Embed Size (px)

Citation preview

1

Chapter 3Understanding Money Management

Nominal and Effective Interest RatesEquivalence CalculationsChanging Interest RatesDebt Management

2

Understanding Money Management

Financial institutions often quote interest rate based on an APR.In all financial analysis, we need to convert the APR into an appropriate effective interest rate based on a payment period.When payment period and interest period differ, calculate an effective interest rate that covers the payment period.

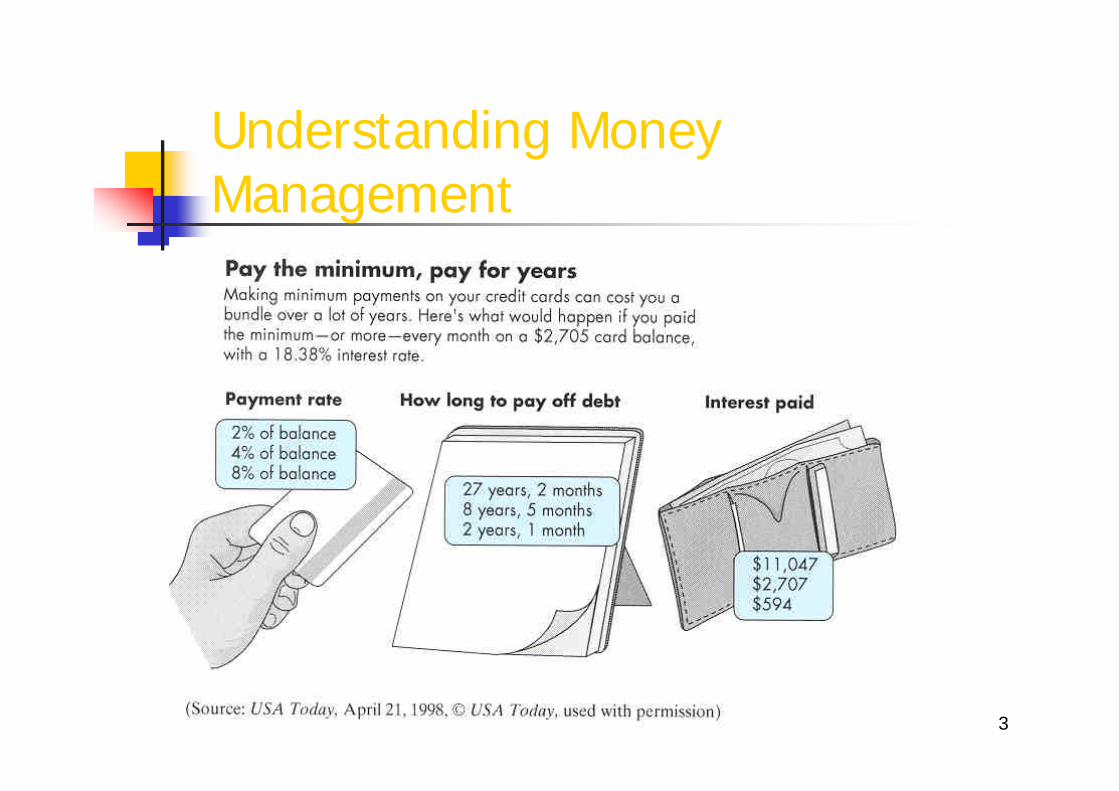

3

Understanding Money Management

4

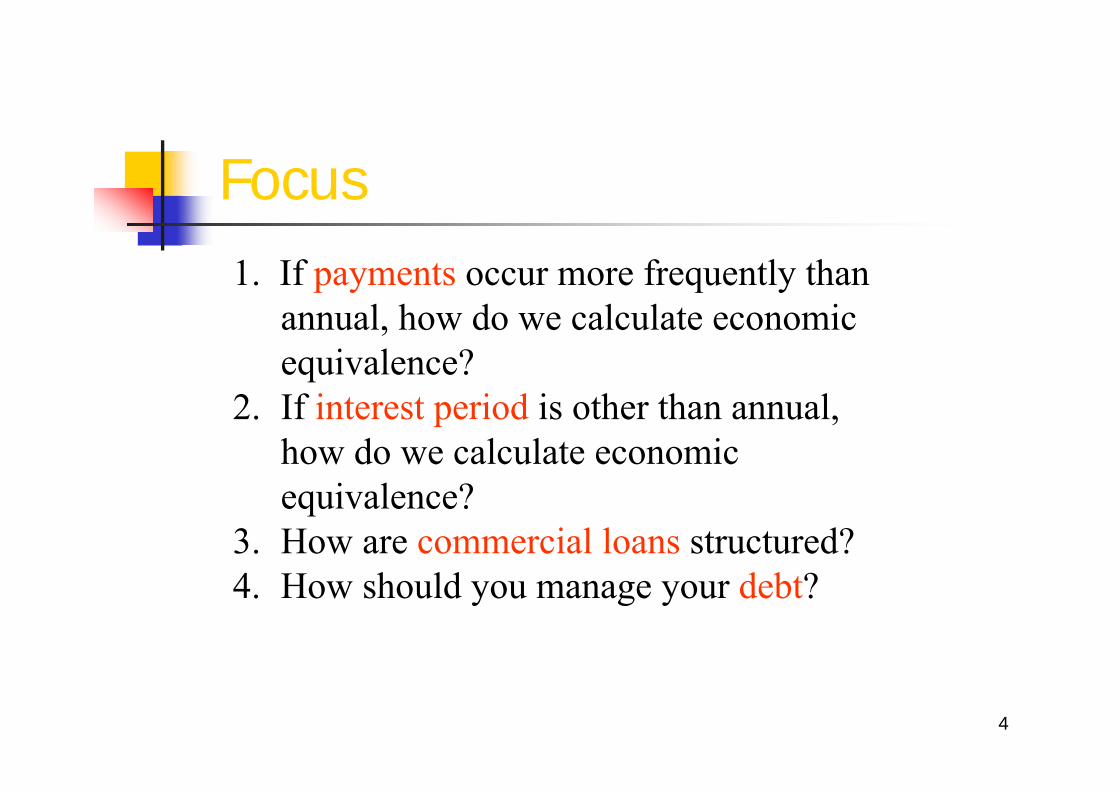

Focus1. If payments occur more frequently than

annual, how do we calculate economic equivalence?

2. If interest period is other than annual, how do we calculate economic equivalence?

3. How are commercial loans structured?4. How should you manage your debt?

5

Nominal Versus Effective Interest Rates

Nominal Interest Rate:Interest rate quoted based on an annual period

Effective Interest Rate:Actual interest earned or paid in a year or some other time period

6

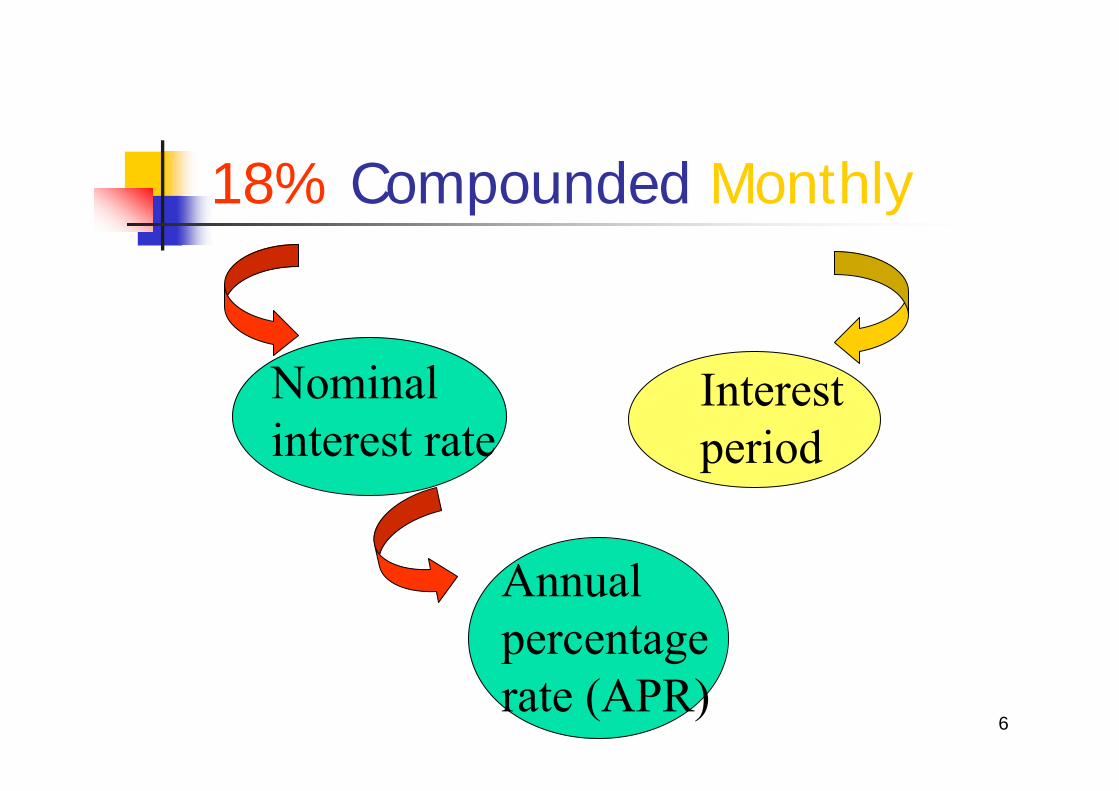

18% Compounded Monthly

Nominal interest rate

Annual percentagerate (APR)

Interest period

7

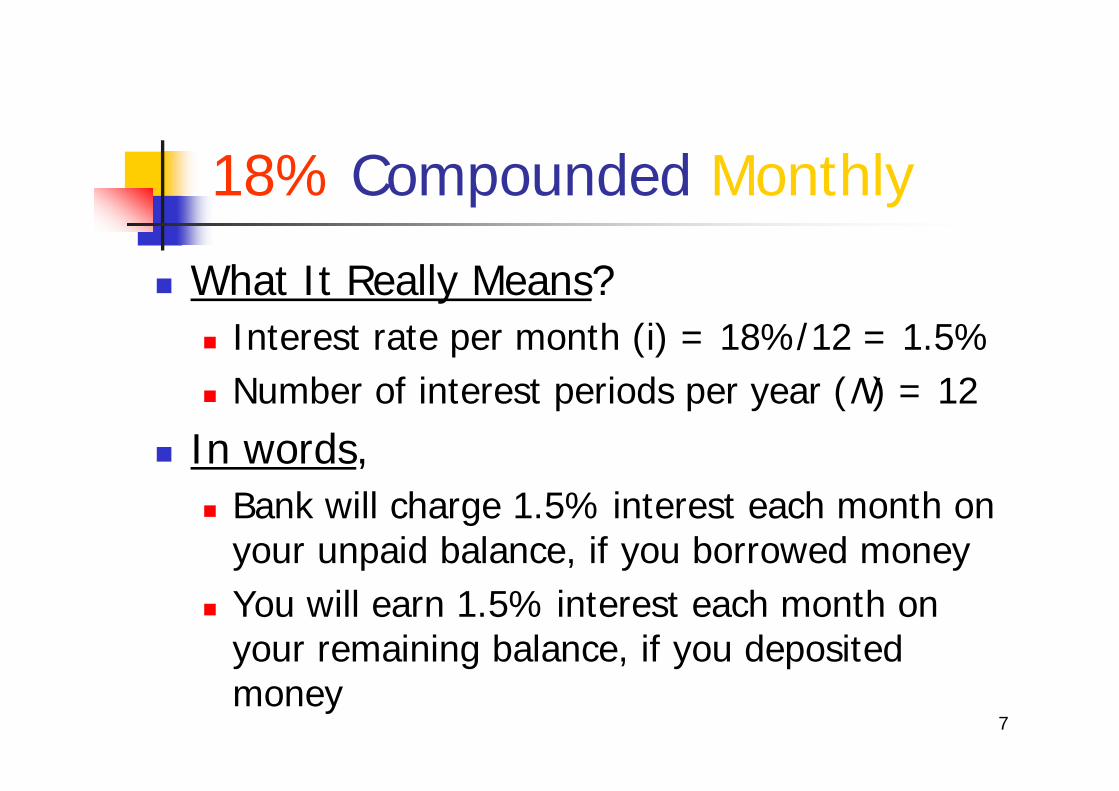

18% Compounded Monthly

What It Really Means?Interest rate per month (i) = 18%/12 = 1.5%Number of interest periods per year (N) = 12

In words,Bank will charge 1.5% interest each month on your unpaid balance, if you borrowed money You will earn 1.5% interest each month on your remaining balance, if you deposited money

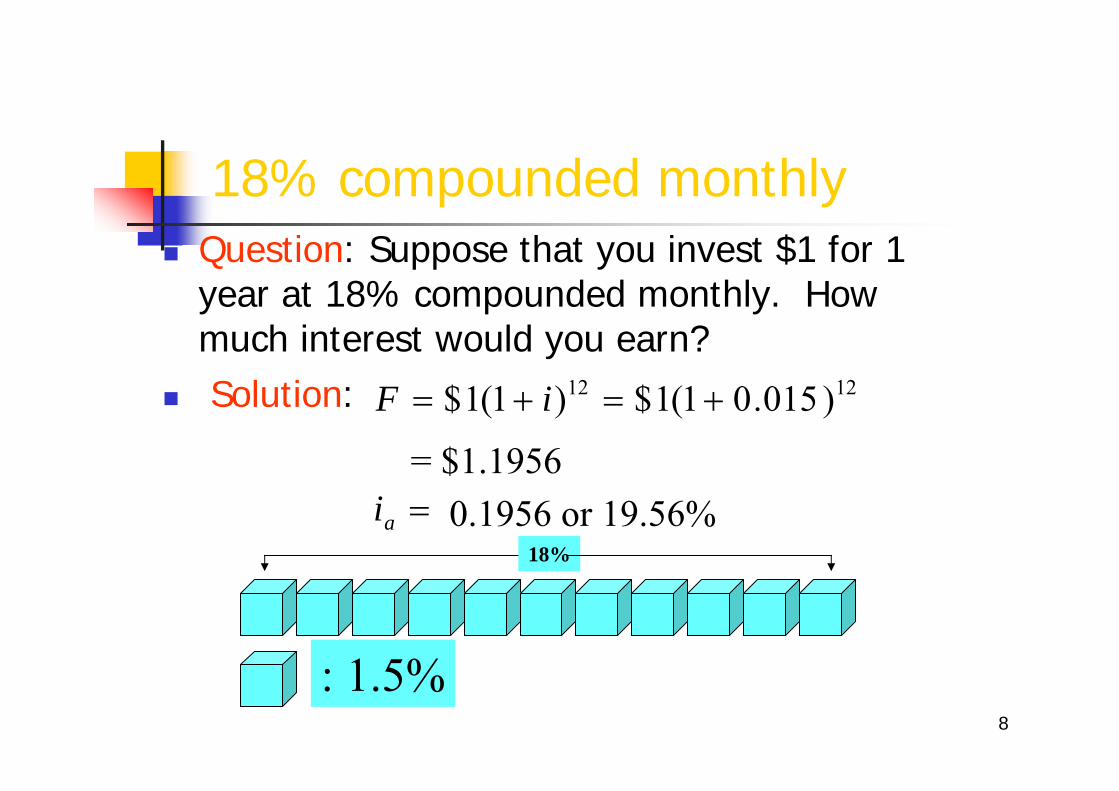

8

18% compounded monthlyQuestion: Suppose that you invest $1 for 1 year at 18% compounded monthly. How much interest would you earn?Solution:

