Embed Size (px)

Citation preview

1

Corporate Purpose and Firm Ownership

Claudine Gartenberg1 University of Pennsylvania

George Serafeim Harvard Business School

June 1, 2019

Analyzing data from approximately 1.5 million employees across 1,100 established public and private US companies, we find that the strength of employee beliefs about their firm’s purpose is lower in public companies. This difference is most pronounced within the salaried middle and hourly ranks, rather than senior executives. Among public companies, purpose becomes progressively lower with more concentrated shareholders, especially among firms with high hedge fund ownership. These patterns can be partly explained by differences in CEO backgrounds and compensation: public firms, particularly those with strong shareholders, choose outsider CEOs at higher rates and pay them more relative to their employees. Our analyses suggest that these results are not driven solely by sorting effects, but appear attributable in part to the impact that firm owners have on their employees. In summary, shareholders appear to influence the strength of corporate purpose deep within organizations via the leadership and corporate practices they enable at the top.

Keywords: Corporate Purpose, Ownership, Leadership, Executive Compensation

1 Corresponding author: Claudine Gartenberg is an Assistant Professor of Management at the Wharton School, University of Pennsylvania, 3620 Locust Walk, SHDH 2035, Wharton School, Philadelphia PA 19104; email: [email protected]. George Serafeim is a Professor of Business Administration at Harvard Business School; 381 Morgan Hall, Harvard Business School, Boston, MA 02163; email: [email protected]. We would like to thank David Frieberg for excellent research assistance, and the Great Place to Work Institute, and particularly Amy Lyman, Ed Frauenheim and Marcus Erb for their support. This paper has benefitted from comments by participants at the Wharton Org Theory workshop, Strategy Research Forum, Strategy Science Conference, Academy of Management Strategy Division Executive Committee annual meeting, Oxford University, University of Rome, and Harvard Business School. We are solely responsible for any errors.

2

Introduction What drives differences in corporate purpose across firms? Purpose has drawn increasing attention

from policy makers, practitioners, and academics as an important foundation for strategy,

employee motivator, and means to articulate an organization’s broader social role (Chapman,

Edmans, Gosling, Hutton, and Mayer, 2017; Hollensbe et al. 2014; Oxford University and Ernst

and Young 2016; Bartlett and Ghoshal, 1994). Despite this growing attention, measurement

challenges have constrained empirical research, and it is only recently that the data to implement

large sample studies on purpose has become available. One recent study by Gartenberg, Prat and

Serafeim (2019) finds that firms with a strong sense of purpose – particularly among their middle-

ranked employees – experience better performance. Yet we know little about why certain firms

might be more or less effective in establishing a credible sense of purpose.2

To this end, we explore the link between corporate purpose and firm ownership. A firm’s

owners are the ultimate arbiters of the organization. Owners influence who is placed in

management positions and where they focus their attention. Owners affect a firm’s investment,

financing and governance choices (Trostel and Nichols 1982; Capron and Shen 2007; Asker,

Farre-Mensa and Ljungqvist 2014; Gilje and Taillard 2016), as well as its innovative direction

(Feldman, Kawano, Patel, Rao, Stevens and Edgerton, 2018; Bernstein 2015). As such, owners

have broad power to affect core aspects of the organization.

Moreover, the role of owners has important contemporary relevance. In recent years, much

attention has been placed on the ‘eclipse’ of the public corporation, as the number of public

companies has declined, and companies remain private for longer (Kahle and Stulz 2017; Doidge

2 We use the term “purpose” throughout this study. “Purpose” generally refers to the content of beliefs. In this study, however, we are interested in the strength of the beliefs, or “purposefulness,” and not the actual beliefs themselves. Similarly, when we refer to “meaning” within the workplace, we generally are interested in “meaningfulness,” or the strength, rather than the content, of meaning. For readability, we shorten “purposefulness” and “meaningfulness” to “purpose” and “meaning”, respectively.

3

et al. 2018). While much discussion has focused on the drivers of this decline, little attention has

been paid to what this phenomenon might mean for how these companies are managed. With this

paper, we seek to provide evidence on the management implications of this important recent

development.

Corporate purpose is an intrinsically imprecise concept that poses a challenge both to

define and measure. We define corporate purpose broadly as “a concrete goal or objective for the

firm that reaches beyond profit maximization,” the definition of purpose proposed by Henderson

and Van den Steen (2015). This definition is not explicitly pro-social, although corporate purpose

often is. Instead, it focusses on the broader contribution of the organization’s work beyond what

is captured in profit measures alone and is consistent with other common definitions of purpose

(e.g., Chapman et al., 2017).

We measure corporate purpose using the approach established by Gartenberg, Prat and

Serafeim (2019), by aggregating actual employee beliefs in the meaning and impact of their work,

rather than via announced corporate purpose statements that have been shown to be

inconsequential “cheap talk” (Guiso, Sapienza, and Zingales, 2015). The reasoning behind this

approach is as follows: as corporate purpose is implemented effectively, then the employees of the

organization should, collectively, believe that their work has greater meaning and impact. As such,

we infer the effectiveness corporate purpose of the entity via the strength of measured employee

beliefs.

