Embed Size (px)

Citation preview

Chapter 2

The structure of the profession

Copyright © 2010 McGraw-Hill Australia Pty Ltd PPTs t/a Auditing and Assurance Services in Australia 4e by Grant Gay and Roger SimnettSlides prepared by Roger Simnett

2-1

Learning objective 1:Professional status of the auditor

• Professional occupations can be distinguished by five common attributes:

1. Systematic theory

2. Professional authority and expertise

3. Community sanction

4. Regulative codes

5. Well-established culture

2-2Copyright © 2010 McGraw-Hill Australia Pty Ltd PPTs t/a Auditing and Assurance Services in Australia 4e by Grant Gay and Roger SimnettSlides prepared by Roger Simnett

Auditing as a profession

• Auditing can be classified as a profession because of its:

– Reliance on an underlying theory of accounting and auditing

– Expertise– Ability to control admissions to the profession– Regulative codes in two areas, technical and ethical – Behavioural subculture exhibiting integrity,

independence, objectivity, confidentiality and public interest.

2-3Copyright © 2010 McGraw-Hill Australia Pty Ltd PPTs t/a Auditing and Assurance Services in Australia 4e by Grant Gay and Roger SimnettSlides prepared by Roger Simnett

Learning objective 2: Regulation of auditing

• Financial Reporting Council (FRC): a statutory body established in 1999 with the responsibility of providing a broad oversight of the accounting standard-setting process. This role was recently expanded to include a broad oversight of auditing standard-setting and the monitoring of auditor independence.

2-4Copyright © 2010 McGraw-Hill Australia Pty Ltd PPTs t/a Auditing and Assurance Services in Australia 4e by Grant Gay and Roger SimnettSlides prepared by Roger Simnett

The Auditing and Assurance Standards Board (AUASB)

The AUASB was reconstituted as an independentstatutory body on 1 July 2004 and is responsible for the development of auditing and assurance services standards.– The Board consists of 12 members appointed by FRC,

and a Chair appointed by the Minister for Superannuation and Corporate Law.

– Responsibility for the final approval of auditing and assurance standards now lies with parliament.

– The AUASB has a long-standing policy of convergence and harmonisation with International Standards on Auditing (ISAs).

2-5Copyright © 2010 McGraw-Hill Australia Pty Ltd PPTs t/a Auditing and Assurance Services in Australia 4e by Grant Gay and Roger SimnettSlides prepared by Roger Simnett

The Accounting Professional and Ethical Standards Board (APESB)

• Until 2006 the accounting bodies in Australia maintained control of the setting of ethical standards.

• Since 2006, setting of ethical standards is to be done by a body independent of the accounting profession, the APESB.

• The APESB establishes ethical standards, as well as professional standards, by which the members of the professional accounting bodies are required to abide.

• The APESB consists of eight members, including two nominated by CPA Australia and two by ICAA.

2-6Copyright © 2010 McGraw-Hill Australia Pty Ltd PPTs t/a Auditing and Assurance Services in Australia 4e by Grant Gay and Roger SimnettSlides prepared by Roger Simnett

Regulation of auditing (cont.)

• Two other government agencies are also involved in the regulation of auditors:

1. Australian Securities and Investments Commission (ASIC) — the administering authority for the Corporations Act 2001.

2. The Companies Auditors and Liquidators Disciplinary Board (CALDB) determines whether a registered auditor or liquidator has failed to carry out his or her duties properly or is not a fit and proper person to be registered.

2-7Copyright © 2010 McGraw-Hill Australia Pty Ltd PPTs t/a Auditing and Assurance Services in Australia 4e by Grant Gay and Roger SimnettSlides prepared by Roger Simnett

Registered company auditor (RCA)

• In order to be appointed as a company auditor under s 1280 of the Corporations Act 2001, a person must:

– Be ordinarily resident in Australia– Be a member of an approved accounting body– Be a graduate of a prescribed university or other prescribed

institution in Australia, and have passed a course in accounting and commercial law acceptable to ASIC

– Have sufficient auditing experience– Be a fit and proper person.

• Auditors are required to fill out a logbook to demonstrate on-the-job experience and have this certified by current RCA.

