Embed Size (px)

Citation preview

CONFIDENTIAL – DO NOT CIRCULATE

OUTSTANDING CANADIAN TAX ISSUES (As at September 26, 2013)

Note:

The following issues are organized by committee or working group, with some general items

As items are successfully addressed or no longer pursued, they are moved to a COMPLETED page without using track changes

Text in bold and highlighted in yellow in the status column indicates the action under way

For U.S. tax matters, contact Andrea Taylor ([email protected]) for FATCA matters and Andrea or Jack Rando ([email protected]) for foreign transaction tax (FTT) matters.

TRFI = tax-reporting financial institution (e.g., dealers).

GENERAL

ISSUE STATUS

1. Miscellaneous technical red tape reduction measures: The IIAC recommends: a file of current withholding tax rates by country and revenue type that can be delivered electronically to firms involved in withholding taxes; push e-mail to, webpages for, online issue-tracking database supporting, access to specialists by, and consultations regarding efficiencies for financial institution tax slip/filing preparers; clarifying revisions to requirement-to-pay (RTP) requirements; and better co-ordination among the CRA, Human Resources and Skills Development Canada (HRSDC), MRQ and on occasion clients and financial institution tax filing/slip preparers

Attended November 13, 2012 meeting with CRA consultation directorate on alleviating small business admin burden; expected report in April 2013; IIAC followed up on September 26 on July 3 CRA announcement by e-mail that the report would be circulated shortly to information session participants; IIAC reviewing report and will summarize for members

2. Strategic general CRA red tape reduction measures: The IIAC, with help from Jillian Welch, PWC, and IFIC, is seeking a partnership with CRA to develop a permanent strong advisory committee as exists for other industry/expert groups.

Proposal sent March 18, 2013; received acknowledgement of letter and agreement to meet at senior level; IIAC and IFIC developed agenda for first meeting; IIAC working to confirm date of first meeting proposed for October 29 or 30

CONFIDENTIAL – DO NOT CIRCULATE - 2 -

TAXATION REPORTING COMMITTEE (TRC)

TAXATION REPORTING COMMITTEE ISSUE STATUS

3. T5013 and T5013A Combination and move to XML: CRA is requiring TRFIs to change all box numbers and moving to a very different form version that would have mostly floating boxes and creating a single XML layout for the new combined slip.

T5013 submission sent May 29, 2012; IIAC advised that a move to XML and combining the forms makes sense but time is needed for implementation and final requirements are needed by May/June; meeting requested for early May; T5013 forms were to be available on the early access site by May 31, 2013 to enable software developers to begin working on them, however, this was delayed; IIAC met, called and exchanged e-mails multiple times and continues pressing CRA on this; as of late August, IIAC meeting weekly with CRA; IIAC to continue meetings until situation resolved and prepare communications strategy and documentation for issuers and accounting firms to mitigate criticisms

4. Annual tax season review: The IIAC shares data re re-filings and does facilitates industry, post mortem. Members meet with CRA to review past year’s reporting and press for early access to information for next tax season to the extent not addressed in other items here

Meeting with CRA held August 8, 2013; significant improvement in error and delay reduction due to ever-greater improvements by IIAC members and staff preparation of issuers; this is expected to reverse in 2014 due to significant changes; no action until completion of 2013 tax year in spring 2014

5. T3 matching: CRA has made effort at determining why CRA cannot match T3s with reported income (with IFIC, CLHIA and CETFA).

IIAC participated in CRA-IFIC-CETFA meeting in January 2013; IFIC taking the lead; CLHIA advised that another matching exercise is to take place in 2013, with a change to the forms to capture income not currently required to be reported because it is in deferred plans; CRA T3 matching deferred from 2013; as the matching exercise is to be carried forward to 2014, CETFA is seeking to work with the IIAC to identify a T3 matching solution for ETFs and IIAC is seeking members for this meeting

