Embed Size (px)

Citation preview

Anjum Asim Shahid RahmanCHARTERED ACCOUNTANTS

Grant Thornton

Auditors’ Report to the Members

a) in our opinion, proper books of account have been kept by the Bank as required by the Companies Ordinance, 1984(XLVII of 1984) and the returns referred to above received from the branches have been found adequate for the purposesof our audit;

b) in our opinion:

We have audited the annexed balance sheet of SME Bank Limited (the “Bank”) as at December 31, 2007 and the relatedprofit and loss account, statement of changes in equity and cash flow statement, together with the notes forming partthereof (here-in-after referred to as the ‘financial statements’) for the year then ended, in which are incorporated theunaudited certified returns from the branches and other offices except for six branches and one treasury office which havebeen audited by us and we state that we have obtained all the information and explanations which, to the best of ourknowledge and belief, were necessary for the purposes of our audit.

It is the responsibility of the Bank’s Board of Directors to establish and maintain a system of internal control, and prepareand present the financial statements in conformity with approved accounting standards and the requirements of theBanking Companies Ordinance, 1962 (LVII of 1962), and the Companies Ordinance, 1984 (XLVII of 1984). Ourresponsibility is to express an opinion on these statements based on our audit.

We conducted our audit in accordance with the International Standards on Auditing as applicable in Pakistan. Thesestandards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statementsare free of any material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts anddisclosures in the financial statements. An audit also includes assessing the accounting policies and significant estimatesmade by management, as well as, evaluating the overall presentation of the financial statements. We believe that our auditprovides a reasonable basis for our opinion and after due verification, which in case of loans and advances covered morethan sixty percent of the total loans and advances of the Bank, we report that:

(iii) the business conducted, investments made and the expenditure incurred during the year were in accordance withthe objects of the Bank and the transactions of the Bank which have come to our notice have been within the powers ofthe Bank;

(i) the balance sheet and profit and loss account together with the notes thereon have been drawn up in conformitywith the Banking Companies Ordinance, 1962 (LVII of 1962), and the Companies Ordinance, 1984 (XLVII of 1984) andare in agreement with the books of account and are further in accordance with accounting policies consistently applied.

(ii) the expenditure incurred during the year was for the purpose of the Bank’s business; and

c) in our opinion and to the best of our information and according to the explanations given to us the balance sheet,profit and loss account, statement of changes in equity and cash flow statement together with the notes forming partthereof conform with the approved accounting standards as applicable in Pakistan and give the information required by theBanking Companies Ordinance, 1962 (LVII of 1962) and the Companies Ordinance, 1984 (XLVII of 1984), in the mannerso required and give a true and fair view of the state of the Bank’s affairs as at December 31, 2007 and its true balance ofthe profit, its changes in equity and cash flows for the year then ended; and

d) in our opinion Zakat deductible at source under the Zakat and Ushr Ordinance, 1980 (XVIII of 1980), wasdeducted by the Bank and deposited in the Central Zakat Fund established under section 7 of that Ordinance.

ANJUM ASIM SHAHID RAHMAN.

Chartered Accountants

Islamabad

Date:

Without qualifying our opinion, we draw attention to contents of note 6 to the financial statements on financialrestructuring of the Bank.

The financial statements of the Bank for the year ended December 31, 2006 were audited by A.F. Ferguson & Co.,Chartered Accountants, who had expressed an unqualified opinion on those financial statements vide report dated March01, 2007.

SME Bank LimitedBalance Sheet as at December 31, 2007

Note 2007 2006Rupees in '000

ASSETSCash and balances with treasury banks 7 286,705 311,954 Balances with other banks 8 52,980 125,704 Lendings to financial institutions 9 258,944 292,454 Investments 10 3,058,130 5,566,582 Advances 11 2,118,347 1,731,271 Operating fixed assets 12 144,589 156,384 Deferred tax assets 13 447,887 447,794 Other assets 14 216,176 992,735

6,583,758 9,624,878

LIABILITIESBills payable 15 40,441 18,090 Borrowings from financial institutions 16 1,400,000 2,600,000 Deposits and other accounts 17 1,879,587 1,666,360 Sub-ordinated loans - - Loan from State Bank of Pakistan 18 - 2,430,000 Liabilities against assets subject to finance lease 19 25,371 19,697 Other liabilities 20 429,752 602,819

3,775,151 7,336,966 NET ASSETS 2,808,607 2,287,912

REPRESENTED BY

Share capital/ Head office capital account 21 2,392,507 2,000,000 Reserves 199,356 177,275 Unappropriated profit 297,418 209,096

2,889,281 2,386,371 (Deficit) on revaluation of investments 22 (80,674) (98,459)

2,808,607 2,287,912

CONTINGENCIES AND COMMITMENTS 23

The annexed notes 1 to 43 form an integral part of these financial statements.

President/Chief Executive Director Director Director

SME Bank LimitedProfit and loss accountfor the year ended December 31, 2007

Note 2007 2006Rupees in ‘000

24 875,560 960,29325 379,956 454,062

Net mark-up/ interest income 495,604 506,231Reversal of provision against non-performing loans and advances 11.4 (104,643) (217,499)Provision/(reversal) for diminution in the value of investments 10 4 804 (16 415)

Mark-up/return/interest earnedMark-up/return/interest expensed

Provision/(reversal) for diminution in the value of investments 10.4 804 (16,415)Reversal of provision in value of other assets (37,466) - Bad debts written off directly 11.5 3,780 1,245

(137,525) (232,669)Net mark-up/ interest income after provisions 633,129 738,900

F i i d b k i

NON MARK-UP/INTEREST INCOME

Fee, commission and brokerage income 3,608 2,591Dividend income 1,013 1,173Gain on sale of securities 25,646 - Other income 26 10,071 23,046Total non-markup/interest income 40,338 26,810

673,467 765,710

NON MARK UP/INTEREST EXPENSES

Administrative expenses 27 526,464 553,867Reversal of other provisions/write offs 14.3 (5,910) (20,000)Other charges 28 819 158Total non-markup/interest expenses 521,373 534,025

152 094 231 685PROFIT BEFORE TAXATION

NON MARK-UP/INTEREST EXPENSES

152,094 231,685Taxation - Current 29 50,863 72,034 - Deferred 29 (9,172) 6,464

41,691 78,498110,403 153,187

Unappropriated/unremitted profit brought forward 209,096 586,546Profit available for appropriation 319,499 739,733

PROFIT AFTER TAXATION

PROFIT BEFORE TAXATION

30 0.48 0.77

The annexed notes 1 to 43 form an integral part of these financial statements.

Basic/ diluted earnings per share- Rupees

President/Chief Executive Director Director Director

SME Bank LimitedCash flow statementfor the year ended December 31, 2007

Note 2007 2006

Rupees in '000'CASH FLOW FROM OPERATING ACTIVITIES

Profit before taxation 152,094 231,685 Less: Dividend income (1,013) (1,173)

151,081 230,512 Adjustments Depreciation 30,046 30,153 Amortization 3,264 3,034 Reversal of provision against non-performing loans and advances (104,643) (217,499) Provision/(reversal) for impairment in value of investments / other assets (36,662) (36,415)

Other provisions/write offs (5,910) 3,780 1,245

Net profit on sale of property and equipment (405) (11,956) Finance charges on leased assets 1,068 743

(109,462) (230,695) 41,619 (183)

(Increase)/ decrease in operating assets Lendings to financial institutions (166,490) (92,454) Advances (286,213) (330,173) Other assets 814,019 14,896

361,316 (407,731) Increase/ (decrease) in operating liabilities Bills payable 22,351 11,819

Bad debts written off directly

Borrowings from financial institutions (1,200,000) 1,070,000 Deposits 213,227 643,658 Other liabilities (excluding current taxation) (120,664) 31,058

(1,085,086) 1,756,535 (682,151) 1,348,621

Income tax paid (98,797) (117,370) Net cash flow from operating activities (780,948) 1,231,251

CASH FLOWS FROM INVESTING ACTIVITIES

Net investments in available-for-sale securities 1,324,025 (75,306) Net investments in held-to-maturity securities 1,210,520 (712,179) Net investments in subsidiary - (15,457) Dividend income 1,013 1,173 Investments in operating fixed assets (9,004) (29,533) Sale proceeds of property and equipment disposed-off 1,904 18,007 Net cash flow from investing activities 2,528,458 (813,295)

CASH FLOWS FROM FINANCING ACTIVITIES

Payment of loan to State Bank of Pakistan (2,430,000) (70,000) Issue of Share capital 392,507 - Payments of lease obligations (7,990) (10,805) Net cash flow from financing activities (2,045,483) (80,805)

(Decrease)/Increase in cash and cash equivalents (297,973) 337,151 Cash and cash equivalents at beginning of the year 31 637,658 300,507 Cash and cash equivalents at end of the year 31 339,685 637,658

The annexed notes 1 to 43 form an integral part of these financial statements.

______________________ President/Chief Executive Director Director Director

SME Bank LimitedStatement of changes in equity

for the year ended December 31, 2007

Share capital Statutory Unappropriated Totalreserve profit/(loss)

Balance as at January 01, 2006 1,500,000 146,638 586,546 2,233,184

Net profit for the current Year - - 153,187 153,187

Transfer to Statutory reserve - 30,637 (30,637) -

Issue of share capital 500,000 - (500,000) -

Balance as at December 31, 2006 2,000,000 177,275 209,096 2,386,371

Net profit for the current Year - - 110,403 110,403

Transfer to Statutory reserve - 22,081 (22,081) -

Issue of share capital 392,507 - - 392,507

Balance as at December 31, 2007 2,392,507 199,356 297,418 2,889,281

The annexed notes 1 to 43 form an integral part of these accounts.

