Embed Size (px)

Citation preview

CONFIDENTIAL DISCLOSURE

DOCUMENT

FOR PORTFOLIO MANAGEMENT SERVICES

PROVIDED BY

ARTHVEDA FUND MANAGEMENT PRIVATE LIMITED

DISCLOSURE DOCUMENT

1

COVER PAGE

i The Disclosure Document has been filed with the Board along with the certificate in the prescribed format in terms of Regulation 14 of the SEBI (Portfolio Managers) Regulations, 1993 as amended from time to time.

ii The Purpose of this Document is to provide essential information about the Portfolio

services in a manner to assist and enable the Investors in making informed decision for engaging Portfolio Manager.

iii The necessary information about Portfolio Manager, required by an investor before

investing are contained in the Disclosure Document, and the investors are advised to retain the document for future reference.

iv The name, phone number, e-mail address of the principal officer as designated by the

Portfolio Manager along with the address of the Portfolio Manager are as follows:

Prinicipal Officer: Mr. Subroto Chakraborty

Address: Arthveda Fund Management Private Limited CIN : U65990MH2005PTC153219 Ground Floor, HDIL Towers, Anant Kanekar Marg, Bandra – East, Mumbai - 400051 Telephone No: 91-22-6774 8500 Email: [email protected]

DISCLOSURE DOCUMENT

2

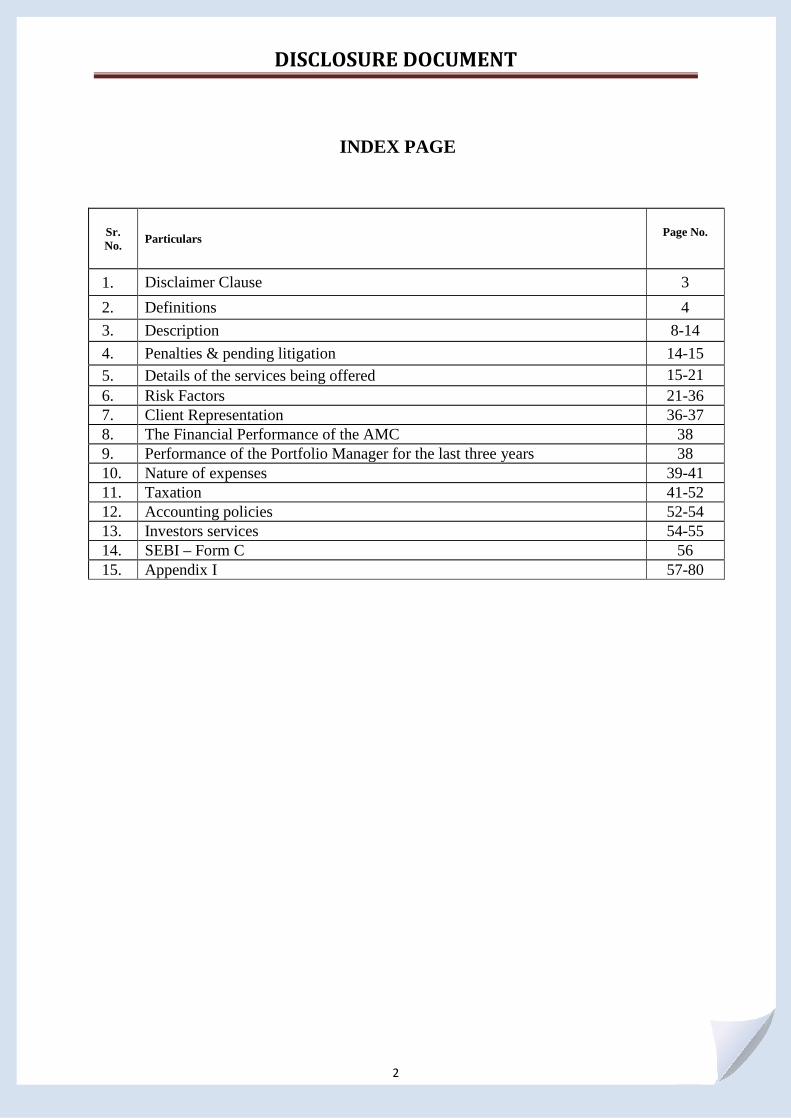

INDEX PAGE

Sr. No. Particulars Page No.

