Embed Size (px)

Citation preview

Contracts and Performance inPrivate Equity Investments ∗

Stefano Caselli Emilia Garcia-Appendini Filippo IppolitoBocconi University Bocconi University Bocconi University

[email protected] [email protected] [email protected]

August 3, 2010

Abstract

Exploiting a unique opportunity offered by the Italian private equity (PE) market, we uncovera positive relationship between the presence of covenants and several measures of performance of PEinvestments at the deal level. We conjecture that covenants contain private information availableto the contracting parties involved in the deal, and set up a structural model in which the inclusionof covenants depends on the expected increase in returns to these parties when the covenant ispresent. The structural model allows us to conclude that (i) deals with a poor governance structurehave a lower performance, (ii) PE investors have a large bargaining power, and (iii) covenants andpricing of PE deals are used by PE investors as complements.

JEL Classifications: G11, G23, G24Keywords:Private equity, venture capital, internal rate of return, covenants

∗We would like to thank MPS Venture SGR for kindly providing the data, and Francesco Corielli, Marco DaRin, Annette Schoar and two anonymous referees for helpful comments. We also thank seminar participants at theEFMA in Milan and FMA in Reno. We acknowledge financial support from CAREFIN Centre for Applied Researchin Finance. All remaining errors are our own. All authors are affiliated with the Department of Finance at BocconiUniversity, Via Roentgen 1, 20136 Milan, Italy.

Contract Characteristics andthe Returns of Private Equity Investments

Abstract

Exploiting a unique opportunity offered by the Italian private equity (PE) market, we uncovera positive relationship between the presence of covenants and several measures of performance of PEinvestments at the deal level. We conjecture that covenants contain private information availableto the contracting parties involved in the deal, and set up a structural model in which the inclusionof covenants depends on the expected increase in returns to these parties when the covenant ispresent. The structural model allows us to conclude that (i) deals with a poor governance structurehave a lower performance, (ii) PE investors have a large bargaining power, and (iii) covenants andpricing of PE deals are used by PE investors as complements.

JEL Classifications: G11, G23, G24Keywords:Private equity, venture capital, internal rate of return, covenants

1 Introduction

In this paper we examine the relationship between covenants and performance in private equity

(PE) investments, an issue that is of primary importance both for academics and practitioners. The

uniqueness and complexity of PE contracts has attracted the interest of academics as a primary

exploratory field for testing theories of optimal contracting (Kaplan and Stromberg (2002), Kaplan

and Stromberg (2004), Cumming (2008), Sahlman (1990)). At the same time, PE investors often

refer to their ability to design contracts that are more complex than plain vanilla equity and debt

as a main motive for the high profitability of their industry and a justification for charging higher

fees than mutual funds (Metrick and Yasuda (2010), Phalippou and Gottschalg (2009)).

Our major finding is that the relationship between covenants and performance is positive.

Covenants are generally associated with higher firm and investment returns, and with more success-

ful exits. Regardless of the measure of performance that one chooses − be it IRR or growth in sales,

in ROA, or in ROE (gross or annualized) − covenants are correlated with higher returns. Similarly,

covenants are associated with a higher likelihood of exiting via an IPO and a lower likelihood of

a write off. As our results are robust to different measures of performance, we conclude that the

relationship between covenants and performance is not only due to the mechanical redistribution

of cash flows associated with specific covenants, such as exit ratchets or redemption rights, which

have the effect of transferring cash flows from PE investors to insiders, or viceversa. On the con-

trary, our result suggests that covenants are associated with more fundamental differences in firm

selection, efficiency and, ultimately, profitability. Moreover, we find that the relationship between

covenants and performance is significant also when we condition for primary firm, fund and market

wide characteristics. This additional finding suggests that covenants are an important predictor of

investment performance, even after accounting for other relevant publicly observable variables.

Although the above finding may appear intuitive, it is rather non obvious. In an optimal

contracting framework, PE investors and target firm managers choose covenants so to minimize

potential agency conflicts which relate to adverse selection and double sided moral hazard (Schimdt

(2003), Cornelli and Yosha (2003), Hellman (2006), Casamatta (2003)). Generally, a model of

1

optimal contracting will offer a closed form solution in which covenants and other contractual

characteristics (the choice variables) depend solely on the parameters of the model, such as firm

and market characteristics. This in turn implies that at the optimum returns should also depend

only on the parameters of the model, and not on choice variables such as covenants.

So why do we observe a positive and significant relationship between covenants and perfor-

mance? A possible answer is that covenants are capturing private information which is observable

by some or all parties involved in the deal, but not by the wider public. While surely not the

only one, an important variable that the wider public cannot easily observe is the expectation that

the contracting parties have about future investment returns. Insofar as the inclusion of specific

covenants reveals information about expectations on returns, a regression that has returns as depen-

dent variable should include covenants as a regressors because covenants are capturing information

that is not entirely reflected in publicly observable firm and market characteristics. For example,

a lockup clause may be included in the deal only if the contracting parties believe that an IPO is

likely to occur. As an IPO is typically associated with higher returns, because it is generally the

most successful form of exit, one should expect to observe a positive relationship between lockups

and investment returns.

How can we explicitly test for the information content of covenants? As Kai and Prabhala

(2007) illustrate in the broader context of self-selection models in corporate finance, the inclusion

of covenants can be examined as a form of self selection. While self selection may be perceived as

a nuisance problem in that it leads to inconsistent estimates of parameters in a regression, it can

alternatively be employed as a test of private information theories. Puri (1996), Song (2004), Fang

(2005), Dunbar (1995) and more closely to our framework Goyal (2005) all provide examples of how

self selection can be employed to study the role of private information in relation to the choices of

economic agents.

Broadly basing our methodology on Heckman (1979) and more closely on Goyal (2005), we

then set up a structural model of self selection to examine the relationship between covenants and

performance. The model proposes a structural equation for covenants according to which the choice

of whether to include a covenant or not depends on the expected performance of the investment.

2

We conjecture that only if expected performance is sufficiently high a covenant will be included. In

particular we expect the differential between expected performance with and without the inclusion

of the covenant to determine the probability of including the covenant itself.

We then identify the reduced form equation for investment returns with and without covenants.

We conjecture that expected returns depend on firm characteristics, PE fund governance and post

investment monitoring. For the firm characteristics we employ market to book value of equity,

profitability, size, leverage and industry.

To proxy for fund governance we identify which funds are majority owned by a bank. Follow-

ing Lerner, Schoar and Wong (2007) and Hellmann, Lindsey and Puri (2008), we expect majority-

owned bank funds to have an objective function that is different from that of other funds. In

particular, the evidence suggests that majority-owned bank funds optimize the returns of the in-

vestment in equity, while also accounting for the effect that this investment has on the default risk

of the invested firm. This is particularly true when the owning bank entertains a credit relation-

ship with the invested firm, outside the fund. In the latter cases there can be a conflict between

value maximization of the equity stake and risk minimization of the credit position. As a result,

we interact fund ownership with the existence of a credit relationship and create a dummy that

takes value of one if the fund is majority owned by a bank which has a credit relationship with the

invested firm. We expect to observe lower returns in investments for which the dummy is one.

We then construct a measure of monitoring by computing the number of firms in which

a given fund manager is acting as board director. In the spirit of Lerner (1995) and Fich and

Shivdasani (2006) we expect fund managers that are simultaneously appointed as board members

of many invested firms to be less able to perform effective monitoring on firms. In other words fund

managers may be ”overstreched” and thus monitor less strictly the invested firms. Monitoring by

PE investors has a positive effect on investment returns because it leads to lower managerial moral

hazard while at the same time it maximizes the network benefits of PE sponsorship for the invested

firm. Therefore, we conjecture that, ceteris paribus, when fund managers are overstreched invested

firms perform relatively worse.

Having thus defined the independent variables of the reduced form equations of returns, we

3

can construct a reduced form equation for the use of covenants. In the reduced form equations,

we conjecture that covenants are a function of the above independent variables as well as of the

prevailing market conditions at the time of investment. As shown by Gompers and Lerner (1999,

2000), market conditions at the time of contracting have an impact on the choices of PE investors,

in particular on pricing, for which we control by including the ratio of market value of equity −as

priced in the deal− to book value of equity. We conjecture that market conditions are also likely

to affect other terms of contracting, such as the inclusion of covenants.

We then start estimating the model step by step. First, we estimate the structural equation

of covenants and compute the inverse Mills ratio that we use in the performance regressions to

adjust for the selectivity bias. To exclude the effect of bargaining power on pricing and other

redistribution effects linked to covenants we use change in sales, rather than IRR, as a main measure

of performance. Our findings are, however, robust to the various performance measures outlined

above.

