Embed Size (px)

Citation preview

EY Tax Alert Central Board of Direct Taxes issues final Guidelines for

determination of Place of Effective Management for corporate

residency

24 January 2017

Tax Alerts cover

significant tax news,

developments and

changes in legislation

that affect Indian

businesses. They act

as technical summaries

to keep you on top of

the latest tax issues.

For more information,

please contact your EY

advisor.

Executive summary

The test of residency for foreign companies in the Indian Tax Laws (ITL) was

amended in 2015. As per the amended rule which was then proposed to be

applicable from tax year commencing on 1 April 2015, a foreign company could

be treated as a resident of India if its Place of Effective Management (POEM), in

a given year, is in India. Pursuant to this, the Central Board of Direct Taxes

(CBDT), the highest Indian tax administrative body, had, vide Press Release

dated 23 December 2015, issued a draft of guidelines for determination of

POEM (Draft Guidelines)1.

Subsequently, the applicability of the POEM provision under the ITL was, vide

Finance Act 2016, deferred to tax years commencing from 1 April 2016

onwards.

On 24 January 2017, after due public consultation, the CBDT issued a Circular

providing the final guiding principles for determination of POEM of a foreign

company in India (the Guidelines).

The Guidelines emphasize that the test of POEM is one of “substance over form”

and is to be determined having regard to the facts and circumstances of each

case on a yearly basis. The Guidelines provide that the determination of POEM is

primarily based on whether or not a company has “Active Business Outside

India” (ABOI). The ABOI test needs to be evaluated on the basis of: (i) Non-

passive income of the taxpayer and (ii) The asset base, number of employees and

payroll expenses outside India. For companies which satisfy ABOI test, the POEM

is deemed to be outside India if majority of the Board meetings are held outside

India, unless facts suggest that the Board of Directors (BOD) is not the de facto

decision-making authority. 1 Refer EY Tax Alert dated 24 December 2015

For companies other than those engaged in

ABOI, the Guidelines prescribe a twin test: (a)

Identification of persons who take key

management and commercial decisions. (b)

Determining the place where these decisions

are, in fact, made. In this behalf, the

Guidelines also provide relevant factors, such

as determination of the location of Board

meetings, or location of the Head Office (HO),

who constitutes senior management etc. It is

also stated that the place of implementation

of decisions or the place where routine day-

to-day decisions are taken is not relevant for

determination of POEM. Furthermore, POEM

is not to be determined by taking a

“snapshot” view, but by considering activities

performed over a period of time during the

year for which POEM is determined. The

Guidelines also deal with determination of

POEM in cases where participation in

decision-making by the Board is by use of

telephone or videoconferencing or by way of

circular resolutions. It also deals with impact

of decisions by shareholders and draws

distinctions between decisions on matters

reserved for shareholders and decision that

restrict the authority of the company.

By way of a safeguard, the Guidelines require

two-step approvals as per which the tax

officer has to seek prior approval from a

senior tax officer before initiation of

proceedings and approval of a collegium of

three senior officers who will give an

opportunity of hearing to the taxpayer before

deciding on the residency of the foreign

company.

The Guidelines also provide five examples

illustrating the applicability of guiding

principles in determination of POEM. Details

of the examples are to be found in the

attached Appendix A.

At Appendix B, we have, for ease of

reference, tabulated the changes which are

made by the Circular as compared to text of

draft Guidelines.

Background

The test of residency for foreign companies under the ITL was amended in 2015. As per the amended rule applicable from tax year commencing on 1 April 2016, a foreign company is treated as a resident of India if its POEM, in a given year, is in India.

The earlier test of residency for foreign companies required that the whole of its control and management should be in India. As explained by the Explanatory Memorandum2 and in the Circular3 issued by the CBDT, such liberal threshold resulted in shift of profits by incorporating shell companies outside India, which were largely controlled from India.

As part of the Explanatory Memorandum, it was clarified that the Government of India (GOI) shall issue a set of guiding principles for determination of POEM for the benefit of taxpayers and the tax administration.

Pursuant to this, after due public consultation the CBDT has vide a Circular4 dated 24 January 2017 (the Circular), issued the final Guidelines for determination of POEM of foreign companies in India. This Tax Alert summarizes the Circular which lays down the Guidelines for determining whether POEM of a company is in India.

General principles: A substance over form approach The Guidelines provide for certain general principles of relevance for determination of POEM as under:

i. Determination of POEM depends on the facts and circumstances of a given case.

