Embed Size (px)

Citation preview

P1 – Management Accounting CH1 – Traditional costing

Page 1

Chapter 1 Traditional Costing Chapter learning objectives: Lead Component Indicative syllabus content

A.1 Discuss costing methods and their results.

(a) Apply marginal (or variable) throughput and absorption accounting methods in respect of profit reporting and inventory valuation.

• Marginal (or variable) throughput and absorption accounting systems of profit reporting and inventory valuation, including the reconciliation of budget and actual profit using absorption and/or marginal costing principles.

C.1 Explain concepts of cost and revenue relevant to pricing and product decisions.

(c) Explain the issues that arise in pricing decisions and the conflict between ‘marginal cost’ principles, and the need for full recovery of all costs incurred.

• Marginal and full cost recovery as bases for pricing decisions in the short and long term.

P1 – Management Accounting CH1 – Traditional costing

Page 2

1. WHY DO WE DETERMINE COSTS? • For inventory valuation in the Statement of Financial Position (SoFP)

• For recording costs in the Statement of Comprehensive Income (SoCI)

• For pricing purposes

• For decision making

TYPES OF COSTS • Fixed cost/Period cost relates to a specific accounting period and is unaffected by

changes in production activity.

• Stepped fixed cost remains fixed for a range of activity then increases when that range is exceeded.

• Variable cost relates to the production activity and increases as activity increases.

• Semi-variable/semi-fixed/mixed cost contains an element of both fixed and variable cost.

2. ABSORPTION COSTING AIM: to work out the full cost of producing a unit.

• Absorption Costing uses the full production cost to determine the cost per unit.

• Overhead absorption rate (OAR) is calculated on the basis of production units, labour hours or machine hours.

• Production overheads are absorbed into units produced on the basis of this absorption rate.

P1 – Management Accounting CH1 – Traditional costing

Page 3

Steps:

1. Allocate / apportion OH to cost centres

2. Re-apportion service centre OH to production cost centres

3. Absorb OH into production

𝑂𝐴𝑅 = 𝐸𝑠𝑡𝑖𝑚𝑎𝑡𝑒𝑑 𝑓𝑖𝑥𝑒𝑑 𝑂𝐻𝐸𝑥𝑝𝑒𝑐𝑡𝑒𝑑 𝑎𝑐𝑡𝑖𝑣𝑖𝑡𝑦 𝑙𝑒𝑣𝑒𝑙

Test Your Understanding 1 – Absorption costing Derek, a fellow accountant in your company, has gathered cost information for Chewy Bubble Gum – a product that your company is producing.

Cost:

Direct Materials $5 per kg used

Direct Labour $17 per h worked

Variable overheads $6 per h of direct labour

Derek has also calculated the fixed production overheads. They are absorbed on a per-unit basis and equal to $360,000 in total.

After a thorough investigation, the team has found that each unit is using 2 kg of material and needs 1.5 hr of direct labour.

Sales and production were budgeted at 30,000 units, but only 27,000 units were actually produced, and 24,000 were actually sold.

There was no opening stock.

Please produce a standard cost card using absorption costing and value the company’s closing stock on that basis.

P1 – Management Accounting CH1 – Traditional costing

Page 4

OVER/UNDER-ABSORPTION (Budgeted overhead absorption rate / unit × actual units) – Actual overheads

Reasons for over/under-absorption

• Expenditure variance – actual OH differed from the budgeted OH.

• Volume variance – actual production activity differed from expected activity levels.

3. Marginal Costing • The cost of producing one more unit includes:

- Direct material

- Direct labour

- Variable overheads

• Contribution per unit = selling price per unit – all variable costs per unit.

• Total contribution: selling price – all variable costs OR profit + fixed costs.

• Inventory is valued at variable cost of production only.