2-8Copyright © 2010 McGraw-Hill Australia Pty Ltd PPTs t/a Auditing and Assurance Services in Australia 4e by Grant Gay and Roger SimnettSlides prepared by Roger Simnett

Learning objective 3:Regulation of subject matter of

audits

• Australian Accounting Standards Board (AASB):

– Responsible for the development of accounting standards in Australia.

• Financial Reporting Panel (FRP):

– Established in 2004 to provide a forum for review of disputes between ASIC and entities lodging reports with ASIC.

2-9Copyright © 2010 McGraw-Hill Australia Pty Ltd PPTs t/a Auditing and Assurance Services in Australia 4e by Grant Gay and Roger SimnettSlides prepared by Roger Simnett

Disciplinary procedures

• Independent auditors are subject to disciplinary provisions of the their professional accounting bodies, either ICAA, CPA Australia and the NIA.

• Sanctions can include:– Exclusion from membership– Suspension from membership– Disbarment from practice– Being fined a sum not exceeding $100 000– Being reprimanded; or– Having to pay costs and expenses of any investigation.

2-10Copyright © 2010 McGraw-Hill Australia Pty Ltd PPTs t/a Auditing and Assurance Services in Australia 4e by Grant Gay and Roger SimnettSlides prepared by Roger Simnett

Learning objective 4: Internationalisation of auditing

• Increased international trade has contributed to the development of international auditing practices.

• Multinational organisations wish to ensure the quality of financial information from subsidiaries and related entities.

• The International Organization of Securities Commissions (IOSCO) (including SEC in the USA and ASIC in Australia) supports the harmonisation of international auditing standards.

• Most countries consider International Standards on Auditing (ISAs) carefully when developing their own standards.

2-11Copyright © 2010 McGraw-Hill Australia Pty Ltd PPTs t/a Auditing and Assurance Services in Australia 4e by Grant Gay and Roger SimnettSlides prepared by Roger Simnett

Internationalisation of auditing (cont.)

• Key groups

– International Federation of Accountants (IFAC): guides efforts to develop technical (accounting and auditing) and ethical standards. Members include 158 accounting bodies (including ICAA, CPA Australia and the NIA) in 123 countries.

– International Auditing and Assurance Standards Board (IAASB): an independent body supported by IFAC that develops standards and guidance for audit and assurance services.

2-12Copyright © 2010 McGraw-Hill Australia Pty Ltd PPTs t/a Auditing and Assurance Services in Australia 4e by Grant Gay and Roger SimnettSlides prepared by Roger Simnett

Internationalisation of auditing (cont.)

• Key groups (cont.)

– Transnational Auditors Committee (TAC): executive committee of the Forum of Firms (FOF) that performs auditing across national boundaries. In 2009 there were 21 full members (international auditing firms) and one provisional member. Commitments by the firms to the obligations of membership of the FOF contributes to raising the standards of the international practice of auditing.

2-13Copyright © 2010 McGraw-Hill Australia Pty Ltd PPTs t/a Auditing and Assurance Services in Australia 4e by Grant Gay and Roger SimnettSlides prepared by Roger Simnett

Learning objective 5: Profile of the auditing profession

• There are three primary professional accounting organisations in Australia:1. CPA Australia

2. The Institute of Chartered Accountants in Australia (ICAA)

3. The National Institute of Accountants.

• Membership of these bodies by public accounting practitioners is voluntary.

• However, membership of one of these bodies (or another prescribed body) is necessary in order to become a registered company auditor.

2-14Copyright © 2010 McGraw-Hill Australia Pty Ltd PPTs t/a Auditing and Assurance Services in Australia 4e by Grant Gay and Roger SimnettSlides prepared by Roger Simnett

