Embed Size (px)

Citation preview

Click to edit Master title style

The Black Sea Trade and Development

BankIMPACT OF THE CRISIS

ON REGIONAL ECONOMIES AND

ECONOMICCOOPERATION

Thessaloniki 2009

Macroeconomic Outlook

After Eight Years of real GDP Growth averaging 5.9%, the Black Sea Region economy has suffered a serious economic downturn as a result of the crisis.

2008 real GDP growth was + 4.3%. For 2009, Contraction of approximately

-6 to -6.5% is projected. It is among the hardest hit region in

the worldPainful adjustment process with

uncertain economic outlookForecasted 1% GDP growth in 2010

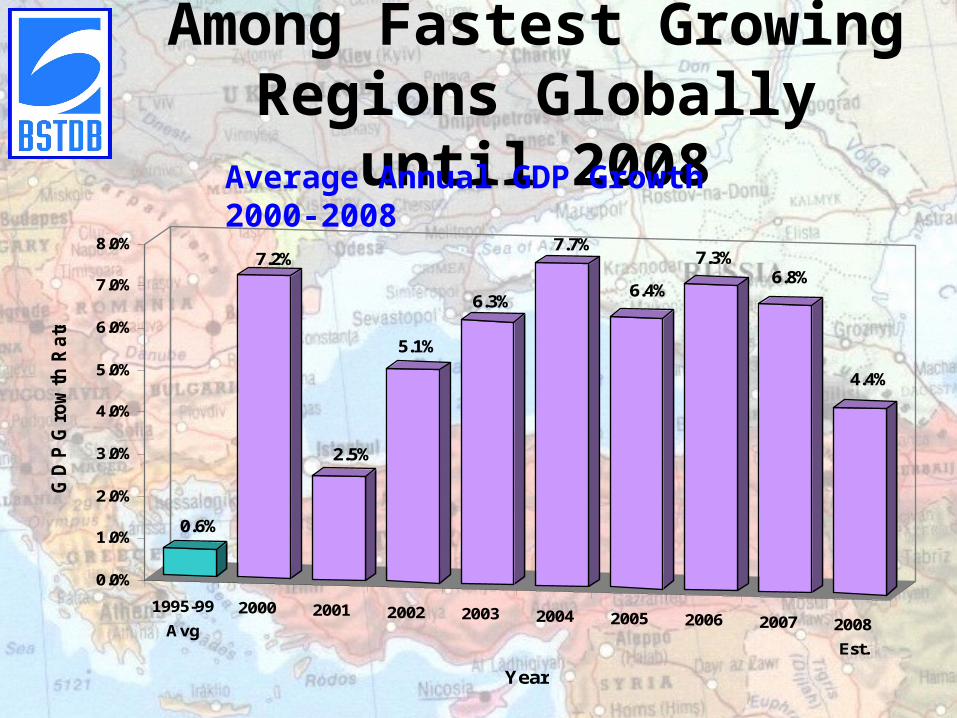

Among Fastest Growing Regions

Globally until 2008Average Annual GDP Growth 2000-2008

1995-99

Avg

2000 2001 2002 2003 2004 2005 2006 2007 2008

Est.

