Embed Size (px)

Citation preview

1

ZON OPTIMUS, SGPS, SA

CONSOLIDATED MANAGEMENT REPORT

1Q14

2

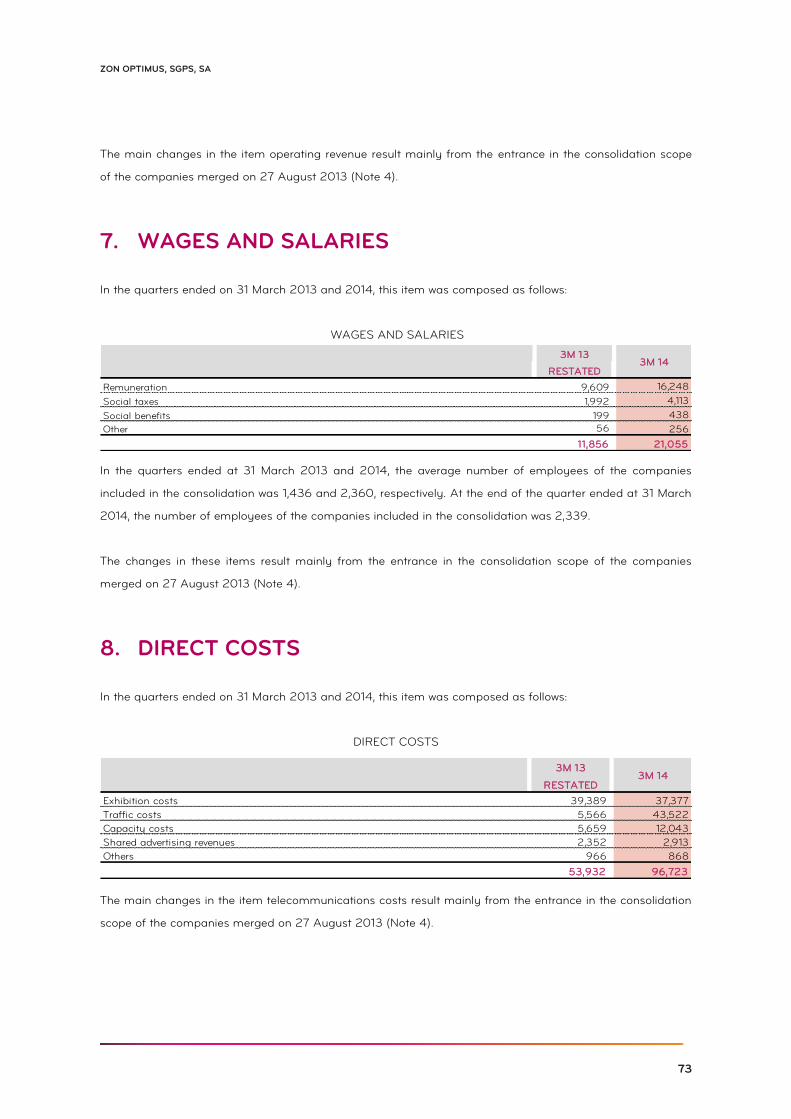

CONSOLIDATED MANAGEMENT REPORT 1Q14

TABLE OF CONTENTS

1. KEY PERFORMANCE INDICATORS 3

2. 1Q14 HIGHLIGHTS 7

3. CORPORATE BODIES 9

4. MANAGEMENT REPORT 12

Business Review 13

Consolidated Financial Review 22

5. CONSOLIDATED FINANCIAL STATEMENTS 29

3

ZON OPTIMUS, SGPS, SA

1.

KPIs

4

CONSOLIDATED MANAGEMENT REPORT 1Q14

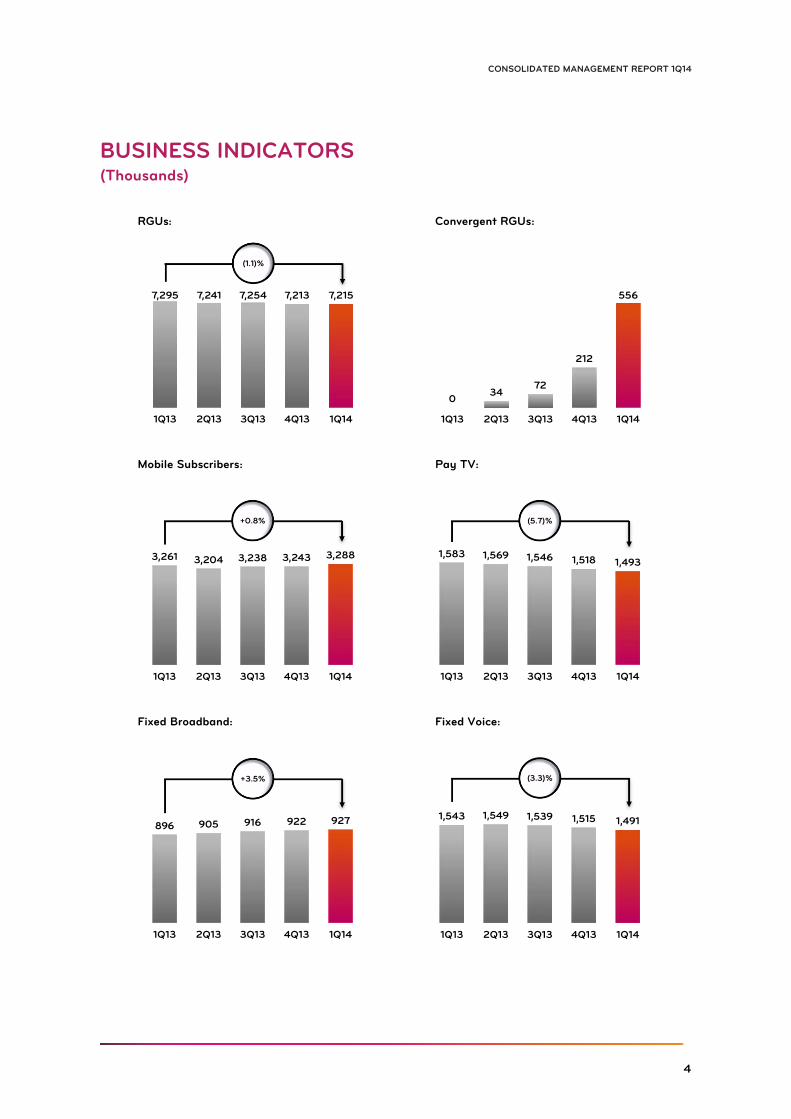

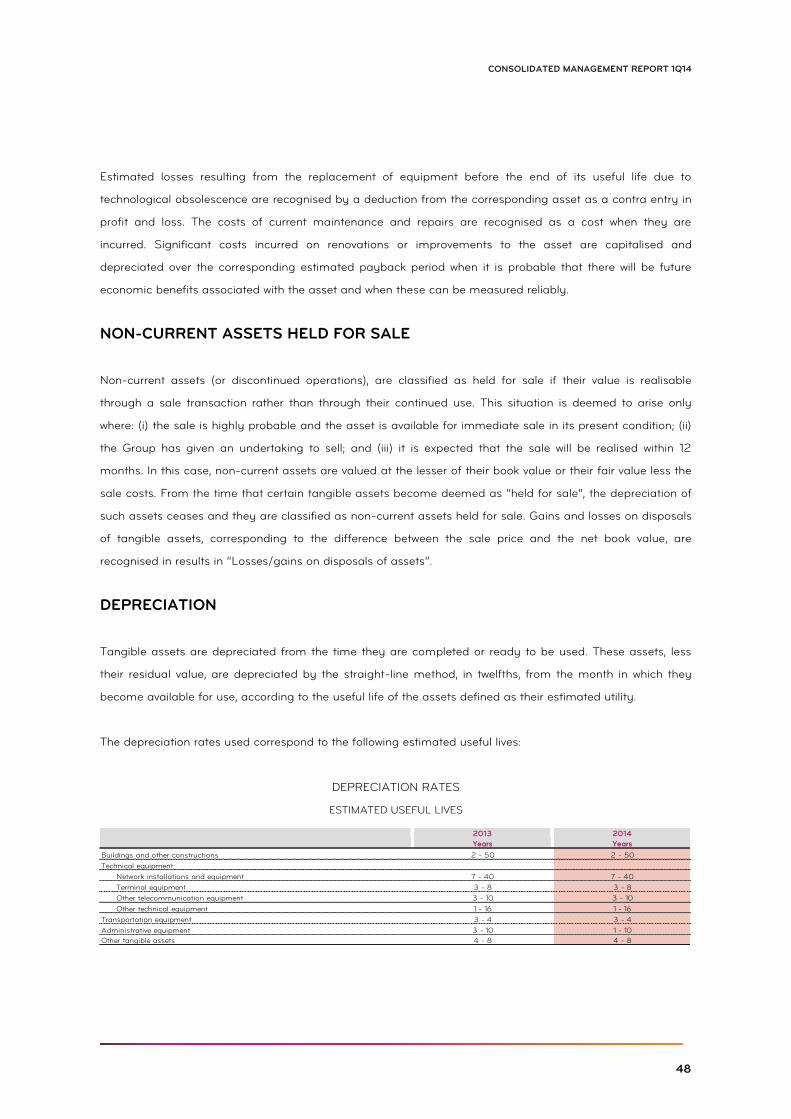

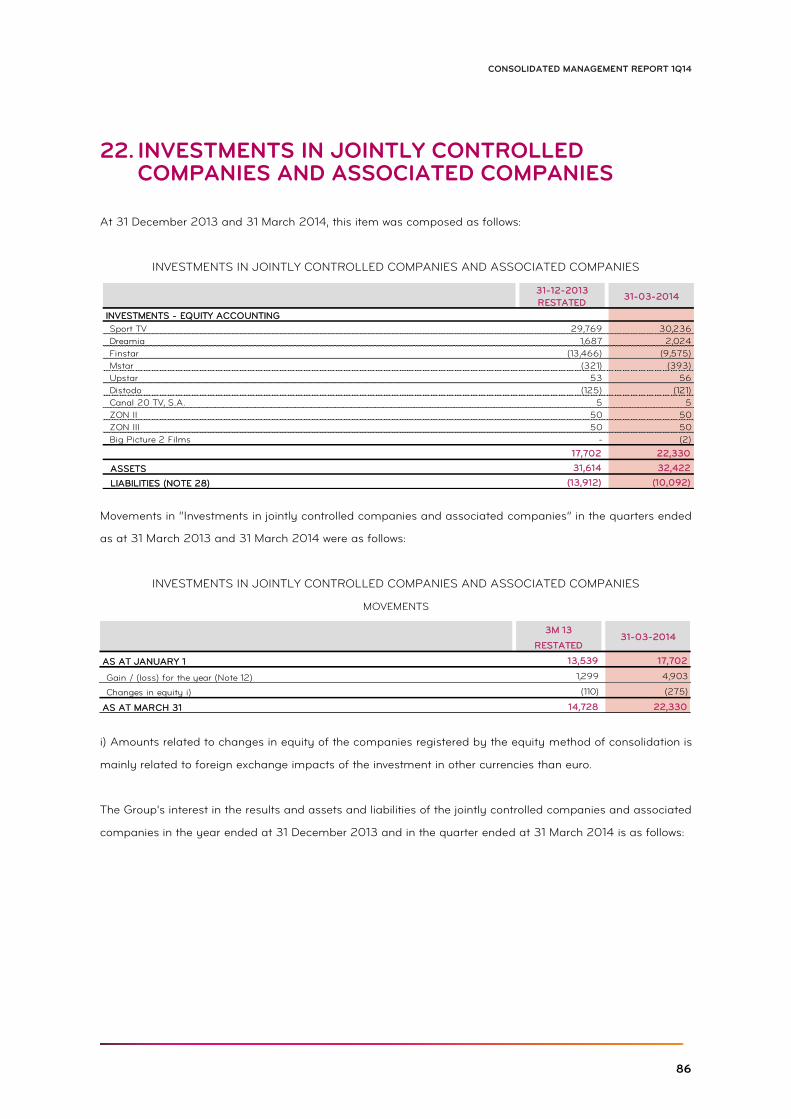

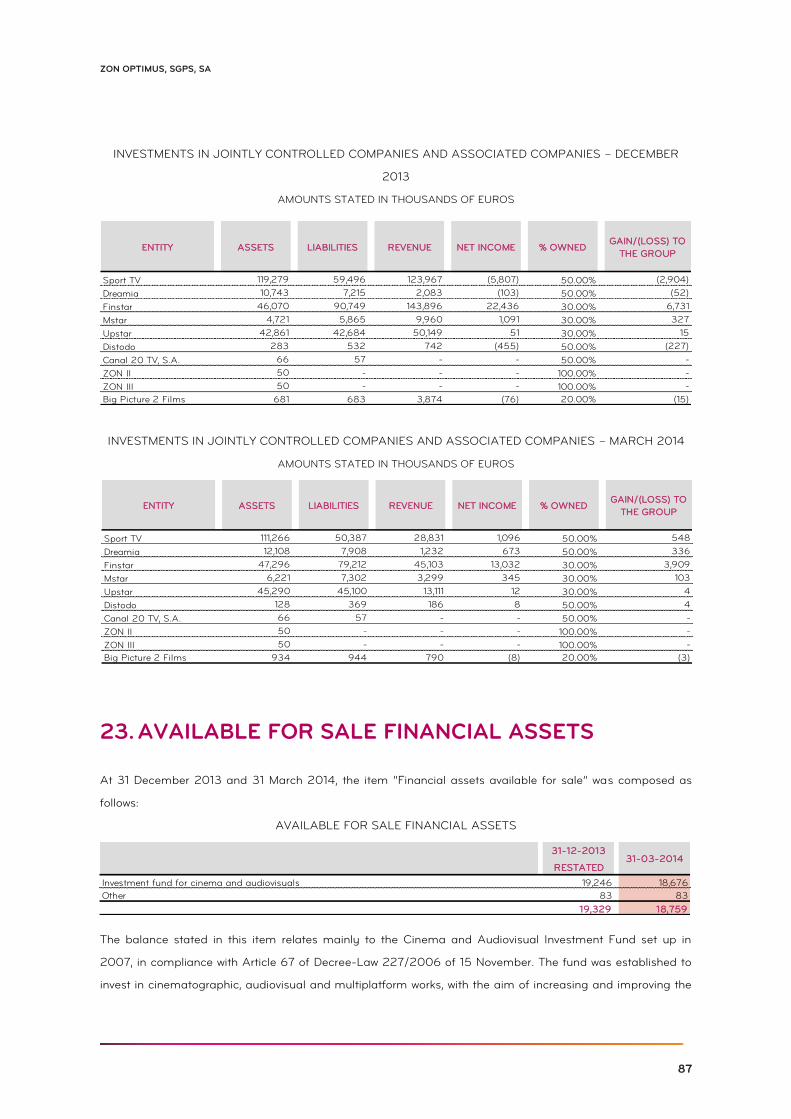

BUSINESS INDICATORS (Thousands)

RGUs: Convergent RGUs:

Mobile Subscribers: Pay TV:

Fixed Broadband: Fixed Voice:

7,295 7,241 7,254 7,213 7,215

1Q13 2Q13 3Q13 4Q13 1Q14

(1.1)%

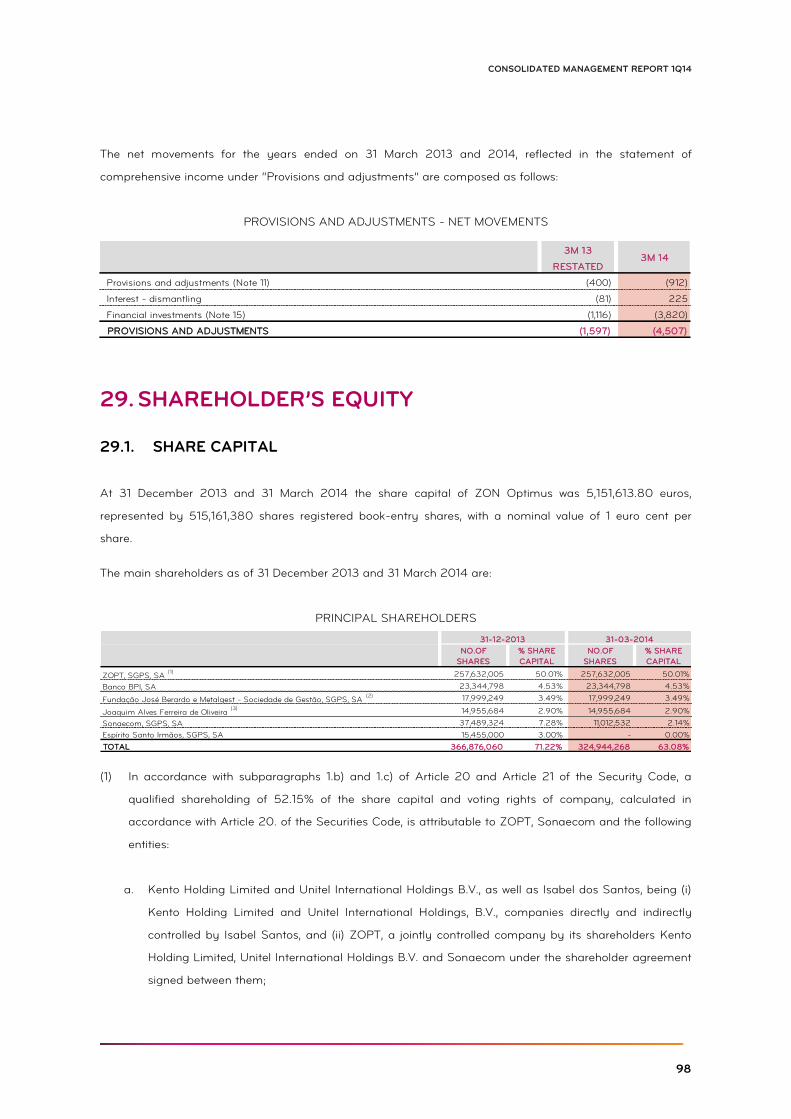

034

72

212

556

1Q13 2Q13 3Q13 4Q13 1Q14

3,261 3,204 3,238 3,243 3,288

1Q13 2Q13 3Q13 4Q13 1Q14

+0.8%

1,583 1,569 1,546 1,518 1,493

1Q13 2Q13 3Q13 4Q13 1Q14

(5.7)%

896 905 916 922 927

1Q13 2Q13 3Q13 4Q13 1Q14

+3.5%

1,543 1,549 1,539 1,515 1,491

1Q13 2Q13 3Q13 4Q13 1Q14

(3.3)%

5

ZON OPTIMUS, SGPS, SA

IRIS Subscribers: IRIS Subscribers as % of 3&4P:

3&4P Subscribers: % 3&4P Subscribers:

284339

390438

499

1Q13 2Q13 3Q13 4Q13 1Q14

+75.2%

35.6%42.0%

48.2%54.3%

61.7%

1Q13 2Q13 3Q13 4Q13 1Q14

+26.1pp

799 806 810 806 808

1Q13 2Q13 3Q13 4Q13 1Q14

+1.1%

64.6% 65.3% 66.4% 66.9% 68.0%

1Q13 2Q13 3Q13 4Q13 1Q14

+3.4pp

6

CONSOLIDATED MANAGEMENT REPORT 1Q14

FINANCIAL INDICATORS (Millions of Euros)

Operating Revenues: EBITDA and EBITDA Margin:

Net Income: CAPEX:

EBITDA – Recurrent CAPEX: Net Financial Debt:

351.9337.3

1Q13 1Q14

(4.1)%

138.0129.9

39.2%38.5%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100 %

0

20

40

60

80

100

120

140

160

1Q13 1Q14

(5.9)%

27.525.3

1Q13 1Q14

(8.2)%

58.6 52.7

2.03.9

60.556.7

1Q13 1Q14

Recurrent CAPEX Non Recurrent CAPEX

(6.4)%

79.4 77.1

1Q13 1Q14

(2.9)%

955.3923.4

600 .00

650 .00

700 .00

750 .00

800 .00

850 .00

900 .00

950 .00

100 0.00

1Q13 1Q14

(3.3)%

7

ZON OPTIMUS, SGPS, SA

2.