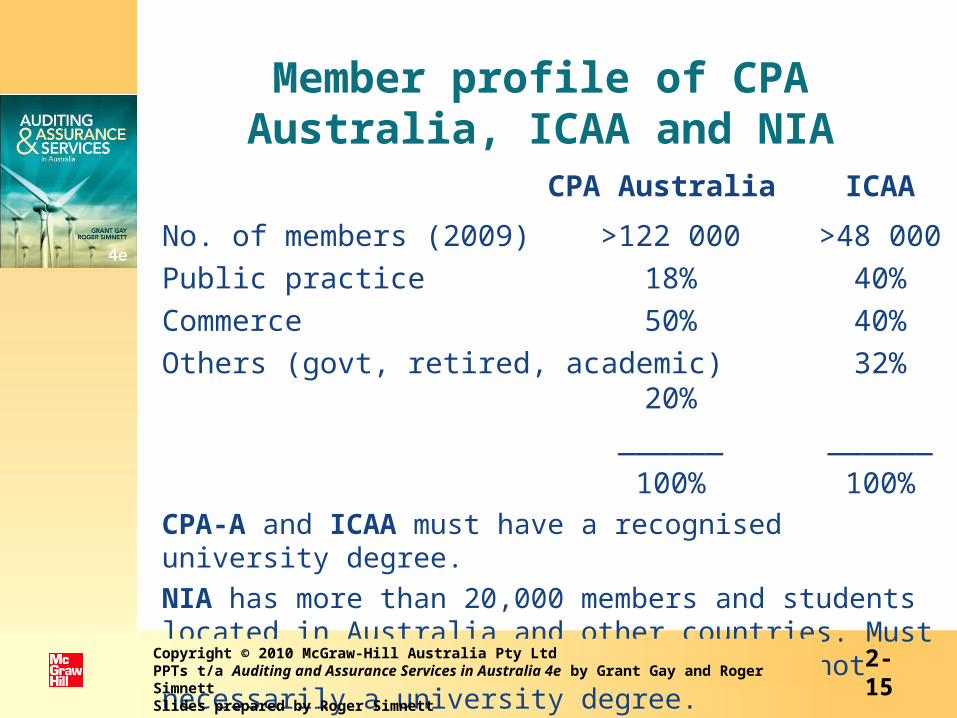

Member profile of CPA Australia, ICAA and NIA

2-15

CPA Australia ICAA

No. of members (2009) >122 000 >48 000

Public practice 18% 40%

Commerce 50% 40%

Others (govt, retired, academic) 32% 20%

______ ______

100% 100%CPA-A and ICAA must have a recognised university degree.

NIA has more than 20,000 members and students located in Australia and other countries. Must have prescribed standard of education, not necessarily a university degree.

Copyright © 2010 McGraw-Hill Australia Pty Ltd PPTs t/a Auditing and Assurance Services in Australia 4e by Grant Gay and Roger SimnettSlides prepared by Roger Simnett

Audit firms

• There are three levels of audit firms in Australia:1. International (including the Big Four and other firms that

are members of Forum of Firms)2. National Firms3. Regional or local firms.

• The largest international firms are known as the 'Big Four'. They are:– PricewaterhouseCoopers– Ernst & Young– KPMG Australia– Deloitte.

• The Big Four dominate the practice of public accounting, especially for listed clients.

2-16Copyright © 2010 McGraw-Hill Australia Pty Ltd PPTs t/a Auditing and Assurance Services in Australia 4e by Grant Gay and Roger SimnettSlides prepared by Roger Simnett

