Embed Size (px)

Citation preview

1

COCA-COLA AMATIL LIMITED ABN 26 004 139 397

ASX Announcement

7 November 2013

CCA HOSTS INVESTOR TOUR

Coca-Cola Amatil Limited is hosting investors on a tour of its beverage production and warehousing facilities in Jakarta, Indonesia. Attached is a copy of the management presentations that will be made as part of the two day trip.

For further information, please contact: Media Analysts Sally Loane Kristina Devon Ph: +61 2 9259 6797 Ph: +61 2 9259 6185 [email protected] [email protected]

2

COCA-COLA AMATIL LIMITED ABN 26 004 139 397

THIS PAGE INTENTIONALLY LEFT BLANK

11

CCA Strategy ReviewIndonesia Investor Tour

Nov 7-8, 2013

Terry Davis Group Managing Director

2

Leading brands in each major NARTD category in each market

Best in class manufacturing, sales and distribution capability

Customer service execution now a real competitive advantage

Delivering on the material growth opportunity in Indonesia

Emerging and already profitable alcoholic beverage business

Balance sheet strength and high operating margins provide base for

long-term investment decisions

“A beverage for every consumption occasion”

3

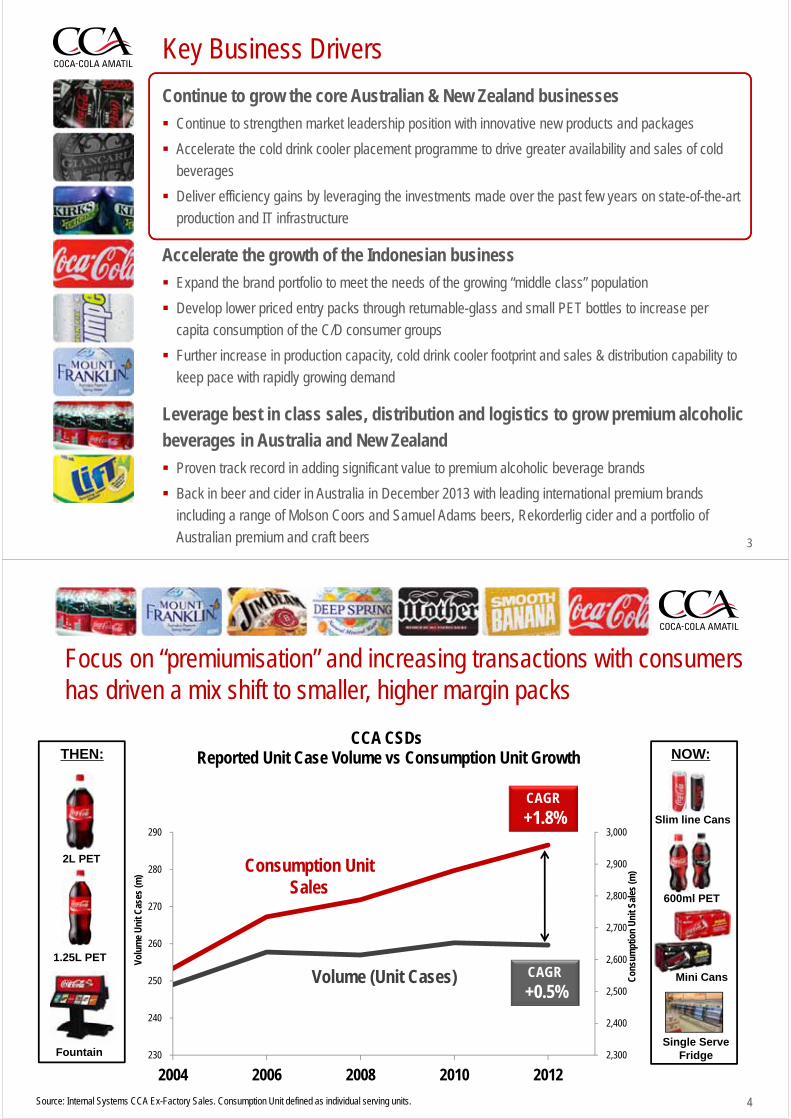

Key Business Drivers

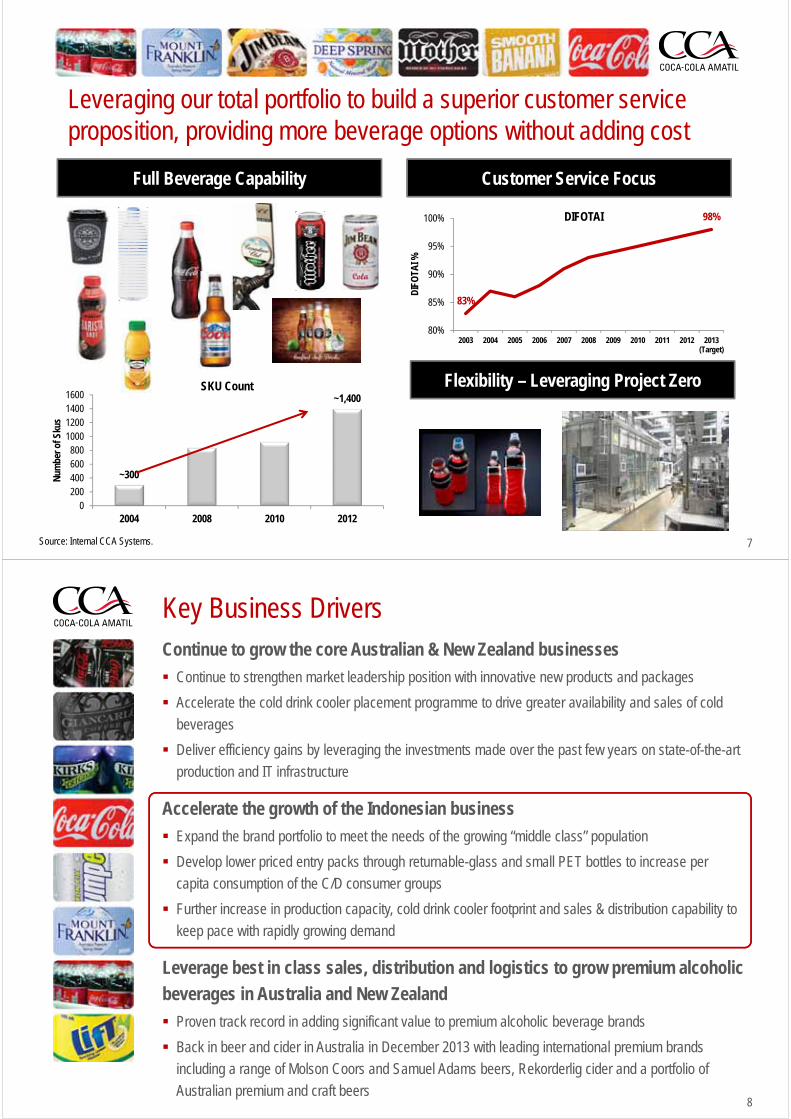

Continue to grow the core Australian & New Zealand businesses

Continue to strengthen market leadership position with innovative new products and packages

Accelerate the cold drink cooler placement programme to drive greater availability and sales of cold

beverages

Deliver efficiency gains by leveraging the investments made over the past few years on state-of-the-art

production and IT infrastructure

Accelerate the growth of the Indonesian business

Expand the brand portfolio to meet the needs of the growing “middle class” population

Develop lower priced entry packs through returnable-glass and small PET bottles to increase per

capita consumption of the C/D consumer groups

Further increase in production capacity, cold drink cooler footprint and sales & distribution capability to

keep pace with rapidly growing demand

Leverage best in class sales, distribution and logistics to grow premium alcoholic

beverages in Australia and New Zealand

Proven track record in adding significant value to premium alcoholic beverage brands

Back in beer and cider in Australia in December 2013 with leading international premium brands

including a range of Molson Coors and Samuel Adams beers, Rekorderlig cider and a portfolio of

Australian premium and craft beers

4

2,300

2,400

2,500

2,600

2,700

2,800

2,900

3,000

230

240

250

260

270

280

290

2004 2006 2008 2010 2012

Con

sum

ptio

n U

nit S

ales

(m)

Volu

me

Uni

t Cas

es (m

)

CCA CSDsReported Unit Case Volume vs Consumption Unit Growth

Volume (Unit Cases)

Consumption Unit Sales

CAGR

+0.5%

CAGR

+1.8%

Source: Internal Systems CCA Ex-Factory Sales. Consumption Unit defined as individual serving units.

2L PET

Mini Cans

THEN: NOW:

1.25L PET

Fountain

600ml PET

Slim line Cans

Single Serve Fridge

Focus on “premiumisation” and increasing transactions with consumers has driven a mix shift to smaller, higher margin packs

5

Product & pack innovation continues to underpin market leadership

6

Consistent investment in product, package and equipment innovation is driving increases in cold drink shelf space in Australia

61%

65%

59%

60%

61%

62%

63%

64%

65%

66%

2008 2012

Shel

f Sha

re (%

)

CCA Cold Drink Shelf Share

+4pts

7

Flexibility – Leveraging Project Zero

Customer Service FocusFull Beverage Capability

83%

98%

80%

85%

90%

95%

100%

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013(Target)

DIF

OTA

I %

DIFOTAI

~300

~1,400

0200400600800

1000120014001600

2004 2008 2010 2012

Num

ber o

f Sku

s

SKU Count

Source: Internal CCA Systems.

Leveraging our total portfolio to build a superior customer service proposition, providing more beverage options without adding cost

8

Key Business DriversContinue to grow the core Australian & New Zealand businesses

Continue to strengthen market leadership position with innovative new products and packages

Accelerate the cold drink cooler placement programme to drive greater availability and sales of cold

beverages

Deliver efficiency gains by leveraging the investments made over the past few years on state-of-the-art

production and IT infrastructure

Accelerate the growth of the Indonesian business

Expand the brand portfolio to meet the needs of the growing “middle class” population

Develop lower priced entry packs through returnable-glass and small PET bottles to increase per

capita consumption of the C/D consumer groups

Further increase in production capacity, cold drink cooler footprint and sales & distribution capability to

keep pace with rapidly growing demand

Leverage best in class sales, distribution and logistics to grow premium alcoholic

beverages in Australia and New Zealand

Proven track record in adding significant value to premium alcoholic beverage brands

Back in beer and cider in Australia in December 2013 with leading international premium brands

including a range of Molson Coors and Samuel Adams beers, Rekorderlig cider and a portfolio of

Australian premium and craft beers

9

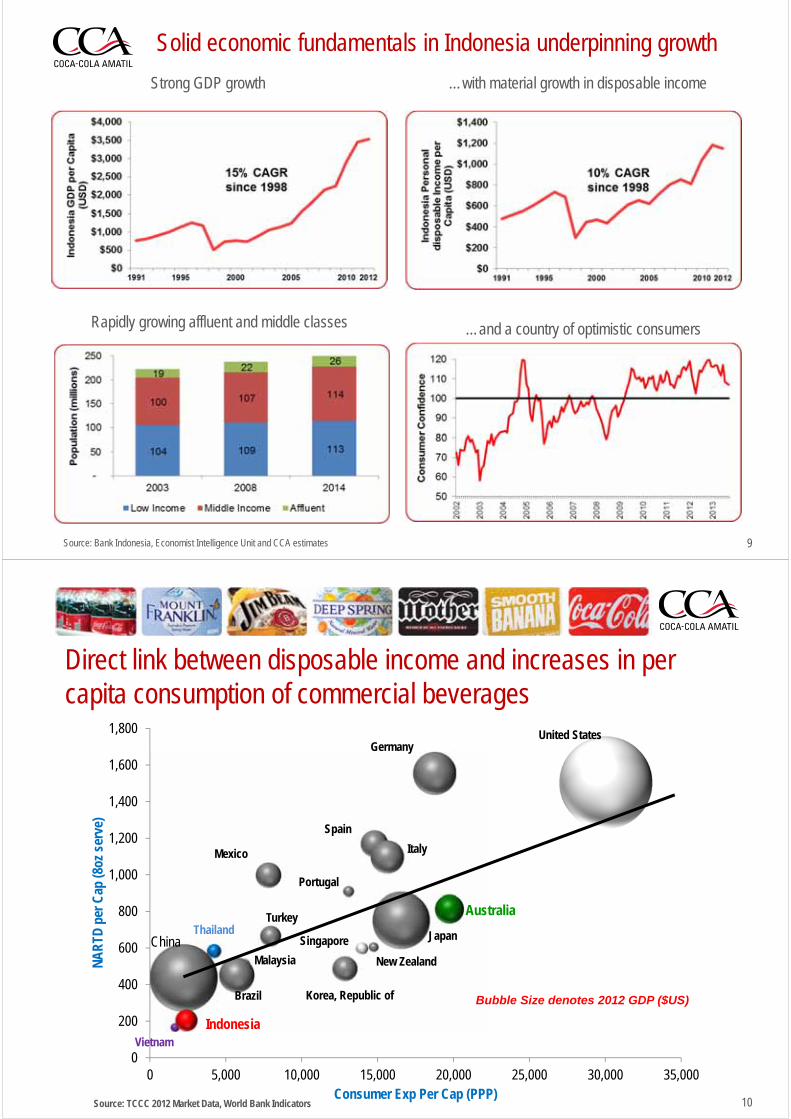

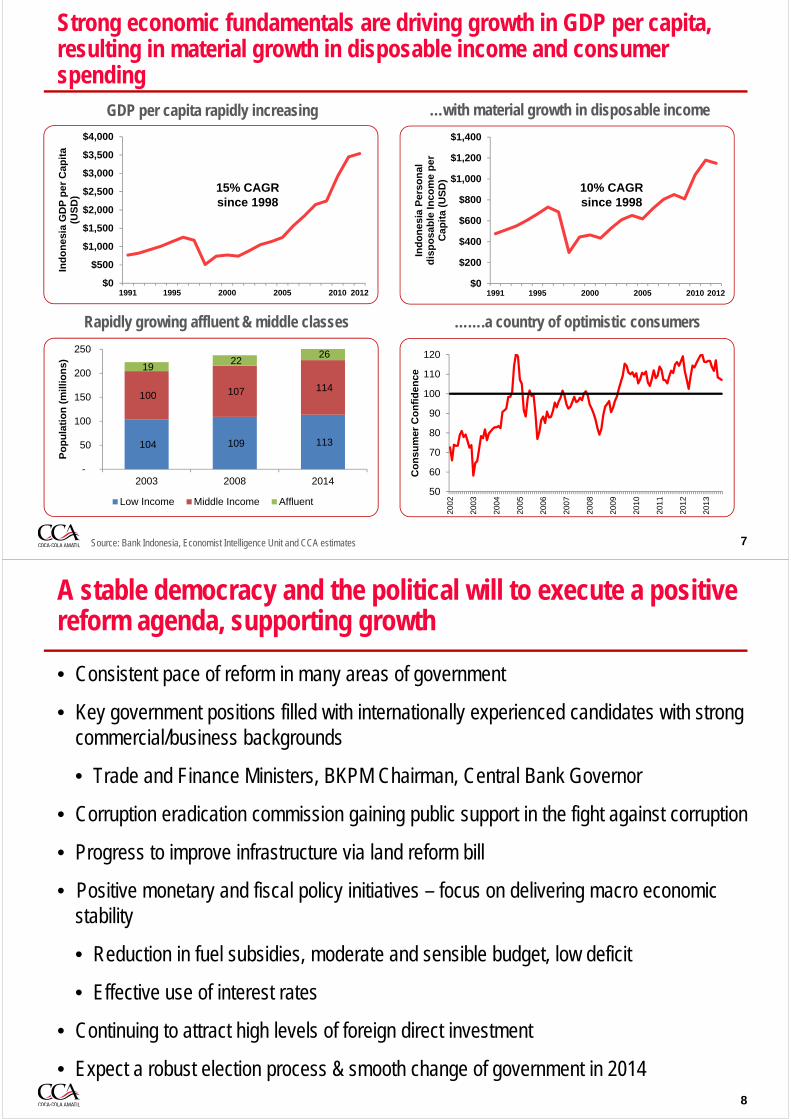

Solid economic fundamentals in Indonesia underpinning growth

Strong GDP growth

Rapidly growing affluent and middle classes …and a country of optimistic consumers

…with material growth in disposable income

Source: Bank Indonesia, Economist Intelligence Unit and CCA estimates

10

Direct link between disposable income and increases in per capita consumption of commercial beverages

Vietnam

China

Indonesia

Thailand

Malaysia

Brazil

Mexico

Turkey

Korea, Republic of

Portugal

Singapore

Australia

New Zealand

Spain

Japan

Italy

GermanyUnited States

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

0 5,000 10,000 15,000 20,000 25,000 30,000 35,000

NA

RTD

per

Cap

(8oz

ser

ve)

Consumer Exp Per Cap (PPP)

Bubble Size denotes 2012 GDP ($US)

Source: TCCC 2012 Market Data, World Bank Indicators

11

Indonesia & PNG track record to date has been excellent, achieving good operational leverage as volumes grow

12

Key Business DriversContinue to grow the core Australian & New Zealand businesses

Continue to strengthen market leadership position with innovative new products and packages

Accelerate the cold drink cooler placement programme to drive greater availability and sales of cold

beverages

Deliver efficiency gains by leveraging the investments made over the past few years on state-of-the-art

production and IT infrastructure

Accelerate the growth of the Indonesian business

Expand the brand portfolio to meet the needs of the growing “middle class” population

Develop lower priced entry packs through returnable-glass and small PET bottles to increase per

capita consumption of the C/D consumer groups

Further increase in production capacity, cold drink cooler footprint and sales & distribution capability to

keep pace with rapidly growing demand

Leverage best in class sales, distribution and logistics to grow premium alcoholic

beverages in Australia and New Zealand

Proven track record in adding significant value to premium alcoholic beverage brands

Back in beer and cider in Australia in December 2013 with leading international premium brands

including a range of Molson Coors and Samuel Adams beers, Rekorderlig cider and a portfolio of

Australian premium and craft beers

13

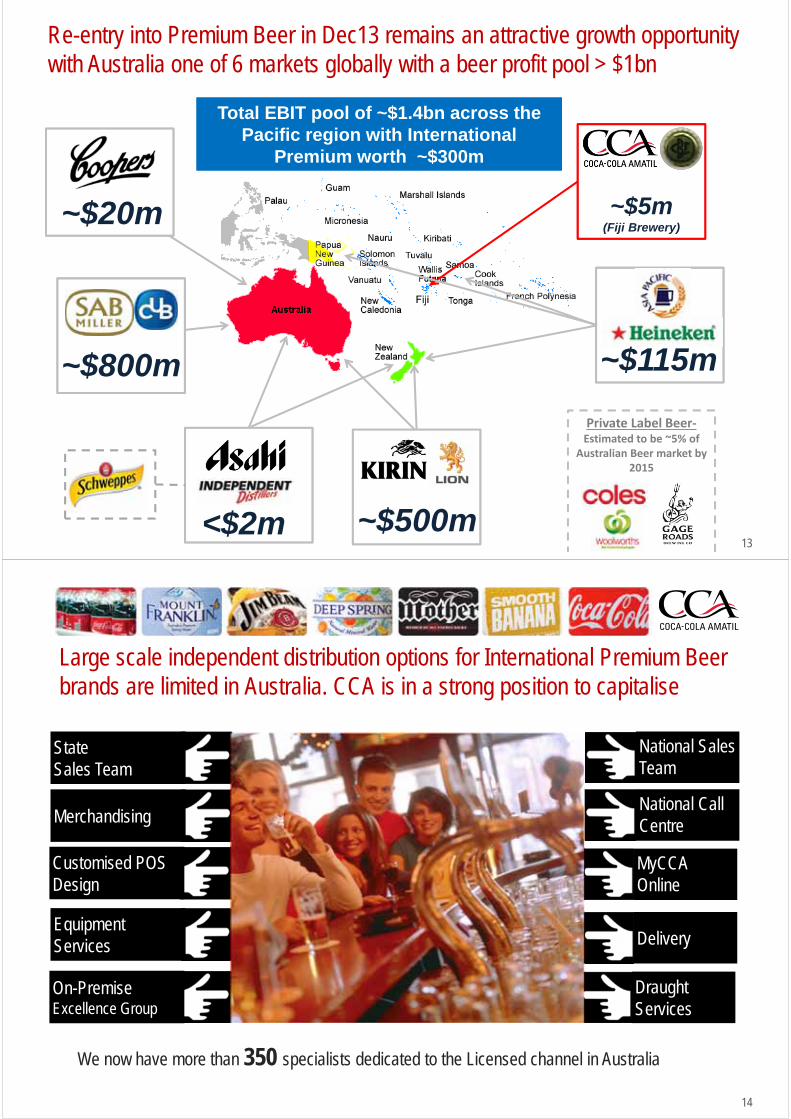

Re-entry into Premium Beer in Dec13 remains an attractive growth opportunity with Australia one of 6 markets globally with a beer profit pool > $1bn

Private Label Beer‐Estimated to be ~5% of

Australian Beer market by 2015

~$20m

~$115m

~$500m

~$800m

<$2m

~$5m(Fiji Brewery)

Total EBIT pool of ~$1.4bn across the Pacific region with International

Premium worth ~$300m

Total EBIT pool of ~$1.4bn across the Pacific region with International

Premium worth ~$300m

14

Large scale independent distribution options for International Premium Beer brands are limited in Australia. CCA is in a strong position to capitalise

National Sales Team

National Call Centre

StateSales Team

Merchandising

Customised POS Design

Equipment Services

MyCCA Online

On-Premise Excellence Group

Delivery

Draught Services

We now have more than 350 specialists dedicated to the Licensed channel in Australia

Licensed picture ????

