Embed Size (px)

Citation preview

Competition of 3G Services in Japan

Tatsushiro Shukunami

Institute for Media and Communications Research

Keio University, Japan

Outline of presentation

• Overview of Mobile Market in Japan

• 3G Market in Japan

• What do customers want?

• Who will win?

Overview of Mobile Market

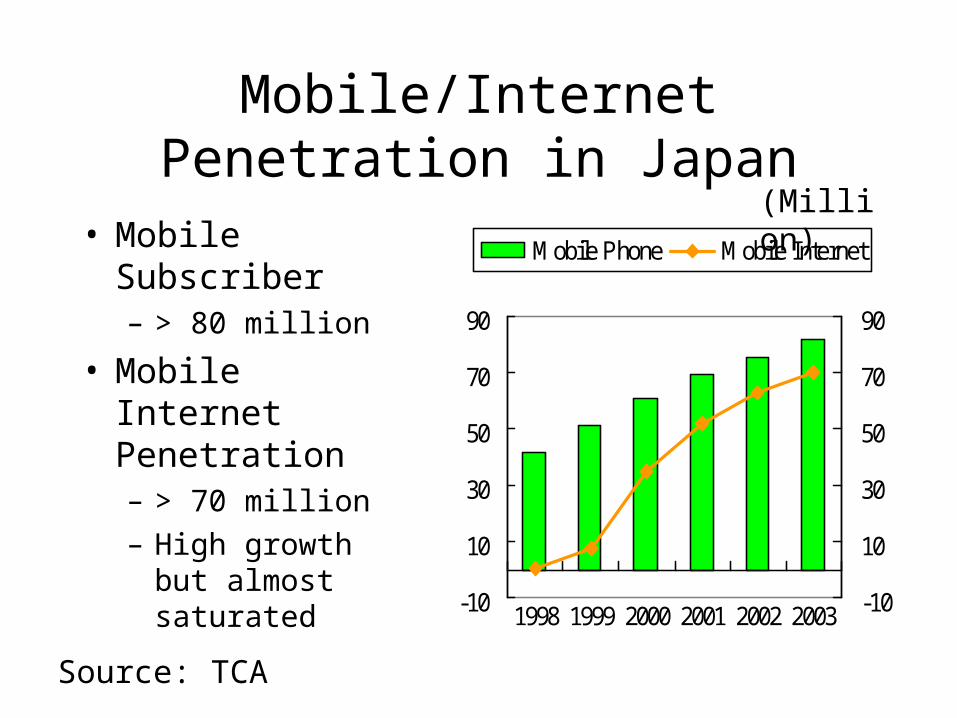

Mobile/Internet Penetration in Japan

• Mobile Subscriber– > 80 million

• Mobile Internet Penetration– > 70 million

– High growth but almost saturated

-10

10

30

50

70

90

1998 1999 2000 2001 2002 2003 -10

10

30

50

70

90

Mobile Phone Mobile Internet

Source: TCA

(Million)

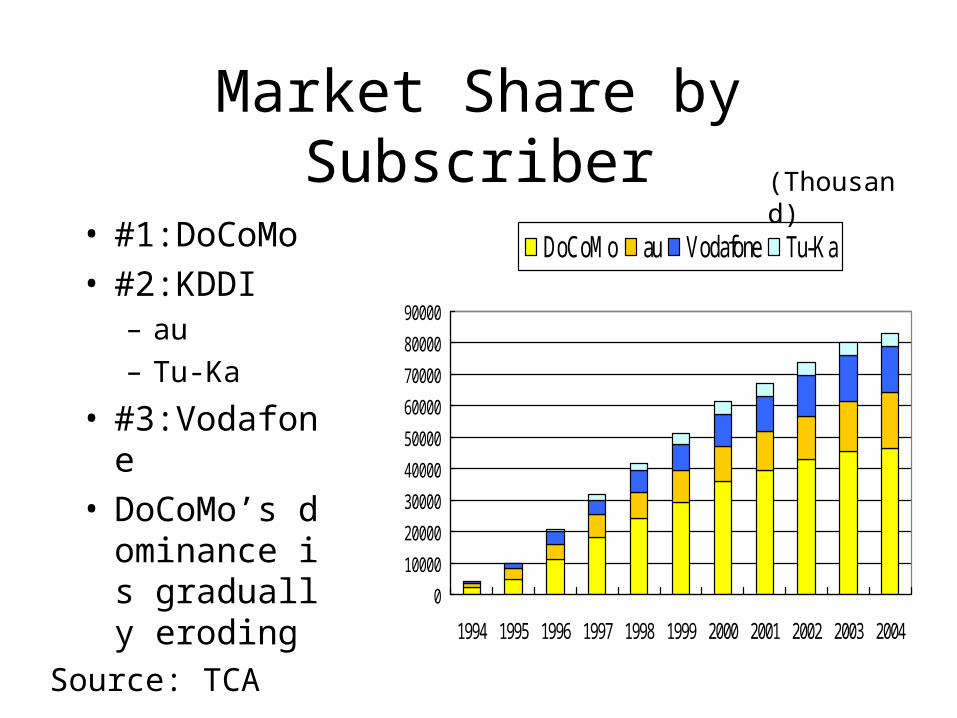

Market Share by Subscriber

• #1:DoCoMo• #2:KDDI

– au

– Tu-Ka

• #3:Vodafone• DoCoMo’s do

minance is gradually eroding

0

10000

20000

30000

40000

50000

60000

70000

80000

90000

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

DoCoMo au Vodafone Tu-Ka

Source: TCA

(Thousand)

