Embed Size (px)

Citation preview

ihs.com

© 2015 IHS

Presentation

IHS

Commodity Plastics Market Update: The Impact of Lower Crude May 15 2015

Joel Morales, Director Polyolefins North America, 832 619 8588, [email protected]

CHEMICALS

© 2015 IHS

Terms of Use

The accompanying materials were prepared by IHS Inc. (IHS Chemical) and are not to be redistributed or reused in any manner without prior written consent, with the exception of client internal distribution as described below.

IHS Chemical strives to be supportive of client internal distribution of IHS Chemical content but requires that:

• IHS Chemical content and information, including but not limited to graphs, charts, tables, figures, and data, are not to be disseminated outside of a client organization to any third party, including a client’s customers, financial institutions, consultants, or the public.

• Content distributed within the client organization must display IHS Chemical’s legal notices and attributions of authorship.

Some information supplied by IHS Chemical may be obtained from sources that IHS Chemical believes to be reliable but are in no way warranted by IHS Chemical as to accuracy or completeness. Absent a specific agreement to the contrary, IHS Chemical has no obligation to update any content or information provided to a client.

Plastics Overview / May 2015

© 2015 IHS

© 2015 IHS

ABOUT IHS CHEMICAL

Plastics Overview / May 2015

© 2015 IHS

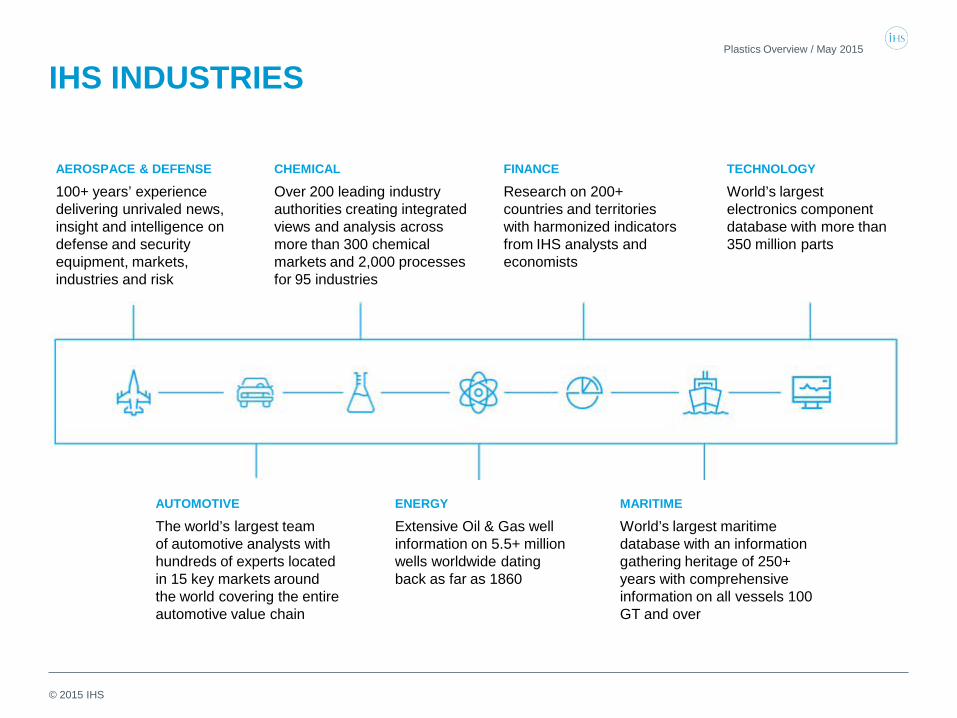

AEROSPACE & DEFENSE

100+ years’ experience delivering unrivaled news, insight and intelligence on defense and security equipment, markets, industries and risk

IHS INDUSTRIES Plastics Overview / May 2015

CHEMICAL

Over 200 leading industry authorities creating integrated views and analysis across more than 300 chemical markets and 2,000 processes for 95 industries

FINANCE

Research on 200+ countries and territories with harmonized indicators from IHS analysts and economists

TECHNOLOGY

World’s largest electronics component database with more than 350 million parts

AUTOMOTIVE

The world’s largest team of automotive analysts with hundreds of experts located in 15 key markets around the world covering the entire automotive value chain

ENERGY

Extensive Oil & Gas well information on 5.5+ million wells worldwide dating back as far as 1860

MARITIME

World’s largest maritime database with an information gathering heritage of 250+ years with comprehensive information on all vessels 100 GT and over

© 2015 IHS

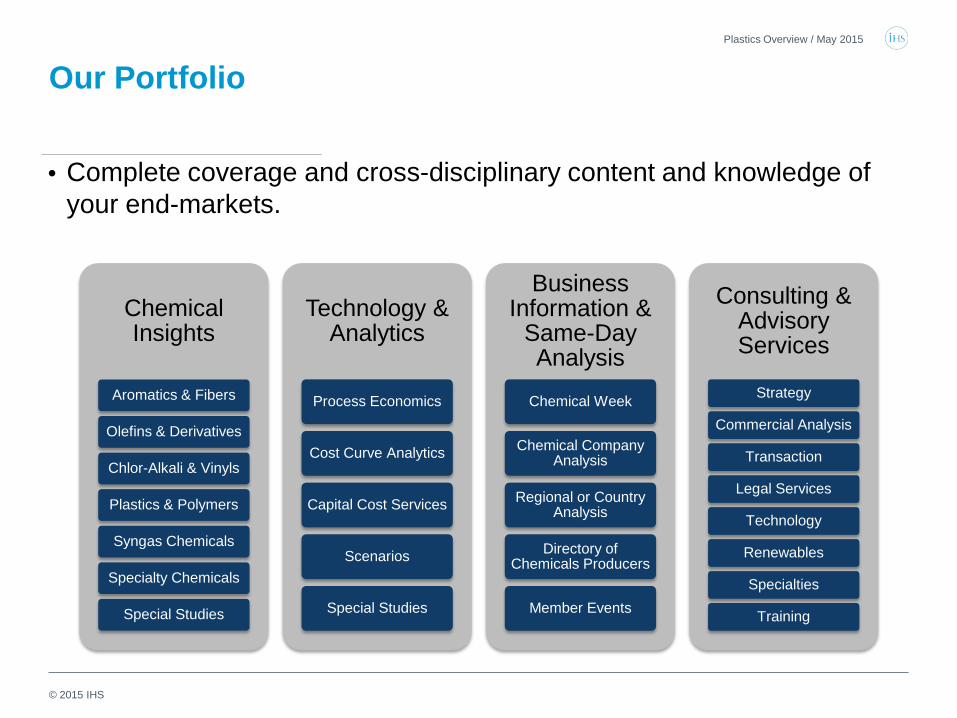

Our Portfolio

• Complete coverage and cross-disciplinary content and knowledge of your end-markets.

Plastics Overview / May 2015

Chemical Insights

Aromatics & Fibers

Olefins & Derivatives

Chlor-Alkali & Vinyls

Plastics & Polymers

Syngas Chemicals

Specialty Chemicals

Special Studies

Technology & Analytics

Process Economics

Cost Curve Analytics

Capital Cost Services

Scenarios

Special Studies

Business Information &

Same-Day Analysis

Chemical Week

Chemical Company Analysis

Regional or Country Analysis

Directory of Chemicals Producers

Member Events

Consulting & Advisory Services

Strategy

Commercial Analysis

Transaction

Legal Services

Technology

Renewables

Specialties

Training

© 2015 IHS

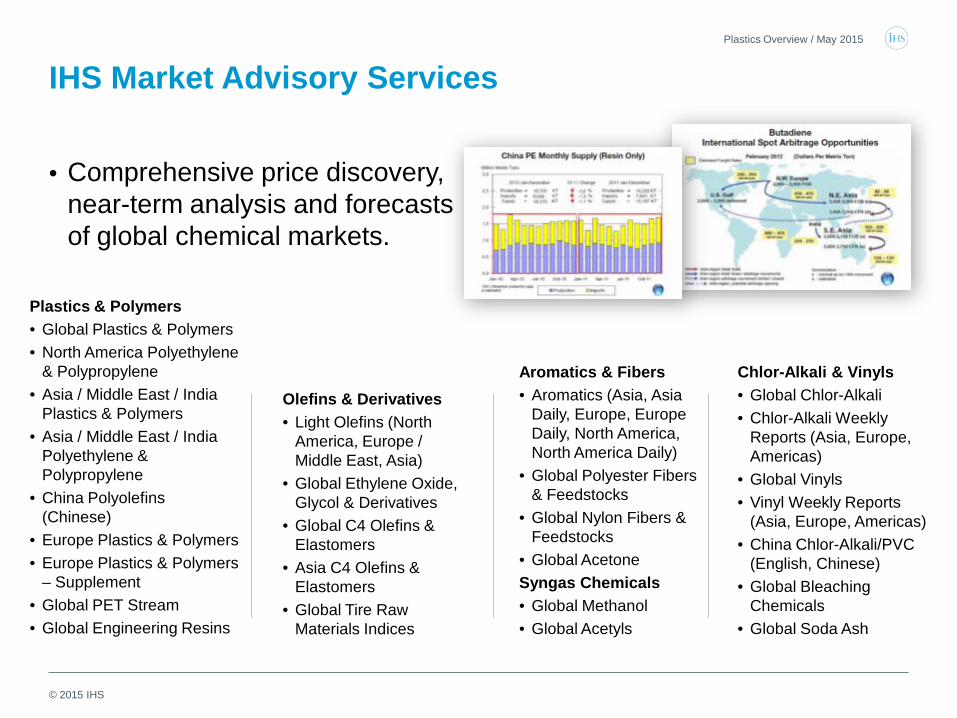

Aromatics & Fibers • Aromatics (Asia, Asia

Daily, Europe, Europe Daily, North America, North America Daily)

• Global Polyester Fibers & Feedstocks

• Global Nylon Fibers & Feedstocks

• Global Acetone Syngas Chemicals • Global Methanol • Global Acetyls

Plastics Overview / May 2015

IHS Market Advisory Services

• Comprehensive price discovery, near-term analysis and forecasts of global chemical markets.

Olefins & Derivatives • Light Olefins (North

America, Europe / Middle East, Asia)

• Global Ethylene Oxide, Glycol & Derivatives

• Global C4 Olefins & Elastomers

• Asia C4 Olefins & Elastomers

• Global Tire Raw Materials Indices

Chlor-Alkali & Vinyls • Global Chlor-Alkali • Chlor-Alkali Weekly

Reports (Asia, Europe, Americas)

• Global Vinyls • Vinyl Weekly Reports

(Asia, Europe, Americas) • China Chlor-Alkali/PVC

(English, Chinese) • Global Bleaching

Chemicals • Global Soda Ash

Plastics & Polymers • Global Plastics & Polymers • North America Polyethylene

& Polypropylene • Asia / Middle East / India

Plastics & Polymers • Asia / Middle East / India

Polyethylene & Polypropylene

• China Polyolefins (Chinese)

• Europe Plastics & Polymers • Europe Plastics & Polymers

– Supplement • Global PET Stream • Global Engineering Resins

© 2015 IHS

Energy Overview

Plastics Overview / May 2015

© 2015 IHS

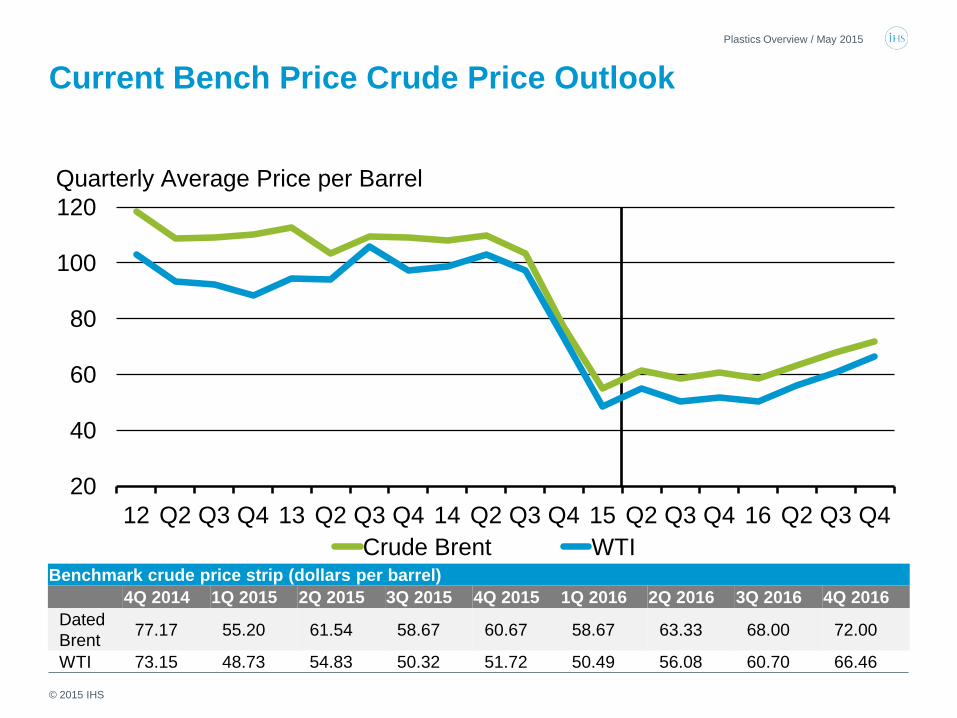

Current Bench Price Crude Price Outlook Plastics Overview / May 2015

Benchmark crude price strip (dollars per barrel) 4Q 2014 1Q 2015 2Q 2015 3Q 2015 4Q 2015 1Q 2016 2Q 2016 3Q 2016 4Q 2016

Dated Brent 77.17 55.20 61.54 58.67 60.67 58.67 63.33 68.00 72.00

WTI 73.15 48.73 54.83 50.32 51.72 50.49 56.08 60.70 66.46

20

40

60

80

100

120

12 Q2 Q3 Q4 13 Q2 Q3 Q4 14 Q2 Q3 Q4 15 Q2 Q3 Q4 16 Q2 Q3 Q4 Crude Brent WTI

Quarterly Average Price per Barrel

© 2015 IHS

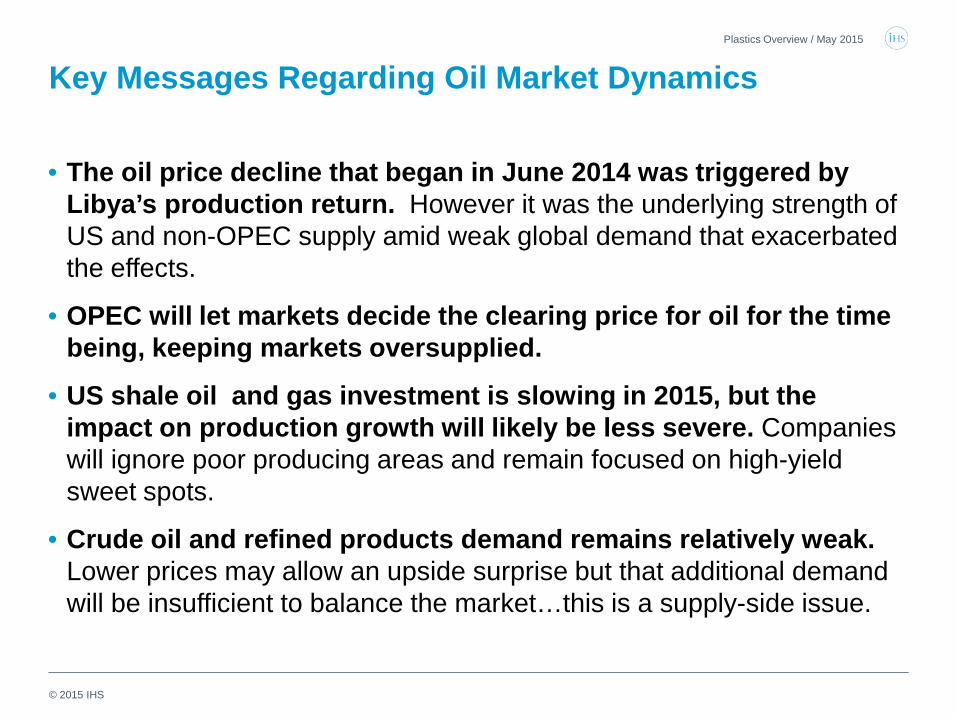

Key Messages Regarding Oil Market Dynamics

• The oil price decline that began in June 2014 was triggered by Libya’s production return. However it was the underlying strength of US and non-OPEC supply amid weak global demand that exacerbated the effects.

• OPEC will let markets decide the clearing price for oil for the time being, keeping markets oversupplied.

• US shale oil and gas investment is slowing in 2015, but the impact on production growth will likely be less severe. Companies will ignore poor producing areas and remain focused on high-yield sweet spots.

• Crude oil and refined products demand remains relatively weak. Lower prices may allow an upside surprise but that additional demand will be insufficient to balance the market…this is a supply-side issue.

Plastics Overview / May 2015

© 2015 IHS

In the Global Economy…Who is Helped and Who is Hurt by Lower Oil Prices? Who is helped?

