Embed Size (px)

Citation preview

CCH Federal TaxationBasic Principles

Chapter 7Deductions:

Business/Investment Losses and Passive Activity Losses

©2003, CCH INCORPORATED4025 W. Peterson Ave.Chicago, IL 60646-6085800 248 3248http://tax.cchgroup.com

CCH Federal Taxation Basic Principles 2 of 45

Chapter 7 Exhibits

1. Abusive Tax Shelters

2. At-Risk Rules

3. Passive Activity Loss Rules

4. Disposing of Entire Passive Activity Interest

5. Inheriting a Passive Activity

6. Receiving a Passive Activity as a Gift

7. Rental Activities

8. Grouping Passive with Nonpassive Activities

9. Grouping Personal and Real Property Rentals

10. Limited Rental Period

11. Insignificant Rentals

12. Non-Exclusive Use During Defined Business Hours

13. Real Estate Professionals

14. Special $25,000 Allowance Under Code Sec. 469(i)

15. Rental Real Estate

16. Casualty and Theft Losses

17. Net Operating Losses—Rules for Individuals

18. Net Operating Losses for Individuals–Example

Chapter 7, Exhibit Contents

CCH Federal Taxation Basic Principles 3 of 45

Abusive Tax Shelters

Before 1987, a 50% or higher return on equity by high-income taxpayerswas not unusual given that

tax rates were high (e.g., the top tax rate from 1965 to 1981 was 70%) and

depreciation allowances were generous (e.g., 1981–1983 depreciation on office buildings could be computed using a 15-yearlife and the 175% declining-balance method; today, it is 39 years with the straight-line method).

Typical tax shelters once provided high returns without necessarily makinga before-tax profit.

Chapter 7, Exhibit 1a

CCH Federal Taxation Basic Principles 4 of 45

Abusive Tax Shelters

Example Before–1987 Tax Shelter

10 investors form "Pay-No-Tax," a limited partnership (LP), and each contributes $10,000.

The LP obtains a $900,000 nonrecourse loan from Easy Money S & L (a federally insured loan) and builds a "Class C" office building. Note: “nonrecourse” means the S & L would have no claims against the investors personally in the event of default. The S & L’s only avenue would be to foreclose on the property.

The building never exceeds 50% occupancy.

Chapter 7, Exhibit 1b

CCH Federal Taxation Basic Principles 5 of 45

Abusive Tax Shelters

At 50% occupancy, the annual cash flows appear as follows:

Description LPEach of the

10 Partners

(a) Rental income $ 70,000 $ 7,000

(b) Operating expenses (40,000) (4,000)

(c) Interest payments (90,000) (9,000)

(d) = (a) – (b) – ( c) Negative cash flow (60,000) (6,000)

(e) Depreciation (100,000) (10,000)

(f) = (d) – (e) Tax loss (160,000) (16,000)

(g) = (f) x 70% Tax benefit from loss (70% tax bracket from 1965 – 1981)

112,000 11,200

(h) = (d) + (g) Net cash [($60,000) + $112,000] $52,000 $ 5,200

(i) = (h) equity Annual return on equity 52% 52%

Chapter 7, Exhibit 1c

CCH Federal Taxation Basic Principles 6 of 45

Congress passed the Code Sec. 465 at-risk rules in 1976. However, the at-risk rules did very little to curb abusive tax shelters.

Effective January 1, 1987, the Code Sec. 469 passive activity loss rules were enacted, virtually eliminating most tax shelters.

Abusive Tax Shelters

Chapter 7, Exhibit 1d

CCH Federal Taxation Basic Principles 7 of 45

The at-risk rules prevent taxpayers from deducting losses in excess of basis (i.e., amounts at-risk).

Cash investment in an activity

+ Basis of other invested property in the activity

+ The activity's borrowings with investor personal guarantees or personal collateral. (Nonrecourse loans are also deemed “at-risk” if from “qualified” lenders.)

+ Income allocation

– Loss allocation, to the extent it “jumps hurdle 1”

– Distributions of cash or other property to investors at FMV

At-Risk Rules

Chapter 7, Exhibit 2a

CCH Federal Taxation Basic Principles 8 of 45

Qualified Nonrecourse Loans. Congress took the “bite” out of the at-risk rules by permitting “qualified” nonrecourse loans to be treated as “at-risk” under Code Sec. 465(b)(6) if they were secured by their activity's property. Generally, nonrecourse secured loans from S & Ls, banks, insurance companies, and federal, state, and local governments are considered to be at-risk.

At-Risk Rules

Chapter 7, Exhibit 2b

CCH Federal Taxation Basic Principles 9 of 45

Penalties for Abusive Tax Shelters. In 1982, Congress passed a law penalizing abusive tax shelters. The IRS, however, had difficulty detecting abusive tax shelters since they were often buried in complex partnership agreements.

At-Risk Rules

Chapter 7, Exhibit 2c

CCH Federal Taxation Basic Principles 10 of 45

Passive Activity Loss Rules

The PAL rules generally provide that all income and loss must be placed in one of three categories:

Active (losses are fully deductible to the extent of basis)

Passive (losses are deductible only against passive income, with some exceptions)

Portfolio (dividends, interest, royalties, etc.; interest expense is limited to net investment income)

Chapter 7, Exhibit 3a

CCH Federal Taxation Basic Principles 11 of 45

Effect of PAL Rules. The PAL rules eliminated most tax shelters effective January 1, 1987. Values that had been artificially inflated due to tax benefits plummeted, and the real estate industry and S & Ls collapsed during the next six years. Taxpayers paid hundreds of billions of dollars to replace federally insured deposits loaned out by the S & L’s and other institutions.

