Embed Size (px)

Citation preview

CCH Federal TaxationComprehensive Topics

Chapter 18Accumulated Earning and

Personal Holding Company Taxes

©2005, CCH INCORPORATED4025 W. Peterson Ave.Chicago, IL 60646-6085800 248 3248http://tax.cchgroup.com

CCH Federal Taxation Comprehensive Topics 2 of 21

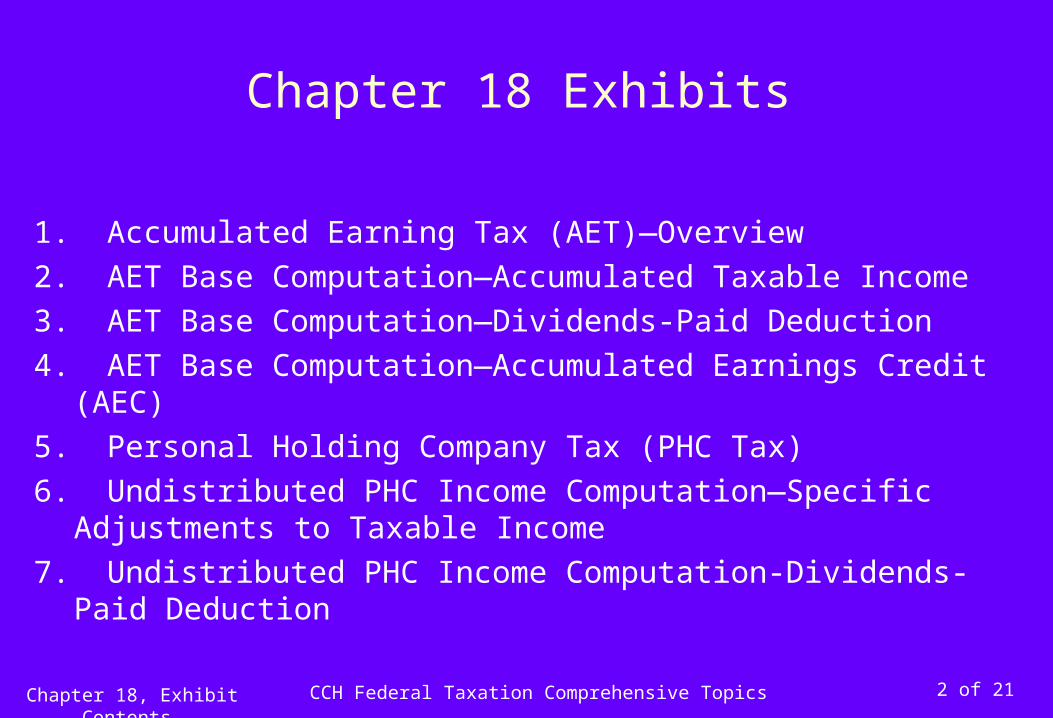

Chapter 18 Exhibits

Chapter 18, Exhibit Contents

1. Accumulated Earning Tax (AET)—Overview

2. AET Base Computation—Accumulated Taxable Income

3. AET Base Computation—Dividends-Paid Deduction

4. AET Base Computation—Accumulated Earnings Credit (AEC)

5. Personal Holding Company Tax (PHC Tax)

6. Undistributed PHC Income Computation—Specific Adjustments to Taxable Income

7. Undistributed PHC Income Computation-Dividends-Paid Deduction

CCH Federal Taxation Comprehensive Topics 3 of 21

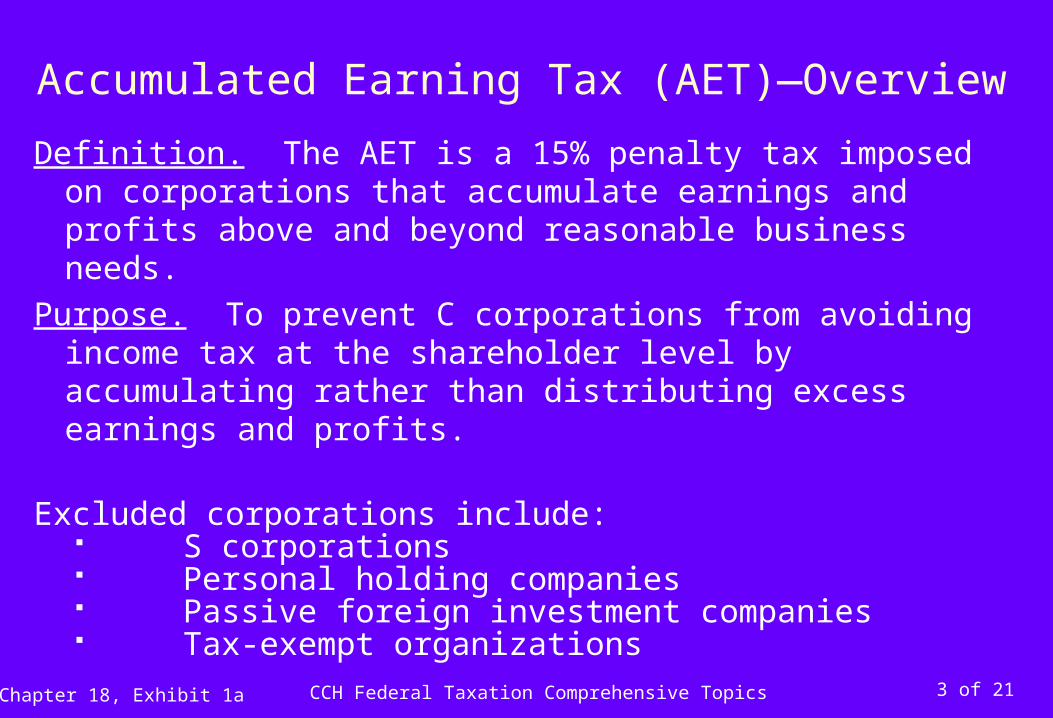

Accumulated Earning Tax (AET)—Overview

Definition. The AET is a 15% penalty tax imposed on corporations that accumulate earnings and profits above and beyond reasonable business needs.

Purpose. To prevent C corporations from avoiding income tax at the shareholder level by accumulating rather than distributing excess earnings and profits.

