Embed Size (px)

Citation preview

Ascensus provides administrative and recordkeeping services and is not a broker-dealer or an investment advisor. Ascensus® and the Ascensus logo are registered trademarks of Ascensus, LLC.Copyright ©2019 Ascensus, LLC. All Rights Reserved.

CIS II Exam Prep Workshop

This course is designed for use in conjunction with seminars conducted by Ascensus. Some areas are not intended to be covered fully, but only highlighted for presentation purposes. It is understood that the publisher is not engaged in rendering legal or accounting services. Every effort has been made to ensure the accuracy of the material presented during the seminar. But retirement plan forms, government regulatory positions and laws are subject to change, so we cannot guarantee the accuracy of the material. The material in this course reflects the law and regulatory interpretations as of the publication date of June 2019.

Much of the information contained in this course is based on the operation of the financial organizations to which we provide services. Some of your procedures may vary if your organization is not a member organization served by us. Ascensus makes no representations regarding compliance of the seminar or guidebook with any state laws or state regulations or federal securities law.

Copyright ©2019 Ascensus, LLC. All Rights Reserved.

No part of this course or presentation may be reproduced in any form by audiotape, photocopy, or any other means without

written permission of the copyright owner.

Copyright ©2019 Ascensus, LLC. All Rights Reserved.800-346-3860 • www.ascensus.com

CIS II Exam Prep Workshop

Copyright ©2019 Ascensus, LLC. All Rights Reserved.800-346-3860 • www.ascensus.com

Table of Contents

CIS II Certification Exam Guidelines . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1

Exam Guidelines . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1

Exam Process . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1

Specific Exam Guidelines . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .2

Maintaining Certification . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .3

Apply Your Knowledge . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .4

Uniform Lifetime Table . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .6

Joint Life Expectancy Table . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .7

Single Life Expectancy Table . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .15

Copyright ©2019 Ascensus, LLC. All Rights Reserved.800-346-3860 • www.ascensus.com

CIS II Exam Prep Workshop

Learning Objectives

At the completion of this course you will be able to

understand the Certified IRA Specialist (CIS) II certification process,

prepare to complete the CIS II exam, and

keep your certification current .

Individual Exercise Group Exercise Group Discussion

Example Job Aid Additional Information

Icon Legend

1Copyright ©2019 Ascensus, LLC. All Rights Reserved.800-346-3860 • www.ascensus.com

CIS II Exam Prep Workshop

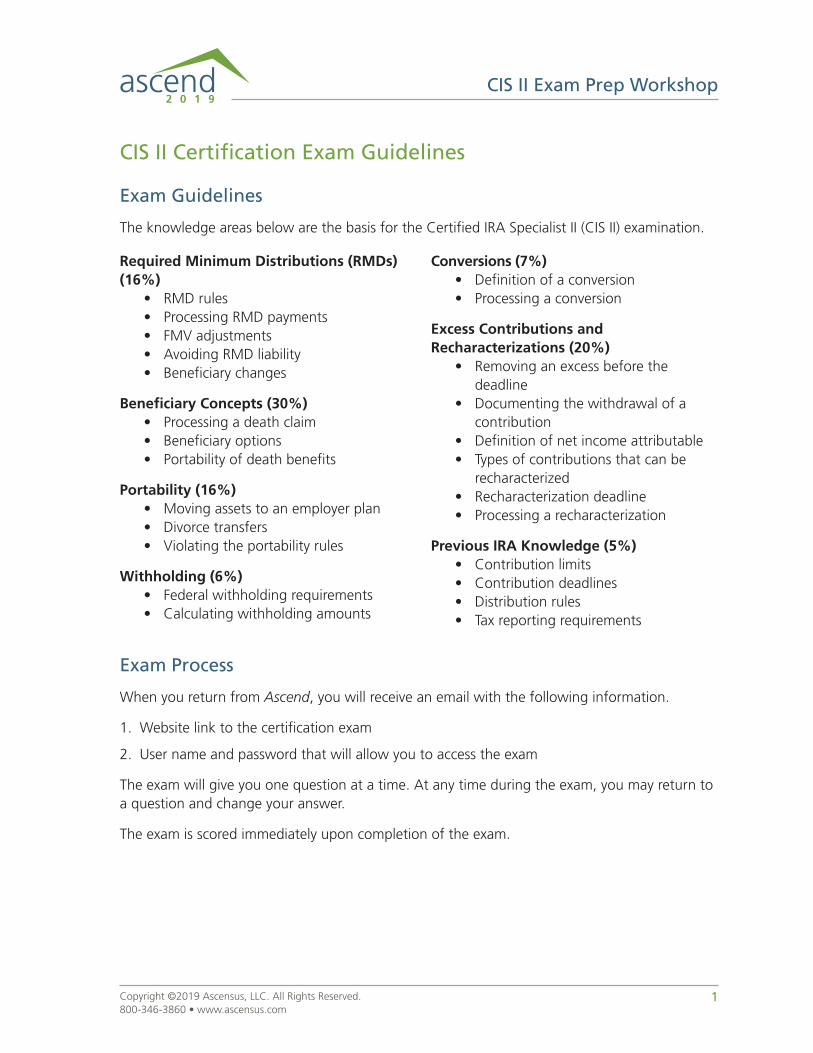

CIS II Certification Exam Guidelines

Exam Guidelines

The knowledge areas below are the basis for the Certified IRA Specialist II (CIS II) examination .

Required Minimum Distributions (RMDs) (16%)

• RMD rules• Processing RMD payments• FMV adjustments• Avoiding RMD liability• Beneficiary changes

Beneficiary Concepts (30%)• Processing a death claim• Beneficiary options• Portability of death benefits

Portability (16%)• Moving assets to an employer plan• Divorce transfers• Violating the portability rules

Withholding (6%)• Federal withholding requirements• Calculating withholding amounts

Conversions (7%)• Definition of a conversion• Processing a conversion

Excess Contributions and Recharacterizations (20%)

• Removing an excess before the deadline

• Documenting the withdrawal of a contribution

• Definition of net income attributable• Types of contributions that can be

recharacterized• Recharacterization deadline• Processing a recharacterization

Previous IRA Knowledge (5%)• Contribution limits• Contribution deadlines• Distribution rules• Tax reporting requirements

Exam Process

When you return from Ascend, you will receive an email with the following information .

1 . Website link to the certification exam

2 . User name and password that will allow you to access the exam

The exam will give you one question at a time . At any time during the exam, you may return to a question and change your answer .

The exam is scored immediately upon completion of the exam .

2 Copyright ©2019 Ascensus, LLC. All Rights Reserved.800-346-3860 • www.ascensus.com

CIS II Exam Prep Workshop

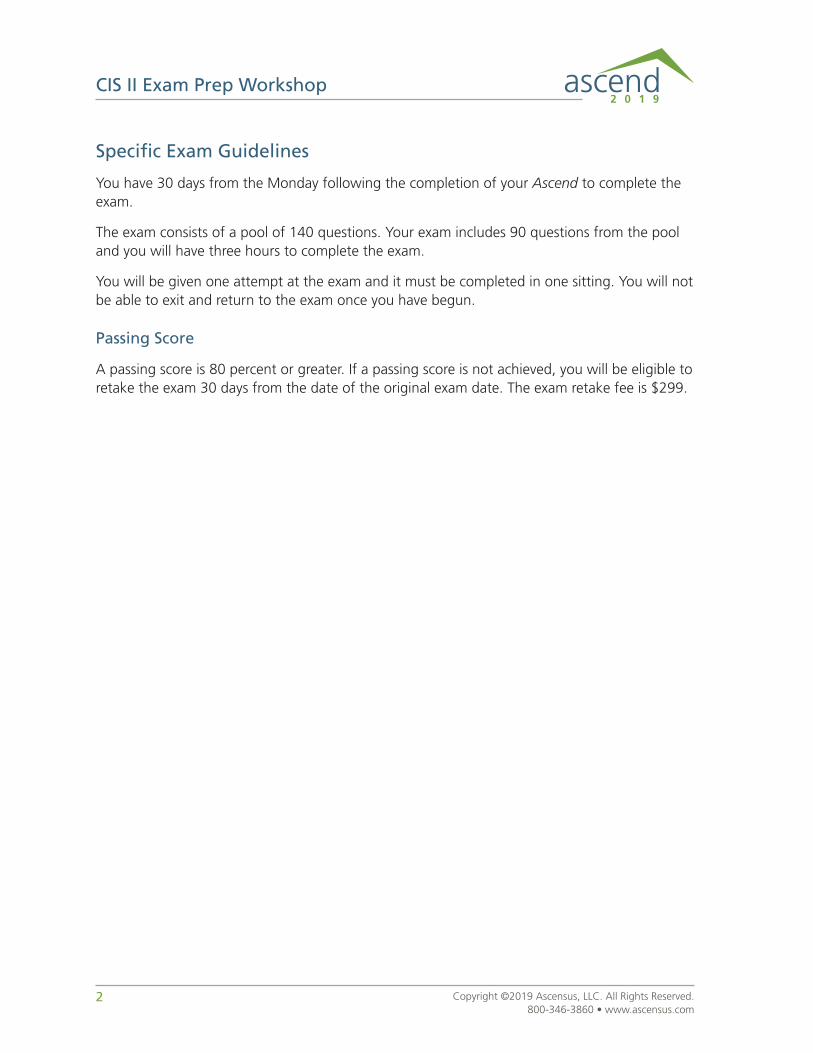

Specific Exam Guidelines

You have 30 days from the Monday following the completion of your Ascend to complete the exam .