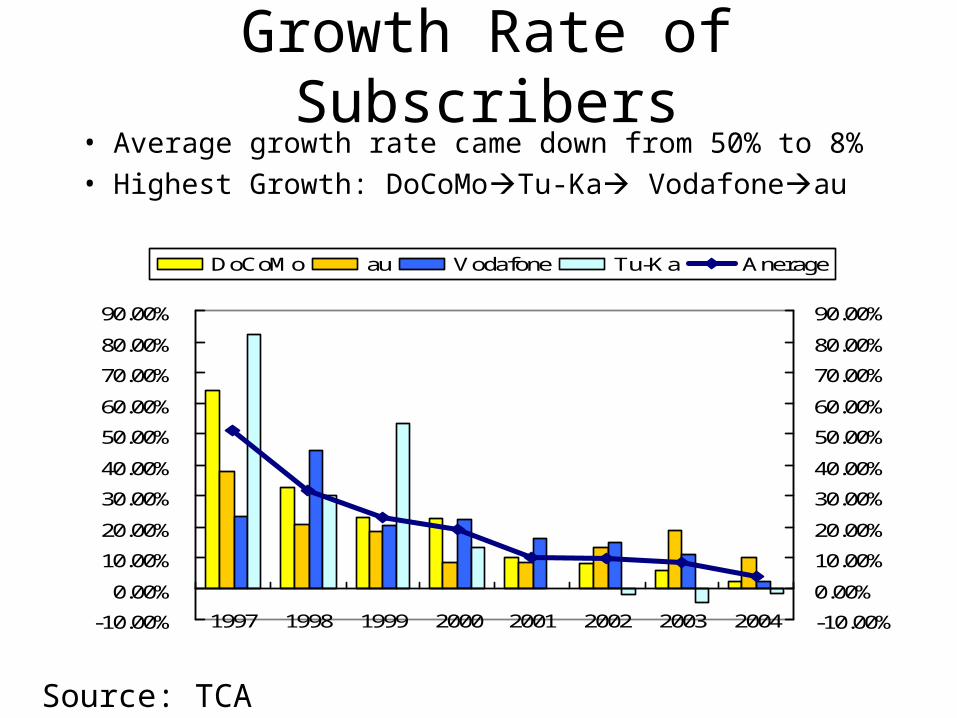

Growth Rate of Subscribers• Average growth rate came down from 50% to 8%

• Highest Growth: DoCoMoTu-Ka Vodafoneau

-10.00%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

90.00%

1997 1998 1999 2000 2001 2002 2003 2004 -10.00%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