=

+=+=

ai

iF 1212 )015.01(1$)1(1$

= $1.19560.1956 or 19.56%

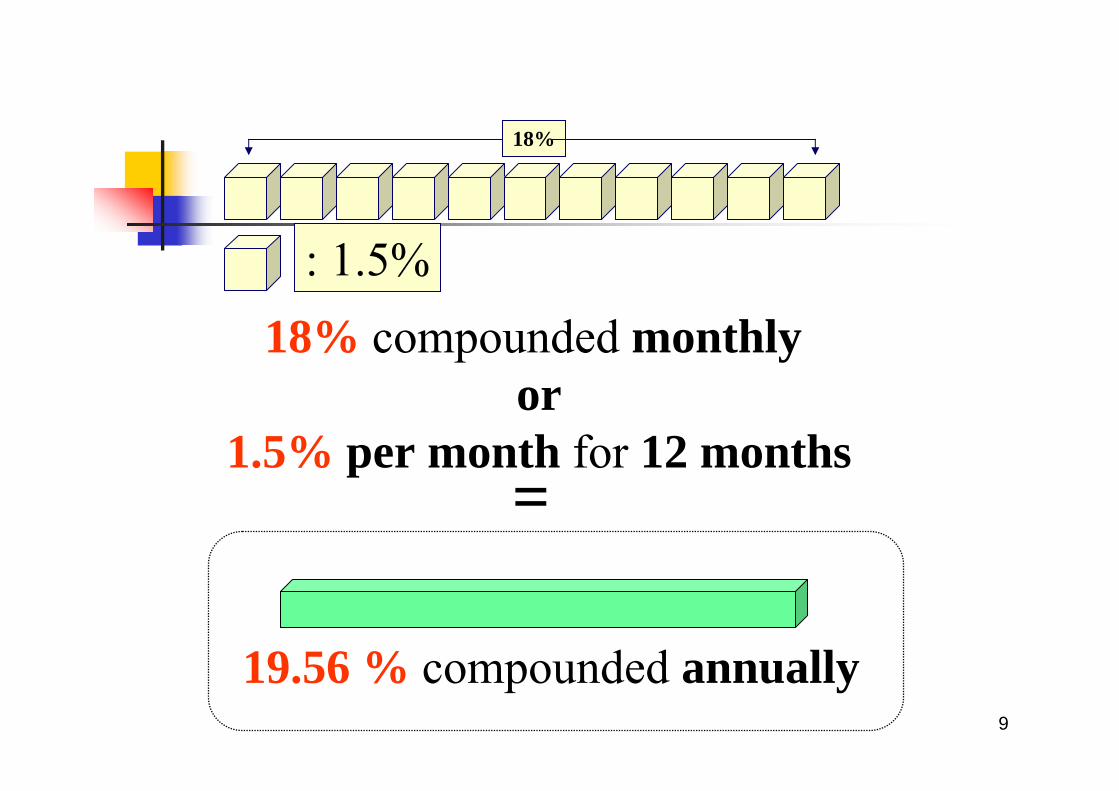

: 1.5%

18%

9

: 1.5%

18%

18% compounded monthly or

1.5% per month for 12 months=

19.56 % compounded annually

10

Effective Annual Interest Rate(Annual Effective Yield)

r = nominal interest rate per yearia = effective annual interest rateM = number of interest periods per

year

1)/1( −+= Ma Mri

11

Practice Problem

If your credit card calculates the interest based on 12.5% APR, what is your monthly interest rate and annual effective interest rate, respectively?Your current outstanding balance is $2,000 and skips payments for 2 months. What would be the total balance 2 months from now?

12

Solution

12

2

Monthly Interest Rate:12.5% 1.0417%

12Annual Effective Interest Rate:

(1 0.010417) 13.24%Total Outstanding Balance:

$2,000( / ,1.0417%,2)$2,041.88

a

i

i

F B F P

= =

= + =

= ==

-1

13

Practice Problem

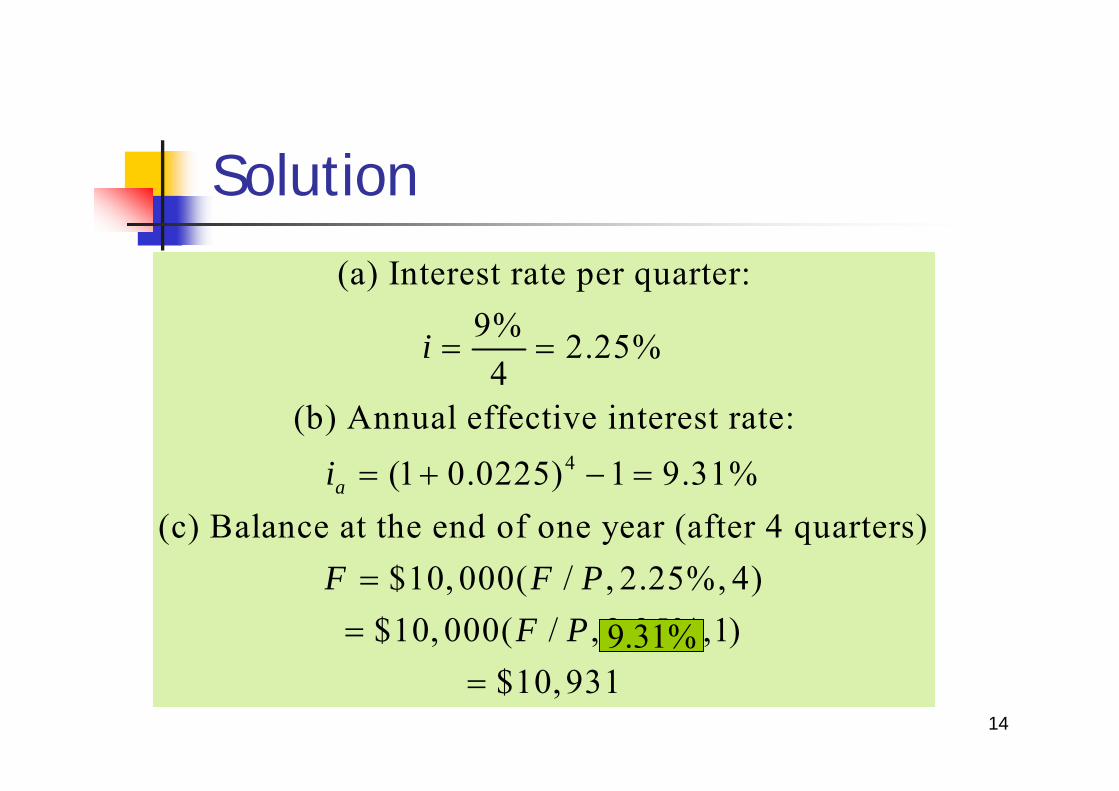

Suppose your savings account pays 9% interest compounded quarterly. If you deposit $10,000 for one year, how much would you have?

14

Solution

4

(a) Interest rate per quarter:9% 2.25%4

(b) Annual effective interest rate:(1 0.0225) 1 9.31%

(c) Balance at the end of one year (after 4 quarters)$10, 000( / , 2.25%, 4)

$10, 000( / , 2.25%,1)$10, 9

a

i

i

F F PF P

= =

= + − =

==

= 319.31%

15

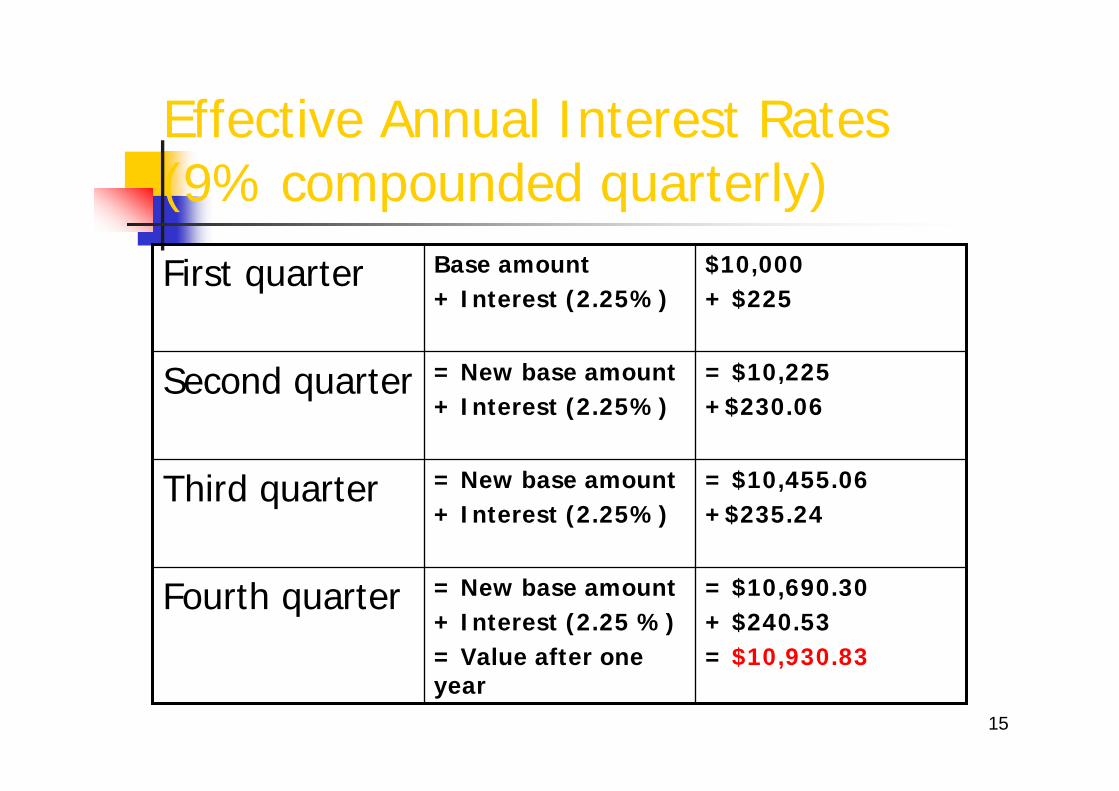

Effective Annual Interest Rates (9% compounded quarterly)

= $10,690.30+ $240.53= $10,930.83

= New base amount+ Interest (2.25 %)= Value after one year

Fourth quarter

= $10,455.06+$235.24

= New base amount+ Interest (2.25%)

Third quarter

= $10,225+$230.06

= New base amount+ Interest (2.25%)

Second quarter

$10,000+ $225

Base amount+ Interest (2.25%)

First quarter

16

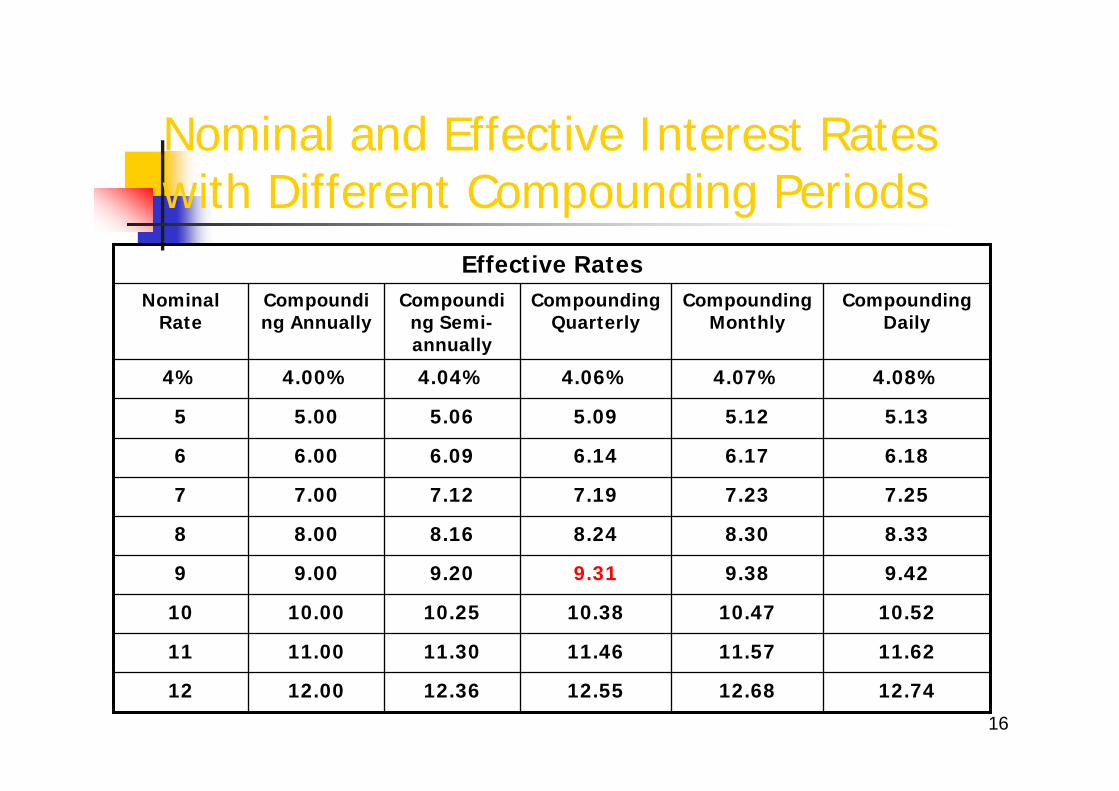

Nominal and Effective Interest Rates with Different Compounding Periods

12.7412.6812.5512.3612.0012

11.6211.5711.4611.3011.0011

10.5210.4710.3810.2510.0010

9.429.389.319.209.009

8.338.308.248.168.008

7.257.237.197.127.007

6.186.176.146.096.006

5.135.125.095.065.005

4.08%4.07%4.06%4.04%4.00%4%

Compounding Daily

Compounding Monthly

Compounding Quarterly

Compounding Semi-annually

Compounding Annually

Nominal Rate

Effective Rates

17

Effective Interest Rate per Payment Period (i)

