Embed Size (px)

Citation preview

China Bond Connect Market: What You Need to Know

January 23, 2018

ICI WebinarAgenda» Introductions» Key developments in the China Bond Connect

market»Opportunities in China’s bond market»Operational considerations for regulated funds»Regulatory update and outlook

1

Panelists

2

Lisa MartinezModerator

Assistant Vice President, Network

ManagementCapital Group

Julien MartinGeneral Manager

Bond Connect Company Limited

Barnaby NelsonManaging DirectorStandard Chartered

Patrick WongHead of China Sales

and Business Development

HSBC

CPE Credit

If you are interested in receiving CPE credit for today’s webinar, please enter the following code in the text box now.

593

3

» Patrick Wong» Head of China Sales and Business Development

» HSBC Securities Services

Opening up more opportunities in the world’s third-largest bond marketBond Connect

5

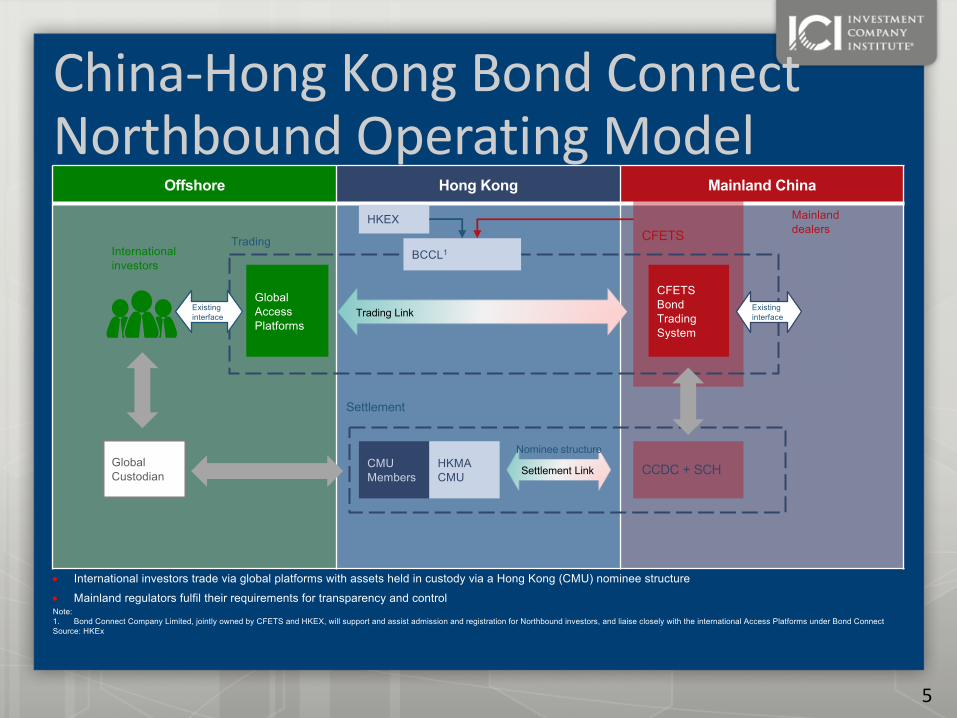

Offshore Hong Kong Mainland China

China-Hong Kong Bond ConnectNorthbound Operating Model

Note:1. Bond Connect Company Limited, jointly owned by CFETS and HKEX, will support and assist admission and registration for Northbound investors, and liaise closely with the international Access Platforms under Bond ConnectSource: HKEx

• International investors trade via global platforms with assets held in custody via a Hong Kong (CMU) nominee structure• Mainland regulators fulfil their requirements for transparency and control

International investors

Global Custodian

Global Access Platforms

HKEX

CMU Members

HKMA CMU

CFETS

CFETS Bond Trading System

CCDC + SCH

Mainland dealers

BCCL1Trading

Settlement

Trading Link

Settlement Link

Existing interface

Existing interface

Nominee structure

5

Comparison between Bond Connect North Bound and CIBM Direct ProgramA detailed comparisonAspect Bond Connect North Bound CIBM Direct Eligibility and Market Entry

Quota • No • As per registered amount

Trading platform

• Through HK trading infrastructure, Tradeweb for Day 1, connecting to CFETS.

• Offshore investors to connect with HK trading infrastructures.

• Each investor will maintain a trading account with CFETS in its own name.

