Embed Size (px)

Citation preview

CHAPTER 4 – EMPLOYEE BENEFITS, SHARE-BASED PAYMENTS AND TAXES

247

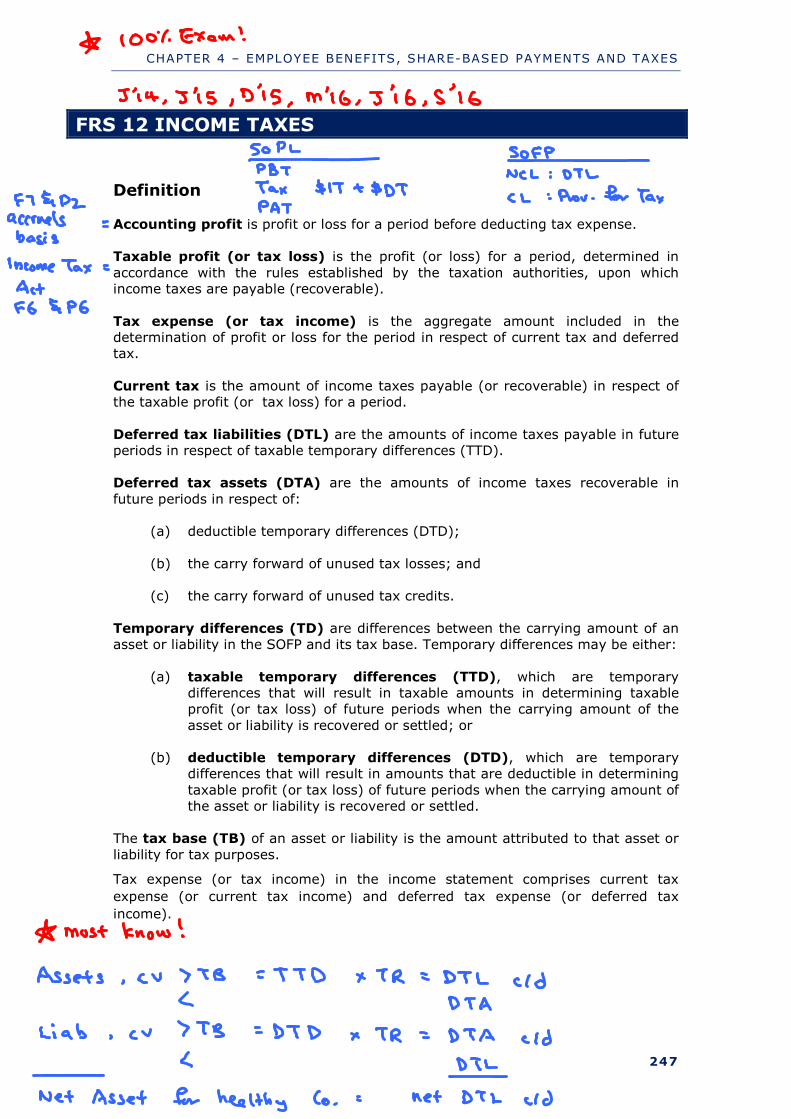

FRS 12 INCOME TAXES

Definition Accounting profit is profit or loss for a period before deducting tax expense. Taxable profit (or tax loss) is the profit (or loss) for a period, determined in

accordance with the rules established by the taxation authorities, upon which income taxes are payable (recoverable).

Tax expense (or tax income) is the aggregate amount included in the determination of profit or loss for the period in respect of current tax and deferred tax.

Current tax is the amount of income taxes payable (or recoverable) in respect of the taxable profit (or tax loss) for a period.

Deferred tax liabilities (DTL) are the amounts of income taxes payable in future periods in respect of taxable temporary differences (TTD). Deferred tax assets (DTA) are the amounts of income taxes recoverable in

future periods in respect of: (a) deductible temporary differences (DTD);

(b) the carry forward of unused tax losses; and (c) the carry forward of unused tax credits.

Temporary differences (TD) are differences between the carrying amount of an asset or liability in the SOFP and its tax base. Temporary differences may be either:

(a) taxable temporary differences (TTD), which are temporary differences that will result in taxable amounts in determining taxable profit (or tax loss) of future periods when the carrying amount of the

asset or liability is recovered or settled; or (b) deductible temporary differences (DTD), which are temporary

differences that will result in amounts that are deductible in determining

taxable profit (or tax loss) of future periods when the carrying amount of the asset or liability is recovered or settled.

The tax base (TB) of an asset or liability is the amount attributed to that asset or

liability for tax purposes.

Tax expense (or tax income) in the income statement comprises current tax

expense (or current tax income) and deferred tax expense (or deferred tax

income).

CHAPTER 4 – EMPLOYEE BENEFITS, SHARE-BASED PAYMENTS AND TAXES

248

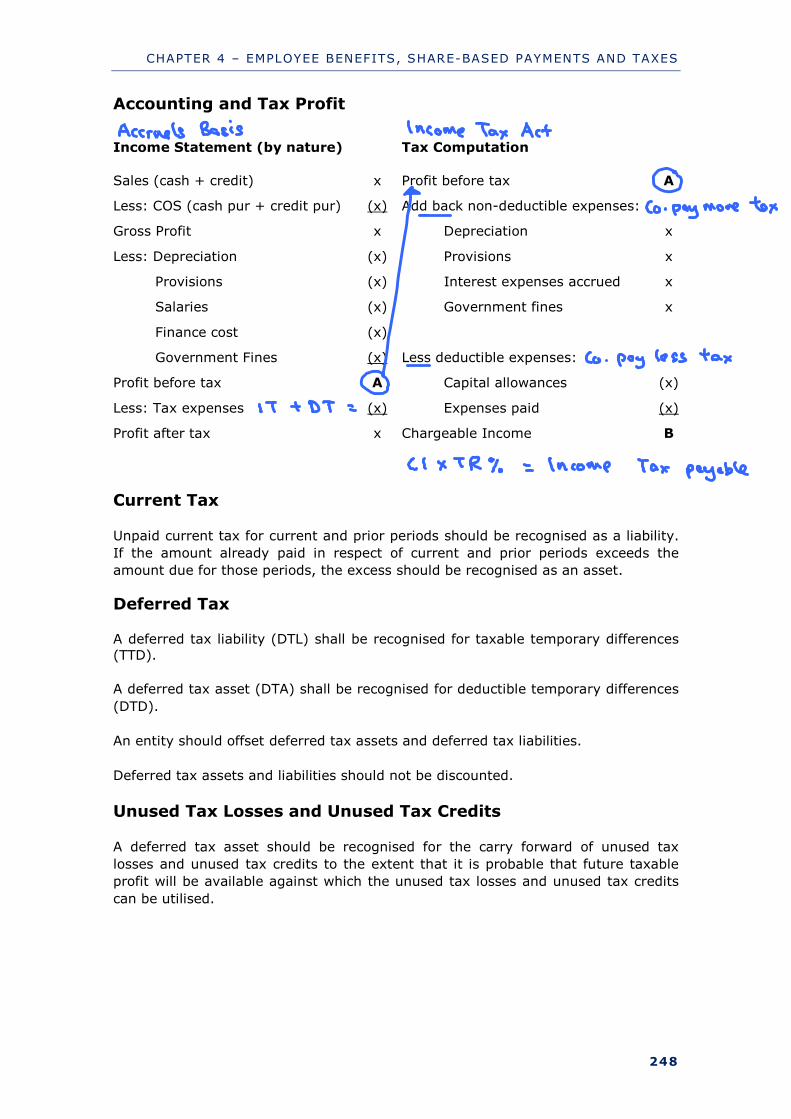

Accounting and Tax Profit

Income Statement (by nature) Tax Computation

Sales (cash + credit)

Less: COS (cash pur + credit pur)

Gross Profit

Less: Depreciation

Provisions

Salaries

Finance cost

Government Fines

Profit before tax

Less: Tax expenses

Profit after tax

x

(x)

x

(x)

(x)

(x)

(x)

(x)

A

(x)

x

Profit before tax

Add back non-deductible expenses:

Depreciation

Provisions

Interest expenses accrued

Government fines

Less deductible expenses:

Capital allowances

Expenses paid

Chargeable Income

A

x

x

x

x

(x)

(x)

B

Current Tax

Unpaid current tax for current and prior periods should be recognised as a liability.

If the amount already paid in respect of current and prior periods exceeds the

amount due for those periods, the excess should be recognised as an asset.

Deferred Tax

A deferred tax liability (DTL) shall be recognised for taxable temporary differences (TTD).

A deferred tax asset (DTA) shall be recognised for deductible temporary differences

(DTD).

An entity should offset deferred tax assets and deferred tax liabilities.

Deferred tax assets and liabilities should not be discounted.

Unused Tax Losses and Unused Tax Credits

A deferred tax asset should be recognised for the carry forward of unused tax

losses and unused tax credits to the extent that it is probable that future taxable

profit will be available against which the unused tax losses and unused tax credits

can be utilised.

