Embed Size (px)

Citation preview

CONSOLIDATEDFINANCIAL

STATEMENTS

inside report 09-part1 12/21/10 8:01 PM Page 27

28

SOCIÉTÉ GÉNÉRALE DE BANQUE AU LIBAN S.A.LCONSOLIDATED FINANCIAL STATEMENTS 31 DECEMBER, 2009

CONSOLIDATEDFINANCIALSTATEMENTS

inside report 09-part1 12/21/10 8:01 PM Page 28

SOCIÉTÉ GÉNÉRALE DE BANQUE AU LIBAN | ANNUAL REPORT 2009 29

INDEPENDENT AUDITORS’ REPORT TO THE SHAREHOLDERS OF SOCIETE GENERALE DE BANQUE AU LIBAN SAL

We have audited the accompanying consolidated financial statements of Société Générale de Banque au Liban SAL (theBank) and its subsidiaries (the Group), which comprise the consolidated statement of financial position as at 31 December2009 and the consolidated income statement, consolidated statement of comprehensive income, consolidated statementof changes in equity and consolidated statement of cash flows for the year then ended, and a summary of significantaccounting policies and other explanatory notes.

Management’s Responsibility for the Financial StatementsManagement is responsible for the preparation and fair presentation of these financial statements in accordance withInternational Financial Reporting Standards. This responsibility includes: designing, implementing and maintaining internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error; selecting and applying appropriate accounting policies; and makingaccounting estimates that are reasonable in the circumstances.

Auditors’ ResponsibilityOur responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit inaccordance with International Standards on Auditing. Those standards require that we comply with ethical requirementsand plan and perform the audit to obtain reasonable assurance whether the financial statements are free from materialmisstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financialstatements. The procedures selected depend on the auditors’ judgment, including the assessment of the risks of materi-al misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditorconsiders internal control relevant to the entity’s preparation and fair presentation of the financial statements in order todesign audit procedures that are appropriate for the circumstances, but not for the purpose of expressing an opinion onthe effectiveness of the entity’s internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluating the overallpresentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

OpinionIn our opinion, the consolidated financial statements present fairly, in all material respects, the financial position of theGroup as of 31 December 2009 and its financial performance and its cash flows for the year then ended in accordance withInternational Financial Reporting Standards.

12 April 2010

Except as to Note 39d which is as of 21 July 2010 (date of audit procedures related to the shareholders’ resolutiondescribed in Note 39d).Beirut, Lebanon

inside report 09-part1 12/21/10 8:01 PM Page 29

30

CONSOLIDATEDFINANCIALSTATEMENTS

CONSOLIDATED INCOME STATEMENTYear ended 31 December 2009

2009Notes

2008[In LL million]

Interest and similar income 4 323,747 271,449

Interest and similar expense 5 (171,669) (144,561)

NET INTEREST INCOME 152,078 126,888

Fee and commission income 64,895 64,183

Fee and commission expense (21,589) (18,916)

NET FEE AND COMMISSION INCOME 6 43,306 45,267

Net trading income 7 7,113 5,824

Net gain (loss) on financial assets designated at fair value

through profit or loss 2,011 (2,248)

Net gain on financial investments 8 16,212 2,528

Other operating income 9 18,185 14,708

TOTAL OPERATING INCOME 238,905 192,967

Net write-back of credit losses 10 2,694 2,360

Write-back of impairment (impairment losses) on financial investments 951 (1,282)

NET OPERATING INCOME 242,550 194,045

Personnel expenses 11 (65,303) (61,724)

Depreciation of property and equipment 25 (4,847) (4,152)

Amortization of intangible assets 26 (341) (343)

Other operating expenses 12 (46,289) (47,953)

TOTAL OPERATING EXPENSES (116,780) (114,172)

OPERATING PROFIT 125,770 79,873

Share of profit from non-consolidated subsidiaries 24 904 -

Net profit from sale or disposal of other assets 52 51

PROFIT BEFORE TAX 126,726 79,924

Income tax expense 34 (20,413) (14,219)

PROFIT FOR THE YEAR 106,313 65,705

Attributable to:

Equity holders of the parent 100,013 58,127

Non-controlling interests 6,300 7,578

106,313 65,705

The attached notes 1 to 56 form part of these consolidated financial statements. T

inside report 09-part1 12/21/10 8:01 PM Page 30

SOCIÉTÉ GÉNÉRALE DE BANQUE AU LIBAN | ANNUAL REPORT 2009 31

CONSOLIDATEDFINANCIAL

STATEMENTS

2009Notes

2008

CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME Year ended 31 December 2009[In LL million]

PROFIT FOR THE YEAR 106,313 65,705

Other comprehensive income

Net gain on available-for-sale financial assets 28,770 9,446

Net movement in foreign currency reserve 38 (250)

Income tax relating to components of other comprehensive income (5,489) (1,060)

Other comprehensive income for the year, net of tax 23,319 8,136

TOTAL COMPREHENSIVE INCOME FOR THE YEAR, NET OF TAX 129,632 73,841

Attributable to:

Equity holders of the parent 122,925 66,499

Non-controlling interests 6,707 7,342

129,632 73,841

The attached notes 1 to 56 form part of these consolidated financial statements.

inside report 09-part1 12/21/10 8:01 PM Page 31

32

CONSOLIDATEDFINANCIALSTATEMENTS

CONSOLIDATED STATEMENT OF FINANCIAL POSITIONAt 31 December 2009

The attached notes 1 to 56 form part of these consolidated financial statements. T

[In LL million]

ASSETSCash and balances with the Central Banks 13 879,086 640,776Deposits with banks and financial institutions 14 203,718 180,363Amounts due from Head Office, branches and affiliates 15 806,604 458,971Derivative financial instruments 16 6,937 300Financial assets held-for-trading 33 927Financial assets designated at fair value through profit or loss 17 6,967 4,401Loans and advances to customers, net 18 2,029,016 1,401,753Loans and advances to related parties, net 19 63,211 55,941Debtors by acceptances 20 65,929 74,642Financial investments – available-for-sale 21 1,029,885 390,347Financial assets classified as loans and receivables 22 1,279,410 1,178,352Financial investments – held-to-maturity 23 500,372 383,824Investments in non-consolidated subsidiaries 24 2,510 1,606Property and equipment 25 62,231 53,200Intangible assets 26 2,561 2,106Non-current assets held for sale 27 122,328 143,567Deferred tax assets 34 5,046 2,208Other assets 28 52,607 72,960Goodwill 29 15,854 2,706Total assets 7,134,305 5,048,950

LIABILITIES AND EQUITYLIABILITIESDue to Central Banks 30 305,110 305,101Due to banks and financial institutions 31 167,658 127,684Amounts due to Head Office, branches and affiliates 32 316,386 322Derivative financial instruments 16 299 783Customers' deposits 33 5,515,275 3,903,315Related parties’ deposits 7,808 11,568Engagements by acceptances 20 65,929 74,642Current tax liabilities 34 12,310 9,779Deferred tax liabilities 34 5,489 1,060Other liabilities 35 127,940 118,726Provision for risks and charges 36 11,883 12,443Employees’ end of service benefits 37 15,394 12,744Total liabilities 6,551,481 4,578,167

EQUITYShare capital – common shares 38a 10,620 10,620Share capital – preferred shares 38b 1,912 1,912Share premium – preferred shares 38b 133,121 133,121Cash contribution by shareholders 38c 106,746 106,746Reserves related to share capital 39 92,038 75,016Revaluation reserve of property 41 3,934 3,934Available-for-sale reserve 42 30,258 7,232Foreign currency reserve (49) (28)Reserve for non-current assets held for sale 40 10,628 5,261Profit for the year 100,013 58,127Retained earnings 17,245 10,624

506,466 412,565Non-controlling interests 76,358 58,218Total equity 582,824 470,783Total liabilities and equity 7,134,305 5,048,950

The consolidated financial statements were authorized for issue on behalf of the Board of Directors on 13 February 2010 by:

Antoun Sehnaoui Georges SaghbiniChairman Deputy General Manager

2009Notes

2008

inside report 09-part1 12/21/10 8:01 PM Page 32

SOCIÉTÉ GÉNÉRALE DE BANQUE AU LIBAN | ANNUAL REPORT 2009 33

CONSOLIDATEDFINANCIAL

STATEMENTS

CONSOLIDATED STATEMENT OF FINANCIAL POSITIONAt 31 December 2009

The attached notes 1 to 56 form part of these consolidated financial statements.

