-

7/28/2019 causes of inadequate use of ADR in tax dispute

settlement

1/42

CERTIFICATION

The undersigned certifies that he has read and hereby

recommends, for the acceptance of the

Institute of Finance Management research entitled Causes for

inadequate use of

Alternative Dispute Resolution in Tax Dispute Settlement, a case

study of Tax Revenue

Appeals tribunal, in partial fulfillment of the requirements for

the award of Postgraduate

Diploma in Tax Management (PGDTM).

.......................................................................................

Zawadi, O.

(SUPERVISOR)

Date...............................................................................

i

-

7/28/2019 causes of inadequate use of ADR in tax dispute

settlement

2/42

DECLARATION

I, Sabiha Abdi Nassib, hereby declare that this research is my

own original work, and that it

has not been submitted to any other university/institute for a

similar or any other degree

award.

Signature

..

Date

ii

-

7/28/2019 causes of inadequate use of ADR in tax dispute

settlement

3/42

Copyright by Sabiha Abdi Nassib

All rights reserved

2011

iii

-

7/28/2019 causes of inadequate use of ADR in tax dispute

settlement

4/42

DEDICATION

I dedicate this work to my dearest son, Abdulrahim Kirondomara

for and to My

Lovely Husband for.

iv

-

7/28/2019 causes of inadequate use of ADR in tax dispute

settlement

5/42

ACKNOWLEDMENT

First and foremost I would like to thank the Merciful Allah who

gives me power and health

all the time for the whole period of my studies.

Many people in one way or another, directly or indirectly,

contributed in accomplishment of

this research paper .Iam grateful to take this opportunity to

acknowledge them.

I sincerely thank Mr. Mujuberi, my supervisor for his tireless

guidance on critical issues

concerning this study.

Also ,I would like to express my deeper gratitude to the member

of my family especially my

beloved husband Mr. Soud H.Soud, my mother Mrs.Mwanjabu

M.Omar,all my sisters and

my brothers for looking after my children .Without their support

it would be very difficult to

reach where I am now.

I am also greatly indebted to the management of Ministry of

Education, Officers, teachers

and all of my respondents. I appreciate the cooperation offered

to me. Without them my work

could go astray.

Special thanks to my sister Sabiha Nassib ,who accorded me with

all the support and

conducive environment during my study .She has been very helpful

and I appreciate what

she has done for me , so I take this opportunity to say a warm

thank you

v

-

7/28/2019 causes of inadequate use of ADR in tax dispute

settlement

6/42

Finally ,I would like to appreciate all my lectures and my

classmates of MPA (Human

Resource Management) in 2007/2009 ,for being cooperative to me

during our study which

has enabled accomplishment of my study.

vi

-

7/28/2019 causes of inadequate use of ADR in tax dispute

settlement

7/42

LIST OF ABBREVIATIONS

TRAA - Tax Revenue Appeals Act

TRAT - Tax Revenue Appeals Tribunal

TRAB - Tax Revenue Appeals Board

R.E - Revised Edition

TRA - Tanzania Revenue Authority

ADR - Alternative Dispute Resolution

vii

-

7/28/2019 causes of inadequate use of ADR in tax dispute

settlement

8/42

LIST OF TABLES

TABLE PAGE

Table 1: Sampling procedure 22

Table 2: Age of respondents 30

Table 3: Gender of respondents 30

Table 4: Age of respondents 35

Table 5: Education level 35

Table 6: Subject respondents used to teach 36

viii

-

7/28/2019 causes of inadequate use of ADR in tax dispute

settlement

9/42

LIST OF FIGURES

Figure Page

Figure 1: Tax Appeal resolution machinery and its hierarchy

28

Figure 2: Education level 31

Figure 3: The level of satisfaction 32

Figure 4: Intention to leave the job 33

Figure 5: Gender of respondents 34

Figure 6: Lengths in Teaching 37

ix

-

7/28/2019 causes of inadequate use of ADR in tax dispute

settlement

10/42

LIST OF STATUTES

x

-

7/28/2019 causes of inadequate use of ADR in tax dispute

settlement

11/42

LIST OS CASES

xi

-

7/28/2019 causes of inadequate use of ADR in tax dispute

settlement

12/42

APPENDICES

Appendix 1: Area of the study 55

Appendix 2: Questionnaire 1 56

Appendix 3: Questionnaire 2 58

Appendix 4: Questionnaire Swahili version 60

Appendix 5: Questionnaire Swahili version 62

xii

-

7/28/2019 causes of inadequate use of ADR in tax dispute

settlement

13/42

ABSTRACT

The study intended to examine the factors contributing to

teachers turnover from

Government Secondary Schools; the Urban West Region in Zanzibar

was the focus of this

study.

Specifically the study was expecting to identify the factors

that contributing teachers change

their jobs or to leave government schools and employed in

private schools. Another objective

is to propose possible measures to the top management of

Ministry of Education in dealing

with the high rate of teachers turnover.