CHAPTER 4 – EMPLOYEE BENEFITS, SHARE-BASED PAYMENTS AND TAXES

249

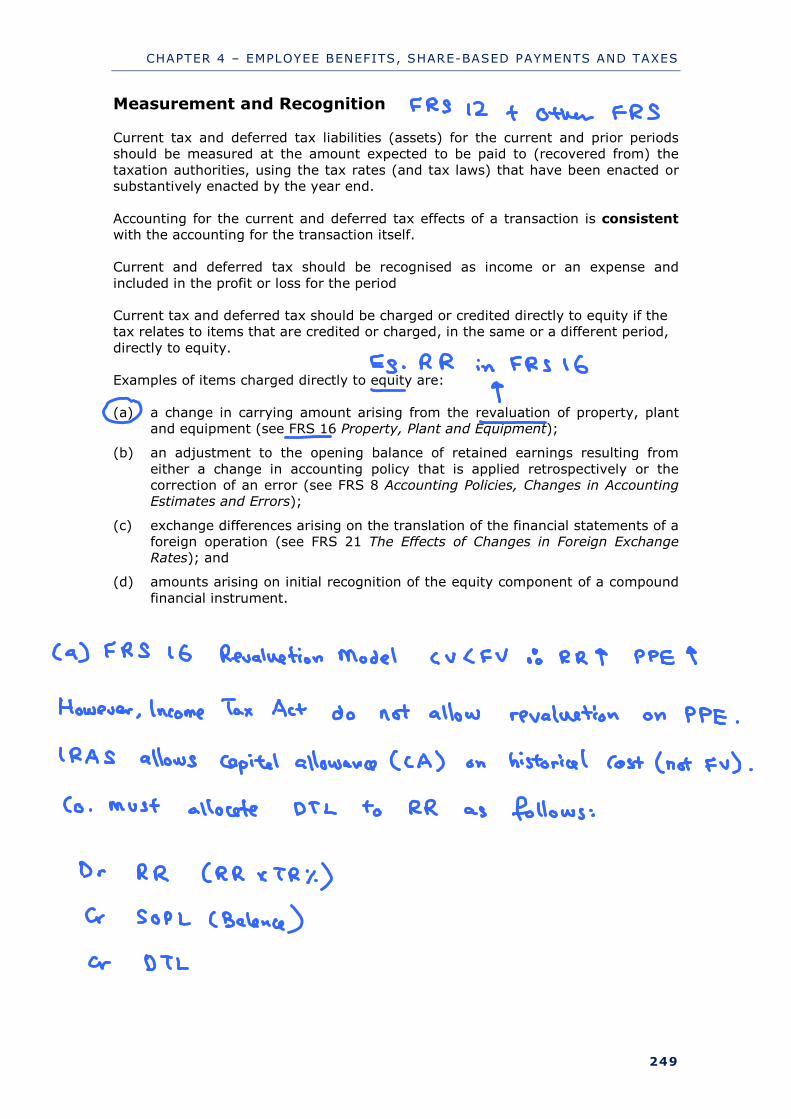

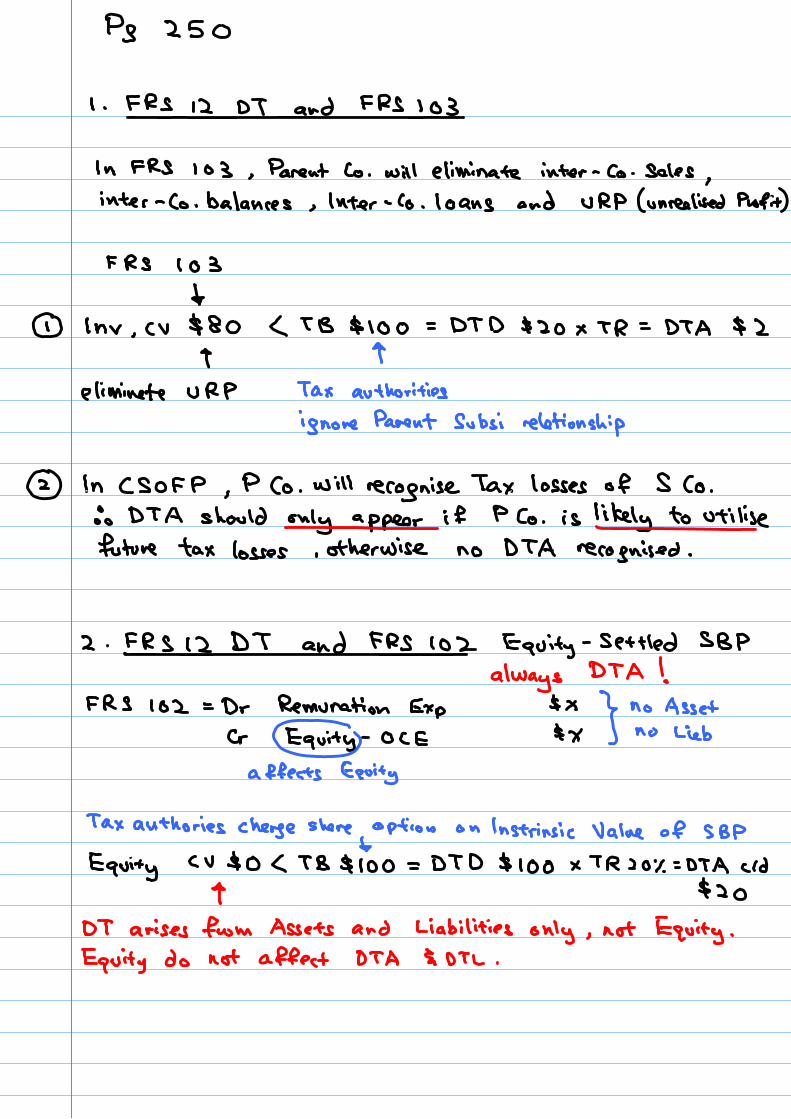

Measurement and Recognition Current tax and deferred tax liabilities (assets) for the current and prior periods should be measured at the amount expected to be paid to (recovered from) the

taxation authorities, using the tax rates (and tax laws) that have been enacted or substantively enacted by the year end.

Accounting for the current and deferred tax effects of a transaction is consistent with the accounting for the transaction itself. Current and deferred tax should be recognised as income or an expense and

included in the profit or loss for the period Current tax and deferred tax should be charged or credited directly to equity if the tax relates to items that are credited or charged, in the same or a different period,

directly to equity. Examples of items charged directly to equity are:

(a) a change in carrying amount arising from the revaluation of property, plant

and equipment (see FRS 16 Property, Plant and Equipment);

(b) an adjustment to the opening balance of retained earnings resulting from

either a change in accounting policy that is applied retrospectively or the correction of an error (see FRS 8 Accounting Policies, Changes in Accounting Estimates and Errors);

(c) exchange differences arising on the translation of the financial statements of a foreign operation (see FRS 21 The Effects of Changes in Foreign Exchange Rates); and

(d) amounts arising on initial recognition of the equity component of a compound

financial instrument.

CHAPTER 4 – EMPLOYEE BENEFITS, SHARE-BASED PAYMENTS AND TAXES

254

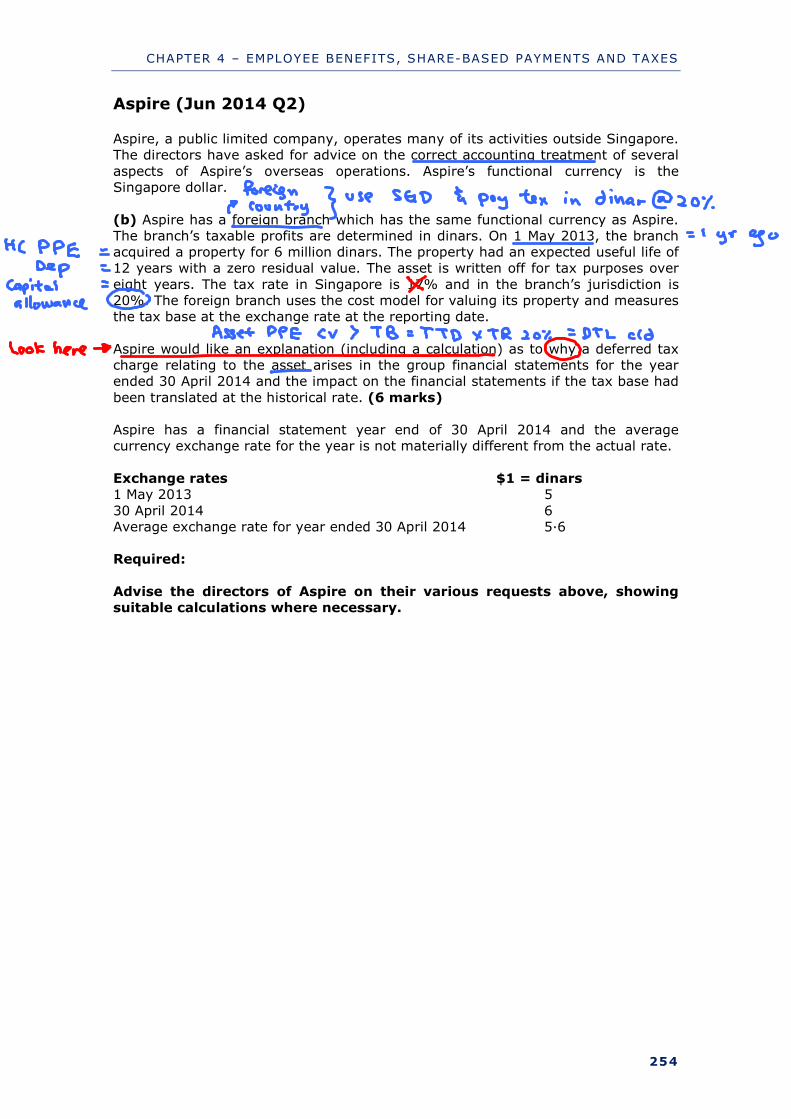

Aspire (Jun 2014 Q2)

Aspire, a public limited company, operates many of its activities outside Singapore. The directors have asked for advice on the correct accounting treatment of several

aspects of Aspire’s overseas operations. Aspire’s functional currency is the Singapore dollar.

(b) Aspire has a foreign branch which has the same functional currency as Aspire. The branch’s taxable profits are determined in dinars. On 1 May 2013, the branch acquired a property for 6 million dinars. The property had an expected useful life of 12 years with a zero residual value. The asset is written off for tax purposes over

eight years. The tax rate in Singapore is 17% and in the branch’s jurisdiction is 20%. The foreign branch uses the cost model for valuing its property and measures the tax base at the exchange rate at the reporting date.

Aspire would like an explanation (including a calculation) as to why a deferred tax charge relating to the asset arises in the group financial statements for the year ended 30 April 2014 and the impact on the financial statements if the tax base had

been translated at the historical rate. (6 marks) Aspire has a financial statement year end of 30 April 2014 and the average currency exchange rate for the year is not materially different from the actual rate.

Exchange rates $1 = dinars 1 May 2013 5

30 April 2014 6 Average exchange rate for year ended 30 April 2014 5·6 Required:

Advise the directors of Aspire on their various requests above, showing suitable calculations where necessary.

CHAPTER 4 – EMPLOYEE BENEFITS, SHARE-BASED PAYMENTS AND TAXES

255

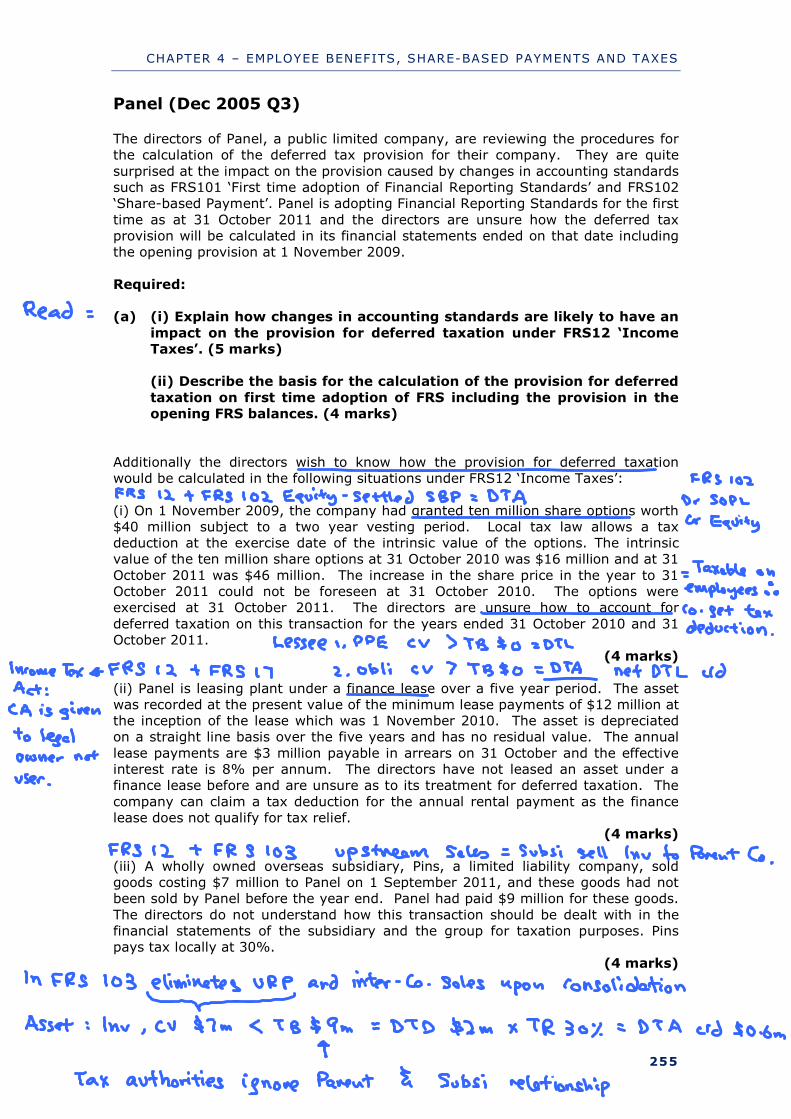

Panel (Dec 2005 Q3)

The directors of Panel, a public limited company, are reviewing the procedures for the calculation of the deferred tax provision for their company. They are quite

surprised at the impact on the provision caused by changes in accounting standards such as FRS101 ‘First time adoption of Financial Reporting Standards’ and FRS102 ‘Share-based Payment’. Panel is adopting Financial Reporting Standards for the first

time as at 31 October 2011 and the directors are unsure how the deferred tax provision will be calculated in its financial statements ended on that date including the opening provision at 1 November 2009.

Required: (a) (i) Explain how changes in accounting standards are likely to have an

impact on the provision for deferred taxation under FRS12 ‘Income Taxes’. (5 marks)

(ii) Describe the basis for the calculation of the provision for deferred

taxation on first time adoption of FRS including the provision in the opening FRS balances. (4 marks)

Additionally the directors wish to know how the provision for deferred taxation would be calculated in the following situations under FRS12 ‘Income Taxes’:

(i) On 1 November 2009, the company had granted ten million share options worth $40 million subject to a two year vesting period. Local tax law allows a tax deduction at the exercise date of the intrinsic value of the options. The intrinsic value of the ten million share options at 31 October 2010 was $16 million and at 31

October 2011 was $46 million. The increase in the share price in the year to 31 October 2011 could not be foreseen at 31 October 2010. The options were exercised at 31 October 2011. The directors are unsure how to account for

deferred taxation on this transaction for the years ended 31 October 2010 and 31 October 2011.

(4 marks)

(ii) Panel is leasing plant under a finance lease over a five year period. The asset was recorded at the present value of the minimum lease payments of $12 million at the inception of the lease which was 1 November 2010. The asset is depreciated on a straight line basis over the five years and has no residual value. The annual

lease payments are $3 million payable in arrears on 31 October and the effective interest rate is 8% per annum. The directors have not leased an asset under a finance lease before and are unsure as to its treatment for deferred taxation. The

company can claim a tax deduction for the annual rental payment as the finance lease does not qualify for tax relief.

(4 marks)

(iii) A wholly owned overseas subsidiary, Pins, a limited liability company, sold goods costing $7 million to Panel on 1 September 2011, and these goods had not been sold by Panel before the year end. Panel had paid $9 million for these goods.

The directors do not understand how this transaction should be dealt with in the financial statements of the subsidiary and the group for taxation purposes. Pins pays tax locally at 30%.