Passive Activity Loss Rules

Chapter 7, Exhibit 3b

CCH Federal Taxation Basic Principles 12 of 45

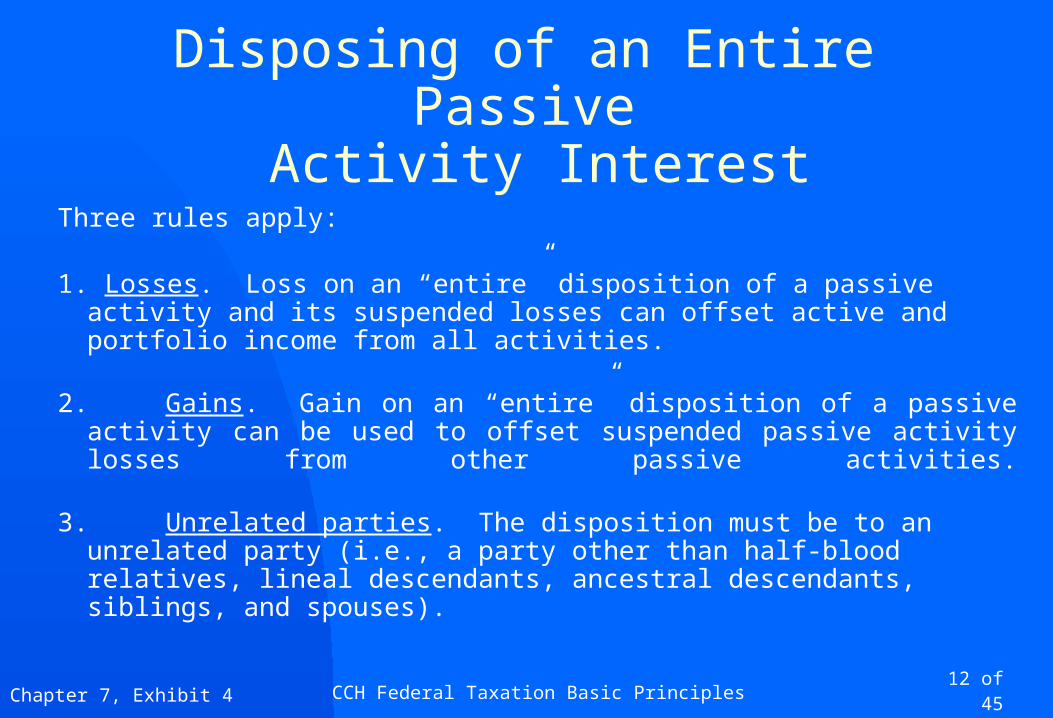

Disposing of an Entire Passive Activity Interest

Three rules apply:

1. Losses. Loss on an “entire” disposition of a passive activity and its suspended losses can offset active and portfolio income from all activities.

2. Gains. Gain on an “entire” disposition of a passive activity can be used to offset suspended passive activity losses from other passive activities.

3. Unrelated parties. The disposition must be to an unrelated party (i.e., a party other than half-blood relatives, lineal descendants, ancestral descendants, siblings, and spouses).

Chapter 7, Exhibit 4

CCH Federal Taxation Basic Principles 13 of 45

Inheriting a Passive ActivityFour rules apply:

1. Beneficiary's step-up basis. Beneficiary gets a step-up basis at fair market value (FMV) on the date of benefactor's death (or, if elected by executor, FMV six months after the date of death.)

2. Beneficiary's at-risk amount. The step-up basis becomes “at risk” to the beneficiary.

3. Decedent's passive loss deduction. In the decedent's final income tax return, suspended losses are deductible to the extent they exceed the “step-up” amount [i.e., to the extent they exceed (FMV at date of death - Adjusted Basis at date of death)].

4. No effect on beneficiary's basis. The beneficiary's step-up basis is not reduced by the decedent's passive loss deduction.