Second, we estimate the performance regressions and find that fund governance is an impor-

tant determinant of performance. In particular, when the dummy for the credit relationship is one,

we observe a reduction in expected annualized sales growth in the range of 1.9 to 2.5%. Further-

more, we find that each extra firm for which a fund director is required to act as board director,

causes a drop in annualized sales growth of approximately 0.3%. We then conclude that fund gover-

nance and monitoring are two important determinants of investment performance, thus confirming

the predictions of Fich and Shivdasani (2006) on the role of monitoring in PE investments and the

findings of Hellmann, Lindsey and Puri (2008) on the effect of governance.

Finally, using the predictions from the performance regressions, we can estimate the covenant

regressions. In a Probit setup we find that the probability of including a lockup clause or an tag

along right increases with the differential in expected performance of PE investors. Furthermore,

covenants appear to be inversely related to pricing, proxied here by the market to book ratio of

equity. This indicates that pricing and covenants are complements, which suggests that they at least

partially reflect bargaining power. When PE investors have more bargaining power, they obtain

lower prices and impose more covenants. Finally, we show that the inclusion of covenants depends

4

positively on prevailing market conditions at the time of contracting. If the relative number of IPOs

and returns in public markets have been high in the six months preceding the deal, we observe a

larger use of covenants. We interpret this finding as also consistent with an explanation based on

bargaining power.

To our knowledge this is the first paper that addresses empirically the relationship between

contracts and performance in PE investments. There is existing work on the performance of PE

investments at the fund level (Ljungqvist and Richardson (2003), Kaplan and Schoar (2005), Lerner,

Schoar and Wong (2007)) but these studies are generally unconcerned about contract characteristics,

simply because contract design occurs at the investment level, not at the fund level. This suggests

that the relationship between covenants and performance necessarily requires the use of investment

level data which is, however, typically not available.

To some extent our research question has been touched upon by Cumming (2008) whose

focus is on the relationship between contracts and exits. He shows that ex-ante stronger PE control

rights increase the likelihood that an entrepreneurial firm will exit via a trade sale, rather than

through a write-off or an IPO. Although his findings indirectly shed some light on the relationship

between contracts and returns, we believe that the variability of returns irrespectively of the form

of exit remains largely unexplored.

In this paper we are able to fill this gap in the literature because we have access to an

uncommonly rich database which contains information on performance, as well as on contract

characteristics, including covenants and governance, at the investment level. We are thus able to

examine the relationship between these variables, and draw conclusions on the effect that contracts

have on returns. Thanks to MPS Venture SGR, the largest active Italian fund, we have access to a

proprietary database that contains the entire universe of completed transactions performed in Italy

by Italian PE investors during the period 1999–2008. The database contains information on the

type of investment distinguishing between early-stage, expansion capital, buy-out and turnaround

finance, exit form, internal rate of return, deal covenants, leverage, percentage of shares owned by

the PE fund, governance characteristics of the invested firm, as well as a number of other accounting

variables for target firms.

5

The rest of the paper is organized as follows. We dedicate Section 2 and 3 to the discussion

of covenants and governance in PE investments. In Sections 4 and 5 we describe the data collection

process and provide some descriptive statistics about our data. Section 6 documents the positive

relationship between covenants and performance. In Section 7 we set up the structural model of

self-selection and present the main results. Conclusions are left to Section 8.

2 Covenants in Private Equity Deals

PE contracts are characterized both by special securities, such as preferred stock, and by the

presence of covenants. The seminal paper in this field is by Kaplan and Stromberg (2002) who

study a sample of contracts between PEs and invested firms. They observe that the distinguishing

characteristic of these contracts is to allow PEs to separately allocate cash flow rights, board rights,

voting rights, liquidation rights and other control rights. These rights are often contingent on

observable measures of financial and non-financial performance.

Subsequent work investigates the effect that covenants have on incentives. There are four

types of agency problems in the PE investment process (Kaplan and Stromberg (2004), Casamatta

(2003), Schmidt (2003)). First, PE investors may be concerned that managers and other executive

inside shareholders are not maximizing the value of the investment, and similarly managers may

be concerned that PE investors do not exert enough effort (double-sided moral hazard). Second, if

insiders know more about the quality/ability of the target firm than do PE investors, then there

may be a problem of adverse selection. Third, a hold-up problem exists if managers with valuable

human capital threaten to leave the firm. The fourth agency problem relates to control : After the

investment, there will be circumstances when PE investors disagree with managers and the former

will want the right to make decisions.

The first three problems outlined above (moral hazard, adverse selection, hold up) indicate

that appropriate contract design is needed to minimize the agency costs. The literature shows that

as a response to moral hazard, PE investors typically tie managerial compensation to performance

(Holmstrom (1979)). As a response to adverse selection, PE investors screen managers of different

6

ability using – again - pay-for-performance contracts (Lazear (1986)). As an alternative screening

mechanism Ross (1977) and Diamond (1991) propose the use of liquidation rights. To deal with

hold-up problems, PE investors can introduce incentive mechanisms based on vesting of managers’

shares (Hart and Moore (1994)). Finally, control theories such as Aghion and Bolton (1992),

Dewatripont and Tirole (1994), and Dessein (2005) show that a solution to the latter problem is to

give control to PE investors in some states and to managers in others.

Covenants tied to a PE contract provide a way to implement the mechanisms necessary to

mitigate the agency and control problems outlined above. For example, Kaplan and Stromberg

(2004) find that greater internal and external risks are associated with more PE cash-flow rights

and PE control rights. Hellman (2006) shows that allocating convertible preferred equity with

automatic conversion to PEs is optimal, because it restores their incentives to promote IPOs (see

also Casamatta (2003) and Cornelli and Yosha (2003)). Cumming (2008) relates the characteristics

of PE contracts to the means by which a PE fund exits, and finds that ex-ante stronger PE control

rights increase the likelihood that an entrepreneurial firm will exit via a trade sale, rather than

through a write-off or an IPO.

In this paper we relate the variability of the performance of PE investments to the presence of

covenants. Table 1 shows the covenants that we include in our analysis: lockup clauses, permitted

transfer rights, redemption rights, tag-along rights, drag-along rights, rights of first refusal, and

exit ratchets. Lockup clauses prohibit, to some or all of the existing firm shareholders, the sale

of shares before a predetermined date. Permitted transfer rights give to some of the shareholders

the permission to make transfers of shares without having to offer them first to the remaining

shareholders. Redemption rights force the firm to buy shares at a predetermined price (a put).

Tag-along rights allow minority shareholders to include their shares in other shareholders’ sales, at

the same price. Drag-along rights force minority shareholders to sell when the majority decides to

sell their own shares. Rights of first refusal, or pre-emption rights, give existing shareholders the

right to be the first to purchase the shares owned by other shareholders, before they are sold to

new investors. Finally, exit ratchets allow shareholders to adjust their participation on the firm

depending on firm performance or on an exit (vesting).

7

Inclusion of each of these covenants in a PE contract can have an effect on managerial

incentives and on cash distribution, as well as act as a proxy for firm quality and market power.

For example, an exit ratchet tends to favor insiders in that their equity stake in the firm increases

when certain predetermined performance targets are met by the firm (cash distribution). The

presence of an exit ratchet thus has the effect of providing the incentives on managers to exert

effort and meet such a performance target (incentives). All else equal, PE investors would prefer

not to increase the equity stake of insiders; thus the inclusion of an exit ratchet in a PE contract

signals a high bargaining power of the insiders relative to the PE investors (market power). Finally,

an exit ratchet can be placed by PE investors into very profitable deals to make the investment

more attractive to insiders (firm quality).

By using several return measures that proxy for the performance of the PE investments for

different stakeholders of the investment, as well as a structural model for covenants, our approach

abstracts from cash distribution and incentive considerations, and focuses on the role of covenants

as proxies of market power and firm quality. As we shall see below, according to the structural

model the choice of whether to include a covenant or not depends on the expected performance of

the investment. As a result, the model shall enable us to uncover the determinants of inclusion of

each covenant into the PE contract, and the role of other firm characteristics in the performance of

the investments.

3 Governance of Private Equity Funds

A second way of implementing the mechanisms that mitigate the agency and control problems iden-

tified above is by imposing a correct governance structure and providing monitoring incentives. The

role of governance and monitoring in PE investments has been previously analyzed by Nikoskelainen

and Wright (2007). The authors find that value increase and return characteristics of LBOs are

to some extent related to the corporate governance mechanisms resulting from a leveraged buyout,

especially managerial equity holdings. They show that return characteristics and the probability of

a positive return are mainly related to size of the buyout target and other acquisitions carried out

8

during the holding period.

We identify two main governance measures that are relevant for addressing managerial agency

costs: First, the number of firms in which the fund manager is acting as board director. This variable

proxies for the ability of PE investors to monitor managers via direct representation in the board of

the firm (Lerner (1995)). In the spirit of Fich and Shivdasani (2006), we expect fund managers that

are simultaneously appointed as board members of many invested firms to be less able to perform

effective monitoring on firms. In other words, fund managers may be too busy to efficiently monitor

the invested firm.