90.00%

DoCoMo au Vodafone Tu-Ka Anerage

Source: TCA

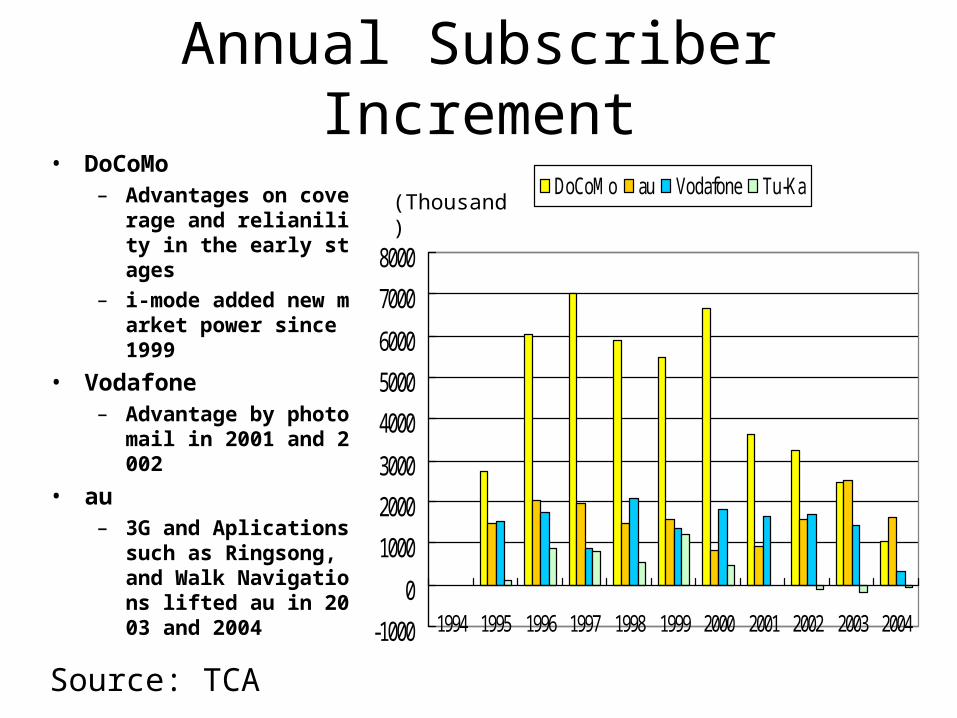

Annual Subscriber Increment• DoCoMo

– Advantages on coverage and relianility in the early stages

– i-mode added new market power since 1999

• Vodafone – Advantage by photo ma

il in 2001 and 2002

• au– 3G and Aplications such

as Ringsong, and Walk Navigations lifted au in 2003 and 2004

-1000

0

1000

2000

3000

4000

5000

6000

7000

8000

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

DoCoMo au Vodafone Tu-Ka

Source: TCA

(Thousand)

3G competition

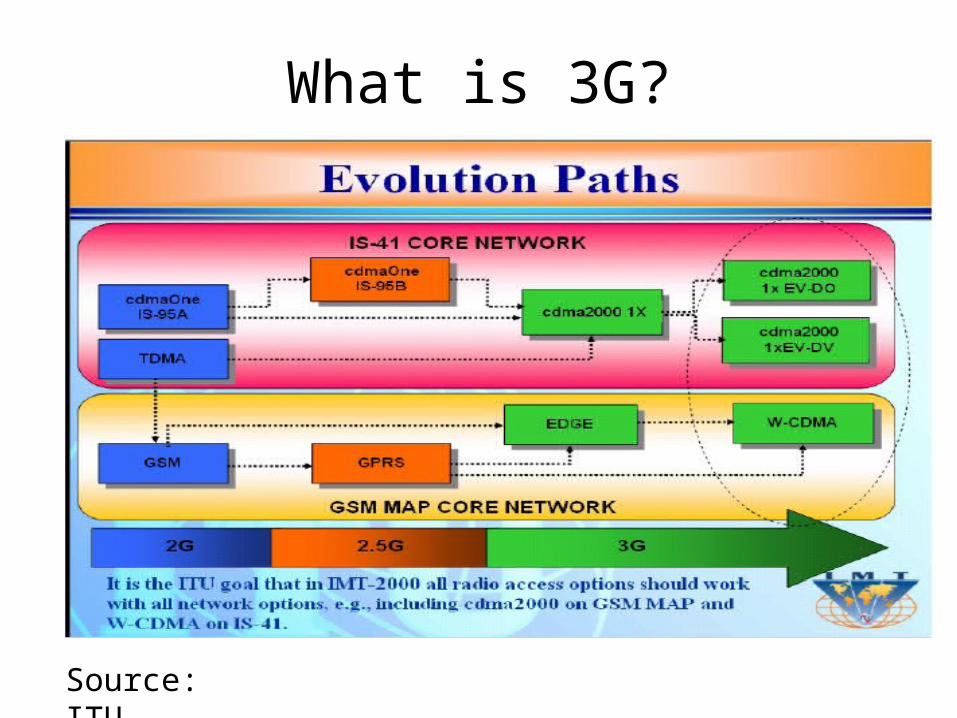

What is 3G?

Source: ITU

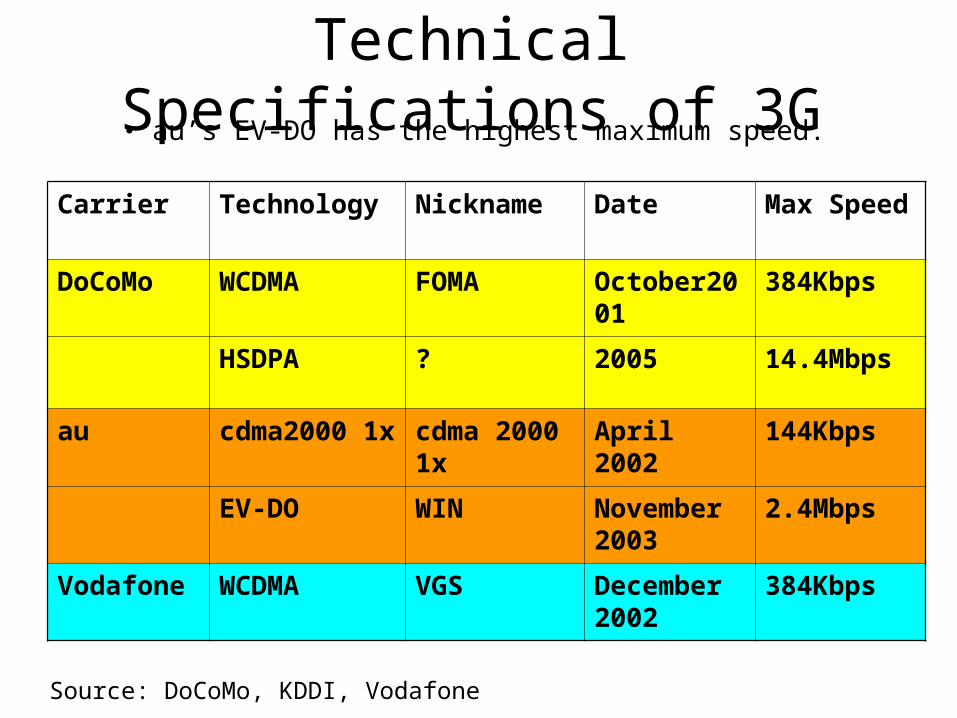

Technical Specifications of 3G• au’s EV-DO has the highest maximum speed.