1Q14 HIGHLIGHTS

8

CONSOLIDATED MANAGEMENT REPORT 1Q14

FIRST QUARTER 2014 HIGHLIGHTS

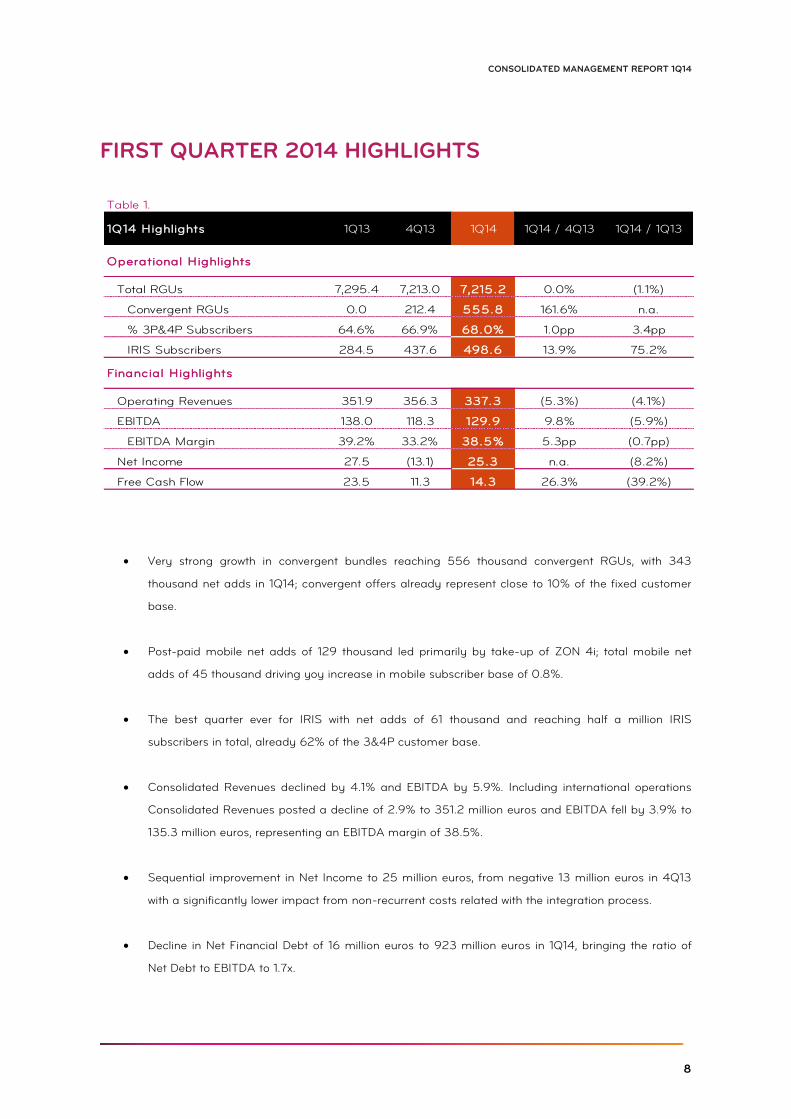

Very strong growth in convergent bundles reaching 556 thousand convergent RGUs, with 343

thousand net adds in 1Q14; convergent offers already represent close to 10% of the fixed customer

base.

Post-paid mobile net adds of 129 thousand led primarily by take-up of ZON 4i; total mobile net

adds of 45 thousand driving yoy increase in mobile subscriber base of 0.8%.

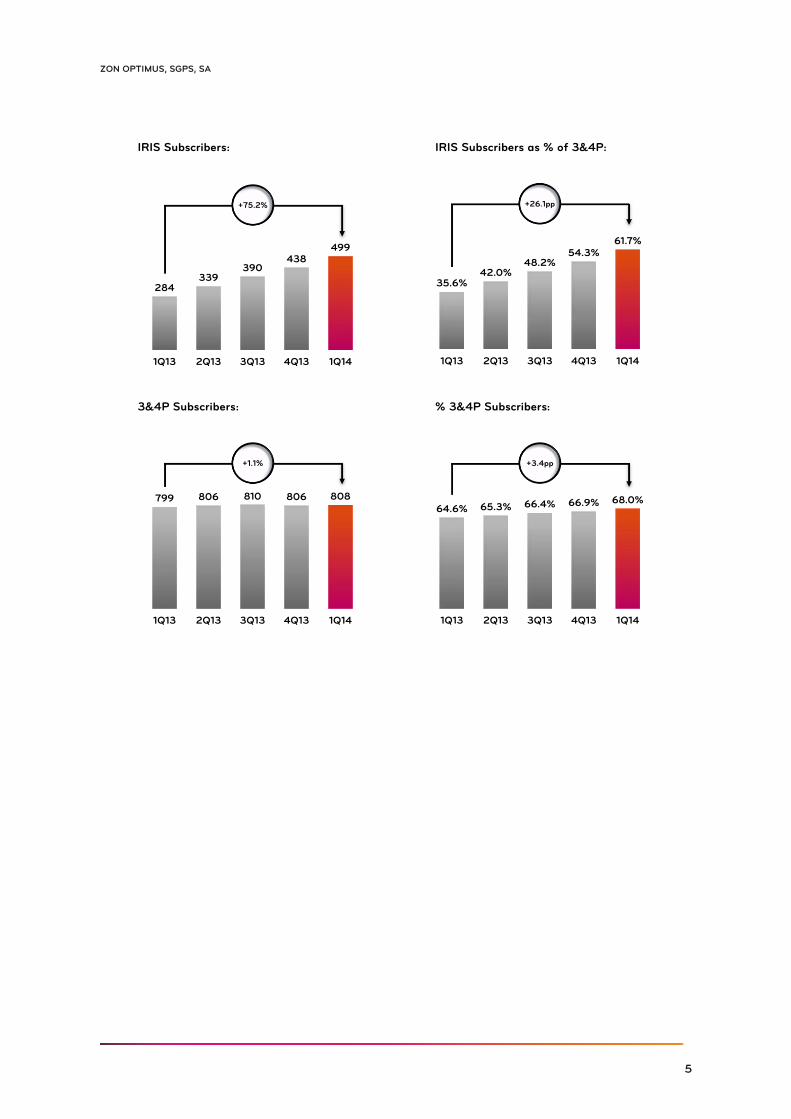

The best quarter ever for IRIS with net adds of 61 thousand and reaching half a million IRIS

subscribers in total, already 62% of the 3&4P customer base.

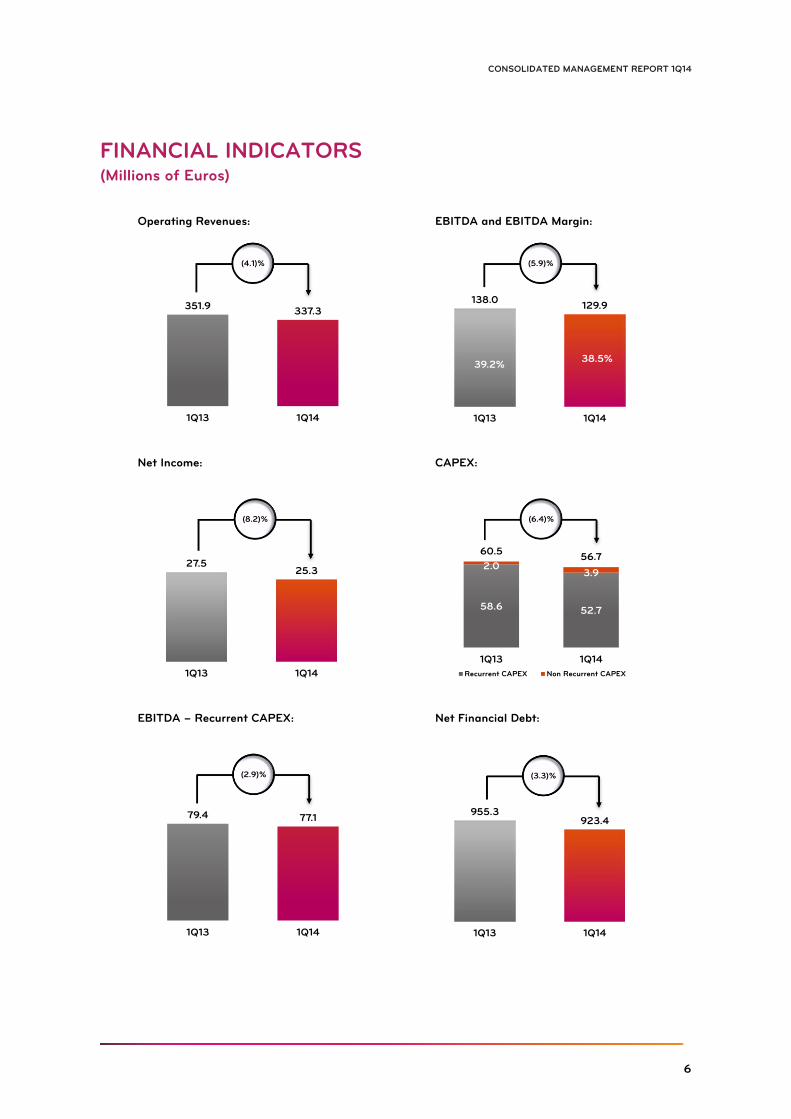

Consolidated Revenues declined by 4.1% and EBITDA by 5.9%. Including international operations

Consolidated Revenues posted a decline of 2.9% to 351.2 million euros and EBITDA fell by 3.9% to

135.3 million euros, representing an EBITDA margin of 38.5%.

Sequential improvement in Net Income to 25 million euros, from negative 13 million euros in 4Q13

with a significantly lower impact from non-recurrent costs related with the integration process.

Decline in Net Financial Debt of 16 million euros to 923 million euros in 1Q14, bringing the ratio of

Net Debt to EBITDA to 1.7x.

Table 1.

Operational Highlights

Total RGUs 7,295.4 7,213.0 7,215.2 0.0% (1.1%)

Convergent RGUs 0.0 212.4 555.8 161.6% n.a.

% 3P&4P Subscribers 64.6% 66.9% 68.0% 1.0pp 3.4pp

IRIS Subscribers 284.5 437.6 498.6 13.9% 75.2%

Financial Highlights

Operating Revenues 351.9 356.3 337.3 (5.3%) (4.1%)

EBITDA 138.0 118.3 129.9 9.8% (5.9%)

EBITDA Margin 39.2% 33.2% 38.5% 5.3pp (0.7pp)

Net Income 27.5 (13.1) 25.3 n.a. (8.2%)

Free Cash Flow 23.5 11.3 14.3 26.3% (39.2%)

1Q14 / 1Q131Q14 Highlights 1Q13 1Q144Q13 1Q14 / 4Q13

9

ZON OPTIMUS, SGPS, SA

3.

CORPORATE BODIES

10

CONSOLIDATED MANAGEMENT REPORT 1Q14

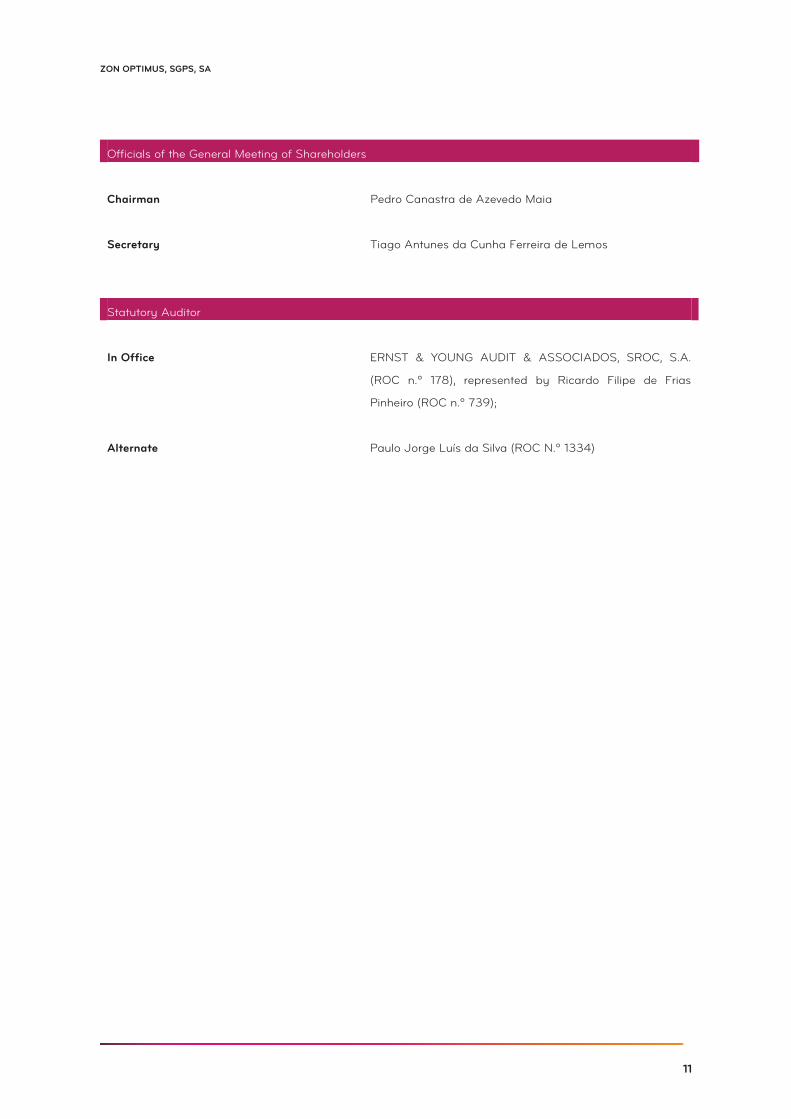

CORPORATE BODIES

As at the date of this report, 7 May 2014, the Governing Bodies of ZON had the following composition:

Board of Directors

Chairman of the Board of Directors Jorge de Brito Pereira

Chairman of the Executive Committee

Members of the Executive Committee

Miguel Almeida

José Pedro Pereira da Costa, Vice-Presidente, CFO

Miguel Veiga Martins, Vice-Presidente, CTO

Ana Paula Marques

André Almeida

Manuel Ramalho Eanes

Members Ângelo Paupério

António Lobo Xavier

António Domingues

Catarina Tavira

Cláudia Azevedo

Fernando Martorell

Isabel dos Santos

Joaquim de Oliveira

Lorena Fernandes

Mário Leite da Silva

Rodrigo Costa

Chairman of the Fiscal Board

Members

Alternate

Paulo Cardoso Correira da Mota Pinto

Eugénio Ferreira

Nuno Sousa Pereira

Luís Filipe da Silva Ferreira

11

ZON OPTIMUS, SGPS, SA

Officials of the General Meeting of Shareholders

Chairman Pedro Canastra de Azevedo Maia

Secretary Tiago Antunes da Cunha Ferreira de Lemos

Statutory Auditor

In Office ERNST & YOUNG AUDIT & ASSOCIADOS, SROC, S.A.

(ROC n.º 178), represented by Ricardo Filipe de Frias

Pinheiro (ROC n.º 739);

Alternate Paulo Jorge Luís da Silva (ROC N.º 1334)

12

CONSOLIDATED MANAGEMENT REPORT 1Q14

4.

MANAGEMENT REPORT

13

ZON OPTIMUS, SGPS, SA

MANAGEMENT REPORT BUSINESS REVIEW

1Q14 Consolidated Results

The integration process is now well underway, with teams focused on ramping up commercial deployment

and restructuring operations in the new, merged entity. We are still in the early months of our strategy

execution and the full benefit of many of the projects underway should only be expected in the medium term,

as detailed in our strategy disclosure to the market last February.

Very strong take up of convergent bundles

The core priority of ZON OPTIMUS’ strategy is to reinforce competitive position through domestic market

share growth with convergence being a strong driver of market dynamics over coming years. ZON OPTIMUS’

unique set of assets provides a strong platform to leverage growth in market share across both the consumer

and enterprise markets.

Consumer appetite for convergent mobile and fixed bundles is clearly very strong. Since launch in mid 4Q13

of ZON4i, ZON OPTIMUS has been witnessing consistently stronger month on month growth in convergent

subscribers.

By the end of 1Q14, ZON OPTIMUS had 556 thousand RGUs within convergent bundles, representing an

average pace of growth of over 20 thousand new households per month, and subscribing to an average of 5

RGUs per account. Of the convergent mobile RGUs, just 12% were previous ZON OPTIMUS customers and

the balance are coming either from other operators or are new mobile numbers, therefore driving relevant net

growth in the total mobile subscriber base. The main anchor of convergent offers is Pay TV, with 90% of

ZON4i customers upgrading from existing ZON offers and with just 54% being previous IRIS customers. The

promotion of ZON 4i is therefore driving not only an increase in penetration of new mobile RGUs but also a

strong take-up of the more sophisticated, premium IRIS interface. As such, ZON OPTIMUS’ strong position in

the Pay TV market, with 48% market share at the end of 2013, is an extremely strong platform to grow in

mobile RGUs.