C = number of interest periods per payment period

K = number of payment periods per yearM = number of interest periods per year

(M=CK)

1]/1[ −+= CCKri

18

12% compounded monthlyPayment Period = QuarterCompounding Period = Month

One-year• Effective interest rate per quarter

• Effective annual interest rate

1% 1% 1%3.030 %

1st Qtr 2nd Qtr 3rd Qtr 4th Qtr

%030.31)01.01( 3 =−+=i

ii

a

a

= + − =

= + − =

( . ) .( . ) .1 0 0 1 1 1 2 6 8 %1 0 0 3 0 3 0 1 1 2 6 8 %

1 2

4

19

Effective Interest Rate per Payment Period with Continuous Compounding

where CK = number of compounding periods per year

continuous compounding => M (=CK) ∞

1]/1[ −+= CCKri

1)(]1)/1lim[(

/1 −=

−+=Kr

C

eCKri

20

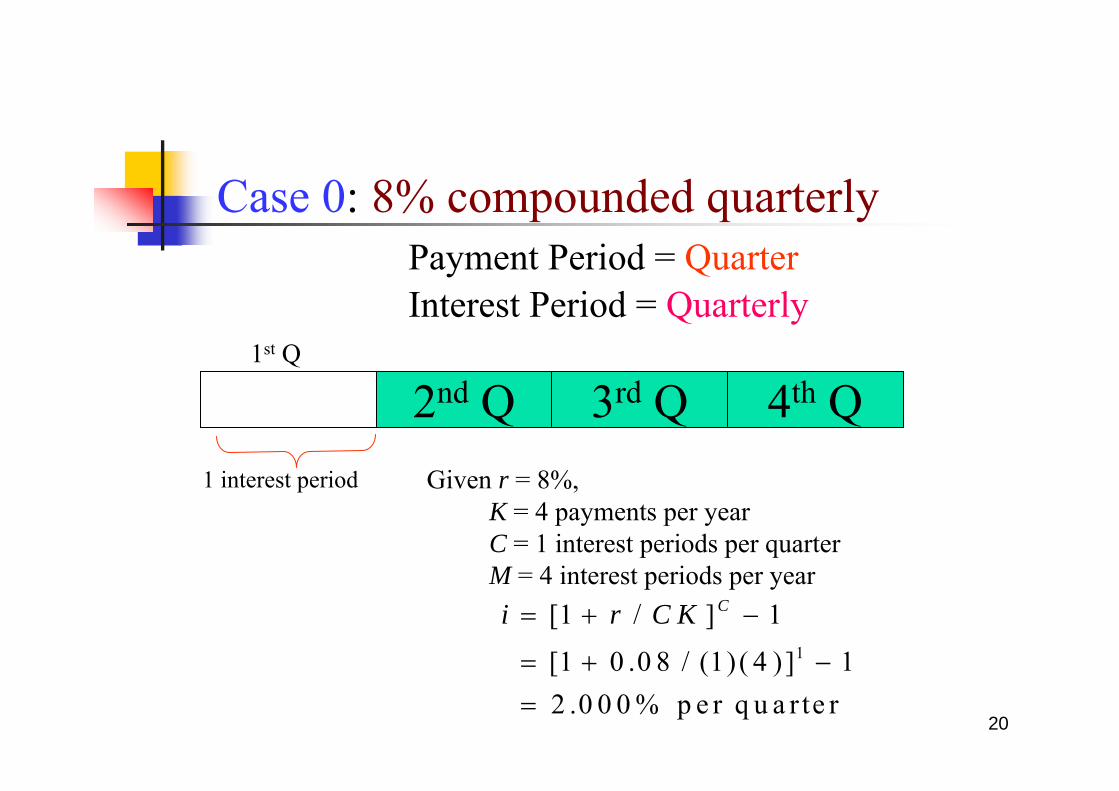

Case 0: 8% compounded quarterlyPayment Period = QuarterInterest Period = Quarterly

1 interest period Given r = 8%,K = 4 payments per yearC = 1 interest periods per quarterM = 4 interest periods per year

2nd Q 3rd Q 4th Q

i r C K C= + −

= + −=

[ / ]

[ . / ( ) ( ) ].

1 1

1 0 0 8 1 4 12 0 0 0 %

1

p e r q u a r te r

1st Q

21

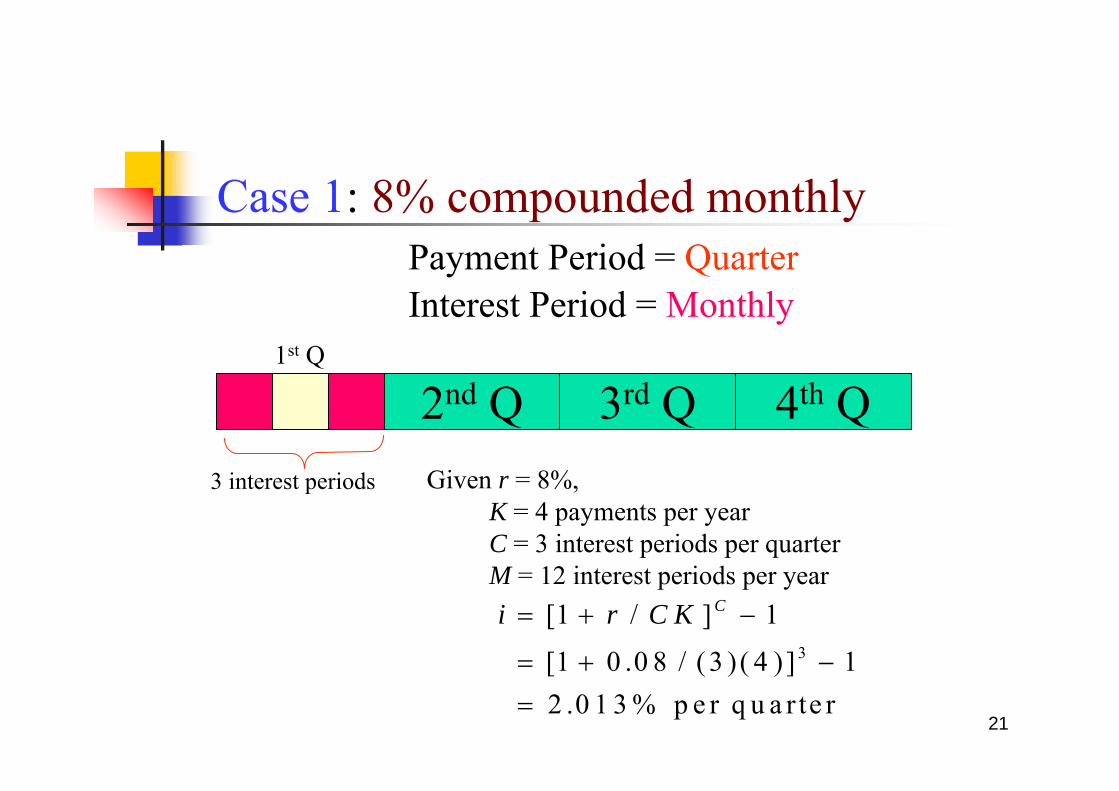

Case 1: 8% compounded monthlyPayment Period = QuarterInterest Period = Monthly

3 interest periods Given r = 8%,K = 4 payments per yearC = 3 interest periods per quarterM = 12 interest periods per year

2nd Q 3rd Q 4th Q

i r C K C= + −

= + −=

[ / ]

[ . / ( ) ( ) ].

1 1

1 0 0 8 3 4 12 0 1 3 %

3

p e r q u a r te r

1st Q

22

Case 2: 8% compounded weeklyPayment Period = QuarterInterest Period = Weekly

13 interest periodsGiven r = 8%,

K = 4 payments per yearC = 13 interest periods per quarterM = 52 interest periods per yeari r C K C= + −

= + −=

[ / ]

[ . / ( )( )].

1 1

1 0 0 8 1 3 4 12 0 1 8 6 %

1 3

p e r q u a rte r

2nd Q 3rd Q 4th Q1st Q

23

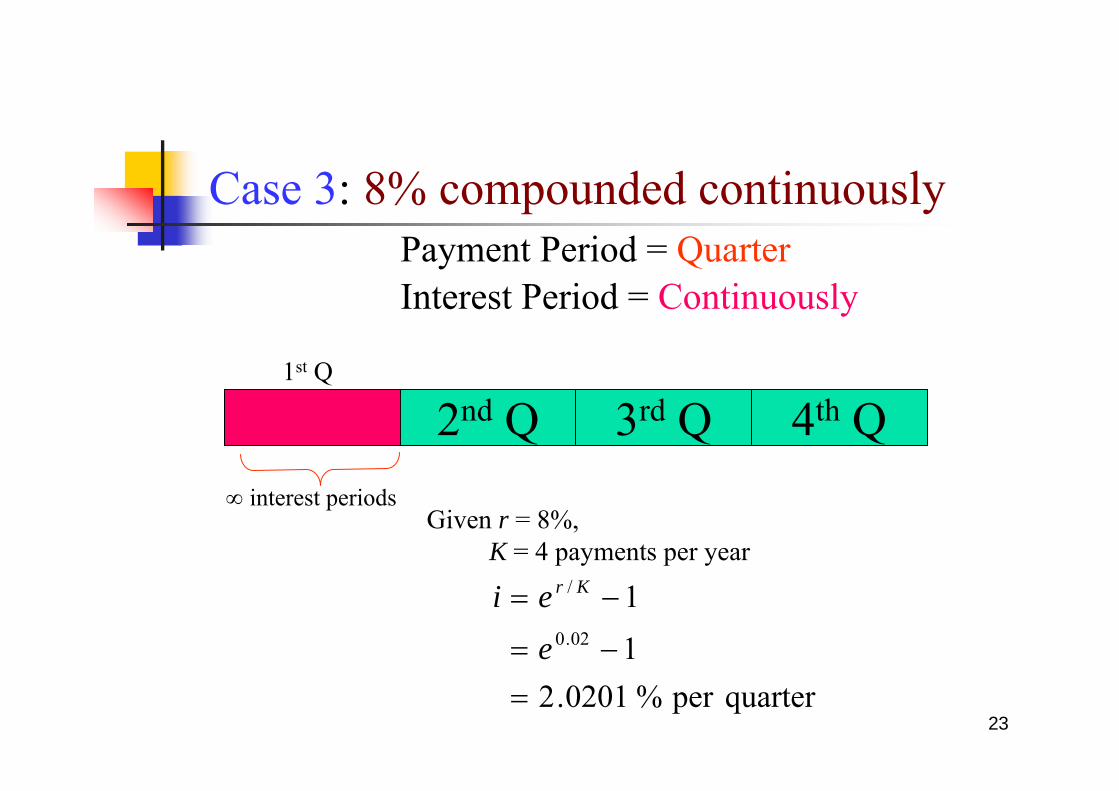

Case 3: 8% compounded continuouslyPayment Period = QuarterInterest Period = Continuously

