Embed Size (px)

Citation preview

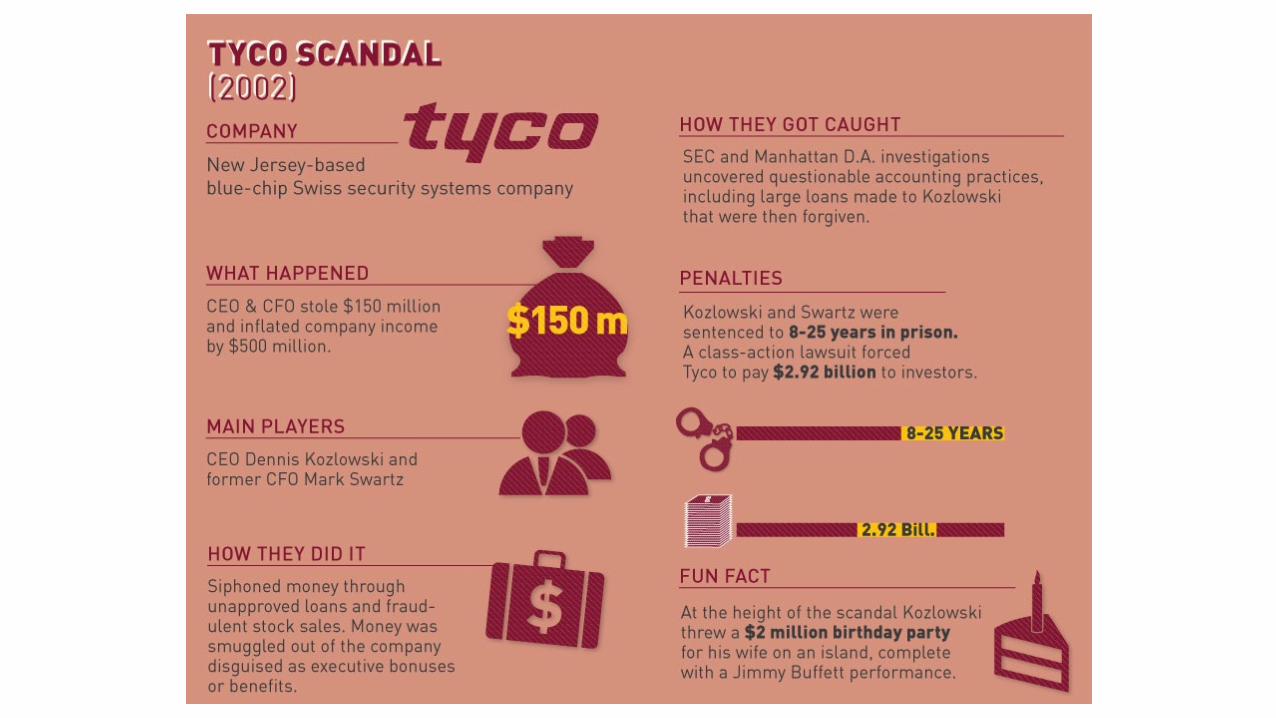

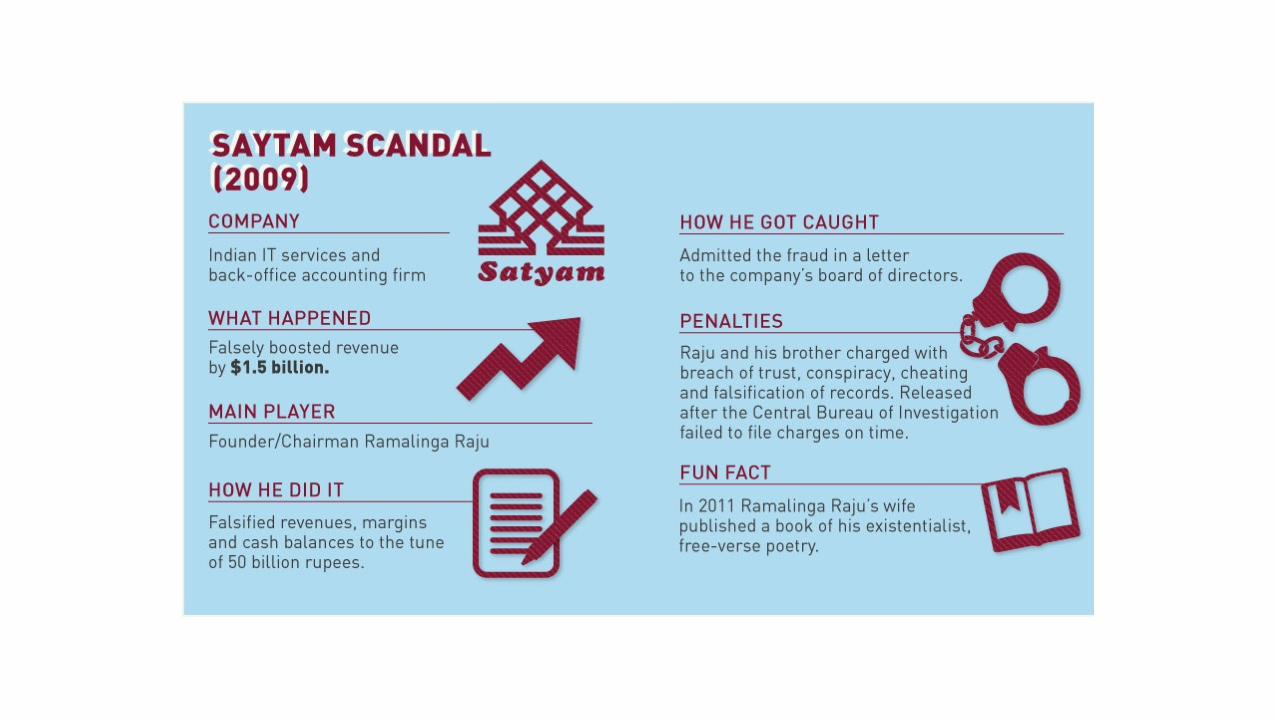

Why

FraudDetection

RisksRisks

Risks RisksRisksRisks

Risks

Risks

Risks

Risks

Risks

