Embed Size (px)

Citation preview

8/6/2019 Commercial Banking II

http://slidepdf.com/reader/full/commercial-banking-ii 1/24

Commercial BankingCommercial Banking --IIIIInstitute of Public EnterpriseInstitute of Public Enterprise

July,2010July,2010HyderabadHyderabad

8/6/2019 Commercial Banking II

http://slidepdf.com/reader/full/commercial-banking-ii 2/24

Bank NationalizationBank Nationalization

Why Nationalization?Why Nationalization?

Concentration of Economic PowerConcentration of Economic Power in few private handsin few private hands

Branch Expansion ( Rural BranchesBranch Expansion ( Rural Branches ±± Mass Banking)Mass Banking)

Credit Allocation ( Not Profit Motive)Credit Allocation ( Not Profit Motive) ±± neglect of neglect of agricultureagriculture

Prevent MalpracticesPrevent Malpractices

Change in attitude & outlook was neededChange in attitude & outlook was needed

When Nationalization ?When Nationalization ?

19691969 ±± applicable in Feb 1970applicable in Feb 1970

19801980 ±± April 1980April 1980

8/6/2019 Commercial Banking II

http://slidepdf.com/reader/full/commercial-banking-ii 3/24

Reserve Bank of IndiaReserve Bank of India

Custodian of Foreign Exchange and other ReservesCustodian of Foreign Exchange and other Reserves

Maintains Currency ChestsMaintains Currency Chests ±± Print NotesPrint Notes

Bankers¶ BankBankers¶ Bank

Controller of CreditController of Credit ±± Selective Credit controlSelective Credit control

Banker to GovernmentBanker to Government ±± Treasury & other Debt ManagementTreasury & other Debt Management Regulatory FunctionRegulatory Function ±± Commercial Banks, Money Market, ForeignCommercial Banks, Money Market, Foreign

Currency Market, NBFCsCurrency Market, NBFCs

Supervisory & Control of Banks & NBFCsSupervisory & Control of Banks & NBFCs --Collects information ,Collects information ,Conducts Inspection / Audit, Issues operational guidelines,Conducts Inspection / Audit, Issues operational guidelines,permission for Branch Expansion, appointment of executivespermission for Branch Expansion, appointment of executives

Control of interest , inflation and exchange rates in the economyControl of interest , inflation and exchange rates in the economy(Zero risk rates, Control of credit & market liquidity / money(Zero risk rates, Control of credit & market liquidity / moneysupply, buying and selling of currency in the market)supply, buying and selling of currency in the market)

8/6/2019 Commercial Banking II

http://slidepdf.com/reader/full/commercial-banking-ii 4/24

Credit ControlCredit Control

Variation in Bank RateVariation in Bank Rate ±± The rate at which RBI discountsThe rate at which RBI discountseligible bills of exchanges of commercial bankseligible bills of exchanges of commercial banks

Variation in CRR & SLR ( Cash Reserve Ratio & StatutoryVariation in CRR & SLR ( Cash Reserve Ratio & StatutoryLiquidity Ratio)Liquidity Ratio)

Open Market Operation ( Buying and selling of Central andOpen Market Operation ( Buying and selling of Central andState Government Securities to infuse or flush out liquidityState Government Securities to infuse or flush out liquidityfrom the market)from the market)

Selective Credit Control ( Prevent hoarding of essentialSelective Credit Control ( Prevent hoarding of essentialcommodities and speculative activitiescommodities and speculative activities

