Embed Size (px)

Citation preview

CEO Home Bias and Corporate Acquisitions

Kiseo Chung, T. Clifton Green, and Breno Schmidt*

January 2018

CEOs are significantly more likely to purchase targets near their birth place, reflecting

either beneficial informational advantages or inefficient managerial objectives. Evidence

from bidder announcement returns supports the latter view. Acquirer returns are

significantly lower for CEO home bias acquisitions, and the negative announcement effect

is stronger when the target is located further away, among poorly-governed firms, and

when the CEO has a deeper birth place connection. Home bias CEOs are more likely to

purchase stock following merger announcements, which supports a familiarity bias

interpretation over agency concerns. Our findings suggest that CEO home bias influences

firm investment.

JEL Classification: G14, G34

Keywords: Mergers and Acquisitions, Home Bias

* Chung is from Rawls College of Business, Texas Tech University, [email protected]; Green is from the

Goizueta Business School, Emory University, [email protected]; and Schmidt is from the University

of New South Wales, [email protected]. We thank seminar participants at Georgia Tech, UNSW,

Católica Lisbon School of Business & Economics, and the Research in Behavioral Finance Conference at

VU Amsterdam for comments.

1

1. Introduction

In 2010, after considering roughly 400 possible targets, Indiana-based

manufacturer of funeral caskets Hillenbrand Inc. announced a plan to acquire K-Tron

International Inc., a Pitman, New Jersey firm which engineers industrial coal crushers and

feeding equipment (including a machine to shoot raisins into breakfast cereal). Despite the

considerable difference in product lines, K-Tron provided Hillenbrand CEO Kenneth

Camp with a unique benefit. Although Camp said the location in Pitman had no influence

on his decision to buy the company, he acknowledged: “When I heard it was in Pitman I

thought people would say I spent all this money to go see my mother.” Camp was raised

in Pitman and his mother Edith still lived nearby in his childhood home.1

In this article, we study the effects of CEO home bias on corporate acquisitions.

We analyze whether CEOs are more likely to acquire companies located near their birth

place, and we explore whether CEO home bias acquisitions are in the best interest of

shareholders. Specifically, we examine whether home bias mergers reflect beneficial

information advantages or are instead driven by inefficient managerial objectives such as

private benefits to the CEO or an underlying bias towards the familiar.

A well-established literature in equity markets finds that investors like to invest

close to home, and evidence is mixed regarding whether local preferences reflect

informational advantages or familiarity bias. Coval and Moskowitz (2001) and Ivkovic and

Weisbenner (2005) find that investors’ local stock holdings outperform, and Kang and

Stulz (1997) find that foreign investors avoid stocks with high information asymmetry. On

1 Details are taken from an article in the Philadelphia Inquirer (Fernandez, 2010). Hillenbrand’s stock price

fell by (CAPM-adjusted) 2.5% in the three-day window around the merger announcement.

2

the other hand, Seasholes and Zhu (2010) and Pool, Stoffman, and Yonker (2012) find no

benefits to local investing, and they observe a greater propensity to invest locally among

less experienced investors, which is more consistent with familiarity bias.2

As with equity investments, a local preference for corporate investment may occur

for beneficial informational reasons. For example, CEOs’ educational or professional

network connections may cluster geographically, which could lead to worthwhile

investment opportunities close to home (e.g., Cohen, Frazzini, and Malloy, 2008; Cai and

Sevilir, 2012). Cultural awareness of a geographic region may also facilitate the process of

merging, which could also lead to more local mergers (Ahern, Daminelli, and Fracassi,

2015).

On the other hand, home bias acquisitions may also be influenced by inefficient

managerial objectives (e.g., Morck, Shleifer, and Vishny, 1990; Harford, Humphery-

Jenner, and Powell, 2012). In particular, local investment may generate private benefits for

the CEO, with home bias acquisitions reflecting the pursuit of CEO pet projects that are

unrelated to value optimization. For example, acquiring and maintaining operations close

to home may raise the CEO’s stature within their home region or facilitate visits to friends

and family.

CEOs may also be susceptible to familiarity bias. Place attachment and place

identity are well-established concepts in environmental psychology (e.g. Manzo, 2003),

and familiarity is viewed as a central cognitive element of place attachment (Scannell and

Gifford, 2010). Familiarity has been linked to confidence in risky gambles (Heath and

2 Other work on equity home bias includes French and Poterba (1991), Tesar and Werner (1995), Huberman

(2001), Coval and Moskowitz (1999), Grinblatt and Keloharju (2001), Bhattacharya and Groznik (2008), and

Parwada (2008).

3

Tversky, 1991), and measures of CEO overconfidence have previously been linked to

corporate investment (e.g. Malmendier and Tate, 2008; Hirshleifer, Low, and Teoh, 2012;

and Ben-David, Graham, and Harvey, 2013). CEOs’ regional upbringing reflects a source

of deep-seated familiarity which may drive CEOs to overestimate the value of their local

connections and investment opportunities.

Our initial tests uncover compelling evidence that CEO home bias influences

corporate acquisitions. We consider two proxies for proximity between an acquirer CEO’s

birth place and the acquisition target based on state boundaries and geographic distance.3

Following an approach similar to Rhodes-Kropf and Robinson (2008), we compare actual

acquirers to hypothetical bidders with similar characteristics. We find that mergers are 27-

29% more likely when the CEO grew up near the target, controlling for bidder, industry,

and state characteristics.

The rest of our analysis seeks to identify the forces that drive CEO home bias

acquisitions. We focus on three potential explanations for CEOs’ proclivity for selecting

targets near their home regions: beneficial informational advantages, managerial objectives

such as status seeking, and a cognitive bias toward the familiar. We conduct a series of

tests to help differentiate between these explanations. As part of our identification strategy,

we distinguish between near and faraway mergers. Our rationale is that we expect the effect

of CEO home bias on target selection to be stronger, through each potential channel, when

the target is distant from the acquirer.

3 We refer to the region of a CEO’s childhood as their “birth” place to denote upbringing and help

differentiate it from their current place of residence. Empirically, our geographic measures emphasize CEO’s

place of residence during their teenage years. Section 2 describes the measures of CEO origin.

4

Our first test considers whether home bias acquisitions reflect beneficial

informational advantages, and we explore this hypothesis by examining bidder merger

announcement returns. We find evidence that the market reacts negatively to acquisition

announcements when the CEO grew up near the target. In particular, after controlling for

firm and deal characteristics, home bias acquisitions are associated with a 40 to 48 basis

point lower bidder announcement return on average, and distant home bias mergers

experience between 1.71 and 1.95 percent lower returns. The findings are robust to

alternative econometric approaches and when considering longer-horizon returns.

Together, they provide evidence against the information advantage hypothesis.

We next explore whether agency or familiarity biases can help explain home bias

acquisitions. In particular, we examine differences in the quality of corporate governance,

and we also consider measures of the strength of connection between CEOs and their home

regions. If CEO home bias acquisitions reflect managerial objectives or personal biases

rather than value maximization, we would expect the practice to be more prevalent among

poorly governed firms. Consistent with the managerial objectives hypothesis, we find a

greater proclivity for home bias mergers when the CEO is also the board chair, the board

is less independent, institutional ownership is low, or the firm has a higher entrenchment

index (Bebchuk, Cohen, and Ferrell, 2009). Moreover, bidder announcement returns for

home bias mergers are also significantly lower among poorly governed firms. The

governance results provide additional evidence in support of the interpretation that home

bias acquisitions reflect either manager preferences or personal biases.

Under the managerial preference and familiarity hypotheses, we anticipate that the

effect of CEO home bias on birth state merger activity will be stronger when the CEO holds

5

a deeper connection to their birth state. Place attachment is generally thought to be the

result of a long-term connection (Altman and Low, 1992) and we conjecture that CEOs

who attended college in their birth state or resided there in early adulthood will hold

stronger attachments. Consistent with both agency and familiarity interpretations, we find

that home bias acquisitions are more likely, and home bias announcement returns are

significantly lower, when the acquirer CEO attended college in the target state or lived

nearby in the region after college.

Taken together, the evidence that markets react negatively to CEOs’ proclivity to

purchase targets near their home region is consistent with a bias for the familiar that leads

to over-optimism regarding the value of the merger. Alternatively, CEOs may understand

that home bias mergers are inefficient, but nevertheless undertake such investments for

personal rather than firm reasons. We distinguish between agency and familiarity

interpretations by examining CEO insider trading around merger announcements. In

particular, if familiarity leads CEOs to overestimate the synergies arising from home bias

mergers, they would be more likely to purchase shares in their company following the

merger. On the other hand, if CEOs engage in suboptimal home bias mergers for the private

benefits they afford, they would be less likely to purchase shares following the merger.

We observe significant differences in the trading behavior of home bias CEOs and

other firm executives following merger announcements. In particular, acquirer CEOs are

roughly 20% more likely to purchase stock if they grew up near the target, whereas other

top executives are between 5% and 15% less likely to purchase the stock for CEO home

bias acquisitions. We find no differences in trading activity among insiders around a

placebo date chosen two years prior to the announcement, which suggests the behavior is

6

related to the home bias merger, rather than specific to the firm or CEO.4 The evidence that

CEOs purchase company stock following home bias merger announcements is inconsistent

with rent extraction through pet projects. Instead, it supports the view that CEO home bias

mergers reflect familiarity-based optimism.

Our evidence of a familiarity-driven birth state home bias is consistent with Pool,

Stoffman, and Yonker (2012), who find mutual fund managers are more likely to invest in

companies with headquarters in their birth state with no evidence of outperformance. Our

results are also in line with Cornaggia, Cornaggia, and Israelsen (2017), who find credit

analysts rate municipal bonds issued in their birth states more favorably. Our setting is

most closely related to Yonker (2016b), who finds that home state CEOs are significantly

less likely to lay off employees than their non-local peers following industry distress.5

The remainder of the paper proceeds as follows. In Section 2 we describe the

sample and construction of the home bias variables. Section 3 examines the effects of CEO

birth state on his or her propensity to make an acquisition. Section 4 explores the market

response to and underlying drivers of home bias acquisitions. Section 5 describes a series

of robustness checks and additional analysis.

2. Data and Variable Construction

This section describes the acquisition sample and provides details for the

construction of the CEO home bias related variables.

4 While trades by insiders are well known to be informative on average (e.g. Seyhun, 1986; Cohen, Malloy,

and Pomorski, 2012; Alldredge and Cicero, 2015), we find no evidence that CEO purchases following home

bias acquisitions are associated with outperformance 6 to 24 months after the announcement. 5 We recognize Jian, Qian, and Yonker (2016) as independent contemporaneous work that also documents a

home bias in corporate acquisitions. Their findings generally support our own results, although they find

evidence of home advantage for a subset of public target mergers.

7

2.1 Acquisition Sample

The merger data are obtained from Securities Data Company (SDC). After

collecting all mergers from 1990 to 2014, we impose data requirements which are similar

to those in Masulis, Wang, and Xie (2007). Acquirers must be publicly traded companies

with stock return data available in the Center for Research in Security Prices (CRSP). We

exclude deals with values lower than $1 million or representing less than 1% of the

acquirer’s market value, as measured at the fiscal year end before the announcement. We

also gather state and zip code information for the firm headquarters of both the acquirer

and target.

The bidder firm CEO data are obtained from both BoardEx and ExecuComp.

Boardex data contains detailed profiles of US executives and board members, covering

virtually all US public companies. ExecuComp data contains detailed information on

executive compensation data for past and current S&P 1500 firms. We also collect

compensation data from BoardEx for firms not covered by ExecuComp. Using the

Boardex/EcecuComp data, we are able to identify the bidder firm CEO for 15,526 of the

mergers of public/private targets reported in SDC data during the sample period.6

2.2 Measuring CEO Home Bias

In order to identify each CEO’s birth state, we collect information on his or her full

name, age, and firm name from both BoardEx and ExecuComp. Using the CEO’s name

6 We require CEO information to be available at the date of the announcement (dates of employment are

occasionally missing early in the sample period). We exclude leverage buyouts, spin-off/split-offs,

recapitalizations, self-tender offers and exchange offers, repurchases, acquisition of minority stakes or

remaining interest, and privatizations, reverse takeovers, and bankruptcies. See Cohen, Frazzini and Malloy

(2008), Ferreira and Matos (2012), Cohen, Frazzini, and Malloy (2012), and Schmidt (2015) for more

detailed descriptions of the database.

8

and age for each acquisition in our sample, we collect data on each CEO’s birth state and

previous addresses from the Lexis Nexis Online Public Records Database following the

methodology of Pool, Stoffman, and Yonker (2012). Specifically, we search by CEO name

and age, and we also use other information such as employment history and email addresses

to pinpoint the correct person. In order to further guarantee each CEO’s identity, we also

require that the firm employing the CEO when the deal was announced corresponds to one

of the employers listed in the CEO’s Lexis Nexis personal file.

For the CEOs for whom we could identify a unique Lexis Nexis ID, we use the first

five digits of their social security number to identify their home state.7 Alternately, for

CEOs for whom a unique Lexis Nexis ID could not be identified, we use firm name, CEO

name, and age to search Google for their home state. In order to be included in our sample,

information on the birth state of the acquirer firm CEO must be available. We were able to

collect CEO public records data for 12,221 mergers, which represents 79% of the number

of mergers and 94% of total deal value for the mapped set of SDC and

Boardex/ExecuComp mergers.

