Embed Size (px)

Citation preview

Copyright © 2013 Pearson Canada Inc. 5 - 1

Chapter 5Legislation

in the

Marketplace

Legal Fundamentals for Canadian Business

Third Edition

Copyright © 2013 Pearson Canada Inc. 5 - 2

Learning Objectives

• Describe the function and form of Sale of Goods Act

• Outline the duties of sellers and buyers• Describe the nature and purpose of

consumer protection legislation• Consider whether proposed changes will

solve current problems(Continued)

Learning Objectives(Continued)

• Discuss the role of federal legislation in controlling competition in the marketplace

• Consider the forms and purpose of securing transactions

• Outline the legislation and its purpose in regulating securities

• Describe the process and objectives of bankruptcy

Copyright © 2013 Pearson Canada Inc. 5 - 3

Copyright © 2013 Pearson Canada Inc. 5 - 4

Sale of Goods Act

• Provincial statutes that imply terms into sale of goods contracts

• Parties can override most provisions of Act

• Act applies if actual sale (transfer of title)– May be immediate or in the future (conditional

sale)

(Continued)

Copyright © 2013 Pearson Canada Inc. 5 - 5

Sale of Goods Act(Continued)

• Goods– Tangible, movable property– Does not apply to service contracts– Where service is incidental to transaction, Act

applies

Copyright © 2013 Pearson Canada Inc. 5 - 6

Title and Risk

• Risk follows title under the Act, but Act can be overridden – Examples:– C.I.F. (Cost-Insurance-Freight)

• Vendor must arrange transportation and insurance against risk

– F.O.B. (Free on board)• Parties specify in contract where title and risk will

transfer

(Continued)

Copyright © 2013 Pearson Canada Inc. 5 - 7

Title and Risk(Continued)

• Examples (Continued) – C.O.D. (Cash on delivery)

• Risk and title pass when goods received and paid for

– Bill of Lading• Can be used to control risk and title when a third party

transports goods

• If seller names self to receive goods, he/she retains control of goods, but also risk

(Continued)

Copyright © 2013 Pearson Canada Inc. 5 - 8

Title and Risk(Continued)

• Normally, transfer of title follows rules set out in Sale of Goods Act– Rule #1 - Specific, identified goods in

deliverable state• Title and risk transfer upon contract of sale

• Payment and delivery may occur later

(Continued)

Copyright © 2013 Pearson Canada Inc. 5 - 9

Title and Risk(Continued)

• Rules of Sale of Goods Act (Continued)– Rule #2 - Specific, identified goods that require

work• Work must be done to put goods in deliverable state

• Title transfers when work is done and purchaser is notified

(Continued)

Copyright © 2013 Pearson Canada Inc. 5 - 10

Title and Risk(Continued)

• Rules of Sale of Goods Act (Continued)– Rule #3 - Specific goods that must be weighed

or measured to determine price• Title transfers when goods are weighed or measured

and purchaser is notified

(Continued)

Copyright © 2013 Pearson Canada Inc. 5 - 11

Title and Risk(Continued)

• Rules of Sale of Goods Act (Continued)– Rule #4 - Specific goods taken on approval (or

sale with right to return)• Title passes when sale is accepted (by notification to

seller, passage of reasonable time, or treating goods as your own)

(Continued)

Copyright © 2013 Pearson Canada Inc. 5 - 12

Title and Risk(Continued)

• Rules of Sale of Goods Act (Continued)– Rule #5 - When goods have not yet been made

or where they have been selected from a sample or floor model

• Title transfers when goods have been created and/or unconditionally committed to the transaction with assent of buyer; assent can be implied

Copyright © 2013 Pearson Canada Inc. 5 - 13

Obligations of Seller

• Act implies following terms related to title– Condition that seller delivers good title to

goods to purchaser– Warranty to deliver quiet possession of goods– Warranty that goods be free of any charge or

encumbrance

(Continued)

Copyright © 2013 Pearson Canada Inc. 5 - 14

Obligations of Seller(Continued)