8/6/2019 Commercial Banking II

http://slidepdf.com/reader/full/commercial-banking-ii 5/24

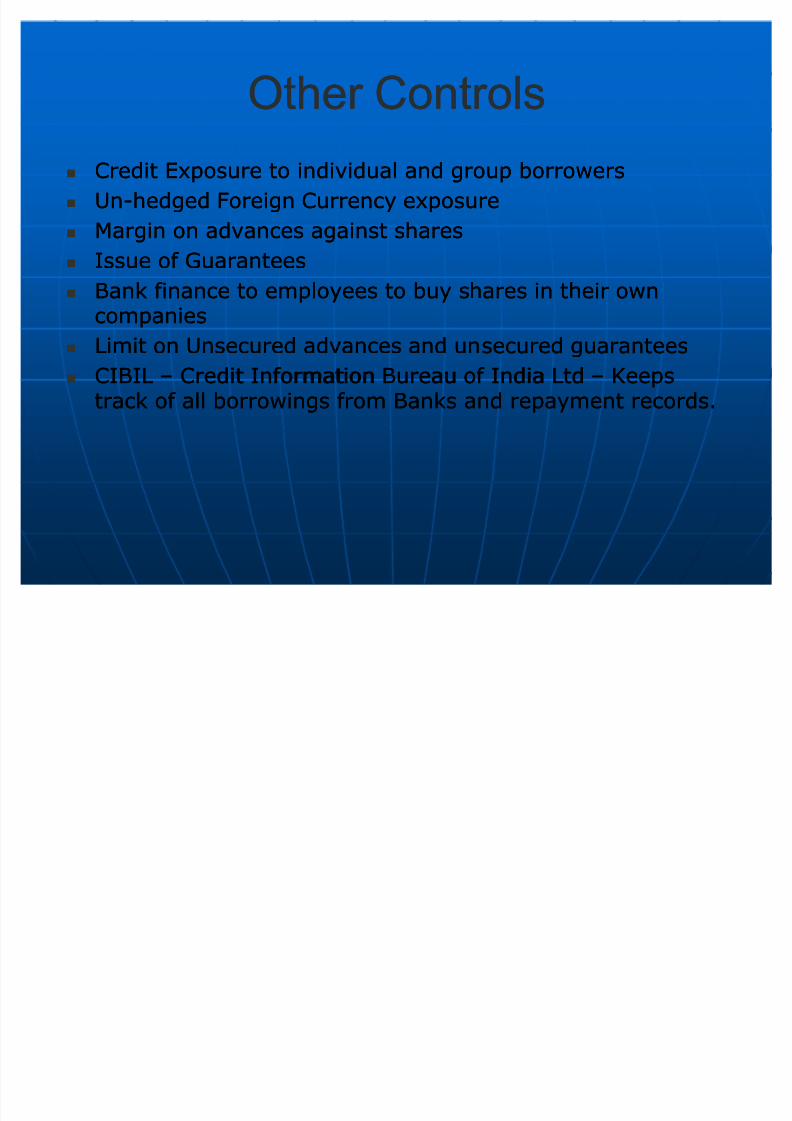

Other ControlsOther Controls

Credit Exposure to individual and group borrowersCredit Exposure to individual and group borrowers

UnUn--hedged Foreign Currency exposurehedged Foreign Currency exposure

Margin on advances against sharesMargin on advances against shares

Issue of GuaranteesIssue of Guarantees

Bank finance to employees to buy shares in their ownBank finance to employees to buy shares in their owncompaniescompanies

Limit on Unsecured advances and unsecured guaranteesLimit on Unsecured advances and unsecured guarantees

CIBILCIBIL ±± Credit Information Bureau of India LtdCredit Information Bureau of India Ltd ±± KeepsKeepstrack of all borrowings from Banks and repayment records.track of all borrowings from Banks and repayment records.

8/6/2019 Commercial Banking II

http://slidepdf.com/reader/full/commercial-banking-ii 6/24

Related DefinitionsRelated Definitions

Repo & Reverse Repo RatesRepo & Reverse Repo Rates ±± RBI issues securities toRBI issues securities toborrow funds and repurchases securities on a future date atborrow funds and repurchases securities on a future date ata given rate ( known as reverse repo rate). Repo rate is thea given rate ( known as reverse repo rate). Repo rate is therate at which RBI lends money to bank by buying outrate at which RBI lends money to bank by buying out

securities to sell them on a future date to the banks at asecurities to sell them on a future date to the banks at agiven price. These are short term rates to control shortgiven price. These are short term rates to control shortterm market liquidity. RBI always borrows cheap and lendsterm market liquidity. RBI always borrows cheap and lendshigh. So reverse Repo rates are lower than repo rates.high. So reverse Repo rates are lower than repo rates.Reverse repo rate is a key or bench mark overnight rate.Reverse repo rate is a key or bench mark overnight rate.

