Embed Size (px)

Citation preview

Daibochi Plastic & Packaging

Industry Berhad

1Q16

Financial Results & Corporate Update

5 May 2016

IR Adviser

AQUILAS

1Q16 Operational Highlights

Growing export businesses…

Operations Highlights Financial Review Investment Merits Corporate Profile

3

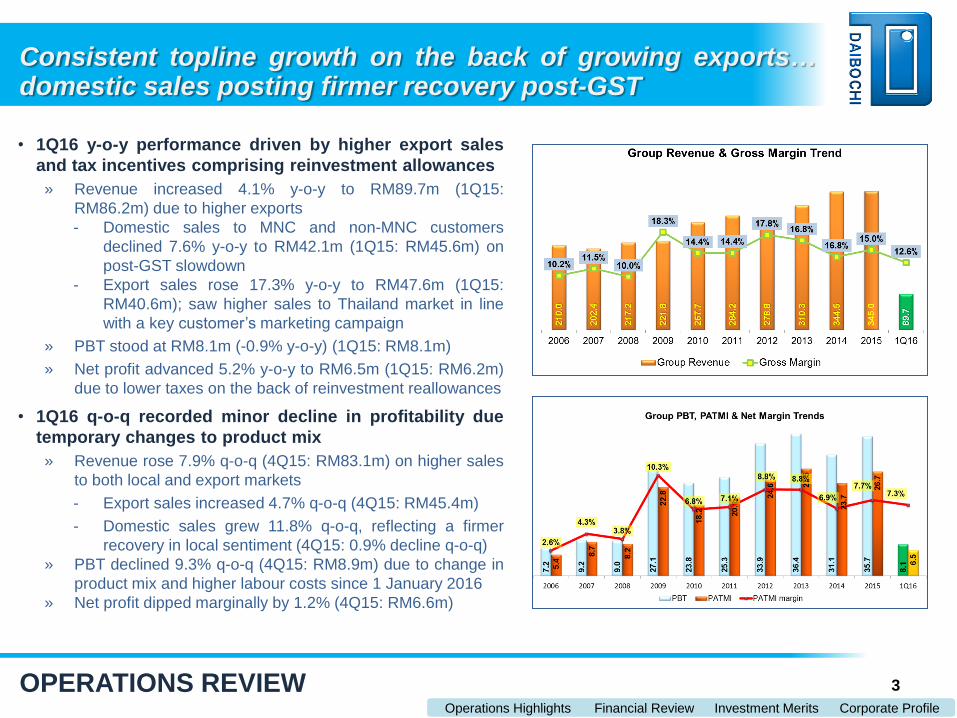

Consistent topline growth on the back of growing exports… domestic sales posting firmer recovery post-GST

OPERATIONS REVIEW

• 1Q16 y-o-y performance driven by higher export sales

and tax incentives comprising reinvestment allowances

» Revenue increased 4.1% y-o-y to RM89.7m (1Q15:

RM86.2m) due to higher exports

- Domestic sales to MNC and non-MNC customers

declined 7.6% y-o-y to RM42.1m (1Q15: RM45.6m) on

post-GST slowdown

- Export sales rose 17.3% y-o-y to RM47.6m (1Q15:

RM40.6m); saw higher sales to Thailand market in line

with a key customer’s marketing campaign

» PBT stood at RM8.1m (-0.9% y-o-y) (1Q15: RM8.1m)

» Net profit advanced 5.2% y-o-y to RM6.5m (1Q15: RM6.2m)

due to lower taxes on the back of reinvestment reallowances

• 1Q16 q-o-q recorded minor decline in profitability due

temporary changes to product mix

» Revenue rose 7.9% q-o-q (4Q15: RM83.1m) on higher sales

to both local and export markets

- Export sales increased 4.7% q-o-q (4Q15: RM45.4m)

- Domestic sales grew 11.8% q-o-q, reflecting a firmer

recovery in local sentiment (4Q15: 0.9% decline q-o-q)

» PBT declined 9.3% q-o-q (4Q15: RM8.9m) due to change in

product mix and higher labour costs since 1 January 2016

» Net profit dipped marginally by 1.2% (4Q15: RM6.6m)

Growth Strategies

Accelerating topline expansion …

Operations Highlights Financial Review Investment Merits Corporate Profile

5

Increasing export contracts from MNCs… also looking to enhance operational efficiency and workforce management

FY2016 OUTLOOK

• Commenced delivery of new contract to ANZ’s FMCG market in April 2016

» Supplying MNCs with new innovation of four-side-seal bags that improves production efficiency

• On track to commence new contract for ANZ’s F&B market in 3Q16

» To begin supply to an MNC for a new structure packaging that provides improved consumer experience

• Investing RM20m CAPEX in FY16 to expand production capacity

» RM13m for second expansion phase of Daibochi Plastic Plant 2 for machinery and other works

- To expand built-up area from existing 80,000 sq ft to approximately 140,000 sq ft

- New blown film machine expected to arrive in 3Q16, to improve operating efficiency

» RM7m for recurring CAPEX for Daibochi Plastic Plant 1

» To benefit from Special Reinvestment Allowance incentive applicable for investments from 2016 to 2018

• Cost and labour-related challenges to be mitigated through improved operational management

