Embed Size (px)

Citation preview

Da

ibo

ch

i Pla

stic &

P

ac

ka

gin

g In

du

stry

Be

rha

d

Inv

esto

rs’ Brie

fing

FY1

2 Fin

an

cia

l Re

sults &

Co

rpo

rate

Up

da

te

26

Feb

rua

ry 2

01

3

IR A

dv

ise

r

AQ

UIL

AS

•Operatio

nal H

ighlights

•Financial H

ighlights

•FY2013 Growth Stra

tegies

2

•FY2013 Growth Stra

tegies

•Appendix:

»Corporate Profile

»Industry

Insig

ht

Opera

tional H

ighlig

hts

3

Opera

tional H

ighlig

hts

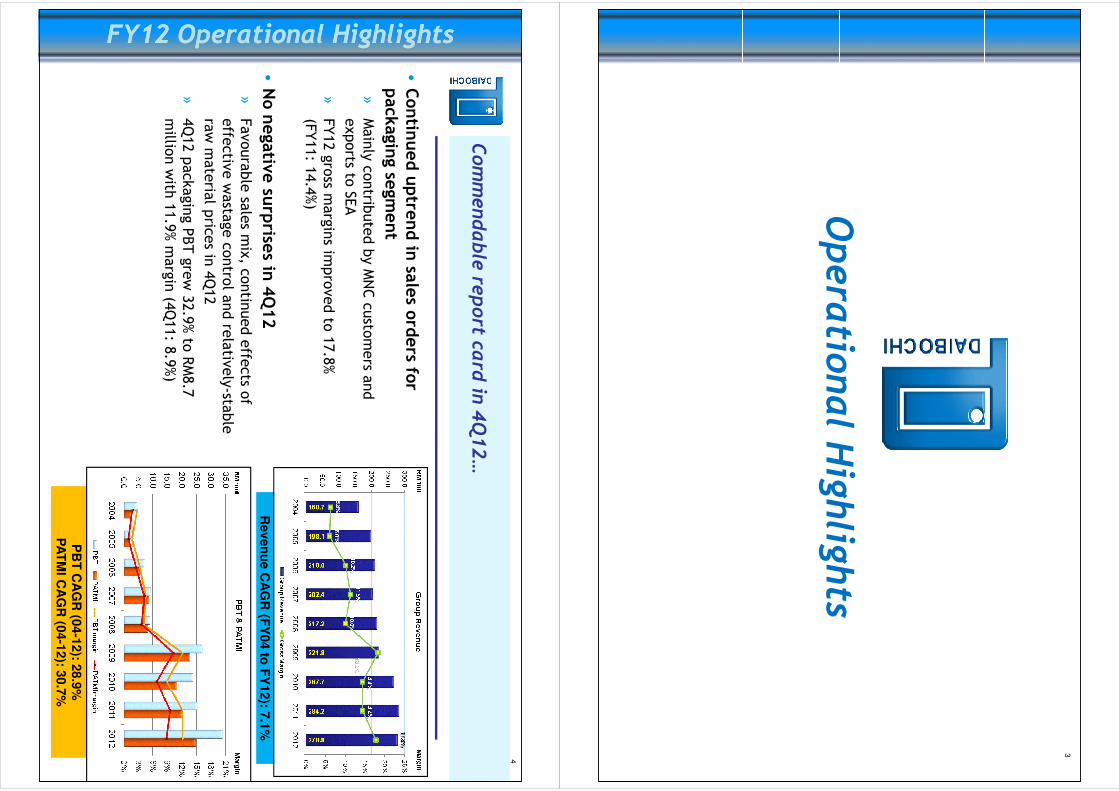

•Contin

ued uptre

nd in sa

les o

rders fo

r packagin

g segm

ent

»Mainly contrib

uted by MNC custo

mers a

nd

exports to

SEA

»FY12 gross m

argins im

proved to

17.8%

(FY11: 1

4.4%)

4

FY12 Operational HighlightsFY12 Operational Highlights

Commendable re

port ca

rd in

4Q12…

•No negative su

rprise

s in 4Q12

»Favourable

sales m

ix, c

ontin

ued effe

cts o

f

effe

ctiv

e wasta

ge contro

l and re

lativ

ely-sta

ble

raw m

ateria

l pric

es in

4Q12

»4Q12 packaging PBT grew 32.9% to

RM8.7

millio

n with

11.9% m

argin (4

Q11: 8

.9%)