15

Back in Beer & Cider on the 17th of December 2013 with a great portfolio of premium offerings

16

Trading update & Outlook for second half of 2013

Australian beverages – Non-grocery has continued to grow but consumer demand more subdued than expected. Improved momentum in grocery, with carbonated beverages returning to growth and an improvement in market share, but aggressive competitor pricing activity limiting price realisation

New Zealand – Positive momentum has continued, delivering improved volumes, earnings and market share gains

Indonesia – Q3 demand slowed as the economy adjusted to higher levels of inflation which impacted consumer spending. Continue to expect to deliver low double-digit volume and earnings growth in 2013

AF&S – Trading in line with expectations. Beam continues to gain share while SPC Ardmona continues to expect a reduction in earnings in 2013

Updated guidance – expect 2013 EBIT to be within a range of a 5% to 7% decline on last year, before significant items. The updated guidance range factors in weaker than expected post-election consumer demand, more aggressive competitor activity in Australia as well as an estimated negative impact of almost 1% to EBIT from weaker IDR and Kina

1717

DisclaimerCCA advises that these presentation slides contain forward looking statements which may be subject to significant uncertainties outside of CCA’s control.

No representation is made as to the accuracy or reliability of forward looking statements or the assumptions on which they are based.

Actual future events may vary from these forward looking statements and you are cautioned not to place undue reliance on any forward looking statement.

11

Nessa O’Sullivan Group Chief Financial Officer

Financial & Sustainability ReviewIndonesia Investor Tour

Nov 7-8, 2013

2

Key Financial Objectives

Sustainably driving shareholder value creation through Earnings – achieving the right balance between price, volume, mix and efficiency

gains to deliver sustainable shareholder returns

Dividends – rewarding shareholders along the way with ordinary dividend payout ratio between 70-80% of earnings

Disciplined investment supporting growth objectives – delivering returns well above cost of capital, supporting innovation and productivity gains as well as increasing capacity and competitive advantages

Maintain balance sheet strength and ability to fund investment to develop growth opportunities Conservative debt level and maturity profile supporting A3/A- credit ratings. Debt

maturities fully funded to mid 2015

Capital investment of ~$410m in 2013, with an expectation of reducing capital investment to $325-$350m in 2014 and 2015

Disciplined allocation of Group capital – investment returns remain well above cost of capital – ROCE maintained >20%

3

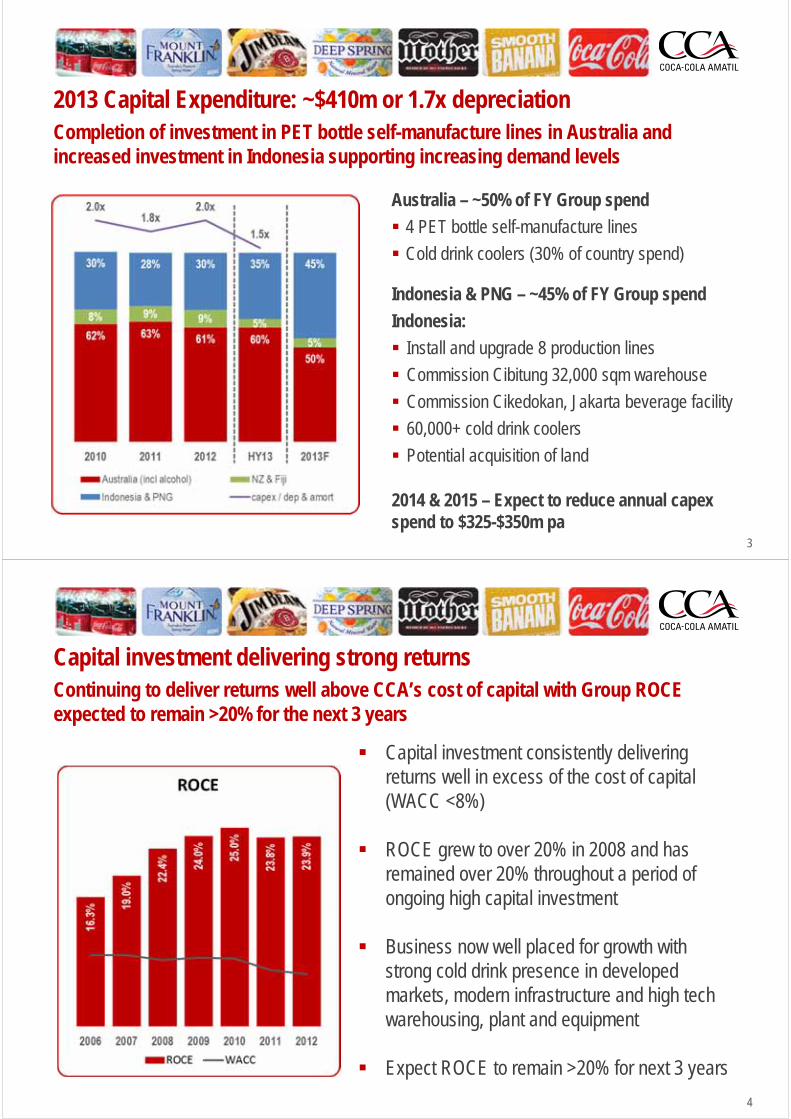

2013 Capital Expenditure: ~$410m or 1.7x depreciationCompletion of investment in PET bottle self-manufacture lines in Australia and increased investment in Indonesia supporting increasing demand levels

Australia – ~50% of FY Group spend

4 PET bottle self-manufacture lines

Cold drink coolers (30% of country spend)

Indonesia & PNG – ~45% of FY Group spend

Indonesia:

Install and upgrade 8 production lines

Commission Cibitung 32,000 sqm warehouse

Commission Cikedokan, Jakarta beverage facility

60,000+ cold drink coolers

Potential acquisition of land

2014 & 2015 – Expect to reduce annual capexspend to $325-$350m pa

4

Capital investment delivering strong returnsContinuing to deliver returns well above CCA’s cost of capital with Group ROCE expected to remain >20% for the next 3 years

Capital investment consistently delivering returns well in excess of the cost of capital (WACC <8%)

ROCE grew to over 20% in 2008 and has remained over 20% throughout a period of ongoing high capital investment

Business now well placed for growth with strong cold drink presence in developed markets, modern infrastructure and high tech warehousing, plant and equipment

Expect ROCE to remain >20% for next 3 years

5

Balance sheet, debt book and interest cover all in a strong positionNet debt remained broadly flat over the past 6 years despite material investment in capex and increase in dividend payout ratio

Capex spend has ranged from 1.7-2.0x depreciation since 2008

Dividend payout ratio has increased from 71% to 76% since 2008 (nb: 2012 payout ratio was 81.5% including the special dividend)

Conservative level of EBIT interest cover

Outlook 2014 and 2015 annual capex spend expected to reduce

by $80-$100m over 2013 level with a shift in investment to Indonesia

Target dividend payout ratio continues to be 70-80%

Conservative debt book with A3/A- credit rating and maturities fully funded to mid 2015

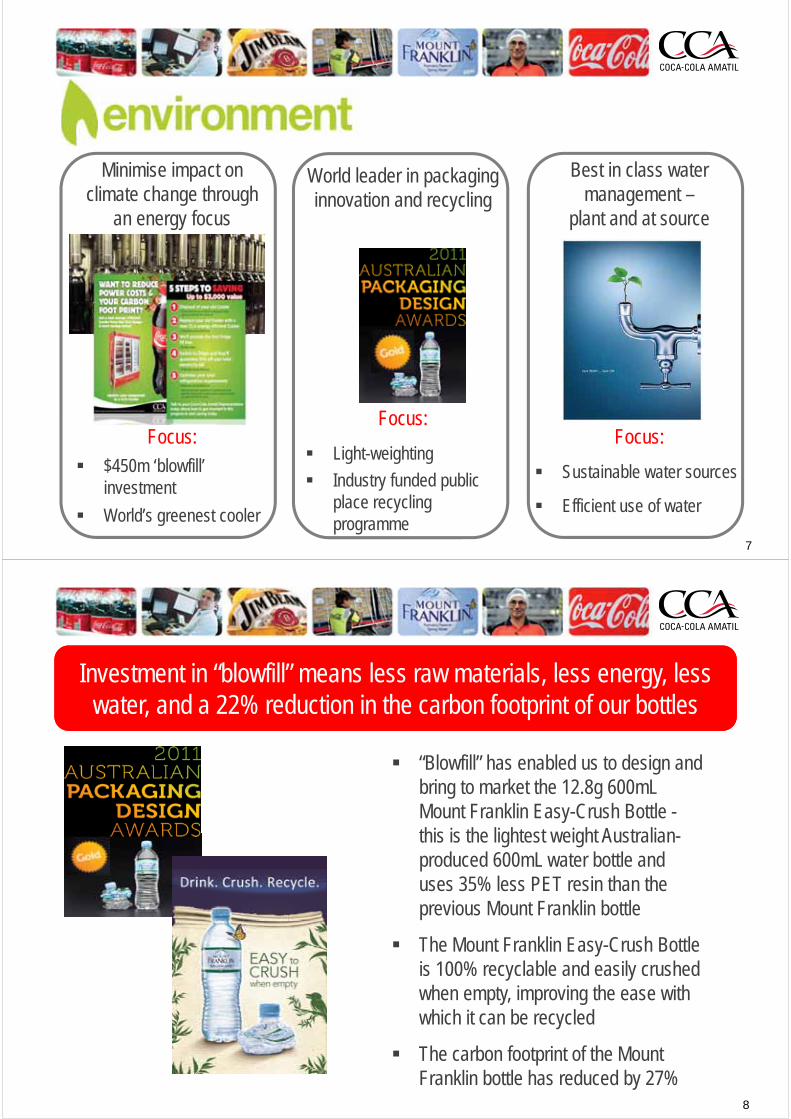

We have a sustainability strategy that focuses on 4 pillarsWe have a sustainability strategy that focuses on 4 pillars

World leader in packaging innovation and recycling

Focus:

Light-weighting

Industry funded public place recycling programme

Minimise impact on climate change through

an energy focus

Focus: $450m ‘blowfill’

investment

World’s greenest cooler

Best in class water management –

plant and at source

Focus:

Sustainable water sources

Efficient use of water

7

Investment in “blowfill” means less raw materials, less energy, less water, and a 22% reduction in the carbon footprint of our bottles

Investment in “blowfill” means less raw materials, less energy, less water, and a 22% reduction in the carbon footprint of our bottles

“Blowfill” has enabled us to design and bring to market the 12.8g 600mL Mount Franklin Easy-Crush Bottle -this is the lightest weight Australian-produced 600mL water bottle and uses 35% less PET resin than the previous Mount Franklin bottle

The Mount Franklin Easy-Crush Bottle is 100% recyclable and easily crushed when empty, improving the ease with which it can be recycled

The carbon footprint of the Mount Franklin bottle has reduced by 27%

8

Case study- CCA coolers

► High Efficiency Motor EC Motors

Design & Technology

► High Efficiency Heat exchangers

► Energy Management System

Refine Design & Technology

► Efficient Refrigeration

► Refine air-flow

► Reduce motor runtime

► Thermal properties

Improved Technology

► LED Lighting► Better Insulation► Improved Thermal Glass

We have Australia’s most energy efficient cold drink equipment, and have reduced the energy consumption of our coolers by ~60%,

helping our customers save an average of $700 p/a

We have Australia’s most energy efficient cold drink equipment, and have reduced the energy consumption of our coolers by ~60%,

helping our customers save an average of $700 p/a

9

Industry plans to deliver increased recycling and reduced litter, efficiently

Industry plans to deliver increased recycling and reduced litter, efficiently

Working with leading companies in the beverage manufacturing and packaging sector – including Amcor Australia (Orora), Lion, Schweppes Australia and Visy – we have devised a proposal which focuses on away from home recycling through a national roll out of bins and other initiatives to improve recovery and recycling of beverage containers.

The proposal sets a target beverage container recycling rate of 70% by 2020, up from the current rate of 48.7%.

10

Water efficiency and water management are one of the highest priorities in our business

Water efficiency and water management are one of the highest priorities in our business

CCA uses 35% less water than industry standard across the Group eg: in Australia, at around 1.6 litres of water per litre of finished product, CCA has achieved one of the best water efficiency ratios in the global Coca-Cola system

CCA has invested significantly into infrastructure, expert hydrogeologists and technology to ensure our water sources are sustainably managed

All CCA underground water sources are within 2 hours drive of our plants, reducing road miles

11

We have zero calorie options

Choices for every occasionChoices for every occasion

With a strong focus on portion control

12

Philanthropic: $1.1M annually

through the Coca-Cola Australia

Foundation

Focus:

Marginalised youth

Cause marketing: $1.5M+ through Mount Franklin;

Deep Spring purple lids

Focus:

Target market-aligned cause

Disaster relief: monetary and product

donations during times of disaster

Focus:

Our local communities

Workplace giving: matching employee

donations

+

Focus:

Our local communities

Giving is good for businessGiving is good for business

13

Safety comes first

Focus:

Live safe

Culture

Focus:

Talent development

Diversity

Focus:

Embracing difference –gender & Indigenous

employment

Training & Development

Focus:

Talent development

Creating a culture that builds a sustainable business

Creating a culture that builds a sustainable business

14

1515

DisclaimerCCA advises that these presentation slides contain forward looking statements which may be subject to significant uncertainties outside of CCA’s control.

No representation is made as to the accuracy or reliability of forward looking statements or the assumptions on which they are based.

Actual future events may vary from these forward looking statements and you are cautioned not to place undue reliance on any forward looking statement.

Indonesian Strategy ReviewIndonesia Investor Tour

Nov 7-8, 2013

Market Overview, Strategy and Marketing

Stuart Comino Finance Director Indonesia

Mark Payne Sales & Marketing Director Indonesia

Indonesia – emerging as a major economic power

• One of the fastest growing G20 economies – 16th largest economy – expected to be bigger than Australia within a decade

• Highly favourable demographics – 50% of the 250m population aged under 29 years, 35m people in the AB consumer class

• Modernising very rapidly

• Second highest users of Facebook – over 60m - second to US

• 290m mobile phone subscriptions

Quotes from Tony Abbott during his recent visit to Indonesia

“Indonesia is a member of the G20 and a leader of ASEAN as well Australia’s most important neighbour.

It’s the world’s most populous Muslim nation.

It’s the world’s third largest democracy.

……along with India, it’s the emerging democratic superpower of Asia.”

“…. it probably won't be very long at all before Indonesia's total GDP dwarfs ours” 2

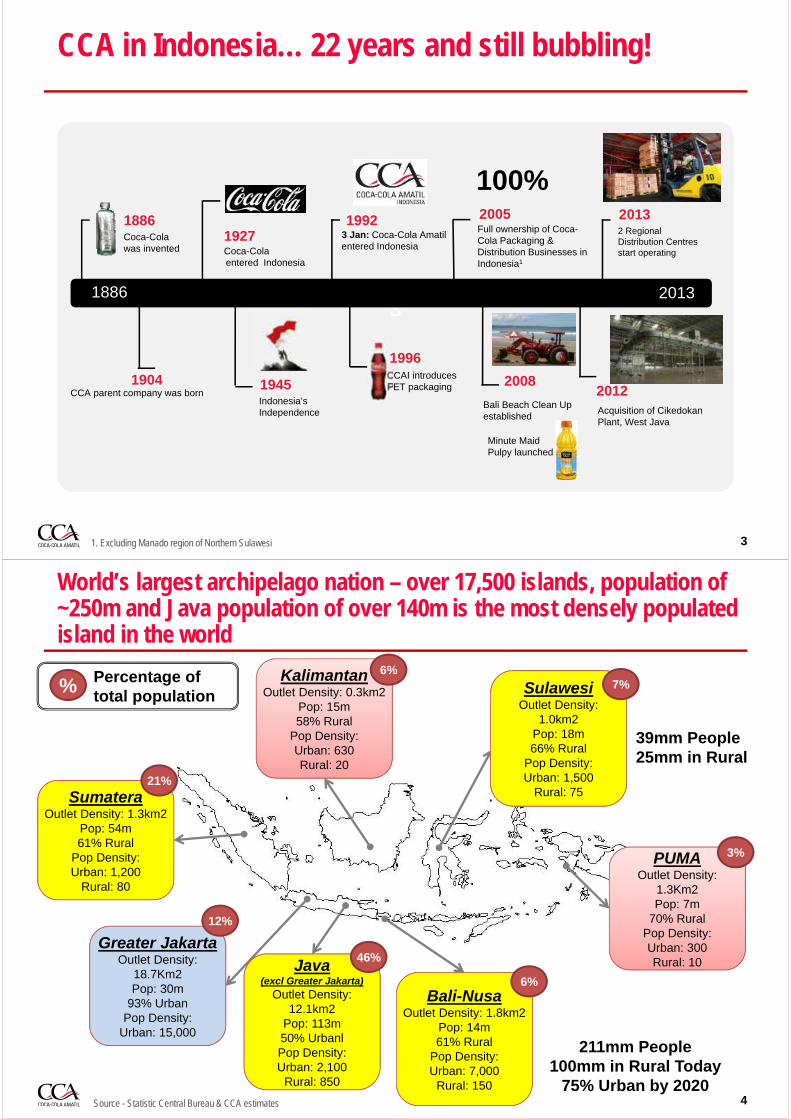

CCA in Indonesia… 22 years and still bubbling!