As a percentage of the fixed customer base, only 5 months after launch of ZON4i, convergent bundles

represent close to 10%. Enthusiasm for these fixed mobile bundles is justified by their very attractive value

proposition. ZON4i combines more and better television programming with 116 channels; fixed Internet which

gives the highest speeds and most extensive coverage with 100 Mbps to all 3.3 million households covered by

ZON OPTIMUS’ next generation HFC network; an unlimited national and international fixed voice service

14

CONSOLIDATED MANAGEMENT REPORT 1Q14

which also includes free use of the ZON Phone app enabling use of a landline number on mobile devices,

benefiting from normal landline tariffs and integrated billing; free access to the largest network of WiFi

hotspots giving instant access to 600 thousand hotspots in Portugal and over 12 million worldwide; unlimited

mobile phone use, offering the best 4G solutions available, for up to four users, mobile Internet with free 200

MB per SIM card which accommodates a flexible top-up facility for those who occasionally go over their data

limit; priority access to the largest network of cinemas in Portugal, through myZONcard, that also gives one

free ticket for every cinema ticket purchased. ZON4i is priced at €79.99 with two mobile users, and can be

adjusted to suit usage profile and requirements.

Already a result of the reinforced competitive strengths created by the merger, at the beginning of 2Q14,

ZON OPTIMUS launched a convergent offer for DTH coverage geographies based on 4G solutions for

broadband and voice, thus mirroring the bundled value proposition provided over the HFC footprint. For the

same prices as HFC based offers, customers can subscribe to 3 and 4 Play bundles including 81 TV

channels, up to 40 Mbps of Internet, unlimited fixed and mobile voice including 2 mobile SIM cards.

Another record quarter for IRIS reaching half a million subscribers

A key lever to reinforce our leadership in Pay TV is our next generation, multi-screen TV offer, IRIS, which is

the default TV offer for all new triple and quad play packages. This was another record quarter for IRIS with

net adds of 61 thousand taking the total number of IRIS subscribers to half a million and already representing

62% of the 3&4P customer base, up from 36% in 1Q13.

Levels of satisfaction and customer experience with IRIS are extremely high, with usage of the leading edge,

cloud based functionalities completely transforming the way people watch TV. 99% of IRIS customers have

used Timewarp and Restart TV and over 75% use them every day, at least twice.

IRIS is the centrepiece of our product strategy, with continuous releases and upgrades always exceeding user

expectations. The focus for 2014 is on extension and interconnection of the TV experience with the mobile

ecosystem, redoubling efforts in research and development in order to continue to respond to the challenges

of the Pay TV market and exploiting the opportunity presented by ZON OPTIMUS’ strong position as a fixed

and mobile player. The importance and success of our TV interface is core to our strategy to lead the market

in convergence given that choice of operator is anchored on the Pay TV provider.

At the beginning of 2014 the IRIS set-top box software underwent a major update, which brought about

significant improvements in performance and usage, as well as a new HTML5 browser that will allow the

development of a new generation of TV applications, including YouTube Leanback. The improvements include

adjustment of the Fast Forward and Rewind speeds in video streaming, which is particularly relevant for the

Restart and Timewarp functions.

15

ZON OPTIMUS, SGPS, SA

We recently launched our Network-DVR which enables customers to record, pause live TV and rewind live

content, fully replicating the experience of a local recorder with the additional advantage of allowing for

unlimited simultaneous recording of programmes and sharing of recorded content over all STBs in the

household. With this development ZON OPTIMUS has become the first Pay TV operator to initiate the

commercial fade-out of DVR centric STBs, generating in the process a much superior user experience.

IRIS has accumulated a number of awards as the best TV interface with widespread recognition from

customers and industry peers. IRIS was voted “Product of the Year” in Portugal for the second consecutive

year and IRIS’ OTT apps were also recognized internationally having won the “Best TV on the Move Service”

award at London’s TV Connect conference.

Strong pick-up in mobile net-adds driving yoy growth in subscriber base

The growth of convergent bundles is driving an important structural shift in mobile customers with more and

more users subscribing to post-paid mobile SIM cards within 4P bundled offers. This trend has been

accelerating for ZON OPTIMUS every month since launch of ZON4i at the end of 2013.

In 1Q14, post-paid mobile subscribers grew by 129 thousand, one of the strongest quarters of the past years.

The growth recorded in post-paid voice subscribers was even more significant with net adds of 147 thousand

however this was somewhat offset by a net decline in post-paid mobile broadband cards of 18 thousand. In

terms of the pre-paid mobile base, net-adds were negative by 84 thousand, impacted by the growing shift

towards convergent offers, however the balance is clearly very positive for ZON OPTIMUS with total net adds

in mobile of 45 thousand.

In the stand-alone mobile segment, marketing efforts remain focused on driving all-net tariffs that provide

easy and unlimited plans without any kind of network restrictions. The two main families of all-net tariffs are

SMART and LIGA, both launched during 2013. SMART is directed at the high-end segment of the market as

a post-paid plan that enables customers to communicate to all networks with an almost unlimited monthly

allowance and without the hassle of having to remember to top-up. All SMART tariffs include at least 1 Gb of

data, providing an excellent 3G and 4G experience. LIGA addresses the need to provide more affordable all-

net access to more segments of the market at a very appealing 9.99 euros / month price point. This offer

has led to a significant increase in the proportion of pre-paid customers with a fixed monthly recharge.

Another lever for growth in personal mobile communication is the push for increased smartphone penetration,

which is currently well below European average at around 25% nationwide. OPTIMUS has a relevant lead

versus its main competitors in terms of 4G network coverage and in order to exploit this advantage and

stimulate mobile data usage, has launched a number of very attractive smartphones incorporated in

competitive post-paid mobile tariff plans. We are actively exploring opportunities to reduce the cost and

16

CONSOLIDATED MANAGEMENT REPORT 1Q14

consequent retail prices for equipment and recently launched a 4G enabled own branded smartphone for

€99.90, “OPTIMUS ZILO”. Importantly, OPTIMUS already posts a significantly higher share of mobile data

traffic when compared to its total share of mobile traffic, 42% of mobile data traffic versus 13% in total.

Over 1 million RGUs in the Enterprise segment

By the end of 1Q14, ZON OPTIMUS had over 1 million RGUs in the business segment reflecting a relevant

pick-up in quarterly net adds to 23.2 thousand. The majority of the growth was in mobile, with net adds of

18.6 thousand in the quarter, driven by convergence. In the SME and SoHo segments in particular, ramp up

of sales channels is now underway, enabling further deployment of cross-sales within the existing footprint of

ZON and OPTIMUS’ customer bases. In the small business segment, timing of revenue growth is still set to

lag volume growth given that the market-wide trend towards convergent offers, initiated at the beginning of

2013, is leading to some repricing of the base. Although representing near term pressure on revenues,

increased RGU volume of convergent SME and SOHO customers will help offset that loss in the medium term

given that ZON OPTIMUS’ net growth will come primarily from new RGUs to the company.

On the Corporate front, the team has been very successful in addressing important new accounts with a

number of important contracts coming to the market for tender in the coming months. ZON OPTIMUS has

already won a number of relevant flagship accounts across many sectors of the market however set-up and

migration of new corporate accounts is a time demanding process and therefore revenues will take at least a

couple of quarters to start showing a material impact. ZON OPTIMUS now stands stronger as a

technologically superior and fully integrated fixed and mobile operator, capable of offering relevant and

competitive integrated and convergent telecommunications and data services for the enterprise segments in

Portugal. The deep coverage, capillarity and high capacity of ZON OPTIMUS’ network are core differentiating

factors for this segment. ZON OPTIMUS is already addressing the market as a single entity, capable of

providing tailor made solutions for the largest corporate and public sector customers, and reaching out to

SME and SoHo companies with specific solutions adapted to usage profile and geographic spread, leveraging

the best national NGN Fixed and Mobile footprint.

17

ZON OPTIMUS, SGPS, SA

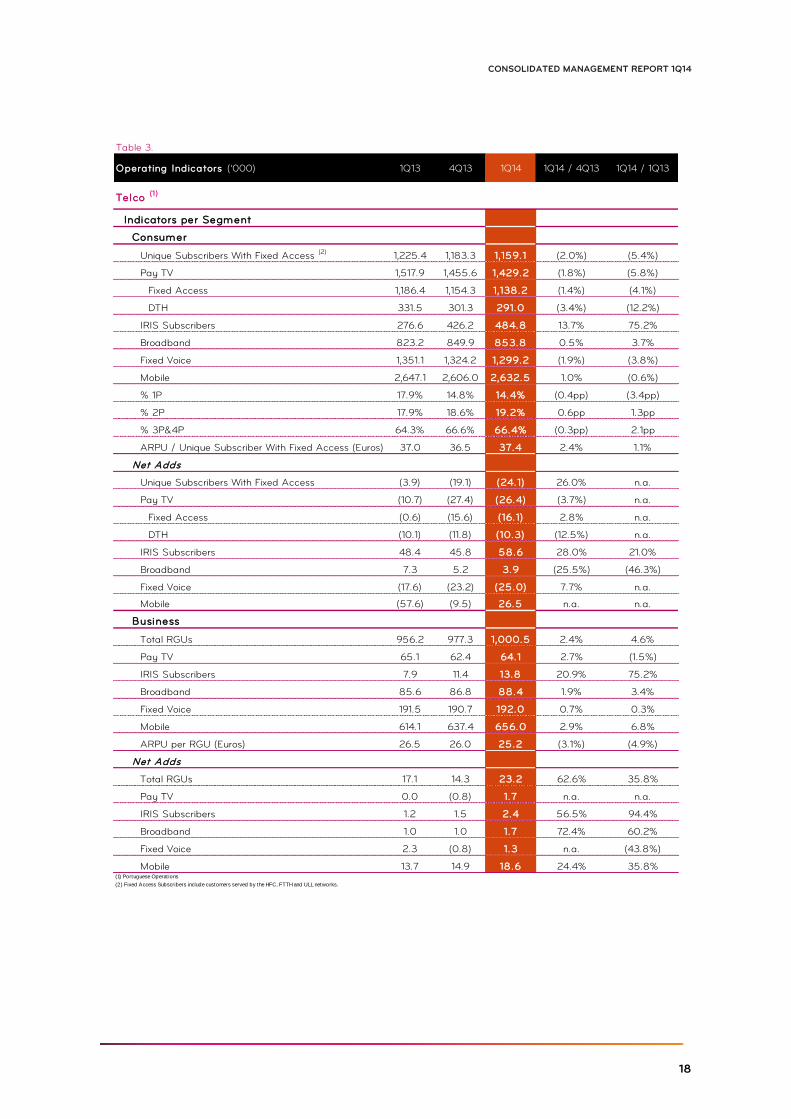

Table 2.

Telco (1 )

Aggregate Indicators

Homes Passed 3,199.7 3,241.8 3,255.5 0.4% 1.7%

Total RGUs 7,295.4 7,213.0 7,215.2 0.0% (1.1%)

Mobile 3,261.1 3,243.4 3,288.4 1.4% 0.8%

Pre-Paid 2,356.1 2,251.0 2,166.9 (3.7%) (8.0%)

Post-Paid 905.1 992.4 1,121.6 13.0% 23.9%

ARPU / Mobile Subscriber (Euros) 9.6 9.2 9.2 (0.7%) (4.7%)

Pay TV 1,583.0 1,518.0 1,493.3 (1.6%) (5.7%)

Fixed Access (2) 1,237.4 1,203.8 1,189.4 (1.2%) (3.9%)

DTH 345.6 314.2 303.9 (3.3%) (12.1%)

Fixed Voice 1,542.6 1,514.9 1,491.3 (1.6%) (3.3%)

Broadband 895.6 922.1 927.0 0.5% 3.5%

Others and Data 13.2 14.6 15.2 4.6% 15.6%

3P&4P Subscribers 799.5 805.9 808.4 0.3% 1.1%

% 3P&4P 64.6% 66.9% 68.0% 1.0pp 3.4pp

Convergent RGUs 0.0 212.4 555.8 161.6% n.a.

IRIS Subscribers 284.5 437.6 498.6 13.9% 75.2%

IRIS as % of 3P&4P Subscribers 35.6% 54.3% 61.7% 7.4pp 26.1pp

Net Adds

Homes Passed 14.1 13.3 13.7 2.6% (3.1%)

Total RGUs (61.5) (40.6) 2.2 n.a. n.a.

Mobile (43.9) 5.4 45.0 n.a. n.a.

Pre-Paid (52.3) (53.0) (84.1) 58.8% 60.7%

Post-Paid 8.4 58.4 129.2 121.1% n.a.

Pay TV (10.7) (28.2) (24.7) (12.3%) 131.6%

Fixed Access (2) (0.1) (16.0) (14.4) (9.6%) n.a.

DTH (10.5) (12.2) (10.3) (15.8%) (2.3%)

Fixed Voice (15.2) (24.0) (23.7) (1.5%) 55.7%

Broadband 7.8 5.8 4.9 (15.8%) (37.2%)

Others and Data 0.5 0.4 0.7 75.1% 33.1%

3P&4P Subscribers 8.3 (4.1) 2.5 n.a. (69.7%)

Convergent RGUs 0.0 140.9 343.4 143.7% n.a.

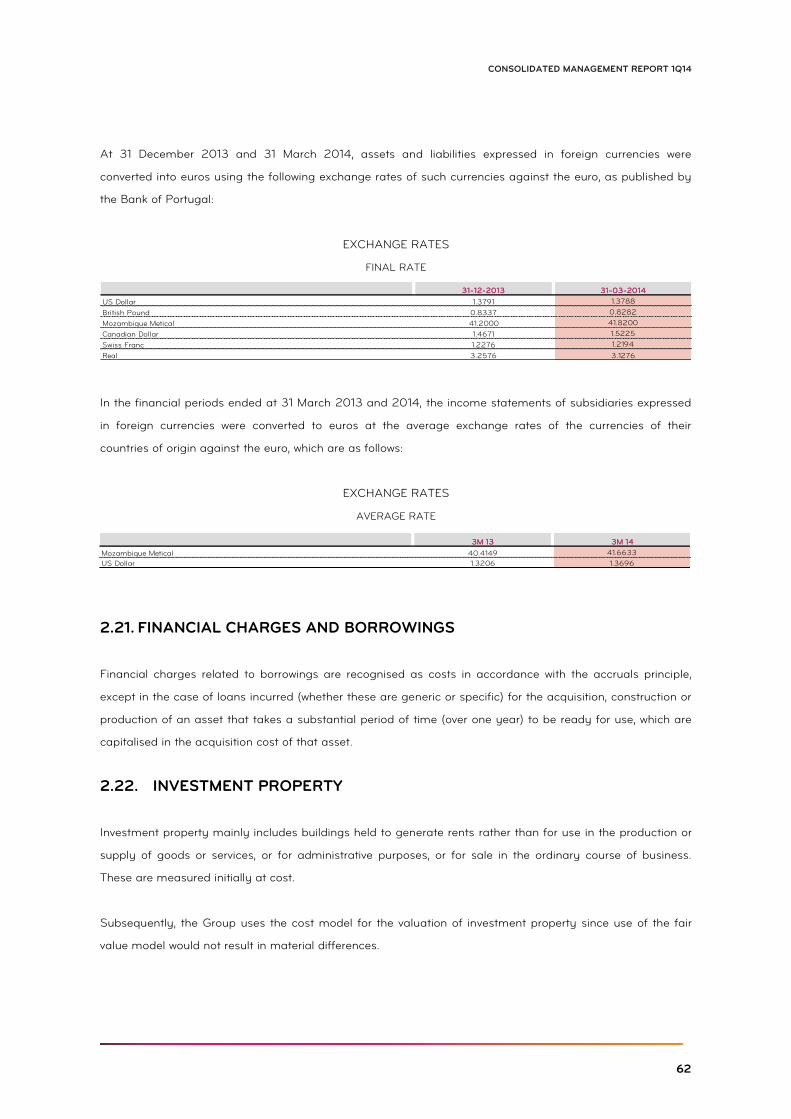

IRIS Subscribers 49.7 47.3 61.0 28.9% 22.8%(1) Portuguese Operat ions

1Q14 / 4Q131Q13

(2) Fixed Access Subscribers include customers served by the HFC, FTTH and ULL networks.

1Q14 1Q14 / 1Q13Operating Indicators ('000) 4Q13

18

CONSOLIDATED MANAGEMENT REPORT 1Q14

Table 3.

Telco (1)

Indicators per Segment

Consumer

Unique Subscribers With Fixed Access (2) 1,225.4 1,183.3 1,159.1 (2.0%) (5.4%)

Pay TV 1,517.9 1,455.6 1,429.2 (1.8%) (5.8%)

Fixed Access 1,186.4 1,154.3 1,138.2 (1.4%) (4.1%)

DTH 331.5 301.3 291.0 (3.4%) (12.2%)

IRIS Subscribers 276.6 426.2 484.8 13.7% 75.2%

Broadband 823.2 849.9 853.8 0.5% 3.7%

Fixed Voice 1,351.1 1,324.2 1,299.2 (1.9%) (3.8%)

Mobile 2,647.1 2,606.0 2,632.5 1.0% (0.6%)

% 1P 17.9% 14.8% 14.4% (0.4pp) (3.4pp)

% 2P 17.9% 18.6% 19.2% 0.6pp 1.3pp

% 3P&4P 64.3% 66.6% 66.4% (0.3pp) 2.1pp

ARPU / Unique Subscriber With Fixed Access (Euros) 37.0 36.5 37.4 2.4% 1.1%

Net Adds

Unique Subscribers With Fixed Access (3.9) (19.1) (24.1) 26.0% n.a.

Pay TV (10.7) (27.4) (26.4) (3.7%) n.a.

Fixed Access (0.6) (15.6) (16.1) 2.8% n.a.

DTH (10.1) (11.8) (10.3) (12.5%) n.a.

IRIS Subscribers 48.4 45.8 58.6 28.0% 21.0%

Broadband 7.3 5.2 3.9 (25.5%) (46.3%)

Fixed Voice (17.6) (23.2) (25.0) 7.7% n.a.

Mobile (57.6) (9.5) 26.5 n.a. n.a.