• CFETS • Each investor will maintain a trading account with

CFETS in its own name• Trading agent to conduct trade on behalf of investors

Eligible investors• Follow PBOC Notice [2016] No. 3 and Yinfa [2015]

No.220 (i.e. same as CIBM Direct)

PBOC Notice [2016] No.3:• FIs including commercial banks, insurance, securities

companies, asset managers• Products launched by these FisYinfa [2015] No.220: • Foreign central banks, international orgnaisations and

sovereign wealth funds

Market entry/Registration

• Eligible overseas investors may entrust CFETS or registration agents recognized by PBOC to apply for registration to the PBOC Shanghai Head Office. Overseas investors may provide registration documents to the above-mentioned registration agents directly or through their overseas counterparts.Registration could be at product level.

• Bond Connect Co. Ltd, a JV between HKEx and CFETS has been set up to support and assist investors admission

• Onshore account opening• Registration at fund level• Registration process through a Bond Settlement Agent• Central banks may submit registration directly to

PBOC HQ

6

Comparison between Bond Connect North Bound and CIBM Direct Program A detailed comparison (cont’d)Aspect Bond Connect North Bound CIBM Direct

Investment Scope and Trading

Investment scope• Cash bonds. Scope same as CIBM Direct• Investors can also access interbank bond market

primary issuance

• Cash bonds. All types of bonds denominated in RMB and traded in the CIBM. Subscription for primary issue are also permitted

Hedging tools available • CNY FX hedging will be provided by “CFETS Direct Members” in Hong Kong

• FX (Spot, Forward, Swap, Options), bond lending, bond forward, IRS, CCS, FRA

Trading• Investors trade by way of RFQ directly with the

onshore Bond Connect Market Makers as counterparty

• Investors trade directly with CEFTS members

Settlement and custodian arrangement

Settlement cycle

• T+0, T+1 and T+2 (Note: the market deadline of 10 am on SD makes it impractical for intermediaries to support T+0 settlement. Investors are requested to negotiate a T+1 or T+2 settlement cycle to avoid settlement failure.)

• T+0, T+1 and T+2

Settlement account structure

• SCH/CDC are the ultimate central securities depository (CSD)

• HKMA CMU will be the nominee holder of the bonds• Investors will need to open a segregated CMU sub-

account via its Global Custodian or directly via a CMU member. Remarks: Bond Connect Application requires investor to provide such CMU sub-account number

• Investors need to open relevant accounts with PBOC (Special RMB account), CCDC, SCH and CFETS

Settlement method• DVP for SCH and Delivery-against-Payment for CDC.

Settlement on gross basis with the relevant Bond Connect Market Makers as counterparty

• Delivery-versus-Payment (DVP) and settlement on gross basis with the relevant CFETS member as counterparty

7

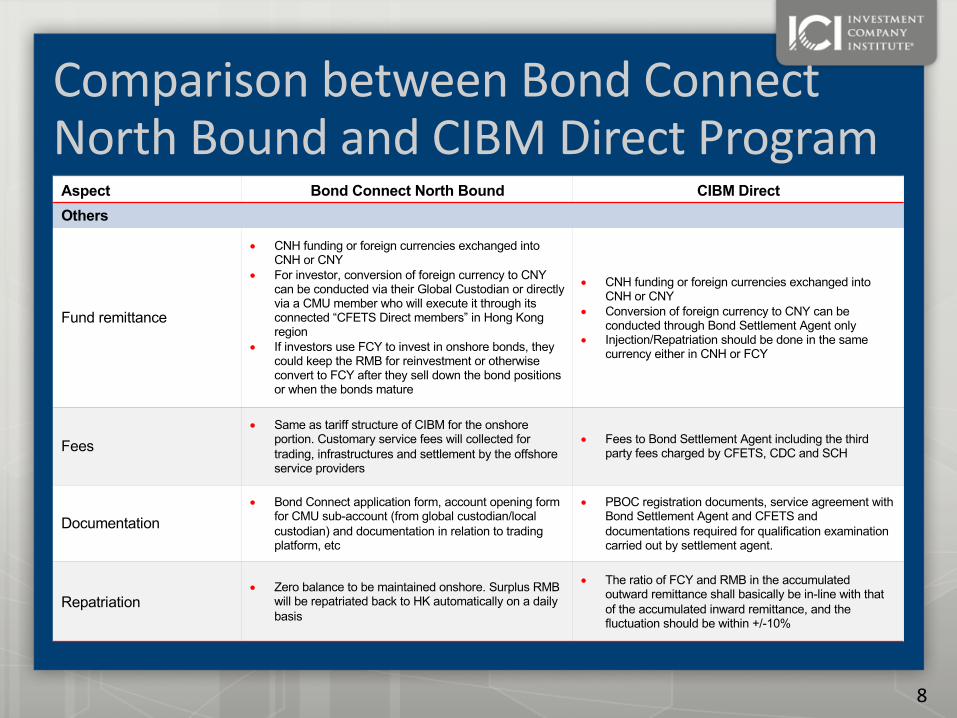

Comparison between Bond Connect North Bound and CIBM Direct ProgramA detailed comparison (cont’d)Aspect Bond Connect North Bound CIBM Direct