[In LL million]

Off-balance sheet

Financing commitments

- Commitments issued to customers 49 29,018 872

- Commitments issued to financial institutions 49 105,208 119,272

- Undrawn commitments to lend 49 367,683 342,616

Guarantees commitments

- Guarantees issued to financial institutions 49 39,138 21,566

- Guarantees issued to customers 49 178,923 135,426

- Guarantees received from financial institutions 160,418 14,777

Foreign currency operations

- Foreign currencies to receive 16 144,645 36,906

- Foreign currencies to deliver 138,007 37,389

Commitments on term financial instruments 16 9,849 17,254

Fiduciary deposits 47 203,854 156,066

Financial assets under management – non discretionary 48 791,924 870,318

Impaired loans fully provided for transferred to off-balance sheet 46 180,975 125,540

2009Notes

2008

inside report 09-part1 12/21/10 8:01 PM Page 33

34The attached notes 1 to 56 form part of these consolidated financial statements.

CONSOLIDATEDFINANCIALSTATEMENTS

CONSOLIDATED STATEMENT OF CHANGES IN EQUITYYear ended 31 December 2009

Sharecapital – common

shares

Attributable to equity holders of the parent

Sharecapital –

preferredshares

Sharepremium –preferred

shares

Cashcontribution

byshare-

holders

[In LL million]

Balance at 1 January 2008 10,620 - - 106,746 67,944 3,934 (1,265) 97 - 16,486 6,471 211,033 36,021 247,054Profit for the year 2008 - - - - - - - - - 58,127 - 58,127 7,578 65,705Other comprehensive income - - - - - - 8,497 (125) - - - 8,372 (236) 8,136

Total comprehensive income - - - - - - 8,497 (125) - 58,127 - 66,499 7,342 73,841Transfer to retained earnings - - - - - - - - - (16,486) 16,486 - - -Transfer to reserve for non-current assets held for sale - - - - - - - - 5,513 - (5,513) - - -Release of reserve upon sale of non-current assets held for sale (note 40) - - - - - - - - (252) - 252 - - -Transfer to reserves related to share capital (note 39) - - - - 7,072 - - - - - (7,072) - - -Issuance of preferred shares (note 38) - 1,912 133,121 - - - - - - - - 135,033 - 135,033Net increase in non-controlling interests’ share due to increase inshare capital of SGBJ (note 3) - - - - - - - - - - - - 17,637 17,637Acquisition of non-controlling interests in Sogecap SAL (note 3) - - - - - - - - - - - - (2,782) (2,782)

Balance at 31 December 2008 10,620 1,912 133,121 106,746 75,016 3,934 7,232 (28) 5,261 58,127 10,624 412,565 58,218 470,783Profit for the year 2009 - - - - - - - - - 100,013 - 100,013 6,300 106,313Other comprehensive income - - - - - - 22,892 20 - - - 22,912 407 23,319

Total comprehensive income - - - - - - 22,892 20 - 100,013 - 122,925 6,707 129,632Transfer to retained earnings - - - - - - - - - (58,127) 58,127 - - -Transfer to reserve for non-current assets held for sale - - - - - - - - 6,830 - (6,830) - - -Release of reserve upon sale of non-current assets held for sale (note 40) - - - - - - - - (1,463) - 1,463 - - -Transfer to reserves related to share capital (note 39) - - - - 17,823 - - - - - (17,823) - - -Acquisition of non-controlling interests in SGBJ (note 3) - - - - - - - - - - - - (3,901) (3,901)Acquisition of non-controlling interests inSociété Générale Bank – Cyprus Ltd (note 3) - - - - - - - - - - - - 15,327 15,327Dividends paid to equity holders of the parent (note 43) - - - - - - - - - - (28,334) (28,334) - (28,334)Dividends paid to non-controlling interests - - - - - - - - - - - - (2) (2)Others - - - - (801) - 134 (41) - - 18 (690) 9 (681)Balance at 31 December 2009 10,620 1,912 133,121 106,746 92,038 3,934 30,258 (49) 10,628 100,013 17,245 506,466 76,358 582,824

inside report 09-part1 12/21/10 8:01 PM Page 34

SOCIÉTÉ GÉNÉRALE DE BANQUE AU LIBAN | ANNUAL REPORT 2009 35

CONSOLIDATEDFINANCIAL

STATEMENTS

CONSOLIDATED STATEMENT OF CHANGES IN EQUITYYear ended 31 December 2009

y holders of the parent

Reservesrelated to

sharecapital

Revaluationreserve ofproperty

Available-for-sale

reserve

Foreigncurrency reserve

Reservefor

non-currentassets

held forsale

Profitfor the

year

Retainedearnings

Total

Non-controlling

interests

Totalequity

6 67,944 3,934 (1,265) 97 - 16,486 6,471 211,033 36,021 247,054- - - - - - 58,127 - 58,127 7,578 65,705- - - 8,497 (125) - - - 8,372 (236) 8,136

- - - 8,497 (125) - 58,127 - 66,499 7,342 73,841- - - - - - (16,486) 16,486 - - -- - - - - 5,513 - (5,513) - - -

- - - - - (252) - 252 - - -- 7,072 - - - - - (7,072) - - -- - - - - - - - 135,033 - 135,033

- - - - - - - - - 17,637 17,637- - - - - - - - - (2,782) (2,782)

6 75,016 3,934 7,232 (28) 5,261 58,127 10,624 412,565 58,218 470,783- - - - - - 100,013 - 100,013 6,300 106,313- - - 22,892 20 - - - 22,912 407 23,319

- - - 22,892 20 - 100,013 - 122,925 6,707 129,632- - - - - - (58,127) 58,127 - - -- - - - - 6,830 - (6,830) - - -

- - - - - (1,463) - 1,463 - - -- 17,823 - - - - - (17,823) - - -- - - - - - - - - (3,901) (3,901)

- - - - - - - - - 15,327 15,327- - - - - - - (28,334) (28,334) - (28,334)- - - - - - - - - (2) (2)- (801) - 134 (41) - - 18 (690) 9 (681)

6 92,038 3,934 30,258 (49) 10,628 100,013 17,245 506,466 76,358 582,824

inside report 09-part1 12/21/10 8:01 PM Page 35

36The attached notes 1 to 56 form part of these consolidated financial statements.

CONSOLIDATEDFINANCIALSTATEMENTS

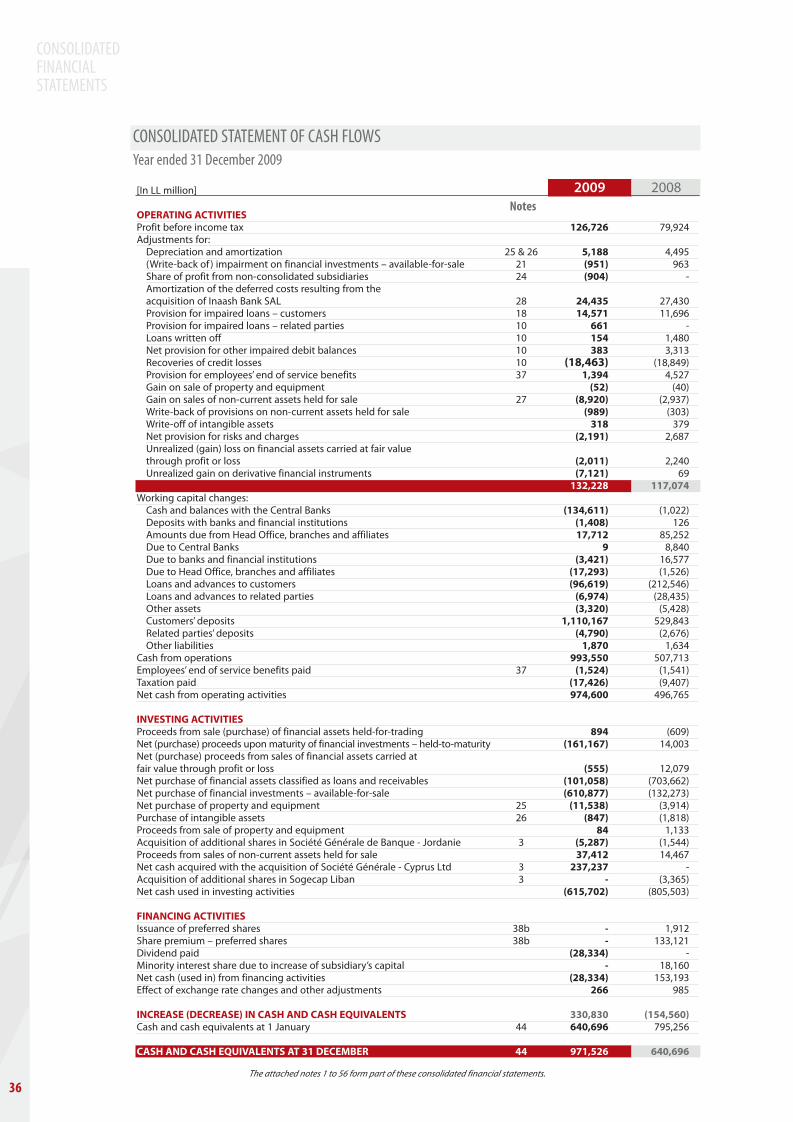

CONSOLIDATED STATEMENT OF CASH FLOWS Year ended 31 December 2009

[In LL million]