4. Comparison – Absorption & Marginal Costing

ABSORPTION COSTING MARGINAL COSTING

Advantages Advantages • Includes the fixed production costs,

which is a large proportion of total costs • Calculation is simpler

• Follows the accruals concept, as production cost is carried forward with inventory

• More relevant for decision making, as it only considers the relevant variable costs

• Over/under-absorptions helps identify inefficient resource utilisation • No arbitrary apportionments

• Absorption costing argues that all costs are variable in the long term

• No issues of under/over-absorption and adjustment

Disadvantages Disadvantages • The bases used for

allocation/apportionment are essentially subjective

• Is ineffective in cases where the fixed costs are a larger proportion of total costs

• Profits can be manipulated with high or low inventory levels

• Direct labour costs might be considered fixed in nature if the employees are on fixed wages

• Encourages over-production in the interest of showing a higher current-year profit

• It would be difficult to determine if the contribution earned will cover the fixed costs

P1 – Management Accounting CH1 – Traditional costing

Page 5

Format – Absorption costing Format – Marginal costing

$ $

Sales X

Less: Cost of Sales (COS)

Opening stock X

+ Production costs X

X

Less: Closing stock (X)

(X)

X

(Under)/Over-absorption ±X

Gross Profit X

Less: Selling, distribution and admin

Variable X

Fixed X

(X)

Net profit/(loss) X

$ $

Sales X

Less: Variable Cost of Sales (COS)

Opening stock X

+ Variable production costs X

X

Less: Closing stock (X)

(X)

X Less: Variable selling, distribution and admin costs ±X

Contribution X

Less: Fixed costs

Production X

Selling, distribution, admin X

(X)

Net profit/(loss) X

Absorption costing complies with IAS 2 on accounting for inventory, while marginal costing doesn’t.

5. Profit reconciliation Profit as per absorption costing – (change in stock × fixed cost per unit)

= Profit as per marginal costing

• If closing inventory is higher than opening inventory, then absorption costing reports higher profits (due to the cost absorbed in the closing inventory being carried forward).

• If closing inventory is lower than opening inventory, then marginal costing reports higher profits.

• If inventory remains the same, then profit is the same under both methods.

• It is the timing of the sales that causes the differing profits.