Others

Fund remittance

• CNH funding or foreign currencies exchanged into

CNH or CNY

• For investor, conversion of foreign currency to CNY

can be conducted via their Global Custodian or directly

via a CMU member who will execute it through its

connected “CFETS Direct members” in Hong Kong

region

• If investors use FCY to invest in onshore bonds, they

could keep the RMB for reinvestment or otherwise

convert to FCY after they sell down the bond positions

or when the bonds mature

• CNH funding or foreign currencies exchanged into

CNH or CNY

• Conversion of foreign currency to CNY can be

conducted through Bond Settlement Agent only

• Injection/Repatriation should be done in the same

currency either in CNH or FCY

Fees

• Same as tariff structure of CIBM for the onshore

portion. Customary service fees will collected for

trading, infrastructures and settlement by the offshore

service providers

• Fees to Bond Settlement Agent including the third

party fees charged by CFETS, CDC and SCH

Documentation

• Bond Connect application form, account opening form

for CMU sub-account (from global custodian/local

custodian) and documentation in relation to trading

platform, etc

• PBOC registration documents, service agreement with

Bond Settlement Agent and CFETS and

documentations required for qualification examination

carried out by settlement agent.

Repatriation

• Zero balance to be maintained onshore. Surplus RMB

will be repatriated back to HK automatically on a daily

basis

• The ratio of FCY and RMB in the accumulated

outward remittance shall basically be in-line with that

of the accumulated inward remittance, and the

fluctuation should be within +/-10%

8

Comparison between Bond Connect North Bound and CIBM Direct Program

Aspect Bond Connect North Bound CIBM Direct

Others

Account Opening

• Investors need to onboard with Bond Connect market maker as trading counterparty

• As mentioned in settlement account structure above, investors will need to open a CMU sub-account via its Global Custodian or directly via a CMU member

• Bond Settlement Agent assists investors to open relevant accounts with PBOC (Special RMB account), CCDC, SCH and CFETS

Taxation • CGT exempted. No withholding mechanism for VAT and CIT

• CGT exempted. No withholding mechanism for VAT and CIT

9

Comparison between Bond Connect North Bound and CIBM Direct ProgramAdvantages and disadvantages

Bond Connect North Bound CIBM Direct

Advantages

• Trading through offshore trading platform(s) that investors

are familiar with

• Investors are registered as direct CFETS member

• Bond coupons and repayment will be automatically

repatriated back to HK on the date of payment

• Nominee account structure: Bonds will be held through

sub-custodian in the CMU account. No need to open

accounts with CDC/SCH

• CNY FX conversion and derivatives can be traded with

offshore CFETS FX settlement bank. Offshore

documentations are used for derivative hedging

transactions

• OTC trading with all CFETS members

• Dedicated service from the Bond Settlement Agents

• Wider scope of hedging tools are available including FX

(Spot, Forward, Swap, Options), bond lending, bond

forward, IRS, CCS, FRA

Disadvantages • Only FX hedging tools are available

• Trading with Bond Connect Market Makers only

• Except for Central Banks, investors need to trade bonds

and hedge through their appointed Bond Settlement

Agents (“BSAs”)

• Onerous documentation including service agreement with

BSAs, account opening with CFETS/CDC/SCH

• Onshore documentation for derivatives hedging

transactions

10

» This document does not necessarily deal with every important topic relating to Bond Connect or cover every aspect of the topics with which it deals. Certain clearing and trading rules and regulations are not yet completely promulgated by the relevant authorities, regulatory bodies and/or exchanges and therefore their understanding might be subject to changes in the future. HSBC is under no obligation to keep current the information in this document. Clients are advised to pay close attention to any rules, regulation and announcement published by the relevant authorities, regulatory bodies or exchanges.

