Embed Size (px)

Citation preview

© 2019 KPMG Tax Services Sdn. Bhd., a company incorporated under Malaysian law and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

1 Tax Developments 8 July 2019

Contents

LABUAN

Labuan Financial Services Authority (“LFSA”)’s Guidelines / Clarifications

Guidelines on Work Permit Application for Licensed and Non-Licensed Labuan Entities

Guidelines on the Establishment of Labuan Marketing Office

Circular on LIC (“Labuan Investment Committee”) Pronouncement 1-2019

CORPORATE TAX

Guidelines / Announcements

Operational Guidelines on Special Voluntary Disclosure Programme (“SVDP”)

Technical Guidelines on Dispute Resolution Proceeding

Technical Guidelines for Approval of Director General of Inland Revenue (“DGIR”) under S44(6) of the Income Tax Act, 1967 (“the ITA”)

Operational Guidelines on Procedures for Submission of Amended Return Form

Technical Guidelines on Taxation of Electronic Commerce Transactions

Technical Guidelines on Application for Approval under Subsection 44(11C) of the ITA

Technical Guidelines on Tax Treatment Related to the MFRS 121 (or Other Similar Standards) (Revised)

Guidebook for e-Form C for Year of Assessment 2019

Guideline for Second Round of Integrated Logistics Services (“ILS”) Incentive for Expansion / Diversification by Existing Approved ILS Companies

Guideline for Green Technology Tax Incentive

Update on MSC Malaysia Status Tax Incentive

Guidelines on Procedures for the Application of Automation Capital Allowance

8 July 2019

© 2019 KPMG Tax Services Sdn. Bhd., a company incorporated under Malaysian law and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

2 Tax Developments 8 July 2019

Income Tax Rules

Income Tax (Deduction for Expenditure on Issuance of Retail Debenture and Retail Sukuk) Rules 2019

Income Tax (Deduction for Expenditure on Issuance of Sukuk) Rules 2019

Income Tax (Deduction for Employment of Senior Citizen, Ex-convict, Parolee, Supervised Person and Ex-Drug Dependent) Rules 2019

Exemption Orders

Income Tax Exemption for Religious Services provided by Non-Residents

Withholding Tax Exemption in relation to Software for Personal Use

Income Tax Exemption on Export of Manufactured Goods and Agricultural Produce

Stamp Duty Exemptions for Purchase of Residential Property under the National Home Ownership Campaign 2019

SALES TAX AND SERVICE TAX

Excise Duty on Sugar Sweetened Beverages

Declaration Forms for the Breach of Exemption Conditions

Compliance Audit Framework

Guide on Sales Tax Drawback

© 2019 KPMG Tax Services Sdn. Bhd., a company incorporated under Malaysian law and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

3 Tax Developments 8 July 2019

LABUAN

Labuan Financial Services Authority (“LFSA”)’s Guidelines / Clarifications

Guidelines on Work Permit Application for Licensed and Non-Licensed Labuan Entities

The purpose of these Guidelines is to facilitate the application of work permits for expatriates working for a licensed and non-licensed entity in Labuan International Business and Financial Centre. The Guidelines are applicable to all licensed and non-licensed entities which are incorporated, licensed or registered under Labuan Companies Act 1990, Labuan Trusts Act 1996, Labuan Foundations Act 2010, Labuan Limited Partnerships and Limited Liability Partnerships Act 2010, Labuan Financial Services and Securities Act 2010 or Labuan Islamic Financial Services and Securities Act 2010. The above Guidelines came into effect on 2 April 2019 and supersede the earlier Guidelines issued on 25 February 2015, including the Clarification Note to the Guidelines which was issued on 13 March 2015. Source for the Guidelines: Official portal of LFSA

Guidelines on the Establishment of Labuan Marketing Office

The purpose of these Guidelines is to provide clarification with regard to the regulatory requirements for the establishment of Labuan Marketing Office (“LMO”) by Labuan companies outside the Labuan Island in Malaysia. The LMO is only permitted to facilitate meetings with existing clients and establish contacts with potential clients. It is not permitted to maintain books and records nor undertake trading activities, from or in the LMO. The above Guidelines came into operation with immediate effect and supersede the earlier Guidelines issued on 5 March 2014. However, all approvals, decisions, directions or exemptions granted by LFSA relating to marketing office under the superseded Guidelines shall continue to remain valid unless revoked. Source for the Guidelines: Official portal of LFSA