Excluded corporations include: S corporations Personal holding companies Passive foreign investment companies Tax-exempt organizations

Chapter 18, Exhibit 1a

CCH Federal Taxation Comprehensive Topics 4 of 21

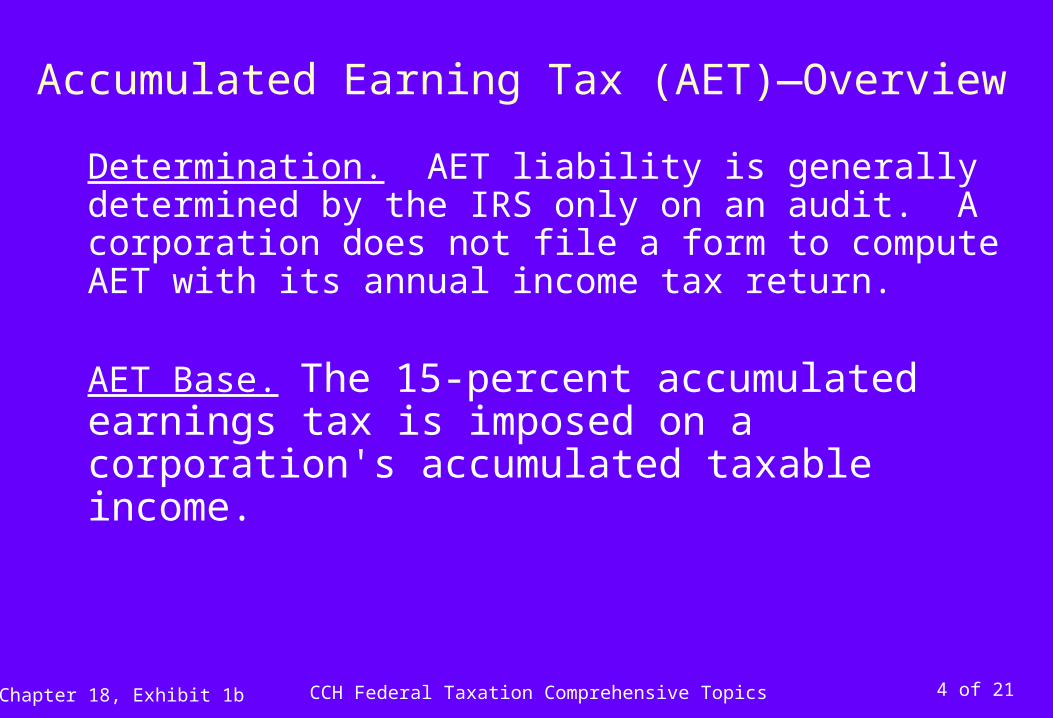

Determination. AET liability is generally determined by the IRS only on an audit. A corporation does not file a form to compute AET with its annual income tax return.

AET Base. The 15-percent accumulated earnings tax is imposed on a corporation's accumulated taxable income.

Accumulated Earning Tax (AET)—Overview

Chapter 18, Exhibit 1b

CCH Federal Taxation Comprehensive Topics 5 of 21

AET Base Computation—Accumulated Taxable Income

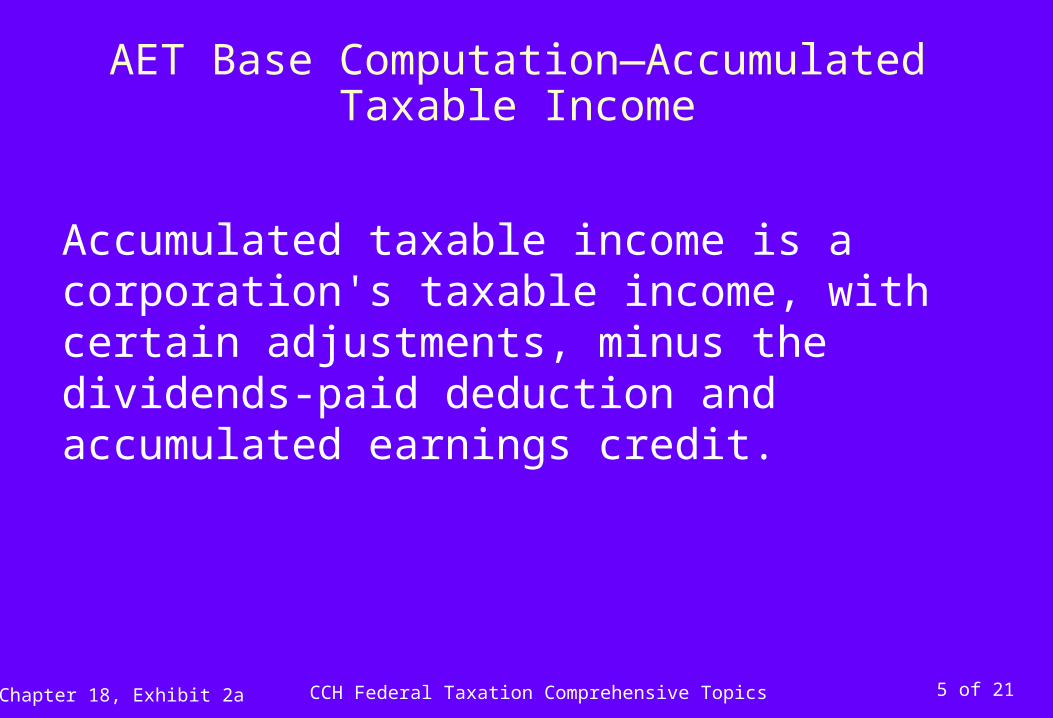

Accumulated taxable income is a corporation's taxable income, with certain adjustments, minus the dividends-paid deduction and accumulated earnings credit.

