Embed Size (px)

Citation preview

. 281

CHAPTER 7

FINDINGS, CONCLUSIONS

AND SUGGESTIONS

. 282

CHAPTER 7: FINDINGS, CONCLUSIONS AND SUGGESTIONS 7.0 SUMMARY OF FINDINGS As discussed in chapter 1, the objectives of the study are (a) to analyze the growth and

performance of Indian Hosiery Industry in the recent era, (b) to study the nature and types

of strategies adopted by Indian Hosiery manufactures to fight the global competition, (c)

to analyze the pricing & product and promotion and distribution management strategies

adopted by Indian Hosiery Manufacturers (d) to analyze the regulatory framework of

Indian government to promote Indian hosiery industry and (e) to find the problems faced

in strategic growth of Indian hosiery industry.

From the detailed analysis done chapter 4, 5 & 6, we discovered various variables

and aspects and their priorities for hosiery units. It is obvious that exploratory research

design fits best for the kind of the problem we had have in hand. We have used expert

interviews, pilot surveys, secondary data analysis and qualitative research to explore the

facts and justify the answers to problem in hand.

After extensive analysis of different aspects of hosiery industry I have been able

to achieve the objectives of the study. The major findings of the study are discussed

below:

7.1) The growth of hosiery industry is not significant in post quota regime. The results

shows in four years of pre-quota elimination i.e. year 2001-02 to year 2004-05 the

. 283

composite growth registered is 33.50% and in next four years after quota elimination i.e.

2005-06 to 2008-09 the composite growth registered is 37.40%. On applying ‘t’ test to

compare the performance of pre-quota and post-quota period, we get the ‘p’ value of

0.003 which is significant at 5% significant level. We had to reject the null hypothesis

Ho(a) i.e. ‘There is significant increase in difference in export performance of hosiery

industry in post quota regime i.e. between 2001-05 and 2005-09” and accept the alternate

hypothesis H1(a) i.e. “There is no significant growth in hosiery exports in post quota

regime”.

One of the reasons for non-performance of hosiery industry is the lack of

participation from non-export sector. Indian hosiery sector is dominated by small scale

players. After 2002, the hosiery sector was de-reserved and there was large opportunity

for non-exporting sector to update their methods of production and enhance capacities,

but there was no such competition to small scale sector from any large players because of

which they neither realized the need to update their methods of production nor did they

understand the opportunity in hand. Although there was no such cap on expansion of

exporting sector units, but these units also did not expanded to the extent they could have.

We have very few large players in hosiery sector. The exporting sector has expanded and

modernized over a period of time but they were always full of orders due to benefit of

quota. When the quota was removed, China flooded the market with its low cost products

and Indian hosiery producers could not compete them. After re-imposition of quota on

Chinese textile products, there was respite for Indian hosiery exporters and since then

they are continuously growing slowly.

. 284

7.2) The exchange rate i.e. US$/INR change significantly during the period of eight

years i.e. 2001-2002 to 2008-09. On applying t test to compare the change in exchange

rate during pre-quota period and post-quota period, we get ‘p’ value equivalent to almost

zero and ‘t’ stat value of 6.0743 that lies outside the ‘t’ critical value of 2.012. We had

have enough evidence to reject null hypothesis Ho(b) - “There is no significant change

in exchange rate between pre-quota elimination and post quota elimination period” and

accept alternate hypothesis H1(b) – “There is significant change in exchange rate

between pre-quota elimination and post quota elimination period”.

The exchange rate always plays an important role in export performance of any

economy. India always desire weaker rupee and stronger dollar, so that our exports are

more competitive in the international markets. Also stronger dollar will curtail the

imports because it will increase the cost of imported products. This will give respite to

domestic producers. RBI may not keep rupee at this level for long time, because to keep

domestic currency weak, a nation has to bear economic cost in the form of increased

inflation in domestic market and losing export competitiveness in long run. Appreciating

rupee will continue to pose threat to hosiery exporters with increasing international

competition from other developing and LDC. Indian exporters need to strengthen their

production capacities, capabilities and managerial skills to cope up the changing business

environment. They must understand the benefit of hedging the export receipts and how it

can benefit them when they enter into long term agreement. Also, government and

financial institutions should take initiatives to educate the small hosiery exporters so that

. 285

they may gain confidence to take on long term price contracts, which will add value to

their value chain.

7.3) Out study conclude that there is no linear relationship between exchange rate and

export performance. This is based on the regression analysis where dependent variable

‘Y’ is value of export performance from 2001-02 to 2008-09 and independent variable

‘X’ is INR/US$ exchange rate. The regression results reveal that the value of ‘t’ statistics

received is -1.62619. From ‘t’ table, the critical Value of ‘t’ for 6 degree of freedom (N-

2) with α =0.05, we get the value of 2.4469. The value of ‘t’ critical is more than value of

‘t’ statistics, thus we have significant evidence to accept the null hypothesis. Also ‘p’

value 0.155034 is more than 0.05. Therefore we have sufficient evidence to accept null

hypothesis Ho(c) i.e. “there is no relationship between exchange rate and export

performance” and reject the alternate hypothesis H1(c) i.e. “there is linear relationship

between exchange rate and export performance”. There is weak correlation between

export performance and exchange rate because the value of coefficient of correlation

obtained is 0.553098.