Our evidence comes from a proprietary survey from the Great Place To Work Institute

(GPTW). This survey, to our knowledge, represents one of the largest data sources on the topic

available to researchers. This survey includes employees within more than a thousand

organizations between 2006 and 2016. These employees span the organizational hierarchy from

4

hourly workers up to executives. Respondents evaluate their workplaces along a series of

organizational dimensions, including workplace collegiality, management, and the nature of the

job itself. Critically, these responses allow us to circumvent corporate cheap talk and measure

actual employee beliefs. It also allows us to separate beliefs in purpose from general job

satisfaction.

Following Gartenberg, Prat and Serafeim (2019), we combine beliefs about the meaning

of work (“My work has special meaning: this is not just a job”; “I feel good about the ways we

contribute to the community”; “When I look at what we accomplish, I feel a sense of pride”; and

“I'm proud to tell others I work here.”) and clarity from management (e.g., “Management makes

its expectations clear”; “Management has a clear view of where the organization is going and

how to get there”) in our measure of corporate purpose. They find that these beliefs tend to co-

move among employees, and only together predict greater company performance. In supplemental

analyses, we corroborate our results using alternative measures of purpose. We obtain measures

of purpose for 1,509,797 employees across 1,108 firms. We aggregate this measure up to the firm-

year level to obtain corporate purpose.

We begin by reporting how corporate purpose differs across four types of firm owners:

public, and three types of private firms: private-equity owned, private subsidiaries of public firms,

and private (non-private equity). This first analysis yields four notable patterns. First, employees

of public firms have a lower sense of purpose than those of private firms. This difference is

significant, translating to more than a quarter standard deviation difference in purpose within the

sample as a whole. Second, the difference in purpose is driven by employees below the top of the

organization—the middle ranked salaried and hourly workers—rather than those at the senior

manager and executive ranks. This difference permits an interpretation of our results as “purpose

5

inequality”, the gap in purpose help by the top ranks and their subordinates. Third, the difference

in purpose (and purpose inequality) is more pronounced for public firms with large, concentrated

blocks of shareholders. In other words, firms with greater shareholder power have employees with

weaker purpose.

We then explore factors that can account for these patterns among public and private firms.

These factors include the background and compensation of the CEO and strategic actions taken by

management that differ across types. Among public firms, those with strong shareholder power

choose more outsider CEOs and pay them more relative to employees. We find that these factors

account for 30% of the difference in corporate purpose between public and private firms. Public

firms also differ in their strategic choices (e.g., mergers, layoffs, and divestitures), as well as

incentives and benefits, which we find collectively to explain an additional 10% of the difference

relative to private firms.

Given we lack a natural experiment, we are cautious about making causal claims regarding

the effect of ownership on corporate purpose. Specifically, we cannot definitively separate the

interpretation that weaker purpose reflects the match between owners and firms from the

interpretation that owners influence the levels of corporate purpose directly. However, we perform

lead-lag analyses and inverse probability weighting matching to test these alternative

interpretations. While we believe both these alternatives are at play in this setting, our results are

aligned more with an interpretation that owners influence the levels of corporate purpose through

their choices.

This study makes several contributions. First, we add to a growing stream of work on the

role of corporate purpose within firms (Chapman et al., 2017; Thakor and Quinn, 2013, Henderson

and Van den Steen, 2015). In doing so, we respond to a call from Hollensbee et al., (2014) for

6

empirical work on the topic. We also contribute to a recent resurgence of interest in the role of

firms in society (Hart and Zingales, 2017). This study is also part of a larger push within corporate

strategy to explore additional complex effects of firm boundaries (Ahuja and Novelli, 2017). Some

emphasize that boundaries have social effects as influencing social comparison groups (Nickerson

and Zenger, 2008) or as carriers of identity (Santos and Eisenhardt, 2005). Our study supports the

idea that firms are also carriers of purpose, and that that this purpose can be predicted, in part, by

ownership structure. This study also fits into work on corporate ownership that shows differences

between public and private firms (Capron and Shen 2007; Asker, Farre-Mensa and Ljungqvist

2014; Gilje and Taillard 2016; Bernstein 2015). Interestingly much of the research in this last area

has occurred outside management. Our work suggests that ownership drives more than financial

decisions and calls for further research focused on the implications of ownership for management.

Corporate Purpose

What Is Corporate Purpose?

Corporate purpose is an often-referenced idea within the business community, with public

discourse increasing five-fold between 1994 and 2016 (Oxford University and Ernst and Young

2016). Satya Nadella, Microsoft CEO who returned the company to its position as the world’s

most valuable technology company, attributed the turnaround to a renewed focus on purpose:

“I wanted to go back to the very genesis of this company: what is that sense of purpose

and drive that made us successful?... In ’92, we used to talk even about our mission

– for example as having a PC in every home and desk. Except by the end of the decade

itself, we had more or less achieved it. Then what? What’s next. And that’s when I

7

felt like we may have confused marketing slogans for our mission. So that’s why I

wanted to get back to that sense of purpose.”

