Embed Size (px)

Citation preview

JRCPPF Escalating Risks

China's Model of Managing the Financial System

Markus K. Brunnermeier Michael Sockin Wei Xiong

Feb, 2017

Discussion by Lin William Cong University of Chicago Booth School of Business

Overview Model Comments Summary

Contribution and Significance

• Government Intervention and Impact on Price Dynamics

• Context of China’s Financial SystemStock market crash in 2015.

• Real, Important, and Timely.

Slide 1/24 — Discussion by Will Cong (Chicago Booth) — China’s Model of Managing the Financial System

Overview Model Comments Summary

Contribution and Significance

• Government Intervention and Impact on Price Dynamics

• Context of China’s Financial SystemStock market crash in 2015.

• Real, Important, and Timely.

Slide 1/24 — Discussion by Will Cong (Chicago Booth) — China’s Model of Managing the Financial System

Overview Model Comments Summary

Contribution and Significance

• Government Intervention and Impact on Price Dynamics

• Context of China’s Financial SystemStock market crash in 2015.

• Real, Important, and Timely.

Slide 1/24 — Discussion by Will Cong (Chicago Booth) — China’s Model of Managing the Financial System

Overview Model Comments Summary

What Happened in China in 2015?

• A taxi-driver’s tale.

Slide 2/24 — Discussion by Will Cong (Chicago Booth) — China’s Model of Managing the Financial System

Overview Model Comments Summary

What Happened in China in 2015?

• A taxi-driver’s tale.

Slide 3/24 — Discussion by Will Cong (Chicago Booth) — China’s Model of Managing the Financial System

Overview Model Comments Summary

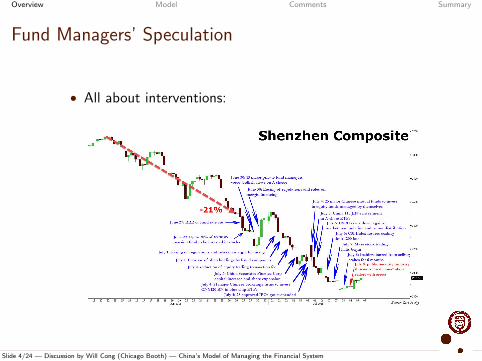

Fund Managers’ Speculation

• All about interventions:

Slide 4/24 — Discussion by Will Cong (Chicago Booth) — China’s Model of Managing the Financial System

Overview Model Comments Summary

Closed-door Round-Table Discussion

• “Anomalous Movements” , Reducing Volatility.

Slide 5/24 — Discussion by Will Cong (Chicago Booth) — China’s Model of Managing the Financial System

From "Saving China's Stock Market" by Yi Huang, Jianjun Miao, and Pengfei Wang

Overview Model Comments Summary

Important

• China’s Economy and Financial Markets.

• By the end of September 2015, 42 trillion RMB, dailyvolume of August 2015 was 514.8 billion RMB

Slide 6/24 — Discussion by Will Cong (Chicago Booth) — China’s Model of Managing the Financial System

Overview Model Comments Summary

Important

• New Investors Dynamics

Slide 7/24 — Discussion by Will Cong (Chicago Booth) — China’s Model of Managing the Financial System

Overview Model Comments Summary

Important

• International Ramifications

• Currency Devaluation August 2015Daily reference rate down 1.9 percent, largest since Jan1994

• Implications for other countriesUnconventional monetary policy in OECDs.Introduction of Euros (Gopinath et al. (2015))Economic stimulus after the global recession.

• Our understanding of business (credit) cycles andallocational efficiency.

• Caballero et. al (1994), Cooper et al (1993), Kiyotaki &Moore (1997), Ramey & Watson (1997)

Slide 8/24 — Discussion by Will Cong (Chicago Booth) — China’s Model of Managing the Financial System

Overview Model Comments Summary

Important

• International Ramifications

• Currency Devaluation August 2015Daily reference rate down 1.9 percent, largest since Jan1994

• Implications for other countriesUnconventional monetary policy in OECDs.Introduction of Euros (Gopinath et al. (2015))Economic stimulus after the global recession.