7.4) Textile Upgradation scheme has not been very popular among the hosiery

producers and exporting units of Ludhiana. Our study concludes that spinning sector has

played dominant role in modernization process. 42% of disbursement goes to spinning

sector alone followed by composite mill sector disbursed about 24% of total amount

disbursed under TUFS. Knitting or hosiery sector has remained laggard with just below

3% of amount disbursed.

. 286

The finance facility availed under TUFS is far less as compared to spinning and

other segments of textiles. The reason is the haphazard growth of hosiery industry. The

hosiery manufacturers don’t have planned expansions and they buy small machines as

and when they have large orders and they required it. So there was no motive to avail

funds under TUFS scheme. The fund requirement at a time is not very large and can

arrange the same through internal accruals or from regular commercial banks. This is

why there are no large capacities the way these are in China and other parts of Far East

Asia or even in Bangladesh. My studies have shown that very few hosiery manufacturers

have expanded their capacities in planned manner.

7.5) Out of seventeen categories of ITC (HS) 61, four categories 6101, 6102, 6112 &

6113 are expected to show negative growth in next four years. Indian hosiery exporters

are not competitive enough in these four categories. Seven categories i.e. 6103, 6104,

6109, 6110 6111, 6114 & 6115 are star categories of Indian hosiery exports. These

categories are expected to grow at significant double digit growth rate. The performance

of Indian hosiery sector is largely dependent on these seven categories. Six categories i.e.

6105, 6106, 6107, 6108, 6116 & 6117 are expected to show either marginal (i.e. 2-3%) to

decent growth (i.e. 6-8%) but below ten percent for next four years.

7.6) Our study reveals that not all of hosiery exporters from Ludhiana are happy with

quota elimination. 60% respondents disagree and 35% agree with the statement that quota

elimination has come out to be good opportunity for them. It has posed various

challenges in front of them and they are struggling to get over these challenges. This is

. 287

because these hosiery units are not competitive to face the challenges. These units were

largely banking on the quota they were carrying and this ensured their performance

before quota elimination. But after quota elimination they were not able to perform. They

could not develop any competitiveness in pre-quota period and this cost them in the form

of less export sales in post quota period.

7.7) It has been found that a small portion of hosiery units are gainer from this

opportunity in true terms. Only 7% respondents have shown annual grown of 75% and

above, 14% have significantly grown at rate of above 50% but below 75%, 15%

respondents shows good signs of growth rate of above 25% but below 50%, 31% have

grown at decent growth of above 10% but below 25% and 20% have grown marginal rate

of below 10%. Also, 15% respondents registered negative growth rate. Difference in

growth rate is due to the adaptability of these hosiery units to the challenged posed by

quota elimination. In post quota period, the buyers are free to move to any nation and

there is no binding of quota. Therefore hosiery units have to be better than their

competitors to get orders.

7.8) Our study conclude that there is no correlation between attitude of hosiery

exporters towards quota limitation as opportunity and the actual growth exhibited by

them. The respondent’s views are independent of their own growth but cognitive and

based on strong deliberation and not influenced by their own growth biased. This is

proved through the results of correlation between respondents view on quota elimination

as an opportunity and average annual growth exhibited by hosiery manufacturers. The

. 288

correlation results exhibits weak correlation of 0.08. Also, 1-tail significance test value is

0.464 which more than p value of 0.025 (p>0.025), which means we can accept the null

hypothesis i.e. Ho(d): “the attitude hosiery exporters is not influenced by the actual

growth achieved” and reject the alternate hypothesis H1(d) i.e. the attitude hosiery

exporters is influenced by the actual growth achieved.

7.9) The findings of studies reveal that exporters who have performed better in past

are not expected to perform same in future. This is proved through testing the

respondent’s view on business now vis-à-vis business they had before quota elimination

and their expectation on future growth in next few years. The results show ‘p’ value (1-

tailed) is 0.327 which is higher that significance level of p=0.025, which is non-

significant. So null hypothesis Ho(e) i.e. “There is no relationship between past

performance and future performance or exporters who have performed in past may not

perform in future too” can be accepted and alternate hypothesis i.e. H1(e): “There is

relationship between past performance and future performance or exporters who have

performed well in past are expected to perform in future too” can be rejected

7.10) Large number of respondents doesn’t have any clear cut positioning strategy. 42%

respondents do not position them in any category. 19% position them low cost mass

producer, 18% as mid segment clothing company, 9% as premium clothing

manufacturers, 11% as niche market clothing company.

. 289

7.11) Sixteen activities undertaken to take advantage of this opportunity are clubbed

into four factor which are four strategies followed by the hosiery manufacturers. The four

strategies are - (a) Forward Integration, (b) Market and product development strategy, (c)

Backward Integration and (d) Expansion Strategy. The strategies are formed through

factor analysis of sixteen activities. There is no defensive activity used in significant way.