We match the SDC and CEO birth state merged dataset with data from CRSP and

Compustat, from which all financial and accounting variables are obtained. Our merger

sample consists of 9,891 acquisitions after applying the initial data requirements. In cases

where the zip code is missing for either the acquirer or target firm in SDC database, we use

7 Currently, US citizens typically obtain social security numbers (SSNs) near birth. For CEOs during the

sample period, they were more likely to obtain SSNs prior to their first jobs or when obtaining a driver’s

license. Yonker (2015a) indicates that a majority of the CEOs in a similarly-constructed sample received

their SSN when they were between the ages of 14 and 17. Therefore, “birth” state is more accurately described

as home state during the mid-teenage years.

9

the headquarters zip code variable in Compustat when available. Our resulting distance

merger sample consists of 9,494 mergers.

We consider two measures of CEO birthplace proximity. Our first measure is based

on state boundaries. We define the dummy variable Home Bias State as equal to one when

the acquirer firm CEO birth state is equal to target headquarters state. We then partition the

merger sample into in-state and cross-state mergers by defining the dummy variable

Faraway State, which is one if the acquirer and target headquarters states differ. We use

headquarters’ state rather than state of incorporation as the latter is often chosen for

regulatory rather than operational reasons.

Our second measure of CEO home proximity is based on the geographic distance

between the target firm headquarters and the CEO’s hometown. We obtain information on

the CEO’s birth town by searching the public records data from Lexis Nexis. We identify

the oldest available address that matches the birth state implied by the Social Security

Number as the CEO’s birthplace. If no address is available that matches the SSN-implied

state, we use the zip code of the largest city in the state as a proxy for hometown.8

Based on the CEO’s hometown, we then use the latitude/longitude of the zip codes

in the census files to determine the distances between the target firm headquarters and

acquirer CEO hometown.9 We set Home Bias Distance equal to one if the distance between

the target headquarters and the acquirer firm CEO’s hometown is less than 100 miles, and

zero otherwise. Analogous to cross-state mergers but capturing geographic distance rather

8 The results are very similar if we use the state capital instead of the largest city for the observations with

state, name, and employer matches but no listed addresses. 9 Census zip code LAT/LONG data is posted here: www2.census.gov/geo/tiger/TIGER2010/ZCTA5/2010/.

10

than state borders, the dummy variable Faraway Distance that we create is equal to one if the

target firm headquarters is located more than 100 miles from the acquirer firm headquarters.

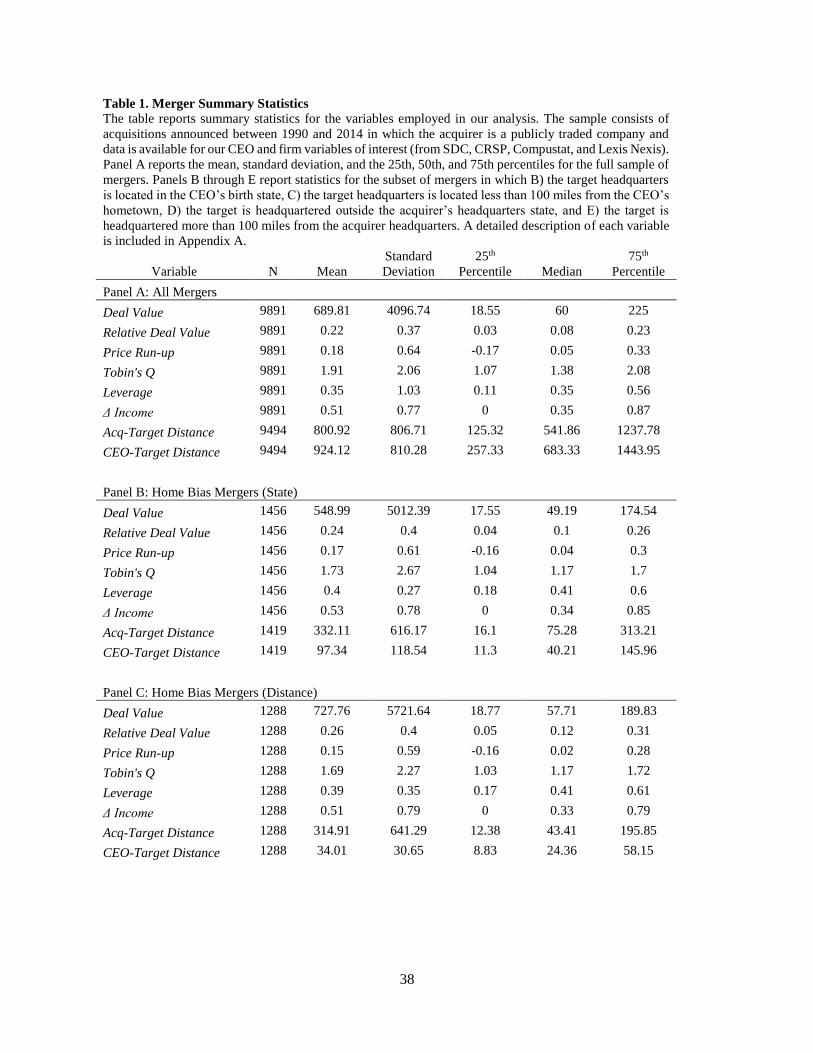

2.3 Sample Summary Statistics

Table 1 presents summary characteristics for the merger sample. The main

takeaway from the table is that deal size and firm characteristics are generally similar for

CEO home bias mergers and the full sample. Cross-state and faraway mergers also do not

differ materially from other types of mergers. Although there is overlap in our measures of

CEO home bias, the state and distance home bias measures do capture different samples.

For example, among the CEO birth state home bias mergers, the CEO grew up more than

100 miles from the target 34% of the time. Also, in 26% of the mergers in which the CEO

grew up within 100 miles of the target, they resided in a nearby state rather than in the

target state. The differences are greater among distant home bias mergers. Specifically,

only 64% of Faraway Home Bias State mergers are also Faraway Home Bias Distance mergers,

and 50% of Faraway Home Bias Distance mergers qualify as Faraway Home Bias State

mergers.10

3. CEO Home Bias and the Choice of Acquisition Targets

We begin by exploring the relation between the geographic location of CEO

upbringing and the location of corporate acquisitions. In particular, we examine whether

acquirer firm CEOs show a greater tendency to acquire targets from the same geographic

region as their birth place. Our approach is similar to Rhodes-Kropf and Robinson (2008),

10 The smaller number of observations for distance- vs. state-based mergers in Panel A (9494 vs 9891) is due

to state information on the target being available more often than zip code information (which we use to

determine distance).

11

and it involves comparing the likelihood of home bias mergers among the population of

actual mergers to a hypothetical sample of control mergers matched on firm characteristics.

For each acquisition, we select hypothetical acquirers from the set of CRSP-

Compustat firms that did not participate in a merger in a three-year window around the

announcement date of the actual merger. We only consider hypothetical acquirers that are

headquartered in the same state as the actual acquirer. This helps ensure that the distribution

of headquarter-states is the same for both actual and hypothetical targets. Additionally,

hypothetical acquirers are required to operate in the same industry as the actual acquirer,

based on the Fama-French 48 industry classification. We further narrow the set of

hypothetical acquirers by selecting those in the same market capitalization and book-to-

market ratio quintiles of the actual acquired firm.

Using this approach, we obtain a sample of 9,891 (9,494) actual acquisitions based

on state (distance), with an average of 43 (44) hypothetical candidates for each merger. For

our main analysis, we select a hypothetical acquirer firm that has the closest size and book

to market ratio to the actual acquirer.11 We then estimate the following probit regression

on the actual and hypothetical merger sample:

𝑃𝑟(𝑀 ∧ 𝐴 = 1| ∙) ∝ 𝑒𝑥𝑝(𝛼 + 𝛽1𝐻𝐵 + 𝛽2𝐹𝑎𝑟 + 𝛽1𝐻𝐵 × 𝐹𝑎𝑟 + 𝐼𝑛𝑑 + 𝑌𝑟 + 𝑆𝑡), (1)

where M&A is set equal to 1 for the actual mergers, HB is either Home Bias State or Home

Bias Distance, and Far is either Faraway State or Faraway Distance. By construction, the

unconditional likelihood of a home bias merger in the sample is 0.5.

11 In Section 5.1, we also consider simulations in which we randomly select one hypothetical candidate from

the size and book quintiles.

12

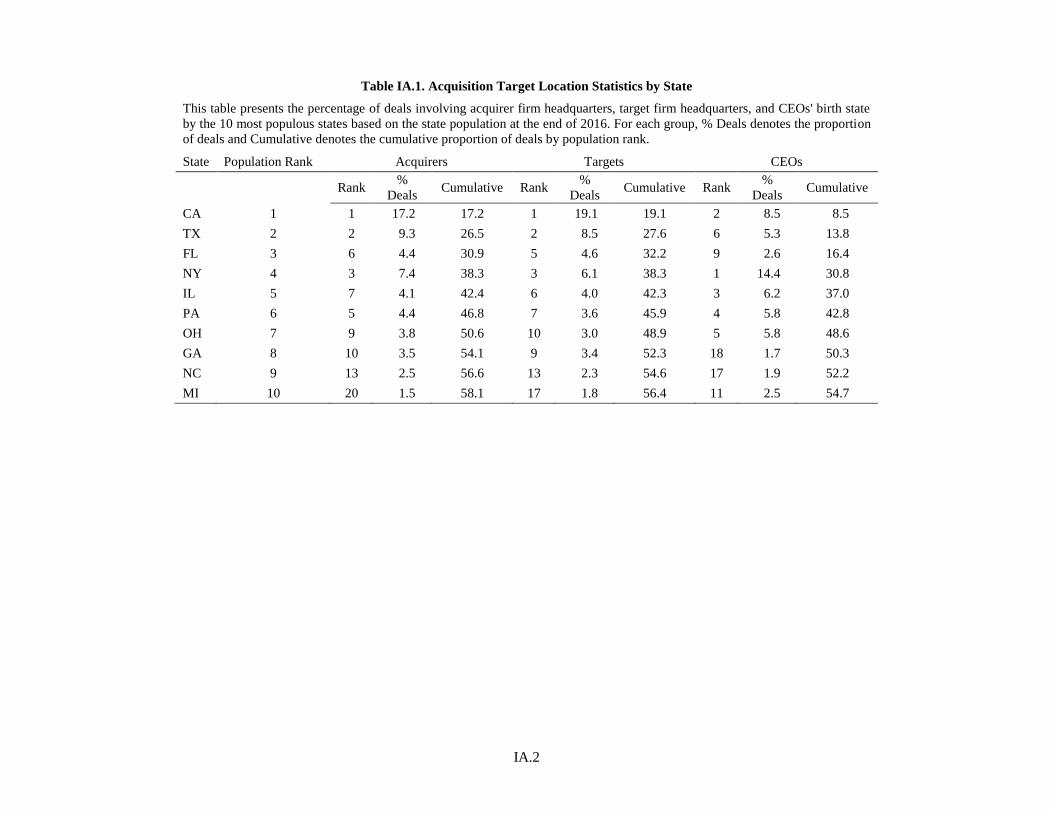

One potential concern with our approach is that CEO birth and firm locations are

not randomly distributed across states. In particular, the top 5 states in terms of population

represent 38% of total acquirer headquarter states, 38% of total target headquarter states,

and 31% of total CEO birth states (tabulated in Table IA.1 in the Internet Appendix). As a

result, state-specific shocks that affect the propensity or value of acquisitions, such as

industry merger waves, could produce spurious home-bias effects. We mitigate this omitted

variable problem by ensuring that the distribution of paired acquirer and target states is the

same for the actual and hypothetical acquisitions, as described above. Moreover, in

addition to year (Yr) and industry (Ind) fixed effects, we also consider state fixed effects

(St) for acquirers from the top five most populous states (California, Texas, New York,

Florida, and Illinois).

As in Rhodes-Kropf and Robinson (2008), our methodological approach does not

measure the probability that a given company will choose to engage in an acquisition.

Instead, the regressions estimate the likelihood that an actual acquirer-target pair will be

selected instead of its hypothetical counterpart. In principle, this matching strategy allows

us to identify the determining characteristics of acquirers without modeling the decision to

acquire.

