Embed Size (px)

Citation preview

The Republic of South Sudan

Ministry of Agriculture, Forestry, Cooperatives and Rural Development

Ministry of Livestock and Fisheries Industries

Comprehensive Agricultural Development Master Plan

Final Report

Annex IV

Situation Analysis Report 2013/2015

May 2015

Japan International Cooperation Agency

JIN Corporation

15-036JRRD

i

Map of South Sudan

Source: Data from the National Baseline Household Survey 2009. Prepared by NBS/CAMP Task Team.

.

ii

Table of contents

Map of South Sudan ............................................................................................................ i

EXECUTIVE SUMMARY ................................................................................................. xxiv

Part 1: Situation Analysis 2013

1. Introduction ............................................................................................................ 1-1

1.1 Background and objective .................................................................................... 1-1 1.1.1 Background .................................................................................................. 1-1 1.1.2 Justification for CAMP formulation ................................................................ 1-3 1.1.3 Objective of the CAMP process .................................................................... 1-3 1.1.4 Target subsectors and geographic area ........................................................ 1-3 1.1.5 Implementation and collaborating ministries ................................................. 1-3

1.2 Guiding principles ................................................................................................. 1-4

1.3 Coordination mechanism ...................................................................................... 1-5

1.4 Work schedule...................................................................................................... 1-7

1.5 Objectives and methodology of the situation analysis ........................................... 1-8 1.5.1 Objectives ..................................................................................................... 1-8 1.5.2 Methodology ................................................................................................. 1-9

1.6 Progress from August 2012 to July 2013 ............................................................ 1-11

2. South Sudan’s economy and agriculture: an overview ....................................... 2-1

2.1 South Sudan’s economy in a historical context ..................................................... 2-1 2.1.1 Pre-Independence Sudan ............................................................................. 2-1 2.1.2 Independence of Sudan ................................................................................ 2-2 2.1.3 After the Comprehensive Peace Agreement ................................................. 2-9 2.1.4 Independence of South Sudan .................................................................... 2-10

2.2 South Sudan’s economy in a regional context .................................................... 2-11 2.2.1 Comparison of socioeconomic situation with neighbouring countries .......... 2-11 2.2.2 Economic relations with neighbouring countries .......................................... 2-13 2.2.3 Participation in regional economic integration ............................................. 2-15

2.3 Importance of agriculture in the national economy .............................................. 2-16

2.4 Overview and recent performance of the agricultural sector ............................... 2-18

3. Natural conditions and environment .................................................................... 3-1

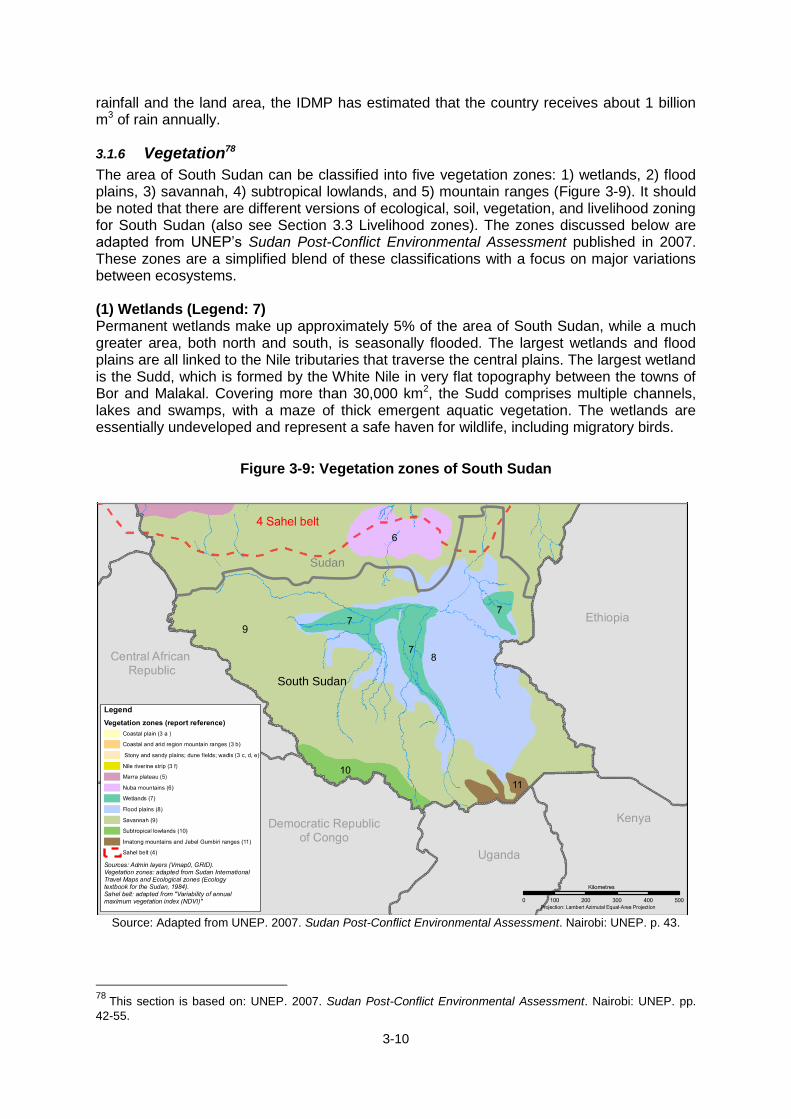

3.1 Natural conditions ................................................................................................. 3-1 3.1.1 Topography .................................................................................................. 3-1 3.1.2 Climate ......................................................................................................... 3-2 3.1.3 Geology and hydrogeology ........................................................................... 3-5 3.1.4 Soils .............................................................................................................. 3-7 3.1.5 Hydrology and water resources .................................................................... 3-7 3.1.6 Vegetation .................................................................................................. 3-10

3.2 Land resources and land use ............................................................................. 3-11

3.3 Livelihood zones ................................................................................................. 3-14

3.4 Environmental issues ......................................................................................... 3-15 3.4.1 Climate change and disaster risk management ........................................... 3-15 3.4.2 Deforestation and land degradation ............................................................ 3-15 3.4.3 Loss of biodiversity resources ..................................................................... 3-17 3.4.4 Lack of effective environmental governance ............................................... 3-17

iii

4. Policy and legal framework for agricultural development ................................... 4-1

4.1 South Sudan Development Plan (SSDP) .............................................................. 4-1

4.2 Current agricultural policies and strategic plans.................................................... 4-2

4.3 Agriculture-related policies and strategic plans ..................................................... 4-3 4.3.1 Land Policy ................................................................................................... 4-3 4.3.2 Strategy for cooperative development ........................................................... 4-4 4.3.3 Other agriculture related policies and strategies ........................................... 4-4