The Factor analysis is supported by the following test statistics:

i. Reliability test shows Chronbach’s Alpha value of 0.692

ii. KMO Value of 0.591

iii. Chi Square 827.5

All above statistics are within acceptable limits, therefore our scale and data are

fit for Factor Analysis.

7.12) Looking at the big opportunity the investment done on various activities by

Ludhiana hosiery manufacturers is not significant. This is being proved by Chi Square

test applied on the responses. The Chi-Square test value obtained is 919.26 which is

higher that the critical value of 25 and ‘p’ value is equivalent to zero. There fore null

hypothesis i.e. Ho(f): “looking at the big opportunity after quota elimination, the

investment done by hosiery manufacturer in various ways is substantial” can be rejected

and alternate hypothesis H1(f): “looking at the big opportunity after quota elimination,

. 290

the hosiery exporters have not done substantial investment in various ways” can be

accepted.

7.13) Ludhiana hosiery industry is not able to develop any competitive advantage.

There are fragmented strengths associated with hosiery units and does not project

Ludhiana as international centre of hosiery production because there is no clear evidence

of any competitive advantage. 5% respondents project good quality as their superior skill,

8% wide range of production, 15% as fast product development capability, 9% ontime

delivery, 17% as low cost of production, 9% as pre-sale and after sale service, 3%

production technology, 6% as skilled labor, 9% as large production capacities, 4% as

close association with buyers, 8% as financial strength, 3% as well established name

among foreign buyers and 5% none. It is obvious Ludhiana hosiery industry is not going

anywhere from here.

7.14) Knitting/fabric production is the core competence in hosiery industry since it is

the basis of widest range of product offerings. 52% respondents believe fabric production

is the most important process in hosiery unit. Also there are others sources of core

competence. Second most important process is garmenting as 17% respondents favors it

as core competence. Spinning is the third most favored process as this reduces the cost

and provide good quality yarn that would help produce good quality end product at less

cost.

. 291

7.15) For Future growth, Ludhiana hosiery manufacturers have to keep their pricing

stable. 40% respondents are of opinion that pricing would play decisive role for future

growth as the competition from domestic and international market will increase and

foreign buyers would always seek pricing as one of the most important element while

selecting vendor. 31% respondents are of opinion that they have to expand horizontally

and develop new product range to grow in times to come as competition will increase and

new products development would be key to survival. 18% are of opinion that they would

enter new markets with existing product range and 10% would prefer to expand in the

current markets with existing product lines.

7.16) Ludhiana hosiery industry caters wide range of products. Almost all segments are

produced. 20% produce garments as per customer specifications only. 15% produce gents

wear clothing, 16% teenage boys clothing, 12% produce kids wear clothing, 17% women

wear clothing, 14 produce teenage girls clothing and 4% other than these categories.

7.17) Most widely sales channels used are through agents and direct dealing with

overseas buyers. 42% respondents use buying agencies or buying houses to sell their

products in international markers, while 21% directly deal with buyers and 33% use both

of the channels. There are very few (only two) hosiery producers having their own retail

shops or other sales channels. Also only two respondents sell their products as branded

one. Almost all units produce for overseas brands and put label as desired by overseas

buyer. There is no brand building effort from any of the hosiery producer.

. 292

7.18) The study reveals that there is no uniform pricing policy prevailing among

Ludhiana hosiery exporters. They use multiple pricing techniques. 20% are of opinion

that international prices determine the price and their power to dominate the price is very

minimal. 22% respondents prefer to negotiate price at the time of confirmation of new

order, 9% follows long term pricing for multiple seasons, 5% work on transparency with

overseas buyer on costing, 23% are opportunist and quote price based on order booking

in hand and 21% do not follow any of above. Cost of the product is the basis of pricing

technique. Above this everything is negotiable. Duty drawback is essential element of

pricing policy.

7.19) Promotional channels used are very conventional and no hybrid promotional

channels are used. Most widely used promotional channel are dealing with buyers to

promote product, participation in trade fairs, though buying houses and Export promotion

cells which are conventional but very effective and low cost in nature. Mass media

communication channels are not used because there is no effort to create brands.

7.20) The promotion budgets are not very high. Only 3% respondents have annual

promotion budget of above 6 lacs but below 7.5 lacs, 12% have promotional budget of

above 4.5 lacs but below 6 lacs, 17% have promotional budget of above 3 lacs but below

4.5 lacs, 27% respondents have promotional budget of above 1.5 lacs but below 3 lacs

and 41% respondents have budget below 1.5 lacs which is marginal. The major part of

this promotion budget goes into abroad visit to meet customers and participation in trade

. 293

fairs. Rest is allocated in other promotional materials like catalogues which constitute a

small portion of it.

7.21) International certification is not very popular among Ludhiana hosiery exporters.

They have just not realized the need of it and latent benefits associated with it. Only 15%

respondents are having or in process of having Social Audit i.e. SA8000 certification.