CONFIDENTIAL – DO NOT CIRCULATE - 3 -

TAXATION REPORTING COMMITTEE ISSUE STATUS

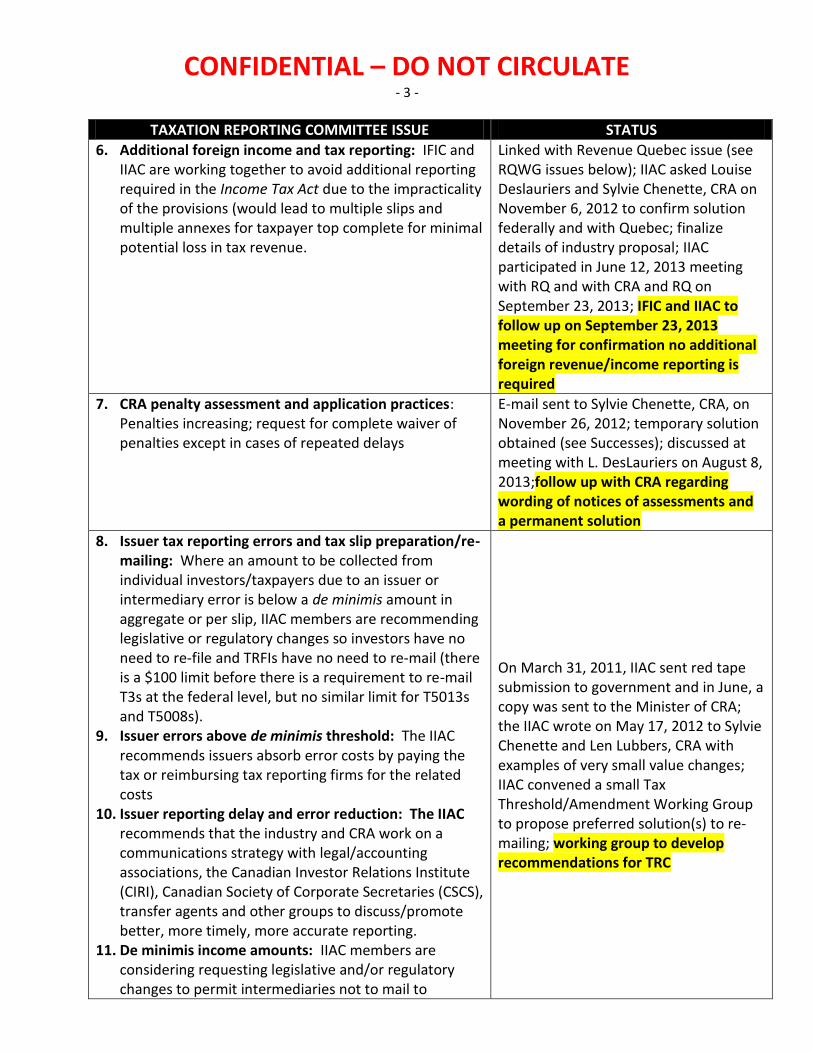

6. Additional foreign income and tax reporting: IFIC and IIAC are working together to avoid additional reporting required in the Income Tax Act due to the impracticality of the provisions (would lead to multiple slips and multiple annexes for taxpayer top complete for minimal potential loss in tax revenue.

Linked with Revenue Quebec issue (see RQWG issues below); IIAC asked Louise Deslauriers and Sylvie Chenette, CRA on November 6, 2012 to confirm solution federally and with Quebec; finalize details of industry proposal; IIAC participated in June 12, 2013 meeting with RQ and with CRA and RQ on September 23, 2013; IFIC and IIAC to follow up on September 23, 2013 meeting for confirmation no additional foreign revenue/income reporting is required

7. CRA penalty assessment and application practices: Penalties increasing; request for complete waiver of penalties except in cases of repeated delays

E-mail sent to Sylvie Chenette, CRA, on November 26, 2012; temporary solution obtained (see Successes); discussed at meeting with L. DesLauriers on August 8, 2013;follow up with CRA regarding wording of notices of assessments and a permanent solution

8. Issuer tax reporting errors and tax slip preparation/re-mailing: Where an amount to be collected from individual investors/taxpayers due to an issuer or intermediary error is below a de minimis amount in aggregate or per slip, IIAC members are recommending legislative or regulatory changes so investors have no need to re-file and TRFIs have no need to re-mail (there is a $100 limit before there is a requirement to re-mail T3s at the federal level, but no similar limit for T5013s and T5008s).