0.6%

7.2%

2.5%

5.1%

6.3%

7.7%

6.4%

7.3%6.8%

4.4%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

GD

P G

row

th R

ate

s

Year

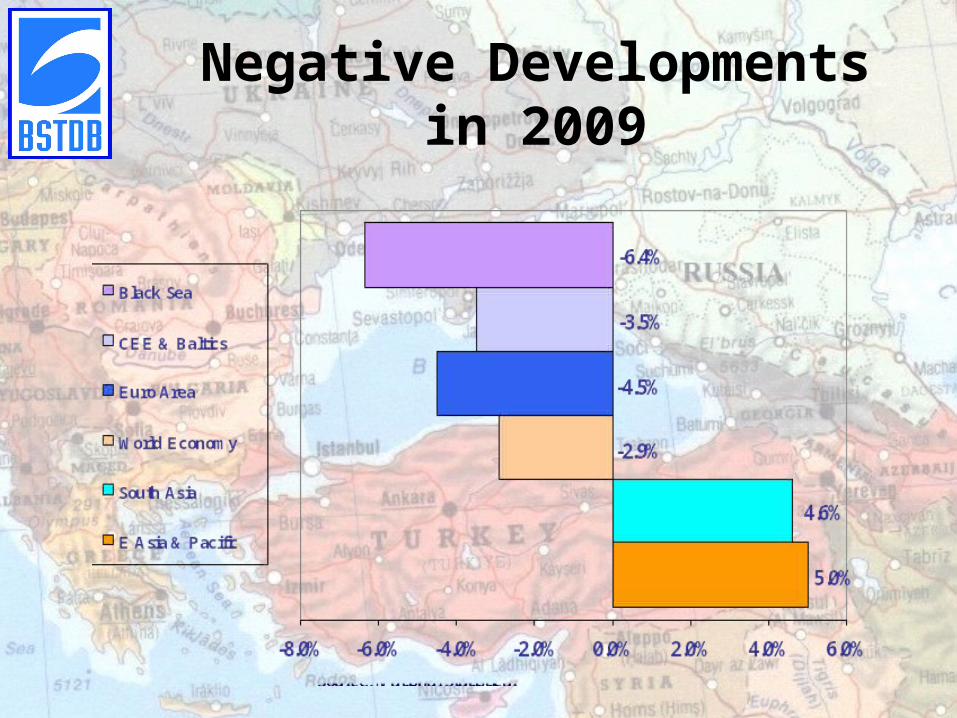

Negative Developments in 2009

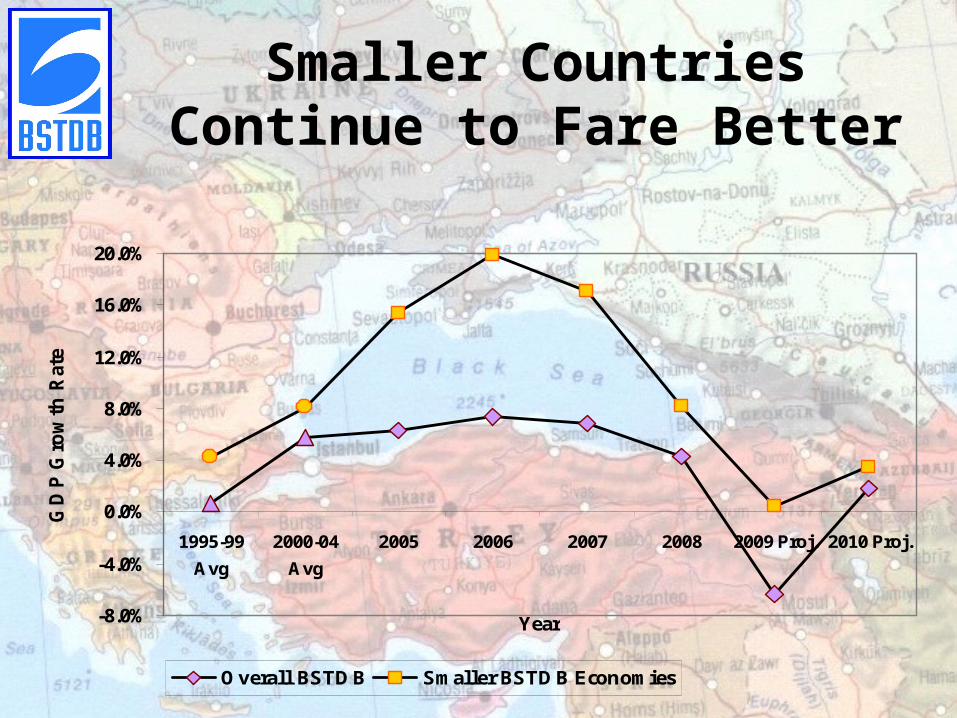

Smaller Countries Continue to Fare Better

-8.0%

-4.0%

0.0%

4.0%

8.0%

12.0%

16.0%

20.0%

1995-99

Avg

2000-04

Avg

2005 2006 2007 2008 2009 Proj. 2010 Proj.