The data for this study were collected from documents,

standardized questionnaires,

interviews and informal discussions. Both statistical and

descriptive methods of data analysis

were used.

From this study the researcher found that job dissatisfaction

was the major reason teachers to

leave government schools and turn either to private schools or

to other institutions. Other

reasons includes poor working condition, low salary, lack of

motivation as well as poor

relationship between teachers and their supervisors.

xiii

-

7/28/2019 causes of inadequate use of ADR in tax dispute

settlement

14/42

DEFINITION OF THE KEY CONCEPT USED

One main concept has been used in this study and the researcher

sees the need of

defining it;

Alternative Dispute Resolution (ADR, sometimes also called

Appropriate Dispute

Resolution or External Dispute Resolution in some countries,

such as Australia) is a

general term, used to define a set of approaches and techniques

aimed at resolving

disputes in a non-confrontational way (i.e. includes dispute

resolution processes and

techniques that fall outside of the government judicial

process).

ADR covers a broad spectrum of approaches, from party-to-party

engagement in

negotiations as the most direct way to reach a mutually accepted

resolution, to

arbitration and adjudication at the other end, where an external

party imposes a solution

(Yona Shamir, 2003).

The ADR movement started in the United States in the 1970s in

response to the need

to find more efficient and effective alternatives to

litigation.

Recently, ADR has become institutionalized as part of many court

systems and system

for justice as a whole throughout the world.

There are four common types of ADR, that are;

(i) Mediation

(ii) Arbitration

(iii) Conciliation

(iv) Adjudication

xiv

-

7/28/2019 causes of inadequate use of ADR in tax dispute

settlement

15/42

TABLE OF CONTENTS

LIST OF

ABBREVIATIONS.............................................................VII

RESEARCH

METHODOLOGY..........................................................11

3

INTRODUCTION.......................................................................11

xv

-

7/28/2019 causes of inadequate use of ADR in tax dispute

settlement

16/42

xvi

-

7/28/2019 causes of inadequate use of ADR in tax dispute

settlement

17/42

xvii

-

7/28/2019 causes of inadequate use of ADR in tax dispute

settlement

18/42

CHAPTER ONE

INTRODUCTION

1.1 BACKGROUND TO THE PROBLEM

Dispute between tax authorities and tax payers are inescapable.

This is irrespective of

how well a tax system is developed. The mechanisms for resolving

tax disputes are

very critical in ensuring that tax administration is not only

efficient but also respectable

and fosters public trust (Luoga, 2009).

In ensuring so, the Government introduced unified Tax Appeal

machinery under which

tax disputes arising from all Revenue Laws administered by

Tanzania Revenue

Authority (TRA) have to be lodged in the same appellant

authority. The Act of

Parliament, Tax Revenue Appeals Act, Cap 408 Revised Edition of

2006 under Section

4 and Section 8 establishes the Tax Revenue Appeals Board (TRAB)

and Tax Revenue

Appeal Tribunal (TRAT) respectively.

One among the powers vested to TRAT under Section 17(1) of TRAA,

Cap 408 R.E of

2006 is to resolve complaint or appeal by using mediation,

conciliation or arbitration,

that is to say the Tribunal is powered to use Alternative

Dispute Resolution (ADR) in

its dispute settlement. The section reads as follows;

17(1) The Board and the Tribunal shall respectively have the

power

(a)

(b) To resolve any complaint or appeal by mediation,

conciliation or

arbitration

Many researches has examined the importance and usefulness of

using ADR especially

mediation in disputes settlement. According to (Merricks, 2007)

conciliation,

mediation, arbitration and adjudication are now commonly

encounted in such diverse

field as family break down, construction disputes, shipping and

insurance and travel

agency complaints. Merrick is of the view that ADR is the

umbrella term for services

that provide for the opportunity of resolving disputes without

going to Court.

1

-

7/28/2019 causes of inadequate use of ADR in tax dispute

settlement

19/42

He concluded by saying that, the Financial Ombudsman Service has

developed a very

different model from that of the Civil Courts and is the

preferred alternative for most

retail Consumers of Financial Service. The comparison in style,

process, institutional

systems and legal approach may offer observers fund for thought

about potential

development in the Civil Courts themselves.

The current resolution procedures which involve heavy emphasis

on the Courts do not

provide an efficient system to meet the needs of contemporary

industrial relation

(Singh, 1995).

Despite of the fact that TRAT is powered to use ADR, and many

studies have been

conducted regarding the importance and usage of ADR, the records

shows that only

1.2% of the cases determined by TRAT have used ADR and the cases

were marked

settled between the parties.

From that history, is where the researchers interest arose in

exploring the causes that

lead to inadequate use of ADR in Tax dispute settlement.