• US consumers….annual fuel savings of at least $80 billion. • Energy-intensive industries (e.g. agriculture, transportation and shipping). • Governments in oil-importing countries with large fuel subsidies (at

governmental level more so than consumer).

Who is hurt? • Oil producers, especially those with high costs. • Major oil exporters, especially those with difficult public finances where the

“fiscal break-even point” is above $100 per barrel, including Iran, Russia, and Venezuela.

Net effect:

• The drop in oil prices represents a transfer of $1.5 trillion annually from oil exporters to oil importers.

Plastics Overview / May 2015

© 2015 IHS

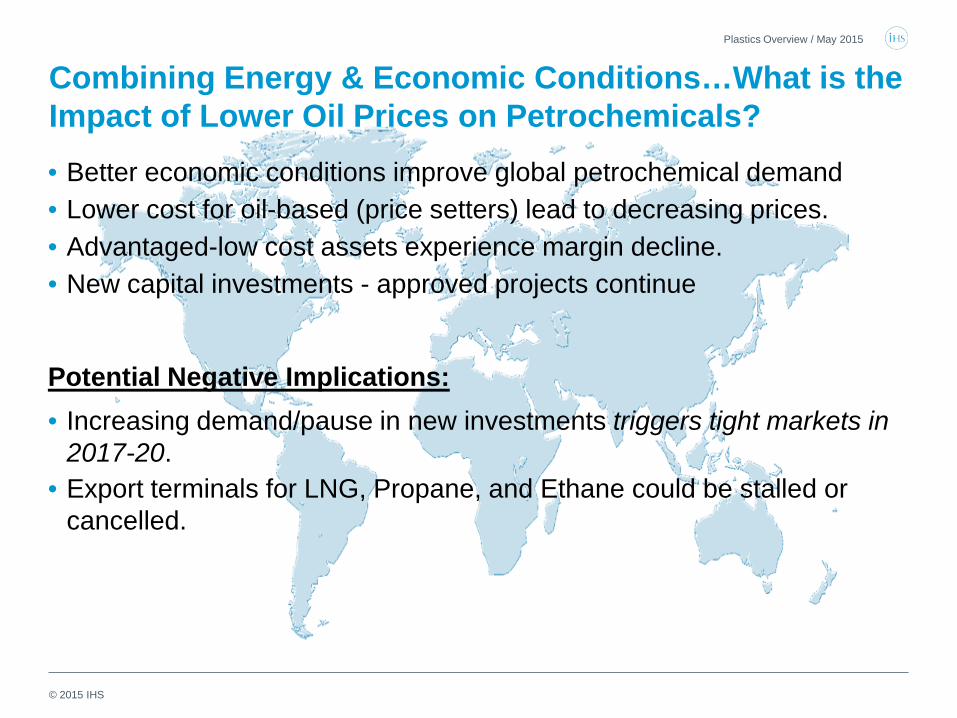

Combining Energy & Economic Conditions…What is the Impact of Lower Oil Prices on Petrochemicals? • Better economic conditions improve global petrochemical demand • Lower cost for oil-based (price setters) lead to decreasing prices. • Advantaged-low cost assets experience margin decline. • New capital investments - approved projects continue

Potential Negative Implications: • Increasing demand/pause in new investments triggers tight markets in

2017-20. • Export terminals for LNG, Propane, and Ethane could be stalled or

cancelled.

Plastics Overview / May 2015

© 2015 IHS

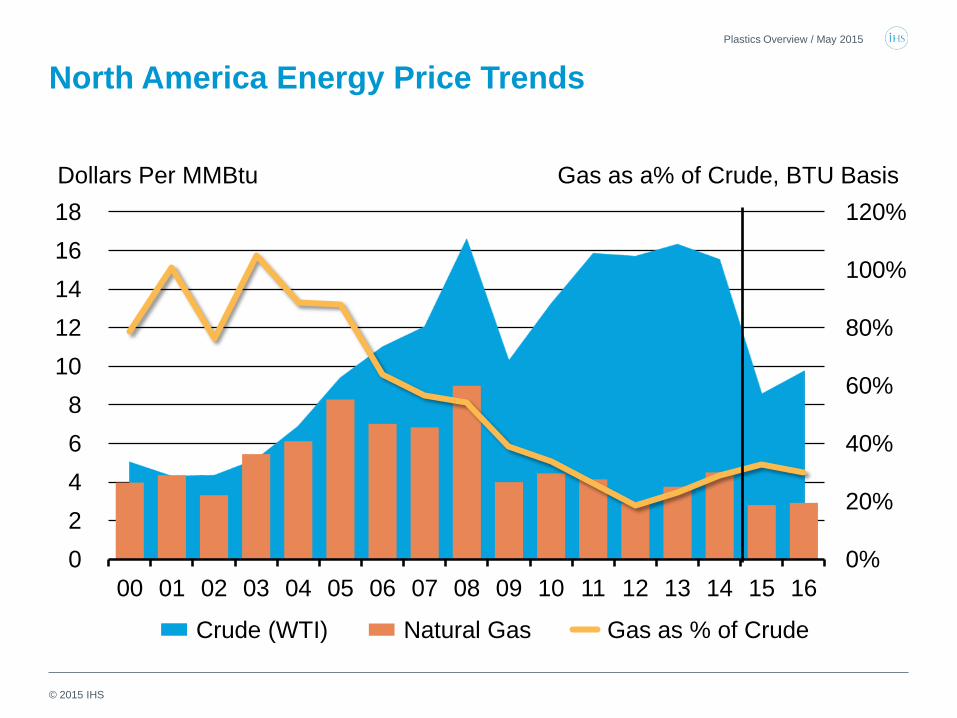

North America Energy Price Trends Plastics Overview / May 2015

0%

20%

40%

60%

80%

100%

120%

0 2 4 6 8

10 12 14 16 18

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16

Crude (WTI) Natural Gas Gas as % of Crude

Dollars Per MMBtu Gas as a% of Crude, BTU Basis

© 2015 IHS

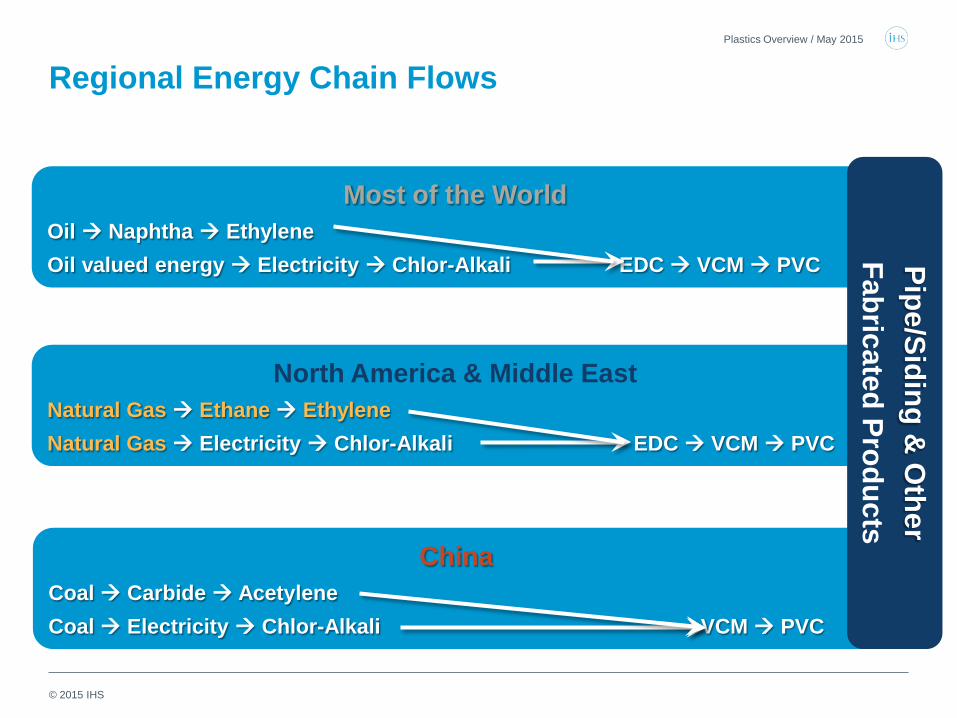

Regional Energy Chain Flows

China Coal Carbide Acetylene Coal Electricity Chlor-Alkali VCM PVC

North America & Middle East Natural Gas Ethane Ethylene Natural Gas Electricity Chlor-Alkali EDC VCM PVC

Most of the World Oil Naphtha Ethylene Oil valued energy Electricity Chlor-Alkali EDC VCM PVC Pipe/Siding &

Other

Fabricated Products

Plastics Overview / May 2015

© 2015 IHS

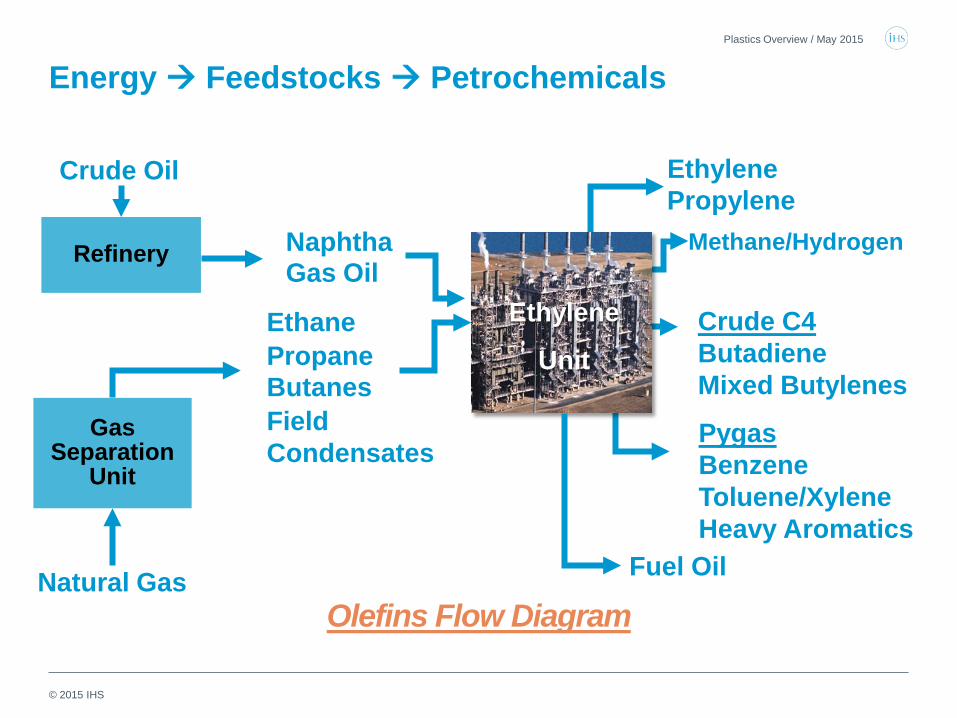

Energy Feedstocks Petrochemicals Plastics Overview / May 2015

Naphtha Gas Oil

Field Condensates

Ethane Propane Butanes

Propylene Ethylene

Fuel Oil

Methane/Hydrogen

Natural Gas

Crude Oil

Refinery

Gas Separation

Unit

Ethylene

Unit

Olefins Flow Diagram

Pygas Benzene Toluene/Xylene Heavy Aromatics

Crude C4 Butadiene Mixed Butylenes

© 2015 IHS

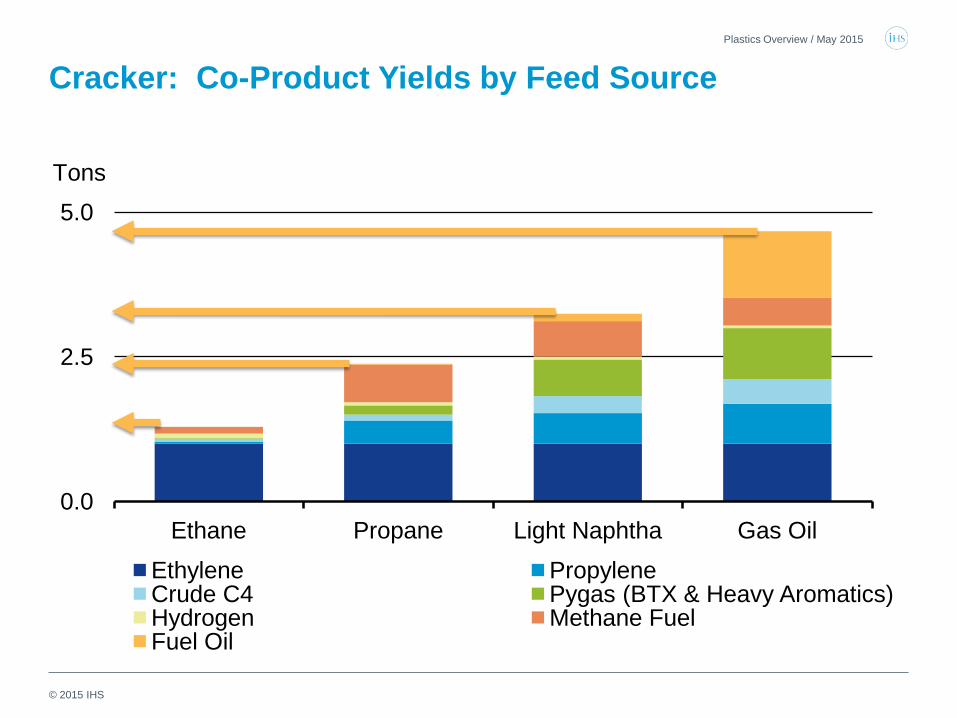

Cracker: Co-Product Yields by Feed Source Plastics Overview / May 2015

0.0

2.5

5.0

Ethane Propane Light Naphtha Gas Oil

Ethylene Propylene Crude C4 Pygas (BTX & Heavy Aromatics) Hydrogen Methane Fuel Fuel Oil

Tons

© 2015 IHS

The US economic expansion will continue • Accelerations in consumer spending and homebuilding, along with

continued robust capital spending, will support growth.

• As the largest net importer of crude oil, the United States is a beneficiary of lower oil prices, but oil industry investment will be cut in 2015.

• Consumers will boost spending in response to declining gasoline prices and gains in employment, real disposable income, and net worth.

• The recovery in homebuilding will gain momentum as labor markets improve and credit standards ease.

• Interest rates will rise significantly over the next three years as monetary accommodation is withdrawn. The petrochemical industry is exposed to a global market.

Plastics Overview / May 2015

© 2015 IHS

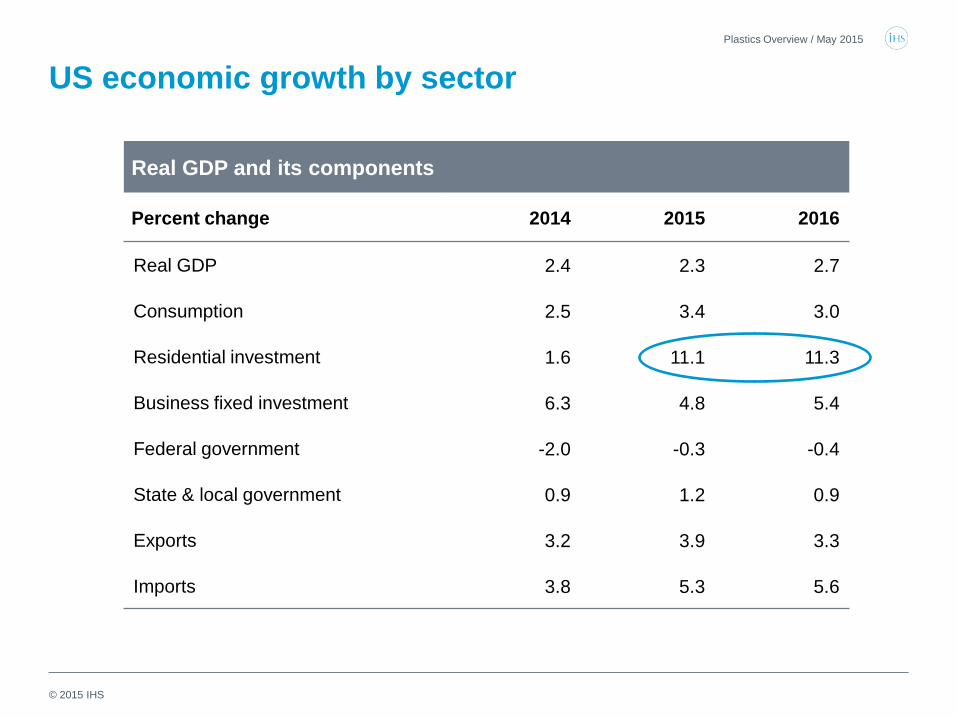

US economic growth by sector

Real GDP and its components

Percent change 2014 2015 2016

Real GDP 2.4 2.3 2.7

Consumption 2.5 3.4 3.0

Residential investment 1.6 11.1 11.3

Business fixed investment 6.3 4.8 5.4

Federal government -2.0 -0.3 -0.4

State & local government 0.9 1.2 0.9

Exports 3.2 3.9 3.3

Imports 3.8 5.3 5.6

Plastics Overview / May 2015

© 2015 IHS

Business Opportunities look slightly brighter for 2015 in the Americas. • U.S. expansion gradually gains momentum and 2015 GPD growth

forecast at 2.8%. • Latin America GDP is expected to grow but at a lower pace of

1.1% for 2015. Mainly due to slow down in Brazil which accounts for almost 50% of the Region’s GDP.