President/Chief Executive Director Director Director

Rupees in '000

SME Bank Limited

Notes to the Financial Statements

for the year ended December 31, 2007

1. GENERAL INFORMATION

1.1

1.2 Amalgamation of defunct RDFC and SBFC

2. BASIS OF PRESENTATION

SME Bank Limited (the Bank) is a public limited company incorporated in Pakistan on October 30, 2001 underthe Companies Ordinance, 1984 having its registered office at 40-Jang Building, Fazal ul Haq road, Blue area,Islamabad. The Bank obtained its business commencement certificate on April 16, 2005 which became effectivefrom the date of its issue. The Bank is now a Scheduled Commercial Bank engaged in the business of bankingwith the primary objective to support and develop SME sector in Pakistan by providing necessary financialassistance and business support services on a sustainable basis. The Bank is operating through a network of 27branches including 13 Commercial banking branches. Based on the latest credit rating report dated February 22,2007 issued by JCR-VIS Credit Rating Company Limited, credit rating of the Bank was BBB (triple B) in the longterm and A - 2 (A two) in the short term.

The Federal Government promulgated the Regional Development Finance Corporation (RDFC) and SmallBusiness Finance Corporation (SBFC) (Amalgamation and Conversion) Ordinance, 2001 (the Ordinance 2001)setting forth the mechanism of amalgamation of defunct RDFC and SBFC. Both these entities were DevelopmentFinancial Institutions (DFIs). In pursuance of the Ordinance 2001, Finance Division, Ministry of Finance issuedan Order (SRO (1) 2001) dated December 29, 2001 setting forth the scheme of amalgamation of RDFC andSBFC with the Bank effective January 1, 2002. Pursuant to this scheme entire assets and liabilities of defunctRDFC and SBFC as at December 31, 2001 were transferred to the Bank at fair value. These two institutions standdissolved and ceased to exist effective January 1, 2002. The Bank allotted its shares to the share holders ofdefunct RDFC and SBFC in proportion to their shareholding therein based on the fair net assets value of defunctRDFC and SBFC on December 31, 2001.

Further, pursuant to clause 6 of the Ordinance 2001, notwithstanding anything contained in any other law for thetime being in force, the Bank shall take and maintain existing deposits, continue lending and any other businesswhich were being undertaken by defunct RDFC and SBFC, respectively, without prejudice to SBP permission forcommencement of banking business.

These financial statements have been prepared in accordance with the requirements of BSD Circular No 4 datedFebruary 17, 2006 issued by SBP.

In accordance with the directives of the Federal Government regarding the shifting of the banking system toIslamic modes, the State Bank of Pakistan has issued various circulars from time to time. Permissible forms oftrade-related modes of financing include purchase of goods by banks from their customers and immediate resaleto them at appropriate mark-up in price on deferred payment basis. The purchases and sales arising under thesearrangements are not reflected in these financial statements as such but are restricted to the amount of facilityactually utilized and the appropriate portion of mark-up thereon.

SME Bank Limited

Notes to the Financial Statements

for the year ended December 31, 2007

3 STATEMENT OF COMPLIANCE

3.1

3.2 Standards not yet adopted by State Bank of Pakistan

3.3

i)

ii)

iii)

iv)

v)

vi)

vii)

Revised IAS 1 - Presentation of financial statements (effective for annual periods beginning on or after January 1,

Revised IAS 23 - Borrowing costs (effective from January 1, 2009).

IFRIC 11 - IFRS 2 - Group and Treasury Share Transactions (effective for annual periods beginning on or after

IFRIC 12 - Service Concession Arrangements (effective for annual periods beginning on or after January 1, 2008).

IFRIC 13 - Customer Loyalty Programmes (effective for annual periods beginning on or after July 1, 2008).

IFRIC 14 - IAS 19 - The limit on Defined Benefit Asset, Minimum Funding Requirements and their interaction.

These financial statements are prepared in accordance with approved accounting standards as applicable inPakistan and the requirements of the Companies Ordinance, 1984, the Banking Companies Ordinance, 1962 andthe directives issued by SECP and SBP. Approved accounting standards comprise of such InternationalAccounting Standards as notified under the provisions of the Companies Ordinance, 1984. Wherever therequirements of the Companies Ordinance, 1984, the Banking Companies Ordinance, 1962 or directives issued bySECP and SBP differ with the requirements of these standards, the requirements of the Companies Ordinance,1984, the Banking Companies Ordinance, 1962 or the requirements of the said directives take precedence.

In terms of BSD circular letter No. 10 dated August 26, 2002, the SBP has deferred the applicability ofInternational Accounting Standard (IAS) 39, 'Financial Instruments: Recognition and Measurement' andInternational Accounting Standard (IAS) 40, 'Investment Property' for Banking Companies through BSD CircularLetter No. 11 dated September 11, 2002. Accordingly, the requirements of these standards have not beenconsidered in the preparation of these financial statements. However, investments have been classified and valuedin accordance with the requirements prescribed by the State Bank of Pakistan through various circulars.

IFRS 8 - Operating segments (effective for the periods beginning on or after January 1, 2009).

IFRS 8 - Operating segments will supersede IAS 14 Segment Reporting. The adoption of IFRS 8 may only impactthe extent of disclosures.

Standards, interpretations and amendments to published approved accounting standards that are not

Following amendment to an existing standard and IFRS applicable to the Bank have been published that aremandatory for the Bank’s accounting periods beginning on or after January 1, 2008 or later periods.

SME Bank Limited

Notes to the Financial Statements

for the year ended December 31, 2007

In terms of the provisions of the State Bank of Pakistan BSD Circular No. 6 of 2005, the Bank was required toincrease its paid-up capital (net of losses) as at December 31, 2007 upto Rs 4 billion. The State Bank of Pakistan(SBP) has granted exemption from meeting the enhanced Minimum Capital Requirement and the Bank is allowedto operate with minimum paid-up capital (net of losses) of Rs 2 billion till privatisation of the Bank.

Adoption of Revised IAS 1 - Presentation of financial statements may only impact the presentation and extent ofdisclosures in group financial.

IAS 23 - revised and other interpretations are not relevant to the Group's operations.

IFRIC 14 clarifies when refunds or reductions in future contributions in relation to defined benefit assets shouldbe regarded as available and provides guidance on Minimum Funding Requirements (MFR) for such asset.Adoption of IFRIC 14 may not have material impact on the group.

SME Bank Limited

Notes to the Financial Statements

for the year ended December 31, 2007

4 BASES OF MEASUREMENT

5 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES AND ESTIMATES

5.1 Cash and cash equivalents

5.2 Investments

Held for trading

Held to maturity

Available for sale

These represent investments which do not fall under held for trading or held to maturity securities.

Investment in subsidiary is carried at cost.

Gain/ loss on sale of investments is included in income currently.

These represent investments acquired by the Bank with the intention and ability to hold them upto maturity.These are carried at amortized cost in accordance with the requirement of BSD cicular No. 14 dated September24, 2004.

These financial statements have been prepared under the historical cost convention as modified for certaininvestments which are shown at revalued amounts.

These represent investments acquired by the Bank with the intention to trade by taking advantage of short-termmarket/ interest rate movements. These are marked to market and surplus / (deficit) arising on revalution istaken to profit and loss account in accordance with the requirement of SBP's BSD circular No. 10 dated July 13,2004.

In accordance with the requirement of SBP's BSD Circular No. 20 dated August 4, 2000 securities for whichready quotations are available on Reuters page (PKRV) or Stock Exchange are valued at quoted price andresulting surplus/ deficit is kept in a separate account and is shown below the shareholders' equity in the balancesheet.

Unquoted equity securities are valued at lower of cost and break-up value. Break-up value of equity securities iscalculated with reference to the net assets of the investee company as per the latest audited financial statements.Other unquoted investments are valued at cost.

Any premium paid or discount received on purchase of securities is amortised. Full year amortisation is chargedin the year of purchase while no amortisation is charged in the year of disposal.

The principal accounting policies applied in the preparation of these financial statements are set out below. Thesepolicies have been consistently applied to all the years presented, unless otherwise stated.

Cash and cash equivalents comprise of cash and balances with treasury banks and balances with other banks andcall money lendings.

In accordance with SBP's BSD circular No. 10 of 2004, investments have been classified into following categories

SME Bank Limited

Notes to the Financial Statements

for the year ended December 31, 2007

5.3 Advances

5.4 Operating fixed assets and depreciation

Capital work-in-progress is stated at cost.

Property and equipment

Intangible assets

5.5 Impairment

Assets subject to finance lease are stated at lower of present value of minimum lease payments under the leaseagreements and the fair value of assets acquired on lease less accumulated depreciation at the rates and basisapplicable to the Bank's owned assets. The outstanding obligation under finance lease less financial chargesallocated to future periods is shown as liability. Finance charges are calculated at interest rates implicit in the leaseand are charged to profit and loss account in the period in which these are incurred.

An intangible asset is recognized only if it is identifiable, the Bank has control over the asset, it is probable thateconomic benefits will flow to the enterprise and the cost of the asset can be measured reliably. All intangibleassets that meet the recognition criteria are initially measured at cost and are amortized on a straight line basis atthe rate given in note 12.3 commencing from the month when these assets are available for use.

The carrying amount of assets are reviewed at each balance sheet date for impairment, whenever events orchanges in circumstances indicate that the carrying amounts of the assets may not be recoverable. If suchindication exists, and where the carrying value exceeds the estimated recoverable amount, assets are writtendown to their recoverable amount. The resulting impairment loss is taken to the profit and loss account exceptfor impairment loss on revalued assets, which is adjusted against the related revaluation surplus to the extent thatthe impairment loss does not exceed the surplus on revaluation of those assets.