• Act implies conditions for goods bought by description or sample– Goods must match description or sample– Buyer may refuse delivery if they don’t

• Act implies conditions related to fitness and quality of goods sold by description (i.e., all mass-produced goods)

(Continued)

Copyright © 2013 Pearson Canada Inc. 5 - 15

Obligations of Seller(Continued)

• Fitness and quality– Goods must be of merchantable quality

• Free from hidden defects that make goods unusable or interfere with effectiveness

– Goods must be suitable for purpose if purchaser relies on recommendation of seller

(Continued)

Copyright © 2013 Pearson Canada Inc. 5 - 16

Obligations of Seller(Continued)

• Fitness and quality– Sellers may attempt to override implied

conditions through limited warranties or exemption clauses

• In consumer transactions, sellers often prevented from contracting out by statute

• Exemption clauses usually enforced in commercial transactions unless unfair

Copyright © 2013 Pearson Canada Inc. 5 - 17

Other Implied Terms

• Sale of Goods Act implies other terms – Examples:– If no purchase price stated, reasonable price is

implied– If no date stated, payment to be made at

reasonable time (usually time of delivery)– Rights to recover goods

• Stoppage in transitu• Provisions under Bankruptcy and Insolvency Act

Copyright © 2013 Pearson Canada Inc. 5 - 18

Consumer Protection Legislation

• Legislation varies by province– Quality and fitness– Trade (or Business) Practices Act

• Prohibits misleading and deceptive practices• Controls unconscionable transactions• Makes false or misleading statements conditions of

contract; may sue for breach• Includes a number of potential remedies

(Continued)

Copyright © 2013 Pearson Canada Inc. 5 - 19

Consumer Protection Legislation (Continued)

• Control of specific businesses– Door-to-Door Sales

• Requires cooling-off period

– Executory contracts• Contracts to be performed in future

• Required to be in writing

(Continued)

Copyright © 2013 Pearson Canada Inc. 5 - 20

Consumer Protection Legislation (Continued)

• Control of specific businesses– Referral selling

• Giving a discount if purchaser provides names of potential buyers to seller is controlled

– Delivery of unsolicited goods• Responsibility is severely restricted

(Continued)

Copyright © 2013 Pearson Canada Inc. 5 - 21

Consumer Protection Legislation (Continued)

• Control of specific businesses– True cost of borrowing must be disclosed

• Actual rate and costs must be disclosed• Must state total amount to be paid

– Purchase of income tax returns and payday loans are restricted

– Credit reporting/debt collection are regulated– Many other businesses subject to consumer protection

legislation

(Continued)

Copyright © 2013 Pearson Canada Inc. 5 - 22

Consumer Protection Legislation (Continued)

• Government agencies are set up to investigate and resolve disputes– Assist consumers to obtain remedies– May impose fines, revoke licenses, etc.– May take civil action for damages/injunction– May involve quasi-criminal prosecution

• Charter of Rights protections apply

Copyright © 2013 Pearson Canada Inc. 5 - 23

Comprehensive Acts

• Some provinces (Ontario and B.C.) have comprehensive consumer protection acts

• Example: Ontario Consumer Protection Act (2002)– Incorporates provisions from several acts into one

– Includes leases and services

– Gives extensive powers to search, seize, make orders, etc.

– Includes regulation of internet consumer transactions

Copyright © 2013 Pearson Canada Inc. 5 - 24

Non-Government Agencies

• Better Business Bureau– Consists of and supported by member

businesses– Attempts to weed out unscrupulous businesses– Provides a service to public where they can

inquire about specific businesses

Copyright © 2013 Pearson Canada Inc. 5 - 25

The Federal Competition Act

• Competition Act– Purpose “is to maintain and encourage

competition in Canada”– Supported by Competition Tribunal Act that

created an enforcement body– Controls anti-competitive practices– Economic principles usually determine outcomes

(Continued)

Copyright © 2013 Pearson Canada Inc. 5 - 26

The Federal Competition Act(Continued)