© 2019 KPMG Tax Services Sdn. Bhd., a company incorporated under Malaysian law and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

4 Tax Developments 8 July 2019

Circular on Labuan Investment Committee (“LIC”) Pronouncement 1-2019

LIC which comprises of the Ministry of Finance (Tax Division), LFSA and the Malaysian Inland Revenue Board (“MIRB”) has been established to recommend policies on substantial activity requirements in Labuan International Business and Financial Centre and monitor the enforcement of related regulations on substantial activity requirements. Clarifications have been made by the LIC on the following:

(a) Non-deductibility of payments made to Labuan entity by resident shall NOT be applicable to payments made by a resident general insurer to a Labuan reinsurer and payments made by a resident to a Labuan entity which has made an election to be taxed under the Income Tax Act, 1967 (“the ITA”);

(b) Labuan entities are required to self-declare their compliance to Labuan Business Activity Tax (Requirements for Labuan Business Activity) Regulations 2019 (Substance Regulations) for the basis year 2019 together with their tax filings. The manner of self-declaration will be informed to the market in due course; Labuan entities which are dormant, struck off or under winding up / liquidation process, which do not derive any source of income need not comply with substantial activity requirements.

(c) “Full time employees” is defined to include at least an officer of a managerial capacity

whilst other employees may be clerical staff / employees with non-managerial capacity.

Source for the Circular: Official portal of LFSA

© 2019 KPMG Tax Services Sdn. Bhd., a company incorporated under Malaysian law and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

5 Tax Developments 8 July 2019

CORPORATE TAX

Guidelines / Announcements

The relevant authorities have issued the following:

Operational Guidelines on Special Voluntary Disclosure Programme (“SVDP”)

Operational Guidelines No.1/2019 on SVDP (GPHDN 1/2019) supersede the earlier Guidelines dated 29 March 2019. The new guidelines are mainly issued to take into account the Ministry of Finance (“MoF”)’s media release in relation to the extension of SVDP period. The notable changes are:

(a) Extension of the SVDP period to 30 September 2019.

(b) SVDP may apply to: (i) the income or gains from disposal of chargeable assets not previously declared

for Year of Assessment (“YA”) 2017 and before; (ii) Companies with financial year ended 31 January 2018, 28 February 2018 or 31

March 2018 that have previously submitted or failed to submit their income tax return forms for YA 2018.

(c) MIRB will accept information voluntarily disclosed under the SVDP in good faith.

However, the computation of tax will be checked to ensure the accuracy of the voluntary disclosure made.

The MIRB has also updated the FAQ on SVDP to reflect the latest Operational Guidelines.

(click here for our earlier Tax Whiz for more information)

Source for the Guidelines: Official portal of MIRB

Technical Guidelines on Dispute Resolution Proceeding The Dispute Resolution Proceeding (“DRP”) is an alternative platform that may be used to resolve disputes arising from an appeal or application for relief between the taxpayers and the MIRB. It gives taxpayers the opportunity to clarify reasons for the appeal/ application for relief to an independent DRP Panel who was not involved in the raising of assessment, with an ultimate goal to achieve a settlement before the appeal/application for relief is forwarded to the Special Commissioners of Income Tax. Source for the Guidelines: Official portal of MIRB

Technical Guidelines for Approval of Director General of Inland Revenue (“DGIR”) under Subsection 44(6) of the ITA

The above Guidelines supersede the earlier Guidelines issued in January 2005 and cover the types of eligible institutions or organisations, the criteria and conditions for approval, responsibilities of an approved institution or organisation and the tax treatment of donors, amongst others. However, the guidelines do not apply to any application related to Houses of Religious Worship and Schools.