CRR and SLR are related to net banks demand and timeCRR and SLR are related to net banks demand and timeliabilities ( Fortnightly). CRR is kept with RBI. SLR is theliabilities ( Fortnightly). CRR is kept with RBI. SLR is theamount of investment ( certain % of Net Demand and Timeamount of investment ( certain % of Net Demand and TimeLiabilities) banks will keep in approved securities like TLiabilities) banks will keep in approved securities like T--BillsBillsand dated securities etc.and dated securities etc.

8/6/2019 Commercial Banking II

http://slidepdf.com/reader/full/commercial-banking-ii 7/24

Related DefinitionsRelated Definitions

M1 = Narrow Money, M3 = Broad MoneyM1 = Narrow Money, M3 = Broad Money

M1 = Net Demand Deposit of Banks ( CA + Certain % of M1 = Net Demand Deposit of Banks ( CA + Certain % of SB) +Other deposits with RBI +Currency Notes & CoinsSB) +Other deposits with RBI +Currency Notes & Coinsheld by publicheld by public

M3= M1 + Net Time Deposit with Banks ( including balanceM3= M1 + Net Time Deposit with Banks ( including balanceportion of SB)portion of SB)

M1 and M3 are measures of money supplyM1 and M3 are measures of money supply

8/6/2019 Commercial Banking II

http://slidepdf.com/reader/full/commercial-banking-ii 8/24

Banking developmentsBanking developments

Any where Banking / Anytime BankingAny where Banking / Anytime Banking ±± ATMS (AutomatedATMS (AutomatedTeller MachinesTeller Machines ±± PINPIN ±± Personal Identification Number)Personal Identification Number)

(Interior ATMS(Interior ATMS±± within the branch /Exterior ATMswithin the branch /Exterior ATMs-- outsideoutsidethe branch , Online ATMsthe branch , Online ATMs-- connected to bank¶s hostconnected to bank¶s host

computer / Offline ATMscomputer / Offline ATMs±± not connected to bank¶s hostnot connected to bank¶s hostcomputer)computer)

Shared ATMsShared ATMs ±± Can draw from any bank ATMs ( Visa,Can draw from any bank ATMs ( Visa,Master Card , Amex )Master Card , Amex )

EE-- BankingBanking ±± Electronic Banking / Internet BankingElectronic Banking / Internet Banking -- IPINIPIN

MM--BankingBanking-- Mobile BankingMobile Banking -- TPINTPIN Debit Cards, Credit Cards, Smart Cards ( with an embeddedDebit Cards, Credit Cards, Smart Cards ( with an embedded

integrated circuitintegrated circuit ±±IC Chip. The IC contains memory, mayIC Chip. The IC contains memory, maycontain a processor and communicates with the externalcontain a processor and communicates with the externalworld through contacts on the surface of the card)world through contacts on the surface of the card)

Electronic Fund TransferElectronic Fund Transfer

8/6/2019 Commercial Banking II

http://slidepdf.com/reader/full/commercial-banking-ii 9/24

ATMs ATMs

Advantages of ATMsAdvantages of ATMs -- CustomersCustomers

24 hour 7 days a week, any where banking24 hour 7 days a week, any where bankingfacility, efficient and quick service, privacy infacility, efficient and quick service, privacy in

transaction, free from errorstransaction, free from errors Advantages For BankAdvantages For Bank ±± No need to extendNo need to extend

working hours, no crowding of branches,working hours, no crowding of branches,reduction in operational cost as it reduces thereduction in operational cost as it reduces theneed of extensive branch network, human errorneed of extensive branch network, human erroreliminated, increased market penetration,eliminated, increased market penetration,employees can be spared for more analyticalemployees can be spared for more analyticalworkwork

8/6/2019 Commercial Banking II

http://slidepdf.com/reader/full/commercial-banking-ii 10/24

ATMs ATMs

Advantages of ATMsAdvantages of ATMs -- CustomersCustomers

24 hour 7 days a week, any where banking24 hour 7 days a week, any where bankingfacility, efficient and quick service, privacy infacility, efficient and quick service, privacy in

transaction, free from errorstransaction, free from errors Advantages For BankAdvantages For Bank ±± No need to extendNo need to extend

working hours, no crowding of branches,working hours, no crowding of branches,reduction in operational cost as it reduces thereduction in operational cost as it reduces theneed of extensive branch network, human errorneed of extensive branch network, human erroreliminated, increased market penetration,eliminated, increased market penetration,employees can be spared for more analyticalemployees can be spared for more analyticalworkwork