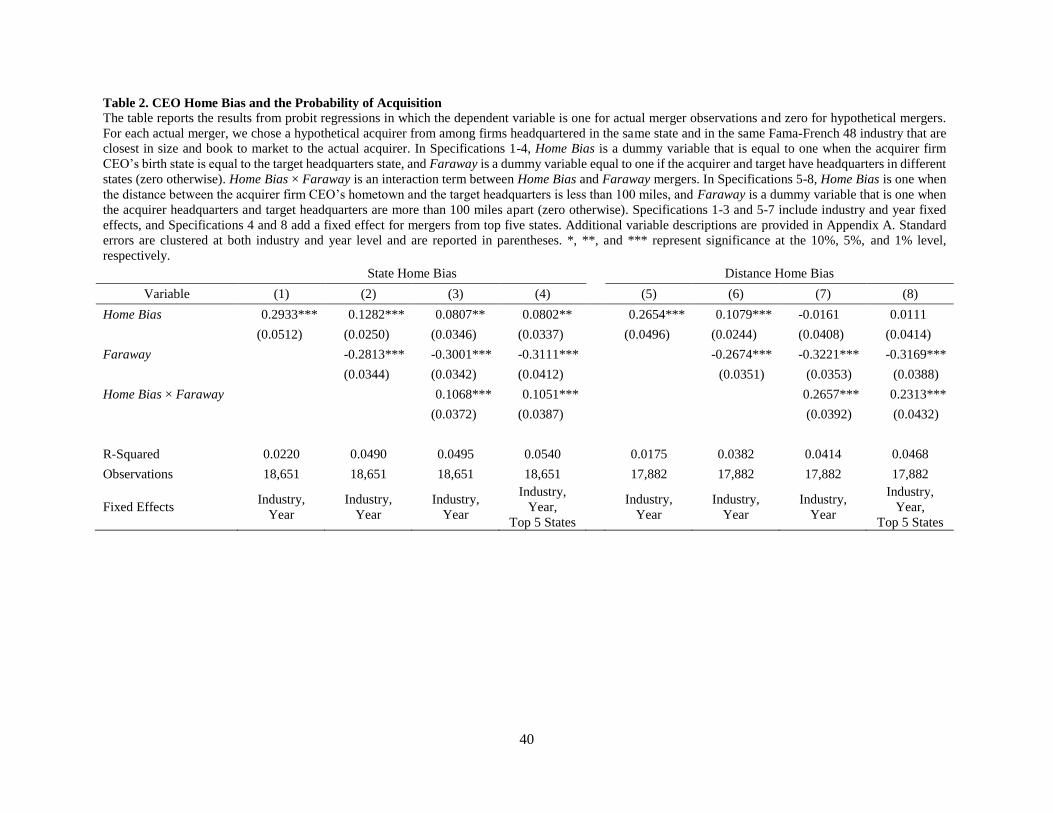

Table 2 reports the results from the probit regressions. The evidence indicates that

home bias mergers happen significantly more often than in the control group. In particular,

actual mergers are 29.3% more likely to be selected when the CEO grew up in the target

state and 26.5% more likely when the CEO grew up less than 100 miles from the target.

The coefficient on Faraway is significantly negative in all specifications, consistent with

close mergers being more likely than expected due to their industry, size, and book-to-

13

market alone. Our emphasis is on whether CEO upbringing serves to narrow the distance

between the acquirer and faraway targets, and we examine this relation by interacting

faraway and home bias measures in Specifications 3 and 6. We observe positive and

significant coefficients for the interaction terms, which indicates that the home bias effect

is stronger for faraway acquisitions. The findings are similar in magnitude when including

Top Five state fixed effects in Specifications 4 and 8. The evidence in Table 2 suggests

that CEO home bias mergers, and especially distant home bias mergers, occur more often

than expected by chance.

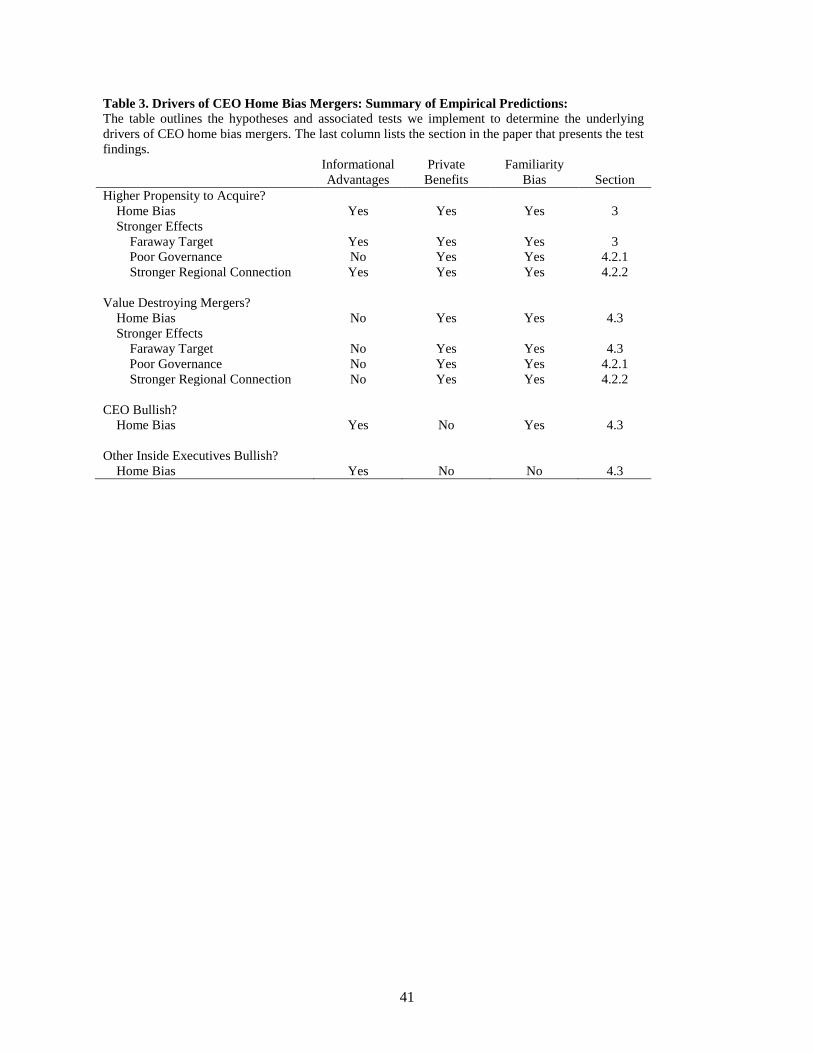

4. Drivers of CEO Home Bias Mergers: Information, Agency, or Familiarity

We consider three potential explanations for CEO’s proclivity for selecting targets

near their home region: beneficial informational advantages, managerial objectives such as

status seeking, and a cognitive bias toward the familiar. Table 3 outlines a series of tests

that we conduct to help differentiate between information, private benefits, and familiarity-

based explanations. The table presents a brief test description, the directional hypotheses,

and also the section headings for each test conducted below. We begin by examining bidder

announcement returns.

4.1 The Informational Advantages Hypothesis: Merger Announcement Return Evidence

The tendency for CEOs to invest in the region of their upbringing could be the result

of comparative advantages. For example, CEOs’ informational networks may cluster

geographically, which could lead to worthwhile investments (e.g. Cohen, Frazzini, and

Malloy, 2008; Cai and Sevilir, 2012). Cultural awareness of a geographic region may also

improve assimilation, which could also lead to more local mergers (Ahern, Daminelli, and

14

Fracassi, 2015). In this section, we examine bidder announcement returns to explore

whether home bias acquisitions reflect informational advantages.

We measure bidder announcement effects using market-model adjusted stock

returns around merger announcements as in Moeller, Schlingemann, and Stulz (2004),

Masulis, Wang, and Xie (2007), and Schmidt (2015). Market-model estimates are obtained

using the daily CRSP value-weighted index as the proxy for market returns. The estimation

period is from 230 days to 11 days before the announcement date, which is obtained from

SDC. We regress cumulative abnormal merger announcement returns on the CEO home

bias measures as follows:

𝐶𝐴𝑅𝑖 = 𝛼 + 𝛽1𝐻𝐵𝑖 + 𝛽2𝐹𝑎𝑟𝑖 + 𝛽1𝐻𝐵𝑖 × 𝐹𝑎𝑟𝑖 + 𝐶𝑜𝑛𝑡𝑟𝑜𝑙𝑠𝑖 + 𝐼𝑛𝑑 + 𝑌𝑟 + 𝑆𝑡, (2)

where CARi is the three-day cumulative abnormal return around the announcement date for

merger i, HB is either Home Bias State or Home Bias Distance, and Far is either Faraway State or

Faraway Distance. Each specification includes fixed effects for year and industry (Fama and

French 48 industries), and standard errors are clustered by both year and industry. We

control for extreme return outliers by winsorizing CARs at the 1st and 99th percentiles each

year.

We follow Schmidt (2015) in selecting control variables. We include Log Total

Assets to capture acquirer size, which has been shown to negatively affect bidder

performance (e.g. Moeller, Schlingemann, and Stulz, 2004). Tobin's Q also has a

documented negative effect on announcement returns (e.g., Lang, Stulz, and Walkling,

1991). We follow Masulis, Wang, and Xie (2007) and Gillan, Hartzell, and Starks (2011)

and use Industry Tobin’s Q rather than firm-level Tobin’s Q due to endogeneity concerns.

We also include Industry Leverage for similar reasons.

15

Shleifer and Vishny (1989) suggest that managers may enter new lines of business

when threatened by poor performance, a view supported by the evidence in Morck, Shleifer,

and Vishny (1990). We follow Morck, Shleifer, and Vishny (1990) and use the change in

operating income during the prior three years as a measure of performance (Δ Income). To

account for past performance of the bidder, we include Price Run-up, which is the bidder's

buy and hold abnormal return from 230 to 11 days before the announcement as in Masulis,

Wang, and Xie (2007).

Acquirer announcement returns have been shown to be related to the method of

payment and the type of target (e.g., Chang, 1998, Moeller, Schlingemann, and Stulz, 2004;

and Officer, Poulsen, and Stegemoller, 2009). To account for this variation, we include

controls for the type of target (a Public dummy variable) and the medium of payment (Cash

Deal and Stock Deal dummy variables). We also include Relative Deal Size to control for

the size of the deal. Appendix A provides more details regarding the construction of the

independent variables.

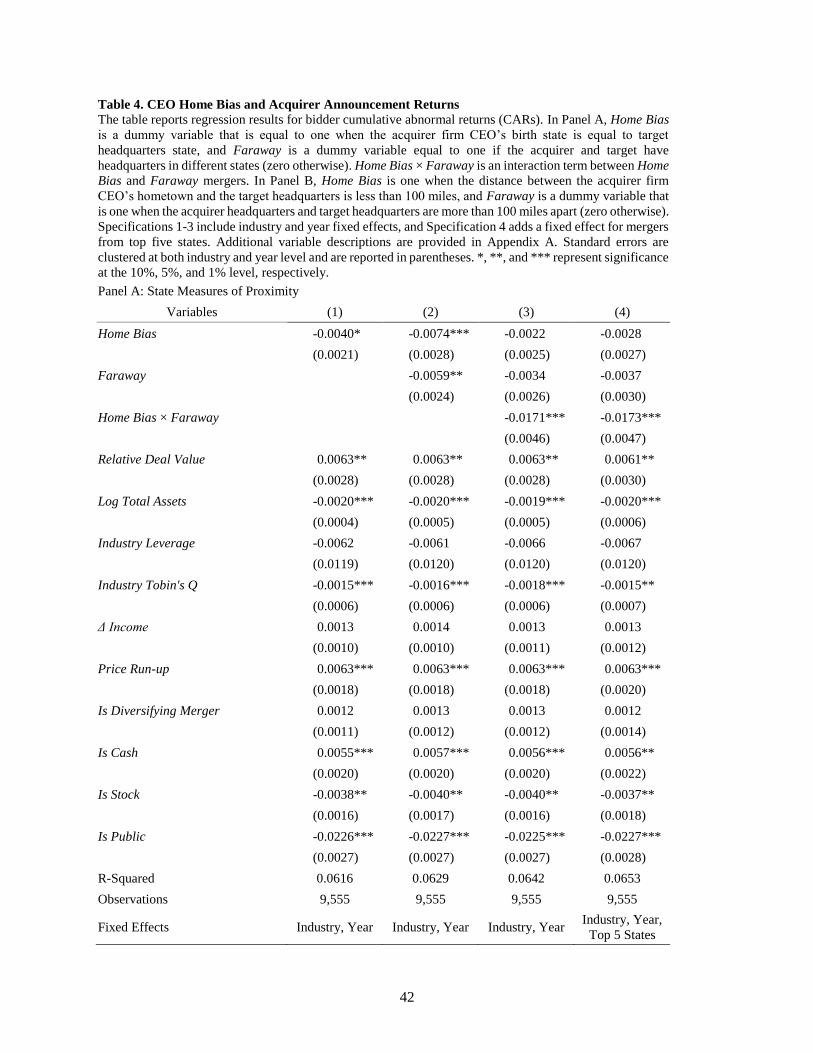

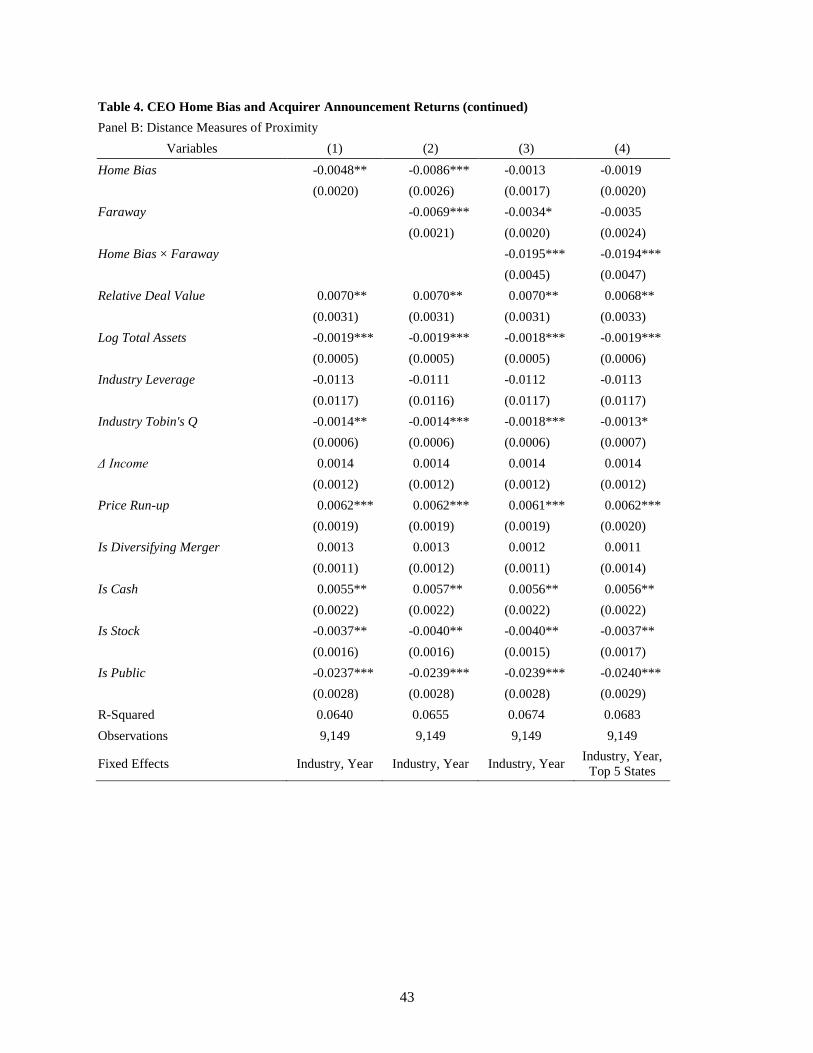

Table 4 reports the results from the bidder CAR regressions, with Panel A (B)