FY12 Operational HighlightsFY12 Operational Highlights

Reven

ue C

AG

R (F

Y04 to

FY

12): 7

.1%

PB

T C

AG

R (0

4-1

2): 2

8.9

%P

AT

MI C

AG

R (0

4-1

2): 3

0.7

%

FY12

5

FY12

Financia

l Review

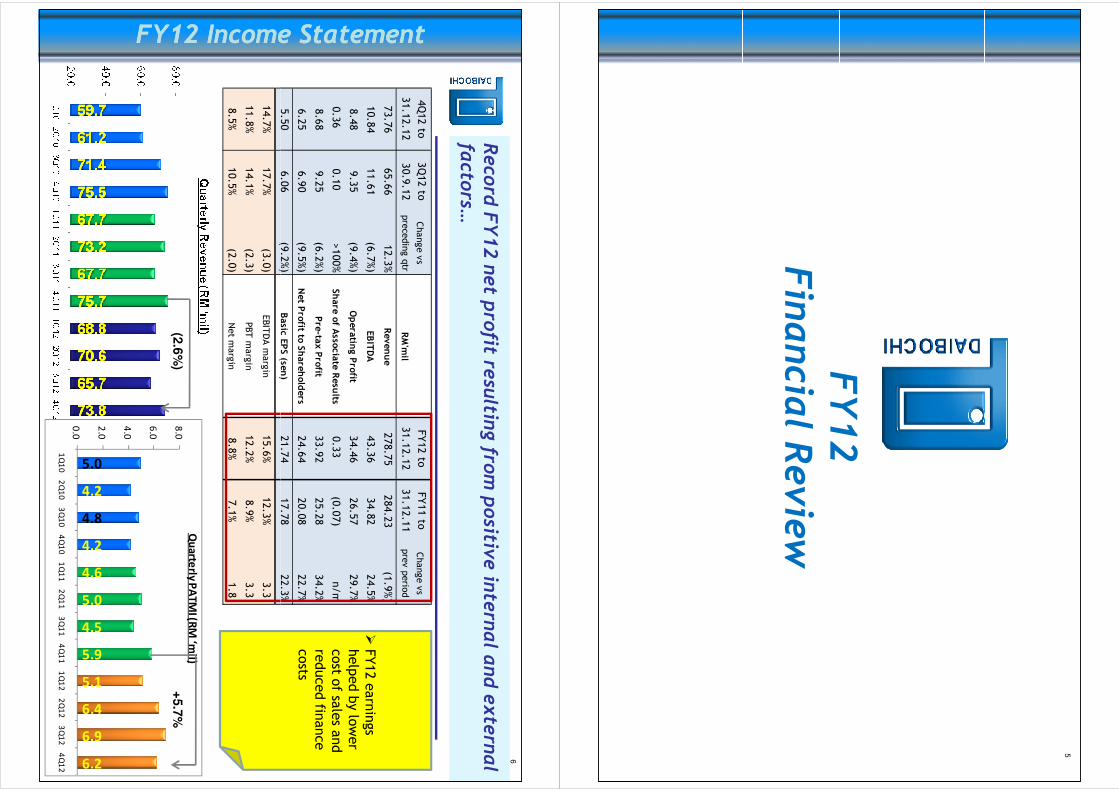

4Q12 to

31.12.12

3Q12 to

30.9.12

Change vs

preceding qtr

RM'mil

FY12 to

31.12.12

FY11 to

31.12.11

Change vs

prev perio

d

73.76

65.66

12.3%

Revenue

278.75

284.23

(1.9%)

10.84

11.61

(6.7%)

EBITDA

43.36

34.82

24.5%

8.48

9.35

(9.4%)

Operatin

g Profit

34.46

26.57

29.7%

0.36

0.10

>100%

Share of A

ssociate Results

0.33

(0.07)

n/m

8.68

9.25

(6.2%)

Pre-ta

x Profit

33.92

25.28

34.2%

6.25

6.90

(9.5%)

Net P

rofit to

Shareholders

24.64

20.08

22.7%

5.50

6.06

(9.2%)

Basic

EPS (se

n)

21.74

17.78

22.3%

6

FY12 Income StatementFY12 Income Statement

Reco

rd FY12 net p

rofit re

sultin

g fro

m positiv

e in

tern

al a

nd extern

al

facto

rs…

�FY12 earnings

helped by lo

wer

cost o

f sales a

nd

reduced fin

ance

costs

5.50

6.06

(9.2%)

Basic

EPS (se

n)

21.74

17.78

22.3%

14.7%

17.7%

(3.0)

EBITDA m

argin

15.6%

12.3%

3.3

11.8%

14.1%

(2.3)

PBT m

argin

12.2%

8.9%

3.3

8.5%

10.5%

(2.0)

Net m

argin

8.8%

7.1%

1.8

FY12 Income StatementFY12 Income Statement

(2.6

%)

5.0

4.2

4.8

4.2

4.6

5.0

4.5

5.9

5.1

6.4

6.9

6.2

0.0

2.0

4.0

6.0

8.0

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

3Q12

4Q12

Qu

arte

rly P

AT

MI (R

M ‘m

il)

