Embed Size (px)

Citation preview

Discussion Paper/Document d’analyse2008-5

China’s Exchange Rate Policy:A Survey of the Literature

by Robert Lafrance

www.bank-banque-canada.ca

Bank of Canada Discussion Paper 2008-5

March 2008

China’s Exchange Rate Policy:A Survey of the Literature

by

Robert Lafrance

International DepartmentBank of Canada

Ottawa, Ontario, Canada K1A [email protected]

Bank of Canada discussion papers are completed research studies on a wide variety of technical subjectsrelevant to central bank policy. The views expressed in this paper are those of the author.

No responsibility for them should be attributed to the Bank of Canada.

ISSN 1914-0568 © 2008 Bank of Canada

ii

Acknowledgements

I wish to thank Loyal Chow for research assistance and Larry Schembri for his helpful comments

and suggestions. All errors and omissions are mine.

d

tured

omic

as

uthor

rough

oving

ater

at

is put

sed.

ul de

pour

oulève

pire du

de

ar les

’auteur

en

s

ipale

à

trise de

du

ent à

caire et

Abstract

China’s integration into the world economy has benefited its people by reducing poverty an

raising living standards, and it has benefited the industrialized world by producing manufac

goods at lower cost. It has also raised geopolitical concerns as China’s power grows, econ

concerns as the manufacturing base in many industrialized countries erodes, and polemics

proposals of protectionist measures to counter China’s export growth are put forward. The a

reviews the literature on how China’s exchange rate regime could evolve and contribute, th

greater flexibility, to tempering domestic inflationary pressures and to facilitating an orderly

resolution of global imbalances. His main conclusions are that China would benefit from m

towards a more flexible exchange rate regime and allowing the People’s Bank of China gre

independence to pursue an inflation-control objective. In a transition phase, a managed flo

would be useful to limit volatility as firms adapt to the new system and the banking system

on a sounder footing, a monetary policy framework is put in place, and capital controls are

progressively eased. Shock therapy (a quick and pronounced revaluation) would be ill advi

JEL classification: F33, F36Bank classification: Exchange rate regimes

Résumé

L’intégration de la Chine dans l’économie mondiale profite à ce pays, où elle favorise le rec

la pauvreté et la hausse du niveau de vie, ainsi qu’aux États industrialisés, qui bénéficient

leur part de la baisse du coût de production des biens manufacturés. Mais cette intégration s

aussi des inquiétudes. Inquiétudes géopolitiques, du fait de la montée en puissance de l’em

Milieu, et inquiétudes économiques – dans le contexte de l’érosion du tissu manufacturier

nombreux pays industrialisés – auxquelles s’ajoute une dimension polémique, alimentée p

mesures protectionnistes proposées pour contrer la croissance des exportations chinoises. L

passe en revue les travaux publiés sur la manière dont une évolution du régime de change

Chine vers un flottement plus libre du yuan pourrait contribuer à l’atténuation des pression

inflationnistes intérieures et à la correction ordonnée des déséquilibres mondiaux. Sa princ

conclusion est que la Chine gagnerait à adopter à terme un régime de changes flottants et

accorder à sa banque centrale davantage de latitude pour la poursuite d’un objectif de maî

l’inflation. Pendant la transition, un régime de flottement dirigé aiderait à contenir la volatilité

taux de change, facilitant ainsi l’adaptation des entreprises, alors que les autorités s’attach

assouplir graduellement le contrôle des mouvements de capitaux, à assainir le système ban

iii

r un

piré.

à mettre en place un cadre approprié pour la conduite de la politique monétaire. Administre

remède de cheval, à savoir réévaluer le yuan de façon subite et marquée, serait ici mal ins

Classification JEL : F33, F36Classification de la Banque : Régimes de taux de change

iv

1

1 Introduction China has awakened. It has become the world’s fourth-largest economy. China’s large and growing trade surpluses, and the speed at which it has been able to accumulate international reserves, have raised tensions with its major trading partners, notably the United States. A moderation of these trends is seen as key to reducing what many consider unsustainable global imbalances.1 China’s integration into the world economy has benefited its people by reducing poverty and raising living standards, and it has benefited the industrialized world by producing manufactured goods at lower cost. It has also raised geopolitical concerns as China’s power grows, economic concerns as the manufacturing base in many industrialized countries erodes, and polemics as proposals of protectionist measures to counter China’s export growth are put forward.

We review the literature on how China’s exchange rate regime could evolve and contribute, through greater flexibility, to tempering domestic inflationary pressures and to facilitating an orderly resolution of global imbalances. The main thrust of this survey is that China should move towards a more flexible exchange rate regime. Our aim is not to predict when true exchange rate flexibility is most likely to occur. The decision to change China’s exchange rate regime (from a de jure float to a de facto float) will likely be based on political rather than economic grounds. We review the challenges that China faces (section 2), and what international experts suggest needs to be done (section 3).

Our main conclusions are that China would benefit from moving towards a more flexible exchange rate regime and allowing the People’s Bank of China (PBC) greater independence to pursue an inflation-control objective. In a transition phase, a managed float would be useful to limit volatility as firms adapt to the new system and the banking system is put on a sounder footing, a monetary policy framework is put in place, and capital controls are progressively eased.