(4 marks)

CHAPTER 4 – EMPLOYEE BENEFITS, SHARE-BASED PAYMENTS AND TAXES

256

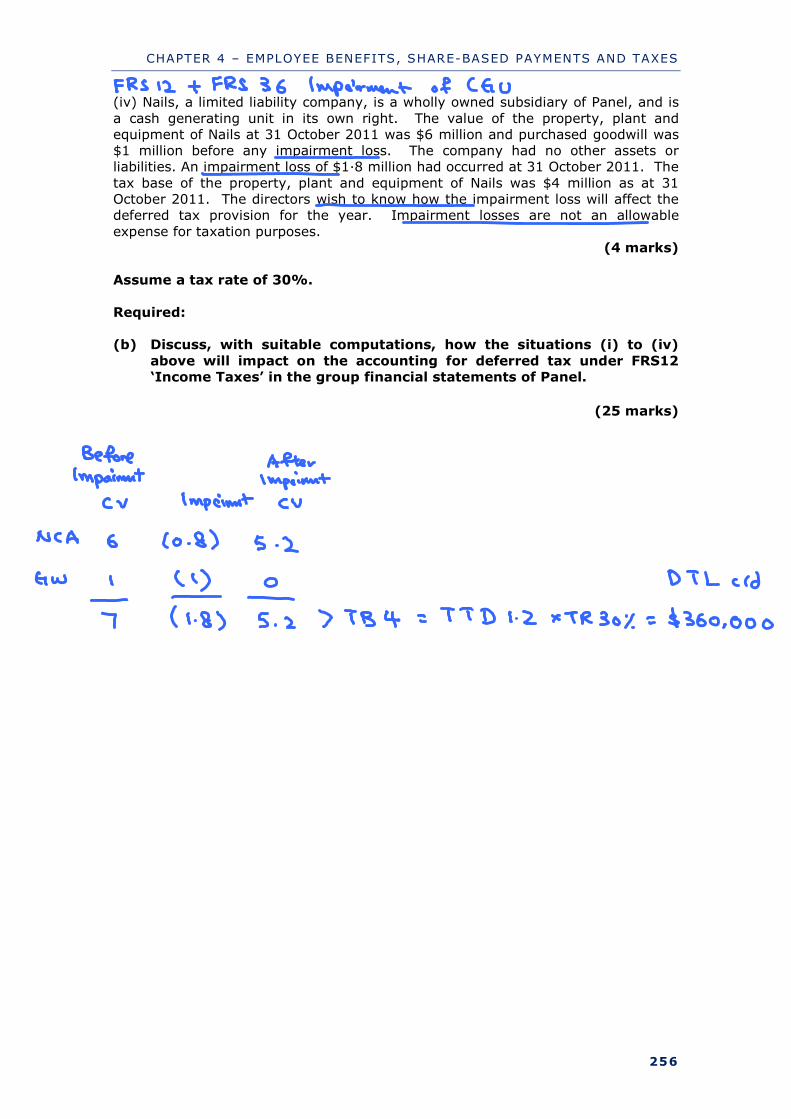

(iv) Nails, a limited liability company, is a wholly owned subsidiary of Panel, and is

a cash generating unit in its own right. The value of the property, plant and equipment of Nails at 31 October 2011 was $6 million and purchased goodwill was $1 million before any impairment loss. The company had no other assets or liabilities. An impairment loss of $1·8 million had occurred at 31 October 2011. The

tax base of the property, plant and equipment of Nails was $4 million as at 31 October 2011. The directors wish to know how the impairment loss will affect the deferred tax provision for the year. Impairment losses are not an allowable

expense for taxation purposes. (4 marks)

Assume a tax rate of 30%.

Required: (b) Discuss, with suitable computations, how the situations (i) to (iv)

above will impact on the accounting for deferred tax under FRS12 ‘Income Taxes’ in the group financial statements of Panel.

(25 marks)

CHAPTER 5 – REVENUE FROM CONTRACTS WITH CUSTOMERS

259

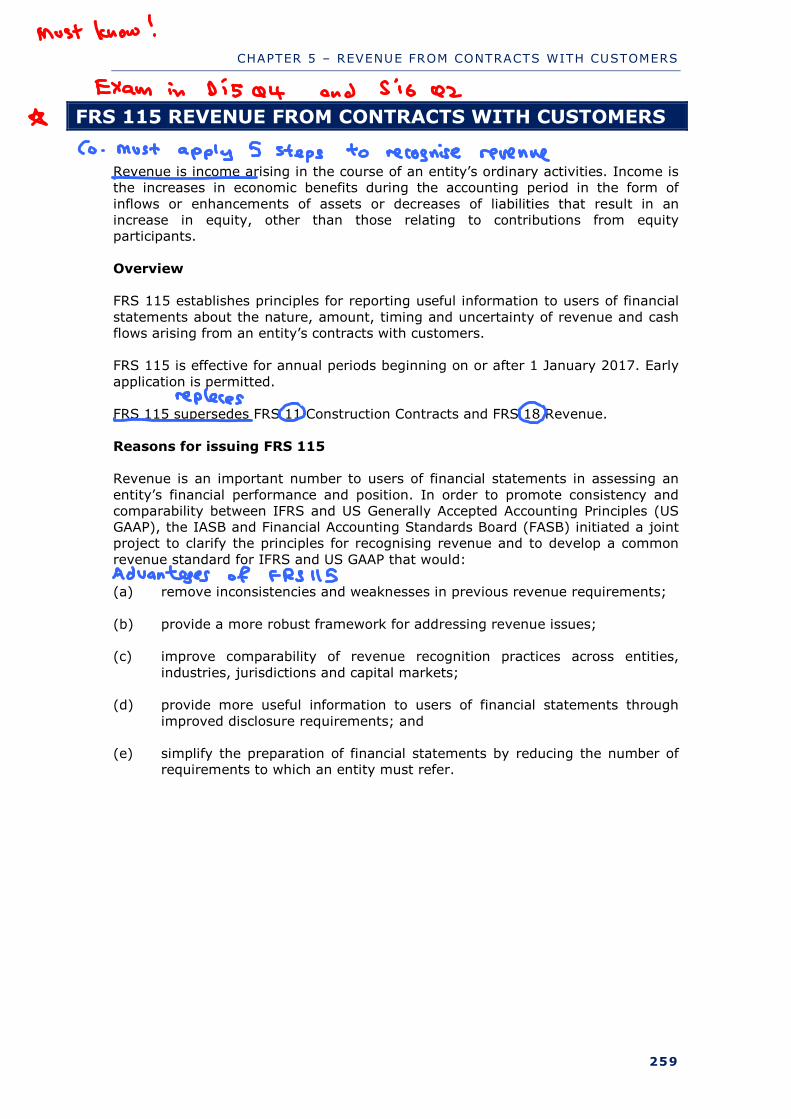

FRS 115 REVENUE FROM CONTRACTS WITH CUSTOMERS

Revenue is income arising in the course of an entity’s ordinary activities. Income is the increases in economic benefits during the accounting period in the form of

inflows or enhancements of assets or decreases of liabilities that result in an increase in equity, other than those relating to contributions from equity participants.

Overview FRS 115 establishes principles for reporting useful information to users of financial

statements about the nature, amount, timing and uncertainty of revenue and cash flows arising from an entity’s contracts with customers. FRS 115 is effective for annual periods beginning on or after 1 January 2017. Early

application is permitted. FRS 115 supersedes FRS 11 Construction Contracts and FRS 18 Revenue.

Reasons for issuing FRS 115 Revenue is an important number to users of financial statements in assessing an

entity’s financial performance and position. In order to promote consistency and comparability between IFRS and US Generally Accepted Accounting Principles (US GAAP), the IASB and Financial Accounting Standards Board (FASB) initiated a joint project to clarify the principles for recognising revenue and to develop a common

revenue standard for IFRS and US GAAP that would: (a) remove inconsistencies and weaknesses in previous revenue requirements;

(b) provide a more robust framework for addressing revenue issues; (c) improve comparability of revenue recognition practices across entities,

industries, jurisdictions and capital markets; (d) provide more useful information to users of financial statements through

improved disclosure requirements; and (e) simplify the preparation of financial statements by reducing the number of

requirements to which an entity must refer.

CHAPTER 5 – REVENUE FROM CONTRACTS WITH CUSTOMERS

261

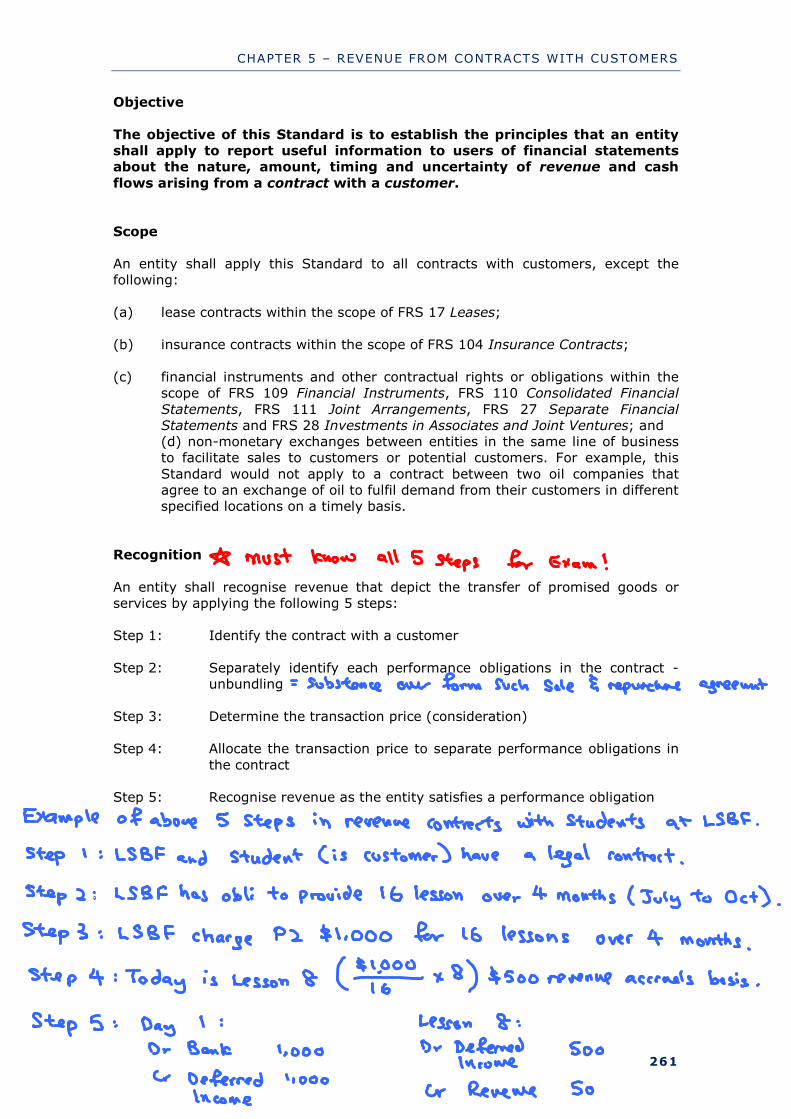

Objective

The objective of this Standard is to establish the principles that an entity shall apply to report useful information to users of financial statements about the nature, amount, timing and uncertainty of revenue and cash

flows arising from a contract with a customer.

Scope An entity shall apply this Standard to all contracts with customers, except the following:

(a) lease contracts within the scope of FRS 17 Leases; (b) insurance contracts within the scope of FRS 104 Insurance Contracts;

(c) financial instruments and other contractual rights or obligations within the

scope of FRS 109 Financial Instruments, FRS 110 Consolidated Financial

Statements, FRS 111 Joint Arrangements, FRS 27 Separate Financial Statements and FRS 28 Investments in Associates and Joint Ventures; and (d) non-monetary exchanges between entities in the same line of business to facilitate sales to customers or potential customers. For example, this

Standard would not apply to a contract between two oil companies that agree to an exchange of oil to fulfil demand from their customers in different specified locations on a timely basis.