2 Explanatory Memorandum reflects statement of object and purpose for introducing a particular legislation. 3 No. 3 of 2015 4 No. 6 of 2017

ii. The concept is one of substance over form.

iii. An entity may have more than one place of management, but it can have only one POEM at any given point of time.

iv. POEM needs to be determined on a year-to-year basis for determining residence.

v. The principles recited in the Guidelines for determining POEM are by way of guidance and no single principle is decisive.

vi. Review and study of all facts related to the management and control of the

company would be relevant and POEM determination cannot be based on isolated facts.

vii. The principles contained in the Guidelines are not to be applied by taking a “snapshot view”, but activities performed over a period of time, during the tax year, need to be considered.

viii. If, during the tax year, POEM is in India as also outside India, POEM shall be presumed to be in India if it was mainly/predominantly in India.

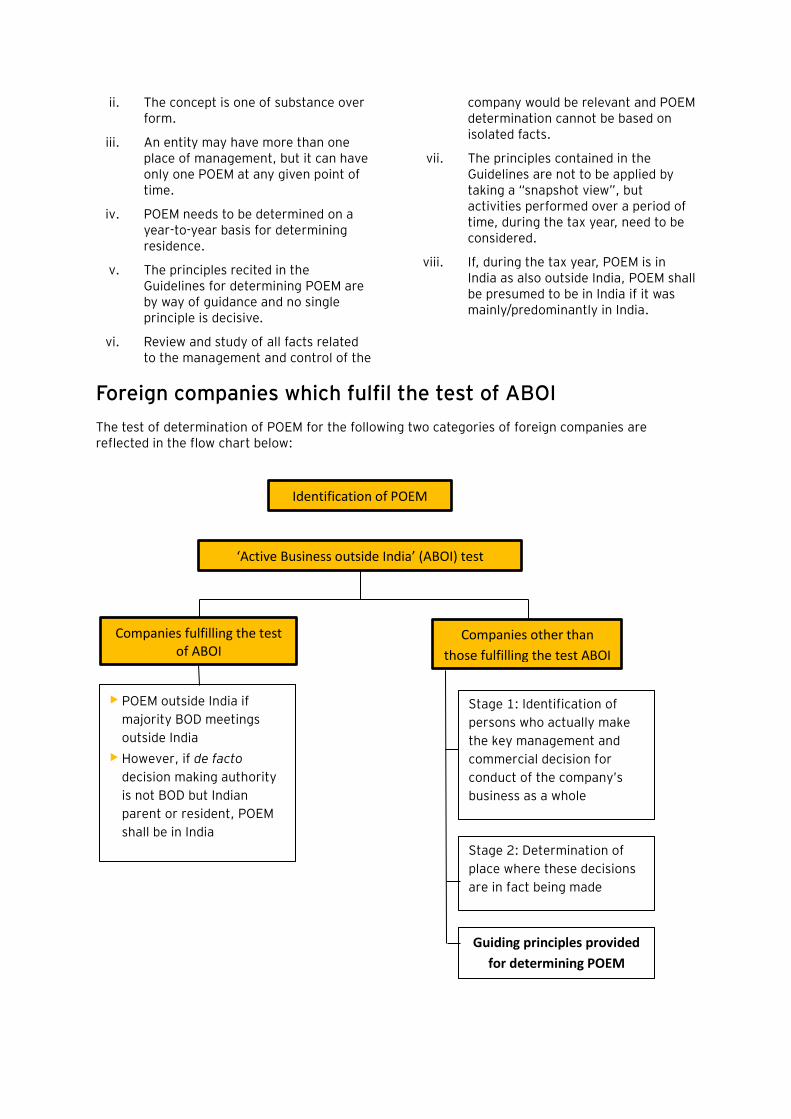

Foreign companies which fulfil the test of ABOI

The test of determination of POEM for the following two categories of foreign companies are reflected in the flow chart below:

‘Active Business outside India’ (ABOI) test

Companies fulfilling the test of ABOI

Companies other than

those fulfilling the test ABOI

Identification of POEM

• POEM outside India if

majority BOD meetings

outside India

• However, if de facto

decision making authority

is not BOD but Indian

parent or resident, POEM

shall be in India

Stage 1: Identification of

persons who actually make

the key management and

commercial decision for

conduct of the company’s

business as a whole

Stage 2: Determination of

place where these decisions

are in fact being made

Guiding principles provided

for determining POEM

POEM determination for

companies fulfilling the

ABOI test

► A company is said to be engaged in ABOI if it fulfils the cumulative conditions of5: a. Its passive income (wherever earned)

is 50% or less of its total income and b. In respect of each of the following,

the threshold is less than 50%: ► Its total assets situated in India (assets

test);

► Total number of employees situated in India or residents in India (employees test);

► Payroll expenses incurred on such employees compared to total payroll expenditure (payroll test).