Also there is no scheme from state government and centre government to promote

international certification among the hosiery products exporters.

7.22) Hosiery prices are likely to rise in future. 48% respondents are of opinion that

prices of hosiery products will rise in near future, 21% expect it to come down further

and of opinion that as more countries like Morocco and Tunisia are becoming new

centers of garment production, the prices will come down further and 31% respondents

are of opinion that prices are already at rock bottom and will remain almost same and

would not at least come down if do not increase.

7.23) Export promotions schemes run by government to promote the export of hosiery

products from country, are not equally successful. TUFS is not very popular among

Ludhiana hosiery exporters. 46% respondents are of view that TUFS has not been able to

modernize the hosiery industry while 26% stand by policy and 28% have kept their views

reserved on this. While EPCG is not very popular. Integrated Textile Part (ITP) is

expected to be very successful. Ludhiana hosiery industry has high hopes from this

. 294

upcoming ITP near Ludhiana. Duty draw back is only cash incentive. Packing credit and

post shipment credit are very popular.

7.24) One of the main reasons of lacking behind of hosiery industry in availing the

funds under TUFS is haphazard growth of hosiery industry. 65% respondents agree with

the statement that Ludhiana hosiery has grown in haphazard way because of which their

requirements were not considerable because of which it could not get popularity among

hosiery producers. Other reasons are interest subvention is not very high and 3 to 4%

interest differential is not very substantial when funds requirement is not very high. But

this interest differential is substantial when requirement is very high for example as in

case of spinning industry where funds requirement is very high, TUFS is most successful.

7.25) Poor productivity level is the weakest link in the entire value chain as 25%

respondents rate poor productivity the major bottleneck in the growth of hosiery industry.

First the labor is not easily available and which is available, their skills are not updated

and productivity levels are not upto the mark. Second weakest link is the high cost of

electricity. Third weaker link in the value chain is the outdated processing technology

available in Ludhiana hosiery cluster.

7.26) Substantial numbers of shipments are not delivered from Ludhiana on time as

93% respondents support this view. This is due to various reasons - improper planning,

poor infrastructure, poor capacities, and poor worker’s productivity. While 65%

respondents are of opinion that competitor country has better record of on-time shipment

. 295

than India. This is one of the major drawbacks of exports from Ludhiana. Most of the

shipments are delayed while competitors are shipping even larger quantities on time.

7.27) Poor infrastructure is the one of the most ailing element in the fast execution of

export shipments as 91% respondents support this view. This can be supported with

applying Chi Square on respondent’s view on India’s performance on on-time shipment,

respondent’s view on-time delivery of competitor countries and poor infrastructure of

India, the ‘p’ value obtained is 6.65E-0.06 (equivalent to 0.00000665) which is almost

zero and is significant at 5% significance level Therefore we have significance evidence

to reject null hypothesis i.e. Ho(g): “Indian physical infrastructure is sufficient to support

the fast execution of export shipments” and alternate hypothesis i.e. H1(g):“Indian

physical infrastructure is not sufficient to support the fast execution of export shipments”

can be accepted. Hence we have enough evidence to write that India’s physical

infrastructure is poor and not sufficient to support the fast execution of export shipments.

7.28) Ludhiana hosiery workers are not very skilled. 15% respondents rate their skills

as raw, 27% rate them as at learning stage, 33% as moderately skilled, 18% skilled and

7% as highly skilled. It is evident that most of the respondents rate them under skilled

and not upto the mark.

7.29) Ludhiana hosiery workers are not as skilled as its competitor country like China

and Bangladesh. 32% respondent rate local workers as poor when compared to its

competitor’s country, 32% rate those somewhat poor, 30% as equivalent, and 11%

. 296

somewhat better. We can conclude that Ludhiana hosiery workers are not skilled through

applying Chi Square test on respondents view on skills level and their skill level as

compared to its competitor countries, we get ‘p’ value is 0.001154 which is less than

significance level of 0.05. Also critical value is less than test statistics. Therefore we have

substantial evidence to reject null hypothesis i.e. Ho(h): “Hosiery workers employed in

Ludhiana hosiery industry are as skillful as employed in competitive countries” can be

rejected and alternate hypothesis i.e. H1(h): “Hosiery workers employed in Ludhiana

hosiery industry are not as skillful as employed in competitive countries” can be

accepted.