Recognition

An entity shall recognise revenue that depict the transfer of promised goods or services by applying the following 5 steps: Step 1: Identify the contract with a customer

Step 2: Separately identify each performance obligations in the contract -

unbundling

Step 3: Determine the transaction price (consideration) Step 4: Allocate the transaction price to separate performance obligations in

the contract Step 5: Recognise revenue as the entity satisfies a performance obligation

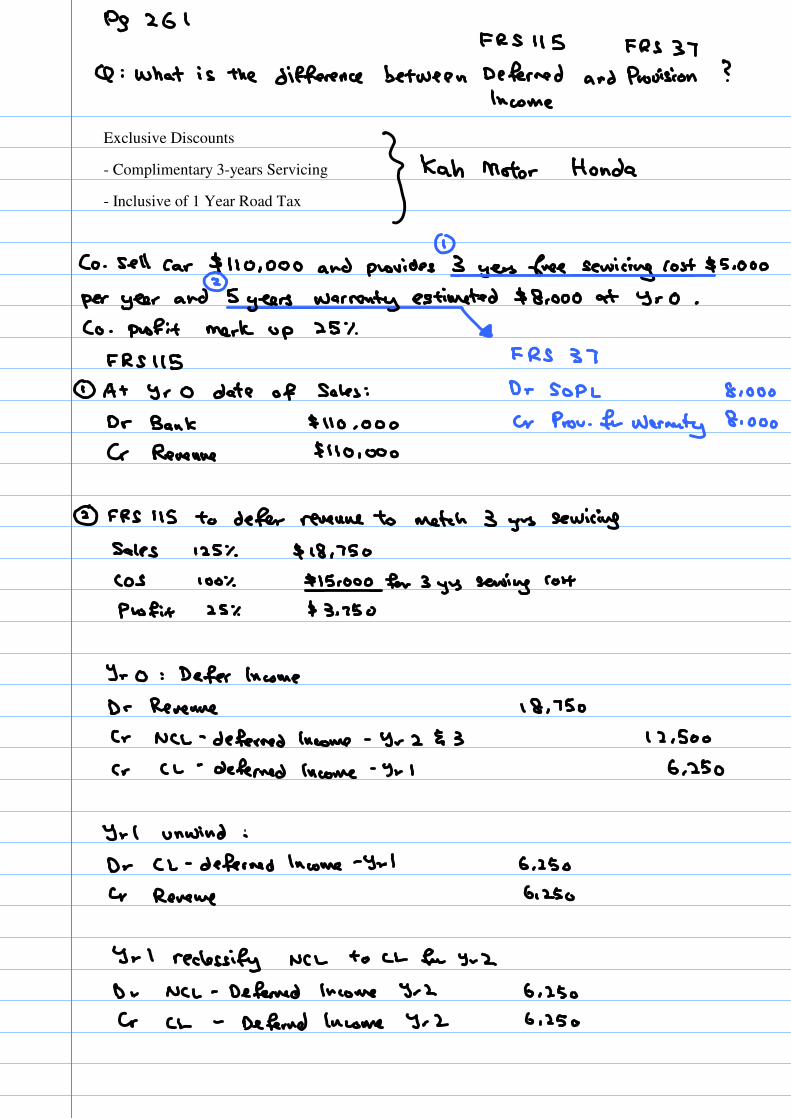

Exclusive Discounts

- Complimentary 3-years Servicing

- Inclusive of 1 Year Road Tax

CHAPTER 5 – REVENUE FROM CONTRACTS WITH CUSTOMERS

265

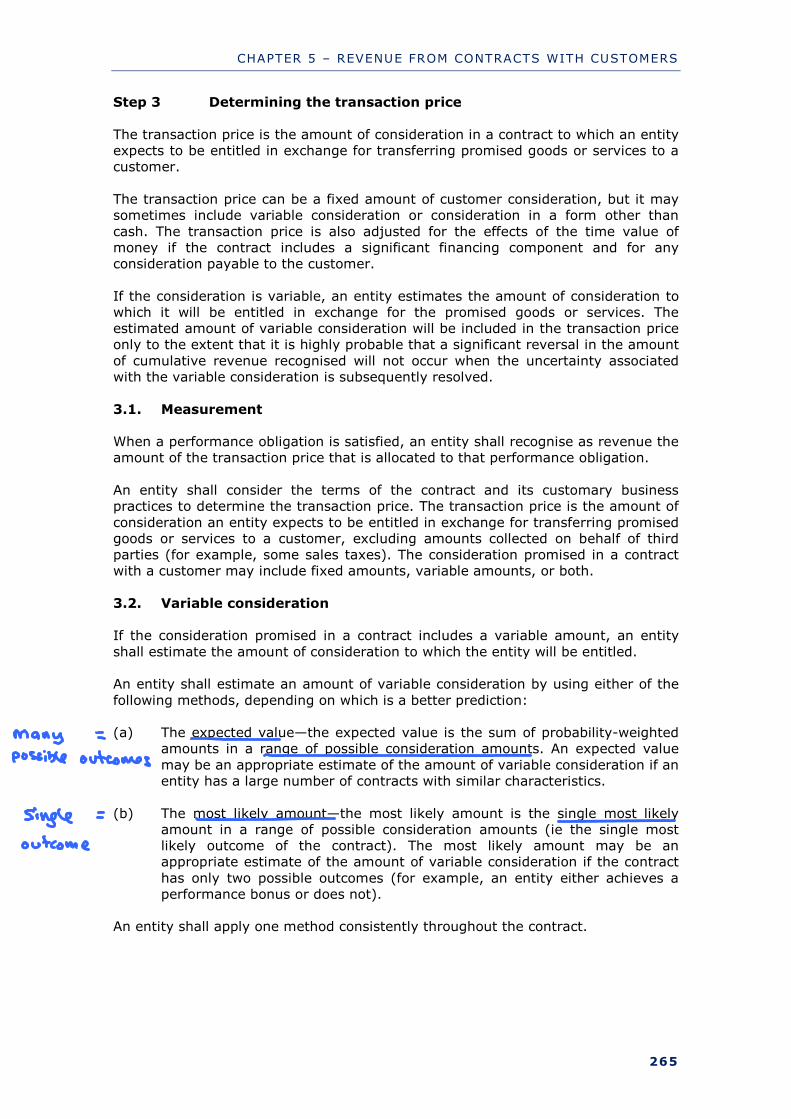

Step 3 Determining the transaction price

The transaction price is the amount of consideration in a contract to which an entity expects to be entitled in exchange for transferring promised goods or services to a customer.

The transaction price can be a fixed amount of customer consideration, but it may sometimes include variable consideration or consideration in a form other than

cash. The transaction price is also adjusted for the effects of the time value of money if the contract includes a significant financing component and for any consideration payable to the customer.

If the consideration is variable, an entity estimates the amount of consideration to which it will be entitled in exchange for the promised goods or services. The estimated amount of variable consideration will be included in the transaction price only to the extent that it is highly probable that a significant reversal in the amount

of cumulative revenue recognised will not occur when the uncertainty associated with the variable consideration is subsequently resolved.

3.1. Measurement When a performance obligation is satisfied, an entity shall recognise as revenue the amount of the transaction price that is allocated to that performance obligation.

An entity shall consider the terms of the contract and its customary business practices to determine the transaction price. The transaction price is the amount of

consideration an entity expects to be entitled in exchange for transferring promised goods or services to a customer, excluding amounts collected on behalf of third parties (for example, some sales taxes). The consideration promised in a contract with a customer may include fixed amounts, variable amounts, or both.

3.2. Variable consideration If the consideration promised in a contract includes a variable amount, an entity

shall estimate the amount of consideration to which the entity will be entitled. An entity shall estimate an amount of variable consideration by using either of the

following methods, depending on which is a better prediction: (a) The expected value—the expected value is the sum of probability-weighted

amounts in a range of possible consideration amounts. An expected value

may be an appropriate estimate of the amount of variable consideration if an entity has a large number of contracts with similar characteristics.

(b) The most likely amount—the most likely amount is the single most likely amount in a range of possible consideration amounts (ie the single most likely outcome of the contract). The most likely amount may be an appropriate estimate of the amount of variable consideration if the contract

has only two possible outcomes (for example, an entity either achieves a performance bonus or does not).

An entity shall apply one method consistently throughout the contract.

CHAPTER 5 – REVENUE FROM CONTRACTS WITH CUSTOMERS

272

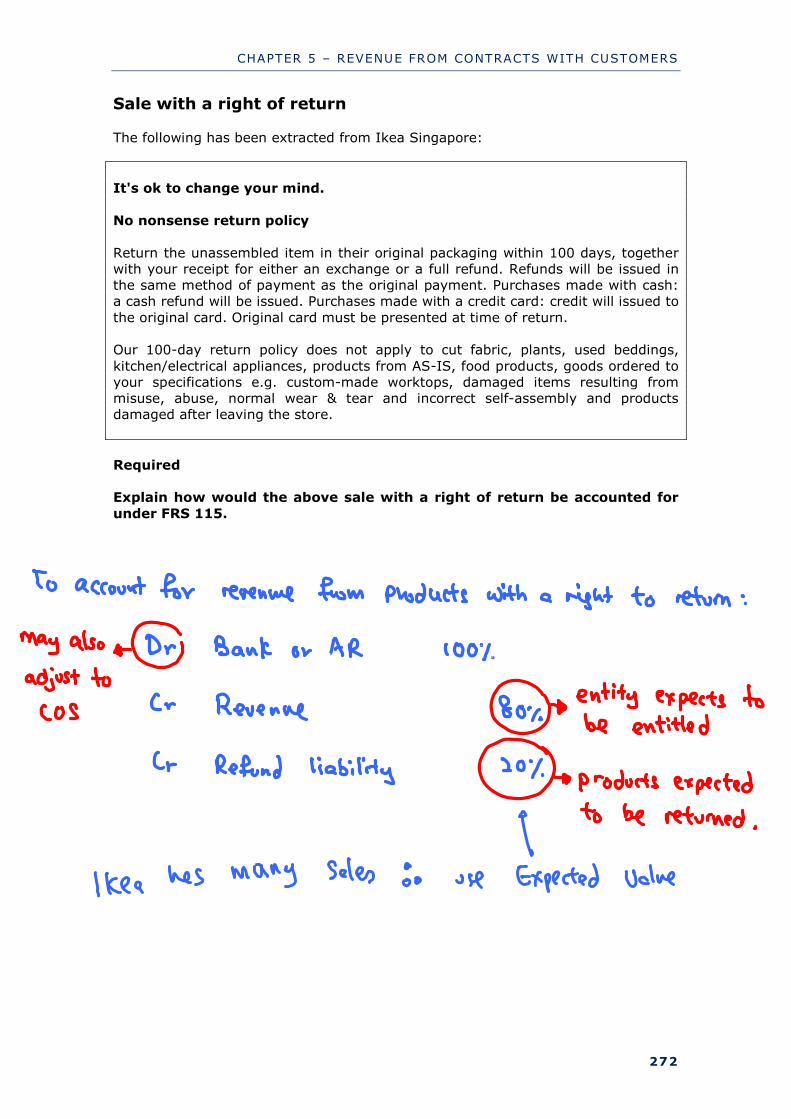

Sale with a right of return The following has been extracted from Ikea Singapore:

It's ok to change your mind.

No nonsense return policy

Return the unassembled item in their original packaging within 100 days, together with your receipt for either an exchange or a full refund. Refunds will be issued in the same method of payment as the original payment. Purchases made with cash: a cash refund will be issued. Purchases made with a credit card: credit will issued to

the original card. Original card must be presented at time of return. Our 100-day return policy does not apply to cut fabric, plants, used beddings,

kitchen/electrical appliances, products from AS-IS, food products, goods ordered to your specifications e.g. custom-made worktops, damaged items resulting from misuse, abuse, normal wear & tear and incorrect self-assembly and products damaged after leaving the store.

Required Explain how would the above sale with a right of return be accounted for

under FRS 115.

CHAPTER 5 – REVENUE FROM CONTRACTS WITH CUSTOMERS

273

Warranties Harvey Norman provides a 3 years standard warranty for the refrigerator it sells. In addition, it also allows customers to buy an extended warranty of up to 5 years

after the manufacturer’s warranty. The benefits include free parts and service and if the product can’t be repaired, it will be replaced for free.

Required Describe how would the warranty be accounted for under relevant standards?

CHAPTER 5 – REVENUE FROM CONTRACTS WITH CUSTOMERS

274

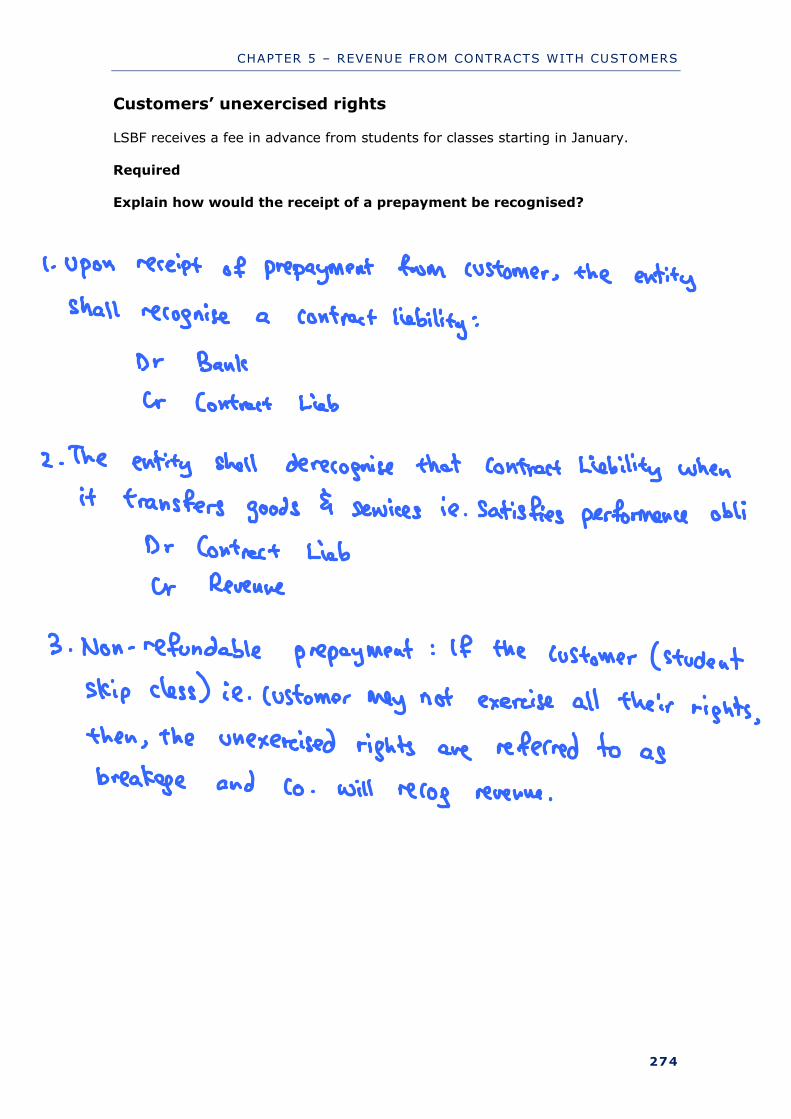

Customers’ unexercised rights LSBF receives a fee in advance from students for classes starting in January.