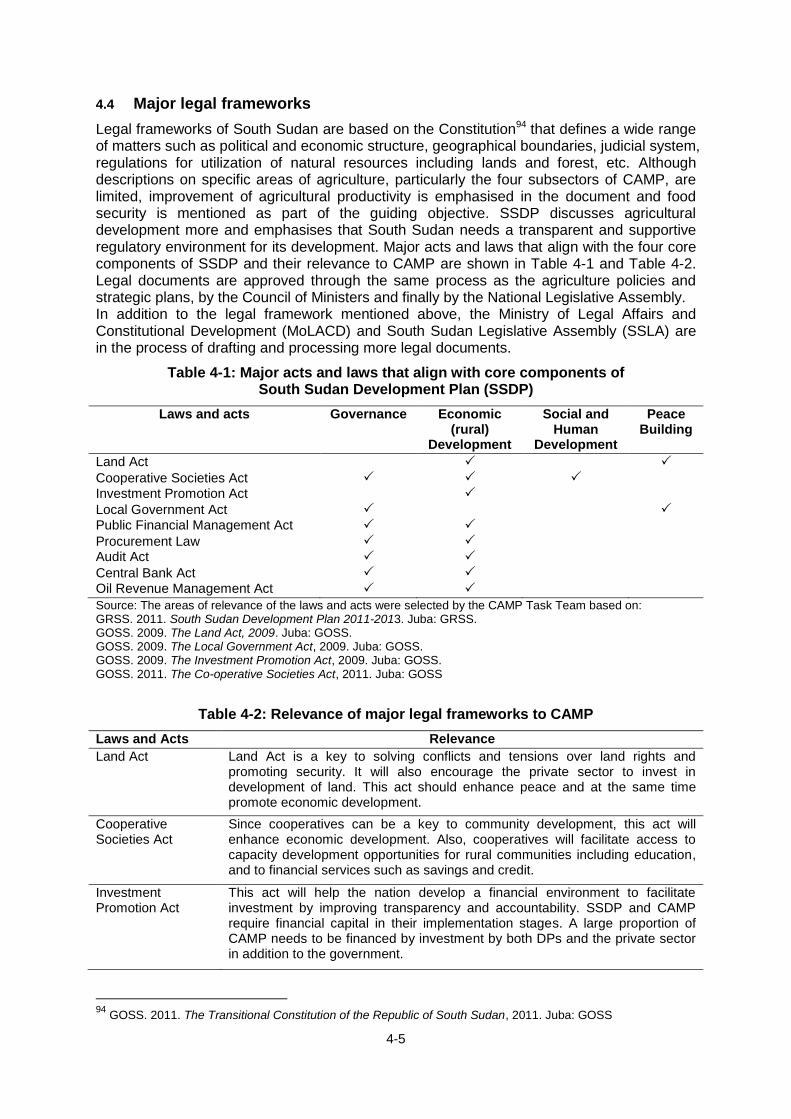

4.4 Major legal frameworks ........................................................................................ 4-5

4.5 Observations ........................................................................................................ 4-6

5. Institutional framework for agricultural development ......................................... 5-1

5.1 Public sector organisations ................................................................................... 5-1 5.1.1 National government ..................................................................................... 5-1 5.1.2 Lead ministries .............................................................................................. 5-2 5.1.3 State and local governments ......................................................................... 5-4 5.1.4 Objectives of Local Government ................................................................... 5-4 5.1.5 Functions of local government ...................................................................... 5-5 5.1.6 Coordination among lead ministries .............................................................. 5-6 5.1.7 Coordination between levels of government ................................................. 5-6

5.2 Public sector capacity ........................................................................................... 5-7 5.2.1 National government ..................................................................................... 5-7 5.2.2 State ministries and county offices .............................................................. 5-10

5.3 Private sector organizations ............................................................................... 5-17 5.3.1 Farmers organizations ................................................................................ 5-17 5.3.2 Agro-input dealers ...................................................................................... 5-17 5.3.3 Processors and traders ............................................................................... 5-18 5.3.4 Financial institutions .................................................................................... 5-19

5.4 Greater Juba market in the context of regional integration .................................. 5-27 5.4.1 Regional market integration ........................................................................ 5-27 5.4.2 Overview of Juba market ............................................................................ 5-27 5.4.3 Functions of Juba market ............................................................................ 5-28 5.4.4 Market arrivals ............................................................................................ 5-30 5.4.5 Organisation of marketing in Juba ............................................................... 5-33 5.4.6 Market trend and competitiveness .............................................................. 5-33 5.4.7 Conclusions ................................................................................................ 5-37

5.5 Education and Training ....................................................................................... 5-37 5.5.1 Background ................................................................................................ 5-37 5.5.2 Government agricultural training centres ..................................................... 5-38 5.5.3 Non-governmental institutions ..................................................................... 5-41 5.5.4 Higher educational institutions .................................................................... 5-41 5.5.5 Other government institutions and schools ................................................. 5-42 5.5.6 Observations............................................................................................... 5-45

5.6 Civil society organisations .................................................................................. 5-45

5.7 Development partners ........................................................................................ 5-46

6. Public financial management and related institutional capacities ..................... 6-1

6.1 Challenges ........................................................................................................... 6-1

6.2 Legal and institutional framework of PFM system ................................................. 6-2 6.2.1 Constitutions, acts, and regulations .............................................................. 6-3

iv

6.2.2 Definition of PFM .......................................................................................... 6-3 6.2.3 Budget preparation guidelines and circulars ................................................. 6-4 6.2.4 Budget documents ........................................................................................ 6-5 6.2.5 PFM policies ................................................................................................. 6-5 6.2.6 Pooled funding mechanisms ......................................................................... 6-6

6.3 Planning and budget procedures .......................................................................... 6-6 6.3.1 Pre-independence budget preparation procedures ....................................... 6-7 6.3.2 Budget Sector Plan development .................................................................. 6-7 6.3.3 Annual budget development ......................................................................... 6-9 6.3.4 Comparison between budget sector plan 2011-2013 and Annual

Budget 2011 .............................................................................................. 6-10 6.3.5 Post-independence planning and budget preparation procedures............... 6-12 6.3.6 Planning and budget preparation of MAFCRD and MARF .......................... 6-15 6.3.7 Planning and budget preparation of state ministries .................................... 6-16 6.3.8 Observations regarding Budget Sector Plans and Annual Budget

preparation ................................................................................................ 6-19

6.4 Budget execution control and procurement procedures ...................................... 6-19 6.4.1 Budget execution control and monitoring .................................................... 6-19 6.4.2 Procurement procedures ............................................................................ 6-20 6.4.3 Execution capacity of MAFCRD and MARF ................................................ 6-23

6.5 Alignment of aid with GRSS's PFM system ........................................................ 6-25 6.5.1 Aid coordination mechanism ....................................................................... 6-25 6.5.2 Aid coordination structure ........................................................................... 6-26 6.5.3 Natural Resources Sector Working Group .................................................. 6-27 6.5.4 Alignment of aid with MARF’s PFM system ................................................. 6-28

6.6 PFM instruments for CAMP implementation and the alignment of aid ................ 6-28 6.6.1 PFM instruments and government's concern regarding aid flows ................ 6-28 6.6.2 Four aid instruments ................................................................................... 6-29 6.6.3 Pooled funding aid instrument ..................................................................... 6-30

6.7 Planning and budget procedures involving state governments ........................... 6-31

7. Food Security ......................................................................................................... 7-1

7.1 Concept of food security ....................................................................................... 7-1

7.2 Overview of food security in South Sudan ............................................................ 7-3

7.3 Major causes of food insecurity ............................................................................ 7-4

7.4 Categories of food insecure people ...................................................................... 7-6

7.5 Farmer’s food insecurity situation ......................................................................... 7-7

7.6 Food security and the market economy .............................................................. 7-11

7.7 Roles of government organisations and development partners .......................... 7-12

8. Rural Society and Livelihood ................................................................................ 8-1

8.1 Population, Communities and Households ........................................................... 8-1

8.2 Reintegration of Returnees and Internally Displaced Persons into Rural Communities ........................................................................................................ 8-4

8.2.1 Returnees ..................................................................................................... 8-4 8.2.2 Internally Displaced Persons (IDPs) .............................................................. 8-5

8.3 Gender Issues ...................................................................................................... 8-6

8.4 Security and Conflicts ........................................................................................... 8-7

v

8.5 Land Tenure and Access to Land ......................................................................... 8-8 8.5.1 Unequal land access ..................................................................................... 8-9 8.5.2 Large-scale land acquisition ........................................................................ 8-10 8.5.3 Land boundary issues ................................................................................. 8-10

8.6 Access to Basic Services ................................................................................... 8-11

8.7 Livelihoods ......................................................................................................... 8-13

8.8 Assets ................................................................................................................ 8-14

8.9 Observations ...................................................................................................... 8-16

8.10 Infrastructure ...................................................................................................... 8-17