8/6/2019 Commercial Banking II

http://slidepdf.com/reader/full/commercial-banking-ii 11/24

Debit Card, Credit Card, Smart Card, Silver, Gold &Debit Card, Credit Card, Smart Card, Silver, Gold &

Platinum CardPlatinum Card

Debit CardDebit Card

Credit CardCredit Card

Smart CardSmart Card

Silver CardSilver Card Gold CardGold Card

Platinum CardPlatinum Card

Petrol Card / Airlines Card/ Diners Club CardPetrol Card / Airlines Card/ Diners Club Card

Visa / Masters / Amex CardsVisa / Masters / Amex Cards

CPPCPP ±±Card Protection Plan www.cppindia.comCard Protection Plan www.cppindia.com

8/6/2019 Commercial Banking II

http://slidepdf.com/reader/full/commercial-banking-ii 12/24

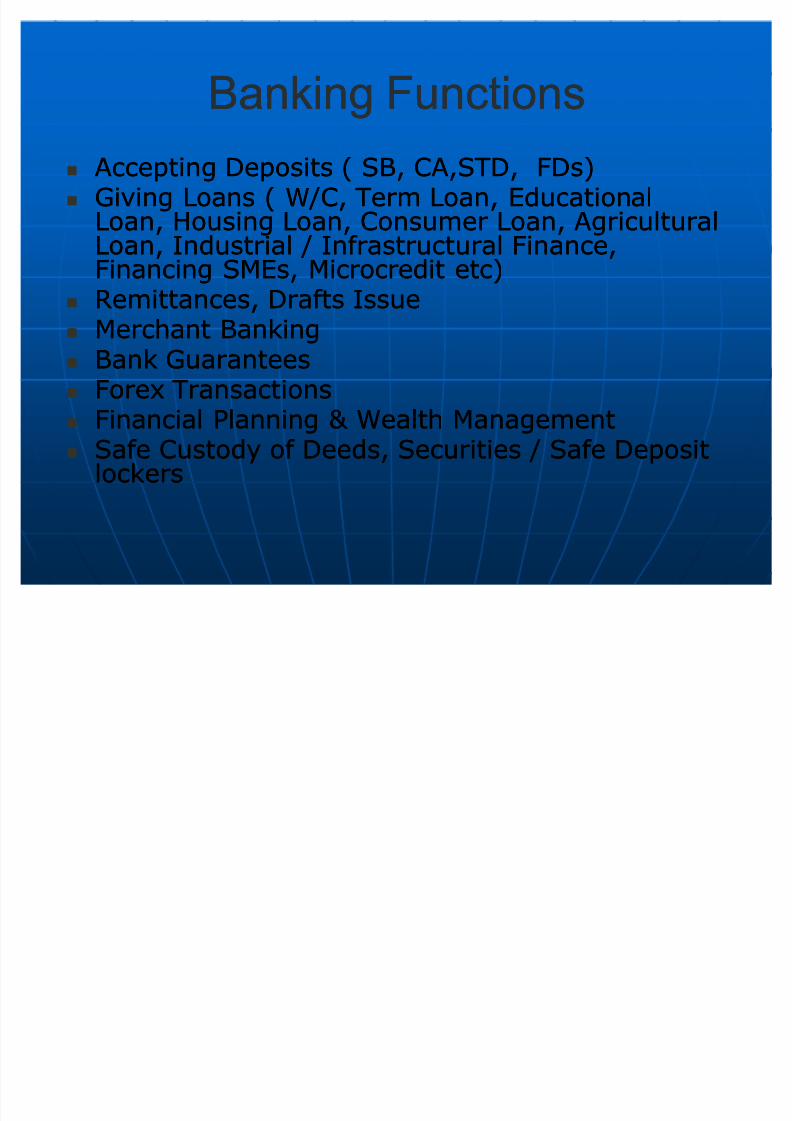

Banking FunctionsBanking Functions

Accepting Deposits ( SB, CA,STD, FDs)Accepting Deposits ( SB, CA,STD, FDs) Giving Loans ( W /C, Term Loan, EducationalGiving Loans ( W /C, Term Loan, Educational