Required Explain how would the receipt of a prepayment be recognised?

CHAPTER 5 – REVENUE FROM CONTRACTS WITH CUSTOMERS

275

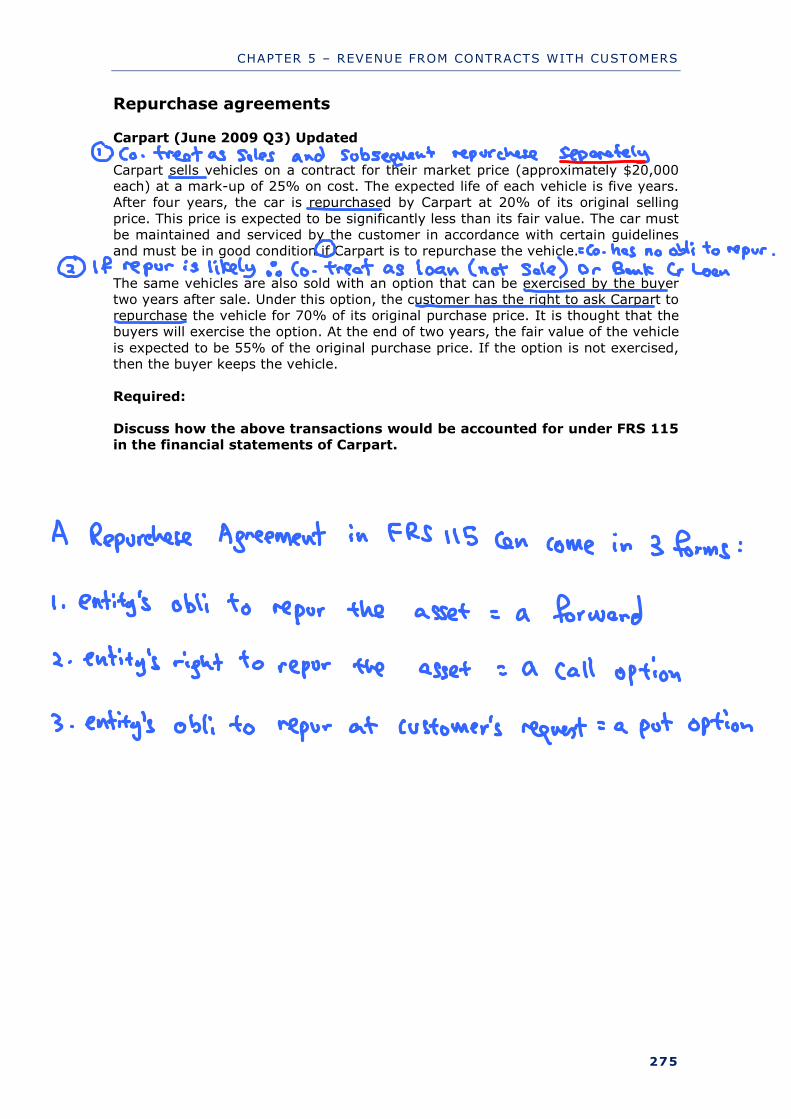

Repurchase agreements Carpart (June 2009 Q3) Updated

Carpart sells vehicles on a contract for their market price (approximately $20,000 each) at a mark-up of 25% on cost. The expected life of each vehicle is five years. After four years, the car is repurchased by Carpart at 20% of its original selling

price. This price is expected to be significantly less than its fair value. The car must be maintained and serviced by the customer in accordance with certain guidelines and must be in good condition if Carpart is to repurchase the vehicle.

The same vehicles are also sold with an option that can be exercised by the buyer two years after sale. Under this option, the customer has the right to ask Carpart to repurchase the vehicle for 70% of its original purchase price. It is thought that the buyers will exercise the option. At the end of two years, the fair value of the vehicle

is expected to be 55% of the original purchase price. If the option is not exercised, then the buyer keeps the vehicle.

Required: Discuss how the above transactions would be accounted for under FRS 115 in the financial statements of Carpart.

CHAPTER 5 – REVENUE FROM CONTRACTS WITH CUSTOMERS

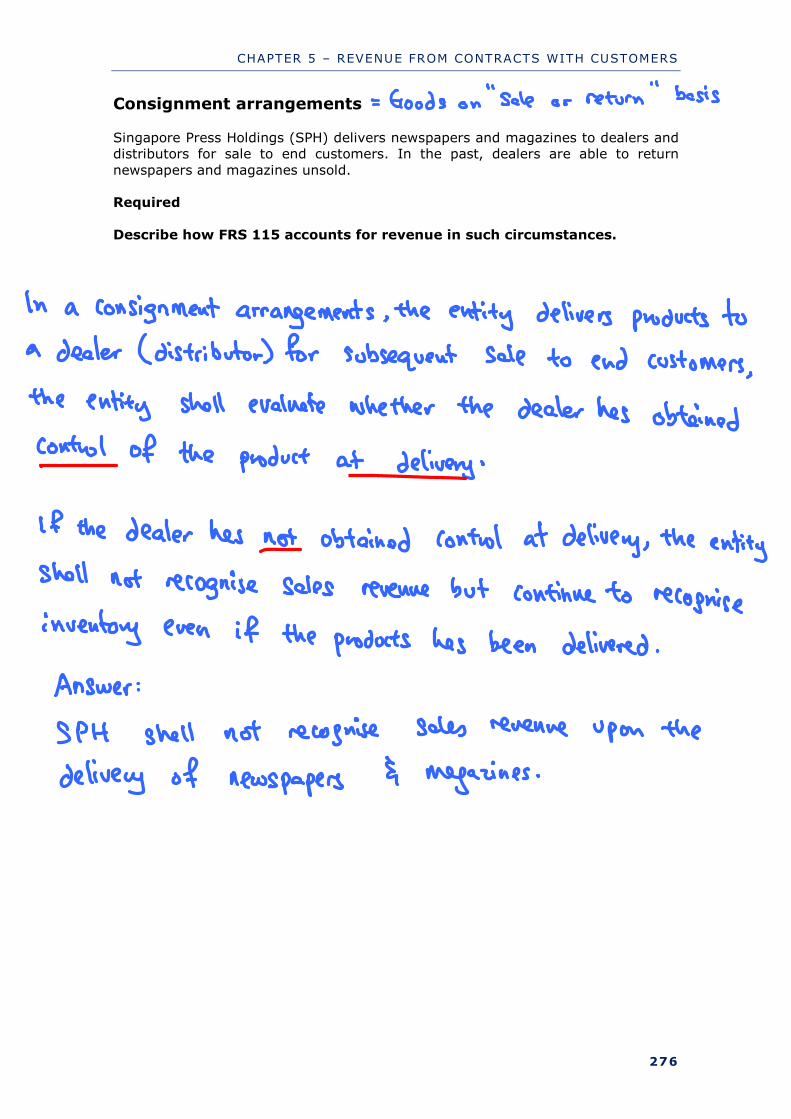

276

Consignment arrangements Singapore Press Holdings (SPH) delivers newspapers and magazines to dealers and distributors for sale to end customers. In the past, dealers are able to return

newspapers and magazines unsold. Required

Describe how FRS 115 accounts for revenue in such circumstances.

CHAPTER 5 – REVENUE FROM CONTRACTS WITH CUSTOMERS

277

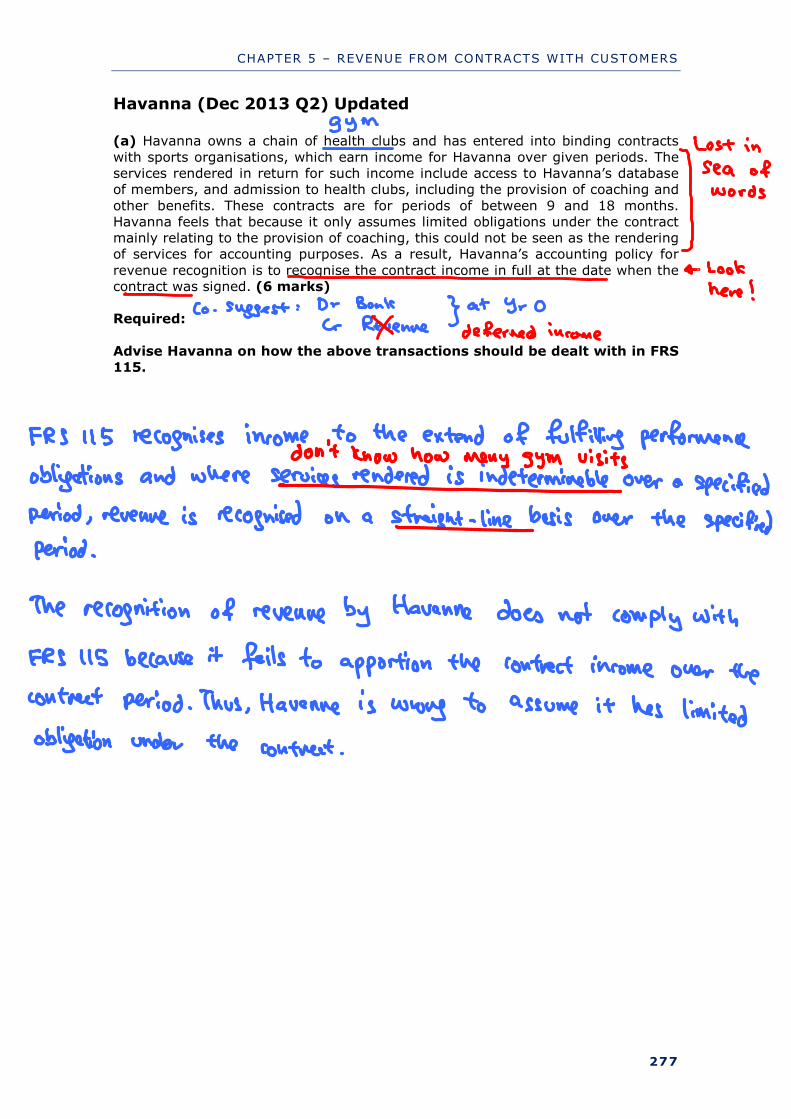

Havanna (Dec 2013 Q2) Updated

(a) Havanna owns a chain of health clubs and has entered into binding contracts

with sports organisations, which earn income for Havanna over given periods. The services rendered in return for such income include access to Havanna’s database of members, and admission to health clubs, including the provision of coaching and

other benefits. These contracts are for periods of between 9 and 18 months. Havanna feels that because it only assumes limited obligations under the contract mainly relating to the provision of coaching, this could not be seen as the rendering of services for accounting purposes. As a result, Havanna’s accounting policy for

revenue recognition is to recognise the contract income in full at the date when the contract was signed. (6 marks) Required:

Advise Havanna on how the above transactions should be dealt with in FRS 115.

CHAPTER 5 – REVENUE FROM CONTRACTS WITH CUSTOMERS

278

Verge (Jun 2013 Q2) Updated

(b) Verge entered into a contract with a government body on 1 April 2011 to undertake maintenance services on a new railway line. The total revenue from the

contract is $5 million over a three-year period. The contract states that $1 million will be paid at the commencement of the contract but, although invoices will be subsequently sent at the end of each year, the government authority will only settle

the subsequent amounts owing when the contract is completed. The invoices sent by Verge to date (including $1 million above) were as follows: Year ended 31 March 2012 $2·8 million

Year ended 31 March 2013 $1·2 million The balance will be invoiced on 31 March 2014. Verge has only accounted for the

initial payment in the financial statements to 31 March 2012 as no subsequent amounts are to be paid until 31 March 2014. The amounts of the invoices reflect the work undertaken in the period. Verge wishes to know how to account for the revenue on the contract in the financial statements to date.