Source for the Guidelines: Official portal of MIRB

© 2019 KPMG Tax Services Sdn. Bhd., a company incorporated under Malaysian law and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

6 Tax Developments 8 July 2019

Operational Guidelines on Procedures for Submission of Amended Return Form Operational Guidelines No.3/2019 (GPHDN 3/2019) (available in Malay language only)

supersede the earlier Guidelines dated 30 November 2010. Below are the notable changes:

(a) The MIRB has encouraged the taxpayers to submit the Amended Return Form via e-filing system;

(b) The Amended Return Form will not be subject to audit unless specified under

cases as set out in the Guidelines; and (c) If the DGIR makes an amendment and issues an amended assessment within six

(6) months from the due date for submission of Income Tax Return Form, the taxpayer is not eligible to submit the Amended Return Form to the DGIR. Notwithstanding that, if the taxpayer wishes to make an amendment to the assessment through voluntary disclosure, a letter shall be forwarded to the MIRB.

Source for the Guidelines: Official portal of MIRB

Technical Guidelines on Taxation of Electronic Commerce Transactions With the evolvement of the e-commerce transactions and the emerging of new business models, the above Guidelines have been issued to replace the Guidelines issued on 1 January 2013. The guidelines define what is meant by an “e-commerce” transaction and identify the common e-commerce business models now in existence. It then covers the scope of tax liability for e-commerce business income, e-commerce transactions falling under Section 4A – Special Classes of Income and e-commerce transactions regarded as “royalty” under the new expanded definition of royalty in Section 2 (effective from YA 2017) with examples. The MIRB has previously issued a Practice Note No.1/2018 to further explain the tax

treatment on digital advertising provided by a non-resident on 16 March 2018. Click here

for our earlier e-announcement on the Practice Note No.1/2018 for more information.

Source for the Guidelines and Practice Note: Official portal of MIRB

Technical Guidelines on Application for Approval under Subsection 44(11C) of the ITA

The above Guidelines issued by the MoF cover the procedures, criteria and conditions for a social enterprise to apply for approval for project of national interest under Section 44(11C) of the ITA, the tax treatment of donors, amongst others.

Source for the Guidelines: Official portal of MoF

© 2019 KPMG Tax Services Sdn. Bhd., a company incorporated under Malaysian law and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

7 Tax Developments 8 July 2019

Technical Guidelines on Tax Treatment Related to the Implementation of MFRS 121 (or Other Similar Standards) (Revised)

The MIRB has reviewed the existing guidelines after considering the feedback from

businesses on the current tax treatment. The earlier Guidelines issued on 24 July 2015 have

now been revoked and replaced with the above Guidelines. The key changes are as follows:

(a) Entities with non-Ringgit Malaysia (“RM”) as functional currency is allowed to translate

its financial statements audited in the functional currency for reporting purpose in the

tax return using the following exchange rates:

(i) The exchange rate used to translate an audited financial statement in functional

currency into presentation currency as prescribed under MFRS 121 (only applicable

to entities adopting MFRS or other similar standards in their financial reporting); or

(ii) The average exchange rate issued by the Accountant General’s Department of Malaysia from time to time based on the rate published by Bank Negara Malaysia for the purpose of managing and accounting transaction involving foreign currencies at the date of the statement of financial position.

Source for the Guidelines: Official portal of MIRB

Guidebook for e-Form C for YA 2019 The MIRB has released the YA 2019 e-Form C and the Company Return Form Guidebook in its website. Amongst others, the YA 2019 e-Form C is accompanied by the following changes, amongst others:

(a) e-Form C incorporates a new disclosure on interest expenses subject to Earning Stripping Rules;

(b) Additional disclosure on controlled transactions; and (c) Additional disclosure on the details of foreign source income received

Guideline for Second Round of Integrated Logistics Services (“ILS”) Incentive for Expansion / Diversification by Existing Approved ILS Companies

To further enhance the capabilities of the local ILS providers, the existing approved logistics company that has enjoyed the ILS incentive (i.e. Pioneer Status or Investment Tax Allowance) can be considered for second round of ILS incentive to undertake expansion / diversification (as defined in the Guidelines) for ILS activity as follows:

(a) Income tax exemption of 70% of statutory income for a period of five years; or (b) Investment Tax Allowance of 60% on qualifying capital expenditure incurred

within five years. The allowance can be offset against 70% of statutory income of each YA.

