Embed Size (px)

Citation preview

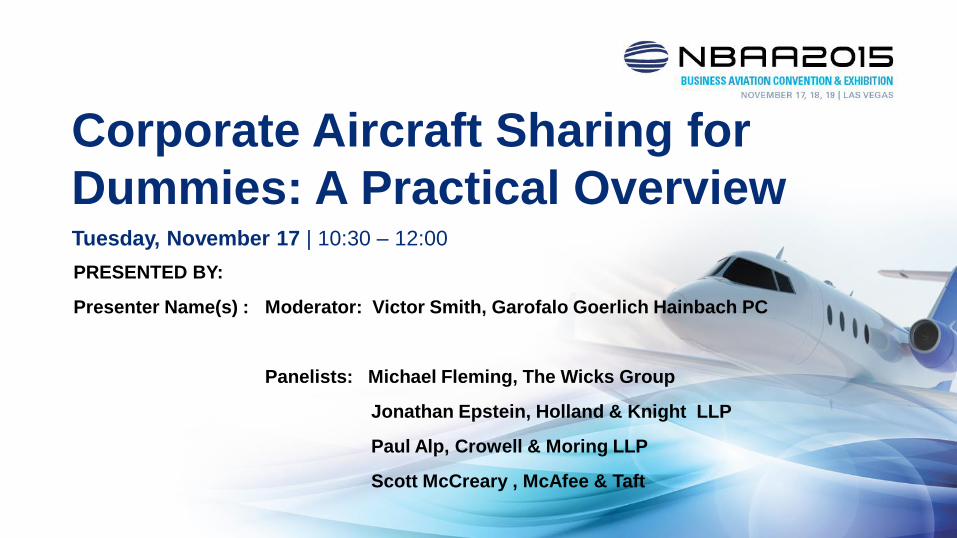

Corporate Aircraft Sharing for

Dummies: A Practical Overview

PRESENTED BY:

Presenter Name(s) : Moderator: Victor Smith, Garofalo Goerlich Hainbach PC

Panelists: Michael Fleming, The Wicks Group

Jonathan Epstein, Holland & Knight LLP

Paul Alp, Crowell & Moring LLP

Scott McCreary , McAfee & Taft

Tuesday, November 17 | 10:30 – 12:00

• Each of the panelists practices in the area of aviation law and is a member of the

Regulatory Issues Advisory Group (RIAG)

• RIAG is the NBAA’s Law Firm.

• RIAG is composed of aviation attorneys who specialize in all aspects of aviation

law including regulatory compliance, aircraft transactions and financing, and

corporate flight department issues.

• RIAG attorneys assist the NBAA by providing legal guidance to NBAA,

committees and members.

Who Are We?

2

• Our Goal: To provide tools for determining the best use of the company’s

corporate aircraft and to provide certain scenarios from a practical perspective

• Considerations:

– Maximize aircraft usage and cost sharing;

– Ensure full regulatory compliance and avoid any regulatory traps for the

unwary

• Structure of Presentation:

– Brief overview of cost sharing arrangements permitted under the FAA regulations

– Discussion of various real world scenarios and more detailed discussions of each cost

sharing arrangement

– Question and Answer

What will I learn in this session?

3

4

• Aircraft cost sharing includes those aircraft arrangements authorized by the FAA

in which an owner, or a group of owners, share the costs associated with owning

and operating a U.S. registered civil aircraft privately under Part 91.

• The presentation will focus on the following cost sharing arrangements:

Intra-Corporate Family Chargebacks Joint Ownership

Interchange Agreements Time Sharing

Co-Ownership

• This discussion does not include charter operations conducted by Part 135

Certificated Carriers and certain other methods of cost recovery (e.g., carriage of

candidates under §91.321).

What is Aircraft Cost Sharing

5

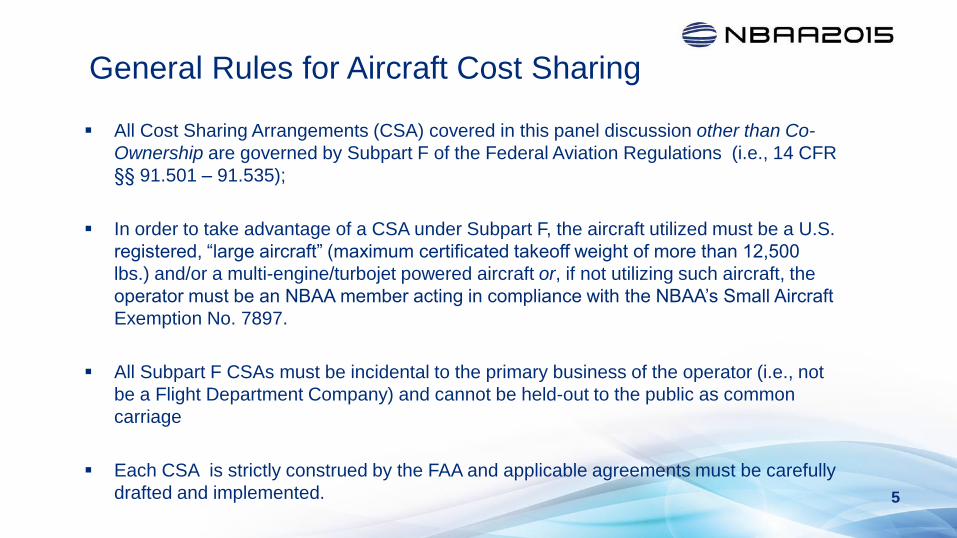

All Cost Sharing Arrangements (CSA) covered in this panel discussion other than Co-

Ownership are governed by Subpart F of the Federal Aviation Regulations (i.e., 14 CFR

§§ 91.501 – 91.535);

In order to take advantage of a CSA under Subpart F, the aircraft utilized must be a U.S.

registered, “large aircraft” (maximum certificated takeoff weight of more than 12,500

lbs.) and/or a multi-engine/turbojet powered aircraft or, if not utilizing such aircraft, the

operator must be an NBAA member acting in compliance with the NBAA’s Small Aircraft

Exemption No. 7897.

All Subpart F CSAs must be incidental to the primary business of the operator (i.e., not

be a Flight Department Company) and cannot be held-out to the public as common

carriage

Each CSA is strictly construed by the FAA and applicable agreements must be carefully

drafted and implemented.

General Rules for Aircraft Cost Sharing

6

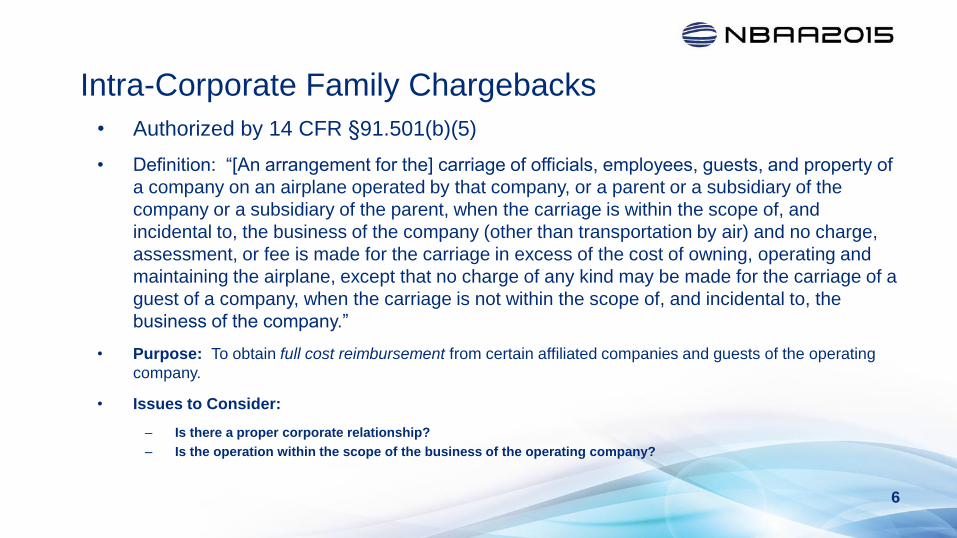

• Authorized by 14 CFR §91.501(b)(5)

• Definition: “[An arrangement for the] carriage of officials, employees, guests, and property of

a company on an airplane operated by that company, or a parent or a subsidiary of the

company or a subsidiary of the parent, when the carriage is within the scope of, and

incidental to, the business of the company (other than transportation by air) and no charge,

assessment, or fee is made for the carriage in excess of the cost of owning, operating and

maintaining the airplane, except that no charge of any kind may be made for the carriage of a

guest of a company, when the carriage is not within the scope of, and incidental to, the

business of the company.”

• Purpose: To obtain full cost reimbursement from certain affiliated companies and guests of the operating

company.

• Issues to Consider:

– Is there a proper corporate relationship?

– Is the operation within the scope of the business of the operating company?