For the above purpose, passive income is the aggregate of:

a. Income from the transactions where both, the purchase and sale of goods, is from or to its associated enterprises (AEs).

b. Income, by way of royalty, dividend, capital gains, interest (except for banking companies/public financial institutions6) or rental income, whether or not involving AEs.

► For the purpose of ABOI test,

► “Income” is income as computed for tax purposes in accordance with laws of country of incorporation or as per books of accounts where there is no requirement of computation of income for tax purposes.

► Value of assets is to be determined

on the basis of average as at the beginning and at the end of the previous year by adopting value for tax purposes in the country of incorporation for depreciable assets and at book value for other assets.

► Number of employees is taken based on average as at the beginning and at the end of the year. Also, this includes other persons who perform

tasks similar to those performed by employees, though not employed directly by the company.

► Payroll cost is defined inclusively to

include the cost of salaries, wages, bonus and all other employee compensation, including related pension and social costs borne by the employer.

► If the foreign company qualifies the ABOI

test, its POEM is presumed to be outside India if majority BOD meetings of the company are held outside India.

► However, if the facts and circumstances establish that the BOD is not the de facto decision-making authority but such powers are, in fact, being exercised either by the Indian parent or any other person resident in India, then POEM shall be considered to be in India.

► Merely because the BOD follows general

and objective principles of global policy of the group laid down by the parent entity for the group without the policies being specific to any entity or group of entities, it would not constitute a case of BOD of companies standing aside. Such policies may be in the field of payroll functions, accounting, Human Resource (HR) functions, IT infrastructure and network platforms, supply chain functions, routine banking operational procedures.

5 An average of the above data of the previous year

and two years prior or shorter period for which company has been in existence needs to be taken into account for the ABOI test. If the accounting year for tax purposes for the foreign entity is different from the tax year in India, then the data of accounting year that ends during the relevant tax year and two preceding years will be considered.

6 Whose activities are regulated under the applicable laws of the country of incorporation

POEM determination for companies other than those fulfilling the ABOI test

For companies other than those engaged in

ABOI, determination of POEM is a two-stage

process:

i. Identification or ascertaining the person or persons who actually make the key management and commercial decision for conduct of the company’s business as a whole.

ii. Determination of place where these decisions are, in fact, being made.

For this purpose, the following guiding

principles may be taken into account:

While enumerating the guiding principles, it is

clarified that the place of decision-making is

more important than that of implementation.

Furthermore, significance of substance over

form is emphasized.

i. Location of BOD

► If the BOD retains and, in substance, exercises the authority to govern the company and make key management and commercial decisions necessary for the conduct of the company’s business as a whole, then the place where the BOD regularly meets and makes decisions may be the company’s POEM.

► If the key decisions are made by the directors at a place other than the place of formal meetings, such other place would be relevant for POEM. For e.g., if the BOD meetings are held at a location other than the HO, or such location is distinct from the place where the predominant activity of the company is carried on.

► If the BOD has delegated the decision-

making authority to the senior management7 or any other person, including shareholder(s), promoter, strategic or legal or financial advisor, etc. and routinely ratifies their decisions,

then the POEM will ordinarily be the place of such actual decision making.

ii. Delegation to committees

► If the BOD has formally or de facto delegated authority to one or more committees consisting of members of senior management (e.g., executive committee consisting of members of senior management), then the place where such a committee develops and formulates key decisions for mere formal approval by the BOD will often be considered to be POEM.

iii. Location of company’s HO

► The location of the company’s HO is an important factor in determination of POEM, as it often represents the place where key decisions are made. The HO is defined to be the place where company’s senior management and their direct support staff are predominantly located.

► If a company is decentralized (e.g., where various members of senior management operate across countries), then the HO would be where the senior managers are predominantly based; or the place to which they normally return to following travel to other locations; or place where they meet when formulating or deciding key strategies and policies for the company as a whole.