9. Lessons learned from previous investments ....................................................... 9-1

9.1 Cooperation with the government ......................................................................... 9-1

9.2 Coordination with DPs .......................................................................................... 9-2

9.3 Partnership with the private sector........................................................................ 9-2

9.4 Participation of farmers ......................................................................................... 9-2

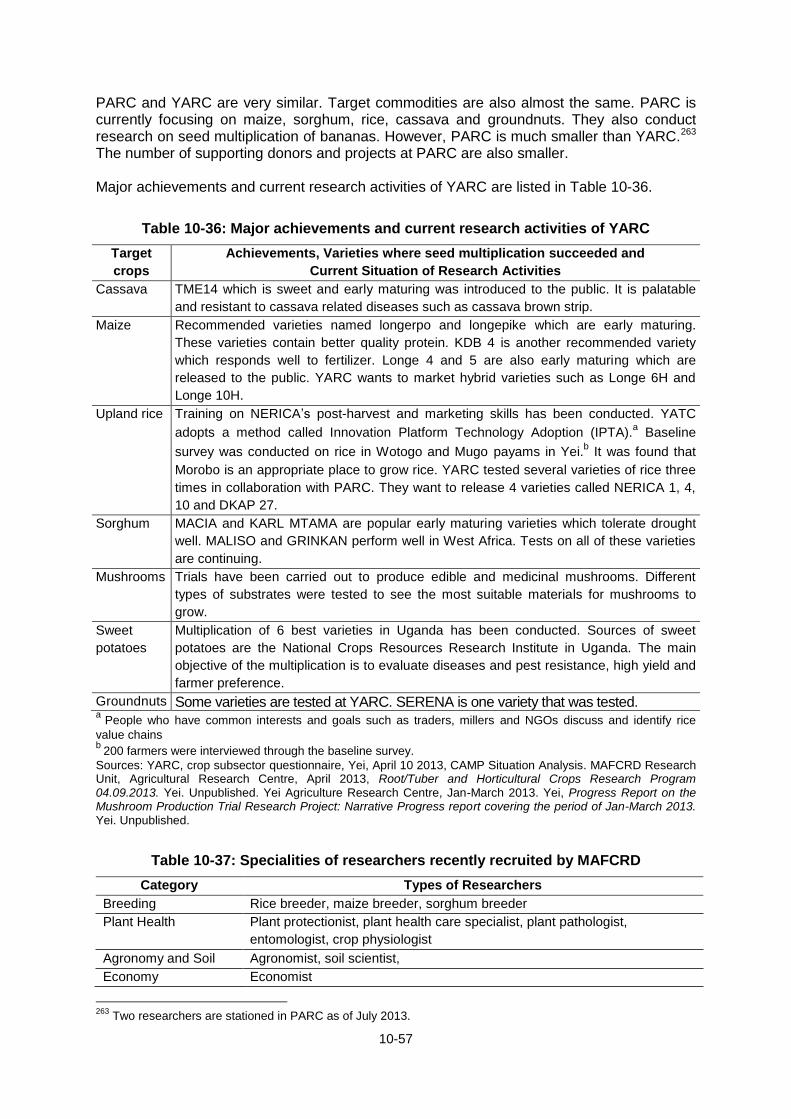

10. Crop ....................................................................................................................... 10-1

10.1 Overview ............................................................................................................ 10-1

10.2 Key issues and challenges ................................................................................. 10-2

10.3 Policy framework ................................................................................................ 10-4

10.4 Institutions .......................................................................................................... 10-6 10.4.1 Ministry of Agriculture, Forestry, Cooperatives and Rural Development ..... 10-6 10.4.2 State government ....................................................................................... 10-8 10.4.3 Land Commission ..................................................................................... 10-10 10.4.4 Development Partners .............................................................................. 10-11 10.4.5 Cooperatives............................................................................................. 10-13 10.4.6 Private sector ............................................................................................ 10-15 10.4.7 Traditional institutions ............................................................................... 10-16

10.5 Food crop production........................................................................................ 10-16 10.5.1 Livelihood Zones ....................................................................................... 10-16 10.5.2 Trend of food crop production ................................................................... 10-20 10.5.3 Food crop production areas and agricultural practices .............................. 10-22 10.5.4 Types of farmers ....................................................................................... 10-28

10.6 Cash crop production ....................................................................................... 10-38 10.6.1 Overview ................................................................................................... 10-38 10.6.2 Production areas and agricultural practices .............................................. 10-39 10.6.3 Economic considerations for cash crop production ................................... 10-44

10.7 Marketing and trade ......................................................................................... 10-45 10.7.1 Characteristics of markets......................................................................... 10-45 10.7.2 Domestic distribution chain ....................................................................... 10-48 10.7.3 Imported agricultural products ................................................................... 10-49 10.7.4 Product price and cost .............................................................................. 10-51 10.7.5 Taxation .................................................................................................... 10-53 10.7.6 Collection and marketing capacity ............................................................. 10-55

10.8 Services ........................................................................................................... 10-55 10.8.1 Research .................................................................................................. 10-55 10.8.2 Training ..................................................................................................... 10-58 10.8.3 Extension services .................................................................................... 10-58

vi

10.8.4 Rural financial services ............................................................................. 10-63 10.8.5 Mechanisation ........................................................................................... 10-65 10.8.6 Agricultural inputs ..................................................................................... 10-66 10.8.7 Plant protection ......................................................................................... 10-67

10.9 Agricultural infrastructure .................................................................................. 10-67

10.10 Investment ........................................................................................................ 10-69

10.11 Cross cutting issues ......................................................................................... 10-71

11. Livestock ............................................................................................................... 11-1

11.1 Overview ............................................................................................................ 11-1

11.2 Key issues and challenges ................................................................................. 11-4

11.3 Policy framework ................................................................................................ 11-7 11.3.1 Policy review: broader policy context .......................................................... 11-7 11.3.2 Livestock subsector policy context .............................................................. 11-8 11.3.3 Legal Frameworks: Legislative and regulatory contexts ............................ 11-11

11.4 Institutions ........................................................................................................ 11-12 11.4.1 Public Sector Institutions ........................................................................... 11-12 11.4.2 Private sector ............................................................................................ 11-21 11.4.3 Educational and training institutions .......................................................... 11-22 11.4.4 Civil Society and Non-Governmental Organizations .................................. 11-24 11.4.5 Development partners ............................................................................... 11-27 11.4.6 Community and Traditional Institutions ..................................................... 11-28 11.4.7 Stakeholder Coordination ......................................................................... 11-29

11.5 Production Systems and Performance of the Livestock Subsector ................... 11-29 11.5.1 Structure of the Livestock Subsector ......................................................... 11-29 11.5.2 Production systems................................................................................... 11-40 11.5.3 Livestock productivity ................................................................................ 11-53 11.5.4 Contribution to livelihoods ......................................................................... 11-60

11.6 Endemic Animal Diseases and Pests ............................................................... 11-64 11.6.1 Priority diseases ....................................................................................... 11-64 11.6.2 Recent disease outbreaks......................................................................... 11-69 11.6.3 Disease impact ......................................................................................... 11-70

11.7 Animal Health Services .................................................................................... 11-72 11.7.1 Provision of Animal Health Services ......................................................... 11-72 11.7.2 Disease prevention and control services ................................................... 11-73

11.8 Marketing and Trade ........................................................................................ 11-82 11.8.1 Demand and supply .................................................................................. 11-82 11.8.2 Main value chains ..................................................................................... 11-86 11.8.3 Imports and Exports .................................................................................. 11-92

11.9 Services ........................................................................................................... 11-94 11.9.1 Extension Services ................................................................................... 11-94 11.9.2 Research and development ...................................................................... 11-95 11.9.3 Input Delivery Systems ............................................................................. 11-95 11.9.4 Food safety assurance .............................................................................. 11-96 11.9.5 Animal welfare .......................................................................................... 11-97