31. Excluding Manado region of Northern Sulawesi

s

Coca-Cola was invented

1886

1904Indonesia’s Independence

1886

2 Regional Distribution Centresstart operating

CCAI introduces PET packaging

2013

Coca-Cola entered Indonesia

1927

1945

3 Jan: Coca-Cola Amatilentered Indonesia

1992

1996

Full ownership of Coca-Cola Packaging & Distribution Businesses in Indonesia1

2005 2013

2012Acquisition of CikedokanPlant, West Java

CCA parent company was born2008

Bali Beach Clean Up established

100%

Minute Maid Pulpy launched

World’s largest archipelago nation – over 17,500 islands, population of ~250m and Java population of over 140m is the most densely populated island in the world

4Source - Statistic Central Bureau & CCA estimates

Greater JakartaOutlet Density:

18.7Km2Pop: 30m

93% UrbanPop Density:

Urban: 15,000

SumateraOutlet Density: 1.3km2

Pop: 54m61% Rural

Pop Density:Urban: 1,200

Rural: 80

KalimantanOutlet Density: 0.3km2

Pop: 15m58% Rural

Pop Density:Urban: 630Rural: 20

Java (excl Greater Jakarta)

Outlet Density: 12.1km2

Pop: 113m50% UrbanlPop Density:Urban: 2,100

Rural: 850

Bali-NusaOutlet Density: 1.8km2

Pop: 14m61% Rural

Pop Density:Urban: 7,000

Rural: 150

SulawesiOutlet Density:

1.0km2Pop: 18m66% Rural

Pop Density:Urban: 1,500

Rural: 7521%

12%

46%

6%

6%7%

PUMAOutlet Density:

1.3Km2Pop: 7m

70% RuralPop Density:Urban: 300Rural: 10

3%

39mm People25mm in Rural

211mm People100mm in Rural Today

75% Urban by 2020

% Percentage of total population

Coca-Cola Amatil in Indonesia has a large scale national sales, manufacturing and distribution footprint supported by a strong investment program to continue to expand our capability

National Manufacturing & Distribution network:

• 9 manufacturing sites

• 36 production lines (with capacity of ~1.4bn litres of beverages)

• 85 distribution centres

• Over 1,300 distribution vehicles

5

National Salesforce of ~4,000 people:

• Selling a full range NARTD beverage portfolio

• We reach ~1.6million customers both directly and indirectly

• With 255,000 pieces of Cold Drink Equipment in the market

Total workforce – 7,400 full time and up to 4,000 casual employees

While market fundamentals remain strong, current headwinds from high inflation and exchange rate movements

6

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

Yr2004 Yr2005 Yr2006 Yr2007 Yr2008 Yr2009 Yr2010 Yr2011 Yr2012 Yr2013

Inflation driven partly by reduction of fuel subsidies

6,000

7,000

8,000

9,000

10,000

11,000

12,000

13,000

With rising USD/IDR exchange rates

-12,000

-10,000

-8,000

-6,000

-4,000

-2,000

0

2,000

4,000

6,000

And a growing current account deficit (USD )

Source: Bank Indonesia

• Indonesia is a developing market

• Growth not expected to be without volatility

• Market fundamentals remain strong

Strong economic fundamentals are driving growth in GDP per capita, resulting in material growth in disposable income and consumer spending

7

Rapidly growing affluent & middle classes …….a country of optimistic consumers

…with material growth in disposable income

50

60

70

80

90

100

110

120

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Co

nsu

mer

Co

nfi

den

ce

Source: Bank Indonesia, Economist Intelligence Unit and CCA estimates

GDP per capita rapidly increasing

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

1991 1995 2000 2005 2010 2012

Ind

on

esia

GD

P p

er C

apit

a (U

SD

)

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

1991 1995 2000 2005 2010 2012

Ind

on

esia

Per

son

al

dis

po

sab

le I

nco

me

per

C

apit

a (U

SD

)

15% CAGR since 1998

10% CAGR since 1998

104 109 113

100 107 114

19 22

26

-

50

100

150

200

250

2003 2008 2014

Po

pu

lati

on

(m

illio

ns)

Low Income Middle Income Affluent

A stable democracy and the political will to execute a positive reform agenda, supporting growth

• Consistent pace of reform in many areas of government

• Key government positions filled with internationally experienced candidates with strong commercial/business backgrounds

• Trade and Finance Ministers, BKPM Chairman, Central Bank Governor

• Corruption eradication commission gaining public support in the fight against corruption

• Progress to improve infrastructure via land reform bill

• Positive monetary and fiscal policy initiatives – focus on delivering macro economic stability

• Reduction in fuel subsidies, moderate and sensible budget, low deficit

• Effective use of interest rates

• Continuing to attract high levels of foreign direct investment

• Expect a robust election process & smooth change of government in 20148

Vietnam

China

Indonesia

Thailand

Malaysia

Brazil

Mexico

Turkey

Korea, Republic of

Portugal

Singapore

Australia

New Zealand

Spain

Japan

Italy

GermanyUnited States

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

0 5,000 10,000 15,000 20,000 25,000 30,000 35,000

NA

RT

D p

er C

ap (

8oz

serv

e)

Consumer Exp Per Cap (PPP)

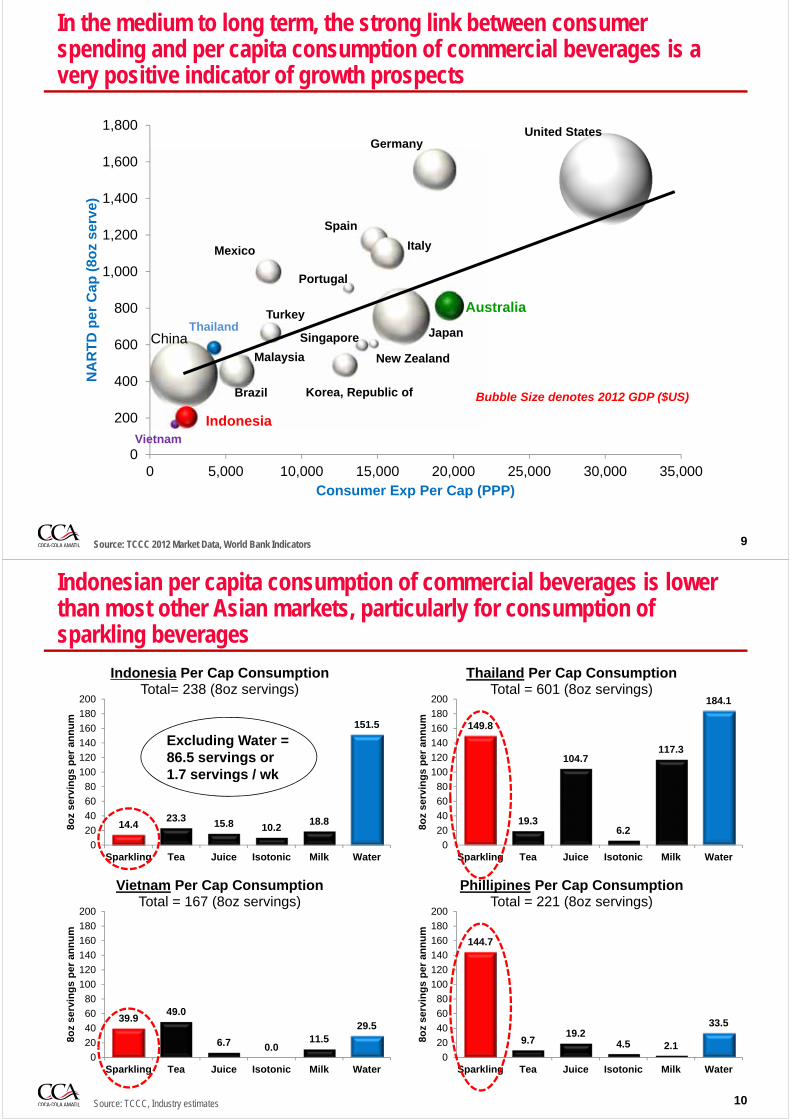

In the medium to long term, the strong link between consumer spending and per capita consumption of commercial beverages is a very positive indicator of growth prospects

9

Bubble Size denotes 2012 GDP ($US)

Source: TCCC 2012 Market Data, World Bank Indicators

Indonesian per capita consumption of commercial beverages is lower than most other Asian markets, particularly for consumption of sparkling beverages

10

14.423.3 15.8 10.2

18.8

151.5

0

20

40

60

80

100

120

140

160

180

200

Sparkling Tea Juice Isotonic Milk Water

8oz

serv

ing

s p

er a

nn

um

Indonesia Per Cap ConsumptionTotal= 238 (8oz servings)

Source: TCCC, Industry estimates

149.8

19.3

104.7

6.2

117.3

184.1

0

20

40

60

80

100

120

140

160

180

200

Sparkling Tea Juice Isotonic Milk Water

8oz

serv

ing

s p

er a

nn

um

Thailand Per Cap ConsumptionTotal = 601 (8oz servings)

39.949.0

6.7 0.011.5

29.5

0

20

40

60

80

100

120

140

160

180

200

Sparkling Tea Juice Isotonic Milk Water

8oz

serv

ing

s p

er a

nn

um

Vietnam Per Cap ConsumptionTotal = 167 (8oz servings)

144.7

9.719.2

4.5 2.1

33.5

0

20

40

60

80

100

120

140

160

180

200

Sparkling Tea Juice Isotonic Milk Water

8oz

serv

ing

s p

er a

nn

um

Phillipines Per Cap ConsumptionTotal = 221 (8oz servings)

Excluding Water = 86.5 servings or 1.7 servings / wk

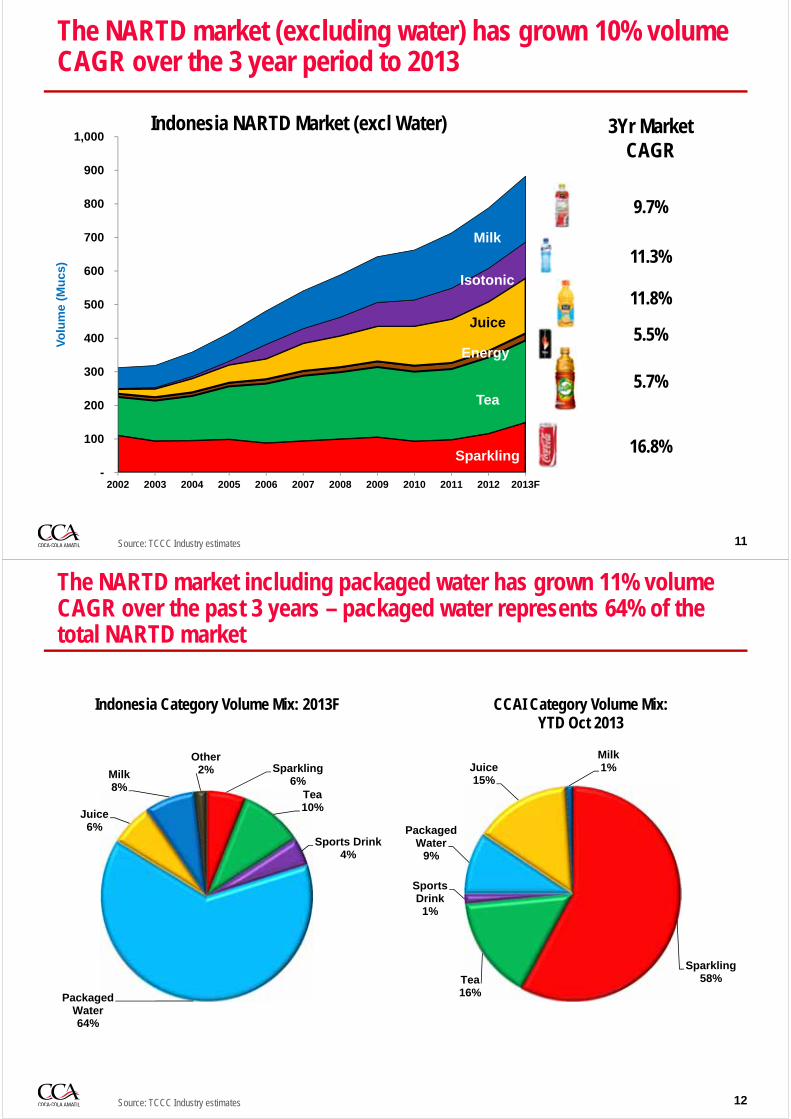

The NARTD market (excluding water) has grown 10% volume CAGR over the 3 year period to 2013

11

-

100

200

300

400

500

600

700

800

900

1,000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013F

Vo

lum

e (M

ucs

)

Indonesia NARTD Market (excl Water) 3Yr MarketCAGR

9.7%

11.3%

11.8%

5.5%

5.7%

16.8%

Milk

Isotonic

Juice

Energy

Tea

Sparkling

Source: TCCC Industry estimates

The NARTD market including packaged water has grown 11% volume CAGR over the past 3 years – packaged water represents 64% of the total NARTD market

12

Sparkling6%

Tea10%

Sports Drink4%

Packaged Water64%

Juice6%

Milk8%

Other2%

Indonesia Category Volume Mix: 2013F

Sparkling58%Tea

16%

Sports Drink

1%

Packaged Water

9%

Juice15%

Milk1%

CCAI Category Volume Mix: YTD Oct 2013

Source: TCCC Industry estimates

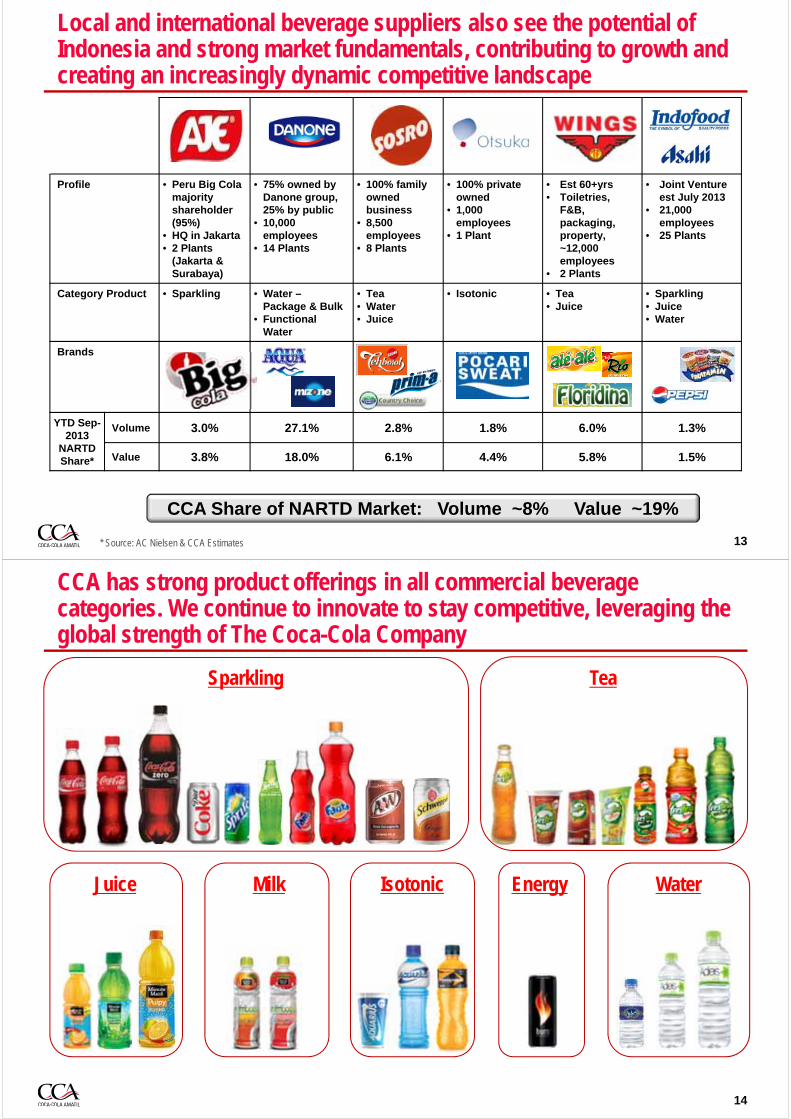

Local and international beverage suppliers also see the potential of Indonesia and strong market fundamentals, contributing to growth and creating an increasingly dynamic competitive landscape

13

Profile • Peru Big Cola majority shareholder (95%)

• HQ in Jakarta • 2 Plants

(Jakarta & Surabaya)

• 75% owned by Danone group, 25% by public

• 10,000 employees

• 14 Plants

• 100% family owned business

• 8,500 employees

• 8 Plants

• 100% privateowned

• 1,000 employees

• 1 Plant

• Est 60+yrs• Toiletries,

F&B, packaging, property, ~12,000 employees

• 2 Plants

• Joint Venture est July 2013

• 21,000 employees

• 25 Plants

Category Product • Sparkling • Water –Package & Bulk

• Functional Water

• Tea• Water• Juice

• Isotonic • Tea• Juice

• Sparkling• Juice• Water

Brands

YTD Sep-2013

NARTD Share*

Volume 3.0% 27.1% 2.8% 1.8% 6.0% 1.3%

Value 3.8% 18.0% 6.1% 4.4% 5.8% 1.5%

* Source: AC Nielsen & CCA Estimates

CCA Share of NARTD Market: Volume ~8% Value ~19%

CCA has strong product offerings in all commercial beverage categories. We continue to innovate to stay competitive, leveraging the global strength of The Coca-Cola Company

Sparkling

WaterEnergyJuice

Tea

Isotonic

14

Milk

The shift to One Way Packs continues, reflecting consumer preference – our innovation platform is targeted at leveraging this preference in all categories – RGB will continue to be a key recruitment package

15

CC

A Vo

lum

e Sp

lit (U

C)

69% 67%62% 57% 55%

48%40%

31%25%

20%14%

31% 33%38% 43% 45%

52%60%

69%75%

80%86%

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013F

Returnable Glass Bottle One Way Pack (PET Bottles & CANs)Source: Internal CCA systems

Sparkling CategoryWe are actively developing sparkling culture using locally developed and international campaigns that are relevant to Indonesians

16

Partnering with the Indonesian Badminton Association

Planning underway for the World Cup Trophy Tour and World Cup in 2014

Ramadhan‘festive

message’ bottles

Local Ramadhan advertising

Sparkling CategoryPackaging innovation in Coca-Cola and the introduction of value priced Fanta Royal – developing consumption habit, expanding choice

Brand : Fanta Royal

Flavor : Orange

Grape

Mixed Fruit

Launch : May 2013

Category : Sparkling

YTD Oct’13 : 1.1m Unit Cases

17

Fanta Royal PET 425mlCoca-Cola PET 540ml

Tea CategoryKey package innovation in Frestea to target In Home occasions and smaller, more affordable packs for On the Go, as well as new flavours

18

300ml FresteaTraditional Trade

750ml FresteaModern Trade

300ml FresteaTraditional Trade

Launched Oct 2013

750ml Frestea – In Home occasions

300ml Frestea

Juice CategoryMinute Maid Pulpy is an increasingly important part of our portfolio –we have a major focus on innovation in package and flavour

19

Brand : Minute Maid

Flavor : Aloe Vera

Launch : January 2013

Category : Juice

YTD Oct’13 : 1.9m Unit Cases

#2 MMP Flavour in

China

250ml PulpyTraditional Trade

1.0L PulpyModern Trade

Milk CategoryExpansion into Dairy Category under the Minute Maid brand with the launch of Minute Maid Nutriboost