9. Issuer errors above de minimis threshold: The IIAC recommends issuers absorb error costs by paying the tax or reimbursing tax reporting firms for the related costs

10. Issuer reporting delay and error reduction: The IIAC recommends that the industry and CRA work on a communications strategy with legal/accounting associations, the Canadian Investor Relations Institute (CIRI), Canadian Society of Corporate Secretaries (CSCS), transfer agents and other groups to discuss/promote better, more timely, more accurate reporting.

11. De minimis income amounts: IIAC members are considering requesting legislative and/or regulatory changes to permit intermediaries not to mail to

On March 31, 2011, IIAC sent red tape submission to government and in June, a copy was sent to the Minister of CRA; the IIAC wrote on May 17, 2012 to Sylvie Chenette and Len Lubbers, CRA with examples of very small value changes; IIAC convened a small Tax Threshold/Amendment Working Group to propose preferred solution(s) to re-mailing; working group to develop recommendations for TRC

CONFIDENTIAL – DO NOT CIRCULATE - 4 -

TAXATION REPORTING COMMITTEE ISSUE STATUS

taxpayers or file slips with CRA recording tax amounts of less than $50 (or some other amount – $100) to avoid mismatches, taxpayer service issues and costs not warranted by revenue

12. Efficient access to withholding tax rate changes: From an efficiency perspective, the IIAC believes that treaty rates per income type per country should be made available by the CRA in an electronic file to all parties that request it, with the file being resent to them as withholding rates are amended. CRA staff said it wants payers to read the actual treaties which are very long, written in a legal rather than plain-language style and is only a fraction of the material required by tax-reporting departments. The CRA, by providing the information in a file format or on a website, would reduce errors and costs for many small (and larger) payers. There are many examples of federal government departments providing simplified compliance guides for businesses.

IIAC requested Janet Schermann, CRA for easier access to foreign withholding rates; request denied in January 2012; raise issue with Mickey Sarazin, DG at CRA (see 2.)

13. Improve withholding remittance process: The IIAC recommends that TRFIs be provided with the option to remit withholding tax on registered plan withdrawals by the middle of January on the previous year’s transactions and remittances, instead of on the third business day of the New Year

Included in March 31, 2011 Red Tape letter to government and June copy sent to Minister of CRA; letter sent to the CRA on June 6, 2013; IIAC received contact on June 17; IIAC to follow up

14. NR301 form updates: Building on the relationship established in 2011 and 2012, the CRA requested input on changes

IIAC provided recommended updates to September 2; IIAC to follow up to confirm changes are made

15. Foreign holdings held in Canadian institutions subject to T1135 foreign income verification reporting: The IIAC recommended the CRA exempt taxpayers from reporting as Canadian financial institutions already disclose foreign income related to financial foreign shareholdings on tax receipts (e.g., T5s), making the T1135 reporting of these assets redundant

Request sent to Sylvie Chenette, CRA on November 25, 2012; received reply that this is expected to be enacted, but for future years; confirmed in 2013 Budget; IIAC confirmed with new CRA rep that this was on schedule for this year; IIAC learned new form may lead to more client complaints and spoke with CRA in late July with comments/questions; he advised that consultations would be undertaken and asked the IIAC to request to participate; on August 28, 2013, the IIAC e-mailed requesting to participate in consultations and providing initial suggestions; IIAC will follow up with the CRA

CONFIDENTIAL – DO NOT CIRCULATE - 5 -

REGISTERED PLANS COMMITTEE

REGISTERED PLANS COMMITTEE ISSUE STATUS

16. TFSA being subject to tax: CRA is auditing and assessing high value TFSAs without addressing issues raised regarding clarity.

Letters sent to CRA on May 7 and May 23, 2013 expressing concern with lack of communication and need for answers, especially clarification regarding what is in the business of trading; IIAC wrote July 18, 2013 requesting Finance to remove substantive risk shift to trustees (and hence by contract to dealers) from registered plans except where there is gross negligence or complicity; IIAC has been following up on a bi-weekly basis follow-up with CRA and Finance, respectively, on outstanding letters

17. De-registering TFSAs due to unmatched TFSA information: The CRA advised the CRA unmatched TFSAs should be deregistered and that tax slips should be issued for the income earned, but was not prepared to advise these TFSA holders of this. Tax reporting firms would have to manage manually the process of changing from registered to non-registered accounts, including producing and mailing tax slips for income for two (three?) years. Specific requests are: a. That member firms that file slips for previous years

are not assessed penalties and interests for late filings – while members can seek administrative relief at http://www.cra-arc.gc.ca/gncy/cmplntsdspts/txpyrrlf-eng.html, the IIAC has requested blanket relief rather than having a requirement for each member firm individually to request relief.

b. That member firms may file regular tax reporting slips for any non-registered TFSAs with a balance as opposed to trust tax returns for accounts that are being closed as they were never properly registered.

c. That the CRA consider a de minimis amount of income that needs to be reported to clients when an unregistered TFSA account is closed.