Loan, Housing Loan, Consumer Loan, AgriculturalLoan, Housing Loan, Consumer Loan, AgriculturalLoan, Industrial / Infrastructural Finance,Loan, Industrial / Infrastructural Finance,

Financing SMEs, Microcredit etc)Financing SMEs, Microcredit etc) Remittances, Drafts IssueRemittances, Drafts Issue Merchant BankingMerchant Banking Bank GuaranteesBank Guarantees Forex TransactionsForex Transactions Financial Planning & Wealth ManagementFinancial Planning & Wealth Management Safe Custody of Deeds, Securities / Safe DepositSafe Custody of Deeds, Securities / Safe Deposit

lockerslockers

8/6/2019 Commercial Banking II

http://slidepdf.com/reader/full/commercial-banking-ii 13/24

Banking FunctionsBanking Functions

Credit Card, Debit CardCredit Card, Debit Card

Bank AssuranceBank Assurance

Sale of Mutual Fund / Insurance ProductsSale of Mutual Fund / Insurance Products

Tax AdvisoryTax Advisory Infrastructure Finance and AdvisoryInfrastructure Finance and Advisory

8/6/2019 Commercial Banking II

http://slidepdf.com/reader/full/commercial-banking-ii 14/24

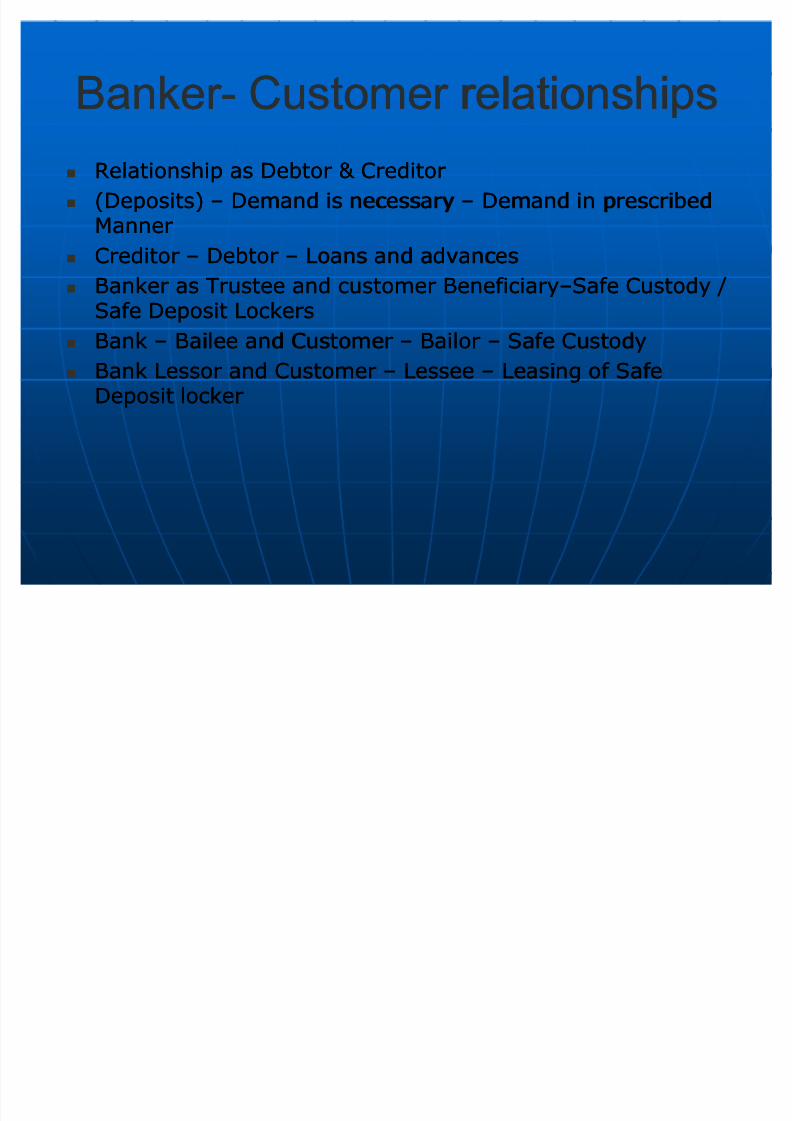

Banker Banker-- Customer relationshipsCustomer relationships

Relationship as Debtor & CreditorRelationship as Debtor & Creditor

(Deposits)(Deposits) ±± Demand is necessaryDemand is necessary ±± Demand in prescribedDemand in prescribedMannerManner

