Embed Size (px)

Citation preview

COGICCOGICChurch AdministrationChurch Administration

Module 7Module 7

Ministry & Non-Profit LawMinistry & Non-Profit Law

Part 2Part 2

General Legal General Legal ConsiderationsConsiderations

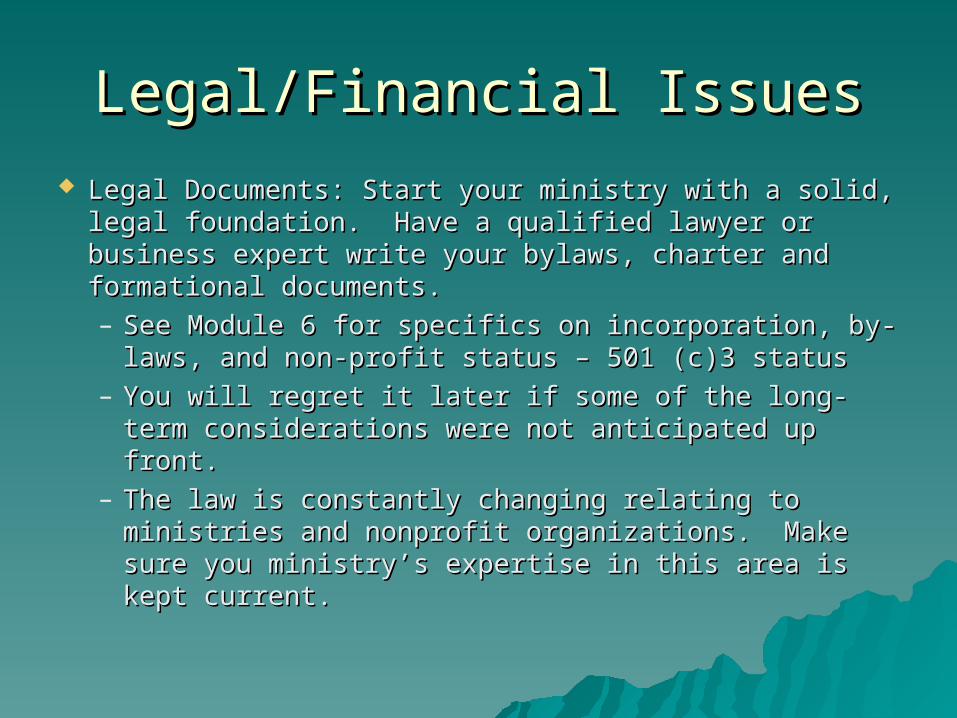

Legal/Financial IssuesLegal/Financial Issues

Legal Documents: Start your ministry with a solid, Legal Documents: Start your ministry with a solid, legal foundation. Have a qualified lawyer or legal foundation. Have a qualified lawyer or business expert write your bylaws, charter and business expert write your bylaws, charter and formational documents.formational documents.– See Module 6 for specifics on incorporation, by-See Module 6 for specifics on incorporation, by-

laws, and non-profit status – 501 (c)3 statuslaws, and non-profit status – 501 (c)3 status– You will regret it later if some of the long-term You will regret it later if some of the long-term

considerations were not anticipated up front.considerations were not anticipated up front.– The law is constantly changing relating to The law is constantly changing relating to

ministries and nonprofit organizations. Make ministries and nonprofit organizations. Make sure you ministry’s expertise in this area is sure you ministry’s expertise in this area is kept current.kept current.

Legal/Financial IssuesLegal/Financial Issues

IRS Requirements: The same principle of excellence IRS Requirements: The same principle of excellence applies to your financial foundation. You need a applies to your financial foundation. You need a specialist to help you prepare for the future. Have a specialist to help you prepare for the future. Have a nonprofit expert help you with the IRS during startup nonprofit expert help you with the IRS during startup and growth. Do not try to tackle this area with people and growth. Do not try to tackle this area with people who are not qualified. Build a strong foundation of who are not qualified. Build a strong foundation of excellence for the future.excellence for the future.– Tax exempt application (1023 A)Tax exempt application (1023 A)– Initial quarterly tax returns (941) and annual Initial quarterly tax returns (941) and annual

reporting (990)reporting (990)– Special Clergy Issues: housing allowances, Special Clergy Issues: housing allowances,

accountable reimbursement policy, exemption from accountable reimbursement policy, exemption from Social Security, salary package, etc.Social Security, salary package, etc.

