Embed Size (px)

Citation preview

www.woodmac.com

Delivering commercial insight

Commercial Drivers of the International Oil Terminal Industry

Ben HoltVice President, Downstream ConsultingWood Mackenzie, London

Tank Storage Istanbul Conference

November 2011

www.woodmac.com

© Wood Mackenzie 2

Delivering commercial insight

1 Crude Oil Outlook

Atlantic Basin Refining and Products

Agenda

2

Oil Infrastructure Developments 3

www.woodmac.com

© Wood Mackenzie 3

Delivering commercial insight

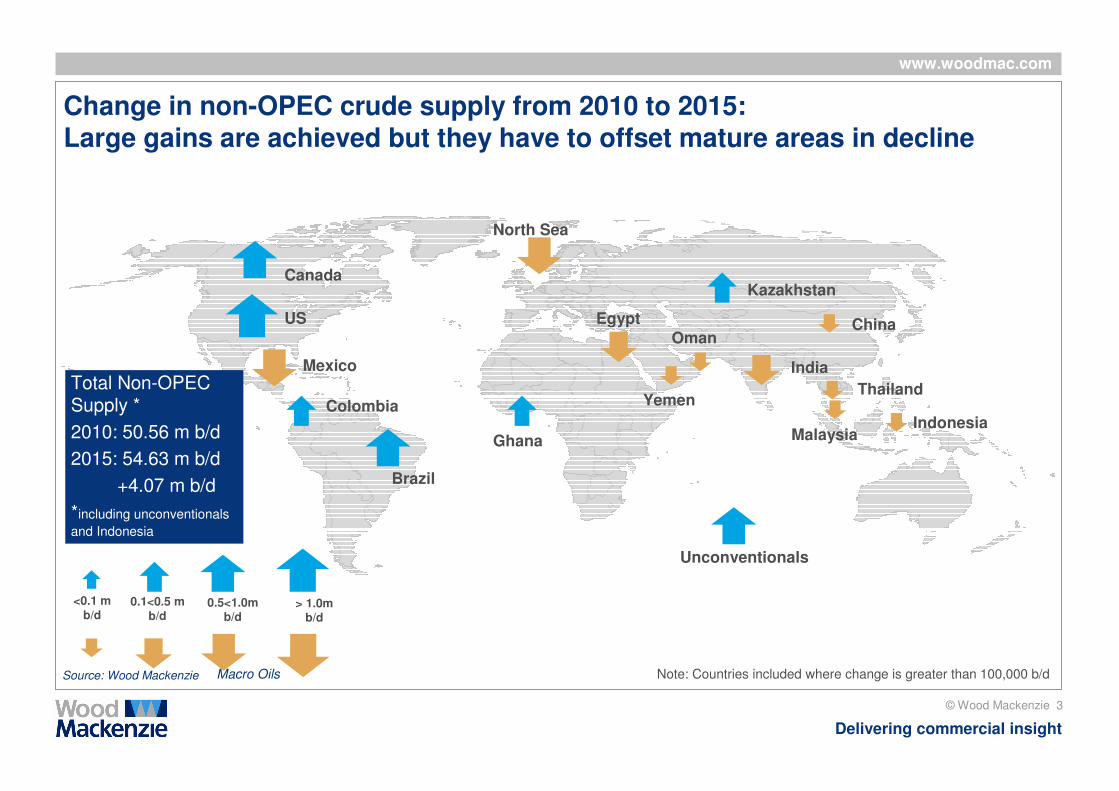

Canada

US

Mexico

North Sea

Brazil

India

Ghana

Kazakhstan

Total Non-OPEC Supply *

2010: 50.56 m b/d

2015: 54.63 m b/d

+4.07 m b/d

*including unconventionals

and Indonesia

Note: Countries included where change is greater than 100,000 b/d

0.1<0.5 m b/d

0.5<1.0m b/d

> 1.0m b/d

Unconventionals

Change in non-OPEC crude supply from 2010 to 2015: Large gains are achieved but they have to offset mature areas in decline

Source: Wood Mackenzie

Colombia

<0.1 m b/d

China

Yemen

Oman

Thailand

MalaysiaIndonesia

Egypt

Macro Oils

www.woodmac.com

© Wood Mackenzie 4

Delivering commercial insight

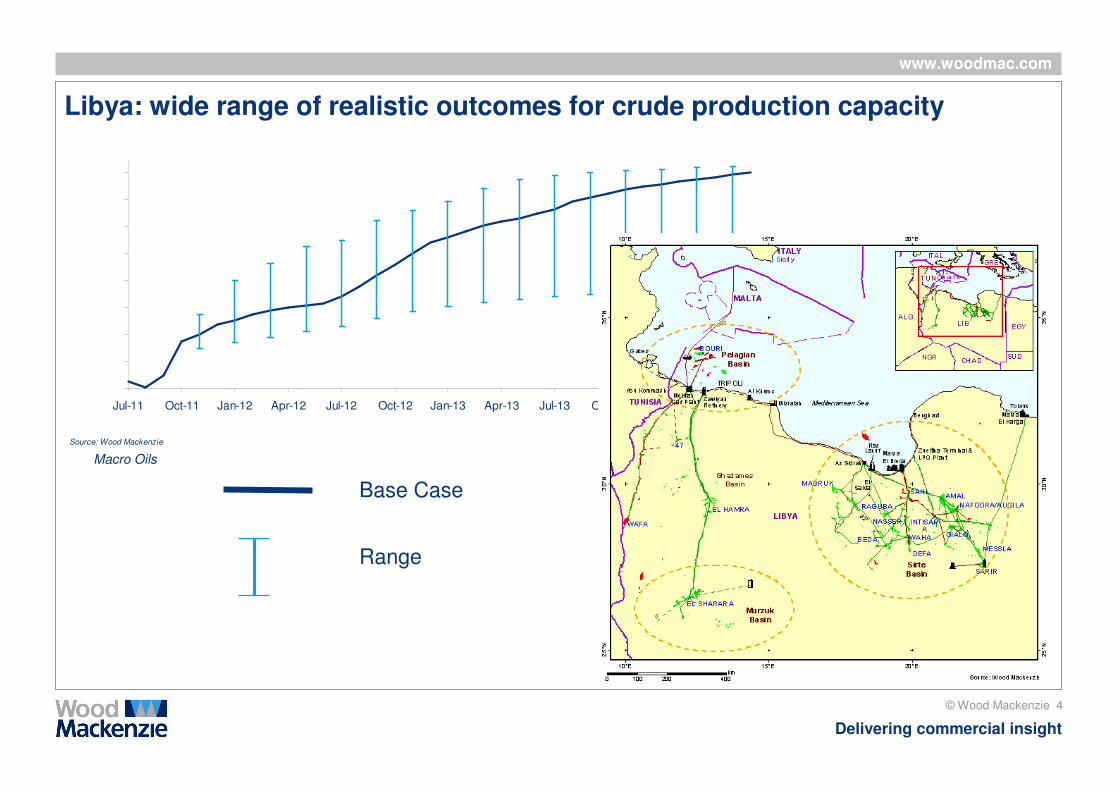

Libya: wide range of realistic outcomes for crude production capacity

Source: Wood Mackenzie

0

200

400

600

800

1,000

1,200

1,400

1,600

Jul-11 Oct-11 Jan-12 Apr-12 Jul-12 Oct-12 Jan-13 Apr-13 Jul-13 Oct-13 Jan-14 Apr-14