• Our understanding of business (credit) cycles andallocational efficiency.

• Caballero et. al (1994), Cooper et al (1993), Kiyotaki &Moore (1997), Ramey & Watson (1997)

Slide 8/24 — Discussion by Will Cong (Chicago Booth) — China’s Model of Managing the Financial System

Overview Model Comments Summary

Important

• International Ramifications

• Currency Devaluation August 2015Daily reference rate down 1.9 percent, largest since Jan1994

• Implications for other countriesUnconventional monetary policy in OECDs.Introduction of Euros (Gopinath et al. (2015))Economic stimulus after the global recession.

• Our understanding of business (credit) cycles andallocational efficiency.

• Caballero et. al (1994), Cooper et al (1993), Kiyotaki &Moore (1997), Ramey & Watson (1997)

Slide 8/24 — Discussion by Will Cong (Chicago Booth) — China’s Model of Managing the Financial System

Overview Model Comments Summary

Timely

• Impact and unintended consequences of marketinterventions.Brunnermeier, Sockin, & Xiong (2017), Bai, Hsieh, & Song (2016), Hachem & Song (2016), Huang, Pagano, & Panizza (2016), Cong & Ponticelli (2017), Chen, He, & Liu (2017)

• Ongoing reforms of financial markets• “Reform Bull”: SOE reforms and transition from

export-based to consumption-based• “Liquidity Bull”: China’s version of QE• “Capital Bull”: abundance capital and excessive shadow

leverage• Registration-based IPO, Microstructure Reforms (T + 1,

down limit, circuit breaker), internationalization of RMB

• Ongoing reforms and interventions in other countries.

Slide 9/24 — Discussion by Will Cong (Chicago Booth) — China’s Model of Managing the Financial System

Overview Model Comments Summary

Timely

• Impact and unintended consequences of marketinterventions.Brunnermeier, Sockin, & Xiong (2017), Bai, Hsieh, &Song (2016), Hachem & Song (2016), Huang, Pagano, & Panizza (2016), Cong & Ponticelli (2017), Chen, He, & Liu (2017)

• Ongoing reforms of financial markets• “Reform Bull”: SOE reforms and transition from

export-based to consumption-based• “Liquidity Bull”: China’s version of QE• “Capital Bull”: abundance capital and excessive shadow

leverage• Registration-based IPO, Microstructure Reforms (T + 1,

down limit, circuit breaker), internationalization of RMB

• Ongoing reforms and interventions in other countries.

Slide 9/24 — Discussion by Will Cong (Chicago Booth) — China’s Model of Managing the Financial System

Overview Model Comments Summary

Timely

• Impact and unintended consequences of marketinterventions.Brunnermeier, Sockin, & Xiong (2017), Bai, Hsieh, & Song (2016), Hachem & Song (2016), Huang, Pagano, & Panizza (2016), Cong & Ponticelli (2017), Chen, He, & Liu (2017)

• Ongoing reforms of financial markets• “Reform Bull”: SOE reforms and transition from

export-based to consumption-based• “Liquidity Bull”: China’s version of QE• “Capital Bull”: abundance capital and excessive shadow

leverage• Registration-based IPO, Microstructure Reforms (T + 1,

down limit, circuit breaker), internationalization of RMB

• Ongoing reforms and interventions in other countries.