2 China’s Dilemma 2.1 Overview

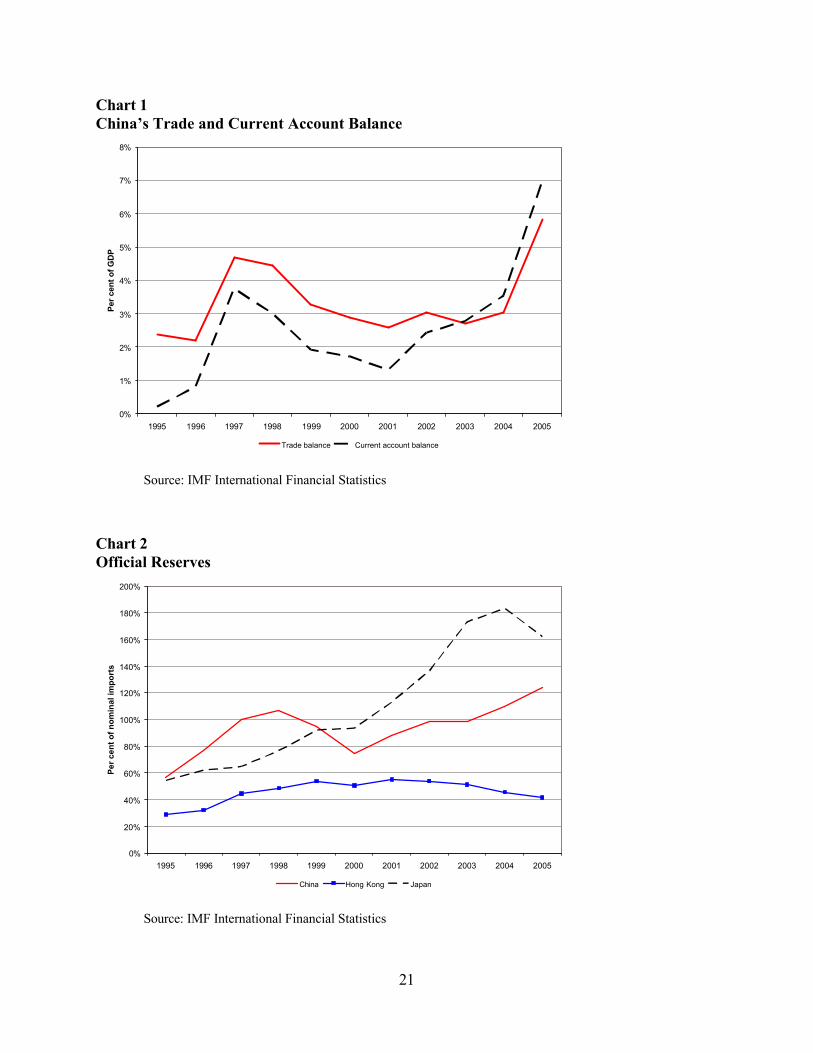

Since its accession to the World Trade Organization in 2001, China’s export-led growth strategy has forged ahead with new momentum as its trade balance has grown substantially (Chart 1). China’s surpluses are viewed by many, notably the U.S. authorities, as a major contributor to

1. Goldstein and Lardy (2007) provide an extensive overview of the debate on China’s current exchange rate policy.

2

global imbalances. Large trade surpluses over a number of years have allowed China to accumulate substantial international reserves (though much less than Japan), exceeding its precautionary needs for prudent import coverage, compared with Hong Kong, and to cover its modest international obligations (Chart 2). A point of contention is China’s exchange rate regime, which is nominally flexible but, in practice, is closely tied to the U.S. dollar. Given the avowed reluctance of the Chinese authorities to let the yuan appreciate relative to the U.S. dollar, and the weakness of the U.S. dollar in recent years in response to America’s growing external deficits, China’s real effective exchange rate is currently weaker than it was at the beginning of the decade (Chart 3). This reflects the fact that the United States accounts only for about one-fifth of China’s trade, as shown by the weights of its effective exchange rate (Chart 4).

China’s exchange rate regime has evolved over the past two decades. Following a period of substantive cumulative inflation, the official yuan–dollar rate was cut sharply in 1994, in tandem with unification of the official and parallel market exchange rates. During the Asian crisis, the authorities resisted substantial depreciation pressures. From 1997 until 21 July 2005, the Chinese authorities pegged the yuan to the U.S. dollar within a narrow range. On 21 July 2005, the PBC announced that it would implement a regulated, managed floating exchange rate system based on market supply and demand, and in reference to a basket of currencies.2 China’s new exchange rate regime was inspired by Singapore’s. McCallum (2006) notes, however, that China, in practice, is likely to allow less flexibility in its regime.3

Complementing this initiative, the PBC has introduced a number of measures to enhance the

operations of China’s foreign exchange market, including introducing an over-the-counter

market, launching yuan and foreign exchange swaps and yuan interest rate swaps on a pilot

basis, in preparation for a gradual exit of the central bank from the foreign exchange market

(Laurens and Maino 2007).

2. According to the PBC’s press release, the general objective of the exchange rate reform is to establish a sound, managed floating exchange rate system based on market supply and demand, and to maintain the basic stability of the exchange rate on a “rational and balanced level.” The official view is that a major fluctuation of the exchange rate would exert a substantial negative impact on China’s economic and financial stability, and is thus not in China’s fundamental interest (People’s Daily Online 2005).

3. Singapore has a basket-band-crawl exchange rate regime, with price stability as its goal. McCallum notes that its regime is not a fixed exchange rate. In fact, the Monetary Authority of Singapore (MAS) does not rely upon autonomous target values for the exchange rate, but merely values that are believed to be helpful in achieving MAS objectives for inflation. In contrast, the Chinese authorities are more concerned with foreign demand for Chinese goods, to sustain employment growth.

3

2.2 The views of international organizations

International organizations have argued for greater exchange rate flexibility. According to the International Monetary Fund (IMF), greater exchange rate flexibility on China’s part would enhance monetary policy independence; facilitate banking reforms; reduce China’s vulnerability to a devaluation of its foreign exchange reserves; and foster social stability and justice, since the underlying real appreciation that is required to rebalance the Chinese economy would have to come from higher domestic inflation if the exchange rate continued to be de facto pegged, hurting poor and rural households (IMF 2006).

An analysis by the European Central Bank (2007) argues that China’s trade surpluses are the result of internal structural weaknesses that encourage high savings.4 Greater exchange rate flexibility in China would improve investment decisions and boost consumers’ purchasing power. Getting the sequencing right in exchange rate reform and capital account liberalization is very important, however. Combined with fiscal reforms to reduce uncertainties surrounding the provision of basic public services, as well as financial reforms to remove borrowing constraints, these measures would reduce precautionary savings and boost consumption.

2.3 Business perspectives

China is not without allies in resisting an appreciation of its currency. Foreign direct investment (FDI) has been a driving force from the beginning in China’s export-led growth. Eichengreen (2005) points out that the peg has been beneficial for multinational companies, facilitating the implantation of diversified production facilities and sourcing from China. Between 1993 and 2003, 65 per cent of China’s exports came from foreign multinationals’ subsidiaries and joint ventures. The share of total exports by private domestically owned firms in China was less than 10 per cent.

In 1979, the Law on Joint Ventures was passed, providing a framework within which foreign firms were allowed to operate. Four special economic zones, or SEZs (Shenzhen, Zhuhai, Shantou, and Xiamen), were established in which foreign firms were offered preferential tax and administrative treatment. In the 1980s, Hong Kong- and Taiwan-based firms dominated, as they sought to benefit from low labour costs in SEZs for export markets. In the 1990s, new investors

4. Contributing factors include: an increase in precautionary savings tied to the need to provide for health care, basic education, and retirement; financial sector weaknesses, limiting consumer finance; and demographic trends, particularly the fall in the youth- dependency ratio in the wake of the one-child policy.

4

– Japanese, American, and European – came in to produce for the domestic market. Japanese, Taiwanese, Hong Kong, and Korean companies competing with China should welcome a revaluation. Other firms in these countries, however, have made, and continue to make, large investments in export-oriented production capacity in China. A revaluation would hit their profit margins hard.5

2.4 Academic views

Lim, Spence, and Hausmann (2006) argue, reflecting a view that is widely shared, that an appreciation of the yuan would help to reduce China’s trade surplus and to promote a more balanced development of the domestic economy. By its dampening effect, the appreciation would enable the economy to avoid going into a state of overheating as a result of a rise in consumption. It would also lead to an increase in the prices of traded goods relative to those of non-traded-goods, and thus promote faster growth in the non-traded-goods sectors, such as services. The magnitude of the appreciation is, however, impossible to estimate precisely ex ante. Hoggarth and Tong (2007) estimate, on the basis of standard trade equations, that a significant yuan appreciation would have mixed effects on the exports of the rest of Asia because of China’s role in the global supply chain. Countries in the region that export mainly consumer goods to China and third markets are unlikely to benefit significantly from yuan appreciation, while countries that supply capital and intermediate goods to China may in fact lose if China’s exports grow at a slower pace.