Business

Total RGUs 956.2 977.3 1,000.5 2.4% 4.6%

Pay TV 65.1 62.4 64.1 2.7% (1.5%)

IRIS Subscribers 7.9 11.4 13.8 20.9% 75.2%

Broadband 85.6 86.8 88.4 1.9% 3.4%

Fixed Voice 191.5 190.7 192.0 0.7% 0.3%

Mobile 614.1 637.4 656.0 2.9% 6.8%

ARPU per RGU (Euros) 26.5 26.0 25.2 (3.1%) (4.9%)

Net Adds

Total RGUs 17.1 14.3 23.2 62.6% 35.8%

Pay TV 0.0 (0.8) 1.7 n.a. n.a.

IRIS Subscribers 1.2 1.5 2.4 56.5% 94.4%

Broadband 1.0 1.0 1.7 72.4% 60.2%

Fixed Voice 2.3 (0.8) 1.3 n.a. (43.8%)

Mobile 13.7 14.9 18.6 24.4% 35.8%(1) Portuguese Operat ions

(2) Fixed Access Subscribers include customers served by the HFC, FTTH and ULL networks.

Operating Indicators ('000) 1Q13 1Q14 1Q14 / 1Q134Q13 1Q14 / 4Q13

19

ZON OPTIMUS, SGPS, SA

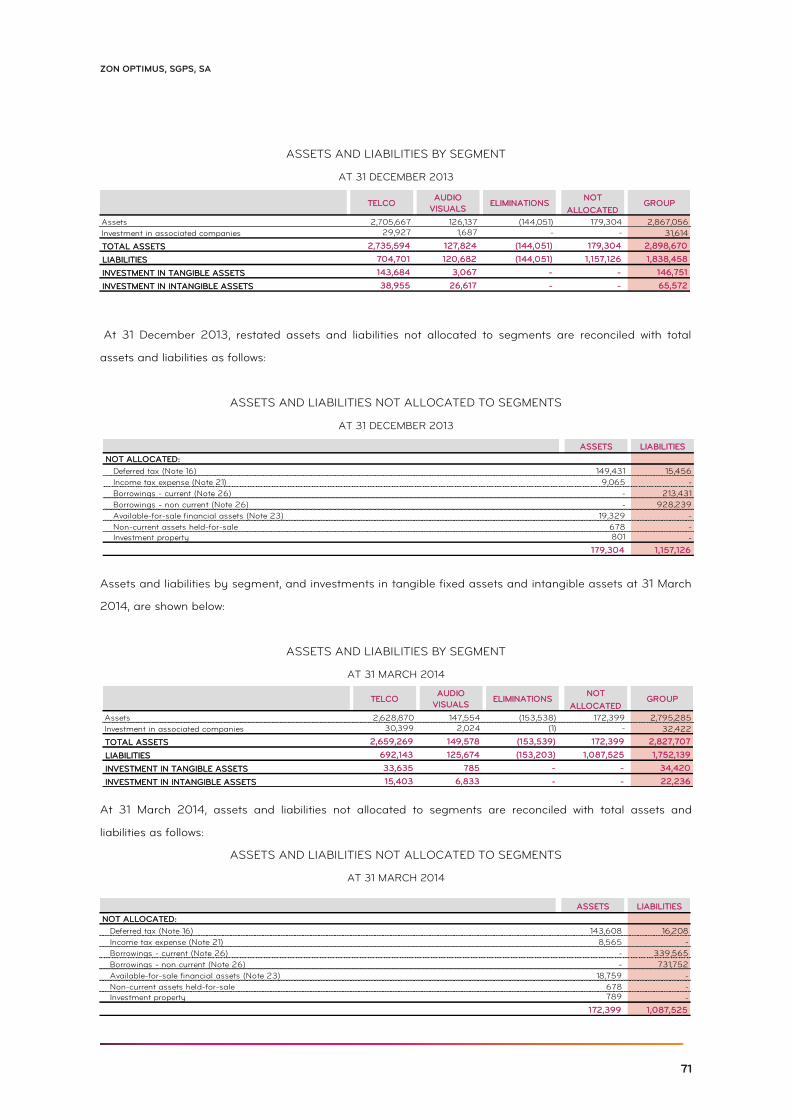

Continued impact of remedies on fixed access base

Fixed access Pay TV customers posted a decline of 14 thousand in 1Q14, still suffering the impact of

remedies imposed by the Competition Authority whereby, upon approval of the merger, ZON OPTIMUS was

forced to release OPTIMUS FTTH subscribers of their loyalty contracts and restricted from addressing them

with commercial offers, providing a relevant opportunity for competitors to target these customers. As a result

of these regulatory constraints, of the 38 thousand OPTIMUS FTTH customers that existed before the

merger, a significant number churned to competitors. ULL fixed access customers are progressively being

migrated onto own HFC infrastructure however, in some situations, they are outside current network footprint

and therefore churn levels in this customer base are higher than normal. Fixed Voice and Broadband

customers were equally impacted by the above mentioned one-off effects.

The DTH Pay TV base fell by 10.3 thousand subscribers in 1Q14, along the same levels as in the previous

quarters. The launch of 3P and 4P offers for the DTH market as from 2Q14 should help to reduce the relative

network disadvantage that ZON OPTIMUS has in areas where it competes against a fixed infrastructure.

Support in Fixed residential ARPU led by increase of convergent penetration

ARPU per unique subscriber with fixed access posted a marginal increase of 1.1% with increased penetration

of convergent offers that generated higher average revenues and the continued upsell of IRIS bundles

offsetting some of the market driven pricing pressure.

Mobile ARPU recorded a 4.7% yoy decline to 9.2 euros however remained flat in comparison with 4Q13,

showing that the substantial growth in convergent post paid contract customers is helping to mitigate the

underlying revenue pressure felt in stand-alone mobile consumption.

On the business front, ARPU per RGU also posted a decline in 1Q14 of 4.9% to 25.2 euros, a reflection

primarily of the repricing of the SME and SOHO customer base due to the increased shift to convergent

solutions, as explained above.

20

CONSOLIDATED MANAGEMENT REPORT 1Q14

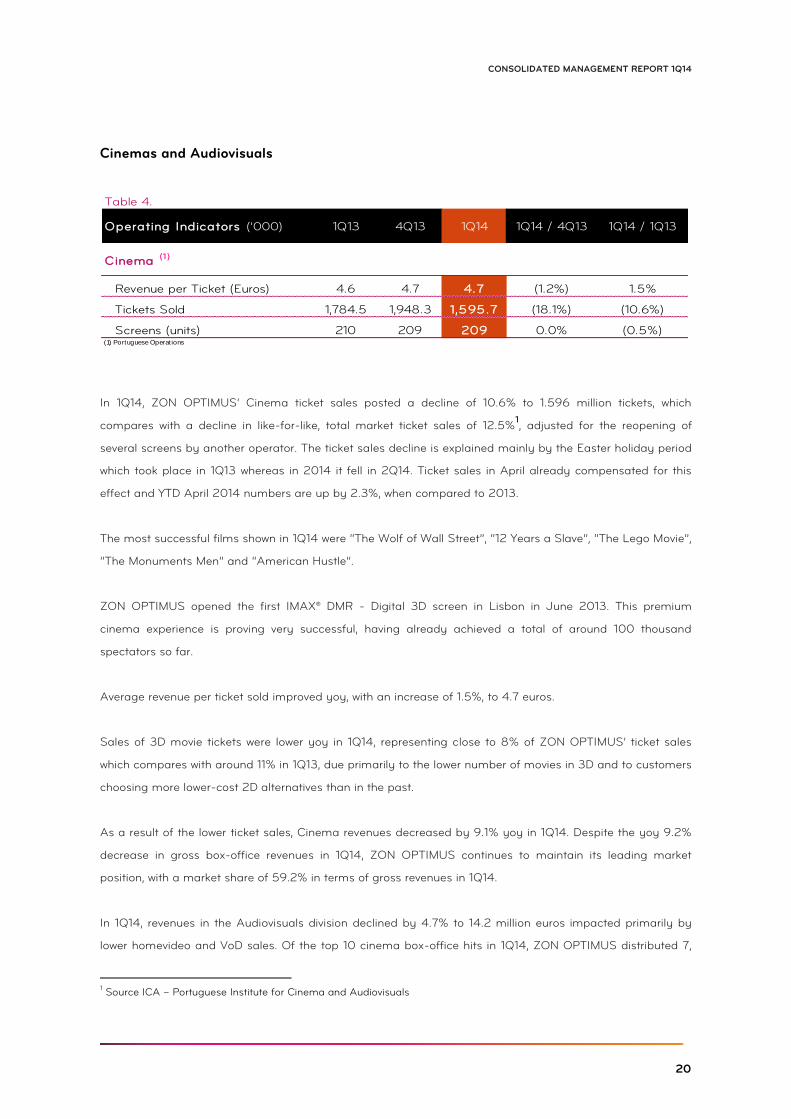

Cinemas and Audiovisuals

In 1Q14, ZON OPTIMUS’ Cinema ticket sales posted a decline of 10.6% to 1.596 million tickets, which

compares with a decline in like-for-like, total market ticket sales of 12.5%1, adjusted for the reopening of

several screens by another operator. The ticket sales decline is explained mainly by the Easter holiday period

which took place in 1Q13 whereas in 2014 it fell in 2Q14. Ticket sales in April already compensated for this

effect and YTD April 2014 numbers are up by 2.3%, when compared to 2013.

The most successful films shown in 1Q14 were “The Wolf of Wall Street”, “12 Years a Slave”, “The Lego Movie”,

“The Monuments Men” and “American Hustle”.

ZON OPTIMUS opened the first IMAX® DMR - Digital 3D screen in Lisbon in June 2013. This premium

cinema experience is proving very successful, having already achieved a total of around 100 thousand

spectators so far.

Average revenue per ticket sold improved yoy, with an increase of 1.5%, to 4.7 euros.

Sales of 3D movie tickets were lower yoy in 1Q14, representing close to 8% of ZON OPTIMUS’ ticket sales

which compares with around 11% in 1Q13, due primarily to the lower number of movies in 3D and to customers

choosing more lower-cost 2D alternatives than in the past.

As a result of the lower ticket sales, Cinema revenues decreased by 9.1% yoy in 1Q14. Despite the yoy 9.2%

decrease in gross box-office revenues in 1Q14, ZON OPTIMUS continues to maintain its leading market

position, with a market share of 59.2% in terms of gross revenues in 1Q14.

In 1Q14, revenues in the Audiovisuals division declined by 4.7% to 14.2 million euros impacted primarily by

lower homevideo and VoD sales. Of the top 10 cinema box-office hits in 1Q14, ZON OPTIMUS distributed 7,

1 Source ICA – Portuguese Institute for Cinema and Audiovisuals

Table 4.

Cinema (1 )

Revenue per Ticket (Euros) 4.6 4.7 4.7 (1.2%) 1.5%

Tickets Sold 1,784.5 1,948.3 1,595.7 (18.1%) (10.6%)

Screens (units) 210 209 209 0.0% (0.5%)(1) Portuguese Operat ions

Operating Indicators ('000) 1Q13 1Q14 1Q14 / 1Q134Q13 1Q14 / 4Q13

21

ZON OPTIMUS, SGPS, SA

“The Wolf of Wall Street”, “12 Years a Slave”, “American Hustle”, “Frozen”, “Robocop”, “47 Ronin” and

“August: Osage County”, maintaining its strong leading position with a 68.2% market share in terms of gross

revenues, having outperformed the market with yoy growth of 16.1%, which compares with a decline of 5.2%

of the market as a whole.

Already in 2014, the Audiovisuals division signed a contract for theatrical distribution of the Warner catalogue

for Portugal, with effect on 1 April, 2014, from which some relevant contribution is therefore expected for the

remainder of 2014.

ZAP

ZAP continues its success story in the Angolan and Mozambican Pay-TV markets and it is today a reference

operator in these countries, in Africa and in the industry. As a local operator, ZAP is focused on increasing its

presence in these territories and it is, therefore, still expanding its sales channels, namely its own stores that

are now 28 in Angola and 7 in Mozambique. Last additions were Soyo (Zaire province) and Dundo (Lunda

Norte) in Angola and Beira and Nampula in Mozambique. Other sales channels are also still expanding and

becoming more effective.

ZAP continues to improve its products and services in order to meet the highest expectations from its

customers and differentiate from competition in these countries. During this quarter ZAP added two new

channels to its packages, STV Notícias (a Mozambican news channel produced by STV, one of the free-to-air

broadcasters in Mozambique) and Cubavision.

22

CONSOLIDATED MANAGEMENT REPORT 1Q14

CONSOLIDATED FINANCIAL REVIEW

The following Consolidated Financial Statements have been subject to limited review. As standard practice,

only the annual accounts are audited; the quarterly results are not audited separately.

Consolidated Income Statement

Table 5.

Operating Revenues 351.9 356.3 337.3 (5.3%) (4.1%)

Telco 336.6 337.3 323.5 (4.1%) (3.9%)

Consumer Revenues 221.9 209.9 207.5 (1.1%) (6.5%)

Business Revenues 94.0 98.1 96.2 (1.9%) 2.4%

Equipment Sales 6.2 11.5 8.2 (28.8%) 30.8%

Others and Eliminations 14.5 17.8 11.6 (34.8%) (19.6%)

Audiovisuals 14.9 17.4 14.2 (18.5%) (4.7%)

Cinema (1) 11.8 13.2 10.7 (19.0%) (9.1%)

Others and Eliminations (11.4) (11.6) (11.0) (5.0%) (2.7%)

Operating Costs Excluding D&A (213.8) (238.0) (207.5) (12.8%) (3.0%)

W&S (23.3) (25.2) (21.0) (16.4%) (9.5%)

Direct Costs (97.7) (105.0) (96.7) (7.9%) (1.0%)

Commercial Costs (2) (19.3) (33.2) (22.7) (31.6%) 17.6%

Other Operating Costs (73.6) (74.6) (67.0) (10.2%) (9.0%)

EBITDA 138.0 118.3 129.9 9.8% (5.9%)

EBITDA Margin 39.2% 33.2% 38.5% 5.3pp (0.7pp)

Telco 131.1 107.4 120.4 12.1% (8.1%)

EBITDA Margin 38.9% 31.8% 37.2% 5.4pp (1.7pp)

Cinema Exhibition and Audiovisuals 7.0 10.9 9.5 (12.8%) 36.3%

EBITDA Margin 28.6% 39.3% 42.4% 3.1pp 13.8pp

Share of results of associates and joint ventures 1.3 1.5 4.9 218.2% 277.5%

EBITDA including results of associates and joint ventures 139.3 119.8 134.8 12.5% (3.3%)

Depreciation and Amortization (87.1) (83.6) (83.9) 0.3% (3.7%)

(Other Expenses) / Income (0.3) (26.8) (2.8) (89.4%) n.a.

Operating Profit (EBIT) (3) 52.0 9.4 48.1 n.a. (7.5%)

(Financial Expenses) / Income (16.7) (13.5) (15.2) 12.1% (9.1%)

Income Before Income Taxes 35.3 (4.1) 32.9 n.a. (6.8%)

Income Taxes (7.6) (9.1) (7.3) (19.5%) (3.2%)

Income From Continued Operations 27.7 (13.2) 25.6 n.a. (7.8%)

o.w. Attributable to Non-Controlling Interests (0.2) 0.1 (0.3) n.a. 50.6%

Net Income 27.5 (13.1) 25.3 n.a. (8.2%)(1) Includes operat ions in M ozambique.

(2) Commercial costs include commissions, market ing and publicity expenses and costs of equipment sold.

(3) EBIT = Income Before Financials and Income Taxes.

4Q13 1Q14 / 4Q13

* The merger by incorporat ion of OPTIM US into ZON that led to the creat ion of ZON OPTIM US was completed on 27 August 2013. Result ing primarily from the merger, in 3Q13 a number of account ing policies, pract ices and

est imates have had to be aligned. The primary changes to account ing policies, with the correspondent restatement of the prior period accounts were the capitalizat ion of customer acquisit ion costs at ZON in order to align with

OPTIMUS’ policy also followed by other telecom operators and capitalizat ion of certain movie rights in the audiovisuals division following IAS 38, which were restated since 1Q12 in the statutory accounts. In addit ion and in

ant icipat ion of the mandatory implementat ion of IFRS 11as from 1Q14, whereby joint ventures may no longer be consolidated proport ionately, ZON OPTIM US has proceeded to deconsolidate the three joint ventures in which it

holds stakes, ZAP (30%), Sport TV (50%) and Dreamia (50%) and has restated prior period f inancial statements to ref lect their recognit ion through the equity method. To facilitate comparison between current and prior period

results for the new ZON OPTIM US, the current pro-forma consolidated f inancial statements have been prepared, ref lect ing not only the statutory accounts restatement due to the changes to account ing policies, but also the

consolidat ion of 12 months of OPTIMUS’ results in 2013 (3 months in 1Q13). The f inancial statements ref lect the impact, since September 2013, in depreciat ion and amort izat ion of the provisional calculat ion of the fair value of

OPTIMUS’ assets and liabilit ies which was used for the purposes of purchase price allocat ion result ing from the consolidat ion of OPTIM US. The present f inancial review is based on these pro-forma financial statements. Appendix

III to this report includes the statutory income statement for ZON OPTIM US.