∞ interest periodsGiven r = 8%,

K = 4 payments per year

2nd Q 3rd Q 4th Q

quarterper %0201.211

02.0

/

=−=

−=

eei Kr

1st Q

24

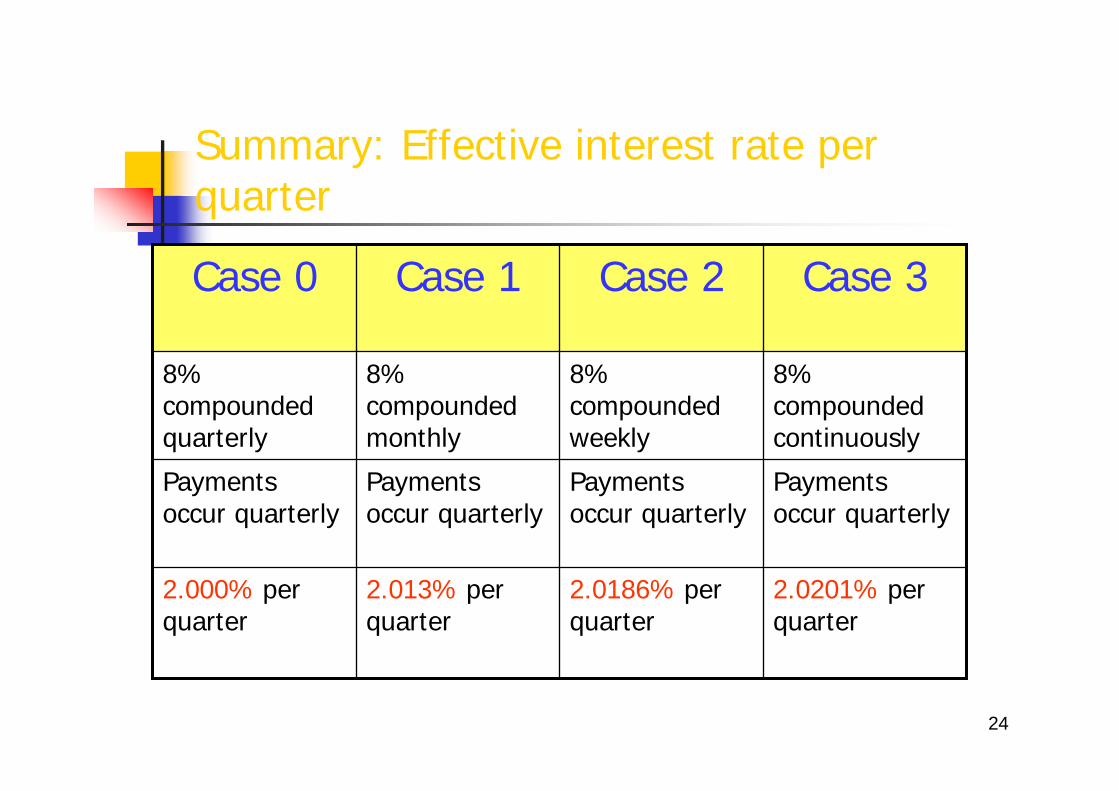

Summary: Effective interest rate per quarter

2.0201% per quarter

2.0186% per quarter

2.013% per quarter

2.000% per quarter

Payments occur quarterly

Payments occur quarterly

Payments occur quarterly

Payments occur quarterly

8% compounded continuously

8% compounded weekly

8% compounded monthly

8% compounded quarterly

Case 3Case 2Case 1Case 0

25

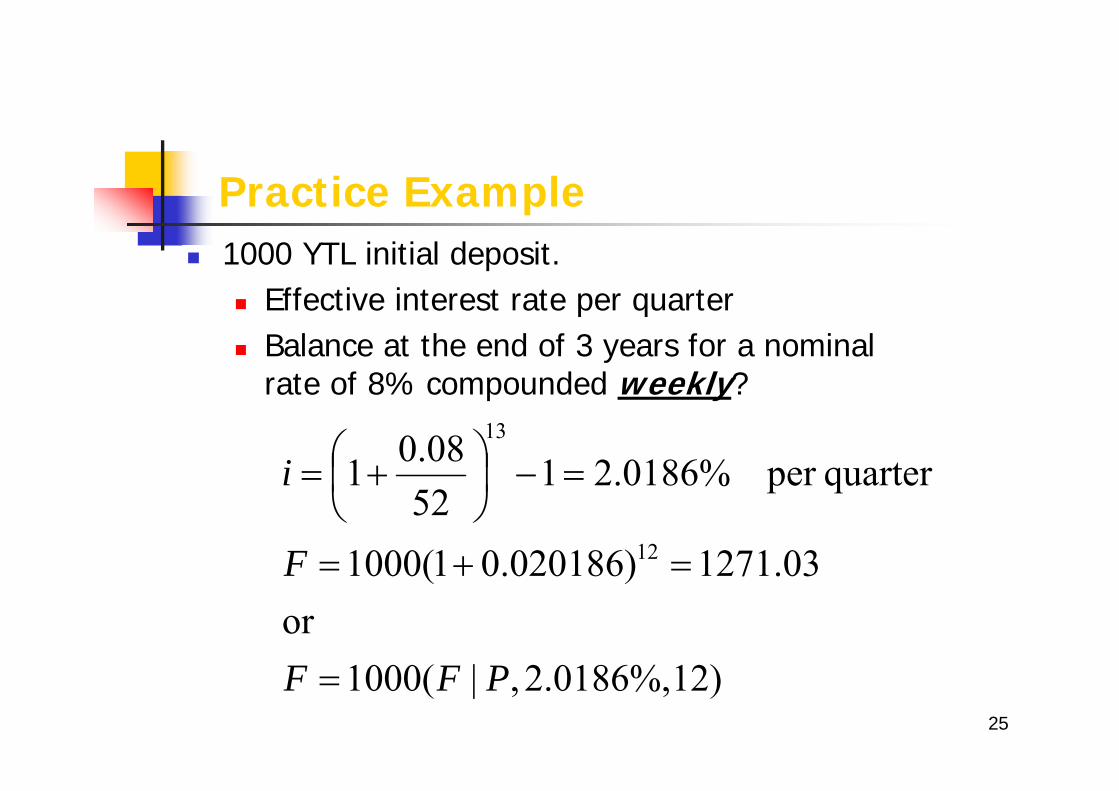

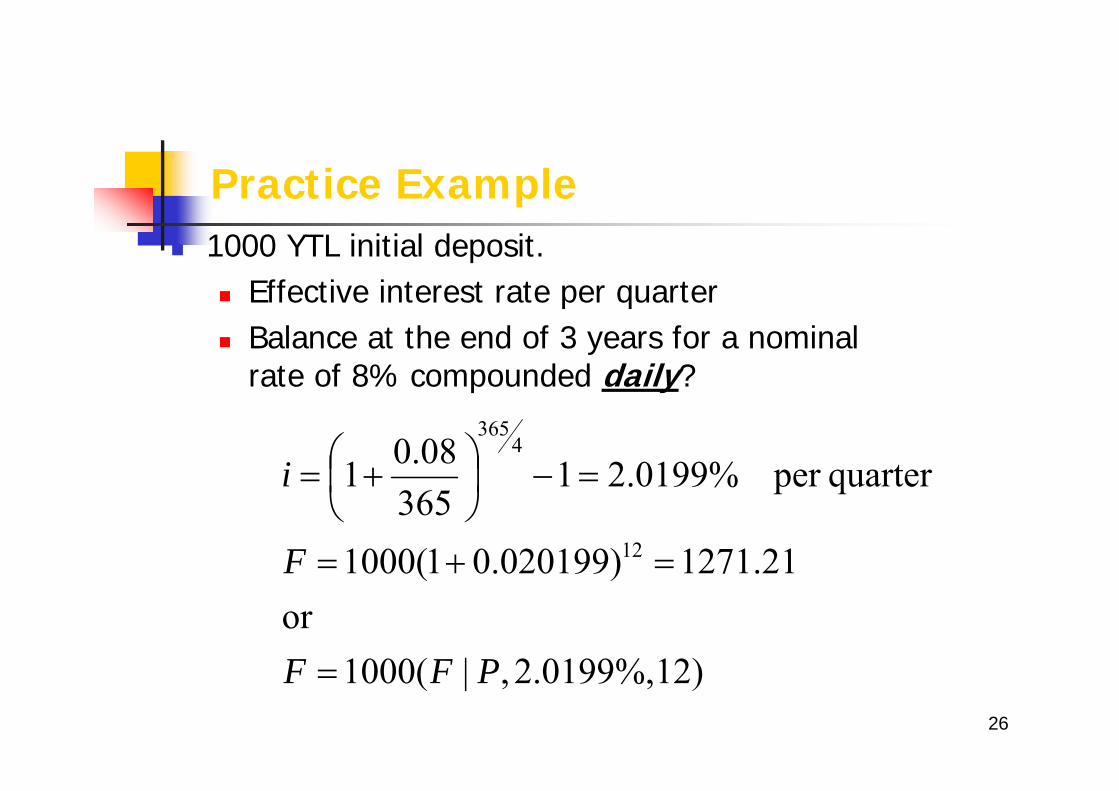

Practice Example1000 YTL initial deposit.

Effective interest rate per quarterBalance at the end of 3 years for a nominal rate of 8% compounded weekly?

)12%,0186.2,|(1000or

03.1271)020186.01(1000

quarterper %0186.215208.01

12

13

PFF

F

i

=

=+=

=−⎟⎠⎞

⎜⎝⎛ +=

26

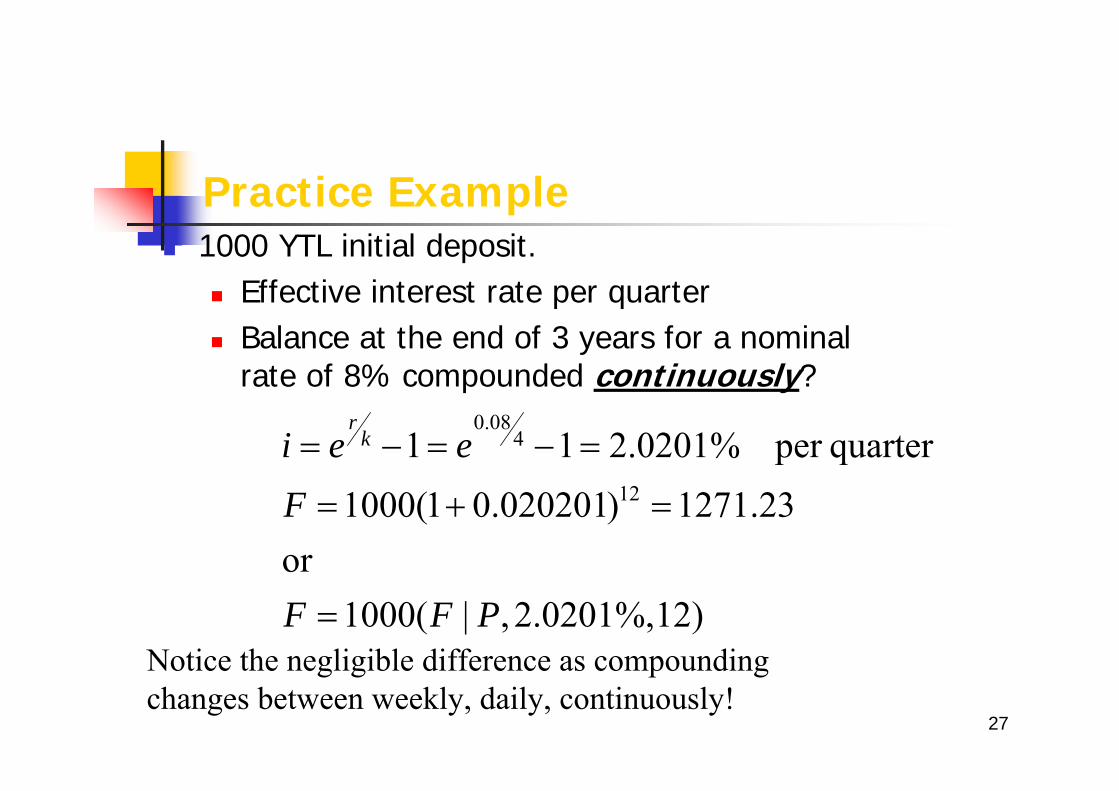

Practice Example1000 YTL initial deposit.

Effective interest rate per quarterBalance at the end of 3 years for a nominal rate of 8% compounded daily?

)12%,0199.2,|(1000or

21.1271)020199.01(1000

quarterper %0199.21365

08.01

12

4365

PFF

F

i

=

=+=

=−⎟⎠⎞

⎜⎝⎛ +=

27

Practice Example1000 YTL initial deposit.

Effective interest rate per quarterBalance at the end of 3 years for a nominal rate of 8% compounded continuously?

)12%,0201.2,|(1000or

23.1271)020201.01(1000quarterper %0201.211

12

408.0

PFF

Feei k

r

=

=+=

=−=−=

Notice the negligible difference as compoundingchanges between weekly, daily, continuously!

28

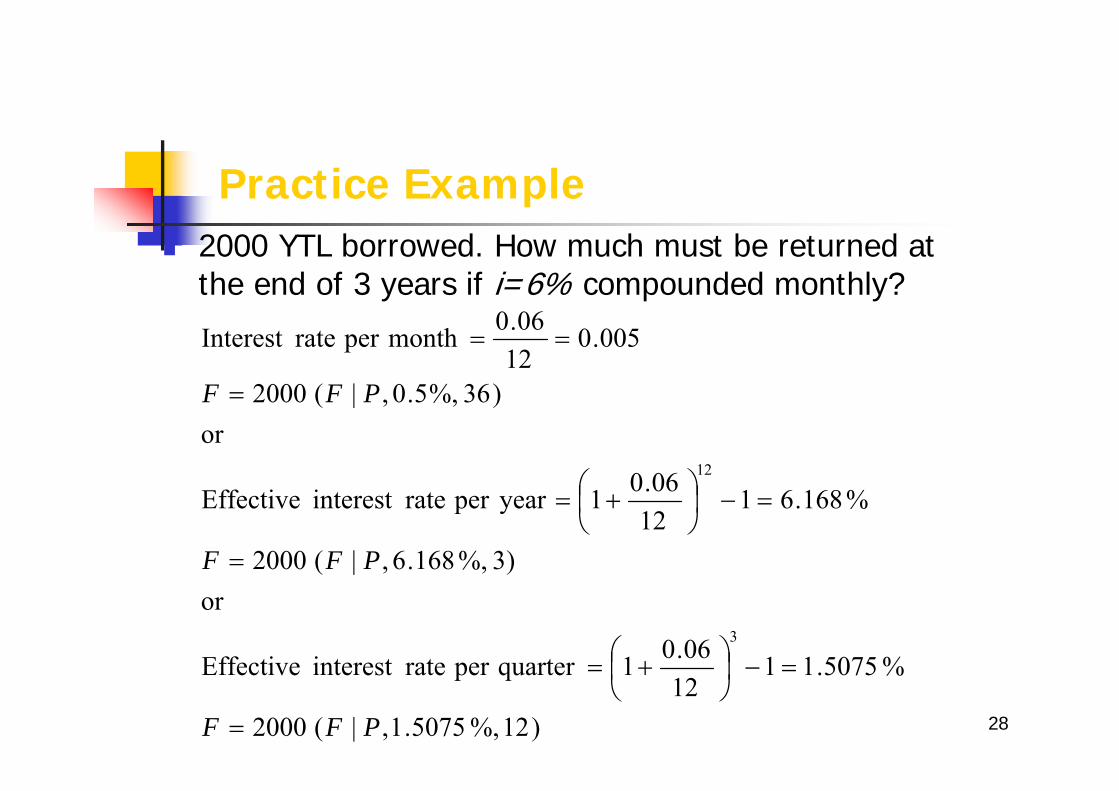

Practice Example2000 YTL borrowed. How much must be returned at the end of 3 years if i=6% compounded monthly?

)12%,5075.1,|(2000

%5075.111206.01quarterper rateinterest Effective

or)3%,168.6,|(2000

%168.611206.01yearper rateinterest Effective

or)36%,5.0,|(2000

005.01206.0monthper rateInterest

3

12

PFF

PFF

PFF

=

=−⎟⎠⎞

⎜⎝⎛ +=

=

=−⎟⎠⎞

⎜⎝⎛ +=

=

==

29

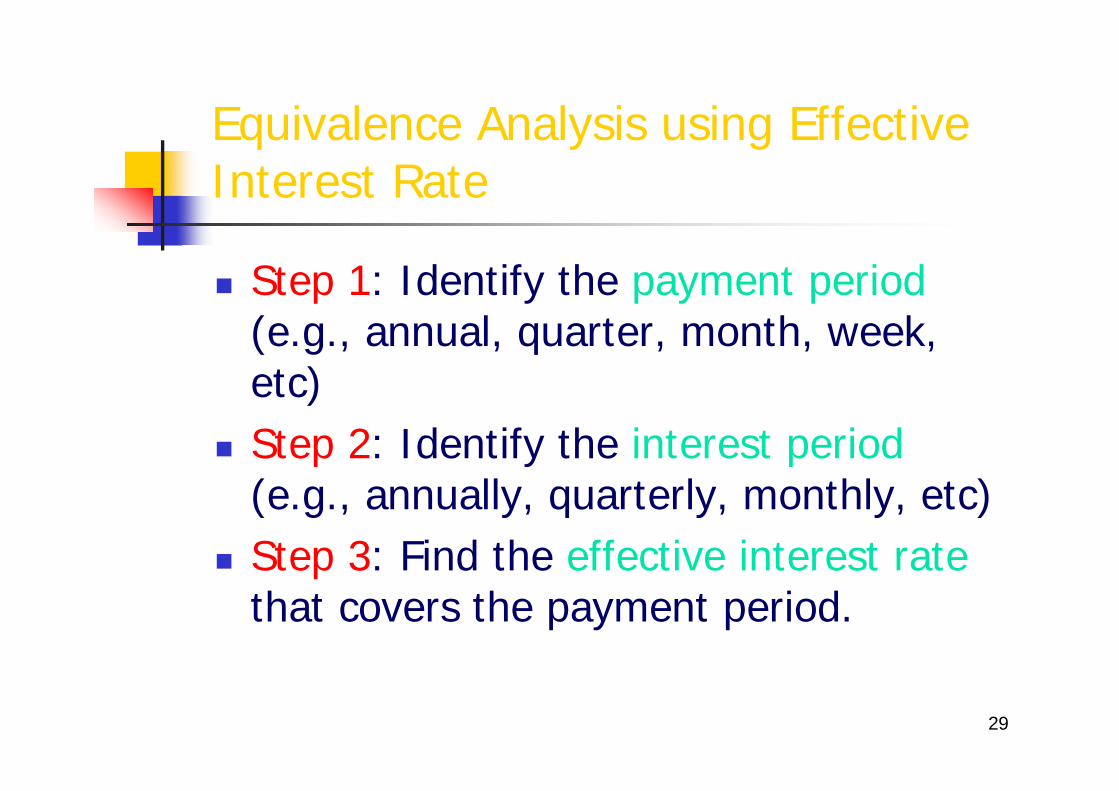

Equivalence Analysis using Effective Interest Rate

Step 1: Identify the payment period(e.g., annual, quarter, month, week, etc)Step 2: Identify the interest period(e.g., annually, quarterly, monthly, etc)Step 3: Find the effective interest ratethat covers the payment period.