• Presidential elections: Chile (Dec, 2013), Colombia (May 2014), Brazil (Oct/Nov 2014), Argentina (Oct 2015), and Peru ( April 2016) define economic policies in these countries. Most of these elections required a second round, an indication of tight races.

• Mexico should feel the positive impact of the U.S. growing economy with GDP expectations of 2.6%.

Plastics Overview / May 2015

© 2015 IHS

Plastics Overview / May 2015

Polyethylene

© 2015 IHS

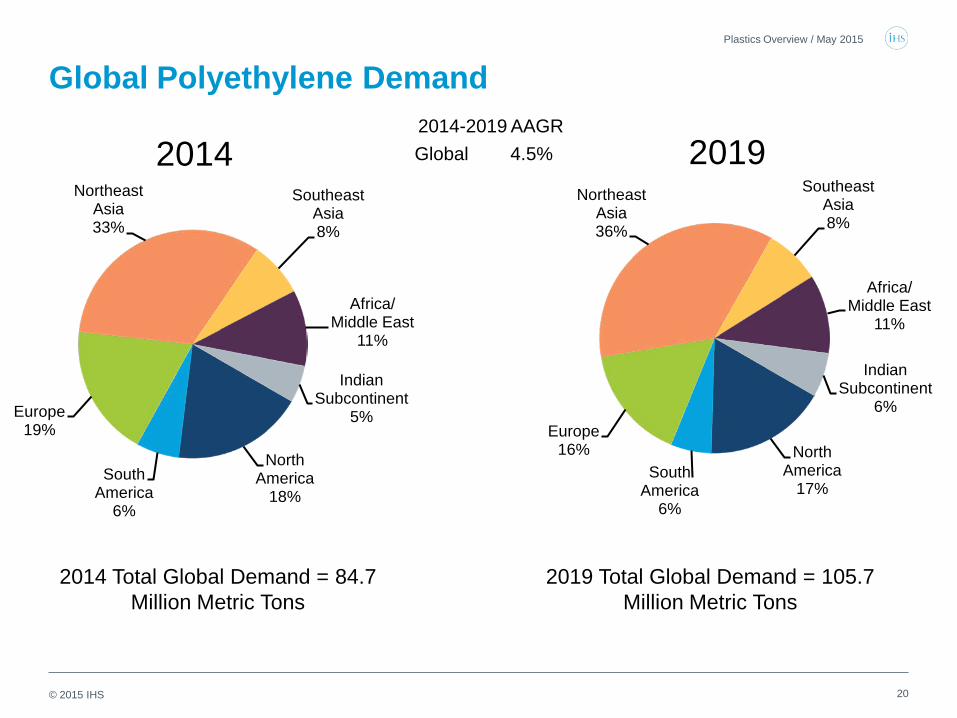

Global Polyethylene Demand

North America

18% South

America 6%

Europe 19%

Northeast Asia 33%

Southeast Asia 8%

Africa/ Middle East

11%

Indian Subcontinent

5%

2014

2014 Total Global Demand = 84.7 Million Metric Tons

2014-2019 AAGR Global 4.5%

2019 Total Global Demand = 105.7 Million Metric Tons

North America

17% South

America 6%

Europe 16%

Northeast Asia 36%

Southeast Asia 8%

Africa/ Middle East

11%

Indian Subcontinent

6%

2019

20

Plastics Overview / May 2015

© 2015 IHS

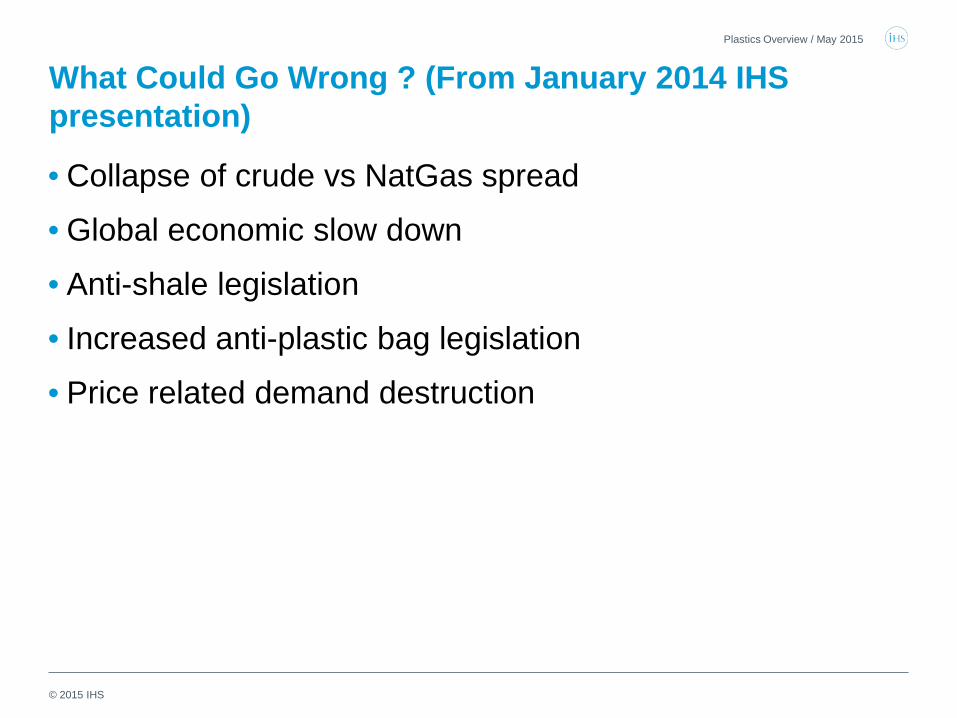

What Could Go Wrong ? (From January 2014 IHS presentation)

• Collapse of crude vs NatGas spread

• Global economic slow down

• Anti-shale legislation

• Increased anti-plastic bag legislation

• Price related demand destruction

Plastics Overview / May 2015

© 2015 IHS

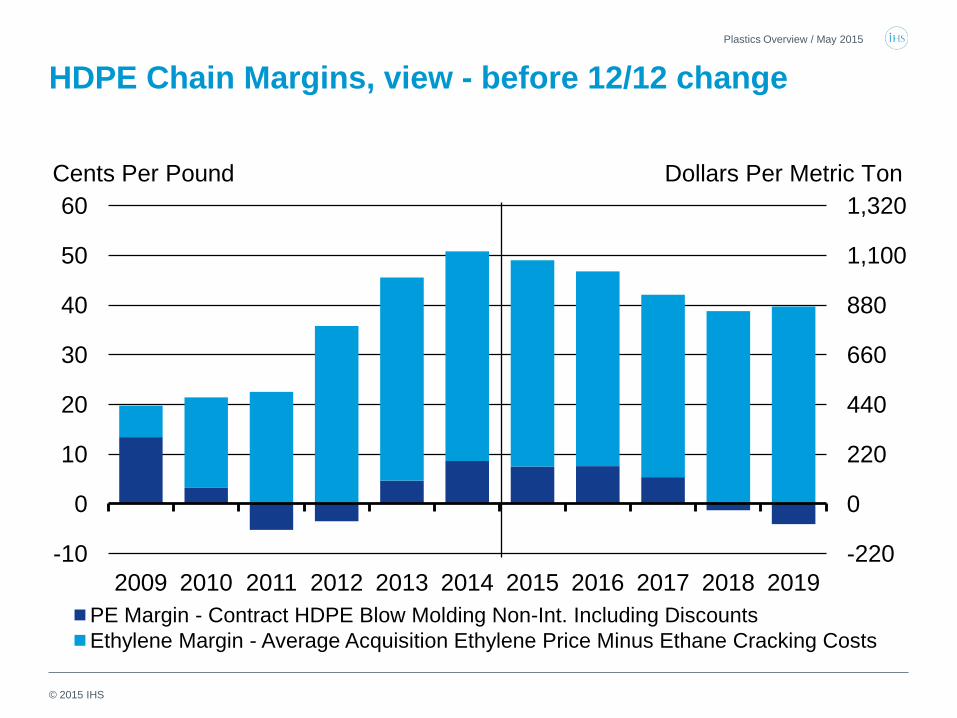

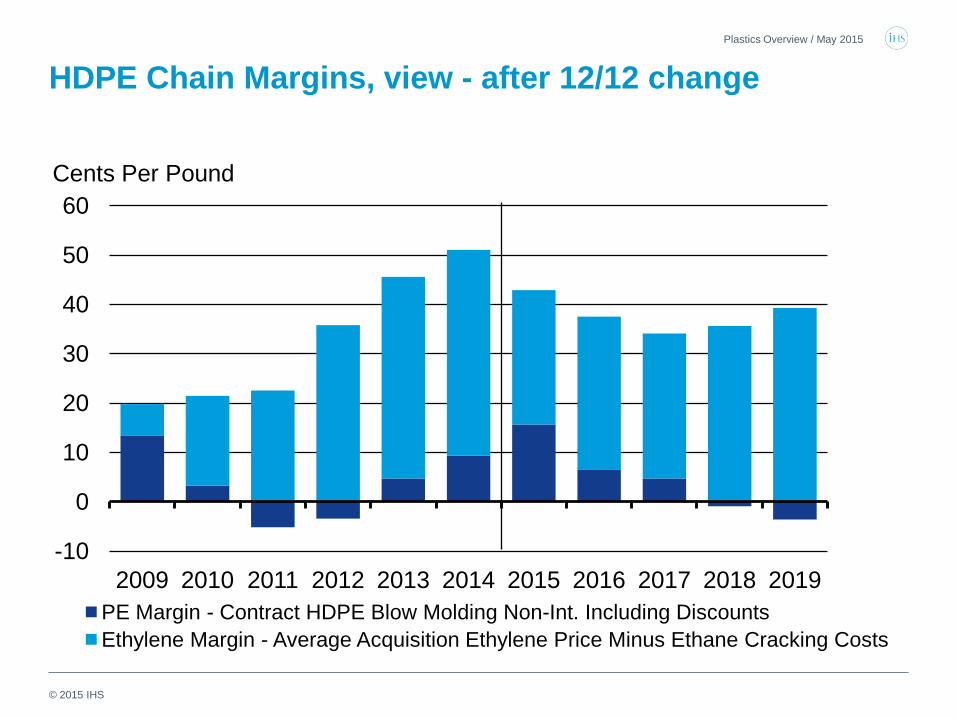

HDPE Chain Margins, view - before 12/12 change Plastics Overview / May 2015

-220

0

220

440

660

880

1,100

1,320

-10

0

10

20

30

40

50

60

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 PE Margin - Contract HDPE Blow Molding Non-Int. Including Discounts Ethylene Margin - Average Acquisition Ethylene Price Minus Ethane Cracking Costs

Cents Per Pound Dollars Per Metric Ton Dollars Per Metric Ton

© 2015 IHS

HDPE Chain Margins, view - after 12/12 change Plastics Overview / May 2015

-10

0

10

20

30

40

50

60

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 PE Margin - Contract HDPE Blow Molding Non-Int. Including Discounts Ethylene Margin - Average Acquisition Ethylene Price Minus Ethane Cracking Costs

Cents Per Pound Dollars Per Metric Ton

© 2015 IHS

0

20

40

60

80

100

Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16

NAM Cash Cost, Integrated NAM LLDPE WEP LLDPE CHINA LLDPE (Spot)

Cents Per Pound

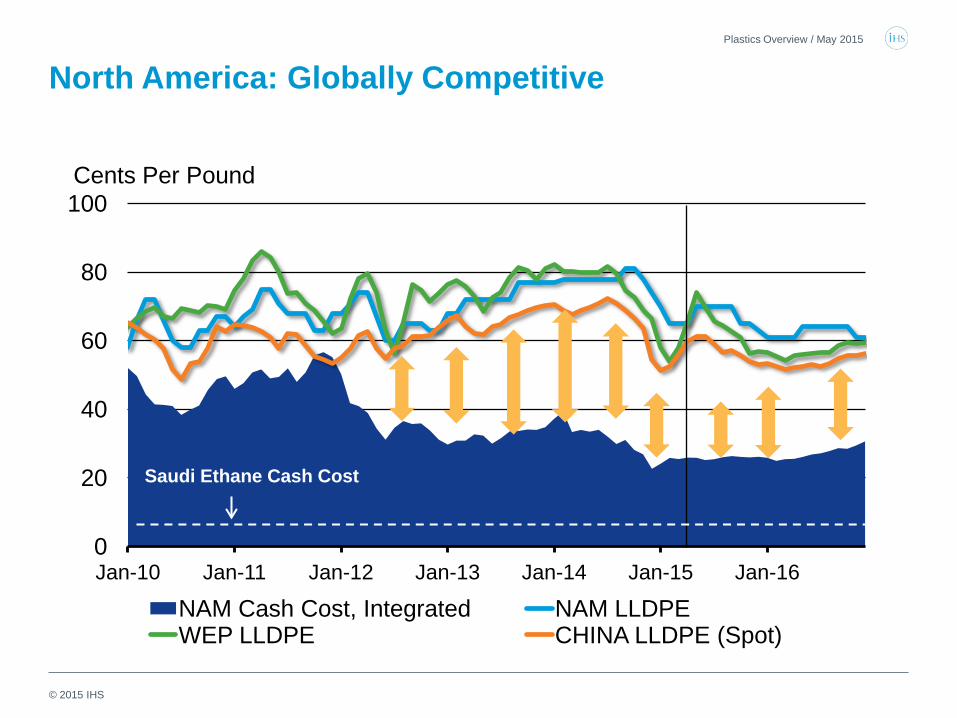

North America: Globally Competitive Plastics Overview / May 2015

Saudi Ethane Cash Cost

© 2015 IHS

2015 Regional PE Forecast Drivers

• Asia prices rebounded after initial declines • Recycle helps set floor, uptick in prime demand likely • Significant restocking after Lunar near year boosted demand

• Continued poor demand in Europe and emerging economies • Europe benefiting from tight supplies, lower Euro and MDE tariffs,

recent closures • Lower crude provides incentives for higher cost producers to run at

higher rates, both in China and Western Europe • Tight supply/demand fundamentals for North America continue into

2015/2016, but global PE price ceiling has been significantly lowered • Elevated arbitrages in 2015/2016 will encourage increased imports of pellets and

finished goods into North America. • Increased incentive to export more product in 2015 with improved supply of existing

assets.