Source for the Guidelines: Official portal of Malaysian Investment Development Authority

(“MIDA”)

© 2019 KPMG Tax Services Sdn. Bhd., a company incorporated under Malaysian law and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

8 Tax Developments 8 July 2019

Guideline for Green Technology Tax Incentive

Following from the announcement in the Budget 2019, the Malaysian Green Technology Corporation has expanded the original list of 9 assets qualifying for Green Technology Investment Tax Allowance incentive to include an additional list of 40 assets. The eligibility period for the incentive would be for the qualifying capital expenditure incurred from 1 January 2019 to 31 December 2020. Source for the Guidelines: MyHIJAU Directory

Update on MSC Malaysia Status Tax Incentive

Pursuant to the government initiative to implement the Base Erosion and Profit Shifting (“BEPS”) Action, Malaysia Digital Economy Corporation (“MDeC”) has reviewed its tax incentives granted under MSC Malaysia Bill of Guarantee No.5 (“BOG 5). Due to the review, the extension of income tax exemption period / adding of new MSC Malaysia Qualifying Activities has been put on hold since 1 July 2018. Previously, the tax exemption for MSC Malaysia Status was granted for the income derived from MSC Malaysia Approved Activities. MDeC has recently announced that the tax exemption will be granted for income derived either from the following:

Type of Activities Remarks

(a) MSC Malaysia Status Services Activities

Regulated under Income Tax (Exemption) (No.10) Order 2018 [P.U.(A) 389/2018] gazetted on 31 December 2018 and the applications can be made starting from 2 April 2019.

(b) Provision of Intellectual Property

Policy is still under review process by the Government.

Source: Official portal of MDeC

© 2019 KPMG Tax Services Sdn. Bhd., a company incorporated under Malaysian law and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

