Embed Size (px)

Citation preview

Copyright © 2008 Pearson Addison-Wesley. All rights reserved.

Chapter 25

The Difference between Short-Run and Long-Run Macroeconomics

25-2Copyright © 2008 Pearson Addison-Wesley. All rights reserved.

In this chapter you will learn to

1. Explain why economists think differently about short-run and long-run changes in macroeconomic variables.

2. Describe how changes in GDP can be decomposed into changes in factor supply, the utilization rate of factors, and productivity.

3. Explain why short-run changes in GDP are mostly caused by changes in factor utilization, whereas long-run changes in GDP are mostly caused by changes in factor supplies and productivity.

4. Explain why macroeconomic policies will have a long-run effect on output only if they influence factor supplies or productivity.

25-3Copyright © 2008 Pearson Addison-Wesley. All rights reserved.

Inflation and Interest Rates in the United StatesThe Federal Reserve’s long-term objectives are a stable overall price level, sustainable real GDP growth, and “moderate” long-term interest rates.

However, the Federal Reserve has responded to an inflationary gap by raising interest rates.

Do high interest rates and the recessionary gap created by the Federal Reserve consistent with its goal?

Two Examples

25-4Copyright © 2008 Pearson Addison-Wesley. All rights reserved.

But in the long run, the downward pressure on wages (recessionary gap) causes inflation and interest rates to fall.

In the short run, the rise in interest rates causes aggregate expenditure to fall, reducing output.

The key to this puzzle:

- recognize the different short-run and long-run effects of monetary policy

The Monetary Policy Puzzle

25-5Copyright © 2008 Pearson Addison-Wesley. All rights reserved.

Saving and Growth in Japan

For the decade following 1990, Japan’s economy was stagnant. Some argue there was too much saving (and too little spending).

Many also argue that Japan’s economic success since World War II was due in part to its high saving rate.

How can both views be correct?- recognize the different short-run and long-run effects of saving

25-6Copyright © 2008 Pearson Addison-Wesley. All rights reserved.

In the short run, an increase in desired saving leads to less aggregate desired spending economic slump.

But in the long run, greater saving expands the pool of funds, drives down interest rates, and makes investment more attractive.

More investment in capital leads to increases in the economy’s long-run productive potential economic growth.

Saving and Growth in Japan

25-7Copyright © 2008 Pearson Addison-Wesley. All rights reserved.

A Need to Think Differently

Short run:

- emphasize changes in output as deviations from potential

- limited price and wage adjustment

Long run:

- emphasize changes in output as changes of potential

- considerable wage and price adjustment takes place

25-8Copyright © 2008 Pearson Addison-Wesley. All rights reserved.

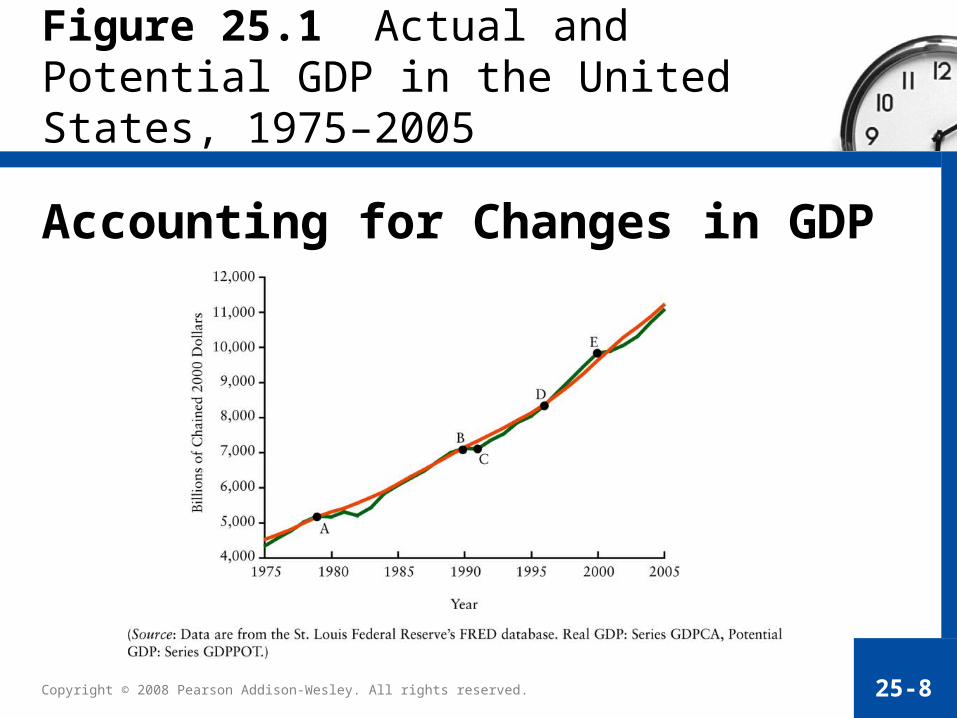

Accounting for Changes in GDP

Figure 25.1 Actual and Potential GDP in the United States, 1975–2005

25-9Copyright © 2008 Pearson Addison-Wesley. All rights reserved.