1.2 STATEMENT OF THE PROBLEM

The usage of ADR in dispute settlement is now common and used in

almost every

corner in the world.

The intension of this research is to deal with the properly and

adequate use of the ADR.

ADR can be used effectively if the parties to the particular

case have interest in that

case, the nature of the case is allow it and the judge has a

knowledge of ADR process.

Many findings from the studies reveals that the usage of ADR is

very effective in cost

savings (Broker, 2009) immediate resolution (of the dispute),

building the good ending

relationship between the parties and openness and transparency

(as the parties get to

know the position of the case and predict the out come and when

the decision

concluded it is known to both parties and do not come as a

surprise as it appears in

normal Civil Courts) (Merricks, 2007).

2

-

7/28/2019 causes of inadequate use of ADR in tax dispute

settlement

20/42

Moreover, (Ilter & Dikbas, 2009) have found out that most of

parties agreed to the

need for moving away from adversarial methods of dispute

resolution. This is because;

ADR is short and low costs process, the fear of bad reputation

in the sector during it

litigation, trying to avoid the deterioration of the close

relationships they have with

other parties, trying to avoid the work hours spent for the

preparation of litigation or

arbitration, and the fear of losing in litigation due to the

tendentious contrasts.

The mediation procedure has found favour with many litigants in

several jurisdictions

and helped to restore the faith of the general public in the

judicial system. In one

jurisdiction over 40% of the over 2,500 cases disposed of in one

year were mediated

settlements (mapigano,J. 1998).

Regardless of that analysis, TRAT still uses common known way of

dispute resolution

under civil proceedings in most of cases.

Therefore this study helped in finding the factor that causes

the inadequate use of the

alternative dispute resolutions in tax dispute settlement and

provide recommendations

that will help to improve the usage hence eliminate the

problem.

1.3 OBJECTIVE OF THE STUDY

1.3.1 GENERAL OBJECTIVE

The general objective of the study is to find out the cause for

inadequate use of ADR in

tax dispute settlement.

1.3.2 SPECIFIC OBJECTIVES

The specific objectives of this study are:-

i. To identify the causes of inadequate use of ADR in the Tax

Revenue Appeals

Tribunal.

ii. To identify whether there is a need of using ADR in dispute

resolution

3

-

7/28/2019 causes of inadequate use of ADR in tax dispute

settlement

21/42

iii. To suggest the measures to be taken by TRAT in dealing with

the identified

problem

1.4 RESEARCH QUESTIONS

This study will answer the following questions;

i. What factors influence inadequate use of ADR in Tax Revenue

Appeals

Tribunal?

ii. Why the ADR has to be used in dispute resolution?

iii. What measures to be taken to improve the usage of ADR?

1.5 SIGNIFICANCE OF THE STUDY

The findings of the study will explore the important element for

the usage of ADR, by

doing so it will help the respective bodies to implement ADR as

it is required by the

law. Also it will introduce the weakness of the ADR and it will

give the parties a wider

room for choosing the usage of the system.

By knowing the importance of ADR this study will also explore

for the need of using

ADR in dispute settlement.

Lastly, the study is expected to enhance TRAT (i.e. members and

parties to the dispute)

to use the ADR so that it can exercises its powers

effectively.

1.6 SCOPE OF THE STUDY

The study will cover the in depth on the usage of ADR at Tax

Revenue Appeals

Tribunal and it will be conducted in Dar es Salaam. This is

because headquarter of the

case is situated in Dar es Salaam and that is where the

researcher will find all expected

respondents.

4

-

7/28/2019 causes of inadequate use of ADR in tax dispute

settlement

22/42

The study data will be referred to eight (8) years. This is

because TRAT has officially

stated its work from 2002.

1.7 CHAPTER SCHEME

The study consists of six chapters.

Chapter one comprises the background of the study, statement of

the problem, objectives

of the study, research questions, significance, scope and

chapter scheme of the Study.

Chapter two present literatures review which look at the

previous study concerning the

problem

Chapter three focuses on research methodology.

Chapter four provide an overview of the Tax Revenue Appeals

Tribunal (TRAT), its

dispute resolution mechanism, cases decided and evaluation of

the method used in

deciding those cases.

Chapter five presents analyses of the research findings.

Chapter six presents summary of the findings, conclusion and

recommendation of the

study

5

-

7/28/2019 causes of inadequate use of ADR in tax dispute

settlement

23/42

CHAPTER TWO

LITERATURE REVIEW

2.1 CONCEPT OF ADR AND THEORETICAL LITERATURE REVIEW

As is appears that disputes are an integral part of human

interaction, we must learn to

manage them, to deal with them in a way that will prevent

escalation and destruction

and come up with innovative and creative ideas to resolve

them.

(Benner, 1995) reveals that, for some time now we have conflict

and it often occurs

when people of different cultures, personalities, expectation

sets, etc interact together.