Individual meetings held; call-in number obtained to expedite resolution; Bruce Gilmour asked on December 6 if the CRA sent the letters, has received all the responses expected and agrees the industry should start deregistering/reporting income; letters received in January 2013 asking Members to reconcile or deregister; meeting held in late March; series of calls placed and e-mail sent; on May 29, CRA said they have got all necessary groups at the table and are gathering data/analysis; promised June meeting deferred until advised in late August a further effort to help members reconcile will take place in the fall; continue following up biweekly

18. RRSP holdings on certain designated stock exchanges: Securities on Alpha and TSX ATS should qualify for RRSPs; the IIAC was advised that this is not permitted as these are hard to value.

IIAC wrote Finance Canada on May 24, 2012; periodically IIAC checks up with Brian Ernewein, Finance; on July 12, 2013, IIAC contacted TSX re NEX,

CONFIDENTIAL – DO NOT CIRCULATE - 6 -

REGISTERED PLANS COMMITTEE ISSUE STATUS

Aequitas and Portfolio Management Association of Canada (PMAC, which is seeking designation on foreign exchanges); learned that Finance does not want to designate exchanges that are too new, without liquidity; IIAC to work with PMAC, exchanges to determine opportunities to work together, and with the IIAC’s Hard-to-Value Securities and Market Value Working Groups

19. Hard-to-value securities: The IIAC is seeking to identify industry-adopted and ideally CRA-supported ways to address problems re hard-to-value securities due to cease-trade orders, private placements, and transfers of registered plans between firms where the value may be in question. Some standards would lead to a more level playing field within the industry and potentially reduce the possibility of investor and member pullback from private share investment

IIAC surveyed member practices and if an agreement can be reached members will discuss approach CRA and/or Finance for administrative guidance/ regulation for fairer, more consistent treatment of clients and minimize member risk; combine work with the Market Value Working Group, which met for the first time on July 10, 2013, and Registered Plans Best Practices Working Group (see below)

20. RRSP, RRIF prohibited investments/TFSA anti-avoidance changes extended to RRSPs/RRIFs: The 2011 Budget brought in anti-avoidance approaches for TFSAs to the RRSP product in the areas of advantage rules, prohibited investment rules and non-qualified investment rules which remain problematic – regulations and administrative guidance may be helpful

IIAC to ask if RRSP to RRIF conversions have disposition tax consequences

IIAC to ask CRA re length of time before an item sold into the market from an RRSP it can be bought back into the TFSA

New RPC subcommittee Registered Plans Best Practices Working Group met in the last week of July 2013; its first task is understanding and creating a decision tree for complex new amendments found in December 2012 draft tax rules; IIAC to work with RPCBPWG task force to help co-ordinate workable decision tree for common approach on prohibited and qualified investments

21. Ontario hardship unlocking: Ontario government transferred responsibility for adjudicating unlocking to the industry, increasing workload, cost and risk

IIAC wrote on January 16, 2013 opposing the measure and requesting protection from liability; the measure proceeded and IIAC participated in meetings with FSCO in the summer and submitted recommendations for Qs&As, etc. in August 2013; new forms received and circulated; IIAC to follow up with FSCO to obtain dealer-favourable documentation in advance of January 1, 2014 implementation date

CONFIDENTIAL – DO NOT CIRCULATE - 7 -

REGISTERED PLANS COMMITTEE ISSUE STATUS

22. Ontario Unclaimed Intangible Property Legislation: The Ontario government continues to wish to introduce unclaimed intangible property legislation, which would include amounts in securities accounts. There are many operational issues related to this, but the most client-facing one is the impact of removing/transferring assets from registered plans to government entities without disadvantaging clients.