Legal/Financial IssuesLegal/Financial Issues Financial Accountability and Excellence: Financial Accountability and Excellence:

Maintain the financial area with excellence Maintain the financial area with excellence continually. Do the right things to get positive continually. Do the right things to get positive results.results.– Become a member of the ECFA (financial Become a member of the ECFA (financial

accountability group) as soon as you are able.accountability group) as soon as you are able.– Get a professional to be your auditor.Get a professional to be your auditor.– Maintain high standards for honest and diligence in Maintain high standards for honest and diligence in

all financial reporting.all financial reporting. Have a weekly Bookkeeper.Have a weekly Bookkeeper. Treat designated funds very strictly. Do not allow any Treat designated funds very strictly. Do not allow any

misuses of these gifts.misuses of these gifts. Send quarterly summary statements of donor giving.Send quarterly summary statements of donor giving.

Specific Financial Specific Financial ConsiderationsConsiderations

Corporate Checking AccountCorporate Checking Account

The by-laws must contain provision that The by-laws must contain provision that empowers the corporation to have and empowers the corporation to have and hold a corporate business checking hold a corporate business checking accountaccount

Have as FEW accounts as possible (one Have as FEW accounts as possible (one by preference, but not more than three). by preference, but not more than three). This ensures fewer ways “in and out” of This ensures fewer ways “in and out” of the bank and is easier to track and auditthe bank and is easier to track and audit

Corporate Checking AccountCorporate Checking Account Have as few signators as possible on the Have as few signators as possible on the

checking accounts. checking accounts. – They should not be relatedThey should not be related– They should have at least one officer, They should have at least one officer,

preferably the treasurerpreferably the treasurer– They should NOT be the pastor if possibleThey should NOT be the pastor if possible– There should always be at least two There should always be at least two

signators, not stamped, but signedsignators, not stamped, but signed– Signators should be rotatedSignators should be rotated– Secure the corporate seal!Secure the corporate seal!

Employee CompensationEmployee Compensation

Non-profit corporations are allowed to Non-profit corporations are allowed to have employees – and pay them fairly!have employees – and pay them fairly!

Payment for a job or service performed is Payment for a job or service performed is NOT inurement to gain!NOT inurement to gain!

All compensation plans must follow by-All compensation plans must follow by-laws regulations as well as state and laws regulations as well as state and federal guidelines and requirementsfederal guidelines and requirements