Intra-Corporate Family Chargebacks

7

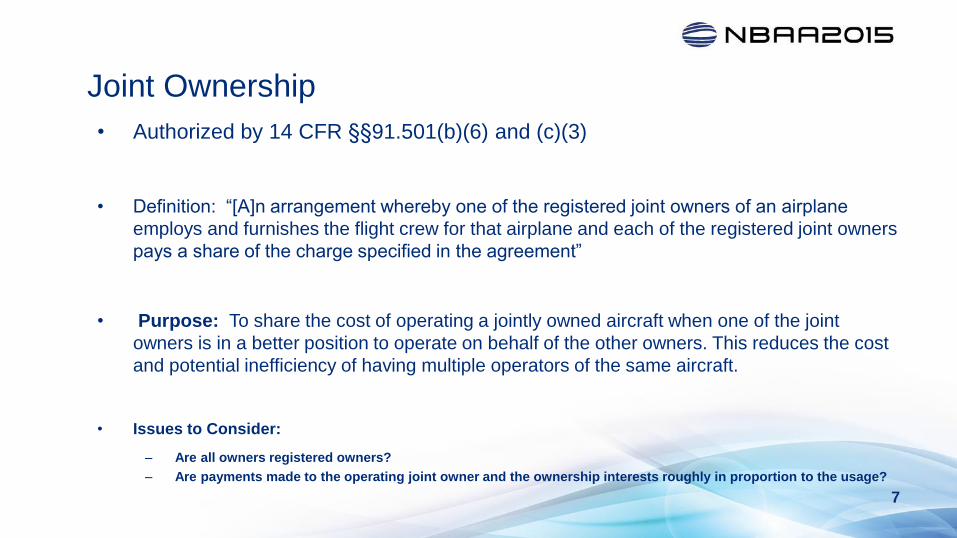

• Authorized by 14 CFR §§91.501(b)(6) and (c)(3)

• Definition: “[A]n arrangement whereby one of the registered joint owners of an airplane

employs and furnishes the flight crew for that airplane and each of the registered joint owners

pays a share of the charge specified in the agreement”

• Purpose: To share the cost of operating a jointly owned aircraft when one of the joint

owners is in a better position to operate on behalf of the other owners. This reduces the cost

and potential inefficiency of having multiple operators of the same aircraft.

• Issues to Consider:

– Are all owners registered owners?

– Are payments made to the operating joint owner and the ownership interests roughly in proportion to the usage?

Joint Ownership

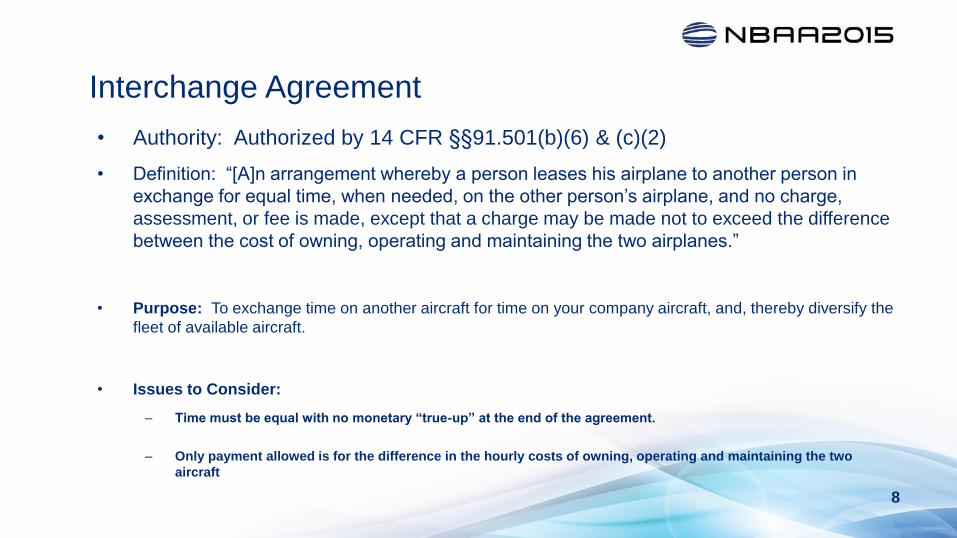

• Authority: Authorized by 14 CFR §§91.501(b)(6) & (c)(2)

• Definition: “[A]n arrangement whereby a person leases his airplane to another person in

exchange for equal time, when needed, on the other person’s airplane, and no charge,

assessment, or fee is made, except that a charge may be made not to exceed the difference

between the cost of owning, operating and maintaining the two airplanes.”

• Purpose: To exchange time on another aircraft for time on your company aircraft, and, thereby diversify the

fleet of available aircraft.

• Issues to Consider:

– Time must be equal with no monetary “true-up” at the end of the agreement.

– Only payment allowed is for the difference in the hourly costs of owning, operating and maintaining the two

aircraft

Interchange Agreement

8

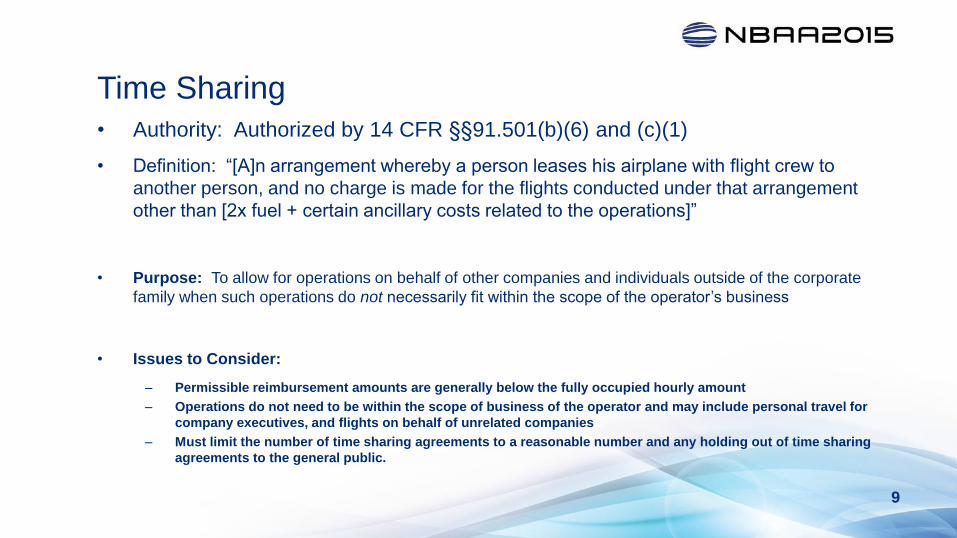

• Authority: Authorized by 14 CFR §§91.501(b)(6) and (c)(1)

• Definition: “[A]n arrangement whereby a person leases his airplane with flight crew to

another person, and no charge is made for the flights conducted under that arrangement

other than [2x fuel + certain ancillary costs related to the operations]”

• Purpose: To allow for operations on behalf of other companies and individuals outside of the corporate

family when such operations do not necessarily fit within the scope of the operator’s business

• Issues to Consider:

– Permissible reimbursement amounts are generally below the fully occupied hourly amount

– Operations do not need to be within the scope of business of the operator and may include personal travel for

company executives, and flights on behalf of unrelated companies

– Must limit the number of time sharing agreements to a reasonable number and any holding out of time sharing

agreements to the general public.

Time Sharing

9

10

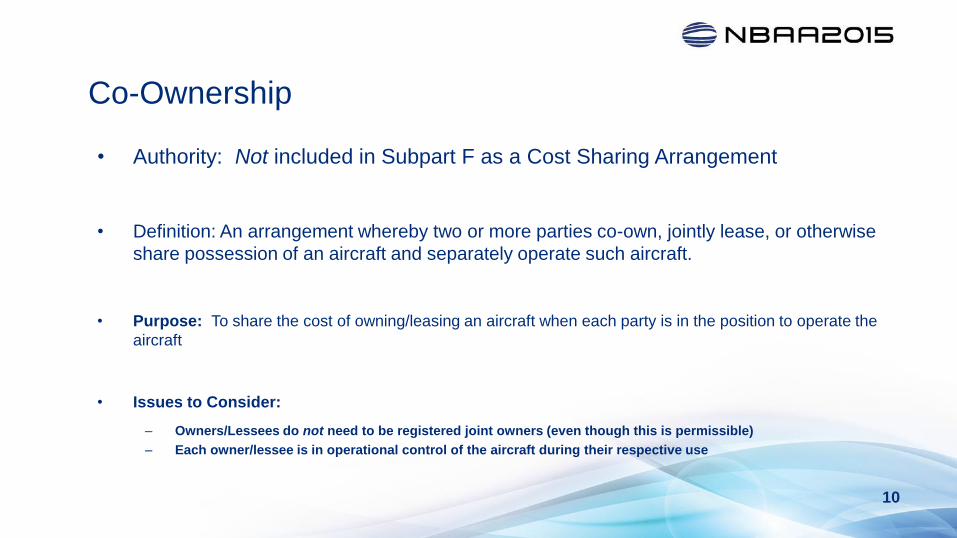

• Authority: Not included in Subpart F as a Cost Sharing Arrangement

• Definition: An arrangement whereby two or more parties co-own, jointly lease, or otherwise

share possession of an aircraft and separately operate such aircraft.