Chapter 7, Exhibit 5

CCH Federal Taxation Basic Principles 14 of 45

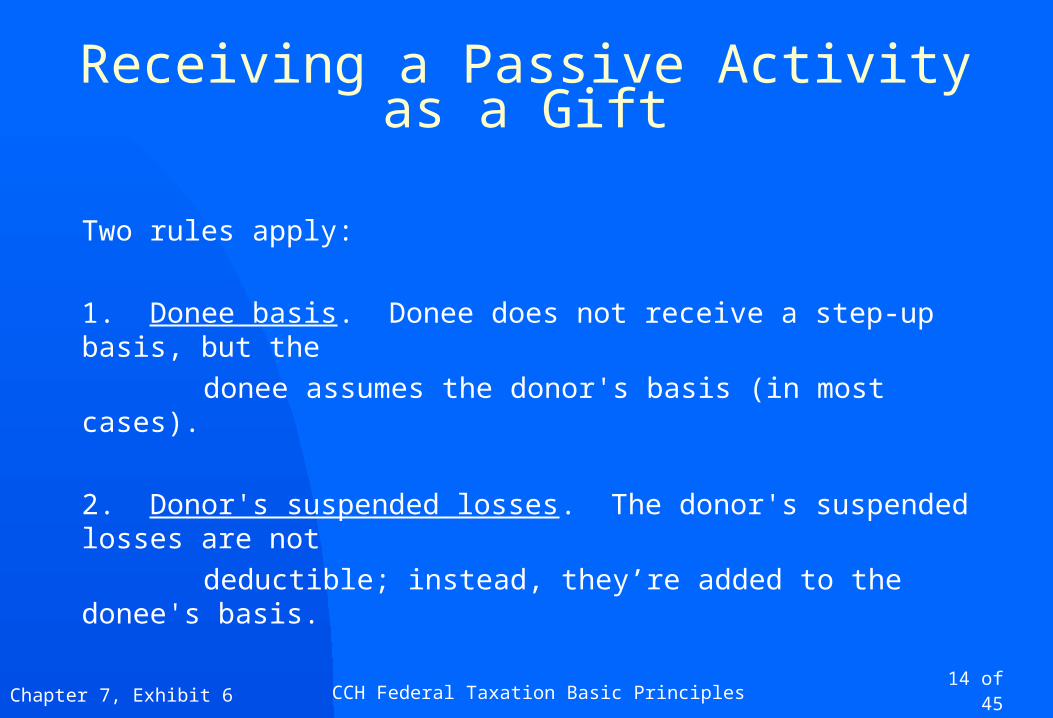

Receiving a Passive Activity as a Gift

Two rules apply:

1. Donee basis. Donee does not receive a step-up basis, but the

donee assumes the donor's basis (in most cases).

2. Donor's suspended losses. The donor's suspended losses are not

deductible; instead, they’re added to the donee's basis.

Chapter 7, Exhibit 6

CCH Federal Taxation Basic Principles 15 of 45

Rental Activities

Generally, rental activities are deemed to be passive without regard to material

participation. However, under the following situations, rental activities may receive

“active” loss treatment. (Note that in each situation, the taxpayer must still satisfy any

one of the seven material participation requirements.)

Grouping passive with nonpassive activities Grouping personal and real property rentals Limited rental periods Insignificant rentals Nonexclusive use during defined business hours Real estate professionals Special $25,000 allowance under Code Sec. 469(i)

Chapter 7, Exhibit 7

CCH Federal Taxation Basic Principles 16 of 45

Grouping Passive with Nonpassive Activities

A passive rental activity may be grouped with an active nonrental activity if the following two rules apply:

1. They are part of the same economic unit, i.e., control is common ownership is common, geographic location is the same, activities are interdependent, and types of businesses are similar.

Chapter 7, Exhibit 8a

CCH Federal Taxation Basic Principles 17 of 45

2. The rental revenue is 20% of the total revenue from both activities (e.g., subleasing a small portion of an inventory- storage warehouse). (Prop. Reg. §1.469-4(d).)

However, note that a disposition of merely the passive activity in this case does not qualify as the “disposition of an entire interest.”

Chapter 7, Exhibit 8b

Grouping Passive with Nonpassive Activities

CCH Federal Taxation Basic Principles 18 of 45

Grouping Personal and Real Property Rentals

The rental of personal property may be grouped with the rental of real property if the personal property is rented in connection with the real property (e.g., coin- operated washing machines in an apartment building.) (Prop. Reg. §1.469-4(e).)

Chapter 7, Exhibit 9

CCH Federal Taxation Basic Principles 19 of 45

Limited Rental Period

Under 8-day average rental. Average customer use is 7 days or less (e.g., hotel rooms, movie rentals).

Chapter 7, Exhibit 10a

CCH Federal Taxation Basic Principles 20 of 45

Limited Rental Period

8–30 days average rental plus significant services. Average customer use is 8 to 30 days and “significant” personal services are provided to the customers (e.g., computer leasing, automobile leasing).

Chapter 7, Exhibit 10b

CCH Federal Taxation Basic Principles 21 of 45

Limited Rental Period

Over 30-day average rental and extraordinary services. Average customer use is over 30 days and “extraordinary” personal services are provided to customers (e.g., lengthy hospitals stays).

Chapter 7, Exhibit 10c

CCH Federal Taxation Basic Principles 22 of 45

Insignificant Rentals

Gross rental income is less than 2% of the lesser of (1) fair market value of the rental asset or (2) the adjusted basis of the rental asset (e.g., renting a small portion of a vast timberland to a farmer)

Chapter 7, Exhibit 11

CCH Federal Taxation Basic Principles 23 of 45

Nonexclusive Use During Defined Business Hours

Property is available during defined business hours for nonexclusive use by the general public (e.g., operating a golf course available during prescribed business hours for nonexclusive use).

Chapter 7, Exhibit 12

CCH Federal Taxation Basic Principles 24 of 45

Real Estate Professionals

Over 750 hours a year are devoted to a real estate business, AND

Over 50% of the taxpayer's personal services for the year are devoted to a real estate business, AND One of the 7 material participation tests is satisfied.

Example: A full-time real estate agent owns and manages a rental house. Any losses from the rental house are nonpassive losses.

Chapter 7, Exhibit 13

CCH Federal Taxation Basic Principles 25 of 45

Special $25,000 Allowance UnderCode Sec. 469(i)

Up to $25,000 of losses from rental real estate activities may be deductible against nonpassive income. This $25,000 allowance is available for all filing statuses except married filing separately (the allowance is $12,500 if married filing separately and living apart).