Market interest rates are currently at 6%. (6 marks) Required:

Advise Verge on how the above accounting issues should be dealt with in its financial statements for the years ending 31 March 2012 (where applicable) and 31 March 2013 according to FRS 115.

CHAPTER 5 – REVENUE FROM CONTRACTS WITH CUSTOMERS

280

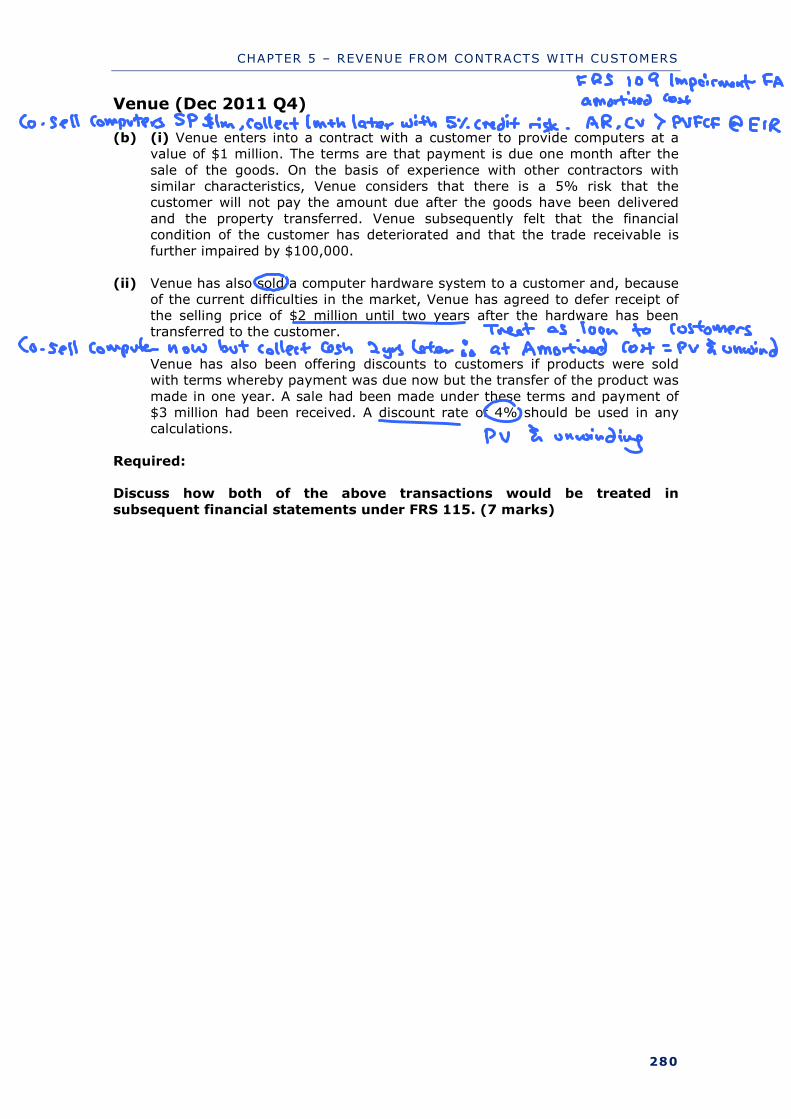

Venue (Dec 2011 Q4) (b) (i) Venue enters into a contract with a customer to provide computers at a

value of $1 million. The terms are that payment is due one month after the

sale of the goods. On the basis of experience with other contractors with similar characteristics, Venue considers that there is a 5% risk that the customer will not pay the amount due after the goods have been delivered

and the property transferred. Venue subsequently felt that the financial condition of the customer has deteriorated and that the trade receivable is further impaired by $100,000.

(ii) Venue has also sold a computer hardware system to a customer and, because of the current difficulties in the market, Venue has agreed to defer receipt of the selling price of $2 million until two years after the hardware has been transferred to the customer.

Venue has also been offering discounts to customers if products were sold with terms whereby payment was due now but the transfer of the product was

made in one year. A sale had been made under these terms and payment of $3 million had been received. A discount rate of 4% should be used in any calculations.

Required: Discuss how both of the above transactions would be treated in

subsequent financial statements under FRS 115. (7 marks)

CHAPTER 6 – REPORTING FINANCIAL PERFORMANCE

296

CHAPTER CONTENTS

FRS 34 INTERIM FINANCIAL REPORTING --------------------------- 297

FRS 108 OPERATING SEGMENTS -------------------------------------- 299

FRS 24 RELATED PARTY DISCLOSURES ------------------------------ 304

FRS 8 ACCOUNTING POLICIES, CHANGES IN ACCOUNTING ESTIMATES AND ERRORS ---------------------------------------- 310

FRS 101 FIRST-TIME ADOPTION OF FINANCIAL REPORTING STANDARDS ------------------------------------------------------- 316

FRS 10 EVENTS AFTER THE REPORTING PERIOD ------------------- 323

FRS 33 EARNINGS PER SHARE ---------------------------------------- 326

CHAPTER 6 – REPORTING FINANCIAL PERFORMANCE

299

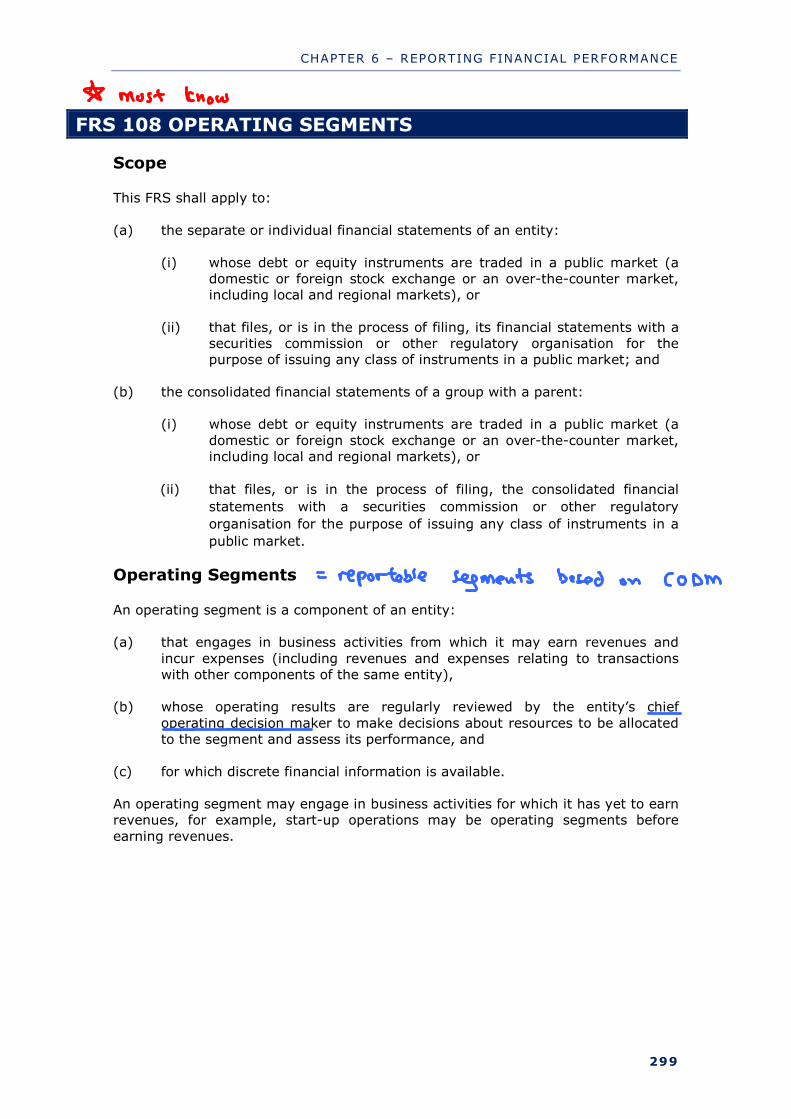

FRS 108 OPERATING SEGMENTS

Scope

This FRS shall apply to:

(a) the separate or individual financial statements of an entity:

(i) whose debt or equity instruments are traded in a public market (a domestic or foreign stock exchange or an over-the-counter market, including local and regional markets), or

(ii) that files, or is in the process of filing, its financial statements with a securities commission or other regulatory organisation for the purpose of issuing any class of instruments in a public market; and

(b) the consolidated financial statements of a group with a parent:

(i) whose debt or equity instruments are traded in a public market (a

domestic or foreign stock exchange or an over-the-counter market, including local and regional markets), or

(ii) that files, or is in the process of filing, the consolidated financial

statements with a securities commission or other regulatory

organisation for the purpose of issuing any class of instruments in a

public market.

Operating Segments

An operating segment is a component of an entity: (a) that engages in business activities from which it may earn revenues and

incur expenses (including revenues and expenses relating to transactions with other components of the same entity),

(b) whose operating results are regularly reviewed by the entity’s chief

operating decision maker to make decisions about resources to be allocated to the segment and assess its performance, and

(c) for which discrete financial information is available. An operating segment may engage in business activities for which it has yet to earn revenues, for example, start-up operations may be operating segments before

earning revenues.

CHAPTER 6 – REPORTING FINANCIAL PERFORMANCE

300

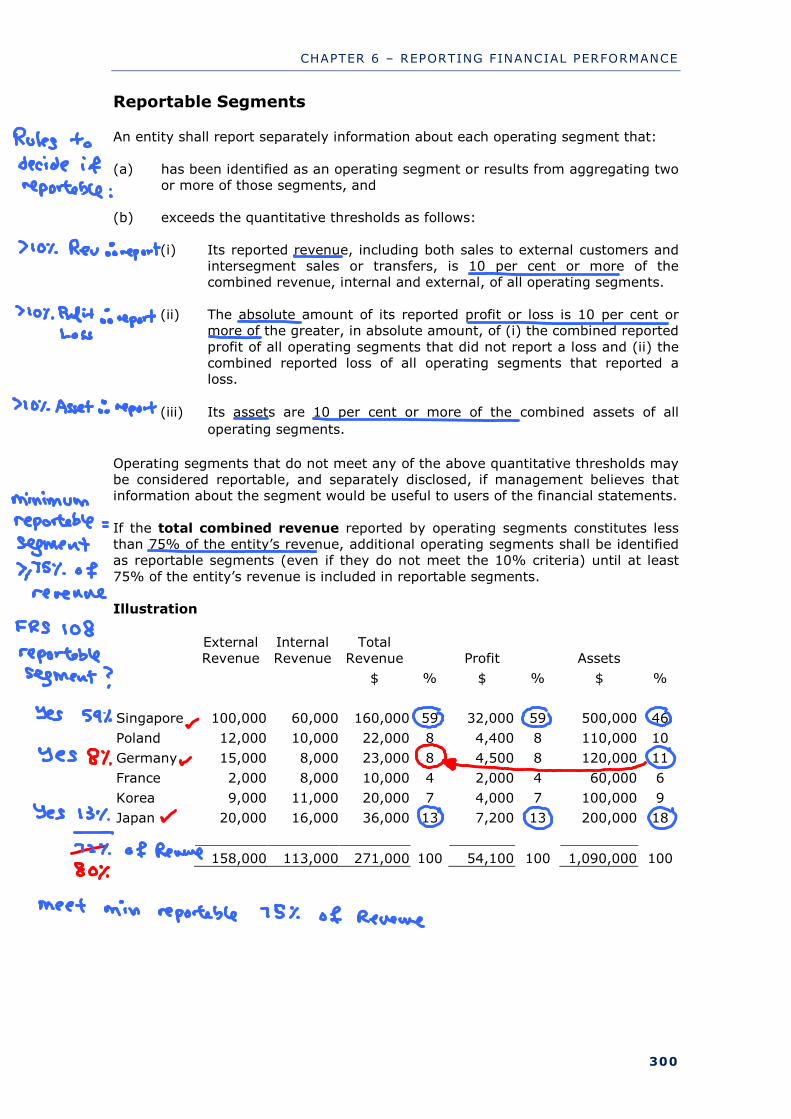

Reportable Segments

An entity shall report separately information about each operating segment that:

(a) has been identified as an operating segment or results from aggregating two or more of those segments, and

(b) exceeds the quantitative thresholds as follows:

(i) Its reported revenue, including both sales to external customers and

intersegment sales or transfers, is 10 per cent or more of the combined revenue, internal and external, of all operating segments.

(ii) The absolute amount of its reported profit or loss is 10 per cent or

more of the greater, in absolute amount, of (i) the combined reported

profit of all operating segments that did not report a loss and (ii) the combined reported loss of all operating segments that reported a loss.

(iii) Its assets are 10 per cent or more of the combined assets of all

operating segments.