00

0 'b

/d

Base case

Base Case

Range

Macro Oils

www.woodmac.com

© Wood Mackenzie 5

Delivering commercial insight

-10

-5

0

5

10

15

20

25

30

Ja

n-0

8

Ap

r-0

8

Ju

l-0

8

Oc

t-0

8

Ja

n-0

9

Ap

r-0

9

Ju

l-0

9

Oc

t-0

9

Ja

n-1

0

Ap

r-1

0

Ju

l-1

0

Oc

t-1

0

Ja

n-1

1

Ap

r-1

1

Ju

l-1

1

$/bbl

Brent - WTI LLS - WTI Brent-LLS

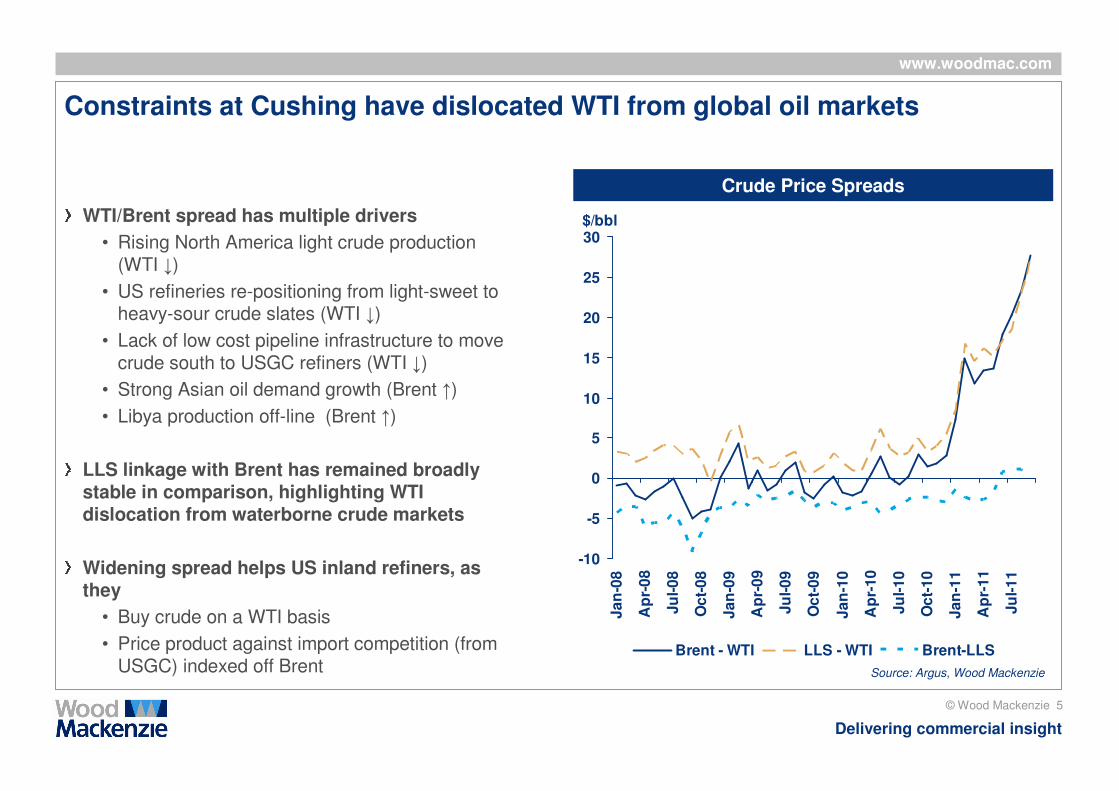

Constraints at Cushing have dislocated WTI from global oil markets

WTI/Brent spread has multiple drivers

• Rising North America light crude production (WTI ↓)

• US refineries re-positioning from light-sweet to heavy-sour crude slates (WTI ↓)

• Lack of low cost pipeline infrastructure to move crude south to USGC refiners (WTI ↓)

• Strong Asian oil demand growth (Brent ↑)

• Libya production off-line (Brent ↑)

LLS linkage with Brent has remained broadly stable in comparison, highlighting WTI dislocation from waterborne crude markets

Widening spread helps US inland refiners, as they

• Buy crude on a WTI basis

• Price product against import competition (from USGC) indexed off Brent

Crude Price Spreads

Source: Argus, Wood Mackenzie

www.woodmac.com

© Wood Mackenzie 6

Delivering commercial insight

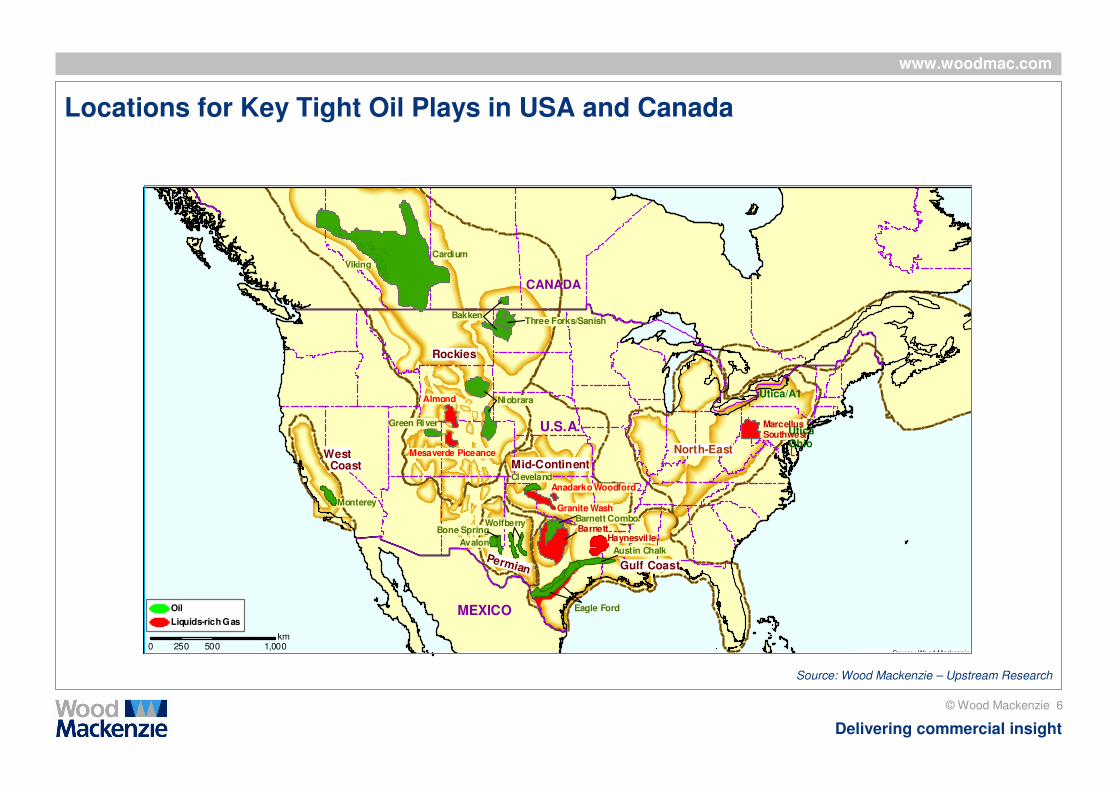

CANADA

MEXICO

Permian Gulf Coast

West

Rockies

Mid-Continent

North-East

Bakken

Niobrara

Eagle Ford

Haynesvil le

Monterey

U.S.A.

Bone Spring

Austin Chalk

Marcellus Southwest

Wolfberry

ClevelandCoast

Avalon

Three Forks/Sanish

CardiumViking

Barnett Combo

Green River

Almond

Barnett

Granite Wash

Anadarko Woodford

Mesaverde Piceance

0 500 1,000250km

Source: Wood Mackenz ie

Oil

Liquids-rich Gas

Utica Ohio

Locations for Key Tight Oil Plays in USA and Canada

Source: Wood Mackenzie – Upstream Research

Utica/A1

www.woodmac.com

© Wood Mackenzie 7

Delivering commercial insight

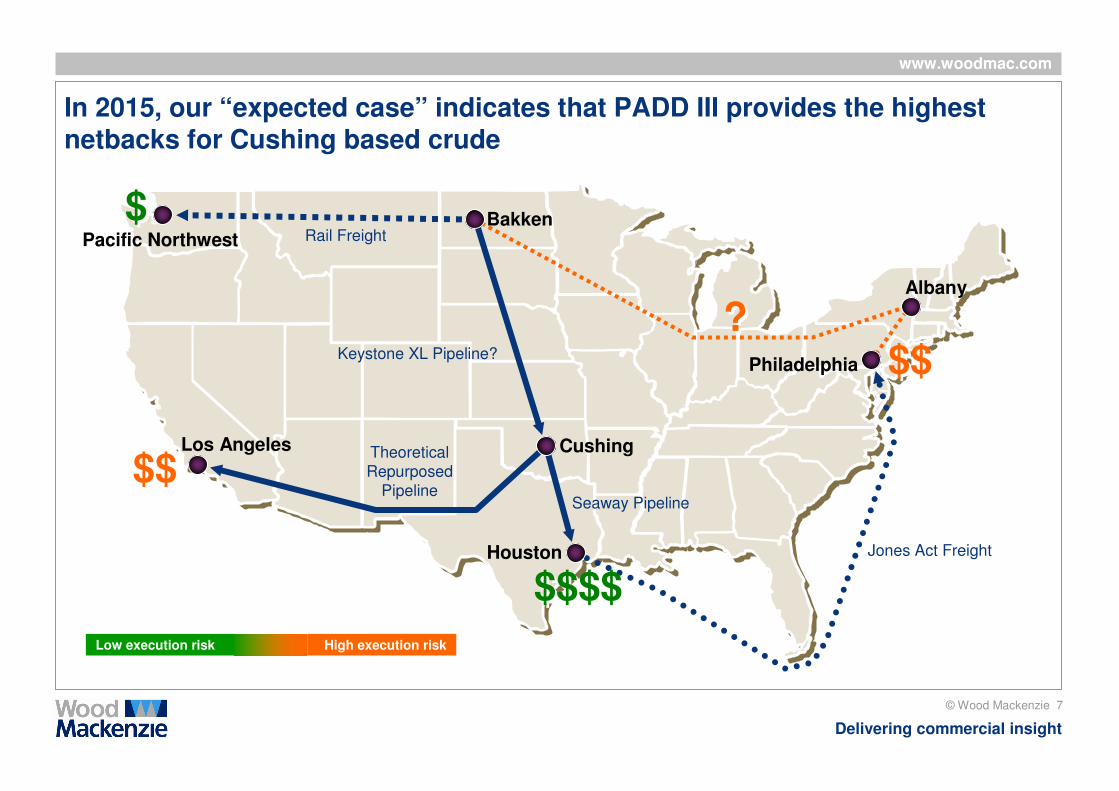

In 2015, our “expected case” indicates that PADD III provides the highest netbacks for Cushing based crude

Cushing

BakkenPacific Northwest

Los Angeles

Philadelphia

Houston Jones Act Freight

Seaway Pipeline

Keystone XL Pipeline?