Year

GD

P G

row

th R

ates

Overall BSTDB Smaller BSTDB Economies

Regional Trends – Before Crisis

Volume of Intra-regional Trade Increasing

Volume of Intra-regional Investment Increasing

Increasing Number and Value of Cross-regional Investment

Promotion of Regional Economic Integration & Development

Trade: Regional Integration Trend

Continued up to 2008

FDI Trend in BSEC since 2000

$0

$20

$40

$60

$80

$100

$120

$140

2000 2001 2002 2003 2004 2005 2006 2007 2008 Est.

US$

Bill

ion

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

% G

DP

Total FDI US$ Billion: Left AxisTotal FDI/ Regional GDP: Right Axis

Impact of the Crisis- Financially (1)

At onset- access to financing disappeared/ markets froze

Economies deemed dependent on external financing flows hit hardest

Governments responded promptly and substantively to support banking systems & avert collapse

While financial sectors still seeking the ‘new normal’, FIs are reasonably capitalized and not main constraint to economic growth

Impact of the Crisis- Financially(2)

Financial systems relatively small - therefore damage less than elsewhere in E. Europe.

For most part in Black Sea Region financial crisis was limited- Ukraine an exception

Lending growth has slowed, but deleveraging limited

Black Sea Region mainly suffering a nasty economic crisis

Biggest risk to Regional financial sectors from NPLs resulting from economic downturn

Economic Crisis in Black Sea

Credit to businesses and consumers disappeared, reducing liquidity & demand, slowing investment

International trade flows dropped, exports down, contraction in key W. European markets

Problems exacerbated by declines in (i) commodity prices, (ii) remittances, (iii) sundry external receipts

Reversal of fortune- poverty/ unemployment/ fiscal deficits up; current account deficits/ trade flows/ inflation down

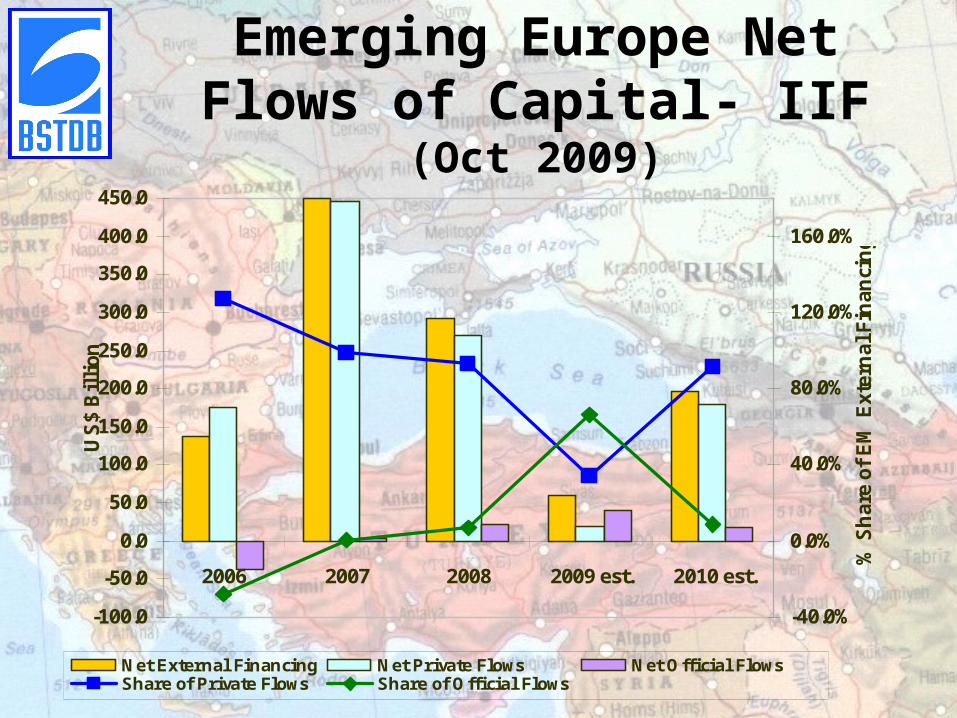

Emerging Europe Net Flows of Capital- IIF (Oct

2009)

-100.0

-50.0

0.0

50.0

100.0

150.0

200.0

250.0

300.0

350.0

400.0

450.0

2006 2007 2008 2009 est. 2010 est.