+5.7

%

7Packaging Revenue & PBT TrendPackaging Revenue & PBT Trend

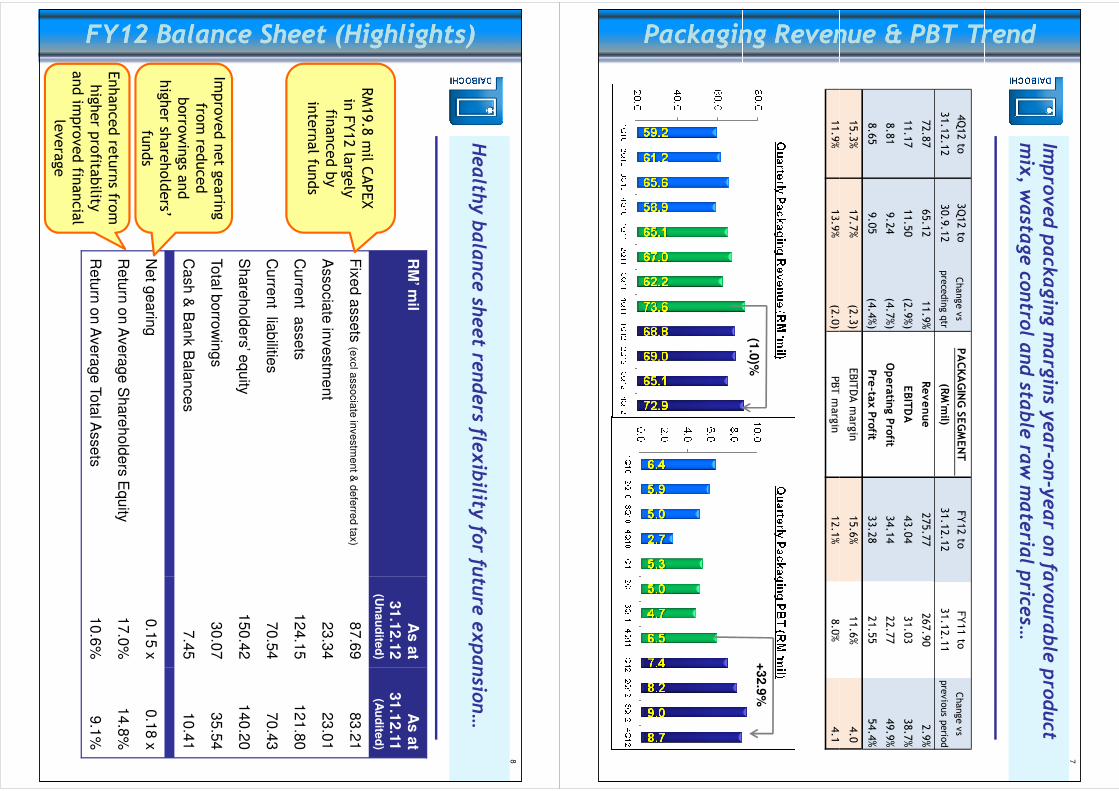

Impro

ved pack

aging m

argins y

ear-o

n-year o

n fa

voura

ble

pro

duct

mix, w

asta

ge co

ntro

l and sta

ble ra

w m

ateria

l price

s…

4Q12 to

31.12.12

3Q12 to

30.9.12

Change vs

preceding qtr

PACKAGING SEGMENT

(RM'mil)

FY12 to

31.12.12

FY11 to

31.12.11

Change vs

previous p

erio

d

72.87

65.12

11.9%

Revenue

275.77

267.90

2.9%

11.17

11.50

(2.9%)

EBITDA

43.04

31.03

38.7%

8.81

9.24

(4.7%)

Operatin

g Profit

34.14

22.77

49.9%

8.65

9.05

(4.4%)

Pre-ta

x Profit

33.28

21.55

54.4%

15.3%

17.7%

(2.3)

EBITDA m

argin

15.6%

11.6%

4.0

11.9%

13.9%

(2.0)

PBT m

argin

12.1%

8.0%

4.1

Packaging Revenue & PBT TrendPackaging Revenue & PBT Trend

(1.0

)%+

32.9

%

11.9%

13.9%

(2.0)

PBT m

argin

12.1%

8.0%

4.1

8

FY12 Balance Sheet (Highlights)FY12 Balance Sheet (Highlights)

Health

y balance

sheet re

nders fle

xibility

for fu

ture expansio

n…

RM

’ mil

As

at

31

.12

.12

(Un

au

dite

d)

As

at

31

.12

.11

(Au

dite

d)

Fix

ed

asse

ts (e

xcl a

sso

cia

te in

ve

stm

en

t & d

efe

rred

tax)

87

.69

83

.21

Asso

cia

te in

ve

stm

en

t 2

3.3

42

3.0

1

Cu

rren

t asse

ts

12

4.1

51

21

.80

RM19.8 m

il CAPEX

in FY12 la

rgely

financed by

internal fu

nds

FY12 Balance Sheet (Highlights)FY12 Balance Sheet (Highlights)

Cu

rren

t liab

ilities

70

.54

70

.43

Sh

are

ho

lde

rs’ e

qu

ity1

50

.42

14

0.2

0

To

tal b

orro

win

gs

30

.07

35

.54

Ca

sh

& B

an

k B

ala

nce

s7

.45

10

.41

Ne

t ge

arin

g0

.15

x0

.18

x

Re

turn

on

Ave

rag

e S

ha

reh

old

ers

Eq

uity

17

.0%

14

.8%

Re

turn

on

Ave

rag

e T

ota

l Asse

ts1

0.6

%9

.1%

Improved net g

earin

g

from re

duced

borro

wings a

nd

higher sh

areholders’

funds

Enhanced re

turns fro

m

higher p

rofita

bility

and im

proved fin

ancial

leverage

9Dividend HistoryDividend History

Reco

rd dividend payout in

line w

ith earn

ings…

distrib

utin

g 61.5% of

FY2012 net p

rofit a

s dividends

•4thinterim

dividendof 3

.5 se

nper sh

are in

respect o

f FY2012

(amountin

g to

RM4.0 m

il) to be paid

on 12 April 2

013

•Dividends in

respect o

f FY2012

Dividend HistoryDividend History

»1stinterim

tax exempt d

ividend of

3.5 se

n/share (p

aid on 8 Jun 2012)

-Adju

sted D

PS: 2

.3 se

n

»2ndinterim

tax exempt d

ividend of

6.0 se

n/share (p

aid on 7 Sep 2012)

-Adju

sted D

PS: 4

.0 se

n

»3rdinterim

tax exempt d

ividend of

3.5 se

n/share (p

aid on 7 Dec 2012)