Among the governance measures we also include the ownership of the fund because it has

been identified in the literature as tied to performance. Lerner, Schoar and Wong (2007) distinguish

between different classes of LPs and find that endowments’ average annual returns from PE funds

are nearly 14% greater than for the average investor. Funds selected by investment advisors and

banks lag sharply. This finding is in line with Hellmann, Lindsey and Puri (2008) who suggest

that banks as limited partners might diverge from maximizing returns on investments in order

to maximize future banking income from the portfolio of firms in which they invested. Following

these findings, we then envisage that bank ownership has a direct impact on fund governance and

an indirect one on firm governance. We therefore interact fund ownership with the existence of a

credit relationship and create a dummy that takes value of one if the fund is majority owned by a

bank which had a previous credit relationship with the invested firm. We expect to observe lower

performance in investments for which the dummy is one.

4 Data and Sample Selection

We use a proprietary database of PE deals which was provided to us by MPS Venture SGR, a

PE management company that is currently one of the most active PE players in Italy, and the

largest one in terms of assets under management. The database covers the entire universe of exited

transactions sponsored by Italian investment management companies in Italy in 1999-2005 and

exited no later than March 2008.

9

Data were collected by MPS Venture SGR from several sources. First, Bank of Italy provided

information on all investment companies managing PE investments in Italy. According to European

regulation (the 1998 Financial Services Directive), all PE investment management companies must

register with the Central Bank of their country of incorporation, and must disclose their ownership

structure as well as the names of each of the funds they manage, some of the funds’ governance

characteristics, and the aggregate number of deals made by each fund. Deal-level information is

not required to be disclosed to the Central Bank; however, the majority of Italian management

companies disclose deal information on a voluntary basis to the Italian Private Equity and Venture

Capital Association (AIFI). AIFI coverage of deal information represents 70 to 75% of all deals

registered at the Bank of Italy, depending on the year. Information disclosed by AIFI to MPS

Venture SGR includes the name of each invested company, the type and size of the investment,

the percentage of shares acquired by the PE fund, entry and exit dates, the type of exit, leverage,

IRR, and the covenants used for each deal, among others. Information provided by AIFI has then

been complemented by MPS Venture SGR on the basis of private interviews with fund managers,

so to cover the missing 25-30% of deals that were not reported to AIFI. This process has allowed a

complete mapping of all deals registered at the Bank of Italy.

Deal-level information was then merged with Bureau Van Dijk’s AIDA/Amadeus Database,

and with the Italian Balance Sheet Central Database (Centrale di Bilanci) to obtain balance sheet

information about each of the invested companies. Information about whether the invested company

had a previous relationship with the bank that owns the PE management company was obtained

from the compulsory registers of the Italian Credit Bureau (Centrale dei Rischi). Finally, data

on the activity of the board members of each fund was obtained from the registers of the Trade

Ministry (Camera di Commercio), Bank of Italy, and Italian Security and Exchange Commission

(Consob).

Due to privacy restrictions, MPS Venture SGR provided us the data without disclosing

the names of PE management companies, funds, and invested companies. This implies that we

are unable to merge our data back into publicly available databases such as Amadeus/AIDA to

complement the balance sheet information that we may be still missing. Also, we cannot distinguish

10

between first, second or higher rounds of financing to the same firm. Finally, we do not know which

firms are public or private at the time of investment.

For each deal, we were provided with information about the type of investment (early-stage,

expansion capital, buy-out and turnaround finance), the exit strategy (trade sale, IPO, write-off),

the entry and exit dates, the total and annualized internal rate of return, the deal covenants (lockups,

permitted transfer, redemption right, tag-along right, drag-along right, right of first refusal, exit

ratchet), the leverage used, the percentage of shares of the invested firm held by the PE fund, the

invested firm’s sector and its organizational form. We also have a few governance characteristics

of the management company (percentage of shares of the management company owned by type

of investor, start year of management company, number of funds managed) and of the PE fund

managing the investments (date of establishment, presences of board director appointed by the fund

to the invested firm in other portfolio firm boards, whether the fund director is external or internal

to the fund). For bank-owned PE management companies, we have information about whether the

invested firm had a previous relationship with that bank. Finally, we were provided with limited

accounting information about invested firms at the time of entry (sales, EBITDA, book value of

assets, book value of equity, book value of debt) and on the rate of growth of sales, ROA and ROE

during the investment period. We complemented the database provided by MPS Venture with

data on the Italian market (public market returns, ratio of IPOs over newly created firms, industry

leverage and ROE) using information from Datastream and AIDA/Amadeus.

5 Sample Characteristics

The sample includes 782 investments made by 87 PE funds, which are respectively owned by a

total of 58 management companies. A large fraction of the invested firms operates in the consumer

goods sector (34%), the general industrial sector (25%), and the services sector (20%). Consistently

with the structure of the Italian corporate sector, we find that most invested firms in the sample

are privately owned by individuals and families (69.28%). Banks, PE investors and managers

respectively control 1.87%, 17.04% and 11.82% of the invested firms before the investment.

11

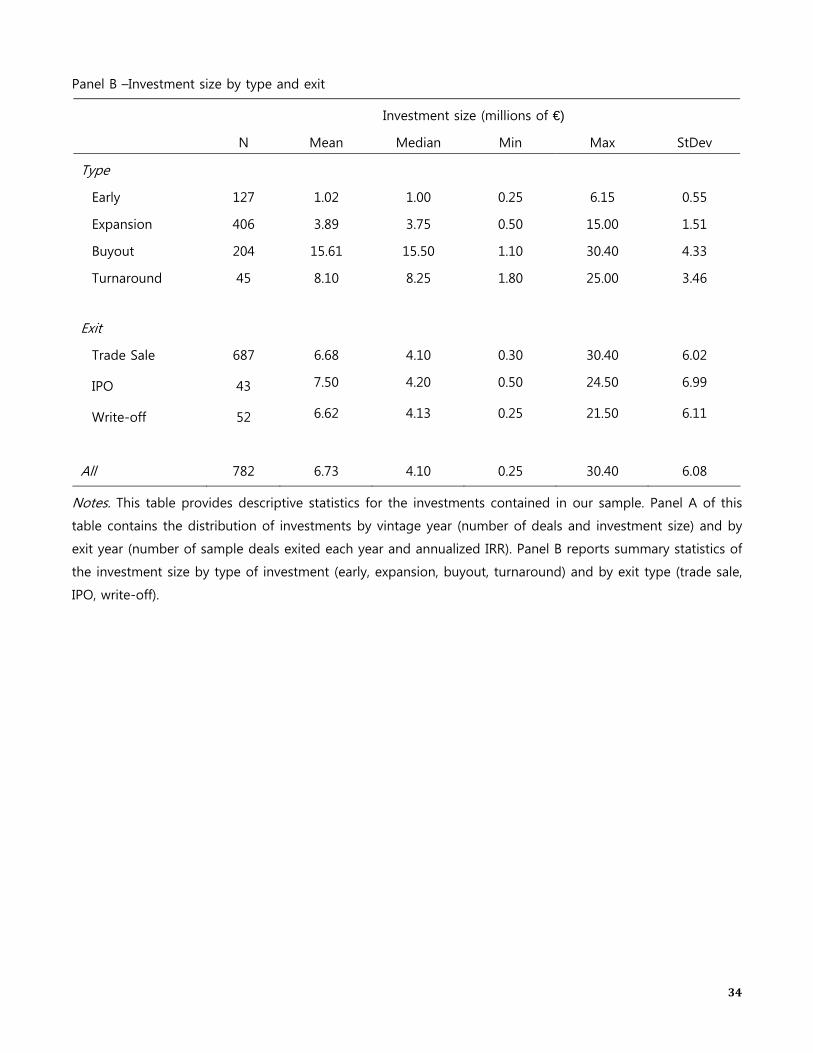

Table 2 offers key summary statistics on the investments contained in our sample. All

investments were financed between 1999 and 2005, with 2000, 2001 and 2004 being peak years. The

median investment size is 4.1 million euros. Deals in our sample exited between 1999 and 2008

and had median annualized internal rate of return ranging from 8.6% to 49.31%, depending on the

year of exit, with the greatest performance observed during the technology bubble of 1999-2001.

As mentioned before, we classify investments in early stage, expansions, buyouts and turnarounds.

The majority of our deals are expansion financing (51.9%), followed by buyouts (26.1%), early stage

(16.2%) and turnaround (5.75%). As Panel B of Table 2 shows, early stage and expansion deals are

much smaller than buyouts and turnarounds. Buyout deals include the largest deals in our sample

(the largest one is e30 million), which however look small by international standards, particularly

if compared to the large buyouts recently witnessed in the US and the UK (see for example Table

4 of Axelson et al. (2010) for statistics on large US and European buyouts).