He said that conflict is seen as given and our best expectation

is to be able to

resolve it or reduce is through the use of strategies, for

examples consensual

approaches and third party intervention. He add that, no one

will dare to suggest that

there assumption, in fact, creates a context for conflict, and

all attempts to deal with it

rise from this basic assumption. People discuss strategies for

resolving conflict,

hopefully in a win-win manner, but no one dares to suggest that

conflict would be

transcended.

Researchers have found that there is a need to initiate special

programmes for conflict

resolution and mediation. They believe that as learned to cope

with conflict and to live

and work more harmoniously with each other we would gain an

increased sense of

control over our own life and the confidence to assume

responsibility for the common

good. The programmed was designed to facilitate a climate of

collaborative learning

and problem solving. The intent was to orient people, connect

them with each other,

and teach them to internalize and apply conflict resolution

skills. (Gahr, Mosca, Sarsar,

1995).

(Mbunda, 1985) writes on dispute settlement prior and after

independence. He

comments on the efforts of the government to have informal

procedures of settling

disputes in Primary Courts. He argued that the procedures used

are not familiar to many

litigants, as they do not resemble customary dispute settlement

procedures. He contends

further that the dominant civil procedure law, which is an

adversarial system of dispute

settlement, presupposes that the litigants are literate, have

enough legal knowledge and

6

-

7/28/2019 causes of inadequate use of ADR in tax dispute

settlement

24/42

know all the technicalities of the law. He further cautions that

the situation in Tanzania

does not allow the application of such rules without causing

injustices. His work is not

based on ADR, but it is relevant to this study in the sense that

it narrates the historical

aspects of disputes resolution mechanisms in Tanzania.

Otaru in her paperAlternative disputes Resolution mechanism in

Tanzania 2003,

discusses the development of ADR in Tanzania. The author also

tries to contrast ADR

and pre-colonial or traditional disputes mechanism and opines

that ADR in Tanzania

can perform better by reintroducing those traditional methods of

dispute settlement, her

main argument being that in most cases even when settlement is

reached under ADR is

not for full satisfaction of both parties unlike in traditional

disputes settlement

mechanism, as the former will have already incurred cost prior

going into process of

mediation. She contends further that in practice some agreements

in form of settlement

are not fulfilled by the very parties, thus bringing them to a

litigation process in trying

to enforce them. The author does not assess other factors such

as the problem of dual

function of court, the importance and advantages of using ADR

and the important

factors to be considered before using ADR adequately which are

discussed in this

study.

(Mapigano, J, 1998) comments that ADR is a solution to inherent

problems and flaws

of litigation created by adversarial model of dispute

resolution, which is very

expensive, long and too complicated for many litigants and

favours the rich and

educated. He further documents the reason for adoption of

mediation in Tanzania and

the conduct of the mediation process. The manual is intended to

be used as a guideline

for mediators. It also provides a guide to researchers on

historical aspects of ADR in

Tanzania.

According to Chipeta, ADR is generally understood in most cases

to mean mediation.This is due to the fact that ADR in Tanzania is

so far has taken a form of mediation and

is forming part and parcel of civil procedure law. This kind of

definition in some cases

in practice has not been extended to cover instances such as

settlement of dispute

mechanism. Therefore, ADR in Tanzania forms part and parcel of

civil procedure law

and is mandatory annexed to the court system (Gillah, 2006)

7

-

7/28/2019 causes of inadequate use of ADR in tax dispute

settlement

25/42

For a tax system to be efficiency, among other elements, it must

have a manageable

dispute mechanism. There must be special and independent

institutions that hold

hearing and solve disputes regarding tax issues, and tax payers

to have the right to

appeal against the assessment during first five years from the

assessment date.

(Vlaseenko 2001).

2.2 EMPERICAL LITERATURE REVIEW

There are several researches on the use ADR in dispute

settlement, which have been

conducted by different sources.

The analysis reveals that nature of case, interest of parties

and skill and knowledge of

Mediator (Judge) and merit of the case are positively related to

the use of ADR.

1.7.1.1 Interest Of The Parties

According to (Brooker, 2009) the findings of the mediation of

the USA study show that

the critical factor for non-settlement of dispute by mediation

was found to be the

attitude of the parties. He is of the view that Mediation was

often ineffective when one

or more of the parties had unrealistic expectations, were

intransigent or unwilling to

compromise or when both parties were too far a part at the

beginning of the process.

1.7.1.2 Nature Of The Case

Nature of the case is one of the determinant of using ADR. Most

cases by their nature

are suitable, but some subject matters will be intristically

unsuitable for ADR. In the

case ofHalsery v. Milton Keyves GeneralNHS [2004] ELUCA GV 576,

the Court

illustrate a number of situation when it might be considered

safe to reject mediation.