Cui (2007) challenges the view that China’s trade is dominated by processing activities with high import content. In effect, advancements in regional vertical integration have helped to extend China’s domestic value-added in the global supply chain. The domestic content of China’s exports has increased and its products have become more sophisticated following years of significant investment and technological upgrades.6 The rising sophistication of China’s exports points to a greater sensitivity of its exports and trade balance to foreign demand and price fluctuations than in the past, suggesting the need to revisit the elasticity pessimism of many

5. This division extends to the United States. For example, the National Association of Manufacturers did not endorse the filing of a trade complaint by a coalition of U.S. industrial and agricultural groups accusing China of manipulating its currency. Large- scale U.S.-based retailers sourcing in China would also lose from a revaluation.

6. In particular, machinery, electronic appliances, and transportation equipment account for more than half of its trade surplus, compared with a significant deficit only a few years ago.

5

studies that find that China’s trade balance has a limited response to an exchange rate appreciation.7

Europe could also benefit from more flexible Asian currencies (notably in the case of the yuan). Its exposure to shocks emanating from the United States would diminish, according to Markovic and Povoledo (2007). Based on a three-country, dynamic general-equilibrium model, their study shows that Asia’s choice of an exchange rate regime has a significant effect on Europe’s exposure to U.S. shocks in the case of a productivity shock to the U.S. non-traded-goods sector, and less so in the case of a demand shock or a productivity shock to the U.S. traded-goods sector.8 Bown et al. (2005) caution, however, that shifting demand towards U.S. suppliers would raise aggregate U.S. production only to the extent that new demand falls on sectors with the capacity to expand without significant price increases. Higher import prices might reduce total aggregate expenditure through a wealth effect that makes Americans feel poorer. While appreciation of the yuan could reduce the overall U.S. trade imbalance, the fundamental cause of the U.S. deficit lies within its internal saving–investment imbalance.

In contrast, and somewhat in isolation, McKinnon (2006) argues that the pressure on China to appreciate is misplaced. In his view, the expectation of a currency appreciation would seriously disrupt the natural tendency for wage growth (as well as prices in the non-traded sectors, owing to a Balassa-Samuelson effect) to match productivity growth. For McKinnon, this is déjà vu. From 1980 on, the erratically appreciating yen undermined the ability of relative wage adjustment to balance the international competitiveness between Japan and the United States, and the resulting deflationary pressure severely depressed the Japanese economy in the 1990s.9

7. Ahearne et al. (2007) report the results of a workshop that attempted to estimate the required currency movements between the U.S. dollar, the yen, the euro, and the yuan to re-establish more sustainable external balances. For the yuan, the range of required appreciation was from 5 to 25 per cent. The authors note that the uncertainty regarding the required appreciation reflects, in part, the difficulty in estimating the sensitivity of Chinese exports and imports to exchange rate movements.

8. Markovic and Povoledo’s results also show that, if China maintained the peg against the dollar, it would likely have only a modest impact on the overall volatility of Europe’s output and inflation; they depend mostly on domestic shocks in their calibration of the model.

9. McKinnon (2007) argues that the income and spending repercussions of a sharp appreciation against the world dominant currency are so strong for an international creditor that the effect of a currency appreciation on its trade surplus is ambiguous. First, the drop in exports would dampen income. Net inward FDI and investment would also decline, and large capital losses on foreign reserves would likely dampen growth. McKinnon argues that, in order to protect its agricultural sector, which would be most harmed by a currency appreciation, China should keep the exchange rate as its nominal anchor, allowing the currency to fluctuate by the difference between the rate of U.S. inflation and a domestic inflation target rate.

6

2.5 China’s perspective

Despite calls for greater exchange rate flexibility, and pressure from U.S. authorities to adopt measures to reduce China’s bilateral trade surplus with the United States, Chinese officials have been reluctant to move aggressively. Part of the reason stems from the lessons learned from the Asian crisis, notably that the stability of the yuan not only contributed to economic and financial stability in China but also probably helped to contain the further spread of the crisis (Zhou 2003). Another lesson learned was that Asian countries needed to maintain higher levels of international reserves for prudential reasons, since the IMF was seen to have responded inadequately to the crisis in the late 1990s (Zhou 2006).

The official perception is that China’s trade gains have come from its comparative advantage of an abundant low-cost supply of labour, the skills of which have increased over time, and not from a manipulation of its currency (Su 2004).10 Moreover, it is generally understood that balancing China’s trade would not solve the problem of the U.S. current account deficit, which reflects a fundamental saving–investment imbalance (Zhou 2006).

According to Lardy (2005), China’s caution can be explained by its internal policy environment that has prevailed since the 16th National Congress of the Communist Party, in the fall of 2002. Newly promoted party officials, strongly supported by provincial and local levels, have been anxious to promote job growth with local infrastructure projects, many of which are financed with funds borrowed from banks. In his view, the leadership appear to believe that they can use unprecedented monetary expansion to promote their pro-growth agenda. They have resisted the efforts of the central bank to consider greater exchange rate flexibility to reduce aggregate demand and facilitate the use of interest rate policy.

China’s prudent strategy is to ensure that its financial market is sufficiently developed before introducing full convertibility of the yuan for capital account transactions, phasing out capital controls, and allowing greater exchange rate flexibility (Zhou 2004). China has also embarked on a multi-pronged medium-term process to reduce its trade and current account surpluses. This includes measures to stimulate domestic demand and increase imports, measures to open up international capital transactions, and policies to reduce domestic savings and achieve greater exchange rate flexibility (Zhou 2006).

10. It is also worth noting that the ongoing and pervasive transformation of the economy makes it difficult to determine an equilibrium value for the exchange rate. Appendix A provides a brief review of the literature on this issue.

7

Given the general consensus on the goal, if not on the timing, that China should move towards a more flexible exchange rate regime, how might this be most favourably achieved?

3 Moving Towards a Flexible Exchange Rate Regime There are three key elements that have to be addressed as China moves towards a more flexible exchange rate regime: the nature of the exchange rate regime in the transition to a floating regime, what type of nominal anchor the central bank should adopt as the currency peg is abandoned, and measures that should be introduced to strenghten the financial system.