» Hike in foreign worker levy to RM1,850/worker (from RM1,250 previously) effective March 2016 to pose

estimated impact of RM150k/year

» Freeze in new foreign worker recruitment leading to uncertainties and lower morale among foreign workers may

lead to labour shortages in near term

» To focus on enhancing remuneration, talent retention, and motivation programmes to address labour

sustainability in the long run

» Set up working team in 3Q15 to enhance operational and production efficiency - targeting to achieve 10%

improvement in production speed and higher efficiency in wastage control

Operations Highlights Financial Review Investment Merits Corporate Profile

6

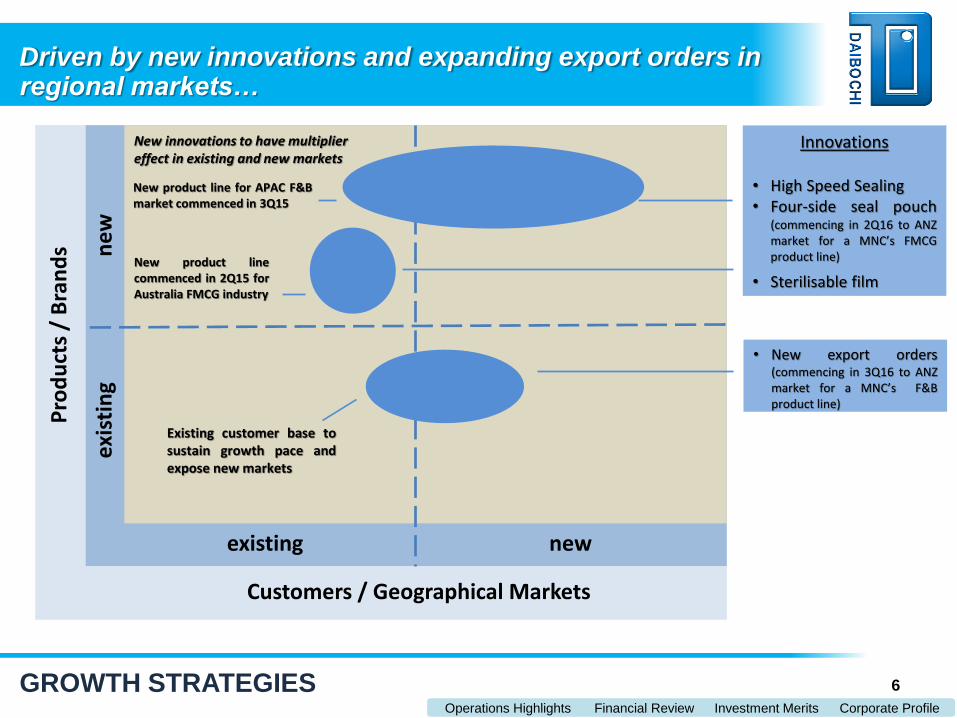

Driven by new innovations and expanding export orders in regional markets…

GROWTH STRATEGIES

exis

tin

g

Pro

du

cts

/ B

ran

ds n

ew

existing new

Customers / Geographical Markets

New product line for APAC F&B market commenced in 3Q15

Innovations

• High Speed Sealing • Four-side seal pouch

(commencing in 2Q16 to ANZ market for a MNC’s FMCG product line)

• Sterilisable film

New product line commenced in 2Q15 for Australia FMCG industry

Existing customer base to sustain growth pace and expose new markets

• New export orders (commencing in 3Q16 to ANZ market for a MNC’s F&B product line)

New innovations to have multiplier effect in existing and new markets

1Q16 Financial Review

Improving financial performance…

Operations Highlights Financial Review Investment Merits Corporate Profile

8

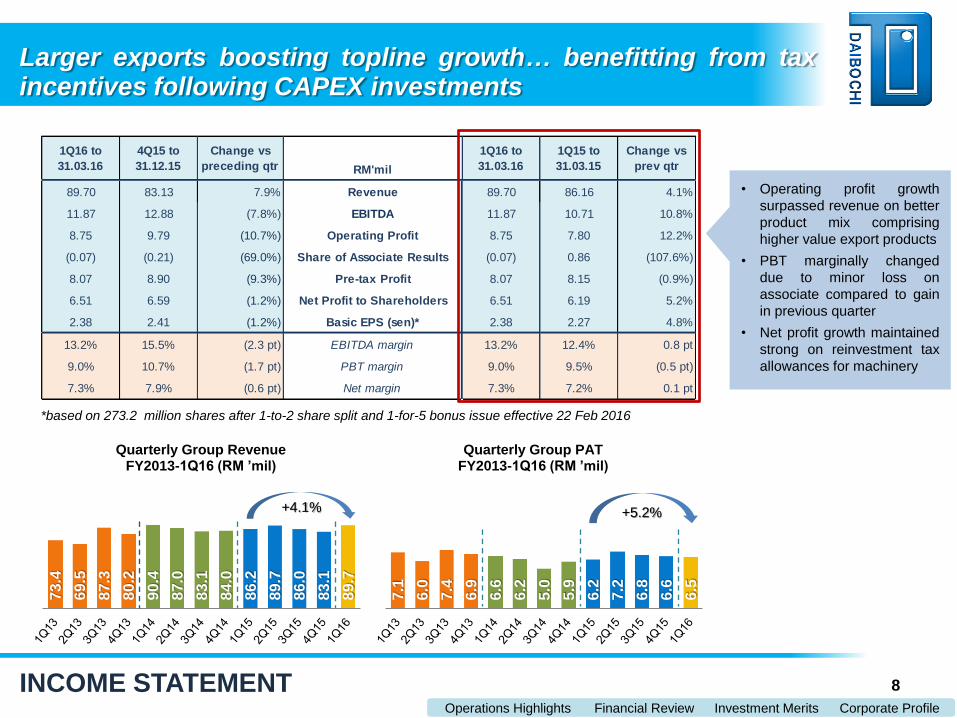

Larger exports boosting topline growth… benefitting from tax incentives following CAPEX investments