There is where:-

A party requires a court determination on a point of law;

The issue are important for future business;

8

-

7/28/2019 causes of inadequate use of ADR in tax dispute

settlement

26/42

A case involves fraud or disreputable commercial conduct;

A party desire an injunction; and

There is a need for a binding precedent

(Ilter & Dikbas, 2009)

1.7.1.3 Skills And Knowledge Of The Mediator

The question of who become a mediator has been one of the mostly

debated issue.

As mediation involves conflict management, behavioral

psychology, communication,

negotiation techniques and voluntariness the judges must be very

well trained and

equipped for going to ADR. The training programs are very

important and had to be

organized for this context and it should be available for all

profession as soon as

possible (Ilter & Dikbas, 2009)

Lack of understanding and experience in ADR can best be overcome

by educating

and training. This should be carried out early on in the working

lives of professionals

by universities, professional institutions and specialist bodies

such as the CEDR.

( Ekene, Ezulike & Hoare, 1998)

2.3 THEORETICAL FRAME WORK

This study reveals that there is one dependant variable which is

the use of ADR and

three independent variables which are interest of the parties,

nature of the case and skill

of the Judges/Mediator.

The dependent variables is influenced by those three independent

variable. Those three

independent variable are also interrelated as explained

below.

Nature of the case naturally have a big impact on the type to be

used for dispute

resolution. Some cases are very complicated and need for the

hard reference of law,

strong arguments, reliable evidence and enough time for

preparation. When nature of

9

-

7/28/2019 causes of inadequate use of ADR in tax dispute

settlement

27/42

the case is ignored and the parties choose to inter into a

dispute resolution the outcome

of it will not be good for either of the case, because when

litigation (normal civil

procedure) is adopted, the parties might end up in bad

relationship at the end of the

case, meanwhile, if ADR is used and the parties feels that they

are un-satified with the

decision they will lose their chance for appeal. From these we

can see that there is an

importance of the Mediator/Judge to have enough skill so he can

advice on the

situation of the case and the parties has to be interested to

use either of the two methods

and this is where this variables relate.

Skill of the Judge/Mediatoris also an important element in the

use of ADR. In order

for the out come of the case to be fair, and effective, not to

be bias and base on one

party, the mediator must have enough skills to sit in the table

and lead to the mediation.

However, even if the judge is well equipped, but the nature of

the case does not support

for ADR, and also parties are not interested. Then it will be

difficult for ADR to be

used.

Interest of partiesare also an important element of ADR. If

parties to the dispute are

not interested in the usage of ADR but all other element are

positive, ADR can not be

used.

In conclusion, both interest of parties, nature of the case and

skill of the mediator

significantly influence the use of ADR.

10

-

7/28/2019 causes of inadequate use of ADR in tax dispute

settlement

28/42

CHAPTER THREE

RESEARCH METHODOLOGY

3 INTRODUCTION

This chapter intended to cover the methodology that used when

conducting the study.

It provides the framework for specifying the relationship among

the study variables

and a plan for selecting the sources and types of information

that used in answering

research questions, and achieving the research objectives. The

sections covered here

aimed in identifying the causes for inadequate use of ADR in tax

dispute settlement.

3.1 RESEARCH DESIGN

The researcher used case study which aimed at identifying the

causes for inadequate

use of ADR in tax dispute settlement at the Revenue Appeal

Tribunal being the case.

The researcher used the case study because this study was aimed

at looking only on

one stage of tax dispute settlement which is TRAT. The

researcher choose TRAT to be

the case because, in hierarchy TRAT as considered as equal to

the High Court in Court

Hierarchy of Tanzania, and the parties after being aggrieved by

the decision of the

TRAT have left with only one place for appeal which is the Court

of Appeal, therefore,

if TRAT is able to use ADR and settle the dispute between tax

payer and tax authority

the parties will have a good room for resolution without going

to the final appellate

body.

3.2 TARGET POPULATIONThe study covered the Chairman and Members

of the TRAT, the tax payers and their

representative, the Offices from Tax Authority who represented

the Commissioner

General, Management and Staff of TRAT.

The researcher intended to analyse five areas as follows,

11

-

7/28/2019 causes of inadequate use of ADR in tax dispute

settlement

29/42

i) The view of the parties to the dispute on the need of using

ADR in tax dispute

resolution.

ii) The current usage of ADR

iii) The intension of the parties in using ADR

iv) The knowledge of TRAT and parties to the case about ADR

v) The important elements in using ADR

3.3 SAMPLING PROCEDURE AND SAMPLING SIZE

3.3.1 Sampling Procedure

The study used both probability and non probability

sampling.

In probability the simple random sampling was employed to the

majority such as tax

payers, tax consultants and auditors, advocates and officers

from TRA representing the

Commissioner General. This was used because the researcher

wanted to give equal

chance to the members of population.