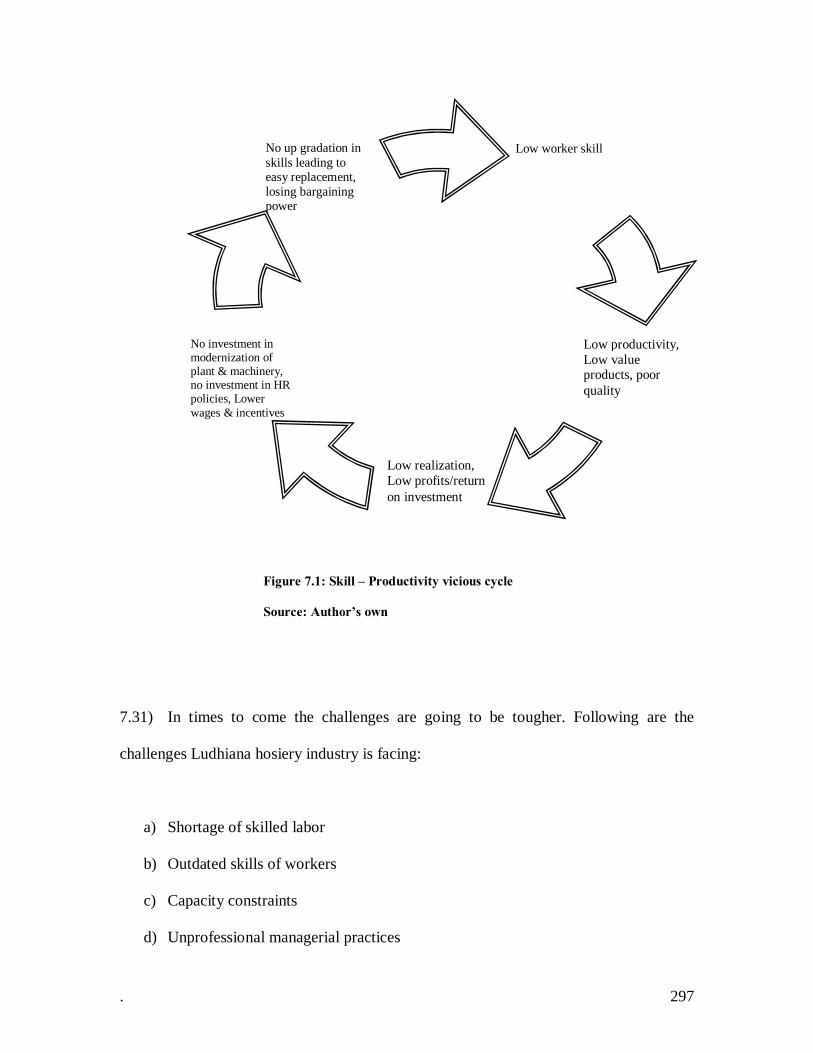

7.30) Low level of skills of workers has significant impact on earnings of both workers

and firm. This is like a vicious cycle. Low skilled worker in an organization will lead to

low productivity, low quality and low value products which will further lead the firm

towards low competitiveness and low returns on investment. This in turn will lead the

company’s apathy towards investment in HR development, updating its methods of

production, technology upgradation. Also, comparative wages, incentives and other

benefits will be lesser. This will also generate sense of mistrust among firm owners and

workers too. This is like vicious cycle as shown in figure 7.1. Eventually the organization

will remain in the vicious cycle of low productivity, low quality of output and low value

output.

. 297

Figure 7.1: Skill – Productivity vicious cycle

Source: Author’s own

7.31) In times to come the challenges are going to be tougher. Following are the

challenges Ludhiana hosiery industry is facing:

a) Shortage of skilled labor

b) Outdated skills of workers

c) Capacity constraints

d) Unprofessional managerial practices

Low worker skill

Low productivity, Low value products, poor quality

Low realization, Low profits/return on investment

No investment in modernization of plant & machinery, no investment in HR policies, Lower wages & incentives

No up gradation in skills leading to easy replacement, losing bargaining power

. 298

e) Infrastructure bottleneck

f) Cost of utilities

8.0 CONCLUSION

Ludhiana hosiery industry has come of age. But in the recent past the problems for

Ludhiana hosiery industry has increased many folds. There has been significant increase

in investment from hosiery manufacturers but it is not as large as expected in the wake of

quota elimination. The sizes of units have not increased to the extent. Small scale units

are not converted to medium scale; rather there is marginal increase in their capacities.

It is obvious from discussion so far done in this chapter that the most of the

problem revolves around the productivity, skills and management style. Hosiery units are

small scale family managed firms having age old management style where lack of trust

rules. Neither management has trust on workers nor do the workers have trust on

management. There exists a kind of compromise between them while none can survive

without other. Management style is like this because the units are small and neither

specialist management practitioners are required to manage such small capacities. They

hesitate to expand due to unavailability of skilled workers. Neither they are ready to

invest on the skills of the workers because of fear of loosing the workers if they become

skilled - would ask for more compensation affecting their profitability and

competitiveness in the international market. Workers are not in position of investing in

. 299

their skill enhancement and only the way they have is to learn at the workplace. Industrial

relations are virtually non-existing in Ludhiana hosiery industry.

There is absolute lack of enthusiasm among the Ludhiana hosiery producers to do

something big when such large opportunities are waiting for them. There is definite lack

of confidence and harmony among different producers. They are not confident to create

their own brands despite financially they are better off and can invest in such activities.

They have not understood the value of brand and its long term dividends. The fear of loss

of competitiveness is there. China is dominating the international markets. But now it is

concentrating more on value added products and leaving the commodity ones which are

becoming the bread and butter for Ludhiana hosiery producers. This way also Ludhiana

hosiery producers are losing its competitiveness of producing high value added products

and killing their own capabilities.