presenting the results for the state-based (distance-based) home bias measures. The first

specification in each panel includes the home bias indicator variable along with the set of

control variables. The coefficient on Home Bias is negative and statistically different from

zero for both measures. Specifically, when bidder firms announce the acquisition of a target

that is headquartered in the state where the CEO grew up, the market response is 0.40%

lower. The evidence from Panel B is similar. If the CEO grew up within 100 miles of the

target, the market response is 0.48% lower.

16

Including the interaction term between home bias and faraway mergers in

Specification 3 reveals that the negative announcement response to CEO home bias

acquisitions is stronger for more distant mergers. In particular, a cross-state merger in

which the bidder CEO grew up in the target state results in significantly lower

announcement returns, with an estimated coefficient of -1.71%. Similarly, announcing the

acquisition of a target greater than 100 miles away that is within 100 miles of the CEOs

birthplace also results in lower returns (-1.95%). The results are very similar after including

the fixed effects for Top Five states in terms of population.12

Another important finding that emerges from Table 4 is that the negative response

to distant mergers, -0.59% (-0.69%) on average for faraway mergers based on state

(distance), is concentrated among CEO home bias mergers. For the subset of faraway

mergers that do not exhibit CEO home bias, the announcement returns are considerably

less negative, at -0.34% for both cross-state and distant mergers. Moreover, the negative

response to non-home bias faraway mergers is no longer significant after the inclusion of

Top Five state fixed effects. Taken together, the evidence of a negative market reaction to

CEO home bias mergers in Table 4 does not support the view that these mergers reflect

valuable information obtained through the CEO’s network.

4.2 Home Bias Acquisitions: Corporate Agency and Familiarity Hypotheses

The negative market response to CEO home bias mergers is inconsistent with CEOs’

possessing important informational advantages when selecting targets in their home region.

If home bias acquisitions reflect managerial objectives or personal biases rather than value

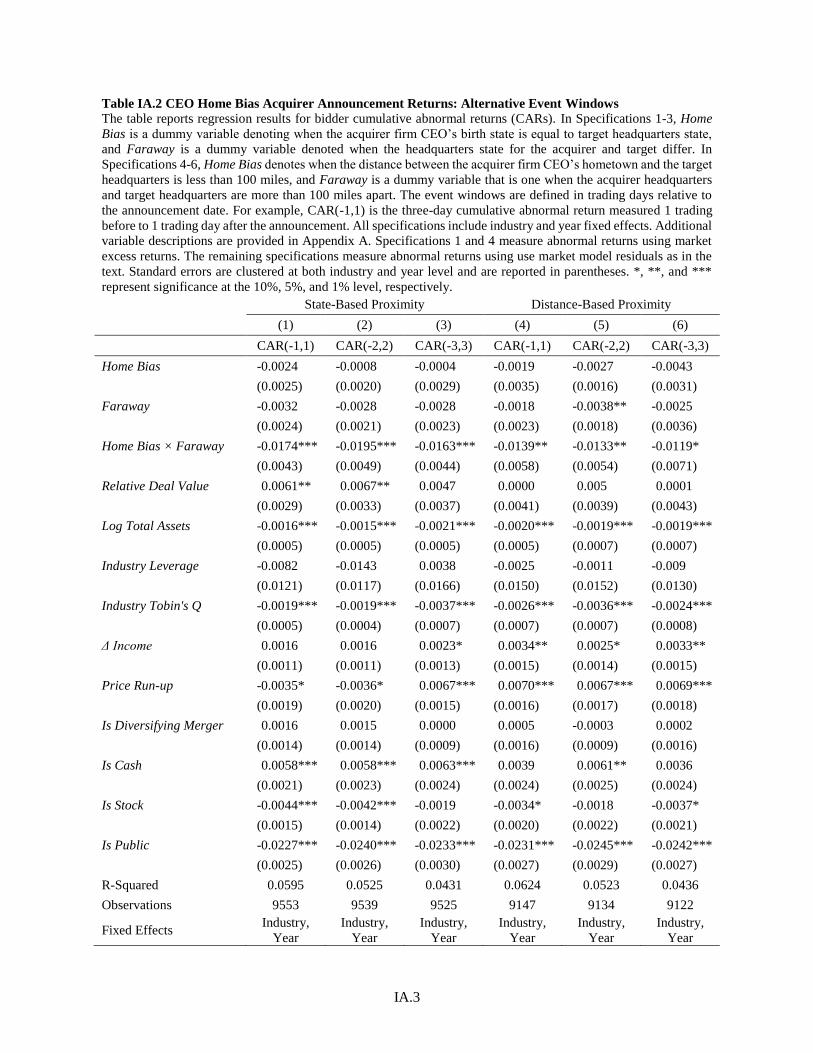

12 In Table IA.2 in the internet appendix, we repeat Table 3 using four- and six-day event windows and find

similar evidence. We also find similar evidence using excess returns rather than market model returns.

17

maximization, we would expect the practice to be more prevalent among poorly governed

firms and when CEOs have a stronger connection to their home region.

4.2.1 Strength of Connection Evidence

If the effect of CEO birth region on merger activity reflects manager preferences or

a bias towards the familiar, we conjecture that it will be stronger when the CEO has a

deeper connection to their home region. We explore this hypothesis using measures of

strength of connection based on CEOs’ educational backgrounds and residence histories.

First, we gather information on CEOs’ educational backgrounds provided by Boardex, and

we find the location of each institution of higher education using data from the U.S.

Department of Education.13 We define a strong education connection if the acquirer firm

CEO attended an institution of higher education within their home state for the state-based

home bias measure, and if the college was within 100 miles of their hometown for the

distance-based home bias measure.

Our second strength of connection measure is based on each CEO’s residence

history. The Lexis Nexis database provides address histories for each person beginning in

their early- to mid-twenties. In our sample, roughly 65% of each CEO’s past address

history became available between the ages of 18 and 25. We conjecture that CEOs who

continued to live in their home state or hometown for ten or more years in adulthood will

hold stronger connections to their home region. We define state- and distance-based

dummy variables accordingly.

13 http://ope.ed.gov/accreditation/GetDownLoadFile.aspx.

18

The propensity results using proxies for a CEO’s strength of connection to his or

her birth region are presented in Table 5. For both of the strength of connection proxies,

we find a significantly greater propensity for home bias mergers for CEOs with strong

home region connections. For example, the interaction term between home bias and strong

connection indicates a 21.8% higher probability of acquiring a target firm located in their

birth state for CEOs who also attended a college in their home state. The evidence is similar

for the residency strength of connection measure, with home bias mergers being 10.96%

more likely when the CEO maintained residency during adulthood for ten or more years in

the region of the target.

In Table 6, we repeat the bidder return analysis in Table 4 after including the

strength of connection interaction terms. As expected, CEO home bias mergers in which

the CEO has more than ten years of residency in adulthood in the target state (100-mile

region) exhibit 3-day bidder CARs of -2.23% (-1.59%), and the estimate is significantly

different from zero at the 5 (1) percent level. We find similar negative response patterns

when we measure strength of connection using CEOs’ educational backgrounds. As can be

seen from the second and fourth specifications, home bias mergers engaged in by CEOs

who attended an institution of higher education located in their birth state show negative

3-day CARs that vary from -1.09 to -0.68%.14 The evidence that home bias mergers are

more prevalent and greeted less warmly by the market when the CEO has a deeper

14 A potential complication arises when we consider foreign-born CEOs who may not exhibit the same degree

of connection to their U.S. home state. Yonker (2016a) classifies CEOs who obtain SSNs after age 21 as

“foreign.” Using this approach, we classify 293 CEOs as foreign, representing roughly 8% of the CEO

population. We might expect foreign CEOs to exhibit a less strong connection with their U.S. home state,

particularly when the connection is not established until adulthood. Consistent with this view, in untabulated

analysis we find evidence of insignificant negative three-day announcement returns when foreign CEOs

engage in home bias mergers.

19

connection to his or her home region is consistent with home bias mergers reflecting

manager preferences or a bias towards the familiar.

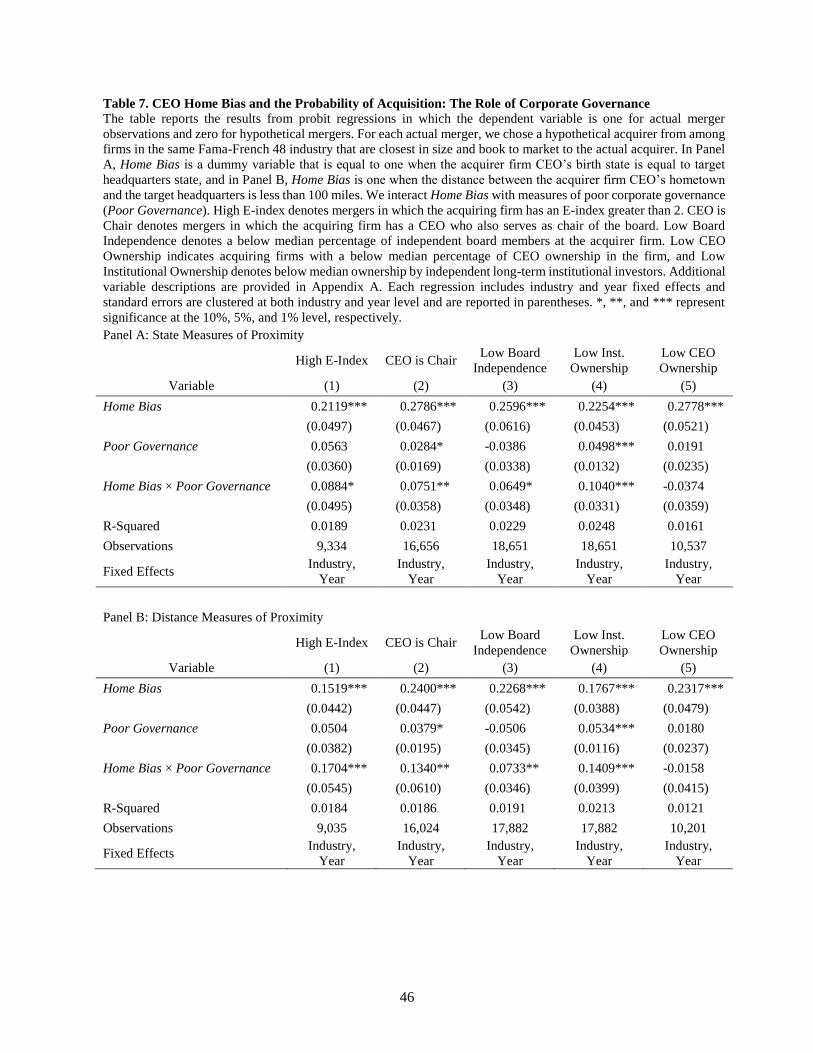

4.2.2 Corporate Governance Evidence

Masulis, Wang, and Xie (2007) find that entrenched managers are less susceptible

to market discipline and may therefore be more likely to engage in value-destroying

acquisitions. In this subsection, we examine whether CEOs of poorly governed firms are

more likely to engage in home bias mergers, and we analyze whether these mergers are

more poorly received by the market on announcement.

We consider several proxies to identify poorly governed firms. Our first governance

measure is the entrenchment index (E-index) of Bebchuk, Cohen, and Ferrell (2009), which

is based on shareholder voting provisions and takeover defenses, such staggered boards

and poison pills. We next consider a dummy variable for when the CEO is also the board

chair, as past literature has found evidence that CEO/chairman duality is associated with

higher CEO compensation (Core, Holthausen, and Larcker, 1999), lower sensitivity of

CEO turnover to firm performance (Goyal and Park, 2002), and a greater likelihood of

participating in merger waves (Duchin and Schmidt, 2013).