► In case of meetings by way of telephone or videoconferencing, the HO would normally be the location where the highest level of management (for e.g., the Managing Director and the Financial Director) and their direct support staff is located.

► If the senior management is decentralized such that it is not possible to determine the HO with reasonable degree of certainty, the HO would not be relevant for determining POEM of the company.

7“Senior management” has been defined to mean

persons generally responsible for developing and formulating key policies and strategies and for ensuring or overseeing implementation of the same on a regular and ongoing basis. While designations may vary, they may include MD, CEO, FD, CFO, COO or divisional/departmental heads (e.g., Chief Information or Technology Officer, Director of Sales or Marketing).

iv. Place of residence of directors/decision-

makers relevant where modern technology

is used

► Use of modern technology means that physical presence is no longer necessary for BOD or committee meetings. In such cases, the place where majority of the directors or decision-making persons usually reside may be relevant.

v. Place of decision making in case of

circular resolutions

► In case of circular resolution8, the POEM evaluation is done having regard to the factors like frequency, type of decisions made, location of the parties involved in those decisions, etc. The proposer of resolution alone would not be relevant. The evaluation will need to be done based on the past practices and general conduct to determine the person who has and who exercises the authority to take decisions.

vi. Decisions by shareholders

► Decisions made by shareholders on the matters which are reserved for shareholder resolution under corporate law are not relevant for determination of POEM since these decisions typically affect the existence of the company itself or the rights of the shareholders, rather than the conduct of the company’s business from a management or commercial perspective. Illustrations of such decisions are: sale of all or substantially all of the company’s assets, the dissolution, liquidation or deregistration of the company, modification of the rights attaching to various classes of shares or the issue of a new class of shares etc.

► In certain situations, involvement of

shareholders may lead to effective management either through formal arrangement- say, by way of shareholders’ agreement, or by actual conduct. This may happen illustratively where the shareholders limit the authority of board and senior managers of a company such that the real authority to make decision is removed from the Board and the shareholder guidance

transforms into usurpation and undue influence.

► However, this is a fact-specific exercise to

be determined on case to case basis.

vii. Place of implementation or execution of

decisions not relevant

► The place where management decisions are taken would be more important than the place where such decisions are implemented.

► Day-to-day routine decisions taken by junior and middle management are not relevant for determining POEM. Operational decisions relating to day to day business operations and activities need to be distinguished from broader strategic and policy decisions.

For Example: A decision regarding opening of a major new manufacturing facility or discontinuing a major product is an example of key commercial decision affecting the company’s business as a whole. As against that, decisions by the plant manager to run the facility, implement countrywide quality control, HR policies, etc. are examples of routine decisions. POEM evaluation is to be done after distinguishing between types of decisions if strategic and routine decisions are taken by the same person.

viii. Secondary factors (if the above do not

lead to clear identification of POEM):

► Place where the main or substantial activity of the company is carried out

or ► Place where the accounting records of

the company are kept.

“No POEM” scenarios illustrated

Illustratively, POEM cannot be established to be in India merely because:

i. The foreign company is completely owned by an Indian company; or

ii. Foreign company has a Permanent Establishment (PE) in India;

8 Or, round robin voting

iii. One or some of the directors of a foreign company reside in India; or

iv. Local management in India is in respect of activities carried out by a foreign company in India; or

v. There exists in India, support functions that are preparatory and auxiliary in character.

Administrative safeguard of two-stage

approval

► If, on the basis of its POEM, the tax officer proposes to initiate proceedings to hold a foreign company to be resident in India, prior approval of senior tax officers, viz., the Principal Commissioner or the Commissioner of Income Tax (PCIT/CIT) shall be necessary.

► Additionally, prior approval of a collegium of three members consisting of Principal Commissioners or the Commissioners (or constituted by them) is needed before holding that foreign company is POEM resident. The collegium will grant opportunity of the hearing to the taxpayer before issuing directions to the tax officer.

Examples illustrating the applicability

of guiding principles

► The Circular provides five examples to illustrate the applicability of the Guidelines. The first three deal primarily with the ABOI test, being (i) the passive income test, (ii) the payroll test and (iii) number of Board meetings. The fourth example illustrates a case of de facto exercise powers by shareholders. The fifth example clarifies that in an outbound structure, merely because the POEM of an overseas intermediate holding company is in India, it would not mean that the POEM of all further subsidiaries held by the intermediate company (who are engaged in ABOI and whose BOD meetings are held outside India) is in India.