^Sin

ce 2

Q12, D

aib

och

i revise

d its d

ivid

end p

olicy

upw

ard

s to p

ay n

o le

ss than 6

0% o

f gro

up n

et p

rofit a

s

div

idends

* Ad

juste

d fo

r 1-fo

r-2 B

on

us Is

su

e, e

ffectiv

e 1

0 S

ep

tem

be

r 20

12

10

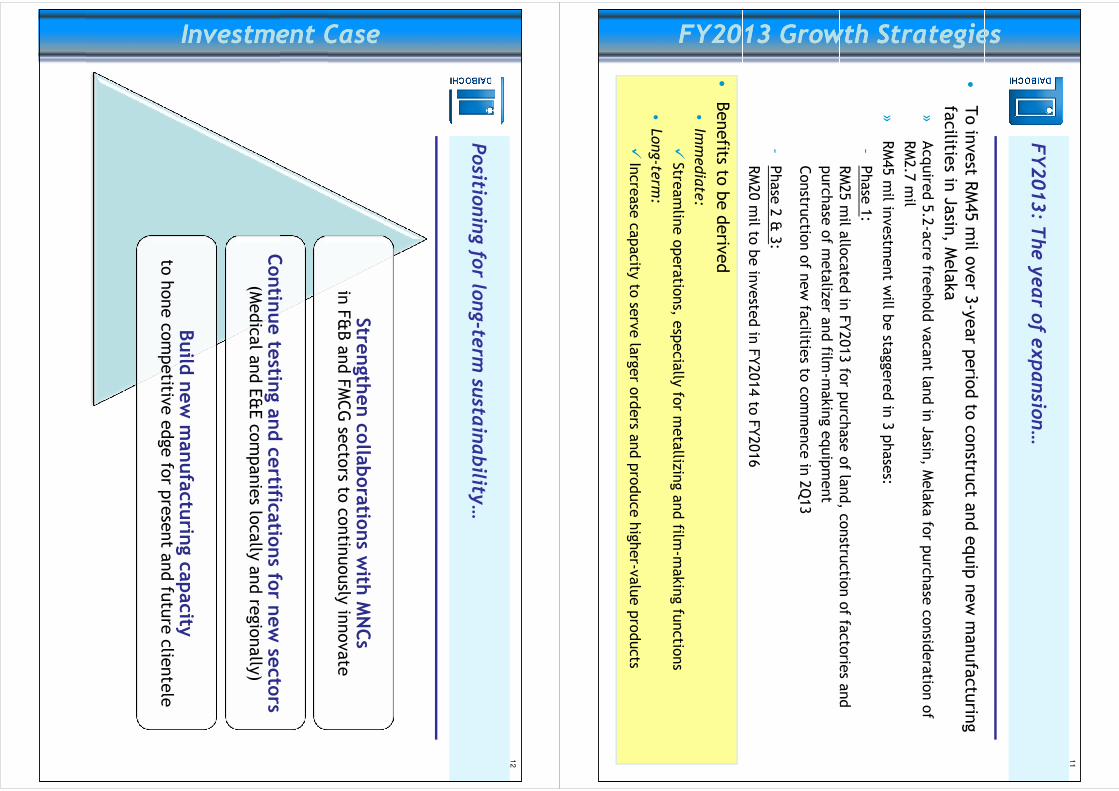

PROSPECTS AND PLANS

•To in

vest R

M45 m

il over 3

-year p

erio

d to

constru

ct a

nd equip new m

anufacturin

g

facilitie

s in Jasin

, Melaka

»Acquire

d 5.2-acre fre

ehold vacant la

nd in

Jasin

, Melaka fo

r purchase consid

eratio

n of

RM2.7 m

il

»RM45 m

il investm

ent w

ill be sta

ggered in

3 phases:

-Phase 1:

RM25 m

il allo

cated in

FY2013 fo

r purchase of la

nd, c

onstru

ctio

n of fa

ctorie

s and

11

FY2013: T

he year o

f expansio

n…

FY2013 Growth StrategiesFY2013 Growth Strategies

RM25 m

il allo

cated in

FY2013 fo

r purchase of la

nd, c

onstru

ctio

n of fa

ctorie

s and

purchase of m

etalizer a

nd film

-making equipment

Constru

ctio

n of n

ew fa

cilitie

s to commence in

2Q13

-Phase 2 & 3:

RM20 m

il to be in

veste

d in

FY2014 to

FY2016

FY2013 Growth StrategiesFY2013 Growth Strategies

•Benefits to

be deriv

ed

•Im

media

te:

�Stre

amlin

e operatio

ns, e

specially

for m

etalliz

ingand film

-making fu

nctio

ns

•Long-te

rm:

�Increase capacity

to se

rve la

rger o

rders a

nd produce higher-v

alue products

Strength

en co

llaboratio

ns w

ith MNCs

in F&B and FMCG se

ctors to

contin

uously

innovate

Contin

ue te

sting a

nd ce

rtificatio

ns fo

r new se

ctors

12

Positio

ning fo

r long-te

rm su

stainability

…

Investment CaseInvestment Case

Contin

ue te

sting a

nd ce

rtificatio

ns fo

r new se

ctors

(Medical a

nd E&E companies lo

cally and re

gionally)