Our next corporate governance measure is related to board independence. Byrd and

Hickman (1992) find evidence that independent boards are associated with higher quality

mergers, and following Weisbach (1988) we construct a dummy variable to capture firms

in which independent directors comprise a minority on the board. Finally, we also consider

ownership by independent long-term institutions. Chen, Harford, and Li (2007) find that

greater institutional ownership is associated with stronger post-merger performance, which

they attribute to the active external monitoring role of independent investors. For the

20

holdings-based and E-index governance measures, we use the median level to divide the

acquisition sample into well- and poorly-governed groups.

Table 7 repeats the probit analysis from Table 2 after including the series of

corporate governance measures, with Panel A (B) providing results for the state-based

(distance-based) home bias variables. In particular, we add interaction terms between the

Home Bias variables with dummy variables that are equal to one if the acquiring firm falls

into the low governance category for each of the corporate governance variables (zero

otherwise). Our objective is to analyze the incremental effect of low governance on the

probability of acquisition.

The home bias coefficients in Table 7 are considerably larger among low

governance firms, consistent with a greater propensity that a target will be selected from

near the acquirer CEO’s birthplace if the acquiring firm is poorly governed. For example,

firms with a high E-Index show a 15.06% higher probability of acquisition if the target

firm is located in the same region as the CEO birth region. We also find significant

interaction terms for CEO is Chair, Low Board Independence, and Low Institutional

Ownership, for both state and distance-based home bias measures.15

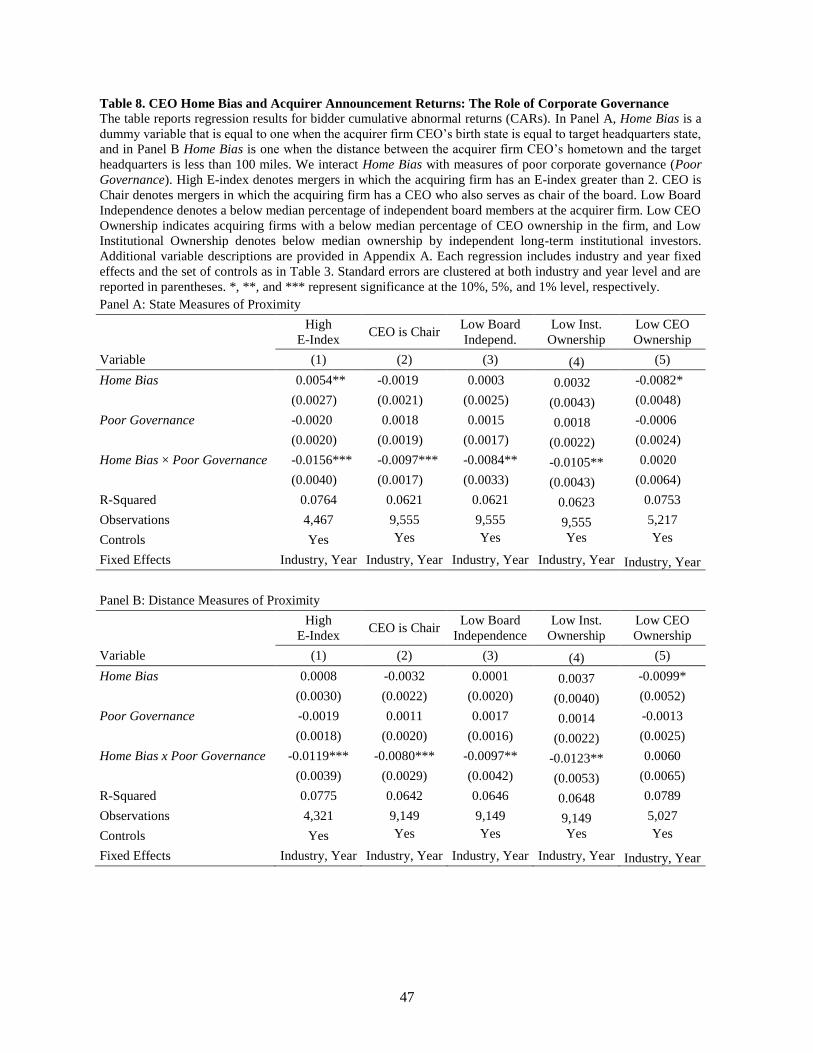

In Table 8, we test our hypothesis that home bias mergers are more likely to be

perceived negatively by the market when conducted by poorly governed firms. The table

provides bidder return results, as in Table 4, interacted with the set of poor governance

measures. Consistent with home bias mergers being influenced by manager preferences,

we find negative and significant coefficients for Poor Governance home bias mergers. The

15 Consistent with Duchin and Schmidt (2013), we also observe a greater likelihood of mergers in general

among poorly governed firms, suggesting poorly governed firms are more likely to participate in mergers.

21

economic magnitude varies from -0.80% to -1.56% depending on which governance

variable we use and whether home region proximity is measured using state or distance,

but we find strong and consistent evidence that the reaction to home bias mergers

conducted by poorly governed firms is more negative than those conducted by well

governed firms. The evidence that the negative market effect of home bias mergers is

stronger among poorly governed firms helps confirm the evidence that investment

decisions of home bias CEOs are affected by reasons other than information advantages.

If home bias mergers are driven by agency considerations alone, with CEOs fully

recognizing that home region targets are unlikely to create value, then we might expect

fewer home bias mergers and more favorable market responses when the CEO’s incentives

are more closely aligned with investors. We explore this conjecture using the low CEO

ownership stake measure of Jensen and Meckling (1976), with low CEO ownership

indicating less alignment with investors and a greater risk of agency-motivated mergers.

We create a dummy variable for whether the CEO’s ownership is below the median level

in the sample, and we interact Low CEO Ownership with home bias as with the governance

measures above.

The CEO ownership results are reported in the last column of Tables 7 and 8. We

observe no evidence of a significant relation between Home Bias and Low CEO Ownership

for either the likelihood or market response analysis, which suggests agency may not be

the primary driver of home bias mergers. In the next subsection, we explore CEO

ownership more thoroughly by examining insider trading around CEO home bias mergers.

4.3 Discriminating Between Agency and Familiarity: Insider Trading Evidence

22

Our findings suggest that markets react negatively to CEOs’ proclivity toward

home bias mergers, especially for distant targets. The evidence is consistent with a bias for

the familiar that leads to over-optimism regarding the value of the merger. On the other

hand, it is possible that CEOs understand that these mergers are inefficient, and yet engage

in them as a type of rent seeking behavior. The evidence that markets react more negatively

to home bias mergers when the firm is poorly governed, as well as when the CEO has a

stronger connection to their birth state, is consistent with both interpretations.

In order to test whether home bias mergers are more consistent with familiarity bias

or a pet project motivation, we examine insider trading by CEOs. If CEOs understand that

home bias mergers are inefficient but engage in them for private benefits, we would expect

a smaller investment in their company stock following the merger announcement compared

to non-home bias mergers. However, if familiarity leads CEOs to be unduly optimistic

about the prospects of the merger, we would be more likely to observe home bias CEOs

buying company stock. We also examine board members and other executives’ trading

behavior as a benchmark which can be compared with the behavior of CEOs.

For each acquisition, we consider a transaction window that begins two days after

the announcement date and ends 60 days after the announcement or the effective date,

whichever comes first. We then compute the market value of shares traded by the CEO,

Top Executives, and Board members during each day in the transaction window.16 If each

group has a positive (negative) average value of shares traded over the transaction period,

16 We take the cross-sectional mean of the group for each date and sum over the window to define whether

the group made a purchase. We find similar results using an alternative approach in which we look at the

largest trade executed during the transaction window and assign a purchase or sell for each group based on

that largest trade. Results are also similar when excluding insiders from the board member group.

23

we classify them to have purchased (sold) shares. Finally, we create three dummy variables

to describe each group’s average trading behavior. We define two additional dummy

variables to identify cases in which the CEO purchases shares on average but other top

executives do not buy (CEO Buys, Top Execs do not Buy), and the case in which the CEO

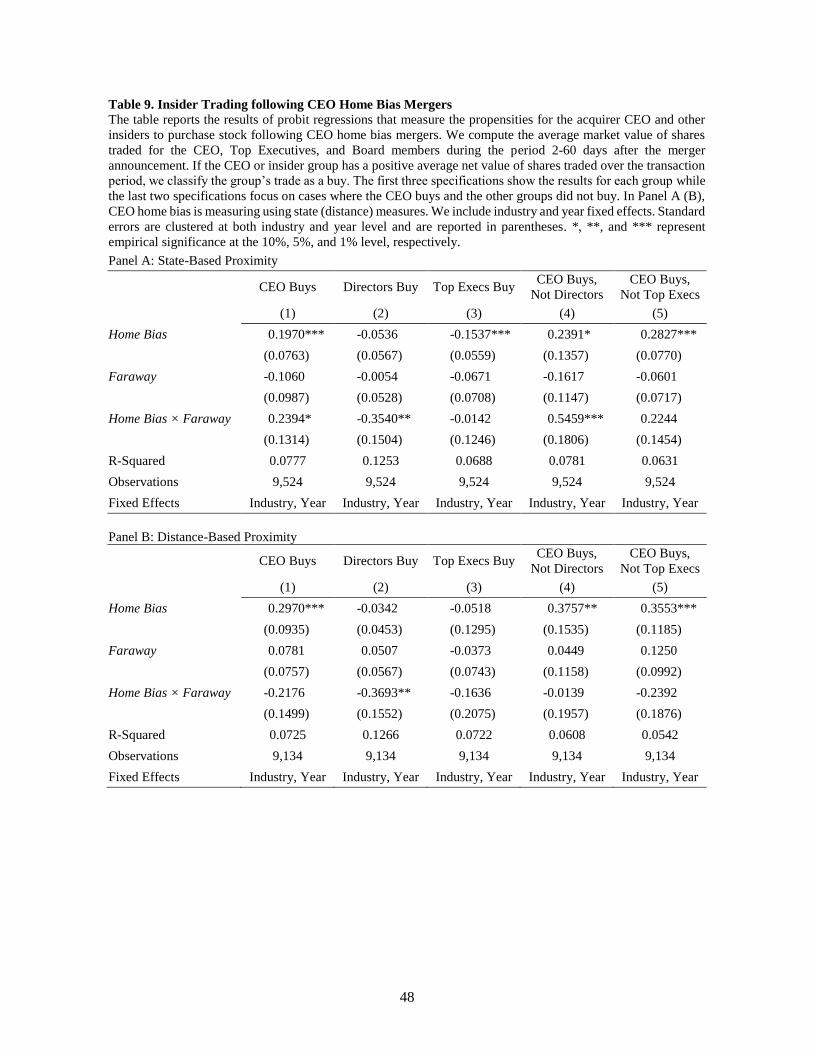

bought shares but other directors did not (CEO Buys, Directors do not Buy).

We estimate probit regressions that measure the propensities for the acquirer CEO

and other corporate insiders to purchase stock following CEO home bias mergers. The

results are reported in Table 9. Consistent with the familiarity bias hypothesis, in Panels A

and B we find CEOs of home bias mergers are significantly more likely to purchase

company stock following the deal announcement for both close and faraway home bias

acquisition. On the other hand, we observe the opposite purchasing pattern for directors

and other executives. The table shows directors and other executives are more likely to sell

following home bias acquisition announcements.

In Specifications 4 and 5, we examine mergers in which CEOs appear to be alone

in their optimism. Specifically, we consider mergers where CEOs purchase shares after the

announcement, but directors and other executives do not purchase shares. The evidence

indicates that optimism exhibited by the CEO alone is much more likely to occur for home

bias mergers than non-home bias mergers. For example, for close mergers, the probability

of home bias CEOs purchasing and other executives not purchasing is 23.91% greater when

compared to non-home bias cases.

The evidence that CEOs are more likely to purchase shares following home bias

mergers, without similar evidence among other firm insiders, is consistent with CEOs

being overly optimistic about the success of targets headquartered near their home regions.

24

CEO optimism is consistent with home bias mergers reflecting a bias toward the familiar

rather than private benefits and agency considerations.

5. Robustness and Additional Analysis

In this section, we provide a series of robustness checks which consider alternative

approaches for measuring the likelihood of CEO home bias acquisitions and their

announcement effects. We also present evidence for the subset of mergers with public

targets, and we analyze measures of overconfidence to help rule out general overconfidence

among home bias CEOs.