Slide 9/24 — Discussion by Will Cong (Chicago Booth) — China’s Model of Managing the Financial System

Overview Model Comments Summary

Model Setup

• Grossman-Stiglitz REE with a large player and OLGagents

• Dividends Dt = θt + σDεDt

persistent component (fundamental) AR(1)θt = ρθθt−1 + σθε

θt

• Excess Payoff: Rt+1 = Dt+1 + Pt+1 − R f Pt

• Participants: noise traders, rational traders (OLG),government

Slide 10/24 — Discussion by Will Cong (Chicago Booth) — China’s Model of Managing the Financial System

Overview Model Comments Summary

Model Setup

• Noise traders: Nt = ρNNt−1 + σNεNt

• Investors:

• i ∈ [0, 1], live for one period

• Endowed with wealth W̄

• CARA utility U it = E[− exp(−γW i

t+1)|Ft ]

• Government

• Minimizes price vol and deviation from fundamental

• min γσVart [∆Pt ] + γθVart[Pt − 1

R f −ρθθt+1

]• γσ risk aversion for price vol; γθ risk aversion for

deviation.

Slide 11/24 — Discussion by Will Cong (Chicago Booth) — China’s Model of Managing the Financial System

Overview Model Comments Summary

Model Setup

• Noise traders: Nt = ρNNt−1 + σNεNt

• Investors:

• i ∈ [0, 1], live for one period

• Endowed with wealth W̄

• CARA utility U it = E[− exp(−γW i

t+1)|Ft ]

• Government

• Minimizes price vol and deviation from fundamental

• min γσVart [∆Pt ] + γθVart[Pt − 1

R f −ρθθt+1

]• γσ risk aversion for price vol; γθ risk aversion for

deviation.

Slide 11/24 — Discussion by Will Cong (Chicago Booth) — China’s Model of Managing the Financial System

Overview Model Comments Summary

Key Results

• Benchmark: perfect information

• No intervention, price vol explode, and marketbreakdown when σN is large.

• Noise trading + Investor myopia

• Role for the government to reduce market vol andstabilize the market.

• Intervention to reduce price volatility consistent withimproving price efficiency (always the case?).

Slide 12/24 — Discussion by Will Cong (Chicago Booth) — China’s Model of Managing the Financial System

Overview Model Comments Summary

Key Results

• With information frictions: unobservable fundamentals

• No intervention, reducing price volatility consistent withimproving price efficiency.

• Intervention introduces additional noise.

• Speculation on gov noise.• Price vol reduced at the expense of price efficiency.• Gov-centric equilibrium has less gov trading• Gov pre-commitment and equilibrium multiplicity.

Slide 13/24 — Discussion by Will Cong (Chicago Booth) — China’s Model of Managing the Financial System

Overview Model Comments Summary

Comment 1: Government’s Objective

• Reducing both asset price deviation from fundamentalsand price vol.

• Alternative 1: preventing crash

Slide 14/24 — Discussion by Will Cong (Chicago Booth) — China’s Model of Managing the Financial System

Overview Model Comments Summary

Comment 1: Government’s Objective

• Alternative 2: Favoring State-connected Firms

• e.g., Song, Storesletten, & Zilibotti (2011); Cong &Ponticelli (2017)

• Alternative 3: Social Stability• Agents with imperfect signal xit• Prior of economy fundamental θt• Government intervention mt

• Market breaks down if too many run Arunt > mt + θ∗t

• Government minimizes Z (mt , z , θt)Astayt L + K (m) (or

threshold), L is loss upon failure.• Learning or info acquisition about z• Government-centric vs Fundamental-centric

Slide 15/24 — Discussion by Will Cong (Chicago Booth) — China’s Model of Managing the Financial System

Overview Model Comments Summary

Comment 1: Government’s Objective

• Alternative 2: Favoring State-connected Firms

• e.g., Song, Storesletten, & Zilibotti (2011); Cong &Ponticelli (2017)

• Alternative 3: Social Stability• Agents with imperfect signal xit• Prior of economy fundamental θt• Government intervention mt

• Market breaks down if too many run Arunt > mt + θ∗t

• Government minimizes Z (mt , z , θt)Astayt L + K (m) (or

threshold), L is loss upon failure.• Learning or info acquisition about z• Government-centric vs Fundamental-centric

Slide 15/24 — Discussion by Will Cong (Chicago Booth) — China’s Model of Managing the Financial System

Overview Model Comments Summary

Comment 2: Minimization of Pricing Error

• Reducing both asset price deviation from fundamentalsand price vol.