• Brand : Minute Maid Nutriboost

• Flavour: Strawberry and Orange

• Launch: May 2013

• Category: Dairy

• YTD Oct’13: 1.3m Unit Cases

20

>30mucs in China

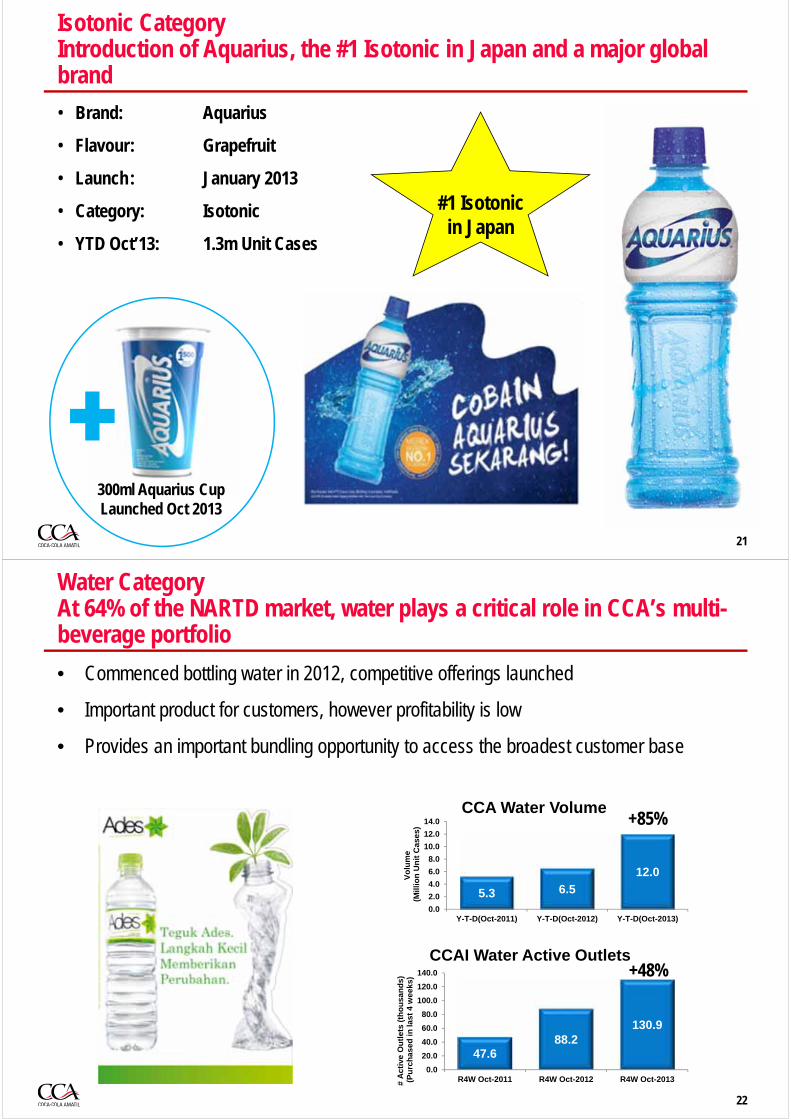

Isotonic CategoryIntroduction of Aquarius, the #1 Isotonic in Japan and a major global brand

• Brand: Aquarius

• Flavour: Grapefruit

• Launch: January 2013

• Category: Isotonic

• YTD Oct’13: 1.3m Unit Cases

21

#1 Isotonic in Japan

300ml Aquarius CupLaunched Oct 2013

Water CategoryAt 64% of the NARTD market, water plays a critical role in CCA’s multi-beverage portfolio

• Commenced bottling water in 2012, competitive offerings launched

• Important product for customers, however profitability is low

• Provides an important bundling opportunity to access the broadest customer base

22

5.3 6.5

12.0

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

Y-T-D(Oct-2011) Y-T-D(Oct-2012) Y-T-D(Oct-2013)

Vo

lum

e(M

illio

n U

nit

Cas

es)

CCA Water Volume

47.688.2

130.9

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

R4W Oct-2011 R4W Oct-2012 R4W Oct-2013# A

ctiv

e O

utl

ets

(th

ou

san

ds)

(Pu

rch

ased

in la

st 4

wee

ks)

CCAI Water Active Outlets

+85%

+48%

Cold Drink EquipmentIncreasing cold availability via continued aggressive cold drink placement is a major driver of increased per capita consumption

• 255,000 CCA coolers in the market

• Supported by a complete beverage portfolio vs competitors

• Space in outlet and electricity challenges - equipment innovation has delivered optimal coolers for Indonesian market, using half the electricity of competitor coolers

23

10.68.2

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

SouthKorea

Philippines Thailand Indonesia2013

Indonesia2012

China India Vietnam

Co

ole

rs p

er 1

0k p

op

ula

tio

n

Cooler Units per 10k Population

+28% in 2013

People Capability – Critical to Support the Growth AgendaOur long term success will be driven by exceptional people capability –education and diversity are key for developing local leadership talent

We continue to develop local talent in key leaderships roles

• Active talent identification, development and retention programs

• Highly educated leadership team……73% of junior management and above are University Degree qualified and fluent English speakers

• Young leadership team……..80% of junior management ranging in age from 23 to 40 years of age

• Females already account for 24% of management

Material ongoing investment in training – averaging ~40hrs training per employee per year –throughout the organisation

24

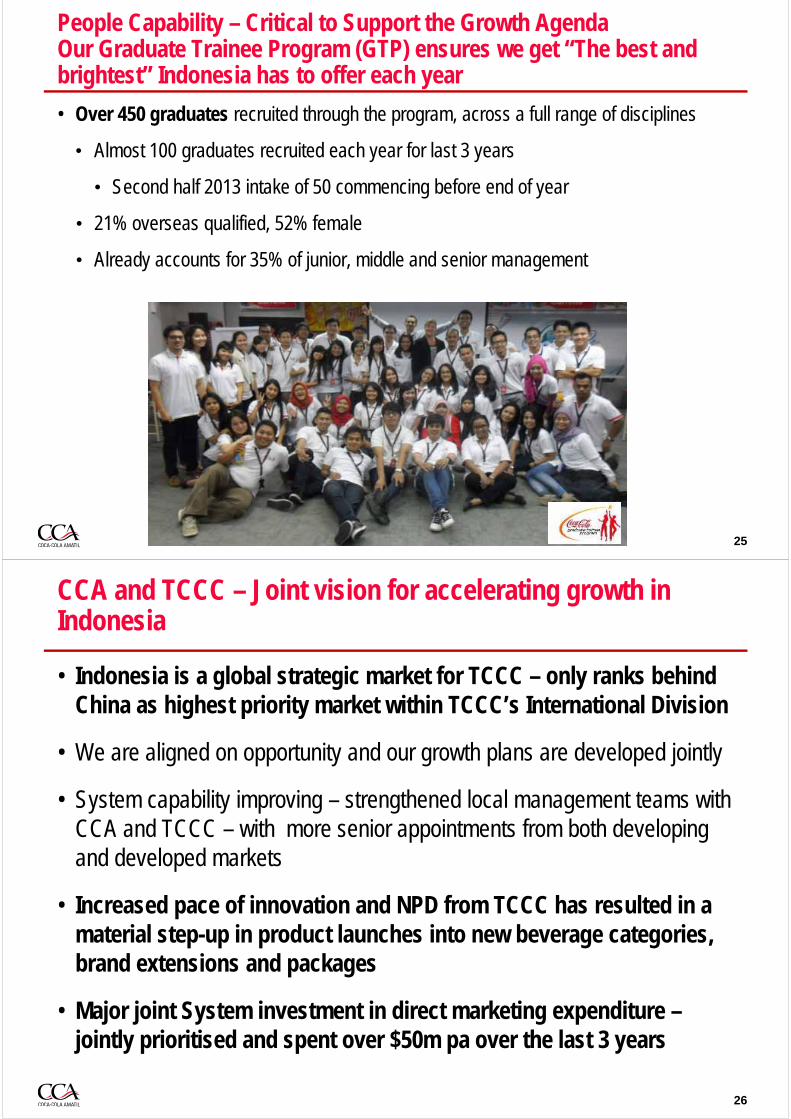

People Capability – Critical to Support the Growth AgendaOur Graduate Trainee Program (GTP) ensures we get “The best and brightest” Indonesia has to offer each year

• Over 450 graduates recruited through the program, across a full range of disciplines

• Almost 100 graduates recruited each year for last 3 years

• Second half 2013 intake of 50 commencing before end of year

• 21% overseas qualified, 52% female

• Already accounts for 35% of junior, middle and senior management

25

CCA and TCCC – Joint vision for accelerating growth in Indonesia

• Indonesia is a global strategic market for TCCC – only ranks behind China as highest priority market within TCCC’s International Division

• We are aligned on opportunity and our growth plans are developed jointly

• System capability improving – strengthened local management teams with CCA and TCCC – with more senior appointments from both developing and developed markets

• Increased pace of innovation and NPD from TCCC has resulted in a material step-up in product launches into new beverage categories, brand extensions and packages

• Major joint System investment in direct marketing expenditure –jointly prioritised and spent over $50m pa over the last 3 years

26

Mark Payne Sales & Marketing Director Indonesia

Indonesian Market Place

Approx 5,000kms

Indonesian Market PlaceModern Foodstores has a high volume per outletTraditional Trade still the majority of total volume

28

Coca-Cola Amatil Market Profile

93%

Outlets

32%

6%

62%

Volume (Unit Cases)

31%

5%

64%

Revenue

Australia~600,000 Outlets

~80,000 Outlets

vs

Approx 4,000kms

Sumatera

JavaTimor

Sulawesi

Kalimantan

Modern FoodstoresModern On PremiseTraditional Trade

Hypermarkets (4% volume)

Mini Mart (20% volume) Supermarkets (6% volume)

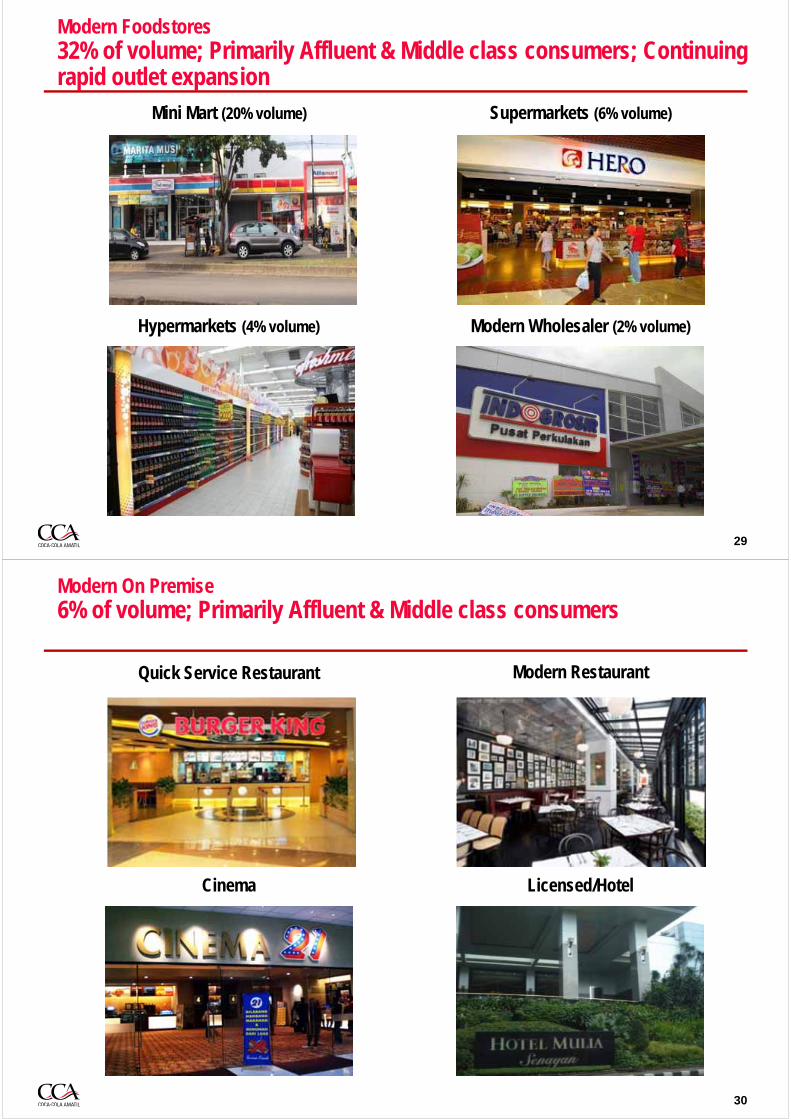

Modern Foodstores32% of volume; Primarily Affluent & Middle class consumers; Continuing rapid outlet expansion

29

Modern Wholesaler (2% volume)

Modern On Premise6% of volume; Primarily Affluent & Middle class consumers

30

Modern RestaurantQuick Service Restaurant

Cinema Licensed/Hotel

Traditional Trade62% of volume; Primarily Middle & Lower class consumers

31

Provision Stores (23% volume)

Education (3% volume)Traditional Food Service (7% volume)

Traditional Wholesalers (15% volume)

Other channels 14% of volume

Traditional Trade Sales Initiatives – Outlet Penetration2 million potential NARTD outlets of which 600,000 are visited by CCA sales reps and another 1 million buy CCA products indirectly

32Source: A C Nielsen

~1m OutletsRange CCA Product/s

Orders & Delivery via Third Party

400,000 OutletsNo CCA Products - Yet

385,000 OutletsCCA Orders; CCA Delivers

215,000 OutletsCCA Orders; CCA Partner

Delivers

CCA Indirect Serve Outlets – 1,000,000• Products sourced via existing Direct Serve

Outlets - wholesalers• Partner Program

• Increase portfolio penetration

CCA Direct Serve Outlets – 600,000• Visited on a weekly basis• Orders generated by CCA Sales Rep• Targeted Sales Initiatives• Direct Marketing & Trade Programs

Non CCA stockist NARTD Outlets – 400,000• Partner Program

• Activate non stockists

Indonesia Outlet Base

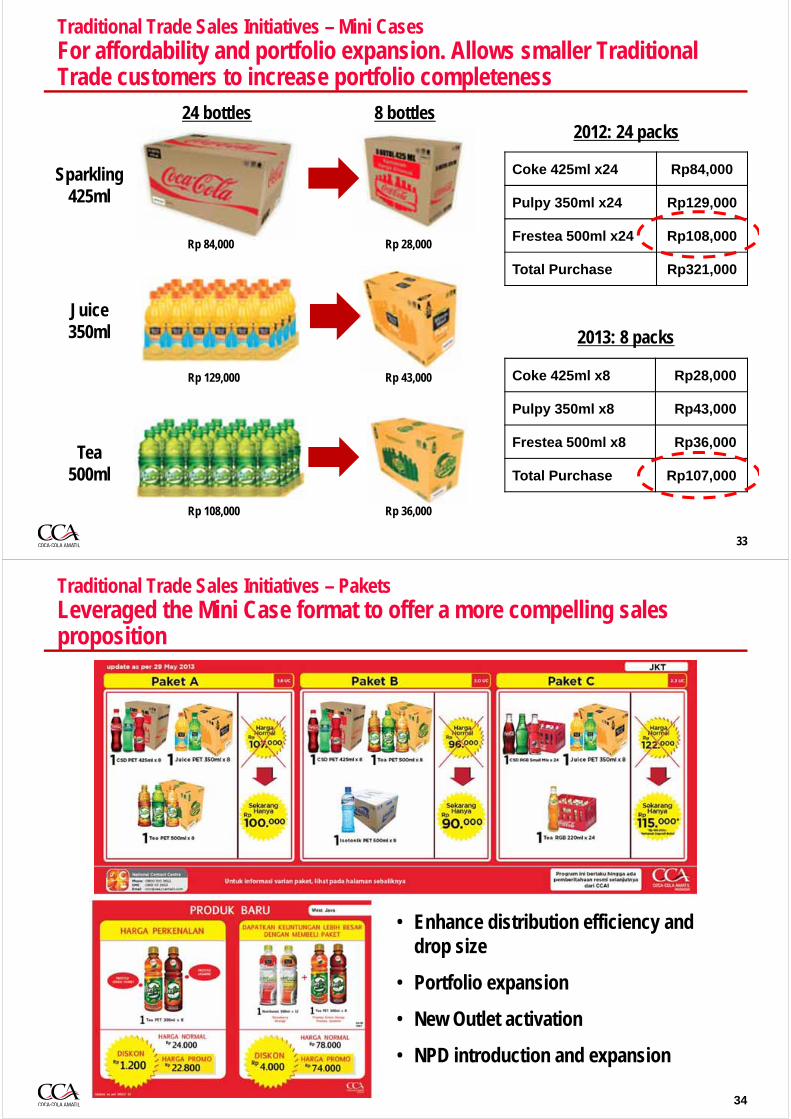

Traditional Trade Sales Initiatives – Mini CasesFor affordability and portfolio expansion. Allows smaller Traditional Trade customers to increase portfolio completeness

33

Rp 28,000Rp 84,000

Coke 425ml x24 Rp84,000

Pulpy 350ml x24 Rp129,000

Frestea 500ml x24 Rp108,000

Total Purchase Rp321,000

Coke 425ml x8 Rp28,000

Pulpy 350ml x8 Rp43,000

Frestea 500ml x8 Rp36,000

Total Purchase Rp107,000

Rp 108,000 Rp 36,000

Rp 129,000 Rp 43,000

24 bottles 8 bottles

Sparkling425ml

Juice350ml

Tea500ml

2012: 24 packs

2013: 8 packs

Traditional Trade Sales Initiatives – PaketsLeveraged the Mini Case format to offer a more compelling sales proposition

• Enhance distribution efficiency and drop size

• Portfolio expansion

• New Outlet activation

• NPD introduction and expansion

34

Traditional Trade Sales Initiatives – Cooler BundlesMini Cases & Pakets integrated with Cooler Rollout program to maximise effectiveness of cooler investment and placements

• Over 1,000 coolers placed each week

• Coolers placed with product paket

• Fully stocked and merchandised

• Ready for immediate sales

• Relevant product range including NPD

• Globally recognised as best practice

• Key strategy to continue in 2014

35

Traditional Trade Sales Initiatives – Partner ProgramIndonesia is characterised by wide scale indirect distribution networks. Enabling CCA to reach over 1 million potential outlets not directly served

36

Sales Partner: Exclusive CCA suppliers; 5yr agreement; deliver CCA orders and canvass

Wholesaler Partner: Non exclusive suppliers; Rolling quarterly agreement; canvass

Partners are incentivised to open new outlets and to increase product penetration and sales in existing outlets

Realising the growth opportunity in Indonesia is a key priority for the Group – continuing to target double-digit annual volume and earnings growth

We are set up to succeed in Indonesia……

Market fundamentals are strong & demographics are ideal

22 years experience in Indonesia, large-scale national footprint, including a range of new technology and capability added over the last 2-3 years

Extending our reach into the significant outlet opportunity in Indonesia across all channels via international best practice innovative sales strategies

Multi-beverage portfolio relevant to customers and consumers and a strong innovation pipeline – NPD, new brands, packs and flavours

Ongoing Cooler Placement program to own cold space and increase cold availability

Strong focus on development of local talent37

DisclaimerCCA advises that these presentation slides contain forward looking statements which may be subject to significant uncertainties outside of CCA’s control.

No representation is made as to the accuracy or reliability of forward looking statements or the assumptions on which they are based.