The exam consists of a pool of 140 questions . Your exam includes 90 questions from the pool and you will have three hours to complete the exam .

You will be given one attempt at the exam and it must be completed in one sitting . You will not be able to exit and return to the exam once you have begun .

Passing Score

A passing score is 80 percent or greater . If a passing score is not achieved, you will be eligible to retake the exam 30 days from the date of the original exam date . The exam retake fee is $299 .

3Copyright ©2019 Ascensus, LLC. All Rights Reserved.800-346-3860 • www.ascensus.com

CIS II Exam Prep Workshop

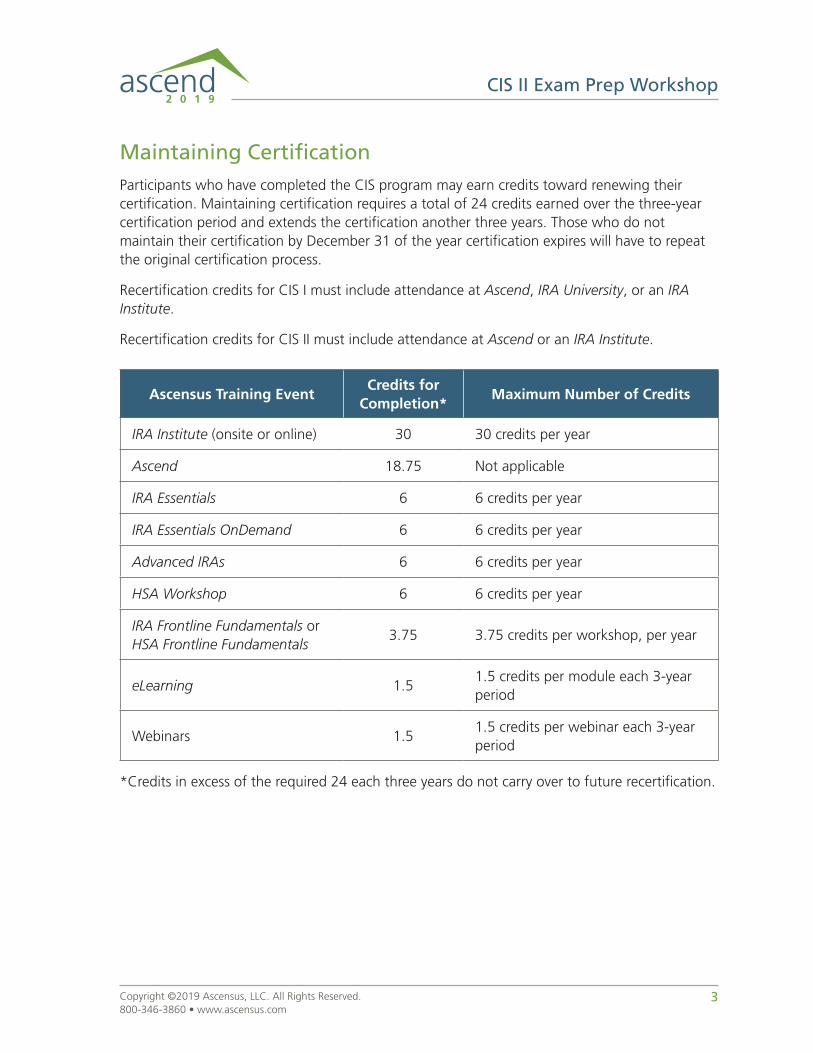

Maintaining CertificationParticipants who have completed the CIS program may earn credits toward renewing their certification . Maintaining certification requires a total of 24 credits earned over the three-year certification period and extends the certification another three years . Those who do not maintain their certification by December 31 of the year certification expires will have to repeat the original certification process .

Recertification credits for CIS I must include attendance at Ascend, IRA University, or an IRA Institute .

Recertification credits for CIS II must include attendance at Ascend or an IRA Institute .

Ascensus Training EventCredits for

Completion*Maximum Number of Credits

IRA Institute (onsite or online) 30 30 credits per year

Ascend 18 .75 Not applicable

IRA Essentials 6 6 credits per year

IRA Essentials OnDemand 6 6 credits per year

Advanced IRAs 6 6 credits per year

HSA Workshop 6 6 credits per year

IRA Frontline Fundamentals or HSA Frontline Fundamentals

3 .75 3 .75 credits per workshop, per year

eLearning 1 .51 .5 credits per module each 3-year period

Webinars 1 .51 .5 credits per webinar each 3-year period

*Credits in excess of the required 24 each three years do not carry over to future recertification .

4 Copyright ©2019 Ascensus, LLC. All Rights Reserved.800-346-3860 • www.ascensus.com

CIS II Exam Prep Workshop

Apply Your KnowledgeAs you learn about IRA regulations and procedures, it is helpful to put your new knowledge to work . This case study is designed to help you apply the information that you learn in the CIS II learning track to real-life situations .

Each exercise will help you use the information in the classes you have completed .

Welcome to Redline Financial

Welcome to Redline Financial . We are glad that you chose Redline Financial as your employer . We heard that you have learned a lot about IRAs, and you are ready to help us with IRA transactions . We are sure you can handle the position you accepted, so let’s get started .

Financial Organization InformationRedline Financial6269 West AvenuePort St . John, FL 32920Phone: (321) 555-5555

5Copyright ©2019 Ascensus, LLC. All Rights Reserved.800-346-3860 • www.ascensus.com

CIS II Exam Prep Workshop

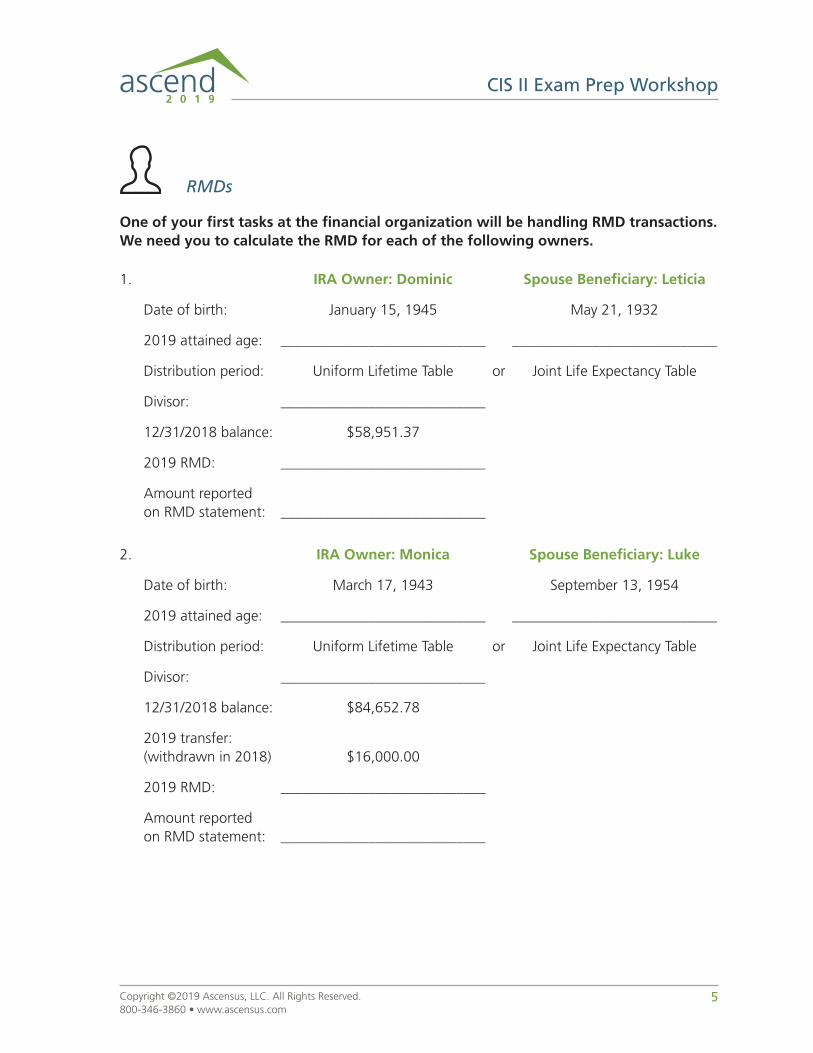

RMDs

One of your first tasks at the financial organization will be handling RMD transactions. We need you to calculate the RMD for each of the following owners.

