Embed Size (px)

Citation preview

Quarterly Bulletin 2 2005

5

Comment

The Irish economy continues to perform well into the early partof this year. After a substantial weakening in the two previousyears when the growth in Gross National Product (GNP) wasonly 1.5 per cent and 2.8 per cent respectively, GNP growthpicked up to an estimated 5.5 per cent last year. Gross DomesticProduct (GDP) growth was slightly lower than this at 4.9 percent. GNP and GDP growth are now projected to grow by 51⁄4

per cent and 51⁄2 per cent, respectively, in 2005 and to continueat a broadly similar pace in 2006.

While economic growth in the medium-term is determinedultimately by increases in employment and improvements inproductivity, demand factors strongly influence short-termfluctuations in growth. In the Irish economy in 2002 and 2003,the two major components of domestic demand, consumptionand investment, increased only modestly. There was also a majoreasing of export demand affecting mainly the export-orientedhigh-technology sectors. This demand weakness occurred inresponse to a less benign external economic environment whichfollowed from a number of events including the ICT shock, asubstantial equity market correction, higher oil prices andincreased geopolitical tensions. Last year, consumer demandpicked up only modestly, although there was significantlystronger housing investment and a better export performance.

As far as the external environment is concerned, the worldeconomy has been in generally good shape in recent times. Lastyear saw the highest growth for the OECD economies for manyyears — about 31⁄2 per cent — although the pace of growthdecelerated in the second half of the year. This year, growth inthe major economies is likely to be somewhat lower. The US andJapan seem likely to experience weaker growth, although stillrelatively satisfactory in the case of the US. Excluding Japan,growth is expected to remain strong in Asia and especially China.The euro-area economy is estimated to have grown by 1.8 percent last year, but with a marked deceleration in the second halfof the year. Because of carryover effects from the latter part oflast year, a slightly lower rate of growth is forecast for this year.While slowing down from last year’s very strong pace, recentIMF estimates suggest world trade volumes are likely to grow byaround 71⁄2 per cent this year, with trade between the advancedeconomies likely to grow by 6 per cent. This provides a benignexternal environment for an economy like Ireland’s with a highdegree of external trade.

Two significant risks still overhang the international economy.After easing for some time, oil prices surged to new heights in

Quarterly Bulletin 2 2005

6

early April, on foot of strong seasonal demand and apparentsupply constraints. This brought oil prices in dollars toapproximately twice their average level in 2003. While mostdeveloped economies are now much less dependent on oil thansome time ago, oil prices still have the capacity to limit growthand increase uncertainty. This could be significant in regions suchas the euro area that have struggled for some time to achieveself-sustaining growth. The near-term prospects for oil prices arequite uncertain. While speculation may be adding to demand,world economic growth is expected to remain strong, includingcontinuing demand associated with the booming Chineseeconomy. This could result in oil prices remaining high. In theshort-run, there are limited substitution possibilities and thedemand for oil is, therefore, relatively unresponsive to pricechanges. The price of oil is, therefore, quite sensitive to supplydisruptions and demand shocks.

The second major external risk is the uncertainty surroundingexchange rates. The US dollar is susceptible to potentially largeswings mainly because of the large fiscal and external deficits.The policy of a significant number of countries of pegging theircurrencies to the dollar places much of the adjustment on theeuro. As a euro-area country with a relatively high proportion ofits trade with the US and the UK, Ireland has a particularexposure to fluctuations in the value of the euro against the USdollar and sterling. The most recent annual trade data show thatthe US accounts for 21 per cent of Irish exports with the UKaccounting for 18 per cent. Thus far, exports have performedrelatively well in this more uncertain environment. This isexplained partly by the fact that much of external trade with theUS is of an intra-firm nature and sterling continues to be relativelystrong, currently being still above its value at the launch of theeuro in 1999. Nonetheless, it remains the case that the possibilityof a rapid appreciation of the euro is one of the most significantrisks facing the Irish economy.

Taken as a whole, growth in Ireland’s export markets is likely tobe slightly slower than last year. This reflects a softer environmentin major markets — the US, the UK and the euro area. The mostpersistent factor remains the sluggish performance of the euro-area economy, particularly in regard to the consumer spendingcomponent of domestic demand. It is encouraging that there aresomewhat more positive indications that the prospects forinward foreign direct investment are improving, and this willenhance the export capacity of the economy.

In spite of the continuing relatively strong growth rate of theIrish economy, inflationary pressures at present seem relativelysubdued with inflation itself being close to what wouldcorrespond to price stability. The increase in the HarmonisedIndex of Consumer Prices (HICP) last year was 2.3 per cent

Quarterly Bulletin 2 2005

7

compared with 2.1 per cent in the euro area. More recentindicators point to some modest further easing of domesticinflation to a rate below that obtaining in the euro area. Therelatively strong euro is exerting downward pressure on goodsprice inflation, although the recent peak in oil prices, if sustained,would moderate this effect. Services inflation this year — forecastto be 4 per cent — will be higher than last year’s 33⁄4 per cent. Itwill be a challenge to hold down services inflation against thebackground of nominal pay increases of 6 per cent last year anda tight labour market registering a low unemployment rate of 41⁄4

per cent. Pay developments last year were heavily influenced byincreases in the public sector and the construction sector, bothof which have a limited direct impact on consumer prices.However, the strong increases in employment, even ifconcentrated in specific sectors, have the capacity to spill overinto higher pay and prices in the wider economy. With a smallereffect from public sector benchmarking increases and a moremuted performance from the construction sector, averagenominal pay is forecast to increase by 43⁄4 per cent this year.Taking account of all of these factors and the state of demand inthe economy, HICP inflation is likely to be about 2 per cent thisyear, marginally less than forecast in the last Bulletin. Beyondthat, however, there is a clear risk of some pick-up in inflationwith the economy operating effectively at full capacity and withvery low unemployment. In this regard, some modestacceleration in inflation is forecast for 2006.

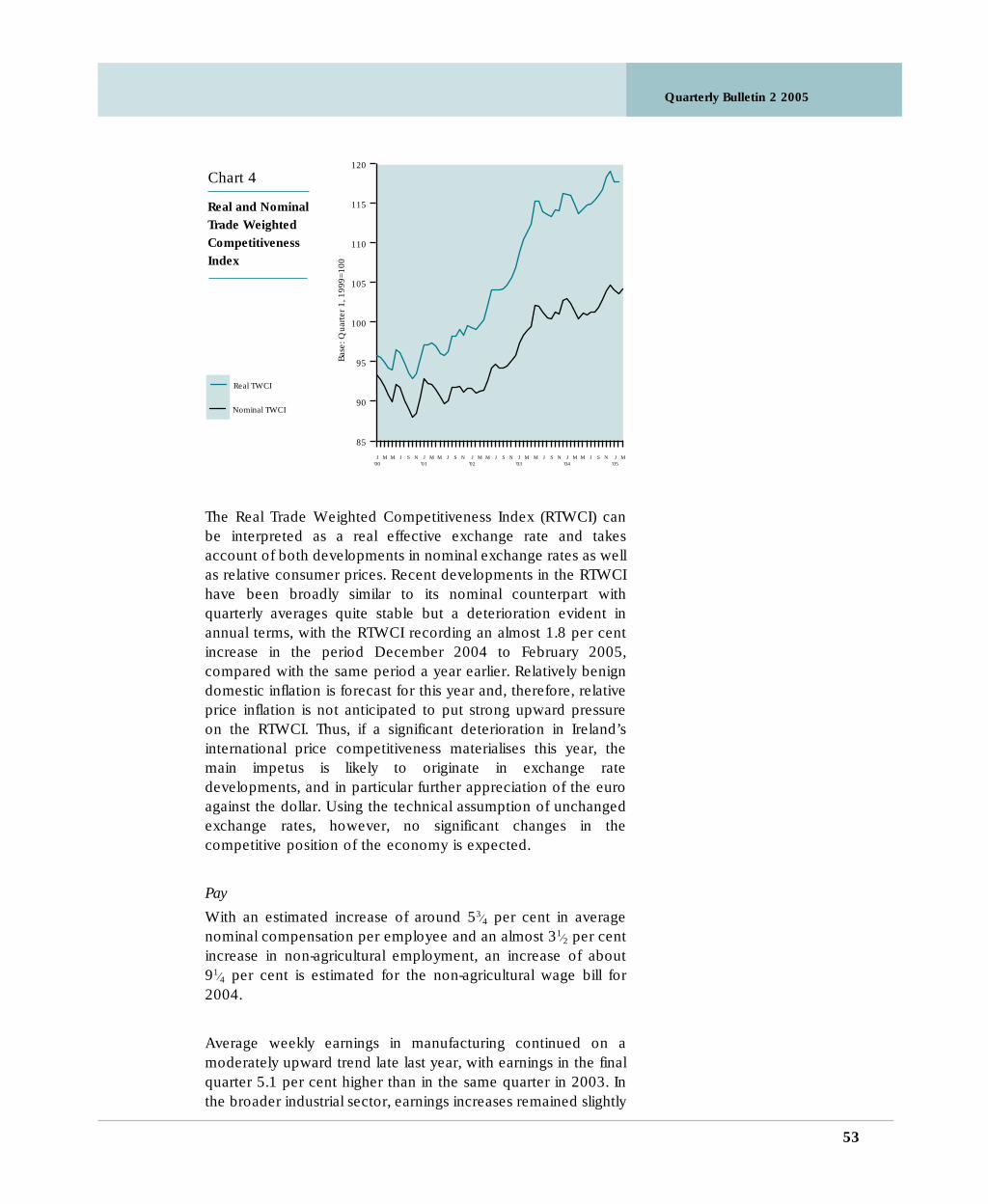

While Ireland’s inflation is now running at a rate close to that ofour main trading partners, this follows a number of years whenour inflation rate was well in excess of that of our tradingpartners. This has resulted in Ireland’s price level now being some16 per cent higher than that of the euro area as a whole. In thepresent low inflation environment, the principal potentialinfluence on the economy’s international competitiveness is theevolution of exchange rates. The US dollar, and to a lesser extentsterling, depreciated significantly from mid-2004, although,through the first quarter of this year, this has been followed bysome strengthening which has served to offset some of thisdepreciation. Nonetheless, the generally weaker US dollar andsterling have contributed to pressure on the economy’sinternational competitiveness. The Bank’s Real Trade WeightedCompetitiveness Index has deteriorated fairly steadily since late2000. As a consequence, the country’s competitiveness is nowmore vulnerable to any further dollar or sterling depreciation.