Chapter 7, Exhibit 14a

CCH Federal Taxation Basic Principles 26 of 45

Special $25,000 Allowance Under Code Sec. 469(i)

The criteria for this special allowance are as follows:

1. AGI, ignoring passive activity loss limitations, must be less than $150,000 when

adjusted as follows:

+ IRA deduction

+ Passive activity loss in excess of passive activity income

– Social Security benefits that are includible (i.e., taxable)

2. The taxpayer must provide “active” participation (i.e., making “some” of the

management decisions). Material participation is not required.

3. The taxpayer must own at least 10% of the passive activity.

4. 50 cents of the special allowance is phased out for every $1 the adjusted AGI is over $100,000.

Chapter 7, Exhibit 14b

CCH Federal Taxation Basic Principles 27 of 45

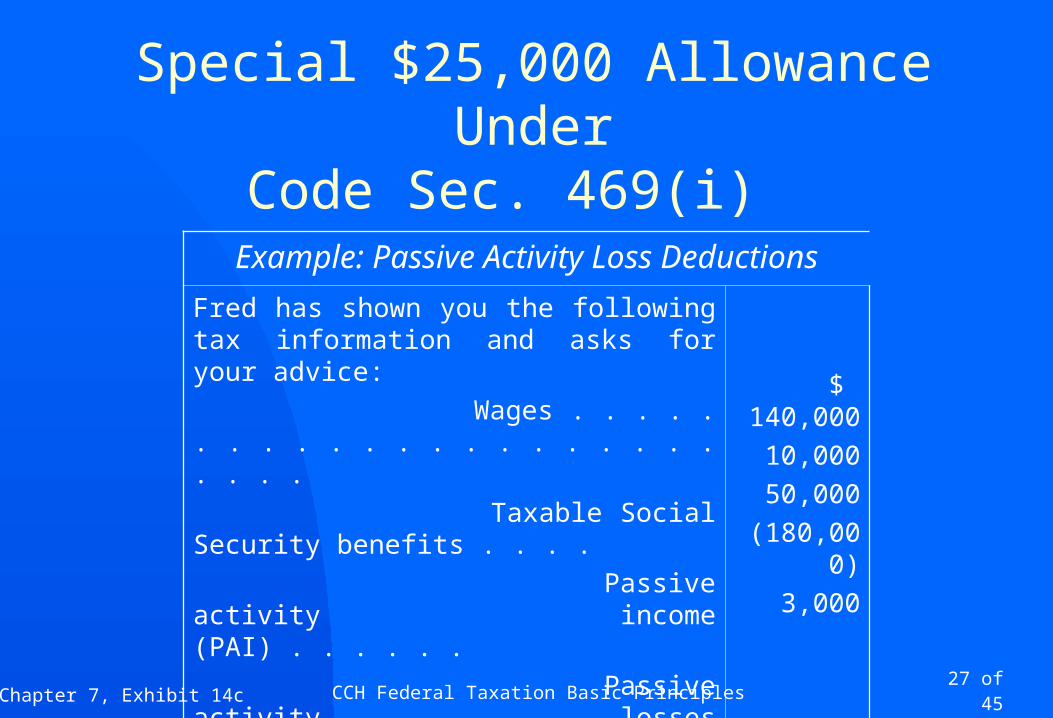

Example: Passive Activity Loss DeductionsFred has shown you the following tax information and asks for your advice:

Wages . . . . . . . . . . . . . . . . . . . . . . . . .

Taxable Social Security benefits . . . .

Passive activity income (PAI) . . . . . .

Passive activity losses (PAL) . . . . . . .

IRA deduction . . . . . . . . . . . . . . . . . .

How much of the passive activity losses are deductible?

How much are suspended?

$ 140,000

10,000

50,000

(180,000)

3,000

Special $25,000 Allowance UnderCode Sec. 469(i)

Chapter 7, Exhibit 14c

CCH Federal Taxation Basic Principles 28 of 45

Computation of adjusted AGI:

+

+

– =

AGI, ignoring PAL limitations

($140,000 + $10,000 +$50,000 - $180,000 - $3,000)

IRA deduction

PALs in excess of PAI, ($180,000 - $50,000)

Taxable Social Security benefits

Adjusted AGI

$ 17,000

3,000

130,000

10,000

$140,000

Chapter 7, Exhibit 14d

Special $25,000 Allowance Under Code Sec. 469(i)

CCH Federal Taxation Basic Principles 29 of 45

Special $25,000 Allowance UnderCode Sec. 469(i)

Chapter 7, Exhibit 14e

Computation of deductible and suspended PALs:

(a) PALs deductible due to offset with passive activity income $ 50,000

(b) PALs in excess of passive activity income ($180,000 - $50,000)

130,000

(c) Excess PAL allowance before phaseout 25,000

(d) Phaseout amount (($140,000 - $100,000) x 50%) 20,000

(e) = (c ) – (d) Allowance after phaseout ($25,000 - $20,000) 5,000

(f) = Lesser

of: (b) or (e)

PAL deduction under Code Sec. 469(i) (i.e., the “adjusted AGI” rules)

5,000

(g) = (a) + (f) Total PALs that are deductible ($50,000 + $5,000) $ 55,000

(h) = (b) – (f) PALs that are suspended to future years ($130,000 - $5,000) $125,000

CCH Federal Taxation Basic Principles 30 of 45

Rental Real EstateCategory Classification Rental Days Personal Days Tax Treatment

1 Personal use, but rental income and expenses are reportable. Loss deductions are not allowed.

> 14 days Greater than

the greater of

14 days or 10% of the rental days

Same as hobby and home office expense rules, that is : 100% of taxes, interest and casualty loss (subject to 10% AGI floor) are deductible on Schedule A. Out-of-pocket expenses and depreciation may not create a loss. Any portions deductible are prorated and treated as miscellaneous itemized deductions (subject to the 2% AGI floor).