• The Bias-Variance Trade-off (Decomposition):E (y0 − f̂ (x0))2 = Var(f̂ (x0)) + [Bias(f̂ (x0))]2 + Var(ε)

Slide 16/24 — Discussion by Will Cong (Chicago Booth) — China’s Model of Managing the Financial System

Overview Model Comments Summary

Comment 2: Minimization of Pricing Error

• Reducing both asset price deviation from fundamentalsand price vol.

• The Bias-Variance Trade-off (Decomposition):E (y0 − f̂ (x0))2 = Var(f̂ (x0)) + [Bias(f̂ (x0))]2 + Var(ε)

Slide 16/24 — Discussion by Will Cong (Chicago Booth) — China’s Model of Managing the Financial System

Overview Model Comments Summary

Comment 2: Minimization of Pricing Error

• Penalty for Pricing Errors

E

[(∑t

Dt − Pt(υN̂,t))2|FMt−1

]= Var(

∑t

Dt) + E [∑t

Dt ]2 + Var [Pt(υN̂,t)]

+E [Pt(υN̂,t)]2 − 2E [(∑t

Dt)Pt(υN̂,t)]

= Var(∑t

Dt) + Var [Pt(υN̂,t)] + E

[Pt(υN̂,t)− E [

∑t

Dt ]

]2

• Natural interpretation of the government’s objective.• For equilibrium existence, Bias-Variance are qualitatively

equivalent. But unclear in general.

Slide 17/24 — Discussion by Will Cong (Chicago Booth) — China’s Model of Managing the Financial System

Overview Model Comments Summary

Comment 3: Information Design and Intervention Costs

• Information Design vs Mechanism Design (Bergemannand Morris (2016))

• Information Structure Design & Symmetric Learning• Intervention impact uncertain, effectiveness less than

expected.• Alteration of the informational environment.• Goldstein and Huang (2016), Cong et al (2017)

• Asymmetric Information and Learning• Footnote 11;

Signaling (Angeletos et al (2006)); Reputation (Huang(2017))

• Multiplicity and commitment

Slide 18/24 — Discussion by Will Cong (Chicago Booth) — China’s Model of Managing the Financial System

Overview Model Comments Summary

Comment 3: Information Design and Intervention Costs

• Information Design vs Mechanism Design (Bergemannand Morris (2016))

• Information Structure Design & Symmetric Learning• Intervention impact uncertain, effectiveness less than

expected.• Alteration of the informational environment.• Goldstein and Huang (2016), Cong et al (2017)

• Asymmetric Information and Learning• Footnote 11;

Signaling (Angeletos et al (2006)); Reputation (Huang(2017))

• Multiplicity and commitment

Slide 18/24 — Discussion by Will Cong (Chicago Booth) — China’s Model of Managing the Financial System

Overview Model Comments Summary

Comment 3: Information Design and Intervention Costs

• Information Design vs Mechanism Design (Bergemannand Morris (2016))

• Information Structure Design & Symmetric Learning• Intervention impact uncertain, effectiveness less than

expected.• Alteration of the informational environment.• Goldstein and Huang (2016), Cong et al (2017)

• Asymmetric Information and Learning• Footnote 11;

Signaling (Angeletos et al (2006)); Reputation (Huang(2017))

• Multiplicity and commitment

Slide 18/24 — Discussion by Will Cong (Chicago Booth) — China’s Model of Managing the Financial System

Overview Model Comments Summary

Comment 3: Information Design and Intervention Costs

• Intervention Costs

• Taxpayers’ money, and investment risks in interventions.• Political capital• Disrupted IPO reform and currency internalization• Firing of head of CSRC, Xiao Gang; imprisonment of

Citic officials.