Second, the most prominent problem existing for Ludhiana hosiery industry is of

infrastructure – be it the problem of scarcity and cost of electricity, distance from sea

port, unavailability of frequent freight trains, congestion at the port or procedural hassles

at different levels, there is definitely lack of coordination and commitment from

government department who provide vital support services to promote the export from

country. There is definite need to provide single window for all logistic problems.

Although private participation is initiated in this direction but results are awaited and can

only hope for better future prospects.

. 300

9.0 SUGGESTIONS

After thorough study of various aspects on the problem in hand, finally I arrive at the

following suggestions to improve the competitiveness of hosiery industry in international

market.

9.1 Skills enhancement: For the growth of Ludhiana hosiery industry there is

desperate need to (a) enhance the skill level of workers already working in this industry

and (b) increase the supply of skilled workers (c) enhance the managerial skills.

In order to increase the skills level of the workers, there is definite need of few hi-

tech training institute. There is already one Apparel Training and Design Centre (ATDC)

for workers training. This institute runs various courses for inexperienced and for

experienced workers. But all are paid programs and substantial fee is charged by ATDC

for these programs.

Workers already employed in some hosiery units may afford to get training from

them but inexperienced migrated labor belonging to a very poor family may not afford to

pay for such courses. For such workers few fresher courses should be started free of cost.

Ministry of textiles, centre government and state government should bear the burden of

training these raw laborers and convert them into human resource and productive assets.

This will fill the gap between demand and supply of workforce. Once these workers

become employable in hosiery units and start earning, they will start believing in these

. 301

training programs and once this confidence is developed among these workers, they will

further approach for skills enhancement and skills upgradation. Also they will bring rope

in more workers to join hosiery worker as their profession. Once this stream of workers is

available, hosiery units would restart investing and would expand their activities. This

would change the whole scenario of stagnating fresh investment in Ludhiana hosiery

industry.

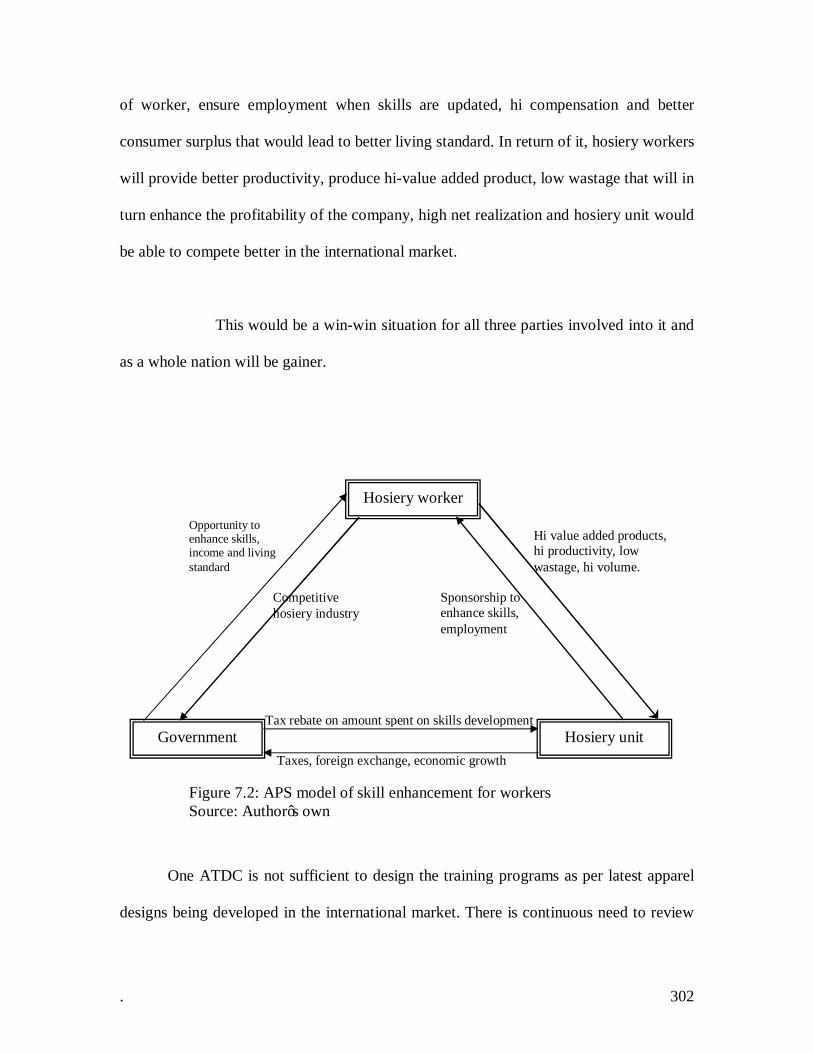

Looking at the desperate need of skill enhancement among hosiery workers,

government should encourage hosiery units to provide sponsorship to workers and cost of

training should be allowed to recover in the form of tax rebate. For this a model is

proposed as given in APS‡ model for skill enhancement of hosiery workers as given in

figure 7.2. This is the model developed based on the specific needs identified during this

research.