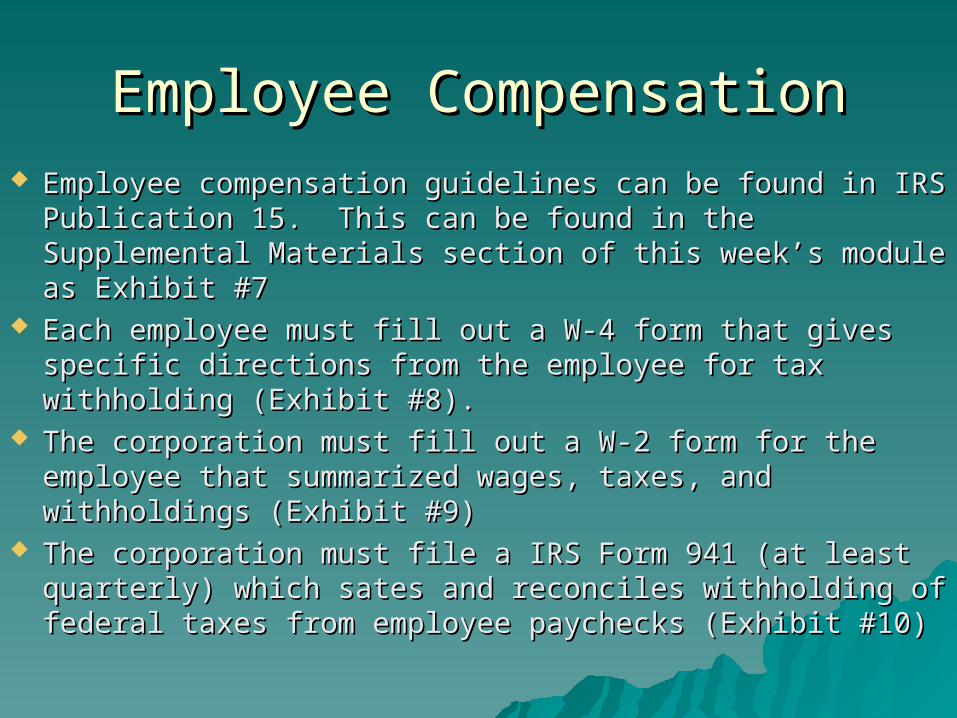

Employee CompensationEmployee Compensation Employee compensation guidelines can be found in IRS Employee compensation guidelines can be found in IRS

Publication 15. This can be found in the Supplemental Publication 15. This can be found in the Supplemental Materials section of this week’s module as Exhibit #7Materials section of this week’s module as Exhibit #7

Each employee must fill out a W-4 form that gives Each employee must fill out a W-4 form that gives specific directions from the employee for tax specific directions from the employee for tax withholding (Exhibit #8). withholding (Exhibit #8).

The corporation must fill out a W-2 form for the The corporation must fill out a W-2 form for the employee that summarized wages, taxes, and employee that summarized wages, taxes, and withholdings (Exhibit #9)withholdings (Exhibit #9)

The corporation must file a IRS Form 941 (at least The corporation must file a IRS Form 941 (at least quarterly) which sates and reconciles withholding of quarterly) which sates and reconciles withholding of federal taxes from employee paychecks (Exhibit #10)federal taxes from employee paychecks (Exhibit #10)

Specific Compensation IssuesSpecific Compensation Issues Specific compensation issues have their authority and Specific compensation issues have their authority and

origination with the Board of Trustees and are made origination with the Board of Trustees and are made official (and legal) by a vote of the Board per by-laws official (and legal) by a vote of the Board per by-laws and as recorded in the Board minutes – this is LAW!and as recorded in the Board minutes – this is LAW!

Specific Board resolutions should be made as close to Specific Board resolutions should be made as close to the first business meeting as possible near the time of the first business meeting as possible near the time of incorporation.incorporation.

It is usual to take care of incorporation, non-profit It is usual to take care of incorporation, non-profit items, and salary/compensation issues right in the first items, and salary/compensation issues right in the first minutes, using technical and legally correct format and minutes, using technical and legally correct format and descriptions. See a sample of the minutes from a first descriptions. See a sample of the minutes from a first Board meeting in the Supplemental Materials section of Board meeting in the Supplemental Materials section of this module, as Exhibit #11this module, as Exhibit #11

Specific Compensation IssuesSpecific Compensation Issues These original minutes of the Board may be used to These original minutes of the Board may be used to

define the following specific compensation issues (or define the following specific compensation issues (or this may be done later by revision of the by-laws and this may be done later by revision of the by-laws and addition to the minutes per vote of the Board:)addition to the minutes per vote of the Board:)– Definition of officers of the corporation by voteDefinition of officers of the corporation by vote– Reiteration of the purpose of the corporationReiteration of the purpose of the corporation– Definition of ministerial (parsonage) housing allowanceDefinition of ministerial (parsonage) housing allowance– Definition of an Accountable Reimbursement PolicyDefinition of an Accountable Reimbursement Policy– Salary Package considerations (salary, specific adoption of Salary Package considerations (salary, specific adoption of

housing request, company vehicle and use, retirement, access housing request, company vehicle and use, retirement, access and limits to accountable reimbursement benefits, cafeteria and limits to accountable reimbursement benefits, cafeteria plan for benefits)plan for benefits)

This is where solid planning saves time and money!This is where solid planning saves time and money!