• Purpose: To share the cost of owning/leasing an aircraft when each party is in the position to operate the

aircraft

• Issues to Consider:

– Owners/Lessees do not need to be registered joint owners (even though this is permissible)

– Each owner/lessee is in operational control of the aircraft during their respective use

Co-Ownership

11

• Scenario I: A Tale of Cost Sharing Among Affiliated Companies

• Scenario II: A Tale of Cost Sharing Among Unrelated Companies

• Scenario III: A Tale of Personal Use

Meet the Players: Arnold (CEO of Arnold’s Apples)

Brenda (CEO of Brenda’s Burgers)

Charlie (CEO of Charlie’s Cookies)

Scenarios to be Discussed

Scenario I. Arnold's Apples

Shares In-House

PRESENTED BY:

Michael Fleming

Partner - The Wicks Group, PLLC

202.457.7790 [email protected]

Tuesday, November 27, 2015

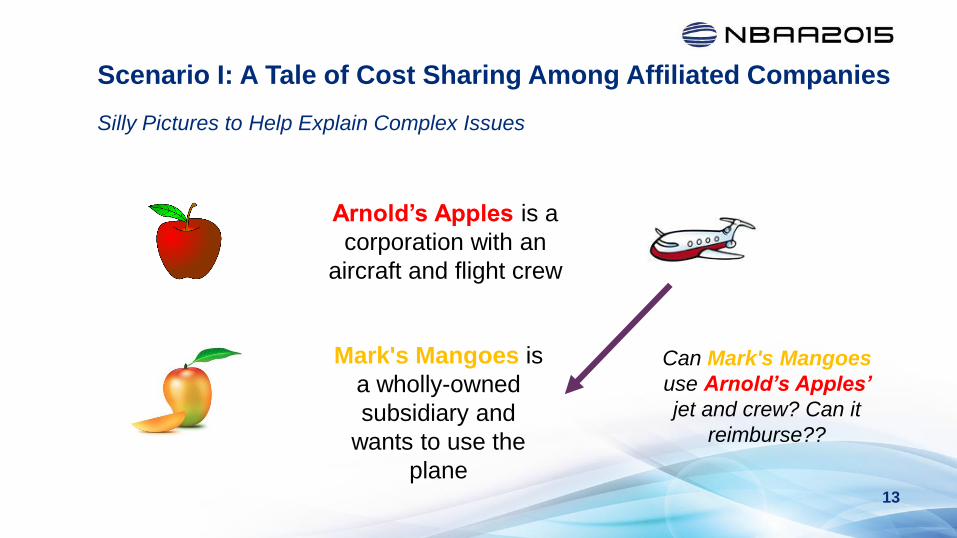

Scenario I: A Tale of Cost Sharing Among Affiliated Companies

13

Silly Pictures to Help Explain Complex Issues

Arnold’s Apples is a

corporation with an

aircraft and flight crew

Mark's Mangoes is

a wholly-owned

subsidiary and

wants to use the

plane

Can Mark's Mangoes

use Arnold’s Apples’

jet and crew? Can it

reimburse??

14

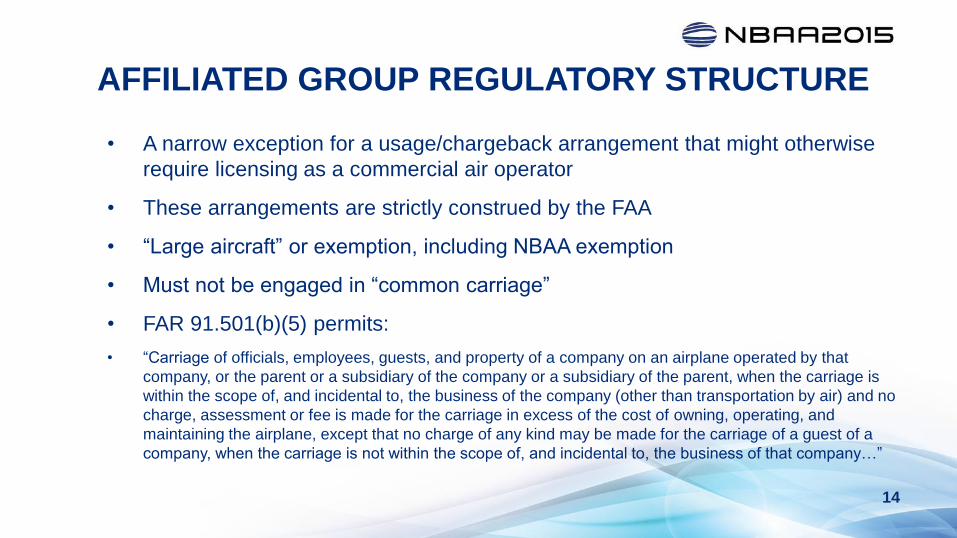

AFFILIATED GROUP REGULATORY STRUCTURE

• A narrow exception for a usage/chargeback arrangement that might otherwise

require licensing as a commercial air operator

• These arrangements are strictly construed by the FAA

• “Large aircraft” or exemption, including NBAA exemption

• Must not be engaged in “common carriage”

• FAR 91.501(b)(5) permits:

• “Carriage of officials, employees, guests, and property of a company on an airplane operated by that

company, or the parent or a subsidiary of the company or a subsidiary of the parent, when the carriage is

within the scope of, and incidental to, the business of the company (other than transportation by air) and no

charge, assessment or fee is made for the carriage in excess of the cost of owning, operating, and

maintaining the airplane, except that no charge of any kind may be made for the carriage of a guest of a

company, when the carriage is not within the scope of, and incidental to, the business of that company…”

15

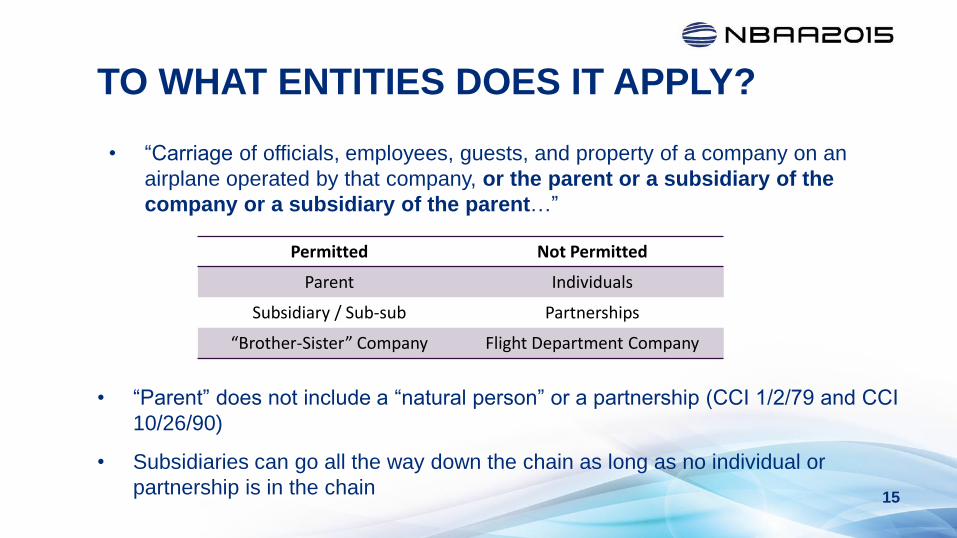

TO WHAT ENTITIES DOES IT APPLY?

• “Carriage of officials, employees, guests, and property of a company on an

airplane operated by that company, or the parent or a subsidiary of the

company or a subsidiary of the parent…”

Permitted Not Permitted

Parent Individuals

Subsidiary / Sub-sub Partnerships

“Brother-Sister” Company Flight Department Company

• “Parent” does not include a “natural person” or a partnership (CCI 1/2/79 and CCI

10/26/90)

• Subsidiaries can go all the way down the chain as long as no individual or

partnership is in the chain

16

APPLICATION TO OUR SCENARIO

Arnold’s Apples has a

subsidiary with business

travel needs

Mark's Mangoes is

a wholly-owned

subsidiary and

wants to use the

plane

The using company is

a subsidiary of the

operating company:

91.501(b)(5) applies,

IF …

17

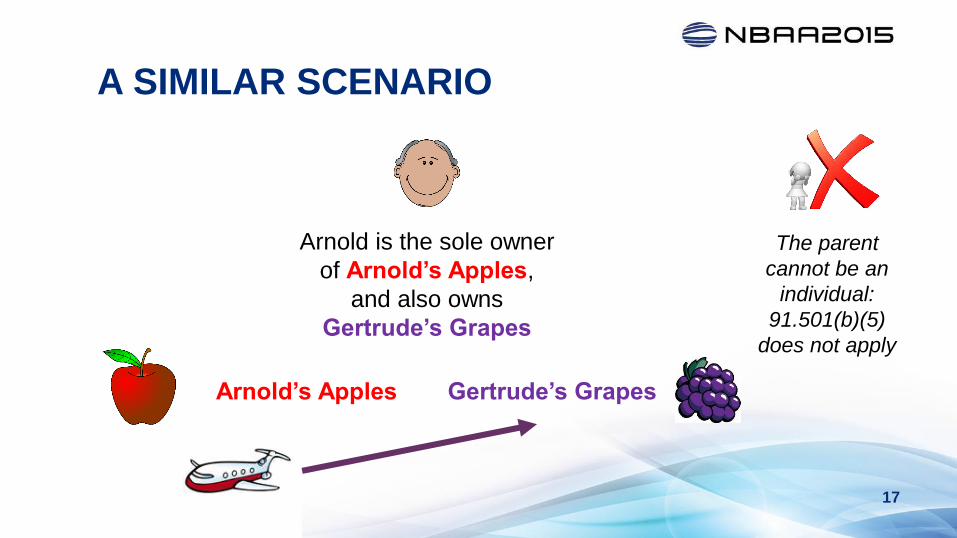

A SIMILAR SCENARIO

Arnold’s Apples

Arnold is the sole owner

of Arnold’s Apples,

and also owns

Gertrude’s Grapes

Gertrude’s Grapes

The parent

cannot be an

individual:

91.501(b)(5)

does not apply

18

INCIDENTAL TO THE BUSINESS

• “… when the carriage is within the scope of, and incidental to, the business

of the company (other than transportation by air)…”

• “The company” refers to the company operating the aircraft (CCI 3/3/11)

• So the carriage must be in the scope of / incidental to the business of the

operating company

• Example: A real estate development company operating on behalf of affiliates in

the auto industry must be able to show that the trips were incidental to its real

estate development business (CCI 11/25/08)

• When choosing the operating entity, consider the nature of each company that

will have use of the aircraft

• In our scenario, the use must be incidental to the business of Arnold’s Apples,

because it is operating the aircraft.

19

AVOID THE FLIGHT DEPARTMENT COMPANY TRAP

• “… when the carriage is within the scope of, and incidental to, the business of the

company (other than transportation by air)…”

• The business of the operating company may not be transportation by air – there

must be some other business to which the transportation is incidental

• A company set up to own an aircraft and operate it on behalf of affiliates is

referred to as a “flight department company” and is not permissible if there is

reimbursement of any kind (see CCI 5/27/05)

• This remains a common problem after decades of industry education

20

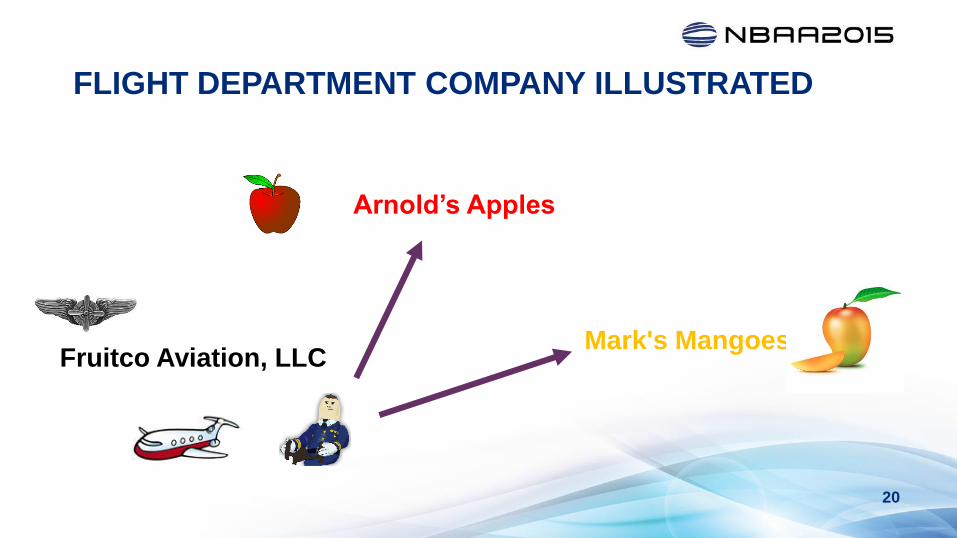

FLIGHT DEPARTMENT COMPANY ILLUSTRATED

Arnold’s Apples

Mark's MangoesFruitco Aviation, LLC

21

WHAT CHARGING IS ALLOWED?

• “… and no charge, assessment or fee is made for the carriage in excess of the

cost of owning, operating, and maintaining the airplane…”

• As opposed to the narrow 91.501(d) list of charges (used for Time Sharing and

etc.), this is a fully-allocated cost concept

• The actual charge may be less; the fully-allocated cost is a cap (“in excess of”

language)

• Can include: aircraft depreciation, insurance premiums, crew training costs, and

maintenance expenses (see CCI 12/2/10)

• There cannot be a profit under private carriage operating rules

• So from our original scenario, Mark’s Mangoes can reimburse Arnold’s Apples

on a fully-allocated basis for its use of the aircraft

22

IRS RULES ARE MORE RESTRICTIVE

• Different set of rules used to determine whether Federal Transportation Excise

Tax (FET) under IRC 4261 will apply to payments made for use of the aircraft

• Hinges on whether the operation is “commercial” by IRS standards

• Payments for transportation by air within the “affiliated group” are not subject to

the FET as long as the aircraft is not available for hire by persons outside of the

affiliated group (IRC 4282)

• “Affiliated group" means “one or more chains of includible corporations connected

through stock ownership with a common parent corporation” holding at least 80%

voting power (IRC 1504(a))

• Applying this to our original scenario, reimbursement by Mark's Mangoes for the

use of Arnold’s Apples’ aircraft will not be subject to the FET, because it is

wholly-owned and exceeds the 80% voting power requirement.

23

USE OF A MANAGEMENT COMPANY

• Management companies provide services requiring aviation expertise to aircraft operators.

The management company is not the operator of the aircraft; it is not in “operational control”

• Use within the affiliate group contemplates that one of the affiliates is operating the aircraft on

behalf of others within its affiliated group, although incidental to its own business; thus the

operating affiliate would typically hire the management company

• If each affiliate is contracting with the management company directly, then each such affiliate

might be in “operational control” when using the aircraft, which is not affiliated group usage

but might still be in compliance with Part 91

• Use of a management company might help to eliminate a Flight Department Company

problem by maintaining ownership in an SPV, while having each user operate the aircraft

independently, using the services of a common manager

• This type of arrangement must be structured very carefully to ensure compliance with the

FARs, analyze tax treatment, and consider liability exposures

24

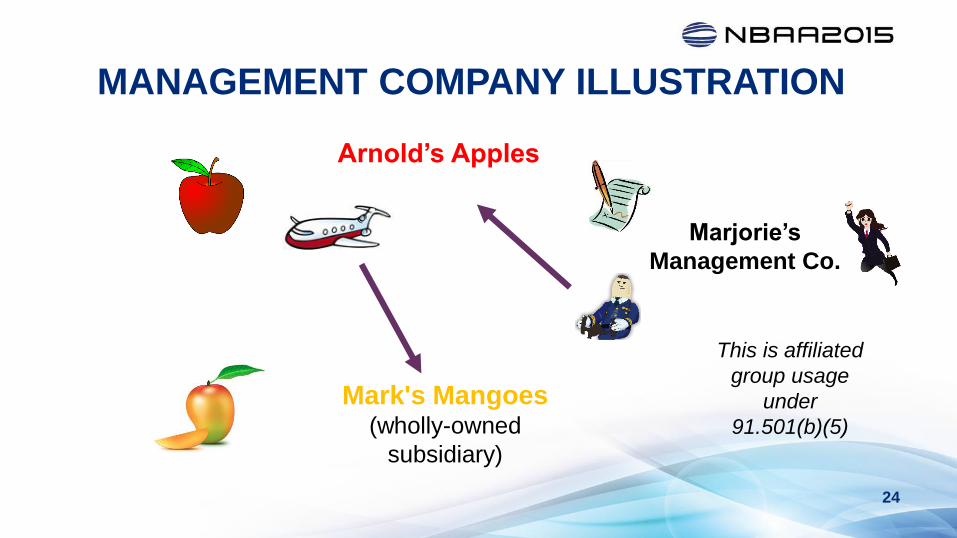

MANAGEMENT COMPANY ILLUSTRATION

Arnold’s Apples

Mark's Mangoes (wholly-owned

subsidiary)

Marjorie’s

Management Co.

This is affiliated

group usage

under

91.501(b)(5)

25

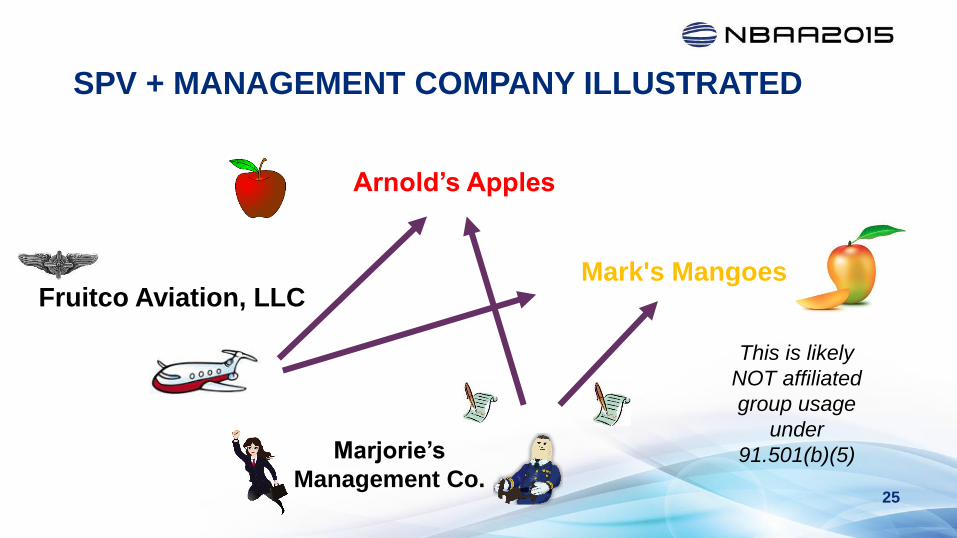

SPV + MANAGEMENT COMPANY ILLUSTRATED

Arnold’s Apples

Mark's MangoesFruitco Aviation, LLC

Marjorie’s

Management Co.