Operating segments that do not meet any of the above quantitative thresholds may be considered reportable, and separately disclosed, if management believes that information about the segment would be useful to users of the financial statements.

If the total combined revenue reported by operating segments constitutes less than 75% of the entity’s revenue, additional operating segments shall be identified as reportable segments (even if they do not meet the 10% criteria) until at least

75% of the entity’s revenue is included in reportable segments. Illustration

External Revenue

Internal Revenue

Total Revenue Profit Assets

$ % $ % $ %

Singapore 100,000 60,000 160,000 59 32,000 59 500,000 46

Poland 12,000 10,000 22,000 8 4,400 8 110,000 10

Germany 15,000 8,000 23,000 8 4,500 8 120,000 11

France 2,000 8,000 10,000 4 2,000 4 60,000 6

Korea 9,000 11,000 20,000 7 4,000 7 100,000 9

Japan 20,000 16,000 36,000 13 7,200 13 200,000 18

158,000 113,000 271,000 100 54,100 100 1,090,000 100

CHAPTER 6 – REPORTING FINANCIAL PERFORMANCE

302

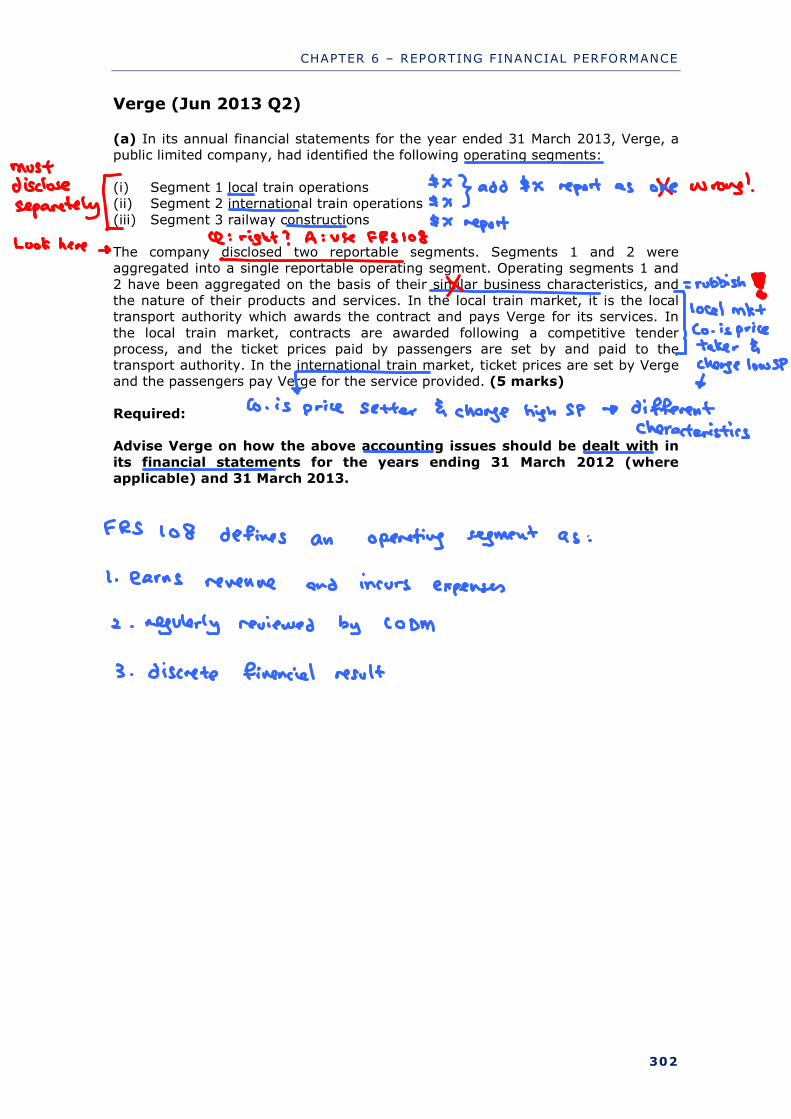

Verge (Jun 2013 Q2)

(a) In its annual financial statements for the year ended 31 March 2013, Verge, a public limited company, had identified the following operating segments:

(i) Segment 1 local train operations (ii) Segment 2 international train operations

(iii) Segment 3 railway constructions The company disclosed two reportable segments. Segments 1 and 2 were aggregated into a single reportable operating segment. Operating segments 1 and

2 have been aggregated on the basis of their similar business characteristics, and the nature of their products and services. In the local train market, it is the local transport authority which awards the contract and pays Verge for its services. In

the local train market, contracts are awarded following a competitive tender process, and the ticket prices paid by passengers are set by and paid to the transport authority. In the international train market, ticket prices are set by Verge and the passengers pay Verge for the service provided. (5 marks)

Required: Advise Verge on how the above accounting issues should be dealt with in

its financial statements for the years ending 31 March 2012 (where applicable) and 31 March 2013.

CHAPTER 6 – REPORTING FINANCIAL PERFORMANCE

303

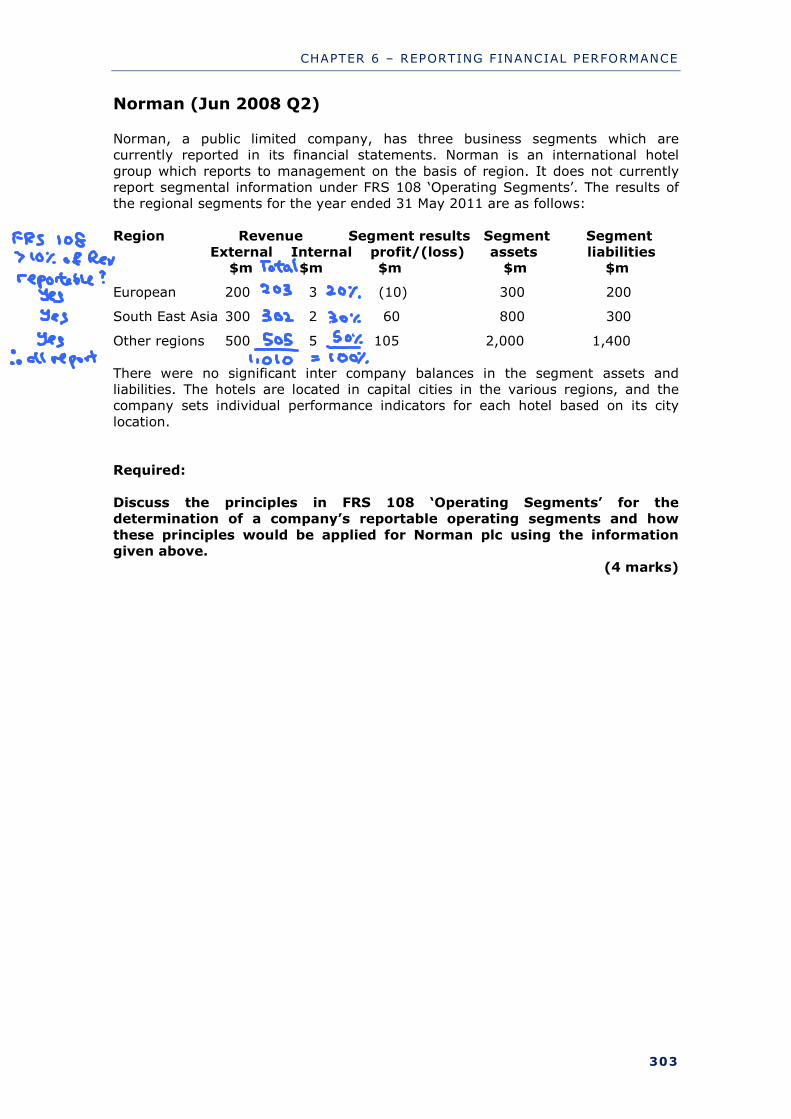

Norman (Jun 2008 Q2)

Norman, a public limited company, has three business segments which are currently reported in its financial statements. Norman is an international hotel

group which reports to management on the basis of region. It does not currently report segmental information under FRS 108 ‘Operating Segments’. The results of the regional segments for the year ended 31 May 2011 are as follows:

Region Revenue Segment results Segment Segment External Internal profit/(loss) assets liabilities $m $m $m $m $m

European 200 3 (10) 300 200

South East Asia 300 2 60 800 300

Other regions 500 5 105 2,000 1,400

There were no significant inter company balances in the segment assets and liabilities. The hotels are located in capital cities in the various regions, and the company sets individual performance indicators for each hotel based on its city

location. Required:

Discuss the principles in FRS 108 ‘Operating Segments’ for the determination of a company’s reportable operating segments and how

these principles would be applied for Norman plc using the information given above.

(4 marks)

CHAPTER 6 – REPORTING FINANCIAL PERFORMANCE

304

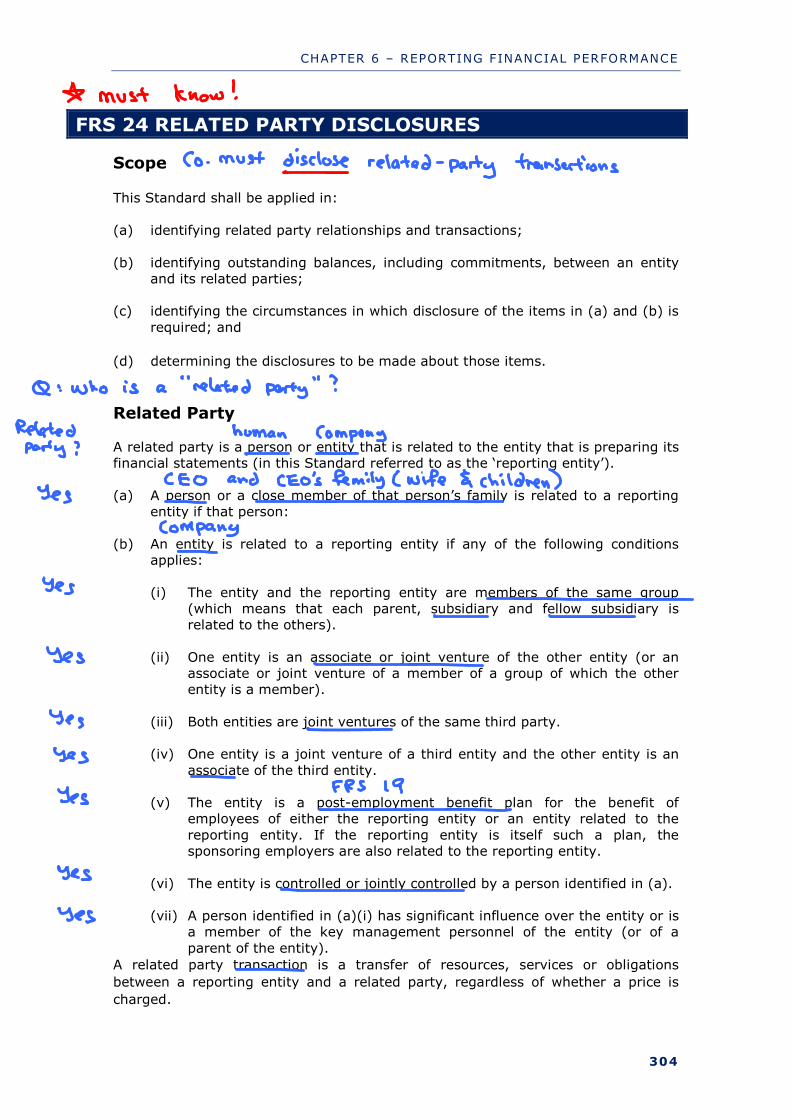

FRS 24 RELATED PARTY DISCLOSURES

Scope

This Standard shall be applied in:

(a) identifying related party relationships and transactions;

(b) identifying outstanding balances, including commitments, between an entity and its related parties;

(c) identifying the circumstances in which disclosure of the items in (a) and (b) is

required; and

(d) determining the disclosures to be made about those items.

Related Party A related party is a person or entity that is related to the entity that is preparing its financial statements (in this Standard referred to as the ‘reporting entity’).

(a) A person or a close member of that person’s family is related to a reporting

entity if that person:

(b) An entity is related to a reporting entity if any of the following conditions applies:

(i) The entity and the reporting entity are members of the same group (which means that each parent, subsidiary and fellow subsidiary is related to the others).

(ii) One entity is an associate or joint venture of the other entity (or an associate or joint venture of a member of a group of which the other entity is a member).

(iii) Both entities are joint ventures of the same third party. (iv) One entity is a joint venture of a third entity and the other entity is an

associate of the third entity. (v) The entity is a post-employment benefit plan for the benefit of

employees of either the reporting entity or an entity related to the

reporting entity. If the reporting entity is itself such a plan, the sponsoring employers are also related to the reporting entity.