• Conspiracies that unduly lessen competition are prohibited– Bid rigging is an indictable offence

– Price fixing can unduly restrain trade

• Pyramid selling is prohibited– Involves paying a fee to participate in a multilevel

organization that isn’t based on the sale of a product

– Constitutes summary conviction offence

(Continued)

Copyright © 2013 Pearson Canada Inc. 5 - 27

The Federal Competition Act(Continued)

• Deceptive marketing practices prohibited

• Full disclosure is required of merchants in many situations

• Predatory practices are reviewable

• Mergers and acquisitions are reviewed to balance the loss of competition against increased business efficiency

Copyright © 2013 Pearson Canada Inc. 5 - 28

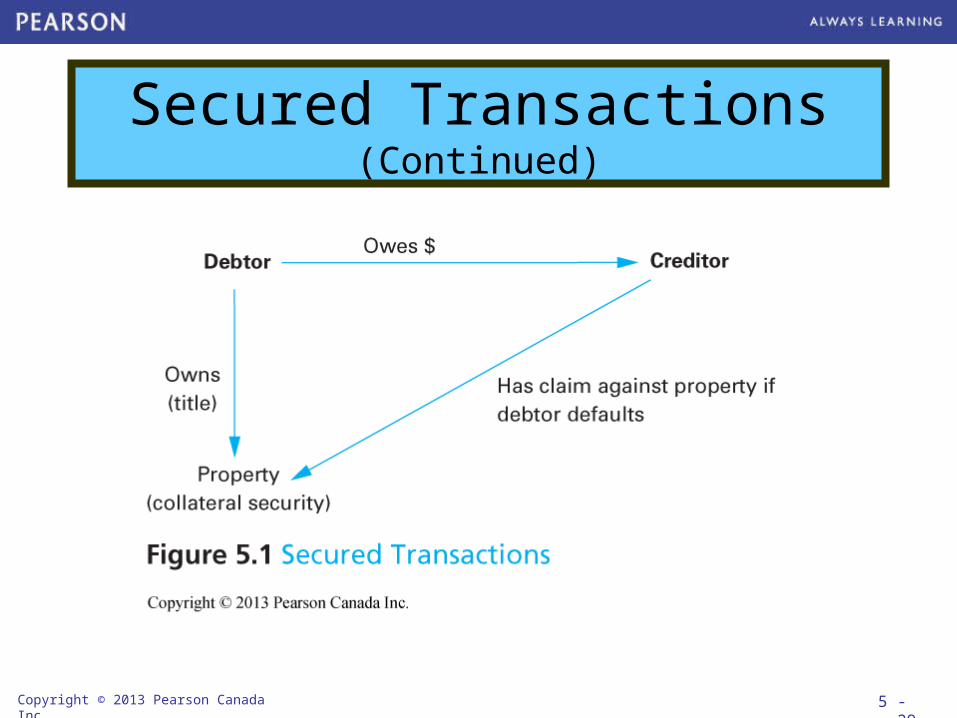

Secured Transactions

• Ensuring a debt will be repaid by providing security of equal or greater value and giving creditor first claim

• May use either real or personal property• Personal Property

– Tangible – chattels (goods)– Intangible – rights or claims (e.g., shares,

cheques)

(Continued)

Copyright © 2013 Pearson Canada Inc. 5 - 29

Secured Transactions(Continued)