9 Tax Developments 8 July 2019

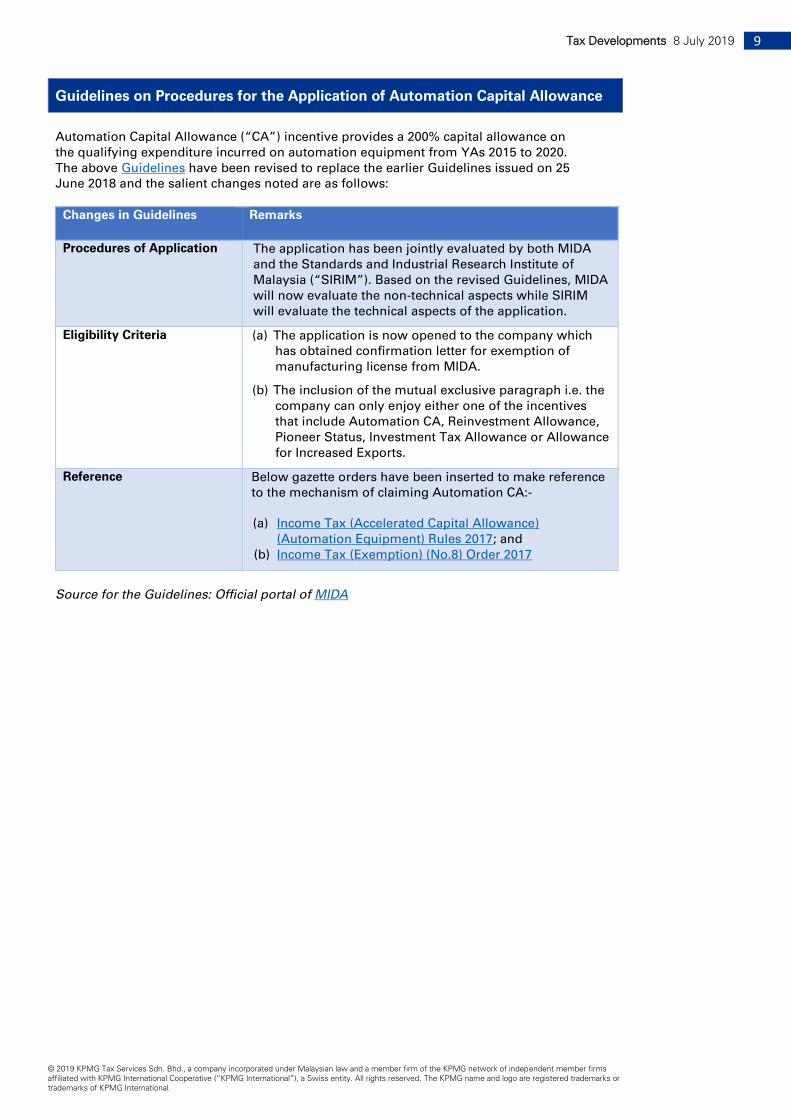

Guidelines on Procedures for the Application of Automation Capital Allowance

Automation Capital Allowance (“CA”) incentive provides a 200% capital allowance on the qualifying expenditure incurred on automation equipment from YAs 2015 to 2020. The above Guidelines have been revised to replace the earlier Guidelines issued on 25 June 2018 and the salient changes noted are as follows:

Changes in Guidelines Remarks

Procedures of Application The application has been jointly evaluated by both MIDA and the Standards and Industrial Research Institute of Malaysia (“SIRIM”). Based on the revised Guidelines, MIDA will now evaluate the non-technical aspects while SIRIM will evaluate the technical aspects of the application.

Eligibility Criteria (a) The application is now opened to the company which has obtained confirmation letter for exemption of manufacturing license from MIDA.

(b) The inclusion of the mutual exclusive paragraph i.e. the company can only enjoy either one of the incentives that include Automation CA, Reinvestment Allowance, Pioneer Status, Investment Tax Allowance or Allowance for Increased Exports.

Reference Below gazette orders have been inserted to make reference to the mechanism of claiming Automation CA:-

(a) Income Tax (Accelerated Capital Allowance)

(Automation Equipment) Rules 2017; and (b) Income Tax (Exemption) (No.8) Order 2017

Source for the Guidelines: Official portal of MIDA

© 2019 KPMG Tax Services Sdn. Bhd., a company incorporated under Malaysian law and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

10 Tax Developments 8 July 2019

Income Tax Rules

Income Tax (Deduction for Expenditure on Issuance of Retail Debenture and Retail Sukuk) Rules 2019 A company resident in Malaysia shall be allowed the following:

(a) Double deduction in respect of specified additional expenses incurred on the issuance of approved / authorised retail debenture and retail sukuk structured under the principles of Murabahah or Bai’Bithaman Ajil (based on the concept of Tawarruq), Mudharabah, Musyarakah, Istisna’ or any Shariah principle other than the principle mentioned in the next bullet point;

(b) Single deduction in respect of specified additional expenses incurred on the issuance of approved / authorised retail sukuk structured under the principle of Ijarah or Wakalah comprising a mixed component of asset and debt.

The above Rules have been issued to extend the qualifying period for this incentive for another two (2) YAs i.e. YAs 2019 and 2020.

Income Tax (Deduction for Expenditure on Issuance of Sukuk) Rules 2019 A company resident in Malaysia shall be allowed a single deduction in respect of expenses incurred on the issuance of approved / authorised sukuk structured under the principle of Ijarah or Wakalah comprising a mixed component of asset and debt.

The above Rules have been issued to extend the qualifying period for this incentive for another two (2) YAs i.e. YAs 2019 and 2020.

Income Tax (Deduction for Employment of Senior Citizen, Ex-convict, Parolee, Supervised Person and Ex-Drug Dependent) Rules 2019

An employer (who has a source of income consisting of business only) shall be allowed a double deduction in respect of the remuneration payable to his employee, who is a Malaysian citizen and resident in Malaysia, from amongst, the following:

(a) a senior citizen; (b) an ex-convict; (c) a parolee; (d) a supervised person; and (e) an ex-drug dependent

subject to meeting the prescribed conditions.

This Rules shall have effect for the YAs 2019 and 2020.