Most of the deals in our sample where exited via a trade sale (87.85%). In our sample, a trade

sale is defined as the sale of the firm to a well identified third party, such as another PE fund or a

corporation. IPOs and write-offs are relatively rarer, respectively 5.50% and 6.65%. Although not

tabulated, we note that IPOs are more commonly associated with buyouts and expansions than for

early-stage and turnarounds. Turnarounds are generally quite risky and are therefore more likely

to end in a write-off.

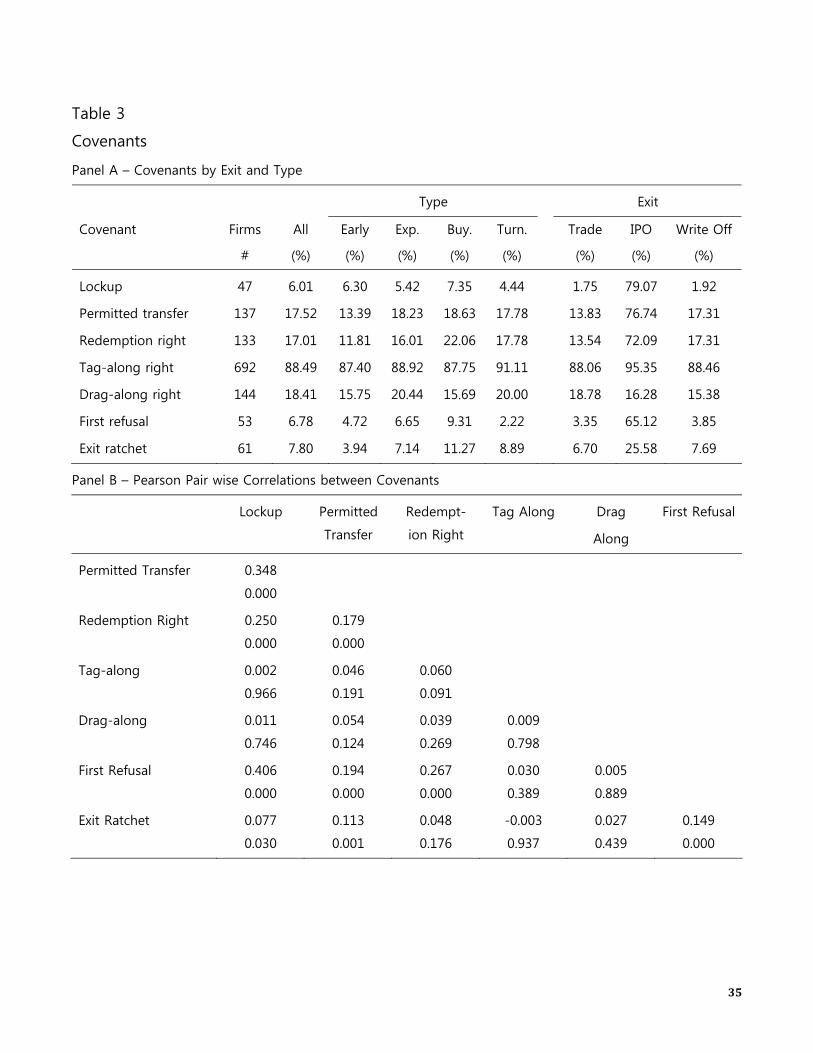

Table 3 provides a picture of the distribution of the deal covenants which include: lockups,

permitted-transfer restrictions, redemption right, tag-along right, drag-along right, rights of first

refusal, and exit ratchet. Panel A shows that tag-long rights are the most common covenant (88.49%

of the deals), followed by drag-along rights, permitted transfer and redemption righs. There is

relatively little variation in the use of covenants across the different investment types. However,

covenants are related to the form of exit. For example, the use of lockups, permitted transfers

or rights of first refusal is more commonly associated to IPOs than to deals exited otherwise. As

discussed before, this is probably due to the endogeneity between the use of covenants, investment

returns and exit strategy.

As some deals employ several covenants simultaneously, in Panel B of Table 3 we report

12

the correlations between these covenants. We find that lockups, permitted transfers, redemption

rights and rights of first refusal exhibit a positive and significant correlation. Finally, in Panel C we

analyze the distribution of covenants across time. We observe that there was a general tendency

towards more ‘covenant-lite’ contracts throughout the years, with especially obvious reductions in

the percentage of contracts including tag-along rights, drag-along rights and redemption rights.

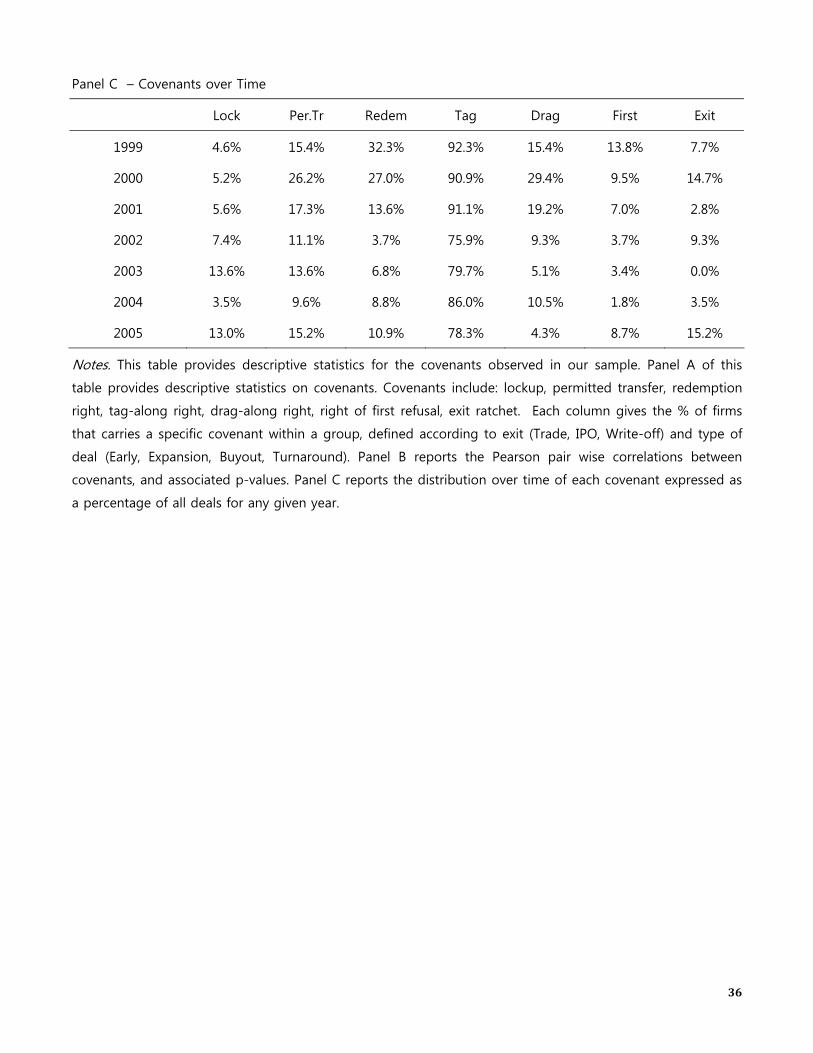

In Table 4 we provide means and medians of several performance measures for all investments

and by investment type and exit. As measures of performance, we use gross and annualized internal

rates of returns of the PE investment, and growth in sales, in ROA, and in ROE during the

investment period. These are proxies for the returns to private equity investors (IRR), to all

stakeholders in the firm (sales growth and growth in ROA) and for equity holders (growth in

ROE). Comparing the numbers across different rows, we note that the most profitable investments

independently of the type of stakeholders to the firm were buyouts, while the less profitable ones were

early-stage investments. We also note that deals exited through and IPO performed considerably

better than trade sales.

