Embed Size (px)

Citation preview

Chapter 12

Principles of

Corporate FinanceEighth Edition

Agency Problems, Management

Compensation, and The Measurement

of PerformanceSlides by

Matthew Will

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

McGraw-Hill/Irwin

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

12- 2

McGraw-Hill/Irwin

Topics Covered

The Capital Investment ProcessDecision Makers Need Good InformationIncentivesResidual Income and EVABias in Accounting Measures of

Performance Measuring Economic Profitability

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

12- 3

McGraw-Hill/Irwin

The Principal Agent Problem

Shareholders = Owners

Managers = Employees

Question: Who has the power?

Answer: Managers

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

12- 4

McGraw-Hill/Irwin

Capital Investment Decision

Project Creation“Bottom Up”

Strategic Planning“Top Down”

Capital Investments

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

12- 5

McGraw-Hill/Irwin

Capital Investment Process

Capital budgetProject authorizationR&DMarketingPost-audits

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

12- 6

McGraw-Hill/Irwin

Off Budget Expenditures

Information TechnologyResearch and DevelopmentMarketingTraining and Development

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

12- 7

McGraw-Hill/Irwin

Information Problems

1. Consistent Forecasts

2. Reducing Forecast Bias

3. Getting Senior Management Needed Information

4. Eliminating Conflicts of Interest

The correct information

is …

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

12- 8

McGraw-Hill/Irwin

Brealey, Myers & Allen’s Second Law

The proportion of proposed The proportion of proposed projects having a positive NPV projects having a positive NPV at the official corporate hurdle at the official corporate hurdle

rate is independent of the rate is independent of the hurdle rate.hurdle rate.

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

12- 9

McGraw-Hill/Irwin

Incentives

Reduced effortPerksEmpire buildingEntrenching investmentAvoiding risk

Agency Problems in Capital Budgeting

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

12- 10

McGraw-Hill/Irwin

Incentive Issues

Monitoring - Reviewing the actions of managers and providing incentives to maximize shareholder value.

Free Rider Problem - When owners rely on the efforts of others to monitor the company.

Management Compensation - How to pay managers so as to reduce the cost and need for monitoring and to maximize shareholder value.

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

12- 11

McGraw-Hill/Irwin

CEO Compensation (2003-04)

0

500

1000

1500

2000

2500

$ 1,

000

s

Aus

tral

ia

Can

ada

Chi

na

Fan

ce

Ger

man

y

Indi

a

Ital

y

Japa

n

Mex

ico

Net

herl

ands

Sing

apor

e

Spai

n

Swed

en

Swit

zerl

and

Uni

ted

Kin

gdom

Uni

ted

Stat

es

Benefits

Perks

Options & Others

Variable Bonus

Basic Compensation

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

12- 12

McGraw-Hill/Irwin

Residual Income & EVA

Techniques for overcoming errors in accounting measurements of performance.

Emphasizes NPV concepts in performance evaluation over accounting standards.

Looks more to long term than short term decisions.

More closely tracks shareholder value than accounting measurements.

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

12- 13

McGraw-Hill/Irwin

Residual Income & EVA

Income

Sales 550

COGS 275

Selling, G&A 75

200

taxes @ 35% 70

Net Income $130

Assets

Net W.C. 80

Property, plant and equipment 1170

less depr. 360

Net Invest.. 810

Other assets 110

Total Assets $1,000

Quayle City Subduction Plant ($mil)Quayle City Subduction Plant ($mil)

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

12- 14

McGraw-Hill/Irwin

Residual Income & EVA

Quayle City Subduction Plant ($mil)Quayle City Subduction Plant ($mil)

13.000,1

130ROI

Given COC = 10%

%3%10%13 NetROI

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

12- 15

McGraw-Hill/Irwin

Residual Income & EVA

Residual Income or EVA = Net Dollar return after deducting the cost of capital

© EVA is copyrighted by Stern-Stewart Consulting Firm and used with permission.

Investment Capital ofCost - Earned Income

required income-Earned Income

Income Residual

EVA

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

12- 16

McGraw-Hill/Irwin

Residual Income & EVA

Quayle City Subduction Plant ($mil)Quayle City Subduction Plant ($mil)

Given COC = 10%

million 03$

)000,110(.130

Income Residual

EVA

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

12- 17

McGraw-Hill/Irwin

Economic Profit

Economic Profit = capital invested multiplied by the spread between return on investment and the cost of capital.

© EVA is copyrighted by Stern-Stewart Consulting Firm and used with permission.

Invested Capital)(

Profit Economic

rROI

EP

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

12- 18

McGraw-Hill/Irwin

Economic Profit

© EVA is copyrighted by Stern-Stewart Consulting Firm and used with permission.

Quayle City Subduction Plant ($mil)Quayle City Subduction Plant ($mil)

Example at 10% COC continued.

million $30

1,000.10)-.13(

Invested Capital)(

rROIEP

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

12- 19

McGraw-Hill/Irwin

Message of EVA

+ Managers are motivated to only invest in projects that earn more than they cost.

+ EVA makes cost of capital visible to managers.

+ Leads to a reduction in assets employed.

