Embed Size (px)

Citation preview

27/04/16

1

CORPORATE PRESENTATION1Q 2016 Results Briefing – 27th April 2016

Aerial view of Phase I of Sembcorp Marine Tuas Boulevard Yard

1

Aerial view of Tuas Boulevard Yard Phase I and II

�CEO Presentation

�CFO Presentation

AGENDA

2

27/04/16

2

CEO ADDRESS

� Macro Environment remains challenging

� Update on Sete Brasil and other rig projects

� Deliveries and other activities

� Outlook and Prospects

3

� Upstream oil & gas industry

into second year of weak

prices and capex cuts.

� Market equilibrium in the oil &

gas industry remains elusive.

� Offshore rig charter rates and

utilization continue to slide.

Market equilibrium remains elusive

4Source: Reuters

27/04/16

3

Key Highlights for 1Q 2016:

� Total revenue of $918 million.

� Net Profit was S$55 million.

Financial Performance

5

106

55

1304

918

0

20

40

60

80

100

120

0

200

400

600

800

1000

1200

1400

1Q 2015 1Q 2016

S$ million

S$ million

1Q 2016 Revenue and Profit performance

Net Profit Revenue

� Brazil political upheaval continues unabated; drive to

impeach current President and deteriorating economy

adding to volatility and uncertainty.

� Sete Brasil shareholders have approved resolution to file

for judicial recovery.

� Sembcorp Marine has commenced arbitration proceedings

against various subsidiaries of Sete Brasil to preserve the

Group’s interest under the Sete Contracts.

� We believe provisions of S$329 million made in 4Q 2015

are adequate under present circumstances.

Update on Sete Brasil drillships contracts

6

27/04/16

4

� Marco Polo Drilling failed to take delivery of its rig. We have

terminated the contract and taken legal action to recover the

balance due from the customer.

� All completed rigs technically accepted by customers.

Sembcorp Marine has finalised or are finalising mutually

acceptable solutions for delivery deferment requests.

� Provisions of S$280 million taken in 4Q 2015, in case of

prolonged deferment or possible cancellation of rigs, should be

adequate under current circumstances.

Update on other drilling rig contracts

7

� Key deliveries in 1Q 2016 include the Safe Zephyrus to

Prosafe in end-January 2016 as well as the FPSO Ghana

Ten to Modec.

� Secured creditable S$60 million in new orders (all non-

drilling solutions), despite very tough market conditions.

We expect to continue to grow our orderbook.

� Net orderbook at S$9.7 billion as at March 31, 2016.

Other Operations Review

8

27/04/16

5

� Down cycle expected to be more protracted than previous

cycles.

� Sembcorp Marine prepared to face and overcome the

challenges ahead

� Acquisition of an additional 44% stake in Gravifloat on March

9, 2016 raises Sembcorp Marine’s stake to 56%

� Headcount optimization ongoing.

� Active management of balance sheet to maintain healthy

financial position.

� Foundations laid for future growth through strategic

investments in hard and soft infrastructure.

Outlook & Prospects

9

Increased stake in Gravifloat to 56% after buying an additional 44% for US$38 million

• Under the agreement, the Company will eventually increase its stake by a further 44% to 100% through an equity purchase at the same price.

• Grav iFloat was formed to design, deliver and operate re-deployable, gravity-based, modularised LNG and LPG Terminals for installation in shallow waters.

• Incorporated in Norway in 2006 as a spin-off of LMG Marin (a marine & engineering and naval architecture company), GraviFloat is headquartered in Bergen.

• Grav iFloat technology allows the LNG terminal to be fully built and completed at a shipyard and installed in shallow waters to facilitate direct ship loading of LNG.

• It offers a more cost effective solution compared with FSRU (floating, storage and regasification units) and land terminals, and can be designed for both liquefaction and receiving terminal services.

10

Growing nonGrowing non--drilling solutions drilling solutions -- GravifloatGravifloat

27/04/16

6

CFO Presentation

� Earnings Performance

� Financial Position

11

Key highlights:

For the 3 months to March 2016:

� Turnover totalled $918 million, down 30% from 1Q 2015’s $1.3 billion.

� Gross profit of $81 million on earnings recognition of ongoing

projects and deliveries.

� Group EBITDA of $106 million.

� Net profit attributable to shareholders of $55 million

� Group net orderbook stands at S$9.7 billion, including S$60 million

in new contracts secured in 1Q 2016.