OPERATING ACTIVITIESProfit before income tax 126,726 79,924Adjustments for:

Depreciation and amortization 25 & 26 5,188 4,495(Write-back of ) impairment on financial investments – available-for-sale 21 (951) 963Share of profit from non-consolidated subsidiaries 24 (904) -Amortization of the deferred costs resulting from the acquisition of Inaash Bank SAL 28 24,435 27,430Provision for impaired loans – customers 18 14,571 11,696Provision for impaired loans – related parties 10 661 -Loans written off 10 154 1,480Net provision for other impaired debit balances 10 383 3,313Recoveries of credit losses 10 (18,463) (18,849)Provision for employees’ end of service benefits 37 1,394 4,527Gain on sale of property and equipment (52) (40)Gain on sales of non-current assets held for sale 27 (8,920) (2,937)Write-back of provisions on non-current assets held for sale (989) (303)Write-off of intangible assets 318 379Net provision for risks and charges (2,191) 2,687Unrealized (gain) loss on financial assets carried at fair valuethrough profit or loss (2,011) 2,240Unrealized gain on derivative financial instruments (7,121) 69

132,228 117,074Working capital changes:

Cash and balances with the Central Banks (134,611) (1,022)Deposits with banks and financial institutions (1,408) 126Amounts due from Head Office, branches and affiliates 17,712 85,252Due to Central Banks 9 8,840Due to banks and financial institutions (3,421) 16,577Due to Head Office, branches and affiliates (17,293) (1,526)Loans and advances to customers (96,619) (212,546)Loans and advances to related parties (6,974) (28,435)Other assets (3,320) (5,428)Customers’ deposits 1,110,167 529,843Related parties’ deposits (4,790) (2,676)Other liabilities 1,870 1,634

Cash from operations 993,550 507,713Employees’ end of service benefits paid 37 (1,524) (1,541)Taxation paid (17,426) (9,407)Net cash from operating activities 974,600 496,765

INVESTING ACTIVITIESProceeds from sale (purchase) of financial assets held-for-trading 894 (609)Net (purchase) proceeds upon maturity of financial investments – held-to-maturity (161,167) 14,003Net (purchase) proceeds from sales of financial assets carried atfair value through profit or loss (555) 12,079Net purchase of financial assets classified as loans and receivables (101,058) (703,662)Net purchase of financial investments – available-for-sale (610,877) (132,273)Net purchase of property and equipment 25 (11,538) (3,914)Purchase of intangible assets 26 (847) (1,818)Proceeds from sale of property and equipment 84 1,133Acquisition of additional shares in Société Générale de Banque - Jordanie 3 (5,287) (1,544)Proceeds from sales of non-current assets held for sale 37,412 14,467Net cash acquired with the acquisition of Société Générale - Cyprus Ltd 3 237,237 -Acquisition of additional shares in Sogecap Liban 3 - (3,365)Net cash used in investing activities (615,702) (805,503)

FINANCING ACTIVITIESIssuance of preferred shares 38b - 1,912Share premium – preferred shares 38b - 133,121Dividend paid (28,334) -Minority interest share due to increase of subsidiary’s capital - 18,160Net cash (used in) from financing activities (28,334) 153,193Effect of exchange rate changes and other adjustments 266 985

INCREASE (DECREASE) IN CASH AND CASH EQUIVALENTS 330,830 (154,560)Cash and cash equivalents at 1 January 44 640,696 795,256

CASH AND CASH EQUIVALENTS AT 31 DECEMBER 44 971,526 640,696

2009Notes

2008

inside report 09-part1 12/21/10 8:01 PM Page 36

SOCIÉTÉ GÉNÉRALE DE BANQUE AU LIBAN | ANNUAL REPORT 2009 37

NOTES TO THECONSOLIDATED

FINANCIALSTATEMENTS

1. ACTIVITIES

Société Générale de Banque au Liban SAL (the Bank) is a shareholding company registered in Beirut, Lebanon. It wasregistered in 1953 under no. 3696 at the Commercial Registry of Beirut and no. 19 on the list of banks published by theBank of Lebanon. The headquarters of the Bank are located at Saloumé Square, Sin El Fil, Lebanon.

The Bank is 19% owned by Société Générale SA (France), which is referred to in these financial statements as the “HeadOffice”.

The Bank, together with its subsidiaries (the Group), Société Générale Bank – Cyprus Ltd, Société Générale de Banque- Jordanie, Sogelease Liban SAL, Sogecap Liban SAL and Fidus SAL are involved in insurance, banking and financialservices activities (commercial, investment and private). The Bank is regulated by the Laws in Lebanon mainly the Codeof Commerce, the Money and Credit Act and the circulars issued by the Bank of Lebanon and the Banking ControlCommission.

The Bank provides a full range of banking activities through its headquarters and its branches in Lebanon.

2. ACCOUNTING POLICIES

2.1 Basis of preparationThe consolidated financial statements are prepared under the historical cost convention as modified for therestatement of certain tangible real estate properties in Lebanon according to the provisions of law No 282 dated 30December 1993, and for the measurement at fair value of derivatives and financial assets held-for-trading andavailable-for-sale financial instruments and fair value through profit or loss investments (related to unit-linkedcontracts) investments.

The consolidated financial statements are presented in million of Lebanese Lira (LL million), which is the functionalcurrency of the Bank, and all values are rounded to the nearest million (LL million) except when otherwise indicated.All other currencies are denominated in units.

Statement of complianceThe consolidated financial statements have been prepared in accordance with International Financial ReportingStandards (IFRS) as issued by the International Accounting Standards Board (IASB), and the regulations of the Bank ofLebanon and the Banking Control Commission.

The Group presents its consolidated statement of financial position broadly in order of liquidity. An analysis regardingrecovery or settlement within 12 months after the consolidated statement of financial position date (current) and morethan 12 months after the consolidated statement of financial position date (non-current) is presented in note 51.

Financial assets and financial liabilities are offset and the net amount reported in the consolidated statement offinancial position only when there is a legally enforceable right to offset the recognized amounts and there is anintention to settle on a net basis, or to realise the assets and settle the liability simultaneously. Income and expense willnot be offset in the income statement unless required or permitted by any accounting standard or interpretation, asspecifically disclosed in the accounting policies of the Bank.

Basis of consolidationThe consolidated financial statements comprise the financial statements of Société Générale de Banque au Liban SALand its controlled subsidiaries drawn up to 31 December each year. The financial statements of the subsidiaries areprepared for the same reporting year as the Bank, using consistent accounting policies.

All intra-group balances, transactions, income and expenses are eliminated in full.

Subsidiaries are fully consolidated from the date on which control is transferred to the Bank. Control is achieved wherethe Bank has the power to govern the financial and operating policies of an entity so as to obtain benefits from itsactivities. The results of subsidiaries acquired or disposed of during the year are included in the consolidated incomestatement from the date of acquisition or up to the date of disposal.