- EVA does not measure present value

- Rewards quick paybacks and ignores time value of money

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

12- 20

McGraw-Hill/Irwin

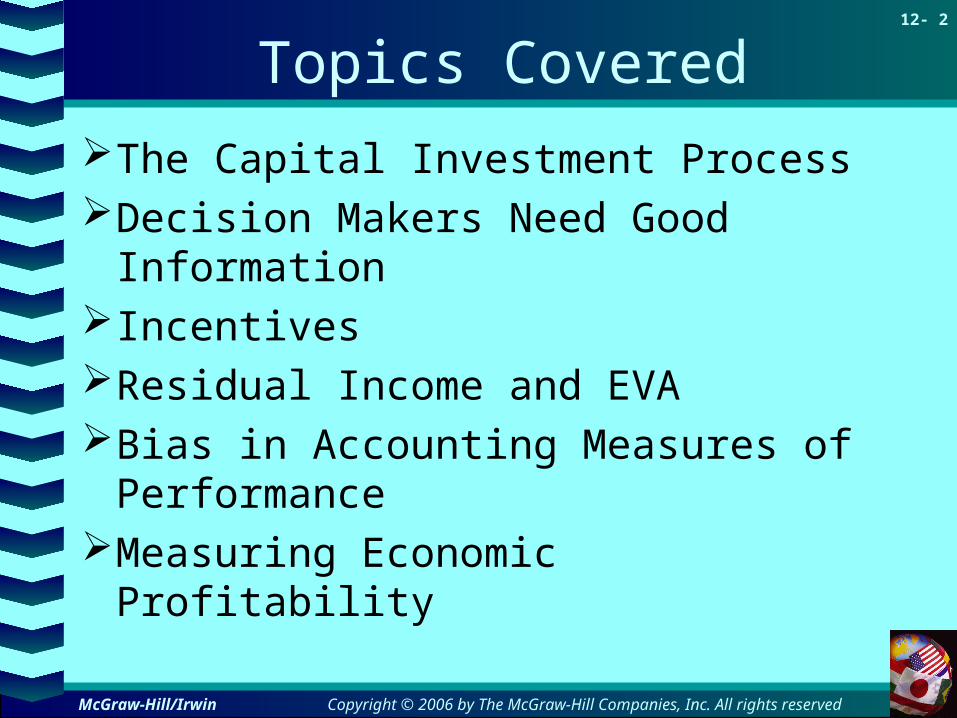

EVA of US firms - 2003

($ in millions)

Econimic Value Added (EVA)

Capital Invested

Return on Capital

Cost of Capital NPV

Wal-Mart Stores 4,525 79,177 12.30% 6.60% 68,380

Johnson & Johnson 4,459 51,508 17.6 8.9 50,351Microsoft 4,027 24,677 29.8 13.5 29,795Merck 3,347 40,941 16.9 8.7 38,588Coca Cola 2,729 20,503 20.1 6.7 41,006Intel Corp. (57) 31,216 15.6 15.8 -395Dow Chemical (1,503) 44,158 3.6 7 -21,448Boeing (1,974) 50,046 2.2 6.1 -31,997Delta Airlines (2,288) 27,238 -0.9 7.5 -30,507Viacom (5,508) 96,515 3.5 9.2 -59,797IBM (7,505) 108,926 4.6 11.5 -65,356

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

12- 21

McGraw-Hill/Irwin

Accounting Measurements

0

011 )(

price beginning

price in changereceipts cashreturn of Rate

P

PPC

Economic income = cash flow + change in present value

0

011 )(return of Rate

PV

PVPVC

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

12- 22

McGraw-Hill/Irwin

Accounting Measurements

ECONOMIC ACCOUNTING

Cash flow + Cash flow +

change in PV = change in book value =

Cash flow - Cash flow -

economic depreciation accounting depreciation

Economic income Accounting income

PV at start of year BV at start of year

INCOME

RETURN

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

12- 23

McGraw-Hill/Irwin

Nodhead Book Income & ROI

1 2 3 4 5 6

Cash flow 100 200 250 298 298 298Book value at start of year, straight-line depreciation 1000 833 667 500 333 167Book value at end of year, straight-line depreciation 833 667 500 333 167 0Book depreciation 167 167 167 167 167 167Book income -67 33 83 131 131 131Book ROI -6.70% 3.96% 12.44% 26.20% 39.34% 78.44%Forecasted EVA -167 -50 16 81 98 114

Year

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

12- 24

McGraw-Hill/Irwin

Elements of a Desirable Monitoring System

Long Run View: Can distinguish between desirable and undesirable

decisions Reflects what is happening to the stockholders’

wealth Takes into account scarce capital allocations Takes into account the opportunity cost of capital

How does EVA and ROI do with respect to these?

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

12- 25

McGraw-Hill/Irwin

Nodhead Store ForecastsEconomic Profitability

1 2 3 4 5 6

Cash flow 100 200 250 298 298 298PV, at start of year, 10 percent discount rate $1,000.81 1000 901 741 517 271PV, at end of year, 10 percent discount rate 1,001 901 741 517 271 0Economic depreciation 0 100 160 224 246 271Economic income $100 $100 $90 $74 $52 $27Rate of return 10.00% 10.00% 10.00% 10.01% 10.00% 10.00%Forecasted EVA (5-.1*2) $0.00 $0.00 $0.00 $0.09 $0.02 ($0.01)Book value at start of year, straight-line depreciation 1000 833 667 500 333 167

Book ROI -6.70% 3.96% 12.44% 26.20% 39.34% 78.44%

Year

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

12- 26

McGraw-Hill/Irwin

Elements of a Desirable Monitoring System

Long Run View: Can distinguish between desirable and undesirable

decisions Reflects what is happening to the stockholders’

wealth Takes into account scarce capital allocations Takes into account the opportunity cost of capital

How does Economic Profitability and Rate of Return do on these dimensions?

Copyright © 2006 by The McGraw-Hill Companies, Inc. All rights reserved

12- 27

McGraw-Hill/Irwin

Web Resources

www.sternstewart.com

www.emblemsvag.com/economic_profit.htm

Click to access web sitesClick to access web sites

Internet connection requiredInternet connection required