The stance of fiscal policy is an important factor in ensuring thatoverheating forces in the economy are contained. LastDecember’s Budget had a moderately expansionary tone. TotalGeneral Government spending is planned to increase by 103⁄4

per cent this year, a relatively large increase. However, the publicfinances are in very sound order, as might be expected with the

Quarterly Bulletin 2 2005

8

significant flow of revenue to the Exchequer associated with theresumption of strong economic growth. Nonetheless, it isimportant to ensure that fiscal policy is supportive of non-inflationary growth in the period ahead when the economy isoperating essentially at full capacity.

House price increases are currently easing compared with therecent past. Based on the permanent tsb index, house pricesincreased by 111⁄2 per cent on average last year, having increasedby 141⁄4 per cent in 2003. This index shows that year-on-yearincreases in recent months have been of the order of 8 per centwith recent annualised increases running at 5 to 6 per cent.

Regarding mortgage credit, although it appears to have peaked,it is still increasing very rapidly at about 25 per cent a year; thisis some three times the increase in nominal disposable income.The easing of house price increases and somewhat reducedhousing construction should, with a lag, contribute to a loweringin credit increases to a more sustainable pace. However, untilthere is some evidence of this, mortgage credit growth continuesto be a matter of concern.

Non-mortgage credit growth has also picked up in the recentpast to rates of increase of close to twice that of a year ago, andsimilar to those of mortgage credit. A significant part of thislending is being extended to the broad property sector. This highrate of increase, accompanied by substantial mortgage creditincreases, underlines the need for prudence and caution indecision-making on the part of borrowers and lenders.

The cyclically low level of interest rates has facilitated borrowersin being able to service much higher debt levels. It is inevitable,however, that interest rates will rise to more normal levels atsome point, and it is of vital importance that borrowers havemade provision for servicing debt in such changedcircumstances.

The booming construction sector underlines a number ofsignificant structural changes in the economy that have becomeevident in recent times. After peaking in early 2001,manufacturing employment has contracted until recently, whenit has broadly stabilised. Over this period, Ireland has begun toresemble typical developed economies in that, althoughmanufacturing output has increased strongly, the relativeimportance of manufacturing, particularly in terms ofemployment, in the economy has tended to decline. This isaccounted for by significant productivity increases in themanufacturing sector which, therefore, had less need for higheremployment, together with an increased demand for serviceswhich are generally more labour intensive. Currently, servicesaccount for 66 per cent of total employment compared with

Quarterly Bulletin 2 2005

9

60 per cent a decade ago. Over this period, the manufacturingproportion of total employment has fallen from 20 per cent to16 per cent. With the strong performance of the constructionsector in recent times, this sector now accounts for nearly 12 percent of total employment; this share is about 50 per cent greaterthan in most other developed countries. At some point, the shareof construction in total employment will inevitably be reduced.It will be important to ensure as far as possible that this labourcan be absorbed into other sectors of the economy withoutdisruption. This will call for significant retraining efforts and themaintenance of a good business environment to promote theestablishment of new enterprises.

International and Euro Area Economy

After growing at its fastest rate in almost three decades betweenmid-2003 and mid-2004, global economic growth has slowedsince last summer. While, in part, this represented a return tomore sustainable levels of growth following a period of robustexpansion, it also reflected the adverse impact of higher oilprices. A feature of the last nine months has been that themoderation in growth has not been uniform across countries. Inparticular, in the US and emerging Asia, especially China, growthhas remained relatively strong. In contrast, in the euro area andJapan, the slowdown has been more marked. As a result, therehas been a growing divergence in economic performance acrossregions, with the global expansion becoming more dependenton the growth of the US economy.

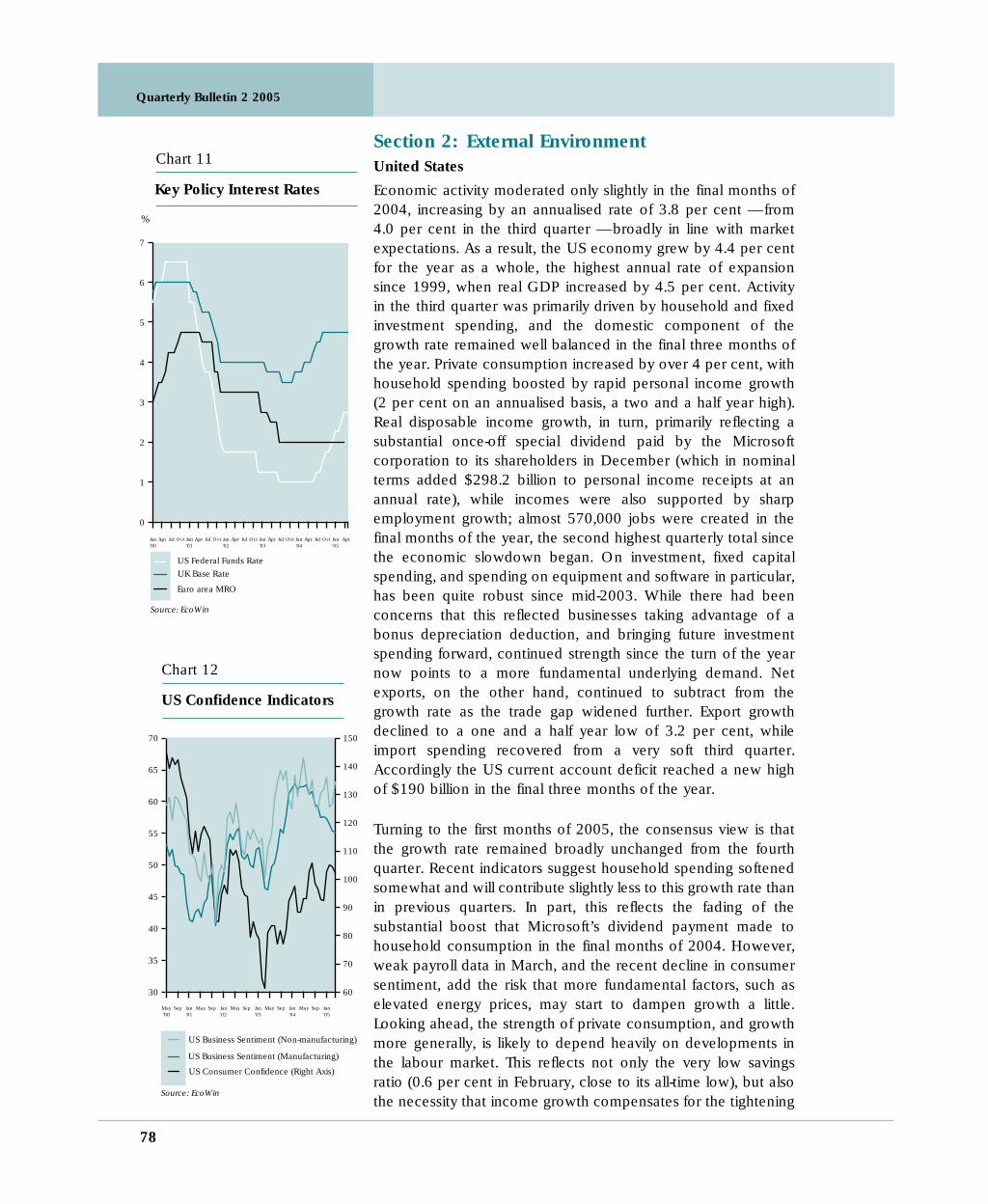

Over the last few quarters, driven by strength of domesticdemand, growth in the US has surpassed expectations. Theslowdown in mid-2004 proved relatively brief, with consumptionrebounding, supported, until recently by rising equity and houseprices. Investment spending has also grown strongly in recentquarters supported, up to now, by buoyant corporateprofitability, underpinned, in turn, by strong productivity growth.As a result, the US economy largely withstood the earlier rises inoil prices reasonably well, though, more recently, there areemerging signs that the latest hike in prices may be having someimpact. Growth in the US has continued to be supported byfavourable financial market conditions. A notable feature of USfinancial markets in recent quarters has been the persistently lowlevel of US bond yields, with current levels (as of late April) lowerthan when the Federal Reserve began tightening monetary policyin mid-2004. As a result, monetary conditions in the US haveremained relatively accommodative, with the low level of bondyields moderating the impact on economic activity of higherpolicy interest rates.

In contrast to the US, the euro-area economy lost momentumduring the second-half of 2004. The moderation of growth in the

Quarterly Bulletin 2 2005

10

euro area was largely the result of a marked decline in theexternal contribution, which was only partially compensated forby higher domestic demand. Slower global growth and thelagged impact on competitiveness of the ongoing appreciationof the euro undercut export growth, while rising oil prices alsotook their toll. As a result, economic growth in the euro area inthe second-half of 2004 was a good deal weaker than in the first-half. Despite some modest improvement in the final quarter of2004, the main disappointment continues to be the performanceof consumer spending. This has been held back by subduedemployment and wage growth, while the level of precautionarysaving has remained high, reflecting ongoing concerns in relationto labour markets and the long-term prospects for health-careand pension systems.