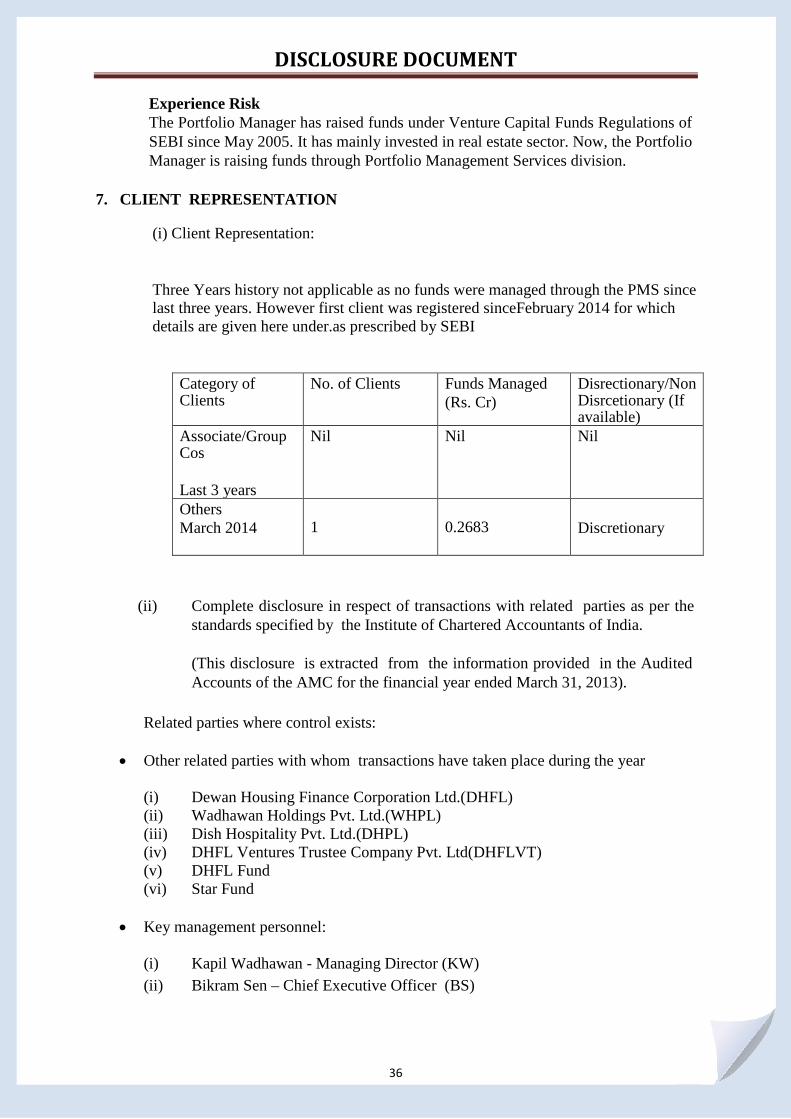

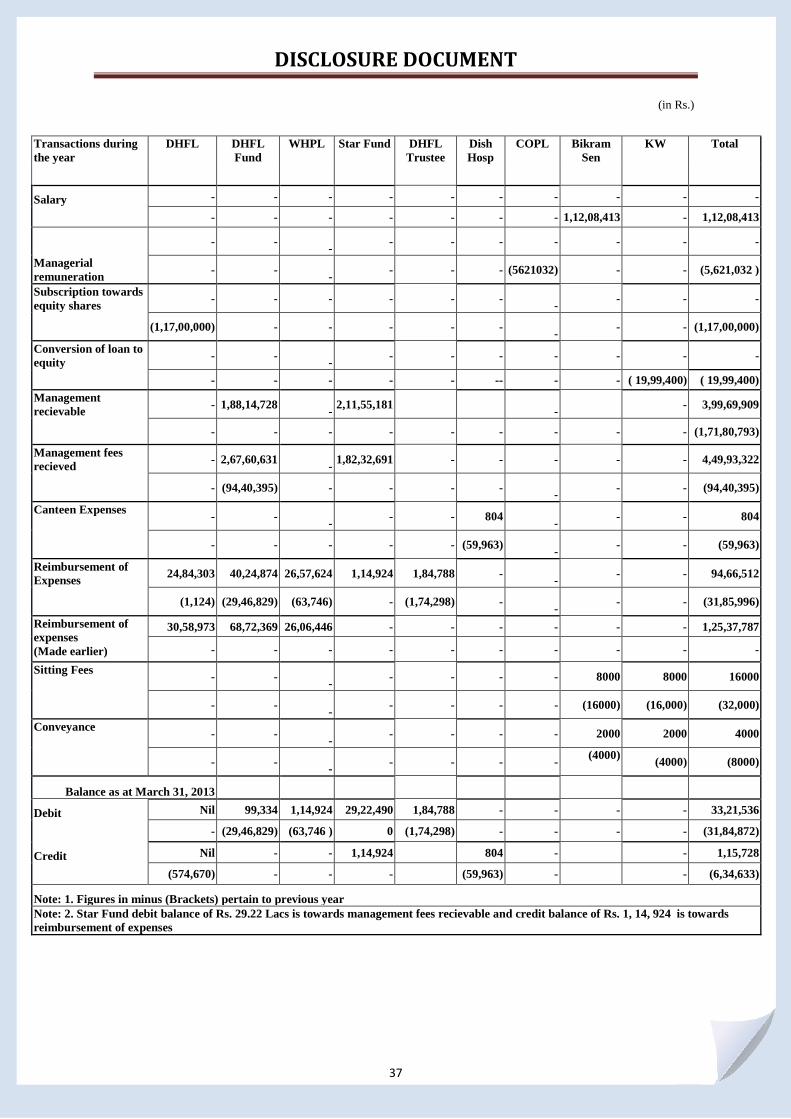

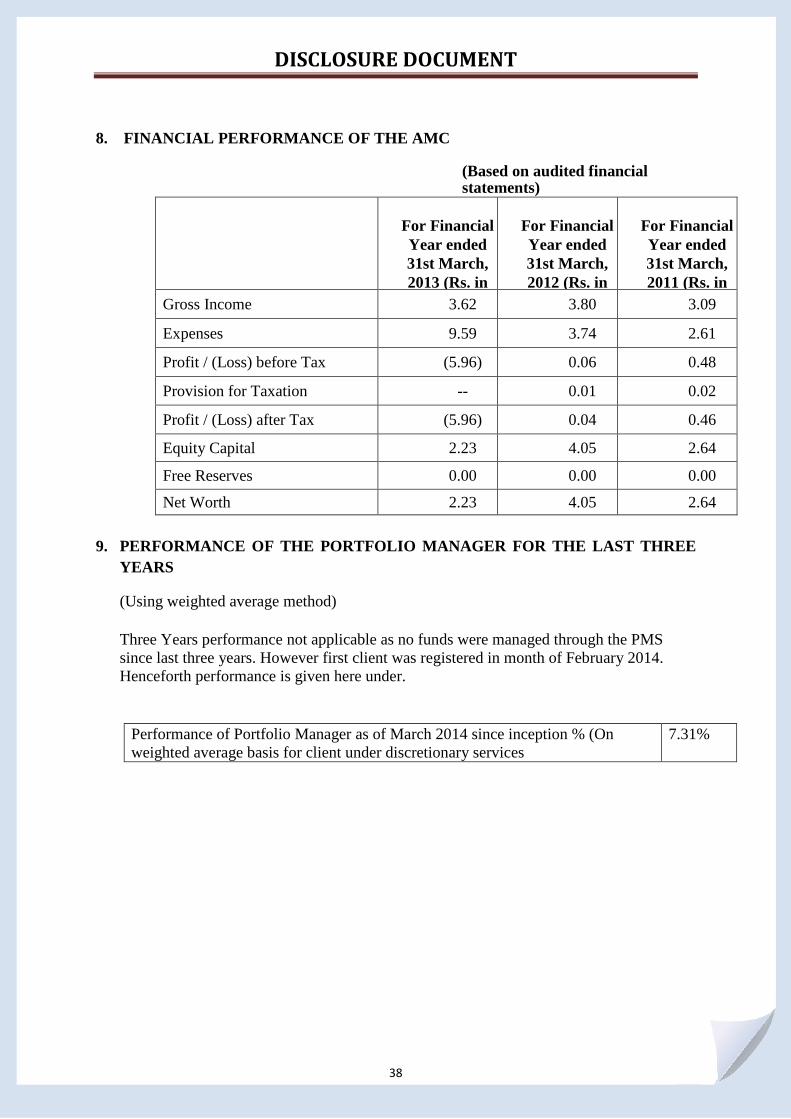

1. Disclaimer Clause 3 2. Definitions 4 3. Description 8-14 4. Penalties & pending litigation 14-15 5. Details of the services being offered 15-21 6. Risk Factors 21-36 7. Client Representation 36-37 8. The Financial Performance of the AMC 38 9. Performance of the Portfolio Manager for the last three years 38 10. Nature of expenses 39-41 11. Taxation 41-52 12. Accounting policies 52-54 13. Investors services 54-55 14. SEBI – Form C 56 15. Appendix I 57-80

DISCLOSURE DOCUMENT

3

CONTENTS OF DOCUMENT

(1) DISCLAIMER CLAUSE

DISCLOSURE DOCUMENT FOR

ARTHVEDA FUND MANAGEMENT PRIVATE LIMITED

AS ON APRIL 11, 2014

{PURSUANT TO REGULATION 14 OF THE SECURITIES AND EXCHANGE BOARD OF INDIA (PORTFOLIO MANAGERS) REGULATIONS, 1993}

i The Disclosure Document has been filed with the Board along with the certificate in the prescribed format in terms of Regulation 14 of the SEBI (Portfolio Managers) Regulations, 1993 as amended from time to time.

ii This Document has neither been approved nor disapproved by SEBI nor has SEBI

certified the accuracy or adequacy of the contents of the Document.

DISCLOSURE DOCUMENT

4

2. DEFINITIONS

In this Disclosure Document, the following words and expressions shall have the meaning specified herein, unless the context otherwise requires:

Applicable Laws Asset Management Company or AMC or AVFM or Portfolio Manager or Company

Any applicable Indian and overseas statute, law, ordinance, regulation including the SEBI Regulations, exchange control laws (including JV/WOS Regulations, LRS as may be applicable), rules, order, by law, administrative interpretation, writ, injunction, directive, judgment or decree or other instrument which has a force of law from time to time. Arthveda Fund Management Private Limited (Formerly known as DHFL Venture Capital India Private Limited),(the Asset Management Company) incorporated under the Companies Act, 1956, having CIN: U65990MH2005PTC153219 and registered with SEBI (Portfolio Managers) Regulations, 1993 as Portfolio Manager vide Registration no. INP000003567 dated July 30, 2013 (Renewed).

AUM Asset Under Management

Advisory Services Advisory Services means services whereby the Portfolio Manager provides advise to Clients on investments as described in the Agreement between the Client and the Portfolio Managers.

Client

Client or Investor

Corpus / Capital Contributed

Client means any person/entity who/which enters into the Agreement with the Portfolio Manager for availing the Portfolio Management Services.

Client or Investor means any person/entity who/which enters into the Agreement with the Portfolio Manager for availing the Portfolio Management Services

Means the value of the funds and / or the market value of securities brought in by the Client at the time of subscribing to Portfolio Management Services including additional

DISCLOSURE DOCUMENT

5

investments

Discretionary Portfolio Manager

A Portfolio Manager who exercises or may, under a contract relating to portfolio management, exercises any degree of discretion as to the investments or management of the portfolio of securities or the funds of the client, as the case may be.

Disclosure Document

Equity Related Instruments / Securities

Disclosure Document means this Disclosure Document dated April 11, 2014 for offering Portfolio Management Services.

Includes convertible bonds and debentures, convertible preference shares, equity warrants, equity derivatives, FCCBs, equity mutual funds and any other like instrument issued in India or abroad.

FII

Financial year

Fund Manager

Funds

Investment Amount

Foreign Institutional Investor registered with SEBI

Financial year means year starting from 1st April and ending on 31st March of the following year

The individual(s) appointed by the Portfolio Manager who manages, advises or directs or undertakes on behalf of the client (whether as a Discretionary Portfolio Manager or otherwise) the management or administration of a portfolio of securities or the funds of the client, as the case may be.

Funds means the monies managed by the Portfolio Manager on behalf of a Client pursuant to the PMS Agreement and includes the monies mentioned in the account opening form, any further monies placed by the Client with the Portfolio Manager for being managed pursuant to the PMS Agreement, the proceeds of sale or other realization of the portfolio and interest, dividend or other monies arising from the assets, so long as the same is managed by the portfolio manager.

The money or securities accepted by the Portfolio Manager from the Client in respect of which the portfolio management services are to be rendered by the Portfolio Manager.

DISCLOSURE DOCUMENT

6

Investment Committee

Investment Committee means the committee constituted by the Portfolio Manager comprising of the Principal Officer, the Chief Executive Officer, Executive Vice President Traded Markets & Investment Research and such other officer selected by the Chief Executive Officer/Principal Officer.

Interested Parties

JV/WOS Regulations

Interested Parties means collectively the Clients the Portfolio Manager, directors of the Portfolio Manager or members of the Investment Committee.

Foreign Exchange Management (Transfer or Issue of Any Foreign Security) Regulations, 2004, as may be amended from time to time, including any notifications issued pursuant thereto.

LRS Non-discretionary Portfolio Management Services

‘Liberalized Remittance Scheme’ issued by the RBI. The individual(s) appointed by the Portfolio Manager who manages, advises or directs or undertakes on behalf of the client (whether as a Discretionary Portfolio Manager or otherwise) the management or administration of a portfolio of securities or the funds of the client, as the case may be.

PMS Agreement or Agreement Includes contract entered between the Portfolio Manager and the Client for the management of funds or securities of the Client.

Portfolio Portfolio means Securities and/or funds managed by the Portfolio Manager on behalf of the Client pursuant to the Portfolio Management Services Agreement and includes any Securities and/or funds mentioned in the account opening form, any further Securities and/or funds placed by the Client with the Portfolio Manager for being managed pursuant to the Portfolio Management Services Agreement, Securities or other realization of the portfolio acquired by the Portfolio Manager through investment of funds and bonus, dividends or other receipts and rights in respect of Securities forming part of the portfolio, so long as the same is managed by the Portfolio Manager under the Portfolio Management Services Agreement.

DISCLOSURE DOCUMENT

7

Principal Officer

Portfolio Companies

Principal Officer means an Officer of the Portfolio Manager who is responsible for the activities of portfolio management and has been designated as principal officer by the Portfolio Manager.

Portfolio Companies means companies, enterprises, entities and special purpose vehicles in whose securities the Portfolio Manager will invest the Investment Amount of the Client pursuant to the Services contemplated by the Agreement.

NRI Non-Resident Indian

RBI Reserve Bank of India, established under the Reserve Bank of India Act, 1934, as amended from time to time.

SEBI or Board Securities and Exchange Board of India established under Securities and Exchange Board of India Act, 1992, as amended from time to time.

Securities

Securities Lending

Shall have its meaning ascribed to in Clause 5(b)(ii) of this Agreement.

Securities Lending means lending of the securities as per the Securities Lending Scheme, 1997 specified by SEBI, as amended from time to time.

The Regulations or SEBI Regulations

Securities and Exchange Board of India (Portfolio Managers) Rules and Regulations, 1993 as amended from time to time.

DISCLOSURE DOCUMENT

8

3. DESCRIPTION

i. History, Present Business and Background of the Portfolio Manager

Arthveda Fund Management Pvt. Ltd. (AVFM) is a company registered under the Companies Act, 1956, and has been registered with SEBI as a Portfolio Manager vide registration number INP000003567 dated July 30, 2013 (Renewed). • Company was formed on 12th May 2005 • Launch of first fund – DREAM FUND I (Real Estate) on 3rd October 2005 • Final closure of DREAM FUND I ( Real Estate) on 31st March 2007 with an AUM of

Rs.101.028 crores. • Eight exits from investments achieving an IRR from 20-45% • Change of name of the Company on 12th November 2011 • PMS licence obtained on 16th February 2010 • Bikram Sen appointed as CEO of the company from April 2010 • Launch of second fund – Arthveda STAR Fund (Real Estate – Middle Income

Housing Fund)(3 year term) on 14th November 2012 under SEBI (Venture Capital Fund) Regulations with a target corpus of Rs.200 crores and a green shoe option of Rs.100 crores.