Advances are stated net of provision for non-performing advances. Provision for non-performing advances isdetermined in accordance with the requirements of Prudential Regulations issued by SBP from time to time. Inaddition to this all advances outstanding for more than one year are fully provided for in accordance with therequirements of the loan agreement for SME Sector Development Programme between GOP and AsianDevelopment Bank.

The provisions are charged to the profit and loss account. Advances are written off when there is no realisticprospect of recovery.

Property and equipment are stated at cost/value on their acquisition less accumulated depreciation except for landwhich is stated at cost. Depreciation is charged on straight line method at the rates given in note 12.2,commencing from the month in which the asset is acquired. No depreciation is charged in the month the asset isdisposed off. Gains or losses on disposal of property and equipment are taken to the profit and loss account.

Maintenance and normal repairs are charged to income as and when incurred. Major renewals and improvementsare capitalised.

SME Bank Limited

Notes to the Financial Statements

for the year ended December 31, 2007

5.6 Taxation

5.7 Staff retirement and other benefits

The Bank operates following staff retirement and other benefit schemes for its employees:

Pension and gratuity scheme

Provident fund

Benevolent fund

Compensated absences

Deferred tax is accounted for using the balance sheet liability method in respect of all temporary differencesbetween the carrying amount of assets and liabilities in the financial statements and the corresponding tax basesused in the computation of taxable profit at the rates that are expected to apply to the period when the differencesreverse based on the tax rates that have been enacted. Deferred tax assets are recognised to the extent that it isprobable that taxable profits will be available against which the deductible temporary differences, unused taxlosses and tax credits can be utilized.

Provision for current taxation represents expected tax payable on the taxable income for the year using applicabletax rates after taking into account tax credits and tax rebates, if any.

The Bank also recognises deferred tax asset/ liability on deficit/ surplus on revaluation of investments which isadjusted against the related deficit/ surplus in accordance with the requirements of International AccountingStandard on 'Income Taxes' (IAS 12).

Fully funded defined benefit pension and gratuity scheme for permanent employees. Contributions are made inaccordance with the actuarial valuation which is carried out periodically using 'Projected Unit Credit Method'.The actuarial gain/ loss in excess of corridor (10% of higher of fair value of plan assets or present value ofobligation) is recognized over the expected average remaining working lives of employees participating in theplan.

For its contractual employees the Bank operates a defined benefit unfunded gratuity scheme. During the year2006, the Bank changed the method of recognition of liability for gratuity scheme and the obligation under thedefined benefit unfunded gratuity scheme is now recognised on the basis of actuarial valuation using the'Projected Unit Credit Method'. The amount recognised in the balance sheet represents the present value ofdefined benefit obligation. Prior to year 2006, annual provision for liabilities towards gratuity scheme was madeon the basis of last drawn basic salary.

Non-contributory scheme for permanent employees. Monthly contributions are made by employees only, at therate of 8% of basic salary.

Defined benefit scheme for permanent employees. Contributions to this fund were made equally by the Bank andemployees till March 2002. Thereafter it is wholly contributed by the Bank at the rate of 2% of basic salary with aceiling of Rs 200 per month per employee.

The Bank allows compensated absences, an unfunded scheme, per entitlement to all its permanent andcontractual employees. Related provision is made in accordance with actuarial valuation.

SME Bank Limited

Notes to the Financial Statements

for the year ended December 31, 2007

5.8 Agreements for sale and purchase of securities (repo and reverse repo)

5.9 Revenue recognition

5.10 Off setting

5.11 Related party transactions

5.12 Borrowing costs

5.13

5.14 Provisions

Government grants

Income on non interest based loans, except loans disbursed by defunct SBFC, is accounted for on accrual basison principal outstanding amounts, and suspended, in compliance with requirements of prudential regulations ofSBP. Income on loans disbursed by defunct SBFC is suspended when accrued and recognised as income on cashbasis owing to the nature and status of the portfolio.

Income on interest based loans, except loans disbursed by defunct SBFC and penal mark-up on all classifiedadvances, is accounted for on accrual basis on principal outstanding amounts and suspended, in compliance withrequirements of prudential regulations of SBP. Income on loans disbursed by defunct SBFC is suspended andrecognised on cash basis owing to the nature and status of the portfolio.

Dividend income is recognized when the bank's right to receive dividend is established. while profit on otherinvestments, bank deposits and staff loans is recognised on accrual basis. Income on non-funded facilities (fee,commission, documentation charges etc.) is recognised on receipt basis.

The Bank follows finance method in recognising income on lease contracts. Under this method, un-earnedincome i.e., the excess of aggregate lease rentals and the estimated residual value over the cost of the leased assetis taken to income over the lease term so as to produce a constant periodic rate of return on outstanding netinvestment in lease. Unrealized lease income is suspended, where required, in accordance with prudentialregulations. Gain or loss on termination of lease contracts, documentation charges, front end fee and other leaseincome are recognised on receipt basis.

Securities sold under repurchase agreement (repo) are retained in the financial statements as investments and aliability for consideration received is included in borrowings. The difference between sale and repurchase price istreated as mark-up expense and recognized over the period of contract.

Securities purchased under agreement to resell (reverse repo) are included in lending to financial institutions. Thedifference between purchase and resale price is treated as mark-up income and recognized over the period ofthe contract.

Financial assets and liabilities are off set and the net amount reported in the balance sheet when there is a legallyenforceable right to set off the recognized amounts and there is an intention either to settle on a net basis orrealize the asset and settle the liability simultaneously.

Transactions between the Bank and its related parties are carried out on arm's length basis determined inaccordance with the generally accepted methods.

All borrowing costs are recognized as expense in the period in which these are incurred.

Government grants are recognized when the conditions attaching to the grant are complied with. Such grants arecredited to income over the period necessary to match them with the related costs which they are intended tocompensate and are netted off from the related expense.

Provisions are recorded when the Bank has a present legal or constructive obligation as a result of past events, it isprobable that an outflow of resources embodying economic benefits will be required to settle the obligation and areliable estimate can be made of the amount of obligation.

SME Bank Limited

Notes to the Financial Statements

for the year ended December 31, 2007

5.15 Segment reporting

5.15.1 Business Segment

Trading and Sales

Commercial banking

5.15.2

5.16

i) classification of investments (note 10)ii) provision against investments (note 10.4) and advances (note 11.4)iii) useful life of operating fixed assets (note 12)iv) income taxes (note 29)v) staff retirement benefits (note 33)

The Bank only operate in Pakistan

This segment undertakes the Bank's treasury, money market and capital market activities.

This includes loans, deposits and other transactions with corporate customers.

Use of critical accounting estimates and judgments

A segment is the distinguishable component of a group that is subject to risks and rewards that are different fromthose of other segments. A business segment is one that is engaged either in providing certain products orservices, whereas a geographical segment is one engaged in providing products and services within a particulareconomic environment. Segment information is presented as per the Bank's functional structure and the guidanceof the State Bank of Pakistan. The Bank's primary formate of reporting is based on business segments:

Geographical Segments

The preparation of financial statements in conformity with approved accounting standards requires the use ofcertain critical accounting estimates. It also requires management to exercise its judgment in the process ofapplying the Bank's accounting policies. The Bank uses estimates and assumptions concerning the future. Theresulting accounting estimates will, by definition, seldom equal the related actual results. Estimates and judgmentsare continually evaluated and are based on historical experience and other factors, including expectations of futureevents that are believed to be reasonable under the circumstances. The areas where assumptions and estimates aresignificant to the Bank's financial statements or where judgement was exercised in application of accountingpolicies are as follows:

SME Bank Limited

Notes to the Financial Statements

for the year ended December 31, 2007

6. FINANCIAL RESTRUCTURING

6.1

i)

ii)

iii)

iv)

v)

vi)

vii) reimbursement by GOP of costs related to VSS launched for all regular employees;viii)

ix) privatization of the Bank by June 2006.

6.2 Current status of the above referred financial restructuring is given below:

i)

ii)

iii)

iv)

v)

vi)

100% provision to be made against non performing financial assistance extended by the defunct RDFCand SBFC prior to January 1, 2002 which provision to be adjusted against SBP credit lines. SBP willrecover this amount from proceeds of ADB loan to GOP;

reduction in the number of recovery branches, staff rationalization through Voluntary SeparationScheme (VSS), human resource audit and hiring of new professional staff on merit;

SBP to issue a banking license to the Bank on compliance with all conditions of restructuring andapplicable SBP regulations. The commercial banking operations will be separate from the recoveryoperations of the defunct RDFC and SBFC portfolio and the two operations will be run as independentunits within the Bank; and

raising the paid-up capital to Rs 1,100 million by issuing additional shares to GOP;

the Ministry of Finance (MOF) shall ensure that SBP's shareholding in the Bank is terminated throughthe purchase of SBP held shares at nominal value by shareholders or otherwise;

VSS was approved by the Board of Directors of the Bank on November 7, 2003. Costs of VSS arereimbursable by GOP under the Small and Medium Enterprise Sector Development Programme loanagreement between GOP and Asian Development Bank. 712 employees opted for VSS. Aggregateestimated cost of VSS for 712 employees amounts to approximately Rs. 1,800 million. 707 employeeswere relieved under the scheme upto December 31, 2005, and the aggregate reported cost for 707employees was Rs. 1,764.268 million, which has been received by the bank by March 31, 2007;

Accumulated balances of Rs 3,275.752 million due from SBP on account of its share in profits andlosses of the Bank have been adjusted against credit lines provided by SBP;

Rs. 7,393 million has been paid to SBP since 2003, to fully adjust the loan liability.