Nadella characterize the importance of purpose as follows:

“The sense of purpose in mission and culture to me are the two pillars…for any

institution…So when we talk about our mission of empowering every person and

every organization on the planet to achieve more, [it] can't be just a set of words. It

has to in some sense capture the very essence of who we are in all of the decisions

we make, in the products we create and how we show up with our customers.”3

These statements reveal that purpose is a meaning-rich articulation of the role of the firm,

an articulation that must be believed and followed throughout the organization, rather than merely

exist within the top ranks of an organization. Given its inherent intangibility, purpose eludes a

settled definition for academic purposes. Purpose has often been defined with a social orientation.

Bartlett and Ghoshal (1994) define purpose as “the statement of a company’s moral response to its

broadly defined responsibilities, not an amoral plan for exploiting commercial opportunity.”

Thakor and Quinn (2013) similarly define it as “something that is perceived as producing a social

benefit over and above the tangible pecuniary payoff that is shared by the principal and the agent.”

The definition of purpose, however, need not include an explicit social orientation. Oxford

Dictionaries define purpose as “the reason for which something is done or created or for which

something exists.”4 We use the definition of Gartenberg, Prat and Serafeim (2019) that corporate

purpose is “a set of beliefs about the meaning of a firm’s work beyond quantitative measures of

financial performance.” This definition is similar to the one used in the Purposeful Company

3 https://www.cnet.com/news/microsofts-ceo-on-helping-a-faded-legend-find-a-sense-of-purpose/ https://www.inc.com/justin-bariso/in-1-short-sentence-satya-nadella-summed-up-what-makes-microsoft-different-from-apple-amazon.html 4 http://www.oxforddictionaries.com/us/definition/american_english/purpose, accessed 3/15/16.

8

Report—written by a consortium of academics studying purpose in businesses—as a company’s

“reason for being,”5 as well as Henderson and Van den Steen (2015)’s definition of “a concrete

goal or objective for the firm that reaches beyond profit maximization.”

How Might Purpose be Related to Firm Ownership?

Motivation

The structure of corporate ownership has been a topic of inquiry for decades. Starting with Berle

and Means (1932), literature asked the question what the separation of ownership and control, as

a result of the rise of the public corporation, might mean for the future of the corporation. More

recently, many business leaders argue that corporate ownership has important implications for how

they run their business and some express strong preferences for specific structures. For example,

Jack Ma, founder of Alibaba, famously said that “If I had another life, I would keep my company

private.”

Many CEOs of public companies suggest that their job becomes very different after going

public. For example, the CEO of Zulily, said that "I don't know that I had a full appreciation for

how much time I would spend on external communication. That requires a lot of discipline and

patience, when many founders would rather be focused on growing the business.” Michael Dell,

who took his namesake company private after 25 years on the public markets, says dealing with

investor relations took up 20 percent of his time as well.

Of course, not all private owners are the same. Some CEOs argue that private equity owners

can be even more complicated to manage than public investors. Jon Oringer, who founded photo

5 The Purposeful Company Interim Report, May 2016. http://www.biginnovationcentre.com/media/uploads/pdf/The%20Purposeful%20Company%20Interim%20Report.pdf, accessed 6/26/16.

9

database Shutterstock in 2003 and took it public nearly a decade later, argues that "If you are a

private company, especially if you have done multiple funding rounds, you have investors who

have been in your business different amounts of time and have different rights." That can get

complicated quickly, he says, whereas "being public, anyone can get in and out of the stock at any

time. That lets us focus on where we think the business should go."

Anecdotal evidence suggests that in public companies stock price fluctuations affect not

only investors but also employees. Market fluctuations could affect their perceptions of both own

net worth and how they are doing at work. On the day of Zulily's IPO, CEO Cavens sent a note to

his staff warning them not to let the stock price drive their emotional engagement. "When the stock

price goes up any given day, we are just not that much smarter," he wrote. "And similarly, when

it goes down any given day, we are not that much dumber." The message, which Cavens reiterated

every quarter, worked at first, but in months, when the stock sharply declined, the company

struggled with internal employee reassurance and external recruiting.

Some business leaders argue that the ownership structure is fundamentally linked to the

purpose of the corporation. For example, MailChimp co-founder Chestnut said that "I build things

and get to watch customers buy and use them--that's tremendously satisfying. Sometimes I see

companies build things I know are for investors--and what is the investor's purpose? Just to

increase wealth. That doesn't align with my mission." For him, even just considering investors

ahead of customers goes against the whole reason he started a business. As a result, MailChimp

has stayed private for 14 years. Ken Grossman, the founder of the craft brewer Sierra Nevada, tells

a similar story. He wrestled with the possibility of going public in the '90s, when many other fast-

growing independent brewers were doing so. "I felt that the fiduciary responsibilities to look out

for shareholders would constrain some of the things I wanted to do that might not provide the