Plastics Overview / May 2015

© 2015 IHS

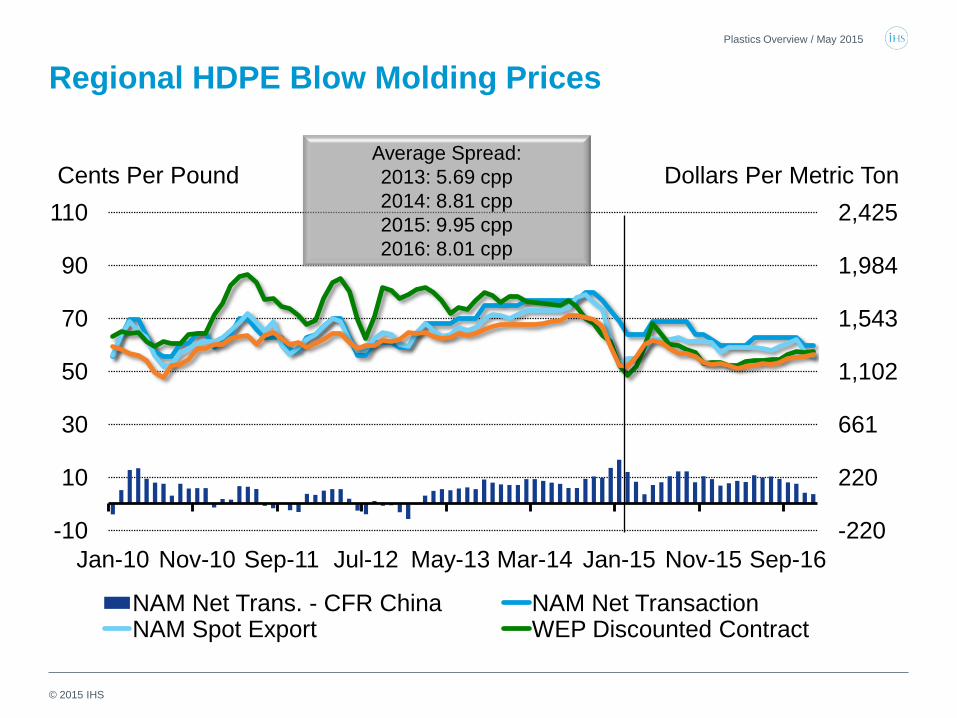

Regional HDPE Blow Molding Prices Plastics Overview / May 2015

-220

220

661

1,102

1,543

1,984

2,425

-10

10

30

50

70

90

110

Jan-10 Nov-10 Sep-11 Jul-12 May-13 Mar-14 Jan-15 Nov-15 Sep-16

NAM Net Trans. - CFR China NAM Net Transaction NAM Spot Export WEP Discounted Contract

Cents Per Pound Dollars Per Metric Ton Average Spread: 2013: 5.69 cpp 2014: 8.81 cpp 2015: 9.95 cpp 2016: 8.01 cpp

© 2015 IHS

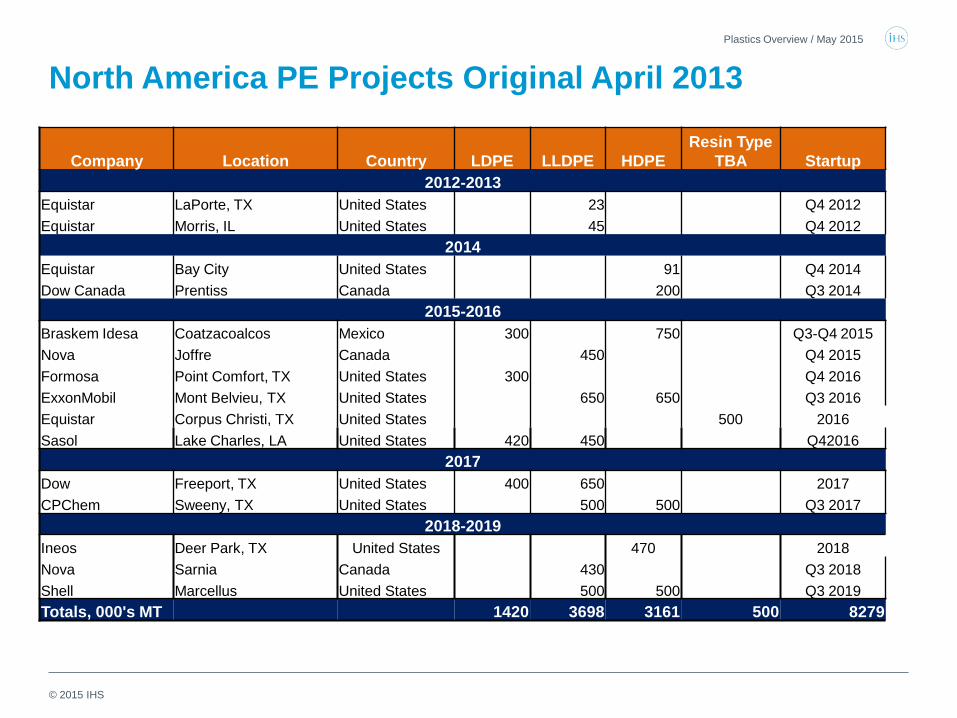

North America PE Projects Original April 2013 Plastics Overview / May 2015

Company Location Country LDPE LLDPE HDPE Resin Type

TBA Startup 2012-2013

Equistar LaPorte, TX United States 23 Q4 2012 Equistar Morris, IL United States 45 Q4 2012

2014 Equistar Bay City United States 91 Q4 2014 Dow Canada Prentiss Canada 200 Q3 2014

2015-2016 Braskem Idesa Coatzacoalcos Mexico 300 750 Q3-Q4 2015 Nova Joffre Canada 450 Q4 2015 Formosa Point Comfort, TX United States 300 Q4 2016 ExxonMobil Mont Belvieu, TX United States 650 650 Q3 2016 Equistar Corpus Christi, TX United States 500 2016 Sasol Lake Charles, LA United States 420 450 Q42016

2017 Dow Freeport, TX United States 400 650 2017 CPChem Sweeny, TX United States 500 500 Q3 2017

2018-2019 Ineos Deer Park, TX United States 470 2018 Nova Sarnia Canada 430 Q3 2018 Shell Marcellus United States 500 500 Q3 2019 Totals, 000's MT 1420 3698 3161 500 8279

© 2015 IHS

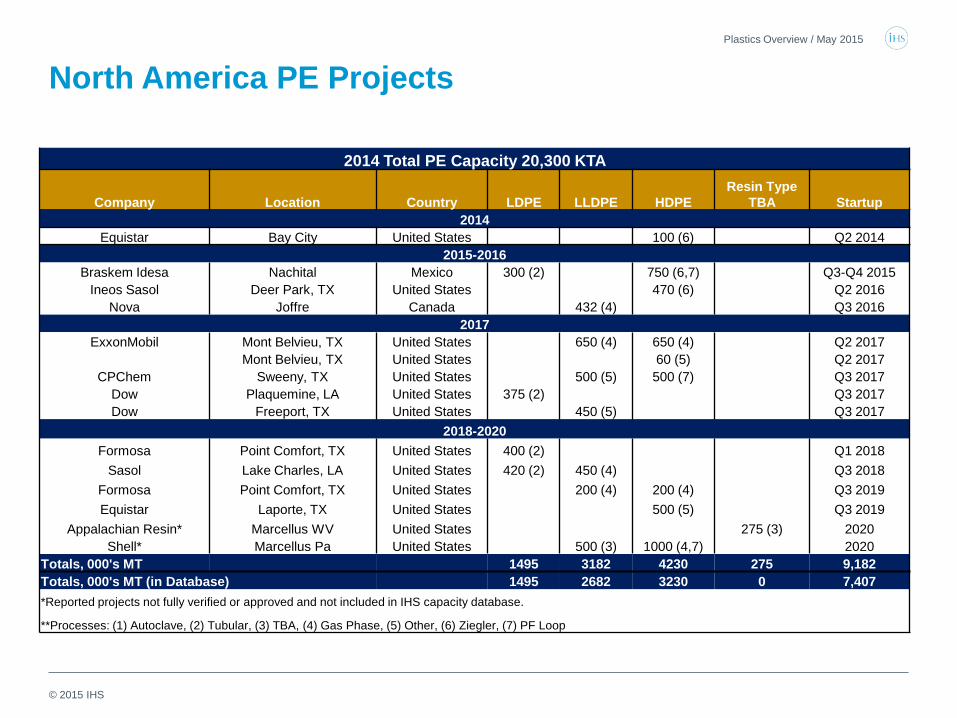

North America PE Projects Plastics Overview / May 2015

2014 Total PE Capacity 20,300 KTA

Company Location Country LDPE LLDPE HDPE Resin Type

TBA Startup 2014

Equistar Bay City United States 100 (6) Q2 2014 2015-2016

Braskem Idesa Nachital Mexico 300 (2) 750 (6,7) Q3-Q4 2015 Ineos Sasol Deer Park, TX United States 470 (6) Q2 2016

Nova Joffre Canada 432 (4) Q3 2016 2017

ExxonMobil Mont Belvieu, TX United States 650 (4) 650 (4) Q2 2017 Mont Belvieu, TX United States 60 (5) Q2 2017

CPChem Sweeny, TX United States 500 (5) 500 (7) Q3 2017 Dow Plaquemine, LA United States 375 (2) Q3 2017 Dow Freeport, TX United States 450 (5) Q3 2017

2018-2020 Formosa Point Comfort, TX United States 400 (2) Q1 2018

Sasol Lake Charles, LA United States 420 (2) 450 (4) Q3 2018 Formosa Point Comfort, TX United States 200 (4) 200 (4) Q3 2019 Equistar Laporte, TX United States 500 (5) Q3 2019

Appalachian Resin* Marcellus WV United States 275 (3) 2020 Shell* Marcellus Pa United States 500 (3) 1000 (4,7) 2020

Totals, 000's MT 1495 3182 4230 275 9,182 Totals, 000's MT (in Database) 1495 2682 3230 0 7,407 *Reported projects not fully verified or approved and not included in IHS capacity database.

**Processes: (1) Autoclave, (2) Tubular, (3) TBA, (4) Gas Phase, (5) Other, (6) Ziegler, (7) PF Loop

© 2015 IHS

-8%

-4%

0%

4%

8%

12%

16%

20%

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

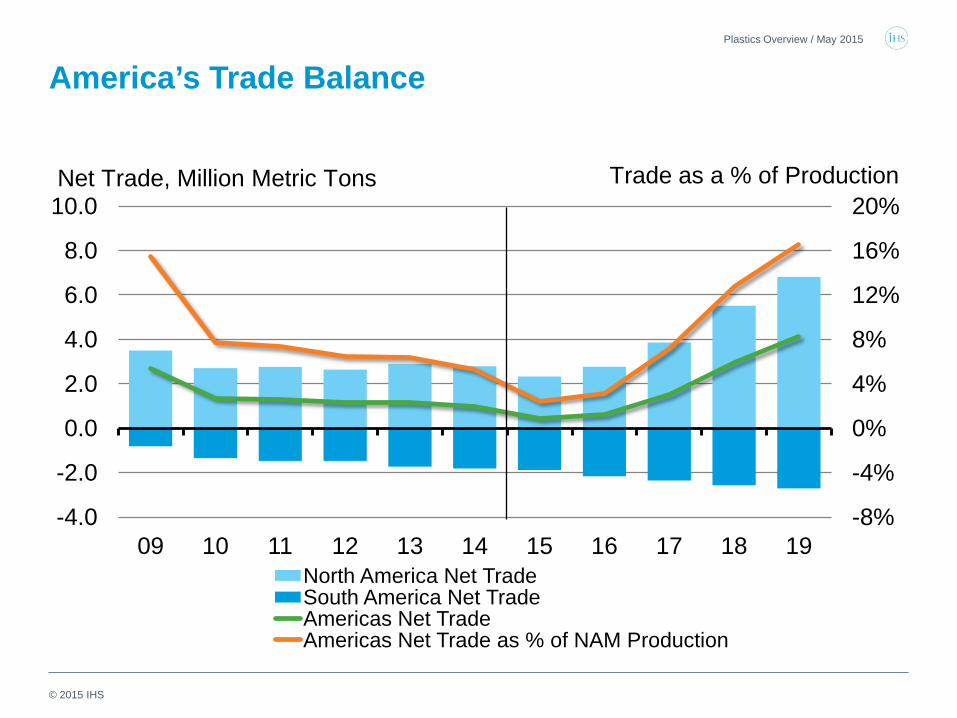

09 10 11 12 13 14 15 16 17 18 19 North America Net Trade South America Net Trade Americas Net Trade Americas Net Trade as % of NAM Production

Net Trade, Million Metric Tons Trade as a % of Production

America’s Trade Balance Plastics Overview / May 2015

© 2015 IHS

North America: PE Key Takeaways

• 7.3 MM tons of expansions included in 2014 -2019 forecast with approx. 5.7 in the US

• Most projects look viable, but start dates for some will slide.

• Cost basis should allow the producers to operate at highest achievable rates, likely 90%+

• Record integrated margins peaked in 2014 but 2015 quite robust

• Increased arbitrage will challenge exports short term but exports of resin and finished goods will increase starting as early as 2016

• Processors will add or repatriate capacity as region becomes more competitive and begins shipping more product around the world

Plastics Overview / May 2015

© 2015 IHS

Presentation

ihs.com

IHS

Polypropylene

CHEMICAL

© 2015 IHS

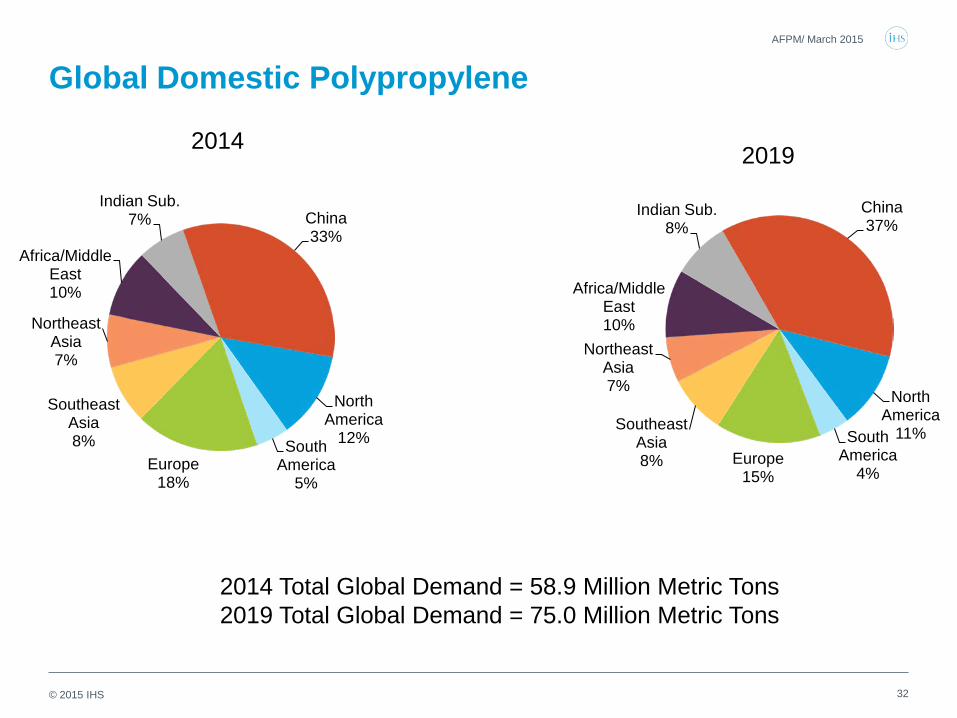

Global Domestic Polypropylene

32

AFPM/ March 2015

North America

12% South America

5% Europe

18%

Southeast Asia 8%

Northeast Asia 7%

Africa/Middle East 10%

Indian Sub. 7% China

33%

2014 Total Global Demand = 58.9 Million Metric Tons 2019 Total Global Demand = 75.0 Million Metric Tons

2014

North America

11% South America

4% Europe

15%

Southeast Asia 8%

Northeast Asia 7%

Africa/Middle East 10%

Indian Sub. 8%

China 37%

2019

© 2015 IHS

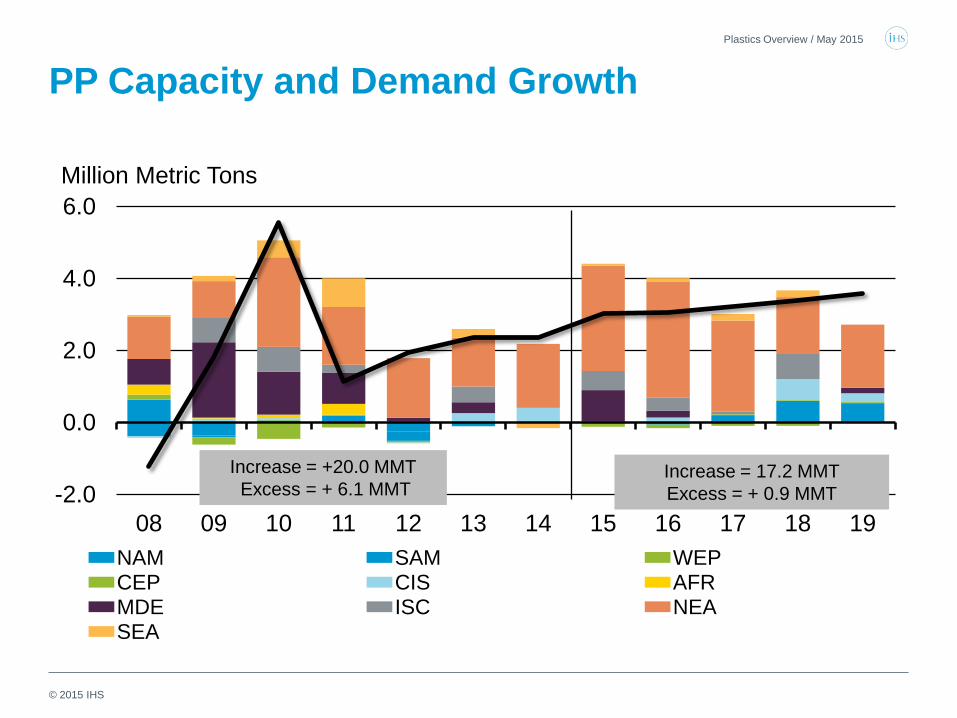

PP Capacity and Demand Growth

-2.0

0.0

2.0

4.0

6.0

08 09 10 11 12 13 14 15 16 17 18 19 NAM SAM WEP CEP CIS AFR MDE ISC NEA SEA Global Demand Change

Million Metric Tons

Increase = +20.0 MMT Excess = + 6.1 MMT

Plastics Overview / May 2015

Increase = 17.2 MMT Excess = + 0.9 MMT

© 2015 IHS

North American PP Update

• 2014 domestic PP consumption (including imports and finished goods) increased 1.6% over 2013

• 2015 Q1 off to a sprinter’s pace ahead of prior year Q1 by over 9%.

• Prices down 29.5 cents since October highs

• Planned / Unplanned outages continue to be an issue; however first quarter operating rates averaging 90% best first quarter since 2008

• Producers are aggressively pushing for margin increases; next increment June? Reinvestment economics in sight?