• Launch of L50 in FY 2013-14 • Approval obtained from SEBI for Alternative Investment Fund - Cat II Vide

registration no. IN/AIF2/13-14/0046 dated 17th April 2013 of infrastructure support related services obtained. Subsequently, converted to AIF - Cat I Vide registration no. IN/AIF1/13-14/0099 dated March 05, 2014.

AVFM is in the business of asset management, with a focus on alternative investment funds covering asset classes such as housing, infrastructure, fixed income, traded markets, agriculture, debt and unlisted equities. AVFM was earlier known as DHFL Venture Capital India Pvt. Ltd (DHFLVC) and is an associate company of Dewan Housing Finance Corporation Ltd (DHFL). DHFL, which owns 45.92 percent of the company, is the third largest housing finance company in India and is listed on the Bombay Stock Exchange and National Stock Exchange.

The objective of AVFM is to float funds (designed by our in-house research team) that offer ample opportunities for extracting alpha, i.e. high risk-adjusted returns. The company believes in “Value Investing” and predominantly follows this principle in all its investment-decisions across asset classes. AVFM’s investor-focused approach is guided by its belief in transparency and high standards of corporate governance.

The first 7 year fund (DREAM Fund-1) of AVFM which is registered with SEBI as a venture capital fund, focused on real estate, has seen eight exits and achieved an IRR ranging between 20 and 45 per cent despite a challenging economic scenario. The remaining five investments are slated for exit apporiximately within the next year.

DISCLOSURE DOCUMENT

9

Arthveda STAR Fund which is registered with SEBI as a venture capital fund, the second fund of AVFM, is focused on mid-income housing in Tier II/III cities.

Currently, AVFM is working on several unique investment strategies for launching specially designed funds suitable for its investors across its various verticals.

ii. Promoters of the Portfolio Manager, directors and their background

(a) Promoters

Kapil Wadhawan – The Vice Chairman and Managing Director of Dewan Housing Corporation Finance Ltd. (DHFL) is one of the two promoters of the company. He has a MBA (Finance) degree from Edith Cowan University at Perth, Australia. He has indepth knowledge and understanding of real estate and financial markets in India. Sarang Wadhawan - The Vice Chairman and Managing Director of Housing Development and Infrastructure (HDIL) was the second promoter of the company. He has resigned from his directorship and holds no shares currently in the company. He has a MBA from Clarks University, Worcester, U.S.A. and is a commerce graduate from Mumbai University. Mr. Sarang Wadhawan has exposure to the real estate and housing finance industry.

DISCLOSURE DOCUMENT

10

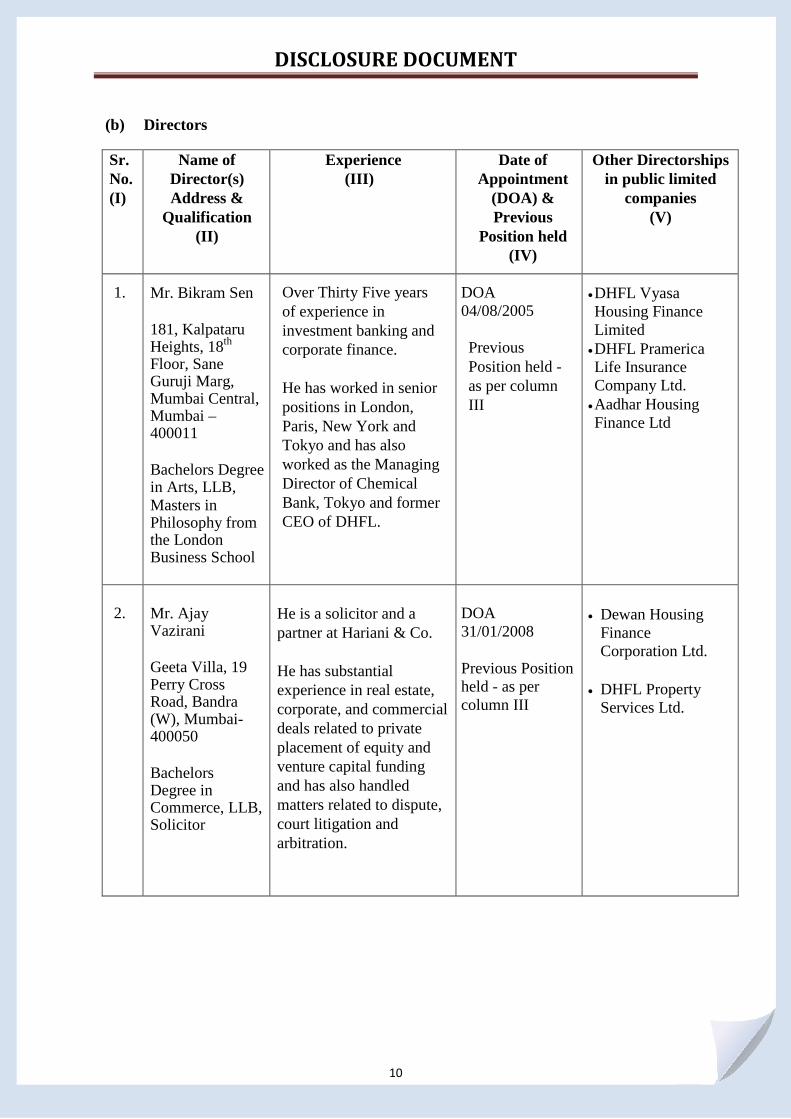

(b) Directors

Sr. No. (I)

Name of Director(s) Address &

Qualification (II)

Experience (III)

Date of Appointment

(DOA) & Previous

Position held (IV)

Other Directorships in public limited

companies (V)

1. Mr. Bikram Sen 181, Kalpataru Heights, 18th Floor, Sane Guruji Marg, Mumbai Central, Mumbai – 400011 Bachelors Degree in Arts, LLB, Masters in Philosophy from the London Business School

Over Thirty Five years of experience in investment banking and corporate finance. He has worked in senior positions in London, Paris, New York and Tokyo and has also worked as the Managing Director of Chemical Bank, Tokyo and former CEO of DHFL.

DOA 04/08/2005 Previous Position held - as per column III

• DHFL Vyasa Housing Finance Limited

• DHFL Pramerica Life Insurance Company Ltd.

• Aadhar Housing Finance Ltd

2.

Mr. Ajay Vazirani Geeta Villa, 19 Perry Cross Road, Bandra (W), Mumbai- 400050 Bachelors Degree in Commerce, LLB, Solicitor

He is a solicitor and a partner at Hariani & Co. He has substantial experience in real estate, corporate, and commercial deals related to private placement of equity and venture capital funding and has also handled matters related to dispute, court litigation and arbitration.

DOA 31/01/2008 Previous Position held - as per column III

• Dewan Housing

Finance Corporation Ltd.

• DHFL Property Services Ltd.

DISCLOSURE DOCUMENT

11

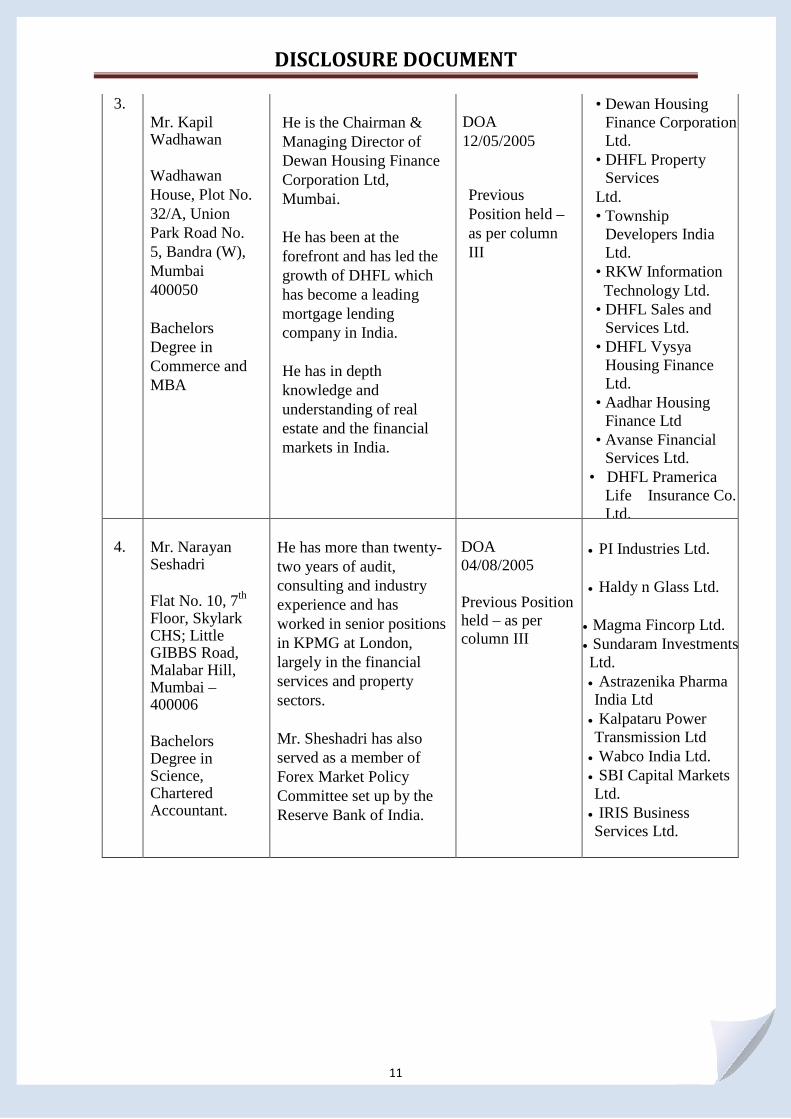

3. Mr. Kapil Wadhawan

Wadhawan House, Plot No. 32/A, Union Park Road No. 5, Bandra (W), Mumbai 400050 Bachelors Degree in Commerce and MBA

He is the Chairman & Managing Director of Dewan Housing Finance Corporation Ltd, Mumbai. He has been at the forefront and has led the growth of DHFL which has become a leading mortgage lending company in India. He has in depth knowledge and understanding of real estate and the financial markets in India.