In non-probability the researcher applied purposive sampling to

selected Chairman,Vice chairman, members of the Tribunal,

management and staff because these are

group of population who hold key position. It was believed that

the selected sample can

give a picture on what they see and understand about the problem

from their

experience.

3.3.2 Sampling Size

One institution was studied which is TRAT and 50 respondents

were selected and

examined.

The sampling was as follows:-

i. Members of the Tribunal including the Chairman/Vice Chairman

- 6

ii. Management and Staff 1 registrar, 3 officers.

12

-

7/28/2019 causes of inadequate use of ADR in tax dispute

settlement

30/42

iii. Parties to the cases which are:-

(a) 15 Tax payers

(b) 15 Tax payers representatives (10 advocates and 5 tax

consultants and

auditors)

(c) 10 Officers from TRA who represented Commissioner

General.

3.4 DATA COLLECTION METHOD

In the course of carrying out this research, the researcher was

able to use both primary

and secondary data since it was very difficult to rely on one

technique or method due to

the nature of the study.

3.4.1 Collection of Primary Data

Methods used to collect primary data/information included

Questionnaires surveys,

Interviews and Participant Observation. These are explained

briefly in the following

sections:

(a) Interviews

Semi- structured interviews were administered to Chairman, Vice

chairman, Members,

Management and Staff of the Tribunal in order to explore the

factual data observed by

people interviewed. The aim was to gather information on the

causes for inadequate use

of alternative dispute resolution.

(b) Questionnaire survey

The questionnaires were used to collect information from tax

payers, representatives of

tax payers and officers from TRA who represented the

Commissioner General. The

researcher used both open ended and close ended questions in the

questionnaire. Each

item of the questionnaire was developed to address a specific

objectives and research

questions of the study.

13

-

7/28/2019 causes of inadequate use of ADR in tax dispute

settlement

31/42

Forty respondents were provided with questionnaires. The

questions were asked in the

questionnaires as researcher could probe on any matter arising

as salient and useful for

this study.

(c) Participant Observation

Other data or information were collected by participant

observation, as a researcher

being a full time employee of the study area who participate in

daily routine of hearing

and determining the cases, she had an opportunity to participate

in the study and attend

all sessions of the Tribunal hence obtain information needed for

the research.

3.4.2 Collection of Secondary Data

Secondary data was obtained from various documents and other

written reports

available from different places and main information centers,

where different materials

were accessed include libraries at University of Dar es Salaam

and High court.

However, most information was available at the TRAT offices

through a perusal on

Tribunal case files, case registers, law reports, unreported

cases, statutes, journal

articles, legal sector reports and various circulars. Textbooks

and websites were also

very resourceful in providing useful information in the course

of writing this research.

3.5 DATA ANALYSIS & INTERPRETATION

Both qualitative and quantitative techniques were used. This is

because of the nature of

the data and information that obtained during the research.

Quantitative data analysis was used to describe the data in the

form of numerical values

accompanied by charts, tables, and percentages. The responses

were summarized and

tabulated and percentages were computed by using MS Excel

software package to

establish relationship of various variables. Finally the

researcher will reveal the internal

validity, reliability and objectivity of the research

conducted.

On the other hand qualitative means was employed to describe

information that is not

of numerical nature.

14

-

7/28/2019 causes of inadequate use of ADR in tax dispute

settlement

32/42

CHAPTER FOUR

AN OVERVIEW OF THE TAX REVENUE APPEALS TRIBUNAL (TRAT)

AND THE CASE SETTLEMENT PROCEDURE.

4. INTRODUCTION

The intension of the researcher was to find out the causes for

inadequate use ADR in

tax disputes settlements where Tax Revenue Appeals Tribunal was

a case study. It

became meaning less to discuss the tax disputes resolution

without having a clue of

what Tax Tribunal is, this is because TRAT is the only

institution in Tanzania which

has the power to entertain tax disputes with an appellate

jurisdiction same as High

Court.

4.1 BACKGROUND

4.1.1 The history before 2000

Prior to the establishment of the New Unified Tax Appeals

Machinery, there was the

National Tax Appeals Board, which had jurisdiction to hear and

determine only Income

Tax Appeals arising from the decisions of the Commissioner of

Income Tax. After that,

the aggrieved party had a room to appeal to the High court and

finally to the Court of

Appeal of Tanzania.

4.1.2 Establishment of the unified tax appeals system

Due to the fact that tax cases are very sensitive and require

special attention as tax

being the main source of income or revenue in our country, and

that following the tax

appealing system in that time, tax cases were taking longer in

determination process

hence either the government was loosing the income or tax payers

was loosing their

access to justice as the saying goes justice delayed is justice

denied.

15

-

7/28/2019 causes of inadequate use of ADR in tax dispute

settlement

33/42

So in year 2000, the Government decided to establish Unified Tax

Appeals machinery

under which tax disputes arising from all Revenue laws

administered by Tanzania

Revenue Authority (TRA) have to be lodged in the same appellate

authority.