• No new capacity planned as market forecasted to get tighter with imports expected to increase

Plastics Overview / May 2015

© 2015 IHS

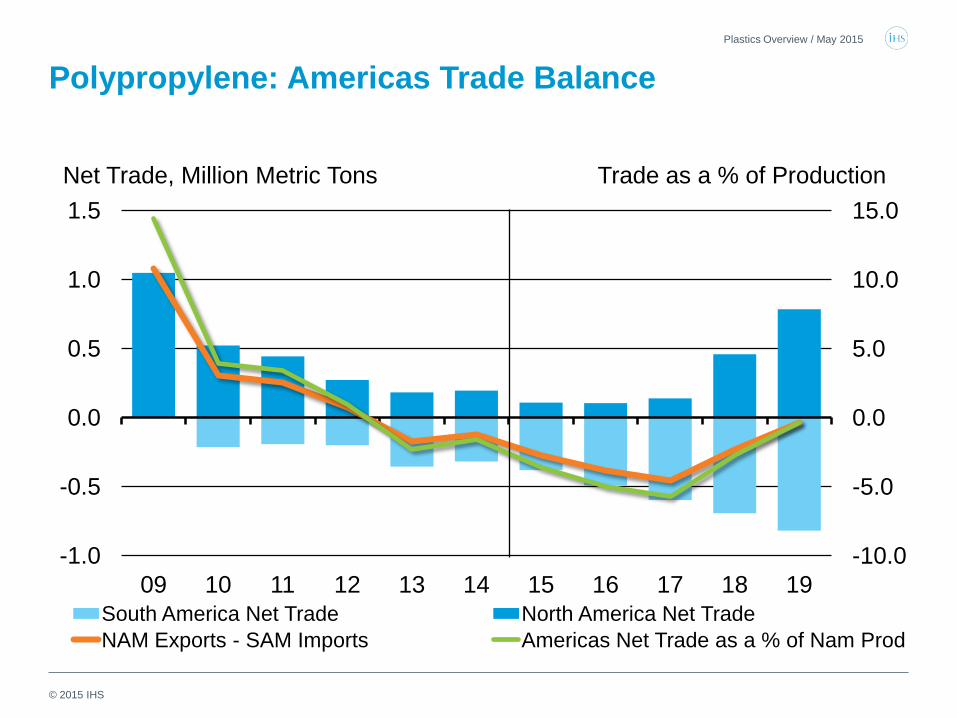

Polypropylene: Americas Trade Balance

-10.0

-5.0

0.0

5.0

10.0

15.0

-1.0

-0.5

0.0

0.5

1.0

1.5

09 10 11 12 13 14 15 16 17 18 19 South America Net Trade North America Net Trade NAM Exports - SAM Imports Americas Net Trade as a % of Nam Prod

Net Trade, Million Metric Tons Trade as a % of Production

Plastics Overview / May 2015

© 2015 IHS

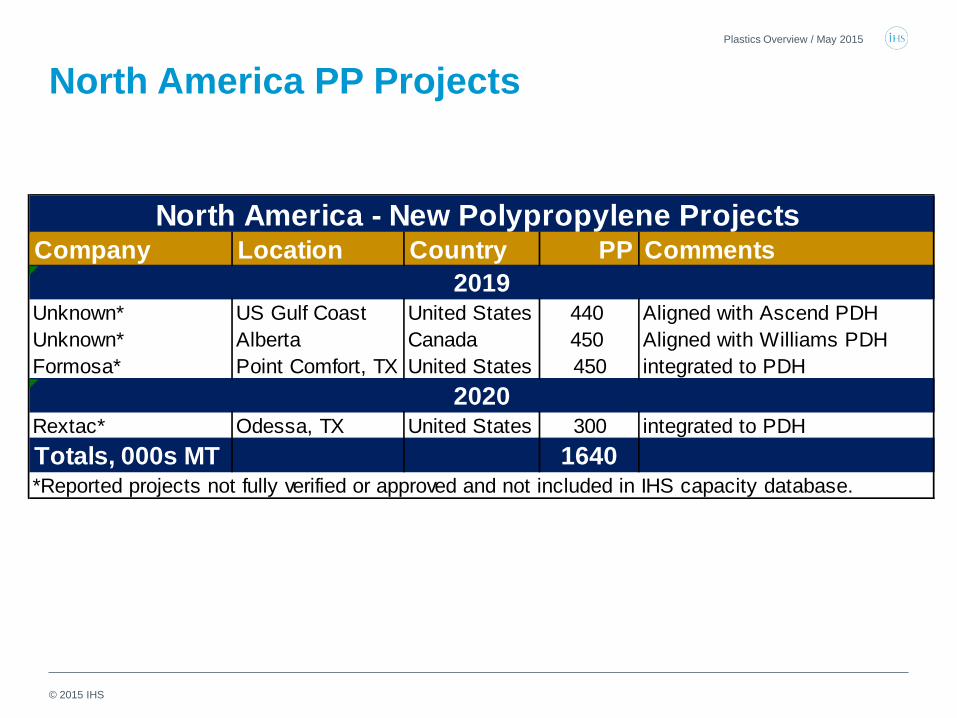

North America PP Projects Plastics Overview / May 2015

Company Location Country PP Comments

Unknown* US Gulf Coast United States 440 Aligned with Ascend PDHUnknown* Alberta Canada 450 Aligned with Williams PDHFormosa* Point Comfort, TX United States 450 integrated to PDH

Rextac* Odessa, TX United States 300 integrated to PDHTotals, 000s MT 1640

North America - New Polypropylene Projects

2019

*Reported projects not fully verified or approved and not included in IHS capacity database.

2020

© 2015 IHS

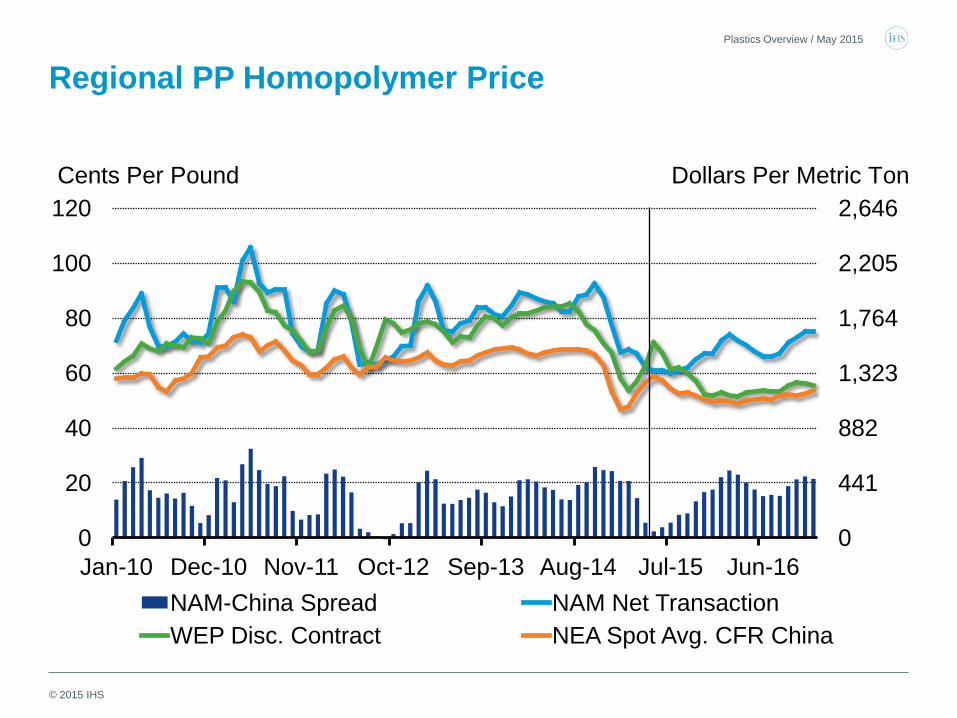

Regional PP Homopolymer Price

0

441

882

1,323

1,764

2,205

2,646

0

20

40

60

80

100

120

Jan-10 Dec-10 Nov-11 Oct-12 Sep-13 Aug-14 Jul-15 Jun-16 NAM-China Spread NAM Net Transaction WEP Disc. Contract NEA Spot Avg. CFR China

Dollars Per Metric Ton Cents Per Pound

Plastics Overview / May 2015

© 2015 IHS

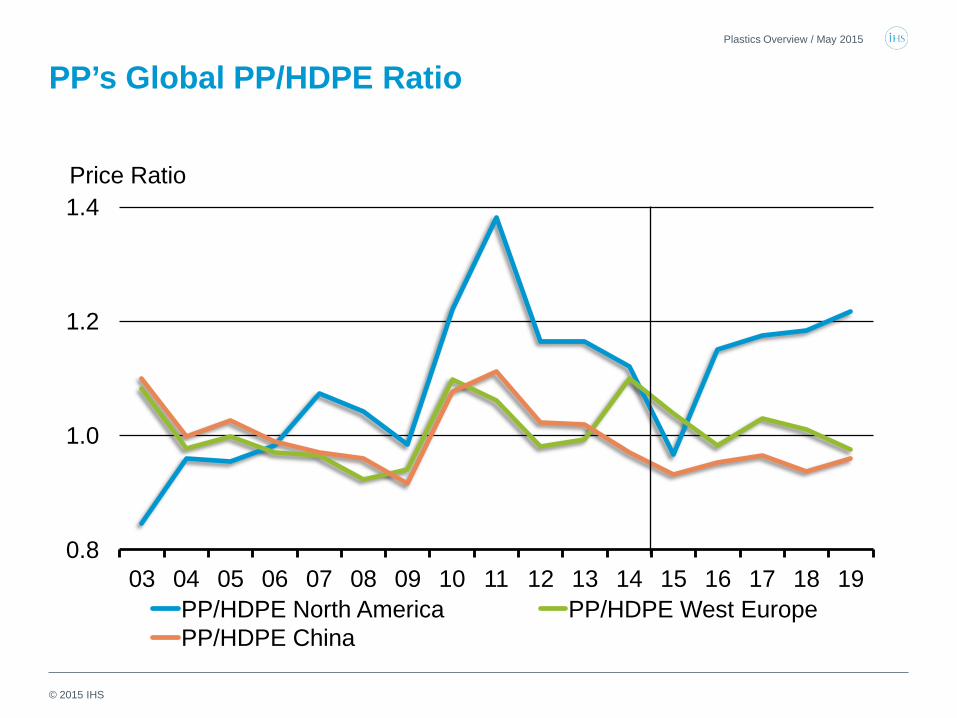

PP’s Global PP/HDPE Ratio

0.8

1.0

1.2

1.4

03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18 19 PP/HDPE North America PP/HDPE West Europe PP/HDPE China

Price Ratio Price Ratio

Plastics Overview / May 2015

© 2015 IHS

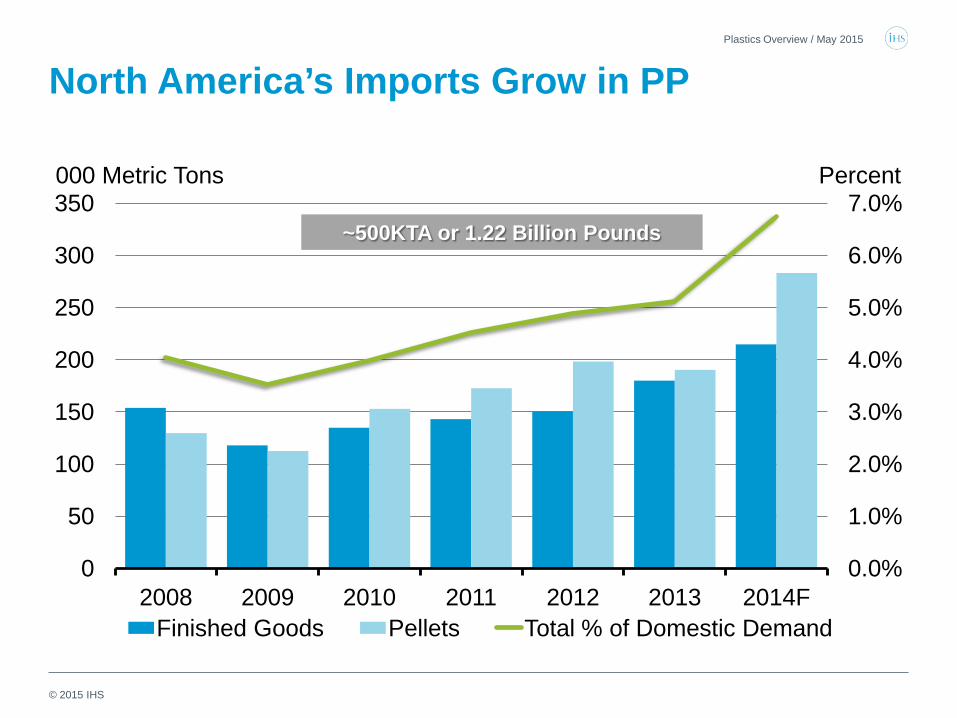

North America’s Imports Grow in PP Plastics Overview / May 2015

~500KTA or 1.22 Billion Pounds

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

0

50

100

150

200

250

300

350

2008 2009 2010 2011 2012 2013 2014F Finished Goods Pellets Total % of Domestic Demand

000 Metric Tons Percent

© 2015 IHS

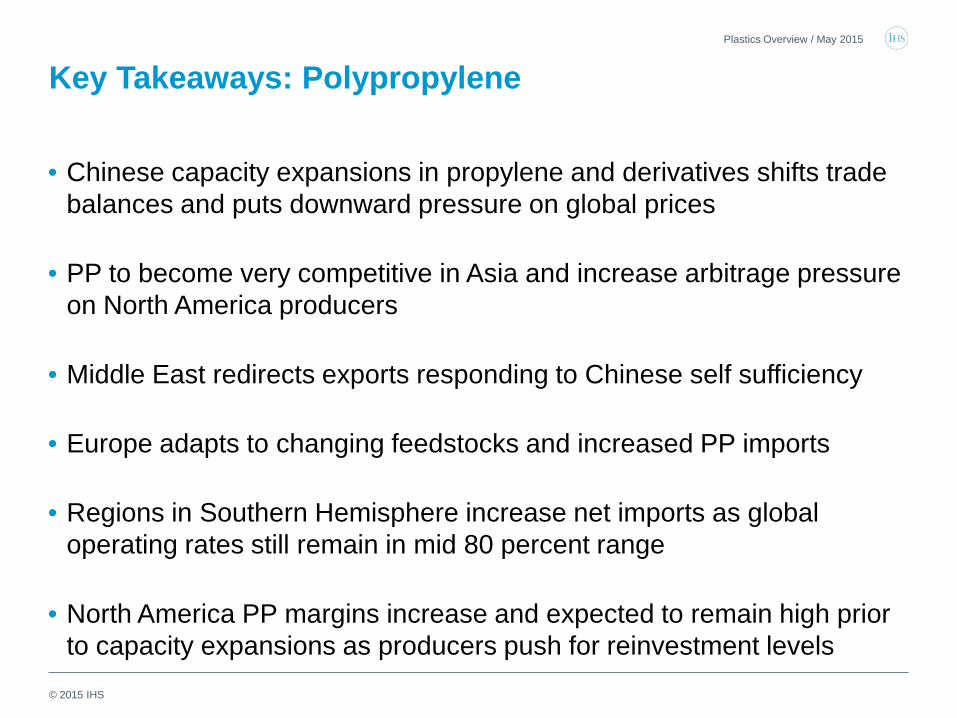

Key Takeaways: Polypropylene • Chinese capacity expansions in propylene and derivatives shifts trade

balances and puts downward pressure on global prices

• PP to become very competitive in Asia and increase arbitrage pressure on North America producers

• Middle East redirects exports responding to Chinese self sufficiency

• Europe adapts to changing feedstocks and increased PP imports

• Regions in Southern Hemisphere increase net imports as global operating rates still remain in mid 80 percent range

• North America PP margins increase and expected to remain high prior to capacity expansions as producers push for reinvestment levels

Plastics Overview / May 2015

© 2015 IHS

Expanded Polystyrene and Polystyrene

Plastics Overview / May 2015

© 2015 IHS

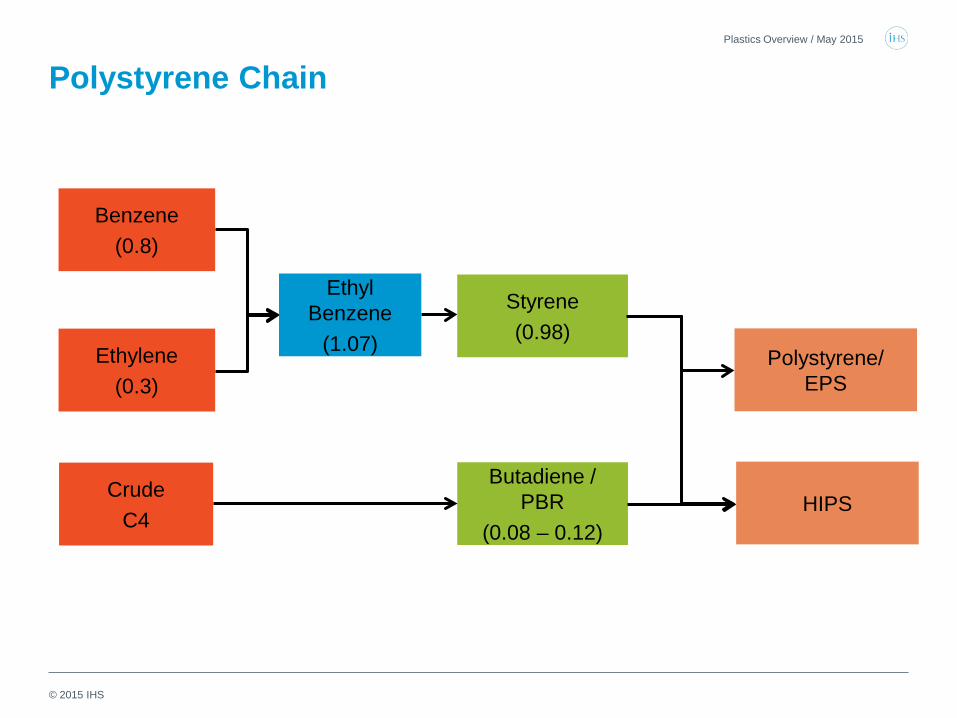

Polystyrene Chain Plastics Overview / May 2015

Polystyrene/ EPS

Benzene (0.8)