DOA 12/05/2005

Previous Position held – as per column III

• Dewan Housing Finance Corporation Ltd.

• DHFL Property Services

Ltd. • Township

Developers India Ltd.

• RKW Information Technology Ltd. • DHFL Sales and

Services Ltd. • DHFL Vysya

Housing Finance Ltd.

• Aadhar Housing Finance Ltd

• Avanse Financial Services Ltd.

• DHFL Pramerica Life Insurance Co. Ltd.

4. Mr. Narayan Seshadri Flat No. 10, 7th

Floor, Skylark CHS; Little GIBBS Road, Malabar Hill, Mumbai – 400006 Bachelors Degree in Science, Chartered Accountant.

He has more than twenty-two years of audit, consulting and industry experience and has worked in senior positions in KPMG at London, largely in the financial services and property sectors. Mr. Sheshadri has also served as a member of Forex Market Policy Committee set up by the Reserve Bank of India.

DOA 04/08/2005 Previous Position held – as per column III

• PI Industries Ltd.

• Haldy n Glass Ltd.

• Magma Fincorp Ltd. • Sundaram Investments Ltd. • Astrazenika Pharma India Ltd

• Kalpataru Power Transmission Ltd

• Wabco India Ltd. • SBI Capital Markets Ltd.

• IRIS Business Services Ltd.

DISCLOSURE DOCUMENT

12

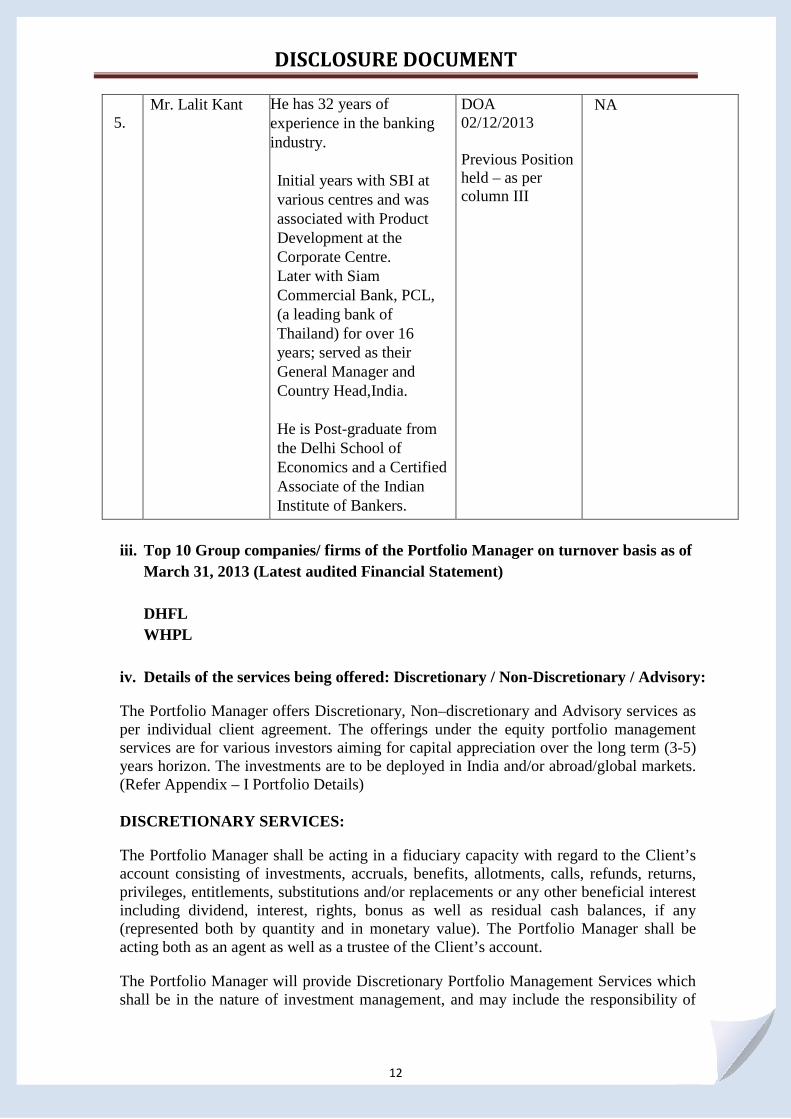

5.

Mr. Lalit Kant He has 32 years of experience in the banking industry. Initial years with SBI at various centres and was associated with Product Development at the Corporate Centre. Later with Siam Commercial Bank, PCL, (a leading bank of Thailand) for over 16 years; served as their General Manager and Country Head,India. He is Post-graduate from the Delhi School of Economics and a Certified Associate of the Indian Institute of Bankers.

DOA 02/12/2013 Previous Position held – as per column III

NA

iii. Top 10 Group companies/ firms of the Portfolio Manager on turnover basis as of

March 31, 2013 (Latest audited Financial Statement) DHFL WHPL

iv. Details of the services being offered: Discretionary / Non-Discretionary / Advisory:

The Portfolio Manager offers Discretionary, Non–discretionary and Advisory services as per individual client agreement. The offerings under the equity portfolio management services are for various investors aiming for capital appreciation over the long term (3-5) years horizon. The investments are to be deployed in India and/or abroad/global markets. (Refer Appendix – I Portfolio Details) DISCRETIONARY SERVICES:

The Portfolio Manager shall be acting in a fiduciary capacity with regard to the Client’s account consisting of investments, accruals, benefits, allotments, calls, refunds, returns, privileges, entitlements, substitutions and/or replacements or any other beneficial interest including dividend, interest, rights, bonus as well as residual cash balances, if any (represented both by quantity and in monetary value). The Portfolio Manager shall be acting both as an agent as well as a trustee of the Client’s account.

The Portfolio Manager will provide Discretionary Portfolio Management Services which shall be in the nature of investment management, and may include the responsibility of

DISCLOSURE DOCUMENT

13

managing, renewing and reshuffling the portfolio, buying and selling the securities, keeping safe custody of the securities and monitoring book closures, dividend, bonus, rights etc. so that all benefits accrue to the Client’s Portfolio, for an agreed fee structure entirely at the Client’s risk; to all eligible category of investors who can invest in Indian market including NRIs, FIIs, etc.

The Portfolio Manager shall have the sole and absolute discretion to invest in respect of the Client’s account in any type of security as per executed Agreement and make such changes in the investments and invest some or all of the Client’s account in such manner and in such markets as it deems fit would benefit the Client. The Portfolio Manager’s decision (taken in good faith) in deployment of the Clients account is absolute and final and cannot be called in question or be open to review at any time during the currency of the Agreement or any time thereafter except on the ground of malafide, conflict of interest or gross negligence. This right of the Portfolio Manager shall be exercised strictly in accordance with the relevant Acts, rules and regulations, guidelines and notifications in force from time to time.

The offerings under the equity portfolio management services are for various investors aiming for capital appreciation over the long term (3-5) years horizon. The investments are to be deployed in India and/or abroad/global markets. (Refer Appendix – I Portfolio Details)

NON-DISCRETIONARY SERVICES:

The Portfolio Manager will provide Nondiscretionary Portfolio Management Services as per express prior instructions issued by the Client from time to time, in the nature of investment consultancy/management, and may include the responsibility of managing, renewing and reshuffling the portfolio, buying and selling the securities, keeping safe custody of the securities and monitoring book closures, dividend, bonus, rights etc. so as to ensure that all benefits accrue to the Client’s Portfolio, for an agreed fee structure entirely at the Client’s risk; to all eligible category of investors who can invest in Indian market including NRIs, FIIs, etc.

The Portfolio Manager’s decision (taken in good faith) in deployment of the Clients account is absolute and final and cannot be called in question or be open to review at any time during the currency of the agreement or any time thereafter except on the ground of malafide or gross negligence. The rights and obligations of the Portfolio Manager shall be exercised strictly in accordance with the relevant Acts, rules and regulations, guidelines and notifications in force from time to time.

The offerings under the equity portfolio management services are for various investors aiming for capital appreciation over the long term (3-5) years horizon. The investments are to be deployed in India and/or abroad/global markets. (Refer Appendix – I Portfolio Details)

ADVISORY SERVICES:

The Portfolio Manager will provide Advisory Portfolio Management Services, in terms of the Regulations, which shall be in the nature of investment advisory and shall include the

DISCLOSURE DOCUMENT

14

responsibility of advising on the portfolio strategy and investment and divestment of individual securities on the clients portfolio, for an agreed fee structure entirely at the Client’s risk; to all eligible category of investors who can invest in Indian market including NRIs, FIIs, etc.

The Portfolio Manager shall be solely acting as an advisor to the portfolio of the client and shall not be responsible for the investment / divestment of securities and / or an administrative activities on the Client’s portfolio. The Portfolio Manager shall, provide advisory services in accordance with such guidelines and/ or directives issued by the regulatory authorities and /or the Client, from time to time, in this regard. The portfolio manager, only if mandated by the client, may also provide the execution services along with advisory service.

The offerings under the equity portfolio management services are for various investors aiming for capital appreciation over the long term (3-5) years horizon. The investments are to be deployed in India and/or abroad/global markets. (Refer Appendix – I Portfolio Details) Minimum Investment Amount: The value of funds for which client seeks portfolio management service including Discretionary, Non-discretionary or Advisory services, as agreed between client and portfolio manager, which is subject to minimum amount as specified under SEBI Regulations or amount specified by overseas regulator, if applicable, as amended from time to time. The Client may on one or more occasion(s) or on a continual basis, make further placement of Securities and / or funds under the service. The Client shall deposit with the Portfolio Manager, an initial corpus consisting of Securities and /or funds of an amount prescribed by Portfolio Manager for a specific Discretionary/Non-discretionary Portfolio.

4. PENALTIES AND PENDING LITIGATION:

Penalties, pending litigation or proceedings, findings of inspection or investigations for which action may have been taken or initiated by any regulatory authority

All cases of penalties imposed by SEBI or the directions issued by SEBI under the Act or Rules or Regulations made thereunder. The nature of the penalty/direction

: None

Penalties imposed for any economic offence and/ or for violation of any securities laws.

: None

Any pending material litigation/legal proceedings against the portfolio manager / key personnel with separate disclosure regarding pending criminal cases, if any.