» This document is issued by The Hongkong and Shanghai Banking Corporation Limited (HSBC). The information contained herein is derived from sources we believe to be reliable, but which we have not independently verified. HSBC makes no representation or warranty (express or implied) of any nature nor is any responsibility of any kind accepted with respect to the completeness or accuracy of any information, projection, representation or warranty (expressed or implied) in, or omission from, this document. No liability is accepted whatsoever for any direct, indirect or consequential loss arising from the use of this document. Any information (including market date, prices, values or levels) contained here are indicative only and any examples given are for the purposes of illustration only and may vary in accordance with changes in market conditions. The opinions in this document constitute our present judgment, which is subject to change without notice. We are not obliged to enter into any actual trade with you based on the any information contained herein. This document does not constitute an offer for, or advice that you should enter into, the purchase or sale of any security, commodity or other investment product or investment agreement, or any other contract, agreement or structure whatsoever. This material is intended for distribution to, or use by, Professional Investors only, as defined in the Hong Kong Securities and Futures Ordinance. The document is intended to be distributed in its entirety. Unless applicable laws permit otherwise, you must contact a HSBC Group member in your home jurisdiction if you wish to use HSBC Group services in effecting a transaction in any investment mentioned in this document. This document, which is not for public circulation, must not be copied, transferred or the content disclosed, to any third party and is not intended for use by any person other than the intended recipient or the intended recipient's professional advisers for the purposes of advising the intended recipient hereon.

» HSBC does not provide legal, tax, accounting, regulatory or other specialist advice and you should make your own arrangements in respect of such matters accordingly. No consideration has been given to the particular investment objectives, financial situation or particular needs of any recipient, you should conduct relevant due diligence and analysis, and seek necessary independent professional advice. You are responsible for making an independent assessment and obtaining specialist professional advice in relation to the merits of the proposals contained herein. In particular, this document may contain certain references to regulation. HSBC makes no representation that the references to regulation, if contained herein, are exhaustive. There could be other references to regulation that may also be relevant to the proposals. HSBC does not give advice on regulation. You should consult your own advisers on regulation.

» Copyright. The Hongkong and Shanghai Banking Corporation Limited 2017. ALL RIGHTS RESERVED. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, on any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior written permission of The Hongkong and Shanghai Banking Corporation Limited.

» For additional information, please contact your local sales or trading representative.

Disclaimer

12

Questions

If you have questions for the panelists,please submit them using the text box.

12

CPE Credit

If you are interested in receiving CPE credit for today’s webinar, please enter the following code in the text box now.

742

13

2018 ICI BOND CONNECT WEBINAR

23 JANUARY 2018

Julien MartinGeneral Manager

Bond Connect Company Limited

DisclaimerThis document and the information contained herein may not be used other than by the person to whom it is addressed or distributed to and may not be reproduced in any form or transferred to any person. The information contained in this document is for general informational purposes only and does not constitute an offer, solicitation, invitation or recommendation to buy or sell any securities or to provide any investment advice or service of any kind. This document is not directed at, and is not intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation or which would subject any of Hong Kong Exchanges and Clearing Limited (“HKEX”), China Foreign Exchange Trade System & National Interbank Funding Centre (“CFETS”), Bond Connect Company Limited (“BCCL”), China Central Depository & Clearing Co., Ltd (“CCDC/ChinaBond”) or Shanghai Clearing House (“SHCH”) (together, the “Entities”, each an “Entity”), or any of their affiliates, or any of the companies that they operate, to any registration requirement within such jurisdiction or country.

No section or clause in this document may be regarded as creating any obligation on the part of any of the Entities. Rights and obligations with regard to the trading and settlement of any securities effected on the CFETS, including through the Bond Connect, shall be set out solely in the applicable rules of the Entities, as well as the applicable laws, rules and regulations of Mainland China and Hong Kong in effect from time to time.

Although the information contained in this document is obtained or compiled from sources believed to be reliable, none of the Entities guarantee the accuracy, validity, timeliness or completeness of the information or data for any particular purpose, and none of the Entities or the companies that they operate or their respective affiliates, agents, nominees, representatives, officers and employees shall accept any responsibility for, or be liable for, errors, omissions or other inaccuracies in the information or for the consequences thereof. The information set out in this document is provided on an “as is” and “as available” basis and may be amended or changed in the course of implementation of Bond Connect. It is not a substitute for professional advice which takes account of your specific circumstances and nothing in this document constitutes legal advice. If you are in any doubt about the contents of this document, you should seek independent professional advice. None of the Entities or any of the companies that they operate or their respective affiliates, agents, nominees, representatives, officers and employees shall be responsible or liable for any cost, expense, loss or damage, directly or indirectly, howsoever caused, of any kind, arising from the use of or reliance upon any information provided in this document, or in the presentation given.