Theoretical Repurposed

Pipeline

Rail Freight

$$$$

$$

$$$$

$$$$$$$$

Low execution risk High execution risk

Albany

??

www.woodmac.com

© Wood Mackenzie 8

Delivering commercial insight

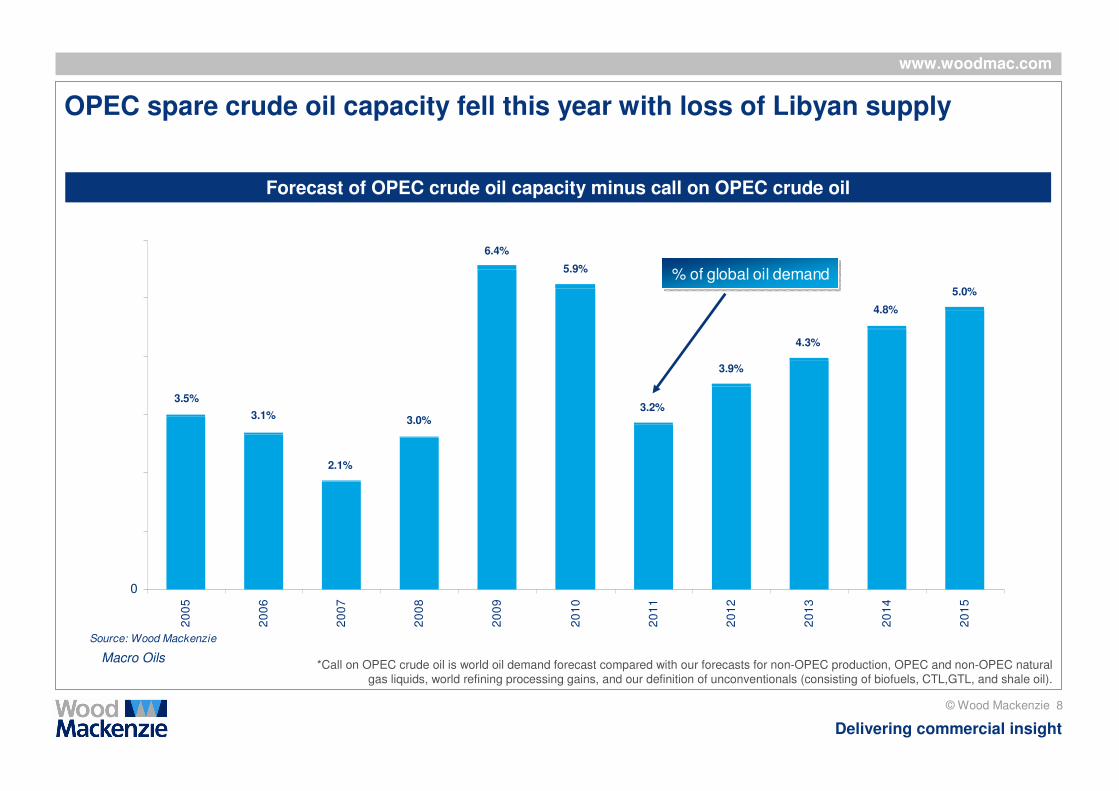

*Call on OPEC crude oil is world oil demand forecast compared with our forecasts for non-OPEC production, OPEC and non-OPEC natural gas liquids, world refining processing gains, and our definition of unconventionals (consisting of biofuels, CTL,GTL, and shale oil).

Forecast of OPEC crude oil capacity minus call on OPEC crude oil

OPEC spare crude oil capacity fell this year with loss of Libyan supply

5.0%

4.8%

4.3%

3.9%

3.2%

5.9%

6.4%

3.0%

2.1%

3.1%

3.5%

0

1

2

3

4

5

6

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

Mil

lio

n b

/d

Source: Wood Mackenzie

% of global oil demand

Macro Oils

www.woodmac.com

© Wood Mackenzie 9

Delivering commercial insight

1 Crude Oil Outlook

Atlantic Basin Refining and Products

Agenda

2

Oil Infrastructure Developments 3

www.woodmac.com

© Wood Mackenzie 10

Delivering commercial insight

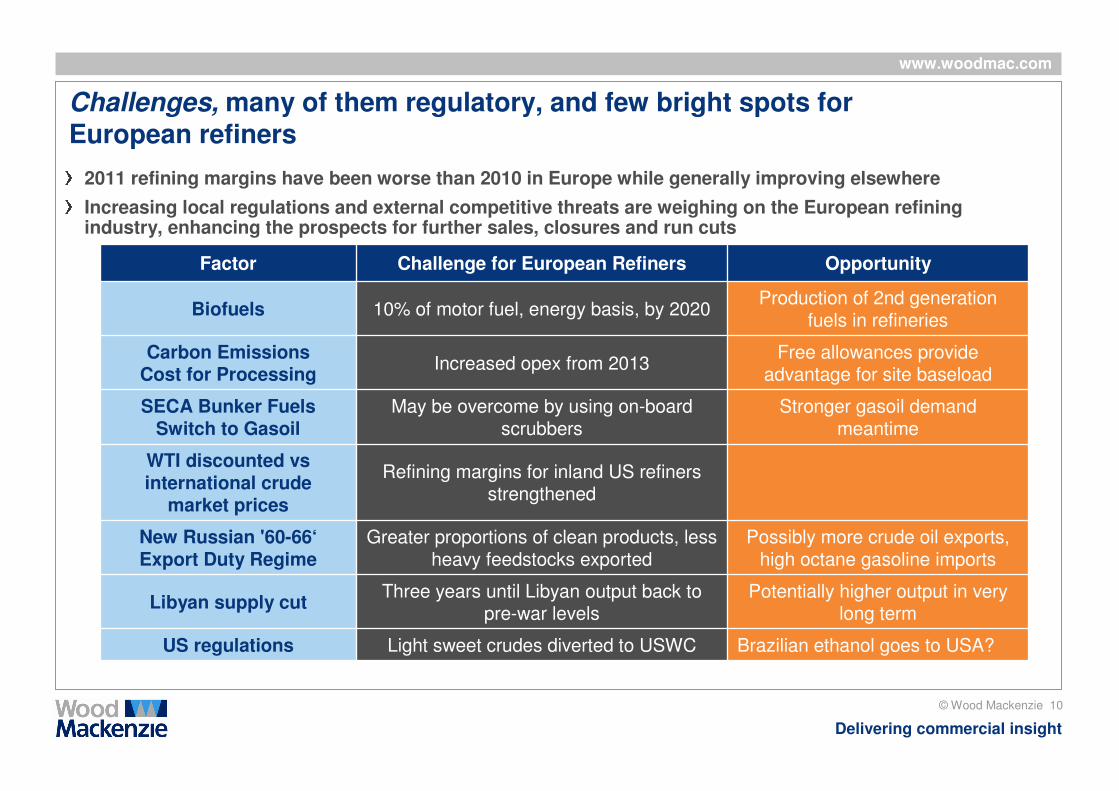

Challenges, many of them regulatory, and few bright spots for European refiners

2011 refining margins have been worse than 2010 in Europe while generally improving elsewhere

Increasing local regulations and external competitive threats are weighing on the European refining industry, enhancing the prospects for further sales, closures and run cuts