• Impact of Intervention Costs

• Interior optimal intervnetion absent cost of intervention.• What is the welfare gains and losses in gov-centric vs

fundamental-centric equilibrium?• Cost matters when there is dynamic information design.• Relevant for multiple interventions: Cong et al (2017).

Slide 19/24 — Discussion by Will Cong (Chicago Booth) — China’s Model of Managing the Financial System

Overview Model Comments Summary

Comment 3: Information Design and Intervention Costs

• Intervention Costs

• Taxpayers’ money, and investment risks in interventions.• Political capital• Disrupted IPO reform and currency internalization• Firing of head of CSRC, Xiao Gang; imprisonment of

Citic officials.

• Impact of Intervention Costs

• Interior optimal intervnetion absent cost of intervention.• What is the welfare gains and losses in gov-centric vs

fundamental-centric equilibrium?• Cost matters when there is dynamic information design.• Relevant for multiple interventions: Cong et al (2017).

Slide 19/24 — Discussion by Will Cong (Chicago Booth) — China’s Model of Managing the Financial System

Overview Model Comments Summary

Comment 3: Information Design and Intervention Costs

• Intervention Costs

• Taxpayers’ money, and investment risks in interventions.• Political capital• Disrupted IPO reform and currency internalization• Firing of head of CSRC, Xiao Gang; imprisonment of

Citic officials.

• Impact of Intervention Costs

• Interior optimal intervnetion absent cost of intervention.• What is the welfare gains and losses in gov-centric vs

fundamental-centric equilibrium?• Cost matters when there is dynamic information design.• Relevant for multiple interventions: Cong et al (2017).

Slide 19/24 — Discussion by Will Cong (Chicago Booth) — China’s Model of Managing the Financial System

Overview Model Comments Summary

Comment 3: Information Design and Intervention Costs

• Intervention Costs

• Taxpayers’ money, and investment risks in interventions.• Political capital• Disrupted IPO reform and currency internalization• Firing of head of CSRC, Xiao Gang; imprisonment of

Citic officials.

• Impact of Intervention Costs

• Interior optimal intervnetion absent cost of intervention.• What is the welfare gains and losses in gov-centric vs

fundamental-centric equilibrium?• Cost matters when there is dynamic information design.• Relevant for multiple interventions: Cong et al (2017).

Slide 19/24 — Discussion by Will Cong (Chicago Booth) — China’s Model of Managing the Financial System

Overview Model Comments Summary

Comment 3: Information Design and Intervention Costs

• Intervention Costs

• Taxpayers’ money, and investment risks in interventions.• Political capital• Disrupted IPO reform and currency internalization• Firing of head of CSRC, Xiao Gang; imprisonment of

Citic officials.

• Impact of Intervention Costs

• Interior optimal intervnetion absent cost of intervention.• What is the welfare gains and losses in gov-centric vs

fundamental-centric equilibrium?• Cost matters when there is dynamic information design.• Relevant for multiple interventions: Cong et al (2017).

Slide 19/24 — Discussion by Will Cong (Chicago Booth) — China’s Model of Managing the Financial System

Overview Model Comments Summary

Comment 4: Cum Dividend Return and Variance

• By p7

Rt+1 = Dt+1 + Pt+1 − R f Pt

= (θt+1 + σDεDt+1) + (pθθt+1 + pNNt+1)− R f Pt

= (1 + pθ)(ρθθt + σθεθt+1) + σDε

Dt+1

+(pN(ρNNt + σNεNt+1))− R f Pt

• Conditional Variance

Vart(Rt+1) = (1 + pθ)2σ2θ + σ2D + p2Nσ2N (1)

where pθ = 1/(R f − ρθ). which differs from theequation on p9.