: None

Any deficiency in the systems and operations of the portfolio manager observed by SEBI or any regulatory agency.

: None

DISCLOSURE DOCUMENT

15

Any enquiry/ adjudication proceedings initiated by SEBI against the portfolio manager or its directors, Principal Officer or employee or any person directly or indirectly connected with the portfolio manager or its directors, principal officer or employee, under the Act or Rules or Regulations made thereunder.

: None

5. DETAILS OF THE SERVICES BEING OFFERED: a. Investment Objectives and Policies: i. The present investment objectives

The Portfolio Manager provides various investment products/ services in India/abroad, based on the mandate of the Client and subject to the scope of investments as agreed upon between the Portfolio Manager and the Client in the Agreement. The investment objectives of the portfolios of the Clients depending on the Clients’ needs would be one or more of the following or any combination thereof:

a) to generate capital appreciation / regular returns by investing in equity/ derivatives / debt/ money market instruments and equity related securities and such other investment instruments as the portfolio manager deems fit in India and/or abroad/global markets.

b) to generate regular returns by primarily investing in debt and money market instruments in India and/or abroad/global markets.

c) to generate capital appreciation/ regular returns by investing in exclusively gilt securities issued by the Central/State Government securities and/or Foreign Governments, Regulators.

d) to generate capital appreciation by actively investing in equity, derivatives and equity related securities and for defensive considerations, the Portfolio Manager may invest in debt, money market instruments and derivatives in India and/or abroad/global markets.

e) to endeavour to preserve certain percentage of Investment Amount by investing in a mix of fixed income and equity derivatives in such a manner so as to secure / preserve certain percentage of Investment Amount while attempting to enhance returns by the use of equity derivatives.

f) to endeavour to earn relatively high returns by buying/selling derivatives product/ instruments in India and/or abroad/global markets.

g) to earn returns through selling options while remaining covered by an equivalent position in the underlying securities in India and/or abroad/global markets.

The Portfolio Manager will require the Client/Investor to follow all the provisions applicable to an ‘Indian Party’1 under JV/WOS Regulations or applicable to an individual under LRS.

1 Regulation 2(k) of JV/WOS Regulations defines an “Indian party” as a company incorporated in India or a body created under an Act of Parliament or a partnership firm registered under the Indian Partnership Act, 1932 making investment in a joint venture or wholly owned subsidiary abroad, and includes any other entity in India as may be notified by the Reserve Bank.

DISCLOSURE DOCUMENT

16

The compliance with JV/WOS Regulations, LRS and notifications issued pursuant thereto will have to be complied with by the Portfolio Manager and the Client/Investor for making/advising investments in international securities/products.

ii. Consistent with the objective and subject to the Regulations, the corpus will be invested in any of (but not exclusively) the following securities in India and/or abroad/global market in accordance with Applicable Laws including the SEBI Regulations and laws of foreign countries:

• Equity and equity related securities including convertible bonds (including equity

linked debentures) and debentures and warrants carrying the right to obtain equity shares;

• Shares, scrips, stocks, bonds, debentures, debentures stock or other marketable securities of a like nature in or of any incorporated company or other body corporate;

• Units or any other instrument issued by any collective investment scheme to the investors in such schemes;

• units or any other such instrument issued to the investors under any mutual fund scheme;

• Any certificate or instrument (by whatever name called), issued to any investor by any issuer being a special purposes distinct entity which possesses any debt or receivable, including mortgage debt, assigned to such entity, and acknowledging beneficial interest of such investor in such debt or receivable, including mortgage debt, as the case may be;

• Securities issued/guaranteed by the Central, State Governments, local governments and Foreign Governments (including but not limited to coupon bearing bonds, zero coupon bonds and treasury bills);

• Obligations of Banks (both public and private sector) and Development Financial Institutions like Certificate of Deposits (CDs), Coupon bearing Bonds, Zero Coupon Bonds;

• Money Market instruments permitted by SEBI/RBI and overseas regulator having jursidiction; • Certificate of Deposits (CDs); Commercial Paper (CPs); • Mutual Fund units, Fixed deposits, Bonds, debentures etc; • Derivatives including but not limited to Futures, Options, Arbitrage etc in accordance

with SEBI Regulations; • Units of venture funds and/or Alternative investement funds; • Securitisation instruments / security receipt as defined in clause (zg) of section 2 of

the Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002;

• Foreign securities as permissible by Regulations from time to time; • Rights or interest in securities; • Any other securities and instruments as permitted by the Regulations from time to

time; (“collectively, “Securities”) The above mentioned Securities are illustrative in nature. Investments can be made apart from the Securities in other instruments for instance, in ETFs and other eligible modes of investment as may permitted by the Regulations from time to time. Investments could also be made in listed, unlisted, convertible, non-convertible, secured, unsecured, rated or unrated securities or of any maturity and acquired through secondary market purchases,

DISCLOSURE DOCUMENT

17

RBI auctions, open market sales conducted by RBI etc., Initial Public Offers (IPOs), other public offers, bilateral offers, placements, rights, offers, negotiated deals, etc. The debt category will include all types of debt securities including but not limited to Securitised Debt, Pass Through Certificates, non-convertible part of partially convertible securities, corporate debt of both public and private sector undertakings, development financial institutions, trade bills, treasury bills, floating rate debt securities and fixed income derivatives like interest rate swaps, forward rate agreements etc. as may be permitted by the Act, Rules and/or Regulations, guidelines and notifications in force from time to time (collectively “other instruments”). For the sake of ease, the terms “Securities” and “and other instruments” shall be used as a single term wherever applicable. Until such time the Portfolio Manager finds appropriate investment opportunities, the Portfolio Manager may at its discretion, in all the Portfolios, invest the Client’s funds in bank deposits, units of Mutual Funds, money market instruments and/or gilt securities issued by Central/State governments/Foreign governments. Asset Classes for deployment shall be always subject to the scope of investments as agreed upon between the Portfolio Manager and the Client in the Agreement. As stated earlier the Portfolio Manager will require the Client/Investor to follow all the provisions applicable to an ‘Indian Party’ under JV/WOS Regulations or applicable to an individual under LRS. The compliance with JV/WOS Regulations, LRS and notifications issued pursuant thereto will have to be complied with by the Portfolio Manager and the Client/Investor for making/advising investments in international securities/products.

b. Types of services / products offered:

The Portfolio Manager shall provide services to all eligible category of investors who can invest in Indian/Global Markets including resident Indians, NRIs, FIIs, etc subject to applicable laws. Investment objectives may vary from client to client. Depending on the individual Client requirements, the portfolio can also be tailor-made based on the Client’s specifications. Currently the Portfolio Manager offers following categories of different portfolios. The features of the products are given below:

i. Traded Markets Portfolio:

AVFM’s strategy for the traded markets is as follows: • To invest in various traded markets across the world in equities, debt and other securities,

including derivatives. • To invest using AVFM’s investment processes which are based on value investing

principles and are designed to generate alpha, i.e. either generate market-beating returns or providing market returns at significantly reduced risks or providing optimal returns commensurate with the liquidity requirements and investment horizon of the investors.

• To invest in index strategies, including those created by and proprietary to AVFM. • To invest in domestic valuation-weighted index strategies of large-caps, mid-caps and

small-caps. • To invest in various global valuation-weighted index strategies. • To follow an active management strategy for investing in small-and-mid-caps exploiting

the mispricing and other under-valuations in the segment due to various reasons. • To follow an active management strategy for investing in large caps exploiting various

mispriced opportunities due to idiosyncrasies of the markets.

DISCLOSURE DOCUMENT

18

• To follow various valuation anomalies in the market place to design a safe portfolio which would be designed for different time durations based on the investors’ preference.

• To follow active management strategy for investing in global markets. • Please also refer Appendix -I

The investments in Traded Markets Portfolio may be made in India and/or abroad/global

markets.

ii. Debt Portfolio:

AVFM’s strategy for the Debt vertical is as follows: • To invest in AAA debt with the focus on getting optimal returns with full safety. • To invest in debt with various ratings by investing in the safest securities within a given

ratings category. The safety of the securities will be analyzed based on AVFM’s proprietary process.

• To invest in primary-issued debt of a company where AVFM’s expertise in structuring the debt would result in enhanced yield for the investors.

• To invest in listed and unlisted debt of various ratings.

The investments in Debt Portfolio may be made in India and/or abroad/global markets.

iii. Unlisted Equities Portfolio:

AVFM’s strategy for the unlisted equities is as follows: • To invest in various consumer-oriented emerging businesses with a large growth

potential, established product line, strong distribution network and brand awareness, including looking for appropriate investment opportunities in the small and medium enterprises.

• To invest in lesser known companies in the tier II/III cities of India/outside India. • To invest in upstream and downstream sectors related to housing in tier II/III cities, such

as manufacturers of construction-related materials, electrical components, bathroom fittings, kitchen fittings, home furnishings, home appliances, kitchen appliances, among others.

• To invest in service-oriented companies in emerging service sectors which are in a nascent stage but growing fast.

• To invest in promising businesses across India and other countries based on value investing principles with extensive due diligence and active monitoring of the investment until exit.

The investments in unlisted equity Portfolio may be made in India and/or abroad/global markets.

iv. Infrastructure Portfolio:

AVFM’s strategy for the infrastructure sector is as follows: • To identify small scale/short term infra investment opportunities such as in power,

roadways, telecommunication, railways, water, sewage among others.

DISCLOSURE DOCUMENT

19

• To invest in infrastructure projects with a ticket size of Rs.5 crores to Rs.50 crores or its equivalent foreign currency.

• To partner with other companies for project execution or large equity deals with companies.

• In addition, to identify larger investment opportunities with larger ticket sizes and longer duration across infrastructure sub-sectors.

The investments in Infrastructure Portfolio may be made in India and/or abroad/global markets.

v. Agriculture Portfolio:

AVFM’s strategy for the agricultural sector is as follows: • To identify investment opportunities in agriculture and agri-infrastructure including urban

infrastructure, agri-corridor development. • It will include agri-industrial development, collection and storage centres, processing

centres, cold storage and logistics and supply chains, dairies, fisheries among others. • Development of agri-focused knowledge hubs, centre of excellence, enabling

infrastructure as port, road, railways, air cargo complexes. • To partner with other companies for project execution or large equity deals with

companies.