Paid-up capital has been increased to Rs. 2,393 million by issue of 73,502,453 additional shares of Rs10 each to GOP without right issue in 2004,issue of 40,000,000 additional shares of Rs 10 each toGOP without right issue in 2005, issue of 50,000,000 additional bonus shares of Rs 10 each to GOPwithout right issue in 2006 and issue of 39,250,700 additional shares of Rs. 10 each to GOP withoutright issue in 2007. Proceeds against issue of additional shares in 2004 were paid by GOP to SBPagainst the Bank's loan balance due to SBP;

Provision of Rs 1,283.196 million against non performing financial assistance extended by the defunctRDFC and SBFC was adjusted against credit lines of SBP in 2003;

The Government of Pakistan (GOP) assisted by Asian Development Bank (ADB) is working on SME SectorDevelopment Programme (SME SDP). Loan agreement for this programme between GOP and ADB and projectagreement between ADB, SBP, Small and Medium Enterprise Development Authority and the Bank have beensigned on February 10, 2004. This programme, apart from other aspects on policy matrix relating to SME sectorof Pakistan, also envisages restructuring of SME Bank Limited. Salient features of the restructuring of the Bankare given below:

adjustment of accumulated balances due from SBP on account of its share in profits and losses of theBank against credit lines provided by SBP;

payment of Rs 3 billion to SBP before January 1, 2004 against outstanding credit lines and conversionof balance of remaining credit lines into a loan repayable in full by June 30, 2006;

Number of recovery branches was reduced to 14 by December 31, 2006;

SME Bank Limited

Notes to the Financial Statements

for the year ended December 31, 2007

vii)

viii)

ix)

x) The transaction model has been approved by Board of Privatization Commission. The next phase willbe publication of expression of interest (EOI) in media to identify interested investors.

Banking license was issued by SBP on September 13, 2004 and the Bank has started banking operationsafter the issue of certificate for commencement of banking business by SBP on April 16, 2005; and

Human resource technical audit has been completed and report has been submitted to the Bank.

Privatization Commission (PC) has constituted a transaction committee which is represented bymembers from the Privatization Commission, State Bank of Pakistan, Ministry of Finance and theBank. Privatization Commission has approved M/S BMA Capital as Financial Advisors for the bankand due diligence exercise for the privatization of the Bank has been carried out.

SME Bank LimitedNotes to the Financial Statementsfor the year ended December 31, 2007

Note 2007 20067 Rupees in '000

In hand- Local currency 64,703 59,108In transit- Local currency 2,519 4,159

National prize bonds 70 7With State Bank of Pakistan in Local currency current account 7.1 207,132 248,451

With National Bank of Pakistan in Local currency deposit account 12,281 229

286,705 311,954

7.1

8 BALANCES WITH OTHER BANKS 2007 2006Rupees in '000

In Pakistan On deposit account 8.1 62,980 135,704Provision for doubtful balances with bank 8.2 (10,000) (10,000)

52,980 125,704

8.1 These carry interest rate ranging from 6.00% to 8.00% (2006: 1.50% to 5.00%) per annum.

8.2

9 LENDINGS TO FINANCIAL INSTITUTIONS 2007 2006Rupees in '000

Call money lendings 9.1 - 200,000Repurchase agreement lendings (reverse repo) 9.2 258,944 92,454

258,944 292,454

9.1

9.2

CASH AND BALANCES WITH TREASURY BANKS

This represents transactions with a bank for purchase of treasury bills under resale obligation (reverse repo) in the inter-bank money market at mark-up rate ranging from 9.48 to 9.95% (2006: 8.35%) per annum for periods upto thirty onedays. These lendings were secured against underlying treasury bills. The difference between purchase and resale price istreated as mark-up income and recognised over the period of reverse repo agreement.

This represents unsecured lendings with banks in the inter-bank money market at mark up rate ranging from 6.50 to11.75% (2006:11.75%) per annum for periods upto thirty two days.

Provision for doubtful balance is in respect of deposit of Rs 10 million with Indus Bank Limited which is underliquidation.

Deposits with the State Bank of Pakistan are maintained to comply with its requirements issued from time to time.

SME Bank LimitedNotes to the Financial Statementsfor the year ended December 31, 2007

Note 2007 20069.3 Held by Further Held by Further

bank given as Total bank given as Totalcollateral collateral

Rupees in '000

Market Treasury Bills 258,944 - 258,944 92,454 - 92,454

258,944 - 258,944 92,454 - 92,454

10 INVESTMENTS 2007 2006Held by Given as Total Held by Given as Total

bank collateral bank collateralRupees in '000

10.1 Investments by types:

Available-for-sale securities

Market Treasury Bill - - - 191,225 - 191,225Pakistan Investment Bonds 472,494 1,888,779 2,361,273 666,069 2,852,792 3,518,861WAPDA Bonds 35,000 - 35,000 35,000 - 35,000Fully paid ordinary shares 297,595 - 297,595 178,192 - 178,192Term Finance Certificates (TFCs) 98,887 - 98,887 193,502 - 193,502

903,976 1,888,779 2,792,755 1,263,988 2,852,792 4,116,780Held-to-maturity securities

Letter of placements - - - 500,410 - 500,410Certificates of investment 98,267 - 98,267 308,282 - 308,282Term deposit receipts 100,590 - 100,590 600,652 - 600,652

198,857 - 198,857 1,409,344 - 1,409,344

Investment in subsidiary

SME Leasing Limited 215,457 - 215,457 215,457 - 215,457Investment at cost 1,318,290 1,888,779 3,207,069 2,888,789 2,852,792 5,741,581Provision for Diminuation in value of Investments 10.4 (23,929) - (23,929) (23,125) - (23,125)Investments (Net of Provisions) 1,294,361 1,888,779 3,183,140 2,865,664 2,852,792 5,718,456

22 3,051 (128,061) (125,010) 3,033 (154,907) (151,874)

1,297,412 1,760,718 3,058,130 2,868,697 2,697,885 5,566,582

(Deficit)/surplus on revaluation of available for sale securities

Securities held as collateral against lendingto financial institutions

SME Bank LimitedNotes to the Financial Statementsfor the year ended December 31, 2007

10.2 Investment by segment: Note 2007 2006

Federal Government Securities: 10.3 -Market Treasury Bills - 191,225 -Pakistan Investment Bonds 2,361,273 3,518,861

2,361,273 3,710,086Fully Paid up Ordinary Shares: -Listed Companies/Mutual fund 10.6 276,592 157,189 -Unlisted Companies/Mutual fund 10.7 21,003 21,003

297,595 178,192Bonds and Participation Term Certificates: 10.8 - Listed TFC's etc. 98,887 193,502 - WAPDA Bonds 35,000 35,000

133,887 228,502Subsidiaries

SME Leasing Limited 215,457 215,457

Other Investments - Letter of placements - 500,410 - Certificates of investment 98,267 308,282 - Term deposit receipts 100,590 600,652

198,857 1,409,344

3,207,069 5,741,581Less: Provision for Diminuation in value of Investments 10.4 (23,929) (23,125)

Investments (Net of Provisions) 3,183,140 5,718,456

Less: Deficit on revaluation of available for sale securities (125,010) (151,874)

Total investment at market value 3,058,130 5,566,582

Rupees in '000

SME Bank LimitedNotes to the Financial Statementsfor the year ended December 31, 2007

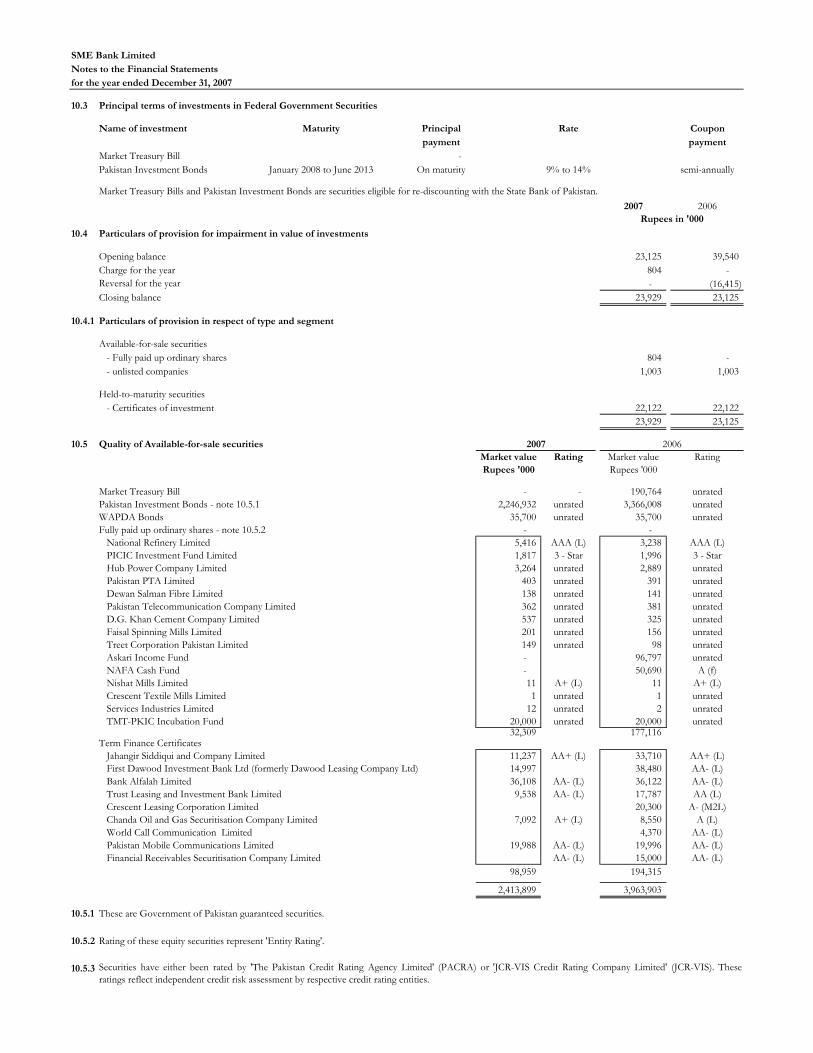

10.3 Principal terms of investments in Federal Government Securities

Name of investment Maturity Principal Rate Couponpayment payment

Market Treasury Bill - Pakistan Investment Bonds January 2008 to June 2013 On maturity 9% to 14% semi-annually