6 The Relationship between Covenants and Performance

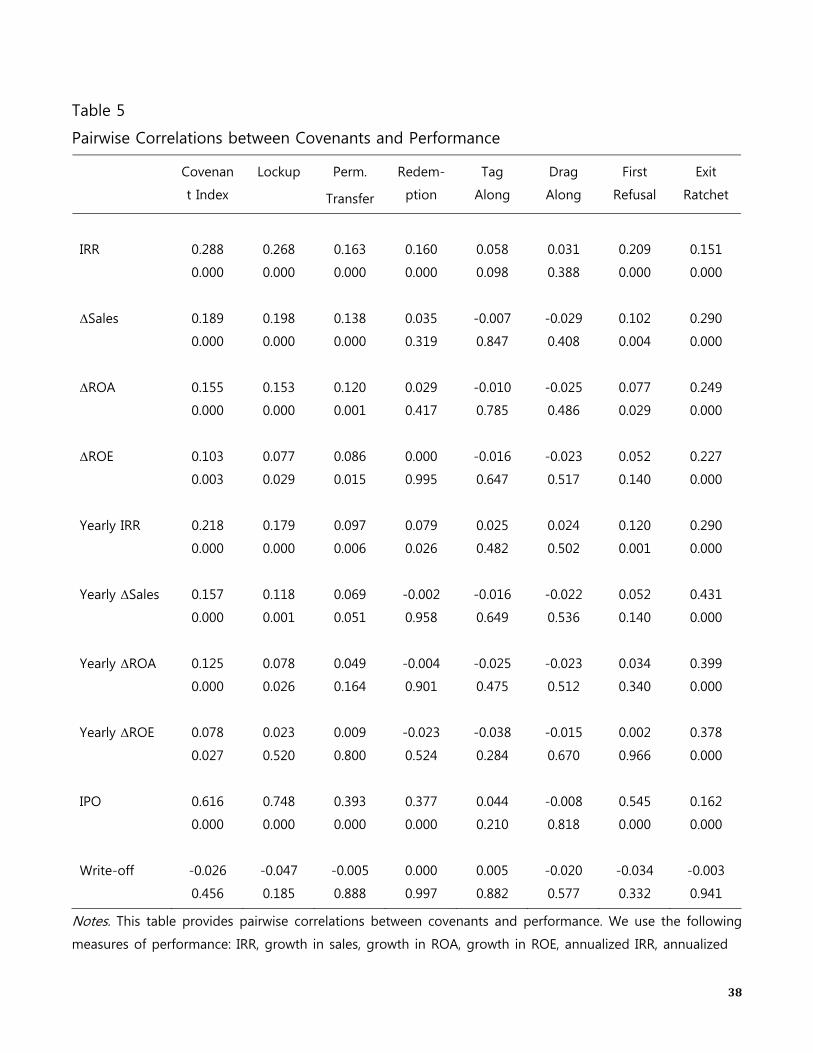

We start our analysis of the relationship between covenants and performance by observing the

pairwise correlation between our performance measures and covenants. As performance measures

we use the eight variables introduced before (gross and yearly IRR, sales growth, ROA growth,

and ROE growth), plus exit via an IPO and via a write-off, where the latter is an inverse measure

of performance. As covenants we include lockups, permitted transfer, redemption right, tag-along

right, drag-along right, right of first refusal, and exit ratchets. We also aggregate all of these

covenants into an index, covenant index, which contains the total number of such covenants and

measures how restrictive the contract is. For each pair of performance measure and covenant, we

report the pairwise correlation coefficient together with its significance level (p-level). Results are

contained in Table 5. The table shows that covenants are positively correlated with all of the

performance measures except write-off, as expected, although the latter negative relationship is

13

not significative. The positive correlation between performance and the presence of covenants is

persistent across all performance measures and is mostly apparent for lockup clauses, permitted

transfer, exit ratchet, and the covenant index.

Next, in Table 6 we compare the univariate differences on average performance measures

between deals that contain the above described covenants and those that do not, using parametric

t-tests and non-parametric Wilcoxon tests of differences on means. Panel A shows that the average

annualized IRR is always higher for the deals containing a covenant (X=1) relative to deals that

do not have one (X=0), and significantly so for all except drag- and tag-along rights. Similarly,

Panel B shows that annualized change in sales is higher when the covenant is present except for

tag-along rights, drag-along rights, and redemption rights, where the differences in means are not

significant. In the last line of each of the tables in Panels A and B we aggregate the covenants into

a new measure which contains a one when a deal has any covenant except tag-along right (as the

latter, we recall, is present in almost every deal). Performance is always higher when a covenant is

present relatively to when it is not present, and significantly so for most measures of performance.

The relationship between covenants and performance observed in Table 5 continues to hold. For

reasons of space, we only report the t-tests for the differences in annualized IRR (Panel A) and

annualized growth in sales (Panel B), but the results are qualitatively very similar for the other

six continuous measures of performance (annualized growth in ROA and in ROE, gross IRR, gross

growth in sales, in ROA, and in ROE).

We next explore whether the positive relationship between covenants and performance found

before can be attributed to observable characteristics about firms or deals. To this end, we per-

form a multivariate analysis where we regress each of our measures of performance on each of

our covenant dummies (or the covenant index defined before) and a set of controls. As controls,

we include a number of firm and deal characteristics (market to book value of equity of the PE

deal; pre-investment profitability, size, and leverage of the invested firm; industry dummies; type of

investment dummies; vintage year of investment dummies; investment duration), and governance

characteristics (whether the invested firm had a previous relationship with the bank owning the PE

fund, as well as the number of presences of the board director appointed by the fund to the invested

14

firm on other portfolio firms of the management company owning the fund). The equations that

we estimate have the following general form:

yi = α+ βCi + γFXFi + γGX

Gi + εi.

Here, yi refers to one of each of the ten previously identified measures of performance (gross and

annualized growth in sales, in ROE, and in ROA; gross and annualized IRR; exit through a write-off

or through an IPO). Ci are the covenants. In each model specification, we respectively include as Ci

a dummy variable for the inclusion of each covenant (lockup clauses, permitted transfer, redemption

rights, tag-along rights, drag-along rights, right of first refusal, and exit ratchet) or the covenant

index. Finally, XF refers to the firm-deal characteristics, and XG are the governance controls. In

each model specification we maintain fixed the vectors of controls XF and XG and we choose one

performance measure and one covenant dummy (or the index). As a result we estimate 80 different

models. We use OLS to estimate all equations involving a continuous measure of performance, and

probit models to estimate the equations involving exits via an IPO or a write-off. We cluster the

standard errors at the fund level to account for similar contracting strategies. The results of all

of the regressions performed above are summarized in Table 8. As reference, we include in Table

7 the definitions of the control variables included in the analysis, their mean and median, and

their pairwise correlations with one of our variables of interest (covenant index) and two of our

performance measures (IRR and growth in sales during the investment period).

Panel A of Table 8 contains the complete model specifications for the regressions of each

of our performance measures on the covenant index. In Panel B we report only the estimated β

coefficients for each of the single covenants on each of the performance measures. The estimated

coefficients of the control variables are qualitatively very similar to the ones reported in Panel A.

The first and central finding of Table 8 is that the relationship between covenants and per-

formance survives to the inclusion of the observable control variables. This is true both when

we aggregate covenants into the index (Panel A) and for each covenant by itself (Panel B). The

only cases where this positive relationship is not statistically significant are tag-along rights and

15

drag-along rights, just as we found in the univariate analysis of Table 6.

Another finding of Table 8 is that governance measures are also significantly correlated with

performance. We observe a negative relationship (i) between having had a previous relationship

with the bank owning the PE fund and the performance of the PE investment, and (ii) between

performance and the number of presences in boards of other portfolio firms of the board director

appointed by the fund to the invested firm. The former relationship is in line with Hellmann, Lindsey

and Puri (2008) who suggest that banks as limited partners might diverge from maximizing returns

on investments in order to maximize future banking income from the portfolio of firms in which

they invested. The latter is consistent with Fich and Shivdasani (2006), who find that a director

sitting simultaneously in many boards can be too “busy” to perform correct monitoring.

Returning to the fundamental issue of the positive relationship between performance and

covenants, should this relationship hold once we control for all firm, deal, fund, and market char-

acteristics? In a complete information setup the answer is no. Let us consider a simple theoretical

model in which y(C,X) is a measure of firm performance, which depends on the choice of covenants

to be included in the contract, C, and a set of exogenous parameters, X. If we assume that contracts

are chosen optimally to maximize the performance and concavity of y, then the optimal contract

must satisfy the first order condition ∂y/∂C = 0. This implies that the optimal choice function

C∗(X) depends only on X. As a consequence, the optimal value of y is y∗(C∗(X), X) = y∗(X). In

other words, performance does not depend on C. X determines both the choice of covenants C∗

and performance y∗.

So why do we observe this positive relationship between covenants and contracts, even after

controlling for all possible observable characteristics? We envisage two possibilities: sample selection

or unobserved heterogeneity.1

Let us consider first the possibility that our results are driven by sample selection. As

discussed in the data section, our sample is representative of all Italian PE deals except that it does

not contain investments that have not been exited. If it is solely due to this selection mechanism

that we arrive at observed relation between covenants and performance, then our results could be

1We thank an anonymous referee for providing the model and the basic arguments contained here and in theprevious paragraph.

16

spurious. To determine whether this is the case, we would have to study the relationships between

covenants and performance in the sample of non-exited investments, or at the very least correct for

sample selection bias using a Heckman selection model or a similar mechanism. Unfortunately, we

cannot carry out any formal analysis because we do not have any information about the deals that

have not been yet exited. While recognizing this econometric limitation, we nevertheless attempt

to argue indirectly that the effect of sample selection on our results should not be significant.