1 . IRA Owner: Dominic Spouse Beneficiary: Leticia

Date of birth: January 15, 1945 May 21, 1932

2019 attained age: ____________________________ ____________________________

Distribution period: Uniform Lifetime Table or Joint Life Expectancy Table

Divisor: ____________________________

12/31/2018 balance: $58,951 .37

2019 RMD: ____________________________

Amount reported on RMD statement: ____________________________

2 . IRA Owner: Monica Spouse Beneficiary: Luke

Date of birth: March 17, 1943 September 13, 1954

2019 attained age: ____________________________ ____________________________

Distribution period: Uniform Lifetime Table or Joint Life Expectancy Table

Divisor: ____________________________

12/31/2018 balance: $84,652 .78

2019 transfer: (withdrawn in 2018) $16,000 .00

2019 RMD: ____________________________

Amount reported on RMD statement: ____________________________

6 Copyright ©2019 Ascensus, LLC. All Rights Reserved.800-346-3860 • www.ascensus.com

CIS II Exam Prep Workshop

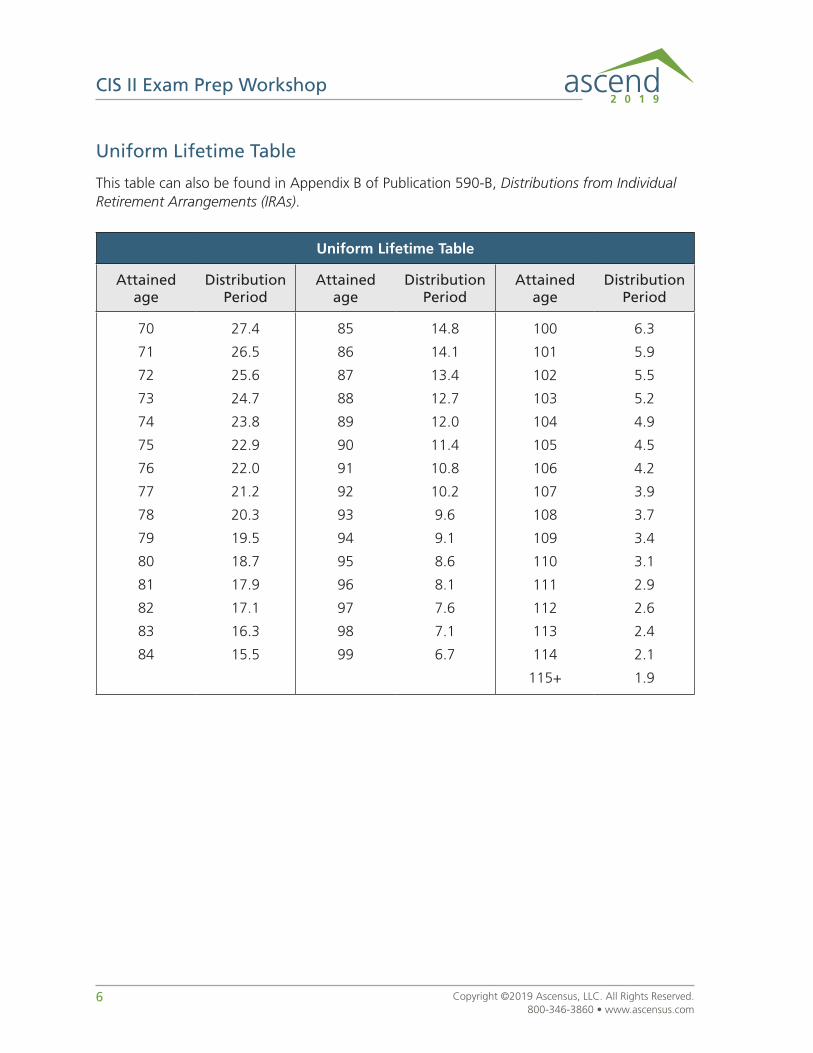

Uniform Lifetime Table

This table can also be found in Appendix B of Publication 590-B, Distributions from Individual Retirement Arrangements (IRAs) .

Uniform Lifetime Table

Attained age

Distribution Period

Attained age

Distribution Period

Attained age

Distribution Period

70

71

72

73

74

75

76

77

78

79

80

81

82

83

84

27 .4

26 .5

25 .6

24 .7

23 .8

22 .9

22 .0

21 .2

20 .3

19 .5

18 .7

17 .9

17 .1

16 .3

15 .5

85

86

87

88

89

90

91

92

93

94

95

96

97

98

99

14 .8

14 .1

13 .4

12 .7

12 .0

11 .4

10 .8

10 .2

9 .6

9 .1

8 .6

8 .1

7 .6

7 .1

6 .7

100

101

102

103

104

105

106

107

108

109

110

111

112

113

114

115+

6 .3

5 .9

5 .5

5 .2

4 .9

4 .5

4 .2

3 .9

3 .7

3 .4

3 .1

2 .9

2 .6

2 .4

2 .1

1 .9

7Copyright ©2019 Ascensus, LLC. All Rights Reserved.800-346-3860 • www.ascensus.com

