Embed Size (px)

Citation preview

KONGSBERG PROPRIETARY: This document contains KONGSBERG information which is proprietary and confidential. Any disclosure, copying, distribution or use is prohibited if not otherwise explicitly agreed with KONGSBERG in writing. Any authorised reproduction in whole or in part, must include this legend. © 2013 KONGSBERG – All rights reserved.

CMD 2013 - Kongsberg Oil & Gas Technologies President & EVP Pål Helsing

Fundamental cost and efficiency challenges

in the O&G industry

07.11.2013 WORLD CLASS - through people, technology and dedication Page 2

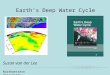

Example from the Norwegian Continental Shelf

Subsea tie-back costs Cost inflation index

Development wells per rig year Avg no of wells drilled per full rig year, all rig types

0

1

2

3

4

5

6

7

8

9

10

11

12

2002 2004 2006 2008 2010 2012

288

80

100

120

140

160

180

200

220

240

260

280

300Subsea

Production

System

Other

categories

2013 11 09 07 05 2003

Kongsberg Oil & Gas Technologies

07.11.2013 WORLD CLASS - through people, technology and dedication Page 4

Subsea Drilling

• Revenue 772* MNOK

• 748* employees

• 18 offices in 8 countries

• Subsea products, Software

and Solutions

• Drilling Software and Solutions

* YTD Q3 2013 figures

Providing market-leading products and

services

07.11.2013 WORLD CLASS - through people, technology and dedication Page 5

Software

and

services

Subsea

Divisions Main offerings

• Software for Safe and Efficient Drilling

Operations

• Flow Modeling Software

• Environmental Monitoring Solutions

• Drilling Rig Management Solutions

Share of KOGT revenues

• Concept Engineering and Solution Design

• EPC Projects

• Subsea Products

• Products and Services for Operational

Support

Software

48.7%

Subsea

51.3%

Offering complete solutions

07.11.2013 WORLD CLASS - through people, technology and dedication Page 6

• Leveraging KONGSBERG technology

base and oil & gas domain expertise

• Developing industry leading

technologies together with technology

leading Oil Companies

• Delivering technologies into

services and solutions

• Engineering close to all major hubs

• 24/7 world wide service and support

Resulting in:

• Cost effective field development and

efficient operations for our customers

• Close customer relations

• Global market channels for our

products

Robust and growing positions

in a consolidated market

Strategy

A global business system ensuring access

to key markets

07.11.2013 WORLD CLASS - through people, technology and dedication Page 7

North Sea, Gulf of Mexico, Brazil and Australia

SOURCE: KONGSBERG data

Kongsberg Oil & Gas Technologies offices

International

Norway

365

337

702

Revenue split, 2012,

MNOK

365

383

748

Employee split, 2012,

# employees

Supporting the overall ambition of the Group

07.11.2013 WORLD CLASS - through people, technology and dedication Page 8

Recent news and developments

• Revenue of MNOK 772 YTD Q3 2013

compared to 519 YTD Q3 2012 (+49%)

• EBITDA of MNOK 24 YTD Q3 2013

compared to 49 YTD Q3 2012 (-51%)

• Q3 2013 order backlog of MNOK 855,

up from 293 at year-end 2012

• Book to bill YTD 2013 of 1.55

• Advali acquisition

• Nemo acquisition

• Established in Brazil

• Strengthening customer base for key

software solutions

• Award of Statoil Polarled

Recent news and developments Current status

Supporting the overall ambition of the Group

103

120 122

183 172 162 185 183

239 277 256

Q3 Q2 Q1 Q4 Q3 Q2 Q1 Q4 Q3 Q2 Q1

Revenues, MNOK

EBITDA, MNOK

2011 2012

• Acquisition of ApplyNemo

• Backlog within Subsea increased

from 132 MNOK to 622 NOK

• Backlog within Software and

Services increase from 155mNOK

to 230 mNOK

Key EBITDA drivers last year

• Achieving critical mass in all

segments

• Optimized operation

• Commercializing products

– Increased subsea product sale

(Thor)

– Increased software product

sale (SiteCom, LedaFlow,

RiserManager and

RigManager)

Q3 Q2 Q1 Q4 Q3 Q2 Q1 Q4 Q3 Q2 Q1

2011 2012

Highlights

2013

2013

-9

10 10

38

9 5

35

-5 -2

8

18

Global offshore E&P spending - expected

growth 7% annually toward 2017

07.11.2013 WORLD CLASS - through people, technology and dedication Page 10

Drilling

4,4%

(12,7%)

Subsea

15,8%

(8,1%)

11 13 10 9 10 14 16 16 17 19 19

53 68 67 72 80

96 108 109 113 117 119 38

47 45 47

52

59

65 70 73

79 88

22

27 26 25

30

33

37 44

51

60

69

55

67 67

69

75

82

89

92

96

99

105

179

221 216

223

247

284

315

331

350

374

399

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

MMO

5,1%

(8,1%)

Prod.