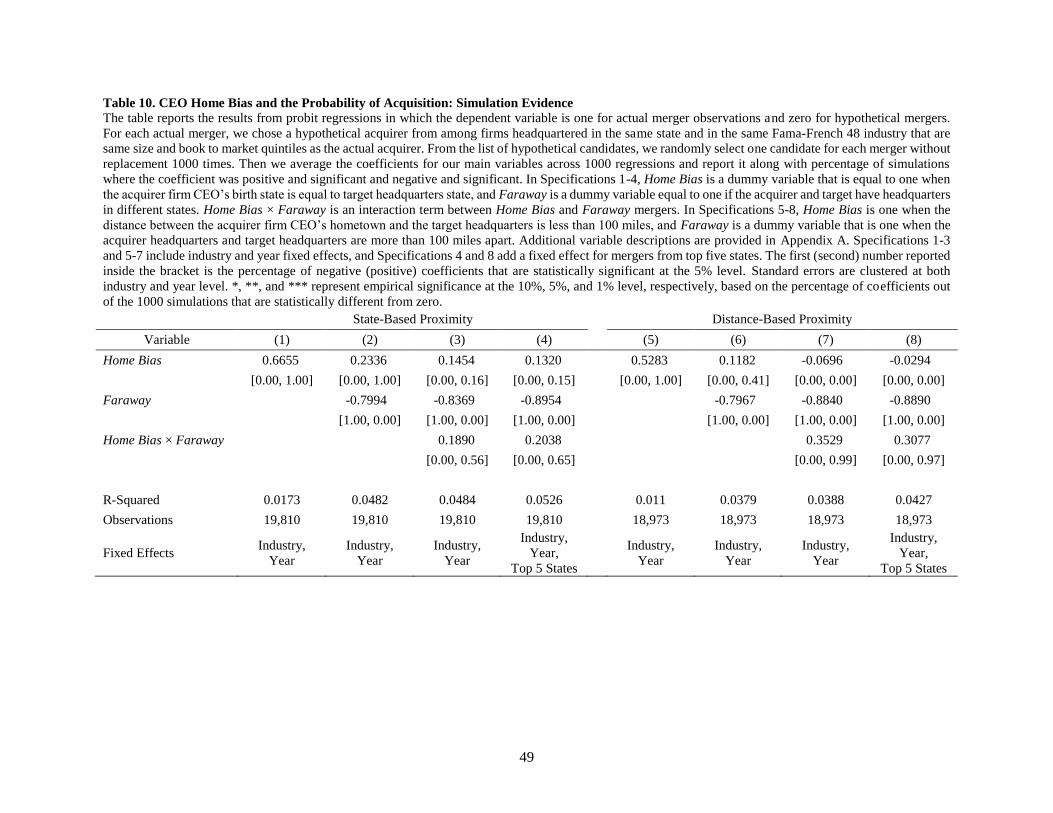

5.1 Simulation Evidence

The probit analysis in Table 2, which examines the propensity of CEOs to engage

in home bias mergers, compares actual mergers to hypothetical mergers with potential

bidders matched on industry, state headquarters, and the closest match on size and book to

market. Although we include year and industry fixed effects as well as a fixed effect for

whether the bidder resides in a Top Five population state, concerns may remain that our

findings are sensitive to the specific hypothetical merger chosen. As a robustness check,

we choose one firm randomly from the set of hypothetical bidders matched on industry,

and size and book-to-market quintiles (rather than the single closest size and book-to-

market match as in Table 2). We then estimate the probit model in Equation (1), draw again

randomly, and repeat the process 1000 times.

The likelihood simulation results are presented in Table 10, with state-based

measures of home bias in Specifications 1-4 and distance-based measures in Specifications

5-8. Consistent with the evidence in Table 2, we find significant evidence of CEO home

bias in target selection. For example, in Specifications 1 and 5, the average home bias

25

coefficients are statistically significant and positive for all 1,000 simulations, suggesting

that actual home bias mergers occur more often than expected.

We also consider a simulation approach for estimating the market reaction to home

bias mergers. In particular, for each home bias merger, we randomly select a matching non-

home bias merger in which the bidder resides in the same state (for state-based proximity)

or the same 100-mile region (distance-based proximity). This drops the sample size

considerably, as the simulated samples are comprised of half home bias mergers and half

non-home bias mergers. We then estimate the regressions in as in Table 4 with the full set

of controls, draw again randomly, and repeat this process 1000 times.

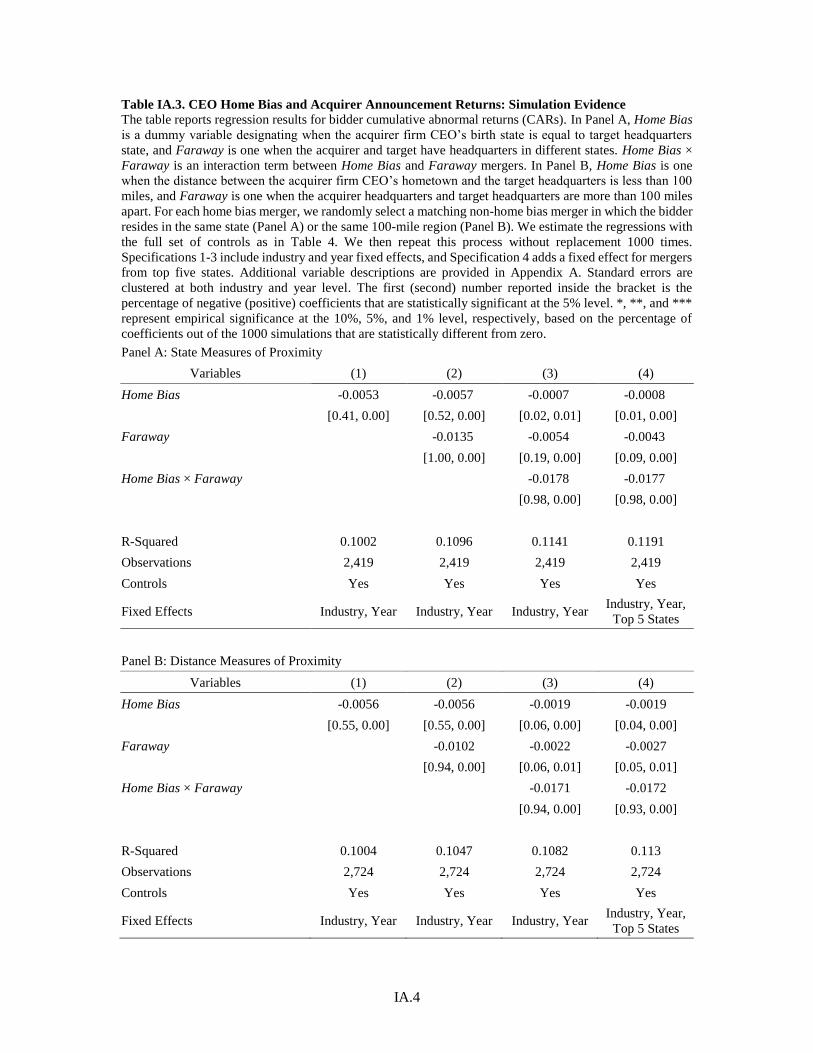

The regression simulation results are reported in Table IA.3 in the Internet

Appendix. The home bias coefficients in Specification (1), -0.53% for state measures and

-0.56% for distance measures, are larger than the analogous coefficients in Table 4, but

they are weaker statistically, with 41% (55% for Home Bias Distance) of the regressions

leading to significant coefficients (none of the estimates were negatively significant). The

announcement effect for faraway home bias mergers is very similar to the evidence in Table

4, with announcement returns of -1.77% for state-measures and -1.72% for distance

measures, and the estimates are significant in no fewer than 93% of the simulation

regressions.

5.2 Calendar Time Announcement Returns

A potential concern regarding the interpretation of the announcement response

coefficients in Table 4 (and Tables 6 and 8) is that our approach relies on bidder

announcement returns, whereas it is possible that the market initially incorrectly assesses

the relative merits of home bias mergers. In Table 11, we estimate the longer-term effects

26

of CEO home bias on the value of the firm using a calendar time approach which is less

susceptible to econometric issues (Barber and Lyon, 1997). The calendar time strategy

involves buying each home bias merger beginning three days after the announcement and

holding for 6, 12, and 24 months. For non-home bias mergers, we sell the acquirer and buy

the risk-free asset and hold for 6, 12, and 24 months. We use the Fama-French 3-factor

model, Fama-French-Carhart 4-factor model, and CAPM to risk-adjust returns, and report

the monthly alpha for the set of home bias mergers.

The evidence in Table 11 does not support the view that the initial negative reaction

to home bias deals reflects misreaction. Abnormal returns of buying home bias mergers

and selling non-home bias mergers are negative on average and statistically significant for

up to 12 months. In particular, the long-short strategy yields roughly 30bps per month for

the 12 months following the deal announcement, depending on the proxy for home bias.

We find a similar pattern when we restrict our focus to faraway mergers and when

measuring abnormal performance using CAPM or the Fama-French-Carhart 4-factor

model.

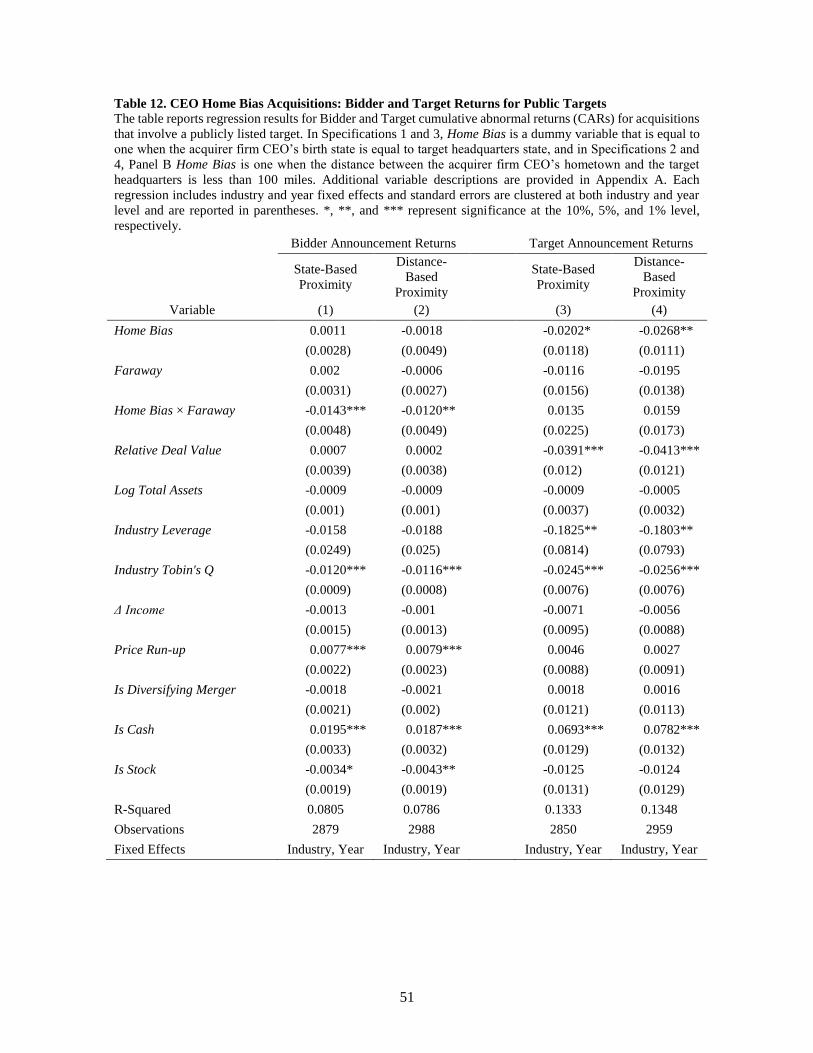

5.3 Announcement Returns for Public Targets

In Table 12, we focus on the subset mergers with publicly traded targets, and we

examine bidder as well as target returns following merger announcements. We use the

same set of controls as in Table 2 and include year and industry fixed effects. Consistent

with past literature, we observe a negative market response on average for acquirers when

the target is publicly traded. Moreover, distant home bias mergers continue to be poorly

27

received by the market, with bidder firms experiencing 1.2-1.4% lower announcement

returns.17

For the subset of public target mergers, we are able to explore whether home bias

CEOs pay larger takeover premiums by examining the target price announcement response.

Columns 3 and 4 of Table 12 report regressions of the public target 3-day price responses

using the same set of controls as for bidder returns. Although neither coefficient is

significantly different from zero, the coefficients for faraway home bias targets are positive

for both state-based and distance-based measures, which is generally consistent with

paying a premium for distant home bias targets.

5.4 Ruling out General Overconfidence Among Home Bias CEOs

The insider trading evidence in Table 9 is consistent with excess optimism among

CEOs when investing near their birth region. A possible alternative explanation is that

CEOs that engage in home bias mergers tend to be overconfident in general. Measures of

CEO overconfidence have previously been linked to merger activity (Malmendier and Tate,

2008). If overconfidence is related to home bias investing, our findings may be capturing

overconfident CEOs engaging in value destroying acquisitions.

If home bias acquisitions are driven by perennially overconfident CEOs, we would

expect these CEOs to be generally more likely to purchase shares of their own stocks than

other insiders. We therefore perform a placebo test of insider trading in which we analyze

17 In contemporaneous work, Jian, Qian, and Yonker (2016) find evidence of a positive market response to

in-state, home bias public target mergers. Their sample is taken from ExecuComp for 1992-2014, which

generally covers S&P 1500 firms (S&P 500 firms for 1992-1993). We broaden the merger sample to also

include smaller public acquirers listed in BoardEx from 1990-2014, and our sample of public target mergers

is roughly twice as large. The evidence in Jian, et al. (2016) is consistent with larger acquirers being less

likely to engage in value destroying home bias mergers, perhaps due to better monitoring.

28

CEOs’ trading behavior two years prior to the announcement of an acquisition, and

examine whether (future) home bias CEOs are more likely to purchase stock than other

company insiders.