Source of the Rules: Federal Gazette Portal of the Attorney General’s Chambers

© 2019 KPMG Tax Services Sdn. Bhd., a company incorporated under Malaysian law and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

11 Tax Developments 8 July 2019

Exemption Orders

Income Tax Exemption for Religious Services provided by Non-Residents

The Income Tax (Exemption) (No.3) Order 2019 exempts a non-resident of Malaysia from income tax payment in respect of income derived from Malaysia in relation to the provision of the following religious services to qualified religious institutions or organisations, subject to conditions:

(a) Religious lectures or study of a religious book including the translation of a holy book or related religious books; or

(b) Preside prayers or rites of worship according to the ritual of each religion.

Withholding tax provision under Section 109A of the ITA shall not apply to the income exempted under this Order.

This Order came into operation on 1 February 2019.

Withholding Tax Exemption in relation to Software for Personal Use

The Income Tax (Exemption) (No.4) Order 2019 exempts a non-resident of Malaysia from income tax payment in respect of income derived from Malaysia in relation to any amount of payment for shrink-wrapped software, site-license, downloaded software or software bundled with personal computer software, smartphone or tablet received from an end user who is an individual resident in Malaysia who purchases or acquires any right to use software for personal usage and not for usage in his business.

Withholding tax provision under Section 109 of the ITA shall not apply to the income exempted under this Order.

This Order came into operation on 1 March 2019.

© 2019 KPMG Tax Services Sdn. Bhd., a company incorporated under Malaysian law and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

12 Tax Developments 8 July 2019

Income Tax Exemption on Export of Manufactured Goods and Agricultural Produce

Income Tax (Exemption) (No. 17) Order 2005 and Income Tax (Allowance for Increased Exports) Rules 1999 relating to the provision of income tax exemption on export sales of product from manufacturing or agricultural produce have been revoked and are now replaced by the Income Tax (Exemption) (No. 5) Order 2019 and Income Tax (Exemption) (No. 6) Order 2019.

Amongst others, the notable changes/updates are as follows:

(a) Issued share capital of the qualifying company must be at least 60% directly owned by Malaysian citizen;

(b) Determination of the value of increased exports is based on the difference between the average free-on-board value of export sales in a basis period with the average free-on-board value of export sales in the immediately preceding basis period where both basis periods of the qualifying company are not 12 months period ending on the same date due to change of the basis period or the qualifying company is newly incorporated;

(c) Expansion of non-application rules, where, amongst others, to include a qualifying company which enjoys double deduction on promotion of exports under the Promotion of Investments Act 1986; and

(d) Changes in harmonised system code for certain products.

Notwithstanding the issuance of the above new orders, the exemption granted under the previous Orders shall continue to be applied as if the Orders have not been revoked.

In addition, Income Tax (Exemption) (No. 7) 2019 has been gazetted to provide similar exemption to qualifying small and medium enterprises (with paid-up share capital in respect of ordinary shares not exceeding RM2.5million at the beginning of the basis period for a YA), but with a more relaxed criteria on the value added conditions.

The above exemption is not subject to the 60% Malaysian owned condition and is deemed to have come into operation from YA 2016 until YA 2020.

Stamp Duty Exemptions for Purchase of Residential Property under the National Home Ownership Campaign 2019

Stamp Duty (Exemption) (No. 2) Order 2019 and Stamp Duty (Exemption) (No. 3) Order 2019 which provides stamp duty exemptions on loan agreement and instrument of transfer executed for the purchase of residential property under the National Home Ownership Campaign 2019 has now been amended to extend the applicability period of the sale and purchase agreement executed i.e. from 1 January 2019 to 30 June 2019 to 1 January 2019 to 31 December 2019.

(Click here for Stamp Duty (Exemption) (No.2) Order 2019 (Amendment) Order 2019 and Stamp Duty (Exemption) (No.3) Order 2019 (Amendment) Order 2019 for more information)

Source of the Exemption Orders: Federal Gazette Portal of the Attorney General’s Chambers

© 2019 KPMG Tax Services Sdn. Bhd., a company incorporated under Malaysian law and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

13 Tax Developments 8 July 2019

SALES TAX AND SERVICE TAX

Excise Duty on Sugar Sweetened Beverages

In preparation for the implementation of Excise Duty (RM0.40 / litre) on sugary beverages effective 1 July 2019, the Royal Malaysian Customs Department (“RMCD”) has issued several Guidelines to assist businesses in complying with the requirements. Amongst others, it includes a list of accredited laboratories for manufacturers. Please click here for a copy of the Guidelines issued by the RMCD.