Ministerial CompensationMinisterial Compensation There are multiple ways provided by federal law that can add There are multiple ways provided by federal law that can add

value to a minister’s compensation package while assuring the value to a minister’s compensation package while assuring the best use of resources. THE BEST WAY TO COMPENSATE A best use of resources. THE BEST WAY TO COMPENSATE A MINISTER IS NOT BY SALARY ALONE! Considerations include:MINISTER IS NOT BY SALARY ALONE! Considerations include:– Base salary (taxable income)Base salary (taxable income)– Housing (parsonage) allowanceHousing (parsonage) allowance– Accountable Reimbursement PolicyAccountable Reimbursement Policy– Social Security Bonus (SECA Bonus)Social Security Bonus (SECA Bonus)– Pension & retirementPension & retirement– Health and disabilityHealth and disability– Medical and Dependant Cafeteria PlansMedical and Dependant Cafeteria Plans– Life InsuranceLife Insurance– Sabbatical, Vacation, Holiday provisionsSabbatical, Vacation, Holiday provisions– Scholarship and Educational BenefitsScholarship and Educational Benefits

Base Salary for MinistersBase Salary for Ministers Base salary is an amount paid in compensation apart from special Base salary is an amount paid in compensation apart from special

considerations. It is the most used method of compensation, but considerations. It is the most used method of compensation, but the least creative and also causes the highest tax consequences the least creative and also causes the highest tax consequences for both minister and ministry.for both minister and ministry.

A minister is considered “self employed for the purposes of social A minister is considered “self employed for the purposes of social security” by the federal government – that means that the minister security” by the federal government – that means that the minister does not pay FICA social security taxes (Federal Insurance does not pay FICA social security taxes (Federal Insurance Contribution Act – 6.2% Social security tax up to $97,500 income Contribution Act – 6.2% Social security tax up to $97,500 income in 2007 & 1.45% Medicare Tax with no income limit in 2007 – in 2007 & 1.45% Medicare Tax with no income limit in 2007 – 7.35% total; the employee pays this by deduction, and the 7.35% total; the employee pays this by deduction, and the employee contributes the same – total is 15.3%)employee contributes the same – total is 15.3%)

The minister pays SECA taxes on salary (Self-Employed The minister pays SECA taxes on salary (Self-Employed Contribution Act) – the entire 15.3%!, making the salary portion a Contribution Act) – the entire 15.3%!, making the salary portion a big hit in federal taxes (wage taxes, SECA taxes, state & local big hit in federal taxes (wage taxes, SECA taxes, state & local taxes)taxes)

Note that the minister should be given a “SECA Bonus” – more Note that the minister should be given a “SECA Bonus” – more later!later!

Base Salary for MinistersBase Salary for Ministers Ministerial compensation is traditionally low, but there are good Ministerial compensation is traditionally low, but there are good

reasons NOT to make the minister and his or her family “suffer for reasons NOT to make the minister and his or her family “suffer for Jesus:”Jesus:”– Creates perception to the world that God is cheap!Creates perception to the world that God is cheap!– Affects the attitude of the minister and his or her familyAffects the attitude of the minister and his or her family– May make a second job necessary for the ministerMay make a second job necessary for the minister– May make it necessary for the spouse to work and leave familyMay make it necessary for the spouse to work and leave family– Does not fulfill “workman worthy of wages” (I Tim 5:18)Does not fulfill “workman worthy of wages” (I Tim 5:18)– ““Muzzles the ox – not benefit or incentive! (I Tim 5:18)Muzzles the ox – not benefit or incentive! (I Tim 5:18)– Does not honor the “prophet” or God’s point personDoes not honor the “prophet” or God’s point person– Poor witness to outsidersPoor witness to outsiders– Does not model the character or heart of God (provider)Does not model the character or heart of God (provider)– Can be a power play or source of control!Can be a power play or source of control!

Ministers Housing AllowanceMinisters Housing Allowance When preparing a housing allowance request, ALL items to buy, maintain, When preparing a housing allowance request, ALL items to buy, maintain,

or keep a house should be included:or keep a house should be included:– Cost of buying a house (down payment, closing costs)Cost of buying a house (down payment, closing costs)– Rent or Mortgage (Principle and Interest)Rent or Mortgage (Principle and Interest)– Real estate taxesReal estate taxes– InsurancesInsurances– Improvements (remodeling, roof, room, garage, patio, fences, Improvements (remodeling, roof, room, garage, patio, fences,

appliances, repairs)appliances, repairs)– Furnishings (furniture, dishwasher, washer, dryer, freezer, refrigerator, Furnishings (furniture, dishwasher, washer, dryer, freezer, refrigerator,

TV, VCR, Stereo, piano, computer, beds, small kitchen items, TV, VCR, Stereo, piano, computer, beds, small kitchen items, cookware, dishes, sewing machines, garage door openers, lawnmower, cookware, dishes, sewing machines, garage door openers, lawnmower, hedge trimmers, etc.)hedge trimmers, etc.)