30

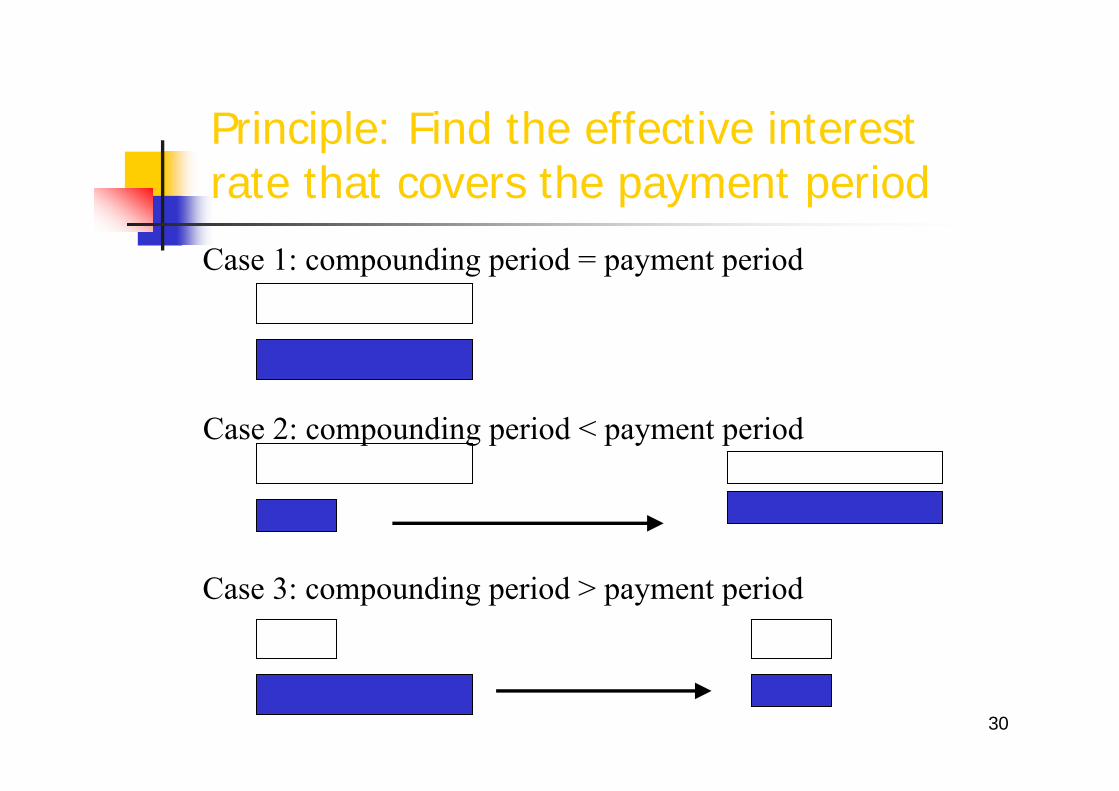

Principle: Find the effective interest rate that covers the payment period

Case 1: compounding period = payment period

Case 2: compounding period < payment period

Case 3: compounding period > payment period

31

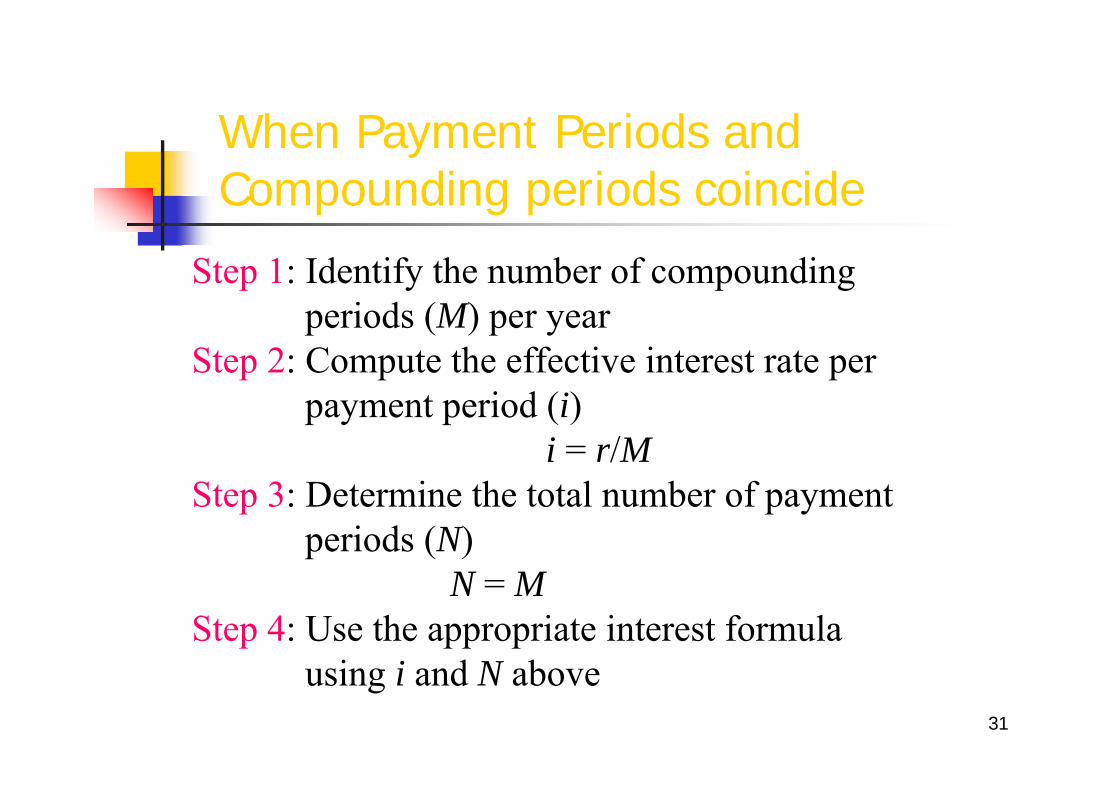

When Payment Periods and Compounding periods coincide

�Step 1: Identify the number of compounding periods (M) per year

�Step 2: Compute the effective interest rate per payment period (i)

i = r/M�Step 3: Determine the total number of payment

periods (N)N = M

�Step 4: Use the appropriate interest formula using i and N above

32

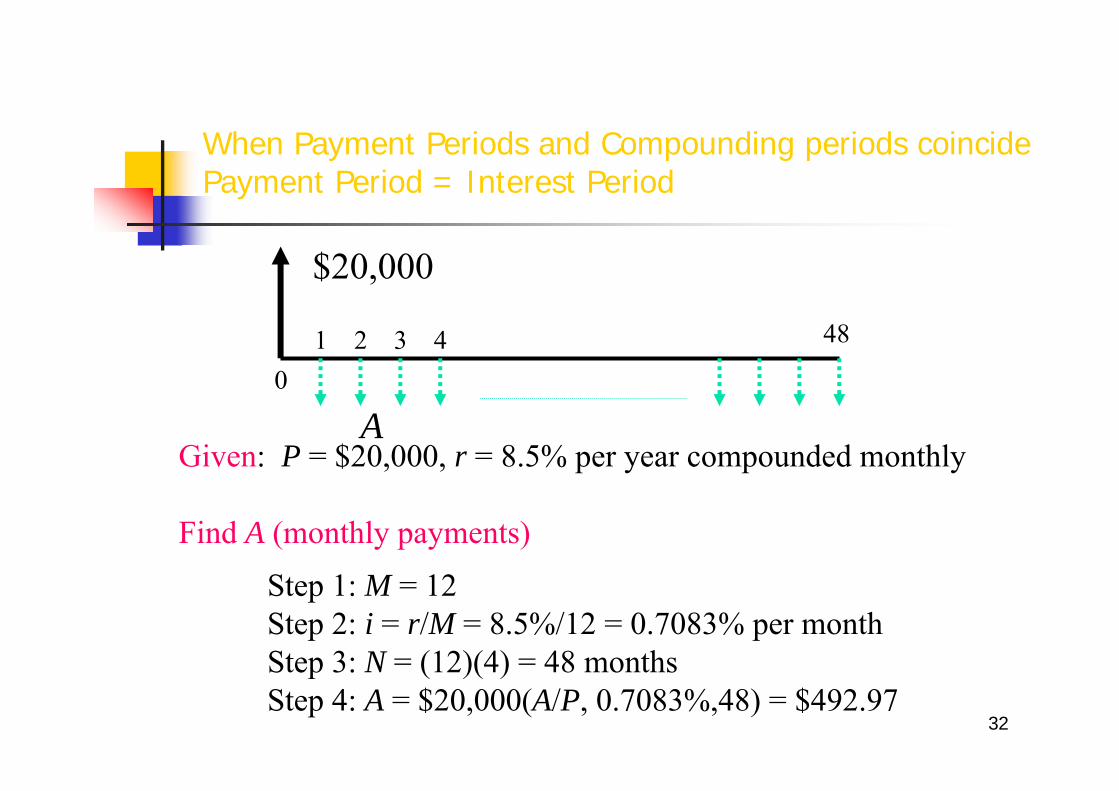

When Payment Periods and Compounding periods coincide Payment Period = Interest Period

Given: P = $20,000, r = 8.5% per year compounded monthly

Find A (monthly payments)

�Step 1: M = 12�Step 2: i = r/M = 8.5%/12 = 0.7083% per month�Step 3: N = (12)(4) = 48 months�Step 4: A = $20,000(A/P, 0.7083%,48) = $492.97

48

01 2 3 4

$20,000

A

33

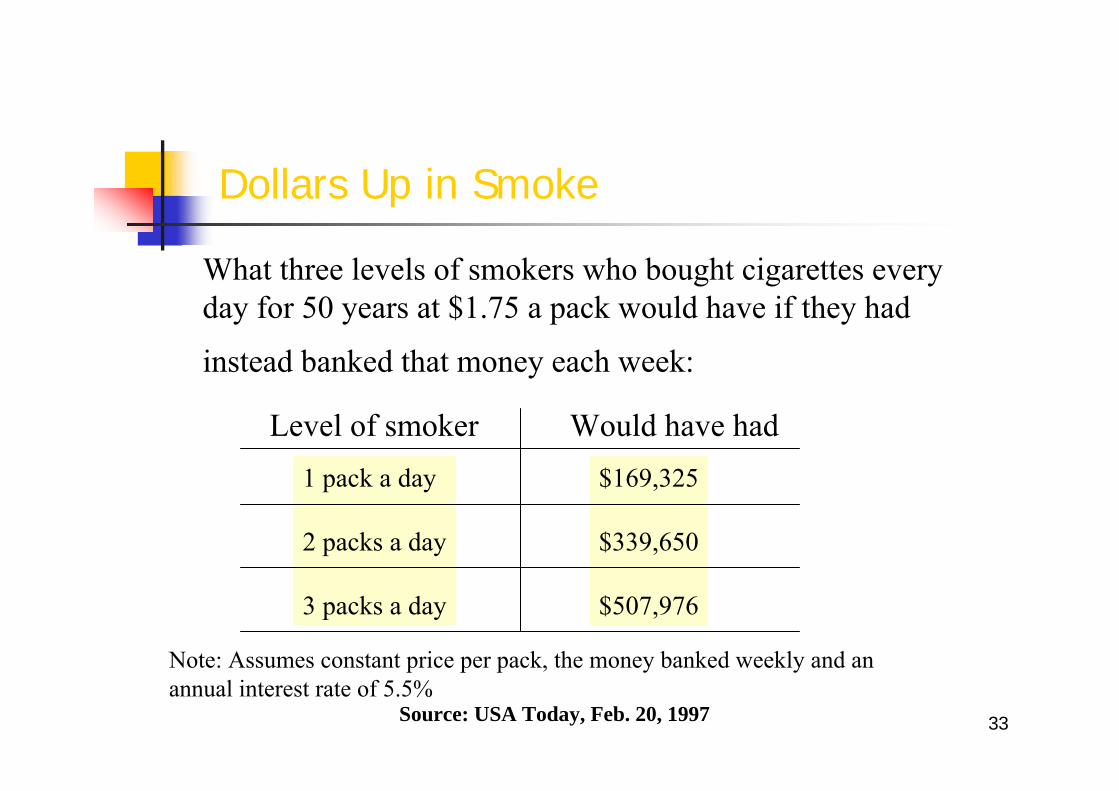

Dollars Up in Smoke

What three levels of smokers who bought cigarettes every day for 50 years at $1.75 a pack would have if they had

instead banked that money each week:

Level of smoker Would have had1 pack a day

2 packs a day

3 packs a day

$169,325

$339,650

$507,976

Note: Assumes constant price per pack, the money banked weekly and an annual interest rate of 5.5%

Source: USA Today, Feb. 20, 1997

34

Sample Calculation: One Pack per Day

Step 1: Determine the effective interest rate per payment period.