INCOME STATEMENT

1Q16 to

31.03.16

4Q15 to

31.12.15

Change vs

preceding qtr RM'mil

1Q16 to

31.03.16

1Q15 to

31.03.15

Change vs

prev qtr

89.70 83.13 7.9% Revenue 89.70 86.16 4.1%

11.87 12.88 (7.8%) EBITDA 11.87 10.71 10.8%

8.75 9.79 (10.7%) Operating Profit 8.75 7.80 12.2%

(0.07) (0.21) (69.0%) Share of Associate Results (0.07) 0.86 (107.6%)

8.07 8.90 (9.3%) Pre-tax Profit 8.07 8.15 (0.9%)

6.51 6.59 (1.2%) Net Profit to Shareholders 6.51 6.19 5.2%

2.38 2.41 (1.2%) Basic EPS (sen)* 2.38 2.27 4.8%

13.2% 15.5% (2.3 pt) EBITDA margin 13.2% 12.4% 0.8 pt

9.0% 10.7% (1.7 pt) PBT margin 9.0% 9.5% (0.5 pt)

7.3% 7.9% (0.6 pt) Net margin 7.3% 7.2% 0.1 pt

73.4

69.5

87.3

80.2

90.4

87.0

83.1

84.0

86.2

89.7

86.0

83.1

89.7

Quarterly Group Revenue FY2013-1Q16 (RM ’mil)

7.1

6.0

7.4

6.9

6.6

6.2

5.0

5.9

6.2

7.2

6.8

6.6

6.5

Quarterly Group PAT FY2013-1Q16 (RM ’mil)

+4.1% +5.2%

• Operating profit growth

surpassed revenue on better

product mix comprising

higher value export products

• PBT marginally changed

due to minor loss on

associate compared to gain

in previous quarter

• Net profit growth maintained

strong on reinvestment tax

allowances for machinery

*based on 273.2 million shares after 1-to-2 share split and 1-for-5 bonus issue effective 22 Feb 2016

Operations Highlights Financial Review Investment Merits Corporate Profile

9

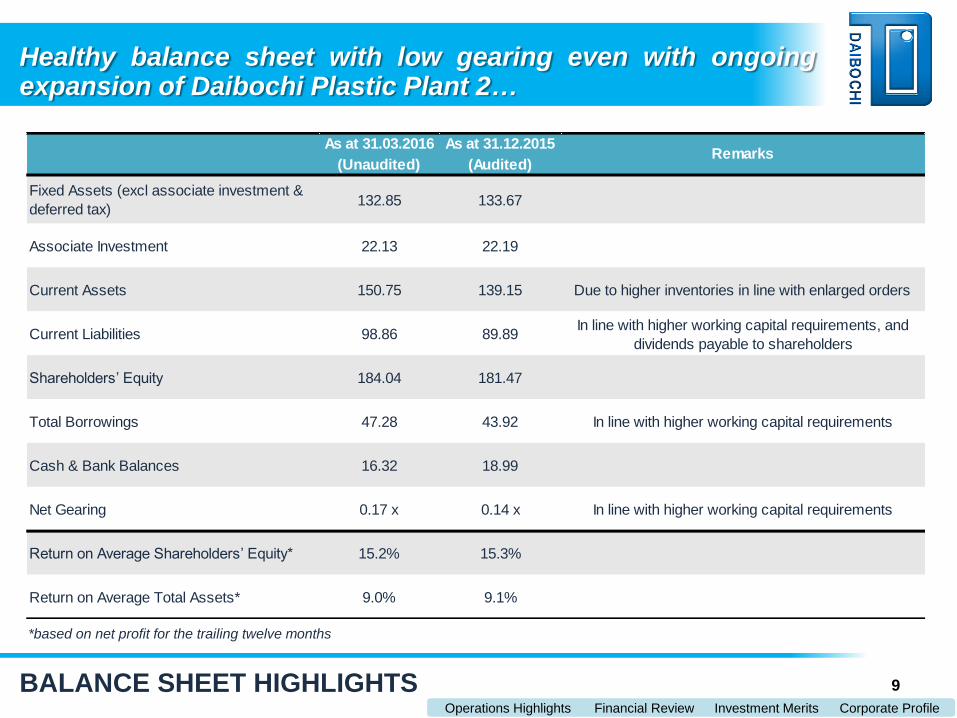

Healthy balance sheet with low gearing even with ongoing expansion of Daibochi Plastic Plant 2…

BALANCE SHEET HIGHLIGHTS

As at 31.03.2016 As at 31.12.2015

(Unaudited) (Audited)