Chapter 18, Exhibit 2a

CCH Federal Taxation Comprehensive Topics 6 of 21

AET Base Computation—Accumulated Taxable Income

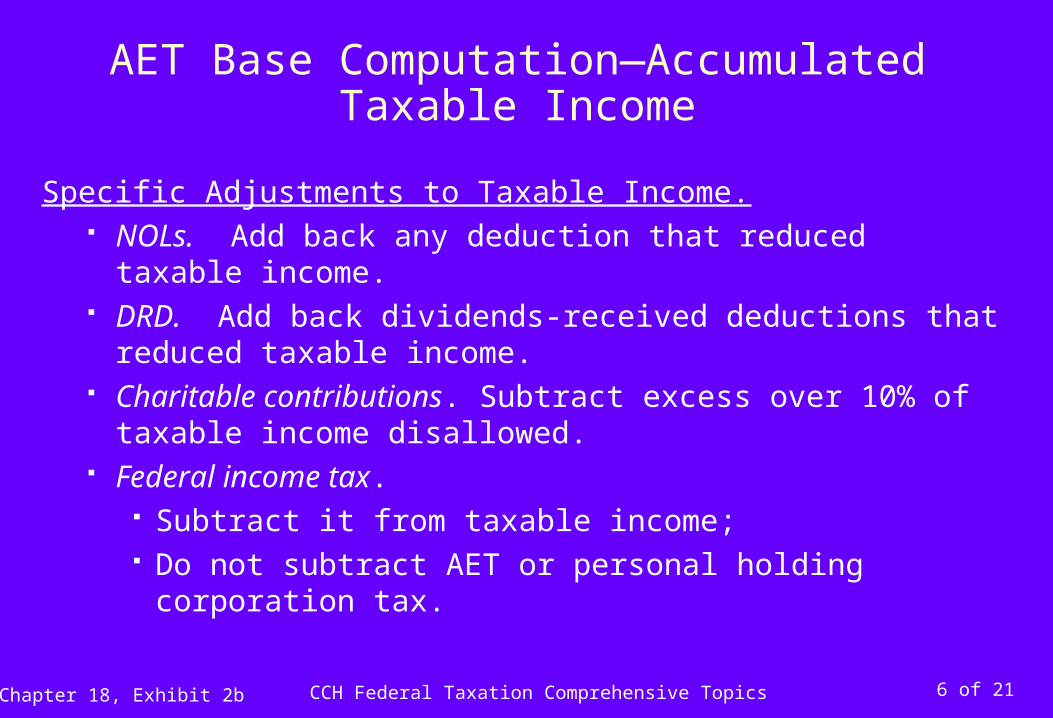

Specific Adjustments to Taxable Income. NOLs. Add back any deduction that reduced taxable income. DRD. Add back dividends-received deductions that reduced taxable

income. Charitable contributions. Subtract excess over 10% of taxable

income disallowed. Federal income tax.

Subtract it from taxable income; Do not subtract AET or personal holding corporation tax.

Chapter 18, Exhibit 2b

CCH Federal Taxation Comprehensive Topics 7 of 21

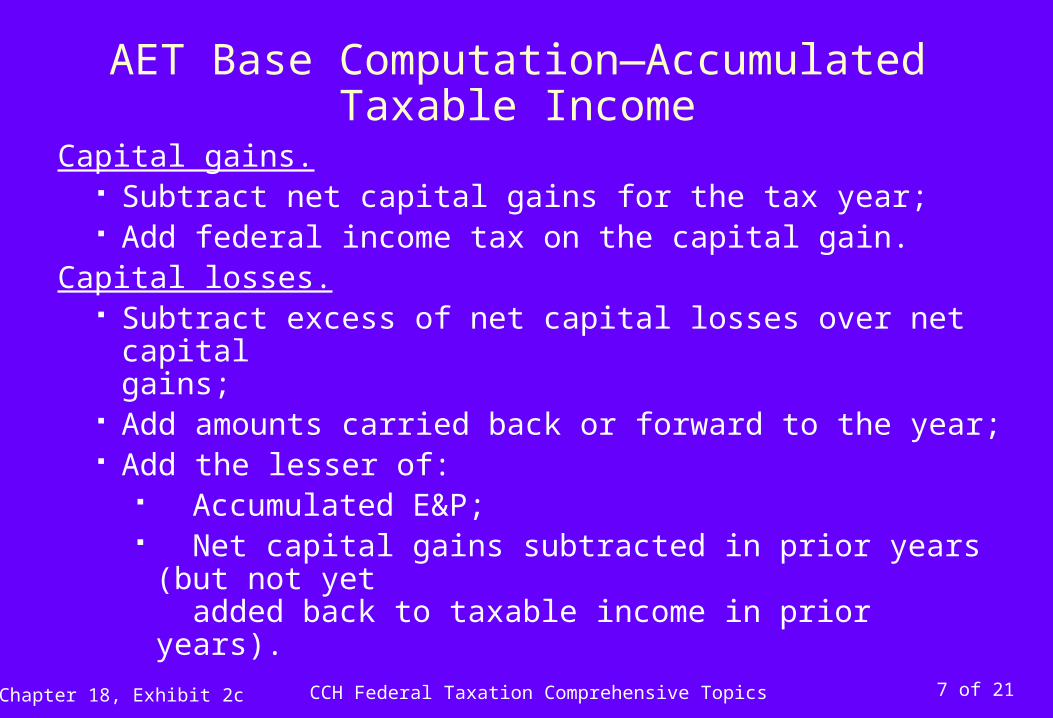

AET Base Computation—Accumulated Taxable Income

Capital gains. Subtract net capital gains for the tax year; Add federal income tax on the capital gain.

Capital losses. Subtract excess of net capital losses over net capital

gains; Add amounts carried back or forward to the year; Add the lesser of:

Accumulated E&P; Net capital gains subtracted in prior years (but not yet

added back to taxable income in prior years).