Build new manufactu

ring ca

pacity

to hone competitiv

e edge fo

r present a

nd fu

ture clie

ntele

Investment CaseInvestment Case

13

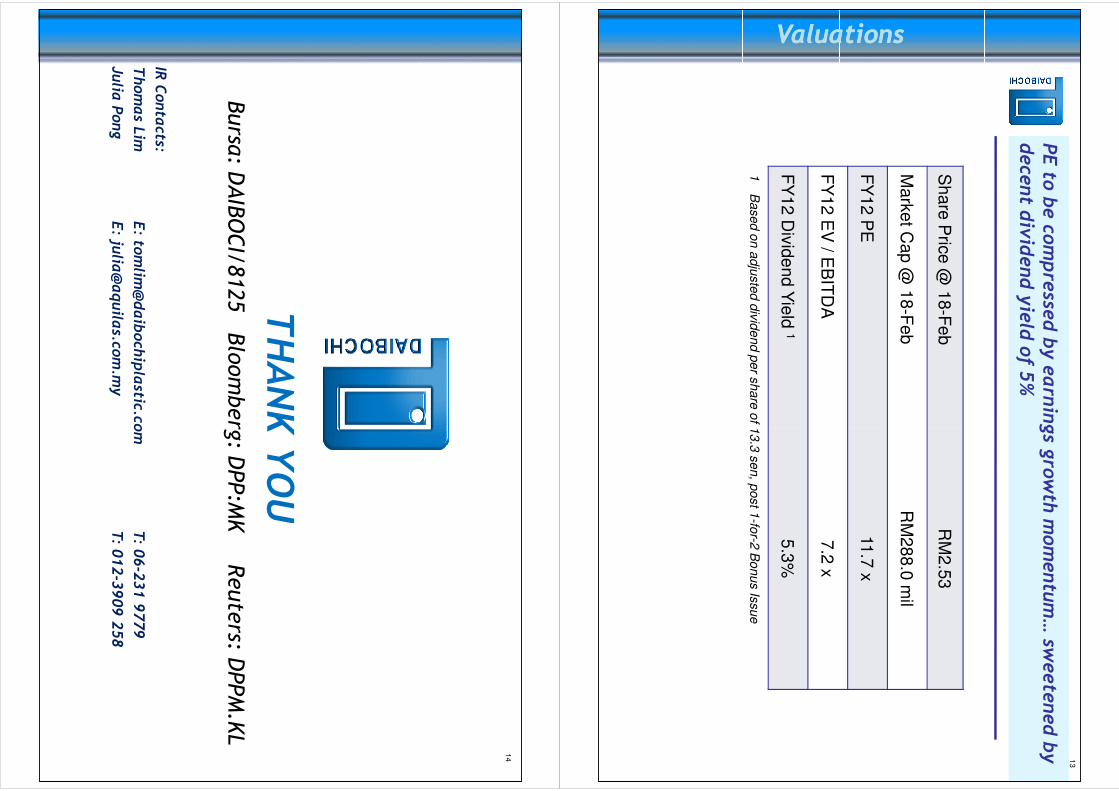

PE to

be co

mpresse

d by earn

ings g

rowth m

omentum… sw

eetened by

dece

nt d

ividend yield of 5

%

ValuationsValuations

Sh

are

Pric

e @

18

-Fe

bR

M2

.53

Ma

rke

t Ca

p @

18

-Fe

bR

M2

88

.0 m

il

FY

12

PE

11

.7 x

ValuationsValuations

FY

12

EV

/ EB

ITD

A7

.2 x

FY

12

Div

ide

nd Y

ield

15

.3%

1B

ased o

n a

dju

ste

d d

ivid

end p

er s

hare

of 1

3.3

sen, p

ost 1

-for-2

Bonus Is

sue

THANK YOU

14

THANK YOU

Bursa

: DAIB

OCI/

8125

Blo

om

berg

: DPP:M

KReute

rs: DPPM

.KL

IR Conta

cts:

Thomas L

imE: to

mlim

@daiboch

iplastic.c

om

T: 0

6-231 9779

Julia

Pong

E: ju

lia@aquila

s.com.m

yT: 0

12-3909 258

APPENDIX

15

APPENDIX

CORPORATE PROFILE

16

CORPORATE PROFILE

The LARGEST su

pplier o

f packagin

g in SE

AThe LARGEST su

pplier o

f packagin

g in SE

A

17

Daiboch

i, a re

silient in

vestm

ent ca

se…

Track RecordTrack Record

The SO

LE su

pplier to

Chembong C

onfectio

nery

The SO

LE su

pplier to

Chembong C

onfectio

nery

Facto

ry in M’sia

Facto

ry in M’sia

Supplier o

f >90% of ’s fle

xible packa

ging in

M’sia

Supplier o

f >90% of ’s fle

xible packa

ging in

M’sia

Track RecordTrack Record

Supplier o

f >90% of ’s fle

xible packa

ging in

M’sia

Supplier o

f >90% of ’s fle

xible packa

ging in

M’sia

The SO

LE su

pplier o

f The SO

LE su

pplier o

f biscu

its in M’sia

biscu

its in M’sia

Other im

porta

nt c

usto

mers:

�Liste

d sin

ce 1990, n

ow on Main Market o

f Bursa

M’sia

�Market ca

p of R

M288.0 mil (1

8.2.2013)

�Dividend policy

of p

aying m

inimum 60% of annual net p

rofit to

shareholders, o

n a quarte

rly basis

DA

IBO

CH

I PL

AS

TIC

& P

AC

KA

GIN

G IN

DU

ST

RY

BE

RH

AD

Lis

ted

Main

Mark

et, B

urs

a M

ala

ysia

sin

ce 1

990

(Tra

nsfe

rred fro

m S

econd B

oard

in 2

003)

Secto

rIn

dustria

l Pro

ducts

18

Liste

d sin

ce 1990…

Corporate InformationCorporate Information

Secto

rIn

dustria

l Pro

ducts

Codes

Burs

a: 8

125 / D

AIB

OC

I

Blo

om

berg

: DP

P:M

K

Reute

rs: D

PP

M.K

L

Share

Capita

lR

M113.9

mil (1

13.8

53 m

il share

s o

f RM

1.0

0 e

ach)

Mark

et C

apita

lizatio

nR

M288.0

mil (R

M2.5

3 a

s a

t 18 F

eb 2

013)

Corporate InformationCorporate Information

Corporate ProfileCorporate Profile1

9

Leading fle

xible pack

aging so

lutio

ns p

rovider, w

ith enviable

reputa

tion exce

eding 35 years…

20

09

-A

cq

uire

d 9

thp

rintin

g m

ach

ine

; Ob

tain

ed

HA

LA

L C

ertific

atio

n;