CIS II Exam Prep Workshop

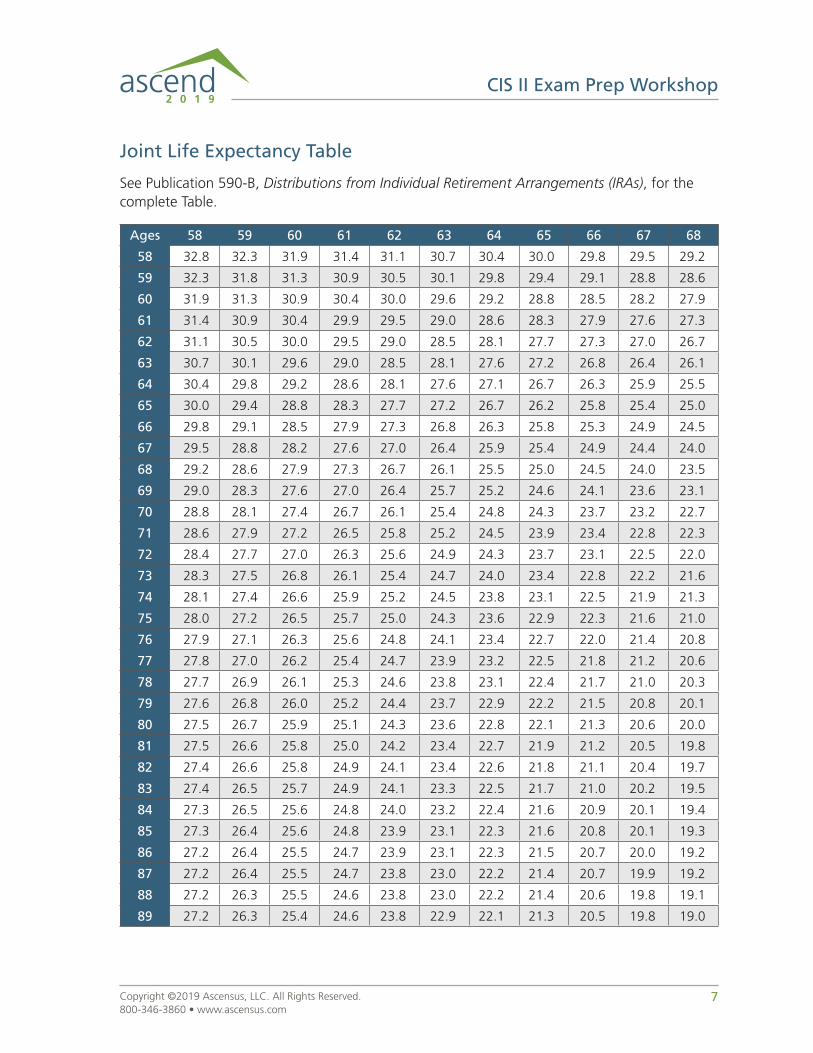

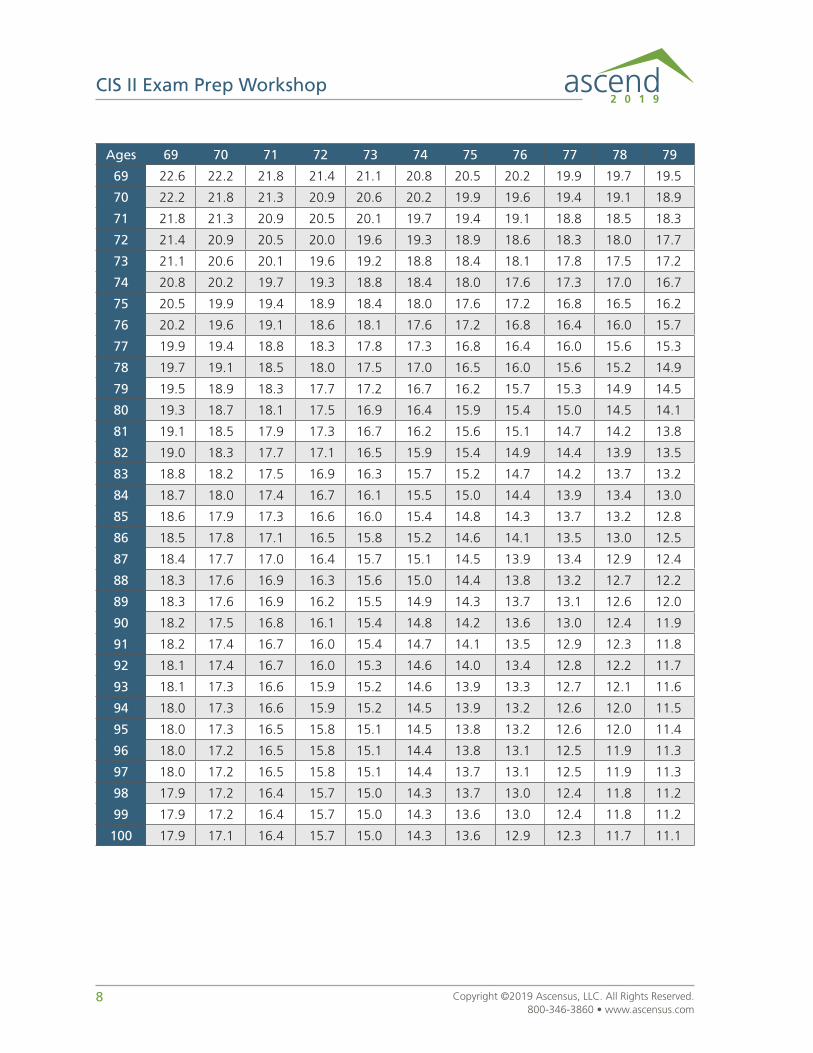

Joint Life Expectancy Table

See Publication 590-B, Distributions from Individual Retirement Arrangements (IRAs), for the complete Table .