– Decoration Items (drapes, rugs, throws, pictures, knick-knacks, Decoration Items (drapes, rugs, throws, pictures, knick-knacks, paintings, wallpaper, bedding, sheets, towels, etc.)paintings, wallpaper, bedding, sheets, towels, etc.)

– Utilities (heat, water, sewage, garbage, Cable, phone, Internet, etc)Utilities (heat, water, sewage, garbage, Cable, phone, Internet, etc)

Ministers Housing AllowanceMinisters Housing Allowance A housing request must be submitted to the Board once per year A housing request must be submitted to the Board once per year

PRIOR to it being activated as part of compensation. See an PRIOR to it being activated as part of compensation. See an example in Supplemental Materials as Exhibit #13example in Supplemental Materials as Exhibit #13

Another huge advantage is that the mortgage taxes and interest Another huge advantage is that the mortgage taxes and interest ARE STILL deductible on Schedule A of the minister’s 1040 tax ARE STILL deductible on Schedule A of the minister’s 1040 tax filing, making this a “double dip” tax shelter that often adds filing, making this a “double dip” tax shelter that often adds substantial savings!substantial savings!

Declare as much as possible in your housing request to the Board – Declare as much as possible in your housing request to the Board – overestimate or add 10% to the final figure you justify. What you overestimate or add 10% to the final figure you justify. What you don’t use in a year can be declared on your 1040 tax return and don’t use in a year can be declared on your 1040 tax return and taxes paid – you cannot go back and increase retroactively if you taxes paid – you cannot go back and increase retroactively if you spend more on housing!spend more on housing!

You can resubmit a new request at any time, BUT you cannot You can resubmit a new request at any time, BUT you cannot make it retroactive – it is in effect from the day the Board approvesmake it retroactive – it is in effect from the day the Board approves

SAVE EVERY RECEIPT (seven year rule!)SAVE EVERY RECEIPT (seven year rule!)

Accountable ReimbursementAccountable Reimbursement The Accountable Reimbursement Policy (ARP) is a PRE-The Accountable Reimbursement Policy (ARP) is a PRE-

TAX method to add value to a minister’s (or other TAX method to add value to a minister’s (or other employee’s) compensation plan. It sets aside pre-employee’s) compensation plan. It sets aside pre-determined sums of money for specific expenses that determined sums of money for specific expenses that the minister may encounter through the year, that are the minister may encounter through the year, that are accessed by submission of receipts or advance accessed by submission of receipts or advance requests. The accountable amount is them reimbursed requests. The accountable amount is them reimbursed to the employee WITH NO TAX CONSEQUENCESto the employee WITH NO TAX CONSEQUENCES

The policy must be set up and defined, in the minutes The policy must be set up and defined, in the minutes of a Board meeting, with specific categories, limits of of a Board meeting, with specific categories, limits of reimbursement, procedures to reimburse, and reimbursement, procedures to reimburse, and Supplemental Materials section of the module for an Supplemental Materials section of the module for an example of an ARP, as Exhibit #12example of an ARP, as Exhibit #12

Accountable ReimbursementAccountable Reimbursement Categories to consider for Accountable Reimbursement Categories to consider for Accountable Reimbursement

include:include:– Auto Expenses (Mileage, etc. for business purposes)Auto Expenses (Mileage, etc. for business purposes)– Education (tuition and books/fees)Education (tuition and books/fees)– Travel (allowance for business purposes)Travel (allowance for business purposes)– Entertainment (meals, time out with guests, etc.)Entertainment (meals, time out with guests, etc.)– Miscellaneous (business expenses)Miscellaneous (business expenses)

The ARP is superior to merely deducting business The ARP is superior to merely deducting business expenses on Schedule A of the 1040 tax return – it is expenses on Schedule A of the 1040 tax return – it is pretax, so not subject not any federal, state, or local pretax, so not subject not any federal, state, or local taxes!taxes!