inside report 09-part1 12/21/10 8:01 PM Page 37

38

NOTES TO THECONSOLIDATEDFINANCIALSTATEMENTS

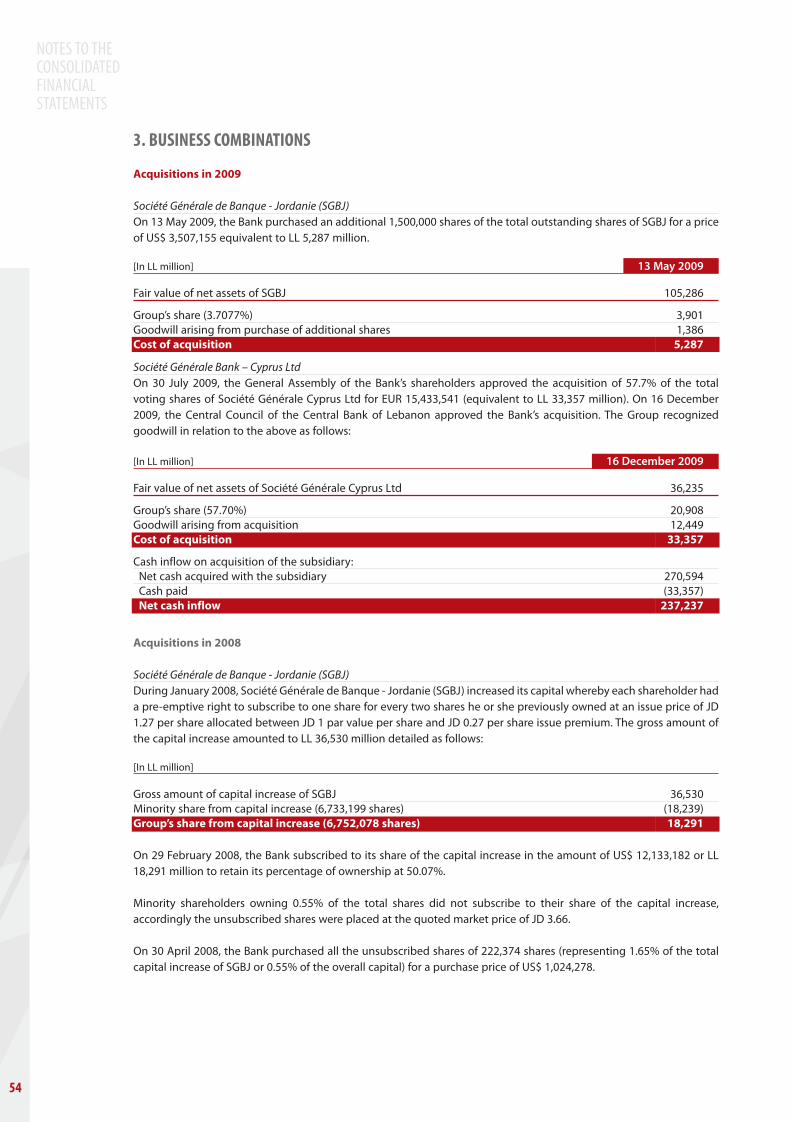

Société Générale Bank - Cyprus Ltd Cyprus Banking 57.70%

Société Générale de Banque - Jordanie Jordan Banking 54.33% 50.62%

Fidus SAL* Lebanon Brokerage services 49.00% 49.00%

Sogelease Liban SAL Lebanon Leasing 99.75% 99.75%

Sogecap Liban SAL Lebanon Insurance 75.00% 75.00%

Percentage of share capitalowned by the Bank

Name Country of Activities 2009 2008incorporation

Non-controlling interests represent the portion of profit or loss and net assets not owned, directly or indirectly, by theBank and are presented separately in the consolidated income statement, consolidated statement of comprehensiveincome and within equity in the consolidated statement of financial position, separately from parent shareholders’equity. Acquisitions of non-controlling interests are accounted for using the parent entity extension method, whereby,the difference between the consideration and the fair value of the share of the net assets acquired is recognized asgoodwill.

The consolidated financial statements represent the financial statements of the Bank and the following subsidiaries:

* Effective 1 January 2004, the Group obtained control, by virtue of agreement with other investors, over Fidus SAL, andconsequently, the financial statements of Fidus SAL have been consolidated with those of the Group.

2.2 Significant accounting judgements and estimates

In the process of applying the Group's accounting policies, management has exercised judgment and estimates indetermining the amounts recognized in the consolidated financial statements. The most significant uses of judgmentand estimates are as follows:

Going concernThe Group’s management has made an assessment of the Group’s ability to continue as a going concern and is satisfiedthat the Group has the resources to continue in business for the foreseeable future. Furthermore, the management isnot aware of any material uncertainties that may cast significant doubt upon the Group’s ability to continue as a goingconcern. Therefore, the consolidated financial statements continue to be prepared on the going concern basis.

Fair value of financial instrumentsWhere the fair values of financial assets and financial liabilities recorded on the consolidated statement of financialposition cannot be derived from active markets, they are determined using a variety of valuation techniques thatinclude the use of mathematical models. The inputs to these models are derived from observable market data wherepossible, but where observable market data are not available, judgment is required to establish fair values. Thejudgments include considerations of liquidity and model inputs such as volatility for longer dated derivatives anddiscount rates, prepayment rates and default rate assumptions for asset backed securities. The valuation of financialinstruments is described in more detail in note 50.

Impairment losses on loans and advancesThe Group reviews its individually significant loans and advances at each consolidated statement of financial positiondate to assess whether an impairment loss should be recorded in the consolidated income statement. In particular,judgment by management is required in the estimation of the amount and timing of future cash flows whendetermining the impairment loss. In estimating these cash flows, the Group makes judgments about the borrower’sfinancial situation and the net realisable value of collateral. These estimates are based on assumptions about anumber of factors and actual results may differ, resulting in future changes to the allowance.

inside report 09-part1 12/21/10 8:01 PM Page 38

SOCIÉTÉ GÉNÉRALE DE BANQUE AU LIBAN | ANNUAL REPORT 2009 39

NOTES TO THECONSOLIDATED

FINANCIALSTATEMENTS

Loans and advances that have been assessed individually and found not to be impaired and all individuallyinsignificant loans and advances are then assessed collectively, in groups of assets with similar risk characteristics,to determine whether provision should be made due to incurred loss events for which there is objective evidencebut whose effects are not yet evident. The collective assessment takes account of data from the loan portfolio (suchas credit quality, levels of arrears, credit utilisation, loan to collateral ratios etc.), concentrations of risks andeconomic data (including levels of unemployment, real estate prices indices, country risk and the performance ofdifferent individual groups).

The impairment loss on loans and advances is disclosed in more detail in note 10 and note 18.

Impairment of available-for-sale investmentsThe Group reviews its debt securities classified as available-for-sale investments at each consolidated statement offinancial position date to assess whether they are impaired. This requires similar judgment as applied to theindividual assessment of loans and advances.

The Group also records impairment charges on available-for-sale equity investments when there has been asignificant or prolonged decline in the fair value below their cost. The determination of what is “significant” or“prolonged” requires judgment. In making this judgment, the Group evaluates, among other factors, historical

share price movements and the duration and extent to which the fair value of an investment is less than its cost.

Deferred tax assetsDeferred tax assets are recognized in respect of tax losses to the extent that it is probable that taxable profit will beavailable against which the losses can be utilized. Judgment is required to determine the amount of deferred taxassets that can be recognized, based upon the likely timing and level of future taxable profits, together with futuretax planning strategies.

2.3 Changes in accounting policies

The accounting policies adopted are consistent with those used in the previous financial year except that the Grouphas adopted the following standards, amendments and interpretations which did not have any effect on thefinancial performance or position of the Group. They did, however, give rise to additional disclosures.

IAS 1 Presentation of financial statementsThis standard requires an entity to present all owner changes in equity and all non-owner changes to be presentedin either one consolidated statement of comprehensive income or in two separate statements of income andcomprehensive income. The revised standard also requires that the income tax effect of each component ofcomprehensive income be disclosed. In addition, it requires entities to present a comparative consolidatedstatement of financial position as at the beginning of the earliest comparative period when the entity has appliedan accounting policy retrospectively, has made a retrospective restatement, or has reclassified items in theconsolidated financial statements.

The Group has elected to present comprehensive income in two separate statements of income and comprehensiveincome. The Group has not provided a restated comparative set of financial position for the earliest comparativeperiod, as it has not adopted any new accounting policies retrospectively, or has made a retrospective restatement,or retrospectively reclassified items in the consolidated financial statements.

Amendments to IFRS 7 Financial Instruments: Disclosures - Improving Disclosures about Financial Instruments The amendments to IFRS 7 were issued in March 2009 to enhance fair value and liquidity disclosures. With respectto fair value, the amendments require disclosure of a three-level fair value hierarchy, by class, for all financialinstruments recognized at fair value and specific disclosures related to the transfers between levels in the hierarchyand detailed disclosures related to level 3 of the fair value hierarchy. In addition, the amendments modify therequired liquidity disclosures with respect to derivative transactions and assets used for liquidity management.

Comparative information has been restated although this is not strictly required by the transition provisions of theamendment.

inside report 09-part1 12/21/10 8:01 PM Page 39

40

NOTES TO THECONSOLIDATEDFINANCIALSTATEMENTS

In addition, the following standards and interpretations are effective for the financial year 2009. The adoption of thesestandards and interpretations did not have any effect on the financial performance or position of the Group:

- IAS 23 Borrowing costs (Revised)- Amendments to IAS 32 Financial Instruments: Presentation and IAS 1 Presentation of Financial Statements, – Puttable

Financial Instruments and Obligations Arising on Liquidation- Amendment to IFRS 2 Share-based Payment – Vesting Conditions and Cancellations- Amendments to IFRIC 9 Reassessment of Embedded Derivatives and IAS 39 Financial Instruments: Recognition and

Measurement – Embedded Derivatives- IFRIC 13 Customer Loyalty Programmes- IFRIC 15 Agreements for the Construction of Real Estate- IFRIC 16 Hedges of a Net Investment in a Foreign Operation- Improvements to International Financial Reporting Standards (issued 2008)- Improvements to International Financial Reporting Standards (issued 2009)

Future changes in accounting policiesBelow is the list of standards issued but not yet effective for the year ended 31 December 2009:

- IFRS 2 Share – based Payment: Group Cash-settled Share - based Payment Transactions- IFRS 3 Business Combinations (Revised) and IAS 27 Consolidated and Separate Financial Statements (Amended)- Amendment to IAS 39 Financial Instruments: Recognition and Measurement – Eligible Hedged items- IFRIC 17 Distributions on Non-cash Assets to Owners- IFRIC 18 Transfers of Assets from Customers- IFRIC 19 Extinguishing Financial Liabilities with Equity Instruments

Management does not expect the above standards to have a significant impact on the Group’s financial statementswhen implemented in future years.