11.10 Infrastructure .................................................................................................... 11-97 11.10.1 Production facilities ................................................................................... 11-98 11.10.2 Marketing facilities .................................................................................... 11-98

11.11 Investment ........................................................................................................ 11-99

vii

11.11.1 Public sector expenditure and investment ................................................. 11-99 11.11.2 Private investment .................................................................................. 11-100 11.11.3 Development partner investment ............................................................ 11-100 11.11.4 Investment climate .................................................................................. 11-101

12. Forestry ................................................................................................................. 12-1

12.1 Overview ............................................................................................................ 12-1

12.2 Key issues and challenges ................................................................................. 12-1

12.3 Forest resources ................................................................................................ 12-3

12.4 Forest policy and legal framework ...................................................................... 12-4 12.4.1 Background ................................................................................................ 12-4 12.4.2 Major policies affecting the Forest Policy 2013 ........................................... 12-5 12.4.3 Devolution of power and benefit sharing arrangement ................................ 12-5 12.4.4 Forest Policy 2013 and legal framework ..................................................... 12-7 12.4.5 The Forest Policy 2013 ............................................................................... 12-7 12.4.6 Forestry Bill 2009 ........................................................................................ 12-9

12.5 State and local governments engaged in forest management .......................... 12-10 12.5.1 Human and physical resources ................................................................. 12-10 12.5.2 Financial resources and revenue collection .............................................. 12-11 12.5.3 Issues of revenue collection by Directorate of Forestry ............................. 12-12

12.6 Public forest reserves ....................................................................................... 12-14 12.6.1 Categories of public forest reserves .......................................................... 12-14 12.6.2 Community Forests (CFs) and enabling legal environment for their

establishment .......................................................................................... 12-15 12.6.3 Central Forest Reserves ........................................................................... 12-15 12.6.4 Forest plantations in Central Forest Reserves .......................................... 12-21 12.6.5 Field observations of Central Forest Reserves and forest plantations ....... 12-23

12.7 Concession forest management ....................................................................... 12-28 12.7.1 Equatoria Teak Company ......................................................................... 12-29 12.7.2 Blue Lakes Limited ................................................................................... 12-32 12.7.3 Central Equatoria Teak Company - legal problem ..................................... 12-33

12.8 Forestry and agroforestry by out-growers ......................................................... 12-34

12.9 Forest products market, trade, and consumption .............................................. 12-36 12.9.1 Forest products and food security, poverty reduction, and income

growth ..................................................................................................... 12-36 12.9.2 Forest products with regional and global markets ..................................... 12-38 12.9.3 Forest products with domestic and regional market .................................. 12-39 12.9.4 Forest products with subsistence and local markets ................................. 12-40

12.10 Forestry education, research, training, and extension....................................... 12-43 12.10.1 Kagelu Forestry Training Centre ............................................................... 12-43

12.11 Activities of development partners and NGOs .................................................. 12-45

12.12 Investment ........................................................................................................ 12-46

13. Fisheries ............................................................................................................... 13-1

13.1 Overview ............................................................................................................ 13-1

13.2 Key issues and challenges ................................................................................. 13-2

13.3 Policy framework ................................................................................................ 13-3 13.3.1 MARF Policy Framework and Strategic Plans 2012-2016 ........................... 13-3 13.3.2 Fisheries and Aquaculture Policy 2012-2017 .............................................. 13-4

viii

13.3.3 Legal framework ......................................................................................... 13-5

13.4 Fisheries Institutions ........................................................................................... 13-5 13.4.1 GRSS MARF .............................................................................................. 13-5 13.4.2 Areas of competencies ............................................................................... 13-6 13.4.3 Organisation ............................................................................................... 13-6 13.4.4 GRSS MARF Directorate of Fisheries and Aquaculture Development ........ 13-6 13.4.5 Organisation, staffing, and facilities ............................................................. 13-7 13.4.6 Fisheries training ........................................................................................ 13-8 13.4.7 Fisheries research ...................................................................................... 13-9 13.4.8 Fisheries planning ..................................................................................... 13-10 13.4.9 Fisheries extension ................................................................................... 13-10 13.4.10 Investment and marketing ......................................................................... 13-10 13.4.11 States ....................................................................................................... 13-11 13.4.12 Areas of competencies ............................................................................. 13-12 13.4.13 Organisation, staffing, and facilities ........................................................... 13-13 13.4.14 Sectoral development ............................................................................... 13-13 13.4.15 Fisheries management ............................................................................. 13-14 13.4.16 Fisheries Investment by states .................................................................. 13-14 13.4.17 Fisheries associations and co-operatives .................................................. 13-14

13.5 Production ........................................................................................................ 13-15 13.5.1 Capture fisheries ....................................................................................... 13-15 13.5.2 Resources ................................................................................................ 13-16 13.5.3 Existing fishing areas and catches ............................................................ 13-18 13.5.4 Fish consumption and food security .......................................................... 13-19 13.5.5 Potential for the development of fisheries ................................................. 13-20 13.5.6 Economic considerations for fisheries development .................................. 13-21 13.5.7 Aquaculture .............................................................................................. 13-22 13.5.8 Existing aquaculture.................................................................................. 13-23 13.5.9 Potential for the development of aquaculture ............................................ 13-23

13.6 Marketing and trade ......................................................................................... 13-25 13.6.1 The local distribution chains ...................................................................... 13-25 13.6.2 Import and export products and markets ................................................... 13-27 13.6.3 Fish product exports ................................................................................. 13-30 13.6.4 Fish market prices .................................................................................... 13-31 13.6.5 Post-harvest losses................................................................................... 13-32 13.6.6 Potential for the fish trade ......................................................................... 13-32

13.7 Services ........................................................................................................... 13-33 13.7.1 Development partners ............................................................................... 13-33 13.7.2 Educational establishments ...................................................................... 13-34 13.7.3 Private sector ............................................................................................ 13-35 13.7.4 Formal credit institutions ........................................................................... 13-35 13.7.5 Informal credit services ............................................................................. 13-35

13.8 Infrastructure .................................................................................................... 13-36

13.9 Important cross cutting issues .......................................................................... 13-37 13.9.1 HIV and AIDS ........................................................................................... 13-37 13.9.2 Gender and child labour in fisheries in South Sudan ................................. 13-38 13.9.3 Security ..................................................................................................... 13-39 13.9.4 Taxation .................................................................................................... 13-39 13.9.5 Transport and fisheries ............................................................................. 13-40 13.9.6 Private investment .................................................................................... 13-40 13.9.7 Public investment ...................................................................................... 13-41

ix

14. Key issues and challenges in the agriculture sector ......................................... 14-1

14.1 Agricultural service delivery: private sector-led development .............................. 14-1

14.2 Understanding the behaviour of the market and the private sector ..................... 14-2

14.3 Crosscutting and subsector issues and challenges ............................................ 14-3 14.3.1 Crosscutting issues and challenges ............................................................ 14-3 14.3.2 Subsector-wise issues and challenges........................................................ 14-4

Part 2: Situation Analysis 2015

15. Pests and diseases .............................................................................................. 15-1

16. Private sector investment .................................................................................... 16-1

16.1 Situation of private sector investment in South Sudan ........................................ 16-1 16.1.1 Micro, small and medium enterprises .......................................................... 16-1 16.1.2 Business environment and the state of competitiveness of South

Sudan........................................................................................................ 16-2 16.1.3 Legal framework for private sector development ......................................... 16-3 16.1.4 Financial services ....................................................................................... 16-5 16.1.5 Agro-input value chains and output markets ............................................... 16-5 16.1.6 Labour markets and human capital ............................................................. 16-6 16.1.7 Agriculture sector business development services ...................................... 16-7