1Q14 / 1Q13Pro-Forma Profit and Loss Statement *

(Millions of Euros)1Q13 1Q14

23

ZON OPTIMUS, SGPS, SA

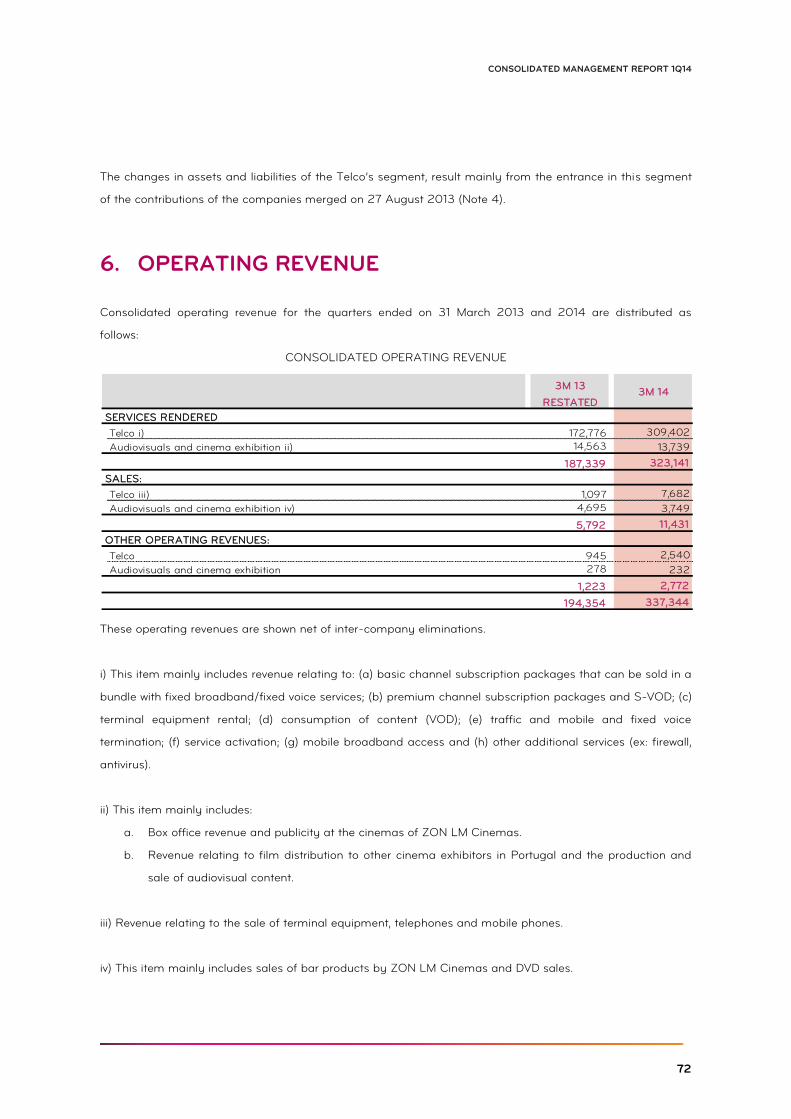

Operating Revenues

Consolidated Operating Revenues were 337.3 million euros in 1Q14, representing a decline of 4.1% in

comparison with 1Q13. Adding back the contribution from the 30% stake in ZAP, Consolidated Revenues

posted a decline of 2.9% to 351.2 million euros.

Combined Revenues for the Telco business declined by 3.9% to 323.5 million euros, albeit posting a

marginal sequential recovery in yoy growth in comparison with 4Q13.

Consumer Revenues, down by 6.5% yoy, were primarily impacted by negative yoy growth in personal mobile

revenues due to lower average subscriber numbers yoy, led by the market wide trend towards convergent

offers and a reduction in mobile ARPU and by continued decline in revenues from the DTH business. The

trend in fixed residential revenues was significantly more positive benefitting from the above mentioned

growth in convergent RGUs and cross-selling initiatives together with the positive incremental ARPU achieved,

which are more than offsetting the temporarily higher churn due to merger remedies imposed on the FTTH

base.

The growth recorded in Business revenues to 96.2 million euros was the result of good yoy trends in RGUs,

which surpassed the 1 million milestone in 1Q14, and by the positive performance in wholesale revenues, which

together helped to offset a yoy decline in ARPU per business RGU of 5%.

Revenues from the Audiovisuals business fell by 4.7% yoy to 14.2 million euros and Cinema Exhibition

revenues fell by 9.1% to 10.7 million euros. In the case of the Cinema Exhibition Business, the negative yoy

performance in revenues is a direct result of a poor quarter for cinema sales due to the previously mentioned

Easter holiday impact, while the decline in the Audiovisuals business was mostly due to lower homevideo and

VoD revenues yoy.

ZAP continued to post strong operational and financial momentum with contribution to revenues of ZON

OPTIMUS’ 30% stake increasing by 38.9% to 13.9 million euros in 1Q14.

EBITDA

Consolidated EBITDA fell by 5.9% in 1Q14 to 129.9 million euros generating a margin of 38.5%. Including the

contribution from ZON OPTIMUS’ 30% stake in ZAP, Consolidated EBITDA would have posted a lower

decline of 3.9% to 135.3 million euros. Telco EBITDA fell by 8.1% in 1Q14 to 120.4 million euros and EBITDA

from the Audiovisuals and Cinema operations increased by 36.3% yoy to 9.5 million euros.

24

CONSOLIDATED MANAGEMENT REPORT 1Q14

Consolidated Operating Costs Excluding D&A

Consolidated Operating Costs fell by 3% yoy to 207.5 million euros and posted a decline of 12.8% in

comparison with 4Q13.

Wages and Salaries fell by 9.5% to 21.0 million euros in 1Q14 as a result mainly of a lower average level of

headcount at the telco division in comparison with 1Q13, down by 11%. The majority of the projected

headcount optimization resulting from the merger process has already occurred and this will continue to be

reflected in yoy savings in this cost line.

Direct Costs recorded a 1% decline to 96.7 million euros, which reflects a combination of significantly lower

yoy programming and capacity related costs of 8% and 18% respectively due to savings already achieved

with the merger, namely the integration of previous OPTIMUS Pay TV and fixed customers onto the ZON

OPTIMUS fixed network and an increase in traffic costs of 16% due to the greater level of mass calling

services and increased payments related with advertising revenue sharing models in place.

Commercial Costs increased by 17.6% in 1Q14 to 22.7 million euros although they were 31.6% lower than in

4Q13 which is always a period of strong commercial activity in the build-up to Christmas. The yoy increase

was mainly driven by a higher level of handset sales and commissions due to the increased commercial push.

Other Operating Costs fell by 9% yoy to 67 million euros due to a combination of effects with the most

relevant impacts due to a decline in Supplies and External Services and a reduction in the level of provisions.

License related costs, included in this aggregate, increased by 22.5% in 1Q14 to 5.7 million euros which is

mostly explained by a 0.75 million euros increase in spectrum fee and a 0.6 million euros quarterly charge

related with the cinema tax imposed on television operators.

Net Income

Net Income reached 25.3 million euros in 1Q14, compared with 27.5 million euros in 1Q13 and increased from

negative 13.1 million euros in the previous quarter due to significantly lower non-recurrent expenses in the

period.

Equity in affiliate companies posted another very positive increase in contribution growing to 4.9 million euros

in 1Q14 compared with 1.3 million in 1Q13, on the back of the very strong financial contribution of the

international JV, ZAP, and also of the contribution of SportTV which recovered from a negative Net Income in

1Q13.

Depreciation and Amortization posted a yoy decline of 3.7% to 83.9 million euros, with no material change

25

ZON OPTIMUS, SGPS, SA

compared with previous periods.

Other Expenses* of 2.8 million euros were significantly lower in 1Q14 than in 4Q13 and a significant part

relates to non-recurrent merger related costs.

Net Financial Expenses fell by 9.1% to 15.2 million euros in 1Q14 compared with 16.7 million euros in 1Q13 as a

result of the lower average level of gross debt and the lower average cost of the new debt contracted in 4Q13.

Income Tax provision amounted to 7.3 million euros in 1Q14, representing a 3.2% decline in comparison with

1Q13.

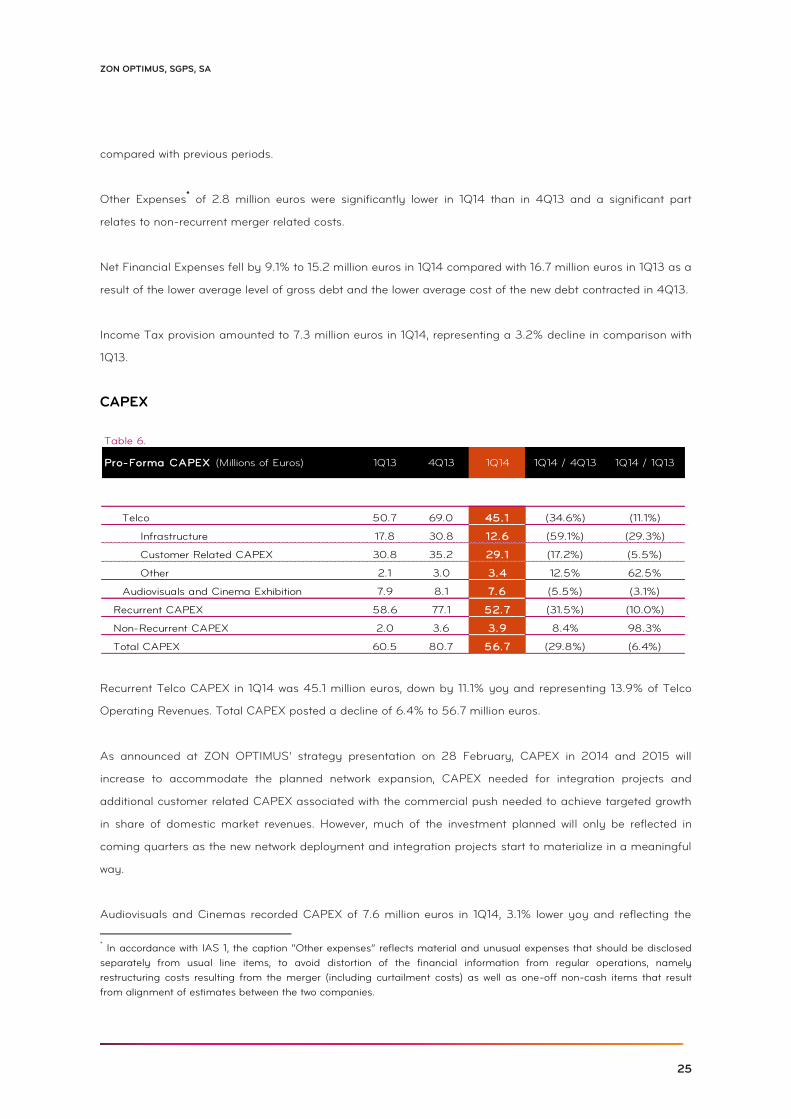

CAPEX

Recurrent Telco CAPEX in 1Q14 was 45.1 million euros, down by 11.1% yoy and representing 13.9% of Telco

Operating Revenues. Total CAPEX posted a decline of 6.4% to 56.7 million euros.

As announced at ZON OPTIMUS’ strategy presentation on 28 February, CAPEX in 2014 and 2015 will

increase to accommodate the planned network expansion, CAPEX needed for integration projects and

additional customer related CAPEX associated with the commercial push needed to achieve targeted growth

in share of domestic market revenues. However, much of the investment planned will only be reflected in

coming quarters as the new network deployment and integration projects start to materialize in a meaningful

way.

Audiovisuals and Cinemas recorded CAPEX of 7.6 million euros in 1Q14, 3.1% lower yoy and reflecting the

* In accordance with IAS 1, the caption “Other expenses” reflects material and unusual expenses that should be disclosed

separately from usual line items, to avoid distortion of the financial information from regular operations, namely

restructuring costs resulting from the merger (including curtailment costs) as well as one-off non-cash items that result

from alignment of estimates between the two companies.

Table 6.

Telco 50.7 69.0 45.1 (34.6%) (11.1%)

Infrastructure 17.8 30.8 12.6 (59.1%) (29.3%)

Customer Related CAPEX 30.8 35.2 29.1 (17.2%) (5.5%)

Other 2.1 3.0 3.4 12.5% 62.5%

Audiovisuals and Cinema Exhibition 7.9 8.1 7.6 (5.5%) (3.1%)

Recurrent CAPEX 58.6 77.1 52.7 (31.5%) (10.0%)

Non-Recurrent CAPEX 2.0 3.6 3.9 8.4% 98.3%

Total CAPEX 60.5 80.7 56.7 (29.8%) (6.4%)

Pro-Forma CAPEX (Millions of Euros) 1Q13 1Q14 1Q14 / 1Q134Q13 1Q14 / 4Q13

26

CONSOLIDATED MANAGEMENT REPORT 1Q14

capitalization of certain movie rights in the Audiovisuals division.

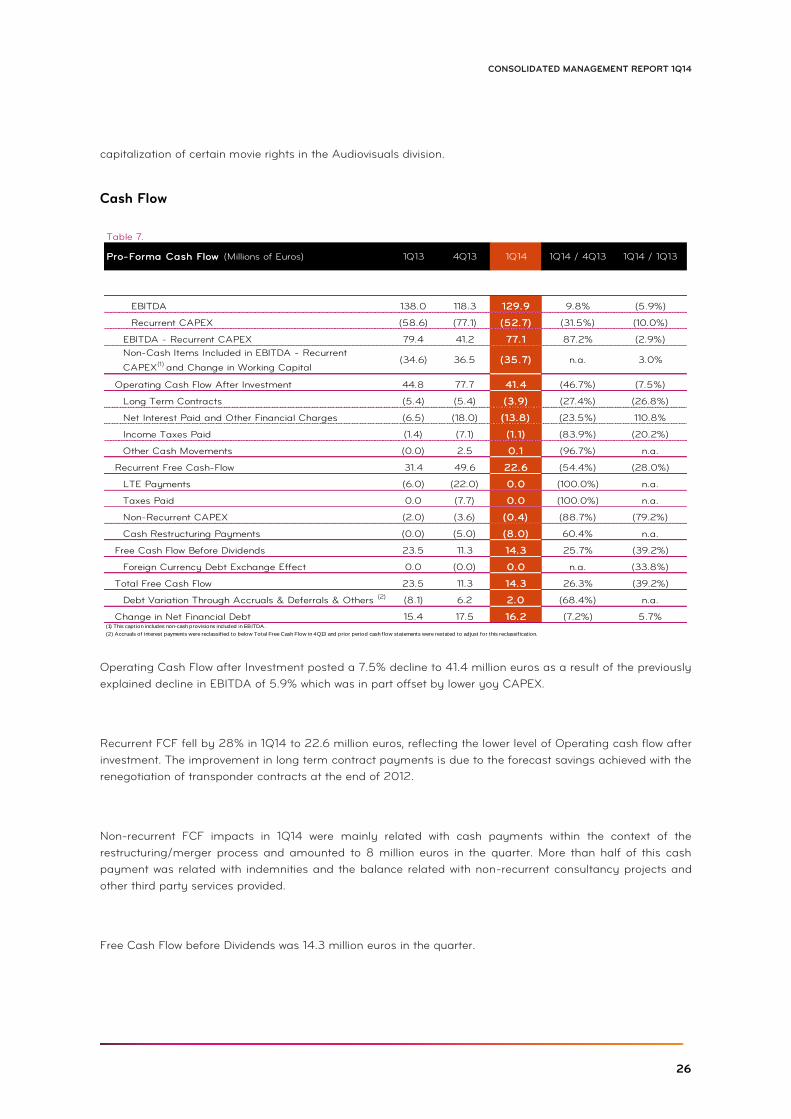

Cash Flow

Operating Cash Flow after Investment posted a 7.5% decline to 41.4 million euros as a result of the previously

explained decline in EBITDA of 5.9% which was in part offset by lower yoy CAPEX.

Recurrent FCF fell by 28% in 1Q14 to 22.6 million euros, reflecting the lower level of Operating cash flow after

investment. The improvement in long term contract payments is due to the forecast savings achieved with the

renegotiation of transponder contracts at the end of 2012.

Non-recurrent FCF impacts in 1Q14 were mainly related with cash payments within the context of the

restructuring/merger process and amounted to 8 million euros in the quarter. More than half of this cash

payment was related with indemnities and the balance related with non-recurrent consultancy projects and

other third party services provided.

Free Cash Flow before Dividends was 14.3 million euros in the quarter.

Table 7.

EBITDA 138.0 118.3 129.9 9.8% (5.9%)

Recurrent CAPEX (58.6) (77.1) (52.7) (31.5%) (10.0%)

EBITDA - Recurrent CAPEX 79.4 41.2 77.1 87.2% (2.9%)

Non-Cash Items Included in EBITDA - Recurrent

CAPEX(1) and Change in Working Capital (34.6) 36.5 (35.7) n.a. 3.0%

Operating Cash Flow After Investment 44.8 77.7 41.4 (46.7%) (7.5%)

Long Term Contracts (5.4) (5.4) (3.9) (27.4%) (26.8%)

Net Interest Paid and Other Financial Charges (6.5) (18.0) (13.8) (23.5%) 110.8%

Income Taxes Paid (1.4) (7.1) (1. 1) (83.9%) (20.2%)

Other Cash Movements (0.0) 2.5 0.1 (96.7%) n.a.

Recurrent Free Cash-Flow 31.4 49.6 22.6 (54.4%) (28.0%)

LTE Payments (6.0) (22.0) 0.0 (100.0%) n.a.

Taxes Paid 0.0 (7.7) 0.0 (100.0%) n.a.

Non-Recurrent CAPEX (2.0) (3.6) (0.4) (88.7%) (79.2%)

Cash Restructuring Payments (0.0) (5.0) (8.0) 60.4% n.a.

Free Cash Flow Before Dividends 23.5 11.3 14.3 25.7% (39.2%)

Foreign Currency Debt Exchange Effect 0.0 (0.0) 0.0 n.a. (33.8%)

Total Free Cash Flow 23.5 11.3 14.3 26.3% (39.2%)

Debt Variation Through Accruals & Deferrals & Others (2) (8.1) 6.2 2.0 (68.4%) n.a.

Change in Net Financial Debt 15.4 17.5 16.2 (7.2%) 5.7%

(2) Accruals of interest payments were reclassif ied to below Total Free Cash Flow in 4Q13 and prior period cash f low statements were restated to adjust for this reclassif icat ion.

4Q13 1Q14 / 4Q13

(1) This capt ion includes non-cash provisions included in EBITDA.

Pro-Forma Cash Flow (Millions of Euros) 1Q13 1Q14 1Q14 / 1Q13

27

ZON OPTIMUS, SGPS, SA

Pro Forma Consolidated Balance Sheet

Table 8.