Ages 58 59 60 61 62 63 64 65 66 67 68

58 32 .8 32 .3 31 .9 31 .4 31 .1 30 .7 30 .4 30 .0 29 .8 29 .5 29 .2

59 32 .3 31 .8 31 .3 30 .9 30 .5 30 .1 29 .8 29 .4 29 .1 28 .8 28 .6

60 31 .9 31 .3 30 .9 30 .4 30 .0 29 .6 29 .2 28 .8 28 .5 28 .2 27 .9

61 31 .4 30 .9 30 .4 29 .9 29 .5 29 .0 28 .6 28 .3 27 .9 27 .6 27 .3

62 31 .1 30 .5 30 .0 29 .5 29 .0 28 .5 28 .1 27 .7 27 .3 27 .0 26 .7

63 30 .7 30 .1 29 .6 29 .0 28 .5 28 .1 27 .6 27 .2 26 .8 26 .4 26 .1

64 30 .4 29 .8 29 .2 28 .6 28 .1 27 .6 27 .1 26 .7 26 .3 25 .9 25 .5

65 30 .0 29 .4 28 .8 28 .3 27 .7 27 .2 26 .7 26 .2 25 .8 25 .4 25 .0

66 29 .8 29 .1 28 .5 27 .9 27 .3 26 .8 26 .3 25 .8 25 .3 24 .9 24 .5

67 29 .5 28 .8 28 .2 27 .6 27 .0 26 .4 25 .9 25 .4 24 .9 24 .4 24 .0

68 29 .2 28 .6 27 .9 27 .3 26 .7 26 .1 25 .5 25 .0 24 .5 24 .0 23 .5

69 29 .0 28 .3 27 .6 27 .0 26 .4 25 .7 25 .2 24 .6 24 .1 23 .6 23 .1

70 28 .8 28 .1 27 .4 26 .7 26 .1 25 .4 24 .8 24 .3 23 .7 23 .2 22 .7

71 28 .6 27 .9 27 .2 26 .5 25 .8 25 .2 24 .5 23 .9 23 .4 22 .8 22 .3

72 28 .4 27 .7 27 .0 26 .3 25 .6 24 .9 24 .3 23 .7 23 .1 22 .5 22 .0

73 28 .3 27 .5 26 .8 26 .1 25 .4 24 .7 24 .0 23 .4 22 .8 22 .2 21 .6

74 28 .1 27 .4 26 .6 25 .9 25 .2 24 .5 23 .8 23 .1 22 .5 21 .9 21 .3

75 28 .0 27 .2 26 .5 25 .7 25 .0 24 .3 23 .6 22 .9 22 .3 21 .6 21 .0

76 27 .9 27 .1 26 .3 25 .6 24 .8 24 .1 23 .4 22 .7 22 .0 21 .4 20 .8

77 27 .8 27 .0 26 .2 25 .4 24 .7 23 .9 23 .2 22 .5 21 .8 21 .2 20 .6

78 27 .7 26 .9 26 .1 25 .3 24 .6 23 .8 23 .1 22 .4 21 .7 21 .0 20 .3

79 27 .6 26 .8 26 .0 25 .2 24 .4 23 .7 22 .9 22 .2 21 .5 20 .8 20 .1

80 27 .5 26 .7 25 .9 25 .1 24 .3 23 .6 22 .8 22 .1 21 .3 20 .6 20 .0

81 27 .5 26 .6 25 .8 25 .0 24 .2 23 .4 22 .7 21 .9 21 .2 20 .5 19 .8

82 27 .4 26 .6 25 .8 24 .9 24 .1 23 .4 22 .6 21 .8 21 .1 20 .4 19 .7

83 27 .4 26 .5 25 .7 24 .9 24 .1 23 .3 22 .5 21 .7 21 .0 20 .2 19 .5

84 27 .3 26 .5 25 .6 24 .8 24 .0 23 .2 22 .4 21 .6 20 .9 20 .1 19 .4

85 27 .3 26 .4 25 .6 24 .8 23 .9 23 .1 22 .3 21 .6 20 .8 20 .1 19 .3

86 27 .2 26 .4 25 .5 24 .7 23 .9 23 .1 22 .3 21 .5 20 .7 20 .0 19 .2

87 27 .2 26 .4 25 .5 24 .7 23 .8 23 .0 22 .2 21 .4 20 .7 19 .9 19 .2

88 27 .2 26 .3 25 .5 24 .6 23 .8 23 .0 22 .2 21 .4 20 .6 19 .8 19 .1

89 27 .2 26 .3 25 .4 24 .6 23 .8 22 .9 22 .1 21 .3 20 .5 19 .8 19 .0

8 Copyright ©2019 Ascensus, LLC. All Rights Reserved.800-346-3860 • www.ascensus.com

CIS II Exam Prep Workshop

Ages 69 70 71 72 73 74 75 76 77 78 79

69 22 .6 22 .2 21 .8 21 .4 21 .1 20 .8 20 .5 20 .2 19 .9 19 .7 19 .5

70 22 .2 21 .8 21 .3 20 .9 20 .6 20 .2 19 .9 19 .6 19 .4 19 .1 18 .9

71 21 .8 21 .3 20 .9 20 .5 20 .1 19 .7 19 .4 19 .1 18 .8 18 .5 18 .3

72 21 .4 20 .9 20 .5 20 .0 19 .6 19 .3 18 .9 18 .6 18 .3 18 .0 17 .7

73 21 .1 20 .6 20 .1 19 .6 19 .2 18 .8 18 .4 18 .1 17 .8 17 .5 17 .2

74 20 .8 20 .2 19 .7 19 .3 18 .8 18 .4 18 .0 17 .6 17 .3 17 .0 16 .7

75 20 .5 19 .9 19 .4 18 .9 18 .4 18 .0 17 .6 17 .2 16 .8 16 .5 16 .2

76 20 .2 19 .6 19 .1 18 .6 18 .1 17 .6 17 .2 16 .8 16 .4 16 .0 15 .7

77 19 .9 19 .4 18 .8 18 .3 17 .8 17 .3 16 .8 16 .4 16 .0 15 .6 15 .3

78 19 .7 19 .1 18 .5 18 .0 17 .5 17 .0 16 .5 16 .0 15 .6 15 .2 14 .9

79 19 .5 18 .9 18 .3 17 .7 17 .2 16 .7 16 .2 15 .7 15 .3 14 .9 14 .5

80 19 .3 18 .7 18 .1 17 .5 16 .9 16 .4 15 .9 15 .4 15 .0 14 .5 14 .1

81 19 .1 18 .5 17 .9 17 .3 16 .7 16 .2 15 .6 15 .1 14 .7 14 .2 13 .8

82 19 .0 18 .3 17 .7 17 .1 16 .5 15 .9 15 .4 14 .9 14 .4 13 .9 13 .5

83 18 .8 18 .2 17 .5 16 .9 16 .3 15 .7 15 .2 14 .7 14 .2 13 .7 13 .2

84 18 .7 18 .0 17 .4 16 .7 16 .1 15 .5 15 .0 14 .4 13 .9 13 .4 13 .0

85 18 .6 17 .9 17 .3 16 .6 16 .0 15 .4 14 .8 14 .3 13 .7 13 .2 12 .8

86 18 .5 17 .8 17 .1 16 .5 15 .8 15 .2 14 .6 14 .1 13 .5 13 .0 12 .5

87 18 .4 17 .7 17 .0 16 .4 15 .7 15 .1 14 .5 13 .9 13 .4 12 .9 12 .4

88 18 .3 17 .6 16 .9 16 .3 15 .6 15 .0 14 .4 13 .8 13 .2 12 .7 12 .2

89 18 .3 17 .6 16 .9 16 .2 15 .5 14 .9 14 .3 13 .7 13 .1 12 .6 12 .0

90 18 .2 17 .5 16 .8 16 .1 15 .4 14 .8 14 .2 13 .6 13 .0 12 .4 11 .9

91 18 .2 17 .4 16 .7 16 .0 15 .4 14 .7 14 .1 13 .5 12 .9 12 .3 11 .8

92 18 .1 17 .4 16 .7 16 .0 15 .3 14 .6 14 .0 13 .4 12 .8 12 .2 11 .7

93 18 .1 17 .3 16 .6 15 .9 15 .2 14 .6 13 .9 13 .3 12 .7 12 .1 11 .6

94 18 .0 17 .3 16 .6 15 .9 15 .2 14 .5 13 .9 13 .2 12 .6 12 .0 11 .5

95 18 .0 17 .3 16 .5 15 .8 15 .1 14 .5 13 .8 13 .2 12 .6 12 .0 11 .4

96 18 .0 17 .2 16 .5 15 .8 15 .1 14 .4 13 .8 13 .1 12 .5 11 .9 11 .3

97 18 .0 17 .2 16 .5 15 .8 15 .1 14 .4 13 .7 13 .1 12 .5 11 .9 11 .3

98 17 .9 17 .2 16 .4 15 .7 15 .0 14 .3 13 .7 13 .0 12 .4 11 .8 11 .2

99 17 .9 17 .2 16 .4 15 .7 15 .0 14 .3 13 .6 13 .0 12 .4 11 .8 11 .2

100 17 .9 17 .1 16 .4 15 .7 15 .0 14 .3 13 .6 12 .9 12 .3 11 .7 11 .1

9Copyright ©2019 Ascensus, LLC. All Rights Reserved.800-346-3860 • www.ascensus.com