Risks

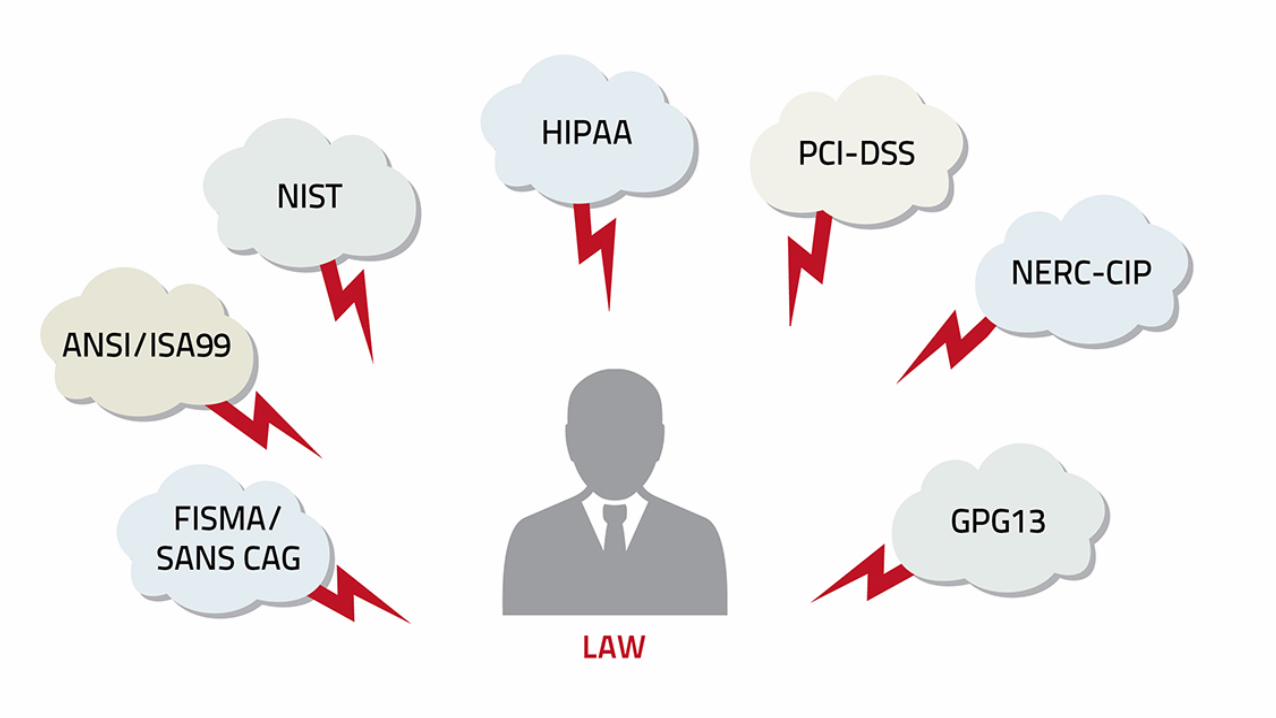

ITFrameworks&RegulatoryStandards

InternalControl:Internalcontrol,asdefinedin accounting and auditing,isaprocessforassuringachievementofanorganization'sobjectivesinoperationaleffectiveness and efficiency,reliablefinancialreporting,andcompliancewithlaws,regulationsandpolicies.Abroadconcept,internalcontrolinvolveseverythingthatcontrolsriskstoanorganization.[1]