Market Treasury Bills and Pakistan Investment Bonds are securities eligible for re-discounting with the State Bank of Pakistan. 2007 2006

10.4 Particulars of provision for impairment in value of investments

Opening balance 23,125 39,540 Charge for the year 804 - Reversal for the year - (16,415) Closing balance 23,929 23,125

10.4.1 Particulars of provision in respect of type and segment

Available-for-sale securities- Fully paid up ordinary shares 804 - - unlisted companies 1,003 1,003

Held-to-maturity securities- Certificates of investment 22,122 22,122

23,929 23,125

10.5 Quality of Available-for-sale securitiesMarket value Rating Market value RatingRupees '000 Rupees '000

Market Treasury Bill - - 190,764 unratedPakistan Investment Bonds - note 10.5.1 2,246,932 unrated 3,366,008 unratedWAPDA Bonds 35,700 unrated 35,700 unratedFully paid up ordinary shares - note 10.5.2 - -

National Refinery Limited 5,416 AAA (L) 3,238 AAA (L)PICIC Investment Fund Limited 1,817 3 - Star 1,996 3 - StarHub Power Company Limited 3,264 unrated 2,889 unratedPakistan PTA Limited 403 unrated 391 unratedDewan Salman Fibre Limited 138 unrated 141 unratedPakistan Telecommunication Company Limited 362 unrated 381 unratedD.G. Khan Cement Company Limited 537 unrated 325 unratedFaisal Spinning Mills Limited 201 unrated 156 unratedTreet Corporation Pakistan Limited 149 unrated 98 unratedAskari Income Fund - 96,797 unratedNAFA Cash Fund - 50,690 A (f)Nishat Mills Limited 11 A+ (L) 11 A+ (L)Crescent Textile Mills Limited 1 unrated 1 unratedServices Industries Limited 12 unrated 2 unratedTMT-PKIC Incubation Fund 20,000 unrated 20,000 unrated

32,309 177,116 Term Finance Certificates

Jahangir Siddiqui and Company Limited 11,237 AA+ (L) 33,710 AA+ (L)First Dawood Investment Bank Ltd (formerly Dawood Leasing Company Ltd) 14,997 38,480 AA- (L)Bank Alfalah Limited 36,108 AA- (L) 36,122 AA- (L)Trust Leasing and Investment Bank Limited 9,538 AA- (L) 17,787 AA (L)Crescent Leasing Corporation Limited 20,300 A- (M2L)Chanda Oil and Gas Securitisation Company Limited 7,092 A+ (L) 8,550 A (L)World Call Communication Limited 4,370 AA- (L)Pakistan Mobile Communications Limited 19,988 AA- (L) 19,996 AA- (L)Financial Receivables Securitisation Company Limited AA- (L) 15,000 AA- (L)

98,959 194,315

2,413,899 3,963,903

10.5.1 These are Government of Pakistan guaranteed securities.

10.5.2 Rating of these equity securities represent 'Entity Rating'.

10.5.3

Rupees in '000

2007 2006

Securities have either been rated by 'The Pakistan Credit Rating Agency Limited' (PACRA) or 'JCR-VIS Credit Rating Company Limited' (JCR-VIS). Theseratings reflect independent credit risk assessment by respective credit rating entities.

SME Bank LimitedNotes to the Financial Statementsfor the year ended December 31, 2007

10.6 Investments in listed companies/ mutual funds

Paid-up 2007 2006 value per Name of companies/ mutual funds 2007 2006

share / average price per unit

Rs

15,000 12,500 354.13 National Refinery Limited 5,312 5,312 137,668 137,668 18.12 PICIC Investment Fund Limited 2,494 2,494 107,000 107,000 18.95 Hub Power Company Limited 2,028 2,028 79,775 79,775 10.15 Pakistan PTA Limited 810 810 18,449 18,449 18.27 Dewan Salman Fibre Limited 337 337 8,600 8,600 68.14 Pakistan Telecommunication Company Limited 586 586 5,672 5,157 49.37 D.G. Khan Cement Company Limited 280 280 4,000 4,000 40.50 Faisal Spinning Mills Limited 162 162

500 500 294.00 Treet Corporation Pakistan Limited 147 147 290 290 103.45 Nishat Mills Limited 30 30 18 17 36.11 Crescent Textile Mills Limited 1 1 72 72 25.00 Services Industries Limited 2 2

Mutual Funds

1,011,004 - Askari Investment Management 106,519 - 13,569,210 4,816,909 NAFA Cash Fund 142,314 50,000

51,324 - HBL Income Fund 5,358 - 96,890 910,946 Askari Income Fund 10,212 95,000

276,592 157,189 Surplus/(deficit) on revaluation of shares / units - (net) 910 (73) Market value as on December 31 277,502 157,116

10.7 Particulars of investments held in unlisted companies and mutual funds 2007 2006

AKD Venture Fund (formerly TMT-PKIC Incubation Fund Limited) 10.7.1 20,000 20,000 Companies delisted from stock exchange 10.7.2 1,003 1,003

21,003 21,003

Percentage Number Cost / Paid-up Total Break up Based on Name ofof of value Paid-up Value accounts Chief Executive

holding units per unit Value auditedheld held as at

(Rupees) (Rupees in '000)10.7.1

8% 2,000,000 10.00 20,000 19,196 June 30, 2007 Kashif Shamim

10.7.2 Particulars of investments in shares of companies delisted from stock exchange and currently under liquidation.

Number Cost / Paid-up Total of value Paid-up

shares per share Valueheld held

(Rupees) (Rupees in '000)

Mohib Exports Company Limited 4,600 23.81 109 Sunflo Citrus Limited 100,000 4.22 422 Tawakal Garments Company Limited 4,000 38.38 154 Tristar Shipping Lines Limited 5,000 23.56 118 Zahoor Textile Mills Limited 15,200 13.16 200

1,003

No. of ordinary shares/units

Rupees in '000

Rupees in '000

AKD Venture Fund (formerly TMT-PKIC Incubation Fund Limited)

SME Bank LimitedNotes to the Financial Statementsfor the year ended December 31, 2007

10.8 Investment in Listed Term Finance Certificates/ Bonds

Nominal 2007 20062007 2006 value per

certificateRupees

9,000 9,000 Jahangir Siddiqui & Company Limited 1,249 11,237 33,747 - 7,400 - - 37,000

7,200 7,200 Bank Alfalah Limited 4,990 35,928 36,979 5,000 5,000 Trust Leasing and Investment Bank Limited 1,908 9,538 17,816

- 4,000 Crescent Leasing Corporation Limited - - 20,000 2,000 2,000 Chanda Oil & Gas Securitisation Company Limited 3,600 7,200 8,680

- 3,000 World Call Communication Limited - - 4,284 4,000 4,000 Pakistan Mobile Communications Limited 4,997 19,988 19,996 3,000 5,000 Financial Receivables Securitisation Company Limited 4,999 14,997 15,000

98,887 193,502 7,000 7,000 WAPDA Bonds 5,000 35,000 35,000

Surplus on revaluation of TFCs/ Bonds 754 1,513 Market value as on December 31 134,641 230,015

10.8.1 These carry rate of return ranging from 11.00% to 13.38% (2006: 9.25% to 13.22%) per annum and having maturity periods of upto 5 years (2006: 7 years).

10.9 Subsidiary company

Rupees in '000

SME Leasing Limited (SMEL) was incorporated on July 12, 2002 as a public limited company under the Companies Ordinance, 1984. Upto the year 2005, SMELwas a wholly owned subsidiary of the Bank, however, a public offering of 10 million ordinary shares was made during the year 2006 at an offer price of Rs 11 pershare. The Bank subscribed for 1,405,205 shares in SMEL and holds 73% shares in SMEL as at December 31, 2007. SMEL is listed on Lahore Stock Exchange.Value of investment in SMEL based on market value as at December 31, 2007 was Rs 257,457 thousand. This investment is designated as a 'Strategic Investment'in terms of BPD Circular Letter No. 16 dated August 1, 2006.

Company's name

Dawood Investment Bank Ltd (formerly Dawood Leasing Company Ltd)

No. of certificates

SME Bank Limited

Notes to the Financial Statements

for the year ended December 31, 2007

11 ADVANCES Note 2007 2006Rupees in '000

Loans, cash credits, running finances, etc.-In Pakistan Extended by: Defunct SBFC 4,812,915 5,143,763 Defunct RDFC 671,449 792,928 SME Bank Limited 1,888,760 1,537,499 Due from ex-employees 24,686 25,013 Due from employees 363,155 308,513

7,760,965 7,807,716

Net investment in finance lease-In Pakistan 11.2 1,253 1,253

Advances- Gross 7,762,218 7,808,969

Provision for non-performing advances 11.4 5,643,871 6,077,698Advances- Net of provision 2,118,347 1,731,271

11.1 Particulars of advances

11.1.1 In local currency 7,762,218 7,808,969In foreign currencies - -

7,762,218 7,808,969

11.1.2 1,193,200 782,5936,569,018 7,026,3767,762,218 7,808,969

Short Term ( for up to one year)Long Term ( for over one year)

SME Bank LimitedNotes to the Financial Statementsfor the year ended December 31, 2007

11.2 NET INVESTMENT IN FINANCE LEASE 2007 2006

Not later Later than Over Total Not later Later than Over Totalthan one one and less five than one one and less five

year than five years years year than five years yearsRupees in '000

Lease rentals receivable 973 - - 973 973 - - 973Residual value 280 - - 280 280 - - 280Minimum lease payments 1,253 1,253 1,253 - - 1,253 Financial charges for future - - - - - - - - periods