SECA BonusSECA Bonus Since a minister is considered “self-employed for the purposes of Since a minister is considered “self-employed for the purposes of

social security,” regardless of whether he or she is self-employed social security,” regardless of whether he or she is self-employed or employed b y the church, he or she must pay SECA rather than or employed b y the church, he or she must pay SECA rather than FICA social security and medical taxesFICA social security and medical taxes

With FICA, the employee pays half of the 15.3% taxes (7.65%) and With FICA, the employee pays half of the 15.3% taxes (7.65%) and the employer pays the other half (7.65%). When the minister pays the employer pays the other half (7.65%). When the minister pays SECA, he or she pays the whole 15.3% by themselves.SECA, he or she pays the whole 15.3% by themselves.

The ministry customarily provides a partial offset for this loss, by The ministry customarily provides a partial offset for this loss, by paying the minister a SECA Bonus of 7.65%, equivalent to what paying the minister a SECA Bonus of 7.65%, equivalent to what they would have paid in FICA taxes anyway.they would have paid in FICA taxes anyway.

The SECA bonus is taxable income for the minister but goes a long The SECA bonus is taxable income for the minister but goes a long way toward making up the difference in loss between FICA way toward making up the difference in loss between FICA employer contribution and self-employment SECAemployer contribution and self-employment SECA

The minister usually “withholds” SECA as extra federal tax The minister usually “withholds” SECA as extra federal tax withholding requested on the W-4 equivalent to the annual withholding requested on the W-4 equivalent to the annual projected SECA taxes (15.3%) divided by the pay period projected SECA taxes (15.3%) divided by the pay period

Pension and RetirementPension and Retirement A wonderful pre-tax benefit is savings and corporate A wonderful pre-tax benefit is savings and corporate

contribution to a retirement or pension accountcontribution to a retirement or pension account There are a series of IRS regulations in sections 403 (b) There are a series of IRS regulations in sections 403 (b)

and 408 (k) that describe the kinds of retirement and and 408 (k) that describe the kinds of retirement and pension funds set up by non-profits, that are usually pension funds set up by non-profits, that are usually more flexible and less expensive than for-profit more flexible and less expensive than for-profit regulations (section 401 (a)regulations (section 401 (a)

Consult a tax professional to construct the pre-tax plan Consult a tax professional to construct the pre-tax plan that is right for your organization and its sizethat is right for your organization and its size

Health and DisabilityHealth and Disability Another pretax benefit is a solid Healthcare plan with Another pretax benefit is a solid Healthcare plan with

excellent medical, dental, and vision benefitsexcellent medical, dental, and vision benefits– Check with small business associations to get group ratesCheck with small business associations to get group rates– Consider self-funding vision benefitsConsider self-funding vision benefits– Offset deductibles with “Cafeteria Plans” - more laterOffset deductibles with “Cafeteria Plans” - more later

Consider self-funding a short and long term disability Consider self-funding a short and long term disability plan for key employees:plan for key employees:– Short term absence due to accident or illness might be covered Short term absence due to accident or illness might be covered

after the first two weeks absence at 75% of salary for 12 weeksafter the first two weeks absence at 75% of salary for 12 weeks– Long term absence due to accident or illness might be covered Long term absence due to accident or illness might be covered

after short term expires at 50% for up to 28 more weeksafter short term expires at 50% for up to 28 more weeks– These benefits can be self funded by the corporation or through These benefits can be self funded by the corporation or through

an insurance planan insurance plan– Define the plans in Board minutes by resolutionDefine the plans in Board minutes by resolution

Cafeteria PlansCafeteria Plans An excellent way to allow for pre-tax benefits for An excellent way to allow for pre-tax benefits for

specific medical or dependent care purposes is a specific medical or dependent care purposes is a “cafeteria plan” that allows for selection of specific “cafeteria plan” that allows for selection of specific benefits of value to the employeebenefits of value to the employee

In this plan, pre-tax money is set aside by employee In this plan, pre-tax money is set aside by employee contribution to be applied for medical or dependent contribution to be applied for medical or dependent care purposes, and then can be accessed by receipt care purposes, and then can be accessed by receipt and accountable reimbursementand accountable reimbursement