IIAC responded to the Ontario consultations on October 22, 2012 recommending financial institution specific consultations and extensive discussion of the tax issue; IIAC attended follow-up consultations with little achieved regarding accounts; IIAC to monitor.

CONFIDENTIAL – DO NOT CIRCULATE - 8 -

REVENUE QUEBEC WORKING GROUP

REVENU QUÉBEC WORKING GROUP ISSUE STATUS

23. Foreign income and tax reporting on RL-16: Identify workable alternatives to requirement to send

Achieved deferral by a year; letters sent jointly by IFIC and IIAC on June 21, 2012 and IFIC, IIAC and CLHIA on November 2, 2012; RQWG will need to undertake further work; IFIC followed up with MRQ and were told no answers to date; see TRC above; work with CRA, RQ and IFIC to avoid need to break out detail or confirm workable approach ensure timely preparation for 2013 reporting

24. Bi-annual big-picture meetings: IIAC to identify and put forward RQ reporting agenda items with details, as well as with respect to IQEE, unclaimed intangible property and other programs managed by RQ

RQ offered higher-level meeting with IIAC (and IFIC); IIAC to develop a list of proposed agenda items

25. Annual tax reporting requirements: a. Release Timeline for Issuing Specifications: Early fall

deadline is too limited b. Testing: Certification requirements; tags to identify

software and make sure it is certified required in both testing (three files: Original, Amended and Cancelled) and production environment; does this mean two sets of XML (one for production and one for testing?)

Letter sent November 12, 2012; response received November 26, 2012 that seems to address a good number of problems; RQWG asked to comment on floating box intentions/expectations; meeting held December 7, 2012; what appears to be industry standard circulated to TRC on December 7, 2012; IFIC followed up with RQ and were told no answers to date; IIAC and IFIC met with RQ on range of technical issues on August 22, 2013 agreed to at least two bigger-pictures planning meetings a year; complete action arising from August 22 joint meeting

26. RL-15: Update and streamline per RQ request Industry to provide guidance after discussion

27. IIEQ/QESI: Encourage RQ to streamline in line with HRSDC RESP model

Working with IFIC; sent July to RQ re QESI; monitor for response/meeting with RQ with IFIC re QESI

CONFIDENTIAL – DO NOT CIRCULATE - 9 -

OTHER ISSUES UNDER WAY WITH CRA, FINANCE, PROVINCES

Other Tax ISSUE Status

28. Non-Taxation of Accrued Gains on Broker Warrants: Federal government changed rules requiring warrants to be taxed on an accrual basis, which is impractical for the little known broker warrants, and which has limited their use

IIAC sent letters dated July 10, 2008i, February 16, 2011, May 2, 2011 (contains confidential information; available to you on request) and July 7, 2011, April 23, 2012); IIAC to follow with Brian Ernewein up on status of letter

29. Requirements to Pay: CRA issues Requirements to Pay (“RTPs”) requiring RTP recipients to immediately pay the Receiver General the tax liability incurred by the client. The language of the RTP is confusing for anyone not in the tax field and the threat that “failure to pay the receiver general the amounts required renders the person required to remit taxes on another’s behalf personally liable to pay those amounts to her majesty” does not encourage delay. The RTP does not say to freeze assets or that there could be a retraction.

Letter sent August 24, 2012; CRA refused to provide clear public information; IIAC escalated to Minister’s office to Connor Robinson who “encouraged” CRA to send draft document to TRFIs; IIAC provided comments on May 17, 2013 and receipt acknowledged; IIAC to follow up in 2014 for final Guide with information

30. Withholding Tax Treaty with Hong Kong: IIAC supported IIAC sent letter to federal Finance Minister (Feb. 2, 2011), B.C. Finance Minister (Feb. 14, 2013), and Finance department (May 5, 2011); intention to sign treaty announced; awaiting passage through Parliament; monitor only

31. GST Policy Review: Pressed by the Investment Funds Institute of Canada and certain other associations, the federal government has begun looking at potential GST reform as it affects financial services. The IIAC suggested no changes be made except to clarify requirements and reduce the administrative burden.

IIAC sent letter to Rainer Nowak on April 2, 2013; monitor only

32. GST on Finders Fees: Following government legislative changes to clarify the GST treatment of a number of services, there appeared a risk that the treatment of finders’ fees associated with non-brokered private placements could be considered taxable, contrary to practice.

