Embed Size (px)

Citation preview

ACC2200 1

Chapter1:Informationforcreatingvalueandmanagingresources1.WhatisManagementAccounting?ManagementaccountingreferstotheprocessesandtechniquesthatfocusontheeffectiveandefficientuseoforganisationalresourcestosupportmanagersintheirtasksofenhancingbothcustomerandshareholdervalueCustomervalue

Valueacustomerplacesonparticularfeaturesofaproduct–satisfyingcustomersiscriticaltoachievingincreasedsalesandmarketshare→achievingshareholdervalue

Shareholdervalue

Involvesimprovingtheworthofabusinessfromtheshareholders’orowners’perspective–increasedprofitability,increasedsharepriceanddividends.Whereaconflictbetweenincreasingcustomerorshareholdervaluearises,shareholdervalueislikelytobegivenpriority

1.1.ManagementAccountingSystemsAmanagementaccountingsystemisaninformationsystemthatproducestheinformationrequiredbymanagerstocreatevalueandmanageresources

• Formspartofanorganisation’swidermanagementinformationsystems• Managementaccountinginformationcanbeprovidedonaregularbasisandcaninclude:

o Costestimatesforproducinggoodsandserviceso Informationforplanningandcontrollingoperationso Informationformeasuringperformance

1.2.ManagementAccountingInformationThe focusofmanagementaccounting ison theneedsofmanagerswithin theorganisation.Becauseaccounting standardsapplyonlytoexternalfinancialreports,thereisgreatflexibilityindecidingthetypeofinformationthatshouldbegeneratedformanagersManager’s information needs vary, and as the nature of the resources they manage varies, the type of managementaccountinginformationrequiredwillalsovary.Otherfactorsthatcausemanagementaccountingsystemstodiffer,include:

• Differencesinproductionorservicetechnologies• Organisationalstructureandsize

• External environment in which the organisationcompetes

• LevelsofsophisticationofcomputersystemsManagement accounting information is relevant tomanagers from the top of the organisations through tomanagers inoperationalareasofabusiness.

• Seniormanagers=needinformationthatprovidesthemwithanoverviewofentireorganisation• Middlemanagers=needinformationontheirareasofresponsibility• Operationalmanagers=need information tohelp themmanage their specificoperationsonaday-to-daybasis, tohelpmeet

performancetarget1.3.DifferencesbetweenManagementsAccountingandFinancialAccountingInformation

ManagementAccounting FinancialAccounting

Usesofinformation

Internalmanagersandemployeesatalllevels Externalshareholders,creditors,banks,securitiesexchange,tradeunionsandgovernmentagencies

RegulationNoaccountingstandardsorexternalrulesareimposed.Informationisgeneratedtosatisfymanagersinformationneeds

Accountingstandardsandcorporationslawregulatethecontentofexternalfinancialreports

Sourceofdata

Bothfinancialandnon-financialdatadrawnfrommanysources–thecoreaccountingsystem;physicalandoperationaldatefromproductionsystems;andmarket,customerandeconomicdatafromsourcesexternaltotheorganisation

Financialdataalmostexclusivelydrawnfromorganisation’scoretransaction-basedaccountingsystem

Natureoftheinformation

Past,currentandfutureoriented;subjective;relevant;timely;andsuppliedatvariouslevelsofdetailtosuitmanager’sspecificneeds

Past;reliable;verifiable;nottimely;notalwaysrelevant;andhighlyaggregated

ACC2200 2

1.4.ManagementAccountingandStrategyManagement accounting plays an important strategic role by contributing to the organisation’s formulation andimplementationofstrategyandbyhelpingmanagersimprovetheorganisationscompetitiveadvantage

VisionDesiredfuturestateoraspirationofanorganisation.Thevisionisoftenusedbyseniormanagementtofocustheattentionandenergyofstaffthroughouttheorganisations

Missionstatement

Astatementthatdefinesthepurposeandboundariesoftheorganisation

ObjectivesSpecificstatementsofwhattheorganisationsaimtoachieve,oftenquantifiedandrelatingtoaspecificperiodoftime.Objectivesareoftenfocusedonprofitability,growth,innovation,qualityofservice,etc.

Strategies

Thedirection that theorganisation intends to takeover the long term, tomeet itsmissionandachieve itsobjectives.Informulatingstrategies,decisionsarebasedonthefollowingquestions:• Inwhatbusinesswillweoperate• Howshouldwecompeteinthatbusiness• Whatsystemsandstructuresshouldwehaveinplacetosupportourstrategies?