CreditorCreditor ±± DebtorDebtor ±± Loans and advancesLoans and advances

Banker as Trustee and customer BeneficiaryBanker as Trustee and customer Beneficiary±±Safe Custody /Safe Custody /Safe Deposit LockersSafe Deposit Lockers

BankBank ±± Bailee and CustomerBailee and Customer ±± BailorBailor ±± Safe CustodySafe Custody

Bank Lessor and CustomerBank Lessor and Customer ±± LesseeLessee ±± Leasing of SafeLeasing of SafeDeposit lockerDeposit locker

8/6/2019 Commercial Banking II

http://slidepdf.com/reader/full/commercial-banking-ii 15/24

Banker Banker-- Customer RelationshipsCustomer Relationships

Banker as an agentBanker as an agent ±± remittances, Clearing , Collection of remittances, Clearing , Collection of ChequesCheques

Bank is Indemnified and Customer is IndemnifierBank is Indemnified and Customer is Indemnifier ±± Issue of Issue of Duplicate against lost draftDuplicate against lost draft

Know Your Customer (KYC) NormsKnow Your Customer (KYC) Norms ±± Identity and addressIdentity and addressproof To monitor transactions of suspicious natureproof To monitor transactions of suspicious nature

8/6/2019 Commercial Banking II

http://slidepdf.com/reader/full/commercial-banking-ii 16/24

Obligations of a Banker Obligations of a Banker

Obligation to Pay ChequesObligation to Pay Cheques ±± Fund available,Fund available,Cheque properly drawn, valid signature, not staleCheque properly drawn, valid signature, not staleor post dated, not a crossed cheque, receivedor post dated, not a crossed cheque, receivedafter stop payment or death of customer orafter stop payment or death of customer orattachment / garnishee order is issuedattachment / garnishee order is issued

Obligation to Maintain Secrecy of AccountObligation to Maintain Secrecy of Account ±±unless required under law, under express orunless required under law, under express orimplied consent of the customer or disclosure isimplied consent of the customer or disclosure is

required in public / national interest, to a fellowrequired in public / national interest, to a fellowbankerbanker