Different Types of Changes in GDP

Figure 25.1 shows two types of changes in GDP:

1. some changes that involve departures of actual GDP from potential GDP (e.g., B to C)

2. change in GDP that involves changes in potential GDP (e.g., B to D)

Therefore, to study:

1. long-run trends: focus on the change in potential output

2. short-run fluctuation: focus on the change in the output gap

25-10Copyright © 2008 Pearson Addison-Wesley. All rights reserved.

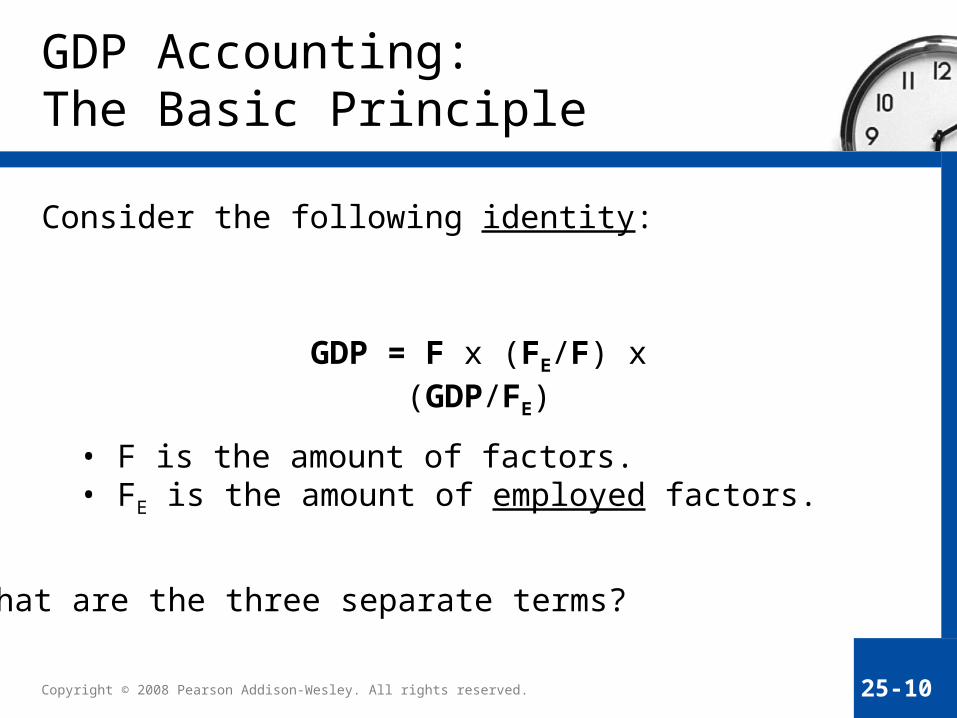

GDP Accounting: The Basic Principle

Consider the following identity:

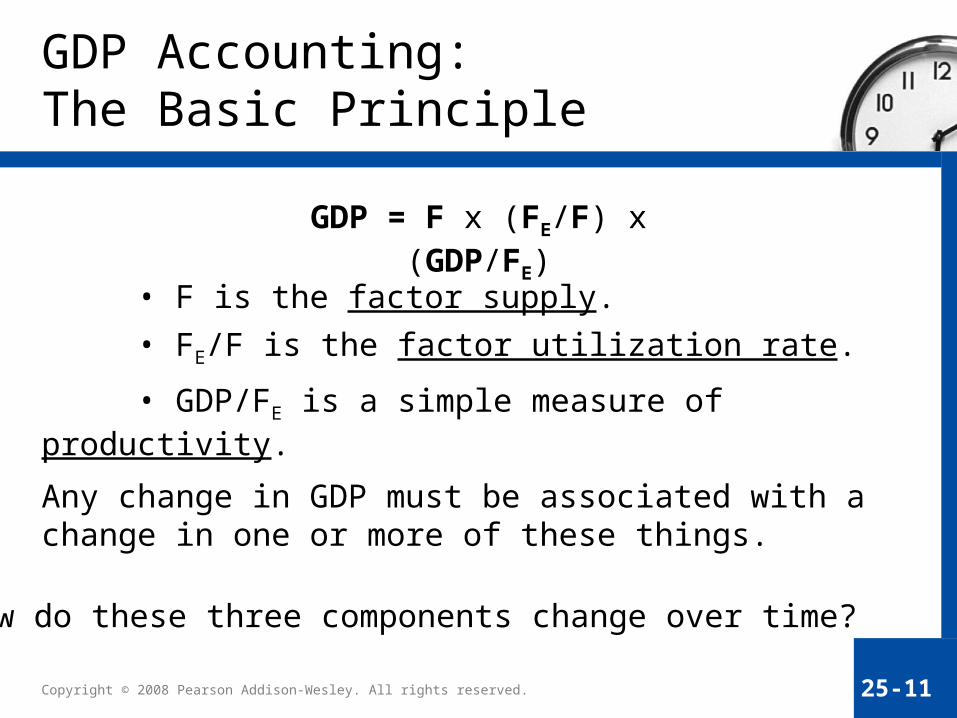

GDP = F x (FE/F) x (GDP/FE)

• F is the amount of factors. • FE is the amount of employed factors.

What are the three separate terms?

25-11Copyright © 2008 Pearson Addison-Wesley. All rights reserved.

• F is the factor supply.

Any change in GDP must be associated with a change in one or more of these things.

• GDP/FE is a simple measure of productivity.

• FE/F is the factor utilization rate.

GDP = F x (FE/F) x (GDP/FE)

How do these three components change over time?

GDP Accounting: The Basic Principle

25-12Copyright © 2008 Pearson Addison-Wesley. All rights reserved.

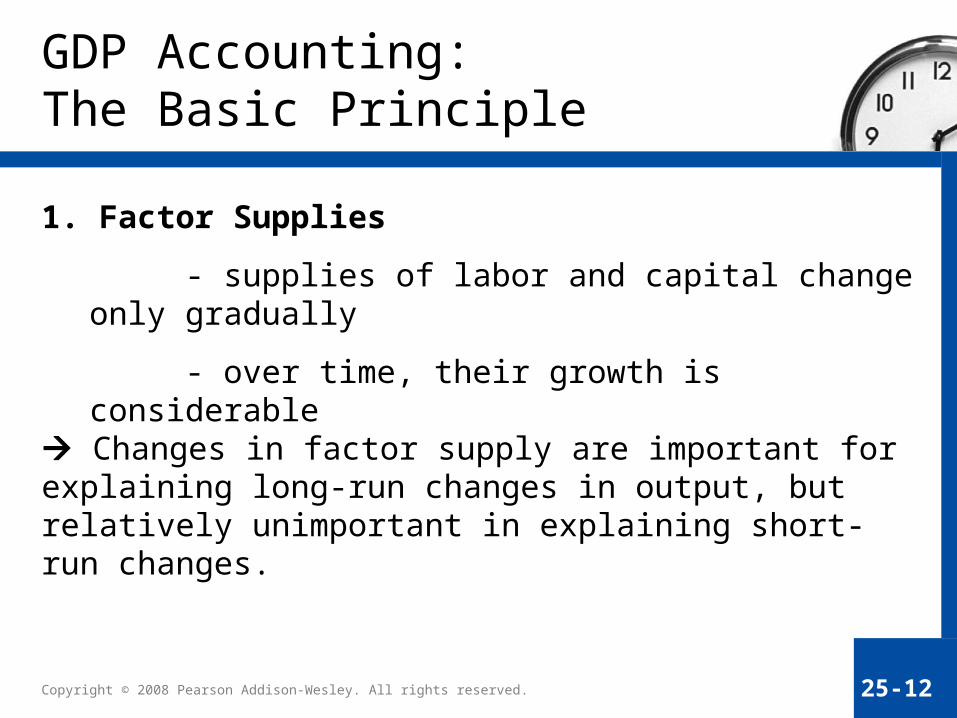

1. Factor Supplies

- supplies of labor and capital change only gradually

- over time, their growth is considerable

Changes in factor supply are important for explaining long-run changes in output, but relatively unimportant in explaining short-run changes.

GDP Accounting: The Basic Principle

25-13Copyright © 2008 Pearson Addison-Wesley. All rights reserved.

2. Productivity

- productivity changes only gradually

- over time, productivity grows substantially

Changes in productivity are important for explaining long-run changes in output, but less important in explaining short-run changes.

GDP Accounting: The Basic Principle

25-14Copyright © 2008 Pearson Addison-Wesley. All rights reserved.