10

greatest short-term gain, like doubling down on quality equipment or investing in green energy,”

he says. "The irony is that if I leveraged the company and went public, it would be easier to get

the resources I needed, but then I would have had different masters with different requirements."6

Similarly, at least since Mitt Romney, a founder of Bain Capital, ran for president in 2012,

there has been a recurring debate regarding the impact of private equity firms on their portfolio

firms. When KKR and Bain Capital purchased Toys “R” Us in 2005, one store manager noted, “it

changed the dynamic of how the store ran.” By 2007, 97 percent of the company’s operating profit

was earmarked to interest expense. The store manager noted, “They kept cutting payroll and

cutting payroll, expecting one person to do the job of two people.” When the company announced

its liquidation in 2017, it attributed its demise to competition from Amazon and Walmart. Others

noted, however, that its debt burden prevented it from investing in stores and employees. “Had

[Toys “R” Us and other bankrupt PE-owned retailers] remained publicly owned, they would have

had a much higher probability of being able to adapt, to invest, and to withstand” the challenging

retail conditions.7 Others dispute this characterization, noting that private ownership increase the

focus of firms and hence their quality.8

Evidence in the literature

As the discussion above suggests, purpose might be related to firm ownership for one of two

reasons. First, owners with different goals may choose different types of firms. Second, different

corporate ownership structures may change the way firms run and operate in ways that affect their

6 https://www.inc.com/magazine/201510/tom-foster/do-you-really-want-to-go-public.html, accessed January 7, 2019. 7 https://www.theatlantic.com/magazine/archive/2018/07/toys-r-us-bankruptcy-private-equity/561758/ , accessed January 7, 2019. https://www.fastcompany.com/90227917/toys-r-us-private-equity-and-stagnant-salaries , accessed January 7, 2019. 8 https://www.economist.com/briefing/2016/10/22/the-barbarian-establishment , accessed January 7, 2019.

11

purpose. In this section, we consider both the various types of owners, and how these types might

relate to corporate purpose.

Companies can be classified into two broad categories of ownership: whether the firm is

publicly listed or privately owned. Within these categories, there are additional differences among

owners. Among private firms, a firm can be owned by individuals such as the firm founders, by

an asset manager such as a private equity fund, or by a corporate parent that itself is a publicly

listed firm. Among public firms, ownership concentration can vary from extremely dispersed to

highly concentrated structures. Public firms can also differ along other dimensions of ownership

(e.g. growth vs value investors, retail vs institutional investors).

We focus here on ownership concentration for several reasons. First, dispersion of

ownership is the defining characteristic of the public corporation that spawned the interest in

corporate governance, management incentive plans, and agency theory (Berle and Means 1932,

Jensen and Meckling 1976). Second, past research has shown that the concentration of ownership,

in particular the presence of large blockholders, is associated with important characteristics such

as lower executive pay levels, higher investment, and lower accounting fraud (Edmans and

Holderness 2017). Third, a public corporation that has ownership concentrated in one or just a few

shareholders is effectively a private company, albeit with more liquidity of its shares. Therefore,

as ownership becomes more concentrated, all else equal, we might expect a public firm to become

more similar to a private firm. However, all else is not equal. In contrast to private owners that

tend to have much longer holding periods and limited liquidity of their shares, public owners tend

to hold the stock of a firm for shorter periods and their shares are traded in a liquid market. This

distinction suggests that although concentrated owners in public markets might yield influence on

12

the corporation, as private owners do, their influence might be focused more on current stock prices

and short-term earnings rather than on long-term profitability.

Evidence on differences across public and private firms

Past research suggests that corporate ownership affects firms’ strategic and financial choices (e.g.,

Asker, Farre-Mensa and Ljungqvist 2014; Gilje and Taillard 2016; Bernstein, 2015). Gilje and

Taillard (2016) study investment choices in the natural gas industry. They find that private firms

adjust their capital expenditures less compared to public firms in the face of changes in investment

opportunities, which they attribute to public firms having easier access to finance. Bernstein (2015)

studies innovation practices, and finds that after going public, the quality of internal innovation

declines and many skilled inventors leave the firm. However, public firms attract new human

capital and acquire external innovation suggesting that the structure of innovation changes.

Bharath, Dittmar and Sivadasan (2014) find that companies going private extensively restructure

their portfolio of plants, selling and closing plants more quickly than others. Asker, Ferra-Menza

and Ljungqvist (2014) find that, compared with private firms, public firms invest substantially less

and are less responsive to changes in investment opportunities, especially in industries in which

stock prices are most sensitive to earnings news. They attribute these findings to short-termist

pressures in public markets distorting investment decisions. Maksimovic, Phillips and Gordon

(2017) find, in contrast, that public firms respond more to demand shocks after going public and

are more productive than their matched private counterparts. This effect is stronger in industries

that are capital intensive and dependent on external financing.