Carrier Technology Nickname Date Max Speed

DoCoMo WCDMA FOMA October2001 384Kbps

HSDPA ? 2005 14.4Mbps

au cdma2000 1x cdma 2000 1x April 2002 144Kbps

EV-DO WIN November 2003

2.4Mbps

Vodafone WCDMA VGS December 2002

384Kbps

Source: DoCoMo, KDDI, Vodafone

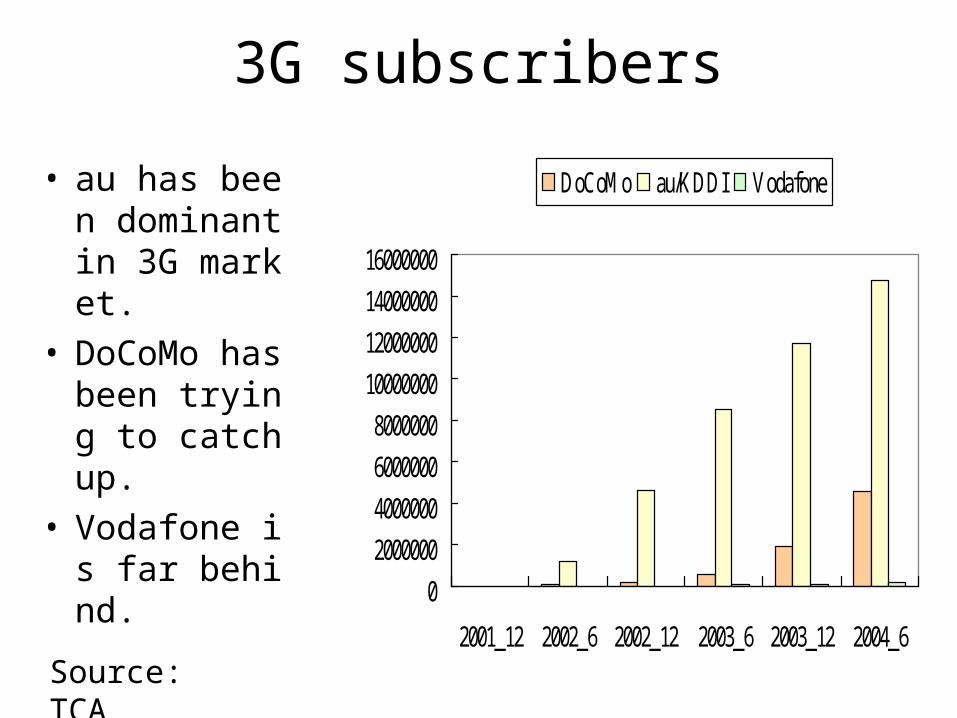

3G subscribers

• au has been dominant in 3G market.

• DoCoMo has been trying to catch up.

• Vodafone is far behind.