The IIAC, contracting Deloitte for a group of members, submitted a request for a ruling (Nov. 4, 2011); the group met with the CRA and submitted a follow-up letter on December 13, 2012; contacting CRA quarterly and on September 26, Luba Baran said hooped to have reply by year-end; follow up in October

33. GST on Trade Execution (Clearing) Fees: IIAC was asked by a member to request that the TMX exempt trade execution fees as had Alpha and on other ATS. Alpha had

IIAC approached TSX on September 6, 2011; in touch quarterly with TMX until a CRA decision is reached;

CONFIDENTIAL – DO NOT CIRCULATE - 10 -

Other Tax ISSUE Status

received a favourable ruling; TMX is still waiting for confirmation although is not charging HST.

follow up with the TMX in October, 2013

34. Pooled Registered Pension Plans (PRPPs): PRPPs, which will compete with RRSPs and DC plans, raise a series of policy issues (level playing field as payroll taxes apply to GRRSPs). B.C., Alberta and Saskatchewan have brought in enabling legislation and Ontario is considering doing the same. Also, Quebec has issued legislation with respect to régimes volontaires d'épargne-retraite (RVER) – PRPP equivalents in Quebec, re-introduced in 2103 in more or less the same form in the new year under Quebec’s new government.

Multiple submissions sent focussing on allowing advise-based option and removing payroll taxes from employer and employee contributions to GRRSPs; IIAC to draft submission to provinces regarding PRPP regulations, legislation

35. Montreal Exchange Values: Audit issue for a few Toronto-based firms only as the CRA in Vancouver and Montreal did not raise this

Currently a Member issue with a few Toronto-based Members; issue is with members at present and may become a matter to be pursued jointly; IIAC to remain abreast with interested parties to see whether joint work would be beneficial

36. CDS Share Values: IIAC received requests for input or possible shared action

Poll Members to determine member positions

37. Ontario Unclaimed Intangible Property Act: After withdrawing the 20-year-old passed but unenacted legislation, the Ontario Office of the Attorney General sought input on a range of issues regarding the transfer of dormant account and other “unclaimed” or forgotten amounts. Should this extend to amounts in brokerage accounts, registered or not, the industry will be subject to additional operational requirements, as well as tax and other risks depending on the tax status of the accounts

IIAC to monitor developments

CONFIDENTIAL – DO NOT CIRCULATE - 11 -

COMPLETED – 2013 ISSUE STATUS

1. Non-qualified reporting in XML (Part 1): Recommend 2012 reporting again be by CD-ROM and due May 31

E-mail sent to CRA on December 5, 2012; CONFIRMED PREVIOUS YEAR’S PROCESS ACCEPTABLE IN FEBRUARY 11, 2013, avoiding rush XML implementation

2. Non-qualified reporting in XML (Part 2): 2014 reporting

RECEIVED XML EARLY IN AUGUST 2013 AND CONFIRMED LATER (MAY 30) FILING DATE, avoiding rush XML implementation and providing more flexibility in filing date

3. Streamline NR7-R forms: Allow one form to be used for claims for all payments related to a single client

Wrote to Mike St. Julien, CRA, on August 23, 2012; rejection response received October 31, 2012 showed a misunderstanding; called and CRA agreed to review decision; CONFIRMED BULK NR-7R RECLAIM PROCESS ACCEPTABLE IN JANUARY 2013; IIAC, L. Dion (NBCN) and M. Barbara (BMONB) developed instructions for consistent use

4. Non-qualified reporting in XML (Part 2): 2014 reporting

RECEIVED XML EARLY IN AUGUST 2013 AND CONFIRMED LATER (MAY 30) FILING DATE, avoiding rush XML implementation and providing more flexibility in filing date

5. CRA penalty assessment and application practices (Part 1): Penalties increasing; request for complete waiver of penalties except in cases of repeated delays

E-mail sent to Sylvie Chenette, CRA, on November 26, 2012; following interactions with L. DesLauriers, including August 8, 2013 meeting, SUCCESSFULLY OBTAINED CRA CUT-OFF OF LATE FILING PENALTIES FOR T3S, T5S AND T5013S AND STREAMLINED PROCESS FOR REFUNDS

6. T5013SUM, FIN and Schedule 50s (Part 1): Confirm that an alternative for the T5013 summaries can be considered for reconciliation; IIAC teleconference to follow up to request confirmation in writing from Rob Bledig regarding no need longer a need for financial return and Schedule 50, as had been requested.