Present value of minimum lease payments 1,253 - - 1,253 1,253 - - 1,253

11.3 Advances include Rs.5,706,118 thousand (2006:Rs. 6,119,396 thousands) which have been placed under non-performing status as detailed below:-

Category of Classification Domestic Overseas Total Provision Provision Required Held

Rupees in '000

Substandard 53,143 - 53,143 13,286 13,286Doubtful 44,778 - 44,778 22,388 22,388Loss 5,608,197 - 5,608,197 5,608,197 5,608,197

5,706,118 - 5,706,118 5,643,871 5,643,871

11.4 Particulars of provision against non-performing advances

Specific General Total Specific General TotalRupees in '000

Opening balance 6,077,698 - 6,077,698 6,767,586 - 6,767,586Amounts written off 11.5 (329,184) - (329,184) (472,389) - (472,389)Charge for the year 19,112 - 19,112 32,089 32,089Reversals (123,756) - (123,756) (249,588) - (249,588)

(104,643) - (104,643) (217,499) - (217,499)

Closing balance 5,643,871 - 5,643,871 6,077,698 - 6,077,698

11.4.1 Particulars of provision against non-performing advances

Specific General Total Specific General TotalRupees in '000

In Local currency 5,643,871 - 5,643,871 6,077,698 - 6,077,698In foreign currency - - - - - -

5,643,871 - 5,643,871 6,077,698 - 6,077,698

2007

2007 2006

20062007

SME Bank LimitedNotes to the Financial Statementsfor the year ended December 31, 2007

11.5 PARTICULARS OF WRITE OFFS: Notes 2007 2006

11.5.1 Against Provisions 11.4 329,184 472,389Directly charged to Profit & Loss account 3,780 1,245

332,964 473,634

11.5.2 Write Offs of Rs. 500,000 and above 11.6 51,229 105,435Write Offs of Below Rs. 500,000 281,735 368,199

332,964 473,634

11.6 DETAILS OF LOAN WRITE OFF OF Rs. 500,000/- AND ABOVE

is given at Annexure-1.

11.7 PARTICULARS OF LOANS AND ADVANCES TO DIRECTORS, ASSOCIATED COMPANIES, ETC.

2007 2006Rupees in '000

Debts due by directors, executives or officers of the bank or any ofthem either severally or jointly with any other persons

Balance at the beginning of the year 29,243 15,412 Loan extended during the year 20,355 19,186 Repayments (5,300) (5,355) Balance at the end of the year 44,298 29,243

Debts due by subsidiary company

Balance at the beginging of the year 95,406 125,184 Loans granted during the year 30,000 25,000 Repayments (72,751) (54,778) Balance at the end of the year 52,655 95,406

96,953 124,649

12 OPERATING FIXED ASSETS 2007 2006Rupees in '000

Capital work-in-progress 12.1 3,541 4,290Property and equipment 12.2 137,863 145,646 Intangible assets 12.3 3,184 6,448

144,589 156,384

12.1 Capital work-in-progress

Assets subject to finance lease 654 1,403 Others (Computer software) 2,887 2,887

3,541 4,290

Rupees in '000

In terms of sub-section (3) of Section 33A of the Banking Companies Ordinance, 1962 the Statement in respect of written-financial relief of five hundred thousand rupees or above allowed to a person(s) during the year ended December 31, 2007 is

SME Bank LimitedNotes to the Financial Statementsfor the year ended December 31, 2007

12.2 FIXED ASSETSC O S T Net book Depreciation

As at Additions/ As at As at As at value as at rateJanuary 1, (Disposals) Dec 31, January 1, Dec 31, Dec 31, per annum

2007 2007 2007 2007 2007 %

Owned Assets Tangible assets

Lease hold land 12.2.1 60,450 - 3,637 64,087 - - - - 64,087 -

Buildings on lease hold land 15,794 - - 15,794 876 - 790 1,666 14,128 5- -

Leasehold improvements 16,635 - 212 16,830 5,794 - 4,472 10,249 6,581 33 1/3(17) (17)

Office furniture and fixtures 13,152 - 392 13,281 8,891 - 1,457 10,109 3,172 20(264) (239)

Library 19 - 19 19 - - 19 - 20-

Office equipment 18,138 - 898 18,927 5,916 - 2,799 8,626 10,301 15

(Rupees '000)DEPRECIATION

Transfer from leased

assets/(own assets)

Transfer from leased

assets/(own assets)

Charge for the year/(disposal)

(109) (89) Computer equipment 62,583 - 3,861 66,303 44,589 - 9,744 54,193 12,111 33 1/3

(141) (141) Vehicles 39,236 7,906 5 42,071 32,360 3,384 6,121 37,898 4,172 20

(5,076) (3,966) 226,007 7,906 9,004 237,311 98,445 3,384 25,382 122,760 114,551

(5,607) (4,452) Assets subject to finance lease

Vehicles 25,167 (7,906) 14,752 31,448 7,083 (3,384) 4,664 8,135 23,313 20(565) (228)

2007 251,174 - 23,756 268,758 105,528 30,046 130,895 137,863 (6,172) - - (4,679) - -

2006 226,603 - 38,221 251,174 82,974 30,153 105,528 145,646 (13,650) (7,599)

12.3 INTANGIBLE ASSETSC O S T Net book Annual

As at Additions/ As at As at As at value as at rateJanuary 1, (Disposals) Dec 31, January 1, Dec 31, Dec 31, of amortization

2007 2007 2007 2007 2007 %

Computer software 19,036 - - 19,036 12,588 - 3,264 15,852 3,184 33 1/32007 19,036 - - 19,036 12,588 - 3,264 15,852 3,184

2006 16,621 - 2,415 19,036 9,554 - 3,034 12,588 6,448

Transfer from leased

assets/(own asset)

Transfer from leased

assets/(own asses)

Amortization

AMORTISATION

SME Bank LimitedNotes to the Financial Statementsfor the year ended December 31, 2007

12.4

Vehicles

Mitsubishi Lancer 1,060 336 724 760 As per Bank policy Mr. Mansoor Khan - ExecutiveSuzuki Mehran 266 266 - 27 -do- Mr. Oshaid Akhtar - ExecutiveHonda City 661 661 - 73 -do- Mr. Tariq Mahmood - ExecutiveSantro Club 540 207 333 297 -do- Mr. Shehzad Abbasi - ExecutiveSuzuki Cultus 564 498 66 113 -do- Mr. Sohail Ishtiaq - ExecutiveSuzuki Cultus 570 503 67 114 -do- Mr. Abdul Razzaq - ExecutiveSuzuki Cultus 570 503 67 114 -do- Mr. Muhammad Ayub - ExecutiveSuzuki Mehran 346 294 52 69 -do- Mr. Barkat Ali LashariSuzuki Mehran 351 301 50 70 -do- Mr. Manzoor Jan - ExecutiveSuzuki Mehran 346 300 46 69 -do- Mr. Kishwar Malik - ExecutiveSuzuki Mehran 353 312 41 71 -do- Mr. Izaj Bashir - ExecutiveYamaha Motor Cycle 14 14 - 23

5,641 4,195 1,446 1,800

Buildings - - - -

Land - - - -

5,641 4,195 1,446 1,800

Other assets havingbook value of morethan Rs 250,000 or cost of Rs.1,000,000Which ever is less - - - -

2007 5,641 4,195 1,446 1,800

2006 13,650 7,599 6,051 18,007

12.5

12.2.1

2007 2006

13 DEFERRED TAX ASSET

Deferred taxation is in respect of:

Deficit on revaluation of investment 44,336 53,415 Provision for non-performing loans related to

defunct SBFC as at December 31, 2001 382,149 382,149 Preliminary expenses charged off in prior years - - Accelerated tax depreciation 7,272 (2,305) Excess of accounting book value of leased assets

over corresponding liabilities (722) 73 Provision for doubtful investments/ receivables 14,852 14,462

447,887 447,794

Cost Accumulated depreciation

Book value

Cost of fully depreciated assets that are still in use was Rs.88,823 thousands (2006: Rs. 58,540 Thousands)

Insurance Claim forburnt motorcycle

Rupees in '000

Rupees in '000

This represent cost of land measuring 500 square yards in sector G-7 and 4666.66 square yards situated in sector G-5/2 originally allotted to SBFC and RDFCrespectivey.CDA required payment of Rs.3.367 million for transferring the plot in the name of the Bank. However on receiving draft of the required amountCDA returned the same requiring payment of market value in view of proposed privatization of SME Bank. The payment has been accounted for as currentyear addition as the matter being pursued by the SME Bank with CDA.