1.4.1.OrganisationalStrategiesThefirstdecisioninvolvesformulatingacorporatestrategy.CorporatestrategyinvolvesmakingdecisionsaboutthetypesofbusinessesinwhichtheorganisationasawholewilloperateThesecondtypeofbusinessdecisions involvesbusinessstrategy.Business(orcompetitive)strategy isconcernedwiththewaythatabusinesscompeteswithin itschosenmarket(e.g. Jetstarwouldcompetewithvirginonbasisof lowcost,whileQantaswillcontinuetobehigherqualityandfullservice)The third type of decision is concerned with strategy implementation. Strategy implementation involves planning andmanagingtheimplementationofstrategies.Thiscanincludenewstructuresandsystems,suchas:

• Settingupnewbusinessunits• Implementingnewproductionprocesses• Implementingnewsoftwarepackages

• Developingnewmarketingapproaches• IntroducinginnovativeHRMpolicies

1.4.2.CompetitiveAdvantageTo create shareholder value, a business must develop and manage its sources of competitive advantage. Competitiveadvantage refers to advantages that a businessmay have over another,which are difficult to imitate. A firm can gain asustainablecompetitiveadvantagethroughadoptingabusinessstrategyofcostleadershipandproductdifferentiation

CostLeadership

Abusinessstrategywhereafirmisalowcostproducer,whichallowsthebusinesstosellitsgoodsorservicesatalowerpricethancompetitors

• Economiesofscaleinproduction• Superiorprocesstechnology• Tightcostcontrol• Costminimisation-marketing,production,R&Dandcustomerservice

ProductDifferentiation

Abusinessstrategywherebyafirmderivescompetitiveadvantagefromofferinggoodsorservicesthathavecharacteristicsdifferentfromthoseofferedbycompetitors.Differentiationstrategies:

• Highqualityproducts(Mercedes)• Strongbrandimage(Rayban)• Superiorcustomerservice• Productinnovation(Apple)

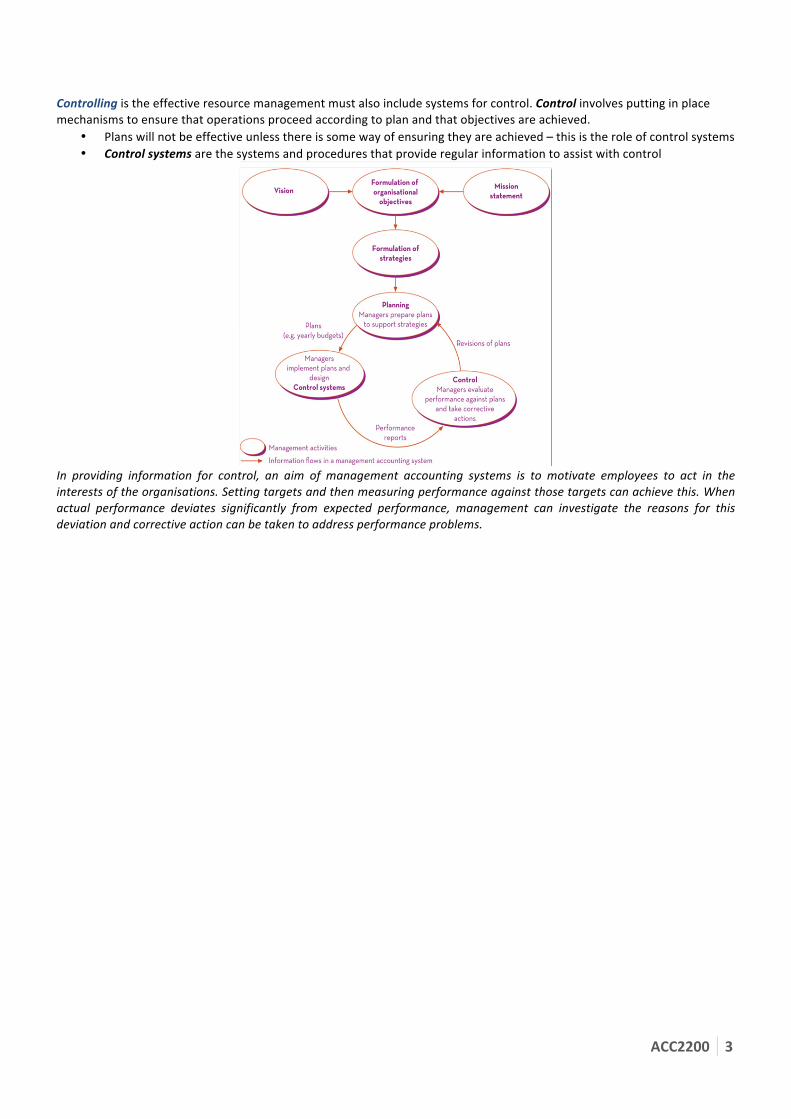

1.5.PlanningandControlPlanningisabroadconceptthatisconcernedwithformulatingthedirectionforfutureoperations• Necessarysoanorganisationcanconsiderandspecifyalltheresourcesthatwillbeneededinthefuture• Abudgetisadetailedplansummarisingthefinancialconsequencesofanorganisation’soperatingactivitiesfora

specificfuturetimeperiod• Managementaccountingsystemsaredesignedtoproducefrequentlyrequiredinformation(forcontrolpurposes),but

needtobeflexibleenoughtogeneratesomeinformationthatisneededforinfrequentoroneoffdecisions