Comments

The Circular issued by the Government provides guiding principles to be followed for determination of POEM. The Circular acknowledges that concept of POEM was introduced in Indian legislation to amend the earlier laws which permitted tax avoidance opportunities for companies to artificially escape residential status by shifting insignificant or isolated control or management outside India. As part of the Circular, guidance is provided on resolution of various parameters of ABOI test. Interest income earned by banks or public financial institution is kept outside the category of passive income. It is clarified that adherence by BOD of foreign company to general group policy on various business functions is not determinative of POEM. Further, decisions by shareholders on matters which are reserved for shareholder decisions or the decisions which may affect the existence of the company, (but not the decisions on conduct and management of the business), do not impact POEM determination. The Circular also provides illustrations on application of ABOI test and also clarifies that POEM trigger for intermediate holding company does not mean that POEM of all further downstream subsidiaries is in India.

However, there are still certain issues which are likely to be of concern to the taxpayers. Particularly, despite the fact that the final Guidelines are issued towards the fag end of the year, the same is expected to apply from 1 April 2016. Further, except interest income of banking company, operative income from interest, royalty etc. continues to get classified as passive income. The final Guidelines continue to look at average of three year parameters of income, assets, employees etc. In respect of companies which do not fulfil the ABOI test, the Circular has listed several criteria and, multiple factors for determination of POEM, without defining the hierarchy of elimination and without providing guidance on the weightage of each factor. This is likely to make the exercise subjective and uncertain, on a year-to-year basis. Given that the stated object of introducing POEM is to target shell structures, it would have been useful to keep entities in comparable tax jurisdictions as also overseas listed companies outside the scrutiny of POEM. An overarching statement that POEM is a deterrent measure, and not a revenue raiser, would also have been of significance to taxpayers. The taxpayer will have to carefully monitor and assess impact on various operations carried out in India and outside India of the foreign entities in the structure to determine their POEM.

`

Appendix A - Gist of illustrations and interpretation provided in the Circular

Illustration no.

Facts CBDT interpretation

1.

In Country X (Outside India)

► ACo is subsidiary of BCo and is a sourcing entity for the

Indian multinational group

► The assets (viz. stocks in warehouses) of ACo are located

in country X

► All the employees of ACo are in Country X

► Average income-wise breakup of total income of A Co for

three years include:

Income % Purchases Sales

30 % Non-AEs AEs

30 % AEs AEs

30 % AEs Non-AEs

10 % Interest income

► Income Test Satisfied:

Passive income is 40%

of the total income of

the company,

consisting of:

30% from the

transaction where

both purchase and

sale is from/to

AEs

10% income from

interest

► Assets Test,

Employees Test:

Since no assets or

employees of A Co are

in India the other

requirements of the test

is also satisfied

► A Co is engaged in

ABOI

2. In addition to facts listed at Illustration no.1,

In Country X (Outside India)

► Out of 50 employees of ACo, 47 employees, who are

managing the warehouse, storekeeping and accounts of

the company, are located in Country X.

► Annual payroll expenditure of 50 employees is INR 50 M

In India

► The other three employees i.e Managing director(MD),

Chief executive officer (CEO) and Sales head are resident

in India

► Annual payroll expenditure of above employees is INR 30

M

► Passive Income Test

(as above) and

Employee Test is

satisfied as more than

50% of the employees

are also situated

outside India

► Assets Test satisfied:

All the assets are

situated outside India

► Payroll Test not

satisfied: The payroll

expenditure in respect

of the MD, CEO and

the Sales head being

employees resident in

India exceeds 50% of

the total payroll

expenditure

► Therefore, A Co is not

engaged in ABOI

3. In addition to facts listed at Illustration no.1,

In Country X (Outside India)

► All the directors of the ACo are Indian residents During the relevant tax year, five meetings of the BOD is held, out of which two are held in Country X and one in Country Y.

► The A Co is engaged in

active business outside

India as the facts

indicated in illustration

1

B Co

A Co

cos. Stock in

warehouses

India

Country X

(Outside India)

100%

Illustration no.