The investments in Agricultural Portfolio may be made in India and/or abroad/global markets.

vi. Housing and Real Estate Portfolio:

AVFM’s strategy for the real estate sector is as follows: • To invest in low/middle/premium and luxury segment housing projects in carefully

selected Tier I, Tier-II/III cities and metro-outskirts with target house prices ranging from Rs. 5 lacs to Rs.5 crores.

• To invest in township, commercial, mixed-use, retail, warehousing and hotels and others. • To invest in cities with large unsatisfied demand and projects with a target ticket size of

Rs.5 crores to Rs.500 crores. • Entry would be either in Greenfield stage or distressed projects which are in under

construction or completed stage, including in leased out yield-generating assets. • To invest in developmental opportunities as well as rental-yield generating opportunities. • Identify local partners who have good experience in land aggregation, obtaining

approvals required for projects from statutory agencies, construction and marketing with the help of the India sub-adviser’s contacts with the local partners.

The investments in Housing and Real Estate Portfolio may be made in India and/or abroad/global markets.

vii. Diversified Portfolio

The portfolio may have a defined tenure. The Portfolio Manager has discretion to invest in a combination of different asset classes including but not limited to listed equities, equity

DISCLOSURE DOCUMENT

20

related instruments, or other unlisted securities/instruments (private equity) including but not limited to units issued by SEBI Registered Venture Capital Funds, Alternative Investment Funds, Mutual Funds and money market instruments in Indian and Global markets. The terms of tenure of the product, subscription and redemption etc. will be as per the agreement executed with the investor. The portfolio may offer third party guarantee on performance of one or more of the underlying funds/portfolios/securities /instruments.

c. Policies including the types of securities in which Portfolio Manager generally

invests / will generally invest

As mentioned above, the scope of investments shall be as agreed upon between the Portfolio Manager and the Client in the Agreement.

d. Investment Style & Philosophy Arthveda follows a value investing philosophy. This philosophy is a risk averse philosophy of investing in risky asset classes. This approach believes that markets are not always efficient and not all parts of the market are efficient at any given point of time. The objective is to identify pockets of inefficiency in the market. A highly selective process within this pocket of inefficiency through a detailed due diligence process is likely to yield investment opportunities which deliver high risk-adjusted returns or alpha. The value investing approach is a largely contrarian approach since the majority of the market is running after certain fads that are considered attractive at that point of time by the majority. However, whatever is the neglected portion of the market is likely to have the actual attractive opportunities and a rigorous selection process will yield lower risk opportunities that also yield high returns. The high returns come about because of the discount to the actual intrinsic value. The investment style would vary depending upon the specific requirements of the client and depending upon the type of the portfolio.

e. The policies for investments in associates / group companies of the Portfolio Manager and the maximum percentage of such investments therein subject to the applicable laws / regulations / guidelines The Portfolio Manager will, before investing in the securities of associate/ group companies, will evaluate such investments, the criteria for the evaluation being the same as is applied to other similar investments to be made under the Portfolio. Investments under the Portfolio in the securities of the group companies will be subject to the limits prescribed in the Agreement (if any) executed with the respective Client and the same would be subject to the applicable laws/regulations/guidelines.

DISCLOSURE DOCUMENT

21

f. Minimum Investment Amount: The value of funds for which client seeks portfolio management service including Discretionary, Non-discretionary or Advisory services, as agreed between client and portfolio manager, which is subject to minimum amount as specified under SEBI Regulations or amount specified by overseas regulator, if applicable, as amended from time to time. The Client may on one or more occasion(s) or on a continual basis, make further placement of Securities and / or funds under the service. The Client shall deposit with the Portfolio Manager, an initial corpus consisting of Securities and /or funds of an amount prescribed by Portfolio Manager for a specific Discretionary/Non-discretionary Portfolio.

6. RISK FACTORS

The risk factors given below are applicable to all the portfolios offered by the Portfolio Manager. Additional portfolio specific risk factors have been separately detailed in this Document.

• Securities investments, Whether in India or abroad are subject to market risks and

there is no assurance or guarantee that the objective of investments will be achieved.

• Past performance of the Portfolio Manager does not indicate its future performance.

• Investors are not being offered any guaranteed or assured return/s i.e. either of

Principal or appreciation on the portfolio.

• Investors may note that the Portfolio Manager’s investment decisions may not be always profitable, as actual market movements may be at variance with anticipated trends.

• The liquidity of the Portfolio’s investments whether in India or abroad is

inherently restricted by trading volumes in the securities in which it invests.

• The valuation of the Portfolio’s investments whether in India or abroad, may be affected generally by factors affecting securities markets, such as price and volume volatility in the capital markets, interest rates, currency exchange rates, changes in policies of the Government, taxation laws or any other appropriate authority policies and other political and economic developments which may have an adverse bearing on individual securities, a specific sector or all sectors including equity and debt markets. There will be no prior intimation or prior indication given to the Clients when the composition/ asset allocation pattern changes.

• Trading volumes, settlement periods and transfer procedures may restrict the

liquidity of the investments made by the Portfolio. Different segments of the Indian financial markets have different settlement periods and such periods may be extended significantly by unforeseen circumstances. The inability of the Portfolio Manager to make intended securities purchases due to settlement

DISCLOSURE DOCUMENT

22

problems could cause the Portfolio to miss certain investment opportunities. By the same rationale, the inability to sell securities held in the Portfolio due to the absence of a well developed and liquid secondary market for debt securities would result, at times, in potential losses to the Portfolio, in case of a subsequent decline in the value of securities held in the Portfolio.

• The Portfolio Manager may, considering the overall level of risk of the

Portfolio, invest in lower rated/ unrated securities offering higher yields. This may increase the risk of the Portfolio. Such investments shall be subject to the scope of investments as laid down in the Agreement.

• In case of Dividend Yield Portfolios, returns of the Portfolio could depend on the

dividend earnings and capital appreciation, if any, from the underlying investments in various dividend yield companies. The dividend earnings of the Portfolio may, vary from year to year based on the philosophy and other consideration of each of the high-dividend yield companies. Further, it should be noted that the actual distribution of dividends and frequency thereof by the high-dividend yield companies in future would depend on the quantum of profits available for distribution by each of such companies. Dividend declaration by such companies will be entirely at the discretion of the shareholders of such companies, based on the recommendations of its board of directors. Past track record of dividend distribution may not be treated as indicative of future dividend declarations. Further, the dividend yield stocks may be relatively less liquid as compared to growth stocks.

• Securities, which are not quoted on the stock exchanges, are inherently illiquid

in nature and carry a larger amount of liquidity risk, in comparison to securities that are listed on the exchanges or offer other exit options to the investor, including a put option. The Portfolio Manager may choose to invest in unlisted securities that offer attractive yields. This may however increase the risk of the Portfolio. Such investments shall be subject to the scope of investments as laid down in the Agreement.

• While securities that are listed on the stock exchange carry relatively lower

liquidity risk, the ability to sell these investments is limited by the overall trading volume on the stock exchanges. Money market securities, while fairly liquid, lack a well-developed secondary market, which may restrict the selling ability of the Portfolio(s) and may lead to the investment(s) incurring losses till the security is finally sold.

• The Portfolio Manager may, subject to authorisation by the Client in writing,

participate in securities lending. The Portfolio Manager may not be able to sell/ lend out securities, which can lead to temporary illiquidity. There are risks inherent in securities lending, including the risk of failure of the other party, in this case the approved intermediary to comply with the terms of the agreement. Such failure can result in a possible loss of rights to the collateral, the inability of the Approved Intermediary to return the securities deposited by the lender and the possible loss of corporate benefits accruing thereon.

DISCLOSURE DOCUMENT

23

• To the extent that the portfolio will be invested in securities denominated in foreign

currencies, the Indian Rupee equivalent of the net assets, distributions and income may be adversely affected by changes in regulations concerning exchange controls or political circumstances as well as the application to it of other restrictions on investment.

• Interest Rate Risk: As with all debt securities, changes in interest rates may affect

valuation of the Portfolios, as the prices of securities generally increase as interest rates decline and generally decrease as interest rates rise. Prices of long-term securities generally fluctuate more in response to interest rate changes than prices of short-term securities. Indian debt markets can be volatile leading to the possibility of price movements up or down in fixed income securities and thereby to possible movements in the valuations of Portfolios.

• Liquidity or Marketability Risk: This refers to the ease with which a security

can be sold at or near to its valuation yield-to-maturity (YTM). The primary measure of liquidity risk is the spread between the bid price and the offer price quoted by a dealer. Liquidity risk is today characteristic of the Indian fixed income market.

• Credit Risk: Credit risk or default risk refers to the risk that an issuer of a fixed

income security may default (i.e., will be unable to make timely principal and interest payments on the security). Because of this risk corporate debentures are sold at a higher yield above those offered on Government Securities which are sovereign obligations and free of credit risk. Normally, the value of a fixed income security will fluctuate depending upon the changes in the perceived level of credit risk as well as any actual event of default. The greater the credit risk, the greater the yield required for someone to be compensated for the increased risk.

• Reinvestment Risk: This risk refers to the interest rate levels at which cash flows

received from the securities under a particular Portfolio are reinvested. The additional income from reinvestment is the “interest on interest” component. The risk is that the rate at which interim cash flows can be reinvested may be lower than that originally assumed.

• Currency Risk: The Portfolio Manager may also invest in overseas Fixed Income

or other Securities/ instruments as permitted by the concerned regulatory authorities in India. To the extent that the portfolio of the Scheme will be invested in securities/ instruments denominated in foreign currencies, the Indian Rupee equivalent of the net assets, distributions and income may be adversely affected by changes/fluctuation in the value of certain foreign currencies relative to the Indian Rupee. The repatriation of capital to India may also be hampered by changes in regulations concerning exchange controls or political circumstances as well as the application to it of other restrictions on investment.

• Overseas Investment Risk: The Portfolio Manager may invest in overseas

securities/products in accordance with the Applicable Laws including the SEBI

DISCLOSURE DOCUMENT

24

Regulations, exchange control laws and laws of overseas market in which the investment is being made. The Client would be required to follow Portfolio Manager’s instructions wherever required/needed and ensure compliance with the same in order to make such overseas investments. Such investments may be subject to several rules/regulations both Indian and overseas and in case of any non-compliance, the value of such investment may be affected. Such overseas investment carry both the regulatory/legal risks as well as risks pertaining to fluctuation in pricing/value of such investments. The currency risk, market price risk, repatriation risk, regulatory risk in India with respect to permissibility of such investments both from the perspective of SEBI and RBI are the factors attached to such overseas investments. The Portfolio Manager may have to modify its offerings from time to time keeping in view some of these risk factors. The Client while signing the portfolio management services agreement should make itself aware of the aforesaid risks.