The effects of ownership have received less attention within management research. Trostel

and Nichols (1982) is one of the few studies that provide evidence on the relation between whether

13

a firm is publicly listed or not and its business strategies and management processes. Using

interview methods, and data from roughly 20 companies, they do not find evidence that

management in private firms is less professional and formal than public firms. More recently and

in a substantially expanded global sample of 10,000 establishments, Bloom, Genakos, Sadun and

Van Reenen (2012) find that public and private equity firms have stronger management practices

than privately owned firms, particularly those that are founder-run.

Ownership concentration in public firms

In general, researchers agree that blockholders influence management behavior. McCahery et al.

(2016) provides evidence on the specific channels of voice that blockholders employ. In order of

frequency, they show that blockholders engage in discussions with top management, vote against

management, communicate with the board away from management, propose specific actions to

management, and aggressively question managers on conference calls.

In terms of operating effects, Brav et al. (2008) find that 13D filings, triggered when an

investor acquires more than 5% of a public company, lead to improvements in total payout, CEO

turnover, and operating performance. Brav et al. (2015) show that the performance improvements

result from higher plant-level productivity, which in turn stems from higher labor productivity—

despite working hours not rising and wages not falling. Brav et al. (2018) show that a 13D filing

is associated with a decline in R&D investment, but also an increase in both the number of future

patents and their quality (as measured by citations). However, this effect is not universal. Recent

work finds that the positive performance effect of blockholders is driven only by the largest

transactions, and that roughly 80% of firms experience no improvement in operating performance

and. insignificant negative long-term returns (deHaan, Larcker, McClure 2018).

14

Given this mixed evidence, we do not know how concentrated ownership will affect

corporate purpose. However, we expect that it will likely have a significant influence given that

its impact on management and governance practices.

Private firm owned by a Private Equity (PE) fund

A growing literature on PE fund ownership suggests that PE firms are managed differently

compared to other firms. Bernstein and Sheen (2016) analyze restaurant chain buyouts between

2002 and 2012 using health inspection records in Florida and find that restaurants become cleaner,

safer, and better maintained after the buyouts. PE targets slightly reduce employee headcount, and

lower menu prices. Because these changes to store-level operations require monitoring, training,

and better alignment of worker incentives, they suggest that PE firms improve management

practices throughout the organization. Bloom, Sadun and Van Reenen (2015) provide more direct

evidence on management practices that PE firms use. They find PE owned firms adopt more

modern management practices, such as lean manufacturing, and show stronger performance

related incentive practices. PE ownership is also associated with greater delegation of authority to

plant managers, especially in demand related activities such as sales and marketing and new

product introductions. The cross-sectional nature of their data does not permit them to distinguish

selection from treatment effects. That is, the superior management of PE owned firms could come

entirely from purchasing well-managed firms, rather than improving firms' management over time.

In contrast, Bernstein and Sheen (2016) observe smaller effects on franchised restaurants, a finding

that they use to claim a causal effect of PE ownership on corporate outcomes. Lerner, Sorensen

and Stromberg (2011) find some support that PE owned funds improve the innovation capacity of

firms, potentially relieving public firms from short-termist pressures. Following going private firm

15

patents get more cited, show no shifts in the fundamental nature of the research, and become more

concentrated in important areas of companies’ innovative portfolios. Davis et al. (2014) find that

PE buyouts lead to modest net job losses but large increases in gross job creation and destruction.

Buyouts also bring productivity gains at target firms, mainly through accelerated exit of less

productive establishments and greater entry of highly productive ones.

Overall, the evidence suggests that PE fund ownership is associated with different, and

generally more productive, ways of running a firm. However, what that effect might be on the way

employees experience the meaning of the work is a priori unclear.

Private firm owned by a Public Parent Company

Many public firms own other private firms that they choose to keep as separate private firms with

their own leadership structure. For example, Chesbrough (2003) studies 35 separate legal entities

created by Xerox between 1984 and 1998 to commercialize output from their research laboratories.

Keeping them as separate legal structures with their own management practices might allow a firm

to maintain a distinct culture thereby influencing its ability to be innovative (Christensen 1997).

This prediction is consistent with work on formal and real authority by Aghion and Tirole (1997),

or the property rights theory of Grossman and Hart (1986). Placing assets in a subsidiary limits the

parent’s exposure on the subsidiary’s debts to the value of the subsidiary’s assets. This implies

that the net loss to the parent when the project assets lose value is smaller than if the project were

run as a division inside the parent entity. This creates stronger incentives for the management of

the subsidiary to innovate but it also gives them more real authority over the subsidiary’s future

(Ayotte 2017).

16

Whether keeping a subsidiary as a separate legal entity is effective at insulating the firm

from the pressures of the parent company is unclear. If indeed this is effective, then we expect the

private firm to exhibit corporate purpose that is closer to other private firms. If it is not effective,

we expect those firms to exhibit a corporate purpose that is much closer to the one exhibited by

public firms.

In summary, ownership is strongly related to core strategic choices of companies. Further,

given anecdotal evidence, there is reason to believe ownership is related to the perceived purpose

of the firms, although the nature of this relationship is unknown. It is to this question that we now

turn.