In recent months, the signals with regard to the outlook for euro-area growth have been mixed. While data for January was largelyfavourable, data since then has been less supportive. Bothconfidence surveys and activity data have weakened against thebackground of the renewed rise in oil prices. This is notencouraging and does not suggest that growth is likely tostrengthen in the near term.

Recent developments once again highlight the extent to whichhigh and volatile oil prices raise risks to the outlook for growth.At current levels, oil prices are around 60 per cent higher in euroterms and 70 per cent higher in US dollar terms than at thebeginning of 2004. While a colder than expected winter in theUS and Europe played some role in holding prices up in recentmonths, the main source of upward pressure has come from thestrength of oil demand from emerging economies, particularlyChina. The impact on prices has been reinforced by uncertaintiesabout OPEC production intentions, falling non-OPEC supply andlow levels of spare capacity. With the demand-supply balanceexpected to remain tight for some time, a new and somewhatworrying feature of oil markets has been the rise in long-termfutures prices, suggesting that higher prices may persist. Althoughthe global economy has weathered the impact of high oil pricesreasonably well to date, this reflects the fact that, in part, higherprices have been a consequence of strong global growth.However, persistently high oil prices pose downside risks to thegrowth outlook.

Oil prices are not the only threat, however. Reflecting thedivergence in growth performances across the major economies,global current account imbalances have widened, with the UScurrent account deficit rising to a record 5.7 per cent of GDP in2004. At the same time, movements in exchange rates havecome to be linked with the evolution of imbalances, with marketsfocussed, in particular, on the question of how the US deficit willcontinue to be financed. Given the relative fixity of some Asian

Quarterly Bulletin 2 2005

11

currencies vis-a-vis the US dollar, from time to time, this has ledto sharp upward movements in the value of the euro. This hasacted to dampen activity in the euro area and the potential forfurther volatility in the exchange rate remains an additionaldownside risk to euro-area growth.

As regards price developments, inflation and inflationarypressures have remained relatively contained. Most recently,however, there is some evidence that in the more cyclicallyadvanced economies, such as the US, some price pressures arebeginning to emerge. In the euro area, however, reflecting themodest nature of the economic recovery, inflationary pressureshave remained subdued. While higher oil prices and increases inindirect taxes and administered prices have kept inflation around2 per cent, there have been no signs of ‘second round’ effectson wage and price setting behaviour. There has been very littleevidence of pass through from higher input prices to final goods,while the continued softness of labour markets has meant thatwage growth has been moderate. Against this background,inflation expectations have remained benign and, while there aresome upside risks, underlying inflationary pressures in the euroarea remain relatively contained.

Quarterly Bulletin 2 2005

13

The Domestic Economy —

Real and Financial

Developments1

Overview

The prospects for the domestic economy remain positive.Preliminary National Accounts data for 2004 indicate that GNPgrew by 5·5 per cent last year in volume terms with acorresponding increase of 4·9 per cent in GDP. Growth shouldbe broadly similar this year. A GNP volume increase of about 51⁄4

per cent is currently projected. GDP growth is likely to besomewhat higher at about 51⁄2 per cent. On the assumption thatthere are no external shocks to the economy and that exchangerates and interest rates remain unchanged, further growth ofabout 51⁄2 per cent in GNP terms and 53⁄4 per cent in GDP termsis in prospect for next year. In broad terms, therefore, theeconomy has returned rapidly to its potential growth rate,following the slowdown in the early years of this decade, and isexpected to continue to grow at about this rate in the short-term.There are, as always, risks surrounding this projection, whichcould result in a less favourable outcome. These have beendiscussed in the preceding Comment section.

The external environment for the domestic economy remainsfavourable. Growth may ease in some of the country’s maintrading partners but only in those regions that grew very rapidlyin the recent past, such as the United States and some parts ofAsia. Other regions, such as the euro area itself, seem set toexperience a modest acceleration in growth. Overall, however,output growth in Ireland’s trading partners, weighted by theirshare in our export trade, seems likely to decelerate slightly thisyear to about 21⁄4 per cent compared with 23⁄4 per cent in 2004.This figure is projected to rise again slightly to 21⁄2 per cent in2006. This assumes that existing imbalances in the internationaleconomy, the most obvious being the large US current accountdeficit, are eliminated gradually and without major sustainedchanges to exchange rates or in the pattern of growth in themajor economies.

Domestic demand grew quite solidly last year, although this wasdue, in large part, to the strength of housing investment.Consumer spending, in contrast, grew at a relatively modestpace. In fact, given the increase in employment and earnings thatoccurred last year, it seems likely that the growth of spending

1 These forecasts were compiled in early April and do not take account of data publishedsubsequently. They assume that interest rates and exchange rates remain unchanged fromaverage levels at that time. The forecasts were produced independently by the Bank andnot as part of a Eurosystem exercise.

Quarterly Bulletin 2 2005

14

failed to keep up with the increase in disposable income. Itseems to be the case that, in spite of some improvement in thelevel of consumer confidence recorded in surveys, householdsremained relatively cautious. A pick-up in the growth ofconsumer expenditure is expected this year with a continuedstrong labour market performance supporting the growth indisposable incomes and helping to underpin consumersentiment. This somewhat faster pace of consumer spendinggrowth is expected to strengthen further next year.

While consumer spending by households came in slightlybelow expectations last year, investment spending in theeconomy grew more sharply than anticipated. This reflectedanother strong rise in residential construction funded, in largepart, by a significant rise in mortgage credit to households.There was also more rapid growth in investment spending byfirms. In contrast to consumer spending, however, the growthof investment expenditure is expected to decelerate this yearand next year. This reflects the fact that new house completionsare already at a very high level, well above the level of long-run underlying demand, and are unlikely to record furthersignificant growth. Spending on non-residential constructionmay pick up somewhat but growth in overall constructionspending and, as a result, overall investment spending seemsset to decelerate. The pick-up in consumer spending shouldoffset this slowing of investment spending to leave overalldomestic demand growth more or less unchanged in 2005 and2006 compared with last year.

Exports put in a slightly weaker than expected performance lastyear. The sectoral distribution of this performance was also alittle different from initial projections. Although the ICT sectorperformed well in terms of output growth, overall hightechnology exports were subdued, mainly reflectingdevelopments in the chemicals sector. On the other hand,exports from the more traditional sectors fared relatively well, atleast in the early part of the year. Exports of services, especiallycomputer and other business and financial services also put in astronger than expected performance. The outlook for this yearand next year is reasonably positive. External demand growth isexpected to remain strong, albeit slightly less so than was thecase last year. Bearing in mind the positive trend in inwardforeign direct investment and the improvement in the fortunesof the ICT sector, it should be possible to avoid a repeat of themarket share losses incurred last year, although this depends onthe performance of the broad chemicals sector. As a result,overall export volumes are likely to grow somewhat more rapidlythan last year, both this year and next year, in spite of slightlyslower growth in world trade. The contribution of external tradeon a net basis may not rise much, however, as import growth is

Quarterly Bulletin 2 2005

15

Table 1. Expenditure on Gross National Product 2004, 2005e and 2006f

2004 % change in 2005e % change in 2006f

\ million Volume Price \ million Volume Price \ million

Personal Consumption Expenditure 66,439 41⁄4 13⁄4 70,577 53⁄4 13⁄4 76,053Public Net Current Expenditure 21,017 41⁄2 43⁄4 23,017 21⁄4 4 24,512Gross Domestic Fixed Capital Formation 36,509 4 31⁄2 39,351 31⁄4 31⁄2 42,002

of which:

• Building and construction 26,700 4 43⁄4 29,129 21⁄2 4 31,076• Machinery and equipment 9,809 4 1⁄4 10,222 5 13⁄4 10,926

Value of physical changes in stocks 81 200 300Statistical Discrepancy −514 −514 −514

Gross Domestic Expenditure 123,532 41⁄2 23⁄4 132,631 41⁄2 23⁄4 142,353

Exports of goods and services 117,363 53⁄4 −1⁄2 123,648 6 11⁄2 133,053

Final Demand 240,895 5 11⁄4 256,279 51⁄4 2 275,406

Imports of goods and services −94,616 41⁄2 1⁄4 −99,206 43⁄4 2 −106,026

Gross Domestic Product 146,279 51⁄2 13⁄4 157,073 53⁄4 2 169,380

Net factor income from rest of the world −23,727 −25,181 −27,331

Gross National Product 122,552 51⁄4 21⁄4 131,892 51⁄2 21⁄4 142,049

likely to be sustained by stronger consumption growth andincreased high-technology exports.

Labour market developments remain very positive. Employmentgrew by about 3 per cent last year reflecting, in part, the relativelyemployment-intensive nature of output growth, with theresidential construction sector and the services sectorcontributing strongly. The scale of employment growth mighthave given rise to more labour market tensions if it had not beenaccompanied by strong labour force growth. Part of this growthcame from domestic sources, reflecting the natural increase inthe population as well as the tendency for participation rates torise again as labour market conditions improved. Anothersignificant element, however, has been stronger than expectedinward migration. A similar pattern may recur this year and nextyear, with inward migration helping to ease labour shortages inthe economy. Employment growth may ease back slightly,however, reflecting changes in the composition of outputgrowth, in particular, less reliance on growth in the labour-intensive residential construction sector. The increase inemployment is still expected to reach 21⁄4 per cent and theunemployment rate may stabilise at about its current level of 41⁄4

per cent, compared with an average of 41⁄2 per cent for last year.Unemployment is expected to remain at a similar level next yearalthough the rate of growth of both employment and the labourforce are likely to ease back somewhat.