Details of disposal of fixed assets to executive and other persons having cost more than Rs. One million or net book value Rs. 250,000 or above are asfollows:

Sale proceeds Mode of disposal Particulars of buyersParticulars of assets

SME Bank LimitedNotes to the Financial Statementsfor the year ended December 31, 2007

14 OTHER ASSETS Note 2007 2006Rupees in '000

Income/ Mark-up accrued in local currency 14.1 121,763 174,418Advances, deposits, advance rent and other prepayments 65,567 43,096VSS cost reimbursable by GOP - 736,147Refund due from defined benefit pension and gratuity fund 12,177 15,634Receivable from subsidiary company 1,323 2,370Receivable from Ravi Securities (Pvt) Limited and 31,447 37,447 Taas Securities (Pvt) LimitedStock exchange membership 18,000 18,000Receivable from Speedway Fondmetall Pakistan Limited 19,640 19,640Receivable from Equity Participation Fund 2,659 2,638Receivable against factorized portfolio 8,522 9,857Others 29,577 35,001

310,675 1,094,248Less: Provision held against other assets 14.2 (94,499) (101,513)Other Assets (Net of Provision) 216,176 992,735

14.1

14.2

14.3 PROVISIONS AGAINST OTHER ASSETS 2007 2006Rupees in '000

Opening balance 101,513 123,737Charge for the year - - Reversals (5,910) (20,000)Amount Writen off (1,104) (2,224)Closing balance 94,499 101,513

Provision balance is in respect of:

Income / mark-up accrued in local currency 15,780 15,780Asset Investment Bank Limited 506 506Prudential Investment Bank Limited 22 22Receivable from Ravi Securities (Pvt) Limited and 31,447 37,447 Taas Securities (Pvt) LimitedReceivable from Speedway Fondmetall Pakistan Limited 19,640 19,640

Other receivables

Advance to Invest Capital and Securities (Pvt) Limited - 372 Legal charges recoverable from borrowers 23,297 24,159 Others 3,807 3,587

94,499 101,513

This balance has been arrived at after adjusting interest in suspense of Rs 4,299,538 thousand (2006: Rs4,640,366 thousand)

This represent amount receivable from Karakuram Co Operative Bank Limited under the debt factoringagreement. As per agreed terms the recovery was due on June 30, 2006, however further extension wasgranted up to September 2007. Out of total outstanding amount of Rs. 18,833 thousands, Rs. 8,522thousands is still outstanding. No provision against this amount has been made as the management isconfident that the amount will be recovered and there is no liklihood of any losses keeping in view theKarakuram Co Operative Bank Limited deposite (TDR) of Rs. 30 million with SME Bank Limited.

SME Bank LimitedNotes to the Financial Statementsfor the year ended December 31, 2007

15 BILLS PAYABLE 2007 2006Rupees in '000

In Pakistan 40,441 18,090Outside Pakistan - -

40,441 18,090

16 BORROWINGS FROM FINANCIAL INSTITUTIONS

In Pakistan 1,400,000 2,600,000Outside Pakistan - -

1,400,000 2,600,000

16.1 Particulars of borrowings from financial institutions

In local currency 1,400,000 2,600,000In foreign currencies - -

1,400,000 2,600,000

16.2 Details of borrowing - secured

Repurchase agreement borrowings - secured 1,400,000 2,600,000

17 DEPOSITS AND OTHER ACCOUNTS 2007 2006Rupees in '000

CustomersFixed deposits 899,246 756,090Savings deposits 674,209 574,238Current Accounts - Non remunerative 299,670 227,578Margin account 6,462 48,140

1,879,587 1,606,046Financial InstitutionsRemunerative deposits - 60,314

1,879,587 1,666,36017.1 Particulars of deposits

In local currency 1,879,587 1,666,360In foreign currencies - -

1,879,587 1,666,360

17.2

These represent transactions with financial institutions for sale of Government Securities under re-purchase agreement (REPO) in the inter bank money market at mark-up rates ranging from 4.00 % to10.50 % (2006: 8.95% to 9.40%) per annum for periods upto one month ( 2006: upto three months) .REPO transactions are secured against investment of the Bank in Government securities.

Savings deposits include Rs 226.535 million (2006: Rs 220.782 million) related to Equity ParticipationFund.

SME Bank LimitedNotes to the Financial Statementsfor the year ended December 31, 2007

(Rupees '000)18 LOAN FROM THE STATE BANK OF PAKISTAN

a) Credit lines on service charge basis from SBP Extended to defunct SBFC 1,542,200

b) Credit lines on profit & loss sharing basis from SBP

Extended to defunct RDFC 1,426,060 Extended to defunct SBFC 9,718,220

11,144,28012,686,480

Less:(1,283,196)

(3,275,752)

Payment to SBP during 2003 (3,000,000)

Balance at December 31, 2003 5,127,532

Less:(735,025)

Payment to SBP during 2004 (392,507)

Balance at December 31, 2004 4,000,000

Less: Payment to SBP during 2005 (1,500,000) Balance at December 31, 2005 2,500,000

Less: Payment to SBP during 2006 (70,000) Balance at December 31, 2006 2,430,000

Less: Payments made during 2007 (2,430,000)

Balance at December 31, 2007 -

Additional provision against advances in accordance withrestructuring plan, charged to SBP

Receivable from SBP against its share in profit/loss adjusted againstborrowing from SBP

Payment by GOP to SBP against issue of 73,502,453 additional sharesof Rs. 10 each to GOP

SME Bank LimitedNotes to the Financial Statementsfor the year ended December 31, 2007

19 LIABILITIES AGAINST ASSETS SUBJECT TO FINANCE LEASE

2007 2006Minimum Financial Principal Minimum Financial Principal

lease charges for outstanding lease charges for outstandingpayments future periods payments future periods

Rupees in '000

Not later than one year 7,420 1,129 6,291 7,864 683 7,181Later than one year and not later than five years 20,186 1,106 19,080 13,008 492 12,516

27,606 2,235 25,371 20,872 1,175 19,697

20 OTHER LIABILITIES Notes 2007 2006Rupees in '000

Mark-up/ Return/ Interest payable in local currency 16,728 99,931Unearned commission on guarantees 929 1,064Accrued expenses 36,471 41,128Current taxation (provisions less payments) 192,789 245,192Accounts payable 1,507 15,058Sundry creditors 14,840 13,847Branch adjustment account 872 (92)Industrial Credit for Rural Women - Promotional Fund 20.1 30,978 30,857Provision for central excise duty 20.2 - 29,233Payable against employees benefit plans Defined benefit unfunded gratuity scheme 33.2 16,338 13,857 Unfunded compensated absences 33.3.3 83,673 75,925Security deposits against lease 284 284Employees' VSS payments withheld 16,543 18,777Payable to Cash Management Scheme 85 133Income tax withheld payable 17,325 17,376Others 390 249

429,752 602,819

20.1 Industrial Credit for Rural Women - Promotional Fund

Funds received including accumulated profit 30,978 30,857Loan outstanding - net of provision - -

30,978 30,857

20.2 Provision for central excise duty

This represents liability against vehicle lease agreements with leasing companies. Monthly lease rentals are payable including financial charges atrates ranging between 6.46 % and 16.00 % (2006: 6.46% and 13.50%) per annum which rates have been used as discounting factor to determinepresent value of minimum lease payments. The purchase option is available with the Bank at the time of payment of the last installment orsurrender of deposit money under the lease agreements.

The Fund is in respect of Rs 21.5 million received by the defunct RDFC in 1995 from GOP, National Development Finance Corporation(now amalgamated with National Bank of Pakistan), IDBP and Pakistan Banking Council (now taken over by SBP) for providing industrialcredit to rural women. The fund balance at year end is included in assets of the Bank.

Central Excise Duty (CED) and penalty thereon was imposed on defunct RDFC in June 1999 by the Additional Collector, Central Excise,Rawalpindi. Defunct RDFC filed an appeal against the order and the case was set-aside by the Collector (Appeals) in November 1999 for duereconciliation and fresh examination by the Additional Collector, Central Excise, Rawalpindi.The reconciliation and fresh examination of therecords of the CED maintained by RDFC was carried out by a team of the office of Central Excise.

Additional Collector of Customs, Sales Tax and Central Excise (Adjudication), Rawalpindi, issued an order on July 30, 2005, thereby, additionalduties were levied. The Bank filed an appeal against the order before the Appellate Tribunal, Customs, Sales Tax and Central Excise, Islamabad,on August 30, 2005. The custom, central excise appellate tribunal has disposed off the appeal filed by the SME Bank Ltd. against the orderspassed by the collector of custom, sales tax and central excise (appeals) Rawalpindi. The appellate tribunal ordered to deposit principal amountof central excise duty amounting to Rs. 202,152/- alongwith addition duty @ 2% per month amounting to Rs. 665,316/- and penalty @ 10%of recoverable amount amounting to Rs. 20,215/- which the SME Bank Ltd has complied with. Accordingly the provision for central exciseduty amounting to Rs. 29.233 Million has been reversed in the books of accounts.

SME Bank LimitedNotes to the Financial Statementsfor the year ended December 31, 2007

21 SHARE CAPITAL

21.1 Authorized Capital

2007 2006 2007 2006Rupees in '000

1,000,000,000 1,000,000,000 Ordinary shares of Rs.10 each 10,000,000 10,000,000

21.2 Issued, subscribed and paid up

2007 2006 Ordinary shares152,853,153 113,602,453 Fully paid in cash 1,528,532 1,136,025 50,000,000 50,000,000 Issued as bonus shares 500,000 500,000 36,397,547 36,397,547 Issued for consideration other than cash 363,975 363,975

239,250,700 200,000,000 2,392,507 2,000,000

Number of 21.3 Break-up of share capital is as follows: shares %

Federal Government 224,615,978 93.89 2,246,160 1,853,653National Bank of Pakistan 6,121,095 2.56 61,211 61,211United Bank Limited 3,975,003 1.66 39,750 39,750Habib Bank Limited 1,987,501 0.83 19,875 19,875MCB Bank Limited 1,490,619 0.62 14,906 14,906Allied Bank Limited 774,351 0.32 7,744 7,744Industrial Development Bank of Pakistan Limited 286,146 0.12 2,861 2,861Directors 7 - - -

239,250,700 100 2,392,507 2,000,000

22 SURPLUS/(DEFICIT) ON REVALUATION OF ASSETS

(Deficit) on revaluation of available for sale securitiesi) Federal and Provincial Government securities

- Market Treasury Bill - (460) - Pakistan Investment bonds (127,373) (152,854)

(127,373) (153,314)ii) Quoted shares/units - Fully paid up ordinary shares/mutual funds 910 (73)

iii) Bonds and Participation Term Certificates - Listed TFC 754 813 -WAPDA Bonds 700 700

1,454 1,513(125,010) (151,874)

Deferred tax thereon 44,336 53,415(80,674) (98,459)