Performance Highlights

12

27/04/16

7

13

FINANCIAL HIGHLIGHTS

1Q2016 TURNOVER: S$918 million

14

943 1,050 1,335 1,304

918

1,217 1,124

1,341 1,208

892 1,659

1,712

1,130

1,378

1,693

1,445

1,327

4,430

5,526 5,832

4,968

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2012 2013 2014 2015 2016

$ m

illi

on

1Q 2Q 3Q 4Q

27/04/16

8

1Q2016 Net Profit at S$55 million

15

113 119 122 106 106 46

145 122 132 109 109

116 130 132

49 70

126 182 174

-535

99

38

-19

9

538 556 560

-290384

55

-800

-600

-400

-200

0

200

400

600

800

2012 2013 2014 2015 2015 excluding provisions and

non-operating items

2016

$ m

illi

on

1Q 2016 Net Profit: S$55 million

1Q 2Q 3Q 4Q NOI

Rigs & Floaters

59%

Repairs & Upgrades

11%

Offshore Platforms

28%

Other Activities

2%

1Q 2016 Turnover: $918 million

Rigs & Floaters

73%

Repairs & Upgrades

8%

Offshore Platforms

18%

Other Activities

1%

1Q 2015 Turnover: $1,304 million

Business Review: Turnover by Segments

16

Turnover (S$ million) 1Q 2016 1Q 2015 % change

Rigs & Floaters 540 947 (43)

Repairs & Upgrades 99 100 (1)

Offshore Platforms 261 237 10

Other Activities 18 20 (10)

TOTAL 918 1,304 (30)

27/04/16

9

17

862943

737

554644

707

459

72986 1,129 866 695 708 844 587 81

15.1

20.7

18.6

12.511.7 12.1

8.97.8

17.2

24.8

21.9

15.7

12.8

14.5

11.4

8.8

0

5

10

15

20

25

30

0

200

400

600

800

1000

1200

2009 2010 2011 2012 2013 2014 2015(excl. provisions)

1Q 2016

% m

arg

ins

$ m

illio

n

Operating Profit $m

Gross Profit $m

Operating Profit Margin %

Gross Profit Margin %

Gross and operating profit margins

0

100

200

300

400

500

600

700

800

2009 2010 2011 2012 2013 2014 2015 1Q 2016

706

646 644 642681

622

557

99

Ship repair revenue ($million)

Core Business: Repairs & Upgrades

18

Year 1Q 2016 1Q 2015 % change

No. of v essels repaired 125 121 +3

Av erage v alue per v essel ($m) 0.8 0.8 -

Total repair rev enue contribution ($m) 99 100 -1

27/04/16

10

• Rig building revenue fell 58% yoy to S$317 million in 1Q 2016,accounting for 35% of total group revenue.

• Delivered one Prosafe accommodation semi-sub in 1Q 2016.

2,127

1,108797

2,0012,295

1,803

670

150

1,508

1,940

1,408

127

836

980

447

156

228

433 996

1311

11

3635

3048

22052356

3564

3779

2428

317

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2009 2010 2011 2012 2013 2014 2015 1Q 2016

S$ MILLION

Jack-up SemiSub- drilling, accomodation, well intervention, crane Drillship

Core Business: Rig Building

JACK-UP RIGS SCHEDULE

No. delivered in 1Q 2016 Nil-

No. of projects in WIP 8

* Oro Negro Vastus JU

* PC400 Jack-up, Perisai Pacific 102

* PC400 JU, Oro Negro P2045

* PC400 JU, Oro Negro P2046

* MSC CJ 70 JU, Noble Mariner

* F&G JU2000E JU, Hercules

* PC400 JU , Perisai Pacific 103

* PC400 JU, BOTL/JDC Hakuryu 14 JU 2

SEMI-SUBS / DRILLSHIPS

No. of projects delivered in 1Q 2016 1 * Prosafe accommodation semi 1

No of projects in WIP stage13 * Drillship 1st unit, SeteBrasil, Arpoador

* Helix semi-well intervention 2 (Q7000)

* Harsh-environment CS60 semi-submersible rig, Seadrill* Drillship 2

ndunit, Sete Brasil

* Prosafe accommodation semi 2

* Drillship 3rd unit, Sete Brasil• Drillship 4

thunit, Sete Brasil

* Drillship 5th

unit, Sete Brasil* Drillship 6

thunit, Sete Brasil

* Drillship 7th

unit, Sete Brasil

* 1st drillship - Transocean, JE III

* 2nd drillship for Transocean, JE III* Heerema new semi-s crane vessel

19

• Floaters revenue increased 15% yoy to $223 million in 1Q 2016

• FPSO Ghana Ten recently delivered in 1Q 2016.