Current Assets 454.8 419.4

Cash and Equivalents 74.4 22.9

Accounts Receivable, Net 309.6 319.9

Inventories, Net 32.6 38.1

Taxes Receivable 11.8 9.5

Prepaid Expenses and Other Current Assets 26.4 29.0

Non-current Assets 2,434.5 2,408.3

Investments in Group Companies 31.6 32.4

Intangible Assets, Net 1,111.1 1,128.3

Fixed Assets, Net 1,096.8 1,078.5

Deferred Taxes 165.4 143.6

Other Non-current Assets 29.5 25.5

Total Assets 2,889.3 2,827.7

Current Liabilities 762.2 879.5

Short Term Debt 213.4 339.6

Accounts Payable 367.6 343.6

Accrued Expenses 129.9 145.8

Deferred Income 25.5 28.1

Taxes Payable 23.0 20.5

Current Provisions and Other Liabilities 2.8 2.0

Non-current Liabilities 1,066.9 872.6

Medium and Long Term Debt 928.2 731.8

Non-current Provisions and Other Liabilities 138.6 140.9

Total Liabilities 1,829.1 1,752.1

Equity Before Non-Controlling Interests 1,050.6 1,065.6

Share Capital 5.2 5.2

Issue Premium 854.2 854.2

Own Shares (2.0) (3.9)

Reserves, Retained Earnings and Other 129.8 184.9

Net Income 63.4 25.3

Non-Controlling Interests 9.6 9.9

Total Shareholders' Equity 1,060.2 1,075.6

Total Liabilities and Shareholders' Equity 2,889.3 2,827.7

Pro-Forma Balance Sheet (Millions of Euros) 2013 1Q14

28

CONSOLIDATED MANAGEMENT REPORT 1Q14

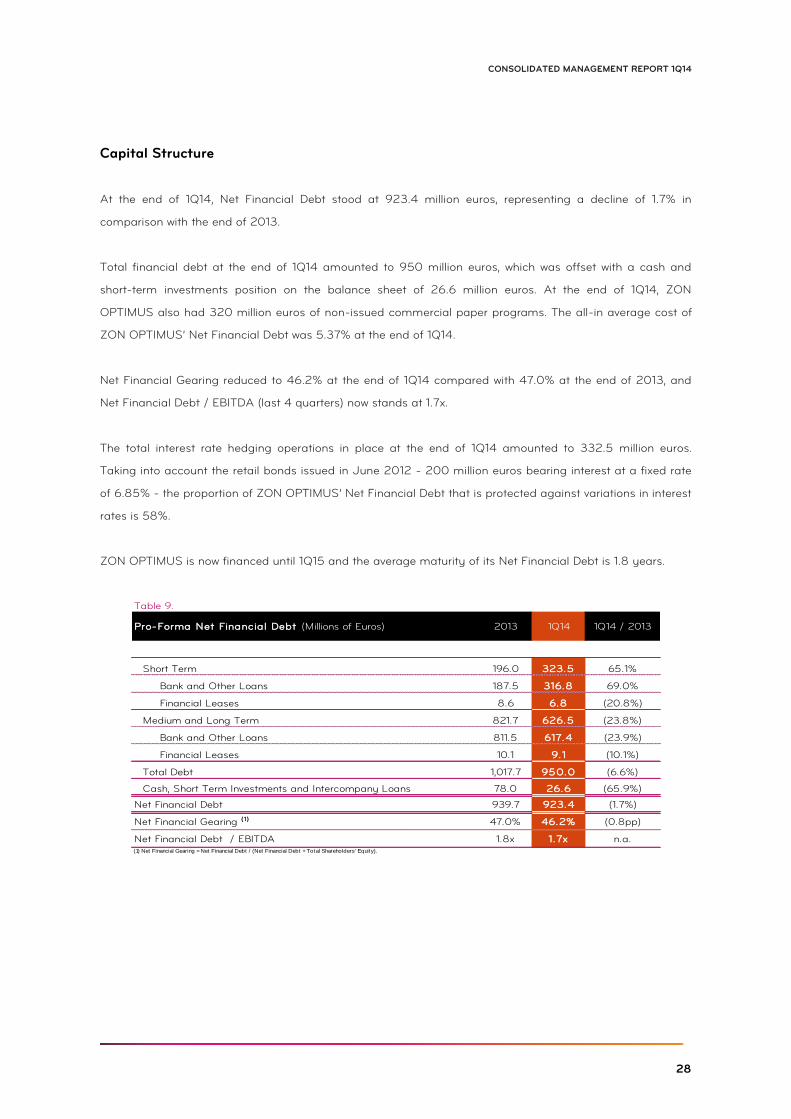

Capital Structure

At the end of 1Q14, Net Financial Debt stood at 923.4 million euros, representing a decline of 1.7% in

comparison with the end of 2013.

Total financial debt at the end of 1Q14 amounted to 950 million euros, which was offset with a cash and

short-term investments position on the balance sheet of 26.6 million euros. At the end of 1Q14, ZON

OPTIMUS also had 320 million euros of non-issued commercial paper programs. The all-in average cost of

ZON OPTIMUS’ Net Financial Debt was 5.37% at the end of 1Q14.

Net Financial Gearing reduced to 46.2% at the end of 1Q14 compared with 47.0% at the end of 2013, and

Net Financial Debt / EBITDA (last 4 quarters) now stands at 1.7x.

The total interest rate hedging operations in place at the end of 1Q14 amounted to 332.5 million euros.

Taking into account the retail bonds issued in June 2012 - 200 million euros bearing interest at a fixed rate

of 6.85% - the proportion of ZON OPTIMUS’ Net Financial Debt that is protected against variations in interest

rates is 58%.

ZON OPTIMUS is now financed until 1Q15 and the average maturity of its Net Financial Debt is 1.8 years.

Table 9.

Short Term 196.0 323.5 65.1%

Bank and Other Loans 187.5 316.8 69.0%

Financial Leases 8.6 6.8 (20.8%)

Medium and Long Term 821.7 626.5 (23.8%)

Bank and Other Loans 811.5 617.4 (23.9%)

Financial Leases 10.1 9.1 (10.1%)

Total Debt 1,017.7 950.0 (6.6%)

Cash, Short Term Investments and Intercompany Loans 78.0 26.6 (65.9%)

Net Financial Debt 939.7 923.4 (1.7%)

Net Financial Gearing ( 1) 47.0% 46.2% (0.8pp)

Net Financial Debt / EBITDA 1.8x 1.7x n.a.(1) Net Financial Gearing = Net Financial Debt / (Net Financial Debt + Total Shareholders' Equity).

Pro-Forma Net Financial Debt (Millions of Euros) 2013 1Q14 / 20131Q14

29

ZON OPTIMUS, SGPS, SA

5.

CONSOLIDATED FINANCIAL STATEMENTS

30

CONSOLIDATED MANAGEMENT REPORT 1Q14

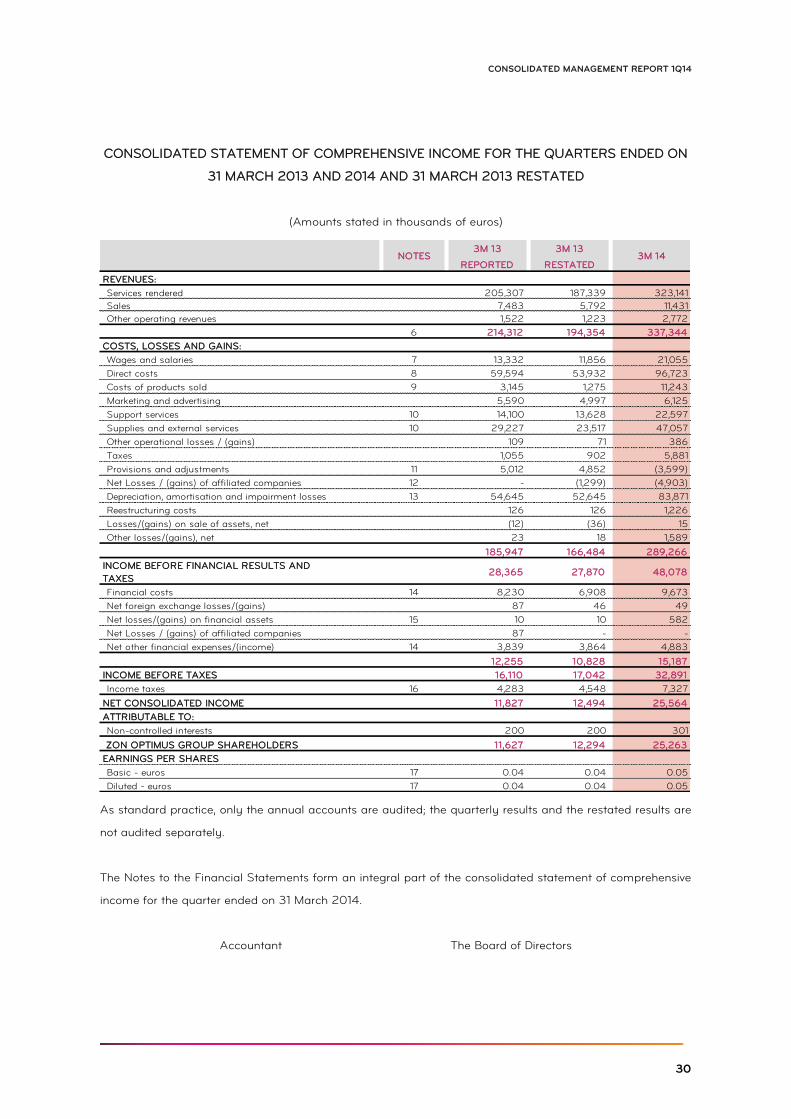

CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME FOR THE QUARTERS ENDED ON

31 MARCH 2013 AND 2014 AND 31 MARCH 2013 RESTATED

(Amounts stated in thousands of euros)

As standard practice, only the annual accounts are audited; the quarterly results and the restated results are

not audited separately.

The Notes to the Financial Statements form an integral part of the consolidated statement of comprehensive

income for the quarter ended on 31 March 2014.

Accountant The Board of Directors

3M 13 3M 13

REPORTED RESTATED

REVENUES:

Services rendered 205,307 187,339 323,141

Sales 7,483 5,792 11,431

Other operating revenues 1,522 1,223 2,772

6 214,312 194,354 337,344

COSTS, LOSSES AND GAINS:

Wages and salaries 7 13,332 11,856 21,055

Direct costs 8 59,594 53,932 96,723

Costs of products sold 9 3,145 1,275 11,243

Marketing and advertising 5,590 4,997 6,125

Support services 10 14,100 13,628 22,597

Supplies and external services 10 29,227 23,517 47,057

Other operational losses / (gains) 109 71 386

Taxes 1,055 902 5,881

Provisions and adjustments 11 5,012 4,852 (3,599)

Net Losses / (gains) of affiliated companies 12 - (1,299) (4,903)

Depreciation, amortisation and impairment losses 13 54,645 52,645 83,871

Reestructuring costs 126 126 1,226

Losses/(gains) on sale of assets, net (12) (36) 15

Other losses/(gains), net 23 18 1,589

185,947 166,484 289,266

28,365 27,870 48,078

Financial costs 14 8,230 6,908 9,673

Net foreign exchange losses/(gains) 87 46 49

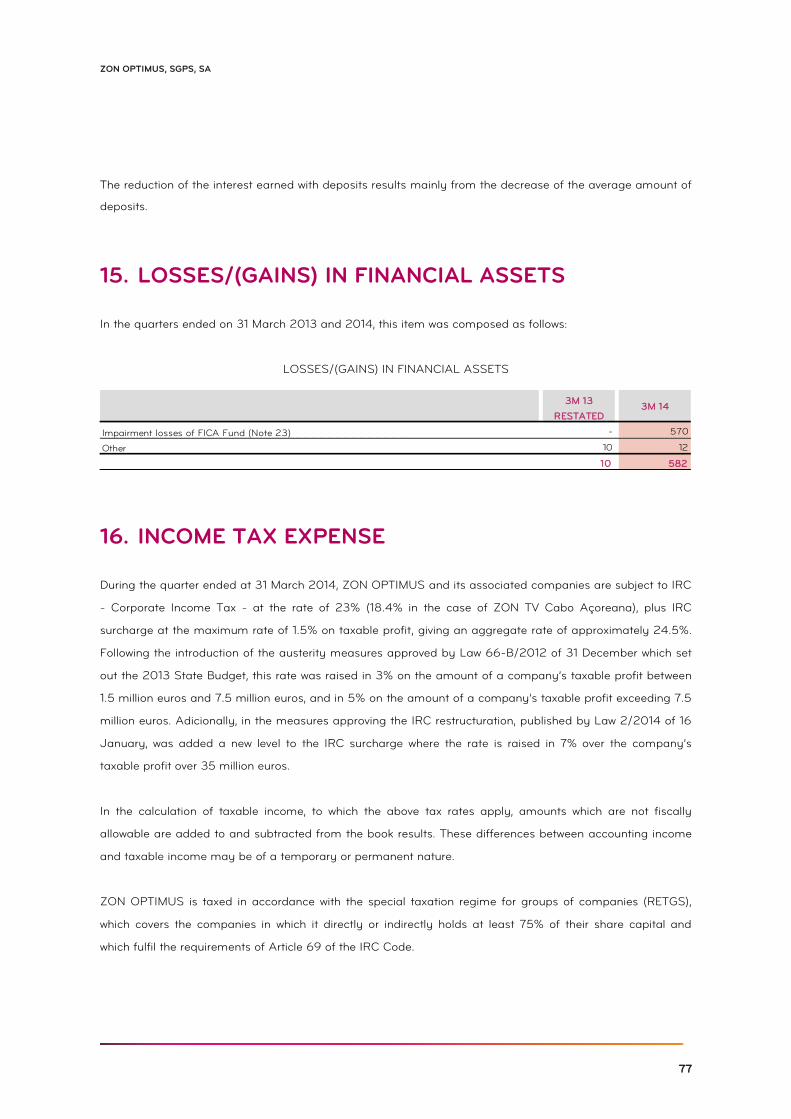

Net losses/(gains) on financial assets 15 10 10 582

Net Losses / (gains) of affiliated companies 87 - -

Net other financial expenses/(income) 14 3,839 3,864 4,883

12,255 10,828 15,187

INCOME BEFORE TAXES 16,110 17,042 32,891

Income taxes 16 4,283 4,548 7,327

NET CONSOLIDATED INCOME 11,827 12,494 25,564

ATTRIBUTABLE TO:

Non-controlled interests 200 200 301

ZON OPTIMUS GROUP SHAREHOLDERS 11,627 12,294 25,263

EARNINGS PER SHARES

Basic - euros 17 0.04 0.04 0.05

Diluted - euros 17 0.04 0.04 0.05

NOTES 3M 14

INCOME BEFORE FINANCIAL RESULTS AND

TAXES

31

ZON OPTIMUS, SGPS, SA

CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME FOR THE QUARTERS ENDED ON

31 MARCH 2013 AND 2014 AND 31 MARCH 2013 RESTATED

(Amounts stated in thousands of euros)

As standard practice, only the annual accounts are audited; the quarterly results and the restated results are

not audited separately.

The Notes to the Financial Statements form an integral part of the consolidated statement of comprehensive

income for the quarter ended on 31 March 2014.

Accountant The Board of Directors

3M 13 3M 13

REPORTED RESTATED

NET INCOME FOR THE YEAR 11,827 12,494 25,564

OTHER INCOME

ITENS THAT MAY BE RECLASSIFIED SUBSEQUENTLY

TO THE INCOME STATEMENT

Accounting for equity method 22 - (110) (275)

Fair value of interest rate swap 30 1,203 1,203 (153)

Deferred income tax - interest rate swap 30 (319) (319) 40

Fair value of exchange rate forward 30 352 352 88

Deferred income tax -exchange rate forward 30 (101) (101) (23)

Currency translation differences (136) (26) (17)

OTHER COMPREHENSIVE INCOME 999 999 (340)

TOTAL COMPREHENSIVE INCOME FOR THE PERIOD 12,826 13,493 25,224

ATTRIBUTABLE TO:

Share owners of the company 12,626 13,293 24,923

Non-controlling interests 200 200 301

NOTES 3M 14

32

CONSOLIDATED MANAGEMENT REPORT 1Q14

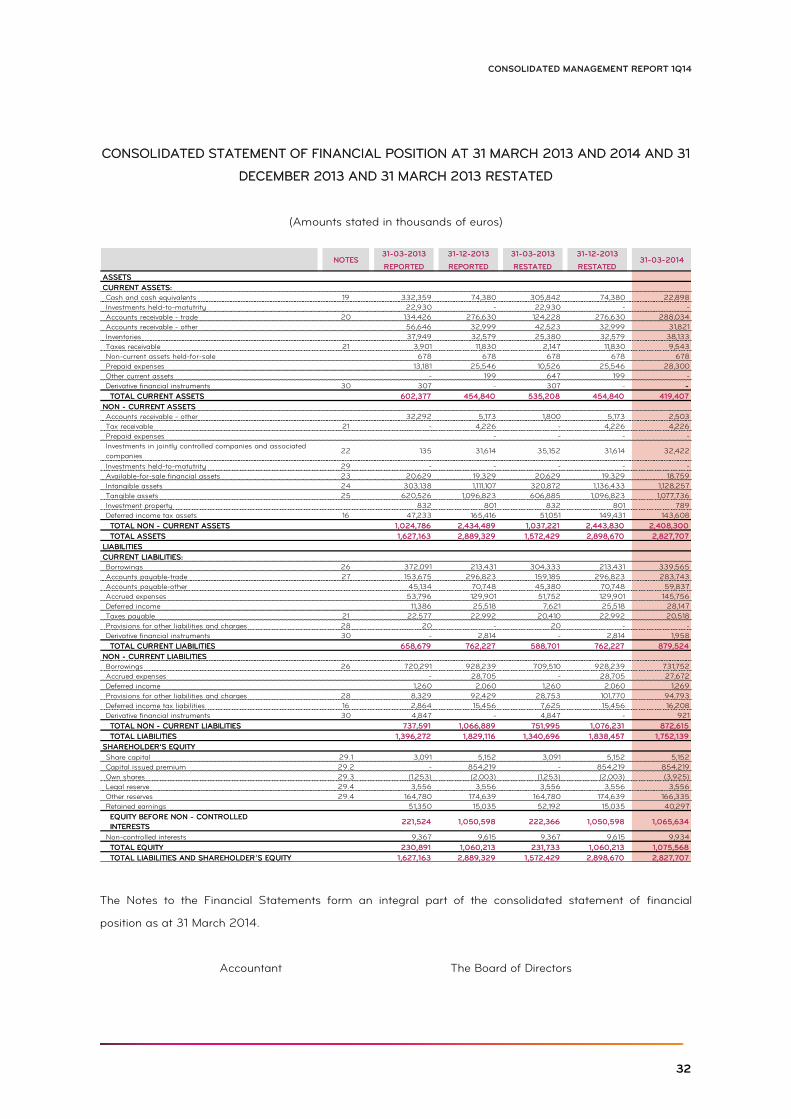

CONSOLIDATED STATEMENT OF FINANCIAL POSITION AT 31 MARCH 2013 AND 2014 AND 31

DECEMBER 2013 AND 31 MARCH 2013 RESTATED

(Amounts stated in thousands of euros)

The Notes to the Financial Statements form an integral part of the consolidated statement of financial

position as at 31 March 2014.