CIS II Exam Prep Workshop

Death Claims

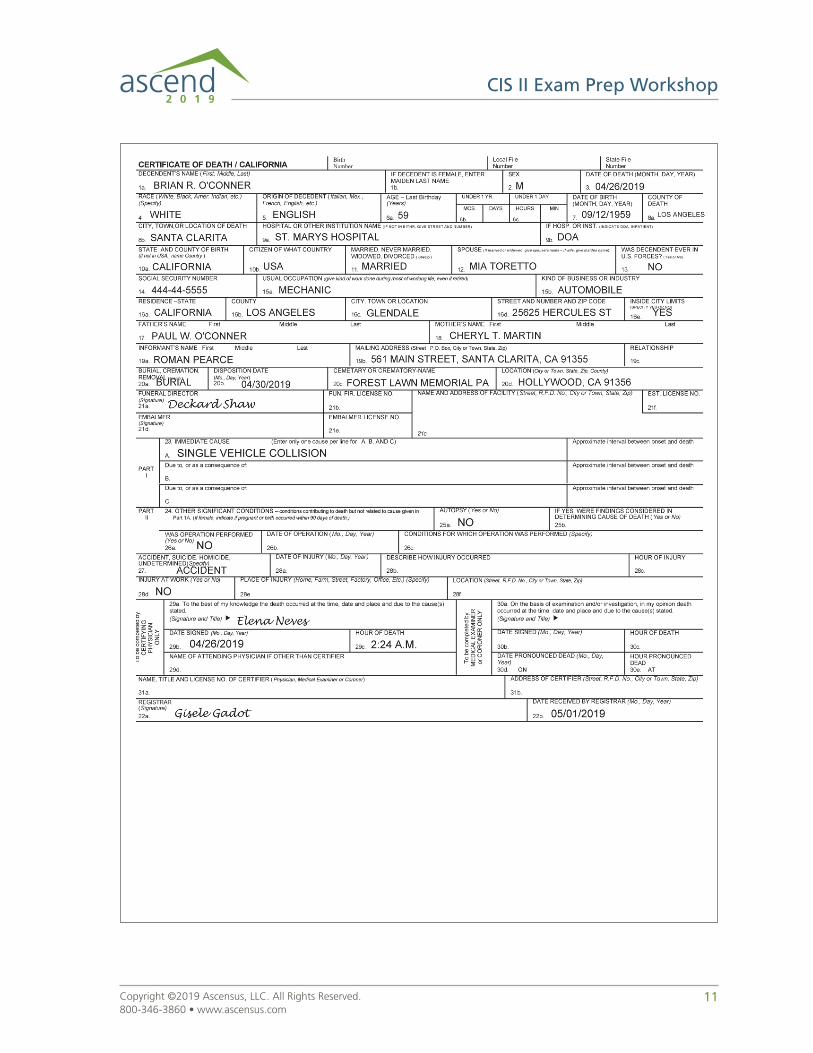

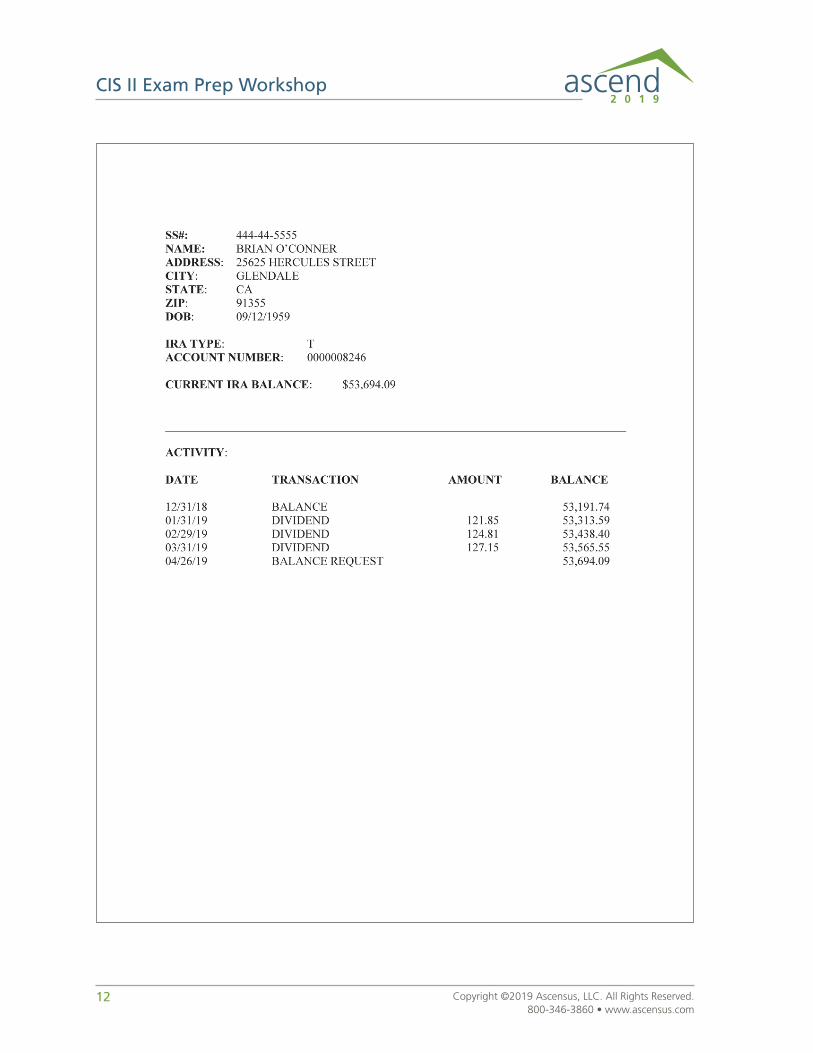

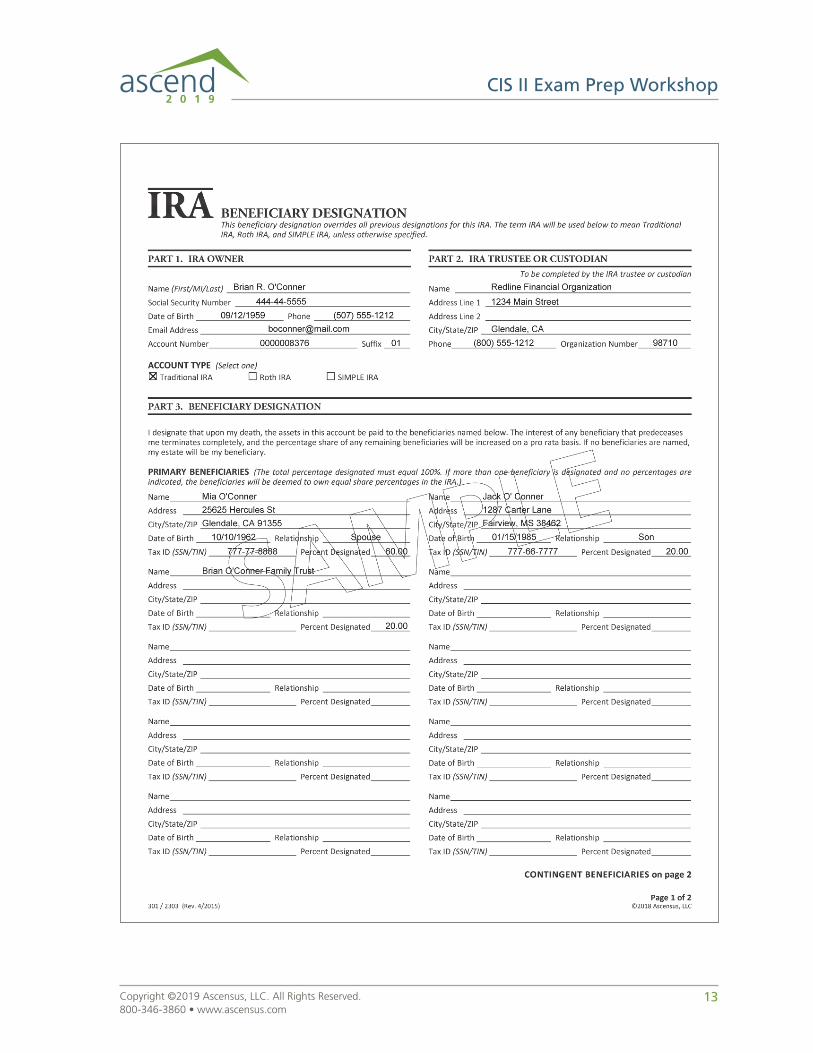

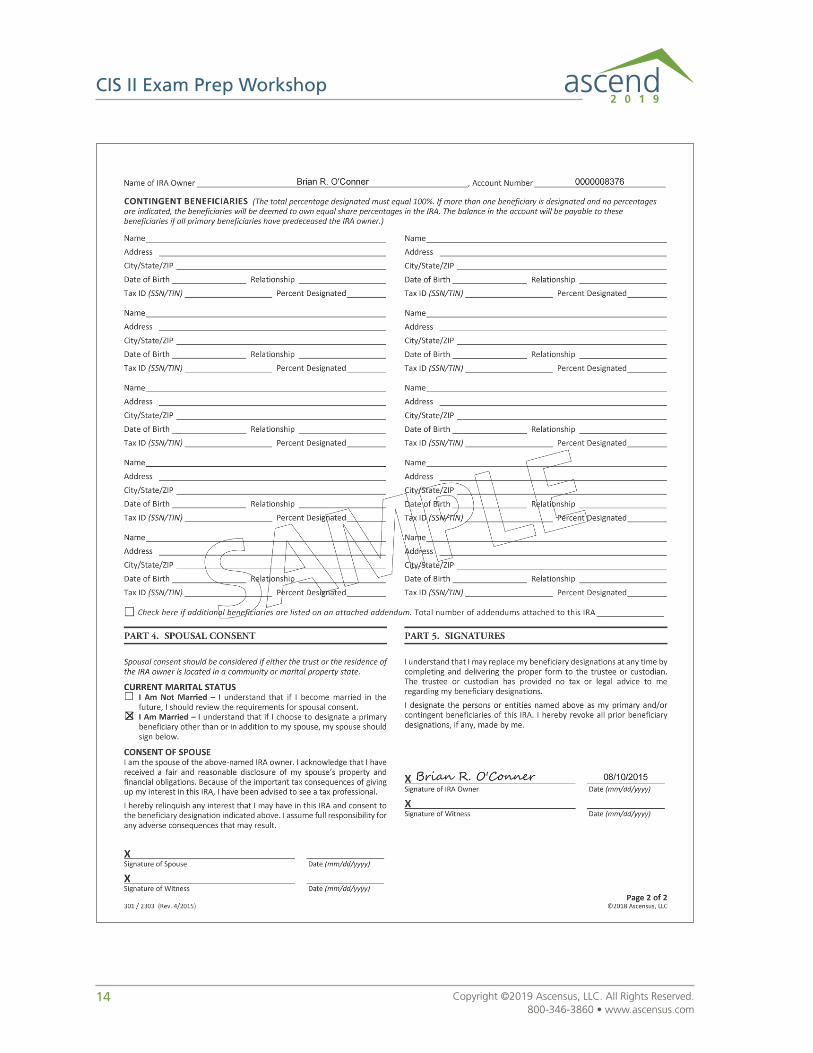

You are provided the following information (and documents on pages 11-14) about a deceased IRA owner.

Brian O’Conner passed away . His wife, Mia, is in the financial organization today, May 12, 2019, to notify you of his death . Brian has not been taking distributions from his IRA .

1 . Date of death: ____________________________________

2 . Date of death value: ____________________________________

3 . Type of account: Traditional IRA

Roth IRA

4 . Traditional IRA owner died: Before required beginning date (RBD)

On or after RBD

5 . Amount of RMD disbursed in the year of death to Traditional IRA owner: ____________________________________

6 . Owner died in: Current year

Previous year

7 . Assuming separate accounting is done, what are Mia’s distribution options?

Life expectancy payments

Five-year rule

Transfer to own IRA

Distribution and rollover

Lump sum

10 Copyright ©2019 Ascensus, LLC. All Rights Reserved.800-346-3860 • www.ascensus.com

CIS II Exam Prep Workshop

8 . What are Jack’s distribution options?

Life expectancy payments

Five-year rule

Transfer to own IRA

Distribution and rollover

Lump sum

9 . What are the distribution options for the Brian O’Conner Revocable Family Trust?

Life expectancy payments

Five-year rule

Transfer to own IRA

Distribution and rollover

Lump sum

10 . What is Jack’s election deadline?

_________________________________________________________________________________

11 . On which IRS form are the distributions to Jack reported?

_________________________________________________________________________________

12 . In whose name and TIN is the distribution to Jack reported?

_________________________________________________________________________________

13 . What is Mia’s election deadline?

_________________________________________________________________________________

14 . If Mia elects life expectancy payments, what is the deadline for Mia to start taking payments?