Domestic Demand

Personal Consumer Spending

Consumer spending grew by 3·2 per cent last year according topreliminary National Accounts data. This was a relatively muted

Quarterly Bulletin 2 2005

-2

0

2

4

6

J'05

DNOSAJJMAMFJ'04

DNOSAJJMAMFJ'03

DNOSAJJMAMFJ'02

Core (excluding Motor Trades)

All Businesses

Year-On-Year % – 3 Month Moving Average (SA)

Index of Volume of

Retail Sales

Chart 1

16

outcome, however, given developments in real disposableincome. Strong employment and earnings growth gave rise toquite a significant rise in incomes. Income tax grew more rapidlythan expected, albeit largely due to the impact of one-off factors,such as payments of tax owed on bogus non-resident accounts.While the rise in income tax receipts may have mechanicallylowered disposable income growth last year, these payments donot typically affect short-term consumption patterns. Recordedlevels of consumer confidence strengthened last year, albeitsomewhat unevenly. The general trend was positive but therewere some months when the recorded level of confidenceactually declined, suggesting that consumers remained cautious.Rising house prices, which are often associated with a decline inthe savings rate, do not seem to have boosted consumption inthe recent past. Paradoxically, high and rising house prices maybe contributing to maintaining savings at a high rate in order toaccumulate deposits for house purchases or make repaymentson new and relatively large mortgages. Equity release forconsumer spending purposes seems limited at this point in time.Older households, who may own property that has appreciated,do not seem to be increasing their consumer spendingsignificantly as a result.

The prospects for this year are for somewhat faster consumerspending growth. Disposable incomes are expected to risesignificantly again. Employment growth is expected to remainstrong, albeit slightly weaker than last year, and to beaccompanied by another significant rise in average earnings.Inflation is also set to remain relatively low, boosting the rise inincomes in real terms. Direct tax payments are also projected torise less rapidly than last year, further increasing disposableincome growth. Only another rise in the savings rate couldprevent an acceleration in consumer spending and this seems,on balance, unlikely in current circumstances. It seems morelikely that a continued rise in consumer confidence will lead to agradual strengthening of spending, although, of course, thisassumes away any negative shocks to the economy. On thisbasis, consumer spending growth should pick up to about 41⁄4

per cent this year. The indications are reasonably positive to date.The volume of retail sales rose by 6·8 per cent, year-on-year, inthe first two months of 2005, although excluding car sales, theincrease was a more modest 4·5 per cent. Car sales were upsignificantly, 7·4 per cent in year-on-year terms, in the first threemonths.

The growth in real disposable incomes may ease back slightly in2006 as employment growth decelerates somewhat and inflationmay edge up again. On the other hand, confidence shouldremain at a high level and there may be some support tospending as households begin to have access to maturing SSIAaccounts, although the greater proportion of these accounts willnot mature until 2007. The latter are not expected to have a

Quarterly Bulletin 2 2005

17

dramatic impact on spending with much of the funds beingtransferred to other savings vehicles or used to reduce existingdebt. It is likely, however, that they will have some impact onexpenditure, albeit much of it directed at purchases of importedconsumer durables. Against this background and taking intoaccount the fact that consumption growth has been relativelysubdued in recent years, the volume of consumer spendinggrowth may accelerate further to about 53⁄4 per cent in 2006.

Government Consumption

The volume of government consumption has tended to growrelatively modestly in recent years, certainly by comparison withthe very strong rates of growth experienced up to 2002. On thebasis of the available information, there seems likely to be somepick-up in the volume growth in government consumption thisyear to about 41⁄2 per cent. It is assumed that growth ingovernment consumption will ease back next year to about 21⁄4

per cent, more in line with the experience of recent years. Thisis in the nature of a technical assumption, however, based oncurrently available information. The Budget for 2006 willdetermine the final outcome in this regard.

Investment

Gross domestic fixed capital formation grew rapidly last year, by9·2 per cent according to the Quarterly National Accounts. Thiswas the highest rate of growth since 1999 and three times as fastas in each of the previous two years. The surge in investmentlast year was driven by a marked upturn in both categories ofinvestment expenditure, with building and constructioninvestment up 7·7 per cent and machinery and equipmentinvestment up 11·4 per cent in the year. In particular, the firsthalf of 2004 was characterised by strong investment, due torecord levels of house building and substantial investments intransport equipment. Activity levels slowed somewhat in thesecond half of the year although investment expenditure, inseasonally adjusted terms, was still up by 4·5 per cent, quarter-on-quarter, in the fourth quarter of 2004.

Building and construction investment grew markedly last yeardue to significant growth in the residential house building sector.In the first six months of 2004, this category of investment wasup about 20 per cent, year-on-year. This contributed to a recordnumber of housing completions last year, with some 77,000 newcompletions, up nearly 12 per cent on the previous record in2003. Residential investment growth levelled off, however, in thesecond half of the year, with investment up by 5 per cent. Itseems that house building levels are beginning to hit a plateauand should peak this year. Other categories of building andconstruction grew by about 3 per cent last year, which largelyreflected a weakness in public investment.

Quarterly Bulletin 2 2005

18

Machinery and equipment investment increased strongly in2004, by 11·4 per cent after growth of 1·2 per cent in 2003. Thisrecovery was driven by significant and predominantly one-offinvestments in transport equipment in the first half of the year.The pick-up in equipment investment is reflected in importfigures with capital imports up by 13 per cent last year, afterdeclining sharply in 2003. The underlying picture, however, wassomewhat weaker when transport investments are excluded asevidenced by the subdued performance of the manufacturingsector in 2004.

Looking ahead to this year and next, a much slower rate ofgrowth in construction investment is envisaged. This is based onthe fact that current levels of house building are in excess of theeconomy’s medium-term requirements. In addition, there is verylimited scope for further increases in housing output given thetightness in the labour market at present, with numbersemployed in the sector up 10 per cent last year alone. A furtherincrease in employment of this magnitude is highly unlikely,particularly given very low unemployment and with the sectoralready accounting for 12 per cent of total employment, whichis exceptionally high by international standards. Furthermore,house price data from last year and for the first quarter of 2005show that house price increases have moderated, which isindicative of demand and supply coming more into line. As aresult, the number of house completions is forecast to peak thisyear at about 78,000 units, marginally up on last year’s outcome,before declining in 2006. The non-residential construction sector,however, is expected to grow somewhat more rapidly in 2005and 2006 given the continuing need for infrastructuralinvestment and with an improving outlook for the commercialsector. For 2005 as a whole, construction investment is forecastto grow by just over 4 per cent, followed by growth of 21⁄2 percent in 2006.

In terms of equipment investment, a reasonably positiveperformance is expected this year and next, given that theprospects in Ireland’s main trading partners appear favourable.In particular, a recovery in the modern sectors of the economy(which include the ICT, chemicals and pharmaceuticals sectors)is envisaged in 2005 and 2006 and this should lead to some pick-up in investment. For 2005, machinery and equipmentinvestment is expected to grow by 4 per cent, with growth of 5per cent in 2006. These forecasts, combined with the estimatesfor the construction sector, mean that overall investment isforecast to grow by 4 per cent this year and by 31⁄4 per cent in2006.

Stock Changes

Preliminary National Accounts data confirm that stocks made anegative contribution to growth last year. While this pattern was

Quarterly Bulletin 2 2005

-25

-20

-15

-10

-5

0

5

10

15

20

25

30

Q4Q3Q2Q1'04

Q4Q3Q2Q1'03

Q4Q3Q2Q1'02

Q4Q3Q2Q1'01

Exports

Imports

Value of

External Trade

Chart 2

% Year-On-Year Seasonally Adjusted

19

expected, the scale of the negative contribution was larger thananticipated. This outcome reflected the fact that there was a verysignificant accumulation of stocks in 2003. The prospects for thisyear are for a positive contribution to growth with continuinggrowth in the economy leading to some planned stockaccumulation. This positive contribution may be a bit larger thanpreviously expected given the weak outcome for 2004. A further,but smaller, positive contribution to growth is projected for 2006.

Merchandise Trade and the Balance of Payments

Merchandise Trade

Merchandise exports grew somewhat more slowly than wasinitially expected last year. This was due to a relatively subduedperformance by the broad chemicals sector following very stronggrowth in previous years. There was a recovery in the outputgrowth of the ICT sector, however, and other more traditionalexporting sectors, such as food, performed reasonably well,particularly in the early part of the year. The monthly trade dataand the National Accounts data give a more accurate picture ofdevelopments in the exporting sectors than the monthlyindustrial production data, which suggested a rather weak picturebut is overly influenced by developments in the chemicals sector(see Box A). Merchandise import volumes also grew by less thananticipated partly reflecting the pattern of exports, although theydid pick up somewhat in the latter part of the year. Overall,however, output growth was less import-intensive in itscomposition than might have been expected at the beginning ofthe year, with somewhat more growth coming from theconstruction and services sectors.

The prospects for export growth this year remain favourable.Import demand in the country’s main trading partners isexpected to be fairly robust, albeit somewhat less so than in2004, reflecting a slowdown in the growth rates of some majoreconomies such as the US. Exports will also be assisted by thereasonably positive trend in foreign direct investment as well asa continued recovery in the ICT sector. These factors may besufficiently strong to allow export volume growth to pick upsomewhat from last year’s outturn, although a return to the largemarket share gains of the 1990s does not seem to be in prospect.