• Risk factors specific to Fixed Defined Tenure Portfolios

The additional risk factors in this portfolio relate to lack of liquidity of instruments including units, frequency of disclosure of valuation of underlying units, valuation risks, risk of change in underlying due to changes or factors which may affect the issuer of units/ decisions of the unitholders and changes in regulation which may adversely affect the interest of the clients.Given that the Portfolio Manager may be investing in units being non- exchange traded instruments, the risks of investment in such non-exchange instruments include counterparty default risks and liquidity risks.

Some underlying sectors based on which units are issued may tend to be illiquid and the illiquidity of the sector may translate into illiquidity of the holdings and hence this portfolio may be exposed to a higher level of liquidity risks than normal portfolio risks exposed only to equity/exchange listed instruments.

• The Portfolio Manager may use various derivative products as permitted by the

Regulations. Use of derivative requires an understanding of not only the underlying instrument but also of the derivative itself. Other risks include, the risk of mispricing or improper valuation and the inability of derivatives to correlate perfectly with underlying assets, rates and indices.

• The Portfolio Manager may use derivatives instruments like Stock Index

Futures, Interest Rate Swaps, Forward Rate Agreements or other derivative instruments, as permitted under the Regulations and guidelines. Usage of derivatives will expose the Portfolio to certain risks inherent to such derivatives.

• The Portfolio and returns offered there from offered by the Investment Manager as

per Appendix – I, may compare unfavourably with benchmark indices like Nifty – Fifty index, Nifty Junior Index, CNX 200 Index, CNX Mid Cap Index, S&P BSE Mid Cap Index, CNX Small Cap Index, S&P BSE Small Cap Index, CNX 500 Index, S&P BSE 500, S&P 500 Index, Dow Jones 30 Index, S&P Midcap 400 Index Etc..on account of various domestic and global economic factors.

DISCLOSURE DOCUMENT

25

• Specific Risk factors pertaining to Diversified Portfolio:

The Portfolio Manager may make substantial investment in unlisted securities/instruments (private equity). The investment in private equity may be made in the units issued by SEBI registered Venture Capital Fund, Alternative Investment Funds, Mutual Funds in Indian and Global markets or any other instrument available in the market. The major risk factors pertaining to investment in Venture Capital Fund, Alternative Investment Funds, Mutual Funds and money market instruments in Indian and Global markets are given herein below. Investors are advised to read carefully the product specific risk factors mentioned in detail, in the Agreement to be executed with Portfolio Manager, before making investment.

Nature of Investment The Portfolio Manager may invest in such Venture Funds, Alternative Investment Funds, Mutual Funds in Indian and Global markets (the Fund), which may invest in companies that are experiencing or have experienced severe financial difficulties. Many of such investments made by the Fund may be illiquid, and there can be no assurance that the Fund will be able to realize profits on its investments in a timely manner.

Since the Fund may make only a limited number of investments and these may involve a high degree of risk, poor performance by even a few of these investments could lead to adverse effects on the returns received by investors.

Restrictions on Withdrawal and Transfer Investors may not be able to voluntarily withdraw from the Fund. In addition, they may not be able to transfer any of the interests, rights, or obligations with regard to the Fund except as may be provided the agreement and the applicable regulations. Risks attached with the use of derivatives As and when the Portfolio Manager trade in the derivatives market there are risk factors and issues concerning the use of derivatives that investors should understand. Derivative products are specialized instruments that require investment techniques and risk analysis different from those associated with stocks and bonds. The use of a derivative requires an understanding not only of the underlying instrument but also of the derivative itself. Derivatives require the maintenance of adequate controls to monitor the transactions entered into, the ability to assess the risk that a derivative adds to the portfolio and the ability to forecast price or interest rate movements correctly. There is the possibility that a loss may be sustained by the portfolio as a result of the failure of another party (usually referred to as the “counter party”) to comply with the terms of the derivatives contract. Other risks in using derivatives include the risk of mis pricing or improper valuation of derivatives and the inability of derivatives to correlate perfectly with underlying assets, rates and indices.

DISCLOSURE DOCUMENT

26

Thus, derivatives are highly leveraged instruments. Even a small price movement in the underlying security could have a large impact on their value. Also, the market for derivative instruments is nascent in India.

Trading in derivatives SEBI in terms of Securities and Exchange Board of India (Portfolio Managers) Amendment Regulations, 2002, has permitted all the Portfolio Managers to participate in the derivatives trading subject to observance of guidelines issued by SEBI in this behalf. Pursuant to this, the Portfolio Managers may use various derivative and hedging products from time to time, as would be available and permitted by SEBI, in an attempt to protect the value of the portfolio and enhance the Clients’ interest.

Accordingly, the Portfolio Manager may use derivatives instruments like Stock Index Futures, Options on Stocks and Stock Indices, Interest Rate Swaps, Forward Rate Agreements or other such derivative instruments as may be introduced from time to time, as permitted by SEBI.

• RISKS SPECIFIC TO INVESTMENTS IN PORTFOLIOS

RELATING TO INVESTMENT IN SECURITIES/INSTRUMENTS WITH UNDERLYING ASSETS ASSOCIATED WITH REAL ESTATE AND INFRASTRUCTURE Title This is a well known fact that the system of documentation of land records in India has still not been fully computerized. In the cities where the system is yet to be computerized, the maintenance and updation of land records is done manually which means that the records of all land related documents are physically updated. In some states, the process of computerization of records is underway which is a long drawn and time consuming process and because of the sheer number of records, the possibility of inaccurate records cannot be ruled out. The process and the report of title verification mainly depend on the availability of records with the respective revenue department and at sub-registrar’s office. Due to pending computerization of records, non- availability of records and errors in the records, the possibility of an error in the title report of the underlying property cannot be ruled out.

Land Acquisition The right to own property in India or abroad is subject to restrictions that may be imposed by the Government of respective countries. Particularly, the Government has a right to acquire any land or a part thereof if such acquisition is for a ‘public purpose’ and after paying the owner reasonable compensation. However, this compensation may not be at the fair market value i.e. the price that such property might have fetched if it were sold in the market.

Therefore, the real property or a part that the underlying assets represent, might be acquired by the Government, if the Government is of the view that such property has to be used for a ‘public purpose’. Further, the

DISCLOSURE DOCUMENT

27

compensation paid for this purpose may not be adequate to compensate for the loss of such real property which may have an adverse impact on AVFM.

Further, the government may specify certain lands to be either allotted for specific purpose and to be developed within a specified time or are leased from municipal corporation/ port trust, industrial development corporation, development authority or similar government or quasi-governmental authority for a long term. On completion of the specific purpose or expiry of lease, the land allotted / leased shall revert to the specified Government body. Certain terms and conditions such as renewal of lease, termination of lease etc. are also attached to the allotment or lease of land and hence the letter of allotment or the lease agreement and the related documents need to be scrutinized thoroughly.

Environmental Laws Courts have implemented the “Polluter pays” principle in the field of Environment Law, whereby the person, company or industry responsible for the pollution, through the use or disposal of hazardous or toxic substance either on under or in a property, would be liable to restore the degradation of the property and the surrounding environment and compensate any victims thereby. The presence of contamination or hazardous or toxic substances, may adversely affect the investments made by AVFM in any underlying assets which may be affected thereby and hence have an adverse impact on the returns. Preventive measures are to be taken by the developer for cleansing the soil with the use of latest technology.

With the changing times and increased awareness among the people, the Government has also become pro-active and over a period of time have introduced various legislations and regulations and accordingly require various approvals from the state pollution control boards (water and air) as well as approvals from Ministry of Environment and Forest (MoEF). Violation of such approvals or non-procurement of such approvals may drastically and adversely affect the progress of the project and may lead to stoppage of project.

Coastal Regulation Zones (CRZ) also prevent development on coastal areas as the same harms or contaminates such areas near to water bodies.

Rent Control Various Countries have enacted rent control laws, which, inter alias, place restriction on the amount of rent that may be collected from tenants. If AVFM has invested in instruments where the underlying assets represent property that comes under the purview of rent control laws, this may adversely impact the returns that AVFM may get from such property and thus consequently have an adverse effect on the performance of AVFM.

Litigation and stay / injunction on development Litigation in India is long drawn and time consuming and complicated process and there is generally a preponderance of litigation with respect to property. If any property in which the investments by AVFM is subjected to any litigation (litigation may commence after AVFM has invested in the underlying asset), this

DISCLOSURE DOCUMENT

28

could have an adverse impact, financial or otherwise on the investments by AVFM.

Tenancy Risk The bankruptcy or insolvency of or vacation by a significant tenant or a number of smaller tenants would have an adverse impact on the cash flows of the project. This risk is primarily faced by yield based investments.

Use of Agricultural Land and Zoning In various countries including India, certain lands are earmarked as agricultural lands, wherein only agricultural activities are permitted to be carried out. In order to carry out any non-agricultural activity, a prior approval/permission from appropriate authority is required to be obtained. This approval may be given by the authority, at its own discretion or with certain conditions. Generally, only an agriculturist (a person indulged in farming or agricultural activities) is permitted to buy agricultural property. Corporates are prohibited from acquiring agricultural properties. Hence, if the Portfolio Company in which AVFM is investing decides to acquire and utilize agricultural land, it is required to necessarily obtain a prior approval for using the land for non-agriclutural purposes. If such Portfolio Company fails to get the authority’s approval for usage for non-agricultural purposes before it has transferred in its name, then the Company would not be able to utilize such land for any non-agricultural purposes and this could affect AVFM. Properties are divided into various zones either generally or through some municipal master plan or development plan for a particular area. Such zones can be industrial zone, commercial zone, residential zone, no development zone, coastal zone etc. Development in such zones is restricted to that particular purpose, for e.g. an industrial zone will not have any residential development. If required, conversion of zone from one zone to another is required before commencement of a particular development/activity. This can be carried out only if permission for conversion is obtained in advance. For instance residential development is usually not permitted in an industrial zone unless and to the extent permitted as ancillary or incidental to the industrial development.