3.1 The transition

Eichengreen (2005) points out that the current time is the best time for China to exit from its peg, while capital is flowing in and there is a tendency for the yuan to appreciate.11, 12 The best strategy for China would be to adopt a monetary policy to limit deviations of inflation and growth from chosen targets. This does not imply neglecting the exchange rate; rather, it means intervening in the exchange market to limit currency fluctuations. Eichengreen stresses that his argument for a rapid transition to a more flexible exchange rate is also not an argument for rapid capital account liberalization. He points out that history is replete with examples of countries that have operated managed floats while retaining capital controls (e.g., Europe in the 1930s, Japan in the 1970s, Chile in the 1990s, Brazil and India currently). In his view, exports are no longer the exclusive driver of growth; the sources of demand for Chinese production have become more diversified. Price stability is now well established as a nominal anchor, and an exchange rate peg is no longer the obvious focal point for monetary policy. What is essential is for China to obtain the additional flexibility necessary to respond optimally to shocks.

11. Eichengreen et al. (1998a) provide a thorough review of the experience of many countries in moving towards a more flexible exchange rate regime. They find that the chances of success are importantly enhanced by replacing the exchange rate anchor by a monetary policy that has a clear commitment to low inflation. Institutional reforms to assure greater discipline and transparency of fiscal policy are also important, as are efforts to strengthen the soundness of the financial sector.

12. Detragiache, Mody, and Okada (2005) examine the experiences of countries that have exited from a peg since the 1980s. They find that the vast majority of exits were followed by depreciation. In about half of the episodes, the exit was orderly and did not lead to a currency crisis or high inflation within the following 12 months. Moreover, further analysis reveals that there are no robust differences between the general circumstances leading to orderly or disorderly exits. In practice, countries do not heed the advice to move away from heavily managed exchange rate regimes when the going is good, but rather wait until the parity is under pressure to depreciate. And, unfortunately, the data do not offer clear indications as to which circumstances best improve the chances of an orderly transition to greater exchange rate flexibility.

8

In contrast, Goldstein (2004, 2007) and Obstfeld (2006) have each proposed a two-step approach, calling for an initial appreciation of the yuan, followed by a progressive increase in the fluctuation band of the currency.13 Eichengreen (2005) is particularly critical of Goldstein’s proposal for a two-step approach that would initially maintain the dollar peg, but with a 25 per cent revaluation of the yuan. In Eichengreen’s view, a change in the exchange rate regime in the direction of managed floating provides needed flexibility; revaluating the yuan by 25 per cent against the dollar does not.

Prasad, Rumbaugh, and Wang (2005) argue that greater exchange rate flexibility is in China’s own interest. Along with a more stable and robust financial system, it should be regarded as a prerequisite for undertaking a substantial liberalization of China’s capital account.14 The authors claim that exchange rate flexibility is unlikely to create strong incentives to take deposits out of the Chinese banking system. The introduction of greater flexibility would create stronger incentives for currency hedging instruments and facilitate capital account liberalization by better preparing the economy to deal with the impact of increased capital flows. Given the weakness of China’s banking system, however, the liberalization of capital flows should be sequenced in a manner that reinforces domestic financial liberalization and allows for institutional capacity building to manage the additional risks.15

In countries with weak financial systems, capital controls can prevent the corporate sector as well as the banks from borrowing excessively from abroad, and permit more monetary policy autonomy under fixed exchange rates. But there is considerable evidence that the effectiveness of capital controls tends to diminish over time. For instance, Japan’s experience in the wake of the collapse of the Bretton Woods system in the 1970s, and the experiences of Latin American countries during the debt crises of the 1980s, demonstrate that capital controls have generally not

13. Goodfriend (2007) argues, however, based on a two-country New Neoclassical Synthesis model, that a (nominal) yuan revaluation per se will not lead to a current account adjustment, if U.S. monetary policy targets inflation credibly. What China needs is not a one-time revaluation of its exchange rate, or a sequence of managed revaluations, but a flexible exchange rate to control inflation at home and to anchor the financial stability of East Asia.

14. In the view of Prasad, Rumbaugh, and Wang, the possible undervaluation of the currency is of secondary importance – with capital controls and speculative inflows it is difficult to estimate its equilibrium value.

15. The authors also point out that China’s fixed exchange rate has generated some specific costs. While the fiscal costs of sterilization have been absent because the central bank’s bills pay a lower interest than industrial country medium- and long-term bonds, maintaining such low domestic interest rates (which have been negative in real terms) requires domestic financial repression, creating large distortions and efficiency losses.

9

been effective in restricting capital outflows (inflows) when there is strong downward (upward) pressure on the exchange rate.

The Chinese authorities have attempted to alleviate recent appreciation pressures by easing controls on capital as well as current account transactions in order to provide more channels for capital outflows. These measures, however, run the risk of getting the sequencing wrong. Opening the capital account without exchange rate flexibility has been the root cause of many emerging-market financial crises.16 Easing of controls on outflows could also be counterproductive, since they could stimulate further inflows (investors knowing that they could more easily get their money out). In principle, an orderly exit from a fixed exchange rate regime to greater flexibility can best be accomplished during a period of relative tranquility in exchange markets.

3.2 A new nominal anchor

Goodfriend and Prasad (2006) note that moving towards a flexible exchange rate requires adopting a new nominal anchor. An inflation objective (they are not actually advocating a formal inflation-targeting regime) can accommodate fluctuations in productivity growth and changing relationships between monetary or credit aggregates and inflation. It also has the virtue of easy communicability. Key to this policy shift is the need to reform the banking system to allow the effective transmission of monetary policy.

The essence of this challenge is to transform the banking system from an off-budget arm of fiscal policy – which uses captive savings of households to support state enterprises, whether commercially viable or not – into a banking system that can direct credit prudently to its most valued uses.17 The reforms should also aim to give the PBC full control of its balance sheet so that the central bank can manage its reserves solely for monetary policy purposes. Reforms also

16. New Zealand was one exception to the general pattern of exchange rate flexibility preceding capital account liberalization. It floated its exchange rate and liberalized capital flows at the same time in 1984, leading to substantial capital inflows and a sharp appreciation of the real exchange rate. While exchange rate flexibility cushioned the impact, the scale of these inflows still contributed to an asset-price boom and subsequent bust.

17. In reviewing the experience of countries at different stages of money market development, Laurens (2005) concludes that the speed of moving towards reliance on money market operations must be tailored to each country’s particular circumstances. Three stages are envisaged. Stage one is the process of developing financial intermediation. At this stage, monetary policy relies on rules-based instruments (e.g., reserve requirements). Stage two involves fostering interbank market development. Stage three involves the diversification of markets. At the end of stage three, liquidity management can fully rely on money market instruments.

10

need to ensure that banks can withstand the financial stresses that can result from fluctuations in interest rates necessary to maintain price stability. In effect, the adoption of an effective monetary policy would facilitate various reforms that have intrinsic benefits of their own, such as modernizing the financial system, improving the statistical base, and enhancing the transparency of monetary policy.