SME Bank LimitedNotes to the Financial Statementsfor the year ended December 31, 2007

23 CONTINGENCIES AND COMMITMENTS 2007 2006Rupees in '000

23.1 Transaction-related Contingent Liabilities

Guarantees in favour of:

Others 58,209 32,941

23.2 Other Contingencies

a)24,972 37,472

b)40,000 40,000

c)23,800 23,800

d)

335,000 209,604

e)9,939 9,939

f)- 162,000

23.3 Commitments in respect of forward lending

Commitments to extend credit 148,730 100,482

23.4 Commitments for the acquisition of operating fixed assets 2,879 4,224

23.5 Commitment in respect of repo/ reverse repo transactions

Repurchase 1,400,000 2,600,000Resale 258,944 92,454

23.6 Other commitments

Undrawn facilities 174,235 217,019

23.7 Bills for collection

Payable in Pakistan 3,186 3,653

Adjustment of loan guarantee amount against borrowing from IDBP repaid in prior years,disputed by IDBP

Benefits claimed by ex-employees pertaining to Voluntary Separation Scheme, notacknowledged as debt

Tax demands raised by the income tax authorities related to defunct SBFC for assessmentyears 2001-02, 2002-03, 2003 and 2004 related to excess perquisites, write-off ofconsumable stores and payment under voluntary separation scheme. No provision in thisrespect has been made in the financial statements pending decision of the appeal filed withthe Commissioner of Income Tax. The Bank is confident of a favourable decision. Incase,the issue of provision for non-performing asset is resolved by the court in favour of bank,a sum of Rs 651 millions will be refundable.

Claims not acknowledged as debt from various borrowers for loss sustained due to non-disbursement

Damages claim by a borrower for delay in recording repaymenty received from a borrower, not acknowledged as debt

Damages claim by Ravi Securities (Private) Limited and Taas Securities (Private) Limited,not acknowledged as debt

SME Bank LimitedNotes to the Financial Statementsfor the year ended December 31, 2007

24 MARK-UP/RETURN/INTEREST EARNED Notes 2007 2006Rupees in '000

a)

Defunct RDFC 4,298 8,027Defunct SBFC 254,772 301,643SME Bank Limited 219,708 154,670

478,778 464,340

ii) Employees 9,525 6,656

iii) Financial InstitutionSME Leasing Limited 7,425 10,328

b)274,622 409,63281,552 65,899

356,174 475,531

c) 3,453 2,991d) 20,205 151e) - 296

875,560 960,293

25 MARK-UP/RETURN/INTEREST EXPENSED

Deposits 133,443 62,852160,260 140,257

Loan from the State Bank of Pakistan 33,378 186,910Amortisation of premium/ discount on investments 50,890 62,259Brokerage and commission 1,056 670

929 1,114379,956 454,062

26 OTHER INCOME

Net profit on sale of property and equipment 405 11,956Profit on off-balance sheet items 26.1 - 734 Others 9,666 10,356

10,071 23,046

26.1 Profit on off-balance sheet items

Equity Participation Funds - 734- 734

Extended by:

Securities sold under repurchase agreements

Bank charges

On Securities purchased under resale agreementsOthers

On Loans and advances to:

On Deposits with financial institutions

On Investments in:i) Available for sale Securitiesii) Held to Maturity Securities

i) Customers

SME Bank LimitedNotes to the Financial Statementsfor the year ended December 31, 2007

Notes 2007 200627 ADMINISTRATIVE EXPENSES Rupees in '000

Salaries, allowances, etc. 313,822 333,406Charge for defined benefit plan- pension fund 23,030 20,481- unfunded gratuity scheme 6,575 6,020Contribution to defined contribution plan-benevolent fund 782 745Non-executive directors' fees, allowances and other expenses 908 552Rent, taxes, insurance, electricity, etc. 54,304 48,504Legal and professional charges 8,808 12,627Communications 6,607 7,618Repairs and maintenance 9,686 10,632Finance charges on leased assets 1,068 743Stationery and printing 3,793 4,211Advertisement and publicity 463 5,796Depreciation 12.2 30,046 30,153Amortization 12.3 3,264 3,034Auditors' remuneration 27.1 2,099 1,804Staff separation costs 2,938 - Staff recovery costs 12,235 16,437Recovery expenses - outsourced portfolio 10,975 16,515Recruitment expenses 438 518Travel and transport 7,263 9,595Vehicle running and maintenance expenses 11,109 10,804Entertainment 1,368 1,163Training 1,071 846Books, subscription and newspapers 2,122 2,356Other expenses 11,690 9,307

526,464 553,867

27.1 Auditors' remuneration

Audit fee 1,399 1,100

525 525Out-of-pocket expenses 175 179

2,099 1,804

28 OTHER CHARGES

Penalties imposed by State Bank of Pakistan 819 158

Special certifications, half yearly review and audit ofconsolidated financial statements

SME Bank LimitedNotes to the Financial Statementsfor the year ended December 31, 2007

29 TAXATION 2007 2006Rupees in '000

For the year- Current 50,863 72,034- Deferred (9,171) 6,464

41,692 78,498

29.1 Relationship between tax expense and accounting profit

Accounting profit for the current year 152,094 231,685% %

Applicable tax rate 35 35Tax effect of

- income chargeable at reduced tax rates (0.20) (0.15)-

(6.03) - - Income exempt from tax (5.90) (0.99)- expenses that are not deductible for tax purposes 4.54 0.02

Average effective tax rate 27.41 33.88

30 BASIC/DILUTED EARNINGS PER SHARE

Profit for the year 110,403 153,187

Weighted average number of ordinary shares 227,636,794 200,000,000

Basic/diluted earnings per share 0.48 0.77

There is no dilutive effect on basic earnings per share of the Bank.

31 CASH AND CASH EQUIVALENTS 2007 2006Rupees in '000

Cash and Balance with Treasury Banks 286,705 311,954Balance with other banks 52,980 125,704Call money lending - 200,000

339,685 637,658

32 STAFF STRENGTH

Permanent 317 318Temporary/ on contractual basis 292 333Bank's own staff strength at the end of the year 609 651Outsourced 13 16Total number of employees at the end of the year 622 667

Number

temporary differences on which deferred tax has beenenacted at reduced tax rate for subsequent years

Number of shares

Rupees in '000

Rupees

SME Bank LimitedNotes to the Financial Statementsfor the year ended December 31, 2007

33. EMPLOYEE BENEFIT PLANS

33.1 Defined benefit pension and gratuity plan

33.1.1 General description

The scheme entitles the members to:

-

-

2007 2006

33.1.2 The amounts recognised in the balance sheet are as follows:

Present value of defined benefit obligation 293,103 245,335 Fair value of plan assets (286,310) (245,919) Deficit/(surplus) 6,793 (584) Unrecognized actuarial loss (11,355) (6,347) Unrecognised past service cost (7,615) (8,703) Net asset (12,177) (15,634)

33.1.3 The amounts recognised in the profit and loss account are as follows:

Current service cost 18,401 18,386 Interest cost 24,534 21,565 Expected return on plan assets (24,592) (20,558) Past service cost - over the vesting period 1,088 1,088 Current year acturial losses recognized 3,599 - Reversal of amount not recognised as an asset - - Expense for the year 23,030 20,481

33.1.4 Actual return on plan assets 21,937 20,813

2007 2006

33.1.5 Changes in present value of defined benefit obligation

Present value of obligation at the beginning of the year 245,335 215,652 Current service cost 18,401 18,386 Interest cost 24,534 21,565 Benefits paid (1,119) (1,037) Actuarial (gain)/ loss 5,952 (9,231) Present value of obligation at the end of the year 293,103 245,335

Bank operates an approved defined benefit pension and gratuity fund for all its permanent and regular employees.Contributions are made in accordance with the actuarial recommendations.

Gratuity payable to members who have completed a minimum of 5 years of service and total service on retirement orcessation of service or death is less than 10 years.

Pension payable to members who have completed a minimum of 10 years of service with the Bank on retirement at age ofsixty years or on completion of 25 years of service with the Bank or on permanent disability or on death during service.

Rupees '000

The expected return on plan assets is based on the market expectations and depend upon the asset portfolio of the Fund, at thebeginning of the year. Expected yield on fixed interest investments is based on gross redemption yields as at the balance sheet .

Rupees '000

SME Bank LimitedNotes to the Financial Statementsfor the year ended December 31, 2007

2007 2006

33.1.6 Changes in fair value of plan assets

Fair value of opening plan assets 245,919 205,580 Expected return on plan assets 24,592 20,558 Contributions 19,573 20,563 Benefits paid (1,119) (1,037) Actuarial gain/ (loss) (2,655) 255 Fair value of closing plan assets 286,310 245,919

33.1.7 Break-up of category of assetsRupees '000 % Rupees '000 %

Defence savings certificates 116,624 41% 140,901 57%Term deposits receipts 163,179 57% 96,343 39%Bank deposit accounts 6,507 2% 8,675 4%

286,310 100% 245,919 100%

33.1.8 Principal actuarial assumptions

2007 2006% %

Discount rate - per annum 10.00% 10.00%Expected return on plan assets - per annum 10.00% 10.00%Salaries increase rate - per annum 9.00% 9.00%

33.1.9 Disclosure for current and previous four annual periods

2007 2006 2005 2004 2003

Present value of obligation 293,103 245,335 215,652 340,506 330,426

Fair value of plan assets (286,310) (245,919) (205,580) (288,426) (224,553)

(Surplus)/ deficit 6,793 (584) 10,072 52,080 105,873

Experience adjustments onplan liabilities (5,953) 9,231 (47,448) 51,548 15,836

Experience adjustments onplan assets 2,655 255 (9,789) 38,669 1,034

2007 2006

2007 2006

Rupees '000