Payment period = weekly“5.5% interest compounded weekly”

i = 5.5%/52 = 0.10577% per week

Step 2: Compute the equivalence value.Weekly deposit amount

A = $1.75 x 7 = $12.25 per week

Total number of deposit periodsN = (52 weeks/yr.)(50 years)

= 2600 weeks

F = $12.25 (F/A, 0.10577%, 2600)= $169,325

35

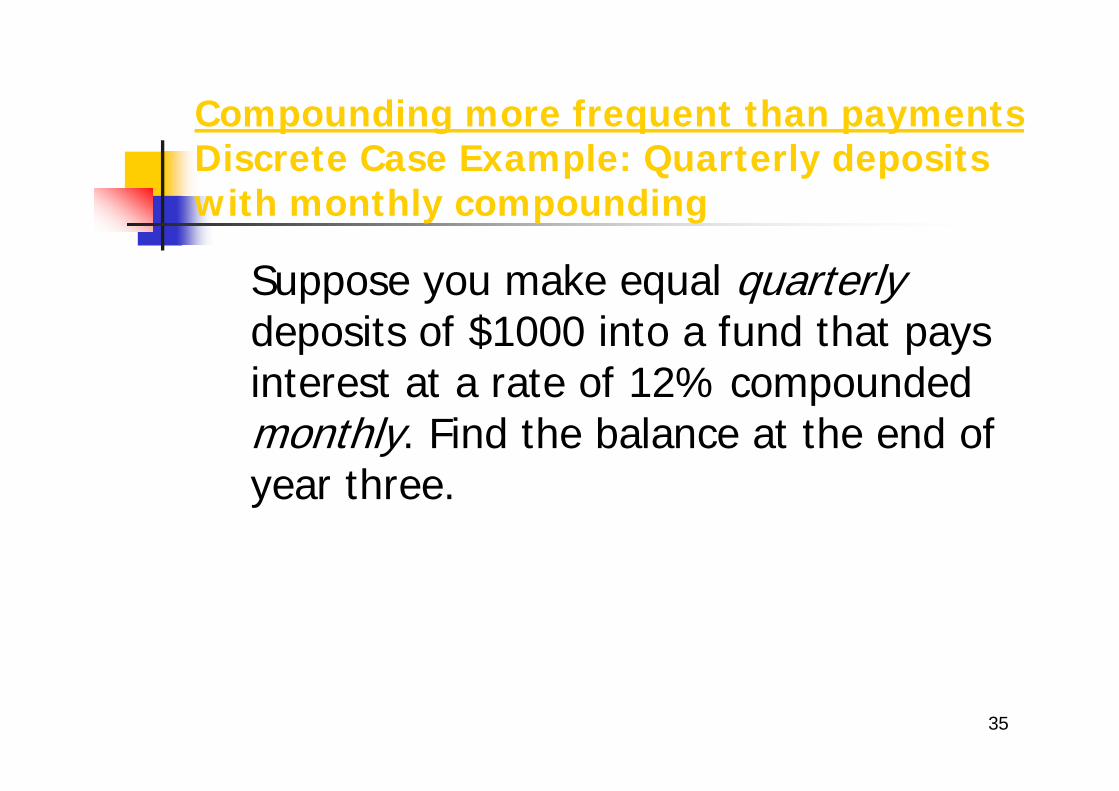

Suppose you make equal quarterlydeposits of $1000 into a fund that paysinterest at a rate of 12% compoundedmonthly. Find the balance at the end of year three.

Compounding more frequent than paymentsDiscrete Case Example: Quarterly deposits with monthly compounding

36

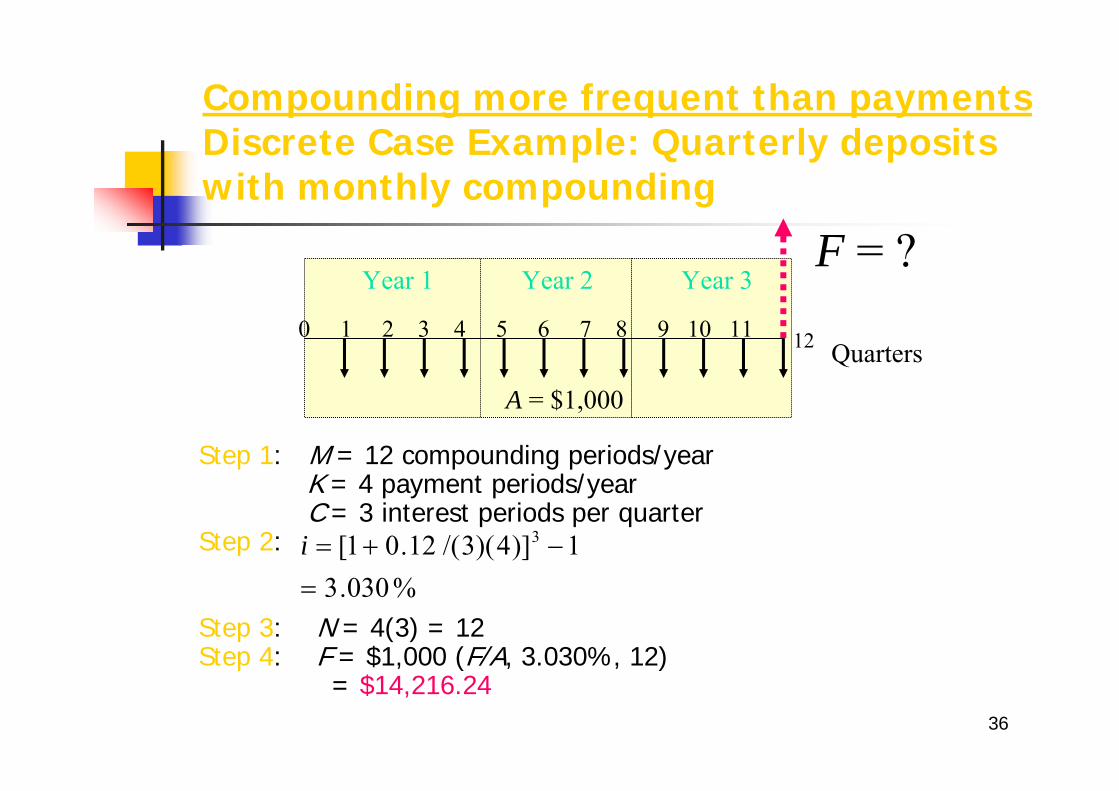

Compounding more frequent than paymentsDiscrete Case Example: Quarterly deposits with monthly compounding

� Step 1: M = 12 compounding periods/year K = 4 payment periods/year C = 3 interest periods per quarter

� Step 2:

� Step 3: N = 4(3) = 12� Step 4: F = $1,000 (F/A, 3.030%, 12)

= $14,216.24

%030.31)]4)(3/(12.01[ 3

=−+=i

F = ?

A = $1,000

0 1 2 3 4 5 6 7 8 9 10 11 12 Quarters

Year 1 Year 2 Year 3

37

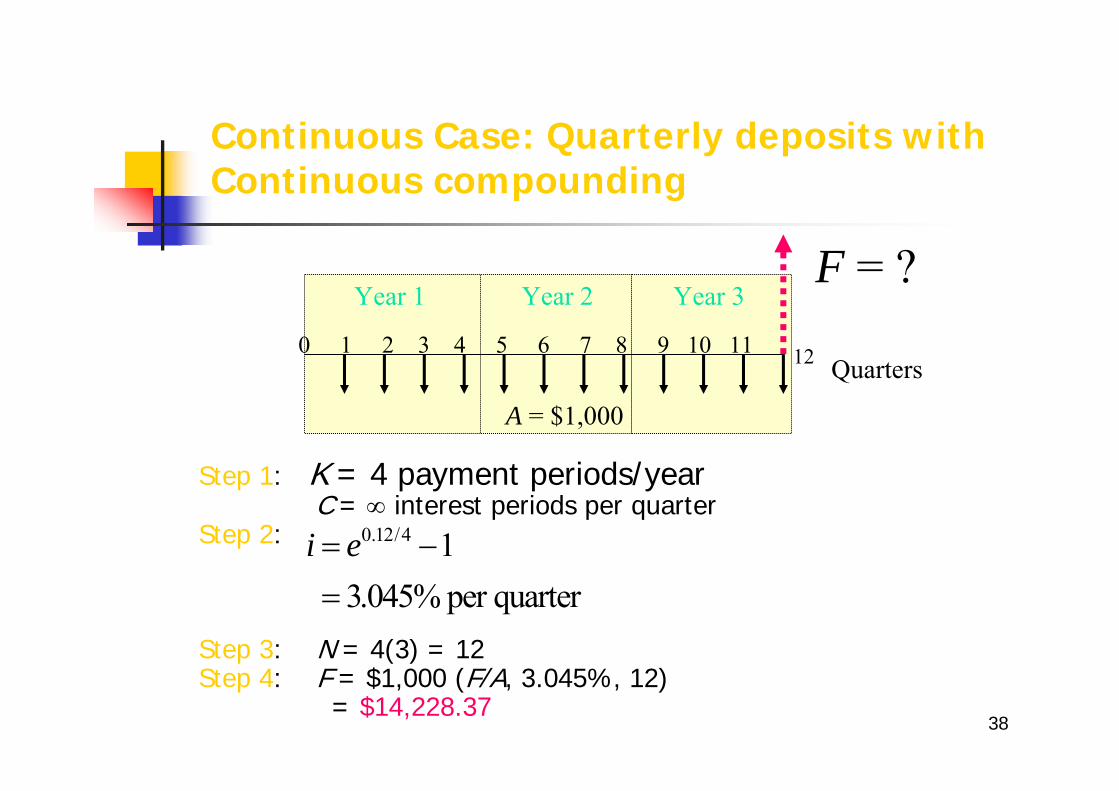

Suppose you make equal quarterlydeposits of $1000 into a fund that paysinterest at a rate of 12% compoundedcontinuously. Find the balance at theend of year three.

Continuous Case: Quarterly deposits with Continuous compounding

38

Continuous Case: Quarterly deposits with Continuous compounding

� Step 1: K = 4 payment periods/year C = ∞ interest periods per quarter

� Step 2:

� Step 3: N = 4(3) = 12� Step 4: F = $1,000 (F/A, 3.045%, 12)

= $14,228.37

F = ?

A = $1,000

0 1 2 3 4 5 6 7 8 9 10 11 12 Quarters

i e= −=

0 12 4 13045%

. /

. per quarter

Year 2Year 1 Year 3

39

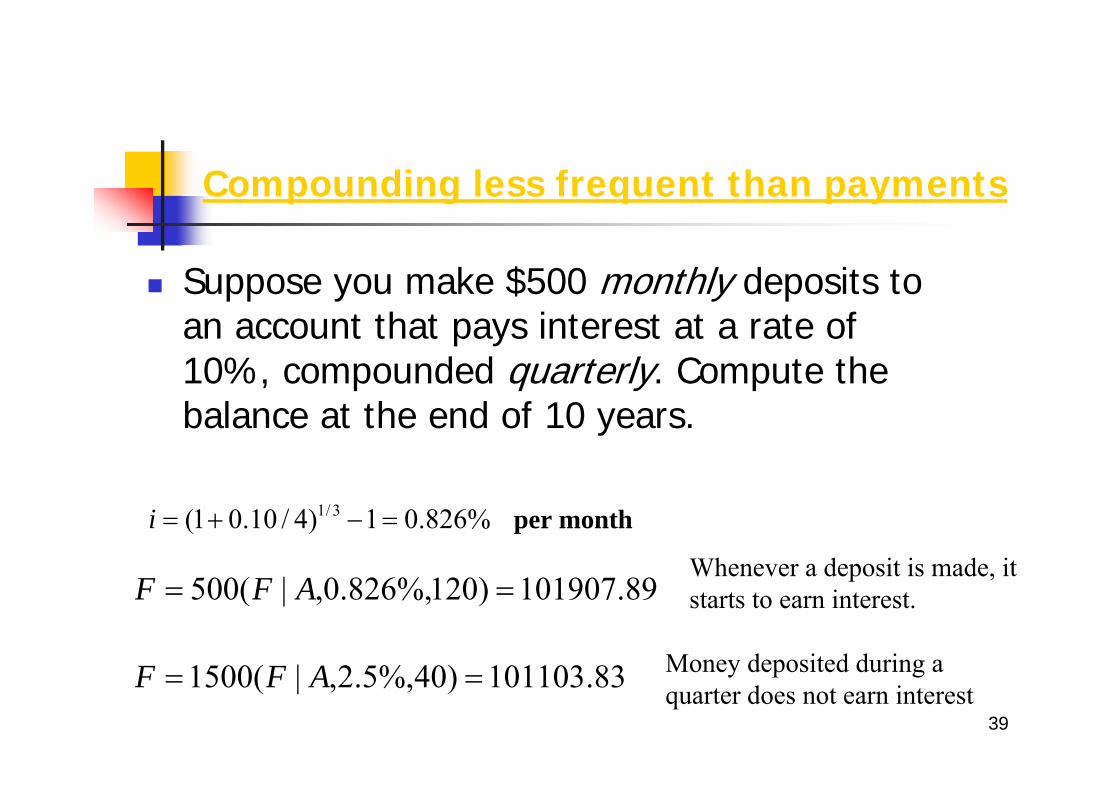

Suppose you make $500 monthly deposits toan account that pays interest at a rate of 10%, compounded quarterly. Compute thebalance at the end of 10 years.

%826.01)4/10.01( 3/1 =−+=i

Compounding less frequent than payments

per month

89.101907)120%,826.0,|(500 == AFF

83.101103)40%,5.2,|(1500 == AFF Money deposited during a quarter does not earn interest

Whenever a deposit is made, it starts to earn interest.