Chapter 18, Exhibit 2c

CCH Federal Taxation Comprehensive Topics 8 of 21

AET Base Computation—Dividends-Paid Deduction

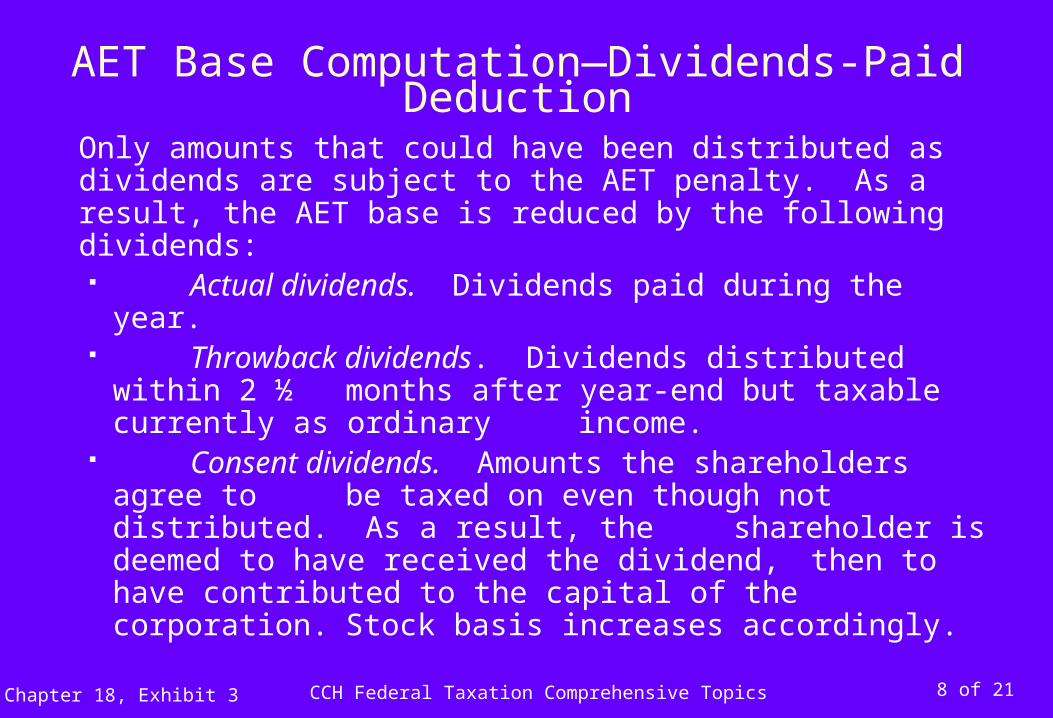

Only amounts that could have been distributed as dividends are subject to the AET penalty. As a result, the AET base is reduced by the following dividends: Actual dividends. Dividends paid during the year. Throwback dividends. Dividends distributed

within 2 ½ months after year-end but taxable currently as ordinary income.

Consent dividends. Amounts the shareholders agree to be taxed on even though not distributed. As a result, the shareholder is deemed to have received the dividend, then to have contributed to the capital of the corporation. Stock basis increases accordingly.

Chapter 18, Exhibit 3

CCH Federal Taxation Comprehensive Topics 9 of 21

AET Base Computation—Accumulated Earnings Credit (AEC)

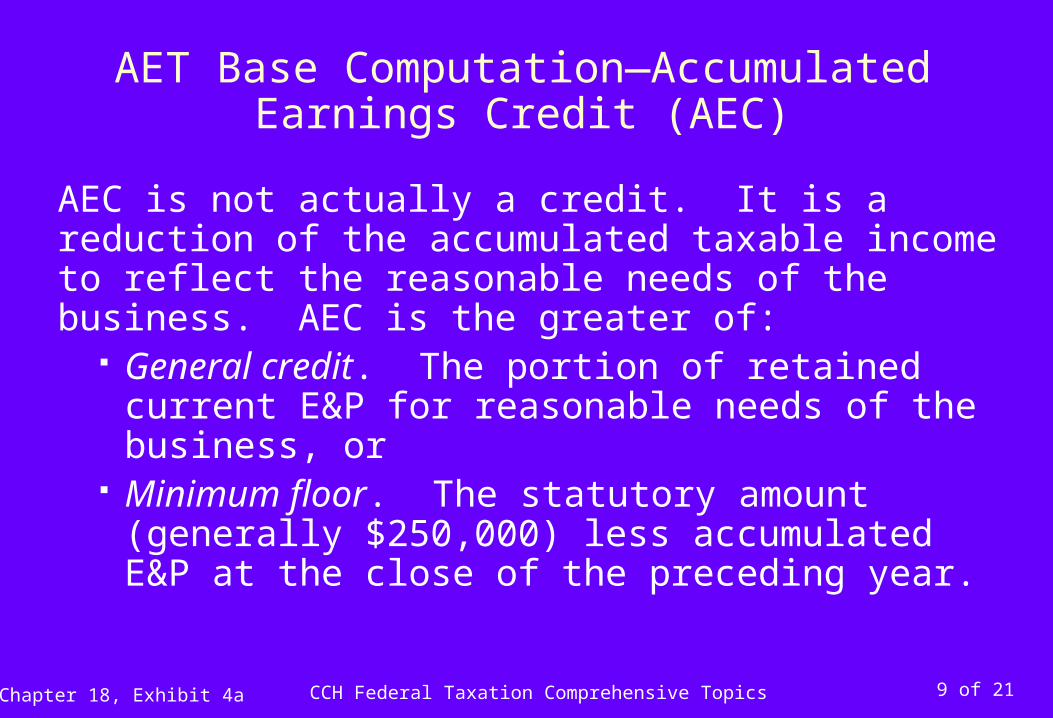

AEC is not actually a credit. It is a reduction of the accumulated taxable income to reflect the reasonable needs of the business. AEC is the greater of:

General credit. The portion of retained current E&P for reasonable needs of the business, or

Minimum floor. The statutory amount (generally $250,000) less accumulated E&P at the close of the preceding year.

Chapter 18, Exhibit 4a

CCH Federal Taxation Comprehensive Topics 10 of 21

AET Base Computation—Accumulated Earnings Credit (AEC)

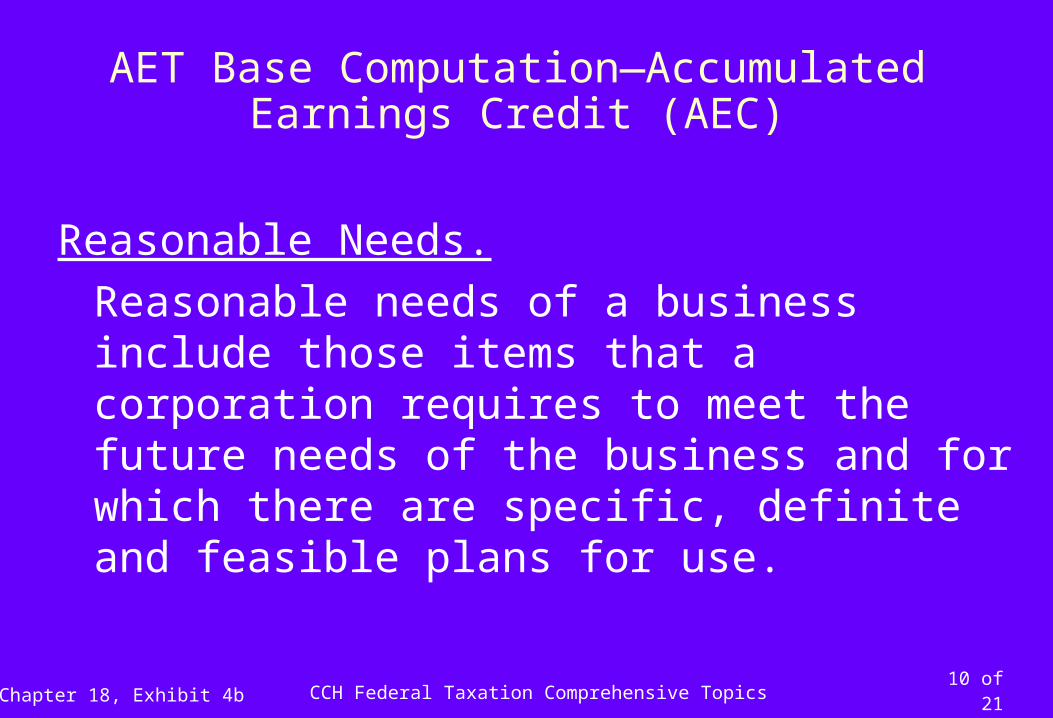

Reasonable Needs.

