essential Financial Planning Solution

www.defaqto.com/advisers

Get in touchPlease contact your Defaqto Account Manager or call us on 0808 1000 804www.defaqto.com/advisers

© Defaqto Limited 2014. All rights reserved. No parts of this publication may be reproduced in any form by any means, whether electrical, mechanical, optical or any other or be stored in a retrieval system without the express written permission of the publisher. The publisher has taken all reasonable measures to ensure the accuracy of the information and ratings in this document and cannot accept responsibility or liability for errors or omissions.

Supported by