Facts CBDT interpretation

In India

► Two out of five BOD meetings were held in India

► The majority of board

meetings have been

held outside India

► Therefore, POEM of

ACo shall be presumed

to be outside India

4. In addition to facts listed at Illustration no.3

It is established by the AO that:

► Although ACo’s senior management team signs all the

contracts, for all the contracts above INR 1M, ACo must

submit its recommendation to BCo and B Co makes the

decision whether or not the contract may be accepted

► It is also seen that during the previous year more than 99%

of the contracts were above INR 1M and over past years

also the same trend in respect of value contribution of

contracts above INR 1M is seen

► The facts suggest that

the effective

management of the

ACo may have been

usurped by the parent

company BCo

► Therefore, POEM of

ACo may, in such

cases, be not

presumed to be outside

India even though ACo

is engaged in active

business outside India

and majority of board

meetings are held

outside India

5.

► An Indian MNC group has a local holding company ACo in

Country X

► ACo has 100% downstream subsidiaries in the form of

BCo and CCo in Country X and DCo in Country Y

► ACo has income only by way of dividend and interest from

investments made in its subsidiaries

► POEM of ACo is in India and is exercised by ultimate

parent company of the group

► BCo, CCo and DCo are engaged in active business

outside India

► Meetings of Board of Directors of B Co, CCo and DCo are

held in respective countries.

► Merely because the

POEM of an

intermediate holding

company is in India the

POEM of its

subsidiaries shall not

be taken to be in India.

► Each subsidiary has to

be examined

separately.

► Since BCo, CCo and

DCo are independently

engaged in active

business outside India

and majority of board

meetings of these

companies are also

held outside lndia,

POEM of these

companies shall be

presumed to be outside

lndia

Parent Co

ACo (Dividend/interest

income)

CCo Op co

BCo Op co

Country X

India

DCo Op co

Country Y

Appendix B: Changes made by the Circular as compared to text of draft Guidelines.

Draft Guidelines Final Guidelines

Determination of POEM primarily based on

whether or not a company has ABOI on the basis

of: (i) Passive income (ii) asset base, (iii) number

of employees and (iv) payroll expenses. For such

companies, the POEM is deemed to be outside

India if majority board meetings are held outside

India, unless facts suggest that the Board of

Directors (BOD) is not the de facto decision-

making authority.

The Final Guidelines contain further Explanation as to the

determination of these factors to reduce ambiguities.

For this purpose,

Income is income as computed for tax purposes in accordance with laws of country of incorporation or as per books of accounts where there is no requirement of computation of income for tax purposes.

Value of assets is determined on the basis of average as at the beginning and at the end of the previous year by adopting value for tax purposes in the country of incorporation for depreciable assets and book value in respect of other assets.

Number of employees are taken based on average as at the beginning and at the end of the year. Also, employees include those person, who perform tasks similar to those performed by employees though not employed directly by the company.

Payroll cost is defined inclusively to include the cost of salaries, wages, bonus and all other employee compensation including related pension and social costs borne by the employer.

Interest income constituted ‘passive’ income for

determination of ABOI.

Clarifies that interest income would not constitute passive income

for banking companies or public financial institutions and whose

activities are regulated as such under the applicable laws of its

country of incorporation.

Where on the basis of facts and circumstances it is

established that the BOD is standing aside and the

management powers are, in fact, being exercised

by the holding company or any other Indian

resident, then the POEM of the company will be

regarded to be India.

Clarifies that merely because the BOD follows general and objective

principles of global policy of the group laid down by the parent entity

and not being specific to any entity or group of entities as such

would not constitute a case of BOD of companies standing aside.

These may be in the field of payroll functions, accounting, Human

Resource (HR) functions, IT infrastructure and network platforms,

supply chain functions, routine banking operational procedures.

In determining ABOI, the average of the data of

the tax year and two years prior to that shall be

taken into account.

Where the accounting year for tax purposes, in accordance with

laws of country of incorporation of the company, is different from the

Indian tax year, then, data of the accounting year that ends during

the relevant tax year and two years preceding it shall be considered

If the BOD has de facto delegated the authority to

make key decisions of the company to the senior

management or any other person including a

shareholder and does nothing more than routinely

ratifying these decisions, the POEM will be the

place where the senior management or other

person makes those decisions.

Scope of ‘any other person’ clarified further by including promoter,

strategic advisor, legal advisor, financial advisor, etc.

