Embed Size (px)

DESCRIPTION

It's Chartered Institute of Management Accountants Course: C-01 Fundamentals of Management Accounting ,Class LSBF Manchester ,Q's By Sir Ian Wilson.

Citation preview

CIMA C1Fundamentals Of Management Accounting

Budgeting

CIMA C1Fundamentals Of Management Accounting

Class Slides – Ian Wilson

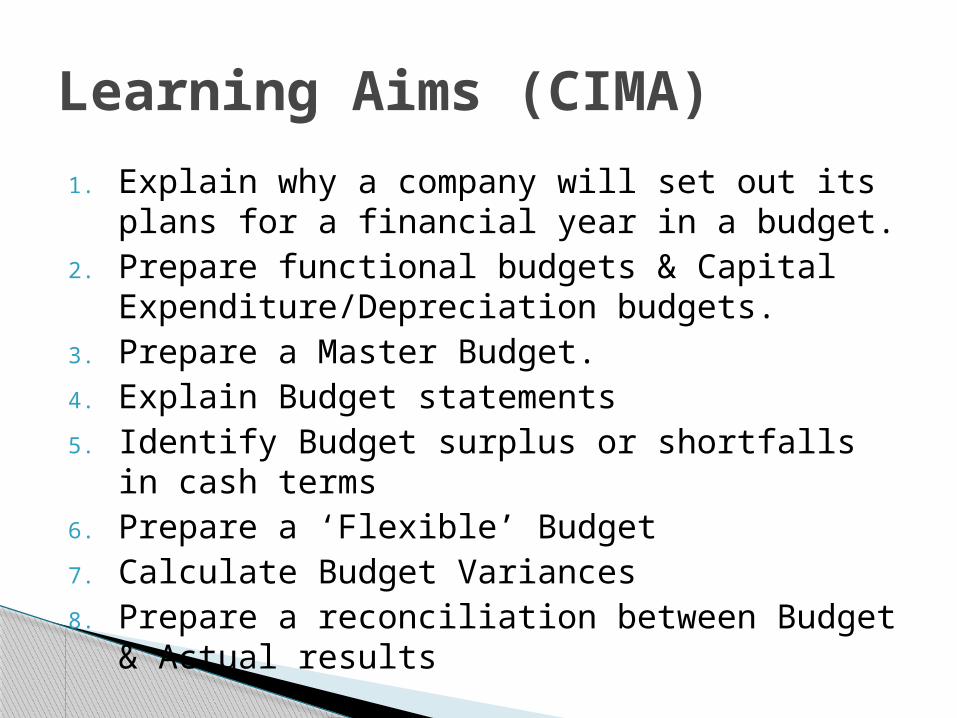

1. Explain why a company will set out its plans for a financial year in a budget.

2. Prepare functional budgets & Capital Expenditure/Depreciation budgets.

3. Prepare a Master Budget.4. Explain Budget statements5. Identify Budget surplus or shortfalls in cash

terms6. Prepare a ‘Flexible’ Budget7. Calculate Budget Variances8. Prepare a reconciliation between Budget &

Actual results

Learning Aims (CIMA)