CONFIRMED PERMANENT ABSOLUTIONN FROM FILING T5013 SUM, FIN AND SCH50 WITH XML IMPLEMENTATION (XML implementation causing new issues; see above)

7. Requirement to Pay (Part I): CRA issues Requirements to Pay (“RTPs”) requiring RTP recipients to immediately pay the Receiver General the tax liability incurred by the client. The language of the

Letter sent August 24, 2012; response awaited from [email protected], Ministerial Correspondence and Service Complaints Officer/ Taxpayer

CONFIDENTIAL – DO NOT CIRCULATE - 12 -

RTP is confusing for anyone not in the tax field and the threat that “failure to pay the receiver general the amounts required renders the person required to remit taxes on another’s behalf personally liable to pay those amounts to her majesty” does not encourage delay. The RTP does not say to freeze assets or that there could be a retraction.

Services and Debt Management Branch; following a an e-mail to the Minister’s policy advisor, IIAC received a draft RTP guide for member comment; comments sent May 20, 2013; GUIDE PLUS INDUSTRY COMMENTS LEAVES INDUSTRY CONSIDERABLY BETTER PREPARED TO AVOID LOSS; response to the effect that some items will be dealt with received; IIAC to follow up in 2014

CONFIDENTIAL – DO NOT CIRCULATE - 13 -

ARE THESE STILL TAX REPORTING COMMITTEE (TRC) ISSUES?

ISSUE STATUS

8. Reporting of income from foreign partnerships: A CRA interpretation notice has indicated reporting foreign income reported on T5s may not appropriate

Given that this has been the industry practice, the item will be tabled for discussions with CRA; timing to be discussed

9. Improve T5013 and T3 filing process (Relevé 15/16): Recommend private income and capital trust/limited partnership issuers be mandated to file tax factors related to income from the instruments as are public issuers of such investments on CDS website. As a minimum, desirable re income and capital trusts/limited partnerships in which public income and capital trusts and LPs invest. This requires (1) a legislative change or (2) for public issuers to include a requirement that if investing in the securities of private issuers, the private issuers must file factors on the CDS website by the end of the third week in February.

Is this advisable? If so, what is the best way for the industry to proceed: legislative change, contract, or ask issuers for views? To be discussed by TPC (as a quid pro quo, IIAC had recommended elimination of any remaining requirement of issuers to file with CRA; it is not clear this was ever done)

10. Trust identification numbers (TINs) before tax season: Recommend trusts be required to get TINs before tax filing and that this be made easily available to tax reporting firms through the CRA to avoid duplicates and errors

In March 31, 2011 Red Tape letter to government and June copy sent to Minister of CRA; draft and send separate letter or link with 2. above; apparently resolved?

11. Improve non-resident tax process: Recommend CRA clarify that issuer is responsible for non-resident withholding tax on notional/in-kind trust income distributions made to non-resident unitholders (notional income distribution paid to unitholders by the issuance of additional trust units, meaning outstanding trust units will be consolidated with additional trust units so each holder will have same number of units as before the distribution). Issuers typically do not know all the details until the final audit of the year-end financials is done early in the following year after the remittance due date and leading to penalties and interest, causing accounting issues for financial institutions as payments made in one year while withholding amount is not determined until the following year

This/these issue(s) arose and have not been widely discussed; Note: Are there two issues? (1) that CRA communicate responsibility clearly or is a legislative change required that the issuer must withhold? collect/remit? report?, and (2) how to deal with late receipt of data?

CONFIDENTIAL – DO NOT CIRCULATE - 14 -

ARE THESE STILL REGISTERED PLAN COMMITTEE (RPC) ISSUES?