Investment Risks Most of the investments made by AVFM may be in unlisted companies whose securities should be considered illiquid. These investments may be difficult to value and to sell or otherwise liquidate, and the risk of investing in such companies is much greater than the risk of investing in publicly traded securities. Moreover, these unlisted companies are not regulated by the same disclosure and investor protection norms that apply to listed companies.

Nature of Investments Many of the investments made by AVFM will be illiquid, and there can be no assurance that AVFM will be able to realize profits on its investments in a timely manner.

DISCLOSURE DOCUMENT

29

AVFM make only a limited number of investments and these may involve high degree of risk. Poor performance by even a few of these investments could lead to adverse effects on the returns received.

In addition, the AVFM will compete with other Investors for investments in Portfolio Companies. This may result in fewer attractive investment opportunities. The Portfolio Manager may not be able to identify and successfully close a sufficient number of high-quality investments. In addition, such competition may have an adverse effect on the length of time required to fully invest the funds of AVFM which may have a substantial adverse impact on potential returns.

Investment Selection The Portfolio Companies may or may not have been identified at the time of commencement of the Portfolio. Accordingly, prospective clients may not have an opportunity to review the Portfolio Companies or the terms of AVFM’s investments in the Portfolio Companies prior to investing in AVFM. Performance Risks A portion of the Portfolio may be invested in companies in highly competitive markets or product segments dominated by firms with substantially greater financial and possibly better technical resources than the Portfolio Companies in which AVFM invests. They may operate in product segments that face technological changes and / or may be dominated by other firms or organizations. These and other inherent business risks could affect the performance of the Portfolio Companies, and affect the value of the equity investments, thereby affecting the Portfolio.

Restriction on Withdrawal and Transfer Investors may not be able to voluntarily withdraw from the Fund or transfer any of the interests, rights, or obligations with regard to the Fund except as may be provided in the Agreement and the applicable regulations.

Dilution and valuation risk Subsequent to the investments in the underlying Portfolio Companies by the Investors of India Real Estate Securities Portfolio, the underlying Portfolio Companies may admit other new investors at a price, which may be at a discount to the prevailing asset value of AVFM’s investment. This may result in dilution of the value of the holdings by the existing Clients of India Real Estate Securities Portfolio. Further, the valuation of such investments is subjective and the value arrived at by the Portfolio Manager or an independent auditor may not reflect the true value of the investments.

Portfolio Risk There is a risk of concentration of investments especially in the asset classes relating to the Portfolio.

To mitigate this risk AVFM will seek to have a fair degree of diversification in its investments both by geographic region or asset type. AVFM will invest across

DISCLOSURE DOCUMENT

30

residential, commercial and retail properties including but not limited to industrial, hotel, hospital, warehousing and other types of properties. Further, to derisk from the down cycle of the market, AVFM proposes to invest in the projects having varying exit horizons.

Entitlement Risks and Development Risk The AVFM generally invests in companies focused on developing some properties in which it is investing from a “Greenfield” start. Although AVFM intends to invest in companies and partners with developers (who could be shareholders in the respective Portfolio Companies) having good track record of handling such development projects, it will still have various development risk, delay in project risk, regulatory risk, statutory approval risk etc.

The entitlement risk associated with the purchase of land can be partly addressed by buying the land from a reliable source and partly by making the developer to bear this risk.

Development risk can be partly mitigated by providing an incentive structure to the developers for timely completion of the project and to have adequate penal clauses in order to deter him from defaulting on the completion timelines. The incentive structure envisaging disproportionate sharing of profit in the Portfolio Company and/or project, after a hurdle rate, will bring in more discipline from the developer towards the project. However, development risk on integrated township projects and Special Economic Zones would be high on account of political and regulatory risks, which could lead to significant time and cost overruns. Besides, projects where the Portfolio Company bids for the land may subsequently get delayed due to time lag in obtaining regulatory or statutory approvals. Non-availability of various building materials and shortage of labour may also lead to delay in the project as well as rise in the project cost. Wrong product-mix, competing project, development at far flung underdeveloped areas may also have an adverse impact on the investment. Cost Overruns The Portfolio Manager will work with investee companies and endeavour to awarding a fixed term contract to reputed construction agencies with the possibility of including penal clauses if there is a material delay or cost overrun in the project. In addition, the investee companies will have a separate Project Group located at the site to ensure timely implementation of the project and also to ensure that the construction quality is as per the contracted norms. Based on the same the risk in delay or cost overrun due to increased construction time expected to be is minimal. There can be opportunity loss due to delays, which may not be fully compensated by liquidated damages from the Engineering Procurement Construction (EPC) contractor. Besides, volatility or upward movement in commodity prices, especially of cement and steel, could result in cost overruns that may not be fully absorbed by the EPC contractors. Projects could also face time and cost overruns due to force majeure risks that may not be mitigated.

DISCLOSURE DOCUMENT

31

FSI / FAR and Height restrictions Floor Space Index (FSI) / Floor Area Ratio (FAR) sanctioned for utilization also affects the potential development of the project as the sanctioned FSI/FAR may vary from that of the one targeted. Height restrictions also prevail in various regions depending proximity from airport and defense base areas, which affect the development of a project in terms of height. Market Cycles Timing to market cycle is very important in this sector. The investment looking favorable in the up market cycle may become a loss-making proposition in the down cycle. There will always be risk associated with the market cycle. This can be partly addressed by diversifying the portfolio across geographic region, asset type and exit time horizon.

Management and Operational Risks Reliance on the Portfolio Manager The Investment Committee advises the Portfolio Manager regarding the investments and divestments and the Clients will not be able to make investment or other decisions in the business of AVFM.

The success of AVFM will depend to a large extent upon the ability of the Portfolio Manager, to source, select, complete and realize appropriate investments. The success of AVFM will also depend upon the judgment of the Investment Committee and the Portfolio Manager in reviewing investment proposals for AVFM. The Portfolio Manager will have considerable latitude in its choice of Portfolio Companies and the structuring of investments. Accordingly, no person should invest in AVFM unless such person is willing to entrust all aspects of the Management to the Portfolio Manager.

Indemnification of Directors and Employees of the Portfolio Manager: The Client Agreement provides for indemnification of the Portfolio Manager for any and all actions, suits, proceedings, claims, damages, settlement payments, losses and liabilities arising in connection with the Client Agreement, unless they result from gross negligence or willful misconduct.

Indemnification of the Directors of the Portfolio Manager, as well as other parties, may impair the financial condition of AVFM and its ability to acquire assets or otherwise achieve its investment objective or meet its obligations.

Failure to Infuse Additional Funds: Default by Clients of their obligations to infuse additional funds in the event of the Drawdown may cause the AVFM to lack the capital necessary to make planned investments in Portfolio Companies. Such default may, consequently, cause AVFM to breach its agreement with a Portfolio Company which may result AVFM to owe damages to such company. Loss of such opportunities, as well as the payment of damages, could result in a material adverse effect on the performance of AVFM.

DISCLOSURE DOCUMENT

32

India-Related Risks: Political, Economic and Social Risk: Political and Socio-Economic factors, changes in Indian law or regulations and the status of India’s relations with other countries may adversely affect the value of the AVFM. In addition, the Indian economy may differ favorably or unfavorably from other economies in several respects, including the rate of growth of gross domestic product, the rate of inflation, capital reinvestment, resource self-sufficiency, future actions of the Indian central government or the respective Indian state governments could have a significant effect on the Indian economy, which could adversely affect private sector companies, market conditions and prices and yields of the portfolio securities. The occurrence of selective unrest, or external tension, could adversely affect India’s political and economic stability and, consequently, adversely affect AVFM’s investment in Portfolio Companies.

India’s Political, Economic and Social stability is related to various factors such as the possibility of nationalization, expropriations or taxation amounting to confiscation, political changes, government regulation, social instability, diplomatic disputes or other similar developments which are beyond the control of the Portfolio Manager, could adversely affect AVFM’s investments.

Government Approvals: Certain governmental approvals, local authority approvals, including approvals from the Securities and Exchange Board of India (SEBI) or the central government may be required before AVFM can make investments in Portfolio Companies. It is likely that all or some of these approvals are required to be obtained prior to the closing of AVFM. While the Portfolio Manager expects to obtain these governmental approvals within three months from the closing of offering of AVFM, the Portfolio Manager cannot be certain that these approvals will be given by the appropriate authority. The Portfolio Manager shall not be liable in any manner if any approval from the Government is not forthcoming and/or is not obtained and / or cannot be obtained for any reason whatsoever.

AVFM operates under Indian laws and securities regulations. If policy announcements or regulations are made subsequent to this offering, which require retrospective changes in the structure or operations of AVFM, these may adversely impact the performance of AVFM.

Tax Risks: Clients invested in AVFM are subject to a number of risks related to tax matters. In particular, the tax laws relevant to AVFM are subject to change, and tax liabilities could be incurred by Clients as a result of such changes. The tax consequences of an investment in AVFM are complex, and the full tax impact of an investment in AVFM will depend on circumstances particular of each investor and the additional peculiarities associated with respect to activities of each Portfolio Company and securities issued by such Companies. Accordingly,

DISCLOSURE DOCUMENT

33

prospective Clients are strongly urged to consult their tax advisors with specific reference to their own situations.

International / Financial Risk: There may also be an impact on saleability, demand-supply of the developed / developable Property based on the prevailing international and financial scenario. Risk of non-deployment of funds

The available funds may not be deployed due to non-availability of appropriate projects / promoter or due to regulatory aspects applicable to AVFM.

Others Risks: Troubled Origination The Portfolio Manager may make substantial investments in non-performing or other troubled assets, which involve a degree of financial risk and which are experiencing or are expected to experience severe financial difficulties, which may never be overcome fully. As a result, the standards by which such investments were originated, the recourse to the selling institution or the standards by which such Investments are being serviced or operated may be adversely affected. Further, Investment in properties operating under the close supervision of a mortgage lender are, in certain circumstances, subject to certain additional potential liabilities which may exceed the value of the Portfolio‘s original investment therein. For example: under certain circumstances, lenders who have inappropriately exercised control of the management and policies of a debtor may have their claims subordinated or disallowed or may be found liable for damages suffered by parties as a result of such actions.