Chapter 7, Exhibit 15a

CCH Federal Taxation Basic Principles 31 of 45

Rental Real Estate

Category Classification Rental Days Personal Days Tax Treatment

2 Personal use, but rental income and expenses are not reportable.

< 14 days N/A None (except taxes, interest, and casualty loss deductions are fully deductible).

Chapter 7, Exhibit 15b

CCH Federal Taxation Basic Principles 32 of 45

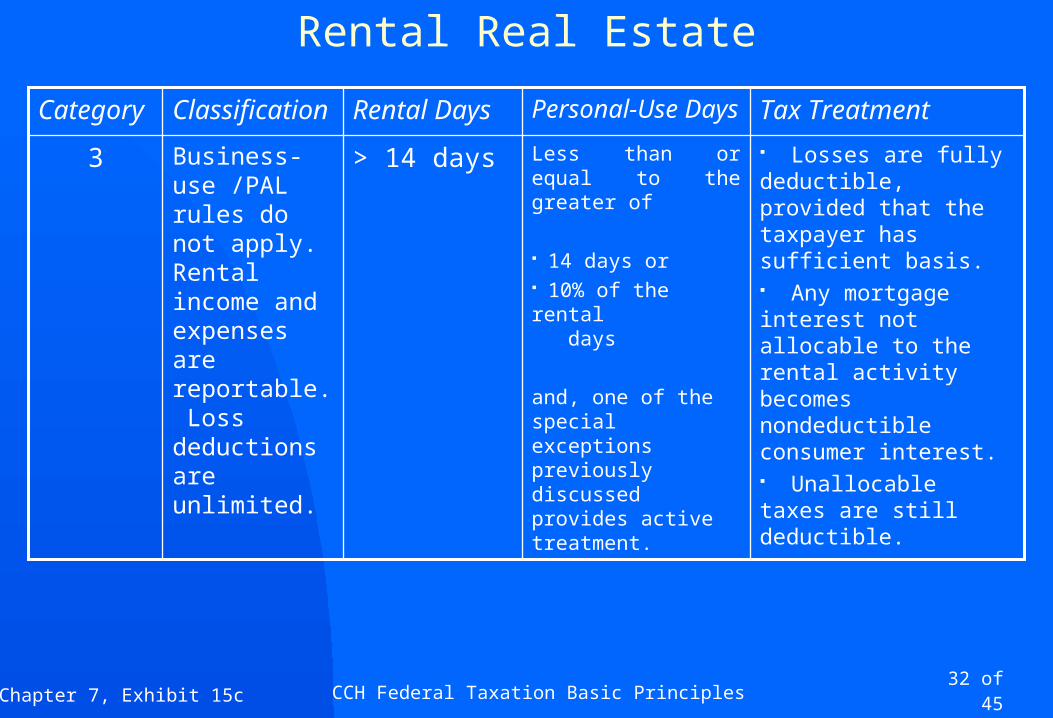

Rental Real Estate

Losses are fully deductible, provided that the taxpayer has sufficient basis. Any mortgage interest not allocable to the rental activity becomes nondeductible consumer interest. Unallocable taxes are still deductible.

Less than or equal to the greater of

14 days or 10% of the rental days

and, one of the special exceptions previously discussed provides active treatment.

> 14 daysBusiness-use /PAL rules do not apply. Rental income and expenses are reportable. Loss deductions are unlimited.

3

Tax TreatmentPersonal-Use DaysRental DaysClassificationCategory

Chapter 7, Exhibit 15c

CCH Federal Taxation Basic Principles 33 of 45

Casualty and Theft LossesComputing Casualty Loss Deductions

Explanation of abbreviations:

“Basis” = Cost minus accumulated depreciation (if any).

““ means “reduce” or “reduced.”

FMV = fair market value.

“IP” refers to insurance proceeds.

Gain or Loss from Casualty:

Nature of the (Personal-Use): (Business-Use):

Casualty: Reimbursements, less: Reimbursements, less:

If total destruction: Lower of basis or FMV Basis

If partial destruction: Lower of Basis or FMV Lower of Basis or FMV

If theft: Lower of basis or FMV Basis

Result: = “Realized” gain or loss = “Recognized” gain or loss

Chapter 7, Exhibit 16a

CCH Federal Taxation Basic Principles 34 of 45

Casualty and Theft Losses

If a personal use gain: = “Tentative” casualty gain.

Do not by $100 per event

If a personal use loss: Reduce by $100 per event to get:

“tentative” casualty loss.

Chapter 7, Exhibit 16b

CCH Federal Taxation Basic Principles 35 of 45

Casualty and Theft Losses

If all personal use tentative gains and losses net to a GAIN:

The result is a net casualty gain that gets capital gains treatment.