US$

Billion

-40.0%

0.0%

40.0%

80.0%

120.0%

160.0%

% S

har

e of

EM

Ext

ernal

Fin

anci

ng

Net External Financing Net Private Flows Net Official FlowsShare of Private Flows Share of Official Flows

Why was Central and Eastern Europe Highly

Vulnerable?pro-cyclical fiscal policy (deficits maintained in

a period of rapid economic growth add an unnecessary stimulus which is both overheating the economy and making it difficult for governments to counteract downturns with increased levels of public spending and/or further tax cuts),

large current account deficits private sector foreign financed domestic

demand lack of a domestic capital base and/or of

domestic champions able to compete internationally

Lessons from the Crisis

“Although the export-oriented growth model has been shaken by the crisis, many countries seem reluctant to recalibrate.” N. Roubini NYT 29/10/09

Why? Financial integration model shaken much more International trust a casualty of crisis (not fatally) E-OG offers greater security & self-reliance

The real economic decline may be aggravated by lack of credit, high interest rates and the absence of a significant fiscal stimulus

Lower foreign demand may result in declining rates of economic growth in the region

‘Silver linings’ to the crisis

Not a debt crisis. In most countries debt levels low and debt servicing still comfortable

Financial systems small - therefore damage less than elsewhere in E. Europe

Governments responded promptly and substantively to support banking systems

IMF programs in Albania, Armenia, Georgia, Moldova, Romania, Ukraine

Foreign Direct Investment down but less than feared, may register 2.5-3% of GDP for 2009

Dealing with the Economic Crisis

Things a Country Can do on Own:Fiscal & Monetary stimulus, if have FX

reserves, low debt, budgetary ‘space’ for public investment

Improve business environment- ease of creation & operation of firms, support domestic capital creation

Promote transparency in markets, and improve public & private governance

Regime(s) for debt restructuring & workouts/ bank resolution & bankruptcy

Reorient trade towards regions with high growth, where demand is going to come from: Latin America, Middle East and North Africa, South-East Asia

Dealing with the Economic Crisis

Regional Level Options:Information Exchange & Policy DialogueInstitutional Cooperation/ Coordination of

PoliciesLegal Harmonization of Rules & FrameworksBilateral Swaps/ Multilateral PoolingScope for trade & investment facilitationCross-country projects- esp. for

infrastructure (energy, transport, etc.)Externally Supported Options:

Inclusion in pan-European support program for banks

Donor & IFI Assistance

Economic Perspectives Opportunities

Economies resilient & adaptable, willing to take difficult measures to turn things around.

Worst of contraction likely over for most countries, low positive growth likely in 2010.