Fixed Assets (excl associate investment &

deferred tax)132.85 133.67

Associate Investment 22.13 22.19

Current Assets 150.75 139.15 Due to higher inventories in line with enlarged orders

Current Liabilities 98.86 89.89In line with higher working capital requirements, and

dividends payable to shareholders

Shareholders’ Equity 184.04 181.47

Total Borrowings 47.28 43.92 In line with higher working capital requirements

Cash & Bank Balances 16.32 18.99

Net Gearing 0.17 x 0.14 x In line with higher working capital requirements

Return on Average Shareholders’ Equity* 15.2% 15.3%

Return on Average Total Assets* 9.0% 9.1%

Remarks

*based on net profit for the trailing twelve months

Operations Highlights Financial Review Investment Merits Corporate Profile

10

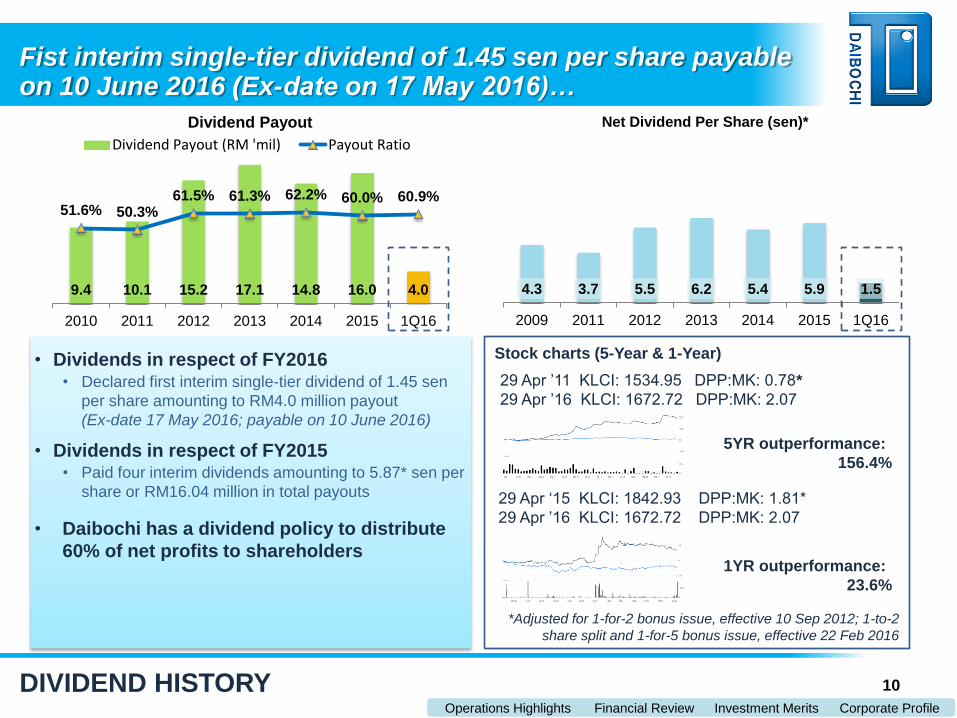

Fist interim single-tier dividend of 1.45 sen per share payable on 10 June 2016 (Ex-date on 17 May 2016)…

DIVIDEND HISTORY

9.4 10.1 15.2 17.1 14.8 16.0 4.0

51.6% 50.3% 61.5% 61.3% 62.2% 60.0% 60.9%

0.0 %

25. 0%

50. 0%

75. 0%

100 .0%

0.0 00

6.0 00

12. 000

18. 000

2010 2011 2012 2013 2014 2015 1Q16

Dividend Payout

Dividend Payout (RM 'mil) Payout Ratio

4.3 3.7 5.5 6.2 5.4 5.9 1.5

2009 2011 2012 2013 2014 2015 1Q16

Net Dividend Per Share (sen)*

• Dividends in respect of FY2016 • Declared first interim single-tier dividend of 1.45 sen

per share amounting to RM4.0 million payout

(Ex-date 17 May 2016; payable on 10 June 2016)

• Dividends in respect of FY2015 • Paid four interim dividends amounting to 5.87* sen per

share or RM16.04 million in total payouts

• Daibochi has a dividend policy to distribute

60% of net profits to shareholders

*Adjusted for 1-for-2 bonus issue, effective 10 Sep 2012; 1-to-2

share split and 1-for-5 bonus issue, effective 22 Feb 2016

Stock charts (5-Year & 1-Year)

5YR outperformance:

156.4%

1YR outperformance:

23.6%

29 Apr ‘15 KLCI: 1842.93 DPP:MK: 1.81*

29 Apr ’16 KLCI: 1672.72 DPP:MK: 2.07

29 Apr ’11 KLCI: 1534.95 DPP:MK: 0.78*

29 Apr ’16 KLCI: 1672.72 DPP:MK: 2.07

Investment Merits

Proxy to region’s growing appetite…

Operations Highlights Financial Review Investment Merits Corporate Profile

12

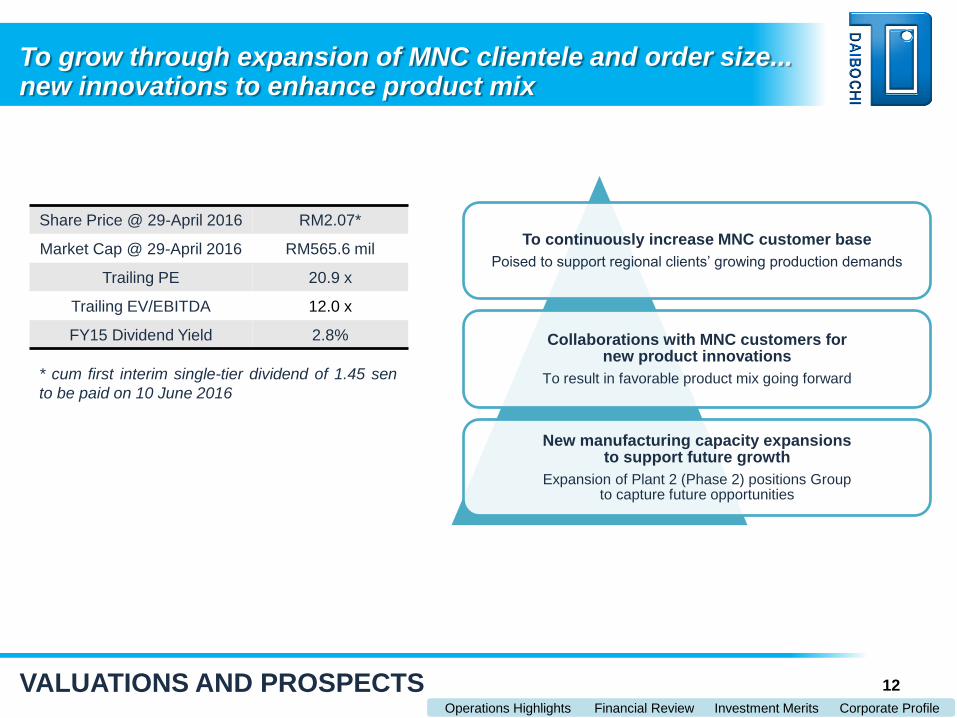

To grow through expansion of MNC clientele and order size... new innovations to enhance product mix

VALUATIONS AND PROSPECTS

To continuously increase MNC customer base

Poised to support regional clients’ growing production demands

Collaborations with MNC customers for new product innovations

To result in favorable product mix going forward

New manufacturing capacity expansions to support future growth

Expansion of Plant 2 (Phase 2) positions Group to capture future opportunities

Share Price @ 29-April 2016 RM2.07*

Market Cap @ 29-April 2016 RM565.6 mil

Trailing PE 20.9 x

Trailing EV/EBITDA 12.0 x

FY15 Dividend Yield 2.8%

* cum first interim single-tier dividend of 1.45 sen

to be paid on 10 June 2016

IR Contacts

Mr. Low Jin Wei

T: 06-231 9779

Ms. Julia Pong

T: 012-390 9258

THANK YOU

Bursa: DAIBOCI/8125 Bloomberg: DPP:MK Reuters: DPPM.KL

Corporate Profile

Operations Highlights Financial Review Investment Merits Corporate Profile

15

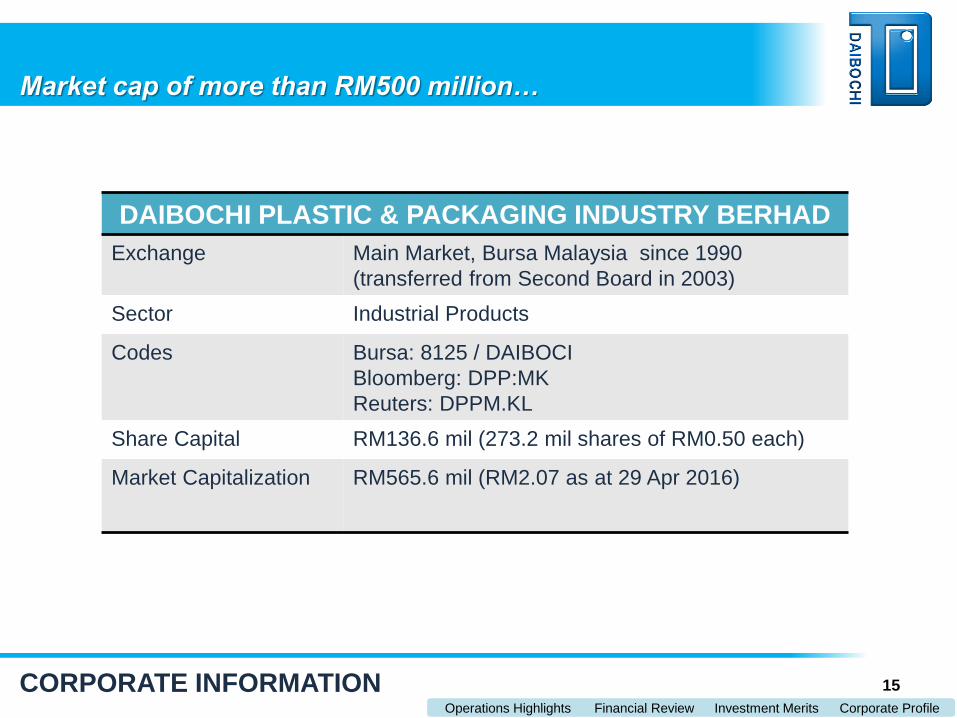

Market cap of more than RM500 million…

CORPORATE INFORMATION

DAIBOCHI PLASTIC & PACKAGING INDUSTRY BERHAD

Exchange Main Market, Bursa Malaysia since 1990

(transferred from Second Board in 2003)