If all tentative gains and losses net to a LOSS:

by 10% AGI (applied once to all events’ combined net loss.) Any loss remaining is deductible “from” AGI

Chapter 7, Exhibit 16c

CCH Federal Taxation Basic Principles 36 of 45

Casualty and Theft Losses

Type of deduction “From” AGI “For” AGI

Type of gain Capital (Ch. 12) Sec 1231 (Ch. 12)

Chapter 7, Exhibit 16d

Personal Use Business Use

CCH Federal Taxation Basic Principles 37 of 45Chapter 7, Exhibit 16e

Casualty and Theft LossesType of Casualty Adjusted basis after casualty:

Complete destruction: N/A (No basis if asset is completely destroyed!)

Partial destruction + Basis immediately BEFORE partial destruction

- Insurance proceeds

- Deductible casualty loss (if any)

+ Casualty gain (if any)

= Basis immediately AFTER partial destruction

Theft N/A (No basis if asset is gone!)

Special Rule for Partial Destruction: If FMV < IP < Basis, then no gain or loss is reported. [Refer to Chapter 7 problem 48(b)].

CCH Federal Taxation Basic Principles 38 of 45

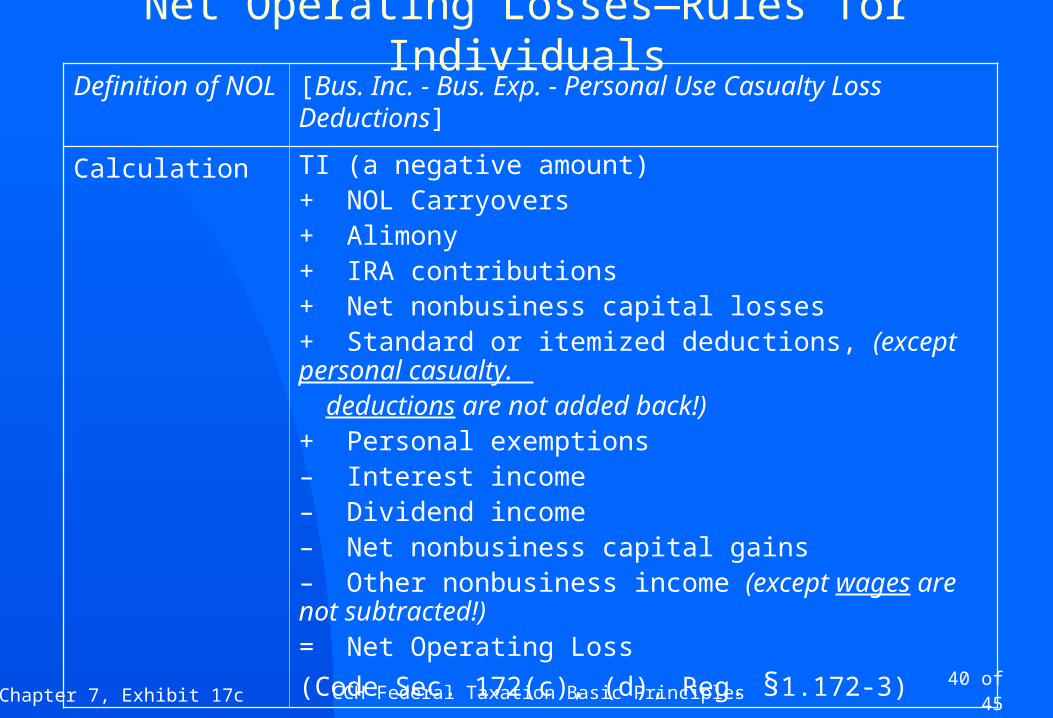

Net Operating Losses—Rules for Individuals

Definition of NOL [Bus. Inc. - Bus. Exp. - Personal Use Casualty Loss Deductions]

Carryovers:

NOLs from tax years beginning on or before 8/5/97:

NOLs other than from casualty deductions from tax years beginning after 8/5/97:

NOLs attributable to personal-use casualty losses:

3 years back, 15 years forward

2 years back, 20 years forward

3 years back, 15 years forward

Chapter 7, Exhibit 17a

CCH Federal Taxation Basic Principles 39 of 45

Definition of NOL [Bus. Inc. - Bus. Exp. - Personal Use Casualty Loss Deductions]

If carried back: The earliest year’s TI is recomputed, & TP files for a refund with an amended

return. Reg. §1.172-5(b)(1)

If carried forward: Deduction for AGI in a subsequent year.

Election: May elect to forego carrybacks. This election must be made when the return reporting an NOL is timely made. Code Sec. 172(b)(3)

Chapter 7, Exhibit 17b

Net Operating Losses—Rules for Individuals

CCH Federal Taxation Basic Principles 40 of 45

Definition of NOL [Bus. Inc. - Bus. Exp. - Personal Use Casualty Loss Deductions]

Calculation TI (a negative amount)+ NOL Carryovers+ Alimony+ IRA contributions+ Net nonbusiness capital losses+ Standard or itemized deductions, (except personal casualty. deductions are not added back!)+ Personal exemptions– Interest income– Dividend income– Net nonbusiness capital gains– Other nonbusiness income (except wages are not subtracted!)= Net Operating Loss

(Code Sec. 172(c), (d), Reg. §1.172-3)

Net Operating Losses—Rules for Individuals

Chapter 7, Exhibit 17c

CCH Federal Taxation Basic Principles 41 of 45

Definition of NOL [Bus. Inc. - Bus. Exp. - Personal Use Casualty Loss Deductions]

How much of an NOL can be used to offset prior year taxable income?