16

Structural Growth of China’s Bond Market

0

2

4

6

8

10

'08 '09 '10 '11 '12 '13 '14 '15 16 '17

Mar

Credit Bonds Rate Bonds

China’s bond market is now the third largest in the world, and is predicted to double in size in the next 10 years

Growth of China’s Bond market

Amount Outstanding, USD

trillions

CAGR 20%

US$10.1tn

Bank Assets Equities Bonds

USD28 tn

USD8.5tn

USD10.1 tn

~90% Interbank

~10% Exchange55% SSE

45% SZSE

Outstanding, USD tn Relative to GDP

20

40

US JP China DE FR UK

212%

87%249% 146% 171% 157%

China’s Domestic Funding Markets

Sources: WIND, CBRC (Jun 2017), IMF, SIFMA

Jun

17

USD28 tn

Relative to GDP

Foreign Participation in China’s Bond Market

Sources: ChinaBond, Bloomberg, BIS

Foreign participation still only ~2%, well below the international average for large bond markets

68%64%

46%41% 39% 38%

29%

13%8%

2.6%

DE FR AU UK IT CA US RU JP China

International Bond Market ComparisonForeign Participation in the CIBM

Average: 38.5%

15%

Achievable target

Foreign Ownership %

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

-

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

Aug-

16

Sep-

16

Oct

-16

Nov

-16

Dec

-16

Jan-

17

Feb-

17

Mar

-17

Apr-1

7

May

-17

Jun-

17

Jul-1

7

Bond Holdings,RMB trillions

As % of total

2.6%

18

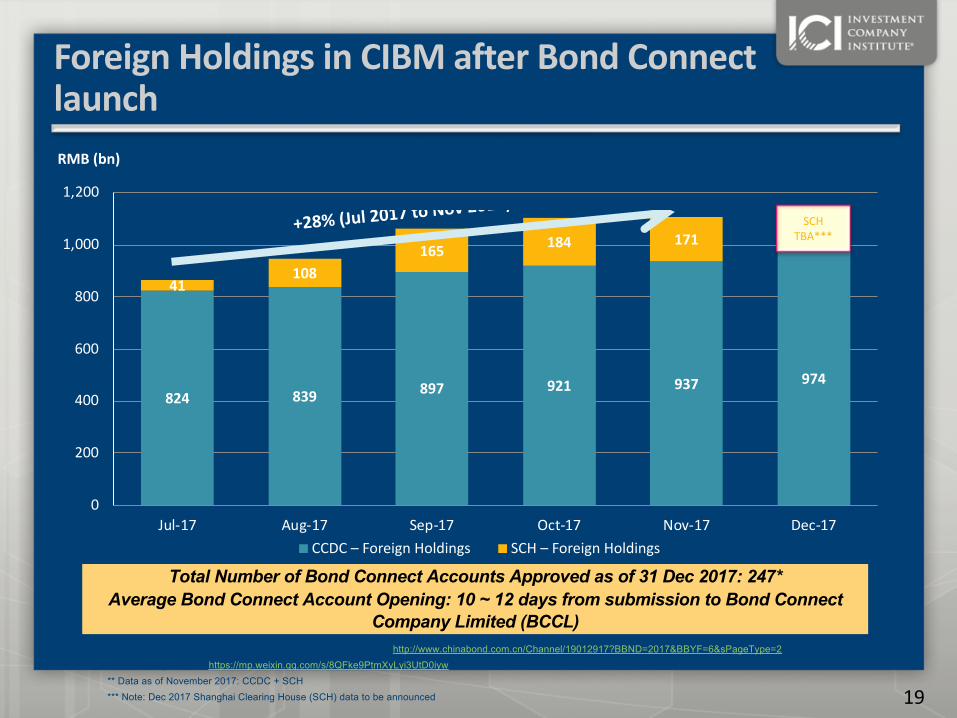

Foreign Holdings in CIBM after Bond Connect launchChina Central Depository & Clearing (CCDC) and Shanghai Clearing House (SCH)

Source: (1) SCH: http://www.shclearing.com/sjtj/tjyb/ (2) CCDC: http://www.chinabond.com.cn/Channel/19012917?BBND=2017&BBYF=6&sPageType=2*Published by CFETS: https://mp.weixin.qq.com/s/8QFke9PtmXyLyi3UtD0iyw** Data as of November 2017: CCDC + SCH*** Note: Dec 2017 Shanghai Clearing House (SCH) data to be announced

824 839 897 921 937 974

41108

165 184 171

0

200

400

600

800

1,000

1,200

Jul-17 Aug-17 Sep-17 Oct-17 Nov-17 Dec-17

RMB (bn)

CCDC – Foreign Holdings SCH – Foreign Holdings

+28% (Jul 2017 to Nov 2017)

Total Number of Bond Connect Accounts Approved as of 31 Dec 2017: 247*Average Bond Connect Account Opening: 10 ~ 12 days from submission to Bond Connect

Company Limited (BCCL)

SCHTBA***

19

Questions

If you have questions for the panelists,please submit them using the text box.