Actual future events may vary from these forward looking statements and you are cautioned not to place undue reliance on any forward looking statement.

Indonesian Supply ChainIndonesia Investor Tour

Nov 7-8, 2013

Bruce Herbert Group Supply Chain DirectorEdward Walters Logistics Director

Gigy Philip Operations Director

CCAI is now a world leader in PET packaging

innovationDIFOTAI now 94%

We are investing in capability and capacity

ahead of the growth curve

Project Zero is delivering an expanding product portfolio

at lower cost

Significant increase in one way pack capacity

Our manufacturing platform is enabling product and packaging innovation

CCAI is building a pre-eminent Supply Chain capability to drive complete market leadership in NARTDs in Indonesia

CAPACITY EFFICIENCY INNOVATION

2

Kalimantan15 millionDensity = 19 / km²

Kalimantan15 millionDensity = 19 / km²Sumatra

54 million Density = 106 / km²

Sumatra54 million Density = 106 / km²

Java143 million

Density = 1,101 / km²

Java143 million

Density = 1,101 / km²

Bali4 million

Density = 701 / km²

Bali4 million

Density = 701 / km²

Sulawesi17 millionDensity = 98 / km²

Sulawesi17 millionDensity = 98 / km²

Rest of Indonesia ►►17 million

Density = 56 / km²

Rest of Indonesia ►►17 million

Density = 56 / km²

Singapore

Malaysia Brunei

Serving ~250 million Indonesians

30 million

5 million

Australia23 millionDensity = 2.9 / km²

Australia23 millionDensity = 2.9 / km² 3

Production Plants (x9)

Distribution Centres (x85)

Legend

4

Kalimantan

Sumatra

Java

Bali

Sulawesi

Lombok

PUMA ►►

Singapore

Malaysia

Thailand

Brunei

85 distribution centers delivering to 385,000 customer locations

Medan

Padang

Lampung

Cibitung

Bandung Semarang

SurabayaBali

Cikedoken

4

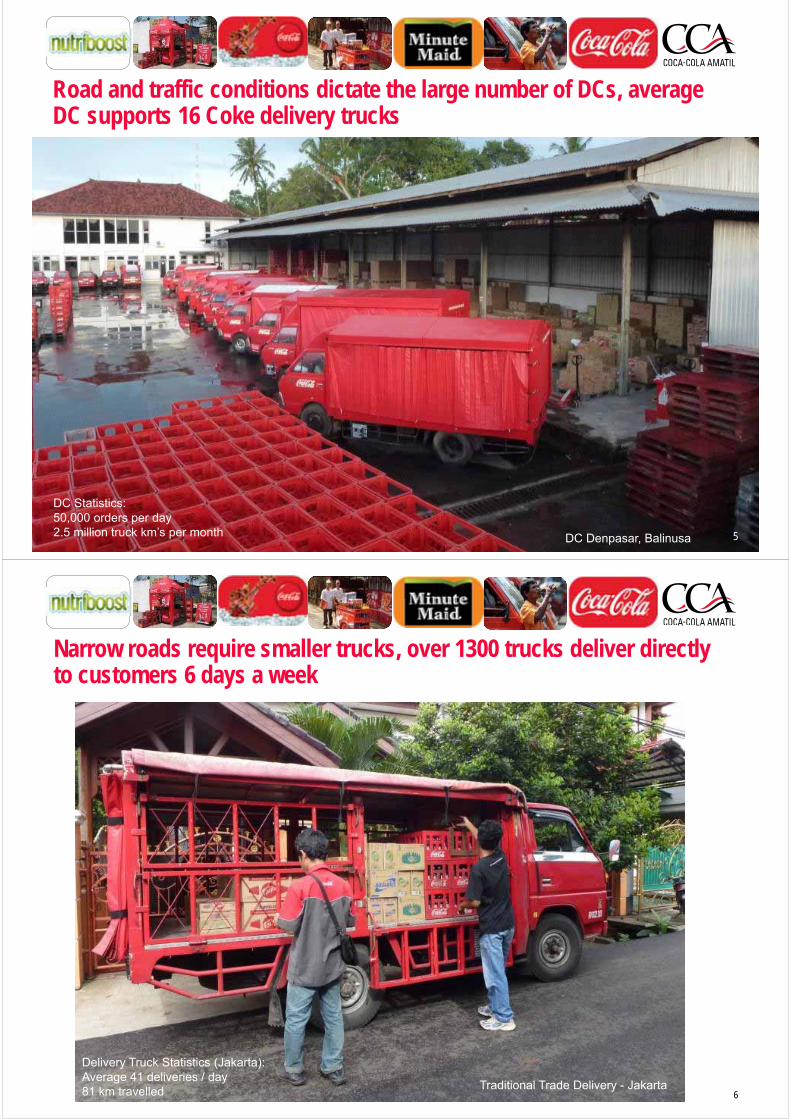

Road and traffic conditions dictate the large number of DCs, average DC supports 16 Coke delivery trucks

DC Denpasar, Balinusa 5

DC Statistics: 50,000 orders per day2.5 million truck km’s per month

6

Narrow roads require smaller trucks, over 1300 trucks deliver directly to customers 6 days a week

Traditional Trade Delivery - Jakarta

Delivery Truck Statistics (Jakarta): Average 41 deliveries / day81 km travelled

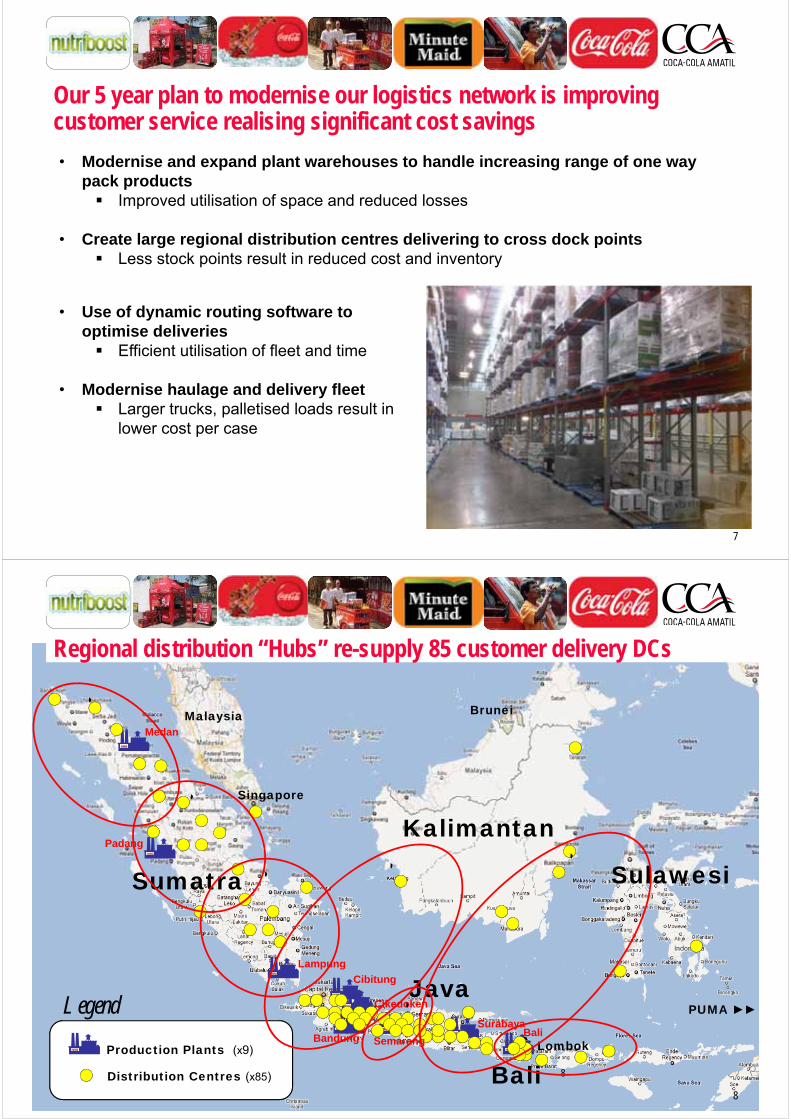

Our 5 year plan to modernise our logistics network is improving customer service realising significant cost savings

• Modernise and expand plant warehouses to handle increasing range of one way pack products Improved utilisation of space and reduced losses

• Create large regional distribution centres delivering to cross dock points Less stock points result in reduced cost and inventory

• Use of dynamic routing software to optimise deliveries Efficient utilisation of fleet and time

• Modernise haulage and delivery fleet Larger trucks, palletised loads result in

lower cost per case

7

Production Plants (x9)

Distribution Centres (x85)

Legend

8

Kalimantan

Sumatra

Java

Bali

Sulawesi

Lombok

PUMA ►►

Singapore

Malaysia

Thailand

Brunei

Regional distribution “Hubs” re-supply 85 customer delivery DCs

Medan

Padang

Lampung

Cibitung

Bandung Semarang

SurabayaBali

Cikedoken

`

8

CCAI is halfway through the expansion of our “hub and spoke” distribution network

Key Facts• Completed 2013• 32,000 m²• 2.0 million case storage capacity• 237,000 cases/day throughput

Cibitung PlantCibitung Plant

Cibitung Regional Distribution CentreCibitung Regional Distribution Centre

9

Central Java Regional DC is under construction in Semarang

Key Facts• Currently under construction• 12,000 m²• 480,000 case storage capacity• 75,000 cases/day throughput• Estimated completion May 2014

Central JavaRegional Distribution CentreCentral JavaRegional Distribution Centre

ground worksground works10

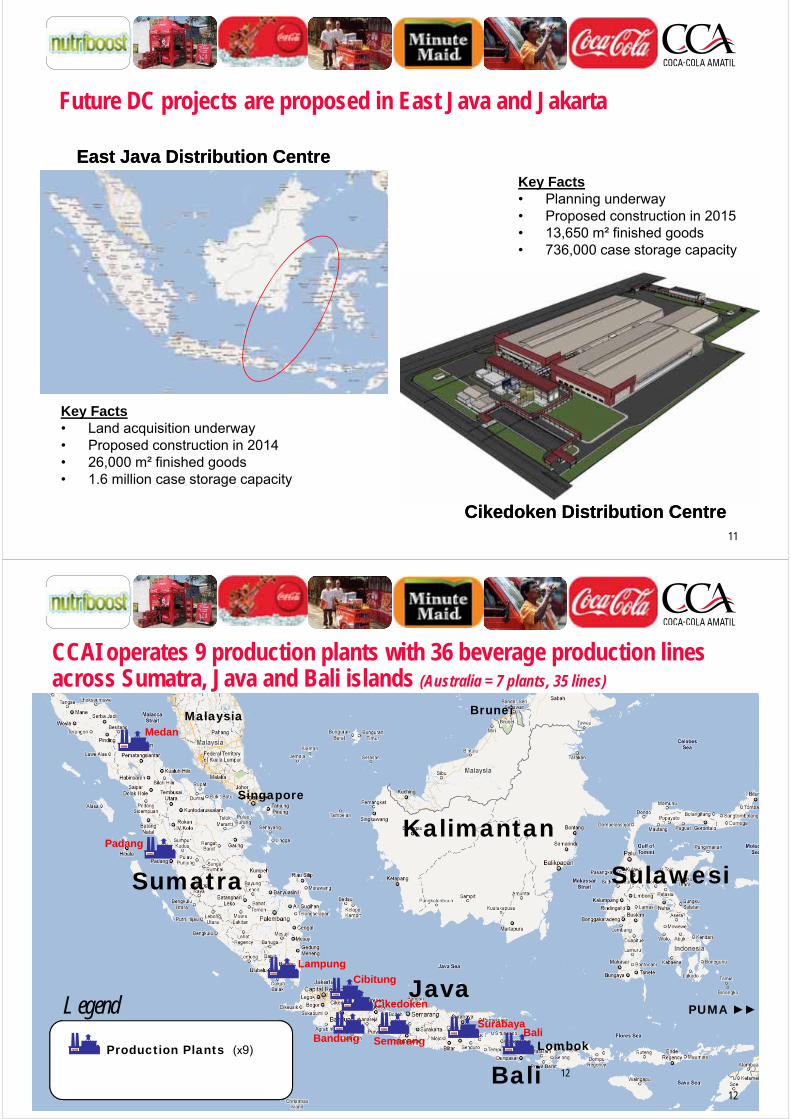

Future DC projects are proposed in East Java and Jakarta

Cikedoken Distribution CentreCikedoken Distribution Centre

Key Facts• Land acquisition underway• Proposed construction in 2014• 26,000 m² finished goods• 1.6 million case storage capacity

East Java Distribution CentreEast Java Distribution CentreKey Facts• Planning underway• Proposed construction in 2015• 13,650 m² finished goods• 736,000 case storage capacity

11

Production Plants (x9)

Legend

12

Kalimantan

Sumatra

Java

Bali

Sulawesi

Lombok

PUMA ►►

Singapore

Malaysia Brunei

Medan

Padang

Lampung

Cibitung

Bandung Semarang

SurabayaBali

Cikedoken

CCAI operates 9 production plants with 36 beverage production lines across Sumatra, Java and Bali islands (Australia = 7 plants, 35 lines)

12

We have invested AUD $400 million to more than double our total capacity since 2010

• In 2013 we expanded into new product categories, adding water and dairy capacity

• Recently installed PET blow-fill lines offer us flexibility to meet changing consumer demand -- flexibility to produce CSD, Hotfill and water all on the same production line

13

We have installed world class equipment in every plant

Hot Fill Line 4, Cibitung14

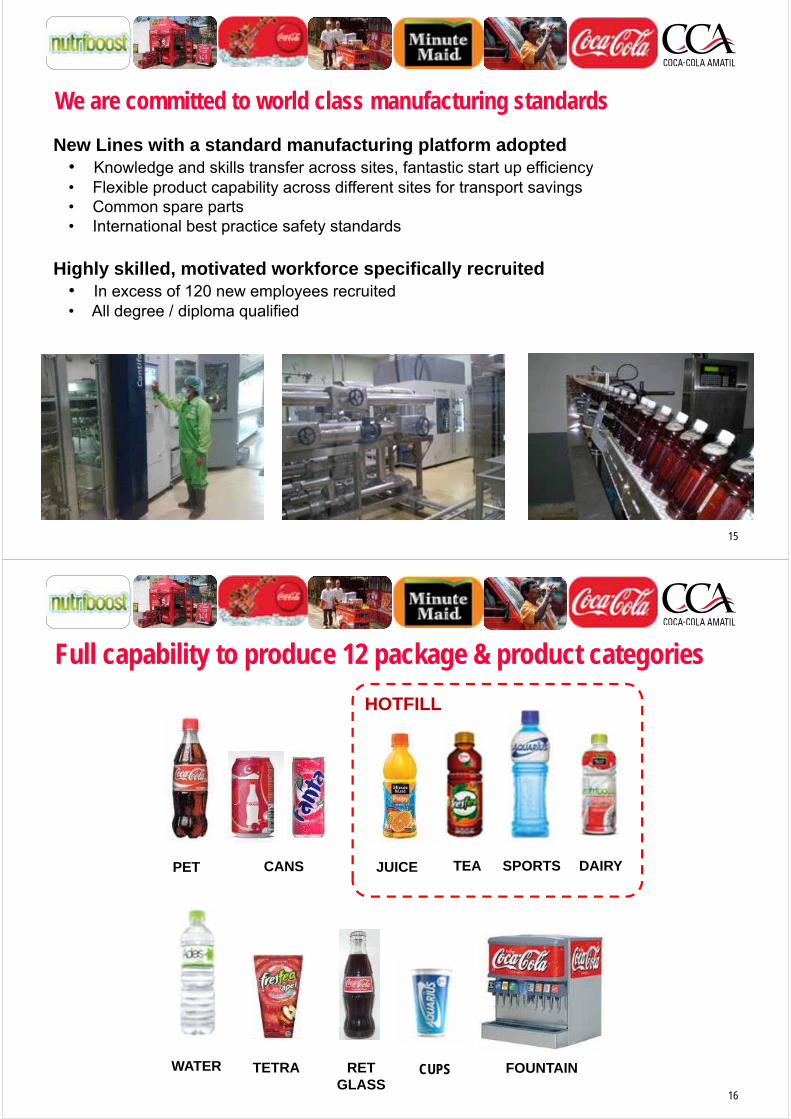

We are committed to world class manufacturing standards

New Lines with a standard manufacturing platform adopted• Knowledge and skills transfer across sites, fantastic start up efficiency• Flexible product capability across different sites for transport savings • Common spare parts • International best practice safety standards

Highly skilled, motivated workforce specifically recruited• In excess of 120 new employees recruited • All degree / diploma qualified

15

Full capability to produce 12 package & product categories

PET TEAJUICE

RET GLASS

CANS

TETRA

DAIRY

WATER

SPORTS

FOUNTAIN

HOTFILL

16

CUPS

We plan to continue production investment ahead of the growth curve

17

Water Line 7, Cibitung

Juice Line 1, Bandung

Our manufacturing platform is now an enabler for Innovation

CCAI now produces some of the lightest weight bottles in the world

-21%-14% -30%

Less PETin our

CSD PET bottles

Smaller closures for

PET bottles

Less PETin our

600ml Water bottle

New products launched in 2013 include:

CSD Tea Dairy Pulpy Sports Drink

18

Cups

vs. 2010 vs. 2010 vs. 2010

PackagingSelf manufacture of PET preforms and bottlesCCAI will produce 100% of our own preforms and bottles by the end of 2015. CCA has a group strategy on bottle and preform manufacture ensuring a common platform across the group.

PSD Preform Plant, Cibitung

19

Production Plants (x9)

Distribution Centres (x85)

Legend

20

Kalimantan

Sumatra

Java

Bali

Sulawesi

Lombok

PUMA ►►

Singapore

Malaysia

Thailand

Brunei

Our investment has created manufacturing and logistics capability that our competitors have not been able to match

Medan

Padang

Lampung

Cibitung

Bandung Semarang

SurabayaBali

Cikedoken

20

DisclaimerCCA advises that these presentation slides contain forward looking statements which may be subject to significant uncertainties outside of CCA’s control.

No representation is made as to the accuracy or reliability of forward looking statements or the assumptions on which they are based.

Actual future events may vary from these forward looking statements and you are cautioned not to place undue reliance on any forward looking statement.

Indonesia: Sustainability & Corporate Social Responsibility

Indonesia Investor TourNov 7-8, 2013

Bruce Waterfield Business Services DirectorPutri Silalahi Head of Corporate Communications

HISTORY IN INDONESIA

22 years of believing in the potential of Indonesia

2

s

Coca-Cola was invented

1886

1904Indonesia’s Independence

1886

2 Regional Distribution Centresstart operating

CCAI introduces PET packaging

2013

Coca-Cola entered Indonesia

1927

1945

3 Jan: Coca-Cola Amatilentered Indonesia

1992

1996

Full ownership of Coca-Cola Packaging & Distribution Businesses in Indonesia*

2005 2013

2012Acquisition of CikedokanPlant, West Java

CCA parent company was born

2008Bali Beach Clean Up established

100%

* Excluding Manado Region of Northern Sulawesi

DEVELOPMENT OF SUSTAINABILITY IN THE COUNTRY

We have a long history of corporate social responsibility in Indonesia through significant infrastructure investments, job creation, community development and support for the

livelihoods of workers and their families

3

Distribution in 1996 Semarang Plant Mosque Polyclinic Cibitung Idul Adha Medan in 2013

COCA-COLA FOUNDATION INDONESIA

4

Mi Classified - Restricted

Raising quality of education and improving

social welfare & community development:

• ‘Small Drops’ supported by local shared

funding with the Coca-Cola Company

• ‘Large Drops’ programs funded by

international donors such, as the Gates

Foundation

• Library Programs

• Scholarship Programs

• Water Programs

OUR COMMITMENT TO SUSTAINABILITY

Build sustainability into the core values of the organisation

and part of our every day decision making processes

5

WORKPLACE MARKETPLACE COMMUNITY ENVIRONMENT

WORKPLACE

IMPACT OF OUR ORGANISATION IN THE COUNTRY

6

Today ‘tens of thousands’ of Indonesian’s, be it employees, suppliers or their dependents directly benefit from CCA’s operational footprint across the country

• 7,400 Permanent Employee

• Up to 4,000 Casual Workers

• More than 2,500 suppliers

WORKPLACEBuilding a capable workforce in an innovative, safe, and Knowledgeable work environment

7

Mi Classified - Restricted

• 458 future leaders recruited through our Indonesian Graduate Trainee Program since 1995

• Developing a strong OH&S culture

• 19,403 training days during 2012

• Support for religious and medical needs for staff and surrounding communities with over 31,000 treatments this year alone

• Well informed staff through Indonesia’s “Best Internal Magazine” as voted by Indonesia Press Association.