This saves all federal, state, and local taxes on This saves all federal, state, and local taxes on anticipated expenses related to medical and dependent anticipated expenses related to medical and dependent carecare

Consult a tax professional for specifics on how to set up Consult a tax professional for specifics on how to set up this kind of valuable planthis kind of valuable plan

Life InsuranceLife Insurance Life insurance was actually a Christian idea at first, to enable a Life insurance was actually a Christian idea at first, to enable a

community of people to cover the loss of one family or individual.community of people to cover the loss of one family or individual. Group Life can be provided for very little cost up to $50,000 with Group Life can be provided for very little cost up to $50,000 with

no tax liability to the employeeno tax liability to the employee Supplemental Life policies can be added by company funded or Supplemental Life policies can be added by company funded or

employee funded methods – any employee provided insurance employee funded methods – any employee provided insurance over $50,000 have premium tax consequences for the employeeover $50,000 have premium tax consequences for the employee

““Key man” insurance, usually in $1 million increments is often Key man” insurance, usually in $1 million increments is often gotten for the senior leader, in case of sudden loss, to provide a gotten for the senior leader, in case of sudden loss, to provide a buffer for the ministrybuffer for the ministry

Prudent planning says that I should multiply my annual salary by Prudent planning says that I should multiply my annual salary by 10 and purchase that much simple life insurance face value on a 10 and purchase that much simple life insurance face value on a policy. That allows the survivors to invest the lump sum and live policy. That allows the survivors to invest the lump sum and live off the interest, without touching the principle, at roughly the same off the interest, without touching the principle, at roughly the same economic level as before their losseconomic level as before their loss

Vacation , Holiday, & SabbaticalVacation , Holiday, & Sabbatical Rest in ministry is not an option, but rather commanded Rest in ministry is not an option, but rather commanded

for all Christiansfor all Christians Ministers are notorious for long hours, seven-day Ministers are notorious for long hours, seven-day

weeks, with little or no rest, followed by burn-outweeks, with little or no rest, followed by burn-out Vacation time off should be defined and fully funded – 3 Vacation time off should be defined and fully funded – 3

– 4 weeks per year (may reward time served) is usual– 4 weeks per year (may reward time served) is usual Defined vacation and holidays should be a part of a Defined vacation and holidays should be a part of a

Board resolution and minutes of a meetingBoard resolution and minutes of a meeting The senior ministers should be given sabbaticals or The senior ministers should be given sabbaticals or

regular breaks (i.e. 1 month – summers) to recharge regular breaks (i.e. 1 month – summers) to recharge and retool – INVESTMENT IN HEALTH – Freshness!and retool – INVESTMENT IN HEALTH – Freshness!

Corporate Tax Filing Corporate Tax Filing RequirementsRequirements

Non-Profit Tax FilingsNon-Profit Tax Filings There are two key tax filing requirements for non-profit There are two key tax filing requirements for non-profit

corporations – the 941 quarterly tax withholding corporations – the 941 quarterly tax withholding reconciliation (already mentioned) and the yearly reconciliation (already mentioned) and the yearly CORPORATE TAX RETURN (990 or 990EZ).CORPORATE TAX RETURN (990 or 990EZ).

The corporation must file a yearly tax return, because it The corporation must file a yearly tax return, because it is seen as a “legal person” in the eyes of the law as a is seen as a “legal person” in the eyes of the law as a corporation.corporation.

The filing date is May 15 of each year, or the Monday The filing date is May 15 of each year, or the Monday after a weekend on which the 15after a weekend on which the 15thth falls. falls.

The form you use to file (990 or 990EZ) depends on the The form you use to file (990 or 990EZ) depends on the level of income and assets for your ministry. An level of income and assets for your ministry. An example of the 990 and 990EZ can be found in the example of the 990 and 990EZ can be found in the Supplemental Materials section of this module as Supplemental Materials section of this module as Exhibits # 14 and 15 respectively.Exhibits # 14 and 15 respectively.