Sector Industrial Products

Codes Bursa: 8125 / DAIBOCI

Bloomberg: DPP:MK

Reuters: DPPM.KL

Share Capital RM136.6 mil (273.2 mil shares of RM0.50 each)

Market Capitalization RM565.6 mil (RM2.07 as at 29 Apr 2016)

Operations Highlights Financial Review Investment Merits Corporate Profile

16

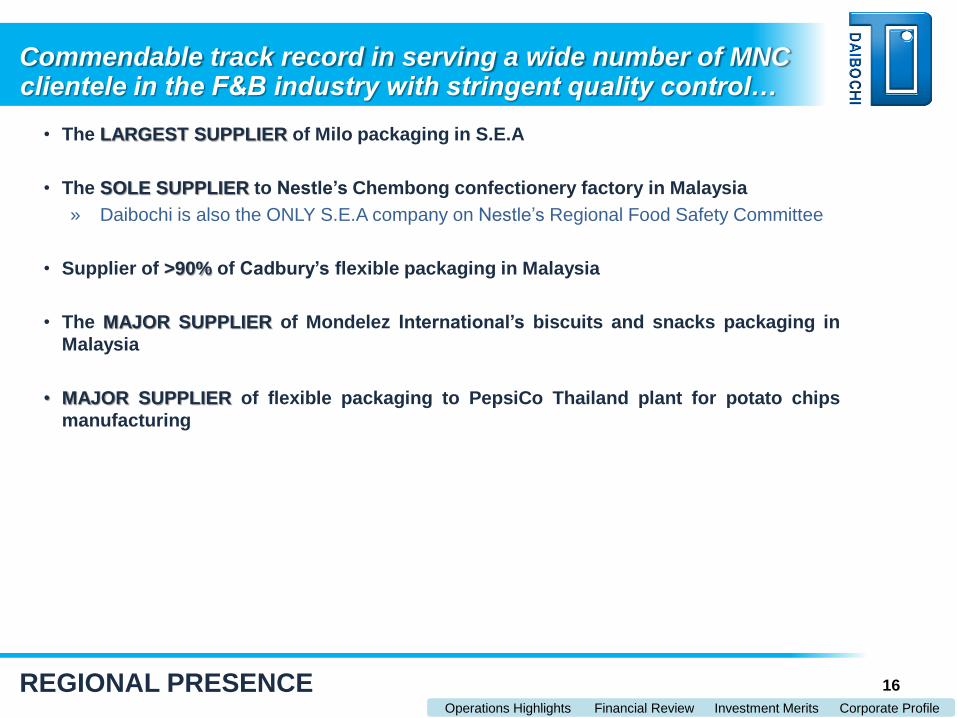

Commendable track record in serving a wide number of MNC clientele in the F&B industry with stringent quality control…

REGIONAL PRESENCE

• The LARGEST SUPPLIER of Milo packaging in S.E.A

• The SOLE SUPPLIER to Nestle’s Chembong confectionery factory in Malaysia

» Daibochi is also the ONLY S.E.A company on Nestle’s Regional Food Safety Committee

• Supplier of >90% of Cadbury’s flexible packaging in Malaysia

• The MAJOR SUPPLIER of Mondelez International’s biscuits and snacks packaging in

Malaysia

• MAJOR SUPPLIER of flexible packaging to PepsiCo Thailand plant for potato chips

manufacturing

Operations Highlights Financial Review Investment Merits Corporate Profile

17

Internationally-certified production facilities that comply with all factory audits by MNC clientele…strength in innovation

PRODUCTION FACILITIES

• Accredited and world-class production facilities

» Attained ISO:9001 and ISO:14001 certifications

» Obtained Food Safety System Certification (FSSC:22000)

in May 2014

• Well-equipped laboratory testing facilities

» To ensure our products consistently exceed customers’

packaging barrier, retention and migration requirements

» Recent breakthrough in producing 2-layer film to

potentially replace conventional 4-layer film

Operations Highlights Financial Review Investment Merits Corporate Profile

18

Integrated end-to-end packaging process… equipped with specialized in-house capabilities

PRODUCTION FACILITIES (CONT’D)

Prepress Cylinder Making

Gravure Printing

Lamination (Extrusion /

Dry)

Slitting / Bagging

CPP Film Metallizer

Up to 9-colour 2-sided printing In-house capabilities Solvent-based/free Capabilities incl Standing Pouch

The only player with in-house cylinder-making, and one of the few with metallizing and

sealing films capabilities for quality assurance and constant improvement at key stages