Brazilian ethanol goes to USA?Light sweet crudes diverted to USWCUS regulations

Potentially higher output in very long term

Three years until Libyan output back to pre-war levels

Libyan supply cut

Possibly more crude oil exports, high octane gasoline imports

Greater proportions of clean products, less heavy feedstocks exported

New Russian '60-66‘Export Duty Regime

Refining margins for inland US refiners strengthened

WTI discounted vsinternational crude

market prices

Stronger gasoil demand meantime

May be overcome by using on-board scrubbers

SECA Bunker Fuels Switch to Gasoil

Free allowances provide advantage for site baseload

Increased opex from 2013Carbon Emissions

Cost for Processing

Production of 2nd generation fuels in refineries

10% of motor fuel, energy basis, by 2020Biofuels

OpportunityChallenge for European Refiners Factor

www.woodmac.com

© Wood Mackenzie 11

Delivering commercial insight

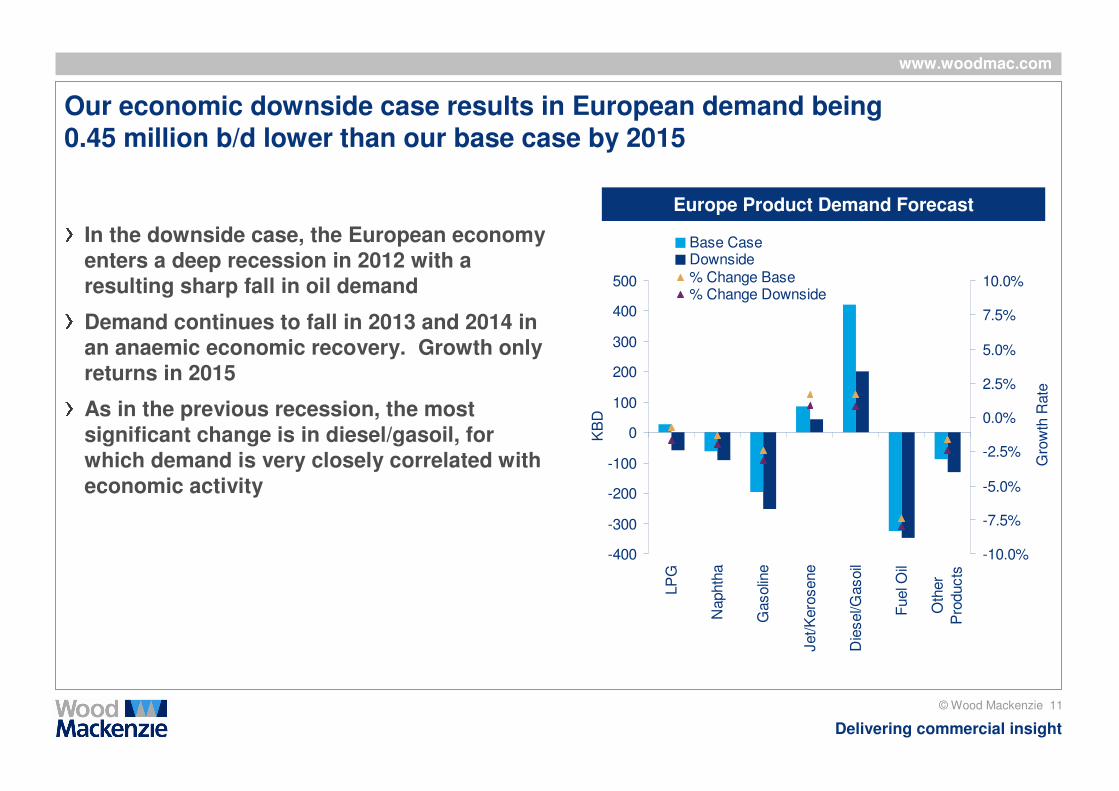

Our economic downside case results in European demand being 0.45 million b/d lower than our base case by 2015

In the downside case, the European economy enters a deep recession in 2012 with a resulting sharp fall in oil demand

Demand continues to fall in 2013 and 2014 in an anaemic economic recovery. Growth only returns in 2015

As in the previous recession, the most significant change is in diesel/gasoil, for which demand is very closely correlated with economic activity

Europe Product Demand Forecast

-400

-300

-200

-100

0

100

200

300

400

500

LP

G

Naphth

a

Gasolin

e

Jet/K

ero

sene

Die

sel/G

asoil

Fuel O

il

Oth

er

Pro

ducts

KB

D .

-10.0%

-7.5%

-5.0%

-2.5%

0.0%

2.5%

5.0%

7.5%

10.0%

Gro

wth

Rate

.