Reasonable needs of a business include those items that a corporation requires to meet the future needs of the business and for which there are specific, definite and feasible plans for use.

Chapter 18, Exhibit 4b

CCH Federal Taxation Comprehensive Topics 11 of 21

AET Base Computation—Accumulated Earnings Credit (AEC)

Reasonable needs include: Working capital Raw material purchases Equipment updates Expansion of production facilities Retirement of business debt Redemption of stock from a deceased shareholder’s estate Reserves for product liability Realistic business contingencies Acquiring a related business Investments or loans to key suppliers or customers

Chapter 18, Exhibit 4c

CCH Federal Taxation Comprehensive Topics 12 of 21

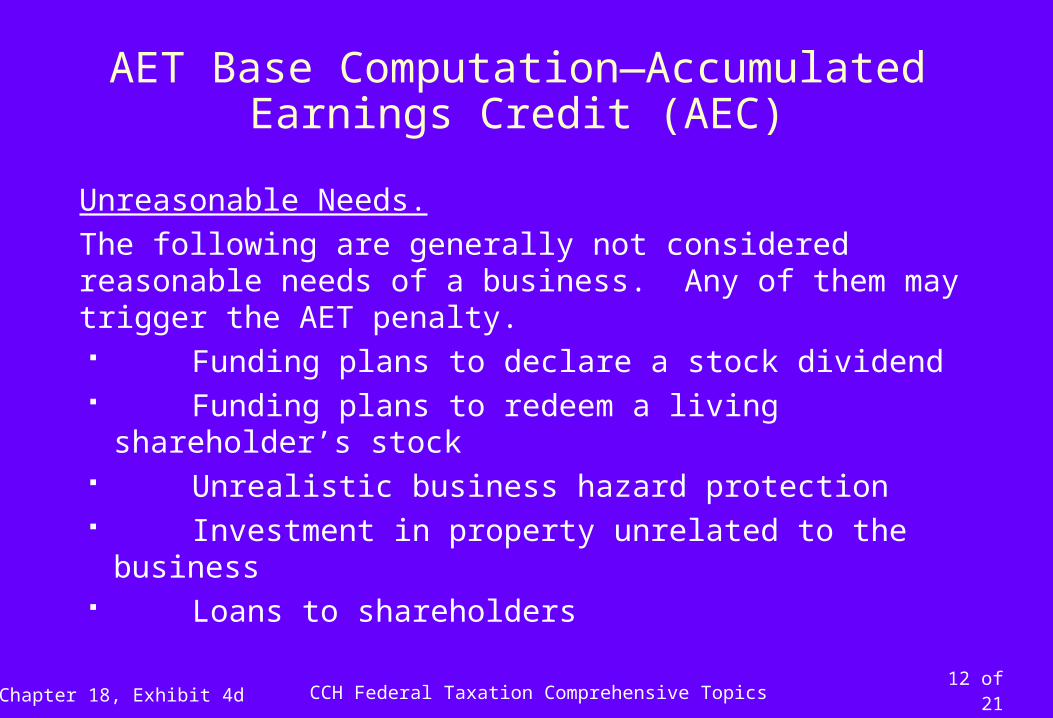

AET Base Computation—Accumulated Earnings Credit (AEC)

Unreasonable Needs.

The following are generally not considered reasonable needs of a business. Any of them may trigger the AET penalty. Funding plans to declare a stock dividend Funding plans to redeem a living shareholder’s stock Unrealistic business hazard protection Investment in property unrelated to the business Loans to shareholders

Chapter 18, Exhibit 4d

CCH Federal Taxation Comprehensive Topics 13 of 21

Personal Holding Company Tax (PHC Tax)

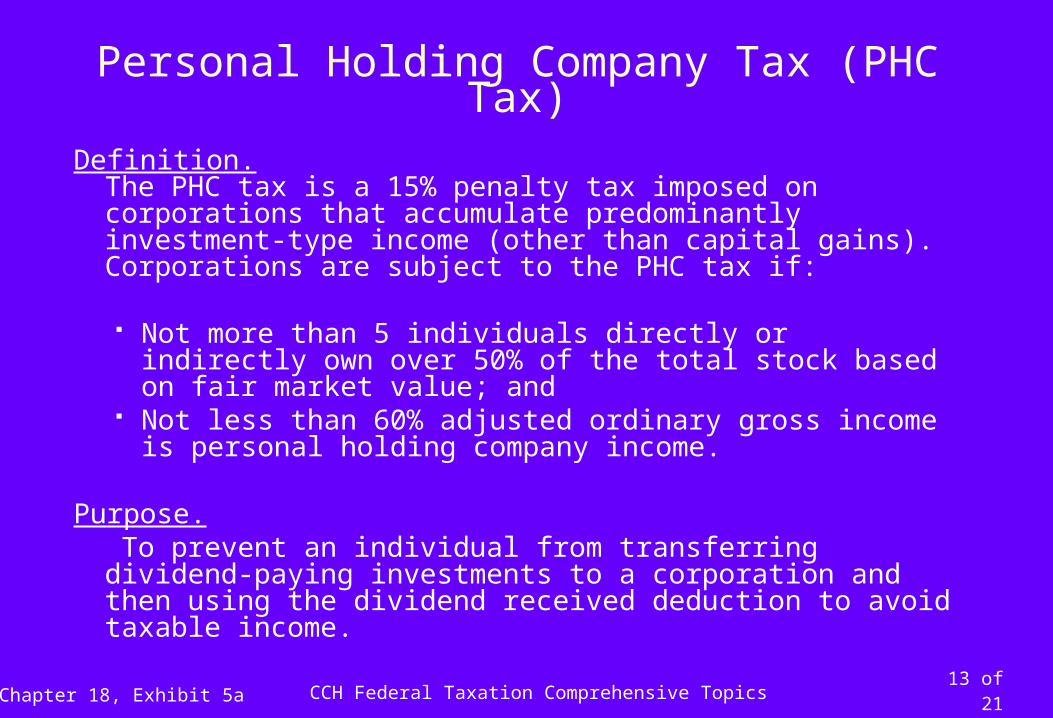

Definition.The PHC tax is a 15% penalty tax imposed on corporations that accumulate predominantly investment-type income (other than capital gains). Corporations are subject to the PHC tax if:

Not more than 5 individuals directly or indirectly own over 50% of the total stock based on fair market value; and

Not less than 60% adjusted ordinary gross income is personal holding company income.