0

2000000

4000000

6000000

8000000

10000000

12000000

14000000

16000000

2001_12 2002_6 2002_12 2003_6 2003_12 2004_6

DoCoMo au/KDDI Vodafone

Source: TCA

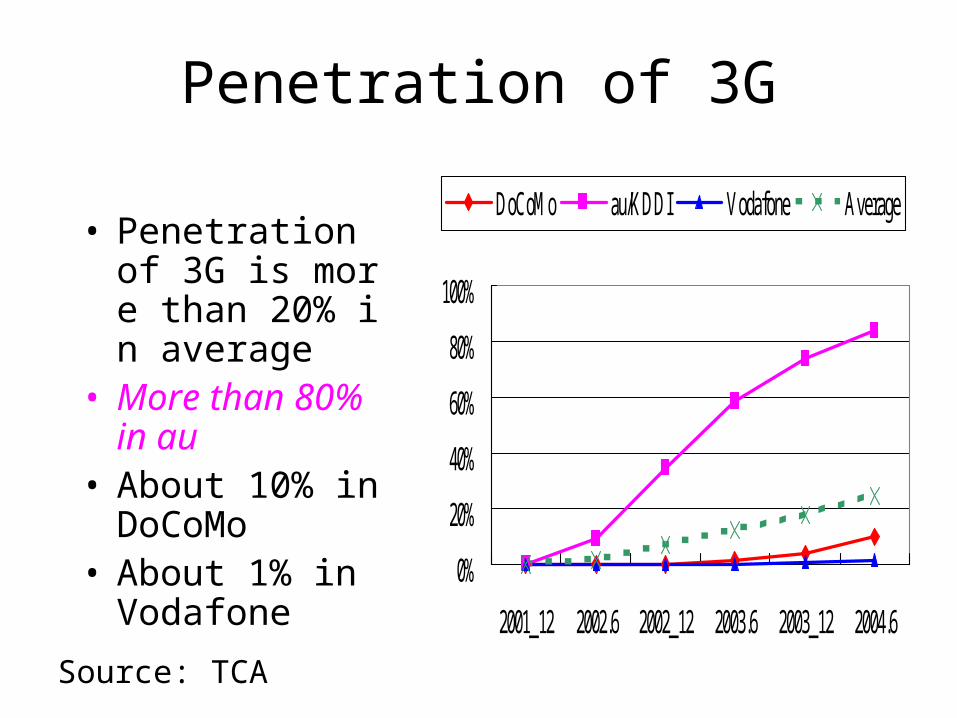

Penetration of 3G

• Penetration of 3G is more than 20% in average

• More than 80% in au

• About 10% in DoCoMo

• About 1% in Vodafone 0%

20%

40%

60%

80%

100%

2001_12 2002.6 2002_12 2003.6 2003_12 2004.6

DoCoMo au/KDDI Vodafone Average

Source: TCA

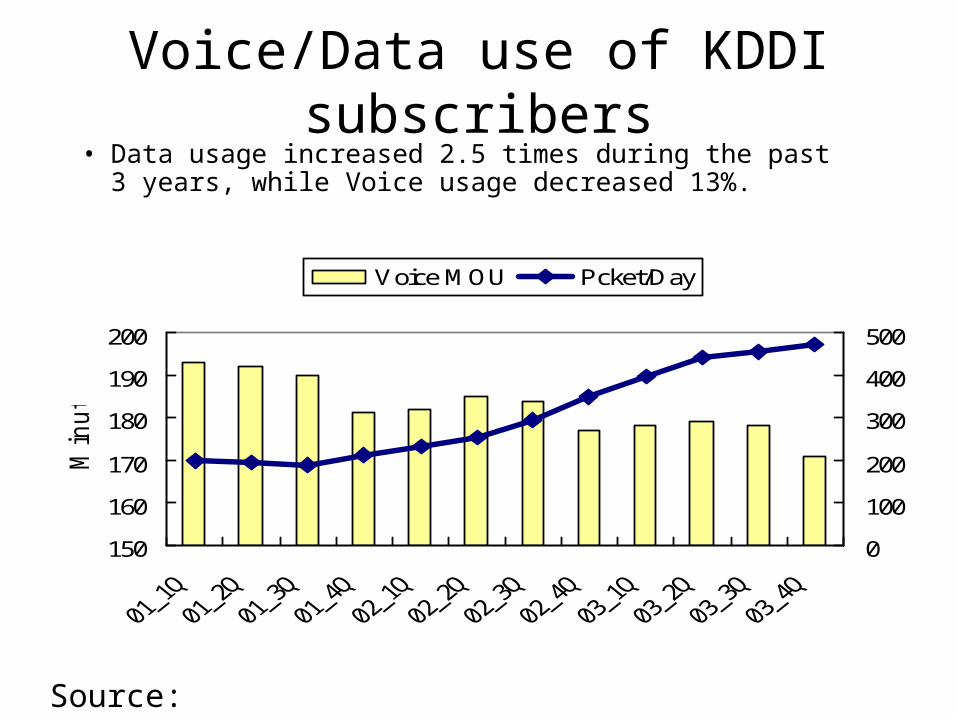

Voice/Data use of KDDI subscribers• Data usage increased 2.5 times during the past 3 years,

while Voice usage decreased 13%.