Copyright © 2013 Pearson Canada Inc. 5 - 30

Personal Property Security Act

• Act controls all secured transactions involving personal property

• Allows any form of personal property to be used as security

• Must have contract creating secured transaction

• Title stays with borrower, but rights given to creditor

Copyright © 2013 Pearson Canada Inc. 5 - 31

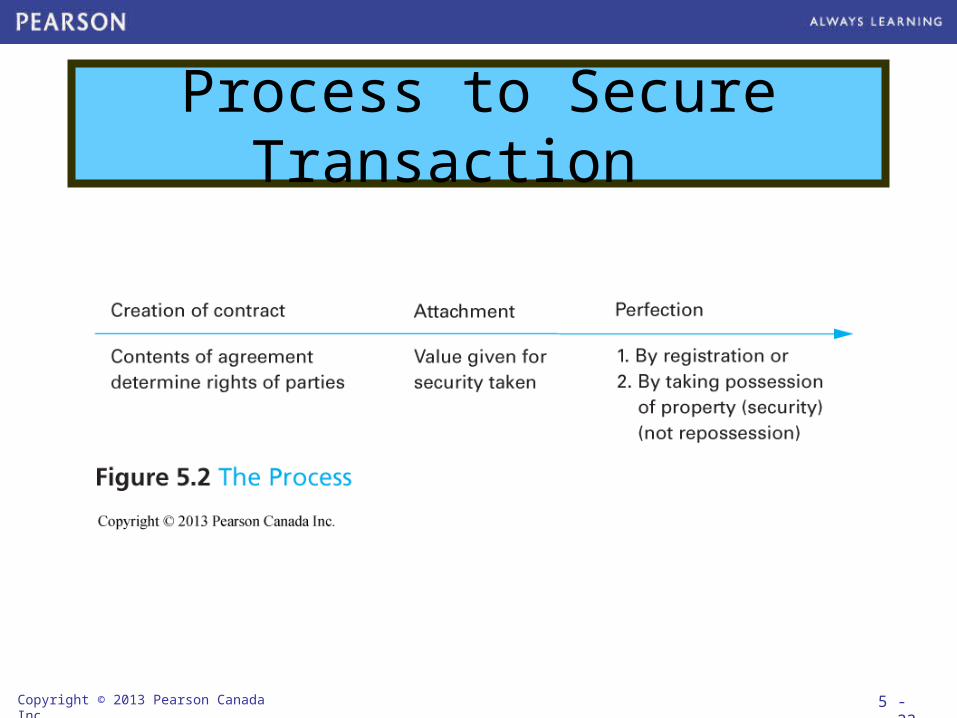

Steps to Secure Transaction

1) Agreement• Contract sets out rights and obligations of parties

• Specifies asset to be used as security• Creditor has no claim at this point

2) Attachment• Value under contract given to debtor, securing

creditor’s claim against asset

(Continued)

Copyright © 2013 Pearson Canada Inc. 5 - 32

Steps to Secure Transaction (Continued)

3) Perfection• Primarily accomplished through registration

(Registry created for each province)• Gives creditor priority against subsequent

holders or claimants• File form with appropriate registry• Can also perfect by taking possession of

property

Copyright © 2013 Pearson Canada Inc. 5 - 33

Process to Secure Transaction

Copyright © 2013 Pearson Canada Inc. 5 - 34

Default

• Creditor has right to obtain and resell property used as security

• Usually happens through creditor, his/her employees, or private bailiff

• No force or violence may be used• No need for court order if contract gives

right to repossess (unless property is not accessible)

Copyright © 2013 Pearson Canada Inc. 5 - 35

Reselling Secured Goods

• Goods may be sold to recover debt

• Anyone with an interest (including debtor) must be notified and given opportunity to redeem goods by paying out debt

• If sold, seller must attempt to obtain fair market price

(Continued)

Copyright © 2013 Pearson Canada Inc. 5 - 36

Reselling Secured Goods (Continued)

• Process of sale must be “commercially reasonable”

• Any excess, minus costs of process, must be paid to the debtor

• If deficit results, amount still owed by debtor may or may not be recoverable, depending on province

Copyright © 2013 Pearson Canada Inc. 5 - 37

Builders’ Liens

• Gives suppliers and subcontractors a claim against property if they are not paid

• May register a lien against property which can eventually force a sale of property

• If property owner retains a percentage of money owed under contract (holdback), this is available to satisfy claims and remove liens

Copyright © 2013 Pearson Canada Inc. 5 - 38

Guarantees

• One person (guarantor) agrees to pay debt to creditor if debtor does not

• Must be in writing to be enforceable; often under seal

• Any defence the debtor has against the creditor is available to the guarantor (except bankruptcy and infancy)