Data and Research Design

Research Design

The aim of our study is to explore the relationship between firm ownership and corporate purpose.

For our measure of firm ownership, we first assign each firm in a given year to four top-level

categories: whether the firm is i) publicly traded, ii) a private subsidiary of a public firm, iii)

private-equity owned, and iv) privately owned, non-private equity. We then further subdivide our

largest category, public firms, by the degree of control of their top public shareholders. This

subdivision allows us to examine whether purpose (and purpose inequality) varies by the degree

of power held by their largest shareholders.

We divide our analysis into two parts. In the first part, we construct and then relate

measures of corporate purpose to various types of firm owners. For corporate purpose (whose

construction is described in detail below) we first measure it at the firm-year level, and then

disaggregate the measure by job level. This disaggregation allows us to explore which employees

17

are driving our differences and, specifically, whether ownership is related not only to corporate

purpose, but also to corporate “purpose inequality;” that is, the difference in purpose felt by the

top-ranked employees to the others within the organization.

Note that our research design is correlational: our setting does not provide a clean

experiment to isolate the causal impact of firm ownership on corporate purpose. As such, at the

end of this first part of our analysis, we provide a set of evidence, by no means definitive, on

whether the correlation between purpose and ownership reflects a sorting or a treatment effect.

In the second part of our analysis, we explore factors that may explain the purpose patterns

reported in the prior section. Specifically, we ask whether the characteristics of the CEO

(background and compensation) differ across types of firm owners, and whether those differences

can explain our results. We then ask whether actions taken by the CEO and top management—

both restructuring moves (M&A, layoffs, divestitures) and provision of employee benefits—also

can explain our results.

The goal of these two analyses together is to gain some large sample evidence on how

corporate purpose differs by firm ownership, as well as potential insight into whether those

differences are causal and the underlying reasons for the identified differences.

Data Description

The primary data for this study is compiled from applications to Fortune Magazine’s annual “100

Best Companies to Work For” list, administered by The Great Place to Work® Institute. The

applications comprise all submissions to the annual list, regardless of whether the companies were

successful. These data have been previously used by Gartenberg, Prat and Serafeim (2019), where

18

it is described in further depth, as well as Guiso, Sapienza and Zingales (2015), and Garrett,

Hoitash and Prawitt (2014).

All applicants are required to employ more than 1,000 workers in the US and to have

existed for seven years or longer. Since the submission process is costly for applicant companies,

our dataset comprises a self-selected sample whose management believes that they have a credible

chance of being included on the list and who place relatively greater value on human capital. One

potential concern is that sample selection may limit the generalizability of our results if public and

private firms differ in their levels of participation in a way that is also related to the strength of

their purpose. On the other hand, this sample may also be a conservative setting for our analysis

since these companies are more likely to aim for a sense of purpose among their employees relative

to the universe of firms, or at least the appearance of such. We consider potential sample bias in

the discussion section.

The application package to the list contains two sections: The Culture Audit Survey©

(CAS) and the Trust Index© employee survey (TI). The CAS includes structure and policy

information about the applying company, including industry and location of headquarters,

employee composition (e.g., numbers, age and tenures at different hierarchical levels), and pay

and benefit information. The TI, the main data of interest for our study, is a randomized employee

survey that captures employees’ beliefs about the workplace climate, including management

quality, coworker relationships, and the nature of their work. The survey is stratified by job level,

where the job levels include hourly employees, sales (commission-based) workers, middle

managers and supervisors, salaried professional and technical workers, and executives and senior

19

managers. The survey consists of 57 questions with responses range from 1 to 5 on a Likert-like

scale, where 1 corresponds to “almost always untrue” and 5 corresponds to “almost always true.”9

Our data agreement with the Institute provides access to all applications – both successful

and unsuccessful – from 2006 to 2016 (Table 1 Panel A). We combine summary information from

the CAS with TI survey data, which we aggregate up to the firm-year level. The sample includes

2,662 firm-year observations, aggregated from 1,509,797 survey responses from full time

employees, with a median level of 565 responses per firm.

We merge this dataset with the following additional data sources: Compustat to identify

the publicly-traded companies in our sample, CapitalIQ to identify private equity owners, Factset

for blockholder information on the public firms, and Execucomp for CEO compensation data.

Measure of Corporate Purpose

We base our purpose measure on an earlier study by Gartenberg, Prat and Serafeim (2019). They

run an exploratory factor analysis on the raw survey questions to identify bundles of beliefs that

co-vary among employees, and identify four factors that explain most of the variance. The factor

analysis is executed at the employee level using all individual survey responses for all full-time

employees of all for-profit firms (both public and private). As they do, we include 53 of the 57

questions, excluding four questions that are outcome measures of overall job satisfaction. While

Gartenberg, Prat and Serafeim (2019)’s sample stops at 2011, our sample extends to 2016 and

includes both public and private firms. Replicating their results on this expanded sample, the factor

analysis yields substantively the same four factors that explain most of the variation, including the

9 While our data agreement precludes us from releasing the full set of questions from the survey, a public description of the survey instrument can be found here: http://www.greatplacetowork.net/our-approach/what-is-a-great-workplace, accessed 6/25/16. Our four questions on purpose fall under the designated “Employee Pride” category.