150

160

170

180

190

200

Min

ute

0

100

200

300

400

500

Voice MOU Pcket/Day

Source: KDDI

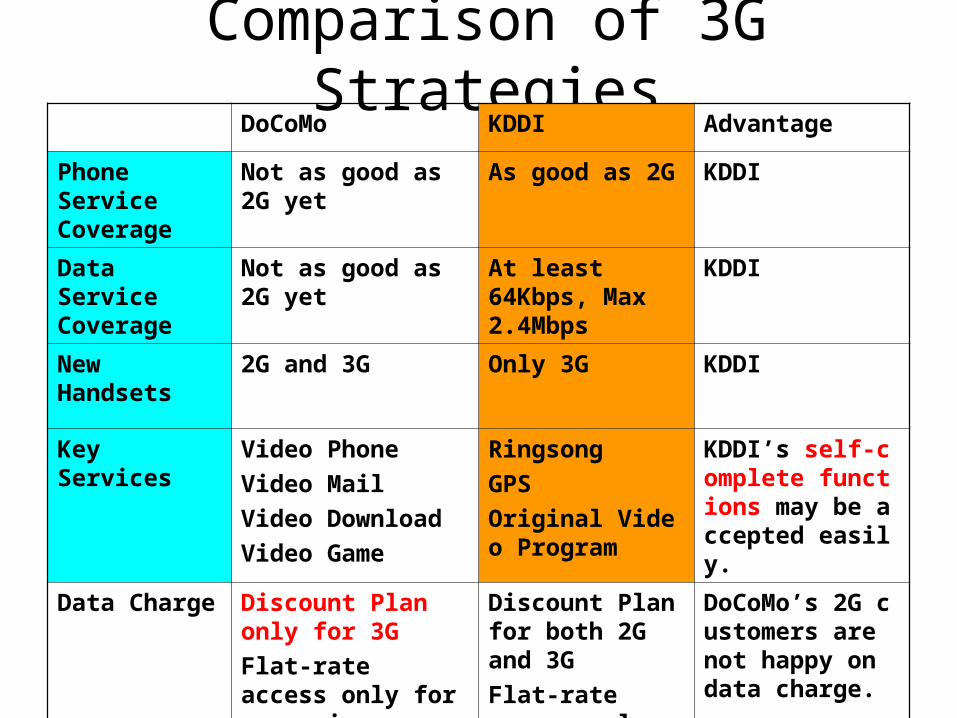

Comparison of 3G StrategiesDoCoMo KDDI Advantage

Phone Service Coverage

Not as good as 2G yet As good as 2G KDDI

Data Service Coverage

Not as good as 2G yet At least 64Kbps, Max 2.4Mbps

KDDI

New Handsets 2G and 3G Only 3G KDDI

Key Services Video Phone

Video Mail

Video Download

Video Game

Ringsong

GPS

Original Video Program

KDDI’s self-complete functions may be accepted easily.

Data Charge Discount Plan only for 3G

Flat-rate access only for expensive monthly plan

Discount Plan for both 2G and 3G

Flat-rate access only for EV-DO

DoCoMo’s 2G customers are not happy on data charge.

What do customers want?

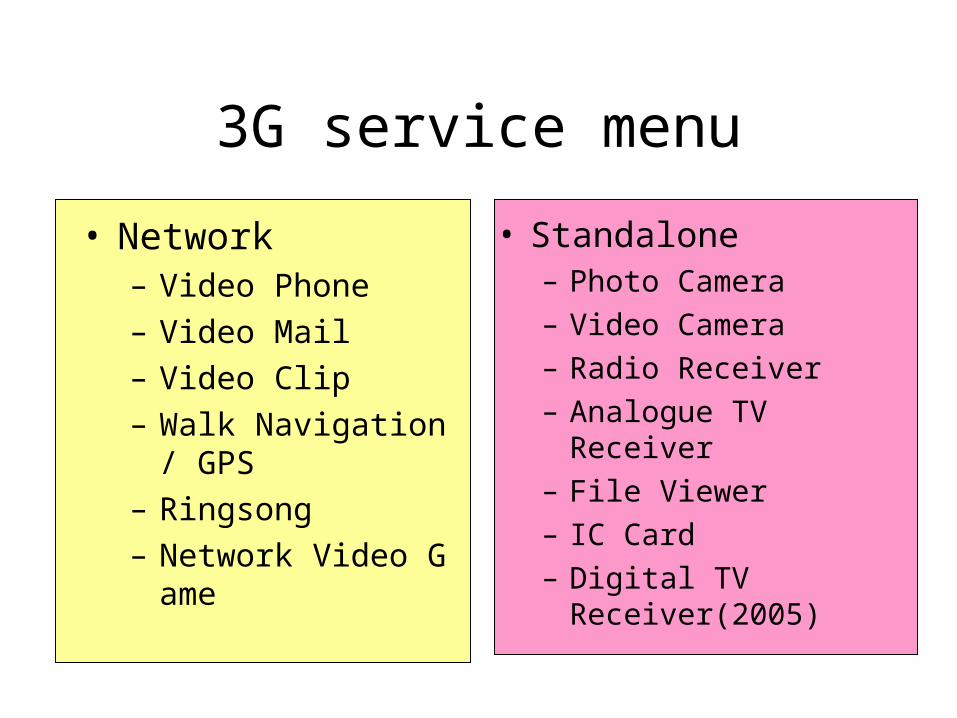

3G service menu

• Network– Video Phone

– Video Mail

– Video Clip

– Walk Navigation/ GPS

– Ringsong

– Network Video Game

• Standalone– Photo Camera

– Video Camera

– Radio Receiver

– Analogue TV Receiver

– File Viewer

– IC Card

– Digital TV Receiver(2005)