Ethylene (0.3)

Crude C4

Ethyl Benzene

(1.07)

Styrene (0.98)

Butadiene / PBR

(0.08 – 0.12) HIPS

© 2015 IHS

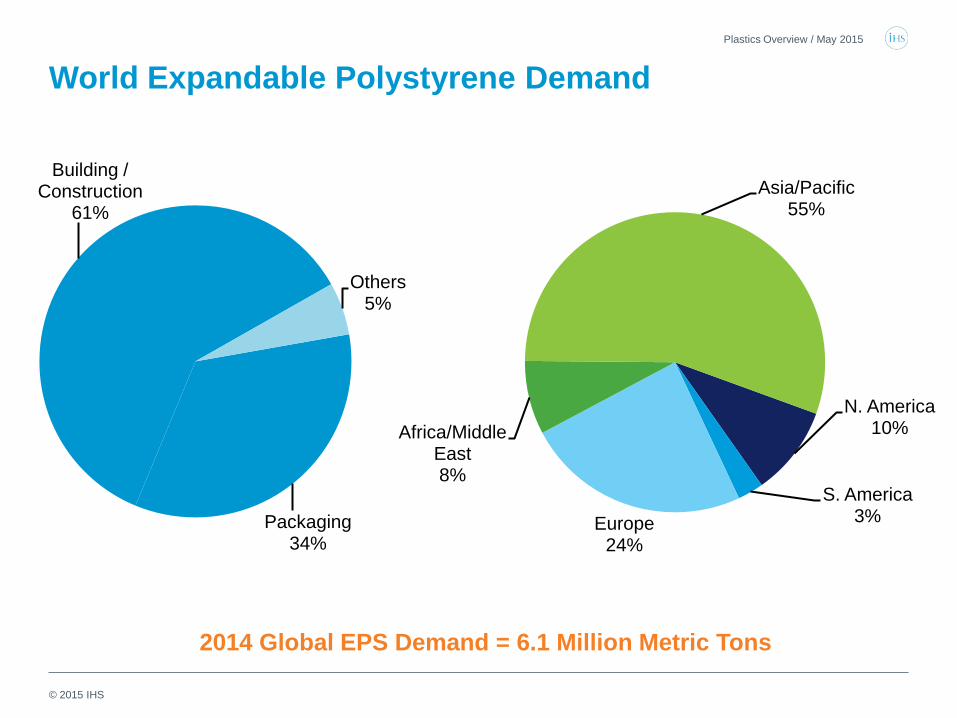

Packaging 34%

Building / Construction

61%

Others 5%

Plastics Overview / May 2015

World Expandable Polystyrene Demand

2014 Global EPS Demand = 6.1 Million Metric Tons

N. America 10%

S. America 3% Europe

24%

Africa/Middle East 8%

Asia/Pacific 55%

© 2015 IHS

Plastics Overview / May 2015

Key Issues For SM and EPS

• California's Office of Environmental Health Hazard Assessment (OEHHA) intends to list styrene as known to the state to cause cancer under Proposition 65

• New Shipping code provision – additional shipping costs - higher price for Asian imports

• Foam cups and containers especially in food packaging facing bans – New York will be implementing the ban on EPS cups and single serve food packaging

© 2015 IHS

Key Take-aways

• The drop in crude oil have lowered the cost of EPS feedstocks - benzene and styrene

• Margins in North America have improved

• EPS capacity surplus globally – mainly Asia

• North America demand growth is strong, while Asia and Europe slowdown.

• Demand from Construction sector leading growth in EPS.

Plastics Overview / May 2015

© 2015 IHS

N. America 20%

S. America 6%

W. Europe 15%

C. Europe 3%

CIS & Baltics 3%

Africa 2%

Middle East 6%

Indian Subc. 3%

NE Asia 37%

SE Asia 5%

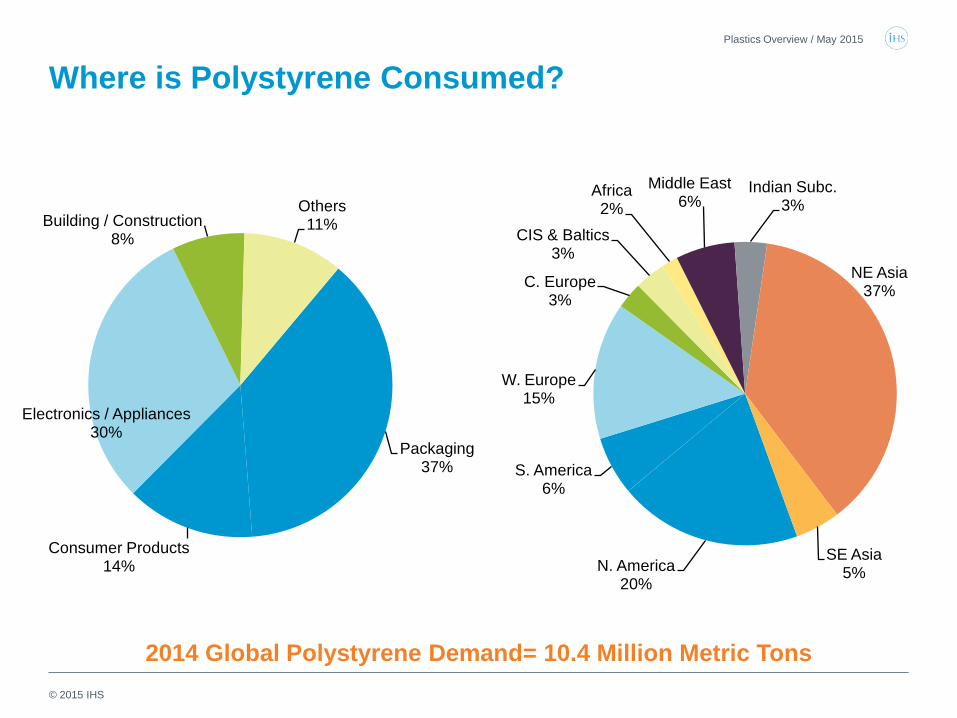

2014 Global Polystyrene Demand= 10.4 Million Metric Tons

Plastics Overview / May 2015

Where is Polystyrene Consumed?

Packaging 37%

Consumer Products 14%

Electronics / Appliances 30%

Building / Construction 8%

Others 11%

© 2015 IHS

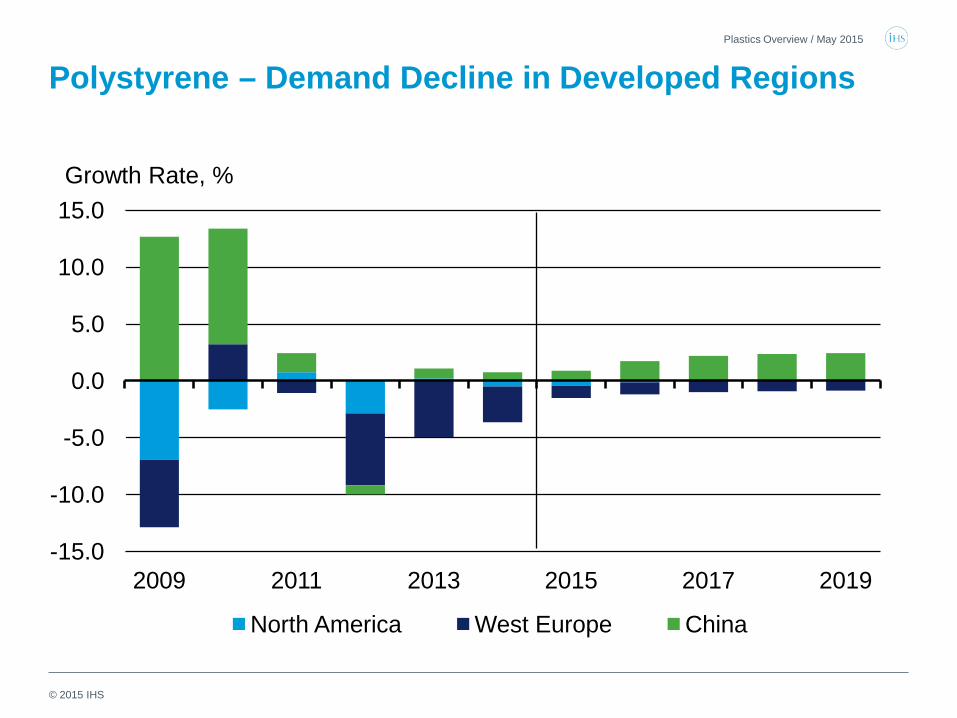

Polystyrene – Demand Decline in Developed Regions Plastics Overview / May 2015

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

2009 2011 2013 2015 2017 2019

North America West Europe China

Growth Rate, %

© 2015 IHS

Plastics Overview / May 2015

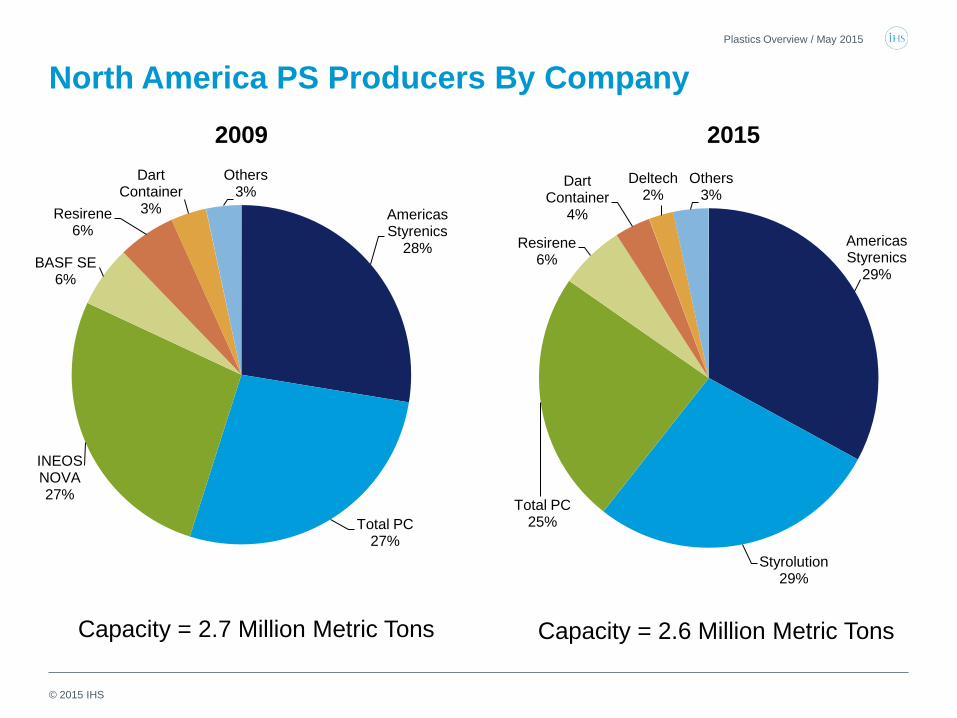

North America PS Producers By Company 2015 2009

Capacity = 2.6 Million Metric Tons Capacity = 2.7 Million Metric Tons

Americas Styrenics

28%

Total PC 27%

INEOS NOVA 27%

BASF SE 6%

Resirene 6%

Dart Container

3%

Others 3%

Americas Styrenics

29%

Styrolution 29%

Total PC 25%

Resirene 6%

Dart Container

4%

Deltech 2%

Others 3%

© 2015 IHS

Conclusions • Global demand for polystyrene growing lower than GDP

• Slowdown in demand in China has slowed global demand growth

• Polystyrene market still in a oversupply situation globally

• Rationalization of capacity has been seen in North America and West Europe,

• Following historically high prices in 2014, the drop in crude and benzene prices has resulted in lower prices for PS

• North America will see demand remain stable and operating rates and margins improve

Plastics Overview / May 2015

© 2015 IHS

Polyvinyl Chloride

Plastics Overview / May 2015

© 2015 IHS

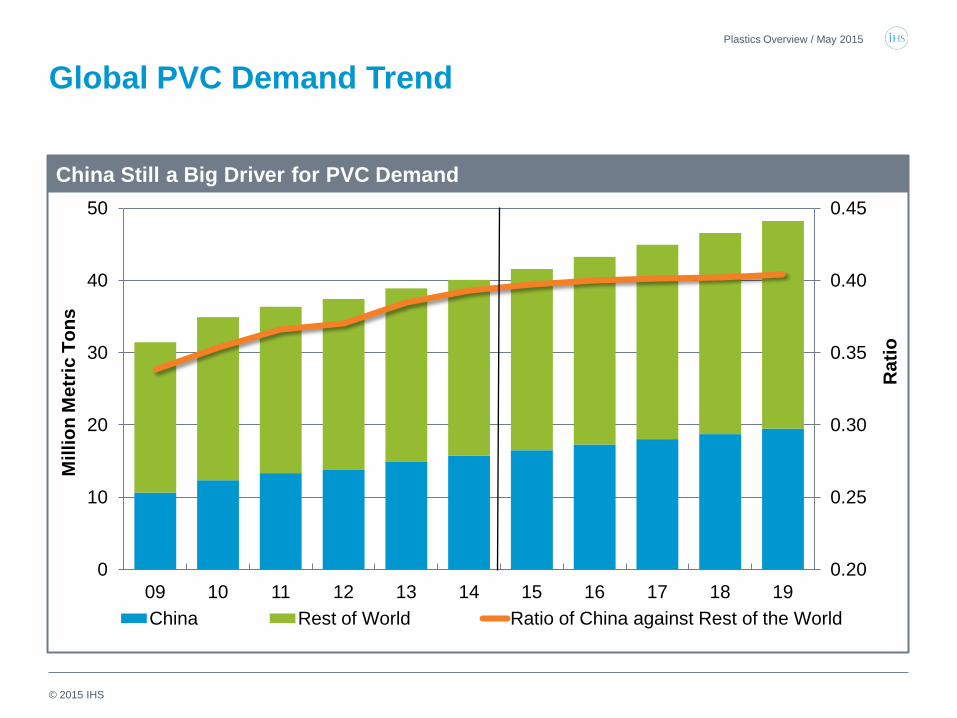

Global PVC Demand Trend

0.20

0.25

0.30

0.35

0.40

0.45

0

10

20

30

40

50

09 10 11 12 13 14 15 16 17 18 19 China Rest of World Ratio of China against Rest of the World

China Still a Big Driver for PVC Demand

Mill

ion

Met

ric T

ons

Rat

io

Plastics Overview / May 2015

© 2015 IHS

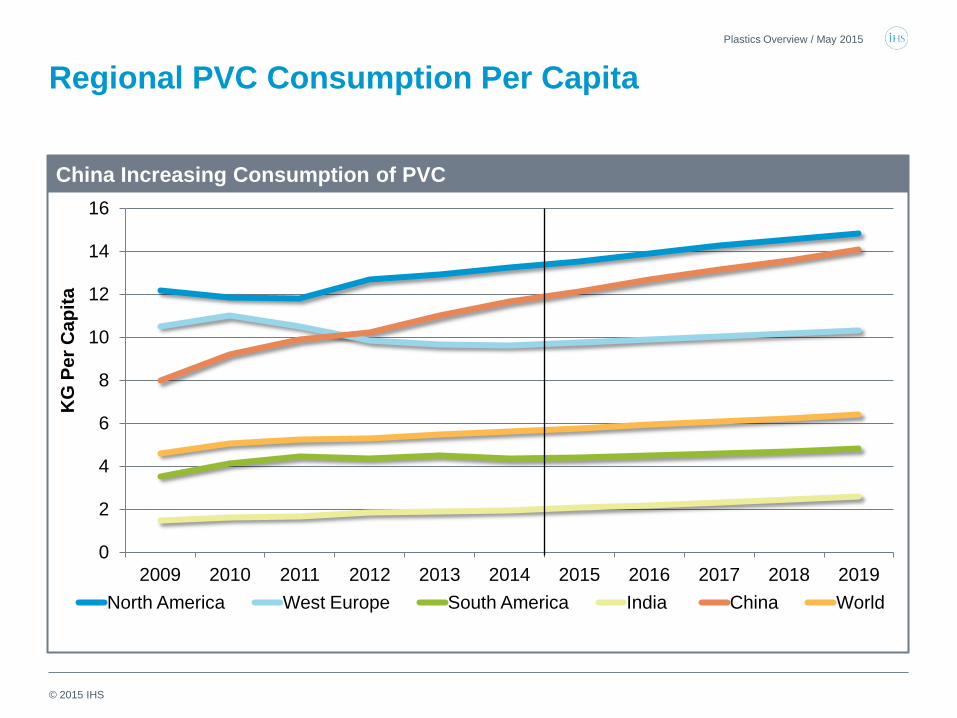

Regional PVC Consumption Per Capita

0

2

4

6

8

10

12

14

16

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 North America West Europe South America India China World