Accountant The Board of Directors

31-03-2013 31-12-2013 31-03-2013 31-12-2013

REPORTED REPORTED RESTATED RESTATED

ASSETS

CURRENT ASSETS:

Cash and cash equivalents 19 332,359 74,380 305,842 74,380 22,898

Investments held-to-matutrity 22,930 - 22,930 - -

Accounts receivable - trade 20 134,426 276,630 124,228 276,630 288,034

Accounts receivable - other 56,646 32,999 42,523 32,999 31,821

Inventories 37,949 32,579 25,380 32,579 38,133

Taxes receivable 21 3,901 11,830 2,147 11,830 9,543

Non-current assets held-for-sale 678 678 678 678 678

Prepaid expenses 13,181 25,546 10,526 25,546 28,300

Other current assets - 199 647 199 -

Derivative financial instruments 30 307 - 307 - -

TOTAL CURRENT ASSETS 602,377 454,840 535,208 454,840 419,407

NON - CURRENT ASSETS

Accounts receivable - other 32,292 5,173 1,800 5,173 2,503

Tax receivable 21 - 4,226 - 4,226 4,226

Prepaid expenses - - - -

22 135 31,614 35,152 31,614 32,422

Investments held-to-matutrity 29 - - - - -

Available-for-sale financial assets 23 20,629 19,329 20,629 19,329 18,759

Intangible assets 24 303,138 1,111,107 320,872 1,136,433 1,128,257

Tangible assets 25 620,526 1,096,823 606,885 1,096,823 1,077,736

Investment property 832 801 832 801 789

Deferred income tax assets 16 47,233 165,416 51,051 149,431 143,608

TOTAL NON - CURRENT ASSETS 1,024,786 2,434,489 1,037,221 2,443,830 2,408,300

TOTAL ASSETS 1,627,163 2,889,329 1,572,429 2,898,670 2,827,707

LIABILITIES

CURRENT LIABILITIES:

Borrowings 26 372,091 213,431 304,333 213,431 339,565

Accounts payable-trade 27 153,675 296,823 159,185 296,823 283,743

Accounts payable-other 45,134 70,748 45,380 70,748 59,837

Accrued expenses 53,796 129,901 51,752 129,901 145,756

Deferred income 11,386 25,518 7,621 25,518 28,147

Taxes payable 21 22,577 22,992 20,410 22,992 20,518

Provisions for other liabilities and charges 28 20 - 20 - -

Derivative financial instruments 30 - 2,814 - 2,814 1,958

TOTAL CURRENT LIABILITIES 658,679 762,227 588,701 762,227 879,524

NON - CURRENT LIABILITIES

Borrowings 26 720,291 928,239 709,510 928,239 731,752

Accrued expenses - 28,705 - 28,705 27,672

Deferred income 1,260 2,060 1,260 2,060 1,269

Provisions for other liabilities and charges 28 8,329 92,429 28,753 101,770 94,793

Deferred income tax liabilities 16 2,864 15,456 7,625 15,456 16,208

Derivative financial instruments 30 4,847 - 4,847 - 921

TOTAL NON - CURRENT LIABILITIES 737,591 1,066,889 751,995 1,076,231 872,615

TOTAL LIABILITIES 1,396,272 1,829,116 1,340,696 1,838,457 1,752,139

SHAREHOLDER'S EQUITY

Share capital 29.1 3,091 5,152 3,091 5,152 5,152

Capital issued premium 29.2 - 854,219 - 854,219 854,219

Own shares 29.3 (1,253) (2,003) (1,253) (2,003) (3,925)

Legal reserve 29.4 3,556 3,556 3,556 3,556 3,556

Other reserves 29.4 164,780 174,639 164,780 174,639 166,335

Retained earnings 51,350 15,035 52,192 15,035 40,297

EQUITY BEFORE NON - CONTROLLED

INTERESTS221,524 1,050,598 222,366 1,050,598 1,065,634

Non-controlled interests 9,367 9,615 9,367 9,615 9,934

TOTAL EQUITY 230,891 1,060,213 231,733 1,060,213 1,075,568

TOTAL LIABILITIES AND SHAREHOLDER´S EQUITY 1,627,163 2,889,329 1,572,429 2,898,670 2,827,707

31-03-2014NOTES

Investments in jointly controlled companies and associated

companies

33

ZON OPTIMUS, SGPS, SA

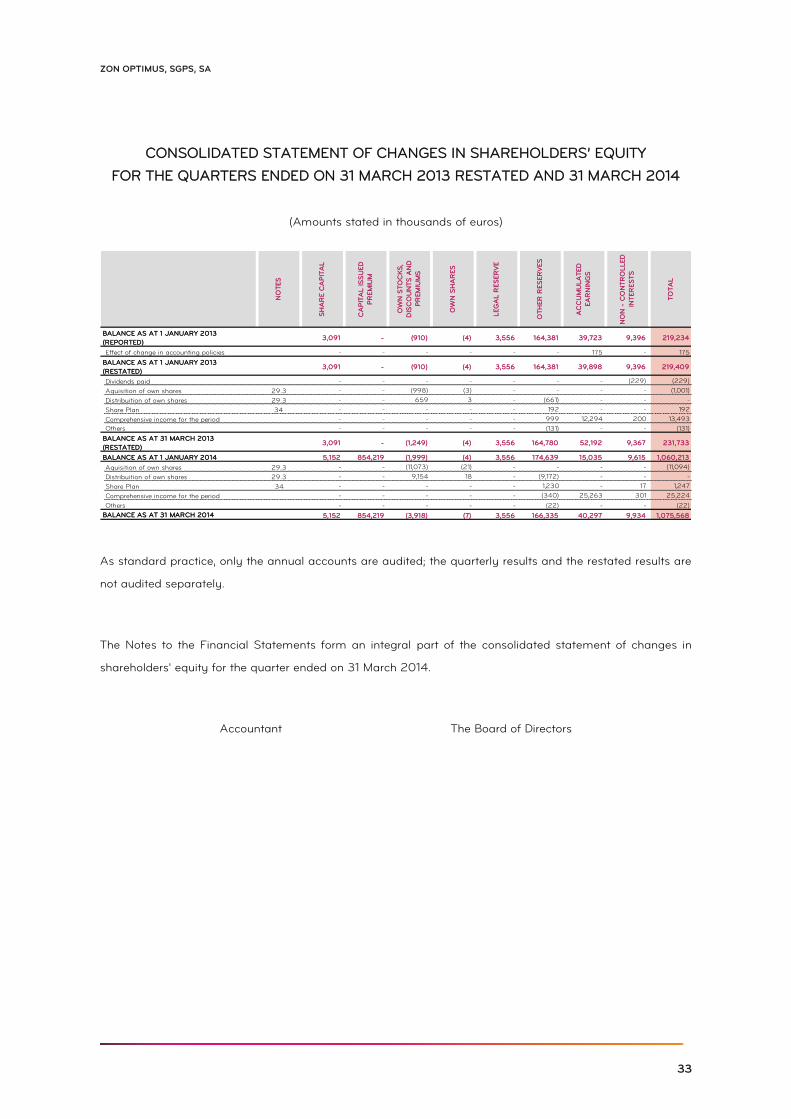

CONSOLIDATED STATEMENT OF CHANGES IN SHAREHOLDERS’ EQUITY

FOR THE QUARTERS ENDED ON 31 MARCH 2013 RESTATED AND 31 MARCH 2014

(Amounts stated in thousands of euros)

As standard practice, only the annual accounts are audited; the quarterly results and the restated results are

not audited separately.

The Notes to the Financial Statements form an integral part of the consolidated statement of changes in

shareholders' equity for the quarter ended on 31 March 2014.

Accountant The Board of Directors

NO

TES

SH

AR

E C

AP

ITA

L

CA

PIT

AL IS

SU

ED

PR

EM

IUM

OW

N S

TO

CK

S,

DIS

CO

UN

TS

AN

D

PR

EM

IUM

S

OW

N S

HA

RES

LEG

AL R

ES

ER

VE

OTH

ER

RES

ER

VES

AC

CU

MU

LA

TED

EA

RN

ING

S

NO

N -

CO

NTR

OLLED

INTER

ES

TS

TO

TA

L

3,091 - (910) (4) 3,556 164,381 39,723 9,396 219,234

Effect of change in accounting policies - - - - - - 175 - 175

3,091 - (910) (4) 3,556 164,381 39,898 9,396 219,409

Dividends paid - - - - - - - (229) (229)

Aquisition of own shares 29.3 - - (998) (3) - - - - (1,001)

Distribuition of own shares 29.3 - - 659 3 - (661) - - -

Share Plan 34 - - - - - 192 - - 192

Comprehensive income for the period - - - - - 999 12,294 200 13,493

Others - - - - - (131) - - (131)

3,091 - (1,249) (4) 3,556 164,780 52,192 9,367 231,733

5,152 854,219 (1,999) (4) 3,556 174,639 15,035 9,615 1,060,213

Aquisition of own shares 29.3 - - (11,073) (21) - - - - (11,094)

Distribuition of own shares 29.3 - - 9,154 18 - (9,172) - - -

Share Plan 34 - - - - - 1,230 - 17 1,247

Comprehensive income for the period - - - - - (340) 25,263 301 25,224

Others - - - - - (22) - - (22)

5,152 854,219 (3,918) (7) 3,556 166,335 40,297 9,934 1,075,568

BALANCE AS AT 1 JANUARY 2013

(REPORTED)

BALANCE AS AT 1 JANUARY 2013

(RESTATED)

BALANCE AS AT 31 MARCH 2013

(RESTATED)

BALANCE AS AT 1 JANUARY 2014

BALANCE AS AT 31 MARCH 2014

34

CONSOLIDATED MANAGEMENT REPORT 1Q14

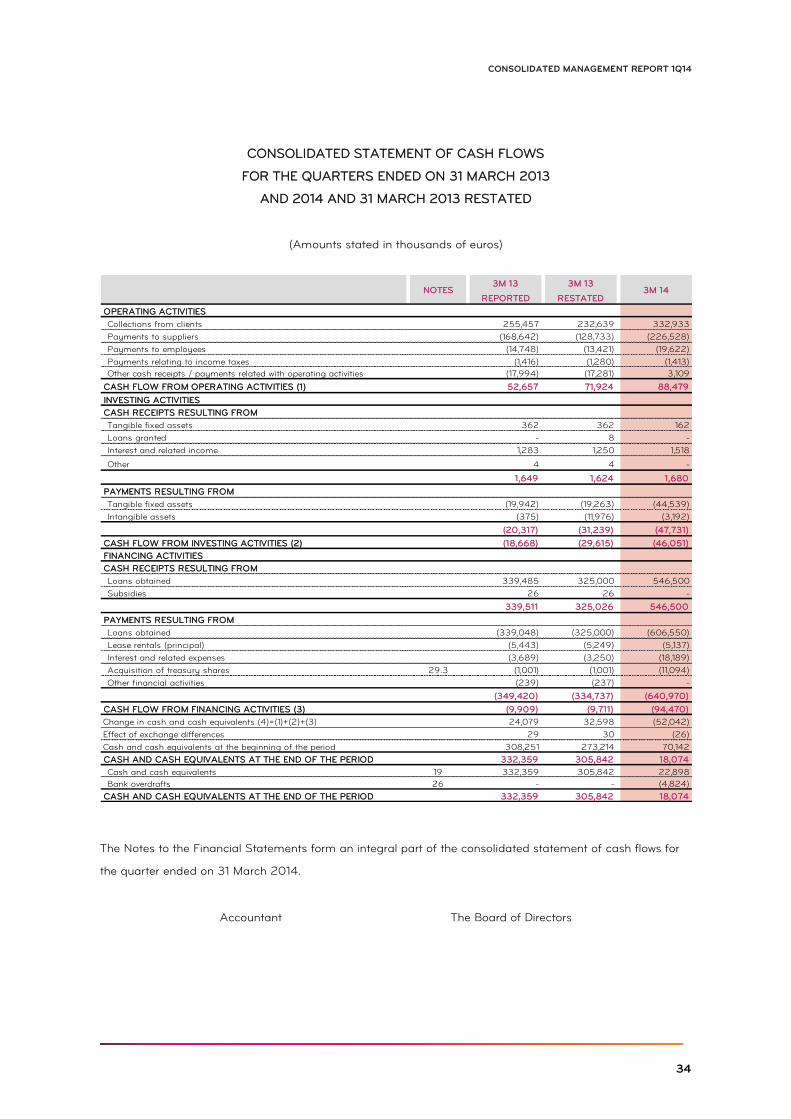

CONSOLIDATED STATEMENT OF CASH FLOWS

FOR THE QUARTERS ENDED ON 31 MARCH 2013

AND 2014 AND 31 MARCH 2013 RESTATED

(Amounts stated in thousands of euros)

The Notes to the Financial Statements form an integral part of the consolidated statement of cash flows for

the quarter ended on 31 March 2014.

Accountant The Board of Directors

3M 13 3M 13

REPORTED RESTATED

OPERATING ACTIVITIES

Collections from clients 255,457 232,639 332,933

Payments to suppliers (168,642) (128,733) (226,528)

Payments to employees (14,748) (13,421) (19,622)

Payments relating to income taxes (1,416) (1,280) (1,413)

Other cash receipts / payments related with operating activities (17,994) (17,281) 3,109

CASH FLOW FROM OPERATING ACTIVITIES (1) 52,657 71,924 88,479

INVESTING ACTIVITIES

CASH RECEIPTS RESULTING FROM

Tangible fixed assets 362 362 162

Loans granted - 8 -

Interest and related income 1,283 1,250 1,518

Other 4 4 -

1,649 1,624 1,680

PAYMENTS RESULTING FROM

Tangible fixed assets (19,942) (19,263) (44,539)

Intangible assets (375) (11,976) (3,192)

(20,317) (31,239) (47,731)

CASH FLOW FROM INVESTING ACTIVITIES (2) (18,668) (29,615) (46,051)

FINANCING ACTIVITIES

CASH RECEIPTS RESULTING FROM

Loans obtained 339,485 325,000 546,500

Subsidies 26 26 -

339,511 325,026 546,500

PAYMENTS RESULTING FROM

Loans obtained (339,048) (325,000) (606,550)

Lease rentals (principal) (5,443) (5,249) (5,137)

Interest and related expenses (3,689) (3,250) (18,189)

Acquisition of treasury shares 29.3 (1,001) (1,001) (11,094)

Other financial activities (239) (237) -

(349,420) (334,737) (640,970)

CASH FLOW FROM FINANCING ACTIVITIES (3) (9,909) (9,711) (94,470)

Change in cash and cash equivalents (4)=(1)+(2)+(3) 24,079 32,598 (52,042)

Effect of exchange differences 29 30 (26)

Cash and cash equivalents at the beginning of the period 308,251 273,214 70,142

CASH AND CASH EQUIVALENTS AT THE END OF THE PERIOD 332,359 305,842 18,074

Cash and cash equivalents 19 332,359 305,842 22,898

Bank overdrafts 26 - - (4,824)

CASH AND CASH EQUIVALENTS AT THE END OF THE PERIOD 332,359 305,842 18,074

3M 14NOTES

35

ZON OPTIMUS, SGPS, SA

INTRODUCTORY NOTE 1.

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS AS AT 31 MARCH

2014

ZON Optimus, SGPS, SA ("Zon Optimus" or "Company"), formerly named ZON Multimédia – Serviços de

Telecomunicações e Multimédia, SGPS, S.A., with Company headquarters registered at Rua Actor Antonio

Silva, 9, Campo Grande, was established by Portugal Telecom, SGPS, SA ("Portugal Telecom") on July 15,

1999 for the purpose of implementing its multimedia business strategy.

During the 2007 financial year, Portugal Telecom proceeded with the spin-off of ZON through the attribution

of its participation in the company to their shareholders, which become fully independent from Portugal

Telecom.

During the 2013 financial year, ZON Multimédia – Serviços de Telecomunicações e Multimédia, SGPS, S.A.,

("ZON") and Optimus, SGPS, S.A. ("Optimus SGPS") have merged through the incorporation of Optimus

SGPS into ZON. Thereafter, the Company adopted the current designation of ZON Optimus, SGPS, S.A..

The businesses operated by ZON Optimus and its associated companies, form the "ZON Optimus Group" or

"Group", which includes cable and satellite television services, voice and Internet access services, video

production and sale, advertising on Pay TV channels, cinema exhibition and distribution, and the production

of channels for Pay TV.

ZON Optimus shares are listed on the Euronext Lisbon market. The Group’s shareholder’s structure as at 31

March 2014 is shown in Note 29.

Cable and satellite television in Portugal is mainly provided by ZON TV Cabo Portugal , S.A. ("ZON TV Cabo")

and its subsidiaries, ZON TV Cabo Açoreana, S.A. ("ZON TV Cabo Açoreana") and ZON TV Cabo

Madeirense, S.A. ("ZON TV Cabo Madeira") . These companies carry out: a) cable and satellite television

distribution; b) the operation of electronic communications services, including data and multimedia

communication services in general; c) IP voice services ("VOIP" - Voice over IP); d) Mobile Virtual Network

Operator (“MVNO”), and e) the provision of consultancy and similar services directly or indirectly related to

the above mentioned activities and services. The business of ZON TV Cabo, ZON TV Cabo Açoreana and

ZON TV Cabo Madeira is regulated by Law no . 5/2004 (Electronic Communications Law), which establishes

the legal regime governing electronic communications networks and services.

36

CONSOLIDATED MANAGEMENT REPORT 1Q14

ZON Conteúdos – Atividade de Televisão e de Produção de Conteúdos, S.A. (“ZON Conteúdos”) and ZON

Lusomundo TV, Lda. (“ZON Lusomundo TV”) operate in the television and content production business, and

currently produce films and series channels, which are distributed, among other operators, by ZON TV Cabo

and its affiliates. ZON Conteúdos also manages the advertising space on Pay TV channels and in the

cinemas of ZON Lusomundo Cinemas, S.A. (“ZON LM Cinemas”).

ZON Lusomundo Audiovisuais, S.A. (“ZON LM Audiovisuais”) and ZON LM Cinemas together with their

associated companies operate in the audiovisual sector, which includes video production and sale, cinema

exhibition and distribution, and the acquisition/negotiation of Pay TV and VOD (video-on-demand) rights.