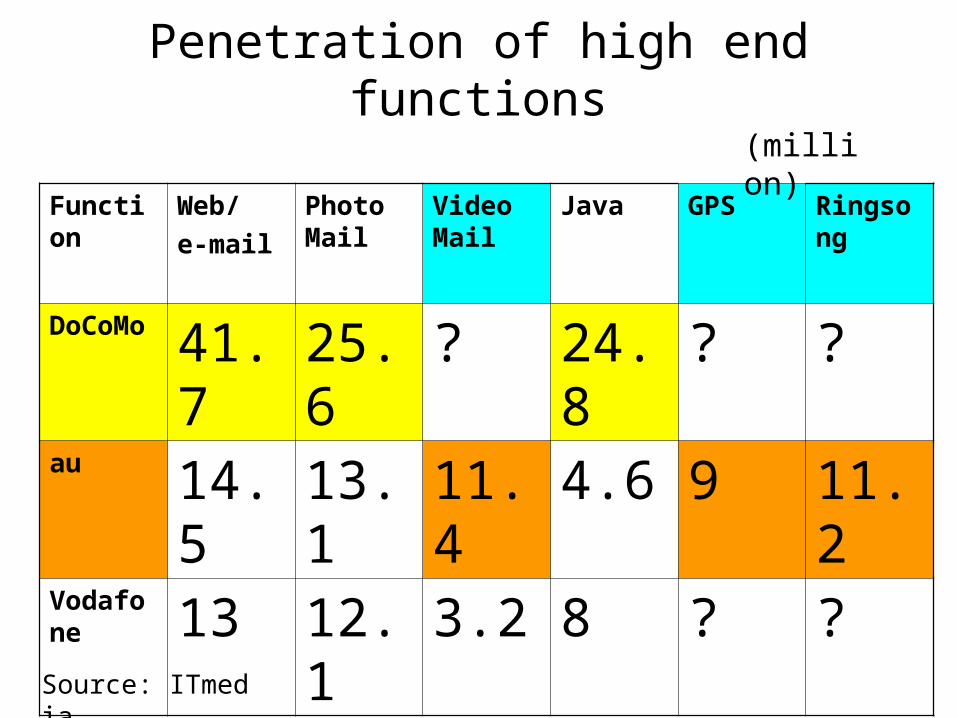

Penetration of high end functions

Function Web/

Photo Mail

Video Mail

Java GPS Ringsong

DoCoMo 41.7 25.6 ? 24.8 ? ?

au 14.5 13.1 11.4 4.6 9 11.2

Vodafone 13 12.1 3.2 8 ? ?

(million)

Source: ITmedia

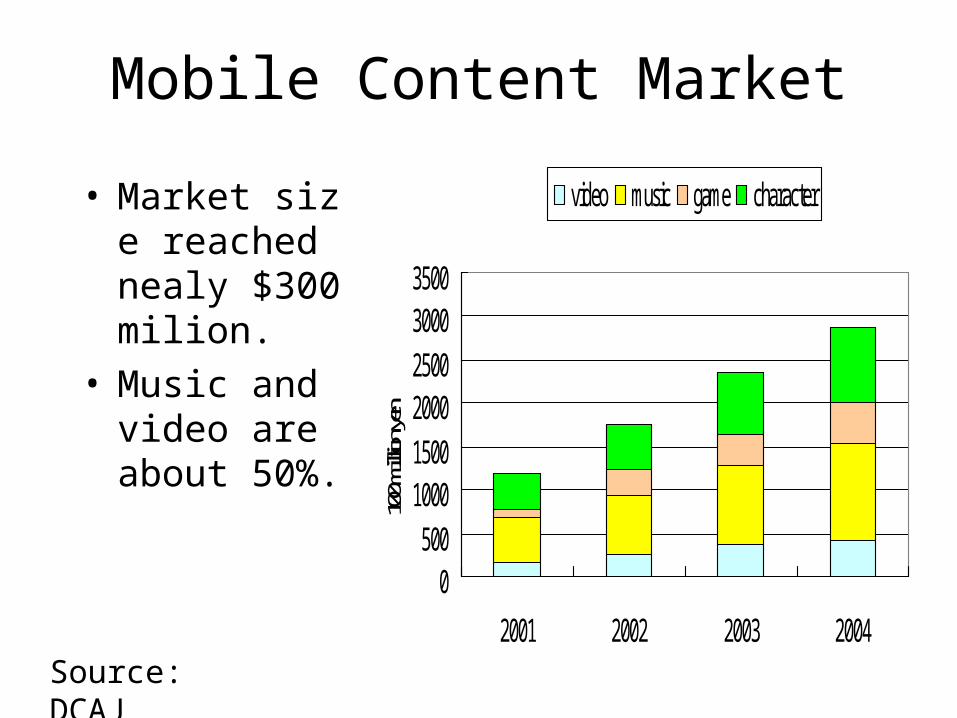

Mobile Content Market

• Market size reached nealy $300 milion.

• Music and video are about 50%.

0500

100015002000250030003500

2001 2002 2003 2004

100 m

illion y

en

video music game character

Source: DCAJ

Most Popular Aplications• Camera and photo mail has become as popular as web access.

• Regular e-mail is as popular as phone call.

0 20 40 60 80 100

%

Video Phone

Video Mail

Location Info

Video Camera

Soft Download

Photo Mail

Web Access

Camera

Phone

Source: MRI

Who will win?

Lessons in the past few years

• Customers want convenience and value. High speed is not the first priority.

• Service coverage problem still bars DoCoMo’s migration strategy.

• Creative, easy-to-understand, and self-complete services are accepted first.

• Full music download has great potential, as Ringsong and iPod has proved.