16.2 Public-private partnerships ................................................................................. 16-7 16.2.1 Case studies ............................................................................................... 16-7 16.2.2 Review of PPPs in Kenya ........................................................................... 16-9

17. Conflict and food security ................................................................................... 17-1

17.1 Situation of current conflict ................................................................................. 17-1

17.2 Historical background and causes of conflict ...................................................... 17-2

17.3 Peace and reconciliation initiatives ..................................................................... 17-3

18. Gender issues....................................................................................................... 18-1

18.1 Gender issues in agricultural production ............................................................. 18-1

18.2 Roles and interests by gender ............................................................................ 18-3 18.2.1 Crop ............................................................................................................ 18-3 18.2.2 Livestock ..................................................................................................... 18-3 18.2.3 Forestry ...................................................................................................... 18-3 18.2.4 Fisheries ..................................................................................................... 18-3

18.3 Policy and legal framework for gender equality................................................... 18-4 References

x

List of tables

Table 1-1: South Sudan’s key indicators ............................................................................ 1-2 Table 1-2: Composition and main functions of the CAMP institutions ................................. 1-6 Table 1-3: Work schedule for CAMP formulation ................................................................ 1-8 Table 1-4: Markets and food security, poverty reduction and economic growth ................ 1-10 Table 2-1: Chronology of South Sudan: from the 19th Century to independence ................ 2-1 Table 2-2: Population and characteristics of economy by district in 1954 ........................... 2-3 Table 2-3: Estimated GDP per capita and output shares by region, 1956 .......................... 2-5 Table 2-4: Planned and realised investment for the Six-Year Development Plan

(1977/78-1982/83) in South Sudan (million Sudanese Pounds) ....................... 2-6 Table 2-5: Population (census of 1955/56, 1973, 1983 and 2008)...................................... 2-7 Table 2-6: South Sudan’s GDP by expenditure method in 2008-2011 ................................ 2-9 Table 2-7: Major socioeconomic indicators of South Sudan and its neighbours (2011) .... 2-12 Table 2-8: Organisations promoting regional economic cooperation and integration

relevant to South Sudan ................................................................................ 2-16 Table 2-9: Profiles of East African Community (EAC) and Common Market for Eastern

and Southern Africa (COMESA) (2011) ......................................................... 2-16 Table 2-10: Shares of agriculture in the national economy ............................................... 2-17 Table 2-11: Estimated cereal area harvested, production, consumption and balance in

Southern/South Sudan in 2009-2012 ............................................................. 2-18 Table 2-12: Livelihood zones of South Sudan .................................................................. 2-19 Table 3-1: Rainfall zones classified by rainfall and moisture regimes ................................. 3-5 Table 3-2: Geology of South Sudan ................................................................................... 3-6 Table 3-3: Area and share of aggregated land use in total land area of South Sudan ...... 3-12 Table 3-4: Share of aggregated land use by state (%) ..................................................... 3-13 Table 4-1: Major acts and laws that align with core components of South Sudan

Development Plan (SSDP)............................................................................... 4-5 Table 4-2: Relevance of major legal frameworks to CAMP ................................................ 4-5 Table 5-1: Ministries in SSDP ............................................................................................ 5-1 Table 5-2: Organization of Ministry of Agriculture, Forestry, Cooperatives and Rural

Development.................................................................................................... 5-2 Table 5-3: Organization of Ministry of Animal Resources and Fisheries ............................. 5-3 Table 5-4: Organization of Ministry of Water Resources and Irrigation ............................... 5-4 Table 5-5: Levels of government and their functions .......................................................... 5-6 Table 5-6: National and state ministries for different subsectors ........................................ 5-7 Table 5-7: Human resources at the former MAFCRD in 2012 ............................................ 5-9 Table 5-8: Education level of officers at the Directorate of Cooperatives and Rural

Development at MAFCRD in 2012 ................................................................. 5-10 Table 5-9: Electricity supply time by state ministry ........................................................... 5-11 Table 5-10: Challenges of physical resources by state ..................................................... 5-12 Table 5-11: Physical resource confirmed from 20 counties visited ................................... 5-13 Table 5-12: Distribution of officers in State Ministry of Agriculture and Forestry, Central

Equatoria State .............................................................................................. 5-14 Table 5-13: Distribution of officers to counties in State Ministry of Agriculture and

Forestry, Central Equatoria State ................................................................... 5-14 Table 5-14: Distribution of officers to counties in State Ministry of Animal Resources

and Fisheries, Central Equatoria State........................................................... 5-15 Table 5-15: An example of officers’ distribution in State Ministry of Animal Resources

and Fisheries, Lakes ...................................................................................... 5-15 Table 5-16: Distribution of officers to counties in State MARF, Lakes .............................. 5-15 Table 5-17: Main challenges of each state in terms of human resources ......................... 5-16 Table 5-18: Financial services by formal and informal providers ...................................... 5-19 Table 5-19: Formal financial institutions in South Sudan .................................................. 5-20

xi

Table 5-20: Annual loan interest rates, loan applicants and authorized loans .................. 5-22 Table 5-21: Major Commodities traded in Juba markets and their major origin ................ 5-30 Table 5-22: Monthly incoming commodities to Juba in 2011 (tonnes) .............................. 5-30 Table 5-23: Government Agricultural Training Centres related to Agriculture in South

Sudan ............................................................................................................ 5-38 Table 5-24: Key Information about Yei Agricultural Training Centre (YATC) .................... 5-41 Table 5-25: Universities Offer Courses of Bachelor’s Degrees in the four Agricultural

Subsectors ..................................................................................................... 5-42 Table 5-26: Number of Bachelor’s Students at University of Juba in College of Natural

Resources and Environmental Studies .......................................................... 5-42 Table 5-27: Key Information about Other Government Institutions that provide

Agricultural Education and/or Training Courses ............................................. 5-43 Table 5-28: List of civil society organizations ................................................................... 5-46 Table 5-29: List of major development partners supporting agriculture in South Sudan .. 5-47 Table 6-1: Challenges of financial capacity by state ........................................................... 6-1 Table 6-2: Schedule for Budget Sector Plan development ................................................. 6-7 Table 6-3: Schedule for annual budget 2011 development .............................................. 6-10 Table 6-4: Overview of Natural Resources Sector budget 2011-2013 and Annual

Budget 2011 .................................................................................................. 6-11 Table 6-5: Budget calendar for 2012/13 budget ............................................................... 6-13 Table 6-6: Budget of Ministry of Agriculture and Forestry (2011/12 and 2012/13),

Lakes State .................................................................................................... 6-17 Table 6-7: Budget of Ministry of Agriculture, Cooperatives and Environment (2012/13),

Western Equatoria ......................................................................................... 6-18 Table 6-8: Budget per professional staff in 2010 and 2011 budget, and 2010

expenditure .................................................................................................... 6-24 Table 6-9: SSLDP's per professional annual expenditure for the period of 2011-2012 ..... 6-25 Table 6-10: Characteristics and preferred use of aid instruments ..................................... 6-28 Table 6-11: Pooled funding mechanisms (as of 2011) ...................................................... 6-31 Table 7-1: Four dimensions of food security ....................................................................... 7-1 Table 7-2: Key characteristics of three types of food insecurity .......................................... 7-2 Table 7-3: Number of refugees, returnees, and IDPs in 2012-2013.................................... 7-4 Table 7-4: Numbers of conflict incidents reported in 2012 (January to November 2012) .... 7-5 Table 7-5: Types of Food Insecure People and their Conditions ........................................ 7-6 Table 7-6: Characteristics of Subsistence Farmers’ Food Security Situation in Each