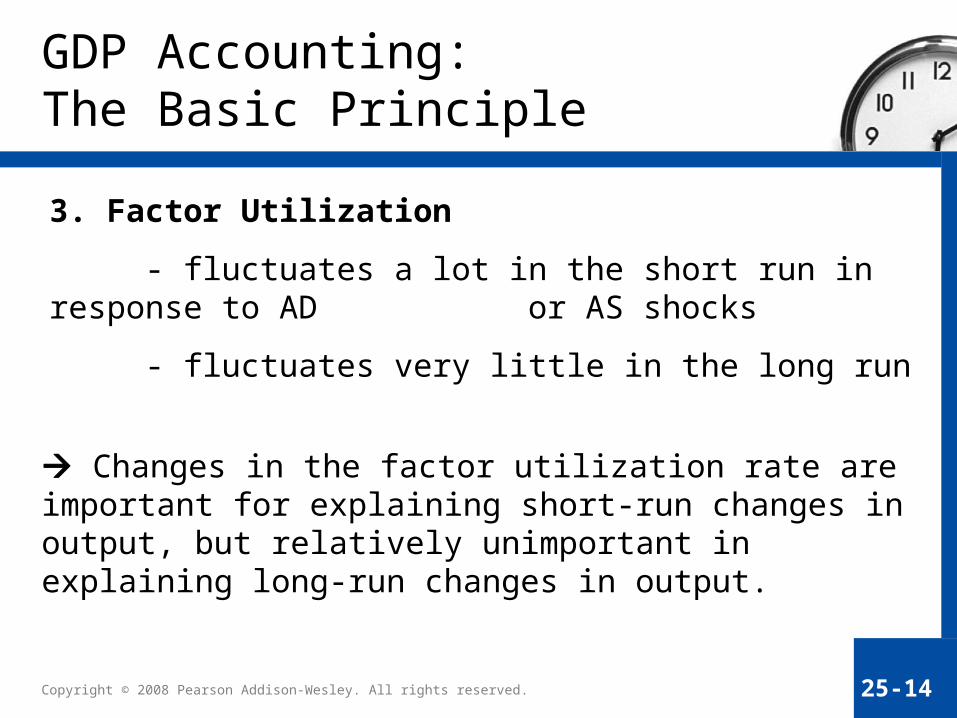

3. Factor Utilization

- fluctuates a lot in the short run in response to AD or AS shocks

- fluctuates very little in the long run

Changes in the factor utilization rate are important for explaining short-run changes in output, but relatively unimportant in explaining long-run changes in output.

GDP Accounting: The Basic Principle

25-15Copyright © 2008 Pearson Addison-Wesley. All rights reserved.