19

10th January 2018

China - Hong Kong Bond Connect

Regulatory Update and Outlook

Overview

• Regulatory requirements

• Market requirements

Key Developments

• Luxembourg• Ireland• Other markets

Regulatory approvals • JPMorgan

• Bloomberg / Barclays

• WGBI

Index Inclusion

22

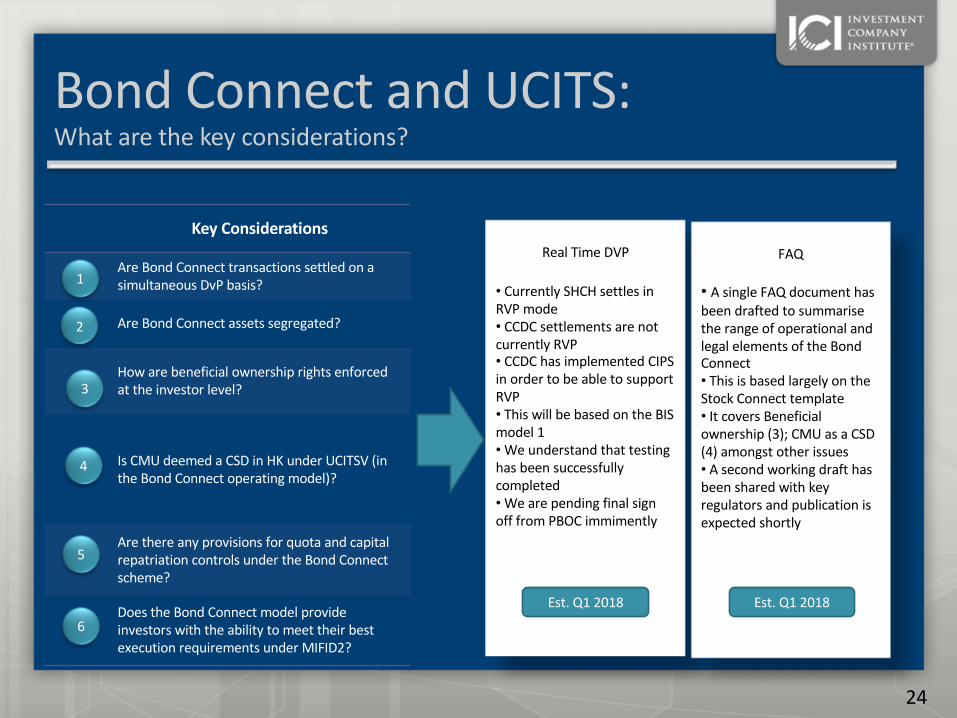

Bond Connect and UCITS:What are the key considerations?

Key Considerations Status Conclusion

Are Bond Connect transactions settled on a

simultaneous DvP basis?

SHCH – Simultaneous DvP

CCDC – Linked DVP (cash before bond delivery at all times)

Are Bond Connect assets segregated?

Assets are distinctly segregated into three levels including both at the onshore

and offshore level - further mandatory segregation is required at the offshore

level for each beneficial owner

How are beneficial ownership rights enforced

at the investor level?

CMU is only responsible as a nominee holder. The end investors are the

beneficiary owners who have bondholder rights, enforcement rights and rights

to take legal actions – including onshore.

Is CMU deemed a CSD in HK under UCITSV (in

the Bond Connect operating model)?

Since the responsibilities of CMU under Bond Connect perform similarly with

HKCSS under Stock Connect, we anticipate, CMU will issue a guidance note to

confirm they should be recognized as a CSD under the Bond Connect Scheme

Are there any provisions for quota and capital

repatriation controls under the Bond Connect

scheme?

No quota and capital repatriation controls under Bond Connect scheme

Does the Bond Connect model provide

investors with the ability to meet their best

execution requirements under MIFID2?

Under Bond Connect, Tradeweb creates a higher pricing transparency and a

more efficient pricing mechanism. Therefore, achieving the best execution

requirements under MIFID2.

1

2

3

4

5

6

23

Bond Connect and UCITS:What are the key considerations?

Key Considerations

Are Bond Connect transactions settled on a simultaneous DvP basis?

Are Bond Connect assets segregated?

How are beneficial ownership rights enforced at the investor level?

Is CMU deemed a CSD in HK under UCITSV (in the Bond Connect operating model)?

Are there any provisions for quota and capital repatriation controls under the Bond Connect scheme?