Because we cannot observe whether the relationship between covenants and performance is

reversed within the sample of unobserved deals, we shall use previous literature to infer the average

performance of the unobserved deals, as well as the average use of covenants within this sample, and

draw a conclusion on how these two should be related. On the first front (performance on unobserved

deals), previous research has shown evidence for a negative relationship between performance and

exit. For example, Cochrane (2005) estimates that average log returns to venture capital should be

substantially reduced after accounting for sample selection because market valuations are observed

only when a firm goes public, receives new financing, or is acquired; all of which are events associated

with good returns. Similarly, Phalippou and Gottschalg (2009) find that a large number of non-

exited investments are ‘living dead’ investments, i.e. deals where there has been virtually no activity

and should be in effect written off, but that have not yet been written off. These papers give us

reasons to think that the average quality of the unobserved deals is lower than the quality of the

deals that are on our sample.

Regarding the relationship between exits and covenants, we resort to Cumming (2008), which

is to the best of our knowledge the only paper that addresses the issue of the use of covenants in a

context where both exited and non-exited deals are included. Conveniently, his sample comprises

European deals, and the summary statistics for the exited deals covered in his sample are quite

similar to ours. In Table 3, Cumming (2008) reports the proportion of deals containing covenants on

the full sample of exited and non-exited investments, and on the subsamples of IPOs, acquisitions,

and write-offs. While proportions are not available for the subsample of non-exited investments,

we may infer whether there are systematic differences across exited and non-exited investments

by comparing the proportions within the complete sample with the proportions within each of

17

the exit channels using weighted averages, where weights are assigned according to how populated

each group is. We find that non-exited deals have on average less covenants than the exited deals.

For example, Cumming finds that redemption rights are present on 37% of all deals (exited and

non-exited), on 31% of IPOs, on 54% of acquisitions, and on 30% of write-offs. Because IPOs,

acquisitions and write-offs represent respectively 14.3%, 33.2% and 28.7% of the total number of

deals, then we infer that the remaining non-exited deals should have a proportion of 25.3% of

redemption rights, which is lower than for all exited categories.2 Similar exercises on the other

covenants reported by Cumming yield similar results. We conclude that non-exited deals have on

average less covenants than deals that have been exited.

Joining the arguments of the previous two paragraphs, we infer that unobserved deals have

both lower average performance and lower average number of covenants. As such, we have reasons

to believe that the positive relationship between performance and covenants should not be reversed

with the inclusion of the non-exited deals which we are not observing.

Instead, we believe that the positive relationship observed between covenants and perfor-

mance can be explained by unobserved heterogeneity. As explained above with the simplified

model, under complete information we should not observe any relationship between performance

and covenants. In reality, PE investors and particularly firm managers are privately informed about

the underlying quality of the investments, and we, as econometricians, do not have access to the

full information set. It is plausible that covenants are capturing the private information that some

or all of the parties involved in the PE investment have. Empirically, this means that the effect of

contracts on performance is capturing precisely some unobserved heterogeneity effect.

One important variable that cannot be observed easily by an econometrician is, for example,

the expectation that the contracting parties have about future returns to their investments. If the

inclusion of covenants reveals information about investors’ expectations about future performance,

a regression that has some measure of performance as a dependent variable should include covenants

as one of the regressors. This is simply because covenants are capturing information that is not

entirely reflected in publicly observable firm and market characteristics. For example, a lockup

2We calculate the proportion on non-exited deals as 0.37 − 0.143 × 0.31 − 0.332 × 0.54 − 0.287 × 0.30.

18

clause may be included in the deal only if the contracting parties believe that an IPO is likely to

occur. An IPO is typically associated with higher returns, because it generally the most successful

form of exit. As a result, we obtain a positive relationship between lockups and investment returns.

In the following section we develop a structural model of self selection that enables us to examine

the relationship between covenants and performance in the context of private information.

7 Empirical Model and Results

7.1 A structural self selection model

As previously suggested, we expect the use of covenants to be influenced by unobservable expec-

tations about investment performance. These expectations are part of the information set that

determines the shape of the contract at the time of investment, which means that the use of

covenants depends on expected performance while in turn performance depends on covenants. In

other words, covenants and performance are endogenously determined. As Li and Prabhala (2007)

illustrate, the issue of simultaneity between contract characteristics and returns is common in cor-

porate finance empirical specifications. It can be generally reconducted to a problem of simultaneity

in self-selection. More precisely, the choice of covenants represents here a form of self selection that

can be used to test for private information regarding expected returns, an interpretation that is

broadly consistent with the modeling framework of self selection of Heckman (1979).

A model set up in which covenants are jointly determined with returns is provided by Goyal

(2005), who examines the joint determination of yield spreads and covenants in a sample of debt

issues. In the framework of Goyal, an issuer’s choice of covenants depends on a consideration of

the expected reduction in yield spreads from offering a more restrictive contract and the net other

costs associated with reduced managerial flexibility.

Adapting Goyal’s model to our context, the decision to include a covenant in the PE contract

can be written as the following probit model:

Pr(Ci = 1) = f (γ(y1i − y2i) + Z ′iξ) (1)

19

where Ci is a dummy variable for the inclusion of the covenant in the contract, y1i is the

expected return on an investment with covenants, and y2i is the expected return on an investment

without covenants; in this way, (y1i−y2i) is the expected increase in performance when the covenant

is included in the contract, relative to where it is not included. Zi contains other variables that

may affect the choice of introducing a covenant apart from the expectations on performance. In

the empirical specification, Zi contains firm and fund-specific characteristics, as well as market

conditions at the time of the investment.

Expected performance is different when the covenant is included and when it is not, so we

model these two separately as a function of vectors XFi and XG

i which we defined in the previous

section:

y1i = XF ′i β1F +XG′

i β1G + u1i, (2)

y2i = XF ′i β2F +XG′

i β2G + u2i. (3)

Equation (2) is the performance regression for investments with covenants and Eq. (3) is for

investments with covenants. We cannot estimate Equations (1)–(3) separately because expected

performance is conditioned on the inclusion of the covenant or not. We therefore implement a

procedure based closely on Goyal (2005) (and which itself borrows from Lee (1978) and Maddala

(1983)) to correct for the bias.

The procedure consists in substituting the performance equations (2) and (3) into the covenant

choice equation (1). This allows us to obtain a reduced-form model in which covenants are solely

a function of firm-deal and governance characteristics, XF , and XG, as well as a vector of market

condition controls ZM :

Pr(Ci = 1) = f(XF ′

i θF +XG′i θG + ZM ′

i ξ). (4)

Equation (4) is estimated using a probit model with maximum likelihood, and the linear

predictions, ψi = XF ′i θF + XG′

i θG + ZM ′i ξ are used to calculate the inverse Mills ratio, which is

defined as φ(ψ)/(1 − Φ(ψ)) when covenants are not included and −φ(ψ)/Φ(ψ) when covenants

20

are included. As usual, φ is the standard normal density function and Φ is the standard normal

cumulative distribution function.

As Lee (1978) and Maddala (1983) show, consistent estimates of β1F , β2F , β1G and β2G

are obtained by augmenting Eqs. (2) and (3) with the inverse Mills ratio as the right-hand side

variables, and estimating the equation with OLS. Finally, by substituting the difference in expected

performance for the whole sample, y1i − y2i, into the structural probit equation (1), we obtain

consistent estimates of the structural probit model parameters γ and ξ.

7.2 Estimates from Performance Regressions

In applying the methodology described in the previous section to our data, the first important issue

to consider is that Equations (2) and (3) model the expected performance for each deal. We do

not have an explicit measure of the expected performance for each deal; the best approximation

for expected performance available to us is the realized performance, as measured by the eight

continuous measures of performance that we used previously (gross and annualized IRR, sales

growth, ROA growth, and ROE growth). We therefore use these measures in the estimations of the

reduced-form equations for returns. As variables XF and XG, we include the same sets that we

used in the OLS regressions of performance on covenants of Section 6, and for the pre-investment

market controls ZM we use the market returns for the six months previous to the investment, the

ratio of IPOs to new firms created in Italy during the six months previous to the investment, and

the average ROE for the firms in the same industry as the target firm.

In this section, we report the coefficients of the OLS estimations of Equation (3) augmented

with the inverse Mills ratio obtained by fitting Equation (4).3 Because it is difficult to interpret

the signs of the combinations of coefficient γ with β1F , β2F , β1G and β2G, we omit the probit

estimations of Equation (4); we solely compute the inverse Mills ratio from these estimations.

Finally, we postpone the discussion of the estimated coefficients for the structural model (1) to the

3In fact, the first stage involves estimation of Equations (2) and (3). For reasons of space we only report the latter.The results for the OLS estimations of Equation 2 augmented with the corresponding Mills ratio, are qualitativelyvery similar but present lower significance levels for the coefficients due to the fact that deals that do not containcovenants are in general more populated than those that have the covenant and therefore the sample size for theseestimations is much smaller (the only exceptions are tag-along rights, which are included in the majority of contracts).