Putri Silalahi

• Head of Media and Communications

• Joined CCA Indonesia in July 2011

• A Graduate of Mass Communication from the University of the Philippines

8

MARKETPLACE

9

• CCAI currently servicing 600,000 customers in the market

• Partnering with TCCC in the 5by20 program which will commence in November 2013

• CCAI plays an active leadership role in economic and industry associations:

• Indonesian Soft Drink Association (ASRIM)

• Indonesian Food & Beverage Association (GAPMMI)

• Indonesian Chamber of Commerce (KADIN)

• Indonesian-Australian Business Council (IABC)

• Indonesian Business Council for Sustainable Development (IBCSD)

Mi Classified - Restricted

MARKETPLACE

A Brand Portfolio that offers choice

10

Mi Classified -Restricted

SPARKLING LOW CALORIES / NO SUGAR

FUNCTIONAL WATERJUICETEADAIRY

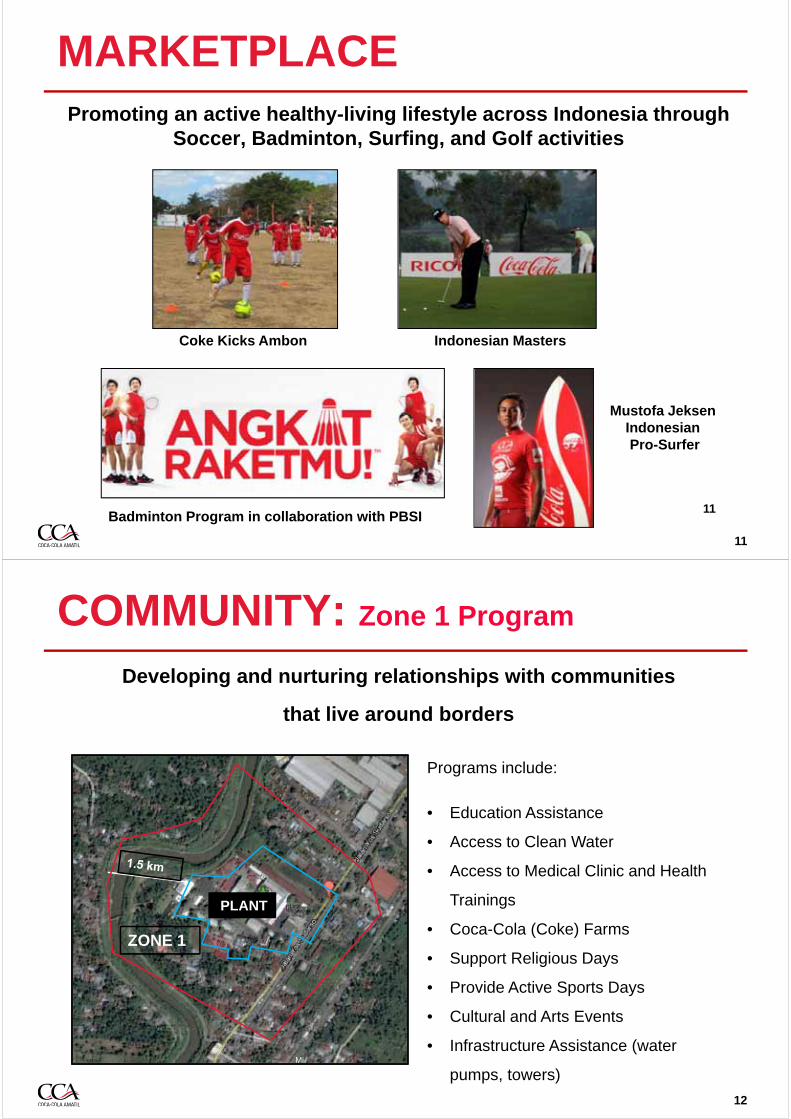

MARKETPLACEPromoting an active healthy-living lifestyle across Indonesia through

Soccer, Badminton, Surfing, and Golf activities

11

11Mi Classified - Restricted

Coke Kicks Ambon Indonesian Masters

Mustofa JeksenIndonesianPro-Surfer

Badminton Program in collaboration with PBSI

COMMUNITY: Zone 1 Program

Developing and nurturing relationships with communities

that live around borders

12

PLANT

ZONE 1

Mi Classified - Restricted

Programs include:

• Education Assistance

• Access to Clean Water

• Access to Medical Clinic and Health

Trainings

• Coca-Cola (Coke) Farms

• Support Religious Days

• Provide Active Sports Days

• Cultural and Arts Events

• Infrastructure Assistance (water

pumps, towers)

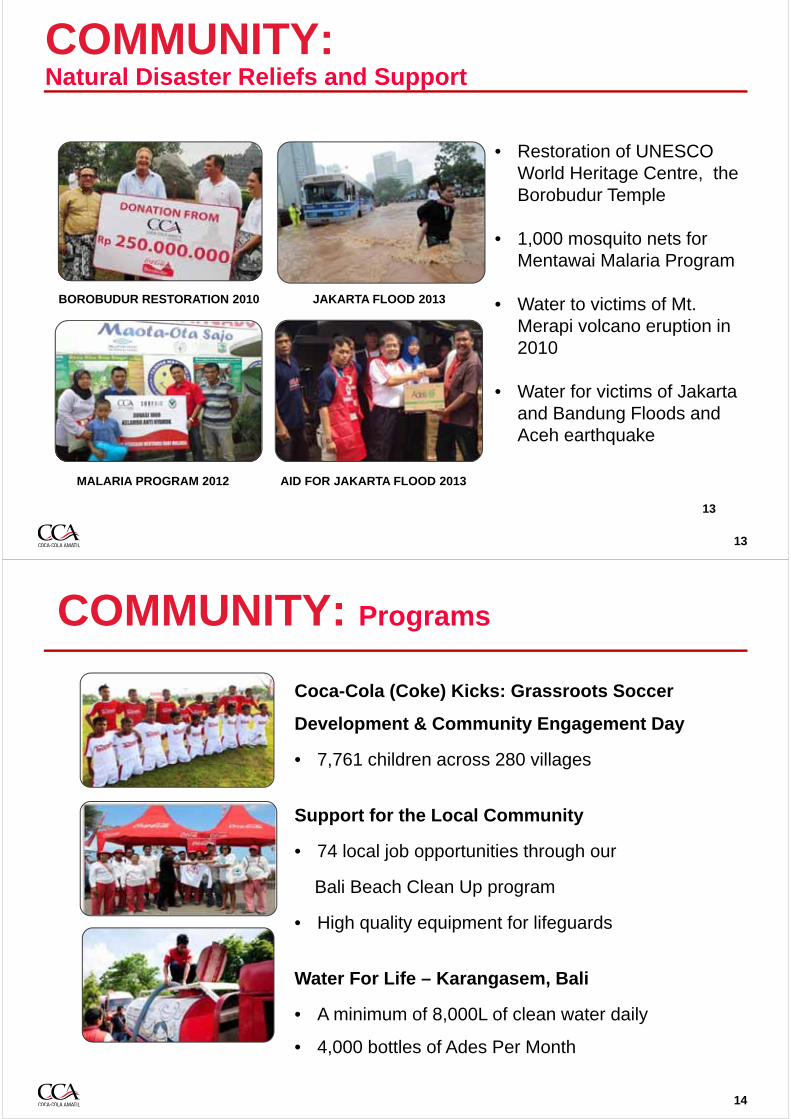

COMMUNITY:Natural Disaster Reliefs and Support

13

• Restoration of UNESCO World Heritage Centre, the Borobudur Temple

• 1,000 mosquito nets for Mentawai Malaria Program

• Water to victims of Mt. Merapi volcano eruption in 2010

• Water for victims of Jakarta and Bandung Floods and Aceh earthquake

13

MALARIA PROGRAM 2012 AID FOR JAKARTA FLOOD 2013

JAKARTA FLOOD 2013BOROBUDUR RESTORATION 2010

COMMUNITY: Programs

14

Coca-Cola (Coke) Kicks: Grassroots Soccer

Development & Community Engagement Day

• 7,761 children across 280 villages

Support for the Local Community

• 74 local job opportunities through our

Bali Beach Clean Up program

• High quality equipment for lifeguards

Water For Life – Karangasem, Bali

• A minimum of 8,000L of clean water daily

• 4,000 bottles of Ades Per Month

Mi Classified - Restricted

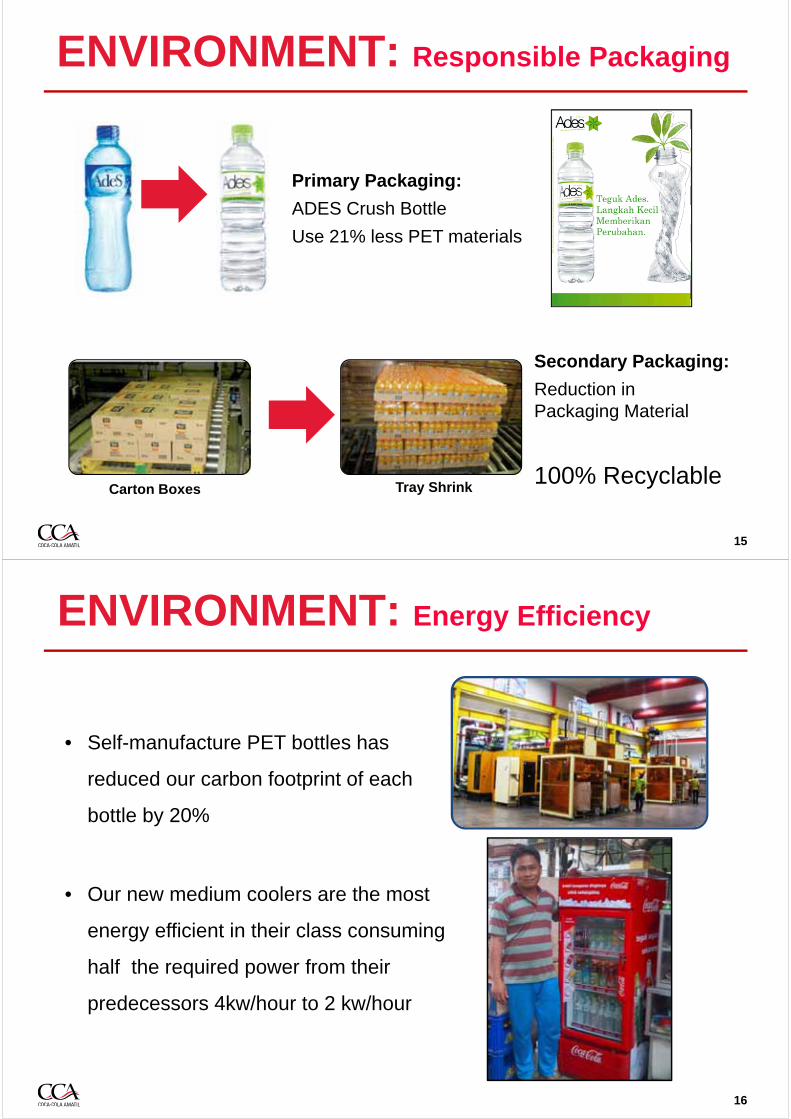

ENVIRONMENT: Responsible Packaging

15

Primary Packaging:

ADES Crush Bottle

Use 21% less PET materials

Secondary Packaging:

Reduction in Packaging Material

100% RecyclableCarton Boxes Tray Shrink

ENVIRONMENT: Energy Efficiency

16

• Self-manufacture PET bottles has

reduced our carbon footprint of each

bottle by 20%

• Our new medium coolers are the most

energy efficient in their class consuming

half the required power from their

predecessors 4kw/hour to 2 kw/hour

Mi Classified - Restricted

ENVIRONMENT: Bali Beach Clean Up

17

2008 2009 2010 2011 2012 2013

923

1,92,2 2,2

2,8

2,5

• In 5 years, 16,000 tons of waste removed from 5 iconic beaches

Mi Classified - Restricted

Rubbish Collected (in Tonnes)

Area Sales Volume (in PCs) 17%

35%-5%

34%

1,947

74,598

2002-2008 2009-2013

Turtle Eggs Collected

Kuta Beach Sea Turtle Conservation

DisclaimerCCA advises that these presentation slides contain forward looking statements which may be subject to significant uncertainties outside of CCA’s control.

No representation is made as to the accuracy or reliability of forward looking statements or the assumptions on which they are based.

Actual future events may vary from these forward looking statements and you are cautioned not to place undue reliance on any forward looking statement.

11

Australasian Strategy ReviewIndonesia Investor Tour

Nov 7-8, 2013

Warwick White Managing Director Australasia

2

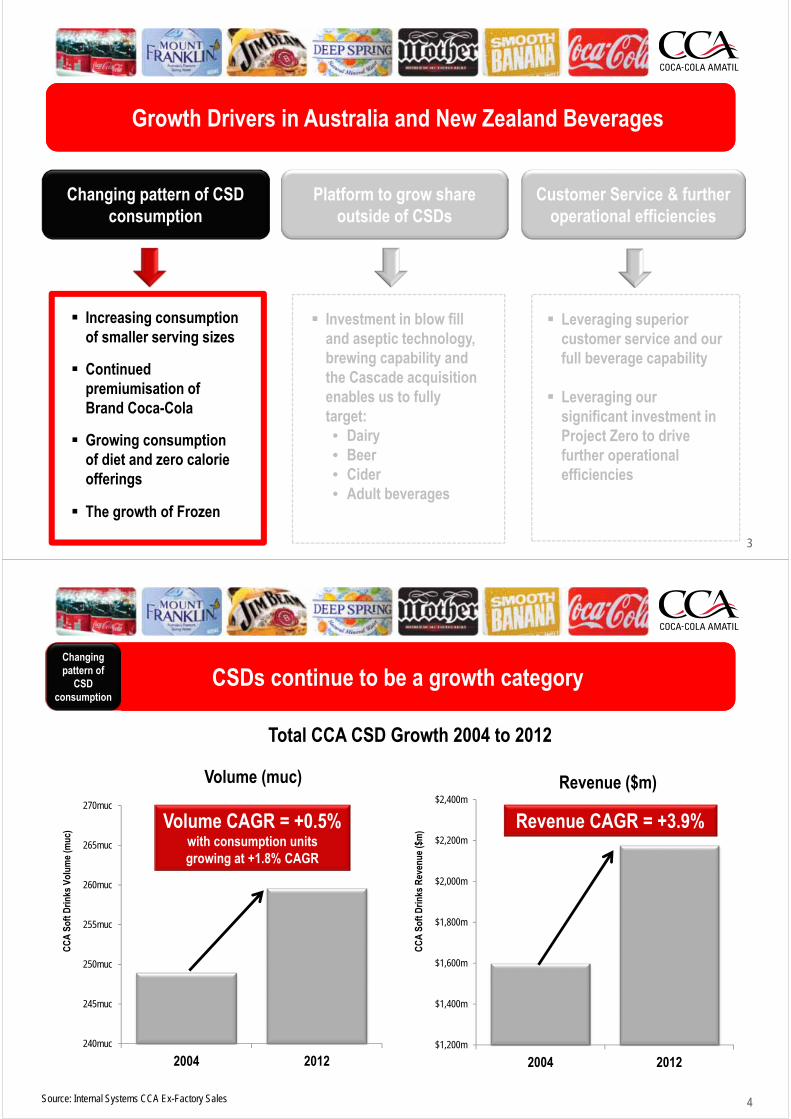

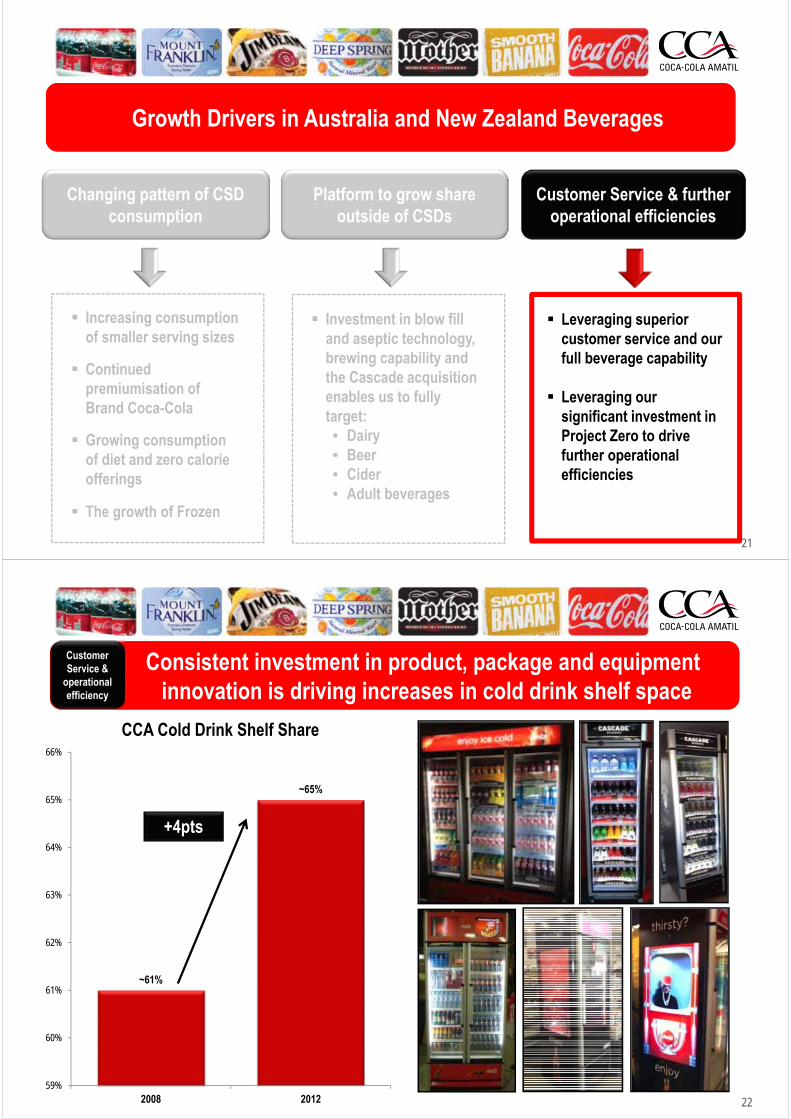

Growth drivers in Australia and New Zealand BeveragesGrowth drivers in Australia and New Zealand Beverages