_________________________________________________________________________________

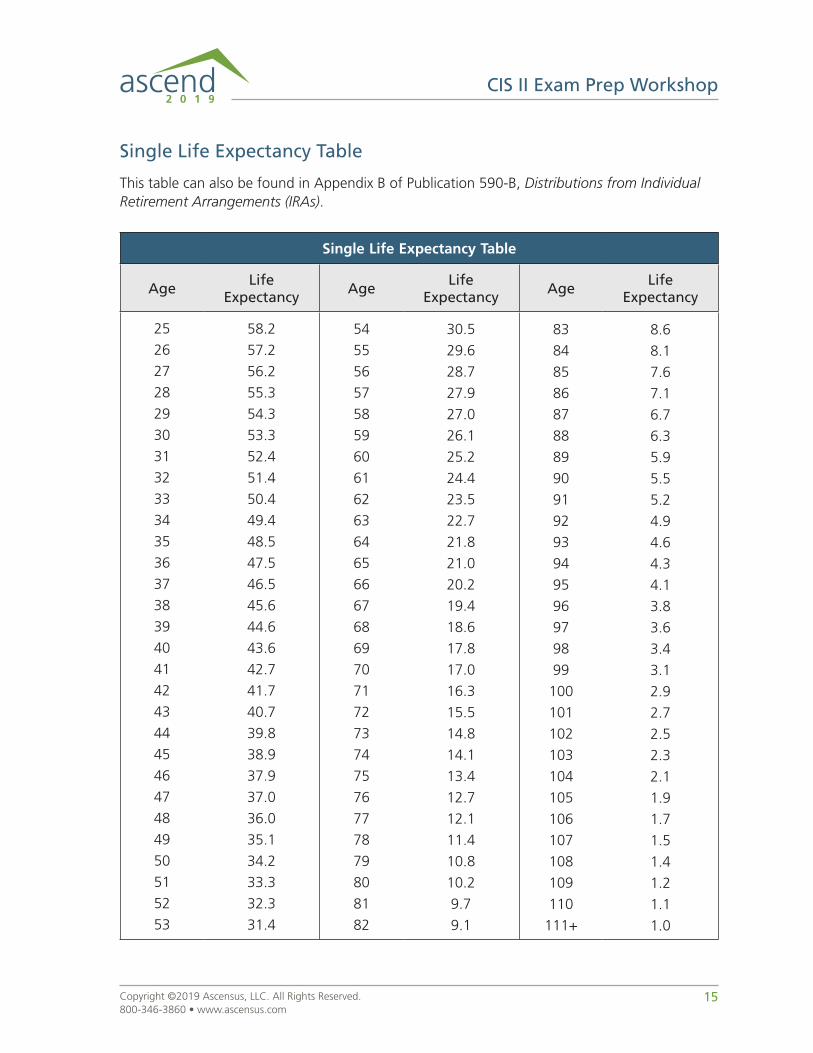

15 . If Jack’s date of birth is January 15, 1985, how much must he withdraw as a life expectancy payment in the first distribution year, if his portion of the IRA balance is $31,799 .49 on December 31, 2019?

_________________________________________________________________________________

11Copyright ©2019 Ascensus, LLC. All Rights Reserved.800-346-3860 • www.ascensus.com

CIS II Exam Prep Workshop

12 Copyright ©2019 Ascensus, LLC. All Rights Reserved.800-346-3860 • www.ascensus.com

CIS II Exam Prep Workshop

13Copyright ©2019 Ascensus, LLC. All Rights Reserved.800-346-3860 • www.ascensus.com

CIS II Exam Prep Workshop

14 Copyright ©2019 Ascensus, LLC. All Rights Reserved.800-346-3860 • www.ascensus.com

CIS II Exam Prep Workshop

15Copyright ©2019 Ascensus, LLC. All Rights Reserved.800-346-3860 • www.ascensus.com

CIS II Exam Prep Workshop

Single Life Expectancy Table

This table can also be found in Appendix B of Publication 590-B, Distributions from Individual Retirement Arrangements (IRAs) .

Single Life Expectancy Table

Age Life Expectancy Age Life

Expectancy Age Life Expectancy

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

46

47

48

49

50

51

52

53

58 .2

57 .2

56 .2

55 .3

54 .3

53 .3

52 .4

51 .4

50 .4

49 .4

48 .5

47 .5

46 .5

45 .6

44 .6

43 .6

42 .7

41 .7

40 .7

39 .8

38 .9

37 .9

37 .0

36 .0

35 .1

34 .2

33 .3

32 .3

31 .4

54

55

56

57

58

59

60

61

62

63

64

65

66

67

68

69

70

71

72

73

74

75

76

77

78

79

80

81

82

30 .5

29 .6

28 .7

27 .9

27 .0

26 .1

25 .2

24 .4

23 .5

22 .7

21 .8

21 .0

20 .2

19 .4

18 .6

17 .8

17 .0

16 .3

15 .5

14 .8

14 .1

13 .4

12 .7

12 .1

11 .4

10 .8

10 .2

9 .7

9 .1

83

84

85

86

87

88

89

90

91

92

93

94

95

96

97

98

99

100

101

102

103

104

105

106

107

108

109

110

111+

8 .6

8 .1

7 .6

7 .1

6 .7

6 .3

5 .9

5 .5

5 .2

4 .9

4 .6

4 .3

4 .1

3 .8

3 .6

3 .4

3 .1

2 .9

2 .7

2 .5

2 .3

2 .1

1 .9

1 .7

1 .5

1 .4

1 .2

1 .1

1 .0

16 Copyright ©2019 Ascensus, LLC. All Rights Reserved.800-346-3860 • www.ascensus.com

CIS II Exam Prep Workshop

Withdrawals and Withholding

Today, you are responsible for handling withdrawals. The following IRA owners have come into the financial organization to take distributions. Determine the amount that will be withdrawn from the IRA, and the amount that will be given to the IRA owner.

1 . Kara is in your financial organization today . She would like to receive $5,000 after 10 percent federal withholding .

What is the amount of the gross distribution? __________________________________

What is the amount of federal withholding? __________________________________

What is the amount of the net payment? __________________________________

2 . Sean is withdrawing the entire $5,000 from his IRA and wants to have 10 percent withheld for federal income taxes .

What is the amount of the gross distribution? __________________________________

What is the amount of federal withholding? __________________________________

What is the amount of the net payment? __________________________________

3 . Frank is taking scheduled quarterly payments in March, June, September and December from his Traditional IRA . Frank elected to have 10 percent of his scheduled payments withheld for federal income taxes . In July, Frank made a $100 withdrawal and chose to waive withholding .

How should withholding be handled on the next scheduled payment if Frank completes no additional paperwork?

________________________________________________________________________________________

________________________________________________________________________________________

How could you ensure that Frank’s scheduled payments stay the same?

________________________________________________________________________________________

________________________________________________________________________________________

17Copyright ©2019 Ascensus, LLC. All Rights Reserved.800-346-3860 • www.ascensus.com

CIS II Exam Prep Workshop

Excess and Recharacterizations

On June 4, 2018, Monica, age 42, deposited $5,500 in her Traditional IRA . On that day, the balance before the contribution was $32,800 . On March 29, 2019, Monica discovers she was ineligible for a 2018 Traditional IRA contribution and decides to remove the $5,500 contribution under the excess contribution rules . Consequently, she must distribute the $5,500 excess contribution plus the net income attributable to the excess amount . No other contributions or distributions have been made .

On March 29, 2019, Monica’s IRA balance is $39,000 . She will incur a $75 loss of investment penalty when she prematurely surrenders the IRA investment to distribute the excess . Monica filed her 2018 taxes timely .