Does the Bond Connect model provide investors with the ability to meet their best execution requirements under MIFID2?

1

2

3

4

5

6

Real Time DVP

• Currently SHCH settles in RVP mode• CCDC settlements are not currently RVP• CCDC has implemented CIPS in order to be able to support RVP• This will be based on the BIS model 1•We understand that testing has been successfully completed•We are pending final sign off from PBOC immimently

FAQ

• A single FAQ document has been drafted to summarise the range of operational and legal elements of the Bond Connect• This is based largely on the Stock Connect template• It covers Beneficial ownership (3); CMU as a CSD (4) amongst other issues• A second working draft has been shared with key regulators and publication is expected shortly

Est. Q1 2018 Est. Q1 2018

24

TBC

Key DevelopmentsMarket Requirements

CNY funding

Tax

Additional trading platforms

Failed trades

Change of custodians

Hedging

CNY Repos and IRS

Fully available but variable across different FX banks

Same as CIBM Direct

Pending confirmation of Bloomberg

Roles and responsibilities for reporting to be included in FAQ

Completed: only for investors who have not yet traded

Fully available but variable across different FX banks

Widely expected in early 2018

Market data Trade data is available for SHCH, not yet for CCDC

Block trading May be available at end of Q1 (dependent on CFETS)

Extended trading hours Under consideration by Chinese authorities

Expe

cted

in Q

1/Q

2Co

nfirm

25

Regulatory Approvals

Luxembourg

• A small number of funds have been approved to use the Bond Connect for less than 10% of AUM

• A small number of funds have been approved to use the Bond Connect as a core part of their investment strategy (ie >10% of AUM): on the condition that they dont start using the Bond Connect until a suitable solution to the counterparty risk issue is put in place.

• Will approve funds for large scale participation in Bond Connect once counterparty risk issue is fully resolved

Ireland

• Currently gathering information on the Bond Connect

• CBI is pending a formal submission from IFIA on the Bond Connect

• Once received, CBI wil review the submission and consult the industry for any specific points

• At the end of the consultation, CBI will issue their own FAQ on the Bond Connect: detailing how depobankscan begin to use the mechanism

Others

• Key regulators (Japan, Hong Kong, etc.) remain focused on real time DVP point

• No other issues identified by other regulators to date

Est. Q1 2018 Est. Q2 2018 Est. Q1 2018

26

Bond Index Inclusion• On 30 November 2015, the Executive Board of the International Monetary Fund (IMF) completed the regular five-

yearly review of the basket of currencies that make up the Special Drawing Right (SDR), and decided to include the RMB into the currency basket of SDR. The new basket will become effective on October 1, 2016.

Inclusion of RMB into the currency basket of SDR

• The potential inclusion of China debt instruments in Global Bond Indices could have a significant impact on investors in benchmarked fixed-income strategies, as they would need to restructure their portfolios to reflect the indices’ realignment.

• Bloomberg Barclays Fixed Income Indices: On 24 January 2017, Bloomberg announced that 3 new indices including CIBM would be enacted with effect from1 Mar 2017o Combining Global Aggregate Index and the government and policy bank component of the China Aggregate

Indexo A new EM Local Currency Government + China Indexo A new EM Local Currency Government + China Index (with 10% cap per country)

• Citi Fixed Income Indices: On 06 March 2017, they announced the inclusion eligibility of Chinese onshore bonds to its Emerging Markets and Regional Government Bond Indices. o China is eligible to join three existing government bond indices, Emerging Markets Government Bond

Index(“EMGBI”), Asian Government Bond Index(“AGBI”) and Asia Pacific Government Bond Index(APGBI”). For EMGBI and AGBI, announcement will be made on June to see whether indices will be available in February 2018. For APGBI, China will enter in February 2018.

o China is also eligible to join one new related index – World Government Bond Index – Extended (“WGBI-Extended”), which will be available in July 2017.

Bond Index Inclusion

Bond Connect • Bond Connect is formally launched on 3 July 2017.• Only Northbound Trading is allowed in the initial phase.• This scheme compliments the existing China market access channels, QFII, RQFII and CIBM Direct. Currently,

foreign participation in China bond market still remains low (less than 2%)