Table 2. Merchandise Trade (Adjusted) 2004, 2005e and 2006f

2004 % change in 2005e % change in 2006f

\ million Volume Price \ million Volume Price \ million

Merchandise Exports 79,450 51⁄2 −11⁄2 82,457 53⁄4 11⁄4 88,320

Merchandise Imports −47,585 51⁄4 − 1⁄4 −49,932 51⁄2 21⁄4 −53,830

Trade Balance 31,865 32,525 34,490

(% of GNP) (26) (243⁄4) (241⁄4)

Quarterly Bulletin 2 2005

20

Box A: The Discrepancy Between Industrial Production Output Data and

Quarterly National Accounts Industry Data

Chart 1 graphs the growth rates of output of the industrial sector accordingto two alternative CSO sources; the Industrial Production release and thequarterly National Accounts. Last year the Industrial Production indexindicated that industrial output grew at a rate of 0·7 per cent, while thequarterly National Accounts pointed to a markedly higher growth rate of3·5 per cent. Indeed, over the last few years the two growth rates haveoften differed. Part of the difference between the Industrial Productionseries and the published National Accounts industry figures can beattributed to the inclusion of building and construction output in the latter.This has been netted out of the chart below so that the two series coverthe same spectrum.

0

5

10

15

20

25

30

35

Royalties Imports

0%

2

4

6

8

10

12

14

16

18

Indu

stria

l Out

put

Yea

r-on-

Yea

r G

row

th

Ro

yalti

es Im

port

s Y

ear-o

n-Y

ear

Gro

wth

National AccountsIndustrial Production

20042003200220012000

Chart 1 Industrial Output Measures – Why the Difference?

% %

The methodology used to calculate the National Accounts figures involvesapplying the Industrial Production monthly volume indices to the NationalAccounts base year’s gross value-added, including royalties. In addition, theCSO, when compiling the National Accounts, also examine the consistencyof the statistical returns of individual large enterprises. As a result, the value-added figures extrapolated from the monthly Industrial Production indexmay be occasionally adjusted. These adjustments are also reflected in theabove figures.

Royalty and licence payments, which are classified as imports of servicespaid by foreign firms (mostly in the chemicals and ICT sectors) based inIreland back to their parent companies need to be deducted from theNational Accounts definition, since they are regarded as inputs intoproduction and not value-added. In the Industrial Production series, noaccount is made for increasing use of service inputs over time. As the chartshows (the right axis measures the growth rate of these royalty payments— classified as imports), these royalty payments have been increasing at ahigh rate since 2000, dropping sharply in 2004. This sudden decrease inthe growth rate of royalty payments last year served to increase the growthrate of industrial output under the National Accounts definition, relative tothe Industrial Production measure, where no deduction was made.

Quarterly Bulletin 2 2005

21

An improvement partly depends, however, on a strongerperformance by the chemicals sector compared with 2004. Italso assumes that there is no major change in the euro exchangerate that would cause a significant loss of competitiveness. Onthis basis, an increase of about 51⁄2 per cent might be expected.On the basis of the same assumptions, there is likely to be furthergrowth of about 53⁄4 per cent in merchandise export volumesnext year against a background of broadly similar export marketgrowth and little change in competitiveness. Import volumegrowth is also expected to pick up this year in response tosomewhat higher growth in merchandise exports and personalconsumption. A similar pattern of somewhat stronger importgrowth is expected next year.

Merchandise trade prices were forced down by the appreciationof the euro in the latter part of last year and this pressure is likelyto have persisted into the early part of this year. The higher levelof oil prices was undoubtedly a factor in the terms of trade losssuffered last year with import prices not falling as sharply asexport prices. The prospects for this year depend largely onexchange rate developments. On the basis of the technicalassumption of unchanged exchange rates, the downwardpressure on trade prices should ease as the year progresses, butboth import and export prices will probably still be marginallydown, on average, this year compared with last year. Oil pricesare assumed to evolve in line with the futures market, whichsuggests that there may be a small easing in prices this year andnext year. Nevertheless, a further terms of trade loss is expectedthis year, although it may be somewhat less than thatexperienced last year. Using the same technical assumptions,there should be a return to small increases in trade prices inline with competitors’ prices next year. These developments are,however, sensitive to the technical assumptions used and eventssuch as a significant appreciation of the euro could obviouslychange these prospects significantly. On the assumption thatsuch events do not occur, the merchandise trade balance shouldincrease from \31·9 billion last year to about \32·5 billion thisyear and \34·5 billion in 2006.

Services, Factor Incomes and International Transfers

In contrast to merchandise exports, exports of servicesperformed more strongly than expected last year. The favourableperformance was mainly in the areas of computer, business andfinancial services rather than in the more traditional sectors suchas tourism and transport where growth was more muted. Theshift towards increased services exports is likely to continue inthe future, reflecting the pattern of inward investment in sectorssuch as computer services and financial services. As a result,further significant growth in services exports is expected boththis year and next year. The growth in imports of services, mainlydriven by the multinational sector, was muted last year but can

Quarterly Bulletin 2 2005

22

be expected to pick up, assuming a stronger performance byother sectors.

The balance of factor income flows was less negative thanexpected last year. This mainly reflected developments on thecredit side with inflows of profits accruing to firms headquarteredin Ireland rising significantly. Outflows were adversely affectedby the relatively modest performance of the foreign-owned high-technology sectors. The result was that GNP growth exceededGDP growth last year in a reversal of the usual pattern. It is worthrecalling the point made in previous Bulletins, that thesemeasures can be affected, particularly in Ireland’s case, not onlyby the large number of foreign multinationals operating in thecountry but also by a relatively small number of multinationalsheadquartered in Ireland with significant operations abroad (seeBox A on page 13 of the Spring 2004 Bulletin). It may be unwise,therefore, to attribute too much significance to short-termmovements in these variables caused by factor income flows. Itis expected that the more usual pattern will reassert itself boththis year and next year with some pick-up in factor incomeoutflows, although this depends, to some extent, on a recoveryin output in the broad chemicals sector. Inflows may also notgrow as rapidly as last year but it has to be conceded thatdevelopments will be driven by a small number of firms and are,as a result, unpredictable.

The international transfer balance deteriorated as expected lastyear and a further deterioration is projected both this year andnext year. This reflects an almost inevitable pattern as thecountry’s improved income position relative to others means thatit attracts less transfers and has to contribute more, for example,to the EU budget. Taking the trends in the various componentsof the current account together suggests that the overall deficitwill remain broadly unchanged this year at about \0·5 billion(about 1⁄2 per cent of GNP) with a small decline likely to about\0·2 billion next year (about 1⁄4 per cent of GDP).

Capital and Financial Account

There was a small surplus of \364 million on the Capital Accountin 2004, which is broadly in line with a \370 million surplus in2003. The Financial Account showed a credit balance of \4·5billion in 2004. This credit balance was due to direct investmentand other investment inflows, which were largely offset byportfolio investment outflows of \20·9 billion. The balancingitem, net errors and omissions, for the balance of payments as awhole, was a debit of over \4 billion for 2004.

Inward direct investment of \11 billion in 2004 was almost halfof direct investment in Ireland of \24 billion in 2003. Thisdecrease was principally due to a sizeable reduction inreinvested earnings in Ireland of \6·2 billion in 2004, and a

Quarterly Bulletin 2 2005

23

Table 3. Balance of Payments 2004, 2005f and 2006f

| million

Current Account 2004 2005f 2006f

• Merchandise Trade Balance (adjusted) 31,865 32,525 35,090

• Services −9,118 −8,083 −8,063

• Net factor Income from Rest of the World −23,727 −25,181 −27,331

• Current International Transfers 332 224 74

Balance on Current Account −648 −515 −230

(% of GNP) (−1⁄2) (−1⁄2) (−1⁄4)

Capital and Financial Account 2003 2004

Full Year Quarter 4

Balance on Capital Account 370 364 362

Financial Account

• Direct Investment 20,686 2,135 −5,622

• Portfolio Investment −49,114 −20,856 −12,263

• Other Investment 29,258 22,009 19,136

• Reserve Assetsa 1,770 1,177 −18

Balance on Financial Account 2,596 4,465 1,233

Net errors and omissions −1,070 −4,179 −1,832

aChange in reserves on a transactions basis, i.e. excluding valuation adjustments. A minus figure equals a net increase in reserve.

reduction in equity investment in Ireland of \5 billion. Outwarddirect investment grew by \6 billion in 2004, with other capitalabroad accounting for a large part of this increase.

Net portfolio investment outflows amounted to \20·9 billion in2004, which was considerably lower than net outflows of \49billion in 2003. Debt instruments accounted for over 70 per centof portfolio investment outflows of \130 billion, with bonds andnotes comprising the largest component. Equity liabilitiesaccounted for \65 billion of inward portfolio investment of \109billion in 2004.

Financial transactions, under the ‘other investment’ heading —mainly loans, currency and deposits — resulted in net inflows of\22 billion. All of these net inflows arose from transactionsinvolving non-IFSC entities.

The official external reserves amounted to \2,141 million in thefourth quarter of 2004. This included a valuation write-down of\27 million in December 2004.

Output Trends and the Labour Market

Industry and Services Output

Since the peak in 2000, growth in the output of the overallmanufacturing sector has been on a steady downward trend.