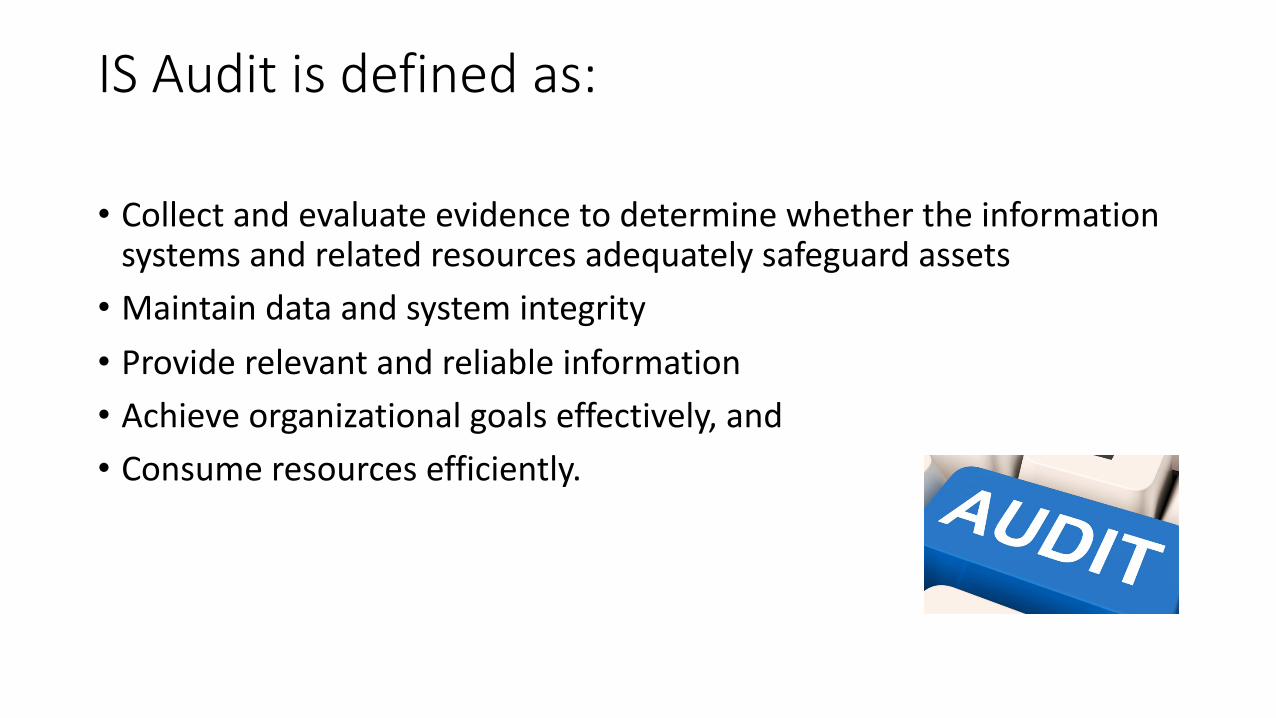

ISAuditisdefinedas:

• Collectandevaluateevidencetodeterminewhethertheinformationsystemsandrelatedresourcesadequatelysafeguardassets• Maintaindataandsystemintegrity• Providerelevantandreliableinformation• Achieveorganizationalgoalseffectively,and• Consumeresourcesefficiently.

AnISAuditisintendedto:

• Assesseswhetherinternalcontrolsprovidereasonableassurancethatbusiness,operationalandcontrolobjectiveswillbemet,and• Thatundesiredeventswillbeprevented,ordetectedandcorrected,inatimelymanner.

TheISAuditProcess

• ISauditorsareexpectedtocomplywithacodeofprofessionalethics,andtoconducttheirworkinaccordancewithspecificstandards,guidelines,andprocedures.

TheAuditCharter

• AnauditcharterestablishestheroleoftheISauditfunction.• AnISauditcanbeintegratedwithinthefinancialoroperationaudit,oritcanbepartofaninternalaudit.• Thechartershouldinclude:• Aclearstatementofmanagement'sresponsibilityandobjectivesfortheauditfunction•Management'sdelegationofauthoritytotheauditfunction• Theoverallauthority,scopeandresponsibilitiesoftheauditfunction• Thereportinglinesandrelationships

TheAuditCharter• Adefinitionoftheorganizationalindependenceoftheinternalaudit,includingaccountabilityoftheauditandprovisionforobjectiveassessmentofitsresourcerequirements• Arecognitionofthecontrolenvironmentoftheorganization(operations,resources,services,responsibilitiestoexternalentities)• Theinternalaudit'srightofaccesstoallrecords,assets,personnelandpremises,includingthoseofpartnerorganizations• Theinternalaudit'sauthoritytoobtaintheinformationandexplanationsitconsidersnecessarytofulfillitsresponsibilities• Thechartershouldbeapprovedatthehighestmanagementlevelandbytheauditcommitteeifavailable.• Oncethecharterhasbeenestablished,anychangesmustbethoroughlyjustified.

AuditObjectives

• Auditobjectivesrefertothespecificgoalsoftheaudit.Theseobjectivesoftenarecenteredonsubstantiatingthatinternalcontrolsarefunctioningtominimizebusinessrisk.Theauditobjectives,then,needtobetranslatedintospecificISauditobjectives.• Forexample,forafinancialaudit,aninternalcontrolisdesignedtoensuretransactionsarepostedcorrectlytothegeneralledger.Theauditobjectiveistodeterminewhetherthiscontrolisperformingasintended.ThecorrespondingISauditobjectivemightbetomakesurethateditingfeaturesareinplacetodetecterrorsinthetransactioncodingthatmayaffectthepostingofthetransactions.