Facilities

8,1%

(9,5%)

Seismic

6,0%

(5,6%)

Global offshore E&P spending

2007-2017 BUSD/year

CAGR: ’12-’17

(’07-’12)

Source: Rystad: INTSOK Annual Report 2014-2017

Solutions for efficient and reliable drilling

operations

07.11.2013 WORLD CLASS - through people, technology and dedication Page 11

Our market: “waste” within drilling spend

• The industry has so far not been able to

address the significant cost of NPT

• KONGSBERG is well positioned through

our software solutions: SiteCom, Well

Advisor, RiserManager and RigManager

program suites

• Clients include BP, Statoil, Chevron,

CNOOC, Petronas and a high number of

rig owners

• Large potential for upselling more

advanced decision support software

KONGSBERG - The Integrated Edge

17%

9%

16%

6%

7%

12%

5%

6%

10%

Shallow water(239 wellbores)

Deep-water(66 wellbores)

Sub-Salt Deep-water(38 wellbores)

28%

23%

Industry average: ~30 %

Weather problems Downhole problems2) Equipment problems3)

Non Productive Time (NPT) within drilling

Steady growth within subsea

07.11.2013 WORLD CLASS - through people, technology and dedication Page 12

Steady growth within the Subsea market

• Increasing number of subsea wells and

pipeline length

• Development of smaller and remote fields

calls for new fit for purpose solutions and

contracting models

• KONGSBERG has enabling technologies

to reduce development cost

• KONGSBERG has got the know-how to

integrate with 3rd party contractors

• KONGSBERG is providing

The Integrated Edge

KONGSBERG - The Integrated Edge

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Km

Year installed

Global offshore pipeline installation forecast

S&B pipelines

H&D infield lines

H&D trunklines

0

100

200

300

400

500

600

700

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

No

. of

tre

es

Installation year

Subsea tree outlook per region

North America

Med/Middle East

Europe

Latin America

Asia-Pacific

Africa

Visible demand

Source: IHS Global Limited

Continuing to broaden product and service

range through innovation

07.11.2013 WORLD CLASS - through people, technology and dedication Page 13

Recent innovations Impact

Subsea Storage Unit

• Solution for storage of utilities or

produced liquids under water

Subsea monitoring solutions

• Equipment integrity monitoring

solutions

• Flow metering solutions

• Pipeline pigging solutions

Well Advisor

• Drilling decision support consoles for

efficient and reliable drilling operations

• Reduced

CAPEX and

OPEX,

increased field

design flexibility

• Reduced

CAPEX and

OPEX

• Reduced NPT,

increase safety

Continuously improvements through tailored

improvement programs

07.11.2013 WORLD CLASS - through people, technology and dedication Page 14

Recent innovations Impact

• Refine our project execution models for

EPC projects

• Software development

• Sourcing and manufacturing strategy

• Enhancing our India engineering

operation for software development,

engineering services and global customer

support

• Continued high focus on Opex cost

throughout the whole organization

• Reduced

project cost

• Reduced

development/

project cost

• Reduced

project cost

The strategy is built on securing existing

market positions and broadening into new

markets

07.11.2013 WORLD CLASS - through people, technology and dedication Page 15

Where we want to go

Where we are today Drilling

• Consolidating our leading position

• Adding value to our installed base

through new add-on products

• Strengthening our position within

solutions for Drill Rig Management

Drilling

• Strong niche product

• Robust global customer base

• Ongoing product development in

partnership with major IOC’s

Subsea

• Increase our international footprint

• Adding products to our offering

• Increased footprint towards fields in

operation (Brown fields)

Subsea

• Strong position engineering in

Norway and increasing international

footprint

• Well positioned for EPC projects in

Norway

• Ongoing product development in

partnership with major IOC’s

kongsberg.com