Base CaseDownside% Change Base% Change Downside

www.woodmac.com

© Wood Mackenzie 12

Delivering commercial insight

1 Crude Oil Outlook

Atlantic Basin Refining and Products

Agenda

2

Oil Infrastructure Developments 3

www.woodmac.com

© Wood Mackenzie 13

Delivering commercial insight

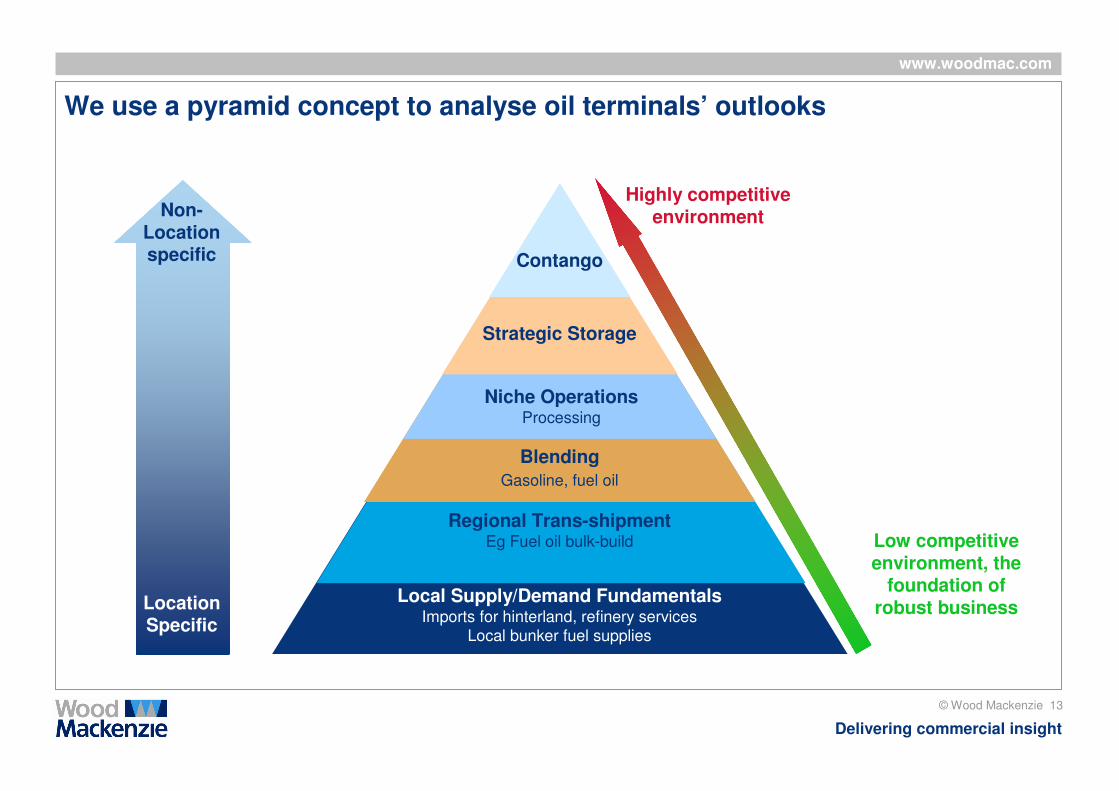

We use a pyramid concept to analyse oil terminals’ outlooks

Location Specific

Non-Location specific

Local Supply/Demand FundamentalsImports for hinterland, refinery services

Local bunker fuel supplies

Regional Trans-shipmentEg Fuel oil bulk-build

Blending Gasoline, fuel oil

Niche OperationsProcessing

Strategic Storage

Contango

Low competitive environment, the

foundation of robust business

Highly competitive environment

www.woodmac.com

© Wood Mackenzie 14

Delivering commercial insight

© Wood Mackenzie 14

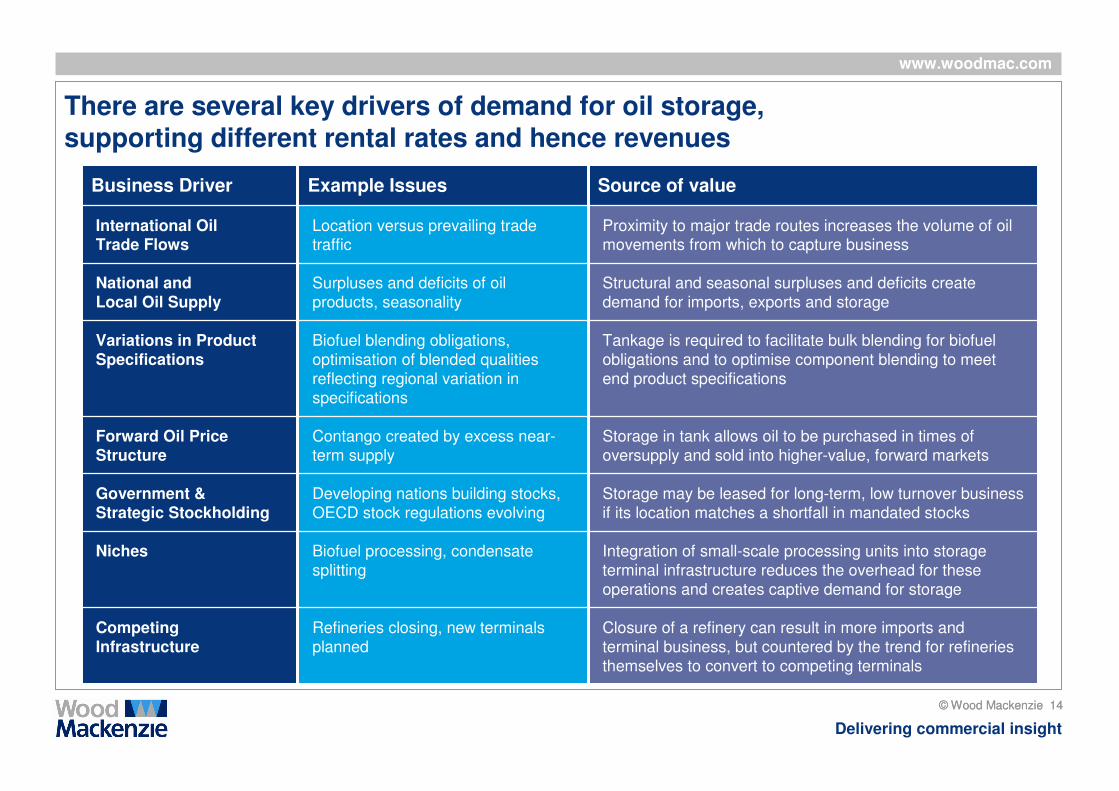

Business Driver Example Issues Source of value

International Oil Trade Flows

Location versus prevailing trade traffic

Proximity to major trade routes increases the volume of oil movements from which to capture business

National and Local Oil Supply

Surpluses and deficits of oil

products, seasonality

Structural and seasonal surpluses and deficits create

demand for imports, exports and storage

Variations in Product Specifications

Biofuel blending obligations,

optimisation of blended qualities

reflecting regional variation in

specifications

Tankage is required to facilitate bulk blending for biofuel

obligations and to optimise component blending to meet

end product specifications

Forward Oil Price Structure

Contango created by excess near-

term supply

Storage in tank allows oil to be purchased in times of

oversupply and sold into higher-value, forward markets

Government & Strategic Stockholding

Developing nations building stocks,

OECD stock regulations evolving

Storage may be leased for long-term, low turnover business

if its location matches a shortfall in mandated stocks

Niches Biofuel processing, condensate

splitting

Integration of small-scale processing units into storage

terminal infrastructure reduces the overhead for these

operations and creates captive demand for storage

Competing Infrastructure

Refineries closing, new terminals

planned

Closure of a refinery can result in more imports and

terminal business, but countered by the trend for refineries

themselves to convert to competing terminals

There are several key drivers of demand for oil storage, supporting different rental rates and hence revenues

www.woodmac.com

© Wood Mackenzie 15

Delivering commercial insight

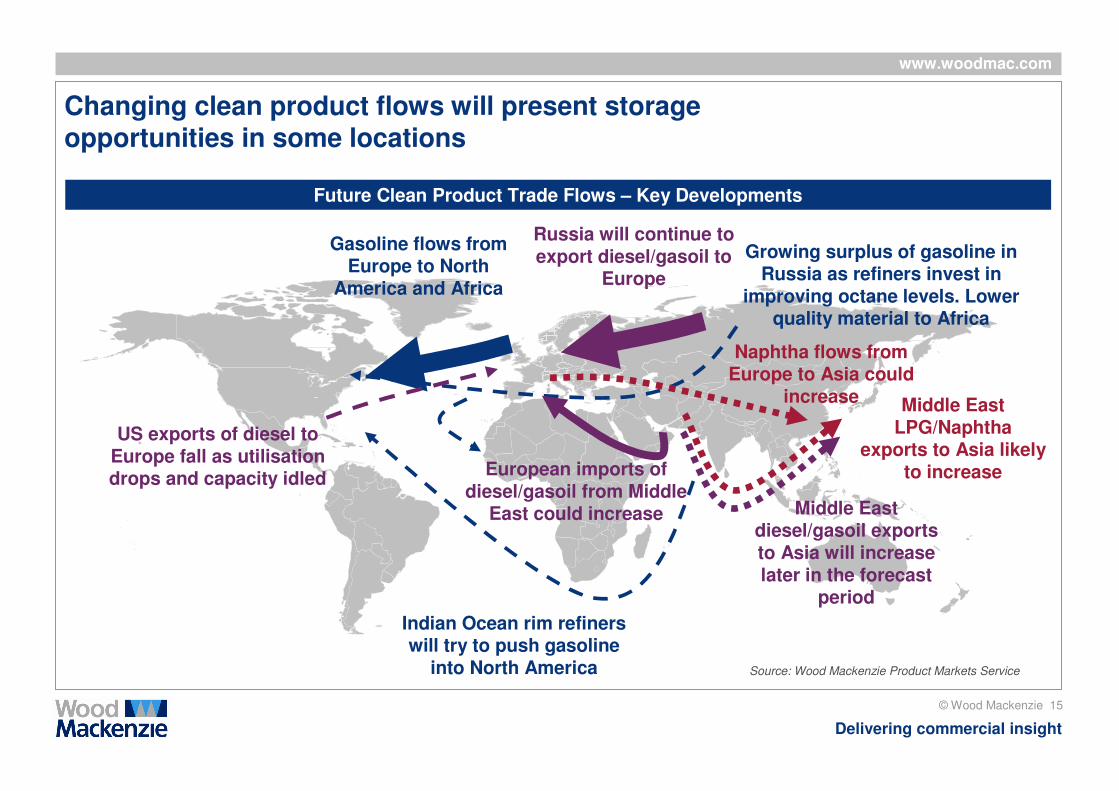

Changing clean product flows will present storage opportunities in some locations

Gasoline flows from Europe to North

America and Africa

Indian Ocean rim refiners will try to push gasoline

into North America

Growing surplus of gasoline in Russia as refiners invest in

improving octane levels. Lower quality material to Africa

European imports of diesel/gasoil from Middle

East could increase

Russia will continue to export diesel/gasoil to

Europe

Middle East diesel/gasoil exports to Asia will increase later in the forecast

period

US exports of diesel to Europe fall as utilisation drops and capacity idled

Middle East LPG/Naphtha

exports to Asia likely to increase

Naphtha flows from Europe to Asia could

increase

Future Clean Product Trade Flows – Key Developments

Source: Wood Mackenzie Product Markets Service

www.woodmac.com

© Wood Mackenzie 16

Delivering commercial insight

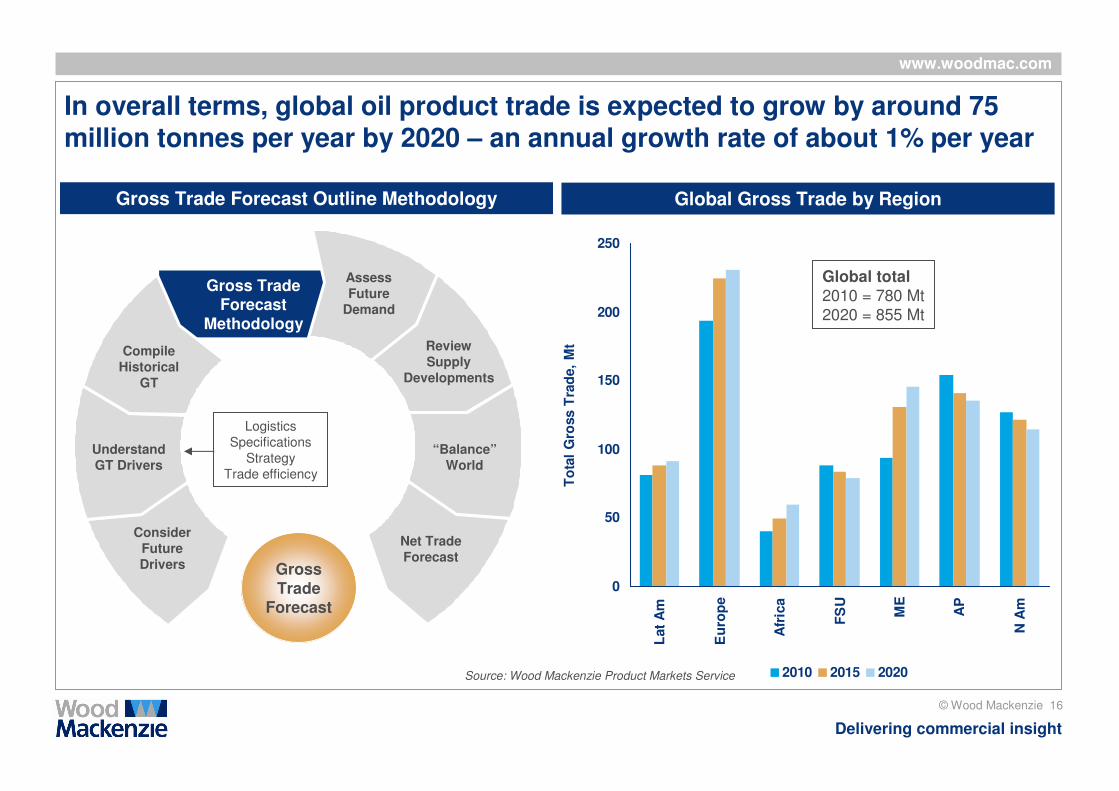

In overall terms, global oil product trade is expected to grow by around 75 million tonnes per year by 2020 – an annual growth rate of about 1% per year