To build high barriers Polypropylene sealing films

Operations Highlights Financial Review Investment Merits Corporate Profile

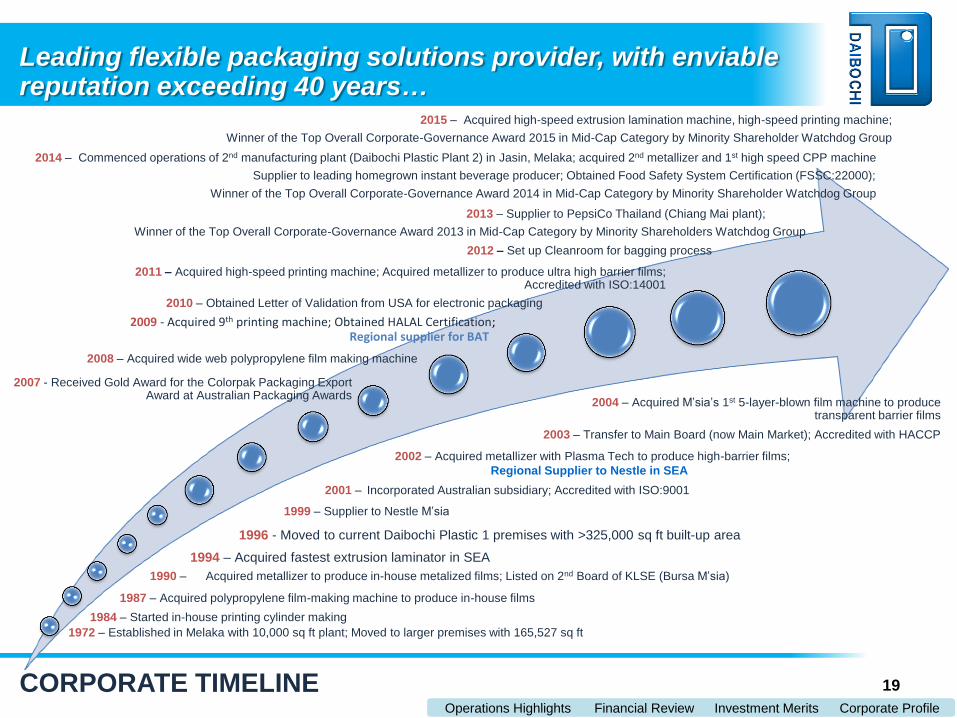

1994 – Acquired fastest extrusion laminator in SEA

1996 - Moved to current Daibochi Plastic 1 premises with >325,000 sq ft built-up area

2001 – Incorporated Australian subsidiary; Accredited with ISO:9001

2009 - Acquired 9th printing machine; Obtained HALAL Certification; Regional supplier for BAT

2010 – Obtained Letter of Validation from USA for electronic packaging

2011 – Acquired high-speed printing machine; Acquired metallizer to produce ultra high barrier films; Accredited with ISO:14001

2012 – Set up Cleanroom for bagging process

2013 – Supplier to PepsiCo Thailand (Chiang Mai plant);

Winner of the Top Overall Corporate-Governance Award 2013 in Mid-Cap Category by Minority Shareholders Watchdog Group

2014 – Commenced operations of 2nd manufacturing plant (Daibochi Plastic Plant 2) in Jasin, Melaka; acquired 2nd metallizer and 1st high speed CPP machine

Supplier to leading homegrown instant beverage producer; Obtained Food Safety System Certification (FSSC:22000);

Winner of the Top Overall Corporate-Governance Award 2014 in Mid-Cap Category by Minority Shareholder Watchdog Group

19

Leading flexible packaging solutions provider, with enviable reputation exceeding 40 years…

CORPORATE TIMELINE

1999 – Supplier to Nestle M’sia

2002 – Acquired metallizer with Plasma Tech to produce high-barrier films;

Regional Supplier to Nestle in SEA

2008 – Acquired wide web polypropylene film making machine

2007 - Received Gold Award for the Colorpak Packaging Export Award at Australian Packaging Awards

2004 – Acquired M’sia’s 1st 5-layer-blown film machine to produce transparent barrier films

2003 – Transfer to Main Board (now Main Market); Accredited with HACCP

1990 – Acquired metallizer to produce in-house metalized films; Listed on 2nd Board of KLSE (Bursa M’sia)

1987 – Acquired polypropylene film-making machine to produce in-house films

1984 – Started in-house printing cylinder making

1972 – Established in Melaka with 10,000 sq ft plant; Moved to larger premises with 165,527 sq ft

2015 – Acquired high-speed extrusion lamination machine, high-speed printing machine;

Winner of the Top Overall Corporate-Governance Award 2015 in Mid-Cap Category by Minority Shareholder Watchdog Group