In order to implement the policy of unified Tax Appeal machinery

the Parliament

enacted the Tax Revenue Appeals Act, Cap 408 [RE 2006], which

establishes Tax

Revenue Appeals Board and Tax Revenue Appeals Tribunal.

These Tax Revenue Appeals Board (TRAB) and Tax Revenue Appeals

Tribunal (TRAT)

are quasi-judicial institutions, established under Sections 4

and 8 of the Tax Revenue

Appeals Act, Cap 408 [RE 2006] respectively. Hierarchically TRAB

is jurisdictionally

equivalent to Resident magistrate court and TRAB is

jurisdictionally equivalent to High

Court.

4.2 AN OVERVIEW OF TRAT

4.2.1 Objective

The core objective of establishing the Tax Revenue Appeals

Tribunal is that of a

speedy, efficient, effective and impartial resolution of tax

appeals arising from decision

of the Tax Revenue Appeals Board.

4.2.2 Function of the Tribunal

The functions of Tax Revenue Appeals Tribunal are as

follows:-

a. To hear and determine, tax appeals arising from decision of

the Tax Revenue

Appeals Board as provided for by Section 11 of the Tax Revenue

Appeals Act,

Cap 408 [R.E 2006].

b. To supervise Tax Revenue Appeals Board in the exercise of its

powers under

Tax Revenue Appeals Act, Cap 408 [RE 2006]

c. Giving advice to parties to tax disputes on procedures of

appealing to the

Tribunal.

16

-

7/28/2019 causes of inadequate use of ADR in tax dispute

settlement

34/42

d. To provide public awareness on Tax Revenue Appeals Act and

other related tax

laws.

4.3 DISPUTE RESOLUTION MECHANISM

4.3.1 Appeal procedure

(a)Start of the Appeal

The appeals start at TRAB after the tax payer being aggrieved by

the decision of the

Commissioner General, TRAB determine the case and give out its

decision. Any one

who is not satisfied with the decision of the Board lodges an

appeal to TRAT.

A person who wishes to appeal to the Tribunal shall issue a

written notice of intention

to appeal within fourteen days from the day of the decision of

Board. The said notice

shall state whether the intended appeal is against the whole

decision or part of the

decision of the Board.

A notice of intention to appeal shall be made in the Form TRT .1

and shall be signed by

or on behalf of the appellant. Where the Registrar has received

a notice of intention to

appeal he shall endorse on it the date on which it was received

and register all

particulars.

An appeal to the Tribunal shall be instituted by lodging a

statement of appeal within 30

days from the date when the decision of the Board was delivered.

Every appeal shall be

made in Form TRT .2. Upon receipt of appeal, the Registrar shall

endorse on it the date

on which he received it. The appellant shall pay the appropriate

amount of fees when

instituting an appeal to the Tribunal.

(b). Fees Payable

A person filing an appeal is required to pay non refundable fee

of Tshs. 10,000 upon

lodging notice of intention to appeal, Tshs. 100,000/= upon

lodging statement of

appeal, Tshs. 20,000/= for preparation of records of appeal,

Tshs. 30,000/= for

17

-

7/28/2019 causes of inadequate use of ADR in tax dispute

settlement

35/42

application for extension of time to appeal, Tshs. 20,000/= for

application for execution

of a decree or order.

(c) Important documents for the appealing procedure

A person who institutes an appeal to the Tribunal shall attach

the following documents:

1.A Certified copy of the proceedings of the Board.

2.A Certified copy of the decision of the Board.

3.A copy of the decision of the Commissioner General which gave

rise to appeal to the

Board.

4.A copy of the notice of intention to appeal to the

Tribunal.

5.Evidence of payment of appropriate fees.

(d) The Composition of the Tribunal

The composition of the Tribunal is made up of a Chairperson, two

Vice Chairperson one of whom

from Tanzania Zanzibar and four members. The quorum in any

meeting is made up of the

Chairperson or Vice Chairperson sitting with two members.

The Tribunal has a Registrar who handles all administrative

matters of the Tribunal. The Registrar

receives and registers appeals and applications. The Registrar

also does taxation of bill of costs.

(e) Missing of the appeal time

If one misses the deadline to appeal to the Tribunal within

stipulated time, may apply to the

Tribunal for extension of time within which to file an appeal.

However, the Tribunal may

extend the time if it is satisfied that the failure by a party

to give notice of appeal, lodge an

appeal or to effect service to the opposite party was occasioned

by absence from the United

Republic, sickness or other reasonable cause.

(f) Procedure to follow after the decision of the Tribunal

After the case being determined by TRAT and a party is

dissatisfied with a decision of the

Tribunal he may appeal to the Court of Appeal of Tanzania being

the last appellate court in

the court system of our country, within fourteen days from the

date the decision of the

18

-

7/28/2019 causes of inadequate use of ADR in tax dispute

settlement

36/42

Tribunal was delivered. The appellant shall pay Tshs. 1,500/=

being a fee for notice of

intention to appeal.