Changing pattern of CSD consumption

Platform to grow share outside of CSDs

Customer Service & further operational efficiencies

Increasing consumption of smaller serving sizes

Continued premiumisation of Brand Coca-Cola

Growing consumption of diet and zero calorie offerings

The growth of Frozen

Investment in blow fill and aseptic technology, brewing capability and the Cascade acquisition enables us to fully target:• Dairy• Beer• Cider• Adult beverages

Leveraging superior customer service and our full beverage capability

Leveraging our significant investment in Project Zero to drive further operational efficiencies

3

Growth Drivers in Australia and New Zealand BeveragesGrowth Drivers in Australia and New Zealand Beverages

Changing pattern of CSD consumption

Platform to grow share outside of CSDs

Customer Service & further operational efficiencies

Investment in blow fill and aseptic technology, brewing capability and the Cascade acquisition enables us to fully target:• Dairy• Beer• Cider• Adult beverages

Leveraging superior customer service and our full beverage capability

Leveraging our significant investment in Project Zero to drive further operational efficiencies

Increasing consumption of smaller serving sizes

Continued premiumisation of Brand Coca-Cola

Growing consumption of diet and zero calorie offerings

The growth of Frozen

4

240muc

245muc

250muc

255muc

260muc

265muc

270muc

2004 2012

CC

A S

oft D

rinks

Vol

ume

(muc

)

Volume (muc)

$1,200m

$1,400m

$1,600m

$1,800m

$2,000m

$2,200m

$2,400m

2004 2012

CC

A S

oft D

rinks

Rev

enue

($m

)

Revenue ($m)

Volume CAGR = +0.5%with consumption units growing at +1.8% CAGR

CSDs continue to be a growth categoryCSDs continue to be a growth category

Revenue CAGR = +3.9%

Total CCA CSD Growth 2004 to 2012

Source: Internal Systems CCA Ex-Factory Sales

Changing pattern of

CSD consumption

5

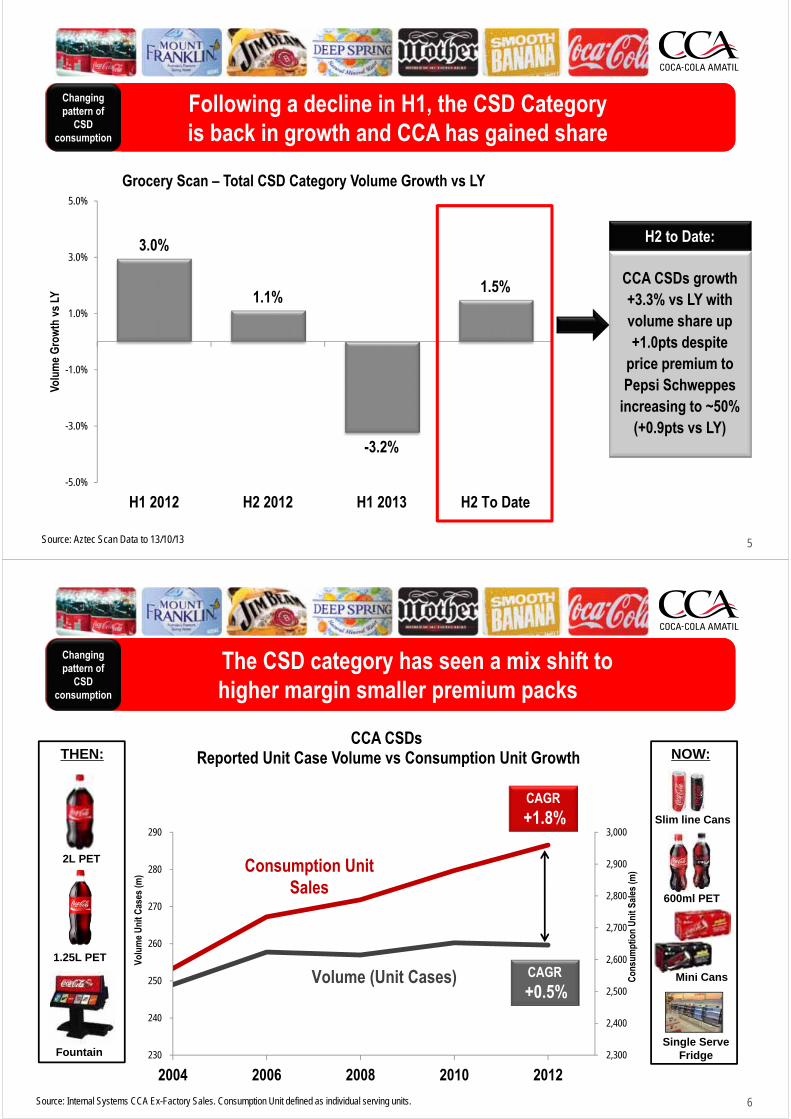

3.0%

1.1%

-3.2%

1.5%

-5.0%

-3.0%

-1.0%

1.0%

3.0%

5.0%

H1 2012 H2 2012 H1 2013 H2 To Date

Volu

me

Gro

wth

vs

LY

Grocery Scan – Total CSD Category Volume Growth vs LY

Following a decline in H1, the CSD Category is back in growth and CCA has gained shareFollowing a decline in H1, the CSD Category is back in growth and CCA has gained share

Source: Aztec Scan Data to 13/10/13

Changing pattern of

CSD consumption

CCA CSDs growth +3.3% vs LY with volume share up +1.0pts despite

price premium to Pepsi Schweppes

increasing to ~50% (+0.9pts vs LY)

H2 to Date:

6

2,300

2,400

2,500

2,600

2,700

2,800

2,900

3,000

230

240

250

260

270

280

290

2004 2006 2008 2010 2012

Con

sum

ptio

n U

nit S

ales

(m)

Volu

me

Uni

t Cas

es (m

)

CCA CSDsReported Unit Case Volume vs Consumption Unit Growth

Volume (Unit Cases)

Consumption Unit Sales

The CSD category has seen a mix shift to higher margin smaller premium packsThe CSD category has seen a mix shift to higher margin smaller premium packs

CAGR

+0.5%

CAGR

+1.8%

Source: Internal Systems CCA Ex-Factory Sales. Consumption Unit defined as individual serving units.

2L PET

Mini Cans

Changing pattern of

CSD consumption

THEN: NOW:

1.25L PET

Fountain

600ml PET

Slim line Cans

Single Serve Fridge

7

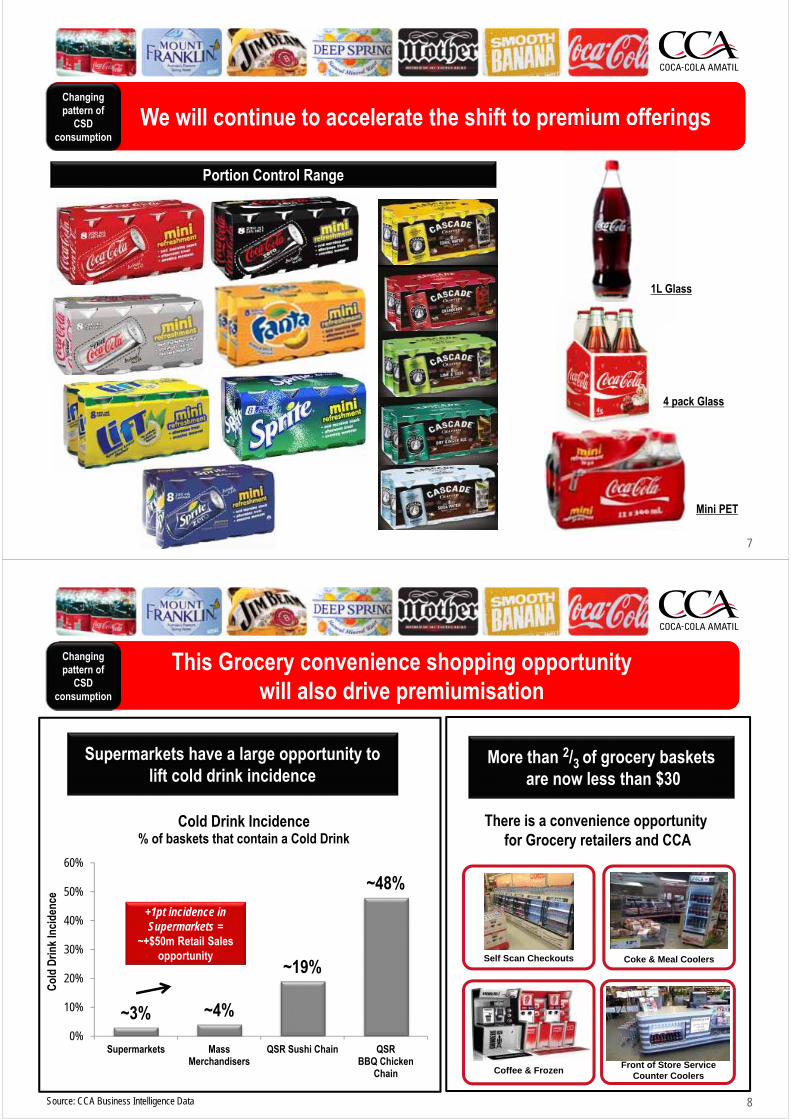

We will continue to accelerate the shift to premium offeringsWe will continue to accelerate the shift to premium offerings

Mini PET

1L Glass

4 pack Glass

Changing pattern of

CSD consumption

Portion Control Range

8

~3% ~4%

~19%

~48%

0%

10%

20%

30%

40%

50%

60%

Supermarkets MassMerchandisers

QSR Sushi Chain QSRBBQ Chicken

Chain

Col

d D

rink

Inci

denc

e

Cold Drink Incidence % of baskets that contain a Cold Drink

Supermarkets have a large opportunity to lift cold drink incidence

This Grocery convenience shopping opportunitywill also drive premiumisation

This Grocery convenience shopping opportunitywill also drive premiumisation

+1pt incidence in Supermarkets =

~+$50m Retail Sales opportunity

There is a convenience opportunityfor Grocery retailers and CCA

More than 2/3 of grocery basketsare now less than $30

Source: CCA Business Intelligence Data

Self Scan Checkouts Coke & Meal Coolers

Coffee & FrozenFront of Store Service

Counter Coolers

Changing pattern of

CSD consumption

9

We continue to invest in brand CokeWe continue to invest in brand CokeChanging pattern of

CSD consumption

10

Coke Zero “Just Add Zero” campaign is working. Coke Zero has the fastest growing household penetration in the cola category.

Coke Zero “Just Add Zero” campaign is working. Coke Zero has the fastest growing household penetration in the cola category.

2013 YTD Results

100,000 new households recruited

Immediate Consumption transactions +7%

Changing pattern of

CSD consumption

Source: Compass transaction data Q2 2013.

11

We are growing Frozen with new flavour variants and now have over 6,000 Frozen Beverage machines in market.

Frozen has grown to ~150m serves annually (Sept 2013 MAT)

We are growing Frozen with new flavour variants and now have over 6,000 Frozen Beverage machines in market.

Frozen has grown to ~150m serves annually (Sept 2013 MAT)

Source: Internal Systems MAT Sept 2013

Changing pattern of

CSD consumption

12

Growth Drivers in Australia and New Zealand BeveragesGrowth Drivers in Australia and New Zealand Beverages

Changing pattern of CSD consumption

Platform to grow share outside of CSDs

Customer Service & further operational efficiencies

Investment in blow fill and Aseptic technology, brewing capability and the Cascade acquisition enables us to fully target:• Dairy• Beer• Cider• Adult beverages

Leveraging superior customer service and our full beverage capability

Leveraging our significant investment in Project Zero to drive further operational efficiencies

Increasing consumption of smaller serving sizes

Continued premiumisation of Brand Coca-Cola

Growing consumption of diet and zero calorie offerings

The growth of Frozen

13

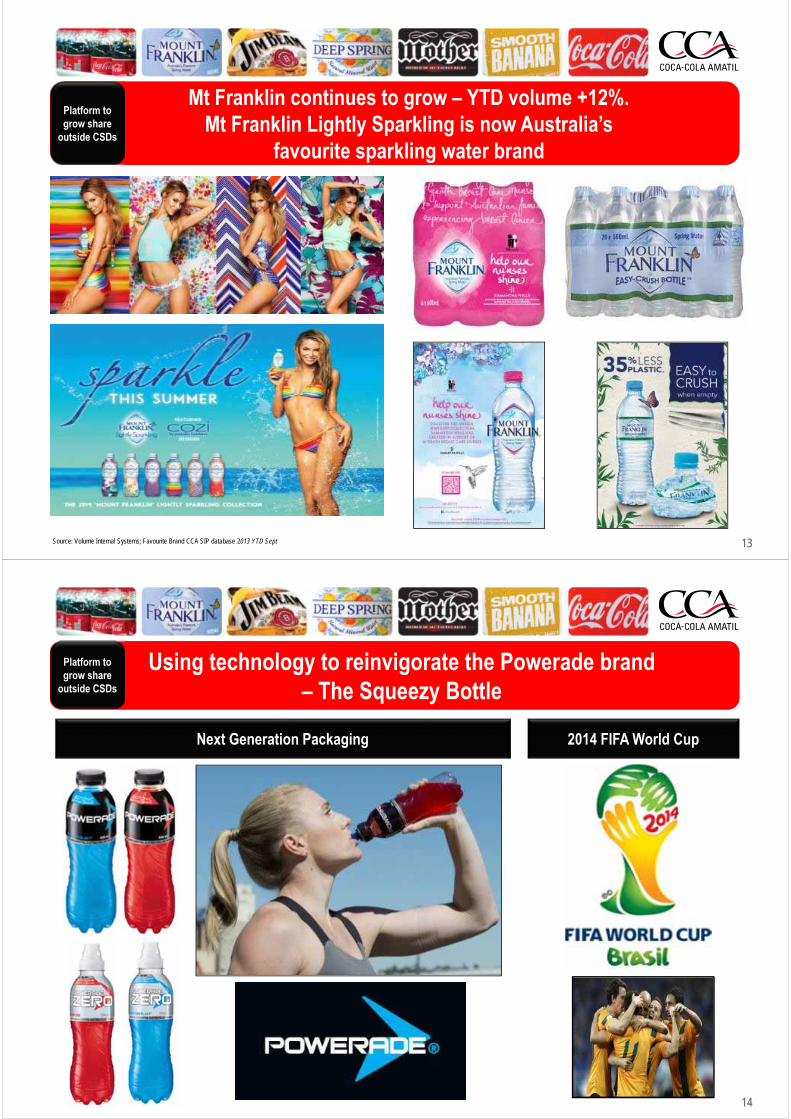

Mt Franklin continues to grow – YTD volume +12%. Mt Franklin Lightly Sparkling is now Australia’s

favourite sparkling water brand

Mt Franklin continues to grow – YTD volume +12%. Mt Franklin Lightly Sparkling is now Australia’s

favourite sparkling water brand

Source: Volume Internal Systems; Favourite Brand CCA SIP database 2013 YTD Sept

Platform to grow share

outside CSDs

14

Using technology to reinvigorate the Powerade brand – The Squeezy Bottle

Using technology to reinvigorate the Powerade brand – The Squeezy Bottle

2014 FIFA World CupNext Generation Packaging

Platform to grow share

outside CSDs

15

Our innovation in the Energy segment is broadening appeal to a wider range of consumers

Our innovation in the Energy segment is broadening appeal to a wider range of consumers

250ml Range - Broadening Appeal

Source: B3 data to August 2013 Past Four Week Consumption

69% 68%

31% 32%

Redbull Mother

Male vs Female Consumption by Brand

Female MaleMother’s

male vs female consumption is

in line with Redbull

500ml Range - Core Consumers

Platform to grow share

outside CSDs

16

We are targeting the premium adult non-alcoholic segment with Cascade

We are targeting the premium adult non-alcoholic segment with Cascade

Platform to grow share

outside CSDs

45%

47%

49%

51%

53%

55%

57%

59%

61%

63%

12-19Years

20-29Years

30-39Years

40-49Years

50-59Years

60-69Years

Volu

me

Shar

e of

Con

sum

ptio

n

TCCC Share of Sparkling Consumption by Age

17

0% 5% 10% 15% 20% 25% 30%

Early Morning Before 8am

Mid‐Morning Between 8‐11am

Midday Between 11‐2pm

Afternoon Between 2‐5pm

Early Evening Between 5‐8pm

Evening After 8pm

Day Part CC System Volume Share

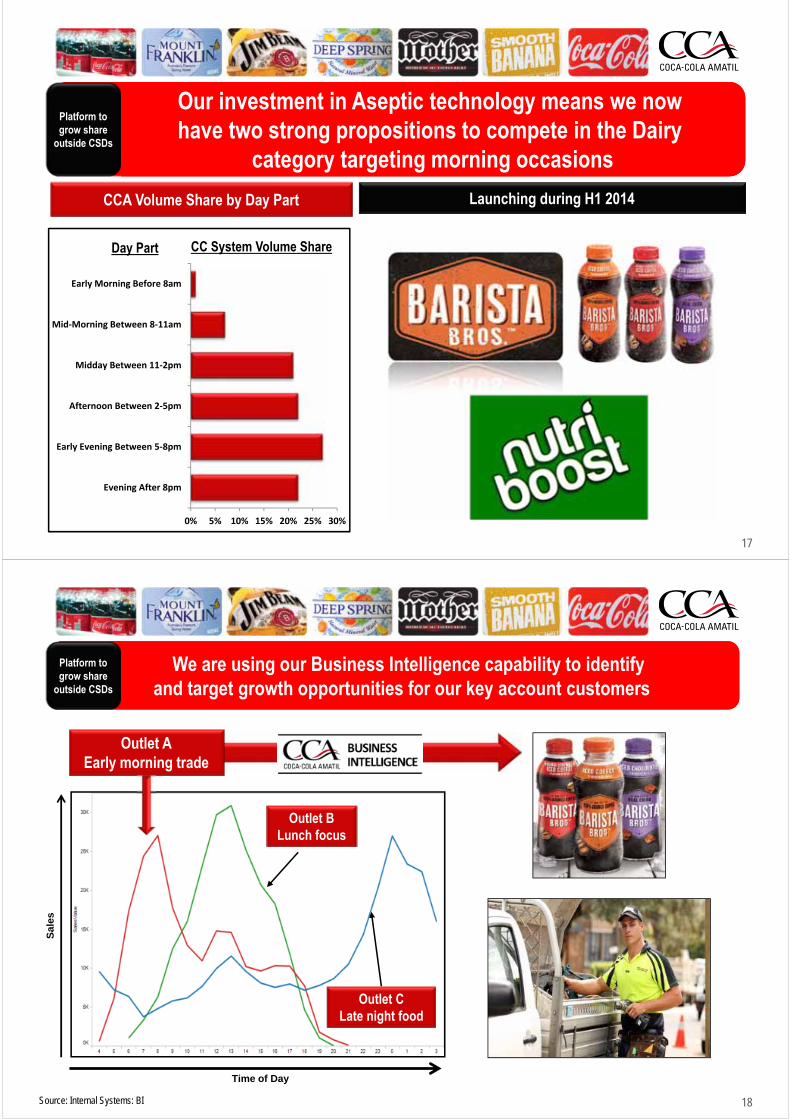

Our investment in Aseptic technology means we now have two strong propositions to compete in the Dairy

category targeting morning occasions

Our investment in Aseptic technology means we now have two strong propositions to compete in the Dairy

category targeting morning occasions

Platform to grow share

outside CSDs

Launching during H1 2014CCA Volume Share by Day Part

18

We are using our Business Intelligence capability to identify and target growth opportunities for our key account customers

We are using our Business Intelligence capability to identify and target growth opportunities for our key account customers

Platform to grow share

outside CSDs

Time of Day

Sal

es

Outlet CLate night food

Outlet BLunch focus

Outlet AEarly morning trade

Source: Internal Systems: BI

19

Trax technology has created the capability to sell against competitors via our call centre

Trax technology has created the capability to sell against competitors via our call centre

Ability to identify ranging gaps in real time Allows CCA sales rep to provide real-time data to

our call centre

Shelf Share Category Share Out of Stocks

Point & Shoot Image Capture

Platform to grow share

outside CSDs

20

In Hot Beverages we will continue to leverage our national distribution network & National Account relationships

In Hot Beverages we will continue to leverage our national distribution network & National Account relationships

Platform to grow share

outside CSDs

21

Growth Drivers in Australia and New Zealand BeveragesGrowth Drivers in Australia and New Zealand Beverages

Changing pattern of CSD consumption

Platform to grow share outside of CSDs

Customer Service & further operational efficiencies

Investment in blow fill and aseptic technology, brewing capability and the Cascade acquisition enables us to fully target:• Dairy• Beer• Cider• Adult beverages

Leveraging superior customer service and our full beverage capability

Leveraging our significant investment in Project Zero to drive further operational efficiencies

Increasing consumption of smaller serving sizes

Continued premiumisation of Brand Coca-Cola

Growing consumption of diet and zero calorie offerings

The growth of Frozen

22

~61%

~65%

59%

60%

61%

62%

63%

64%

65%

66%

2008 2012

CCA Cold Drink Shelf Share

Consistent investment in product, package and equipment innovation is driving increases in cold drink shelf space

Consistent investment in product, package and equipment innovation is driving increases in cold drink shelf space

+4pts

Customer Service &

operational efficiency

23

We are moving our vending business into cashless, resulting in ease of use & more placement opportunities

We are moving our vending business into cashless, resulting in ease of use & more placement opportunities

CCA is the largest National vending operator with more than 30,000 machines in market

In 2014 we are targeting to increase cashless capability from 50% to >75% of the fleet

Cashless Vending

Customer Service &

operational efficiency

24

Leveraging our total portfolio to build a superior customer service proposition – A beverage for every occasion

Leveraging our total portfolio to build a superior customer service proposition – A beverage for every occasion

Flexibility – Leveraging Project Zero

Customer Service FocusFull Beverage Capability

83%

98%

80%

85%

90%

95%

100%

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013(Target)

DIF

OTA

I %

DIFOTAI

Customer Service &

operational efficiency

~300

~1,400

0200400600800

1000120014001600

2004 2008 2010 2012

Num

ber o

f Sku

s

SKU Count

Source: Internal CCA Systems.