20

08

–A

cq

uire

d w

ide

we

b p

oly

pro

pyle

ne

film m

akin

g m

ach

ine

20

07

-R

ece

ive

d G

old

Aw

ard

for th

e C

olo

rpa

kP

acka

gin

g

Exp

ort A

wa

rd a

t Au

stra

lian

Pa

cka

gin

g A

wa

rds

20

04

–A

cq

uire

d M

’sia

’s 1

st5

-laye

r-blo

wn

film m

ach

ine

to

pro

du

ce

tran

sp

are

nt b

arrie

r films

Re

gio

na

l su

pp

lier fo

r BA

T

20

10

–O

bta

ine

d L

ette

r of V

alid

atio

n fro

m U

SA

for e

lectro

nic

pa

cka

gin

g

20

11

–A

cq

uire

d h

igh

-sp

ee

d p

rintin

g m

ach

ine

; Acq

uire

d m

eta

llize

rto

pro

du

ce

ultra

hig

h b

arrie

r films;

Accre

dite

d w

ith IS

O:1

40

01

20

12

–S

et u

p C

lea

nro

om

for b

ag

gin

g p

roce

ss

Corporate ProfileCorporate Profile

19

94

–A

cq

uire

d fa

ste

st e

xtru

sio

n la

min

ato

r in S

EA

19

96

-M

ove

d to

cu

rren

t pre

mis

es w

ith >

32

5,0

00

sq

ft bu

ilt-up

are

a

20

01

–In

co

rpo

rate

d A

ustra

lian

su

bsid

iary

; Accre

dite

d w

ith IS

O:9

00

1

19

99

–S

up

plie

r to N

estle

M’s

ia

20

02

–A

cq

uire

d m

eta

llize

r with

Pla

sm

a T

ech

to p

rod

uce

hig

h-b

arrie

r films;

Re

gio

na

l Su

pp

lier to

Ne

stle

in S

EA

20

03

–T

ran

sfe

r to M

ain

Bo

ard

(no

w M

ain

Ma

rke

t); Accre

dite

d w

ith H

AC

CP

19

90

–A

cq

uire

d m

eta

llize

rto

pro

du

ce

in-h

ou

se

me

taliz

ed

films; L

iste

d o

n 2

nd

Bo

ard

of K

LS

E (B

urs

a M

’sia

)

19

87

–A

cq

uire

d p

oly

pro

pyle

ne

film-m

akin

g m

ach

ine

to p

rod

uce

in-h

ou

se

films

19

84

–S

tarte

d in

-ho

use

prin

ting

cylin

de

r ma

kin

g

19

72

–E

sta

blis

he

d in

Me

laka

with

10

,00

0 s

q ft p

lan

t; Mo

ve

d to

larg

er p

rem

ise

s w

ith 1

65

,52

7 s

q ft

Corporate Profile (con’t)Corporate Profile (con’t)

••Accre

dite

d and world

Accre

dite

d and world

--class

class

productio

n facilitie

sproductio

n facilitie

s»

Atta

ined ISO

:9001and ISO

:14001

certific

atio

ns

»Hazard Analysis C

ritical C

ontro

l Points

(HACCP) c

ompliant to

ensure

20

Intern

atio

nally

-certifie

d pro

ductio

n fa

cilities th

at co

mply

with

all fa

ctory

audits b

y our M

NC clie

ntele…

Corporate Profile (con’t)Corporate Profile (con’t)

(HACCP) c

ompliant to

ensure

adherence to

food sa

fety re

quire

ments

••Well

Well--e

quipped laboratory te

sting

equipped laboratory te

sting

facilitie

sfacilitie

s»

To ensure our p

roducts e

xceed custo

mers’

pack

agin

g b

arrie

r (MVTR ASTM F1249, O

2TR

ASTM D3895-35), re

tentio

n(GC with

Headspace) a

nd m

igra

tion(COF ASTM

D1894) re

quire

ments.