Purpose. To prevent an individual from transferring dividend-paying investments to a corporation and then using the dividend received deduction to avoid taxable income.

Chapter 18, Exhibit 5a

CCH Federal Taxation Comprehensive Topics 14 of 21

Personal Holding Company Tax (PHC Tax)

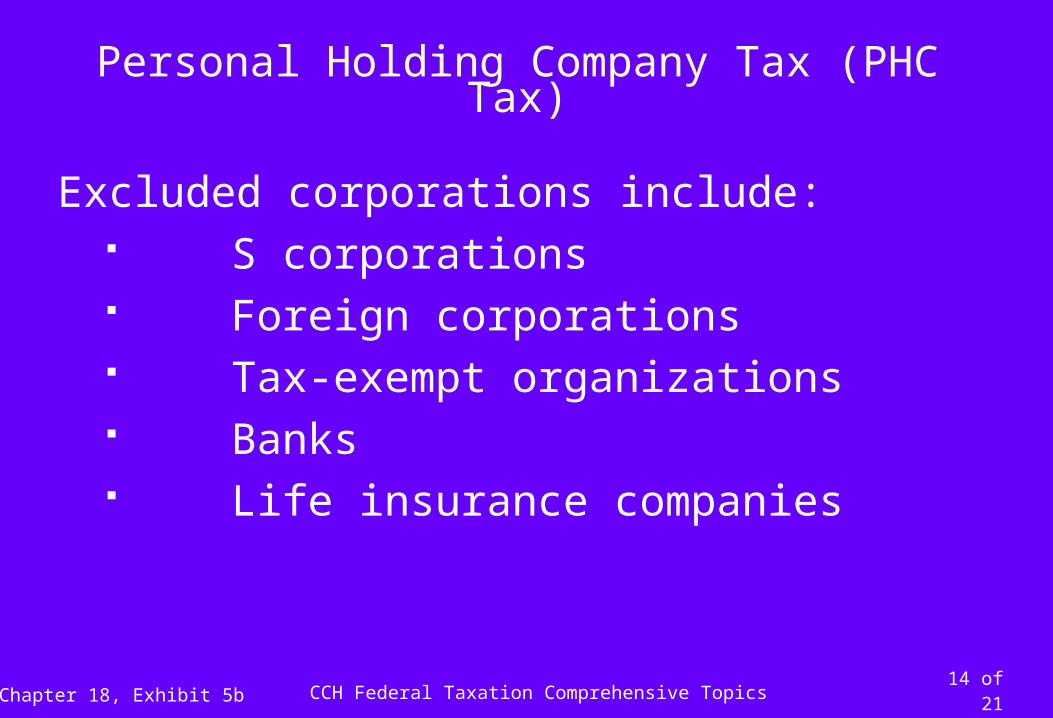

Excluded corporations include: S corporations Foreign corporations Tax-exempt organizations Banks Life insurance companies

Chapter 18, Exhibit 5b

CCH Federal Taxation Comprehensive Topics 15 of 21

Personal Holding Company Tax (PHC Tax)

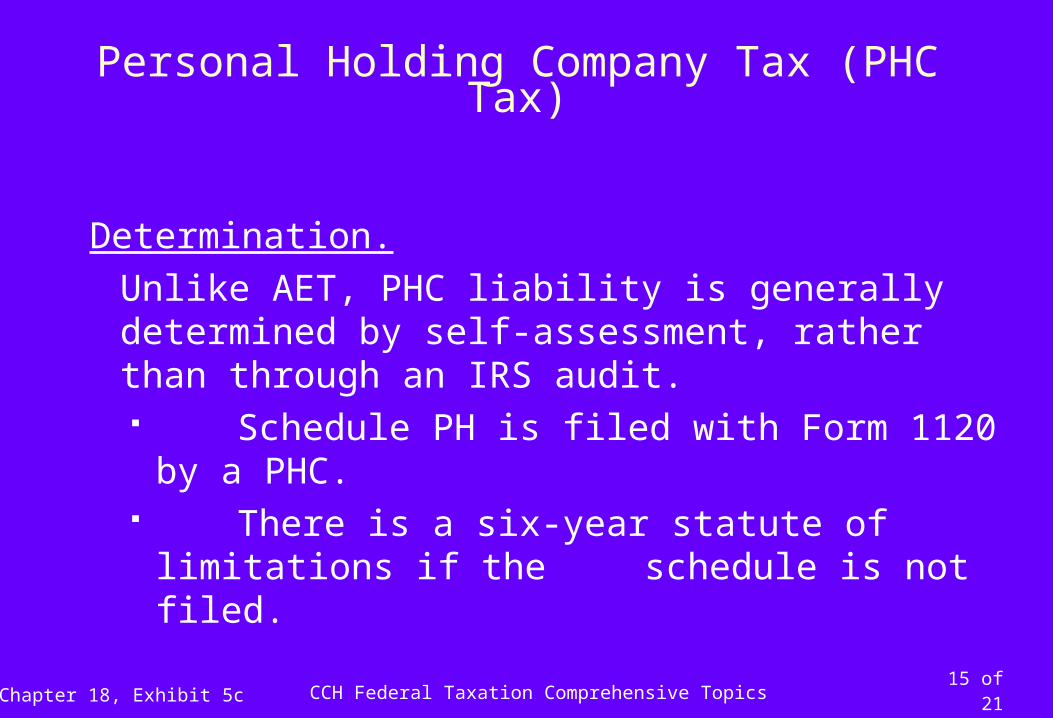

Determination.