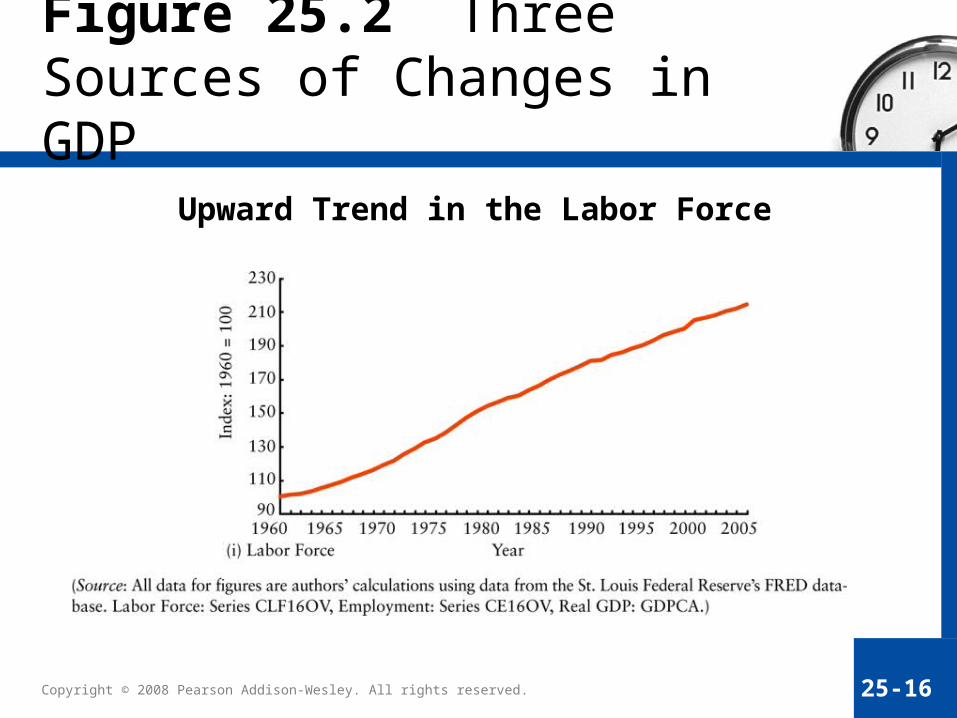

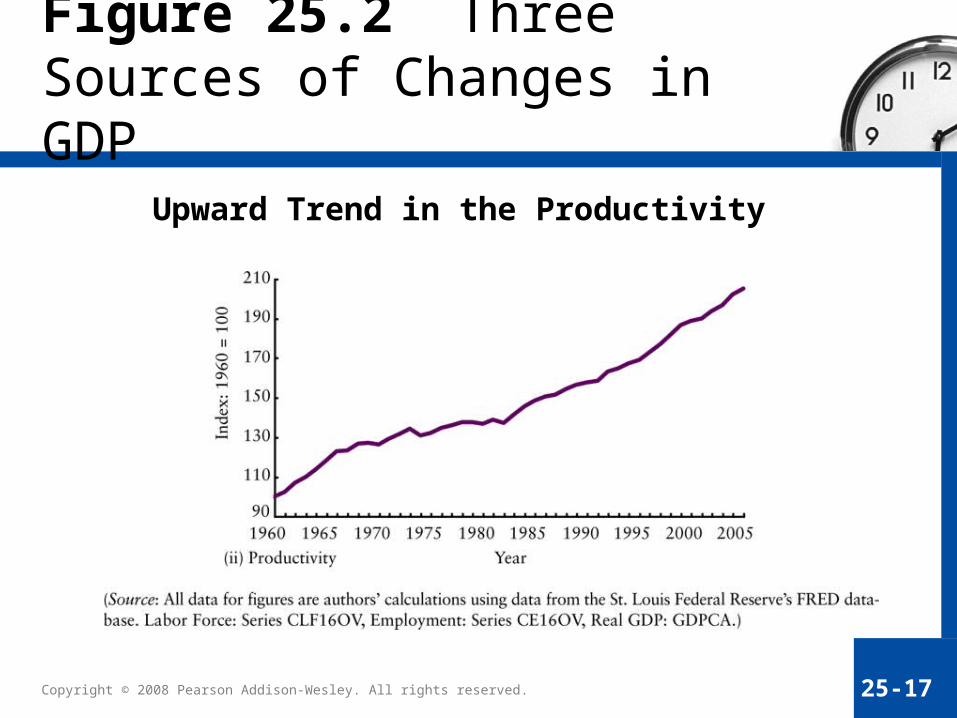

GDP Accounting: An Application

Consider just one factor of production — labor.

The identity becomes:

GDP = L x (E/L) x (GDP/E)

- L is the labor force

- E/L is the employment rate

- GDP/E is a simple measure of labor productivity

How have these components actually moved in the U.S.?

25-16Copyright © 2008 Pearson Addison-Wesley. All rights reserved.

Upward Trend in the Labor Force

Figure 25.2 Three Sources of Changes in GDP

25-17Copyright © 2008 Pearson Addison-Wesley. All rights reserved.

Upward Trend in the Productivity

Figure 25.2 Three Sources of Changes in GDP

25-18Copyright © 2008 Pearson Addison-Wesley. All rights reserved.

Employment Rate

Figure 25.2 Three Sources of Changes in GDP

25-19Copyright © 2008 Pearson Addison-Wesley. All rights reserved.

To understand long-run changes in GDP:- need to understand labour force growth and productivity growth

To understand short-run changes in GDP:- need to understand changes in the utilization rate of labor — the employment rate

Summing Up

25-20Copyright © 2008 Pearson Addison-Wesley. All rights reserved.

Policy Implications

When studying short-run fluctuations, economist focus on:

– deviations of actual output from potential

When studying long-run changes, economist focus on:

– potential output

25-21Copyright © 2008 Pearson Addison-Wesley. All rights reserved.

Policy Implications

Fiscal and monetary policies affect the short-run level of GDP because they alter the level of aggregate demand.

But unless they are able to affect the level of potential output, they will have no effect on long-run GDP.z

- broad consensus that monetary policy has only limited effects on Y*

- fiscal policy probably has more effect on Y*

25-22Copyright © 2008 Pearson Addison-Wesley. All rights reserved.

Looking Ahead

This chapter has focused on the difference between the short run and the long run.

Short-run movements in GDP are mostly accounted for by changes in the factor utilization rate.

Long-run changes in GDP are mostly accounted for by changes in factor supplies and productivity.

This difference forces economists to think differently about macroeconomic relationships that exist over a few months as compared to those that exist over several years.