State ................................................................................................................ 7-8 Table 7-7: DPs involved in food security issues in South Sudan ...................................... 7-13 Table 8-1: Population related data of South Sudan ............................................................ 8-1 Table 8-2: Key indicators on gender disparity .................................................................... 8-6 Table 8-3: Type of farmland tenure and acquisition of farmland ......................................... 8-9 Table 8-4: Proportion households owning specific animals by State (%) .......................... 8-16 Table 8-5: Major road projects funded by MDTF .............................................................. 8-18 Table 8-6: List of Road Projects based on Road Section in South Sudan ........................ 8-21 Table 10-1: Summary of Agriculture Sector Policy Framework 2012-2017 ....................... 10-4 Table 10-2: Subsector policies as of July 2013 ................................................................ 10-5 Table 10-3: Crop related directorates and departments ................................................... 10-7 Table 10-4: Budget of MAFCRD and crop related directorates (SSP) .............................. 10-8 Table 10-5: Vision, Mission, Values and Mandate of the Ministry of ................................. 10-8 Table 10-6: Estimated revenue and expenditures 2013/14 of Western Bahr el Ghazal

State (SSP) .................................................................................................... 10-9 Table 10-7: Estimated budget 2013/14 of Ministry of Agriculture and Forestry, .............. 10-10 Table 10-8: Donor support to crop subsector ................................................................. 10-11 Table 10-9: Major NGOs assisting in the areas related to crop production ..................... 10-13 Table 10-10: Type of cooperative societies .................................................................... 10-14 Table 10-11: Nationwide cooperative structure (proposed) ............................................ 10-15

xii

Table 10-12: Agro dealers in South Sudan ..................................................................... 10-15 Table 10-13: Livelihood zones and characteristics ......................................................... 10-18 Table 10-14: Cereal area harvested, population and cereal area harvested by capita in

South Sudan ................................................................................................ 10-21 Table 10-15: Yields (t/ha) of selected cereals ................................................................ 10-22 Table 10-16: Number of households producing major staple crops by state in 2009 ...... 10-23 Table 10-17: Consumption of sorghum in 2009 .............................................................. 10-25 Table 10-18: Number of crop(s) harvested by households ............................................. 10-28 Table 10-19: Number of plots cultivated by household ................................................... 10-28 Table 10-20: Proportion of households by status of owning agricultural land and

livestock by state in 2009 ............................................................................. 10-30 Table 10-21: Number of farmer interviewees for situation analysis................................. 10-31 Table 10-22: Issues of subsistence farmers ................................................................... 10-34 Table 10-23: Origins and prices of selected crops at major markets (April-June, 2013) . 10-38 Table 10-24: Constraints for cash crop production ......................................................... 10-44 Table 10-25: Characteristics of major markets in each state .......................................... 10-45 Table 10-26: Key players in market and their roles ........................................................ 10-46 Table 10-27: Identified local products and major distribution chains for ten states ......... 10-48 Table 10-28: Origins of imported agricultural products by state ...................................... 10-49 Table 10-29: Selling prices of locally grown and imported maize in Wau, Western Bahr

el Ghazal State ............................................................................................ 10-51 Table 10-30: Market fees at major markets .................................................................... 10-52 Table 10-31: List of costs for domestic trade from Morobo to Yei River County, CES .... 10-53 Table 10-32: Simulated impact of lower transport prices on maize and sorghum prices

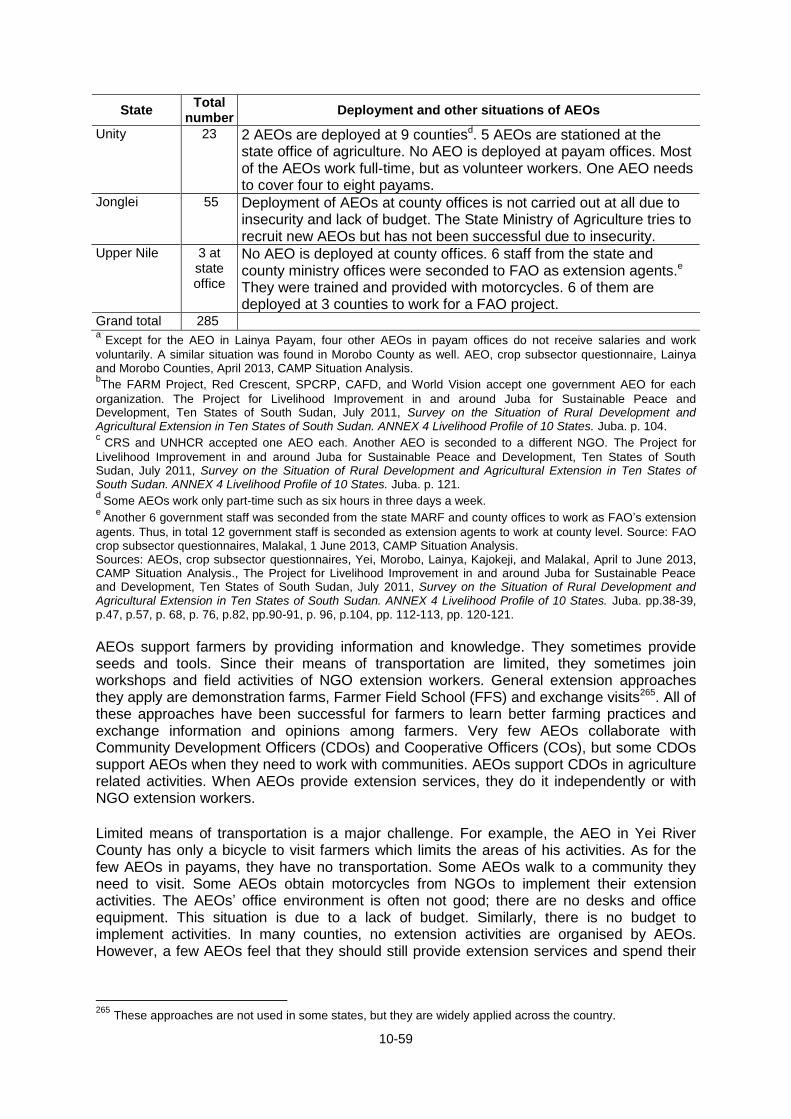

in South Sudan (USD/ton)............................................................................ 10-53 Table 10-33: Type of taxes that merchants need to pay ................................................. 10-54 Table 10-34: Formal and informal payments during transit between border and Juba .... 10-54 Table 10-35: Profile of YARC ......................................................................................... 10-56 Table 10-36: Major achievements and current research activities of YARC ................... 10-57 Table 10-37: Specialities of researchers recently recruited by MAFCRD........................ 10-57 Table 10-38: Total numbers of AEOs and their deployment situation (as of June 2013) . 10-58 Table 10-39: Total numbers of CDOs by State ............................................................... 10-60 Table 10-40: Number of COs by state ............................................................................ 10-61 Table 10-41: Key information about extension workers of the FARM Project in CES ..... 10-62 Table 10-42: Number of household borrowed money last 12 months in 2009 ................ 10-63 Table 10-43: Percentage (%) of households that borrowed money last 12 months by

the main reason for borrowing money in 2009 ............................................. 10-64 Table 10-44: Percentage (%) of households with main reasons for not borrowing

money in 2009 ............................................................................................. 10-64 Table 10-45: Tractor services in different places ............................................................ 10-65 Table 10-46: Approved budget 2012/13 ......................................................................... 10-70 Table 10-47: Tax concessions and incentives regime .................................................... 10-71 Table 11-1 Livestock population in selected African countries in 2011 ............................. 11-2 Table 11-2: MARF Policy Framework 2012- 2016 ............................................................ 11-9 Table 11-3: A comparison of the focus, outlook and strategies of the PFSP 2012-2017

and the ARSP 2006-2011 ............................................................................ 11-11 Table 11-4: National MARF structure (Fisheries Directorate excluded) .......................... 11-12 Table 11-5: Key facets of the state strategic plans ......................................................... 11-15 Table 11-6: Directorates of the national and state ministries .......................................... 11-18 Table 11-7: MARF and SMARF technical personnel as of December 2012 ................... 11-18 Table 11-8: Budget allocation of the Animal Production and Range Management