Unlike AET, PHC liability is generally determined by self-assessment, rather than through an IRS audit. Schedule PH is filed with Form 1120 by a

PHC. There is a six-year statute of limitations if

the schedule is not filed.

Chapter 18, Exhibit 5c

CCH Federal Taxation Comprehensive Topics 16 of 21

Personal Holding Company Tax (PHC Tax)

Undistributed Personal Holding Company Income (UPHCI).

The PHC tax is 15% of UPHCI. UPHCI is taxable income, net of specific adjustments and a dividend-paid deduction.

Chapter 18, Exhibit 5d

CCH Federal Taxation Comprehensive Topics 17 of 21

Undistributed PHC Income Computation—Specific Adjustments to Taxable Income

UPHCI is taxable income, net of specific adjustments

and a dividends-paid deduction.

Chapter 18, Exhibit 6a

CCH Federal Taxation Comprehensive Topics 18 of 21

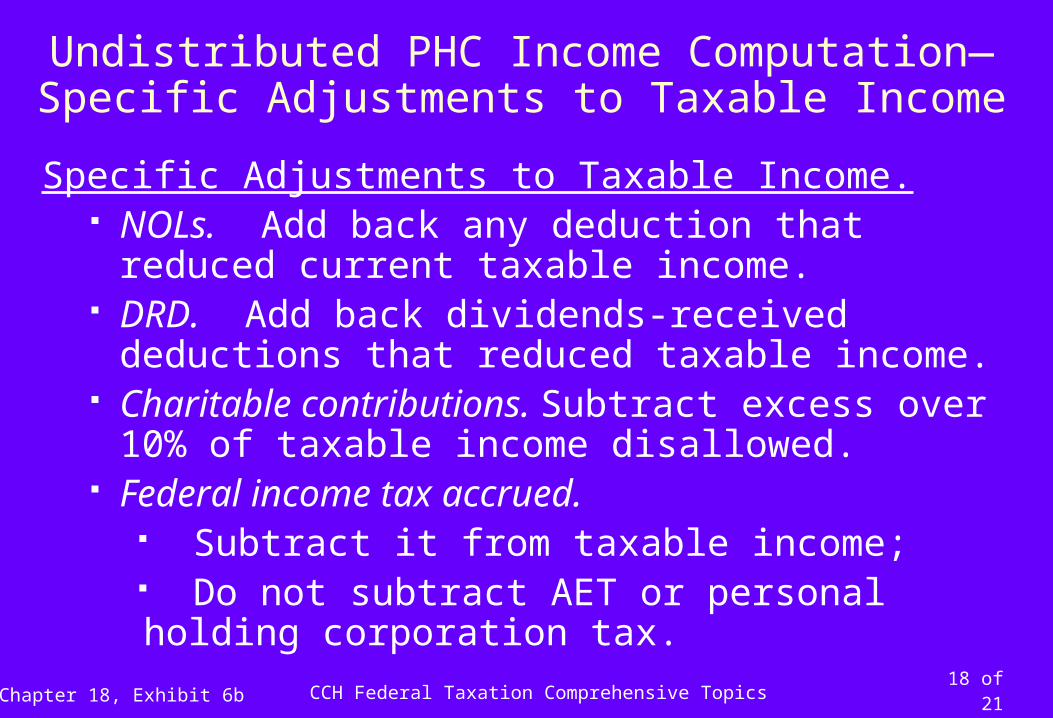

Undistributed PHC Income Computation—Specific Adjustments to Taxable Income

Specific Adjustments to Taxable Income. NOLs. Add back any deduction that reduced current

taxable income. DRD. Add back dividends-received deductions that

reduced taxable income. Charitable contributions. Subtract excess over 10% of

taxable income disallowed. Federal income tax accrued.

Subtract it from taxable income; Do not subtract AET or personal holding corporation tax.

Chapter 18, Exhibit 6b

CCH Federal Taxation Comprehensive Topics 19 of 21

Undistributed PHC Income Computation—Specific Adjustments to Taxable Income

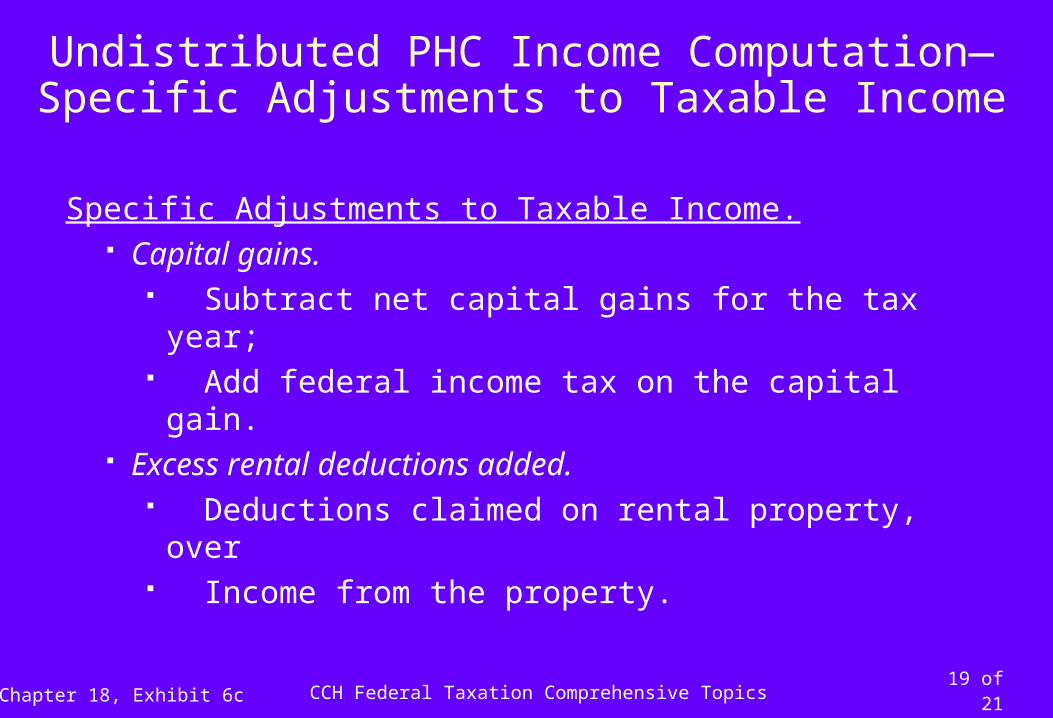

Specific Adjustments to Taxable Income. Capital gains.