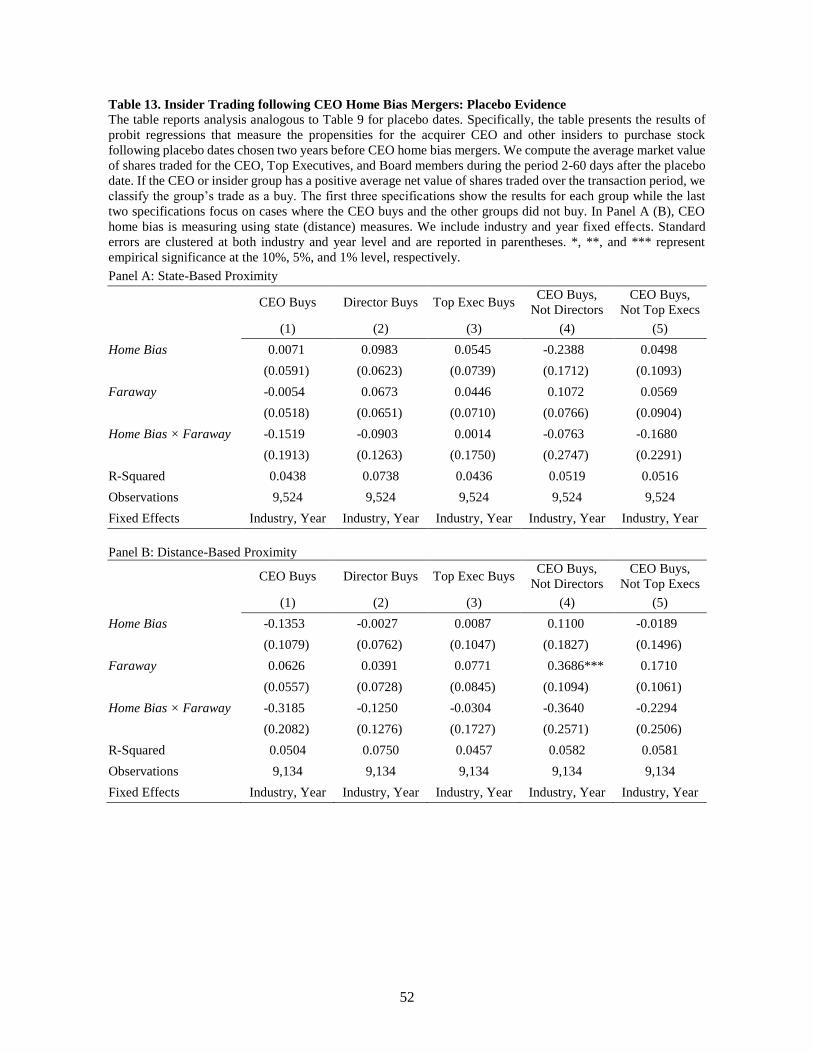

In Table 13, we report results of insider trading by CEOs, directors, and top

executives during the placebo period. For both state- and distance-based home bias

variables, we no longer observe the same pattern as in Table 9. In particular, we find no

evidence that CEOs are more likely than other company insiders to purchase their own

stock during the placebo period, which is inconsistent with general overconfidence among

home bias CEOs.

The placebo analysis considers trading over a relatively short, 60-day window. We

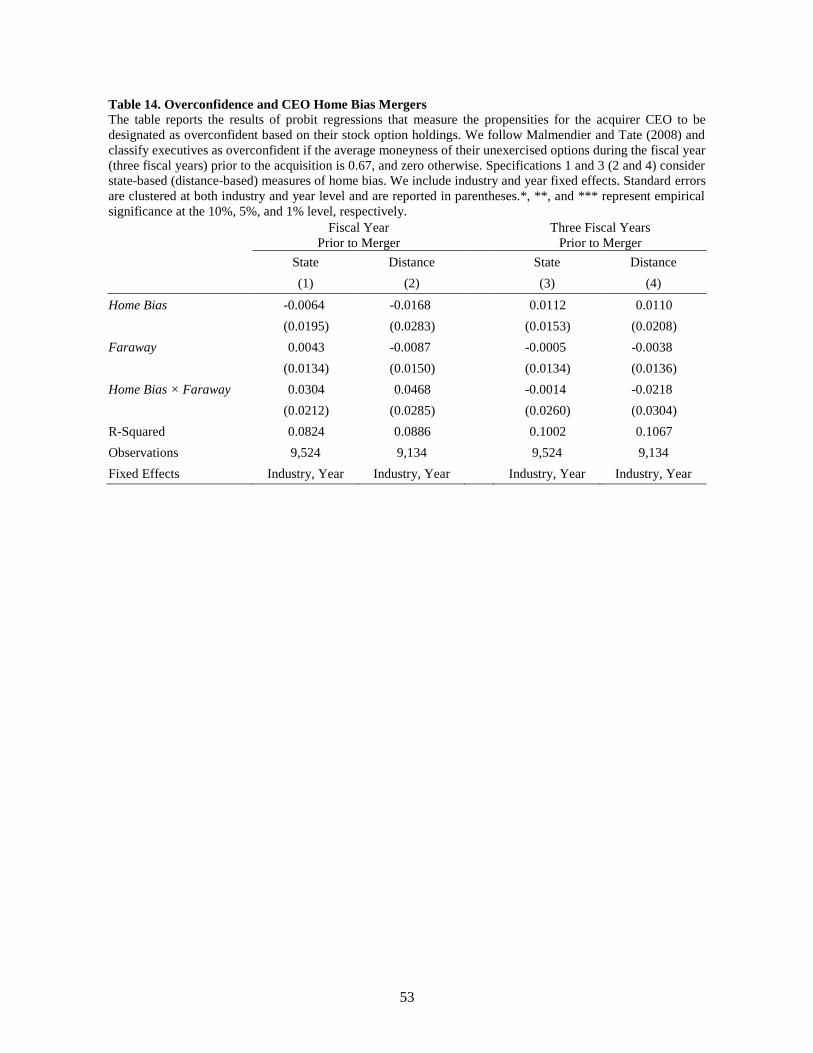

further explore the conjecture that home bias CEOs may be generally overconfident by

examining overconfidence measures based on the moneyness of their unexercised options

(Malmendier and Tate, 2008). Specifically, we classify executives as overconfident if the

average moneyness of their unexercised options during the fiscal year prior to the

acquisition is 0.67, and zero otherwise. We estimate similar probit analyses and present the

evidence in Table 14. For both state- and distance-based home bias variables, we find no

evidence that CEOs are more likely to be overconfident in the year prior to home bias

acquisitions. Taken together, the placebo insider trading and overconfidence evidence

supports the view that CEO’s are uniquely optimistic about investing near the birth region.

6. Conclusions

We consider CEOs’ regional upbringing as a source of deep-seated familiarity, and

we explore whether a CEO’s birth state location influences the firm’s acquisition behavior.

We find evidence that CEOs are significantly more likely to acquire targets from their birth

29

region, and the effects are stronger when the CEO does not currently live near their

hometown. We follow up the initial analysis with a number of tests to help determine

whether CEO home bias mergers reflect beneficial information advantages or are instead

driven by inefficient managerial objectives such as private benefits or an underlying bias

towards the familiar.

We find evidence of negative acquirer market responses to CEO home bias mergers.

For example, the market response to faraway home bias mergers is 1.71-1.95% lower than

non-home bias mergers, and the differences are statistically significant after controlling for

firm and deal characteristics. The negative announcement effect of home bias mergers is

stronger when the CEO has a deeper connection to his or her birth state. The effect is also

stronger among poorly governed firms, which is consistent with these projects reflecting

manager preferences rather than informational advantages.

We help distinguish whether home bias mergers reflect agency considerations and

private benefits to the CEO such as status seeking, or excess optimism through an

underlying bias toward the familiar, by studying how CEOs and other insiders trade

following home bias merger announcements. We find evidence that CEOs are significantly

more likely to purchase company shares following home bias acquisition announcements,

consistent with familiarity-driven optimism interpretations rather than explanations related

to private benefits.

Our findings present compelling evidence that CEOs are more likely to invest in

their home regions through acquisitions. Our findings of a familiarity-oriented home bias

are consistent with evidence from mutual funds managers and credit rating analysts, and

30

support the interpretation that familiarity can lead to misplaced confidence in firm

investment.

31

Appendix A: Variable Definitions:

Measures of Home Bias and Proximity

Home Bias – Denotes either Home Bias State or Home Bias Distance

o Home Bias State – A dummy variable that is equal to one when the acquirer firm

CEO birth state is the same as the target headquarters state, zero otherwise.

o Home Bias Distance – A dummy variable that is equal to one when the distance

between the acquirer firm CEO’s home town and the target headquarters

location is less than 100 miles, zero otherwise.

Faraway – Denotes either Faraway State or Faraway Distance

o Faraway State – A dummy variable that is equal to one when the acquirer

headquarters state is different from target headquarters state.

o Faraway Distance – A dummy variable that is equal to one when the distance

between acquirer firm CEO’s hometown and the target headquarters location is

less than 100 miles.

Home Bias × Faraway – The interaction between Home Bias and Faraway.

Interaction Effects

Strong Connection – A variable that denotes either Attended College or Long-Time

Resident

o Attended College – A dummy variable that is equal to one if the acquiring firm

CEO obtained a degree from institution of higher education that is located in

their birth state (state measures), or within 100 miles of the CEO’s hometown

(distance measures), zero otherwise.

o Long-Time Resident – A dummy variable that is equal to one if the acquiring

firm CEO lived in their birth state/hometown for more than 10 years after they

reach adulthood, zero otherwise.

Poor Governance – A variable that denotes one of the following corporate governance

measures:

o High E-Index – A dummy variable that is equal to one if the entrenchment index

of Bebchuk, Cohen and Ferrell (2009) is above 2 (the median), zero otherwise.

o CEO is Chair – A dummy variable that is equal to one when the CEO is also

the chair of the board, zero otherwise.

o Low Board Independence – A dummy variable that is equal to one when less

than 50% of the board is comprised of independent directors, zero otherwise.

o Low CEO Ownership – A dummy variable that is equal to one when the CEO

ownership stake in the firm is below median using the measure, zero otherwise.

o Low Inst. Ownership – A dummy variable that is equal to one when the acquirer

firm’s institutional ownership is below the median, zero otherwise. Institutional

ownership is measured as the (industry-adjusted) proportion of shares

32

outstanding (in percent) in the hands of US independent, non-transient, long-

term institutional investors (Chen, Harford, and Li, 2007).

Insider Trading Measures

CEO Buys – A dummy variable that is equal to one if the acquirer CEO has a positive

average market value of shares traded (bought less sold) during the period two days

after the merger announcement date to effective date or 60 days after the announcement,

whichever comes first (zero otherwise).

Directors Buy – A dummy variable that is equal to one if the acquirer firm (non-CEO)

directors have a positive average market value of shares traded (bought less sold)

during the period two days after the merger announcement date to effective date or 60

days after the announcement, whichever comes first (zero otherwise). We take the

cross-sectional mean of the group for each date and sum over event window.

Top Execs Buy – A dummy variable that is equal to one if the acquirer firm (non-CEO)

top executives have a positive average market value of shares traded (bought less sold)

during the period two days after the merger announcement date to effective date or 60

days after the announcement, whichever comes first (zero otherwise). We take the

cross-sectional mean of the group for each date and sum over the event window.

CEO Buys, Not Directors – A dummy variable that is equal to one when CEO Buys

equals one and Directors Buys equals zero, zero otherwise.

CEO Buys, Not Top Execs – A dummy variable that is equal to one when CEO Buys

equals one and Top Exec Buy equals zero, zero otherwise.

Control Variables

Δ Income (x100) – Industry-adjusted three-year income growth, defined as log(It-1) –

log(It-4), where It-1 is the sum of net income, interest, and deferred taxes for the fiscal

year preceding the announcement (Morck, Shleifer and Vishny, 1990).

Cash Deal – A dummy variable that is equal to one when the acquisition is financed

entirely with cash.

Industry Leverage – Acquirer's industry median leverage across all Compustat firms

classified using four-digit standard industrial classification (SIC) codes. Leverage is

defined as representing the sum of long-term debt (DLTT) and debt in current liabilities

(DLC) over common equity (CEQ).

Industry Tobin's Q – Acquirer's industry median Tobin's Q across all Compustat firms

(using four-digit SIC codes) divided by 100. See Tobin's Q.

Is Cash – A dummy variable that is equal to one when the acquisition is financed

entirely with cash.

Is Diversifying Merger – A dummy variable that is equal to one when the acquirer and

the target are in different four-digit SIC code industries.

33

Is Public – A dummy variable that is equal to one when the target firm is publicly

traded.

Is Stock – A dummy variable that is equal to one when the acquisition is financed

entirely with bidder stocks.

Leverage – Sum of long-term debt (DLTT) and debt in current liabilities (DLC) over

common equity (CEQ).

Log Total Assets – Logarithm of total assets (AT).

Price Run-up – Bidder's buy-and-hold abnormal return from 230 to 11 days before the

announcement. The CRSP value-weighted index is used as the benchmark.

Relative Deal Size – Value of the deal as reported by Securities Data Company over

the market value of the acquirer measured at the end of the fiscal year preceding the

announcement.

Tobin's Q – Sum of the market value of book assets (AT) and the market value of

common equity (CSHO x PRCC) minus the sum of common equity (CEQ) and deferred

taxes (TXDB), all over the sum of 0.9 x book value of assets (AT) and 0.1 x market

value of assets.

Total Assets – Total book assets (AT) in billions of dollars.