Directorate to model farms ........................................................................... 11-20 Table 11-9: Statistics of enrolment and graduation from the Faculty of Veterinary

Medicine, Upper Nile University for Academic Year 2012/2013 ................... 11-22 Table 11-10: NGOs operating in Animal Production and Animal Health in South Sudan 11-25

xiii

Table 11-11: Livestock population in South Sudan: a comparison of data sets used by different stakeholders ................................................................................... 11-31

Table 11-12: Livelihood Zones ....................................................................................... 11-41 Table 11-13: Breeds of South Sudan ............................................................................. 11-55 Table 11-14: Cattle herd structure .................................................................................. 11-59 Table 11-15: Number of cattle owned per household ..................................................... 11-61 Table 11-16: Important endemic livestock diseases in South Sudan .............................. 11-64 Table 11-17: Cattle disease prioritization by different methods ...................................... 11-67 Table 11-18: Goat disease prioritization by different methods ........................................ 11-68 Table 11-19: Sheep disease prioritization by different methods ..................................... 11-68 Table 11-20: Poultry disease prioritisation by different methods ..................................... 11-68 Table 11-21: Cost of treatment in SSP of common livestock diseases in South Sudan .. 11-73 Table 11-22: Comparison of disease outbreaks: South Sudan and neighbouring

countries ...................................................................................................... 11-74 Table 11-23: States submission of reports to MARF in 2012 .......................................... 11-76 Table 11-24: Summary of samples received and analyzed, January - December 2012 .. 11-77 Table 11-25: Completed and on-going projects in animal health .................................... 11-78 Table 11-26: Lessons learnt in project implementation ................................................... 11-79 Table 11-27: On-going regional disease control programmes ........................................ 11-80 Table 11-28: Vaccination coverage in 2012 ................................................................... 11-80 Table 11-29: Consumption of meat, milk and other livestock products in South Sudan .. 11-83 Table 11-30: Consumption of meat and milk in selected African countries ..................... 11-84 Table 11-31: Prices of Commonly used Veterinary Medicines and Products .................. 11-96 Table 12-1: Summary of the legal and policy framework for forestry in South Sudan ....... 12-6 Table 12-2: Structure of policy statements of Forest Policy 2013 ..................................... 12-8 Table 12-3: Strength and opportunities and challenges identified in the Forest Policy

2013 .............................................................................................................. 12-9 Table 12-4: Summary of Forestry Bill 2009 ...................................................................... 12-9 Table 12-5: Human and physical resources of state Forestry Directorates interviewed .. 12-11 Table 12-6: Budget sources of and revenue collection by Directorates of Forestry ........ 12-12 Table 12-7: Conditional transfers from GRSS to state ministries of agriculture ............... 12-12 Table 12-8: Rates schedule for forestry products in Western Equatoria State ................ 12-13 Table 12-9: Categories of permanent forest estates (PFEs) ........................................... 12-14 Table 12-10: Reserved Forests within the category of Central Forest Reserve .............. 12-17 Table 12-11: Under Reservation forests within the category of Central Forest Reserve . 12-19 Table 12-12: Forest plantations established in the Central Forest Reserves .................. 12-22 Table 12-13: Management status of Northern and Southern CFR Groups visited .......... 12-26 Table 12-14: Concessionaires and CFRs and plantations under their management ...... 12-28 Table 12-15: Organization and staffing of Equatoria Teak Company (ETC) ................... 12-30 Table 12-16: Volume and average height and diameter in teak plantations managed by

ETC ............................................................................................................. 12-31 Table 12-17: Estimated allowable production from teak plantations managed by ETC ... 12-31 Table 12-18: Forest products and food security, poverty reduction, and income growth . 12-36 Table 12-19: Major domestic actors for production and trade of forest products ............. 12-38 Table 12-20: Estimated annual charcoal consumption in urban and rural areas in 2009 12-39 Table 12-21: Average charcoal prices by state and urban and rural areas ..................... 12-40 Table 12-22: Fuelwood consumption and sources in urban and rural areas in May-

June 2009 .................................................................................................... 12-42 Table 12-23: Expenditure and budget of KFTC for fiscal year 2010/11 and 2011/12 ...... 12-44 Table 13-1: Number of fisheries associations set up by the site (2009-2013) ................. 13-15 Table 13-2: Fish consumption South Sudan ................................................................... 13-20 Table 13-3: Constraint and effect of fisheries commercialisation .................................... 13-21 Table 13-4: Number of fish ponds in 2013 ...................................................................... 13-22 Table 16-1: Micro, small and medium enterprises definition ............................................. 16-1 Table 16-2: Ease of doing business indicators ................................................................. 16-2

xiv

Table 16-3: Main reforms for agribusiness development - Kenya ................................... 16-10 Table 18-1: Access to and control, ownership of productive/economic assets ................. 18-1 Table 18-2: Access to market by gender .......................................................................... 18-2

List of figures

Figure 1-1: Coordination mechanism of the CAMP process ............................................... 1-5 Figure 1-2: Progress of the CAMP process ...................................................................... 1-11 Figure 2-1: Ecological regions of South Sudanas of 1954 .................................................. 2-5 Figure 2-2: Major crops area harvested in Southern Sudan in 1960/61-2004/05 (1,000

feddans) ........................................................................................................... 2-8 Figure 2-3: CPI Annual changes (%) ................................................................................ 2-10 Figure 2-4: GDP and GDP per capita of South Sudan and its neighbours in 2011 ........... 2-12 Figure 2-5: GDP of South Sudan’s neighbours in 2001-2012 (constant 2005 USD

billion) ............................................................................................................ 2-13 Figure 2-6: Imports from and exports to Uganda and Kenya (USD million) ...................... 2-14 Figure 2-7: Imports from Uganda and Kenya by commodity ............................................. 2-15 Figure 2-8: Livelihood Zones of South Sudan .................................................................. 2-19 Figure 2-9: Estimated cereal area harvested and production in 2005-2012 ...................... 2-21 Figure 2-10: Agricultural value added and growth in 2008-2011 ....................................... 2-21 Figure 3-1: Topographic map of South Sudan .................................................................... 3-1 Figure 3-2: Rainfall regimes at eight locations in South Sudan ........................................... 3-2 Figure 3-3: Rainfall contour maps: Annual and July (mm) (created by IDMP) .................... 3-4 Figure 3-4: Geological map of South Sudan ....................................................................... 3-6 Figure 3-5: Hydrogeological map of South Sudan .............................................................. 3-6 Figure 3-6: Soil map of South Sudan (created by IDMP) .................................................... 3-7 Figure 3-7: Main basins of South Sudan ............................................................................ 3-8 Figure 3-8: Annual evaporation map of the Sudd basin (mm/year) ..................................... 3-9 Figure 3-9: Vegetation zones of South Sudan .................................................................. 3-10 Figure 3-10: Aggregated land use/cover map .................................................................. 3-12 Figure 3-11: Combination of roads, agricultural potential zones and cropland areas ........ 3-13 Figure 3-12: Land productivity potential map of South Sudan (prepared by IDMP) .......... 3-14 Figure 3-13: Livelihood zones of South Sudan ................................................................. 3-15 Figure 3-14: Deforestation and expansion of rain-fed agriculture in Yambio ..................... 3-17 Figure 5-1: The Equity Bank, Consolidated Income statement and Balance Sheet .......... 5-24 Figure 5-2: Monthly price of maize flour in Juba Market ................................................... 5-34 Figure 5-3: Monthly price of agricultural commodities in Juba market, 2011 ..................... 5-34 Figure 5-4: Trends of prices of major agricultural commodities from 2010 to 2013 ........... 5-34 Figure 5-5: Maize retail prices in Juba, Nairobi, and Kampala April 2012-March 2013 ..... 5-36 Figure 6-1: Aid coordination structure .............................................................................. 6-27 Figure 7-1: Food security status by state in 2012 and 2013 ............................................... 7-3 Figure 7-2: Percentages of negative factors impacted on household food security ............ 7-5 Figure 8-1: Literacy rate (above 15 years old) by state and location (%) ............................ 8-2 Figure 8-2: Net attendance rate and Gross enrolment rate in primary education by