8/6/2019 Commercial Banking II

http://slidepdf.com/reader/full/commercial-banking-ii 17/24

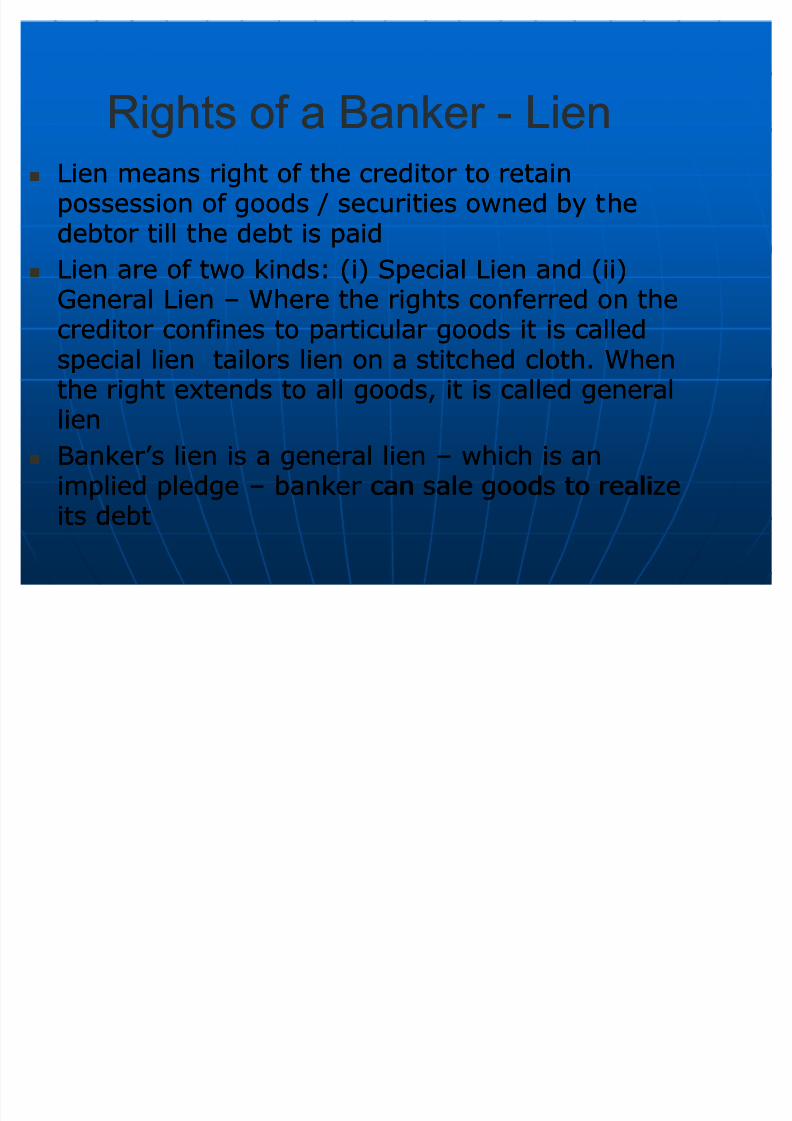

Rights of a Banker Rights of a Banker -- LienLien

Lien means right of the creditor to retainLien means right of the creditor to retainpossession of goods / securities owned by thepossession of goods / securities owned by thedebtor till the debt is paiddebtor till the debt is paid

Lien are of two kinds: (i) Special Lien and (ii)Lien are of two kinds: (i) Special Lien and (ii)General LienGeneral Lien ±± Where the rights conferred on theWhere the rights conferred on thecreditor confines to particular goods it is calledcreditor confines to particular goods it is calledspecial lien tailors lien on a stitched cloth. Whenspecial lien tailors lien on a stitched cloth. Whenthe right extends to all goods, it is called generalthe right extends to all goods, it is called general

lienlien Banker¶s lien is a general lienBanker¶s lien is a general lien ±± which is anwhich is an

implied pledgeimplied pledge ±± banker can sale goods to realizebanker can sale goods to realizeits debtits debt

8/6/2019 Commercial Banking II

http://slidepdf.com/reader/full/commercial-banking-ii 18/24

Right to SetRight to Set--off & Appropriationoff & Appropriation When the bank transfers a part of balance from oneWhen the bank transfers a part of balance from one

account to another of the same customer, both accountsaccount to another of the same customer, both accountsoperated by him in the same capacity, it is setoperated by him in the same capacity, it is set--off off

When there are several debt accounts of the debtor, theWhen there are several debt accounts of the debtor, the

right of appropriation of any credits of any such account isright of appropriation of any credits of any such account iswith the debtor. In case the debtor fails to give instruction,with the debtor. In case the debtor fails to give instruction,the right of appropriation is with the creditor / bankerthe right of appropriation is with the creditor / banker

In partnership account if a partner dies, the firms accountIn partnership account if a partner dies, the firms accountshould be discontinued and the remaining partners shouldshould be discontinued and the remaining partners should

open a separate account for their furt

her transactionsopen a separate account for t

heir furt

her transactions

Claytons RuleClaytons Rule ±±Credit entries adjust debts in chronologicalCredit entries adjust debts in chronologicalorderorder ±± partner / guarantor¶s death / insolvencypartner / guarantor¶s death / insolvency

8/6/2019 Commercial Banking II

http://slidepdf.com/reader/full/commercial-banking-ii 19/24

Right of SetRight of Set--off off

The accounts should be of same name and sameThe accounts should be of same name and samerightright

Sole proprietor and individual account can beSole proprietor and individual account can becombinedcombined

Unless nothing is agreed to the contrary, aUnless nothing is agreed to the contrary, apartners individual account can be setpartners individual account can be set--off againstoff againstdebt of partnership firm as partners are jointlydebt of partnership firm as partners are jointlyand severally liable for the debts taken by theand severally liable for the debts taken by thefirmfirm

Right to set off can be applied for debts due butRight to set off can be applied for debts due butnot future or contingent debtsnot future or contingent debts