China Increasing Consumption of PVC

KG

Per

Cap

ita

Plastics Overview / May 2015

© 2015 IHS

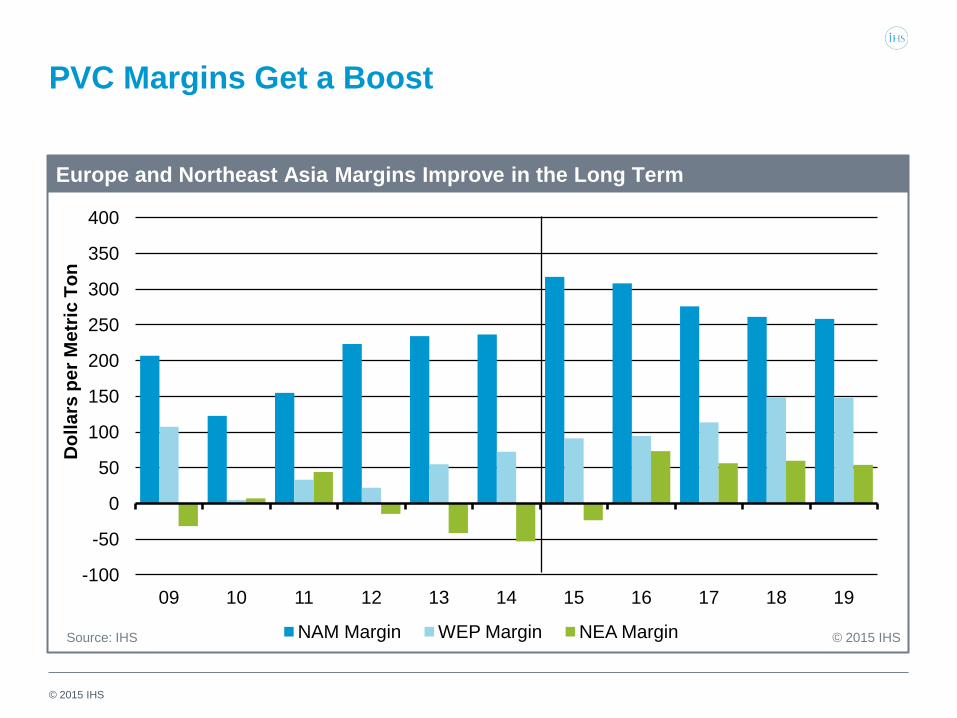

PVC Margins Get a Boost Plastics Overview / May 2015

Dol

lars

per

Met

ric T

on

Source: IHS © 2015 IHS

Europe and Northeast Asia Margins Improve in the Long Term

-100

-50

0

50

100

150

200

250

300

350

400

09 10 11 12 13 14 15 16 17 18 19

NAM Margin WEP Margin NEA Margin

© 2015 IHS

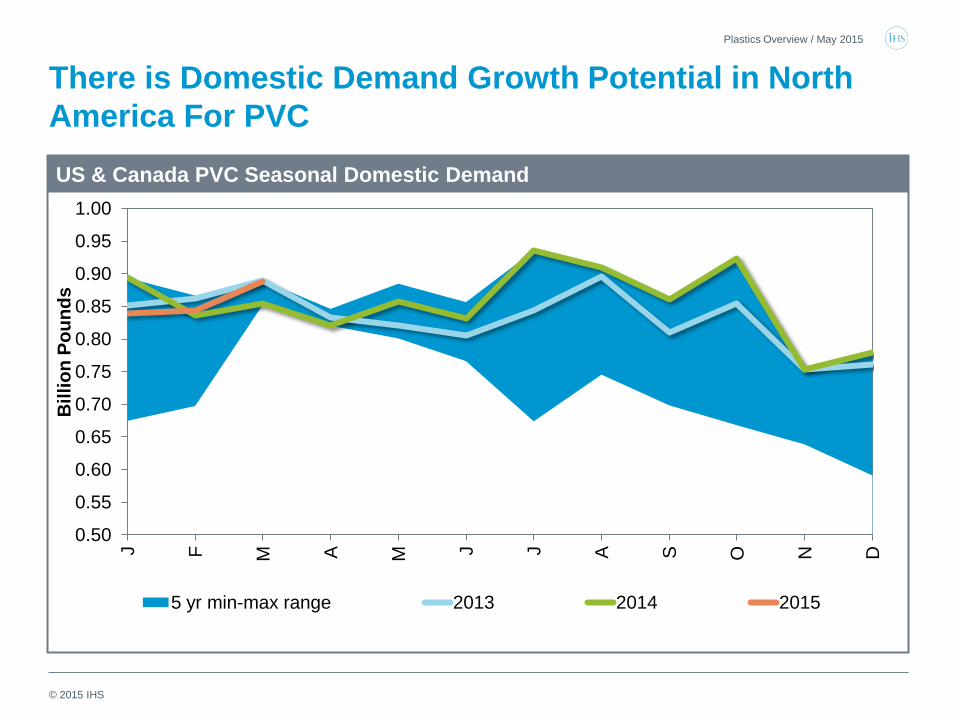

There is Domestic Demand Growth Potential in North America For PVC

0.50

0.55

0.60

0.65

0.70

0.75

0.80

0.85

0.90

0.95

1.00

J F M

A

M J J A

S

O

N

D

Bill

ion

Poun

ds

5 yr min-max range 2013 2014 2015

US & Canada PVC Seasonal Domestic Demand

Plastics Overview / May 2015

© 2015 IHS

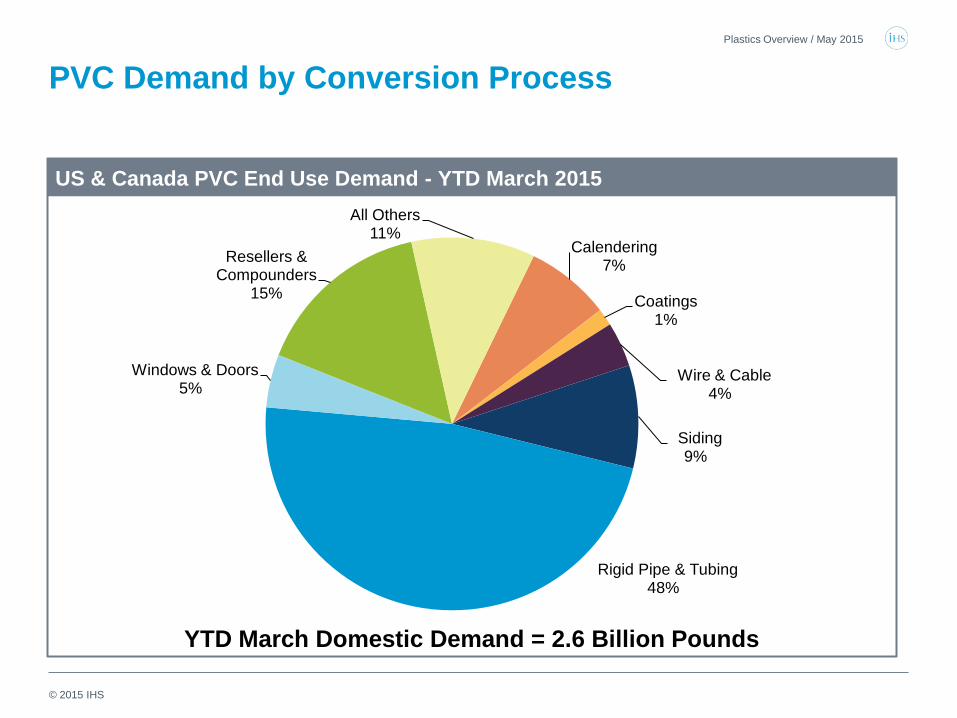

PVC Demand by Conversion Process

Calendering 7%

Coatings 1%

Wire & Cable 4%

Siding 9%

Rigid Pipe & Tubing 48%

Windows & Doors 5%

Resellers & Compounders

15%

All Others 11%

YTD March Domestic Demand = 2.6 Billion Pounds

US & Canada PVC End Use Demand - YTD March 2015

Plastics Overview / May 2015

© 2015 IHS

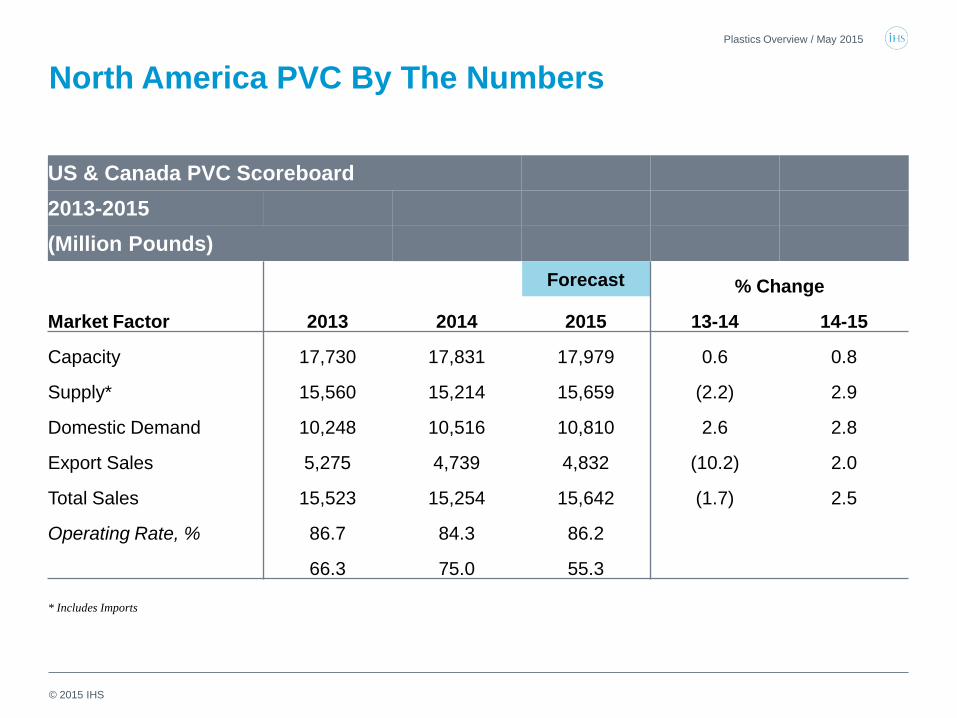

North America PVC By The Numbers

US & Canada PVC Scoreboard

2013-2015

(Million Pounds)

Forecast % Change

Market Factor 2013 2014 2015 13-14 14-15

Capacity 17,730 17,831 17,979 0.6 0.8

Supply* 15,560 15,214 15,659 (2.2) 2.9

Domestic Demand 10,248 10,516 10,810 2.6 2.8

Export Sales 5,275 4,739 4,832 (10.2) 2.0

Total Sales 15,523 15,254 15,642 (1.7) 2.5

Operating Rate, % 86.7 84.3 86.2

66.3 75.0 55.3

* Includes Imports

Plastics Overview / May 2015

© 2015 IHS

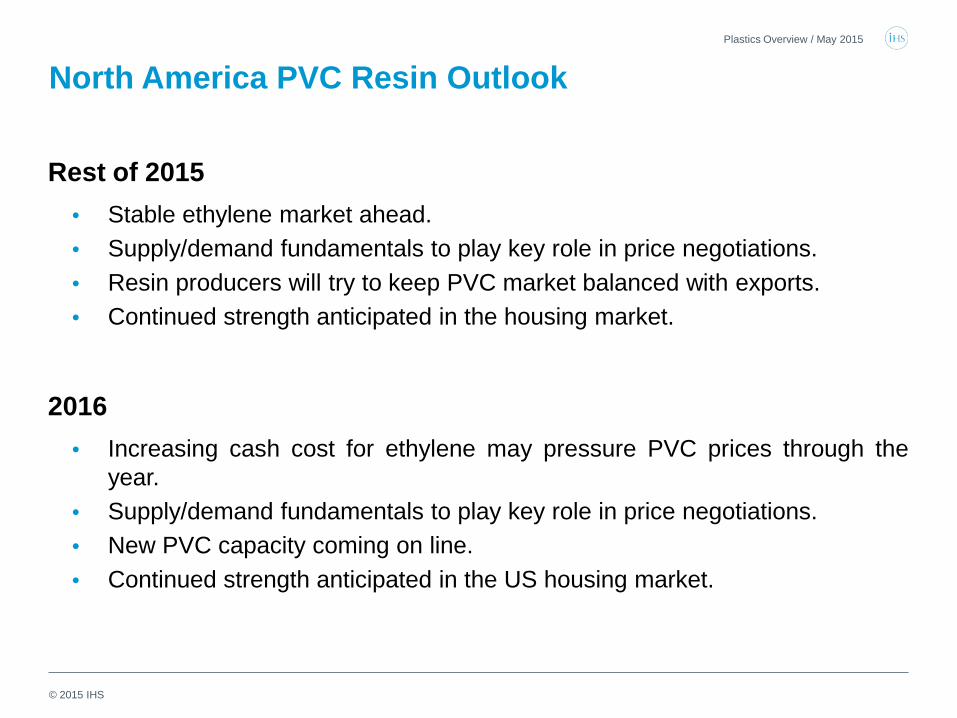

North America PVC Resin Outlook

Rest of 2015 • Stable ethylene market ahead. • Supply/demand fundamentals to play key role in price negotiations. • Resin producers will try to keep PVC market balanced with exports. • Continued strength anticipated in the housing market.

2016 • Increasing cash cost for ethylene may pressure PVC prices through the

year. • Supply/demand fundamentals to play key role in price negotiations. • New PVC capacity coming on line. • Continued strength anticipated in the US housing market.

Plastics Overview / May 2015

© 2015 IHS

Key Take Aways

• North America advantaged cash cost position continues for PVC, however currency appreciation in combination with the energy swing have changed the competitive landscape in the short term.

• Ethylene availability is key for vinyl capacity expansions in the future for non integrated producers.

• Domestic demand in North America will continue to grow hand in hand with activity mainly in the construction market.