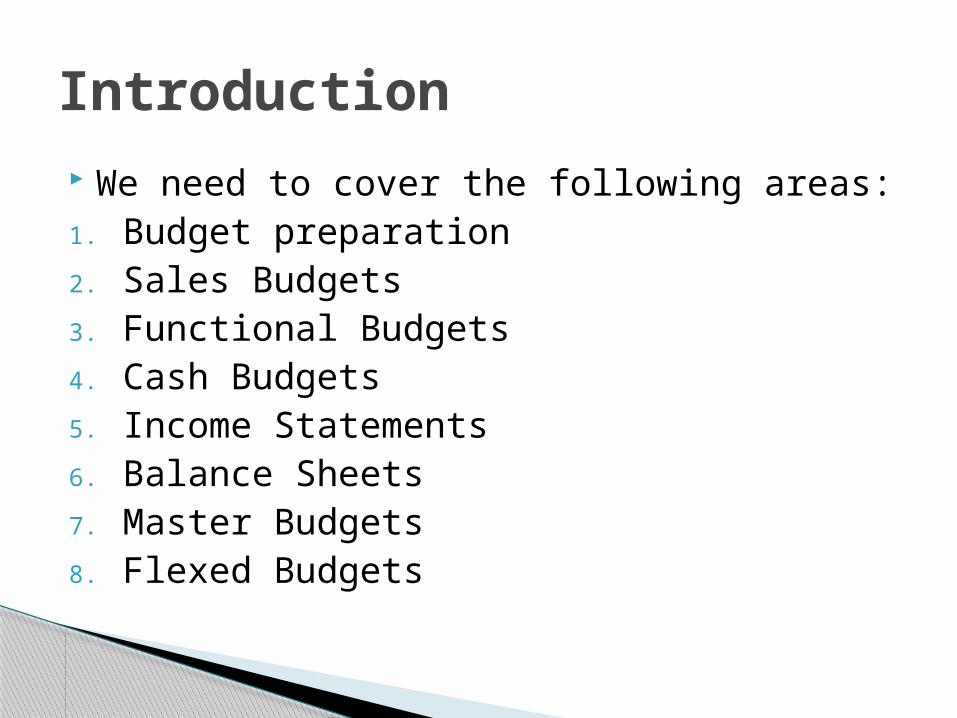

We need to cover the following areas:1. Budget preparation2. Sales Budgets3. Functional Budgets4. Cash Budgets5. Income Statements6. Balance Sheets7. Master Budgets8. Flexed Budgets

Introduction

Why do you as individuals Budget? Think about a company – what do they

need to do! Business planning at Pepsi was “The Plan is

nothing… but Planning is everything.” People just didn’t budget at Pepsi, they

made commitments. “The budget should be a numerical

expression of the strategic plan.” I really love that, it says so much with so few words.

Why do we Budget?

A Budget, What is it?. ‘a quantitative statement, for a defined

period of time, which may include planned revenues, expenses, assets, liabilities and cash flows for a forthcoming accounting period’.

A budget (from old French word bougette, purse) is a financial plan and a list of all planned expenses and revenues. It is a plan for saving, borrowing and spending

Introduction

Budgets are prepared to:1. Set & communicate targets2. Establish a standard to which actual

performance can be compared3. Co-ordinate inter/intra functional activities

Both functional budgets & a master budget can be prepared Remember P:D/M:C

Introduction

Typical functional budgets:1. Sales Budget2. Sales Overhead Budget3. Production Budget4. Materials Usage Budget5. Materials Purchase Budget6. Labour Budget

Functional Budgets

A ‘MASTER’ BUDGET will include:

1. Income Statement2. Cash Budget3. Balance Sheet (Statement of Financial

Position)

Budget construction is overseen by a BUDGET COMMITTEE who often produce a BUDGET MANUAL.

Master Budget

Contains the following:1. Objectives behind the Budget2. Lists of organisational structures, Major

Budgets & Budget responsibility3. Procedures & control4. Timetables5. Key assumptions made6. Principle Budget Factors (PBF’s)

The Budget Manual

Functional budgets prepared BEFORE the Master Budget.

Many Budget changes can be expected and are made before a final version is complete.

Process begins with identifying the PBF (Principal Budget Factor)

This is a ‘Limiting factor’. Sales, Labour Materials & Cash may all be

PBF’s.

Budget Preparation

See pages 76 to 80 for Budget preparation practice & examples.

Exercise 1 Sales Budgets Exercise 2 Planning Production Exercise 3 Material Needs –Usage &

Purchases Exercise 4 Labour Budgets

Budget Preparation

Truro Ltd1. Prepare Production Budget2. Prepare Direct Labour Budget

Exercise 5

What is a Cash Budget?. Recording of the cash impacts of the

functional budgets and is used as a planning tool to deal with a cash surplus/deficit positions.

1. Short term cash surplus2. Short term cash deficit3. Long term cash surplus4. Long term cash deficit

Cash Budgets

Golden rules: Cash items only NO DEPRECIATION Timing - when cash impacts

Exercise 6 X Ltd Constructing a Cash Budget

A Pro-Forma is the best approach

Constructing a Cash Budget

The MASTER BUDGET is an additional & vital BUDGET prepared after the FUNCTIONAL BUDGETS are known

For your C1 exam, the master budget will include:

1. Budgeted Income Statements (IS)2. Budgeted Statement of Financial Position

(SFP)

Master Budgets

This is a Profit & Loss Account Students may be given a partially

completed Income Statement on screen and asked to complete with missing figures.

Pro-Forma on page 83

Budgeted Income Statements

A student may be asked to calculate key balance sheet figures.

This could involve either updating a current balance sheet for a trading period or drafting a balance sheet for a new business.

Pro-forma on page 84

Exercise 7 Budgeted Balance Sheet

Budgeted Balance Sheet

All we have looked at to-date centre of ‘Fixed’ Budgets.

We now have to consider ‘Flexible’ Budgets. A ‘Flexed’ budget considers varying levels

of activity. ‘a budget by which, by recognising different

cost behaviour patterns, is designed to change as volume of activity changes’

Flexible Budgets

Relatively straightforward to produce as they use marginal costing principles.

Fixed & Variable Costs are straightforward Care needs to be taken with Semi-Variable

Costs. You may have to use the High-Low method,

see earlier sessions. Exercise 8 Flexing a Budget

Flexible Budgets

![CIMA C1 Unit 8 2012 [Read-Only]](https://img.pdfslide.net/doc/110x75/563db87c550346aa9a942542/cima-c1-unit-8-2012-read-only.jpg)