40

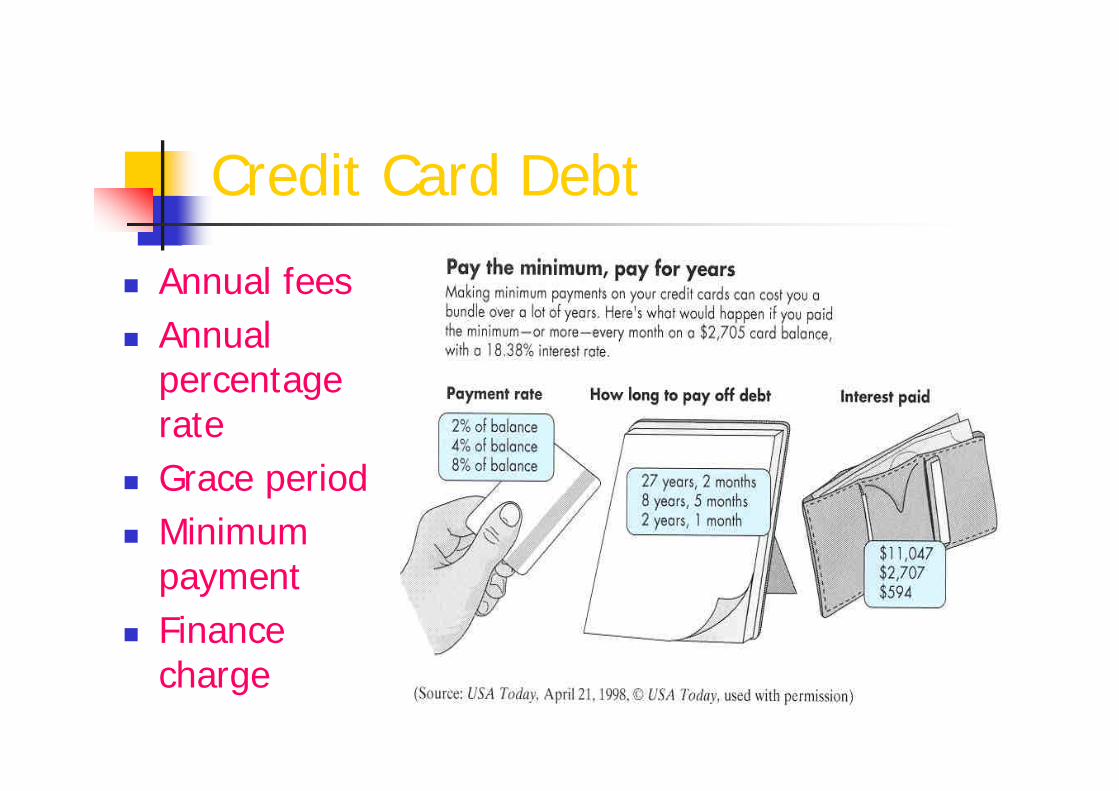

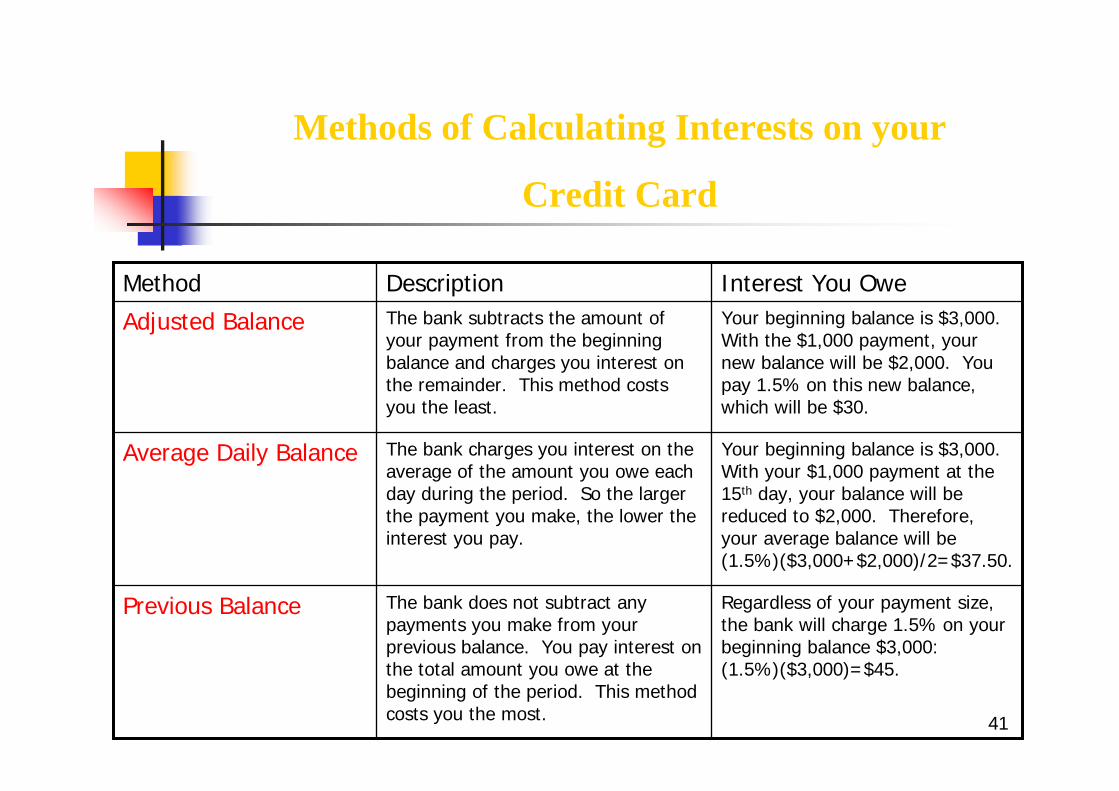

Credit Card Debt

Annual feesAnnual percentage rateGrace periodMinimum paymentFinance charge

41

Regardless of your payment size, the bank will charge 1.5% on your beginning balance $3,000: (1.5%)($3,000)=$45.

The bank does not subtract any payments you make from your previous balance. You pay interest on the total amount you owe at the beginning of the period. This method costs you the most.

Previous Balance

Your beginning balance is $3,000. With your $1,000 payment at the 15th day, your balance will be reduced to $2,000. Therefore, your average balance will be (1.5%)($3,000+$2,000)/2=$37.50.

The bank charges you interest on the average of the amount you owe each day during the period. So the larger the payment you make, the lower the interest you pay.

Average Daily Balance

Your beginning balance is $3,000. With the $1,000 payment, your new balance will be $2,000. You pay 1.5% on this new balance, which will be $30.

The bank subtracts the amount of your payment from the beginning balance and charges you interest on the remainder. This method costs you the least.

Adjusted Balance

Interest You OweDescriptionMethod

Methods of Calculating Interests on your

Credit Card

42

Commercial Loans

�Amortized Loans• Effective interest rate specified• Paid off in installments over time (equal periodic amounts)• What is the cost of borrowing? NOT necessarily the loan

with lowest payments or lowest interest rate. Have to lookat the total cost of borrowing (interest rate and fees, lengthof time it takes you to repay (term))

43

Auto Loan

$20,000

0481 2 2524

Given: APR = 8.5%, N = 48 months, andP = $20,000

Find: AA = $20,000(A/P,8.5%/12,48)

= $492.97

44

Suppose you want to pay off the remaining loan in lump sum right after making the 25th payment. How much would this lump be?

$20,000

0481 2 2524

$492.97$492.97

23 payments that are still outstanding

25 payments that were already made

P = $492.97 (P/A, 0.7083%, 23)= $10,428.96

45

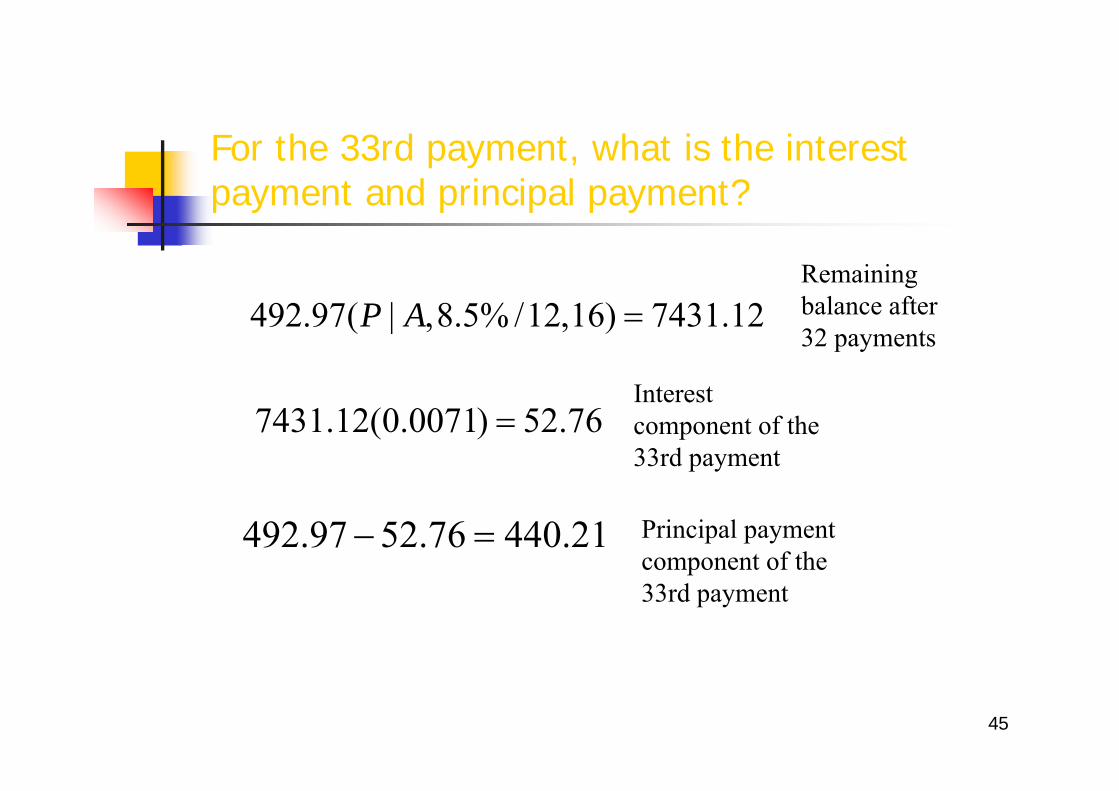

For the 33rd payment, what is the interestpayment and principal payment?

76.52)0071.0(12.7431 =

12.7431)16,12/%5.8,|(97.492 =AP

21.44076.5297.492 =−

Remainingbalance after32 payments

Interestcomponent of the33rd payment

Principal paymentcomponent of the33rd payment

46

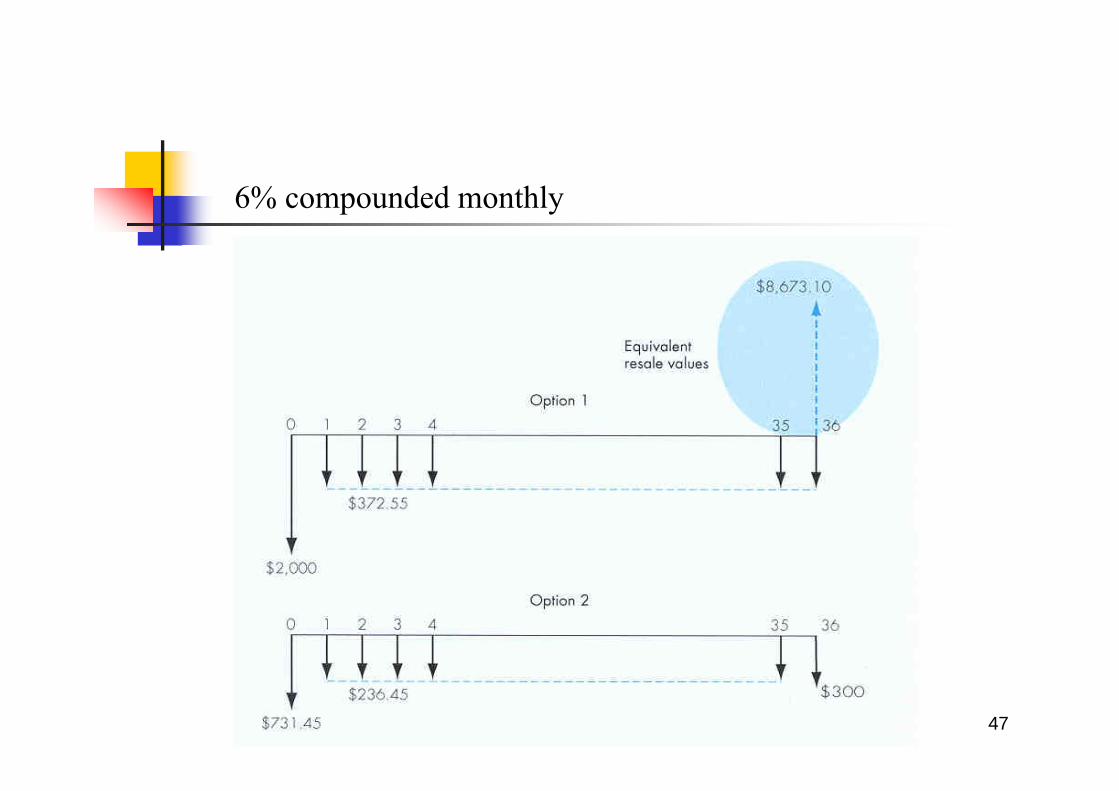

Buying versus Lease Decision

$731.45$2,000Cash due at signing

$8.673.10Purchase option at lease end

$300Cash due at lease end

$495Fees

36 months36 monthsLength

$236.45$372.55Monthly payment

3.6%APR (%)

0$2,000Down payment

$14,695$14,695Price

Option 2Lease Financing

Option 1Debt Financing

47

6% compounded monthly

48

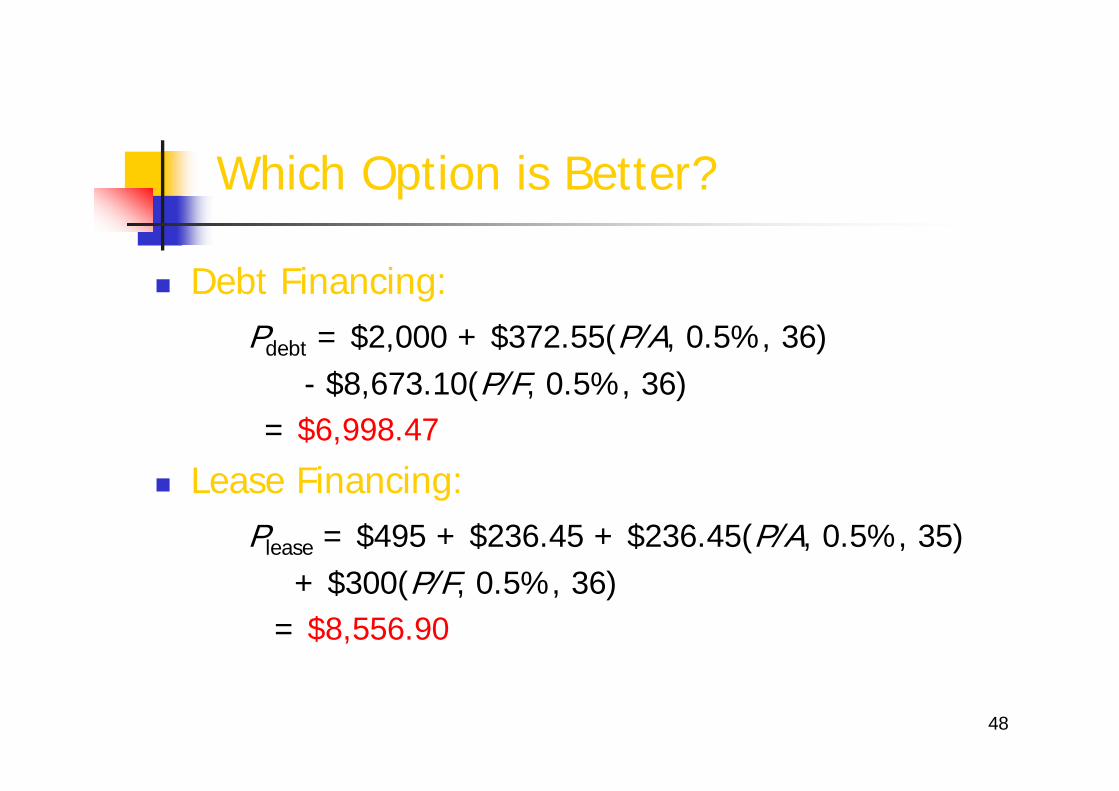

Which Option is Better?