0

50

100

150

200

250

Lat

Am

Eu

rop

e

Afr

ica

FS

U

ME

AP

N A

m

To

tal

Gro

ss T

rad

e,

Mt

2010 2015 2020

Global Gross Trade by Region

Global total2010 = 780 Mt

2020 = 855 Mt

Gross TradeForecast

Methodology

AssessFuture

Demand

ReviewSupply

Developments

“Balance”World

Net TradeForecast

CompileHistorical

GT

UnderstandGT Drivers

ConsiderFutureDrivers Gross

TradeForecast

Logistics

Specifications

Strategy

Trade efficiency

Gross Trade Forecast Outline Methodology

Source: Wood Mackenzie Product Markets Service

www.woodmac.com

© Wood Mackenzie 17

Delivering commercial insight

© Wood Mackenzie 17

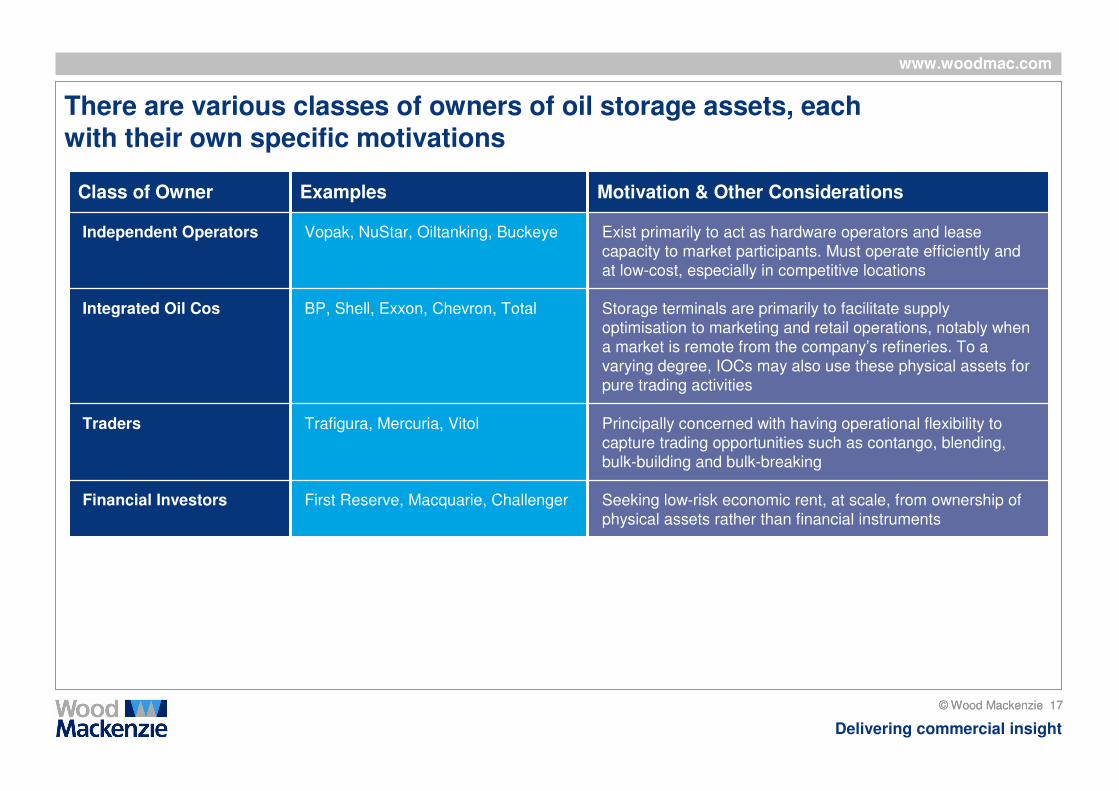

There are various classes of owners of oil storage assets, each with their own specific motivations

Class of Owner Examples Motivation & Other Considerations

Independent Operators Vopak, NuStar, Oiltanking, Buckeye Exist primarily to act as hardware operators and lease

capacity to market participants. Must operate efficiently and

at low-cost, especially in competitive locations

Integrated Oil Cos BP, Shell, Exxon, Chevron, Total Storage terminals are primarily to facilitate supply

optimisation to marketing and retail operations, notably when

a market is remote from the company’s refineries. To a

varying degree, IOCs may also use these physical assets for

pure trading activities

Traders Trafigura, Mercuria, Vitol Principally concerned with having operational flexibility to

capture trading opportunities such as contango, blending,

bulk-building and bulk-breaking

Financial Investors First Reserve, Macquarie, Challenger Seeking low-risk economic rent, at scale, from ownership of

physical assets rather than financial instruments

www.woodmac.com

© Wood Mackenzie 18

Delivering commercial insight

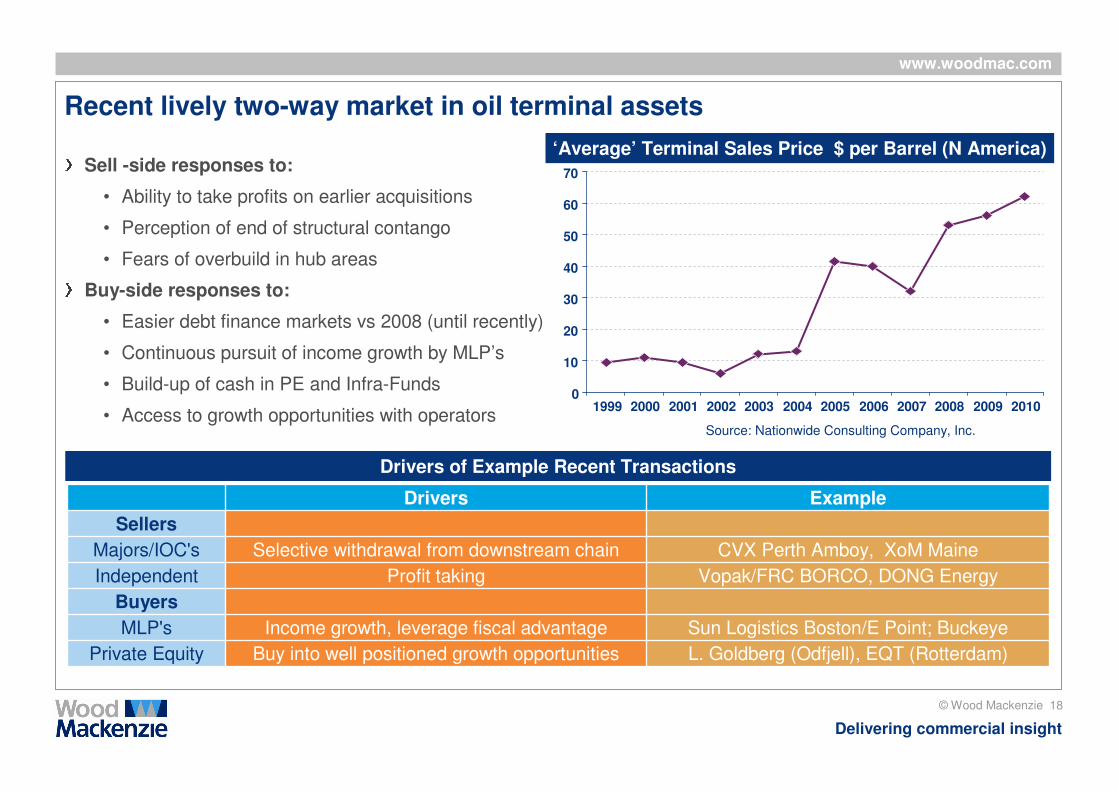

Recent lively two-way market in oil terminal assets

Sell -side responses to:

• Ability to take profits on earlier acquisitions

• Perception of end of structural contango

• Fears of overbuild in hub areas

Buy-side responses to:

• Easier debt finance markets vs 2008 (until recently)

• Continuous pursuit of income growth by MLP’s

• Build-up of cash in PE and Infra-Funds

• Access to growth opportunities with operatorsSource: Nationwide Consulting Company, Inc.