Hosiery unit will identify the workers and skills that need to be inculcated among

workers. The initial sponsorship will be paid by hosiery unit which it should be allowed

to cover in the form of tax rebate from government. This will ensure its payback to

hosiery unit in case the worker/s leaves the job and join other hosiery unit at higher

salary. In return of it, hosiery unit earn foreign exchange, pays other taxes and participate

in national economic growth. Government will give up a portion of tax collection but in

return of it, foreign exchange inflows will increase, national productivity increases and a

competitive hosiery industry would developed in the country that would ensure long term

sustainability and its contribution in economic growth. This will also increase the income ‡ APS model is given by the author of this thesis which is short form of his name.

. 302

of worker, ensure employment when skills are updated, hi compensation and better

consumer surplus that would lead to better living standard. In return of it, hosiery workers

will provide better productivity, produce hi-value added product, low wastage that will in

turn enhance the profitability of the company, high net realization and hosiery unit would

be able to compete better in the international market.

This would be a win-win situation for all three parties involved into it and

as a whole nation will be gainer.

One ATDC is not sufficient to design the training programs as per latest apparel

designs being developed in the international market. There is continuous need to review

Hosiery worker

Competitive hosiery industry

Opportunity to enhance skills, income and living standard

Hi value added products, hi productivity, low wastage, hi volume.

Sponsorship to enhance skills, employment

Tax rebate on amount spent on skills development Government

Taxes, foreign exchange, economic growth

Hosiery unit

Figure 7.2: APS model of skill enhancement for workers Source: Author’s own

. 303

and update the course content as per market requirement. It needs more professional

approach. There fore there is definite need that hosiery manufacturing associations should

come forward and participate actively in such initiatives. There are already few

associations working in Ludhiana like Knitwear Club, APPEAL, which are association

created by hosiery manufacturers. It is recommended that some of these associations may

set up a training centre with 50 machines and qualified trained instructor from NIFT with

specialization in production management may be hired to train workers. The members

should identify the training needs of their workers and should nominate and sponsor the

workers for these training programs. On completion of training successfully, they should

be awarded with certificate of training. The hosiery units should recognize and approve

this training institute and curriculum of training. Workers who have attended these

training programs should be given preference. With this both workers and hosiery units

will be benefited. The benefits to the hosiery units will be in the form of availability of

skilled workers. Hosiery units then would be confidently able to take orders of high value

added products which are so far given to companies of Korea, Hong Kong and Vietnam.

The same quality of hosiery products can be produced in India if the skilled workers are

available. Also, workers are able to take on these products and their earnings will also

increase considerably. Also, foreign buyers will be more confident with these kinds of

training programs and their confidence in Ludhiana hosiery industry will increase.

To enhance the managerial skills among the management, merchandisers and

production heads, Universities should join hands with hosiery association. Normally

hosiery units never entertain any initiative from any university or researcher. Hosiery

. 304

association should rather join hands with researchers and academicians from universities

in identifying the skill gap and ensure the gap is filled as soon as possible.

Ludhiana Hosiery industry desperately needs to understand how to develop core

competence and competitive advantage in them. This will help them bring out good

product mix into the market and will increase their confidence in building their own

brands in international markets. Also, they need to update their skills in CAD base

garment designing, understanding lifetime value of customer and customer relationship

management which is becoming the decisive factor in export marketing today.

9.2 Joint Marketing Effort: there is desperate need to establish Ludhiana as a brand

known for hosiery production. As discussed earlier Ludhiana hosiery sector is dominated

by small scale industries and their promotional budgets are marginal. There

manufacturers don’t have capacities to promote themselves as individual brand but

together they can contribute towards this and Ludhiana as a brand can be established

globally. Ludhiana is already known for hosiery production but in a fragmented way.

Quality standards are fragmented, capacities are fragmented and individually represented.

If a collective effort is put, it can bring Ludhiana as Hosiery Cluster of international

standard. For this purpose hosiery associations have to play vital role. All members

should contribute towards the functioning of the organization and establishing sufficient

infrastructure for the same. The model is further discussed in detail in thesis.

. 305

9.3 Individual approach for each cluster: Each textile cluster has its own problems.

Textile ministry should tackle these problems individually. For example for Tirupur

hosiery industry, seaport is not an issue because it is just few hours away from it, but for

Ludhiana it is the major problem because it is minimum six days away from it. For

Ludhiana hosiery there must be at least one train everyday to support the fast execution

of export shipment. Textile ministry should look into the problems of individual cluster

separately instead of having generalized policy on pan India basis. This will dilute the

purpose and sometimes might even clash with other policies because of which

implementation are not affective to support the desired industry.

9.4 Encouragement to Integrated Textile Parks: Government should encourage

more integrated textile parks and especially for hosiery industry which is prominent in

Ludhiana. It must contain all necessary infrastructures along with labor housing project to

provide housing solution to migrated workforce working in Ludhiana.