21

next section.

Coefficients of Equation (3) augmented with the inverse Mills ratio obtained by fitting Equa-

tion (4) are presented in Table 9. Each column of the table contains the estimated coefficients

for the reduced-form equations for each of the seven covenants available in the sample: lock-up,

permitted transfer, redemption right, tag-along right, drag-along right, right of first refusal, and

exit ratchet. The number of observations in each regression is different as it reflects the number of

deals that do not have the corresponding covenant. All the columns have as dependent variable the

annualized growth in sales as we believe that this is the best measure of firm performance which

is neutral regarding how cashflows are distributed among the different investors. In Section 7.4 we

discuss the results for other performance measures.

The main finding of Table 9 is that governance characteristics are good predictors of perfor-

mance. Deals that have bad governance perform on average worse than those that do not. The

presence of a busy board director in the board of the portfolio firm significantly reduces performance.

Similarly, firms that are financed by funds owned by a bank that previously had a relationship with

the firm perform worse than others. The economic significance of these variables varies depending

on which covenant and sample (with or without covenant) is considered. The values reported, cor-

responding to the sample where covenants are not included, imply that a director that increases the

number of presences in boards of fund portfolio firms by one would decrease the annualized growth

in sales by 0.3 to 0.4%. Analogously, being managed by a fund owned by a bank with which the

firm had a previous relationship leads to a gross growth in sales which is, ceteris paribus, 1.7% to

2.2% lower than for firms that are not in a similar situation. Considering that the average growth

in sales is 7%, this effect is considerable.

Although in the light of the structural model presented above the regressions of Table 8 are

misspecified, we note that the negative effect of a bad governance on performance is a feature that

we had already observed there. We do not report the selection-adjusted effect on growth of sales for

the sample of deals containing the covenant; nevertheless, the negative impact of the governance

measures on the performance measures is also present in those untabulated regressions. In this case,

the ranges of the impact of one more presence of the director in the board of other portfolio firms

22

on growth of sales goes is from -0.1% to -1.4%, where the maximum value occurs when lockups are

present. Similarly, being owned by a fund with which the firm had a previous relationship leads

to a gross growth in sales which is approximately 2.5% lower than for other firms, although due to

sample size considerations the latter results are less statistically significant on the samples where

the covenants are present.

We conclude that funds with a bad governance structure in place – where by governance we

refer to the incentives towards value maximization of the management company owning the fund

that invests in the firm, as well as the degree of busyness of the board director appointed by the

PE fund to the invested firm – perform worse than those with a better governance structure. As

mentioned before, these results are consistent respectively with Hellmann, Lindsey and Puri (2008)

and with Fich and Shivdasani (2006). In Section 7.4 we shall discuss about the robustness of these

results.

7.3 Determinants of the Use of Covenants

We now turn to a discussion of the estimations of the structural equations determining the use of

covenants, Equation (1), in order to uncover what drives the variation in the choice of contracts by

PE investors. The estimated coefficients are contained in Table 10.

Panel A contains the coefficients for Equation (1), considering each covenant by itself, i.e.

independently of the inclusion or exclusion of the other covenants. Acknowledging that the inclusion

or exclusion of each covenant depends on which other covenants are present in the deal, in Panel B

we condition each covenant choice on the rest of the covenants. Both Panels A and B are estimated

using as a measure of performance the difference in the annualized increase in sales when the

covenant is included, relatively to when it is not included. Finally, because the choice of covenants

could reflect expected returns for PE investors (rather than for any general stakeholder to the firm),

in Panel C we repeat the estimations of Panel B using the difference in annualized IRR when the

covenant is included relative to when it is not included as the measure of performance.

Panel A of Table 10 shows that that the probability of including each covenant is rather

independent of the differential in general firm performance (as measured by annualized sales growth)

23

when such covenant is included, relatively to when it is not included. A notable exception for this

neutral relationship between performance differential and covenant inclusion are redemption rights,

which are unexpectedly negatively related to the differential. We explore whether this negative

relationship results because we are ignoring that the decision to include each covenant is done jointly

with all other covenants. To consider the co-determination of all covenants in a simple manner,

in Panel B we condition the choice of each covenant on the presence of the other covenants. The

negative relationship still holds after conditioning on the other covenants; however, we notice that

the presence of redemption rights are very positively correlated with lockup clauses, themselves

positively correlated with performance differential. By simply conditioning on the presence of the

other covenants we are probably failing to capture the feedback effects of the choice of one covenant

on the others, obtaining as a result this unexpected negative sign of the differential on performance

on the inclusion of the covenant.

The measure of performance used in Panels A and B is sales growth, a measure that does not

consider how returns are distributed among the different stakeholders to the firm. It is possible that

each of the stakeholders estimates the expected returns differential of including a covenant, and that

at the end the determination of which covenant to include is determined by the relative bargaining

power of each of the parties involved. As a result, the inclusion of each covenant could be neutral or

even detrimental to the overall firm performance (as seems to be the case with redemption rights),

but beneficial to some of the parties involved. To investigate this possibility from the PE investors’

point of view, we substitute the differential in sales growth with the differential in annualized IRR.

In Panel C we present the estimated coefficients for Equation (1) when we consider the differential

in annualized IRR as the measure of performance in Equations (2) and (3). We find that the

differential of IRR when the covenants are included is positively related with most covenants, and

statistically so with lockup clauses and tag along rights. We infer that the inclusion of lock-up

clauses and tag-along rights was most beneficial for PE investors than for the other stakeholders in

the firm. These covenants were probably determined by a high bargaining power of PE investors

who benefitted the most by their inclusion, even though we do not find statistical evidence that

with their inclusion the overall expected firm performance is better. Regarding the other covenants,

24

we only find a negative relationship between covenants and IRR differential for permitted transfer

clauses (although not statistically significant), and once again, for redemption rights, albeit with

a slightly lower economic significance than in the regressions in Panels A and B. However, once

again we notice that the presence of redemption rights is strongly positively correlated with the

presence of lockup clauses, themselves positively correlated with performance differential. It would

be interesting as a further research to consider a more formal model for the co-determination of all

covenants, considering the feedback effects of the choice of one covenant on the others.

Other results in Table 10 are very similar across the different panels. For example, the

negative coefficients for the market to book value of equity that are present Panels A, B, and C,

indicate that covenants are inversely related to pricing. This relationship is in fact statistically

significant for redemption rights and tag-along rights. This negative relationship indicates that

pricing and these covenants are complements, i.e., when PE investors obtain lower prices they also

impose more covenants. As well as the previous ones, these results also suggest that PE investors

have a large bargaining power.

Results in Table 10 also show that smaller firms, as well as firms that were more profitable at

the time of the investment, are more likely to contract with covenants. Using firm size as an inverse

proxy for information asymmetry, then the former result is consistent with the use of covenants

to reduce moral hazard and adverse selection. The latter result is consistent, once more, with a

high bargaining power of PE investors who use covenants to extract more returns from the most

profitable firms.

Finally, Table 10 also shows that the inclusion of covenants depends positively on prevailing

market conditions at the time of contracting. If the relative number of IPOs and returns in public

markets have been high in the six months preceding the deal, we observe in general a larger use of

covenants. Similarly, when the average industry return on equity has been high in the previous six

months before the deal, inclusion of covenants is more likely. These findings suggest that prevailing

market conditions at the time of investing affect how PE investors contract with invested firms, and

are consistent with Gompers and Lerner (1999, 2000). This finding also suggests that PE investors

have more bargaining power.

25

7.4 Robustness Checks

As robustness checks for the results for the previous section, we also perform the regressions con-

tained in Table 9 (Equation (3)) using the other continuous measures of performance (gross increase

in sales, and gross and annualized IRR, increase in ROE, and increase in ROA). The results -which

we do not report for reasons of space-, are qualitatively very similar. In particular, the negative

relationship between both our governance measures on performance appears in all of our regres-

sions, and is in most cases very strongly statistically significant independently of which covenant

or measure of performance we use. Instead, the statistical and economic significance of the rest of

the controls on performance changes slightly depending on the sample and performance measure

considered, although the signs are relatively stable across all the specifications. Therefore, we feel

comfortable in drawing inferences of the effect of governance on performance, which is rather per-

sistent and significative, and survives after controlling for the endogeneity between contracts and

performance.

We also repeat the estimations in Table 10 using the differential in the other measures of

performance (increase in ROE, increase in ROA; estimations not reported). Consistently with the

results described in the previous section, we find that the differential in performance as measured by

ROA is not related to the inclusion of covenants, with the only except being redemption rights which

are negatively correlated with the performance differential. We also find that lockup clauses and

drag-along rights are positively correlated with the differential in the increase in ROE, suggesting

that these covenants were put in place by all equity investors. The rest of the variables have roughly

the same signs as those reported in Table 10, with statistical significance varying depending on the

measure of performance used. The main conclusions of the previous section thus remain unchanged.