• 7 projects in WIP & Planning stages

Core Business: Floaters revenue robust

-

100

200

300

400

500

600

700

800

900

2009 2010 2011 2012 2013 2014 2015 1Q 2016

599

501

719

621

336

428

891

223

$ MILLION

Revenue – Floaters ($m) Offshore conversionsNo. of

projects Brief description

No. of Projects recently delivered 1 * Ghana Ten

No. of projects in the WIP and

Planning & Engineering Stage 6 * FSO Gina Krog

* P68 FPSO for Petrobras* P71 FPSO for Petrobras

* FPSO Norte - Kaombo(Olympia)

* FPSO Libra

* FPSO Sul - Kaombo(Antartica)

No. of Projects in Planning & Engineering Stage

1 * FPSO Culzean Modec

20

27/04/16

11

-

200

400

600

800

1,000

1,200

2009 2010 2011 2012 2013 2014 2015 1Q 2016

744

319 354

774 868

925 1,017

261

Revenue - Offshore Platforms ($m)

Core Business: Offshore Platforms sales in healthy uptrend

Offshore PlatformsNo. of

projects Brief description

Number of projects delivered in 1Q 2016 - Nil

Number of projects in the WIP stage 5 * Ivar Aasen

* Wheatstone

* Siemens Dudgeon

Number of projects in Planning and

Engineering stage 1

* Maersk Culzeantopsides

* Yamal LNG Batch 3* Yamal PAU module

21

• Offshore Platforms revenue increased 10% yoy to $261 million in 1Q 2016

• 6 projects in WIP & Planning and Engineering stages.

CAPITAL, GEARING &ROE

22

Group (S$ million) Mar-16 Mar-15 % change

Shareholders' Funds 2,553 3,106 (18)

Net Debt 2,945 908 n.m.

Net Working Capital 1,888 1,204 57

Return on Equity (ROE) (%) (Annualised) 8.7 14.0 (38)

ROE - exclude NOI (%) (Annualised) 7.2 13.9 (48)

Net Asset Value (cents) 122.2 148.7 (18)

Return on Total Assets (ROTA) (%) (Annualised) 3.1 5.7 (46)

ROTA - exclude NOI (%) (Anualised) 2.7 5.7 (53)

27/04/16

12

23

CASHFLOW

Group (S$ million) 1Q 2016 1Q 2015 % change

Operating profit before working capital changes 84 174 (52)

Net cash outflow from operating activities (73) (50) 46

Net cash outflow from investing activities (149) (221) (33)

Net cash inflow from financing activities 572 306 87

Cash & cash equivalents 957 1,126 (15)

Borrowings (3,902) (2,034) 92

Net Debt (2,945) (908) n.m.

Progress Billing > WIP 336 917 (63)

292 556 693 1,009 -

1,643

314

723 -

376 1,557 439

1,292

-

1,935

1,875 1,335

871

-

1,245

3,041

3,724

10,979

4,194 4,172

3,171

60-

2,000

4,000

6,000

8,000

10,000

12,000

2009 2010 2011 2012 2013 2014 2015 2016 YTD

New Contracts Secured by Product (excludes Repairs and Upgrades)

Floaters

Offshore Platforms

Semi-submersible/intervention/crane

Jack Up

Drillship

New Contracts Secured by Product Type ($million)

24* Semisubmersibles include drilling, well intervention, accommodation and crane units

27/04/16

13

797 647 765 1,352 968

2,232 1,876 1,655 409 638 1,070

782 1,267

887 1,832 1,659

871 1,642

2,775 2,020 2,398

1,591 625 513 3,463 1,491

486 1,908 1,608

660 1,533 1,408

6,666 6,096

6,062 4,502

4,461

5,540

4,418

5,096

12,728 12,337

11,432

10,368

9,696

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

2009 2010 2011 2012 2013 2014 2015 2016 YTD

Net Order Book (excludes Repairs and Upgrades)

Floaters Offshore Platform

Jack Up Semi-submersible*

Drillship

* Semisubmersibles include drilling, well intervention, accommodation and crane units

Net Order Book at $9.7 billion

25

26

OFFSHORE PLATFORMS

18%

RIGS & FLOATERS

82%

Offshore Platforms

18%

Floaters18%

Jackup6%

* Semisubs15%

Drillships43%

At 31 Dec 2015

Total $10.4 billion

OFFSHORE PLATFORMS

17%

RIGS & FLOATERS

83%

Offshore Platforms

17%

Floaters17%

Jackup5%

* Semisubs15%

Drillships46%

At 31 March 2016

Total $9.7 billion

Net order backlog by division and product type

* Semisubmersibles include drilling, well intervention, accommodation and crane units