Debts should be a sum certain absolute beforeDebts should be a sum certain absolute beforeexercising the right to setexercising the right to set--off off

8/6/2019 Commercial Banking II

http://slidepdf.com/reader/full/commercial-banking-ii 20/24

Right to SetRight to Set--off ( Continued)off ( Continued)

It is banker¶s discretion whether to applyIt is banker¶s discretion whether to applyright to setright to set--off or notoff or not

Right to setRight to set--off should be applied beforeoff should be applied before

the garnishee order becomes effective.the garnishee order becomes effective.After it becomes effective, the right canAfter it becomes effective, the right cannot be exercised.not be exercised.

Banker must obtain a letter to exerciseBanker must obtain a letter to exercise

right to setright to set--off and lien at the time of off and lien at the time of granting a loan.granting a loan.

Banker can exercise this right withoutBanker can exercise this right withoutgiving any notice.giving any notice.

8/6/2019 Commercial Banking II

http://slidepdf.com/reader/full/commercial-banking-ii 21/24

Automatic Right to Set Automatic Right to Set--off in certainoff in certain

casescases

On death of customer closing theOn death of customer closing theaccount by credit of the debt accountaccount by credit of the debt account

When the customer becomes insolventWhen the customer becomes insolventor lunaticor lunatic

When a garnishee order is issued onWhen a garnishee order is issued onthe customer¶s account by the courtthe customer¶s account by the court

When a notice of assignment of creditWhen a notice of assignment of creditbalance to some one else has beenbalance to some one else has beengiven by the customer to the bankergiven by the customer to the banker

8/6/2019 Commercial Banking II

http://slidepdf.com/reader/full/commercial-banking-ii 22/24

Right of AppropriationRight of Appropriation--Indian LawIndian Law

& Clayton¶s Rule& Clayton¶s Rule If the debtor does not indicate / intimateIf the debtor does not indicate / intimate

the right of appropriation is vested with the right of appropriation is vested with the creditorthe creditor

Creditor may apply at his discretion to anyCreditor may apply at his discretion to anylawful debt actually due and payable tolawful debt actually due and payable tohim from the debtorhim from the debtor

Where neither party makes any indicationWhere neither party makes any indicationregarding appropriation, the paymentregarding appropriation, the payment

shall be applied in discharge of the debt inshall be applied in discharge of the debt inorder of time.order of time. If the debts are of equal standing (date) ,If the debts are of equal standing (date) ,

the payment shall be applied in dischargethe payment shall be applied in dischargeof each proportionatelyof each proportionately

8/6/2019 Commercial Banking II

http://slidepdf.com/reader/full/commercial-banking-ii 23/24

Rights of a Banker Rights of a Banker ± ± Clayton¶s RuleClayton¶s Rule

In case of a debt due with interest, any paymentIn case of a debt due with interest, any paymentmade by the debtor in first instance to be appliedmade by the debtor in first instance to be appliedtowards satisfaction of interest and there aftertowards satisfaction of interest and there afterprincipal unless there is an agreement to theprincipal unless there is an agreement to thecontrarycontrary

If the customer has two or more accountsIf the customer has two or more accountsClayton's rule would not apply, however right toClayton's rule would not apply, however right tosetset--off would be applicableoff would be applicable

Clayton¶s rule is applicable to running currentClayton¶s rule is applicable to running currentaccount or cash credit account only and does notaccount or cash credit account only and does notapply to FD and SB Accountsapply to FD and SB Accounts

8/6/2019 Commercial Banking II

http://slidepdf.com/reader/full/commercial-banking-ii 24/24

Special Type of CustomersSpecial Type of Customers

MinorMinor

Joint AccountJoint Account

HUFHUF PartnershipPartnership

Limited CompaniesLimited Companies

TrustsTrusts Clubs & SocietiesClubs & Societies

Government & Public BodiesGovernment & Public Bodies

OthersOthers

![Modern commercial banking []](https://img.pdfslide.net/doc/110x75/55a494801a28ab081b8b4639/modern-commercial-banking-wwwbconnect24com.jpg)

![Commercial Banking[1]](https://img.pdfslide.net/doc/110x75/577d348f1a28ab3a6b8e528e/commercial-banking1.jpg)