(vi) The entity is controlled or jointly controlled by a person identified in (a). (vii) A person identified in (a)(i) has significant influence over the entity or is

a member of the key management personnel of the entity (or of a

parent of the entity).

A related party transaction is a transfer of resources, services or obligations

between a reporting entity and a related party, regardless of whether a price is

charged.

CHAPTER 6 – REPORTING FINANCIAL PERFORMANCE

306

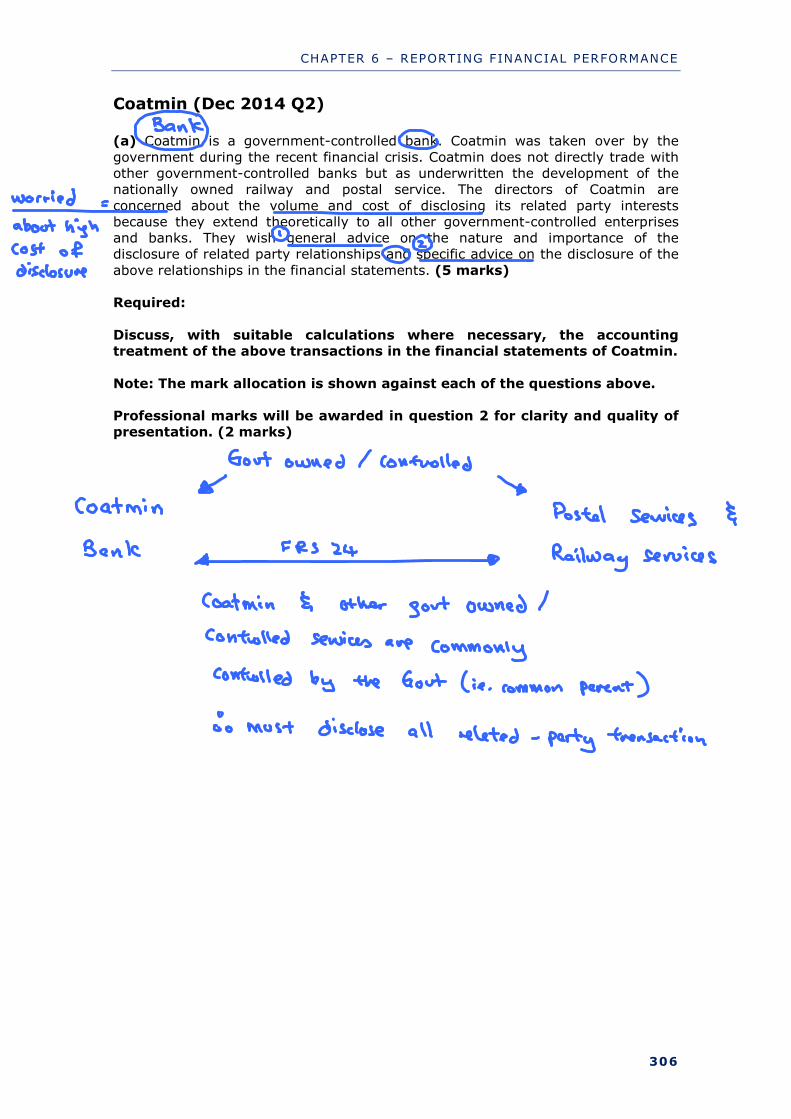

Coatmin (Dec 2014 Q2)

(a) Coatmin is a government-controlled bank. Coatmin was taken over by the

government during the recent financial crisis. Coatmin does not directly trade with other government-controlled banks but as underwritten the development of the nationally owned railway and postal service. The directors of Coatmin are

concerned about the volume and cost of disclosing its related party interests because they extend theoretically to all other government-controlled enterprises and banks. They wish general advice on the nature and importance of the disclosure of related party relationships and specific advice on the disclosure of the

above relationships in the financial statements. (5 marks) Required:

Discuss, with suitable calculations where necessary, the accounting treatment of the above transactions in the financial statements of Coatmin.

Note: The mark allocation is shown against each of the questions above. Professional marks will be awarded in question 2 for clarity and quality of presentation. (2 marks)

CHAPTER 6 – REPORTING FINANCIAL PERFORMANCE

310

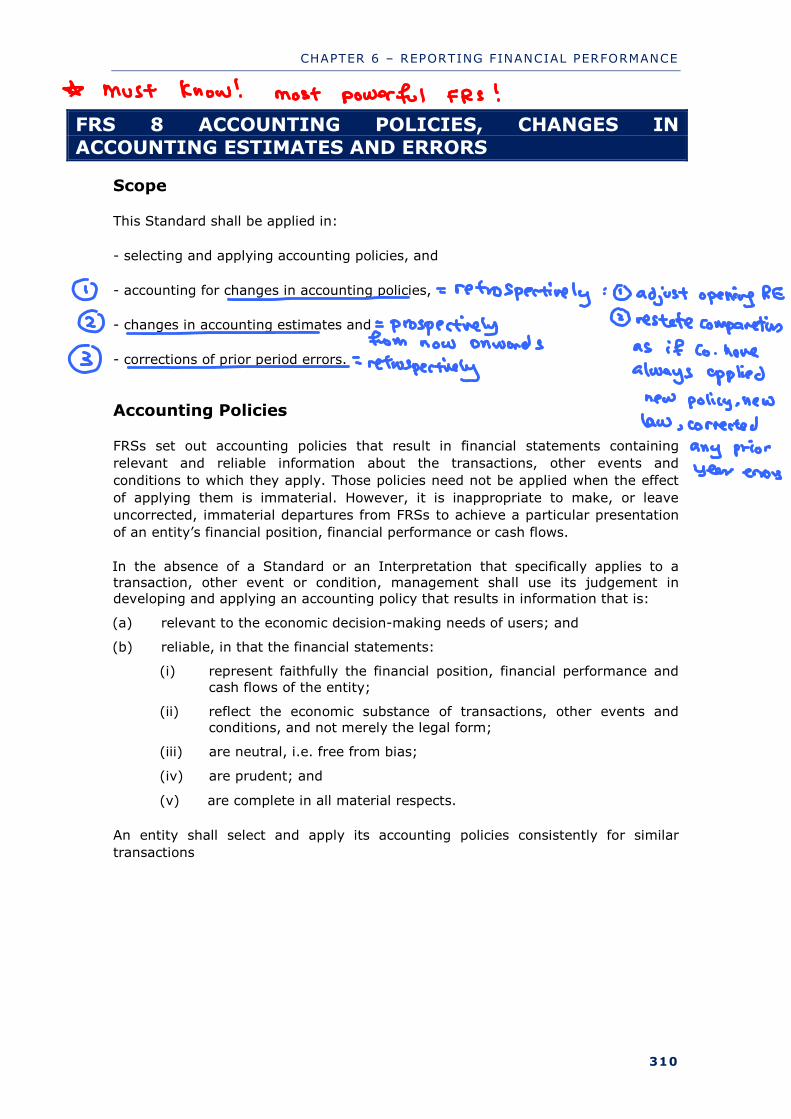

FRS 8 ACCOUNTING POLICIES, CHANGES IN

ACCOUNTING ESTIMATES AND ERRORS

Scope

This Standard shall be applied in:

- selecting and applying accounting policies, and

- accounting for changes in accounting policies,

- changes in accounting estimates and

- corrections of prior period errors.

Accounting Policies

FRSs set out accounting policies that result in financial statements containing

relevant and reliable information about the transactions, other events and

conditions to which they apply. Those policies need not be applied when the effect

of applying them is immaterial. However, it is inappropriate to make, or leave

uncorrected, immaterial departures from FRSs to achieve a particular presentation

of an entity’s financial position, financial performance or cash flows.

In the absence of a Standard or an Interpretation that specifically applies to a transaction, other event or condition, management shall use its judgement in developing and applying an accounting policy that results in information that is:

(a) relevant to the economic decision-making needs of users; and

(b) reliable, in that the financial statements:

(i) represent faithfully the financial position, financial performance and

cash flows of the entity;

(ii) reflect the economic substance of transactions, other events and conditions, and not merely the legal form;

(iii) are neutral, i.e. free from bias;

(iv) are prudent; and

(v) are complete in all material respects.

An entity shall select and apply its accounting policies consistently for similar

transactions

CHAPTER 6 – REPORTING FINANCIAL PERFORMANCE

316

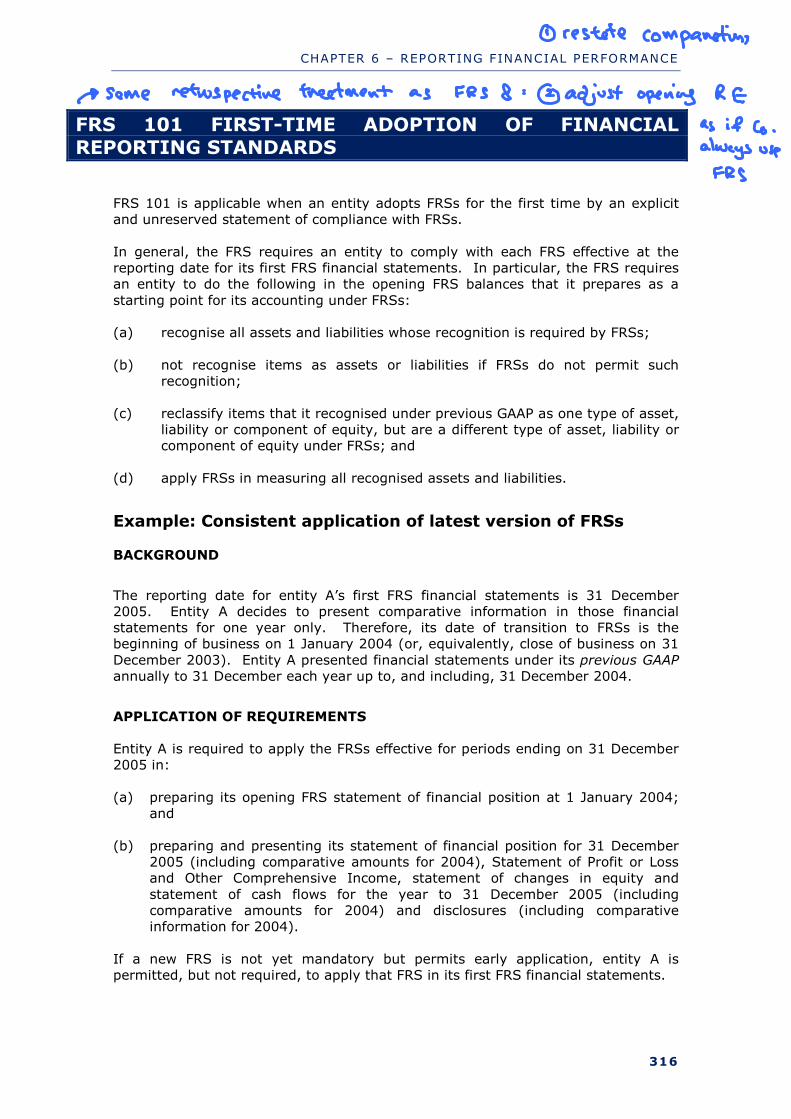

FRS 101 FIRST-TIME ADOPTION OF FINANCIAL

REPORTING STANDARDS

FRS 101 is applicable when an entity adopts FRSs for the first time by an explicit and unreserved statement of compliance with FRSs.

In general, the FRS requires an entity to comply with each FRS effective at the reporting date for its first FRS financial statements. In particular, the FRS requires an entity to do the following in the opening FRS balances that it prepares as a

starting point for its accounting under FRSs: (a) recognise all assets and liabilities whose recognition is required by FRSs;

(b) not recognise items as assets or liabilities if FRSs do not permit such recognition;

(c) reclassify items that it recognised under previous GAAP as one type of asset, liability or component of equity, but are a different type of asset, liability or component of equity under FRSs; and

(d) apply FRSs in measuring all recognised assets and liabilities.

Example: Consistent application of latest version of FRSs BACKGROUND

The reporting date for entity A’s first FRS financial statements is 31 December 2005. Entity A decides to present comparative information in those financial statements for one year only. Therefore, its date of transition to FRSs is the beginning of business on 1 January 2004 (or, equivalently, close of business on 31

December 2003). Entity A presented financial statements under its previous GAAP annually to 31 December each year up to, and including, 31 December 2004.

APPLICATION OF REQUIREMENTS Entity A is required to apply the FRSs effective for periods ending on 31 December 2005 in:

(a) preparing its opening FRS statement of financial position at 1 January 2004;

and

(b) preparing and presenting its statement of financial position for 31 December 2005 (including comparative amounts for 2004), Statement of Profit or Loss and Other Comprehensive Income, statement of changes in equity and

statement of cash flows for the year to 31 December 2005 (including comparative amounts for 2004) and disclosures (including comparative information for 2004).

If a new FRS is not yet mandatory but permits early application, entity A is permitted, but not required, to apply that FRS in its first FRS financial statements.