High Investment in Infrastructure over next 10 years

Relocation of Foreign Production Capacity to the Region likely to continue

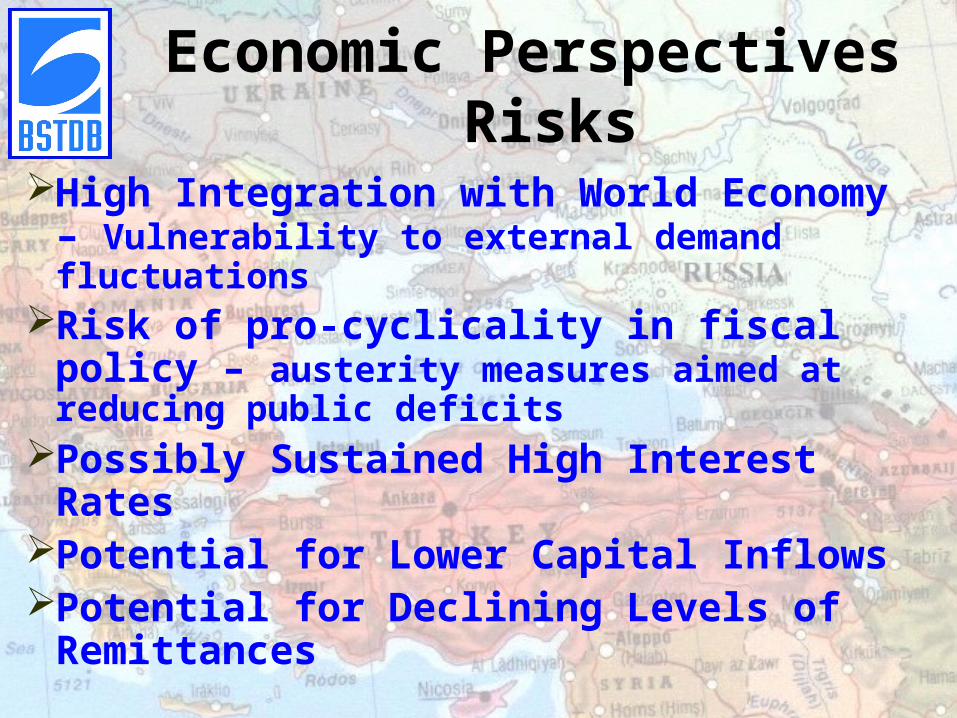

Economic Perspectives Risks

High Integration with World Economy – Vulnerability to external demand fluctuations

Risk of pro-cyclicality in fiscal policy – austerity measures aimed at reducing public deficits

Possibly Sustained High Interest Rates

Potential for Lower Capital InflowsPotential for Declining Levels of

Remittances

Key Regional Challenges for Future

Current Global Crisis- Returning to Path of High Economic Growth

Evolution of Political Economy Relations with External Actors, Especially EUAlso:Long Term Demographic Trends & Issues

they Pose for (i) Need to Adapt Structurally, (ii) Quantity & Quality of the Workforce, (iii) Pressures on Government Finances

Improving the Competitiveness & Productivity of Regional Economies

Promoting Regional Cooperation

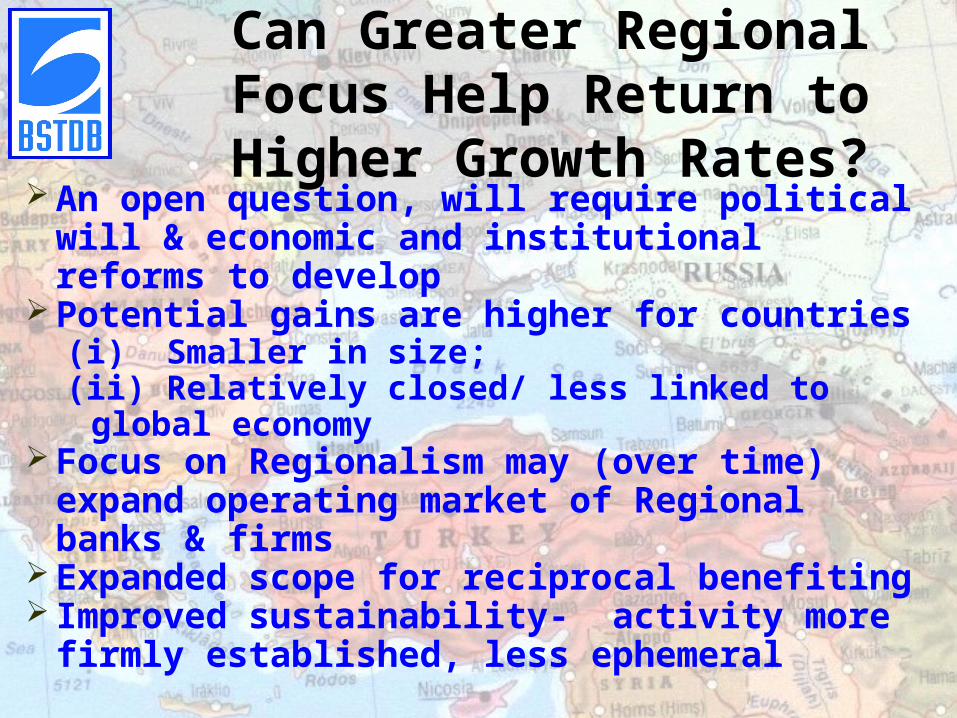

Can Greater Regional Focus Help Return to Higher Growth Rates?

An open question, will require political will & economic and institutional reforms to develop

Potential gains are higher for countries(i) Smaller in size;(ii) Relatively closed/ less linked to global

economy Focus on Regionalism may (over time)

expand operating market of Regional banks & firms

Expanded scope for reciprocal benefiting Improved sustainability- activity more

firmly established, less ephemeral

Click to edit Master title style

Thank you