This is likely

NOT affiliated

group usage

under

91.501(b)(5)

Scenario II: A Tale of Cost Sharing Among

Underelated Companies

PRESENTED BY:

Jonathan Epstein

Partner, Holland & Knight LLP, Washington D.C.

1.202.828.1870 [email protected]

Tuesday, November 27. 2015 | 10:45 a.m. – 11:00 a.m.

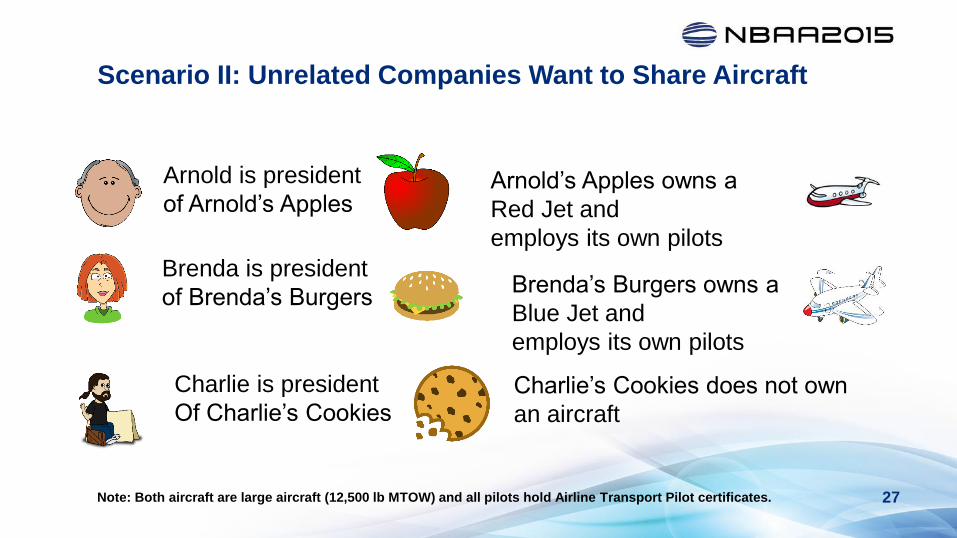

Scenario II: Unrelated Companies Want to Share Aircraft

27Note: Both aircraft are large aircraft (12,500 lb MTOW) and all pilots hold Airline Transport Pilot certificates.

Arnold is president

of Arnold’s Apples

Brenda is president

of Brenda’s Burgers

Arnold’s Apples owns a

Red Jet and

employs its own pilots

Brenda’s Burgers owns a

Blue Jet and

employs its own pilots

Charlie is president

Of Charlie’s CookiesCharlie’s Cookies does not own

an aircraft

28

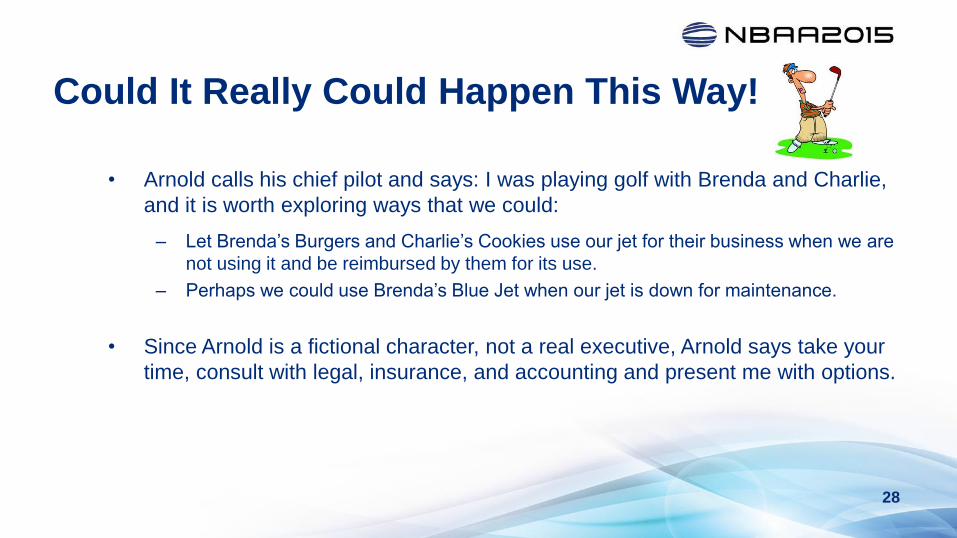

Could It Really Could Happen This Way!

• Arnold calls his chief pilot and says: I was playing golf with Brenda and Charlie,

and it is worth exploring ways that we could:

– Let Brenda’s Burgers and Charlie’s Cookies use our jet for their business when we are

not using it and be reimbursed by them for its use.

– Perhaps we could use Brenda’s Blue Jet when our jet is down for maintenance.

• Since Arnold is a fictional character, not a real executive, Arnold says take your

time, consult with legal, insurance, and accounting and present me with options.

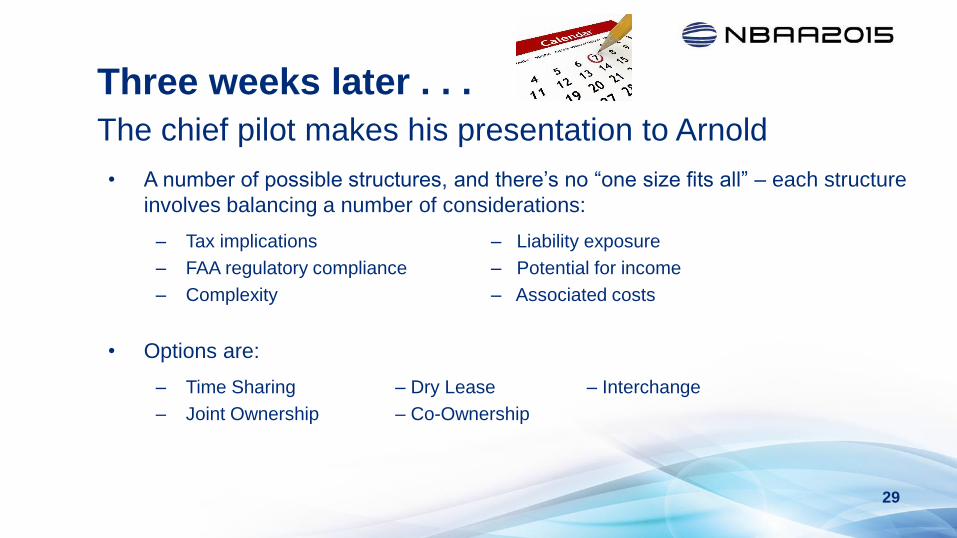

Three weeks later . . .

• A number of possible structures, and there’s no “one size fits all” – each structure

involves balancing a number of considerations:

– Tax implications – Liability exposure

– FAA regulatory compliance – Potential for income

– Complexity – Associated costs

• Options are:

– Time Sharing – Dry Lease – Interchange

– Joint Ownership – Co-Ownership

The chief pilot makes his presentation to Arnold

29

30

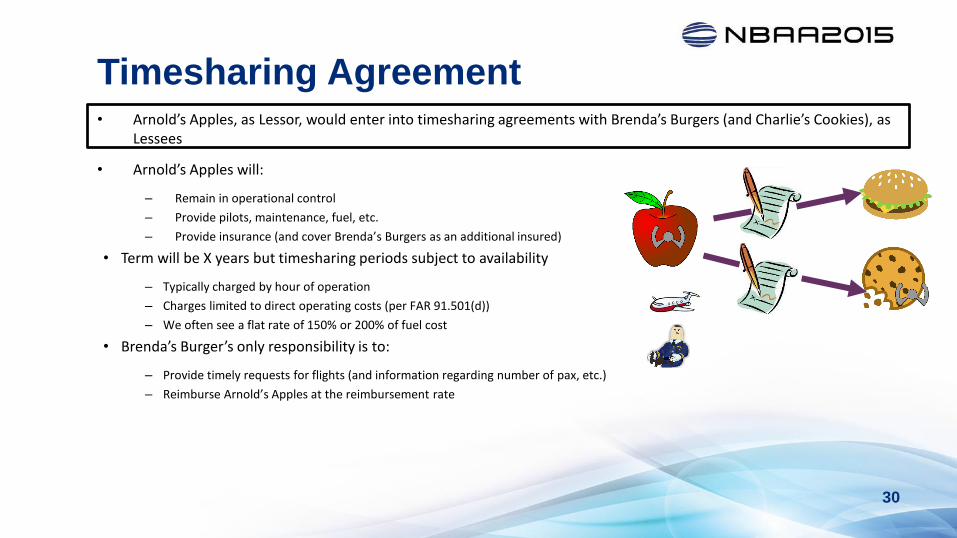

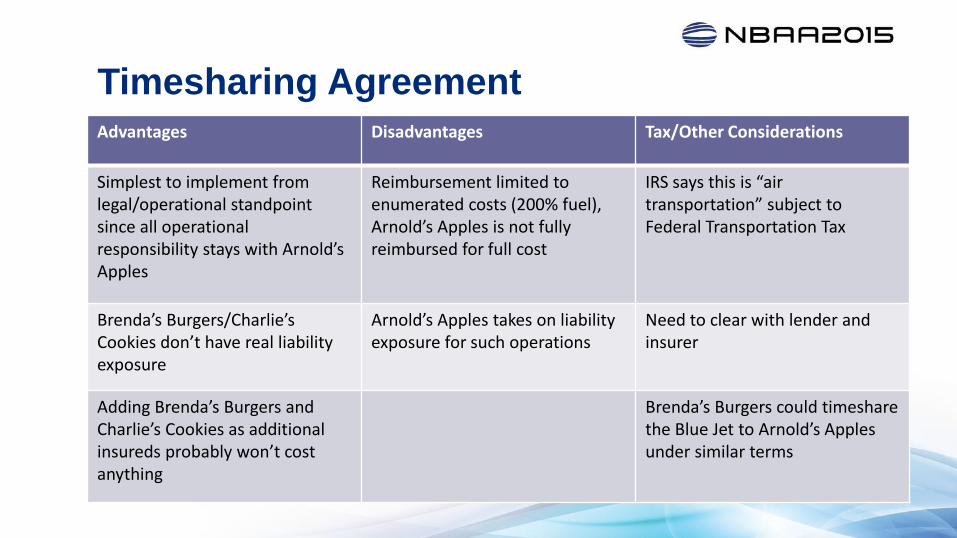

Timesharing Agreement• Arnold’s Apples, as Lessor, would enter into timesharing agreements with Brenda’s Burgers (and Charlie’s Cookies), as

Lessees

• Arnold’s Apples will:

– Remain in operational control

– Provide pilots, maintenance, fuel, etc.

– Provide insurance (and cover Brenda’s Burgers as an additional insured)

• Term will be X years but timesharing periods subject to availability

– Typically charged by hour of operation

– Charges limited to direct operating costs (per FAR 91.501(d))

– We often see a flat rate of 150% or 200% of fuel cost

• Brenda’s Burger’s only responsibility is to:

– Provide timely requests for flights (and information regarding number of pax, etc.)

– Reimburse Arnold’s Apples at the reimbursement rate

Timesharing Agreement

31

Advantages Disadvantages Tax/Other Considerations

Simplest to implement from legal/operational standpoint since all operational responsibility stays with Arnold’s Apples

Reimbursement limited to enumerated costs (200% fuel), Arnold’s Apples is not fully reimbursed for full cost

IRS says this is “air transportation” subject to Federal Transportation Tax

Brenda’s Burgers/Charlie’s Cookies don’t have real liability exposure

Arnold’s Apples takes on liability exposure for such operations

Need to clear with lender and insurer

Adding Brenda’s Burgers and Charlie’s Cookies as additional insureds probably won’t cost anything

Brenda’s Burgers could timeshare the Blue Jet to Arnold’s Apples under similar terms

32

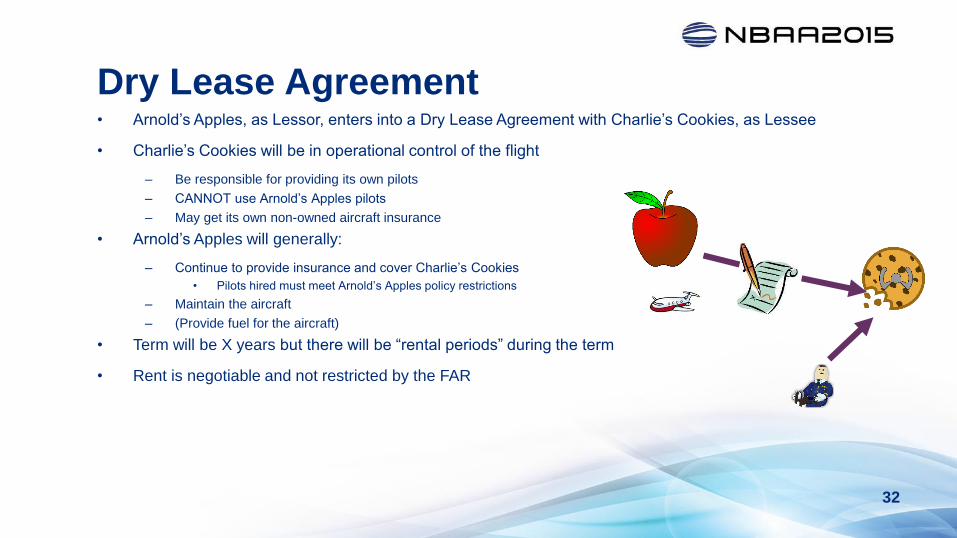

Dry Lease Agreement• Arnold’s Apples, as Lessor, enters into a Dry Lease Agreement with Charlie’s Cookies, as Lessee

• Charlie’s Cookies will be in operational control of the flight

– Be responsible for providing its own pilots

– CANNOT use Arnold’s Apples pilots

– May get its own non-owned aircraft insurance

• Arnold’s Apples will generally:

– Continue to provide insurance and cover Charlie’s Cookies

• Pilots hired must meet Arnold’s Apples policy restrictions

– Maintain the aircraft

– (Provide fuel for the aircraft)

• Term will be X years but there will be “rental periods” during the term

• Rent is negotiable and not restricted by the FAR

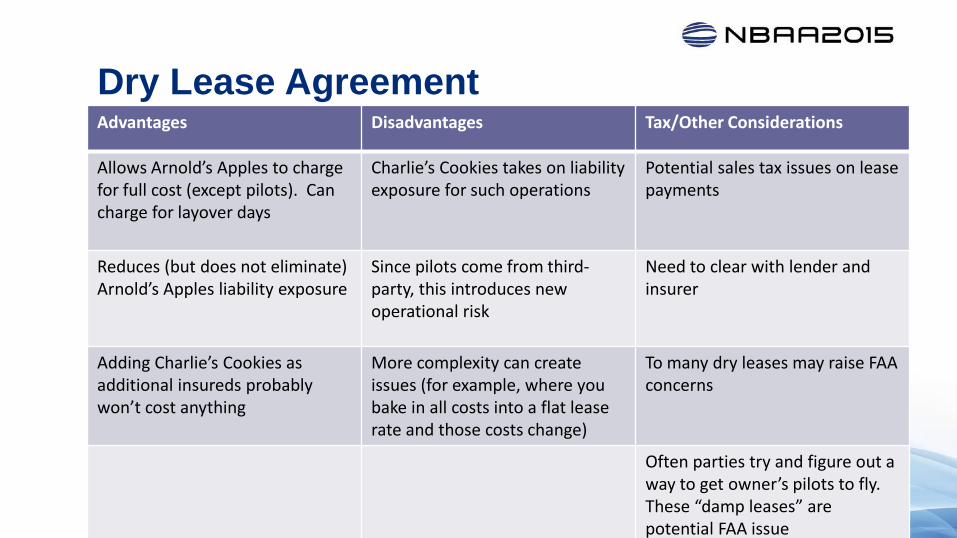

Dry Lease Agreement

33

Advantages Disadvantages Tax/Other Considerations

Allows Arnold’s Apples to charge for full cost (except pilots). Can charge for layover days

Charlie’s Cookies takes on liability exposure for such operations

Potential sales tax issues on lease payments

Reduces (but does not eliminate) Arnold’s Apples liability exposure

Since pilots come from third-party, this introduces new operational risk

Need to clear with lender and insurer

Adding Charlie’s Cookies as additional insureds probably won’t cost anything

More complexity can create issues (for example, where you bake in all costs into a flat lease rate and those costs change)

To many dry leases may raise FAA concerns

Often parties try and figure out a way to get owner’s pilots to fly. These “damp leases” are potential FAA issue