Subtract net capital gains for the tax year; Add federal income tax on the capital gain.

Excess rental deductions added. Deductions claimed on rental property, over Income from the property.

Chapter 18, Exhibit 6c

CCH Federal Taxation Comprehensive Topics 20 of 21

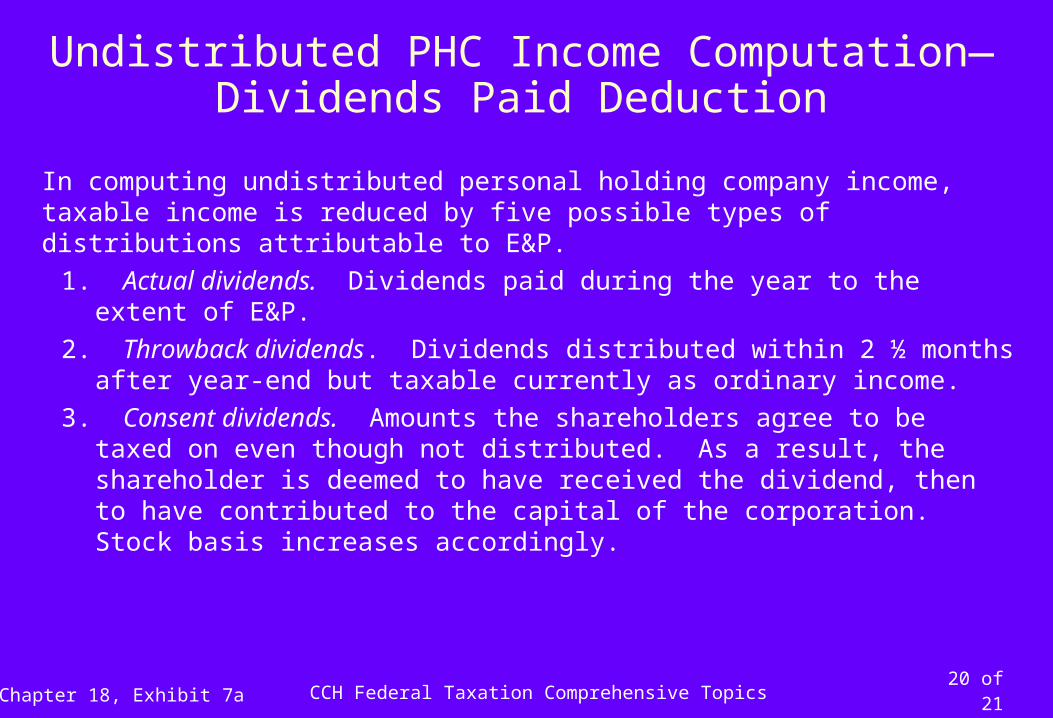

Undistributed PHC Income Computation—Dividends Paid Deduction

In computing undistributed personal holding company income, taxable income is reduced by five possible types of distributions attributable to E&P.

1. Actual dividends. Dividends paid during the year to the extent of E&P.

2. Throwback dividends. Dividends distributed within 2 ½ months after year-end but taxable currently as ordinary income.

3. Consent dividends. Amounts the shareholders agree to be taxed on even though not distributed. As a result, the shareholder is deemed to have received the dividend, then to have contributed to the capital of the corporation. Stock basis increases accordingly.

Chapter 18, Exhibit 7a

CCH Federal Taxation Comprehensive Topics 21 of 21

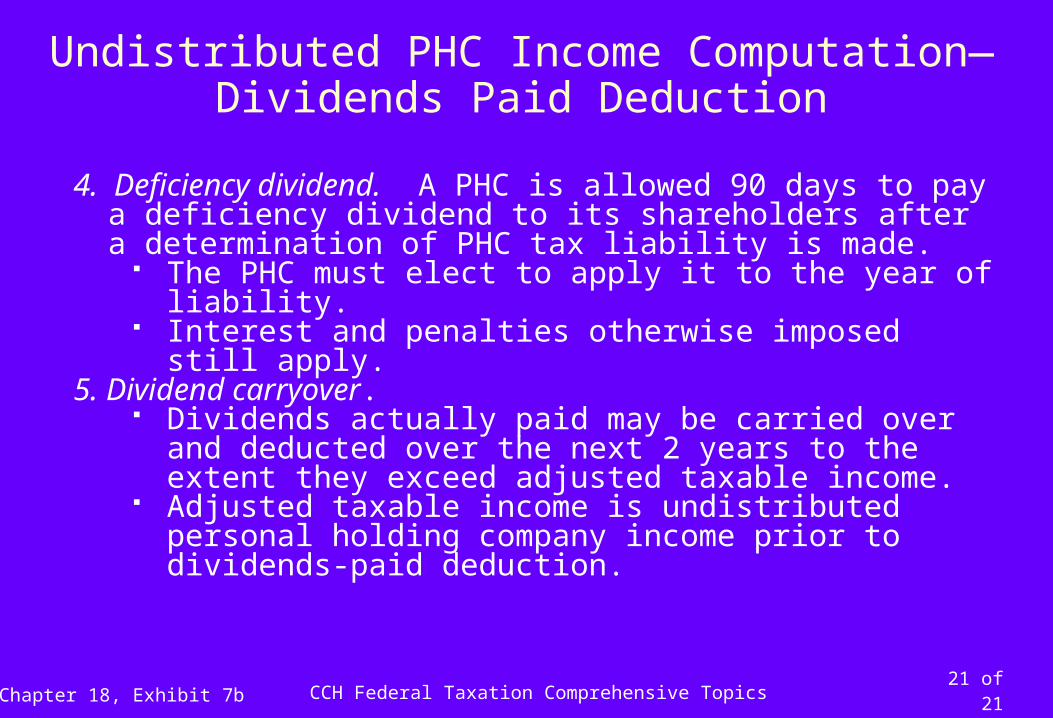

Undistributed PHC Income Computation—Dividends Paid Deduction

4. Deficiency dividend. A PHC is allowed 90 days to pay a deficiency dividend to its shareholders after a determination of PHC tax liability is made.

The PHC must elect to apply it to the year of liability. Interest and penalties otherwise imposed still apply.

5. Dividend carryover. Dividends actually paid may be carried over and

deducted over the next 2 years to the extent they exceed adjusted taxable income.

Adjusted taxable income is undistributed personal holding company income prior to dividends-paid deduction.

Chapter 18, Exhibit 7b