20

factor that captures corporate purpose.10 To construct firm-year level measures, we follow their

approach and average the scores for each factor across all individuals within each firm in given

year.

Of the four identified factors, they dub one “Purpose-Clarity.” We, for expositional

simplicity, refer to this factor as “Corporate Purpose.” This factor includes beliefs in the meaning

of work combined with clarity from management. The four meaning-related questions are “My

work has special meaning: this is ‘not just a job’”, “When I look at what we accomplish, I feel a

sense of pride”, “I feel good about the ways we contribute to the community”, and “I'm proud to

tell others I work here.” The questions that relate to clarity focus on whether management provides

clear direction, job responsibilities, and tools that can be used to achieve the desired outcomes.

The two items with the highest loadings on this factor, aside from the four purpose questions, are

“Management has a clear view of where the organization is going and how to get there” and

“Management makes its expectations clear.” A third question, “I am given the resources and

equipment to do my job” also loads highly in this factor. Meaning and clarity matter in combination

in accordance with the construct of “meaningful work”, work that is “purposeful and significant”

(Pratt and Ashforth, 2003, pg. 311), in ways that purpose or clarity alone are not. See Gartenberg,

Prat and Serafeim (2019) for a more detailed discussion of this measure. They find that this factor,

and none of the other factors, positively predicts firm performance. Later in the paper, we substitute

this variable for other measures of purpose to assess how the results vary with the choice of purpose

measure.

10 Refer to their study for detailed descriptions of the other three factors, which they refer to as “management,” “purpose-camaraderie”, and “non-discrimination.” We later consider “Purpose-camaraderie,” as well as a composite index of the four meaning questions on their own, in the discussion section as alternative measures of corporate purpose.

21

Measures of Ownership

We sort firms into four top-level categories: public, private (non-PE owned), private (PE owned),

and private with public owners. We identify public firms by whether they have a corresponding

record in Compustat, private equity-owned firms by whether they are identified as such in

CapitalIQ, and public parent-owned firms by whether they self-identify as such in the Culture

Audit survey.

We identify the blockholder concentration data by merging our sample with Factset. We

allocate firms to two ownership concentration groups each year according to the percentage of

shares held by the top five investors in a firm. If the percentage of shares is higher (lower) than the

median then a firm is allocated to the high (low) ownership concentration group.

Control variables

We include the following control variables in our specifications: the natural logarithms of firm and

number of employees, as the sense of purpose may be related to the size of the firm and the

corresponding degree of bureaucracy required. We also include fixed effects for year, industry,

and the state in which the firm is headquartered, as all of these factors may influence the degree of

purpose within firms.11 Finally, we include controls for age and tenure brackets of the employees

to account for the fact that people of different age and tenure might systematically choose to work

for companies with different strengths of corporate purpose. These controls are also important to

include if, for example, some firms grow more quickly and attract new employees with weaker set

of beliefs about a firm’s corporate purpose.

11 Controlling for firm fixed effects is difficult in our setting because we observe few changes in ownership for the period and the firms in our sample and we do not have a good understanding of how fast changes in ownership might translate into changes in purpose. We leave this important question for future research.

22

Summary statistics

Table 1 contains summary statistics. As is apparent from this table, these are large, established

firms with two thirds of the observations represented by the following five industries:

manufacturing, financial services, retail, professional services, and IT.

<<< Insert Table 1 here >>>

Purpose and Firm Ownership

Empirical Specification

We estimate the relation between corporate purpose and ownership characteristics using an OLS

model, clustering standard errors at the firm level to account for serial correlation within a firm

over time. The model we estimate is:

Purposeit = a + b1 x Publicit + b2 x PrivatePublicit+b3 x PEi + b4 x Industryit + b5 x Yeart + b6 x Statet +

∑Firmcontrolsit + ∑Employeecontrolsit + ϵ23 (1)

where Purpose is the purpose-clarity factor for firm i in year t. Public is an indicator variable that

takes the value of one if the firm is publicly listed. PrivatePublic is an indicator variable that takes

the value of one if the firm is private but its ultimate owner is a public company. PE is an indicator

variable that takes the value of one if the firm is owned by a private equity fund. The omitted group

in the regression is private firms that are not owned either by public firms or private equity funds.

The coefficients b1 - b3 are our main estimates of interest. They represent the incremental increase

or decrease in purpose associated with the respective ownership structure relative to a firm that is

privately owned. State, Industry and Year represent the state of corporate headquarters, industry

23

and year fixed effects. Firm controls include the natural logarithm of total assets and employees.

Employee controls include employee age and tenure.

Purpose and Firm Ownership

Figure 1 shows the distribution of corporate purpose by ownership type. The top left figure shows

the histogram distribution of purpose for private (non-PE, no public owner) firms. Since this group

forms the comparison group against which we compare the other firms, we overlay the histogram

with the kernel density of this same distribution (the red line) in this and all subsequent figures.