P1 – Management Accounting CH1 – Traditional costing

Page 6

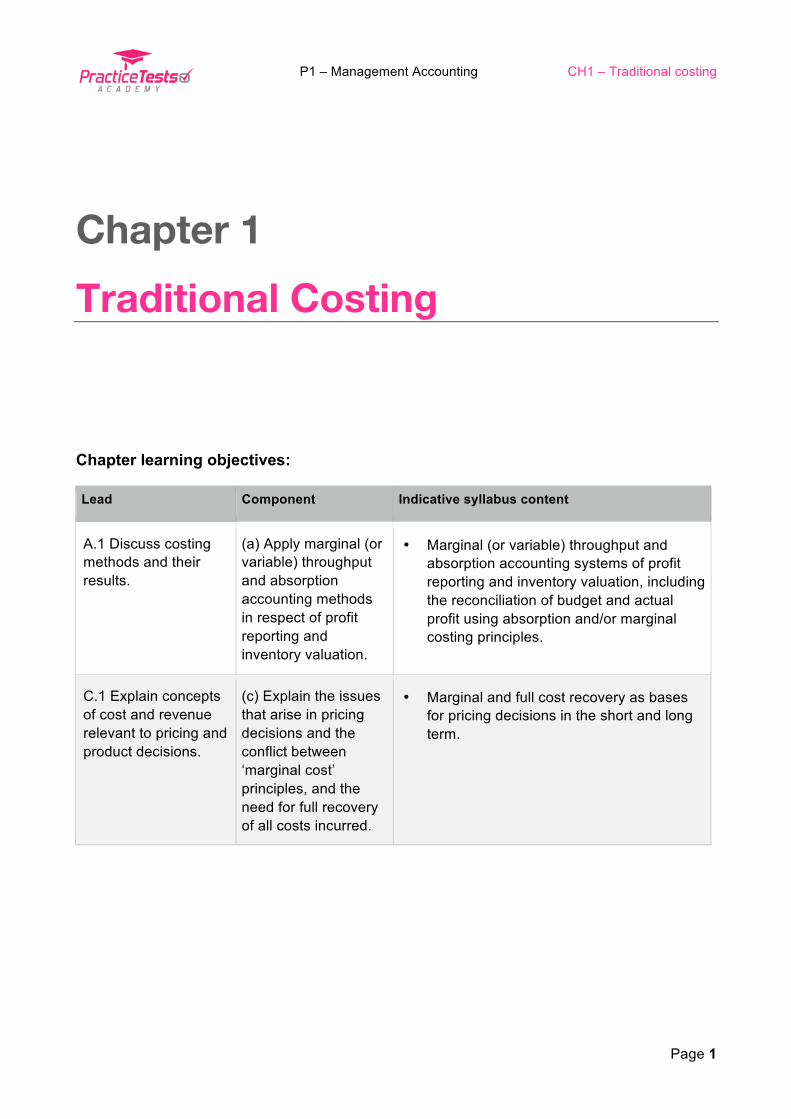

Test Your Understanding 2 – Reporting profits Lumia Ltd makes and sells an LED desk lamp. The budgeted selling price and variable cost details are as follows:

$

Selling price 45.00

Variable costs per unit

Direct materials 14.50

Direct labour 11.00

Variable overhead 5.50

Budgeted production is 45,000 units per annum.

Budgeted fixed overhead costs are $144,000 per annum, charged equally throughout the year.

In September the actual production was 12,500 units and exceeded sales by 320 units.