27/04/16

14

1Q 2016 ResultsAppendix

27

ROBUST BUSINESS MODEL

27/04/16

15

FOUR KEY CAPABILITIES

Leaders in offshore marine engineering solutions

30

27/04/16

16

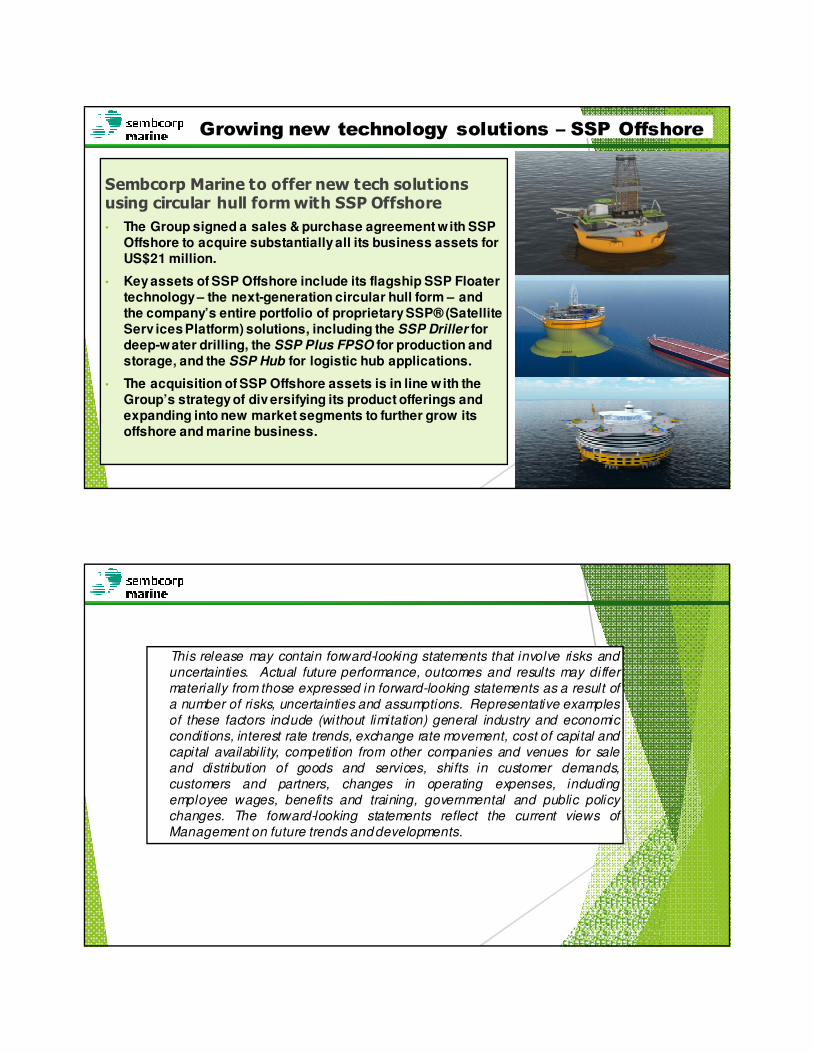

Growing new technology solutions – SSP Offshore

Sembcorp Marine to offer new tech solutions using circular hull form with SSP Offshore

• The Group signed a sales & purchase agreement with SSP Offshore to acquire substantially all its business assets for US$21 million.

• Key assets of SSP Offshore include its flagship SSP Floater technology – the next-generation circular hull form – and the company’s entire portfolio of proprietary SSP® (Satellite Serv ices Platform) solutions, including the SSP Driller for deep-water drilling, the SSP Plus FPSO for production and storage, and the SSP Hub for logistic hub applications.

• The acquisition of SSP Offshore assets is in line with the Group’s strategy of div ersifying its product offerings and expanding into new market segments to further grow its offshore and marine business.

31

This release may contain forward-looking statements that involve risks and

uncertainties. Actual future performance, outcomes and results may differ

materially from those expressed in forward-looking statements as a result of

a number of risks, uncertainties and assumptions. Representative examples

of these factors include (without limitation) general industry and economic

conditions, interest rate trends, exchange rate movement, cost of capital and

capital availability, competition from other companies and venues for sale

and distribution of goods and services, shifts in customer demands,

customers and partners, changes in operating expenses, including

employee wages, benefits and training, governmental and public policy

changes. The forward-looking statements reflect the current views of

Management on future trends and developments.