‘Average’ Terminal Sales Price $ per Barrel (N America)

Drivers of Example Recent Transactions

0

10

20

30

40

50

60

70

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

L. Goldberg (Odfjell), EQT (Rotterdam)Buy into well positioned growth opportunitiesPrivate Equity

Sun Logistics Boston/E Point; BuckeyeIncome growth, leverage fiscal advantageMLP's

Buyers

Vopak/FRC BORCO, DONG EnergyProfit takingIndependent

CVX Perth Amboy, XoM MaineSelective withdrawal from downstream chainMajors/IOC's

Sellers

ExampleDrivers

www.woodmac.com

© Wood Mackenzie 19

Delivering commercial insight

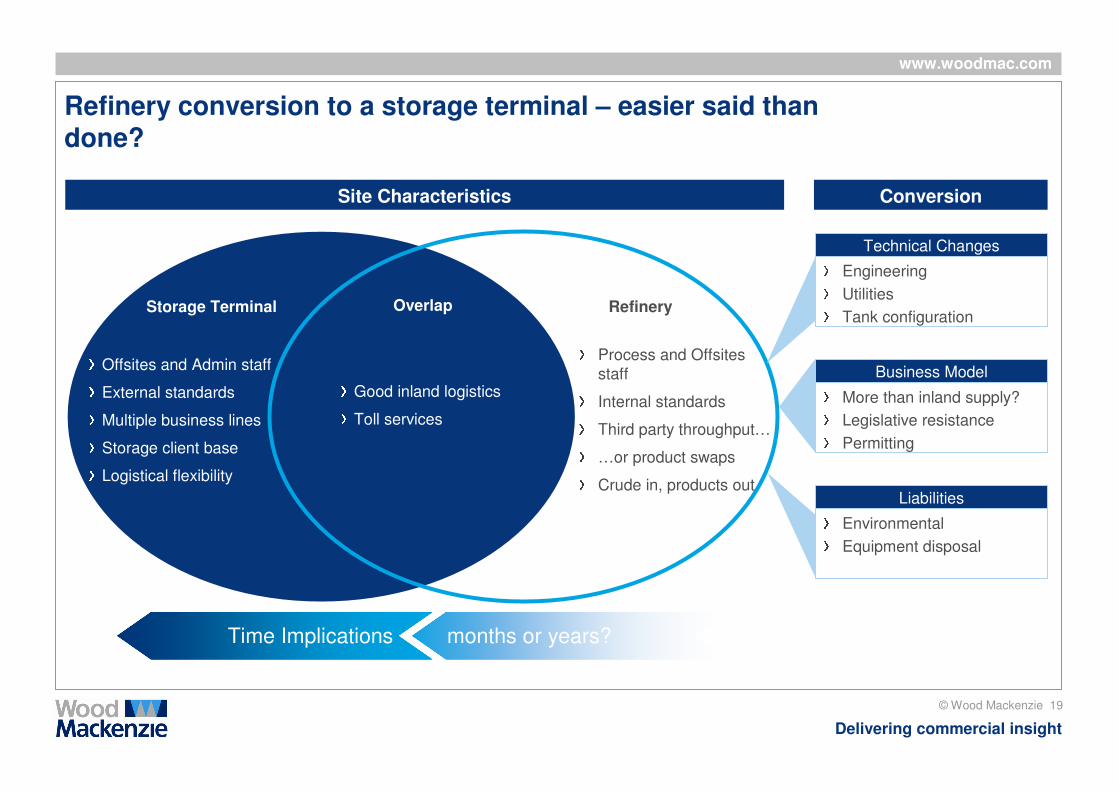

Storage Terminal Refinery

Conversion Considerations

Good inland logistics

Toll services

Offsites and Admin staff

External standards

Multiple business lines

Storage client base

Logistical flexibility

Process and Offsites

staff

Internal standards

Third party throughput…

…or product swaps

Crude in, products out

Technical Changes

Engineering

Utilities

Tank configuration

Business Model

More than inland supply?

Legislative resistance

Permitting

Liabilities

Environmental

Equipment disposal

Refinery conversion to a storage terminal – easier said than done?

Overlap

Site Characteristics

Time Implications months or years?

www.woodmac.com

© Wood Mackenzie 20

Delivering commercial insight

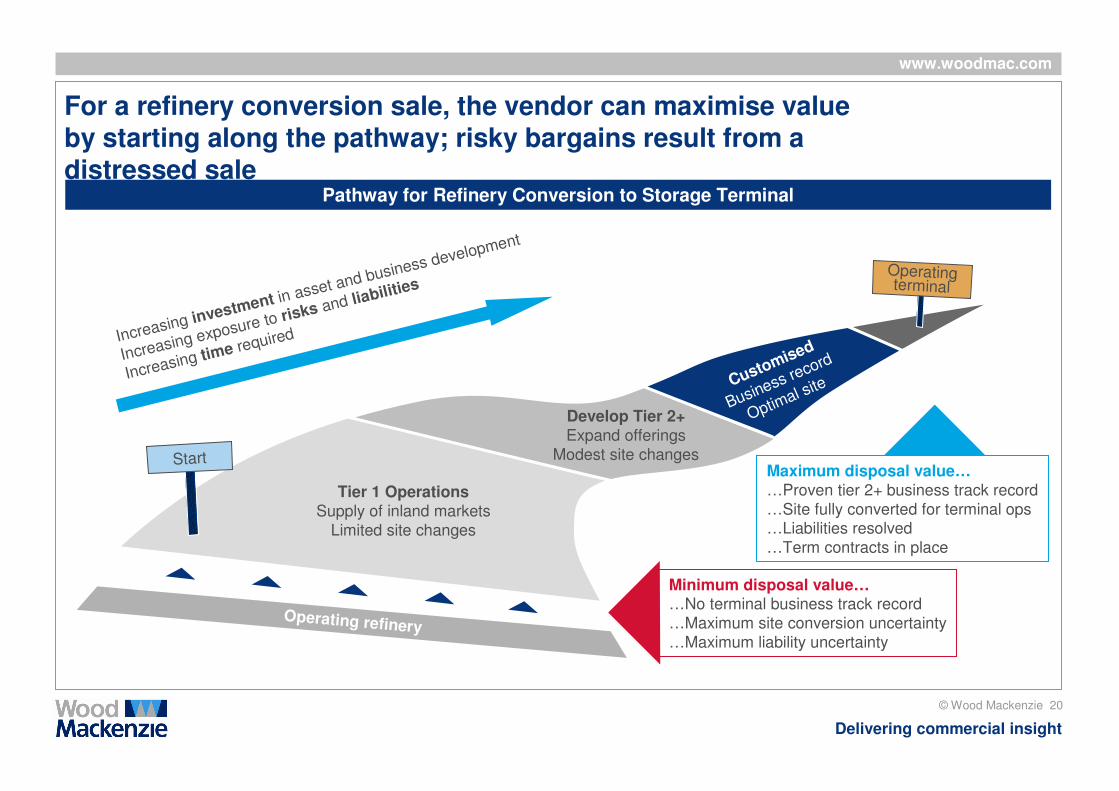

Operating refinery

Start

Operating terminal

Tier 1 OperationsSupply of inland markets

Limited site changes

Develop Tier 2+Expand offerings

Modest site changes

Customised

Business record

Optimal site

For a refinery conversion sale, the vendor can maximise value by starting along the pathway; risky bargains result from a distressed sale