25

We have a 3 year programme to leverage our significant investment in Project Zero to drive operational efficiencies

across all areas of our business

We have a 3 year programme to leverage our significant investment in Project Zero to drive operational efficiencies

across all areas of our business

Customer Service &

operational efficiency

myCCA Operational Excellence Capital Investments

Online platform which allows CCA Customers to place orders, pay invoices

& request assistance

A culture of innovation and efficiency within a structured framework

2626

New Zealand

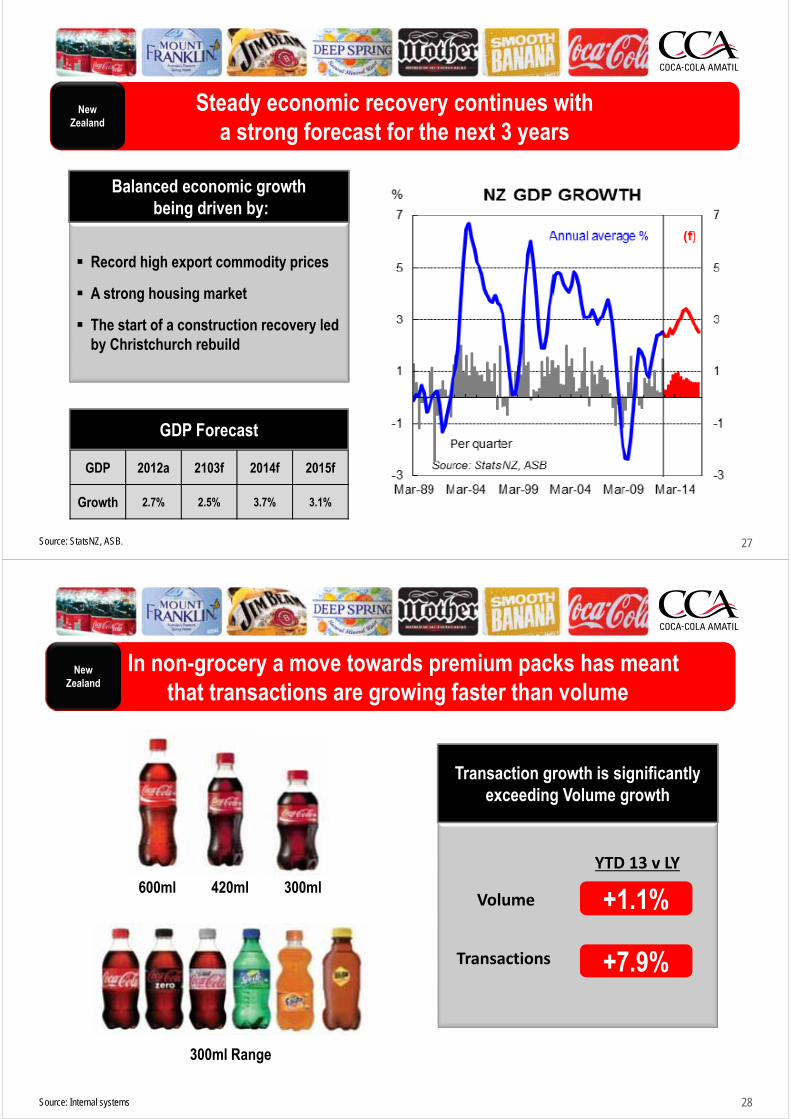

27

GDP 2012a 2103f 2014f 2015f

Growth 2.7% 2.5% 3.7% 3.1%

Steady economic recovery continues with a strong forecast for the next 3 years

Steady economic recovery continues with a strong forecast for the next 3 years

Record high export commodity prices

A strong housing market

The start of a construction recovery led by Christchurch rebuild

Balanced economic growthbeing driven by:

GDP Forecast

New Zealand

Source: StatsNZ, ASB.

28

In non-grocery a move towards premium packs has meantthat transactions are growing faster than volume

In non-grocery a move towards premium packs has meantthat transactions are growing faster than volume

+1.1%

+7.9%

Volume

Transactions

YTD 13 v LY

Source: Internal systems

600ml 420ml 300ml

300ml Range

New Zealand

Transaction growth is significantly exceeding Volume growth

29

66%75%

55%

26%

70%

22% 22%

1% 0% 0% 0%

34%25%

36%

74%

30%

78% 78%

99% 100% 100% 100%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

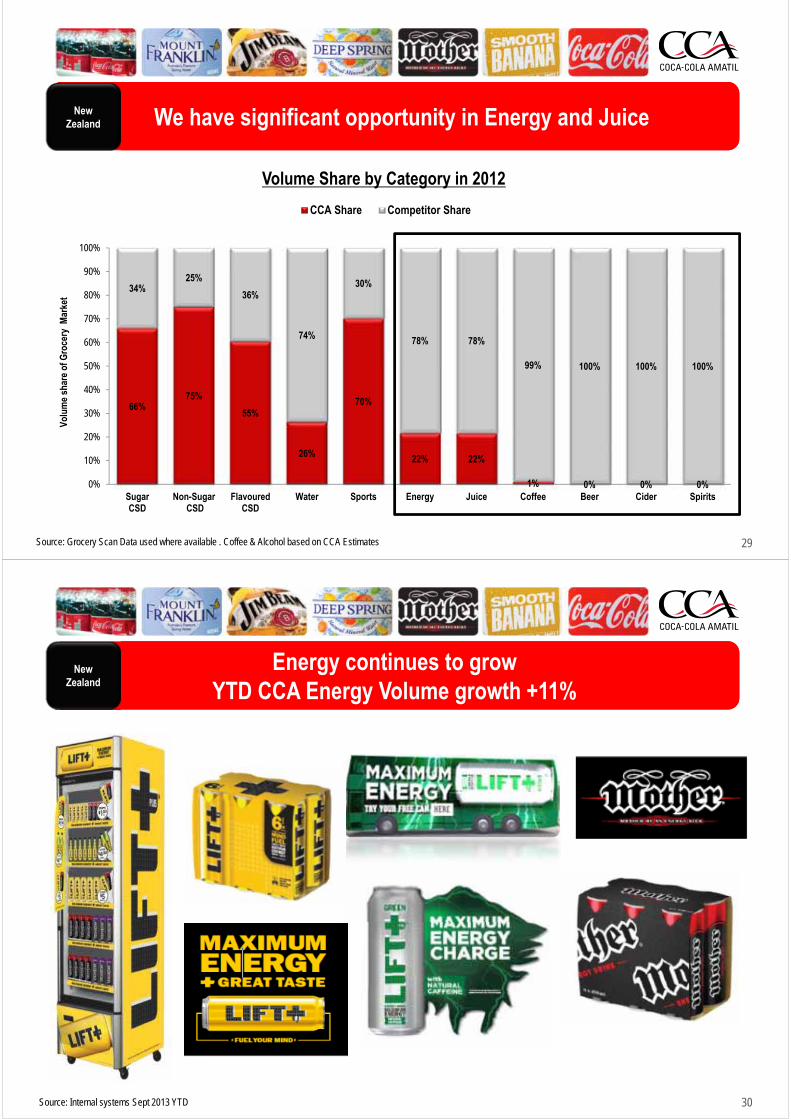

SugarCSD

Non-Sugar CSD

FlavouredCSD

Water Sports Energy Juice Coffee Beer Cider Spirits

Volu

me

shar

e of

Gro

cery

Mar

ket

Volume Share by Category in 2012

CCA Share Competitor Share

We have significant opportunity in Energy and JuiceWe have significant opportunity in Energy and Juice

Source: Grocery Scan Data used where available . Coffee & Alcohol based on CCA Estimates

New Zealand

30

Energy continues to grow YTD CCA Energy Volume growth +11%

Energy continues to grow YTD CCA Energy Volume growth +11%

Source: Internal systems Sept 2013 YTD

New Zealand

31

Juice is performing strongly – YTD CCA Juice volume +7%Juice is performing strongly – YTD CCA Juice volume +7%

Source: Internal sources; Ex factory volume YTD Sept 2013

Packaging Refresh(with new technology)

Pulpy Range

New Zealand

32

We have had success in the Adult Non-Alcoholic Beverages segment with L&P with more innovation to come. YTD Volume growth +17%

We have had success in the Adult Non-Alcoholic Beverages segment with L&P with more innovation to come. YTD Volume growth +17%

New Zealand

Source: Internal systems Sept 2013 YTD

33

Growth Drivers in Australia and New Zealand BeveragesGrowth Drivers in Australia and New Zealand Beverages

Changing pattern of CSD consumption

Platform to grow share outside of CSDs

Customer Service & further operational efficiencies

Increasing consumption of smaller serving sizes

Continued premiumisation of Brand Coca-Cola

Growing consumption of diet and zero calorie offerings

The growth of Frozen

Investment in blow fill and aseptic technology, brewing capability and the Cascade acquisition enables us to fully target:• Dairy• Beer • Cider• Adult beverages

Leveraging superior customer service and our full beverage capability

Leveraging our significant investment in Project Zero to drive further operational efficiencies

3434

Alcoholic Beverages

35

87%

61%

37%31%

58% 61%

21% 24%

11%5% 1% 6%

22%

13%

39%

63%69%

42% 39%

79% 76%

89%95% 99%

94%

78%

100% 100%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

SugarCola

DietCola

Flavours NonFunctional

Water

Functional Water

Sports Energy Tea AdultBeverages& Mixers

Juice ValueAddedDairy

Roast &GroundCoffee

Spirits Beer Cider

Volu

me

Shar

e of

Tot

al M

arke

t

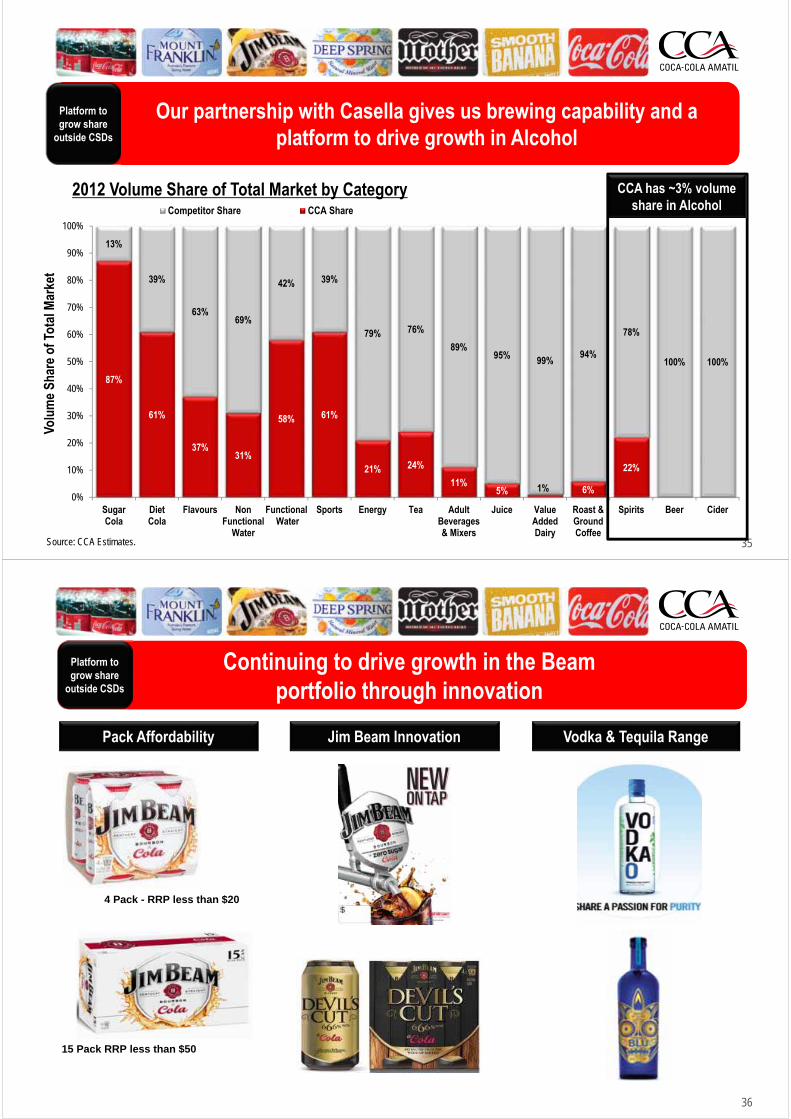

2012 Volume Share of Total Market by CategoryCompetitor Share CCA Share

Our partnership with Casella gives us brewing capability and a platform to drive growth in Alcohol

Our partnership with Casella gives us brewing capability and a platform to drive growth in Alcohol

Platform to grow share

outside CSDs

CCA has ~3% volume share in Alcohol

Source: CCA Estimates.

36

Continuing to drive growth in the Beam portfolio through innovation

Continuing to drive growth in the Beam portfolio through innovation

Pack Affordability Jim Beam Innovation Vodka & Tequila Range

4 Pack - RRP less than $20

15 Pack RRP less than $50

Platform to grow share

outside CSDs

37

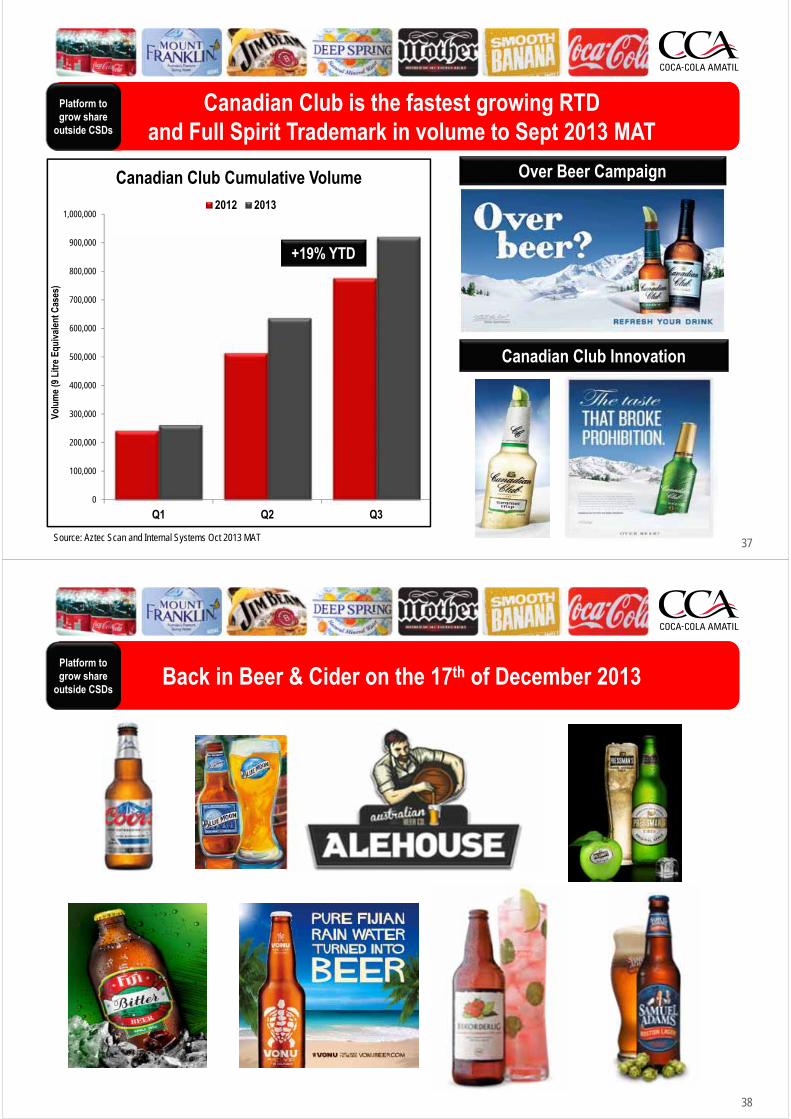

Canadian Club is the fastest growing RTD and Full Spirit Trademark in volume to Sept 2013 MAT

Canadian Club is the fastest growing RTD and Full Spirit Trademark in volume to Sept 2013 MAT

Platform to grow share

outside CSDs

Source: Aztec Scan and Internal Systems Oct 2013 MAT

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

900,000

1,000,000

Q1 Q2 Q3

Volu

me

(9 L

itre

Equi

vale

nt C

ases

)

Canadian Club Cumulative Volume2012 2013

+19% YTD

Over Beer Campaign

Canadian Club Innovation

38

Back in Beer & Cider on the 17th of December 2013Back in Beer & Cider on the 17th of December 2013Platform to grow share

outside CSDs

3939

SPC Ardmona

40

Significant support for Australian made from retailers and application for Australian Government support is progressing

Significant support for Australian made from retailers and application for Australian Government support is progressing

By late 2014, close to 100% of the private label canned fruit business in grocery will be supplied locally by SPCA

SPCA