Improvements to IFRSsIn May 2008 and April 2009 the IASB issued an omnibus of amendments to its standards, primarily with a view toremoving inconsistencies and clarifying wording. There are separate transitional provisions for each standard. Theamendments to the following standards below did not have any impact on the accounting policies, financial positionor performance of the Group:

IFRS 5: Non-current Assets Held for Sale and Discontinued OperationsIAS 7: Statement of Cash Flows IAS 8: Accounting Policies, Change in Accounting Estimates and ErrorIAS 10: Events after the Reporting PeriodIAS 16: Property, Plant and EquipmentIAS 18: RevenueIAS 19: Employee BenefitsIAS 20: Accounting for Government Grants and Disclosures of Government AssistanceIAS 28: Investment in AssociatesIAS 31: Interest in Joint venturesIAS 34: Interim Financial ReportingIAS 36: Impairment of AssetsIAS 38: Intangible AssetsIAS 39: Financial Instruments: Recognition and MeasurementIAS 40: Investment Properties

2.4 Summary of significant accounting policies

(1) Foreign currency translationThe consolidated financial statements are presented in Lebanese Lira. Each entity in the Group determines its own

fuctional currency and items included in the financial statements of each entity are measured using that functionalcurrency.

inside report 09-part1 12/21/10 8:01 PM Page 40

SOCIÉTÉ GÉNÉRALE DE BANQUE AU LIBAN | ANNUAL REPORT 2009 41

NOTES TO THECONSOLIDATED

FINANCIALSTATEMENTS

(i) Transactions and balancesTransactions in foreign currencies are initially recorded at the functional currency at the rate of exchange ruling atthe date of the transaction.

Monetary assets and liabilities denominated in foreign currencies are retranslated at the functional currency rate ofexchange at the consolidated statement of financial position date. All differences arising on non-trading activitiesare taken to the consolidated income statement, with the exception of differences on foreign currency borrowingsthat provide effective hedge against a net investment in a foreign entity. These differences are taken directly toequity until the disposal of the net investment, at which time they are recognized in the consolidated incomestatement. Tax charges and credits attributable to exchange differences on those borrowings are also recorded in equity.

Non-monetary items that are measured in terms of historical cost in a foreign currency are translated using theexchange rates as at the dates of the initial transactions. Non-monetary items measured at fair value in a foreigncurrency are translated using the exchange rates at the date when the fair value was determined. Any goodwill arisingon the acquisition of a foreign operation and any fair adjustments to the carrying amounts of assets and liabilitiesarising on the acquisition are treated as assets and liabilities of the foreign operations and translated at closing rate.

(ii) Group companiesAt the reporting date, the assets and liabilities of subsidiaries are translated into the Bank’s presentation currency atthe rate of exchange as at statement of financial position date, and their income statements are translated at theweighted average exchange rates for the year. Exchange differences arising on translation are taken directly to aseparate component of equity. On disposal of a foreign entity, the deferred cumulative amount recognized inequity relating to that particular foreign operation is recognized in the consolidated income statement in “Otheroperating expenses” or “Other operating income”.

(2) Financial Instruments - initial recognition and subsequent measurement(i) Date of recognitionAll financial assets and liabilities are initially recognized on the trade date, i.e., the date that the Group becomes aparty to the contractual provisions of the instrument. This includes “regular way trades”: purchases or sales offinancial assets that require delivery of assets within the time frame generally established by regulation orconvention in the market place.

(ii) Initial measurement of financial instrumentsThe classification of financial instruments at initial recognition depends on the purpose and the management’sintention for which the financial instruments were acquired and their characteristics. All financial instruments aremeasured initially at their fair value plus transaction costs, except in the case of financial assets and financialliabilities recorded at fair value through profit or loss.

(iii) Derivatives recorded at fair value through profit or lossThe Group uses derivatives such as interest rate swaps and forward foreign exchange contracts. Derivatives arerecorded at fair value and carried as assets when their fair value is positive and as liabilities when their fair value isnegative. Changes in the fair value of derivatives are included in “Net trading income”.

Derivatives embedded in other financial instruments, such as the conversion option in an acquired convertiblebond, are treated as separate derivatives and recorded at fair value if their economic characteristics and risks are notclosely related to those of the host contract, and the host contract is not itself held-for-trading or designated at fairvalue through profit or loss. The embedded derivatives separated from the host are carried at fair value in thetrading portfolio with changes in fair value recognized in the consolidated income statement.

(iv) Financial assets or financial liabilities held-for-tradingFinancial assets or financial liabilities held-for-trading are recorded in the consolidated statement of financialposition at fair value. Changes in fair value are recognized in “Net trading income”. Interest and dividend income orexpense is recorded in “Net trading income” according to the terms of the contract, or when the right to thepayment has been established.

Included in this classification are debt securities and equities which have been acquired principally for the purposeof selling or repurchasing in the near term.

inside report 09-part1 12/21/10 8:01 PM Page 41

NOTES TO THECONSOLIDATEDFINANCIALSTATEMENTS

(v) ‘Day 1’ profit or loss When the transaction price is different to the fair value from other observable current market transactions in the sameinstrument or based on a valuation technique whose variables include only data from observable markets, the Bankimmediately recognizes the difference between the transaction price and fair value (a ‘Day 1’ profit or loss) in “Nettrading income”. In cases where fair value is determined using data which is not observable, the difference between thetransaction price and model value is only recognized in the consolidated income statement when the inputs becomeobservable, or when the instrument is derecognized.

(vi) Held-to-maturity financial investmentsHeld-to-maturity financial instruments are non-derivative financial assets with fixed or determinable payments and

have fixed maturities and which the Group has the intention and ability to hold to maturity. After initial measurement,held-to-maturity financial investments are subsequently measured at amortized cost using the effective interestmethod, less allowance for impairment. Amortized cost is calculated by taking into account any discount or premiumon acquisition and fees that are an integral part of the effective interest rate. The amortization is included in “Interestand similar income” in the consolidated income statement. The losses arising from impairment of such investments arerecognized in the consolidated income statement under “impairment losses on financial investments”.

If the Group were to sell or reclassify more than an insignificant amount of held-to-maturity investments beforematurity (other than in certain specific circumstances), the entire category would be tainted and would have to bereclassified as available-for-sale. Furthermore, the Group would be prohibited from classifying any financial asset asheld to maturity during the following two years.

(vii) Financial assets designated at fair value through profit or lossFinancial assets classified in this category are those that have been designated by management on initial recognition.Management may only designate an instrument at fair value through profit or loss upon initial recognition when thefollowing criteria are met, and designation is determined on an instrument by instrument basis:

• The designation eliminates or significantly reduces the inconsistent treatment that would otherwise arise frommeasuring the assets or liabilities or recognizing gains or losses on them on a different basis; or

• The assets are part of a group of financial assets which are managed and their performance evaluated on a fair valuebasis, in accordance with a documented risk management or investment strategy; or

• The financial instrument contains one or more embedded derivatives which significantly modify the cash flows thatwould be otherwise required by the contract.

Financial assets at fair value through profit or loss are recorded in the consolidated statement of financial position atfair value. Changes in fair value are recorded in “Net gain or loss on financial assets designated at fair value throughprofit or loss”. Interest earned is accrued in “Interest income” using the effective interest rate, while dividend income isrecorded in “Other operating income” when the right to the payment has been established.

Included in this classification are listed equities and bonds held to cover unit-linked liabilities.

(viii) Available-for-sale financial investmentsAvailable-for-sale investments include equity and debt securities. Equity investments classified as available-for-sale arethose which are neither classified as held-for-trading nor designated at fair value through profit or loss. Debt securitiesin this category are those which are intended to be held for an indefinite period of time and which may be sold inresponse to needs for liquidity or in response to changes in the market conditions.

After initial measurement, available-for-sale financial investments are subsequently measured at fair value. Unrealizedgains and losses are recognized directly in equity in the “available-for-sale reserve”. When the investment is disposed ofthe cumulative gain or loss previously recognized in equity is recognized in the income statement. Interest earnedwhilst holding available-for-sale financial investments is reported as interest income using the effective interest ratemethod. Dividends earned whilst holding available-for-sale financial investments are recognized in the consolidatedincome statement as “Net gain on financial investments” when the right of the payment has been established. Thelosses arising from impairment of such investments are recognized in the consolidated income statement as“Impairment losses on financial investments” and removed from the “available-for-sale reserve”.

42

inside report 09-part1 12/21/10 8:01 PM Page 42

NOTES TO THECONSOLIDATED

FINANCIALSTATEMENTS

(ix) Financial assets classified as loans and receivablesLoans and receivables, include non-derivative financial assets with fixed or determinable payments that are notquoted in an active market. These financial assets are initially recognized at cost, being the fair value of theconsideration paid for the acquisition of the investment. All transaction costs directly attributed to the acquisitionare also included in the cost of investment.