9.5 Ensure power supply: State government should ensure uninterrupted supply of

electricity to these textile parks. For this state government may invite private players for

power generation and distribution. This will ensure continuous supply to industry and

government can concentrate on domestic and agriculture sector. Also, power theft is very

high in industry. State government can shed off this segment and give it to private

players. There are various power generation companies in India who can do this job and

sometimes the tariff is even lesser than government tariffs due to better management

practices.

. 306

9.6 FDI: Foreign direct investment should be allowed through automatic route in

knitting/hosiery sector. This is must for upliftment for this industry. Although inviting

FDI in hosiery sector would not be an easy task. Indian infrastructure is too poor to build

confidence in overseas investors.

9.7 Encouragement to international certification: International certification or

textile industry is going to be compulsion in times to come. In order to export textile

products to Europe and US, it is likely to be must to have certain international

certification. Ministry of textile must encourage hosiery units or rather whole textile

industry to obtain these international certification. This will build confidence in overseas

buyers on compliance of various sensitive issues. Ministry of textile should constitute an

agency of international repute to provide complete package on consultancy, audit and

certifications.

9.8 Exchange risk: There must be a series of awareness programs among hosiery

producers on various hedging tools and techniques to cover transaction risks and ensure

safeguard from exchange rate fluctuation. Banks could be major participant in this

program. This will help exporters enter into long term agreements and provide price

stability which is must in international trade.

9.9 Capacity building: Ludhiana hosiery exporters should build new capacities in

order to cater large orders and fulfill them in time. Partially production can be increased

. 307

through enhancing worker’s skills and rest is to be done with capacity expansion. Major

investment is needed in hosiery fabric production and processing. There is no constrains

of funds from financial institutions therefore large projects can be easily planned and got

sanctioned.

9.10 Improvement in management practices: Although it is too early to expect from

Ludhiana hosiery industry to adopt some of the latest management practices like LEAN

manufacturing, it is advised that they should gear up for the same because garment

companies in Far East Asian countries have adopted these practices and got tremendous

success in bringing down the cost of production.

9.11 Concentration on domestic market: Although most of the hosiery

manufacturers and exporters have their domestic brands but their prime interest is

exports. In domestic market they prefer to sell only surplus and rejections. But they

should be serious about the domestic market. Indian domestic market is vast enough and

all global brands are setting up their shops in India. The hosiery producers should use

domestic market as their strategic place and should sell only branded products with

international quality. This will give them dividends in long term and save them from

global economic turmoil.

9.12 Be innovative, service oriented and quality conscious: Ludhiana hosiery

manufacturers need to concentrate on three basic principles of international marketing –

First to be innovative in product and production techniques. This is the greyest area of

. 308

Indian hosiery industry. They need to be more innovative and start designing new product

mix right from the yarn stage. They must learn the chemistry of colors combinations,

adopt designs from nature, understands themes of designs which are hot topics these days

for designers. International designers do not speak the language of designs; but of themes

and follow the nature. Then they must respond at the speed of electricity so that

customers feel attended and must get your attention. Then third is the quality

consciousness. Manufacturers must consider the retail price at which this garment will be

sold to ultimate consumer and not the price at which they are selling it to retailer. There is

huge difference in the retail price and garment buying price. Most of times the price of

garment at which garment is sold to retailer are mere forty percent or less than the retail

price at which it is sold to consumer. The consumer must get value for money he/she is

paying for it and it must be delivered through delivering optimum quality standards.

10.0 LIMITATIONS OF THE STUDY

Although due time and efforts were put to make this dissertation a success, but there are

few areas where few uncontrollable constraints evolved which are recorded as limitations

of the study. These are as discussed below:

10.1 The biggest limitation of the study was to collect the information from the

respondents. Respondents were not enthusiastic to participate and convincing

them to share the information was not an easy task. Pre-appointment with

respondent was must and on many occasions despite the fixed appointment the

. 309

respondents were not available or refused to interact due to some reasons. So it

required lots of efforts to reach them.

10.2 Second problem faced was the lack of literature. There is so such study done on

Ludhiana hosiery sector before it. So there were no evidence on the structure and

functioning of such units, problems and variables prevailing among Ludhiana

hosiery industry.

10.3 Due to specific knowledge required to get the questionnaire filled, no researcher

could be hired to facilitate the data collection process.

10.4 Most of the responders were looking at the problem as individual hosiery

producer and not as part of the collective industry which required the

interventions at the various occasions and that lead to change in the natural

response of respondent. This intervention lead to bias or removed bias is still a

question mark.

10.5 Distance was also one of the key barriers in the data collection.

11.0 AGENDA FOR FURTHER RESEARCH

Further research is needed in the following areas:

. 310

a) Methods of training an evaluation of training programs.

b) Impact of training on productivity, income levels and lifestyle of workers.

c) Impact of training on growth of organization.

d) Methods of training for middle level and top level executives of the hosiery

manufacturing companies.

e) Study the impact of Joint marketing effort on the growth of Ludhiana hosiery

industry

f) Impact of training on Forex management practices of hosiery manufacturing

companies.