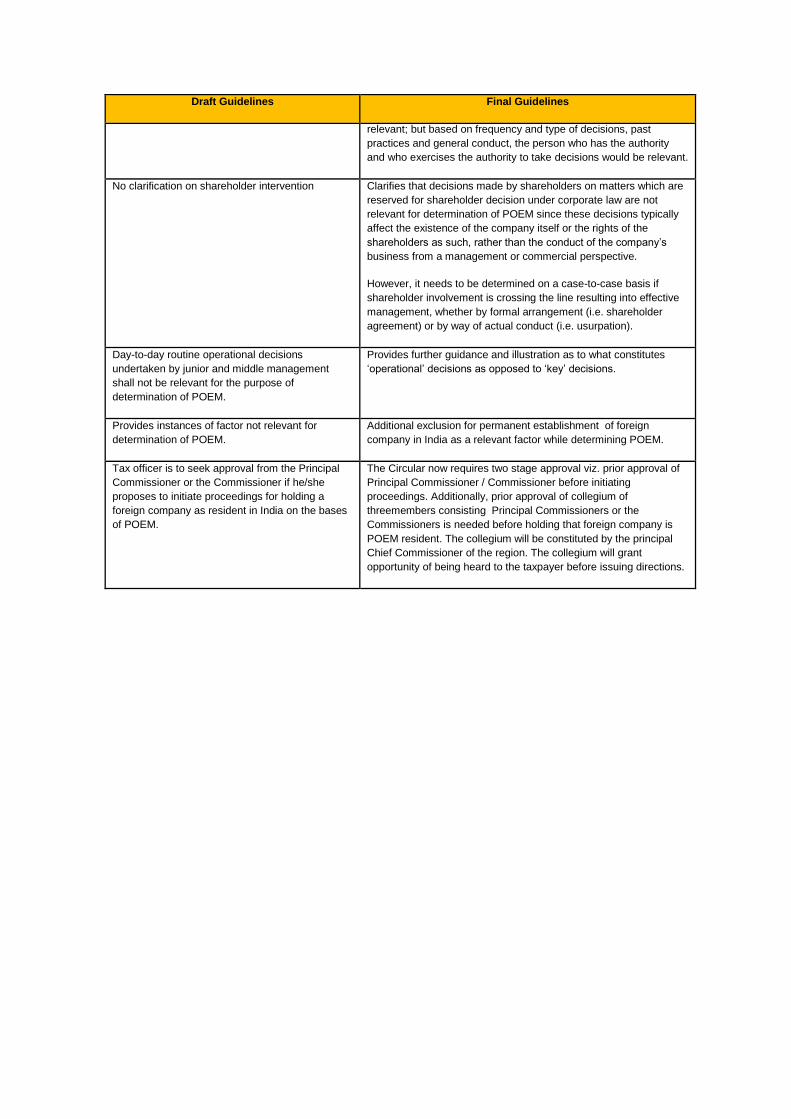

No clarification on circular resolutions Provides guidance on use of circular resolutions for taking key

decisions. The proposer of decisions alone would be not be

Draft Guidelines Final Guidelines

relevant; but based on frequency and type of decisions, past

practices and general conduct, the person who has the authority

and who exercises the authority to take decisions would be relevant.

No clarification on shareholder intervention Clarifies that decisions made by shareholders on matters which are

reserved for shareholder decision under corporate law are not

relevant for determination of POEM since these decisions typically

affect the existence of the company itself or the rights of the

shareholders as such, rather than the conduct of the company’s

business from a management or commercial perspective.

However, it needs to be determined on a case-to-case basis if

shareholder involvement is crossing the line resulting into effective

management, whether by formal arrangement (i.e. shareholder

agreement) or by way of actual conduct (i.e. usurpation).

Day-to-day routine operational decisions

undertaken by junior and middle management

shall not be relevant for the purpose of

determination of POEM.

Provides further guidance and illustration as to what constitutes

‘operational’ decisions as opposed to ‘key’ decisions.

Provides instances of factor not relevant for

determination of POEM.

Additional exclusion for permanent establishment of foreign

company in India as a relevant factor while determining POEM.

Tax officer is to seek approval from the Principal

Commissioner or the Commissioner if he/she

proposes to initiate proceedings for holding a

foreign company as resident in India on the bases

of POEM.

The Circular now requires two stage approval viz. prior approval of

Principal Commissioner / Commissioner before initiating

proceedings. Additionally, prior approval of collegium of

threemembers consisting Principal Commissioners or the

Commissioners is needed before holding that foreign company is

POEM resident. The collegium will be constituted by the principal

Chief Commissioner of the region. The collegium will grant

opportunity of being heard to the taxpayer before issuing directions.