A central bank’s control of bank reserves is compromised when it is obliged to acquire or sell assets for reasons other than managing aggregate bank reserves to stabilize inflation. When a country chooses to manage its currency within a narrow range, the central bank must accommodate the market’s excess demand or supply of foreign exchange by creating or draining bank reserves. Sterilization does little to reduce the incentives that give rise to the foreign exchange rate flows. Even when supplemented with capital controls, sterilization of inflows typically leads to rising quasi-fiscal costs or other implicit costs associated with financial repression. And the buildup of reserves exposes the central bank’s balance sheet to risks of capital losses associated with exchange rate and interest rate fluctuations.18

Mishkin (2000) argues that some advantages of inflation targeting (IT) are particularly relevant for emerging-market countries.19 For one, a stable relationship between money and inflation is not critical to its success. Moreover, IT is easily understood by the public and it focuses the political debate on what monetary policy can do in the long run. On the other hand, inflation may be particularly hard to control because of relatively underdeveloped financial systems. In addition, IT requires fiscal policy support, and the exchange rate flexibility required for IT might be difficult for policy-makers to allow. Furthermore, to implement the policy, a central bank has to develop reliable indicators of inflation pressures, as well as techniques to produce efficient conditional forecasts of inflation and output growth.

18. PBC bills have become the primary instrument for sterilization of capital inflows. Sterilization has been facilitated by high savings rates, notably corporate savings, which have made the banks flush with liquidity. PBC bills also help banks to meet their capital adequacy requirements: corporate lending requires a capital requirement of 100 per cent, while no capital needs to be set aside for lending to the government. Moreover, given the structure of interest rates, sterilization is essentially a money-making operation for the PBC. Green (2005) estimates that, in 2004, the PBC sterilized about 48 per cent of foreign exchange inflows.

19. Schaechter, Stone, and Zelmer (2000) review the experience of six emerging-market countries that have adopted an IT regime. They conclude that the IT countries are large and have more developed financial systems compared with their counterparts. Moreover, experience reveals that a strong fiscal position and entrenched macroeconomic stability are equally important elements of a successful IT regime.

11

In the current environment, the inability of the PBC to use interest rates as the main policy tool implies that credit growth is controlled by much blunter instruments. Prasad and Rajan (2005) argue that this vitiates the process of banking reform, perpetuating large efficiency costs via provision of cheap subsidized credit to inefficient state enterprises. In their view, the interbank market is relatively illiquid, major players have excessive market power, and non-bank participants have the potential to destabilize the market. They argue that the PBC should refrain from discretionary reserve requirement adjustments because they induce volatility in excess reserve demand as banks try to anticipate and prepare for these changes by building up excess reserves in advance. Moreover, the PBC ought to discontinue paying interest on excess reserves.

Blanchard and Giavazzi (2005) also argue in favour of allowing the yuan to appreciate to reduce trade surpluses. They recommend that the PBC should remove capital controls asymmetrically, allowing outflows but restricting inflows, to relieve pressure on the exchange rate. But they couch their position within a broader strategy to ensure greater success. Thus, China must also improve the ability of individuals to insure against educational, health, and retirement risk in order to reduce high household saving rates and temper potential social unrest. According to Modigliani and Cao (2004), China’s saving rate is consistent with the life-cycle model once we take account of the high growth rate and the one-child policy. Blanchard and Giavazzi argue, however, that there is plenty of evidence that at least part of the high saving rate reflects precautionary saving (or the need for self-insurance).With the privatization of town and village enterprises and an increased focus on profit rather than social insurance, much of the health care infrastructure has not been maintained.20 Moreover, the Chinese authorities should adopt measures to reduce or reallocate investment. Investment appears to be too high in manufacturing and too low in services, especially public services.21

Aziz and Dunaway (2007) point out that many factors have contributed to over- investment in China. The most important factor is the low cost of capital, since 90 per cent of investment is financed domestically. Whereas real GDP growth in China has averaged about 10 per cent, the

20. Vietnam’s health insurance program could be a good model (Wagstaff and Pradhan 2005). The collapse of social insurance has left individuals with the need to self-insure – an expensive and very imperfect solution. The decrease in safety nets has become particularly relevant in the area of health, and the transition to a fee-based health care and education system has compounded the effects of widening income inequality.

21. Hofman and Kuijs (2007) note that China’s rapid investment- and export-led growth has given rise to major macroeconomic, environmental, and social challenges. Their model simulations show that, without reforms, current account surpluses, environmental stress, and inequality are likely to remain features of China’s growth. A policy package that would better price capital and environmental damage and favour more labour mobility would produce better outcomes on all three counts. Surprisingly, the exchange rate plays only a minor role in the simulations, serving mainly to limit expectations of a yuan appreciation.

12

real cost of investment has hovered around 1 to 2 per cent. The real cost of capital is not just low; it has fallen relative to wages, despite China’s abundant labour supply. In most countries, 3 to 4 per cent GDP growth is associated with 2 to 3 per cent employment growth, but in China, 10 per cent growth is generating only 1 per cent employment growth. One consequence is that consumption as a share of GDP has fallen to about 40 per cent. Nearly all the decline is attributable to a falling share of national income going to households, including wages, investment income, and government transfers.

Lardy (2007) also argues that shifting to a more consumption-driven growth path in China will require significant changes in its exchange rate policy. Since personal taxes are low in China, fiscal policy should focus on broadening health and pension coverage and the social safety net.22

The exchange rate regime matters because China’s current policy has seriously limited the independence of monetary policy. In Lardy’s view, the PBC has been reluctant to raise domestic interest rates, since this would reduce the carry costs of foreigners moving money into China in anticipation of the yuan’s appreciation. The low resulting cost of capital has led to overinvestment and restrained the disposable income of households.

Prasad (2007) also notes the importance of moving on many fronts simultaneously to establish a more flexible macroeconomic framework within which to respond to negative shocks that are likely to occur in the future. In Prasad’s view, the financial sector is in poor shape and it has distorted domestic demand towards investment; the patterns of investment financing could lead to a resurgence of non-performing loans (NPLs) in the future. Meanwhile, in the short term, pressures are becoming evident in other forms, such as asset booms. Prasad points out that while it is easy to create a list of reforms, many of them are interrelated and China’s evolution towards a market-based economy has reached a point at which it is not effective to try to implement the reforms in isolation. For instance, stable macroeconomic policies and a well-developed and efficient financial sector are essential for balanced and sustainable growth. In turn, these two objectives would be helped by effective monetary policy and further capital account liberalization. And a flexible exchange rate is a prerequisite for both of these.

22. For example, in 2003, only about half of the urban population, and less than one-fifth of the rural population, had basic health insurance. In 2005, only 14 per cent of China’s workforce was covered by unemployment insurance, and only 11 per cent was covered by workers’ compensation.