• Conditional mean:(1 + pθ)ρθθt + pNρNNt − R f (pθθt + pNNt)= ((1 + pθ)ρθ − R f pθ)θt + pN(ρN − R f )Nt

Slide 20/24 — Discussion by Will Cong (Chicago Booth) — China’s Model of Managing the Financial System

Overview Model Comments Summary

Comment 4: Cum Dividend Return and Variance

• cum dividend?

• Dt + Pt linear in θt and noise?

• No qualitative changes to the results.

• But should be consistent.

Slide 21/24 — Discussion by Will Cong (Chicago Booth) — China’s Model of Managing the Financial System

Overview Model Comments Summary

Other Comments

1 Uniqueness of pN

• Focus on less negative root of pN because it convergeswhen σN → 0

• What about σN →∞? Is the other root more stable?• Not an issue in Wincoop (2006, 2008)

2 Microfoundation of government noise and investorlearning.Footnote 11: Gov possesses private signals.

Slide 22/24 — Discussion by Will Cong (Chicago Booth) — China’s Model of Managing the Financial System

Overview Model Comments Summary

Other Comments

1 Uniqueness of pN

• Focus on less negative root of pN because it convergeswhen σN → 0

• What about σN →∞? Is the other root more stable?• Not an issue in Wincoop (2006, 2008)

2 Microfoundation of government noise and investorlearning.Footnote 11: Gov possesses private signals.

Slide 22/24 — Discussion by Will Cong (Chicago Booth) — China’s Model of Managing the Financial System

Overview Model Comments Summary

Other Comments

1 Role of leverage and deleveraging-driven firesale.

2 Empirical predictions or evidence that the govintervention is indeed a priced factor.

3 coordination failures among regulatory agencies. StateCouncil, PBOC, CBRC, CSRC, and CIRC.

4 Online Appendix.

Slide 23/24 — Discussion by Will Cong (Chicago Booth) — China’s Model of Managing the Financial System

Overview Model Comments Summary

Other Comments

1 Role of leverage and deleveraging-driven firesale.

2 Empirical predictions or evidence that the govintervention is indeed a priced factor.

3 coordination failures among regulatory agencies. StateCouncil, PBOC, CBRC, CSRC, and CIRC.

4 Online Appendix.

Slide 23/24 — Discussion by Will Cong (Chicago Booth) — China’s Model of Managing the Financial System

Overview Model Comments Summary

Other Comments

1 Role of leverage and deleveraging-driven firesale.

2 Empirical predictions or evidence that the govintervention is indeed a priced factor.

3 coordination failures among regulatory agencies. StateCouncil, PBOC, CBRC, CSRC, and CIRC.

4 Online Appendix.

Slide 23/24 — Discussion by Will Cong (Chicago Booth) — China’s Model of Managing the Financial System

Overview Model Comments Summary

Other Comments

1 Role of leverage and deleveraging-driven firesale.

2 Empirical predictions or evidence that the govintervention is indeed a priced factor.

3 coordination failures among regulatory agencies. StateCouncil, PBOC, CBRC, CSRC, and CIRC.

4 Online Appendix.

Slide 23/24 — Discussion by Will Cong (Chicago Booth) — China’s Model of Managing the Financial System

Overview Model Comments Summary

Recap

1 Realistic, important, and timely.

2 More research on the effectiveness and unintendedconsequences of interventions.

3 Empirical studies and policy applications.

Slide 24/24 — Discussion by Will Cong (Chicago Booth) — China’s Model of Managing the Financial System

Overview Model Comments Summary

Recap

1 Realistic, important, and timely.

2 More research on the effectiveness and unintendedconsequences of interventions.

3 Empirical studies and policy applications.

Slide 24/24 — Discussion by Will Cong (Chicago Booth) — China’s Model of Managing the Financial System

Overview Model Comments Summary

Recap

1 Realistic, important, and timely.

2 More research on the effectiveness and unintendedconsequences of interventions.

3 Empirical studies and policy applications.

Slide 24/24 — Discussion by Will Cong (Chicago Booth) — China’s Model of Managing the Financial System