21

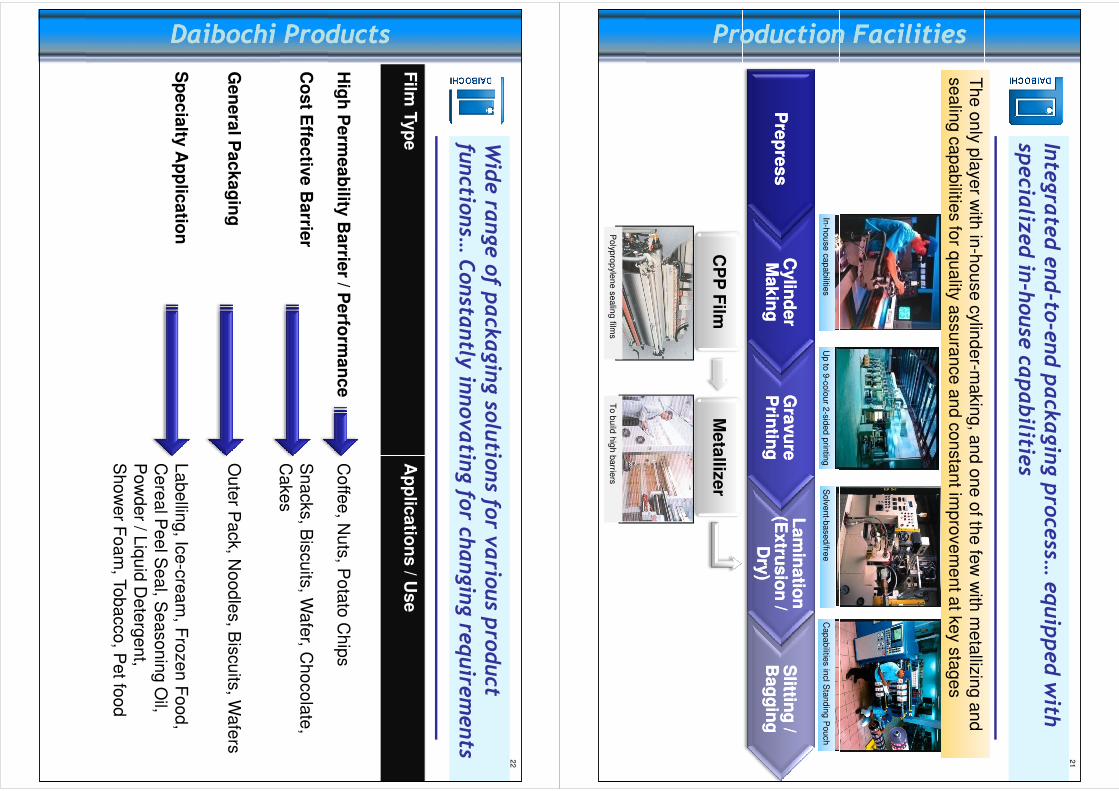

Production FacilitiesProduction Facilities

Integra

ted end-to

-end pack

aging pro

cess…

equipped w

ith

specia

lized in

-house

capabilitie

s

Th

e o

nly

pla

ye

r with

in-h

ou

se

cylin

de

r-ma

kin

g, a

nd

on

e o

f the

few

with

me

talliz

ing

an

d

se

alin

g c

ap

abilitie

s fo

r qu

ality

assu

ran

ce

an

d c

on

sta

nt im

pro

ve

me

nt a

t ke

y s

tag

es

Production FacilitiesProduction Facilities

Pre

pre

ss

Pre

pre

ss

Cylin

de

r C

ylin

de

r M

ak

ing

Ma

kin

gG

ravu

re

Gra

vu

re

Prin

ting

Prin

ting

La

min

atio

n

La

min

atio

n

(Ex

trus

ion

/ (E

xtru

sio

n /

Dry

)D

ry)