After initial measurement, loans and receivables are measured at amortized cost using the effective interest ratemethod, less allowance for impairment. Amortized cost is calculated by taking into account any discount orpremium on acquisition and fees and costs that are an integral part of the effective interest rate. The amortisation isincluded in “Interest and similar income“ in the consolidated income statement. The losses arising from impairmentare recognized in the consolidated income statement in “Impairment losses on financial instruments”. Gains orlosses are recognized in the consolidated income statement when the investments are derecognized or impaired.The losses arising from impairment are recognized in the consolidated income statement in “Credit loss expenses”.

(x) Due from banks and loans and advances to customers“Due from banks“ and “Loans and advances to customers”, include non-derivative financial assets with fixed ordeterminable payments that are not quoted in an active market, other than:

a. Those that the Group intends to sell immediately or in the near term and those that the Group upon initialrecognition designates as at fair value through profit or loss;

b. Those that the Group, upon initial recognition, designates as available-for-sale; orc. Those for which the Group may not recover substantially all of its initial investment, other than because of

credit deterioration.

After initial measurement, amount “Due from banks” and “Loans and advances to customers” are subsequentlymeasured at amortized cost using the effective interest rate, less allowance for impairment. Amortized cost iscalculated by taking into account any discount or premium on acquisition and fees and costs that are an integralpart of the effective interest rate. The amortization is included in “Interest and similar income” in the consolidatedincome statement. The losses arising from impairment are recognized in the consolidated income statement in“Credit loss expense”.

(xi) Reclassification of financial assetsEffective from 1 July 2008, the Group may reclassify, in certain circumstances, non-derivative financial assets out ofthe “Held-for-trading” category and into the “Available-for-sale”, “Loans and receivables”, or “Held-to maturity”categories. From this date it may also reclassify, in certain circumstances, financial instruments out of the “Available-for-sale“ category and into the “Loans and receivables” category. Reclassifications are recorded at fair value at thedate of reclassification, which becomes the new amortized cost.

The Group may reclassify a non-derivative trading asset out of the “Held-for-trading” category and into the “Loansand receivables” category if it meets the definition of loans and receivables and the Group has the intention andability to hold the financial asset for the foreseeable future or until maturity. If a financial asset is reclassified, and ifthe Group subsequently increases its estimates of future cash receipts as a result of increased recoverability of thosecash receipts, the effect of that increase is recognized as an adjustment to the effective interest rate from the dateof the change in estimate.

For a financial asset reclassified out of the “Available-for-sale” category, any previous gain or loss on that asset thathas been recognized in equity is amortized to profit or loss over the remaining life of the investment using theeffective interest rate. Any difference between the new amortized cost and the expected cash flows is alsoamortized over the remaining life of the asset using the effective interest rate. If the asset is subsequentlydetermined to be impaired then the amount recorded in equity is recycled to the consolidated income statement.

Reclassification is at the election of management, and is determined on an instrument by instrument basis.

SOCIÉTÉ GÉNÉRALE DE BANQUE AU LIBAN | ANNUAL REPORT 2009 43

inside report 09-part1 12/21/10 8:01 PM Page 43

NOTES TO THECONSOLIDATEDFINANCIALSTATEMENTS

(3) Derecognition of financial assets and financial liabilities

Financial assetsA financial asset (or where applicable, a part of a financial asset or part of a group of similar financial assets) isderecognized when:

• The rights to receive cash flows from the asset have expired, or • The Group has transferred its rights to receive cash flows from the asset, or has assumed an obligation to pay the

received cash flow in full without material delay to a third party under a “pass through” arrangement; and • Either (a) the Group has transferred substantially all the risks and rewards of the asset, or (b) the Bank has neither

transferred nor retained substantially all the risks and rewards of the asset, but has transferred control of the asset.

When the Group has transferred its rights to receive cash flows from an asset and has neither transferred nor retainedsubstantially all the risks and rewards of the asset nor transferred control of the asset, the asset is derecognized to theextent of the Group’s continuing involvement in the asset. Continuing involvement that takes the form of a guaranteeover the transferred asset is measured at the lower of the original carrying amount of the asset and the maximumamount of consideration that the Group could be required to repay.

Continuing involvement that takes the form of a guarantee over the transferred asset is measured at the lower of theoriginal carrying amount of the asset and the maximum amount of consideration that the Group could be required torepay.

Financial liabilities A financial liability is derecognized when the obligation under the liability is discharged or cancelled or expired. Wherean existing financial liability is replaced by another from the same lender on substantially different terms, or the termsof an existing liability are substantially modified, such an exchange or modification is treated as a derecognition of theoriginal liability and the recognition of a new liability and the difference in the respective carrying amount isrecognized in the consolidated income statement.

(4) Repurchase and reverse repurchase agreementsSecurities sold under agreements to repurchase at a specified future date are not derecognized from the consolidatedstatement of financial position as the Group retains substantially all the risks and rewards of ownership. Thecorresponding cash received is recognized in the consolidated statement of financial position as an asset with acorresponding obligation to return it, including accrued interest as a liability, reflecting the transaction’s economicsubstance as a loan to the Group. The difference between the sale and repurchase prices is treated as interest expenseand is accrued over the life of the agreement using the effective interest rate.

Conversely, securities purchased under agreements to resell at a specified future date are not recognized in theconsolidated statement of financial position. The consideration paid, including accrued interest, is recorded in theconsolidated statement of financial position, reflecting the transaction’s economic substance as a loan by the Bank. Thedifference between the purchase and resale prices is recorded in “Net interest income“ and is accrued over the life ofthe agreement using the effective interest rate.

If securities purchased under agreement to resell are subsequently sold to third parties, the obligation to return thesecurities is recorded as a short sale within “Financial liabilities held-for-trading“ and measured at fair value with anygains or losses included in “Net trading income”.

(5) Securities lending and borrowingSecurities lending and borrowing transactions are usually collateralised by securities or cash. The transfer of thesecurities to counterparties is only reflected on the consolidated statement of financial position if the risks and rewardsof ownership are also transferred. Cash advanced or received as collateral is recorded as an asset or liability.

Securities borrowed are not recognized on the consolidated statement of financial position, unless they are then soldto third parties, in which case the obligation to return the securities is recorded as a trading liability and measured atfair value with any gains or losses included in “Net trading income”.

44

inside report 09-part1 12/21/10 8:01 PM Page 44

NOTES TO THECONSOLIDATED

FINANCIALSTATEMENTS

(6) Determination of fair valueThe fair value for financial instruments traded in active markets at the consolidated statement of financial positiondate is based on their quoted market price or dealer price quotations (bid price for long positions and ask price forshort positions), without any deduction for transaction costs.

For all other financial instruments not traded in an active market, the fair value is determined by using appropriatevaluation techniques. Valuation techniques include the discounted cash flow method, comparison to similarinstruments for which market observable prices exist, option pricing models, credit models and other relevantvaluation models.

Certain financial instruments are recorded at fair value using valuation techniques in which current markettransactions or observable market data are not available. Their fair value is determined using a valuation model thathas been tested against prices or inputs to actual market transactions and using the Bank’s best estimate of the mostappropriate model assumptions. Models are adjusted to reflect the spread for bid and ask prices to reflect costs toclose out positions, counterparty credit and liquidity spread and limitations in the models. Also, profit or losscalculated when such financial instruments are first recorded (‘Day 1’ profit or loss) is deferred and recognized onlywhen the inputs become observable or on derecognition of the instrument.

An analysis of fair values of financial instruments and further details as to how they are measured are provided innote 50.

(7) Impairment of financial assetsThe Group assesses at each consolidated statement of financial position date whether there is any objectiveevidence that a financial asset or a group of financial assets is impaired. A financial asset or a group of financial assetsis deemed to be impaired if, and only if, there is objective evidence of impairment as a result of one or more eventsthat has occurred after the initial recognition of the asset (an incurred ‘loss event’) and that loss event (or events) hasan impact on the estimated future cash flows of the financial asset or the group of financial assets that can bereliably estimated.

Evidence of impairment may include indications that the borrower or a group of borrowers is experiencingsignificant financial difficulty, the probability that they will enter bankruptcy or other financial reorganisation,default or delinquency in interest or principal payments and where observable data indicates that there is ameasurable decrease in the estimated future cash flows, such as changes in arrears or economic conditions thatcorrelate with defaults.

(i) Financial assets carried at amortized costFor financial assets carried at amortized cost (such as deposits with bank and financial institutions, amounts duefrom head office, branches and affiliates, loans and advances to customers, loans and advances to related parties,held to maturity financial instruments and financial assets classified as loans and receivables), the Group first assessesindividually whether objective evidence of impairment exists individually for financial assets that are individuallysignificant, or collectively for financial assets that are not individually significant. If the Group determines that noobjective evidence of impairment exists for an individually assessed financial asset, it includes the asset in a groupof financial assets with similar credit risk characteristics and collectively assesses them for impairment. Assets thatare individually assessed for impairment and for which an impairment loss is, or continues to be, recognized are notincluded in a collective assessment of impairment.