13

3.3 Strengthening China’s financial system

A key impediment in moving towards greater exchange rate flexibility has been the concern that the Chinese financial system, and in particular its banking system, may not be sufficiently robust to adapt to large exchange rate variations were they to occur. The China Banking Regulatory Commission has set out three broad steps in its plan to reform the four large state-owned commercial banks (SOCBs) that dominate the banking industry in China.

First, the banks are to reduce their NPLs to internationally acceptable levels. Second, the banks are to become listed with initial public offerings (IPOs) on mainland and foreign stock exchanges.23 Third, the banks are to be managed with a view to becoming internationally competitive. The importance of attaining this objective is driven in part by China’s commitment to the World Trade Organization in 2001 to allow full foreign entry into the Chinese banking sector.

Official statistics show that the ratio of NPLs fell from about 30 per cent in 2001 to around 7 per cent of all loans currently. Chinese banks’ IPOs have been successful and bank profitability has increased. Analysts are cautious, however, in interpreting the official statistics, suspecting an underreporting of NPLs, which are likely to increase as financial conditions tighten. Moreover, to ensure that the NPL problem does not reoccur, lending practices will have to change from a political to a more commercial basis. Unfortunately, Dobson and Kashyap (2006) find that managers at the largest SOCB continue to behave like Communist Party members who are more concerned with social and economic objectives than profitability. This is likely to persist as long as the state has a majority stake in these banks. Thus, progressive privatization is key to greater efficiency and resiliency of China’s banking system. Chinese officials have also progressively relaxed capital controls, with the aim of balancing capital inflows that are putting pressure on the yuan, and of providing more opportunities for Chinese nationals to diversify their portfolios and invest abroad.

Is China on the right track? There is a vast literature on capital account liberalization and the proper sequencing of reforms, and a myriad of experiences to draw on to see what works and what does not. Eichengreen et al. (1998a) provide an overview. They point out that capital account liberalization is inevitable for countries that wish to benefit from the global economic

23. Foreign ownership in a single Chinese bank is limited to 19.9 per cent of total equity for a single investor, and to 25 per cent for all foreign investors.

14

system. It is not without dangers, however, and the process has to be supported by a combination of sound macroeconomic policies to contain aggregate financial imbalances and sound prudential policies, backed by adequate supervision of the financial system, to ensure proper incentives for risk management.24 As Eichengreen et al. (1998b, 27) acknowledge: “there is no generally applicable cookbook recipe for the sequence of steps to undertake in financial and capital account liberalization, and there is no general guideline for how long the process should take.”

A sound banking system is essential for the efficient allocation of capital and the transmission of monetary policy, and it is closely tied to the objective of capital account convertibility. Anderson (2006) argues that financial risk has diminished in China’s banking sector as many NPLs have been taken off the banks’ balance sheets and off-loaded to an asset management corporation. Dobson and Kashyap (2006) are less optimistic. They point out that the Chinese banking system remains fragmented and often dominated by local branches and decision making, the objectives of which may differ from those of the Beijing headquarters. The previous NPL problems arose because the government was committed to financing loss-making state-owned enterprises (SOEs), which were not only the main source of employment but also provided the social safety net. Moreover, the government decided to fund the SOEs through the banking system to move losses off the Ministry of Finance’s balance sheet. This created two significant distortions: a moral hazard problem (since bad loans to SOEs would be bailed out) and a reduction of the pressure on SOEs to improve their efficiency, given their easy access to credit. Dobson and Kashyap believe that the best solutions to these problems are to transfer the burden of policy-driven lending to the policy banks that have been given this mandate, and to let the banking system evolve towards sound risk management and profitability objectives.25

24. Eichengreen et al. (1998b, 27) also warn of trying to drive domestic reforms by leveraging on capital account liberalization: “Domestic and international liberalization can benefit from symbiotic interactions, but one needs to be careful about perverse interactions, particularly if opportunities made possible by international liberalization get ahead of relevant domestic preparations.”

25. State policy banks were established and are guaranteed by the government. Their primary aim is to implement the nation’s industrial and development policies. There are three policy banks: the China Development Bank, the Export-Import Bank of China, and the Agricultural Bank of China.

15

4 Conclusion

They must often change who would be constant in happiness and wisdom. – Confucius

What have we learned? First, China would benefit from moving towards a more flexible exchange rate regime and allowing the PBC greater independence to pursue an inflation-control objective. A managed float would be best in a transition phase, since firms need to adapt to the new system and the banking system needs to be put on a sounder footing. Capital controls should be progressively eased, but not precipitously. The Chinese authorities have made progress in reforming their banking system and setting the basis for a market-based monetary policy. We encourage them to pursue their efforts. The progressive privatization of China’s banking system holds the key to success.

It is most likely that China will move to a flexible exchange rate regime at a time of its own choosing and that it will be a political decision, not one swayed by economic analysis per se. There are two reasons for this, in our view. First, the currency peg has been key to China’s export-led growth strategy, which has provided strong sustained output growth, substantial poverty reduction, and rapid industrialization in certain regions, as well as helped to maintain political stability. Second, the central bank is not independent. Monetary policy at the PBC is decided by its board, which is dominated by external senior state officials. Effective monetary policy, which a flexible exchange rate both permits and requires, will not be feasible until a political decision is taken to give the PBC the required autonomy to carry it out.

16

References

Ahearne, A., W. R. Cline, K. T. Lee, Y. C. Park, J. Pisani-Ferry, and J. Williamson. 2007. “Global Imbalances: Time for Action.” Peterson Institute for International Economics Policy Brief No. 07-4.

Anderson, J. 2006. “How Real is China’s Bank Cleanup?” UBS Investment Research Asian Focus, 18 January.

Aziz, J. and S. Dunaway. 2007. “China’s Rebalancing Act.” Finance & Development 44 (3): 27–31.

Blanchard, O. J. and F. Giavazzi. 2005. “Rebalancing Growth in China: A Three-Handed Approach.” Massachusetts Institute of Technology (MIT) Department of Economics Working Paper No. 05-32.

Bown, C. P., M. A. Crowley, R. McCulloch, and D. J. Nakajima. 2005. “The U.S. Trade Deficit: Made in China?” Economic Perspectives 29 (4): 2–18.

Cheung, Y.-W., M. D. Chinn, and E. Fuji. 2007. “The Overvaluation of Renminbi Undervaluation.” National Bureau of Economic Research (NBER) Working Paper No. 12850.

Chinn, M. D. 2000. “Three Measures of East Asian Currency Overvaluation.” Contemporary Economic Policy 18 (2): 205–14.

Chou, W. L. and Y. C. Shih. 1998. “The Equilibrium Exchange Rate of the Chinese Renminbi.” Journal of Comparative Economics 26 (1): 165–74.