8 Conclusions

In this paper we examine the relationship between the performance of PE investments and contract

characteristics. We identify covenants and governance as the two main contract features that are

relevant for the analysis (Kaplan and Stromberg (2002, 2004)). Previous research shows that the

26

choice of securities is also important. However, we find that in Italy PE investors generally report

to hold common equity. This does not imply that they effectively hold a plain equity contract, as

the addition of covenants fundamentally changes the nature of the payoffs associated with their

securities.

We find that there is a strong positive relationship between the presence of covenants and

investment performance. This relationship is robust to several measures of performance of the firm;

therefore it is not dependent on how cash flows are distributed among the different parties involved

in the PE investment. The positive relationship between covenants and return is also robust to the

conditioning on several control variables that are likely to affect performance of the PE investments.

We argue that in an optimal contracting setup, this relationship between covenants and performance

should not exist, so the positive relationship must be reflecting unobserved heterogeneity / private

information available to the parties involved in the PE contracting.

Recognizing that covenants must be capturing private information, we set up structural

models of self selection according to which the choice of whether to include each covenant depends

on the expected performance of the investment. Through the structural models we observe that

investments that have weak PE governance measures (such as those that are owned by a bank,

or those that have busy directors) perform worse than than the average PE investment. The

structural models also allow us to conclude that PE investors have more bargaining power than

other shareholders, and that PE investors use pricing and covenants as complements. We model

the inclusion of each covenant independently of the others; leaving a simultaneous model for all

covenants for future research.

27

References

[1] Aghion, P. and P. Bolton (1992): “An Incomplete Contracts Approach to Financial Contract-

ing,” Review of Economic Studies 77, 338-10l

[2] Axelson, U., T. Jenkinson, P. Stromberg and M. S. Weisbach (2010): “Leverage and Pricing

in Buyouts: An Empirical Analysis”, Working Paper, SIFR

[3] BVCA (2007): “A Guide to Venture Capital Term Sheets”, British Venture Capital Associa-

tion, http://www.bvca.co.uk/

[4] Casamatta, C. (2003): “Financing and Advising: Optimal Financial Contracts with Venture

Capitalists,” Journal of Finance, 58(5), 2059–2085

[5] Cochrane, J. H. (2005): “The Risk and Return of Venture Capital,” Journal of Financial

Economics, 75(1), 3–52

[6] Cornelli, F., and O. Yosha (2003): “Stage Financing and the Role of Convertible Securities,”

Review of Economic Studies, 70(1), 1 – 32

[7] Cumming, D. (2008): “Contracts and Exits in Venture Capital Finance” Review of Financial

Studies, 21(5), 1947–1982

[8] Dessein, W. (2005): “Information and Control in Alliances and Ventures,” Journal of Finance,

60(5) 2513-2549

[9] Dewatripont, M. and J. Tirole (1994): “A Theory of Debt and Equity: Diversity of Securities

and Manager-Shareholder Congruence,” Quarterly Journal of Economics 109, 1027-1054

[10] Diamond, D. (1991): “Debt Maturity Structure and Liquidity Risk,” Quarterly Journal of

Economics 106, 709-737

[11] Dunbar, C.G. (1995): “The use of warrants as underwriter compensation in initial public

offerings,” Journal of Financial Economics, 38, 59-78

28

[12] Fang, L.H. (2005): “Investment bank reputation and the price and quality of underwriting

services,” Journal of Finance 60 (6), pp. 2729-2761

[13] Fich, Eliezer M. and A. Shivdasani (2006): “Are Busy Boards Effective Monitors?”, Journal

of Finance 61 (2), pp. 689-724

[14] Gompers, P., and J. Lerner (1999): “An analysis of compensation in the U.S. venture capital

partnership,” Journal of Financial Economics, 51 (1), 3-44

[15] Gompers, P., and J. Lerner (2000): “Money Chasing Deals? The Impact of Fund Inflows in

Private Equity Valuations,” Journal of Financial Economics, 55, 281–325

[16] Goyal, V.K. (2005): “Market discipline of bank risk: Evidence from subordinated debt con-

tracts,” Journal of Financial Intermediation, 14, 318-350

[17] Hart, O. and J. Moore (1994): “A Theory of Debt Based on the Inalienability of Human

Capital,” Quarterly Journal of Economics 109, 841-879

[18] Heckman, J.J. (1979): “Sample selection as a specification error,” Econometrica, 47, 153-161

[19] Hellmann, T. (2006): “IPOs, Acquisitions, and the Use of Convertible Securities in Venture

Capital,” Journal of Financial Economics, 81, 649-79

[20] Hellmann, T. F., L. Lindsey and M. Puri (2008): “Building Relationships Early: Banks in

Venture Capital,” Review of Financial Studies, 21(2), 513-541

[21] Holmstrom, B. (1979): “Moral Hazard and Observability,” Bell Journal of Economics 10, 74-9l

[22] Kaplan, S. and A. Schoar (2005): “Private Equity Performance: Returns, Persistence and

Capital Flows”, Journal of Finance, 60 (4), 1791–1823

[23] Kaplan, S. N. and P. Stromberg (2002): “Financial Contracting Theory Meets The Real World:

An Empirical Analysis of Venture Capital Contracts,” Review of Economic Studies, 70(2), 281–

315.

29

[24] Kaplan, S. N. and P. Stromberg (2004): “Characteristics, Contracts, and Actions: Evidence

from Venture Capitalist Analyses,” Journal of Finance, 59(5), 2173–2206.

[25] Lazear, E. (1986): “Salaries and Piece-rates,” Journal of Business 59, 405-43l

[26] Lee, L.F. (1978): “Unionism and wage rates: a simultaneous equations model with quantitative

and limited dependent variables,” Int. Econ. Rev. 19, 415-433

[27] Lerner, J. (1995): “Venture Capitalists and the Oversight of Private Firms,” Journal of Finance

50, 301-318

[28] Lerner, J., A. Schoar and W. Wong (2007): “Smart Institutions, Foolish Choices?: The Limited

Partner Performance Puzzle,” Journal of Finance 62, 731–64.

[29] Li, K. and N.R. Prabhala (2007): “Self-Selection Models in Corporate Finance,” in “Handbook

of Corporate Finance Volume I,” edited by B.Espen Eckbo, Elsevier 2007.

[30] Ljungqvist, A. and M. Richardson (2003): “The Cash-Flow, Return and Risk Characteristics

of Private Equity,” NYU, Finance Working Paper, (No. 03-001).

[31] Ljungqvist, A. and M. Richardson (2003b): “The Investment Behavior of Private Equity Fund

Managers,” Mimeo

[32] Maddala, G.S. (1983): “Limited-Dependent and Qualitative Variables in Economet-

rics,”Cambridge Univ. Press, Cambridge.

[33] Metrick, A. and A. Yasuda (2010): “The economics of private equity funds,”Review of Financial

Studies (23), pp. 2303-2341

[34] Nikoskelainen, E. and M. Wright (2007): “The Impact of Corporate Governance Mechanisms

in Value Increase in Leveraged Buyouts,” Journal of Corporate Finance 13, 511–537

[35] Phalippou, L. and O. Gottschalg (2009): “The Performance of Private Equity Funds”, Review

of Financial Studies 22(4), 1747–1776

30

[36] Puri, M. (1996): “Commercial banks in investment banking: Conflict of interest or certification

role?,” Journal of Financial Economics, 40, 373-401

[37] Ross, S. (1977): “The Determination of Financial Structure: The Incentive Signaling Ap-

proach,” Bell Journal of Economics 8, 23-40

[38] Sahlman, W. A. (1990): “The Structure and Governance of Venture Capital Organizations”,

Journal of Financial Economics 27, 473–521

[39] Schmidt, K.M. (2003): “Convertible securities and venture capital finance,”Journal of Finance

58 (5), pp. 2059-86

[40] Song, W. (2004): “Competition and coalition among underwriters: The decision to join a

syndicate,”Journal of Finance, 59, 2421-2444.

[41] Yates, G and M. Hinchliffe (2010): “A Practical Guide to Private Equity Transac-

tions,”Cambridge University Press

31

32

Table 1

Definitions of Covenants

Lockup A provision in the underwriting agreement between some or all existing

shareholders that prohibits the sale of shares before a predetermined date.

Permitted Transfer The permission to make transfers of shares without pre-emption in favor of the

remaining shareholders. The types of permitted transfers may vary according to

the class of shares. Where the class of shares is held by PE investors, there will

usually be a permitted transfer provision allowing transfers between two or more

separate funds managed by the same PE manager. These mechanisms are often