On 27 August 2013, the Company completed a merger operation by incorporation of Optimus SGPS into

ZON. Optimus SGPS was a parent company of a group of companies which includes Optimus -

Comunicações S.A. which operates the latest generation mobile communication network, GSM/UMTS/LTE,

with extensive coverage in the national territory , as well as latest next generation wireline network, which

includes a transmission component, a backbone component and local access fiber components. As a result

of the merger, all Optimus SGPS subsidiaries were included in the consolidation scope: Be Artis – Concepção,

Construção e Gestão de Redes de Comunicação, S.A. (“Be Artis”), which operates in the design, construction,

management and exploitation of electronic communications networks and their equipment and infrastructure,

management of technologic assets and rendering of related services; Be Towering – Gestão de Torres de

Telecomunicações, S.A. (“Be Towering”), which operates in the implementation, installation and exploitation of

towers and other sites for the installation of telecommunications equipment; Optimus - Communications , SA

("Optimus") , which operates in the implementation, operation, exploitation and offer of networks and

rendering services of electronic communications and related resources; offer and commercialization of

products and equipments of electronic communications; Per-mar – Sociedade de Construções, S.A. (“Per-

mar”), which operates in the purchase, sale, renting and operation of property and commercial

establishments, and Sontária – Empreendimentos Imobiliários, S.A. (“Sontária”), which operates in the

undertaking of urbanization and building construction, planning, urban management, studies, construction

and property management, purchase and sale of properties and resale of properties purchased for that

purpose.

These Notes to the Consolidated Financial Statements follow the order in which the items are shown in the

consolidated financial statements.

The consolidated financial statements for the period ended on 31 March 2014 were approved by the Board of

Directors and their issue authorised on 7 May 2014.

The Board of Directors believes that the financial statements give a true and fair view of the Company’s

operations, financial performance and cash flows.

37

ZON OPTIMUS, SGPS, SA

ACCOUNTING POLICIES 2.

The principal accounting policies adopted in the preparation of the financial statements are described below.

These policies were consistently applied to all the financial years presented, unless otherwise indicated.

2.1. PRINCIPLES OF PRESENTATION

The consolidated financial statements are presented in euros as this is the main currency of the Group's

operations. The financial statements of subsidiaries located abroad were converted into euros in accordance

with the accounting policies described in Note 2.20.

The consolidated financial statements of ZON Optimus were prepared in accordance with the International

Financial Reporting Standards (“IFRS”) issued by the International Accounting Standards Board (“IASB”), and

Interpretations issued by the International Financial Reporting Committee (“IFRIC”) or the previous Standing

Interpretations Committee (“SIC”), adopted by the European Union, in force as at 1 January 2014.

These consolidated finantial statements are presented in accordance with IAS 34 — Interim Financial

Reporting (“IAS 34”). Therefore, these financial statements do not include all the information required by the

IFRS and so they should be analysed together with the consolidated financial statements of the period ended

at 31 December 2013.

The consolidated financial statements were prepared on a going concern basis from the ledgers and

accounting records of the companies included in the consolidation (Annex A), using the historical cost

convention, adjusted where applicable for the valuation of financial assets and liabilities (including derivatives)

at their fair value.

In preparing the consolidated financial statements in accordance with IFRS, the Board used estimates,

assumptions and critical judgements with impact on the value of assets and liabilities and the recognition of

income and costs in each reporting period. Although these estimates were based on the best information

available at the date of preparation of the consolidated financial statements, current and future results may

differ from these estimates. The areas involving a higher element of judgment and estimates are described in

Note 3.

38

CONSOLIDATED MANAGEMENT REPORT 1Q14

CHANGES IN ACCOUNTING POLICIES AND DISCLOSURES

The standards and interpretations that became effective as of 1 January 2014 are as follows:

IFRS 10 (new), “Consolidated financial statements”. IFRS 10 replaces all the guidance on control and

consolidation included in IAS 27 and SIC 12, amending the definition of control and the criteria for

determining control. The basic principle that the consolidated financial statements present the parent

company and subsidiaries as a single entity remains unchanged. This standard did not have any

significant impact on the Group’s financial statements. The Group has early adopted this standard in

the year ended at 31 December 2013.

IFRS 11 (new), “Joint Agreements”. IFRS 11 focuses on the rights and obligations associated with the joint

arrangements, rather than its legal form. Joint arrangements may be either joint operations (rights over

assets and obligations) or joint ventures (rights to the net assets of the arrangement as measured by

the equity method). Proportionate consolidation is no longer allowed when assessing jointly controlled

Entities. The Group has early adopted this standard in the year ended at 31 December 2013, resulting in

changing the accounting of jointly controlled entities, previously proportionately consolidated, being

recorded according to the equity method. Jointly controlled entities are disclosed in the attached maps.

IFRS 12 (new) – “Disclosure of interests in other entities”. This reporting standard establishes disclosure

requirements for all types of interests in other entities, including joint ventures, associates and special

purpose entities, in order to assess the nature, risk and financial impacts associated with the entity’s

interest. This standard resulted in additional disclosures about interests in other entities (Map attached).

IAS 27 (2011 revision), “Separate financial statements”. IAS 27 was revised after the issue of IFRS 10

and contains the accounting and disclosure requirements for investments in subsidiaries, joint ventures

and associates where an entity prepares separate financial statements. This standard did not have any

impact on the Group’s financial statements.

IFRS 28 (2011 revision), “Investments in associates and joint ventures”. IAS 28 was revised after the

issue of IFRS 11 and prescribes the accounting treatment of investments in associates and joint ventures,

establishing the requirements for applying the equity method. Early adoption of this standard resulted in

changing the accounting of jointly controlled entities, previously proportionately consolidated, being

recorded according to the equity method. Jointly controlled entities are disclosed in the attached maps.

Amendment to IFRS 10, IFRS 12 and IFRS 27 – “Bodies Managing Financial Contributions”. This

amendment includes the definition of an Entity managing financial contributions and introduces the

regime of exception to the obligation for Entities managing financial partnerships that qualify to provide

39

ZON OPTIMUS, SGPS, SA

funding, once all investments are measured against fair value. Specific disclosures are required for IFRS

12. This standard does not apply to the Group.

IAS 32 (amendment), “Disclosures – offsetting financial assets and financial liabilities”. This amendment

is part of the IASB’s “assets and liabilities offsetting” project and clarifies the meaning of “currently has

a legally enforceable right of set-off” and clarifies that some gross settlement systems (clearing houses)

may be considered equivalent to net settlement. This amendment does not have any impact on the

Group’s consolidated financial statements.

IAS 36 (amendment), “Recoverable Amount Disclosures for Non-Financial Assets”. This amendment

eliminates the disclosure requirements of the recoverable amount of a cash-generating unit like goodwill

or intangible assets with indefinite useful lives allocated to periods where it was not recorded any

impairment loss or reversal of impairment. Introduces additional disclosure requirements for assets for

which it was recorded an impairment loss or reversal of impairment and the recoverable amount of these

has been determined based on fair value less costs to sell. This amendment does not have any impact

on the Group’s consolidated financial statements.

IAS 39 (amendment), “Financial Instruments: Recognition and Measurement (Novation of Derivatives

and Continuation of Hedge Accounting)”. This amendment permits, the continuation of hedge

accounting when a derivative designated as a hedging instrument is legally imposed, subject to the

contract counterparty novation to a clearing house. This amendment does not have any impact on the

Group’s consolidated financial statements.

The following standards, interpretations, amendments and revisions, with mandatory application in future

financial years, have not yet been approved (endorsed) by the European Union, at the date of approval of

these financial statements:

IFRS 9 (new), “Financial instruments – classification and measurement” (effective date to be

designated). The initial phase of IFRS 9 forecasts two types of measurement: amortised cost and fair

value. All equity instruments are measured at fair value. A financial instrument is measured at

amortised cost only if the company has it to collect contractual cash flows and the cash flows represent

principal and interest. Otherwise, financial instruments are measured at fair value through profit and

loss.

IFRS 7 and 9 (Amendment), "Financial Instruments" (effective date to be designated). The amendment

to IFRS 9 is part of the draft revision of IAS 39 and establishes the requirements for the application of

hedge accounting. IFRS 7 was also revised as a result of this amendment.

40

CONSOLIDATED MANAGEMENT REPORT 1Q14

IFRS 14 (new), “Regulatory Deferral Accounts” (effective for annual periods beginning on or after 1

January 2016). This standard’s main purpose is to improve comparability of financial reports for

companies in regulated markets, allowing the companies that currently record assets and liabilities in

result of the regulation form the markets where they operate, in accordance with the adopted

accounting principles, do not have the need to eliminate those assets and liabilities in the first time

adoption of the IFRS. This standard will have no impact on the Group’s consolidated financial

statements.

IAS 19 (Amendment), “Employee benefits” (effective for annual periods beginning on or after 1 July

2014). This amendment clarifies the circumstances in which employee contribution plans for post-

employment benefits are a reduction in the cost of short-term benefits. This standard is not applicable

to the Group.

Improvements to Financial Reporting Standards (2010-2012 cycle and 2011-2013 cycle) (effective for

annual periods beginning on or after 1 July 2014). These improvements involve the review of several

standards.

IFRIC 21 (new), “Levies” (effective for annual periods beginning on or after 1 January 2014). This

amendment establishes the conditions regarding the timing of recognition of a liability related to pay a

levy by an entity as a result of a particular event (eg, participation in a particular market), without having

goods and specified services associated.

The Group is calculating the impact of this alteration and will apply this standard as soon as it becomes

effective.

VOLUNTARY CHANGES IN ACCOUNTING POLICIES

During the third quarter of the year ended at 31 December 2013, the Group, in addition to the early adoption

of IFRS 10, IFRS 11, IFRS 12, and the amendments of IAS 27 and IAS 28, in line with in the sector and,

particularly, considering the necessary standardization of policies with Optimus SGPS subsidiaries, changed

its accounting criteria for costs related to customers’ loyalty contracts. To date, these were recorded as an

expense in the year they occurred.

From 1 January 2013, the costs incurred for customers’ loyalty contracts, which include compensation

clauses in the event of early termination, are capitalized as "Intangible assets" and amortized over the period

of their contracts, since it is possible to apply a reliable cost allocation to the respective contracts, as well as

the revenue generated by each contract, thus fulfilling the criteria for capitalization required by IAS 38 -

Intangible Assets . When a contract is terminated, the net value of intangible assets associated with that

41

ZON OPTIMUS, SGPS, SA

contract is immediately recognized as an expense in the consolidated statement of comprehensive income.

This accounting policy allows a more true, fair and reliable presentation of the financial position and the

financial performance of the Group, as it allows the alignment between costs incurred with customer’s loyalty

contracts and the revenue generated.

Additionally, at the date of each statement of financial position and whenever an event or change of

circumstances indicates that the recorded amount of an asset may not be recoverable, impairment tests are

carried out to ensure that the current value of the estimated revenues associated with each contract is greater

than the amount that is capitalized.

Also, during the year ended 31 December 2013, the Group changed the accounting policy regarding the

future rights of use of movies and series. To date, these were recorded as an expense in the year they

occurred. The costs are capitalized as "Intangible assets" once it is possible to measure, reliably, the costs

incurred with each contract as well as the revenue generated, meeting the criteria for capitalization as

required by IAS 38 - Intangible assets. Additionally, the model of amortization and impairment of those

rights has been adjusted, reflecting the business and how the rights are used more reliably.

Additionally, at the date of each statement of financial position and whenever an event or change of

circumstances indicates that the recorded amount of an asset may not be recoverable, impairment tests are

carried out to ensure that the current value of the estimated revenues associated with each right is greater

than the amount that is capitalized.

Also, during the quarter ended 31 March 2014, “Net Losses / (gains) of affiliated companies” started to be

presented in “Income before financial results and taxes” (“Operational Results”), reflecting the operational

nature of investments accounted for using the equity method.

As provided under IAS 8 - Accounting Policies, Changes in Accounting Estimates and Errors , these policy

changes were applied retrospectively. Therefore changes were made to the consolidated statement of

financial position of 1 January 2013 and 31 March 2013, to the consolidated statements of comprehensive

income for the quarter ended 31 March 2013 and to the consolidated statement of cash flows for the quarter

ended 31 March 2013.

The effects of early adoption of new standards and amendments, and changes in accounting policies in the

consolidated statements of comprehensive income are presented in the tables below.

42

CONSOLIDATED MANAGEMENT REPORT 1Q14

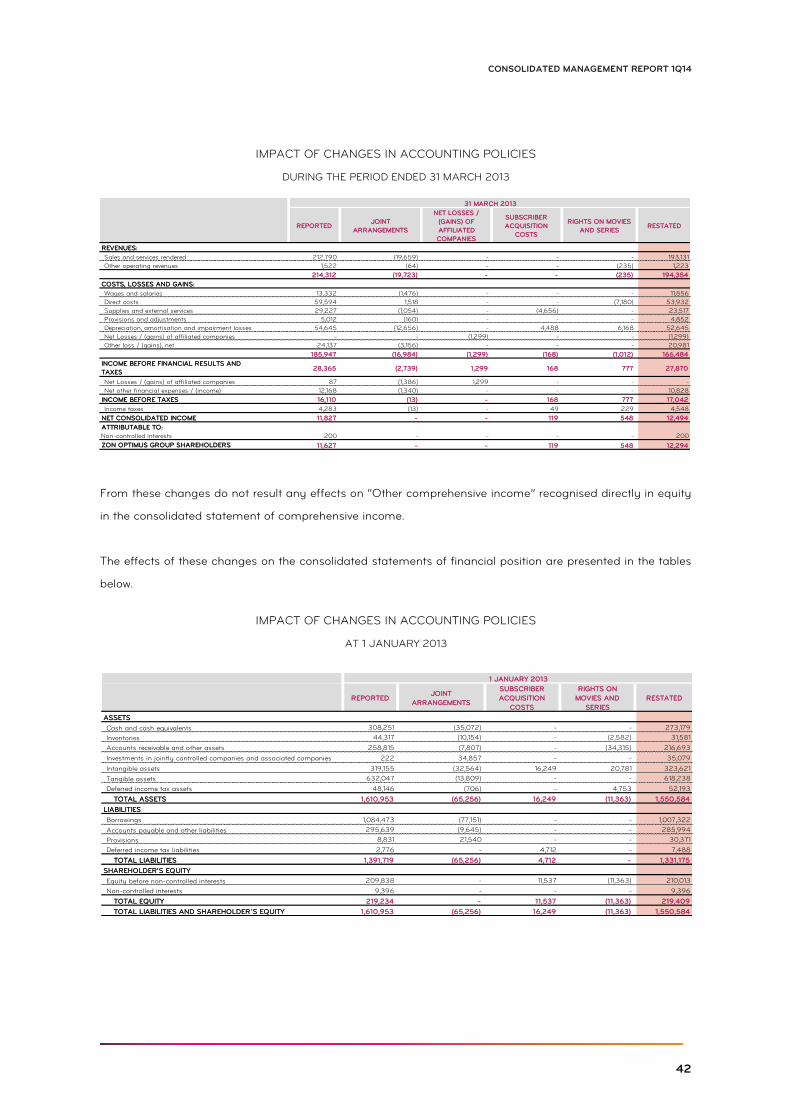

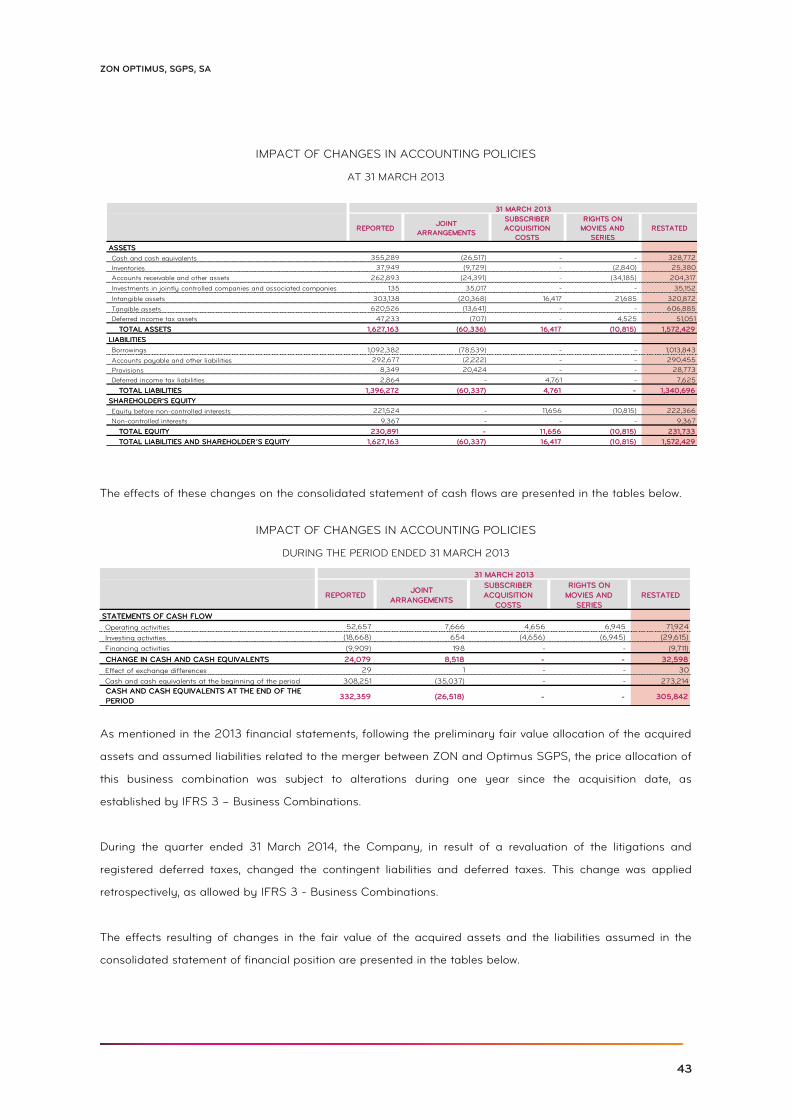

IMPACT OF CHANGES IN ACCOUNTING POLICIES

DURING THE PERIOD ENDED 31 MARCH 2013

From these changes do not result any effects on “Other comprehensive income” recognised directly in equity

in the consolidated statement of comprehensive income.

The effects of these changes on the consolidated statements of financial position are presented in the tables

below.