26

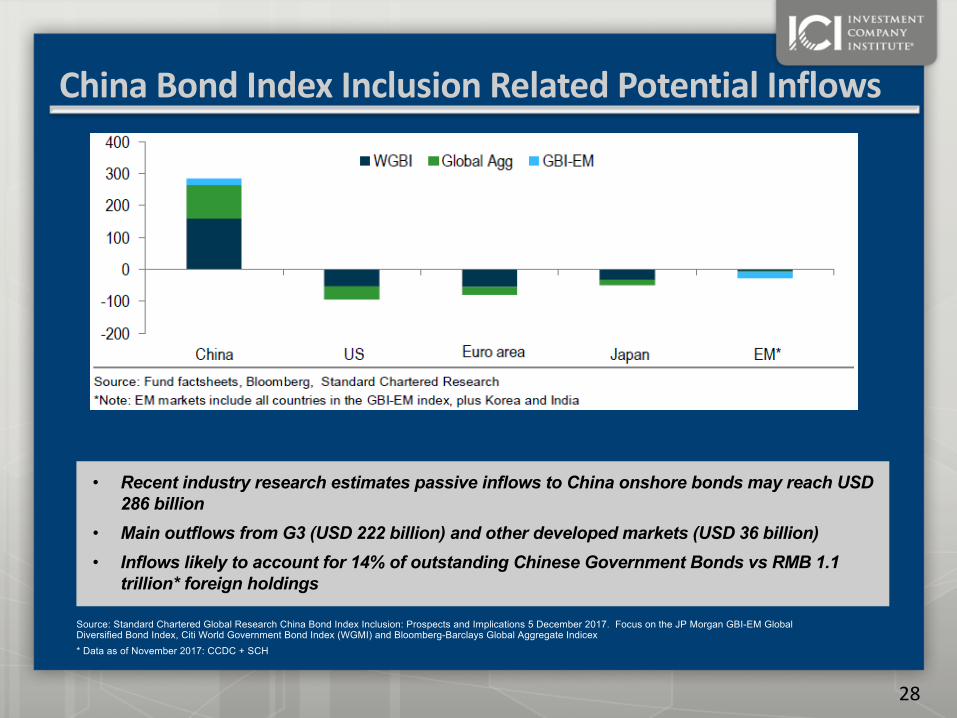

China Bond Index Inclusion Related Potential Inflows

• Recent industry research estimates passive inflows to China onshore bonds may reach USD 286 billion

• Main outflows from G3 (USD 222 billion) and other developed markets (USD 36 billion)• Inflows likely to account for 14% of outstanding Chinese Government Bonds vs RMB 1.1

trillion* foreign holdings

Source: Standard Chartered Global Research China Bond Index Inclusion: Prospects and Implications 5 December 2017. Focus on the JP Morgan GBI-EM Global Diversified Bond Index, Citi World Government Bond Index (WGMI) and Bloomberg-Barclays Global Aggregate Indicex* Data as of November 2017: CCDC + SCH

28

Inclusion Criteria in Major Emerging Market Bond Indices

Source: Standard Chartered Global Research China Bond Index Inclusion: Prospects and Implications 5 December 2017

ü Onshore Accessibility, Tradability and Convertibility

ü Absence of Capital Control

ü FX hedgeabilityHard Criteria

Soft Criteria

? Settlement Risk - Lack of True Delivery vs Payment (DVP) settlement

? Full services offering by global custody banks and local settlement banks

? Further clarification on tax

? FX operational Issues

Soft criteria are subject to resolution in 3 to 6 months pending regulatory approval

29

Index Inclusion: SCB Research ViewCore index providers

JPMorgan• September 2017 review: China not eligible but remains on Index watch• Re-assessment in Q2/Q3 2018• Likely impact USD20bn

Bloomberg-Barclays• Pending confirmation of 2017 review• Next review in Q4 2018•Likely impact USD107bn

World Gov’t bond Index • Next review in Q4 2018• Likely to be most conservative index provider (no new inclusions since 1984)• Likely impact USD159bn

80% chance for China bonds to be included in one of the major global bond indices in the 2018 governance review, with actual inclusion starting

in 2019

China has met ‘hard’ inclusion criteria, but still gaps to meet ‘soft’ criteria

Our analysis showed that some Asia LCY markets already included in the indices have more

restrictive FX access than China

Potential inflows to China is significant, at USD 286bn, which is about 14% of outstanding CGBs

or government budget deficit in 2017

The bulk of the outflows will likely to come from G3 and other developed markets, instead of EM

LCY bond markets

Key Deliverables

‘Must Haves’• Settlement Risk / DVP• Global Custodians’ readiness (on CNY)• Tax • FX Operational issues

Nice-to-have’s• Harmonisation of schemes• CNY access via multiple banks• Block trading

30

CPE Credit

If you are interested in receiving CPE credit for today’s webinar, please enter the following code in the text box now.

681

30

Questions

If you have questions for the panelists,please submit them using the text box.

31

Evaluation

Please click here to complete the webinar evaluation.

32