Cline, W. R. and J. Williamson. 2007. “Estimates of the Equilibrium Exchange Rate of the Renminbi: Is There a Consensus and, If Not, Why Not?” Paper presented at a conference on “China’s Exchange Rate Policy” held by the Peterson Institute for International Economics, Washington, D.C., 12 October. Available at <http://www.petersoninstitute.org/publications/papers/cline-williamson1007.pdf>.

Cui, L. 2007. “China’s Growing External Dependence.” Finance & Development 44 (3): 42–5.

Detragiache, E., A. Mody, and E. Okada. 2005. “Exits from Heavily Managed Exchange Rate Regimes.” International Monetary Fund (IMF) Working Paper No. 05/39.

Dobson, W. and A. K. Kashyap. 2006. “The Contradiction in China’s Gradualist Banking Reforms.” Rotman School of Management, University of Toronto. October.

Dunaway, S., L. Leigh, and X. Li. 2006. “How Robust Are Estimates of Equilibrium Exchange Rates: The Case of China.” International Monetary Fund (IMF) Working Paper No. 06-220.

17

Dunaway, S. and X. Li. 2005. “Estimating China’s ‘Equilibrium’ Real Exchange Rate.” International Monetary Fund (IMF) Working Paper No. 05/202.

Eichengreen, B. 2005. “Is a Change in the Renminbi Exchange Rate in China’s Interest?” Asian Economic Papers 4 (1): 40–75.

Eichengreen, B., P. Masson, H. Bredenkamp, B. Johnston, J. Hamann, E. Jadresic, and I. Ötker. 1998a. “Exit Strategies: Policy Options for Countries Seeking Greater Exchange Rate Flexibility.” International Monetary Fund (IMF) Occasional Paper No. 168.

Eichengreen, B., M. Mussa, G. Dell’Ariccia, E. Detragiache, G. M. Milesi-Ferretti, and A. Tweedie. 1998b. “Capital Account Liberalization: Theoretical and Practical Aspects.” International Monetary Fund (IMF) Occasional Paper No. 172.

European Central Bank. 2007. “Putting China’s Economic Expansion in Perspective.” ECB Monthly Bulletin (January): 77–87.

Fung, K. C., L. J. Lau, and Y. Xiong. 2006. “Adjusted Estimates of United States-China Bilateral Trade Balances? An Update.” Stanford Center for International Development Working Paper No. 278.

Goldstein, M. 2004. “Adjusting China’s Exchange Rate Policies.” Peterson Institute for International Economics Working Paper No. 04-1.

———. 2007. “A (Lack of) Progress Report on China’s Exchange Rate Policies.” Peterson Institute for International Economics Working Paper No. 07-5.

Goldstein, M. and N. Lardy. 2007. “China’s Exchange Rate Policy: An Overview of Some Key Issues.” Paper presented at a conference on “China’s Exchange Rate Policy” held by the Peterson Institute for International Economics, Washington, D.C., 12 October. Available at <http://www.petersoninstitute.org/publications/papers/goldstein-lardy1007.pdf>.

Goodfriend, M. 2007. “Monetary Policy in East Asia: Common Concerns.” Bank of Japan Institute for Monetary and Economic Studies (IMES) Discussion Paper No. 2007-E-18.

Goodfriend, M. and E. Prasad. 2006. “A Framework for Independent Monetary Policy in China.” International Monetary Fund (IMF) Working Paper No. 06/111.

Green, S. 2005. “Making Monetary Policy Work in China: A Report from the Money Market Front Line.” Paper presented at a conference on “China’s Policy Reforms: Capital Markets, Banking and Foreign Exchange Management” held by the Stanford Center for International Development and the National Center for Economic Research at Tsinghua University, Beijing, China, 27–28 April. Available at <http://scid.stanford.edu/pdf/SCID245.pdf>.

18

Hofman, B. and L. Kuijs. 2007. “Rebalancing China’s Growth.” Paper presented at a conference on “China’s Exchange Rate Policy” held by the Peterson Institute for International Economics, Washington, D.C., 18 October. Available at <http://www.iie.com/publications/papers/hofman1007.pdf>.

Hoggarth, G. and H. Tong. 2007. “The Impact of Yuan Revaluation on the Asian Region.” Bank of England Working Paper No. 329.

International Monetary Fund (IMF). 2006. “People’s Republic of China: 2006 Article IV Consultation – Staff Report; Staff Statement; and Public Information Notice on the Executive Board Decision.” IMF Country Report No. 06/394.

Lardy, N. R. 2002. Integrating China into the Global Economy. Washington, D.C.: Brookings Institution Press.

———. 2005. “Exchange Rate and Monetary Policy in China.” Cato Journal 25 (1):19–25.

———. 2007. “China: Rebalancing Economic Growth.” In The China Balance Sheet in 2007 and Beyond, Chapter 1. A compendium of papers for a conference held by the Peterson Institute for International Economics, 2 May. Washington, D.C.: Peterson Institute for International Economics.

Laurens, B. J. 2005. “Monetary Policy Implementation at Different Stages of Market Development.” International Monetary Fund (IMF) Occasional Paper No. 244.

Laurens, B. J. and R. Maino. 2007. “China: Strengthening Monetary Policy Implementation.” International Monetary Fund (IMF) Working Paper No. 07/14.

Lim, E., M. Spence, and R. Hausmann. 2006. “China and the Global Economy: Medium-Term Issues and Options – A Synthesis Report.” Center for International Development at Harvard University (CID) Working Paper No. 126.

Markovic, B. and L. Povoledo. 2007. “Does Asia’s Choice of Exchange Rate Regime Affect Europe’s Exposure to US Shocks?” Bank of England Working Paper No. 318.

Marquez, J. and J. W. Schindler. 2006. “Exchange-Rate Effects on China's Trade: An Interim Report.” Board of Governors of the Federal Reserve System International Finance Discussion Paper No. 861.

McCallum, B. T. 2006. “Singapore’s Exchange Rate-Centered Monetary Policy Regime and its Relevance for China.” Monetary Authority of Singapore (MAS) Staff Paper No. 43.

McKinnon, R. 2006. “China’s Exchange Rate Appreciation in the Light of the Earlier Japanese Experience.” Centre for European Economic Research (ZEW) Discussion Paper No. 06-035.

———. 2007. “Why China Should Keep Its Dollar Peg.” International Finance 10 (1): 43–70.

19

Mishkin, F. S. 2000. “Inflation Targeting in Emerging-Market Countries.” American Economic Review 90 (2): 105–9.

Modigliani, F. and S. L. Cao. 2004. “The Chinese Saving Puzzle and the Life-Cycle Hypothesis.” Journal of Economic Literature 42 (1): 145–70.

Obstfeld, M. 2006. “The Renminbi’s Dollar Peg at the Crossroads.” University of California, Berkeley, Center for International and Development Economics Research Paper No. C06-148.

People’s Daily Online. 2005. “PBOC on Reforming the RMB Exchange Rate Regime.” 22 July. Available at <http://english.peopledaily.com.cn/200507/22/eng20050722_197772.html>.