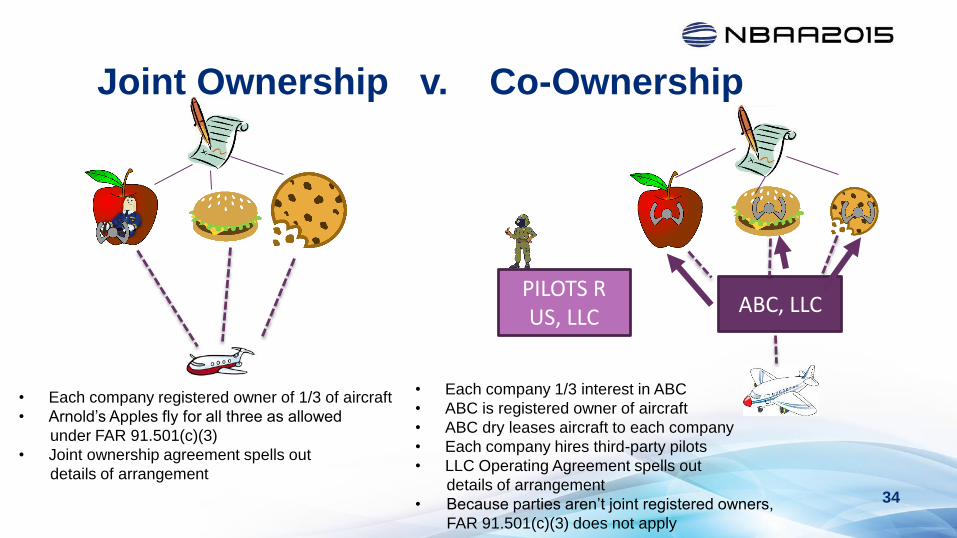

Joint Ownership v. Co-Ownership

ABC, LLC

• Each company registered owner of 1/3 of aircraft

• Arnold’s Apples fly for all three as allowed

under FAR 91.501(c)(3)

• Joint ownership agreement spells out

details of arrangement

PILOTS R US, LLC

• Each company 1/3 interest in ABC

• ABC is registered owner of aircraft

• ABC dry leases aircraft to each company

• Each company hires third-party pilots

• LLC Operating Agreement spells out

details of arrangement

• Because parties aren’t joint registered owners,

FAR 91.501(c)(3) does not apply

34

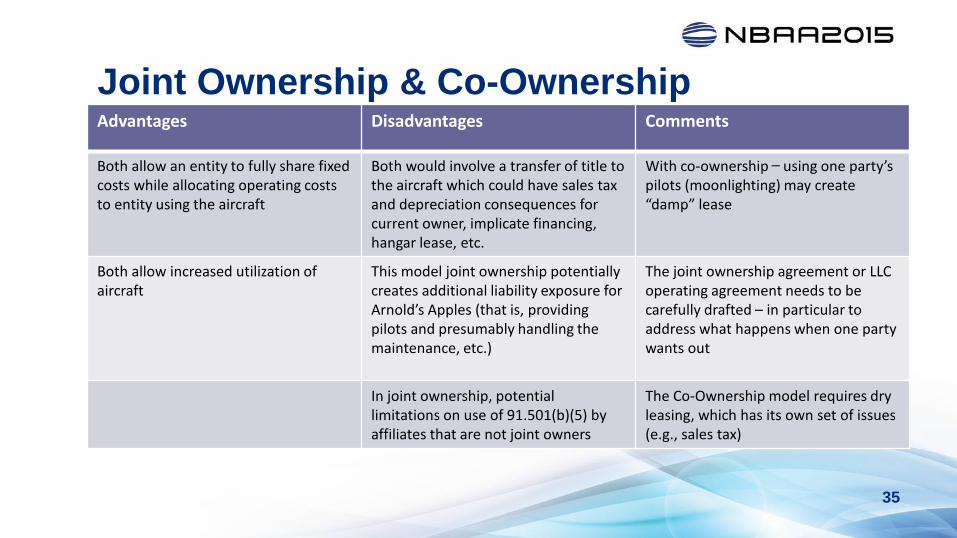

Joint Ownership & Co-Ownership

35

Advantages Disadvantages Comments

Both allow an entity to fully share fixed costs while allocating operating costs to entity using the aircraft

Both would involve a transfer of title to the aircraft which could have sales tax and depreciation consequences for current owner, implicate financing, hangar lease, etc.

With co-ownership ̶ using one party’s pilots (moonlighting) may create “damp” lease

Both allow increased utilization of aircraft

This model joint ownership potentially creates additional liability exposure for Arnold’s Apples (that is, providing pilots and presumably handling the maintenance, etc.)

The joint ownership agreement or LLC operating agreement needs to be carefully drafted – in particular to address what happens when one party wants out

In joint ownership, potentiallimitations on use of 91.501(b)(5) by affiliates that are not joint owners

The Co-Ownership model requires dryleasing, which has its own set of issues (e.g., sales tax)

36

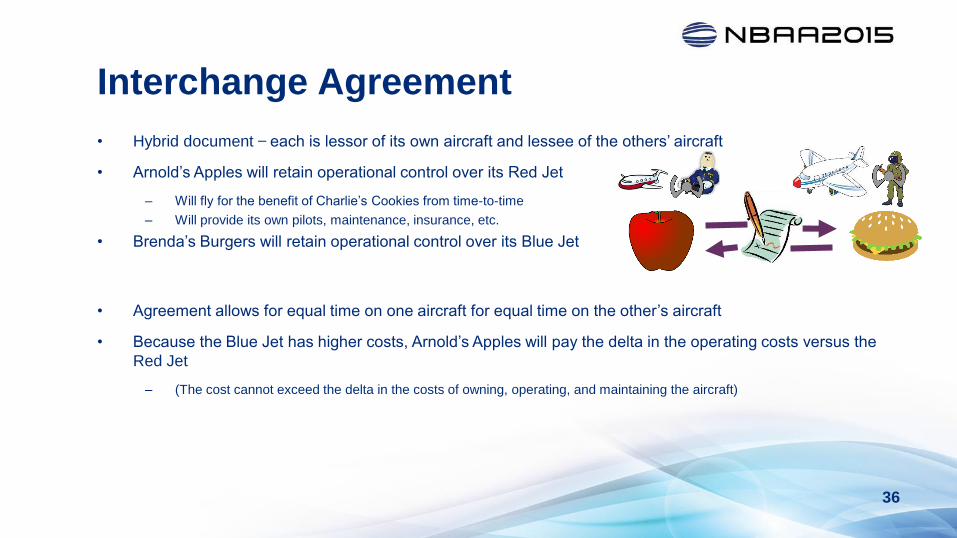

Interchange Agreement

• Hybrid document ̶ each is lessor of its own aircraft and lessee of the others’ aircraft

• Arnold’s Apples will retain operational control over its Red Jet

– Will fly for the benefit of Charlie’s Cookies from time-to-time

– Will provide its own pilots, maintenance, insurance, etc.

• Brenda’s Burgers will retain operational control over its Blue Jet

• Agreement allows for equal time on one aircraft for equal time on the other’s aircraft

• Because the Blue Jet has higher costs, Arnold’s Apples will pay the delta in the operating costs versus the

Red Jet

– (The cost cannot exceed the delta in the costs of owning, operating, and maintaining the aircraft)

Interchange Agreement

37

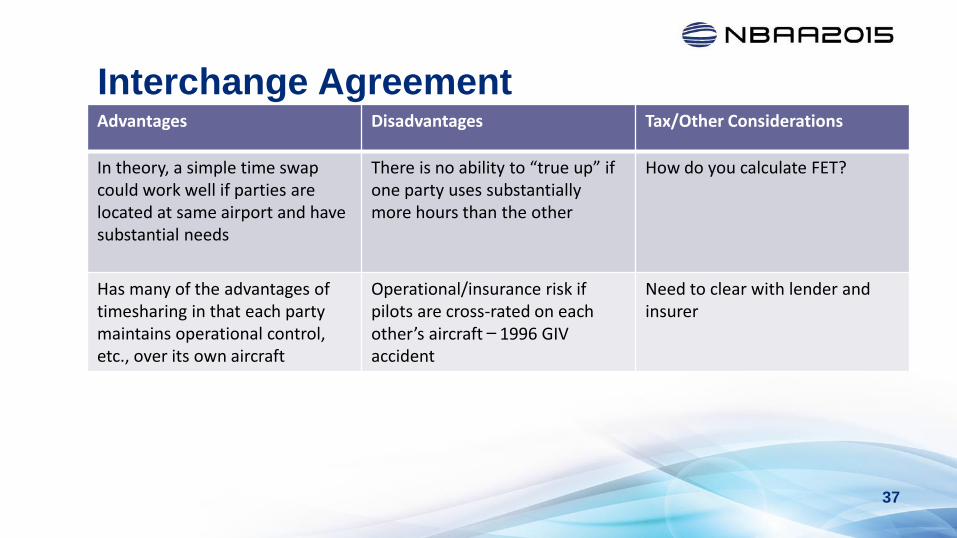

Advantages Disadvantages Tax/Other Considerations

In theory, a simple time swapcould work well if parties are located at same airport and have substantial needs

There is no ability to “true up” if one party uses substantially more hours than the other

How do you calculate FET?

Has many of the advantages of timesharing in that each party maintains operational control, etc., over its own aircraft

Operational/insurance risk if pilots are cross-rated on each other’s aircraft ̶ 1996 GIV accident

Need to clear with lender and insurer

Aircraft Registration and Cape Town Treaty Considerations

Just when you thought the structure was set!