(Continued)

Copyright © 2013 Pearson Canada Inc. 5 - 39

Guarantees(Continued)

• If guarantor pays, he/she assumes all rights of the creditor to collect debt

• If the creditor and debtor change the terms of the original agreement, the guarantor will not be bound by the guarantee unless the guarantor has been informed and has given permission for the changes

Copyright © 2013 Pearson Canada Inc. 5 - 40

Bankruptcy and Insolvency

• Insolvent – unable to pay bills as they become due

• Bankrupt – debtor’s assets have been transferred to a trustee for distribution to unpaid creditors

• Governed by the federal Bankruptcy and Insolvency Act– Preserve assets of debtor for benefit of creditors– Promote rehabilitation of debtor and give him/her a

fresh start

(Continued)

Copyright © 2013 Pearson Canada Inc. 5 - 41

Bankruptcy and Insolvency(Continued)

• Two ways to become bankrupt– Voluntary transfer of assets to trustee

• Assignment in bankruptcy

– Being forced into bankruptcy by creditors• Requires a receiving order from court

• Must owe at least $1000 and have committed an act of bankruptcy (e.g., insolvent, fraudulent transfer, or fraudulent preference)

(Continued)

Copyright © 2013 Pearson Canada Inc. 5 - 42

Bankruptcy and Insolvency(Continued)

• Trustee– Counsels debtor– Preserves and looks after the assets– Determines priorities among creditors– Sells assets– Distributes proceeds to creditors

(Continued)

Copyright © 2013 Pearson Canada Inc. 5 - 43

Bankruptcy and Insolvency(Continued)

• Secured Creditors– Trustee must surrender asset to them or pay out– If shortfall, they become unsecured creditors for

balance of debt

• Preferred Creditors – set out in Act– Funeral expenses, costs of bankruptcy, some

taxes, E.I. and W.C.B. premiums, limited amount of employees’ wages and rent

(Continued)

Copyright © 2013 Pearson Canada Inc. 5 - 44

Bankruptcy and Insolvency(Continued)

• Unsecured Creditors– Receive any amount left over– Receive a percentage based on their claim vs.

total amount of debt– Often very little left to distribute

• Debtors– Some assets are exempt from seizure so debtor

keeps them (Continued)

Copyright © 2013 Pearson Canada Inc. 5 - 45

Bankruptcy and Insolvency(Continued)

• Bankruptcy Offences– Failing to fully disclose information, lying,

transferring property to a spouse or friend (fraudulent transfer)

– May interfere with being discharged from bankruptcy

– Include fines up to $10,000 or 3 years in jail

(Continued)

Copyright © 2013 Pearson Canada Inc. 5 - 46

Bankruptcy and Insolvency(Continued)

• Discharge for individuals– Application for discharge automatically made

after 9 months– If first bankruptcy, will be discharged unless

creditors object or bankruptcy offences– Conditional discharge may be given, requiring

further payments

(Continued)

Copyright © 2013 Pearson Canada Inc. 5 - 47

Bankruptcy and Insolvency(Continued)

• Discharge for individuals (Continued)– Once discharged, free of any former

indebtedness– Exceptions:

• Student loans less than 7 years old

• Family maintenance obligations

• Child support

• Court-imposed fines

Copyright © 2013 Pearson Canada Inc. 5 - 48

Alternatives to Bankruptcy

• Negotiate alternate arrangements• Proposal to creditors

– If personal debt over $75,000, individuals may make a Division Two proposal to creditors

– Companies and larger debtors owing over $75,000 make Division One proposal

– Any action to seize property is stopped during this process; time may be extended

(Continued)

Copyright © 2013 Pearson Canada Inc. 5 - 49

Alternatives to Bankruptcy(Continued)

• Large corporations may proceed under Companies’ Creditors Arrangement Act

• Receivership - Secured creditors often make arrangements in contract to take over management of company if in default