ACC2200 3

Controllingistheeffectiveresourcemanagementmustalsoincludesystemsforcontrol.Controlinvolvesputtinginplacemechanismstoensurethatoperationsproceedaccordingtoplanandthatobjectivesareachieved.

• Planswillnotbeeffectiveunlessthereissomewayofensuringtheyareachieved–thisistheroleofcontrolsystems• Controlsystemsarethesystemsandproceduresthatprovideregularinformationtoassistwithcontrol

In providing information for control, an aim of management accounting systems is to motivate employees to act in theinterestsoftheorganisations.Settingtargetsandthenmeasuringperformanceagainstthosetargetscanachievethis.Whenactual performance deviates significantly from expected performance, management can investigate the reasons for thisdeviationandcorrectiveactioncanbetakentoaddressperformanceproblems.

ACC2200 4

Chapter2:CostTermsandConcepts2.1 ManagementAccountingInformation2.1.1.ComponentsofManagementAccountingSystemManagementaccountingsystemsaretailoredtoorganisationsneedsbuttheyoftenincludethefollowing:

Costingsystem Estimatesthecostofgoodsorservices,aswellastheycostoforganisationalunits,suchasdepartments

Budgetingsystem Usedtoprepareadetailedplan,whichshowsthefinancialconsequencesoftheorganisationsoperatingactivities,foraspecificfuturetimeperiod.Thesystemestimatesplannedrevenuesandcosts

Performancemeasurementsystem

Measuresperformancebycomparingactualresultswithsometarget

Costmanagementsystem

Focusesonimprovingtheorganisationscosteffectivenessthroughunderstandingandmanagingtherealcausesofcosts

2.2 TraditionalversusModernApproachestoManagementAccounting2.2.1 CostingSystems TraditionalSystems ModernSystems

CostingSystems

Estimate thecostsoforganisationalunits, suchasdepartments, andofproducts (goodsor services).In analysing costs they assume that productionvolumeistheonlyfactorthatcancausechange

Farmore detailed. Estimate the cost of the individualactivities performed in the organisation and use thisinformation to cost goods and services, customers,organisational unit and other items. Modern costingrecognises that production volume can cause costs tochange, but so can other factors. These systems arecalledactivity-basedcostingsystems.

2.2.2 BudgetingSystems TraditionalSystems ModernSystems

BudgetingSystems

Estimate planned revenues and costs fororganisational units, such as departments.Department budgets are aggregated to obtain abudgetfortheoverallorganisation.

Modern approach is called activity-based budgetingandisfarmoredetailedandbuiltaroundactivities

2.2.3 PerformanceMeasurementSystems TraditionalSystems ModernSystems

PerformanceMeasurementSystems

Providemeasuresoffinancialperformance.Focuslargely on controlling costs, by reportingdifferences between budgeted and actual costs.Monitorperformancewithintheorganisation

Provide measures of performance across a wholerange of critical success factors, such as quality,delivery, innovation and sustainability, as well asfinancialperformance.These factors derive from business’ competitivestrategyandarecriticaltoitssurvival.Modernsystemslookatwhatishappeningoutsidetheorganisations, analysing competitors, customersatisfaction and stakeholders. Includes balancedscorecard, benchmarking and activity-basedperformancemeasures

ACC2200 5

2.2.4 CostManagementSystems TraditionalSystems ModernSystems

CostingSystems

Provide information to help managers controlcosts, by focusing ondifferences between accrualandbudgetedcosts.

Farmorepro-activeinprovidinginformationtomanageresources. Developed not only to control costs butreduce them. Identifies and eliminates wastefulactivities

2.3 CostClassifications:DifferentClassificationsforDifferentPurposesBeforemanagementaccountantscanclassifycosts,theyneedtoconsiderhowmanagerswillusetheinformation.Differentcostconceptsandclassificationsareusedfordifferentpurposes.Thetotaldollaramountofcostdoesnotchange;onlythewaywelookatit

Thesamecostscanbeclassifiedinanumberofwaysdependingontheintendeduseofcostinformation