Our offices Ernst & Young LLP

EY | Assurance | Tax | Transactions | Advisory

About EY

EY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization and may refer to one or more of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

Ernst & Young LLP is one of the Indian client serving member

firms of EYGM Limited. For more information about our

organization, please visit www.ey.com/in.

Ernst & Young LLP is a Limited Liability Partnership, registered

under the Limited Liability Partnership Act, 2008 in India, having

its registered office at 22 Camac Street, 3rd Floor, Block C,

Kolkata – 700016.

© 2017 Ernst & Young LLP. Published in India. All Rights Reserved.

ED None

This publication contains information in summary form and is

therefore intended for general guidance only. It is not intended to

be a substitute for detailed research or the exercise of

professional judgment. Neither Ernst & Young LLP nor any other

member of the global Ernst & Young organization can accept any

responsibility for loss occasioned to any person acting or

refraining from action as a result of any material in this

publication. On any specific matter, reference should be made to

the appropriate advisor.

EY refers to global organization, and/or one or

more of the independent member firms of

Ernst & Young Global Limited

Join India Tax Insights from EY on

Ahmedabad 2nd floor, Shivalik Ishaan Near C.N. Vidhyalaya Ambawadi Ahmedabad - 380 015 Tel: + 91 79 6608 3800 Fax: + 91 79 6608 3900

Bengaluru 6th, 12th & 13th floor “UB City”, Canberra Block No.24 Vittal Mallya Road Bengaluru - 560 001 Tel: + 91 80 4027 5000 + 91 80 6727 5000 + 91 80 2224 0696 Fax: + 91 80 2210 6000

Ground Floor, ‘A’ wing Divyasree Chambers # 11, O’Shaughnessy Road Langford Gardens Bengaluru - 560 025 Tel: +91 80 6727 5000 Fax: +91 80 2222 9914

Chandigarh 1st Floor, SCO: 166-167 Sector 9-C, Madhya Marg Chandigarh - 160 009 Tel: +91 172 331 7800 Fax: +91 172 331 7888

Chennai Tidel Park, 6th & 7th Floor A Block (Module 601,701-702) No.4, Rajiv Gandhi Salai Taramani, Chennai - 600 113 Tel: + 91 44 6654 8100 Fax: + 91 44 2254 0120

Delhi NCR Golf View Corporate Tower B Sector 42, Sector Road Gurgaon - 122 002 Tel: + 91 124 464 4000 Fax: + 91 124 464 4050

3rd & 6th Floor, Worldmark-1 IGI Airport Hospitality District Aerocity, New Delhi - 110 037 Tel: + 91 11 6671 8000 Fax + 91 11 6671 9999

4th & 5th Floor, Plot No 2B Tower 2, Sector 126 NOIDA - 201 304 Gautam Budh Nagar, U.P. Tel: + 91 120 671 7000 Fax: + 91 120 671 7171

Hyderabad Oval Office, 18, iLabs Centre Hitech City, Madhapur Hyderabad - 500 081 Tel: + 91 40 6736 2000 Fax: + 91 40 6736 2200

Jamshedpur 1st Floor, Shantiniketan Building Holding No. 1, SB Shop Area Bistupur, Jamshedpur – 831 001 Tel: +91 657 663 1000 BSNL: +91 657 223 0441

Kochi 9th Floor, ABAD Nucleus NH-49, Maradu PO Kochi - 682 304 Tel: + 91 484 304 4000 Fax: + 91 484 270 5393

Kolkata 22 Camac Street 3rd Floor, Block ‘C’ Kolkata - 700 016 Tel: + 91 33 6615 3400 Fax: + 91 33 2281 7750

Mumbai 14th Floor, The Ruby 29 Senapati Bapat Marg Dadar (W), Mumbai - 400 028 Tel: + 91 22 6192 0000 Fax: + 91 22 6192 1000

5th Floor, Block B-2 Nirlon Knowledge Park Off. Western Express Highway Goregaon (E) Mumbai - 400 063 Tel: + 91 22 6192 0000 Fax: + 91 22 6192 3000

Pune C-401, 4th floor Panchshil Tech Park Yerwada (Near Don Bosco School) Pune - 411 006 Tel: + 91 20 6603 6000 Fax: + 91 20 6601 5900