Quarterly Bulletin 2 2005

-10

0

10

20

30

40

50

Q4Q3Q2Q1'04

Q4Q3Q2Q1'03

Q4Q3Q2Q1'02

Q4Q3Q2Q1'01

All Other Manufacturing Sectors

Modern Sector

Manufacturing

Volume of Production

in Manufacturing

Chart 3

Year-On-Year % Change

24

Table 4. Industry and Manufacturing Output, Annual Percentage Change

Manufacturing All Industries

Year Total Modern Sector Other Sectors

1996 81⁄2 8 133⁄4 21⁄21997 191⁄4 171⁄2 291⁄4 41998 211⁄4 20 301⁄2 41⁄21999 15 143⁄4 211⁄4 32000 153⁄4 151⁄4 201⁄4 51⁄22001 10 10 143⁄4 21⁄42002 71⁄2 71⁄2 12 −1⁄22003 41⁄2 5 6 32004 1⁄2 3⁄4 −1⁄2 32005f 3 3 3 32006f 51⁄4 51⁄4 6 3

Average 1996-2006 91⁄4 91⁄4 63⁄4 31⁄4

Now that full year figures for 2004 are available, it is apparentthat the slowdown in manufacturing documented in the lastBulletin continued throughout the year, although the extent ofthe slowdown varies according to data sources (see Box A). Thereturn to potential economic growth in 2004, it would seem, hasnot spread to the entire manufacturing sector.

The CSO industrial production index indicates that the volumeof manufacturing output increased by only 0·4 per cent in 2004,compared with the previous year, its lowest rate of increase inover twenty years. In a reversal of historical trends, the output ofthe ‘modern’ sector (largely the chemicals and ICT firms) actuallycontracted by 0·4 per cent last year, whereas the output of the‘traditional’, mainly Irish-owned firms, increased by a relativelyhealthy 3·1 per cent over the same period.

The poor performance of the ‘modern’ sector was not, however,across the board. The ICT sector (mainly electrical and opticalequipment) experienced significant year-on-year growth of 11·6per cent in 2004, further progressing its recovery since the lowpoint of 2002. The reproduction of recorded media sub-sector,also part of the ICT sector, recorded strong year-on-year growthof 31 per cent in 2004. The performance of the overallmanufacturing sector last year was, however, heavily influencedby weakness in the chemicals sector but, again, performancewithin this sector varied significantly. Output of the overallchemicals sector decreased by 9·3 per cent in 2004, drivenmainly by weakness in the basic chemicals sub-sector (typicallyfirms that manufacture the raw materials for pharmaceuticals),where output last year was down 15·9 per cent on the previousyear. This sector, in particular, has a large share in gross valueadded and, therefore, a significant weighting in the overall series.Developments in this sector can easily influence the overallmanufacturing output figure. The pharmaceuticals, medicalchemicals and botanical products sub-sector, on the other hand,

Quarterly Bulletin 2 2005

25

performed well last year, with output up 29 per cent on theprevious years output.

The ‘traditional’ and mainly Irish-owned sector posted steadyreturns in 2004, where output increased by 3·1 per cent, year-on-year, led mainly by positive developments in the food sector.Irish manufacturers that have re-orientated production to highervalue added products which often involve considerably morescientific research and technological production than waspreviously the case, reported strong growth. The ‘other foods’sub-sector of the industrial production index, which typicallycaptures these goods, increased output by a sizeable 17 per centlast year. Production in the overall food sector increased by 9·1per cent, year-on-year, in 2004. There was weakness, however,in the output of the beverages (down 5 per cent) and tobacco(down 28·9 per cent) sub-sectors.

Turning to more recent trends (provisional industrial productionfigures for February of 2005 were the latest available data at thetime of writing), and bearing in mind that monthly productionfigures are often volatile, the ICT sector continued to recordstrong growth, with output over the three-month periodDecember 2004 to February 2005 increasing by 20·3 per cent,relative to the same period last year. This was largely as a resultof significant output growth in the office machinery andcomputers sub-sector, up 24·8 per cent in the same three-monthperiod, year-on-year, and strong year-on-year growth in the radio,television and communication equipment sub-sector — up 26·9per cent on the same period last year. The reproduction ofrecorded media sub-sector also performed well, registering year-on-year growth of 41·7 per cent over the same period.

The weakness of the overall chemicals sector reported in the lastBulletin seems to have continued into this year, with December2004 to February 2005 output down 14·9 per cent on the sameperiod last year, although, the seasonally adjusted figure mayindicate some more recent moderation in this contraction,registering a slight contraction of 0·9 per cent over the precedingthree-month period. However, as stated previously, performancewithin the sector is varied. While the year-on-year growth rates inthe basic chemicals sub-sector were still extremely poor, there wasa slight increase in the three-month (December 2004 to February2005) seasonally adjusted output figure of 0·3 per cent, pointingto some possible pick-up in output growth, or at least somemoderation in the rate of decline. The pharmaceuticals sectorshowed strong increases in the three-month year-on-year figure (up28·2 per cent) but showed signs of a deceleration in the seasonallyadjusted three-month quarter-on-quarter figure, which recorded acontraction of 7·5 per cent in output over the preceding three-month period. On the indigenous front, the ‘other foods’ sub-sector, showed reasonably solid growth, registering growth on a

Quarterly Bulletin 2 2005

26

seasonally adjusted basis over the same three-month period of 2·3per cent compared with the previous three-month period.

Industry figures in the latest quarterly National Accounts (Q4 of2004) paint a somewhat more positive picture than the industrialproduction figures quoted above but are not, however, directlycomparable (for an explanation of the difference — see Box A).While only aggregate industry data are available, they indicatethat output growth in the industrial sector (net of building andconstruction) increased by approximately 3·1 per cent, year-on-year, in 2004. Within 2004, however, the quarterly year-on-yearprofile revealed some more recent weakness, reporting outputgrowth of 8, 3·7, 3·8 and -2·2 per cent in the first, second, thirdand fourth quarters, respectively.

The most recent survey evidence for the manufacturing sectorfrom the NCB Purchasing Managers Index (PMI) Report onManufacturing provides some less than positive evidence for thesector. In a turnaround since the last Bulletin, the Report showsthat rate of expansion of the sector fell for a third consecutivemonth. The PMI — an indicator designed to provide a singlefigure measure of the economic health of the manufacturingsector — fell consecutively from a December 2004 value of 53·1to 50·7 in March 2005. Although a value above 50 indicatesimproved conditions, the trend appears somewhat negative. TheReport highlighted that output had expanded at weaker rates inMarch with new export orders showing a slight decline. Panelfirms attributed the fall to weaker demand in export markets andstrong competition from foreign rivals.

For the current year, assuming a broadly positive externalenvironment and no further adverse movements in exchangerates and oil prices, the output of the manufacturing sector isforecast to be up on last year to the tune of about 3 per cent. Thecontinued resurgence of the ICT sector, along with the steadyperformance of some indigenous sectors should ensure areasonable outturn. Due to the unusually large weighting of thechemicals sector, however, and its current volatility, the finaloutturn is somewhat uncertain. With prospects for the globalpharmaceuticals and chemicals sectors (often the inputs topharmaceuticals) being somewhat uncertain at the moment, therisks to overall industry output growth would appear to be onthe downside. It is worth bearing in mind, however, that althoughthe chemical sector might contribute heavily to value added, itseffect on the domestic economy in terms of employment andincome is not that large. For next year, again assuming noadverse developments on the global economic stage, outputgrowth in the manufacturing sector is forecast to pick up toabout 5·2 per cent. This improvement, however, depends on theassumption of stronger growth in the volatile chemicals sector.

Quarterly Bulletin 2 2005

27

The latest available indicators for the services sector, on the otherhand, point to a much more positive picture than that for themanufacturing sector. The latest available PMI Report onServices (March) indicated that activity in the Irish service sectorincreased at its fastest rate in nearly three years. Surveyed firmsreported that the increase in activity stemmed from higher levelsof new business. Levels of confidence about future businessactivities also remained high. The quarterly National Accountsindicate that the overall service sector grew by a healthy 3·9 percent in 2004. Activity in the distribution, transport andcommunication sub-sector increased by 3·4 per cent over theprevious year, while the ‘other services’ category expanded at arate of 4·5 per cent. Furthermore, the latest employment data forthe services is very strong (see Labour Market section).

For the construction sector, output growth seems set to moderatethis year, as the supply of housing comes more into line withdemand. Investment in building and construction this year isforecast to increase by about 3·8 per cent with a correspondingdecline in the rate of output growth. The level of housecompletions is set to remain high this year and, looking forward,non-housing construction should accelerate to offset the impact ofa peak in housing output. Nevertheless, over the medium term thesector will probably have to adjust downwards as a proportion ofoverall output and employment in the economy.

Agricultural Output

Preliminary estimates for output and income in the agriculturalsector indicate that 2004 was a relatively favourable year for theagricultural sector. The value of agricultural output increased by3·1 per cent, while agricultural income (operating surplus)increased by 3 per cent. The volume of agricultural output lastyear increased only marginally, by 0·6 per cent, with outputprices up approximately 2·5 per cent. The volume ofintermediate consumption (inputs) decreased by approximately1·6 per cent, as input costs increased by about 2·7 per cent. Netsubsidies for the year were unchanged.

The latest available quarterly National Accounts show that thevolume of production in the broader agricultural sector (inclusiveof forestry and fishing) increased by 2·1 per cent in 2004. Thequarterly profile reveals that production increased strongly in thefirst half of the year, followed by a deceleration in the latter half,with growth of 5·8, 4, -0·7, and -3·4 per cent, year-on-year,respectively, in the four quarters of the year. There was weaknesson a seasonal adjusted basis in the latter half of the year, withoutput falling by 2 per cent and 1·2 per cent in the third andfourth quarters, relative to the previous quarters.