The amount of an NOL that can be carried back to a prior year is limited to modified taxable income (“MTI”). MTI is computed as follows:

+ Taxable income per prior-year return

+ Personal & dependency exemptions per prior-year return;

+ Excess capital losses per prior-yr. return;

+ Adjustment to itemized deductions claimed in prior year that were based on and limited by AGI. This adjustment is necessitated by the capital loss adjustment above, which results in increased AGI. Charitable deductions MUST NOT be adjusted.

= Modified taxable income (“MTI”)

(Reg. §1.172-5)

Net Operating Losses—Rules for Individuals

Chapter 7, Exhibit 17d

CCH Federal Taxation Basic Principles 42 of 45

Definition of NOL [Bus. Inc. - Bus. Exp. - Personal Use Casualty Loss Deductions]

How is the tax refund determined?

After NOLs are used to offset prior-year MTI, taxes are recomputed based on MTI less the NOL. The tax refund is the difference between

(a) Taxes per the prior-year return, and

(b) The recomputed tax for the prior year.

Net Operating Losses—Rules for Individuals

Chapter 7, Exhibit 17e

CCH Federal Taxation Basic Principles 43 of 45Chapter 7, Exhibit 18a

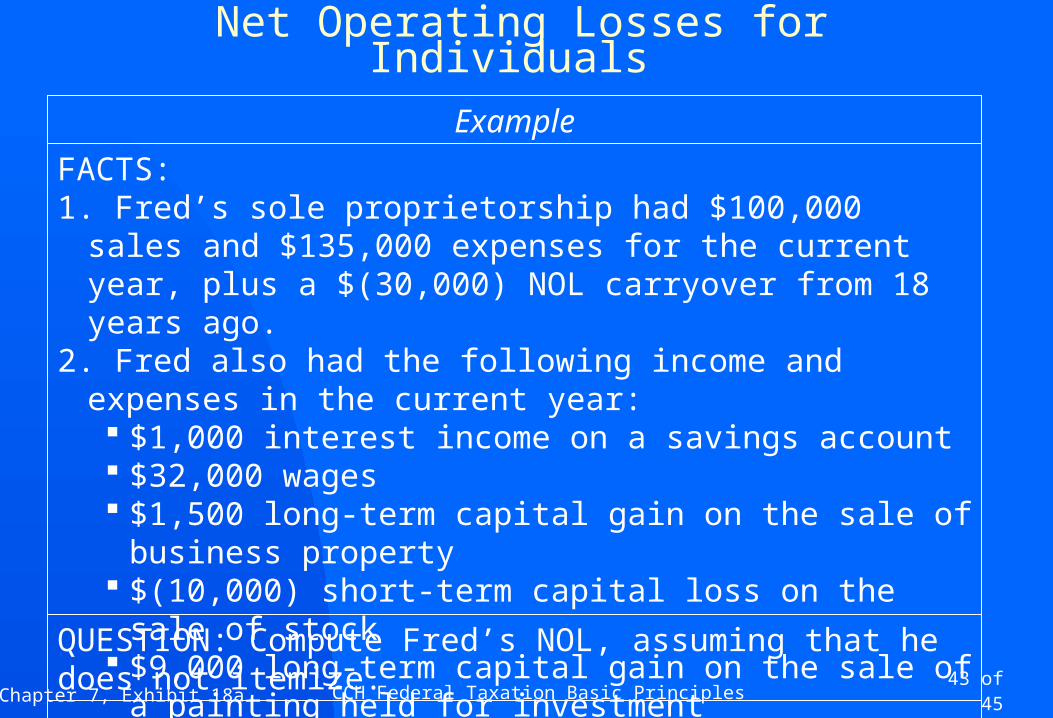

Net Operating Losses for Individuals

FACTS:1. Fred’s sole proprietorship had $100,000 sales and $135,000

expenses for the current year, plus a $(30,000) NOL carryover from 18 years ago.

2. Fred also had the following income and expenses in the current year: $1,000 interest income on a savings account $32,000 wages $1,500 long-term capital gain on the sale of business property $(10,000) short-term capital loss on the sale of stock $9,000 long-term capital gain on the sale of a painting held for

investment $(6,000) alimony payments

QUESTION: Compute Fred’s NOL, assuming that he does not itemize.