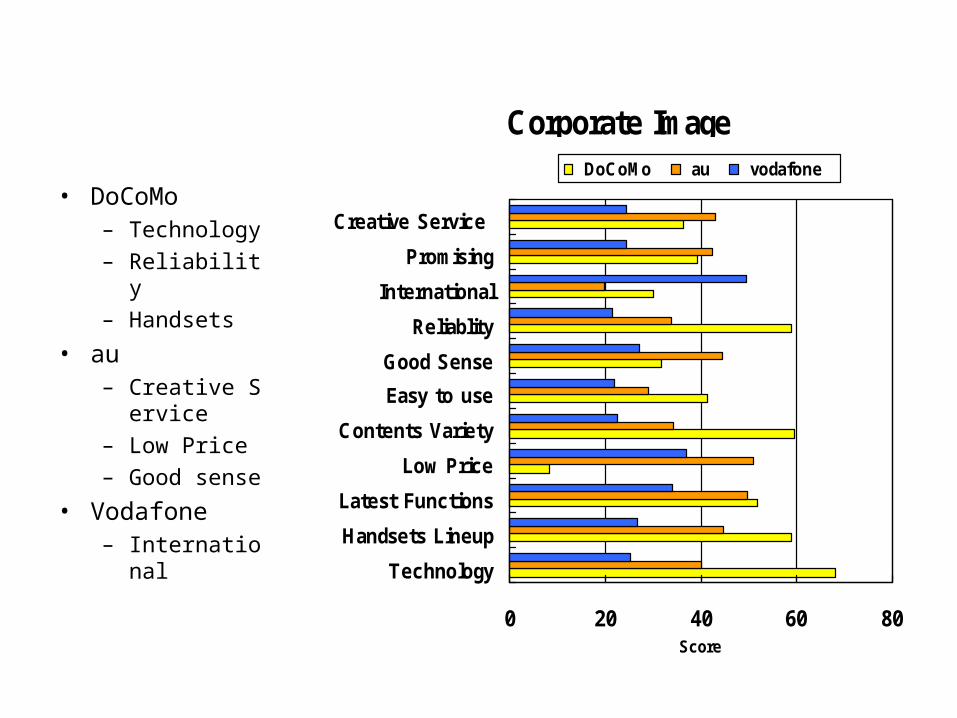

• DoCoMo– Technology

– Reliability

– Handsets

• au– Creative Ser

vice

– Low Price

– Good sense

• Vodafone– International

Corporate Image

0 20 40 60 80

Technology

Handsets Lineup

Latest Functions

Low Price

Contents Variety

Easy to use

Good Sense

Reliablity

International

Promising

Creative Service

Score

DoCoMo au vodafone

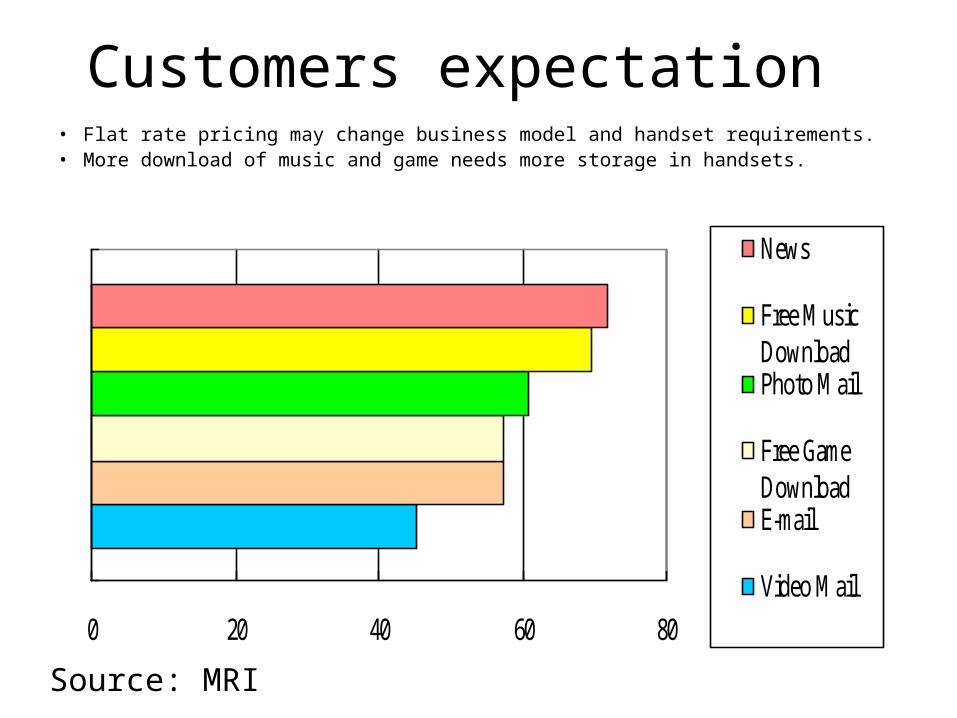

Customers expectation• Flat rate pricing may change business model and handset requirements.• More download of music and game needs more storage in handsets.

0 20 40 60 80

News

Free MusicDownloadPhoto Mail

Free GameDownloadE-mail

Video Mail

Source: MRI

Issues on 3G Business• Identification of killer applications for 3G• Sustainability of WiFi and new entries• New business model for content provider

– Rich content suitable for flat-rate

• Flat-rate for “full” internet access– Handsets, PDA, and PC

• Handsets Improvement– Weight, size, battery, and price– Standalone functions such as Digital TV reception

• Service Coverage– Domestic and Global