This year is expected to be a broadly similar one for theagricultural sector. There are, however, a number of risks, mainly

Quarterly Bulletin 2 2005

28

Table 5. Summary of Agricultural Output and Income 2004e, 2005f and 2006f

2004e % change in 2005f % change in 2006f

\ million Value Volume Price \ million Value Volume Price \ million

Goods Output at Producer Pricesa 4,968 23⁄4 1⁄2 21⁄4 5,104 1⁄2 −11⁄2 2 5,130

Intermediate Consumption 3,409 −1 −1 2 3,375 −2 −3 1 3,307

Net Subsidies plus Services Outputless Expenses 1,475 0 1,475 0 1,475

Operating Surplus 2,144 23⁄4 2,203 1 2,225

a Including the value of stock changes.

on the downside, inherent in any projection — principally,adverse weather conditions, further strength of the euro againstthe dollar and the next phase of the Medium-Term Review of theCommon Agricultural Policy. In terms of beef slaughterings, itappears unlikely that any major de-stocking associated withdecoupling will take place this year and any fall in output shouldbe relatively minor. Agricultural output is forecast to rise by asimilar amount as 2004, somewhere in the region of 23⁄4 per cent,with agricultural incomes also increasing by about 23⁄4 per cent.For next year, assuming no adverse developments (weather,further exchange rate movements, favourable global economicclimate) agricultural output is forecast to remain broadlystatic, with some decoupling-related decreases in volume ofapproximately 1·5 per cent. Agricultural incomes in 2006 areforecast to increase by approximately 1 per cent.

The Labour Market

Total employment in the economy grew by 3·0 per cent onaverage last year, with numbers at work up by 54,400, based ondata from the Quarterly National Household Survey (QNHS).This marked the fastest rate of growth since 2001. The labourmarket strengthened in the second half of 2004, with numbersat work up by 3·6 per cent annually in the fourth quarter toexceed 1·89 million. Furthermore, most of the new jobs createdwere in full-time positions with part-time employment accountingfor just under one fifth of the change in employment.

Substantial growth was recorded in the construction sector lastyear, with an additional 19,100 persons employed (+9·8 percent). There were also significant gains in certain parts of theservices sector with numbers employed in the ‘‘other servicessector’’ increasing by 12,100 (+12·2 per cent) and an additional11,800 persons employed in financial and business services (+5·1per cent). Numbers at work in the health and education sectorincreased by 9,900 (+3·4 per cent) and by 9,200 in wholesaleand retail trades sector (+3·6 per cent). Employment declined inmanufacturing last year by 3,100 (−1·0 per cent) and by 3,500

Quarterly Bulletin 2 2005

29

Table 6. Employment and Unemployment 2004, 2005e and 2006f

(annual average ’000) 2004 2005e 2006f

Agriculture 117 115 112Industry (including construction) 516 518 516Services 1,232 1,274 1,318

Total Employment 1,865 1,907 1,946Unemployment 87 87 85

Labour Force 1,952 1,994 2,031Unemployment Rate (%) 41⁄2 41⁄4 41⁄4

Note: Figures may not sum to the total because of rounding.

in the hotels and restaurants sector (−3·0 per cent). Agriculturalemployment also fell by 2,600 persons (−2·2 per cent) last year.

The labour force grew by 2·8 per cent last year, which was thefastest rate of increase since 2000. By the end of 2004, therewere approximately 1·98 million persons in the labour force. Thisincrease was driven by increased labour force participation anddemographic factors. In terms of the former, there was a rise inthe labour force participation rate last year to 60·7 per cent from60·2 per cent. In particular, the contribution of higherparticipation from females drove much of the growth in the workforce, with the female participation rate rising to 50·2 per centfrom 49·6 per cent in 2003. In addition, net migration isestimated to have added significantly to the labour force last yearaccounting for approximately one third of the increase, roughly18,000 persons. Given the growth in employment and the labourforce last year, the unemployment rate declined furtheraveraging approximately 4·4 per cent, down from 4·6 per centin 2003.

The labour market entered 2005 with considerable momentum,given seasonally adjusted data which show that numbers at workgrew by 1·2 per cent, quarter-on-quarter, in the fourth quarter of2004, due to very large increases in employment in construction(+3·5 per cent), in the public sector (+3·7 per cent) and in partsof the services sector. The labour force grew in seasonallyadjusted terms by 1·3 per cent, quarter-on-quarter, with theunemployment rate at 4·4 per cent at the end of 2004. Datafrom the Live Register for the first three months of 2005 showthat numbers on the Register, in seasonally adjusted terms, fellby 1·9 per cent on the preceding three-month period. In addition,the standardised unemployment rate averaged 4·2 per cent inthe first quarter of 2005, down from 4·3 per cent in the finalquarter of 2004.

The information above combined with overall growth forecastsfor the year suggest that another strong year is in prospect forthe labour market. It seems likely, however, that growth in theconstruction sector, which accounted for over a third of all jobs

Quarterly Bulletin 2 2005

30

created last year will slow, given investment forecasts andpossible capacity constraints within the economy reflectingeffective full employment conditions. It is envisaged that thenumbers employed in the services sector will continue toincrease and there may well be some very modest recovery inmanufacturing employment. For 2005 as a whole, employmentis expected to grow by approximately 21⁄4 per cent, slightly inexcess of the anticipated growth in the labour force. As a result,the unemployment rate is forecast to decline to 41⁄4 per cent onaverage in 2005.

Looking ahead to 2006, there is likely to be some fall-off inemployment in the labour intensive construction sector, as theresidential house-building sector slows. This is based on thepresumption that house building levels will decline next year, ascurrent levels of house building are in excess of the economy’smedium-term requirements. While some construction workersmay find alternative employment in the non-residentialconstruction sector, there is likely to be some displacement. Theanticipated slowdown in construction should also lead to a moremodest rate of growth in the labour force as net immigrationmoderates. The services sector is expected to grow strongly in2006 spurred on by higher consumer spending. Overall, totalemployment is forecast to grow by about 2 per cent next year.The number of persons in the labour force is expected to exceed2 million next year, growing by just under 2 per cent, with theunemployment rate remaining at 41⁄4 per cent.

The Public Finances

2004 Outturn

According to Ireland’s March 2005 EDP notification2, the outturnfor the General Government3 Balance in 2004 was a GeneralGovernment Surplus (GGS) of 1·3 per cent of GDP. Thisrepresents an upward revision of 0·4 per cent of GDP relativeto the estimate reported in the 2005 Budget announced at thebeginning of December last. This improved outcome reflected astronger than expected economic performance in 2004 as wellas a number of one-off effects on the revenue side.

2 EMU Member States are required to report their Excessive Deficit Procedure (EDP)notification to the European Commission on a bi-annual basis. The reporting deadlinesoccur on 1st March and 1st September each year. In the March 2005 EDP notification, theDepartment of Finance provided details of the actual 2004 deficit and debt levels, alongsideits projections for 2005.

3 ‘‘General Government’’ refers to Central Government (i.e. Exchequer), Local Government,the Social Insurance Fund and the National Pensions Reserve Fund; the Exchequer refersto Central Government alone. It is noteworthy, however, that differences exist between theaccounting practices of the Exchequer and General Government data. Exchequer data isrecorded on a cash basis, which means that the Exchequer balance can be affected by thesometimes arbitrary advancement or deferral of cash payments whilst General Governmentdata generally follows an accruals-based concept, which limits the scope for inter-yearadvancements and deferrals affecting the General Government Balance.

Quarterly Bulletin 2 2005

31

Table 7. Exchequer Returns at End-March 2005

2004 — 2005 — End-March 2005Outturn Budget Outturn

Estimate

% change % ofyear-on- Budget

Outturn \ million % change \ million year estimate\ million

Current Expenditure— Central Fund Servicesa 3,584 4,012 +11·9 638 −19·9 15·9— Net Voted Expenditureb 27,179 29,997 +10·4 7,126 12·0 23·8

Total 30,763 34,009 +10·6 7,765 8·4 22·8

Current Revenue— Tax revenue 35,581 37,505 +5·4 9,024 12·6 24·1— Non-tax revenuec 802 596 −25·7 105 14·1 17·6

Total 36,383 38,101 +4·7 9,129 12·7 24·0

Current Budget Surplus +5,620 +4,092 +1,365

Capital Budget Deficit −5,587 −7,080 −484

Exchequer Surplus +33 −2,988 +880

General Government Balance +1·3 −0·8(% of GDP)(+: surplus/−: deficit)

a Debt servicing, judicial salaries and pensions and EU Budget contribution.b Government current expenditure on areas such as Social Welfare, Health, etc.c Central Bank surplus income, National Lottery surplus, interest and dividends, etc.

2005 Projections

The forecast General Government Balance for 2005 included inthe March 2005 EDP notification is a deficit of 0·7 per cent ofGDP. This compares with a forecast deficit of 0·8 per cent ofGDP assumed in the 2005 Budget. The EDP figures indicate thatGeneral Government Debt is estimated to decline marginallyfrom 29·9 per cent of GDP at the end of 2004 to 29·5 per centof GDP in 2005.

End-March 2005 Exchequer Returns

The Exchequer Returns for end-March 2005 show an Exchequersurplus of \880 million for the first three months of 2005. Thiscompares with an Exchequer surplus of \272 million in the firstquarter of 2004 and a budgeted deficit of \2,988 million for2005 as a whole. This reflects stronger than anticipated taxrevenue combined with below profile total expenditure levels forthis stage of the year. Table 7 contains the main details ofrevenue and expenditure.

Current Revenue

Total current revenue in the first quarter of 2005 amounted to\9,129 million, an increase of 12·7 per cent compared with thesame period in 2004. Non-tax revenue amounted to \105million; this compares with \92 million at the same time last yearand is broadly in line with expectations. Tax revenue, at \9,024million, is 12·6 per cent higher, year-on-year, and \221 million(or 2·5 per cent) higher than the profile of expected tax revenue

Quarterly Bulletin 2 2005

32

to end-March published at end-January. This overshoot reflectsstronger than expected growth in VAT and Stamp Duty receipts.VAT receipts, which were \139 million ahead of the expectedprofile, accounted for the bulk of this overshoot. This reflectedrelatively strong consumer demand and a continuation of highlevels of activity in the construction sector. Stamp Duty receiptsincreased by 28·9 per cent on the same period last year largelyas a result of the continued buoyancy of the housing market. Inspite of the current favourable labour market conditions, incometax receipts were \12 million lower than their expected profile —Budget Day income tax changes may account for this shortfall.