If there is objective evidence that an impairment loss has been incurred, the amount of the loss is measured as thedifference between the asset’s carrying amount and the present value of estimated future cash flows (excludingfuture expected credit losses that have not yet been incurred). The carrying amount of the asset is reduced throughthe use of an allowance account and the amount of the loss is recognized in the consolidated income statement.Loans together with the associated allowance are written off when there is no realistic prospect of future recoveryand all collateral has been realised or has been transferred to the Group. If, in a subsequent year, the amount of theestimated impairment loss increases or decreases because of an event occurring after the impairment wasrecognized, the previously recognized impairment loss is increased or reduced by adjusting the allowance account.If a future write-off is later recovered, the recovery is credited to the ‘Credit loss expense’.

SOCIÉTÉ GÉNÉRALE DE BANQUE AU LIBAN | ANNUAL REPORT 2009 45

inside report 09-part1 12/21/10 8:01 PM Page 45

NOTES TO THECONSOLIDATEDFINANCIALSTATEMENTS

The present value of the estimated future cash flows is discounted at the financial asset’s original effective interest rate.If a loan has a variable interest rate, the discount rate for measuring any impairment loss is the current effectiveinterest rate. If the Group has reclassified trading assets to loans and advances, the discount rate for measuring anyimpairment loss is the new effective interest rate determined at the reclassification date. The calculation of the presentvalue of the estimated future cash flows of a collateralised financial asset reflects the cash flows that may result fromforeclosure less costs for obtaining and selling the collateral, whether or not foreclosure is probable.

For the purpose of a collective evaluation of impairment, financial assets are grouped on the basis of the Group’sinternal credit grading system, that considers credit risk characteristics such as asset type, industry, geographicallocation, collateral type, past-due status and other relevant factors.

Future cash flows on a group of financial assets that are collectively evaluated for impairment are estimated on thebasis of historical loss experience for assets with credit risk characteristics similar to those in the group. Historical lossexperience is adjusted on the basis of current observable data to reflect the effects of current conditions on which thehistorical loss experience is based and to remove the effects of conditions in the historical period that do not existcurrently. Estimates of changes in future cash flows reflect, and are directionally consistent with, changes in relatedobservable data from year to year (such as changes in unemployment rates, property prices, commodity prices,payment status, or other factors that are indicative of incurred losses in the group and their magnitude). Themethodology and assumptions used for estimating future cash flows are reviewed regularly to reduce any differencesbetween loss estimates and actual loss experience.

(ii) Available-for-sale financial investmentsFor available-for-sale financial investments, the Group assess at each statement of financial position date whetherthere is objective evidence that an investment is impaired.

In the case of debt instruments classified as available-for-sale, the Bank assesses individually whether there is objectiveevidence of impairment based on the same criteria as financial assets carried at amortized cost. However, the amountrecorded for impairment is the cumulative loss measured as the difference between the amortized cost and thecurrent fair value, less any impairment loss on that investment previously recognized in the consolidated incomestatement. Future interest income is based on the reduced carrying amount and is accrued using the rate of interestused to discount the future cash flows for the purpose of measuring the impairment loss. The interest income is recordedas part of “Interest and similar income”. If, in a subsequent period, the fair value of a debt instrument increases and theincrease can be objectively related to a credit event occurring after the impairment loss was recognized in theconsolidated income statement, the impairment loss is reversed through the consolidated income statement.

In the case of equity investments classified as available-for-sale, objective evidence would also include a “significant“or “prolonged“ decline in the fair value of the investment below its cost. Where there is evidence of impairment, thecumulative loss measured as the difference between the acquisition cost and the current fair value, less anyimpairment loss on that investment previously recognized in the consolidated income statement – is removed fromequity and recognized in the consolidated income statement. Impairment losses on equity investments are notreversed through the consolidated income statement; increases in the fair value after impairment are recognizeddirectly in equity.

(iii) Renegotiated loansWhere possible, the Group seeks to restructure loans rather than to take possession of collateral. This may involveextending the payment arrangements and the agreement of new loan conditions. Once the terms have beenrenegotiated any impairment is measured using the original effective interest rate as calculated before themodification of terms and the loan is no longer considered past due. Management continuously reviews renegotiatedloans to ensure that all criteria are met and that future payments are likely to occur. The loans continue to be subjectto an individual or collective impairment assessment, calculated using the loan’s original effective interest rate.

(8) Hedge accountingThe Group makes use of derivative instruments to manage exposures to interest rate and foreign currency risks. Inorder to manage particular risks, the Group applies hedge accounting for transactions which meet the specified criteria.

At inception of the hedge relationship, the Group formally documents the relationship between the hedged item andthe hedging instrument, including the nature of the risk, the objective and strategy for undertaking the hedge and themethod that will be used to assess the effectiveness of the hedging relationship.

46

inside report 09-part1 12/21/10 8:01 PM Page 46

NOTES TO THECONSOLIDATED

FINANCIALSTATEMENTS

Also at the inception of the hedge relationship, a formal assessment is undertaken to ensure the hedginginstrument is expected to be highly effective in offsetting the designated risk in the hedged item. A hedge isexpected to be highly effective if the changes in fair value or cash flows attributable to the hedged risk during theperiod for which the hedge is designated are expected to offset in a range of 80% to 125%. For situations where thathedged item is a forecast transaction, the Group assesses whether the transaction is highly probable and presentsan exposure to variations in cash flows that could ultimately affect the consolidated income statement.

(i) Fair value hedgesFor designated and qualifying fair value hedges, the change in the fair value of a hedging derivative is recognizedin the consolidated income statement in “Net trading income”. Meanwhile, the change in the fair value of thehedged item attributable to the risk hedged is recorded as part of the carrying value of the hedged item and is alsorecognized in the income statement in “Net trading income”.

If the hedging instrument expires or is sold, terminated or exercised, or where the hedge no longer meets thecriteria for hedge accounting, the hedge relationship is terminated. For hedged items recorded at amortized cost,the difference between the carrying value of the hedged item on termination and the face value is amortized overthe remaining term of the original hedge using the effective interest rate. If the hedged item is derecognized, theunamortized fair value adjustment is recognized immediately in the consolidated income statement.

(ii) Cash flow hedgesFor designated and qualifying cash flow hedges, the effective portion of the gain or loss on the hedging instrumentis initially recognized directly in equity in the “Cash flow hedge reserve”. The ineffective portion of the gain or losson the hedging instrument is recognized immediately in the consolidated income statement.

When the hedged cash flow affects the income statement, the gain or loss on the hedging instrument is recordedin the corresponding income or expense line of the consolidated income statement. When a hedging instrumentexpires, or is sold, terminated, exercised, or when a hedge no longer meets the criteria for hedge accounting, anycumulative gain or loss existing in equity at that time remains in equity and is recognized when the hedged forecasttransaction is ultimately recognized in the consolidated income statement. When a forecast transaction is no longerexpected to occur, the cumulative gain or loss that was reported in equity is immediately transferred to theconsolidated income statement.

(iii) Hedge of a net investmentHedges of net investments in a foreign operation, including a hedge of a monetary item that is accounted for as partof the net investment, are accounted for in a way similar to cash flow hedges. Gains or losses on the hedginginstrument relating to the effective portion of the hedge are recognized directly in equity while any gains or lossesrelating to the ineffective portion are recognized in the consolidated income statement. On disposal of the foreignoperation, the cumulative value of any such gains or losses recognized directly in equity is transferred to theconsolidated income statement.

(9) Offsetting financial instrumentsFinancial assets and financial liabilities are offset and the net amount reported in the statement of financial positionif, and only if, there is a currently enforceable legal right to offset the recognized amounts and there is an intentionto settle on a net basis, or to realise the asset and settle the liability simultaneously. This is not generally the casewith master netting agreements, therefore, the related assets and liabilities are presented gross in the consolidatedstatement of financial position.

(10) LeasingThe determination of whether an arrangement is a lease, or it contains a lease, is based on the substance of thearrangement and requires an assessment of whether the fulfilment of the arrangement is dependent on the use ofa specific asset or assets and the arrangement conveys a right to use the asset.

Group as a lesseeLeases which do not transfer to the Group substantially all the risks and benefits incidental to ownership of theleased items are operating leases. Operating lease payments are recognized as an expense in the consolidatedincome statement on a straight line basis over the lease term. Contingent rents payable are recognized as anexpense in the period in which they are incurred.