AuditDocumentation

• Inadditiontotheauditplan,thedocumentationforanISauditincludes:• AdescriptionordiagramoftheISenvironment• Auditprograms• Minutesofmeetings• Auditevidence• Findings• Conclusionsandrecommendations• Anyreportissuedasaresultoftheauditwork• Supervisoryreviewcomments,ifany

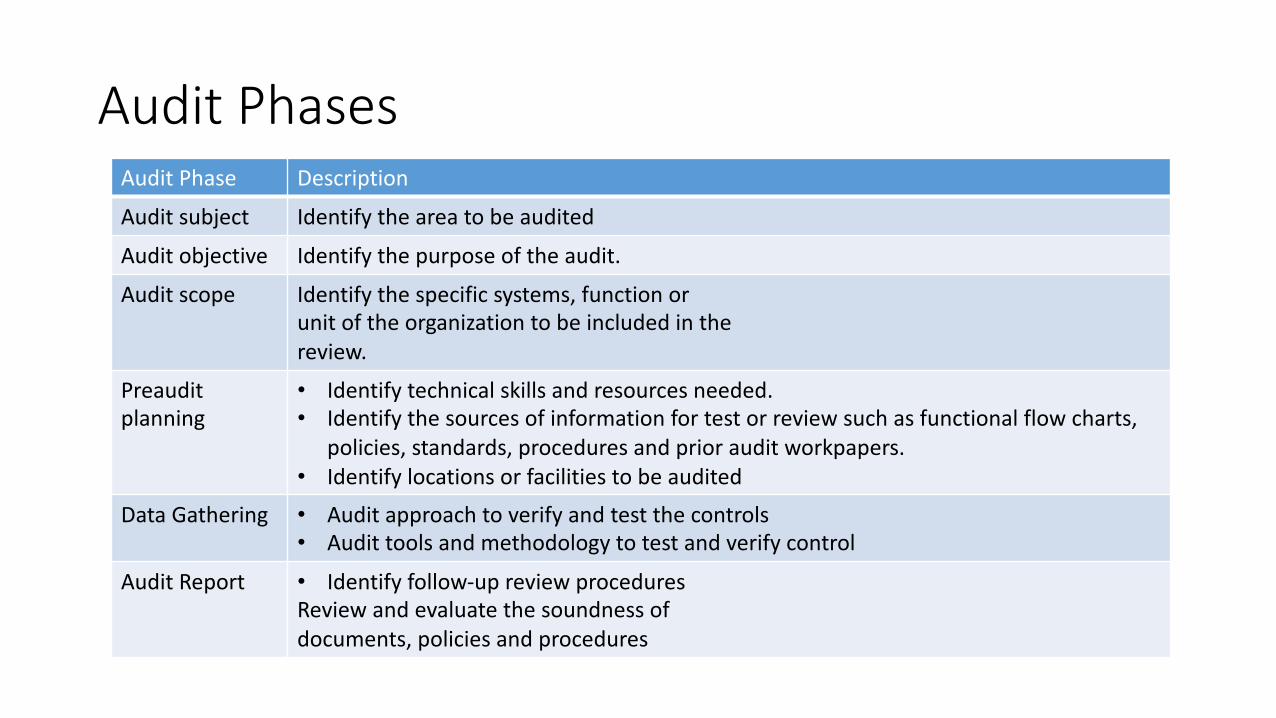

AuditPhasesAuditPhase Description

Auditsubject Identifytheareatobeaudited

Auditobjective Identifythepurposeoftheaudit.

Auditscope Identifythespecificsystems,functionorunitoftheorganizationtobeincludedinthereview.

Preauditplanning

• Identifytechnicalskillsandresourcesneeded.• Identifythesourcesofinformationfortestorreviewsuchasfunctionalflowcharts,

policies,standards,proceduresandpriorauditworkpapers.• Identifylocationsorfacilitiestobeaudited

Data Gathering • Audit approachtoverifyandtestthecontrols• Audittoolsandmethodologytotestandverifycontrol

AuditReport • Identifyfollow-upreviewproceduresReviewandevaluatethesoundnessofdocuments,policiesandprocedures

COMPLIANCEVS.SUBSTANTIVETESTING

• Compliancetestingisevidencegatheringforthepurposeoftestinganorganization'scompliancewithcontrolprocedures.• Substantivetestingisevidencegatheringtoevaluatetheintegrityofindividualtransactions,dataorotherinformation.