Prasad, E. S. 2007. “Monetary Policy Independence, the Currency Regime, and the Capital Account in China.” Paper presented at the conference on “China’s Exchange Rate Policy” held by the Peterson Institute for International Economics, Washington, D.C., 19 October. Available at <http://www.iie.com/publications/papers/prasad1007.pdf>.

Prasad, E. S. and R. G. Rajan. 2005. “Controlled Capital Account Liberalization: A Proposal.” International Monetary Fund (IMF) Policy Discussion Paper No. 05/7.

Prasad, E., T. Rumbaugh, and Q. Wang. 2005. “Putting the Cart before the Horse?: Capital Account Liberalization and Exchange Rate Flexibility in China.” International Monetary Fund (IMF) Policy Discussion Paper No. 05/1.

Schaechter, A., M. R. Stone, and M. Zelmer. 2000. “Adopting Inflation Targeting: Practical Issues for Emerging Market Countries.” International Monetary Fund (IMF) Occasional Paper No. 202.

Shi, J. and H. Yu. 2005. “Renminbi Equilibrium Exchange Rate and China’s Exchange Rate Misalignment: 1991–2004.” Economic Research Journal 40 (4): 34–45.

Su, N. 2004. “China’s Economic Development and the Current Macroeconomic Policy.” Remarks at the Conference of Montréal, 9 June 2004. Available at <http://www.pbc.gov.cn/english//detail.asp?col=6500&ID=29>.

Wagstaff, A. and M. Pradhan. 2005. “Health Insurance Impacts on Health and Non-Medical Consumption in a Developing Country.” World Bank Policy Research Working Paper No. 3563.

Zhang, Z. 2001. “Real Exchange Rate Misalignment in China: An Empirical Investigation.” Journal of Comparative Economics 29 (1): 80–94.

20

Zhou, X. 2003. “Statement at the Eighth Meeting of the International Monetary and Financial Committee, Dubai, 21 September.” Available at <http://www.pbc.gov.cn/english//detail.asp?col=6500&ID=15&keyword=statement>.

———. 2004. “The Current Financial Situation and the Development of the Financial Market in China.” Speech at the “National Conference for the Work of Foreign-Funded Banks,” 12 April. Available at <http://www.pbc.gov.cn/english// detail.asp?col=6500&ID=23&keyword=current%20financial%20situation>.

———. 2006. “Remarks on China’s Trade Balance and Exchange Rate.” Remarks at the “China Development Forum,” sponsored by the Development Research Center of the State Council, 20 March. Available at <http://www.pbc.gov.cn/english//detail.asp?col=6500&ID=109&keyword=zhou>.

21

Chart 1 China’s Trade and Current Account Balance

0%

1%

2%

3%

4%

5%

6%

7%

8%

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Per

cen

t of

GD

P

Trade balance Current account balance

Source: IMF International Financial Statistics

Chart 2 Official Reserves

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

200%

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Per

cen

t of n

om

inal

imp

ort

s

China Hong Kong Japan

Source: IMF International Financial Statistics

22

Chart 3 Chinese Exchange Rate Indexes (a rise in the index denotes an appreciation)

Source: Bank of Canada, Bank for International Settlements

Chart 4 Yuan Broad Real Effective Exchange Rate 2002–04 trade weights

Japan17%

Canada2%

Emerging Asia32%

Other7% U.S.

19%

Euro area16%

Other industrial countries

9%

Source: Bank for International Settlements

80

85

90

95

100

105

110

115

120

125

130

135

Jan 95 Jan 96 Jan 97 Jan 98 Jan 99 Jan 00 Jan 01 Jan 02 Jan 03 Jan 04 Jan 05

Inde

x (J

an 1

995=

100)

U.S. dollar/yuan Yuan broad real effective

23

Appendix A: Evaluating the Yuan

Determining a reasonable “equilibrium value” for the yuan is a challenge. Studies typically rely on two approaches. The macroeconomic balance approach derives an estimate of the required change in the exchange rate to reach balance-of-payments equilibrium. This is defined as either: (i) a situation where “normal” capital flows equal the underlying current account balance, or (ii) a stable NFA/GDP ratio. The extended purchasing-power-parity (PPP) approach assumes PPP in the long run, but allows deviations in the short run. Taking into account the predicted influence of these factors, often derived from cross-country samples, an equilibrium exchange rate is estimated.

Dunaway and Li (2005) review a number of papers that estimate the equilibrium exchange rate. The estimates provide a wide range for the undervaluation of the yuan–dollar rate, from zero to 50 per cent. The authors attribute the wide variation in the estimates to methodological differences, differences in subjective judgments by researchers, and the instability of underlying economic relationships in their models, notably owing to the rapid development of the Chinese economy. In a follow-up paper, Dunaway, Leigh, and Li (2006) test the robustness of these measures. They conclude that, for China, small changes in model specification, explanatory variable definitions, and time periods used in the estimation can lead to very substantial differences in equilibrium real exchange rate estimates.1 Thus, such estimates should be treated with great caution. While estimates vary widely, all but 1 of 18 papers reviewed by Cline and Williamson (2007) suggest that the yuan was undervalued at the time the studies were done.

A complicating factor is that there is wide disagreement on the extent of the bilateral China–

U.S. trade balance. In 2005, the U.S. merchandise trade deficit with China was $202 billion

according to U.S. government data, but only $142 billion according to Chinese government data.

Fung, Lau, and Xiong (2006) provide adjusted estimates, with four corrections: (i) use of

freight on board–free on board and cost, insurance, and freight conversions; (ii) re-exports

through Hong Kong (and elsewhere); (iii) re-export markups; and (iv) trade in services.

1. Comparisons can also be tricky, since assessments differ in terms of methodology and timing. For example, Goldstein (2004) estimates that the yuan was undervalued by 15 – 30 per cent in 2003; Shi and Yu (2005) use a behavioural equilibrium exchange rate approach and come up with a 12 per cent undervaluation over 2002–04. Other studies of interest include Cheung, Chinn, and Fuji (2007); Chinn (2000); Chou and Shih (1998); Zhang (2001).

24

Fung, Lau, and Xiong’s best estimate for the 2005 bilateral trade balance on goods and services

is $171 billion in China’s favour. Moreover, it is difficult to get reliable estimates of trade

elasticities for China to gauge the response of the trade balance to a revaluation of the exchange

rate. Marquez and Schindler (2006) note problems in estimating trade elasticities that are

particular to China. These include state control prior to reforms, the relative historical stability

of the real effective exchange rate, and the lack of data on Chinese trade prices.2 They also point

to problems with the use of proxies, and parameter instability in the reported results.

2. Lardy (2002) notes that, through the mid-1980s, the volumes of Chinese exports and imports were not responsive to changes in the real exchange rate, because the government specified quantitative targets for most exports and imports.