Declaration Forms for the Breach of Exemption Conditions

Various exemptions are available for qualified businesses to be exempted from paying Sales Tax and Service Tax, subject to meeting conditions. Where an exemption is granted but the person fails to comply with any conditions to which the exemptions relates, the relevant tax shall become due and payable. A copy of the Forms for the declaration of such breach of conditions is now available on the RMCD’s official portal – MySST (click here).

Compliance Audit Framework

The RMCD has issued a Compliance Audit Framework dated 30 April 2019 which sets out various aspects of RMCD’ audit, including the documents required and the rights as well as responsibilities of auditee. Click here (available in Malay version only) for a copy of the Framework.

Guide on Sales Tax Drawback

On 14 June 2019, the RMCD issued a Guide on application for drawback of Sales Tax paid on taxable goods, which are subsequently exported from Malaysia. Amongst others, the application is to be done via the JKDM No.2 Form which must be submitted within 3 months from the date the goods are exported and supported by the relevant export declarations (e.g. K2 Form).

Click here (available in Malay version only) for a copy of the Framework.

© 2019 KPMG Tax Services Sdn. Bhd., a company incorporated under Malaysian law and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

14 Tax Developments 8 July 2019

Insights on Earlier Tax Whiz / Tax Flash

Please refer below on our earlier Tax Whiz for more information.

No Subject Matter

1 Amendment Bills 2019

2 Amendment Bills 2019 – Part 2

3 Departure Levy Bill 2019

4 Goods and Services Tax ("GST") Adjustments Post 1 September 2018

5 Service Tax on Digital Services

6 Amendments to Excise Duty Regulations and Orders

7 Malaysia – New “e-CP39” System Introduced from July for MTD Data Submission

7 Malaysia – New “e-CP39” System Introduced from July for MTD Data Submission

© 2019 KPMG Tax Services Sdn. Bhd., a company incorporated under Malaysian law and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. The KPMG name and logo are registered trademarks or trademarks of KPMG International.

15 Tax Developments 8 July 2019

Soh Lian Seng

Executive Director –

Head of Tax Risk Management

+603 7721 7019

Ng Sue Lynn

Executive Director –

Head of Indirect Tax

+603 7721 7271

Tai Lai Kok

Executive Director –

Head of Tax and

Head of Corporate Tax

+603 7721 7020

Long Yen Ping

Executive Director –

Head of Global Mobility

Services

+603 7721 7018

facebook.com/KPMGMalaysia

twitter.com/kpmg_malaysia

© 2019 KPMG Tax Services Sdn. Bhd., a company incorporated under the Malaysian law and a member firm of the KPMG network of

independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity.

Although we endeavor to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it

is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice

after a thorough examination of the particular situation.

The KPMG name and logo are registered trademarks or trademarks of KPMG International.

Contact Us

linkedin.com/company/kpmg-malaysia

instagram.com/kpmgmalaysia

Bob Kee

Executive Director –

Head of Transfer Pricing

+603 7721 7029

Kuching Office

Regina Lau

Executive Director –

Kuching Tax

+6082 268 308 (ext. 2188)

Penang Office

Evelyn Lee

Executive Director –

Penang Tax

+604 238 2288 (ext. 312)

Kota Kinabalu Office

Titus Tseu

Executive Director –

Kota Kinabalu Tax

+6088 363 020 (ext. 2822)

Johor Bahru Office

Ng Fie Lih

Executive Director –

Johor Bahru Tax

+607 266 2213 (ext. 2514)

Ipoh Office

Crystal Chuah Yoke Chin

Tax Manager –

Ipoh Tax

+605 253 1188 (ext. 320)

kpmg.com/my

Petaling Jaya Office

Outstation Offices