Please state the profit reported under absorption costing. $__________

P1 – Management Accounting CH1 – Traditional costing

Page 7

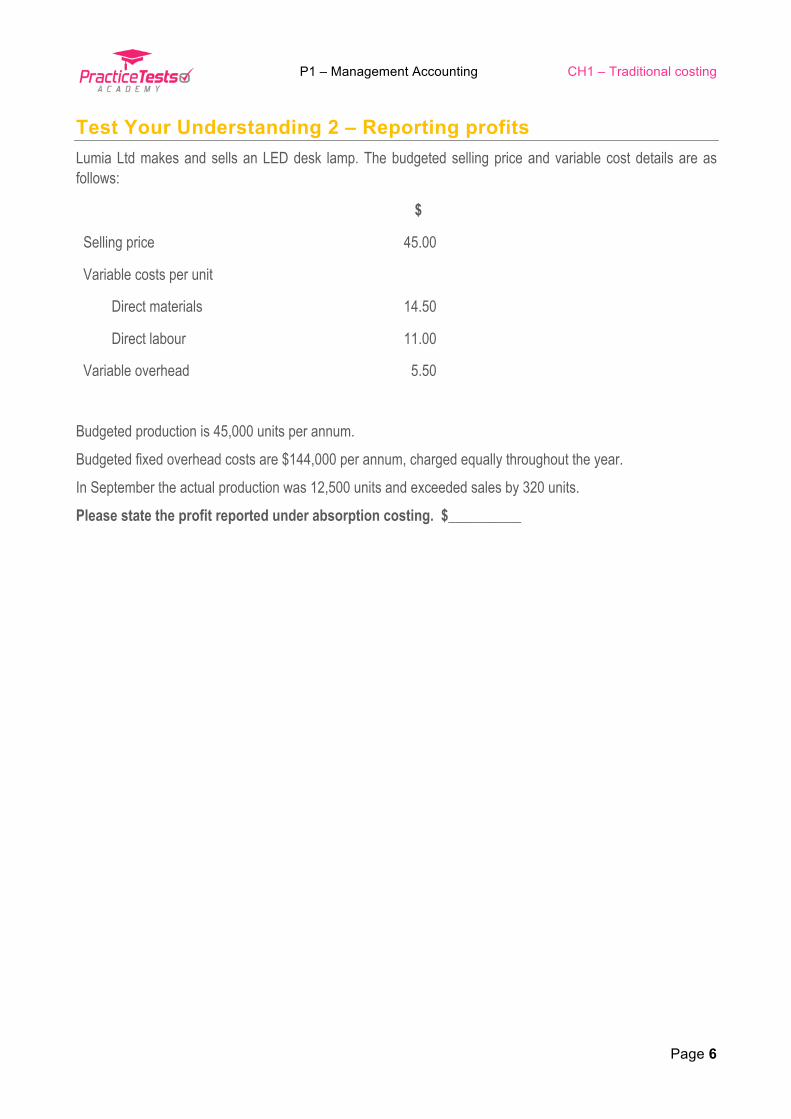

6. Pricing strategies • Full cost plus pricing, calculated as: full cost/unit × (1 + markup %)

• Marginal cost plus pricing, calculated as: marginal cost/unit × (1 + markup %)

7. Comparison: full cost plus & marginal cost plus pricing

FULL COST PLUS PRICING MARGINAL COST PLUS PRICING

Advantages Advantages

• Target profit will be achieved when budgeted sales are reached

• Allows a lower selling price to be set while covering the variable costs

• More relevant for industries where fixed costs are high in proportion to variable costs

• More relevant for one-off orders/contracts

• Validates the selling price set so as to cover all costs

• More useful in situations where there are bottlenecks/scarce resources

Disadvantages Disadvantages • Selling prices can vary depending on

what the apportionment basis was • A randomly chosen mark-up is expected to cover the fixed costs as well as earn a profit

• If the actual volume is lower than budgeted, overheads may not be completely recovered

8. Solutions to the ‘Test Your Understanding’ examples

Test Your Understanding 1 – Absorption costing The answer is $169,500.

Standard cost card:

$

Direct materials per unit 2 kgs × $5/kg 10

Direct labour per unit 1.5 hrs × $17/hr 25.5

Variable overheads 1.5 hrs × $6/hr 9

Production overheads per unit (*) 12

Full/absorption cost per unit 56.5

P1 – Management Accounting CH1 – Traditional costing

Page 8

(*) Production overhead per unit in the standard cost card should be based on budgeted production. Therefore they will be $360,000/30,000 = $12

Stock valuation

If 27,000 units were actually produced and 24,000 were actually sold, then there should be 3,000 units in closing stock.

Valuation

3,000 units × $56.50 = $169,500

Test Your Understanding 2 – Reporting profits The answer is $159,544. The quickest way would be to calculate the marginal profit and then use the reconciliation of profits to get to absorption costing profit.

The profit under marginal costing:

Contribution per unit = $45 – (14.50 + 11.00 + 5.50) = $14.00

Number of units sold = 12,500 - 320 = 12,180 units

$

Total contribution

$14.00/unit × 12,180 units

170,520

Fixed cost

$144,000 pa/12 months

12,000

158,520

As production is greater than sales, absorption costing will show the higher profit.

Difference in profit = change in inventory × fixed production overhead per unit (FOAR*)

Difference in profit = 320 units × $3.20*/unit = $1,024

Therefore, profit reported under absorption costing = $158,520 + $1,024 = $159,544

𝐹𝑂𝐴𝑅 =𝐵𝑢𝑑𝑔𝑒𝑡𝑒𝑑 𝑜𝑣𝑒𝑟ℎ𝑒𝑎𝑑𝑠

𝐵𝑢𝑑𝑔𝑒𝑡𝑒𝑑 𝑙𝑒𝑣𝑒𝑙 𝑜𝑓 𝑎𝑐𝑡𝑖𝑣𝑖𝑡𝑦 =$144,000$45,000 = $3.20 𝑝𝑒𝑟 𝑢𝑛𝑖𝑡

P1 – Management Accounting CH1 – Traditional costing

Page 9

9. Chapter summary