Slittin

g /

Slittin

g /

Ba

gg

ing

Ba

gg

ing

CP

P F

ilmM

eta

llize

r

Up to

9-c

olo

ur 2

-sid

ed p

rintin

gIn

-house c

apabilitie

sS

olv

ent-b

ase

d/fre

eC

apabilitie

s in

cl S

tandin

g P

ouch

To b

uild

hig

h b

arrie

rsP

olyp

rop

yle

ne s

ealin

g film

s

22

Daibochi ProductsDaibochi Products

Wide ra

nge of p

ack

aging so

lutio

ns fo

r vario

us p

roduct

functio

ns…

Consta

ntly

innovatin

g fo

r changing re

quire

ments

Film

Typ

eA

pp

lica

tion

s / U

se

Hig

h P

erm

ea

bility

Ba

rrier / P

erfo

rma

nc

eC

offe

e, N

uts

, Po

tato

Ch

ips

Co

st E

ffec

tive

Ba

rrier

Sn

acks, B

iscu

its, W

afe

r, Ch

oco

late

, C

ake

s

Daibochi ProductsDaibochi Products

Ca

ke

s

Ge

ne

ral P

ac

ka

gin

gO

ute

r Pa

ck, N

oo

dle

s, B

iscu

its, W

afe

rs

Sp

ec

ialty

Ap

plic

atio

nL

ab

ellin

g, Ic

e-c

rea

m, F

roze

n F

oo

d,

Ce

rea

l Pe

el S

ea

l, Se

aso

nin

g O

il, P

ow

de

r / Liq

uid

De

terg

en

t, S

ho

we

r Fo

am

, To

ba

cco

, Pe

t foo

d

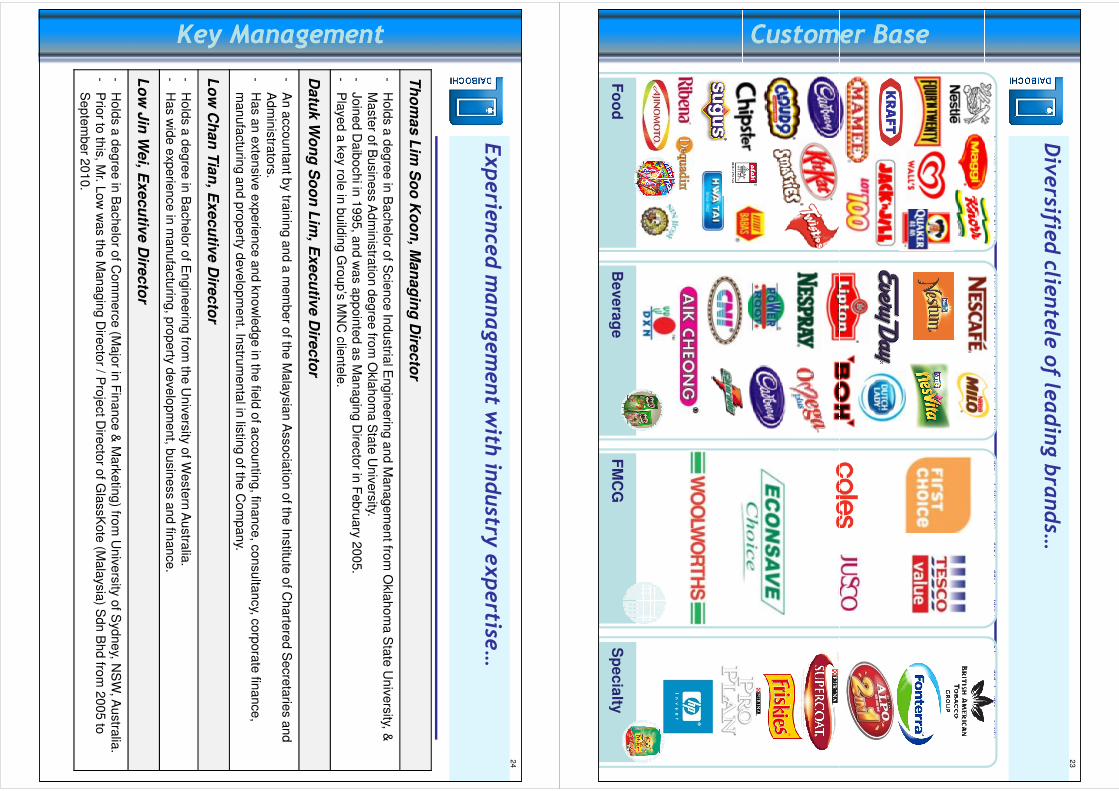

Customer BaseCustomer Base

Diversifie

d clie

ntele of le

ading bra

nds…

2

3

Fo

od

Be

ve

rag

eF

MC

GS

pe

cia

lty

Customer BaseCustomer Base

24

Key ManagementKey Management

Experie

nce

d m

anagement w

ith in

dustry

expertise

…

Th

om

as

Lim

So

o K

oo

n, M

an

ag

ing

Dire

cto

r

-H

old

s a

degre

e in

Bachelo

r of S

cie

nce In

dustria

l Engin

eerin

g a

nd M

anagem

ent fro

m O

kla

hom

a S

tate

Univ

ers

ity, &

Maste

r of B

usin

ess A

dm

inis

tratio

n d

egre

e fro

m O

kla

hom

a S

tate

Univ

ers

ity.

-Join

ed D

aib

ochi in

1995, a

nd w

as a

ppoin

ted a

s M

anagin

g D

irecto

r in F

ebru

ary

2005.

-P

layed a

key ro

le in

build

ing G

roup’s

MN

C c

liente

le.

Da

tuk

Wo

ng

So

on

Lim

, Ex

ec

utiv

e D

irec

tor

-A

n a

ccounta

nt b

y tra

inin

g a

nd a

mem

ber o

f the M

ala

ysia

n A

ssocia

tion o

f the In

stitu

te o

f Charte

red S

ecre

tarie

s a

nd

Key ManagementKey Management

-A

n a

ccounta

nt b

y tra

inin

g a

nd a

mem

ber o

f the M

ala

ysia

n A

ssocia

tion o

f the In

stitu

te o

f Charte

red S

ecre

tarie

s a

nd

Adm

inis

trato

rs.

-H

as a

n e

xte

nsiv

e e

xperie

nce a

nd k

now

ledge in

the fie

ld o

f accountin

g, fin

ance, c

onsulta

ncy, c

orp

ora

te fin

ance,

manufa

ctu

ring a

nd p

roperty

develo

pm

ent. In

stru

menta

l in lis

ting o

f the C

om

pany.

Lo

w C

ha

n T

ian

, Ex

ec

utiv

e D

irec

tor

-H

old

s a

degre

e in

Bachelo

r of E

ngin

eerin

g fro

m th

e U

niv

ers

ity o

f Weste

rn A

ustra

lia.

-H

as w

ide e

xperie

nce in

manufa

ctu

ring, p

roperty

develo

pm

ent, b

usin

ess a

nd fin

ance.

Lo

w J

in W

ei, E

xe

cu

tive

Dire

cto

r

-H

old

s a

degre

e in

Bachelo

r of C

om

merc

e (M

ajo

r in F

inance &

Mark

etin

g) fro

m U

niv

ers

ity o

f Sydney, N

SW

, Austra

lia.

-P

rior to

this

, Mr. L

ow

was th

e M

anagin

g D

irecto

r / Pro

ject D

irecto

r of G

lassK

ote

(Mala

ysia

) Sdn B

hd fro

m 2

005 to

Septe

mber 2

010.

25

Major ShareholdersMajor Shareholders

Gro

wing in

stitutio

nal fo

llowing… Free flo

at re

tained at >

50%

No. o

f shares (‘m

il)(31.12.2012)

Perce

ntage *

Low Chan Tian, E

D10.10

8.9%

Datuk Wong Soon Lim, E

D7.02

6.2%

Major ShareholdersMajor Shareholders

Lim Koy Peng

8.62

7.6%

* Exclu

din

g 4

16

,30

0 s

ha

res b

ou

gh

t ba

ck b

y th

e C

om

pa

ny a

nd

reta

ine

d a

s tre

asu

ry s

ha

res

••Flexible packagin

g market, w

orth

Flexible packagin

g market, w

orth

$58.3 bil in

2011, e

stimated to

$58.3 bil in

2011, e

stimated to

reach $71.3 bil in

2016

reach $71.3 bil in

2016*

»Favoured fo

r its versa

tility, c

omparativ

e

low cost a

nd potentia

l for in

novatio

n.

26

Industry InsightIndustry Insight

Gro

wth in

flexible pack

aging to

be le

d by th

e Asia

n re

gion…

Global co

nsumer fle

xible packa

ging

consumptio

n by re

gion, 2

011

(% sh

are by volume)

••Asia

: the large

st and faste

stAsia

: the large

st and faste

st--gro

wing fle

xible packagin

g market

growing fle

xible packagin

g market

»Represented 29.1% of g

lobal m

arket

volume

»Forecast C

AGR of 7

.9% fo

r 2011 to

2016;

becoming one of th

e fa

stest g

rowing

markets in

the re

gion; le

d by In

dia and

China in

line with

their d

eveloping

economies

Industry InsightIndustry Insight

*S

ou

rce

: “Th

e F

utu

re o

f Glo

ba

l Fle

xib

le P

acka

gin

g to

20

16

” by P

ira In

tern

atio

na

l