PVC Demand in North America is Doing Better Than Before

Plastics Overview / May 2015

© 2015 IHS

PET

Plastics Overview / May 2015

© 2015 IHS

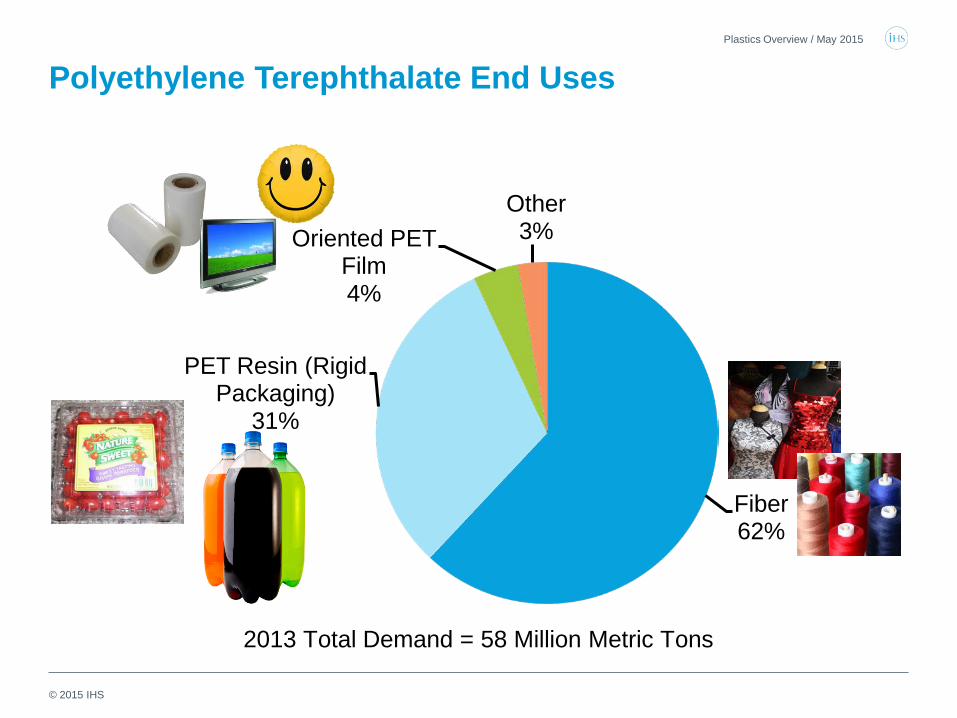

Fiber 62%

PET Resin (Rigid Packaging)

31%

Oriented PET Film 4%

Other 3%

2013 Total Demand = 58 Million Metric Tons

Polyethylene Terephthalate End Uses Plastics Overview / May 2015

© 2015 IHS

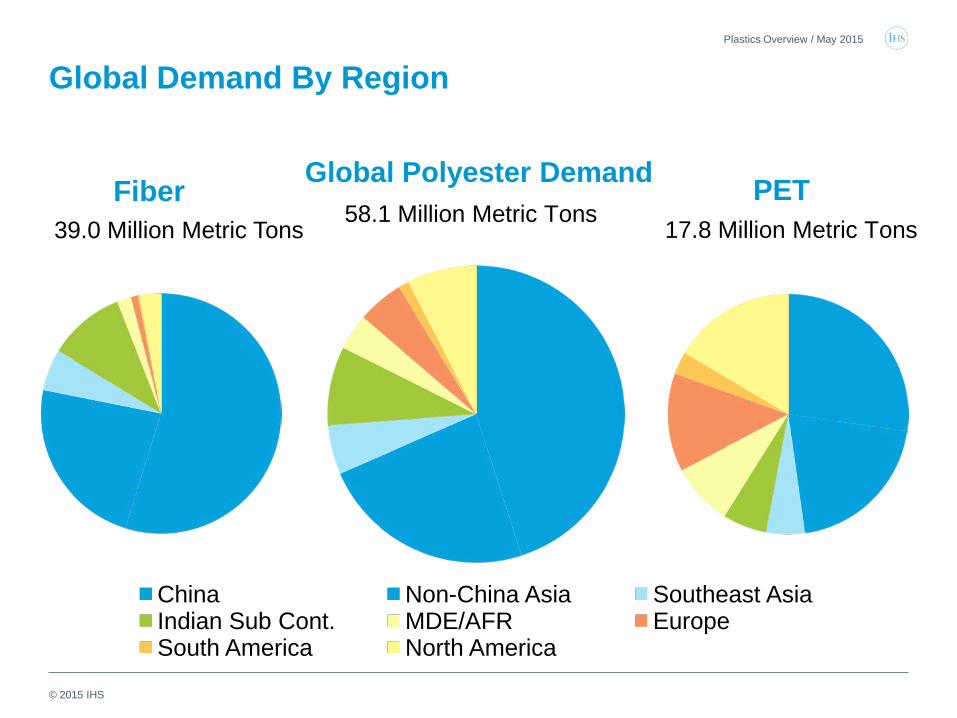

Global Polyester Demand

China Non-China Asia Southeast Asia Indian Sub Cont. MDE/AFR Europe South America North America

58.1 Million Metric Tons

Global Demand By Region

Fiber 39.0 Million Metric Tons

17.8 Million Metric Tons

PET

Plastics Overview / May 2015

© 2015 IHS

Global PET Supply/Demand Notes

• With very low barriers to entry, capacity growth continues to outpace demand growth despite massive overcapacity.

• Asia continues to be the incremental supplier to the world capping prices in any region at Asian cash costs plus freight and duty.

• Overall industry cost structure is falling with new world scale assets and falling margins in PX.

Plastics Overview / May 2015

© 2015 IHS

30 40 50 60 70 80 90 100

-2.0

-1.0

0.0

1.0

2.0

3.0

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

DAK Indorama M&G Nan Ya Selenis Eastman Invista Wellman Hypothetical Virgin Resin Demand Growth Excess Regional Capacity Operating Rate

Operating Rate, Percent Million Metric Tons

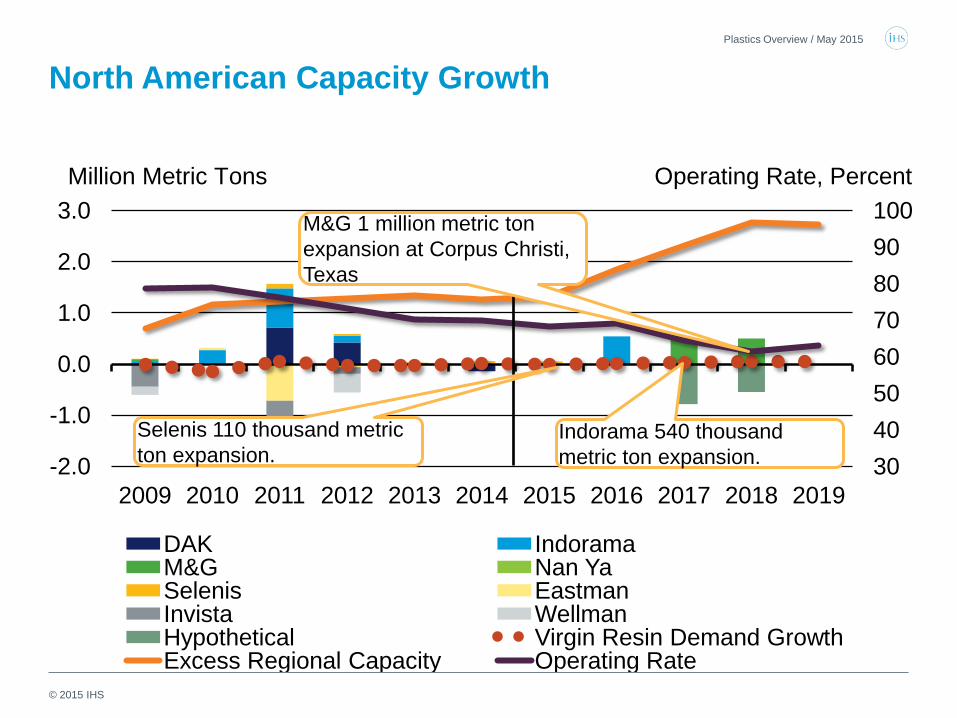

North American Capacity Growth

M&G 1 million metric ton expansion at Corpus Christi, Texas

Indorama 540 thousand metric ton expansion.

Selenis 110 thousand metric ton expansion.

Plastics Overview / May 2015

© 2015 IHS

North America PET Supply Notes

• M&G – 1.2 million tons PTA & 1 million tons PET at Corpus Christi around 2016

• Indorama - 540 thousand ton PET plant at Decatur with completion by Q4 2015.

• Combined announcements will increase North American capacity by over 35 percent

• North American domestic demand will increase less than 7 percent over the same period.

Plastics Overview / May 2015

© 2015 IHS

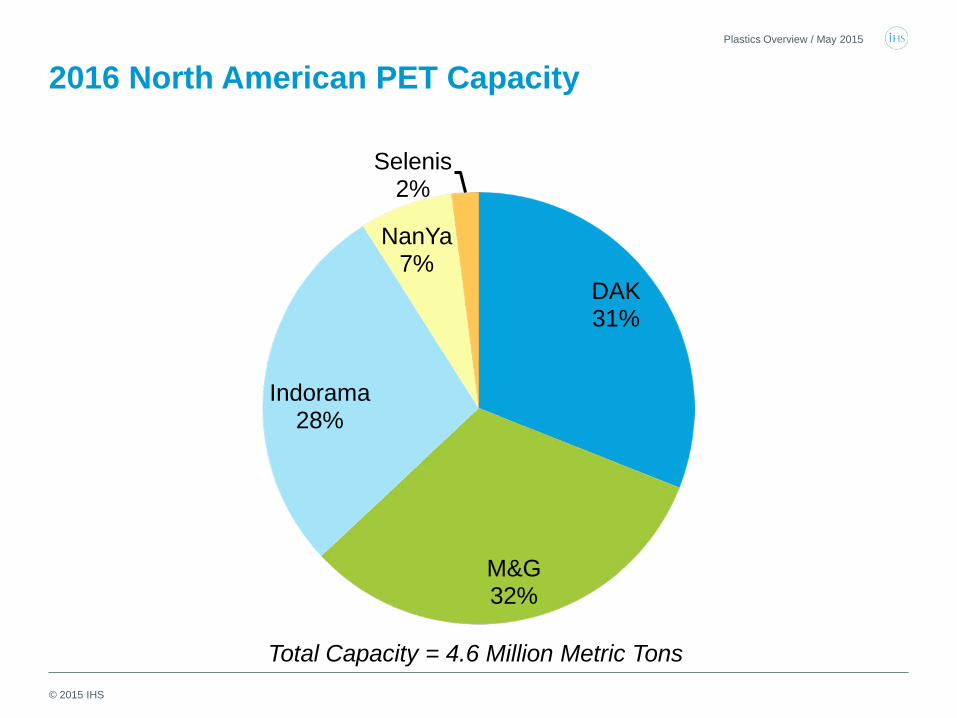

2016 North American PET Capacity

DAK 31%

M&G 32%

Indorama 28%

NanYa 7%

Selenis 2%

Total Capacity = 4.6 Million Metric Tons

Plastics Overview / May 2015

© 2015 IHS

• Global PET markets will continue to be vastly oversupplied.

• North America is embarking on even further capacity expansion which will change the economic dynamic.

• Falling PX will reduce PX prices with PX margins suffering due to increasing capacity.

Conclusions - PET PLASTICS OVERVIEW / MAY 2015

© 2015 IHS

Inter-material competition and the impact to global trade

• Which products will be advantaged in North America?

• Does North America import more less products by 2019?

• Can logistical challenges be overcome with the onset of new capacities?

Plastics Overview / May 2015

© 2015 IHS

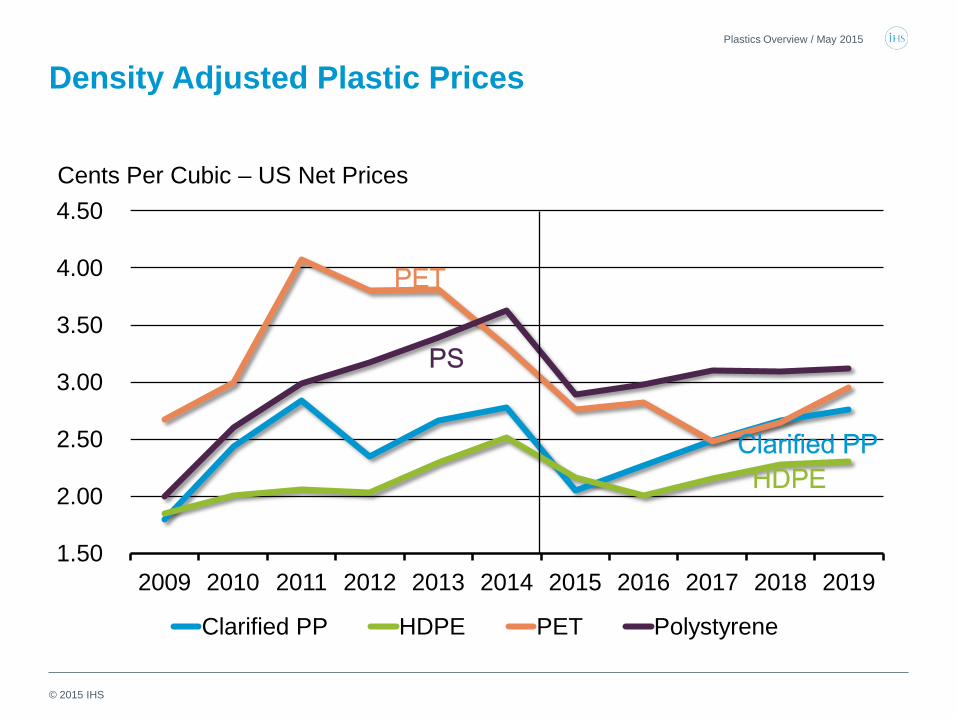

Density Adjusted Plastic Prices

1.50

2.00

2.50

3.00

3.50

4.00

4.50

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Clarified PP HDPE PET Polystyrene

Cents Per Cubic – US Net Prices

Plastics Overview / May 2015

© 2015 IHS

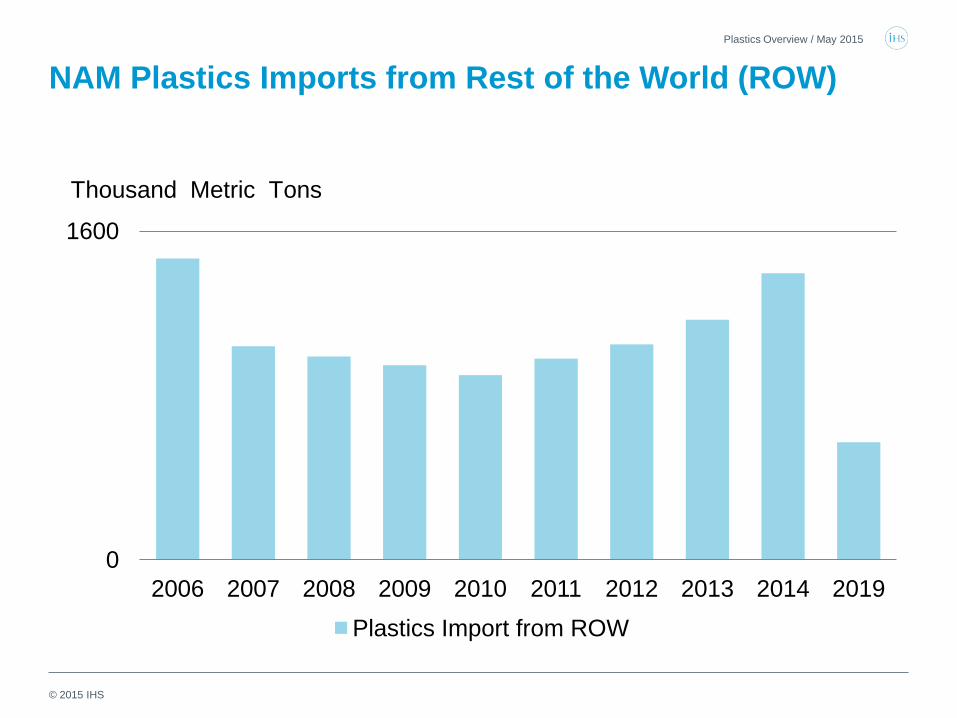

NAM Plastics Imports from Rest of the World (ROW)

Plastics Overview / May 2015

0

1600

2006 2007 2008 2009 2010 2011 2012 2013 2014 2019 Plastics Import from ROW

Thousand Metric Tons

© 2015 IHS

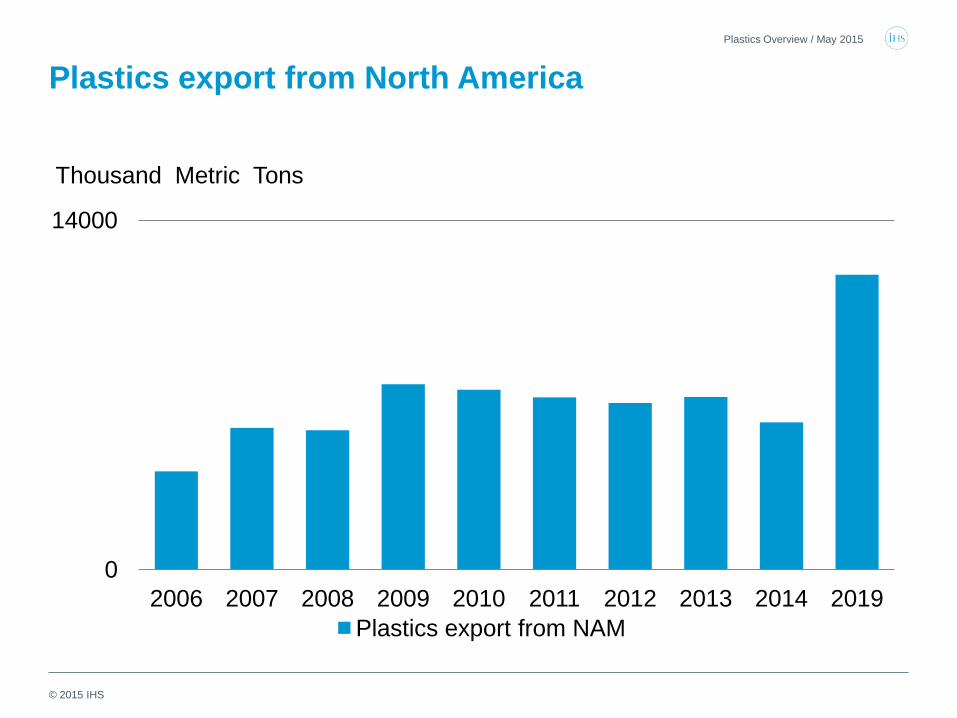

Plastics export from North America

Plastics Overview / May 2015

0

14000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2019 Plastics export from NAM

Thousand Metric Tons

© 2015 IHS

Plastics Overview / May 2015

Conclusions

• Defining factor in new energy world order is OPEC stepping down from the role of supply buffer maintain price.

• All base chemicals and derivatives & plastics markets adjusting to this new energy environment

• Price setters have lower cost…prices will decline unless tight markets exist

• Demand pause, likely to see surge once crude markets are stable; trade patterns likely to shift; look for higher volatility as a result

• Approved new capacity in advantaged regions continue; new projects pause

• Integrated margins for low-cost producers decline, some high-cost producers see margin improvement