UNDER WAY REGISTERED PLANS COMMITTEE STATUS

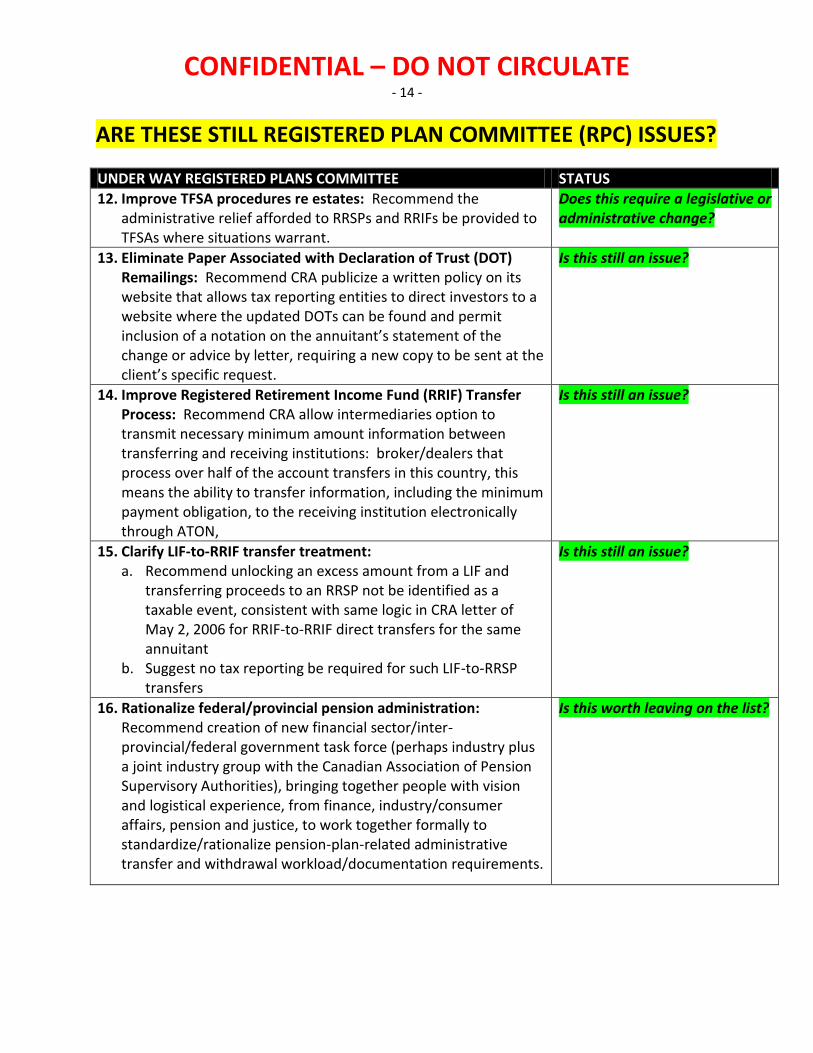

12. Improve TFSA procedures re estates: Recommend the administrative relief afforded to RRSPs and RRIFs be provided to TFSAs where situations warrant.

Does this require a legislative or administrative change?

13. Eliminate Paper Associated with Declaration of Trust (DOT) Remailings: Recommend CRA publicize a written policy on its website that allows tax reporting entities to direct investors to a website where the updated DOTs can be found and permit inclusion of a notation on the annuitant’s statement of the change or advice by letter, requiring a new copy to be sent at the client’s specific request.

Is this still an issue?

14. Improve Registered Retirement Income Fund (RRIF) Transfer Process: Recommend CRA allow intermediaries option to transmit necessary minimum amount information between transferring and receiving institutions: broker/dealers that process over half of the account transfers in this country, this means the ability to transfer information, including the minimum payment obligation, to the receiving institution electronically through ATON,

Is this still an issue?

15. Clarify LIF-to-RRIF transfer treatment: a. Recommend unlocking an excess amount from a LIF and

transferring proceeds to an RRSP not be identified as a taxable event, consistent with same logic in CRA letter of May 2, 2006 for RRIF-to-RRIF direct transfers for the same annuitant

b. Suggest no tax reporting be required for such LIF-to-RRSP transfers

Is this still an issue?

16. Rationalize federal/provincial pension administration: Recommend creation of new financial sector/inter-provincial/federal government task force (perhaps industry plus a joint industry group with the Canadian Association of Pension Supervisory Authorities), bringing together people with vision and logistical experience, from finance, industry/consumer affairs, pension and justice, to work together formally to standardize/rationalize pension-plan-related administrative transfer and withdrawal workload/documentation requirements.

Is this worth leaving on the list?