Debt Financing:Pdebt = $2,000 + $372.55(P/A, 0.5%, 36)

- $8,673.10(P/F, 0.5%, 36)= $6,998.47

Lease Financing:Please = $495 + $236.45 + $236.45(P/A, 0.5%, 35)

+ $300(P/F, 0.5%, 36)= $8,556.90

49

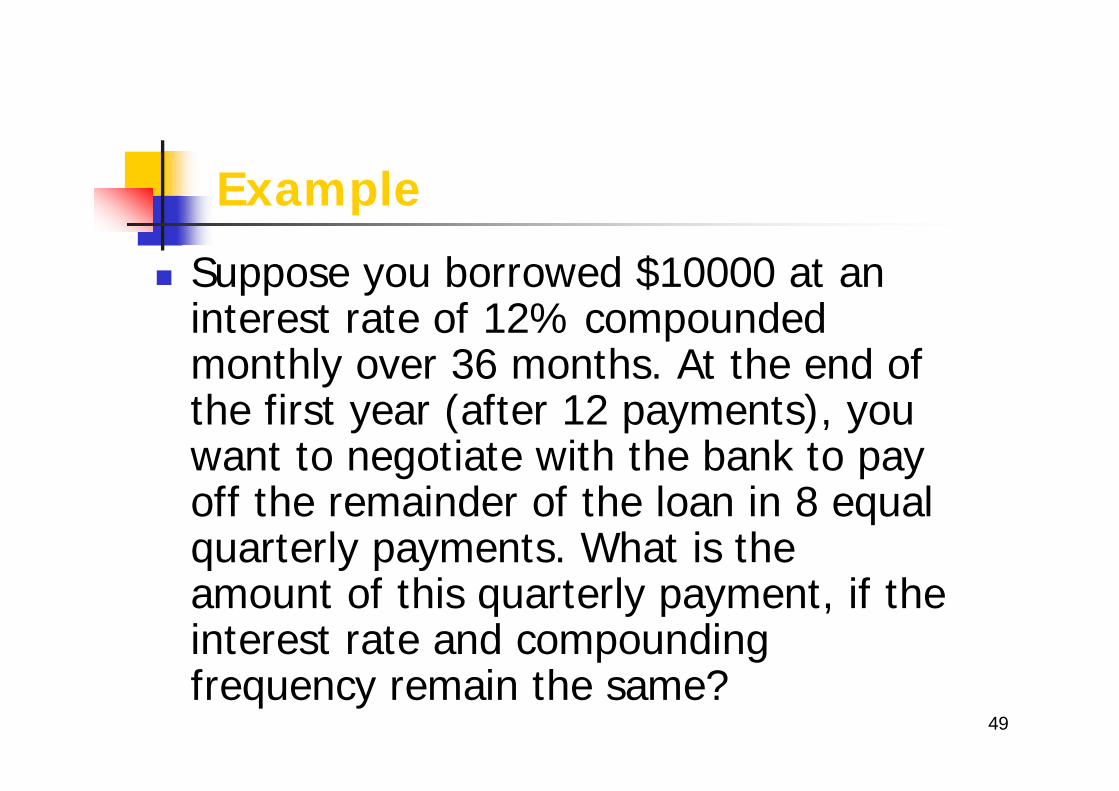

Example

Suppose you borrowed $10000 at an interest rate of 12% compoundedmonthly over 36 months. At the end of the first year (after 12 payments), youwant to negotiate with the bank to pay off the remainder of the loan in 8 equalquarterly payments. What is theamount of this quarterly payment, if theinterest rate and compoundingfrequency remain the same?

50

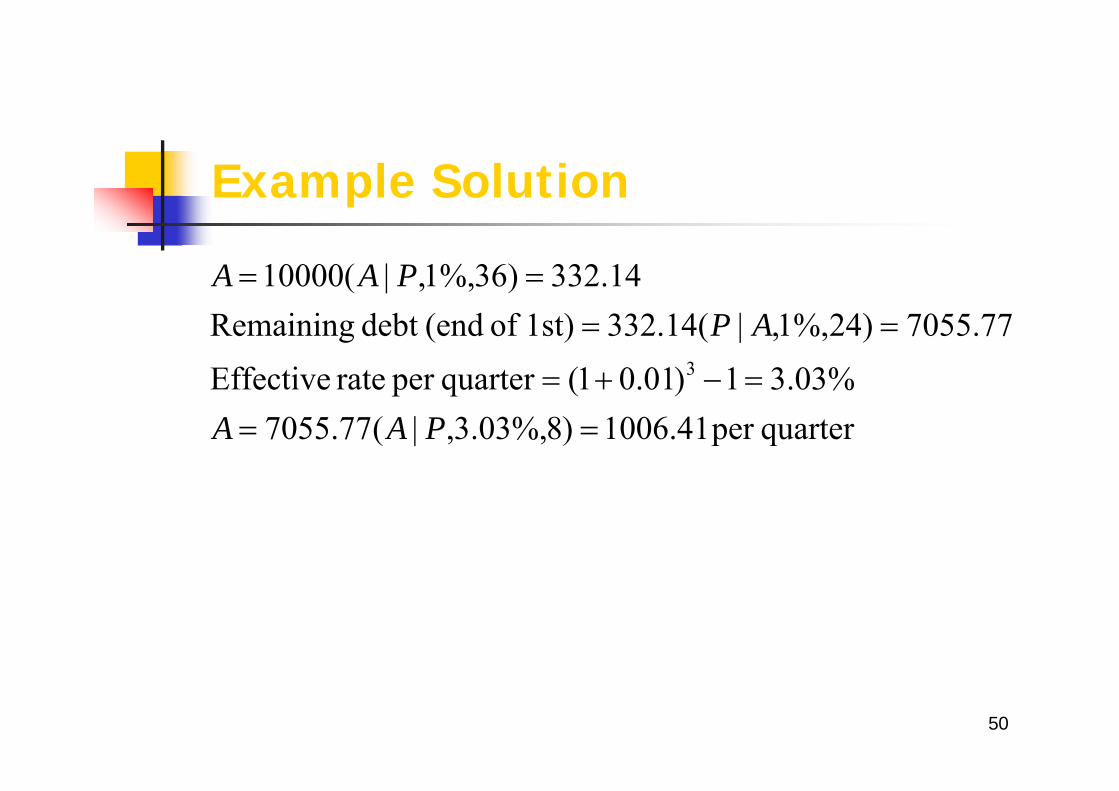

Example Solution

quarterper 41.1006)8%,03.3,|(77.7055%03.31)01.01(quarterper rate Effective

77.7055)24%,1,|(14.3321st) of (enddebt Remaining14.332)36%,1,|(10000

3

===−+=

====

PAA

APPAA

51

Example

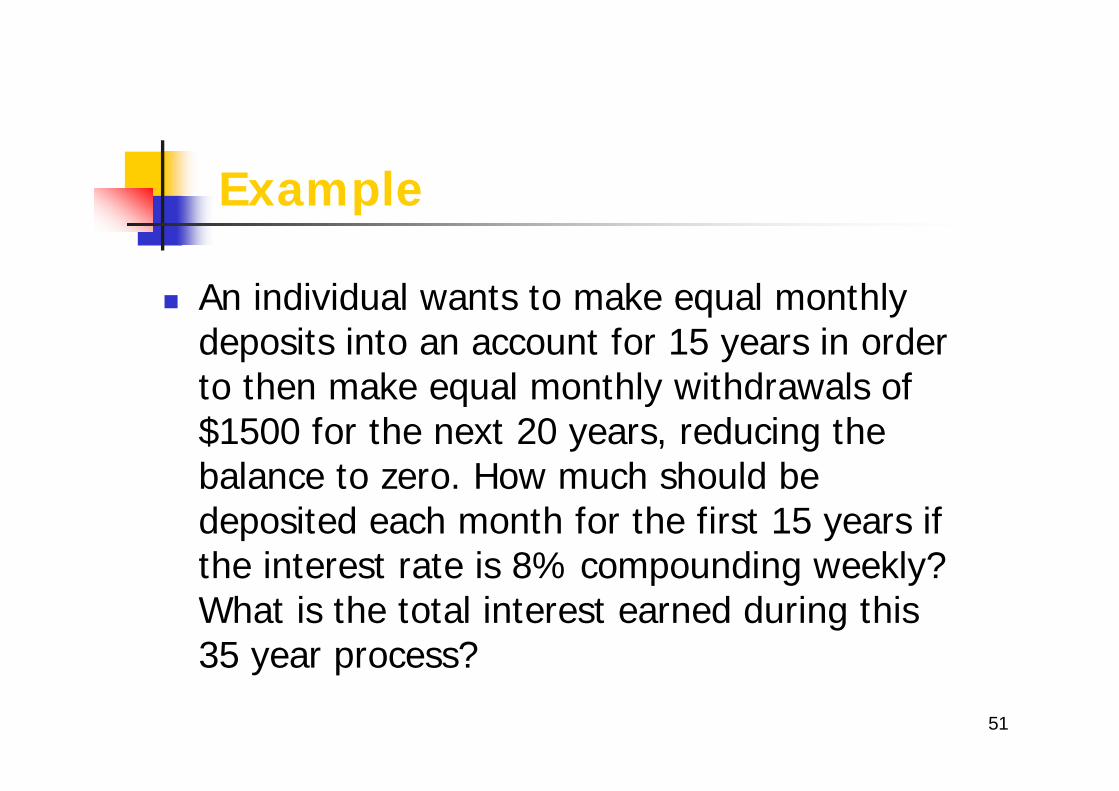

An individual wants to make equal monthlydeposits into an account for 15 years in orderto then make equal monthly withdrawals of $1500 for the next 20 years, reducing thebalance to zero. How much should be deposited each month for the first 15 years ifthe interest rate is 8% compounding weekly? What is the total interest earned during this35 year process?

52

Example

A family has a $30000, 20 year mortgage at 15% compounded monthly.

Find the monthly payment and the total interestpaid.Suppose the family decides to add an extra $100 to its mortgage payment each month starting fromthe first payment of the 6th year. How long will it take the family to pay off the mortgage? Howmuch interest will the family save?

53

Example

A man borrows a loan of $10000 from a bank. Aaccording to theagreement between the bank and the man, the man will pay nothing during the first year and will pay equal amounts of A every month for the next 4 years. If the interest rate is 12% compounded weekly, find

the payment amount AThe interest payment and principal payment for the 20th payment.Suppose you want to pay off the remaining loan in lump sum right after making the 25th payment. How much would this lump be?

54

Example

A man’s current salary is $60000 per year and he is planning toretire 25 years from now. He anticipates that his annual salarywill increase by $3000 each year and he plans to deposit 5% of his yearly salary into a retirement fund that earns 7% interestcompounded daily. What will be the amount accumulated at thetime of his retirement.

55

Example

A series of equal quarterly payments of $1000 extends over a period of 5 years. What is the present worth of this quarterly-payment series at 9.75% interest compounded continuously?

56

Example

A lender requires that monthly mortgage payments be no morethan 25% of gross monthly income, with a maximum term of 30 years. If you can make only a 15% down payment, what is theminimum monthly income needed in order to purchase a $200,000 house when the interest rate is 9% compoundedmonthly?

57

ExampleAlice wanted to purchase a new car for $18,400. A dealer offered her financing through a local bank at an interest rate of 13.5% compounded monthly. The dealer’s financing required a 10% downpayment and 48 equal monthly payments. Because the interest rate is rather high, Alice checked with her credit union for other possiblefinancing options. The loan officer at the credit union quoted her 10.5% interest for a new-car loan and 12.25% for a used-car loan. But to be eligible for the loan, Alice had to have been a member of thecredit union for at least six months. Since she joined the credit uniontwo months ago, she has to wait four more months to apply for theloan. Alice decides to go ahead with the dealer’s financing and 4 months later refinances the balance through the credit union at an interest rate of 12.25%(because the car is no longer new)

a)Compute the monthly payment to the dealerb)Compute the monthly payment to the credit unionc)What is the total interest payment for each loan transaction

58

Example

A loan of $10000 is to be financed over a period of 24 months. The agency quotes a nominal interest rate of 8%for the first 12 months and a nominal interest rate of 9% for any remainingunpaid balance after 12 months, with both rates compoundedmonthly. Based on these rates, what equal end-of-monthpayments for 24 months would be required in order to repaythe loan?

59

ExampleSuppose you are in the market for a new car worth $18000. You areoffered a deal to make a $1800 down payment now and to pay thebalance in equal end-of-month payments of $421.85 over a 48 month period. Consider the following situations:

a) Instead of going through the dealer’s financing, you want to make a down payment of $1800 and take out an auto loan from a bank at 11.75% compounded monthly. What would be your monthlypayments to pay off the loan in 4 years?

b) If you were to accept the dealer’s offer, what would be the effectiverate of interest per month charged by the dealer on your financing?

60

Example

A man borrowed money from a bank to finance a smallfishing boat. The bank’s loan terms allowed him to deferpayments for six months and then to make 36 equal end-of-month payments thereafter. The original bank note was for$4800 with an interest rate of 12% compounded weekly. After 16 monthly payments, David found himself in a financialbind and went to a loan company for assistance in loweringhis monthy payments. Fortunately, the loan company offeredto pay his debts in one lump sum, provided that he pays thecompany $104 per month for the next 36 months. Whatmonthly rate of interest is the loan company charging on thistransaction?