Non-Profit Tax FilingsNon-Profit Tax Filings The form 990 and 990 EZ filings provide an The form 990 and 990 EZ filings provide an

accountability with the federal government for your accountability with the federal government for your stewardship of the non-profit tax status you hold. They stewardship of the non-profit tax status you hold. They report on:report on:– Revenues, Expenses, Fund Balances, AssetsRevenues, Expenses, Fund Balances, Assets– Donors, Board members, officersDonors, Board members, officers– Program services and accomplishmentsProgram services and accomplishments– Balance sheets and use of funds to accomplish missionBalance sheets and use of funds to accomplish mission– Audit certifications of finances and financial systemsAudit certifications of finances and financial systems– Other compliance data of interest to demonstrate strict Other compliance data of interest to demonstrate strict

adherence to 501(c)3 codeadherence to 501(c)3 code The 990 EZ is less involved and complicated to prepareThe 990 EZ is less involved and complicated to prepare

Non-Profit Tax FilingsNon-Profit Tax Filings The 990 form is filed if your corporation normally has The 990 form is filed if your corporation normally has

more than $100,000 in revenue in a year and/or more more than $100,000 in revenue in a year and/or more than $250,000 in assetsthan $250,000 in assets

The 990 EZ is filed if your corporation normally has The 990 EZ is filed if your corporation normally has between $25,000 - $100,000 in income per year AND between $25,000 - $100,000 in income per year AND less than $250,000 in assetsless than $250,000 in assets

No filing is required is your corporation has less than No filing is required is your corporation has less than $25,000 in assets per year, BUT you must use a 990EZ $25,000 in assets per year, BUT you must use a 990EZ form filed with the box checked “no filing required” to form filed with the box checked “no filing required” to let them know.let them know.

In the event of declining income, the form is In the event of declining income, the form is determined by the average of the last previous three determined by the average of the last previous three years incomeyears income

Final ConsiderationsFinal Considerations Consider joining the Evangelical Council for Financial Consider joining the Evangelical Council for Financial

Accountability (EFCA) for added accountability and Accountability (EFCA) for added accountability and credibility, in addition to their resourcescredibility, in addition to their resources

Plan for yearly financial reviews, and a full financial Plan for yearly financial reviews, and a full financial audit at least every three years by an outside CPA firm audit at least every three years by an outside CPA firm to add safety and accountability to the ministryto add safety and accountability to the ministry

Use the accrual method of accounting, which considers Use the accrual method of accounting, which considers bills which are not yet paid as expenses to be tougher bills which are not yet paid as expenses to be tougher on accounting and budgetingon accounting and budgeting

Build in strict internal and external controls and policy Build in strict internal and external controls and policy for every step of the financial process, with double for every step of the financial process, with double independent accountability checks at each point – this independent accountability checks at each point – this is to avoid temptation, by reducing the likelihood of is to avoid temptation, by reducing the likelihood of success at deception!success at deception!

Final ConsiderationsFinal Considerations Limit the number of checking accounts (1 preferred 3 at Limit the number of checking accounts (1 preferred 3 at

most!)most!) Limit the number of check signators (two on each Limit the number of check signators (two on each

check, limited people who are not related and have no check, limited people who are not related and have no vested interest)vested interest)

Limit access to checks (locked up); limit cash on site!Limit access to checks (locked up); limit cash on site! Different person prepares checks and balances the Different person prepares checks and balances the

checking account: no one every handles or counts checking account: no one every handles or counts money alone!money alone!

Prepare key monthly updates for the Board, and Prepare key monthly updates for the Board, and quarterly updates for the congregationquarterly updates for the congregation

All expenses must have an invoice to back them up – All expenses must have an invoice to back them up – no exceptions!no exceptions!

In Closing….In Closing…. Solid financial structures contributes to sound Solid financial structures contributes to sound

stewardship of God’s resourcesstewardship of God’s resources Reducing temptation to do wrong is actually a favor to Reducing temptation to do wrong is actually a favor to

those who are still maturing in characterthose who are still maturing in character Adequate compensation for ministers and other Adequate compensation for ministers and other

ministry employees glorifies God and is an investment ministry employees glorifies God and is an investment in ministry!in ministry!

Use financial and legal professionals to set up the more Use financial and legal professionals to set up the more complicated aspects of the corporation and to provide complicated aspects of the corporation and to provide auditing services.auditing services.

Hang on: God will never ask you to do something that Hang on: God will never ask you to do something that you could do by yourself – He is counting on you you could do by yourself – He is counting on you partnering with Him!partnering with Him!