Minimum disposal value……No terminal business track record

…Maximum site conversion uncertainty

…Maximum liability uncertainty

Maximum disposal value……Proven tier 2+ business track record

…Site fully converted for terminal ops…Liabilities resolved

…Term contracts in place

Increasing investment in asset and business development

Increasing exposure to risks and liabilities

Increasing time required

Pathway for Refinery Conversion to Storage Terminal

www.woodmac.com

© Wood Mackenzie 21

Delivering commercial insight

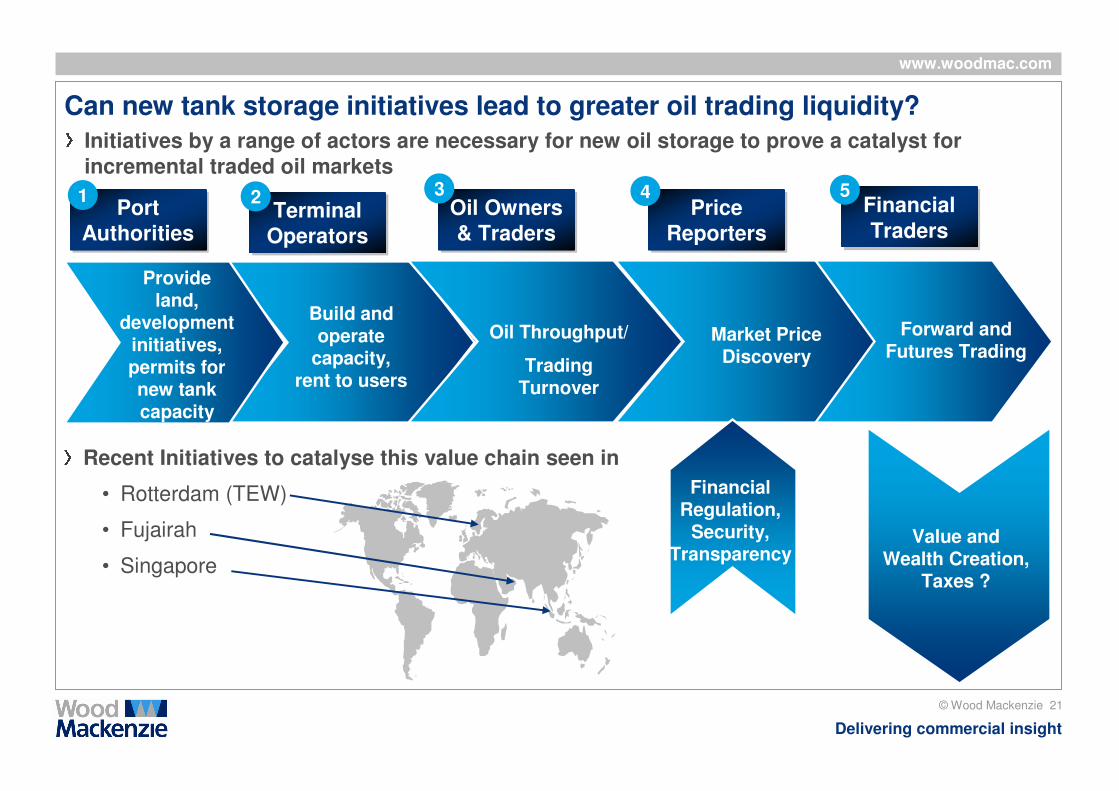

Can new tank storage initiatives lead to greater oil trading liquidity?

Initiatives by a range of actors are necessary for new oil storage to prove a catalyst for incremental traded oil markets

Oil Throughput/

Trading Turnover

Market Price Discovery

Forward and Futures Trading

Port Authorities

Port Authorities

Build and operate

capacity, rent to users

Provide land,

development initiatives, permits for new tank capacity

Terminal Operators

Terminal Operators

Oil Owners & Traders

Oil Owners & Traders

Price Reporters

Price Reporters

Financial Traders

Financial Traders

1 2 3 4 5

Recent Initiatives to catalyse this value chain seen in

• Rotterdam (TEW)

• Fujairah

• Singapore

Financial Regulation,

Security, Transparency

Value and Wealth Creation,

Taxes ?

www.woodmac.com

© Wood Mackenzie 22

Delivering commercial insight

Ben Holt

VP Downstream Consulting, EMEA

+44 20 3060 0467

Ben Holt

VP Downstream Consulting, EMEA

+44 20 3060 0467

Contacts

Onur Capan

Research Analyst

+44 20 3060 0448

Onur Capan

Research Analyst

+44 20 3060 0448

www.woodmac.com

© Wood Mackenzie 23

Delivering commercial insight

Wood Mackenzie Disclaimer

This presentation has been prepared by Wood Mackenzie Limited for delivery at the Tank Storage Istanbul 2011 Conference. It has not been prepared for the benefit of any particular attendee and may not be relied upon by any attendee or other third party. If, notwithstanding the foregoing, this presentation is relied upon by any person, Wood Mackenzie Limited does not accept, and disclaims, all liability for loss and damage suffered as a result.

The information contained in these slides may be retained by attendees. However, these slides and the contents of this presentation may not be disclosed to any other person or published by any means without Wood Mackenzie Limited's prior written permission.

www.woodmac.com

© Wood Mackenzie 24

Delivering commercial insight

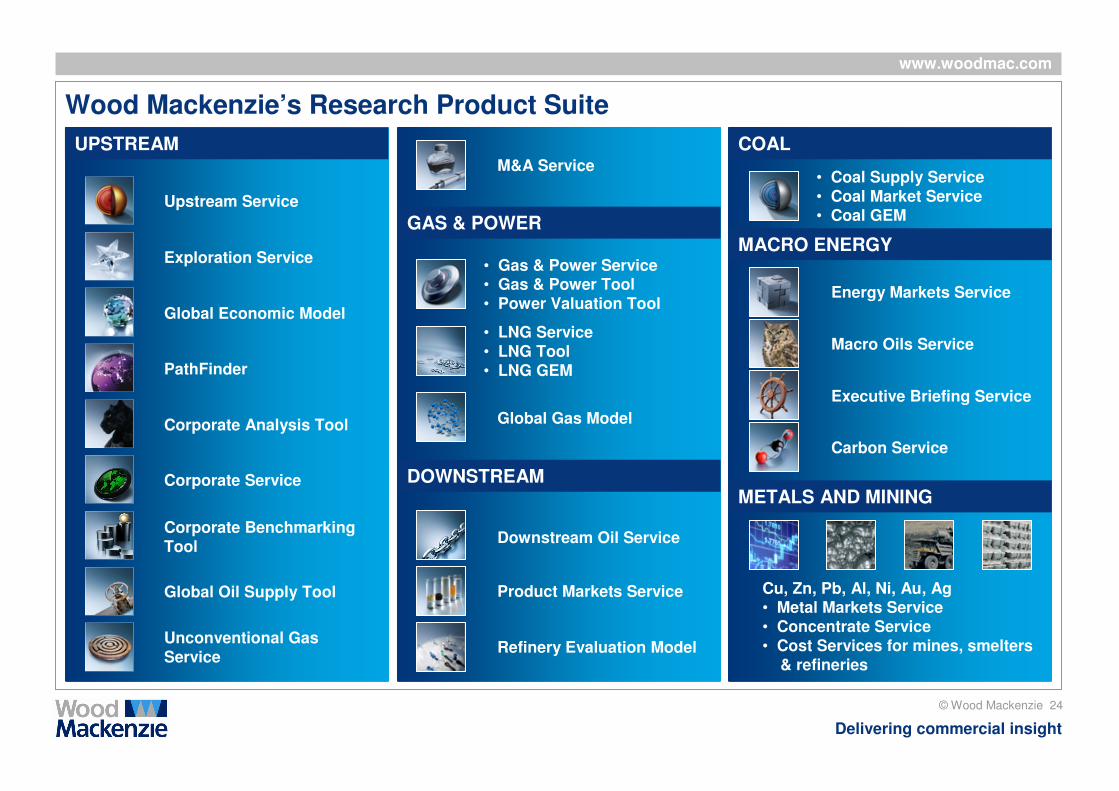

Wood Mackenzie’s Research Product Suite

• LNG Service• LNG Tool• LNG GEM

GAS & POWER

DOWNSTREAM

Upstream Service

UPSTREAM

Global Economic Model

PathFinder

Unconventional Gas Service

Corporate Analysis Tool

Energy Markets Service

Downstream Oil Service

Macro Oils Service

MACRO ENERGY

Global Oil Supply Tool Product Markets Service

• Gas & Power Service• Gas & Power Tool• Power Valuation Tool

Global Gas Model

Refinery Evaluation Model

Exploration Service

COAL

• Coal Supply Service• Coal Market Service• Coal GEM

Corporate Service METALS AND MINING

Corporate BenchmarkingTool

Cu, Zn, Pb, Al, Ni, Au, Ag• Metal Markets Service• Concentrate Service• Cost Services for mines, smelters

& refineries

M&A Service

Executive Briefing Service

Carbon Service

www.woodmac.com

© Wood Mackenzie 25

Delivering commercial insight

Wood Mackenzie has a presence in all the major energy centres of the world

FIJI

New Delhi

Calgary

Houston

Boston

EdinburghMoscow

Beijing

Singapore

Sydney

Kuala Lumpur

Tokyo

New York

Dubai

Rio de Janeiro

Wood Mackenzie Offices

Perth Brisbane

AnnapolisDenver

Guildford

Seoul

London

Jakarta

Algiers

Abuja

www.woodmac.com

© Wood Mackenzie 26

Delivering commercial insight

Wood Mackenzie

Kintore House

74-77 Queen Street

Edinburgh EH2 4NS

Global Contact Details

Europe +44 (0)131 243 4400

Americas +1 713 470 1600

Asia Pacific +65 6518 0800

Email [email protected]

Global Offices

Australia - Canada - China - Japan - Malaysia - Russia - Singapore - South Africa - United Arab Emirates - United Kingdom - United States

Wood Mackenzie has been providing its unique range of research products and consulting services to the Energy industry for over 30 years. Wood Mackenzie provides forward-looking commercial insight that enables clients to make better

business decisions. For more information visit: www.woodmac.com

![Commercial Drivers Final [Compatibility Mode]](https://img.pdfslide.net/doc/110x75/58f2ed611a28ab0b428b4629/commercial-drivers-final-compatibility-mode.jpg)