PRESENTED BY:

Scott McCreary

Shareholder, McAfee & Taft A Professional Corporation, Oklahoma City, Oklahoma

1.405.552.2367 [email protected]

Tuesday, November 27. 2015 | 10:45 a.m. – 11:00 a.m.

39

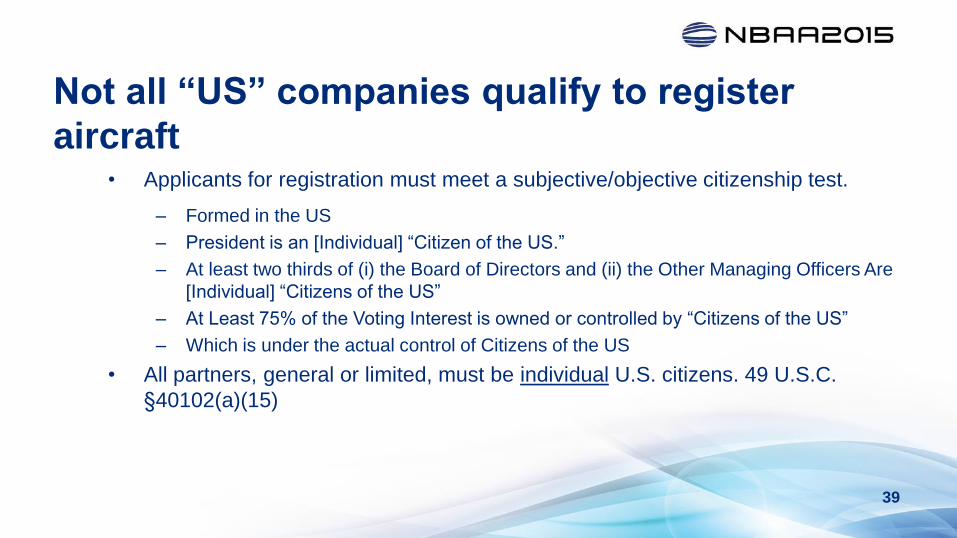

Not all “US” companies qualify to register

aircraft• Applicants for registration must meet a subjective/objective citizenship test.

– Formed in the US

– President is an [Individual] “Citizen of the US.”

– At least two thirds of (i) the Board of Directors and (ii) the Other Managing Officers Are

[Individual] “Citizens of the US”

– At Least 75% of the Voting Interest is owned or controlled by “Citizens of the US”

– Which is under the actual control of Citizens of the US

• All partners, general or limited, must be individual U.S. citizens. 49 U.S.C.

§40102(a)(15)

40

Additional registration considerations• Aircraft must be registered in the name of owner, not nominee

– Name is in public record

– LLC Statements in Support may disclose additional confidential information

– Registered owner receives FAA notices / re-registration requirements

– Registered owner may have additional liability

• Carefully designate fractional or percentage interests

– International Registry uses percentage interests

• Invalid registration may

– subject parties to fines/penalties

– ground aircraft

– insurance issues

• When should Arnold’s Apples care if Brenda’s Burgers has properly registered its

aircraft?

41

Other issues

• Dry leases may create “power to dispose” issues under Cape Town Treaty

– Official Commentary - if the lease is not registered on International Registry the lessee

may have power to sell or encumber aircraft/engines

– Interchange and Timesharing Agreements are not leases under the Treaty

• Lender’s may require dry leases be recorded with FAA and registered on the

International Registry

– To address power to dispose issue

– Only way to perfect collateral assignment of the leases

– Truth in Leasing filings are not perfection filings

• Additional joint ownership / co-ownership considerations

– Put/call options

– Security agreement to secure joint owner obligations

– Powers of attorney

Scenario III. Personal Use by

Individuals

PRESENTED BY:

Paul Alp

Counsel, Crowell & Moring LLP

202.624.2747 [email protected]

Tuesday, November 27. 2015

43

A Common Situation

• Brenda wants to fly in her company’s jet

to Aspen with her family for a ski weekend

• Will stop in Dallas on the way for a company meeting

• Questions:

– Whether or to what extent Brenda may reimburse

Brenda’s Burgers for the trip

– What are the FAA issues?

– What are the IRS issues?

44

Personal Use

• Definition: flight by employee not for company business on an

aircraft provided by employer

– Can include non-business portion of trip where business and

pleasure are mixed

– “Employee” includes guests of the employee

• Fundamental principles

– FAA: employee reimbursement to company for personal use of

aircraft is highly limited

– IRS: value of unreimbursed personal flights must be treated as a

fringe benefit to the employee – taxable income

45

FAA Considerations

46

Reimbursement Under the FARs

• FAA generally prohibits aircraft operators from obtaining

reimbursement for flights conducted under Part 91, with limited

exceptions, such as:

– A corporation owning a business jet may obtain limited

reimbursement from an employee for certain costs if the flight is

• (i) “within the scope of” and

• (ii) “incidental to”

• the business of the company. [FAR 91.501(b)(5)]

• Employee reimbursement for personal use of company aircraft is

highly limited

Nichols Opinion (Pt 1)

• An employee may reimburse employer for costs of certain personal

flights if various conditions are met:

– Employee is a key executive named by company whose routine

personal travel plans often change due to nature of his or her

position with the company

– Company keeps a list of such executives and makes it available

to the FAA

– Company keeps records indicating its determination that the flight

in question was of a “routine personal nature”

47

48

Nichols Opinion (Pt 2)

• What does this mean?

– Example: senior executive whose routine personal travel plans are

likely to be changed for business reasons

• As a practical matter, how is the rule applied?

– Determinations: Which executives? Which flights?

– Which flights can’t be charged?

– What can be reimbursed?

• Maximum amount that may be charged is amount that does not exceed

pro-rata share of costs of owning, operating, and maintaining the aircraft

49

Alternative Arrangements

• Dry Leasing

• Time Sharing

• Charter from management company

50

Dry Leasing

• Lease aircraft to executive without crew

• Advantage: no limits on amount the company can charge the

employee for the lease

• Disadvantage: employee is personally responsible and

potentially liable for operation of the aircraft

51

Time Sharing

• Owner wet leases the aircraft to employee with limited rights to

recover certain costs

• Advantage: avoids making employee accept personal

responsibility and liability

• Disadvantages

– Amount that may be reimbursed is strictly limited to certain per-flight

items [see FAR 91.501(d)]

– Charges are subject to Federal Excise Tax

52

IRS Considerations

53

Imputation of Income

• If a flight is provided to an employee (or guest) the flight is

potentially taxable to the employee

– Why?

– When flying on a company aircraft for personal reasons, the

employee receives something of value

• Calculation of value of flight to employee

– Charter rate method: reference how much it would cost to charter

the same or comparable aircraft for the flight (rarely used), or

– Standard Industry Fair Level (SIFL): a mileage based formula

54

Valuation Under SIFL (Pt 1)

• Based on cents-per-mile cost of trip published by DOT

• Different rates for control v. non-control employees

• A multiple for aircraft weight (MTOW) is applied

• Includes a “terminal charge” determined by DOT

• Less tax consequences for employees than charter rate method

55

Valuation Under SIFL (Pt 2)

• Calculated on a passenger by passenger basis

• Based on mileage (statute miles flown)

– From where individual boards to where they deplane

• Employee status

– Control employee: owns 5% of more of company, most officers or

directors, etc.

– Non-control employee: everyone else

• Lower valuation multiple used (pays less tax)

56

Valuation Under SIFL (Pt 3)

• Spouse of employee

– Generally considered personal travel; imputed benefit to employee

– May be treated as a business flight if “bona fide business purpose”

• The seating capacity rule (aka the “50% Rule”)

– If 50% capacity filled with business travelers when employee or

family member boards, no fringe benefit is imputed

• Security: the “Safe Harbor Rules”

– Bona fide security concern

– 200% multiplier

57

Mixing Business With Pleasure

• One destination: two purposes

– What was primary purpose of employee’s travel?

• How much time on business? Travelling with family?

• Multiple destinations: some business, some pleasure

– Primarily business flights

• If trip primarily for company business, include as income total value of

trip minus business flights

– Primarily personal flights

• Include as income value of personal flights that would have been taken

if no company business was conducted

58

Other Considerations

59

SEC Issues

• Public companies must disclose “value” of unreimbursed aircraft

personal use by key executives (“Named Executive Officer”)

– Amounts exceeding $10,000 must be disclosed as part of annual

reporting to shareholders

– Amounts exceeding the greater of $25,000 or 10% of total

perquisites (personal benefits) require a separate explanation

• Value = “Aggregate Incremental Cost” of providing the

compensation

– Costs the company would not have incurred without the personal

use of the aircraft by the NEO

60

Questions & AnswersYour Panel:

Victor Smith (Moderator)

Garofalo Goerlich Hainbach PC

(202) 776-3978

Michael Fleming

The Wicks Group PLLC

(202) 457-7790

Jonathan Epstein

Holland & Knight LLP

(202) 828-1870

Paul Alp

Crowell & Moring LLP

(202) 624-2747

Scott McCreary

McAfee & Taft

(405) 552-2367