state (%) .......................................................................................................... 8-2 Figure 8-3: Judicial system and community level dispute settlement system ...................... 8-3 Figure 8-4: Cumulative number of the returnees (2007- May 2013) ................................... 8-4 Figure 8-5: Returnees and State average cereal yield (t/ha) ............................................. 8-4 Figure 8-6: Cumulative numbers of conflicts ...................................................................... 8-7 Figure 8-7: Female marital status by age group ............................................................... 8-10 Figure 8-8: Main source of drinking water (%) .................................................................. 8-12 Figure 8-9: Gross attendance rates in primary and sedoncary school (%) ........................ 8-12

xv

Figure 8-10: Main source of energy for cooking (%) ......................................................... 8-13 Figure 8-11: Health care facility most visit (%).................................................................. 8-13 Figure 8-12: Proportion of monthly expenditure ................................................................ 8-14 Figure 8-13: Type of transportation owned (%) ................................................................ 8-15 Figure 8-14: Type of dwelling (%)..................................................................................... 8-15 Figure 8-15: Type of items owned (%) ............................................................................. 8-15 Figure 8-16: Type of animal owned (%)............................................................................ 8-15 Figure 8-17: Roads maintained by the Southern Sudan Roads Maintenance Project ....... 8-19 Figure 8-18: Roads opened by the WFP since 2004 in South Sudan ............................... 8-20 Figure 8-19: Completed Road Projects ............................................................................ 8-25 Figure 8-20: On-going Road Projects (as of October 1, 2013) .......................................... 8-26 Figure 10-1: Organogram of MAFCRD ............................................................................. 10-7 Figure 10-2: Organogram of the Ministry of Agriculture and Forestry, Lakes State ........... 10-9 Figure 10-3: Livelihood zones in South Sudan ............................................................... 10-17 Figure 10-4: Annual precipitation of South Sudan .......................................................... 10-18 Figure 10-5: Cereal net production and deficit ................................................................ 10-20 Figure 10-6: Cereal area harvested, net yield and net production .................................. 10-20 Figure 10-7: Trend of area harvested for cereal ............................................................. 10-21 Figure 10-8: Number of households harvesting crops (Top 10) in 2008/2009 ................ 10-23 Figure 10-9: Main areas of sorghum production ............................................................. 10-24 Figure 10-10: Main areas of maize production ............................................................... 10-26 Figure 10-11: Main areas of cassava production ............................................................ 10-27 Figure 10-12: Main areas of rice production ................................................................... 10-27 Figure 10-13: Proportion of households by status of owning agricultural land and

livestock ....................................................................................................... 10-29 Figure 10-14: Crop calendar of subsistence farmers in Rumbek, Lakes State

(Ironstone Plateau zone) .............................................................................. 10-32 Figure 10-15: Crop calendar of subsistence farmers in Yambio, Western Equatoria

State (Greenbelt zone) ................................................................................. 10-33 Figure 10-16: Crop calendar of large-scale farmers in Renk, Upper Nile State (Flood

Plains zone) ................................................................................................. 10-37 Figure 10-17: High potential vegetable Production Areas ............................................... 10-39 Figure 10-18: Price trend of coffee in the international market ....................................... 10-42 Figure 10-19: Production of coffee beans (green) by country ......................................... 10-42 Figure 10-20: Producer price trend of sesame seed by country ..................................... 10-43 Figure 10-21: Production of sesame seed by country..................................................... 10-43 Figure 10-22: Price trend of sunflower oil in the international market ............................. 10-43 Figure 10-23: Production of sunflower seeds by country ................................................ 10-43 Figure 10-24: Key players and relationships .................................................................. 10-47 Figure 10-25: Major flows of imported agricultural products in South Sudan .................. 10-51 Figure 10-26: Agricultural infrastructure established by public and private sectors ......... 10-69 Figure 11-1: Key areas of intervention of NGOs working in the livestock subsector ....... 11-27 Figure 11-2: Cattle populations at state level in South Sudan ........................................ 11-34 Figure 11-3: Areas of concentration of cattle in South Sudan ......................................... 11-35 Figure 11-4: Goat population across South Sudan states .............................................. 11-36 Figure 11-5: Goat concentration ..................................................................................... 11-37 Figure 11-6: Sheep population across South Sudan states ............................................ 11-38 Figure 11-7: Areas of concentration of honey production ............................................... 11-39 Figure 11-8: Areas where pigs are currently being reared in South Sudan ..................... 11-40 Figure 11-9: Main cattle production systems in South Sudan ......................................... 11-41 Figure 11-10: Importance of livestock as a main source of livelihood ............................. 11-61 Figure 11-11: Main coping strategies employed by households affected by shock ......... 11-63 Figure 11-12: How households coped with different shocks experienced ....................... 11-64 Figure 11-13: Disease outbreaks reported in 2012 ......................................................... 11-70 Figure 11-14: Benefits derived from cattle in South Sudan (%) ...................................... 11-71

xvi

Figure 11-15: Cattle disease impact on livelihood benefits (%) ...................................... 11-72 Figure 11-16: Disease outbreaks between 2008 and 2012 ............................................ 11-74 Figure 11-17: Disease outbreaks investigated, 2008-2012 ............................................. 11-75 Figure 11-18: Live animal and red meat value chain ...................................................... 11-86 Figure 11-19: Poultry value chain ................................................................................... 11-87 Figure 11-20: Milk value chain ....................................................................................... 11-89 Figure 11-21: Hides and skins value chain ..................................................................... 11-91 Figure 11-22: Honey value chain ................................................................................... 11-92 Figure 12-1: Forest cover (trees closed-to-sparse) in South Sudan .................................. 12-4 Figure 12-2: Organogram of Directorate of Forestry, Western Equatoria State

Government ................................................................................................. 12-11 Figure 12-3: Locations of Central Forest Reserves in South Sudan ............................... 12-16 Figure 12-4: Teak plantation established by an out-grower in Yei River County ............. 12-35 Figure 12-5: Spatial distribution of perceived fuelwood prices in May-June 2009 ........... 12-43 Figure 12-6: Organization of Kagelu Forestry Training Centre ....................................... 12-44 Figure 13-1: Organogram of the Directorate of Fisheries and Aquaculture Development . 13-8 Figure 13-2: Organogram of the Fisheries Department, Northern Bahr el Ghazal State . 13-13 Figure 13-3: Fishing season of South Sudan ................................................................. 13-16 Figure 17-1: IDP and refugee map ................................................................................... 17-2

List of boxes

Box 4-1: Objective of SSDP ............................................................................................... 4-1 Box 4-2: Vision and Mission of MAFCRD ........................................................................... 4-2 Box 4-3: Vision and mission of MARF ................................................................................ 4-3 Box 4-4: Draft land policy ................................................................................................... 4-4 Box 5-1: Objectives of local government ............................................................................ 5-4 Box 5-2: Principles of local governance ............................................................................. 5-5 Box 5-3: Case study - Equity Bank: successful management of a foreign-own

commercial bank ............................................................................................ 5-23 Box 5-4: Case study - Nile Commercial Bank: unsuccessful management of a

commercial bank ............................................................................................ 5-24 Box 5-5: Case study - Agricultural Bank of South Sudan: government-owned bank to

provide specialised finance to agriculture ....................................................... 5-25 Box 5-6: Case study - Co-operative bank of South Sudan: a newly established bank to