Excess contribution = ______________________

Adjusted opening balance = ______________________

Adjusted closing balance = ______________________

Total earnings = ______________________

NIA = ______________________

18 Copyright ©2019 Ascensus, LLC. All Rights Reserved.800-346-3860 • www.ascensus.com

CIS II Exam Prep Workshop

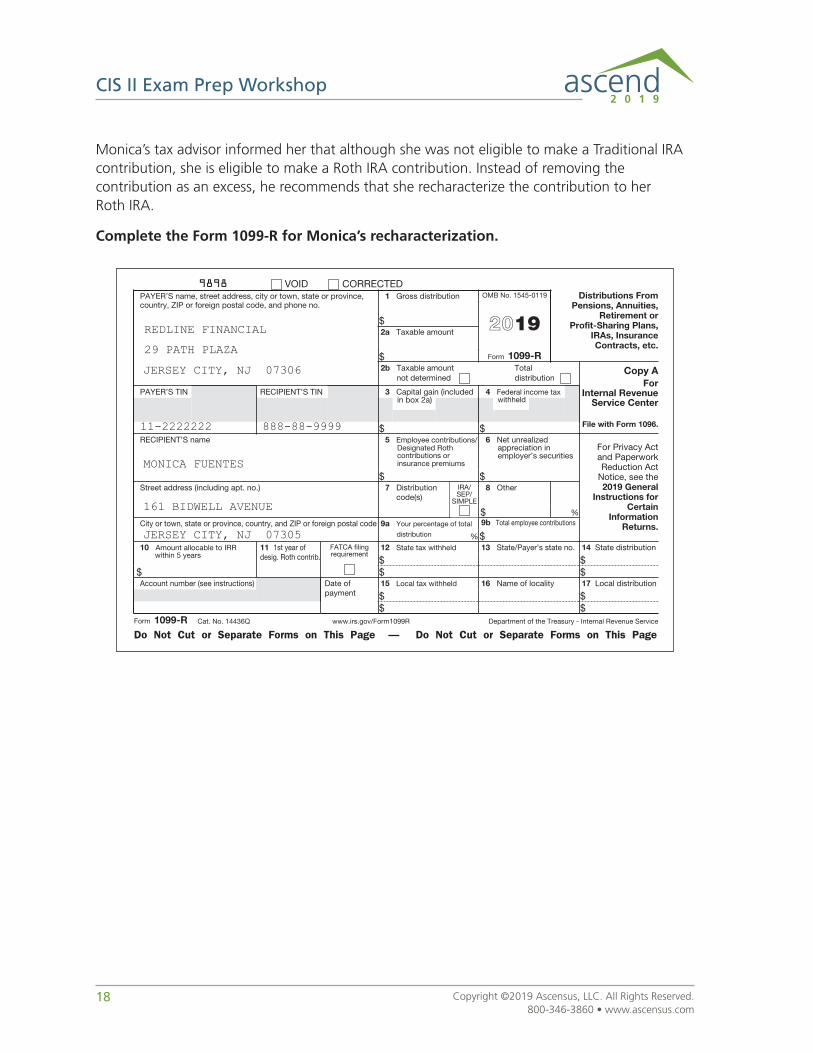

Monica’s tax advisor informed her that although she was not eligible to make a Traditional IRA contribution, she is eligible to make a Roth IRA contribution . Instead of removing the contribution as an excess, he recommends that she recharacterize the contribution to her Roth IRA .

Complete the Form 1099-R for Monica’s recharacterization.

19Copyright ©2019 Ascensus, LLC. All Rights Reserved.800-346-3860 • www.ascensus.com

CIS II Exam Prep Workshop

Monica’s tax advisor informed her that although she was not eligible to make a Traditional IRA contribution, she is eligible to make a Roth IRA contribution . Instead of recharacterizing the contribution, Monica decided to withdraw the assets .

Complete the Form 1099-R for Monica’s removal of the excess contribution.

20 Copyright ©2019 Ascensus, LLC. All Rights Reserved.800-346-3860 • www.ascensus.com

CIS II Exam Prep Workshop

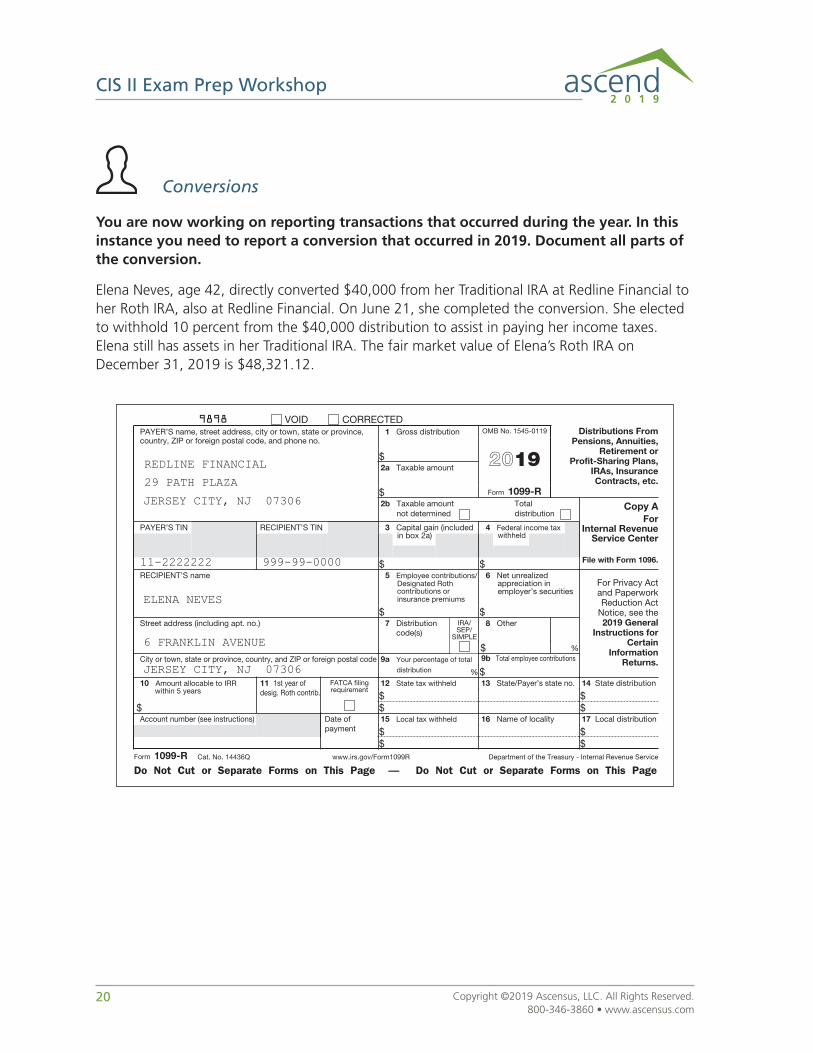

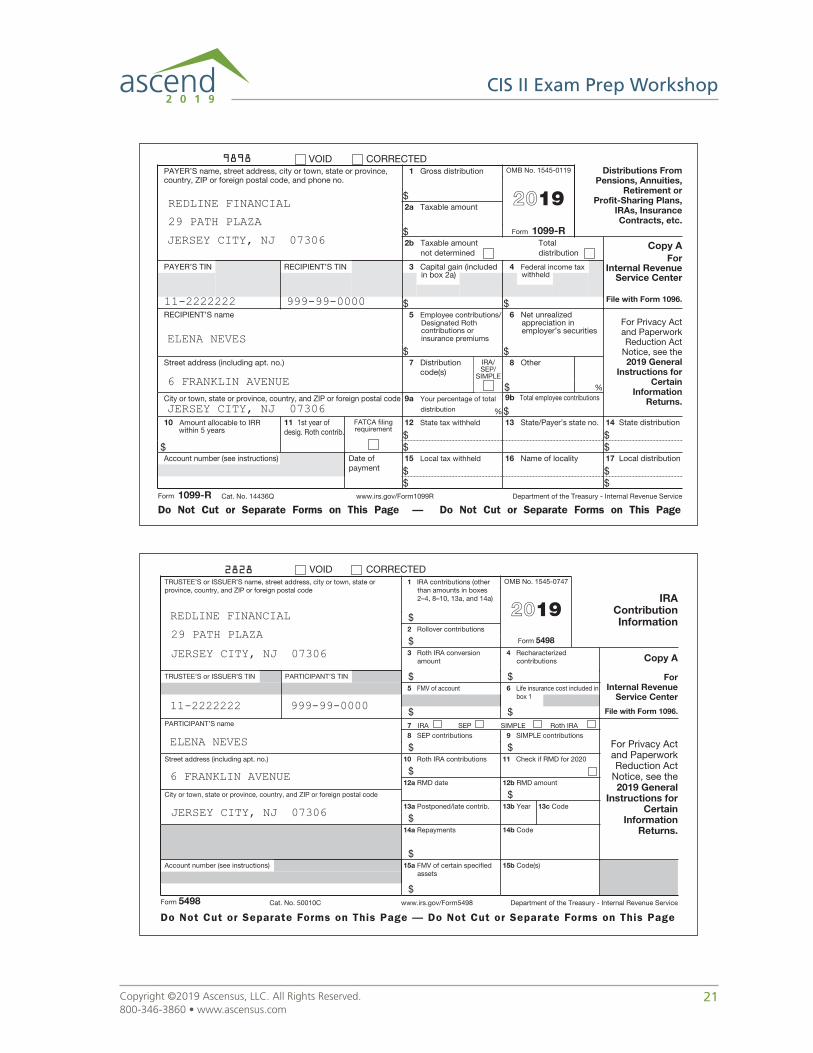

Conversions

You are now working on reporting transactions that occurred during the year. In this instance you need to report a conversion that occurred in 2019. Document all parts of the conversion.

Elena Neves, age 42, directly converted $40,000 from her Traditional IRA at Redline Financial to her Roth IRA, also at Redline Financial . On June 21, she completed the conversion . She elected to withhold 10 percent from the $40,000 distribution to assist in paying her income taxes . Elena still has assets in her Traditional IRA . The fair market value of Elena’s Roth IRA on December 31, 2019 is $48,321 .12 .

21Copyright ©2019 Ascensus, LLC. All Rights Reserved.800-346-3860 • www.ascensus.com

CIS II Exam Prep Workshop