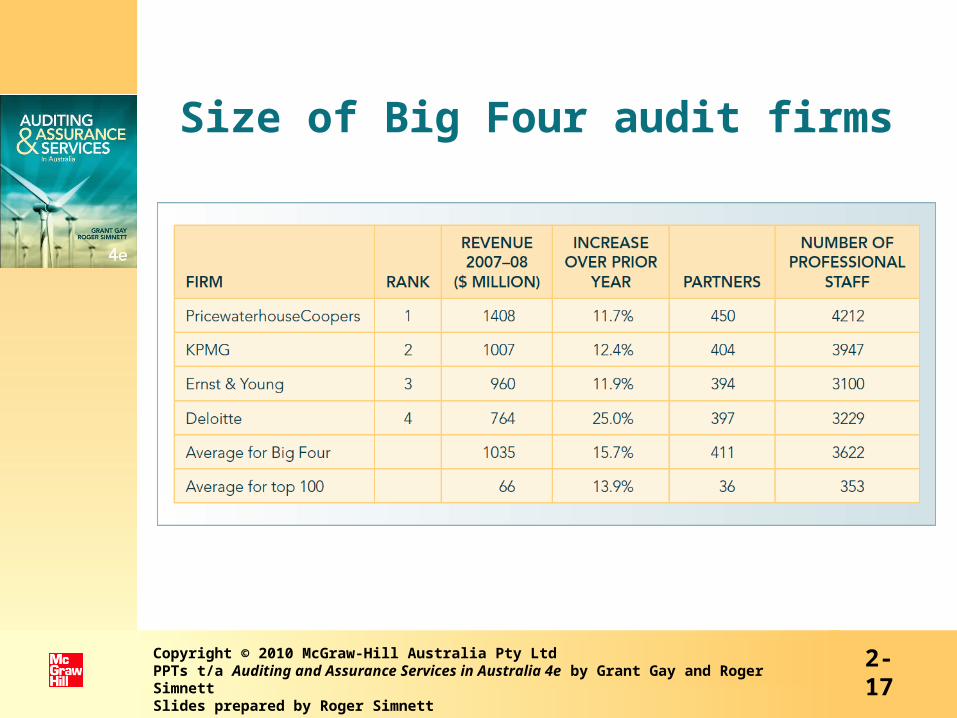

Size of Big Four audit firms

2-17Copyright © 2010 McGraw-Hill Australia Pty Ltd PPTs t/a Auditing and Assurance Services in Australia 4e by Grant Gay and Roger SimnettSlides prepared by Roger Simnett

Other services offered

• While audit and assurance services form a substantial part of a public accounting firm’s client base and revenue stream, most firms also offer:

– Taxation– Management services– Internal audit– Accounting services– Insolvency services

2-18Copyright © 2010 McGraw-Hill Australia Pty Ltd PPTs t/a Auditing and Assurance Services in Australia 4e by Grant Gay and Roger SimnettSlides prepared by Roger Simnett

Learning objective 6: Internal structure of an audit firm

• Currently, an audit firm generally practises as a partnership.

• An audit firm can now apply to be an authorised audit company. This provides advantages of limitations in liability and majority of voting power must be in hands of Registered Company Auditors. Adequate professional indemnity insurance must be maintained.

• Most large audit practices are usually structured along industry specialisations.

2-19Copyright © 2010 McGraw-Hill Australia Pty Ltd PPTs t/a Auditing and Assurance Services in Australia 4e by Grant Gay and Roger SimnettSlides prepared by Roger Simnett

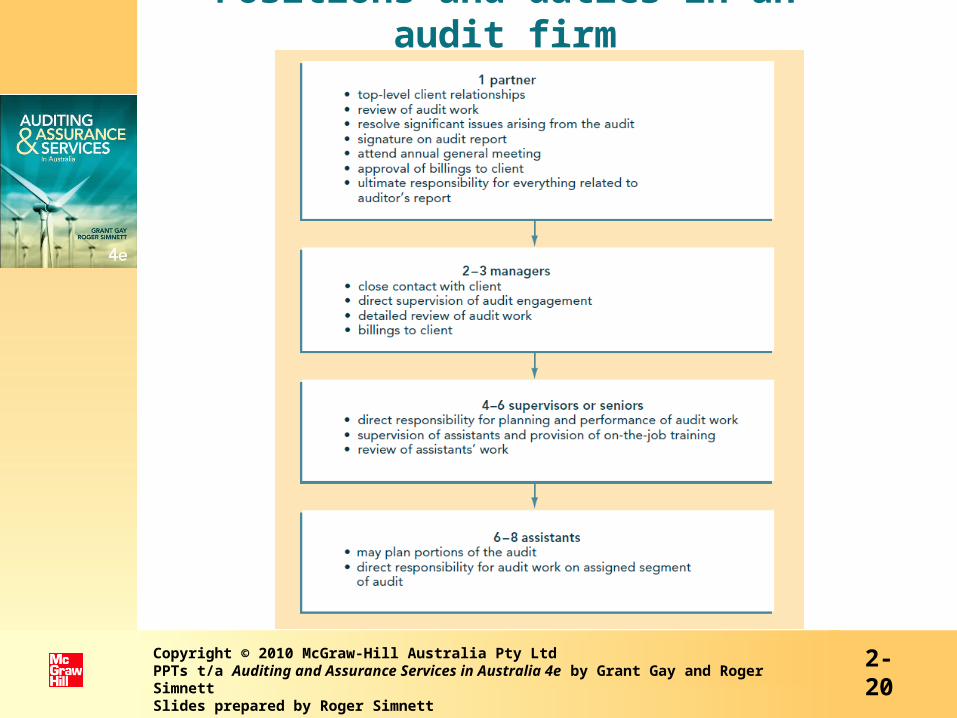

Positions and duties in an audit firm

2-20Copyright © 2010 McGraw-Hill Australia Pty Ltd PPTs t/a Auditing and Assurance Services in Australia 4e by Grant Gay and Roger SimnettSlides prepared by Roger Simnett

Learning objective 7:Quality control

• Quality controls (QCs) are implemented at both the audit firm level and at the audit engagement level.