34

References

Ahern, K.R., Daminelli, D. and Fracassi, C., 2015. Lost in translation? The effect of

cultural values on mergers around the world. Journal of Financial Economics, 117(1),

165-189.

Alldredge, D., and Cicero, D., 2015. Attentive insider trading. Journal of Financial

Economics 115, 84–101.

Altman, I., Low, S., 1992. Place attachment. Plenum Press.

Barber, B., and Lyon, J. D., 1997. Detecting long-run abnormal stock returns: The

empirical power and specification of test statistics. Journal of Financial Economics,

43, 341-372.

Bebchuk, L. A., Cohen, A., Ferrell, A., 2009. What matters in corporate governance?

Review of Financial Studies, 22, 783–827.

Ben-David, I., Graham, J.R. and Harvey, C.R., 2013. Managerial miscalibration. The

Quarterly Journal of Economics, 128, 1547-1584.

Bhattacharya, U., and Groznik, P., 2008. Melting pot or salad bowl: Some evidence from

U.S. investments abroad. Journal of Financial Markets 11, 228–58.

Byrd, J. W., and Hickman, K. A., 1992. Do outside directors monitor managers? Evidence

from tender offer bids. Journal of Financial Economics, 32.2, 195-221.

Cai, Y. and Sevilir, M., 2012. Board connections and M&A transactions. Journal of

Financial Economics, 103(2), 327-349.

Capron, L. and Shen, J.C., 2007. Acquisitions of private vs. public firms: Private

information, target selection, and acquirer returns. Strategic Management

Journal, 28(9), 891-911.

Carhart, M. M., 1997. On persistence in mutual fund performance. Journal of Finance, 52,

57–82.

Chang, S., 1998. Takeovers of privately held targets, methods of payment, and bidder

returns. Journal of Finance, 53, 773–784.

Chen, X., Harford, J., Li, K., 2007. Monitoring: which institutions matter? Journal of

Financial Economics, 86, 279–305.

Cohen, L., Frazzini, A., Malloy, C., 2008. The small world of investing: board connections

and mutual fund returns. Journal of Political Economy, 116, 951–979.

Cohen, L., Frazzini, A., Malloy, C., 2012. Hiring cheerleaders: board appointments of

“independent” directors. Management Science, 58, 1039–1058.

35

Core, J. E., Holthausen, R. W., and Larcker, D. F., 1999. Corporate governance, chief

executive officer compensation, and firm performance. Journal of Financial

Economics, 51.3, 371-406.

Cornaggia J., Cornaggia K. R., and Israelsen R. D., 2017. Where the heart is: Information

production and the home bias. SSRN Scholarly Paper ID 2518040, Social Science

Research Network, Rochester, NY

Cohen, L., Malloy, C., and Pomorski L., 2012, Decoding Inside Information. Journal of

Finance 67, 1009–1043.

Coval, J.D., Moskowitz, T.J., 1999. Home bias at home: Local equity preference in

domestic portfolios. Journal of Finance, 54, 2045–2073.

Coval, J.D., Moskowitz, T.J., 2001. The geography of investment: informed trading and

asset prices. Journal of Political Economy, 109, 811–841.

Cumming D. and Dai. N., 2010. Local bias in venture capital investments. Journal of

Empirical Finance, 17(3): 362-380.

Duchin, R., and Schmidt, B., 2013. Riding the merger wave: Uncertainty, reduced

monitoring, and bad acquisitions. Journal of Financial Economics, 107, 69-88.

Fernandez, B., 2010 (Jan 2010), “Casket maker to buy Pitman's K-Tron International” The

Philadelphia Inquirer.

Ferreira, M.A. and Matos, P., 2012. Universal banks and corporate control: Evidence from

the global syndicated loan market. Review of Financial Studies, 25(9), 2703-2744.

French, K.R., and Poterba, J.M., 1991. Investor diversification and international equity

markets. American Economic Review, 81 (2), 222-226.

Gillan, S. L., Hartzell, J. C., Starks, L. T., 2011. Tradeoffs in corporate governance:

evidence from board structures and charter provisions. Quarterly Journal of Finance,

1(04), 667-705

Goyal, V. K., and Park, C. W., 2002. Board leadership structure and CEO turnover. Journal

of Corporate Finance, 8, 49-66.

Grinblatt, M., and Keloharju, M., 2001. Distance, language, and culture bias: The role of

investor sophistication. Journal of Finance, 56, 1053–1073.

Heath, C. and Tversky, A., 1991. Preference and belief: Ambiguity and competence in

choice under uncertainty. Journal of Risk and Uncertainty, 4(1), 5-28.

Hirshleifer, D., Low, A. and Teoh, S.H., 2012. Are overconfident CEOs better innovators?

The Journal of Finance, 67(4), 1457-1498.

Huberman, G., 2001. Familiarity breeds investment. Review of Financial Studies, 14, 659–

680.

36

Ivkovic, Z., and Weisbenner, S. 2005. Local does as local is: Information content of the

geography of individual investors’ common stock investments. Journal of Finance, 60

(1), 267-306.

Jian, Feng, Qian, Yiming, and Yonker, Scott E., 2016, Home biased acquisitions, Working

Paper, University of Buffalo.

Kang, J., and Stulz, R.M., 1997. Why is there a home bias? An analysis of foreign portfolio

equity ownership in Japan. Journal of Financial Economics, 46, 3-28.

Lang, L. H. P., Stulz, R. M., Walkling, R. A., 1991. A test of the free cash flow hypothesis:

the case of bidder returns. Journal of Financial Economics, 29, 315–335.

Malmendier, U. and Tate, G., 2008. Who makes acquisitions? CEO overconfidence and

the market's reaction. Journal of financial Economics, 89(1), 20-43.

Manzo, L., 2003. Beyond house and haven: toward a revisioning of emotional relationships

with places. Journal of Environmental Psychology, 23 (1), 47-61.

Masulis, R. W., Wang, C., Xie, F., 2007. Corporate governance and acquirer returns.

Journal of Finance, 62, 1851–1889.

Moeller, S. B., Schlingemann, F. P., Stulz, R. M., 2004. Firm size and the gains from

acquisitions. Journal of Financial Economics, 73, 201–228.

Morck R., Shleifer A., and Vishny R.W., 1990. Do managerial objectives drive bad

acquisitions? Journal of Finance, 45(1): 31-48.

Myers, S. C., Majluf, N. S., 1984. Corporate financing and investment decisions when

firms have information that investors do not have. Journal of Financial Economics, 13,

187–221.

Officer, M. S., Poulsen, A. B., Stegemoller, M., 2009. Target-firm information asymmetry

and acquirer returns. Review of Finance, 13, 467–493.

Parwada, J. T., 2008. The genesis of home bias? The location and portfolio choices of

investment company start-ups. Journal of Financial and Quantitative Analysis, 43,

245–66.

Pool, V.K., Stoffman, N., and Yonker, S.E., 2012. No place like home: Familiarity in

mutual fund manager portfolio choice. Review of Financial Studies, 25 (8), 2563-2599.

Ravina, E. and Sapienza, P., 2010. What do independent directors know? Evidence from

their trading. Review of Financial Studies, 23(3), 962-1003.

Rhodes-Kropf, M., Robinson, D. T., 2008. The market for mergers and the boundaries of

the firm. Journal of Finance, 63, 1169–1211.

Roll, R., 1986. The hubris hypothesis of corporate takeovers. Journal of Business, 59, 197–

216.

37

Shleifer, A., Vishny, R. W., 1989. Management entrenchment: the case of manager-

specific investments. Journal of Financial Economics, 25, 123–139.

Scannell, Leila; Robert Gifford, 2010. Defining place attachment: a tripartite organizing

framework. Journal of Environmental Psychology 30: 1–10.

Schmidt, B., 2015. Costs and benefits of friendly boards during mergers and

acquisitions. Journal of Financial Economics, 117(2), 424-447.

Seasholes, M.S., and Zhu, N., 2010. Individual investors and local bias. Journal of Finance,

65 (5), 1987-2010.

Seyhun, N., N., 1986. Insiders’ profits, costs of trading, and market efficiency. Journal of

Financial Economics 16, 189–212.

Taylor, R.B., Gottfredson, S.D. and Brower, S., 1985. Attachment to place: Discriminant

validity, and impacts of disorder and diversity. American Journal of Community

Psychology, 13(5), 525-542.

Tesar, L.L., and Werner, I., 1995. Home bias and high turnover. Journal of International

Money and Finance, 14 (4), 467-492.

Weisbach, M. S., 1988. Outside directors and CEO turnover. Journal of Financial

Economics, 20, 431-460.

Yonker, S.E., 2017a. Geography and the market for CEOs. Management Science, 63 (3),

609-630

Yonker, S.E., 2017b. Do managers give hometown labor an edge? Review of Financial

Studies, 30 (10), 3581-3604

38

Table 1. Merger Summary Statistics

The table reports summary statistics for the variables employed in our analysis. The sample consists of

acquisitions announced between 1990 and 2014 in which the acquirer is a publicly traded company and

data is available for our CEO and firm variables of interest (from SDC, CRSP, Compustat, and Lexis Nexis).

Panel A reports the mean, standard deviation, and the 25th, 50th, and 75th percentiles for the full sample of

mergers. Panels B through E report statistics for the subset of mergers in which B) the target headquarters

is located in the CEO’s birth state, C) the target headquarters is located less than 100 miles from the CEO’s

hometown, D) the target is headquartered outside the acquirer’s headquarters state, and E) the target is

headquartered more than 100 miles from the acquirer headquarters. A detailed description of each variable

is included in Appendix A.

Variable N Mean

Standard

Deviation

25th

Percentile Median

75th

Percentile

Panel A: All Mergers

Deal Value 9891 689.81 4096.74 18.55 60 225

Relative Deal Value 9891 0.22 0.37 0.03 0.08 0.23

Price Run-up 9891 0.18 0.64 -0.17 0.05 0.33

Tobin's Q 9891 1.91 2.06 1.07 1.38 2.08

Leverage 9891 0.35 1.03 0.11 0.35 0.56

Δ Income 9891 0.51 0.77 0 0.35 0.87

Acq-Target Distance 9494 800.92 806.71 125.32 541.86 1237.78

CEO-Target Distance 9494 924.12 810.28 257.33 683.33 1443.95

Panel B: Home Bias Mergers (State)

Deal Value 1456 548.99 5012.39 17.55 49.19 174.54

Relative Deal Value 1456 0.24 0.4 0.04 0.1 0.26

Price Run-up 1456 0.17 0.61 -0.16 0.04 0.3

Tobin's Q 1456 1.73 2.67 1.04 1.17 1.7

Leverage 1456 0.4 0.27 0.18 0.41 0.6

Δ Income 1456 0.53 0.78 0 0.34 0.85

Acq-Target Distance 1419 332.11 616.17 16.1 75.28 313.21

CEO-Target Distance 1419 97.34 118.54 11.3 40.21 145.96

Panel C: Home Bias Mergers (Distance)

Deal Value 1288 727.76 5721.64 18.77 57.71 189.83

Relative Deal Value 1288 0.26 0.4 0.05 0.12 0.31

Price Run-up 1288 0.15 0.59 -0.16 0.02 0.28

Tobin's Q 1288 1.69 2.27 1.03 1.17 1.72

Leverage 1288 0.39 0.35 0.17 0.41 0.61

Δ Income 1288 0.51 0.79 0 0.33 0.79

Acq-Target Distance 1288 314.91 641.29 12.38 43.41 195.85

CEO-Target Distance 1288 34.01 30.65 8.83 24.36 58.15

39

Table 1 Merger Summary Statistics (continued)

Variable N Mean

Standard

Deviation

25th

Percentile Median

75th

Percentile

Panel D: Faraway Mergers (Cross-State)

Deal Value 7227 735.56 4359.34 19 62 242.39

Relative Deal Value 7227 0.21 0.36 0.03 0.08 0.22

Price Run-up 7227 0.17 0.62 -0.16 0.04 0.32

Tobin's Q 7227 1.88 1.51 1.09 1.42 2.11

Leverage 7227 0.34 1.19 0.11 0.34 0.56

Δ Income 7227 0.51 0.77 0 0.36 0.87

Acq-Target Distance 6871 1071.09 791.13 422.3 855.1 1621.55

CEO-Target Distance 6871 995.2 781 369 757.3 1499.22

Panel E: Faraway Mergers (Distance)

Deal Value 7313 670.74 3953.25 19.59 61.84 239.32

Relative Deal Value 7313 0.21 0.36 0.03 0.08 0.22

Price Run-up 7313 0.18 0.64 -0.16 0.05 0.33

Tobin's Q 7313 1.91 1.95 1.09 1.4 2.11

Leverage 7313 0.34 1.19 0.1 0.35 0.56

Δ Income 7313 0.51 0.77 0 0.36 0.87

Acq-Target Distance 7313 1031.21 782.38 364.88 794.42 1568.75

CEO-Target Distance 7313 1010.94 785.02 368.19 769.11 1535.63

40

Table 2. CEO Home Bias and the Probability of Acquisition

The table reports the results from probit regressions in which the dependent variable is one for actual merger observations and zero for hypothetical mergers.

For each actual merger, we chose a hypothetical acquirer from among firms headquartered in the same state and in the same Fama-French 48 industry that are

closest in size and book to market to the actual acquirer. In Specifications 1-4, Home Bias is a dummy variable that is equal to one when the acquirer firm