Operations Highlights Financial Review Investment Merits Corporate Profile

20

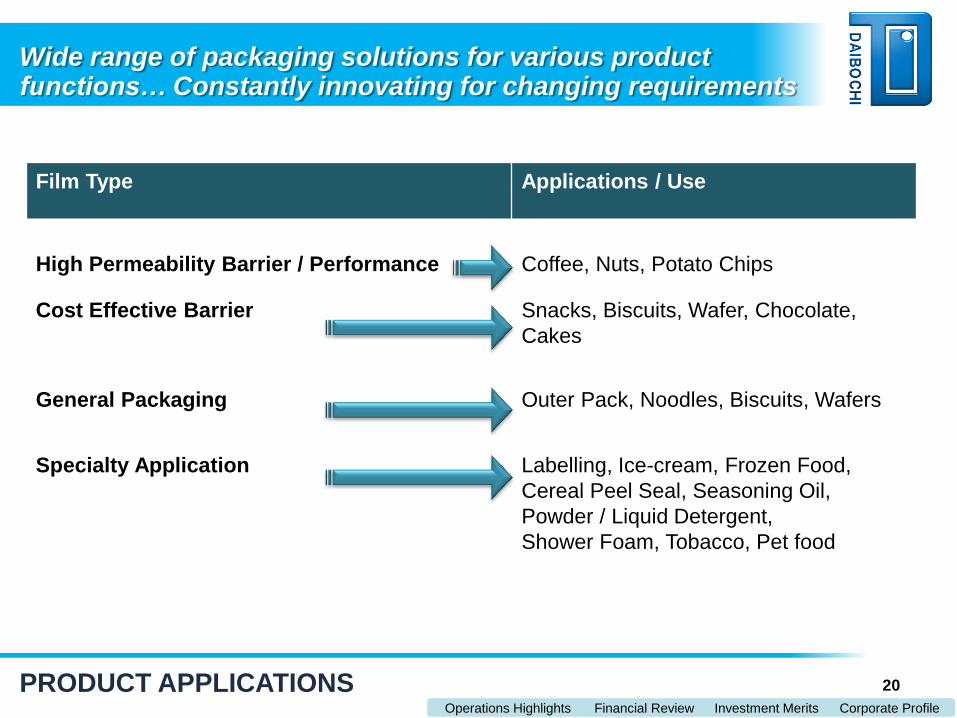

Wide range of packaging solutions for various product functions… Constantly innovating for changing requirements

PRODUCT APPLICATIONS

Film Type Applications / Use

High Permeability Barrier / Performance

Coffee, Nuts, Potato Chips

Cost Effective Barrier Snacks, Biscuits, Wafer, Chocolate,

Cakes

General Packaging Outer Pack, Noodles, Biscuits, Wafers

Specialty Application Labelling, Ice-cream, Frozen Food,

Cereal Peel Seal, Seasoning Oil,

Powder / Liquid Detergent,

Shower Foam, Tobacco, Pet food

Operations Highlights Financial Review Investment Merits Corporate Profile

21

Experienced management with industry expertise…

KEY MANAGEMENT

Thomas Lim Soo Koon, Managing Director

- Holds a degree in Bachelor of Science Industrial Engineering and Management from Oklahoma State University, &

Master of Business Administration degree from Oklahoma State University.

- Joined Daibochi in 1995, and was appointed as Managing Director in February 2005.

- Played a key role in building Group’s MNC clientele.

Datuk Wira Wong Soon Lim, Executive Director

- An accountant by training and a member of the Malaysian Association of the Institute of Chartered Secretaries and

Administrators.

- Has an extensive experience and knowledge in the field of accounting, finance, consultancy, corporate finance,

manufacturing and property development. Instrumental in listing of the Company.

Low Chan Tian, Executive Director

- Holds a degree in Bachelor of Engineering from the University of Western Australia.

- Has wide experience in manufacturing, property development, business and finance.

Low Jin Wei, Executive Director

- Holds a degree in Bachelor of Commerce (Major in Finance & Marketing) from University of Sydney, NSW, Australia.

- Prior to this, Mr. Low was the Managing Director / Project Director of GlassKote (Malaysia) Sdn Bhd from 2005 to

September 2010.

Operations Highlights Financial Review Investment Merits Corporate Profile

22

Institutional investors holding approximately 30%...

MAJOR SHAREHOLDERS

No. of shares (‘mil) (31.03.2016)

Percentage *

Low Chan Tian, ED 28.2 10.3%

Apollo Asia Fund Ltd 25.6 9.4%

Lim Koy Peng 23.1 8.5%

Datuk Wira Wong Soon Lim, ED 15.9 5.8%

Halley Sicav – Halley Asian Prosperity 15.1 5.5%

Operations Highlights Financial Review Investment Merits Corporate Profile

23

Growth in flexible packaging to be led by the Asian region… penetration into new product categories to bring next wave

INDUSTRY INSIGHT

• Worldwide consumer flexible packaging market worth $92 bil in 2015 – Estimated to grow 4% p.a. to reach $114 bil in 2020

– Growth to be led by Asia Pacific & other emerging regions (e.g. South & Central America)

Source: Smithers’ Pira – The Global Flexible Packaging Market – Trends and Forecasts

• Growth catalysts for Asia’s flexible packaging market: – Higher demand for cheaper and smaller pack sizes in line with affordability of general

population (especially post economic slowdown)

– Increase in working mothers / dual-income households leading to preference for convenience

packaging

– Development of multinational food retailers and manufacturers in the region; indicating the

long-term growth potential in Asia

Source: The Asia Pacific Flexible Packaging Market to 2016 by PCI Consulting Films Ltd

![[i] · Nestle (Malaysia) Berhad 0.10 0.21 PPB Group Berhad 0.68 0.79 QL Resources Berhad -* -* UMW Holdings Berhad 1.77 1.29 * Peratusan kurang daripada 0.01% Kewangan AmBank Berhad](https://img.pdfslide.net/doc/110x75/5b4c331c7f8b9a9a408b8254/i-nestle-malaysia-berhad-010-021-ppb-group-berhad-068-079-ql-resources.jpg)