Example

CCH Federal Taxation Basic Principles 44 of 45

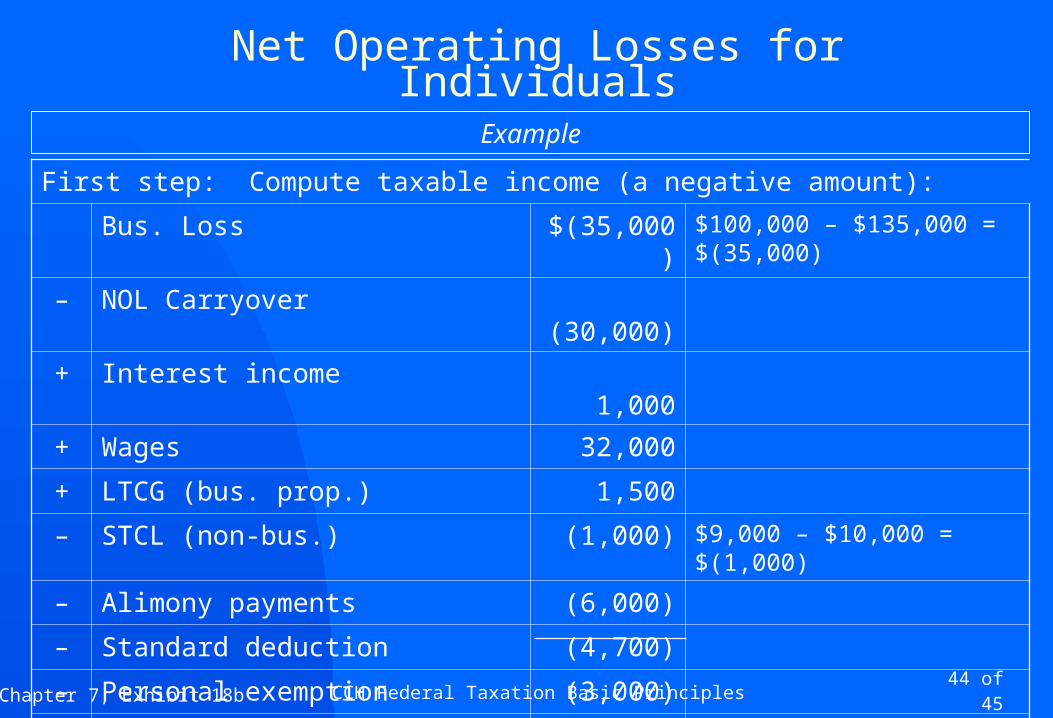

First step: Compute taxable income (a negative amount):

Bus. Loss $(35,000) $100,000 – $135,000 = $(35,000)

– NOL Carryover (30,000)

+ Interest income 1,000

+ Wages 32,000

+ LTCG (bus. prop.) 1,500

– STCL (non-bus.) (1,000) $9,000 – $10,000 = $(1,000)

– Alimony payments (6,000)

– Standard deduction (4,700)

– Personal exemption (3,000)

= Taxable income (45,200)

Net Operating Losses for Individuals

Chapter 7, Exhibit 18b

Example

CCH Federal Taxation Basic Principles 45 of 45

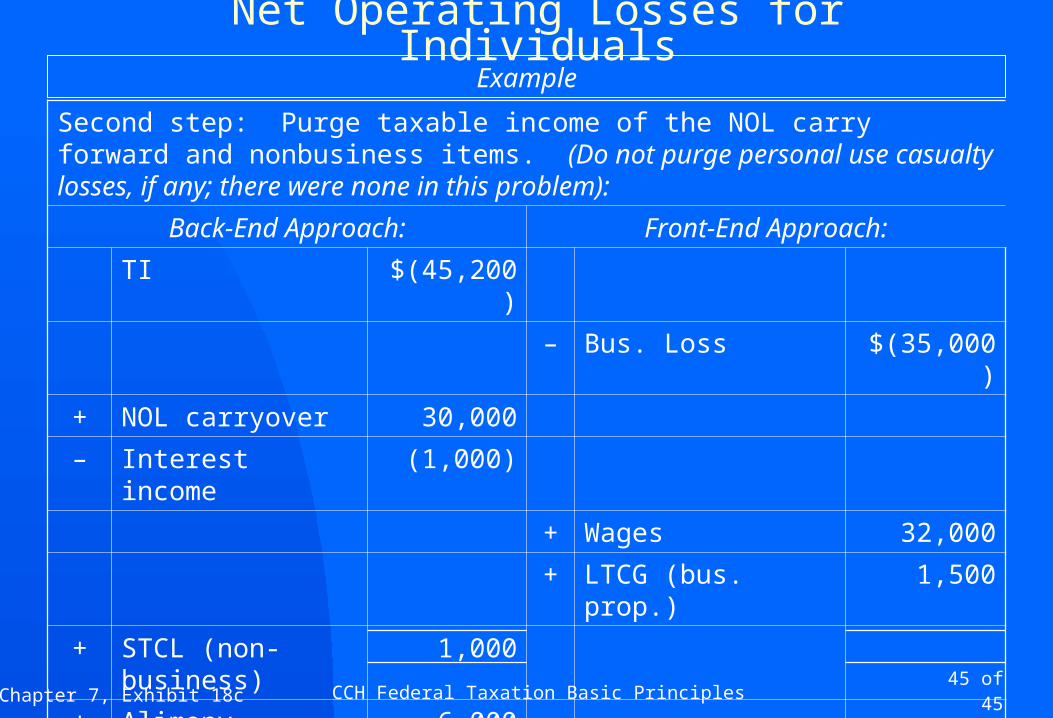

Second step: Purge taxable income of the NOL carry forward and nonbusiness items. (Do not purge personal use casualty losses, if any; there were none in this problem):

Back-End Approach: Front-End Approach:

TI $(45,200)

– Bus. Loss $(35,000)

+ NOL carryover 30,000

– Interest income (1,000)

+ Wages 32,000

+ LTCG (bus. prop.) 1,500

+ STCL (non-business) 1,000

+ Alimony payments 6,000

+ Standard deduction 4,700

+ Personal exemption 3,000

= Net operating loss (1,500) = Net oper. loss (1,500)

Chapter 7, Exhibit 18c

Net Operating Losses for IndividualsExample