SOCIÉTÉ GÉNÉRALE DE BANQUE AU LIBAN | ANNUAL REPORT 2009 47

inside report 09-part1 12/21/10 8:01 PM Page 47

NOTES TO THECONSOLIDATEDFINANCIALSTATEMENTS

Group as a lessorLeases where the Group does not transfer substantially all the risk and benefits of ownership of the asset areclassified as operating leases. Initial direct costs incurred in negotiating operating leases are added to the carryingamount of the leased asset and recognized over the lease term on the same basis as rental income. Contingentrents are recognized as revenue in the period in which they are earned.

(11) Recognition of income and expenseRevenue is recognized to the extent that it is probable that the economic benefits will flow to the Group and therevenue can be reliably measured. The following specific recognition criteria must also be met before revenue isrecognized.

(i) Interest and similar income and expenses For all financial instruments measured at amortized cost, interest bearing financial assets classified as available-for-saleand financial instruments designated at fair value through profit or loss, interest income or expense is recorded usingthe effective interest rate, which is the rate that exactly discounts estimated future cash payments or receipts throughthe expected life of the financial instrument or a shorter period, where appropriate, to the net carrying amount of thefinancial asset or financial liability. The calculation takes into account all contractual terms of the financial instrumentand includes any fees or incremental costs that are directly attributable to the instrument and are an integral part ofthe effective interest rate, but not future credit losses. The carrying amount of the financial asset or financial liability isadjusted if the Group revises its estimates of payments or receipts. The adjusted carrying amount is calculated basedon the original effective interest rate. However, for a reclassified financial asset (see Note 2.4 (2) for which the Groupsubsequently increases its estimates of future cash receipts as a result of increased recoverability of those cash receipts,the effect of that increase is recognized as an adjustment to the effective interest rate from the date of the change inestimate.

Once the recorded value of a financial asset or a group of similar financial assets has been reduced due to animpairment loss, interest income continues to be recognized using the rate of interest used to discount the future cashflows for the purpose of measuring the impairment loss.

(ii) Fee and commission incomeThe Group earns fee and commission income from a diverse range of services it provides to its customers. Fee incomecan be divided into the following two categories:

Fee income earned from services that are provided over a certain period of timeFees earned for the provision of services over a period of time are accrued over that period. These fees includecommission income and asset management, custody and other management and advisory fees.

Loan commitment fees for loans that are likely to be drawn down and other credit related fees are deferred (togetherwith any incremental costs) and recognized as an adjustment to the effective interest rate on the loan. When it isunlikely that a loan be drawn down, the loan commitment fees are recognized over the commitment period on astraight line basis.

Fee income from providing transaction servicesFees arising from negotiating or participating in the negotiation of a transaction for a third party, such as thearrangement of the acquisition of shares or other securities or the purchase or sale of businesses, are recognized oncompletion of the underlying transaction. Fees or components of fees that are linked to a certain performance arerecognized after fulfilling the corresponding criteria.

(iii) Dividend incomeDividend income is recognized when the Group’s right to receive the payment is established.

(iv) Net trading incomeResults arising from trading activities include all gains and losses from changes in fair value and related interest incomeor expense and dividends for financial assets and financial liabilities “Held-for-trading”. This includes any ineffectivenessrecorded in hedging transactions.

48

inside report 09-part1 12/21/10 8:01 PM Page 48

NOTES TO THECONSOLIDATED

FINANCIALSTATEMENTS

(12) Cash and cash equivalentsCash and cash equivalents as referred to in the consolidated statement of cash flows comprise cash and balanceswith the Central Banks, treasury bills, deposits with banks and financial institutions, amounts due from head office,branches and affiliates, due to banks and other financial institutions and amounts due to head office, branches andaffiliates with an original maturity of three months or less.

(13) Investments in subsidiaries and associatesInvestments in subsidiaries and associates are carried at cost less impairment. Subsidiaries are enterprises which theBank controls, normally where it holds more than 50% of the voting power. Associates are enterprises in which theBank exercises significant influence, but not control, normally where it holds 20% to 50% of the voting power.

(14) Property and equipment Property and equipment are initially recorded at cost less accumulated depreciation and any impairment in value.Buildings acquired prior to 1 January 1994 were restated for the changes in the general purchasing power ofLebanese Lira after the approval of the Bank of Lebanon. Net surplus arising on restatement is credited to“Revaluation reserve of property”. Changes in the expected useful life are accounted for by changing thedepreciation period or method, as appropriate, and treated as changes in accounting estimates.

Depreciation is calculated using the straight line method on all tangible fixed assets. The rates of depreciation arebased upon the following estimated useful lives:

• Buildings 50 years• Furniture and fixtures 5 to 12.5 years• Installations 16.67 years• Vehicles 10 years

Property and equipment is derecognized on disposal or when no future economic benefits are expected from itsuse. Any gain or loss arising on derecognition of the asset (calculated as the difference between the net disposalproceeds and the carrying amount of the asset) is recognized in “Net profit from sale or disposal of other assets” inthe consolidated income statement in the year the asset is derecognized.

(15) Business combinations and goodwillBusiness combinations are accounted for using the purchase method of accounting. This involves recognizingidentifiable assets (including previously unrecognized intangible assets) and liabilities (including contingentliabilities but excluding future restructuring) of the acquired business at fair value. Any excess of the cost ofacquisition over the fair values of the identifiable net assets acquired is recognized as goodwill. If the cost ofacquisition is less than the fair values of the identifiable net assets acquired, the discount on acquisition isrecognized directly in the income statement in the year of acquisition.

Goodwill acquired in a business combination is initially measured at cost being the excess of the cost of thebusiness combination over the Group’s interest in the net fair value of the identifiable assets, liabilities andcontingent liabilities acquired.

Following initial recognition, goodwill is measured at cost less any accumulated impairment losses. Goodwill isreviewed for impairment annually or more frequently if events or changes in circumstances indicate that thecarrying value may be impaired. For the purpose of impairment testing, goodwill acquired in a businesscombination is, from the acquisition date, allocated to each of the Bank’s cash-generating units, or groups ofcash-generating units, that are expected to benefit from the synergies of the combination, irrespective of whetherother assets or liabilities of the acquiree are assigned to those units or groups of units. Each unit or group of units towhich the goodwill is allocated:• represents the lowest level within the Group at which the goodwill is monitored for internal management

purposes; and• is not larger than a segment in accordance with IFRS 8 Operating Segments.

Where goodwill forms part of a cash generating unit or a group of cash generating units and part of the operationwithin that unit is disposed of, the goodwill associated with the operation disposed of is included in the carrying

SOCIÉTÉ GÉNÉRALE DE BANQUE AU LIBAN | ANNUAL REPORT 2009 49

inside report 09-part1 12/21/10 8:01 PM Page 49

NOTES TO THECONSOLIDATEDFINANCIALSTATEMENTS

amount of the operation when determining the gain or loss on disposal of the operation. Goodwill disposed of in thiscircumstance is measured based on the relative values of the operation disposed of and the portion of the cashgenerating unit retained.

When subsidiaries are sold, the difference between the selling price and the net assets plus cumulative translationdifferences and goodwill is recognized in the consolidated income statement.

(16) Intangible assetsThe Group’s intangible assets include the value of computer software and key money. An intangible asset is recognizedonly when its cost can be measured reliably and it is probable that the expected future economic benefits that areattributable to it will flow to the Bank.

Intangible assets acquired separately are measured on initial recognition at cost. The cost of intangible assets acquiredin a business combination is their fair value as at the date of acquisition. Following initial recognition, intangible assetsare carried at cost less any accumulated amortization and any accumulated impairment losses.

The useful lives of intangible assets are assessed to be either finite or indefinite. Intangible assets with finite lives areamortized over the useful economic life. The amortization period and the amortization method for an intangible assetwith a finite useful life are reviewed at least at each financial year-end. Changes in the expected useful life or theexpected pattern of consumption of future economic benefits embodied in the asset are accounted for by changingthe amortization period or method, as appropriate, and treated as changes in accounting estimates. The amortizationexpense on intangible assets with finite lives is recognized in the consolidated income statement in the expensecategory consistent with the function of the intangible asset.

Amortization is calculated using the straight line method to write down the cost of intangible assets to their residualvalues over 5 years.

(17) Non-current assets held for saleThe Group occasionally acquires real estate in settlement of certain loans and advances. Such real estate is stated atthe lower of the net realizable value of the related loans and advances and the current fair value of such assets basedon the instructions of the regulators. Gains or losses on disposal, and revaluation losses, are recognized in theconsolidated income statement for the period.

(18) Deferred costsDeferred costs are the difference between the cost of the acquisition and the Bank’s interest in the net assets of InaashBank SAL. Deferred costs are amortized over the period of the soft loan granted by the Bank of Lebanon following theacquisition. Amortization expense is reported as a contra revenue account on interest revenue on treasury bills as thesoft loan received from the Bank of Lebanon is invested in Lebanese treasury bills.

Deferred costs are stated at cost less accumulated amortization and accumulated impairment losses.