The overall difference between current revenue and currentexpenditure gave a current budget surplus of \1,365 million inthe first quarter of 2005. This compares with a \942 millioncurrent budget surplus for the same period in 2004 and abudgeted surplus of \4,092 million for 2005 as a whole.

Capital Budget

Exchequer borrowing for capital purposes amounted to \484million at end-March 2005 which compared with \670 millionfor the same period last year and a figure of \7,080 million forthe year as a whole. Net voted capital expenditure amounted to\414 million, \137 million below expected profile. According tothe Department of Finance, timing factors account for some ofthis variation. The carryover of unspent allocations4 from 2004facilitated supplementary capital expenditure in the first quarterof 2005 totalling \131 million. Non-voted capital expenditure,which was broadly in line with expectations, included the firstquarter of the annual one per cent of GNP contribution to theNational Pensions Reserve Fund. Capital receipts amounted to\259 million, which was 24 per cent lower, year-on-year.

Exchequer Financing

As the Exchequer surplus of \880 million in the first three monthsof 2005 was more than double that of the same period last year,net Exchequer borrowing was lower in the first three months ofthis year — net exchequer borrowing in the first quarter of 2005was \1·2 billion, compared with \1·8 billion in the same periodlast year. Table 8, which shows the source and application ofExchequer funds, indicates that Exchequer borrowing waspredominantly short-term in nature — net issuance of commercialpaper amounted to \894 million in the first three months of2005, more than double that for the same period last year.Repayment to ministerial funds amounted to \155 million in thefirst quarter of 2005. This compares with borrowing fromministerial funds to the tune of \102 million in the first three

4 Under the five year multi-annual envelope scheme announced in the 2004 Budget, unspentcapital allocations, up to a maximum of 10 per cent, can be carried over to the next year.

Quarterly Bulletin 2 2005

33

Table 8. Source and Application of Funds

\ million January to January toMarch 2004 March 2005

1. Borrowing (−)/repayments (+): −1,799 −1,165Irish Government bonds listed on the Irish Stock Exchange −1,370 −133Other Irish Government public bond issues 66 0EIB loans 1 0Medium-Term Notes 0 201Private Placements 0 0National saving schemes −105 −111Commercial paper −415 −894Miscellaneous debt 126 −382Borrowing from ministerial funds −102 155

2. Increase (+)/decrease (−) in Exchequer deposits and other balances: 2,071 2,045Increase (+)/decrease (−) in Exchequer balance 2,011 1,872Increase (+)/decrease (−) in other bank deposits 0 270Increase (+)/decrease (−) in other balances 60 −97

Exchequer Surplus (1+2): 272 880

months of 2004. Net issues of Irish Government bonds listed inthe Irish Stock Exchange amounted to \133 million in the firstquarter of 2005 compared with \1·4 billion for the same periodin 2004. Net Exchequer borrowing combined with the Exchequersurplus resulted in an increase in Exchequer deposits and otherbalances. This increase amounted to \2 billion in the first quarterof 2005.

Conclusion

The end-March Exchequer Returns indicate relatively favourabletrends in both revenue and expenditure compared to the targetsset in the 2005 Budget. Tax revenue during the first quarter of2005 was \221 million above its expected profile published atend-January while total expenditure levels have been runningbelow profile for this stage of the year. This favourable outturnon the revenue side results from strong economic activity, whichhas had positive implications for cyclically sensitive revenuestreams — in particular, VAT. According to the Department ofFinance, timing issues account for the below profile expenditureoutcome.

If these early positive trends are sustained for the remainder of2005, public finance targets will be comfortably achieved thisyear. One factor, which may affect this favourable position,however, is the cost to the Exchequer of reimbursing recipientsof long-term public care for the elderly. On the other hand, thepublic finances may benefit by more than expected from theone-off boost to tax receipts arising from the RevenueCommissioner‘s investigation into undisclosed tax liabilitiesrelating to funds invested in life assurance products. Thus, whilefirst quarter Exchequer Returns data augur well for publicfinances, it is too early at this stage to make a definitivejudgement on the need for a revision of 2005 projections.

Quarterly Bulletin 2 2005

34

Financial Sector Developments

Overview

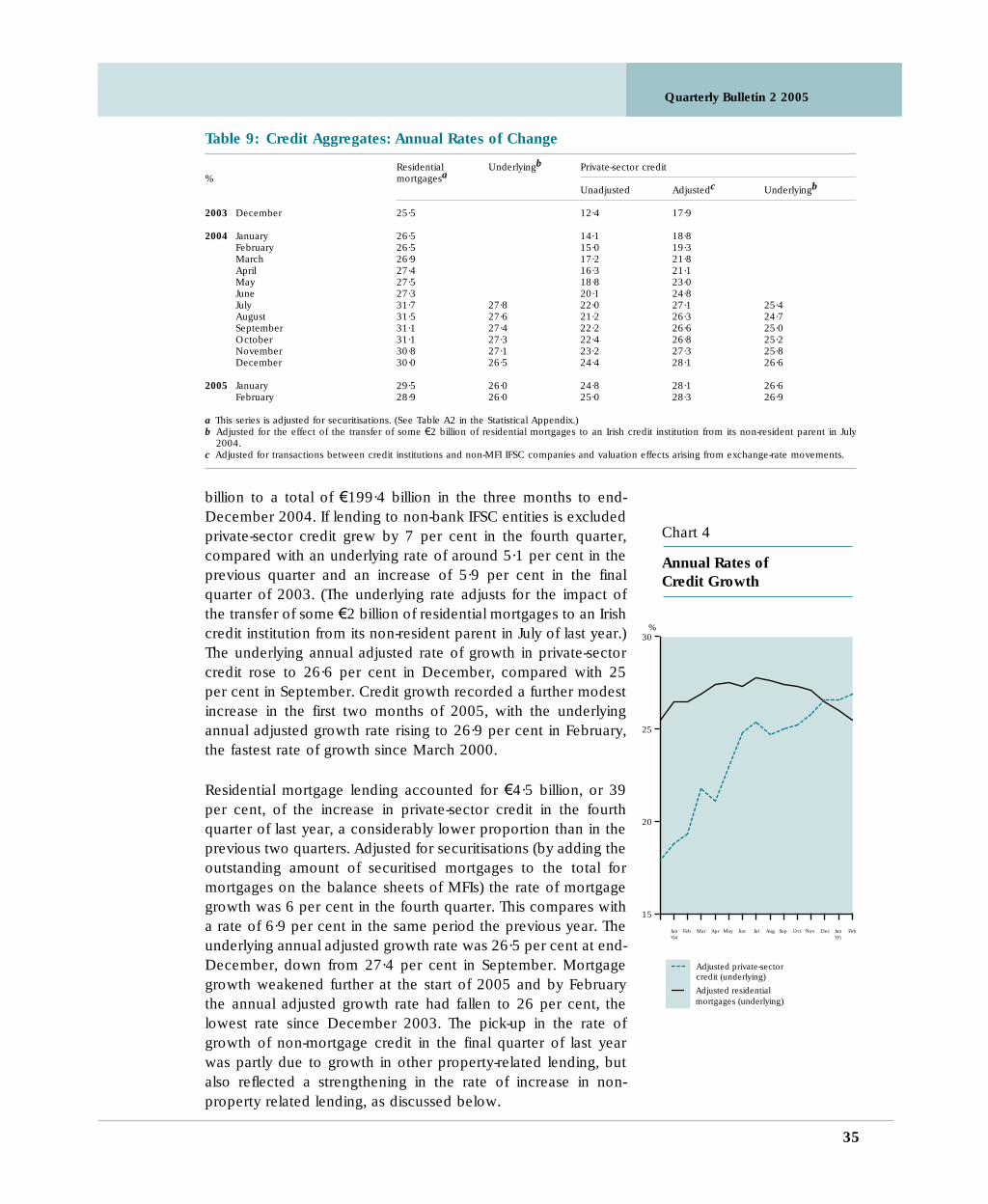

The underlying annual adjusted rate of private-sector creditgrowth5 has been on a steadily upward trend since the middle of2003, although the rate of acceleration appears to have slowedsomewhat in recent months. Credit growth increased from anannual rate of under 18 per cent at the end of 2003 to 26·6 percent at the end of last year. The growth rate rose slightly to 26·9per cent in February 2005, the fastest rate of credit growth forfive years. Property-related lending continues to dominateprivate-sector credit growth and the largest component of thisis residential mortgage lending. However the latter item, whilecontinuing to grow strongly, has shown signs of decelerating.The underlying annual adjusted mortgage growth rate fell steadilyfrom 27·8 per cent in July 2004 to 26 per cent in February ofthis year, the lowest level since the end of 2003. However, otherproperty-related lending strengthened in the final quarter of lastyear. There was also a pick-up in non-property related lendingwhich was spread across a number of sectors with the largestcontributor being non-housing related lending to the personalsector.

The Irish results for the euro area bank lending survey show thatcredit standards for loans to enterprises were slightly tighter inthe fourth quarter of last year and demand for loans and creditlines by enterprises was reported as increasing slightly. Demandfor credit by households for house purchase was also reportedto have increased slightly in the three months to end-December.The expectation was that demand for credit by both enterprisesand households would increase modestly in the first quarter of2005.