• ASA 220 (ISA 220) requires the audit engagement team to implement QC procedures.

• ASQC 1 and APES 320 (ISQC 1)requires the audit firm to implement QCs.

• ASA 220 (ISA 220) acknowledge that the engagement team may rely on the audit firm’s system of QC.

2-21Copyright © 2010 McGraw-Hill Australia Pty Ltd PPTs t/a Auditing and Assurance Services in Australia 4e by Grant Gay and Roger SimnettSlides prepared by Roger Simnett

2-22

APESB standardsTwo APESB standards relate to QC:1. APES 210 establishes auditors’ responsibilities

in relation to compliance with Australian auditing and assurance standards.

2. APES 320 establishes basic principles and essential procedures at the audit firm level. Under APES 320, firms must document QC procedures and communicate these to the firm’s personnel, and implement more comprehensive policies and procedures for the assurance part of the firm.

As part of the clarity project, AUASB issued ASQC 1, (based on ISQC 1), with similar requirements toAPES 320.Copyright © 2010 McGraw-Hill Australia Pty Ltd PPTs t/a Auditing and Assurance Services in Australia 4e by Grant Gay and Roger SimnettSlides prepared by Roger Simnett

APES 320 and ASQC 1APES 320 and ASQC 1 (ISQC 1) require a firm’s

system of QC to include policies and procedures

relating to:– Leadership responsibilities for quality within

the firm– Relevant ethical requirements– Acceptance and continuance and client

relationships– Human resources– Engagement performance; and– Monitoring.

2-23Copyright © 2010 McGraw-Hill Australia Pty Ltd PPTs t/a Auditing and Assurance Services in Australia 4e by Grant Gay and Roger SimnettSlides prepared by Roger Simnett

APES 320 and ASQC 1 (cont.)QC procedures adopted by auditing firms should

provide reasonable assurance of:• Ethics: personnel should adhere to principles of integrity, objectivity,

independence, confidentiality and professional behaviour• Employment: employ personnel with necessary technical skills and

professional competence• Assignment: work should be assigned to appropriately qualified

personnel• Supervision: work should be properly directed, supervised and

reviewed• Guidance and assistance: appropriate consultation should occur• Client evaluation: prospective and ongoing clients should be

evaluated for decision to accept or retain; and• Monitor: adequacy and effectiveness of QC procedures should be

continually monitored.

2-24Copyright © 2010 McGraw-Hill Australia Pty Ltd PPTs t/a Auditing and Assurance Services in Australia 4e by Grant Gay and Roger SimnettSlides prepared by Roger Simnett

2-25

Other quality control procedures

• Other key quality control procedures employed include:

– Internal review (engagement quality control review) — auditor subject to review by another partner in the practice

– Periodical rotation of auditors (partners and staff) to limit length of time spent on one client

– Peer reviews — independent periodic review by another firm of public accountants

– Continuing professional education requirements.

Copyright © 2010 McGraw-Hill Australia Pty Ltd PPTs t/a Auditing and Assurance Services in Australia 4e by Grant Gay and Roger SimnettSlides prepared by Roger Simnett

2-26

Learning objective 8: Auditing in the public sector

• Another important auditing sector, separate to the private auditing sector, is the public auditing sector.

• Many public sector entities require auditing.• Responsibility for public sector audits rests with

the Commonwealth and State Auditors-General.• They use auditing standards approved by the AUASB

as the basis of their auditing standards.• Sometimes audit mandate prescribes wider

inclusions than just financial statements. Compliance and performance audits may be required. (This is further discussed in Ch 15).

Copyright © 2010 McGraw-Hill Australia Pty Ltd PPTs t/a Auditing and Assurance Services in Australia 4e by Grant Gay and Roger SimnettSlides prepared by Roger Simnett