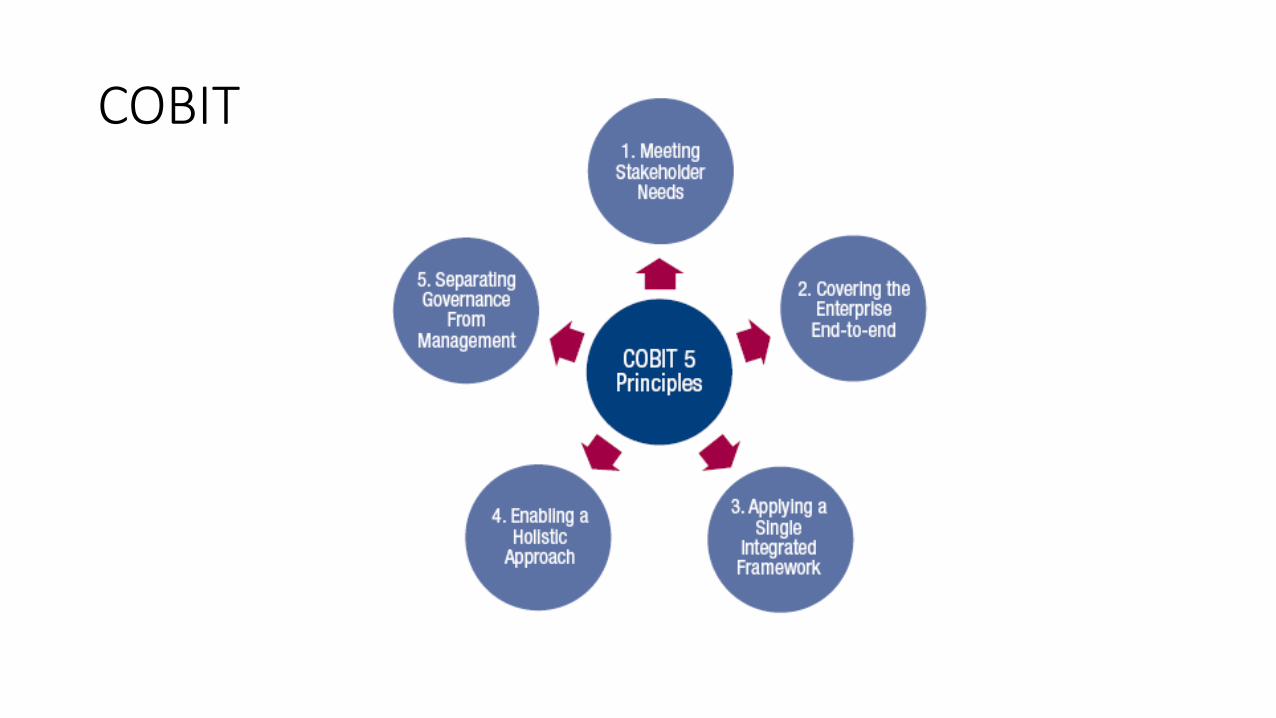

COBIT

COBIT5:GovernanceandManagementGovernance ensures that enterprise objectives are achieved by evaluating stakeholder needs, conditions and options; setting direction through prioritisation and decision making; and monitoring performance, compliance and progress against agreed-on direction and objectives (EDM).

Management plans, builds, runs and monitors activities in alignment with the direction set by the governance body to achieve the enterprise objectives (PBRM).

ITGovernanceeIQnetworksSecureVueRSAArcherIBMOpenPagesMetricStream