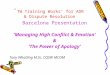

4.3.2 Diagram to show tax appeal resolution machinery and its

hierarchy

Figure I; tax appeal resolution machinery and its hierarchy from

2000 to date

Source: Researcher in the field, 2010

4.3.3 Cases registered and decided since establishment

As stated earlier that TRAT was established by the Act of

Parliament of 2000, Cap 408,

but it became operationally in 2002. Since then the Tribunal has

registered, heard and

determined the appeals and applications as follow;

19

COURT OF APPEAL OF TANZANIA

TAX REVENUE APPEALS TRIBUNAL

TAX REVENUE APPEALS BOARD

FINAL DECISION OF THE

COMMISSIONER GENERAL

-

7/28/2019 causes of inadequate use of ADR in tax dispute

settlement

37/42

Table I; Summary of the cases registered since 2002

YearNumber of Appeals

Registered

Number of

Application

Registered

Total

2002 10 3 13

2003 10 8 18

2004 7 7 14

2005 13 18 31

2006 38 33 71

2007 20 30 50

2008 7 11 18

2009 15 9 24

2010 21 8 29

TOTAL 141 127 268

Source: TRAT register

4.3.4 Evaluation of the methods used in deciding those cases

As a matter of procedure, after the case being filled to

Tribunals registry, it has to be

heard hence the decision has to be made. Regularly cases went

for full hearing as it was

started by section 18(1) of the TRAA, Cap 408 R.E of 2006 which

states that:

18(1) Proceedings of the Board and Tribunal shall be of

judicial

nature and shall be conducted on such occasions and at places as

the

chairman may direct.

20

-

7/28/2019 causes of inadequate use of ADR in tax dispute

settlement

38/42

However, Tribunal is also powered to use ADR which includes

mediation, arbitration,

and conciliation in dispute settlement procedure. This power is

provided under section

17(1) of TRAA, Cap 408 R.E of 2006 which states as follows:

17(1) The Board and the Tribunal shall respectively have the

power

(c)

(d) To resolve any complaint or appeal by mediation,

conciliation or

arbitration

The table below represents the summary of the procedure used in

dealing with the

registered cases.

Table 2; Methods used to determine the registered cases

Number of

cases

registered

Number of

cases

withdrawn

Number of cases

went for full

hearing

Number of

cases settled

between the

parties

268

Percentage

(%)

Source: TRAT register

21

-

7/28/2019 causes of inadequate use of ADR in tax dispute

settlement

39/42

CHAPTER FIVE

RESEARCH FINDINGS AND DATA ANALYSIS

22

-

7/28/2019 causes of inadequate use of ADR in tax dispute

settlement

40/42

CHAPTER SIX

SUMMARY OF THE FINDINGS, CONCLUSION AND RECOMMENDATIONS

23

-

7/28/2019 causes of inadequate use of ADR in tax dispute

settlement

41/42

BIBLIOGRAPHY

Adam, J & Kamuzara, R. (2008) Research Methods for Business

and Social Studies.

Morogoro,Mzumbe Book Project

Banner, D.K (1995) Conflict Resolution: A

RecontextualizationLeadership & Organization Development

Journal

16(1), 31-34

Brooker, P (2009) Criteria for the appropriate use of mediation

in construction disputes

International Journal of Law in the Built of Environment

1(1), 82 97

Ezeluke, I. & Hoare J. D. (1998) The need for education in

alternative disputeresolution (ADR) in the construction

industry

Engineering, Construction and Architectural Management

5(2), 144 - 149

Gahr, R., & Mosca J. B. & Sarsa, S., (1995) Conflict

Resolution and Mediation

.Leadership & Organization Development Journal

16(8), 37-39

Ilter, D. & Dikbas, A. (2009) An analysis of the key

challenges to the widespread useof mediation in the Turkish

construction industry

International Journal of Law in the Built Environment

1(2), 143-155

Merricks, W (2007) The financial Ombudsman Service: not just an

alternative to court

Journal of Financial Regulation and Compliance15(2), 135 142

Osland, A & Osland, S J. (2007) Aracruz Celulose: Best

practices icon but still at riskInternational Journal and

Manpower

28(5), 435 450

Richardson, J (1995) Avoidance as an active mode of conflict

resolution

Team Performance Management an International Journal

1(4)

Sigh, R (1995) Dispute resolution in Britain: contemporary

trends

International Journal of Manpower16(9), 42-52

Vlassenko, I (2001) Evaluation of the efficiency and fairness of

British, French andSwedish property tax systems

Property Management

19(5), 384 416

24

-

7/28/2019 causes of inadequate use of ADR in tax dispute

settlement

42/42

APPENDICES