This red line enables a visual comparison of the distribution of purpose in private (non-PE, no

public owner) to the other ownership types. The top right figure depicts the histogram distribution

of purpose for public firms. As can be seen in the comparison to the red line, the distribution is left

skewed, indicating that purpose is lower in public firms. The bottom two figures, private firms

with public owners (left) and private equity owned firms (right), also show that purpose is left

shifted for both of these types of firms.

<<< Insert Figure 1 here >>>

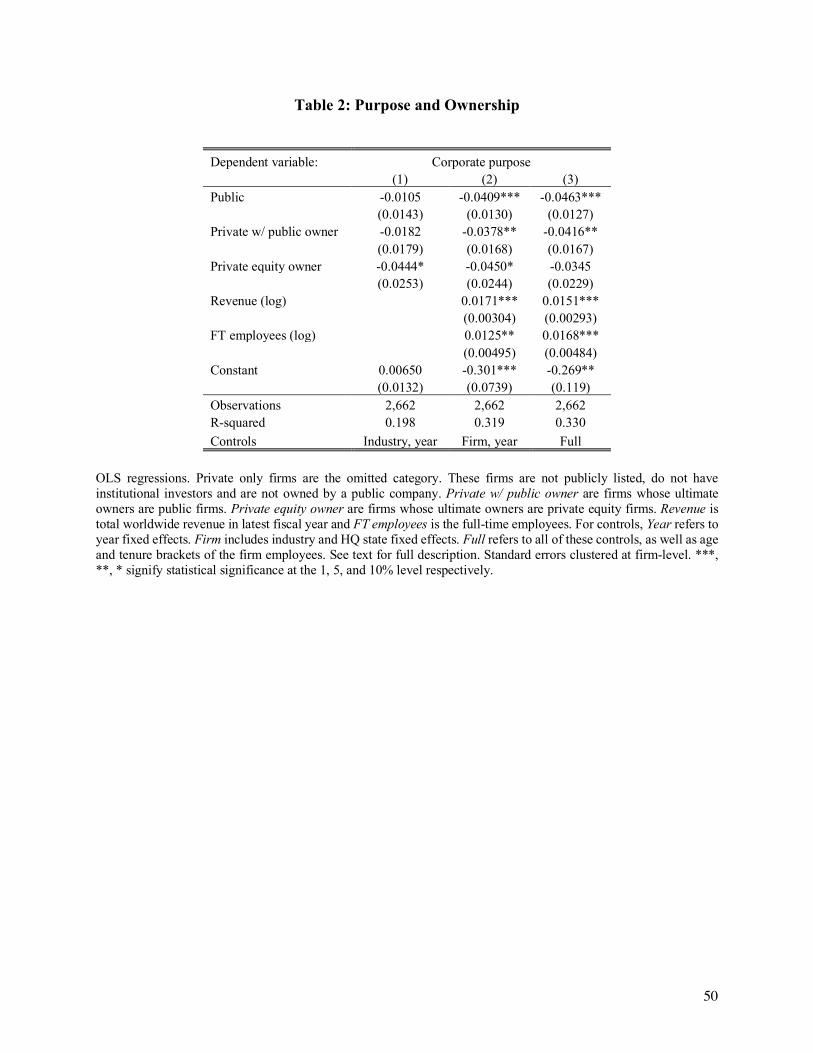

Table 2 presents the results of estimating model (1). Columns 1-3 introduce progressively

more control variables. In column 1, we control only for year fixed effects. In Column 2, we add

industry and state fixed effects as well as firm controls. In Column 3, we include employee

controls. In Column 1, the coefficients on the ownership variables do not obtain significance

except for the coefficient on PE owned firms. This changes in Column 2 where now the

coefficients on public firms, private firms owned by a public firm and PE owned firms are all

negative and significant. Moreover, the explanatory power of the model increases from 19.8 to

31.6% suggesting that industry membership and firm size are both important explanatory factors.

24

Adding employee controls changes the models little as the explanatory power increases to 32.7%,

and the coefficients on the ownership variables change very little, although the coefficient on PE

owned firms is now negative but insignificant. The coefficient on public firms is significant at the

1% level and that on private firms that are owned by a public firm at the 5% level. Larger firms

have stronger corporate purpose as the estimated coefficients on firm sales and employees are both

positive and significant.

Public and private firms differ systematically both in terms of size and sector membership.

Although we control for both sector fixed effects as well as firm size, we are worried that our

controls might not adequately mitigate these differences. To understand the robustness of our

results to a more balanced sample we implement a matching process where we implement exact

matching without replacement on year and sector membership and nearest neighbor on firm size.

In untabulated analysis using a smaller more balanced sample, the results are very similar where

public and private firms owned by public firms have significantly lower purpose compared to

private firms. Later in the paper we present more results from matched sample analysis.

<<< Insert Table 2 here >>>

Table 3 presents the same model as in Table 2 column 3 but now disaggregating corporate

purpose by job level. Several findings emerge. First, public firms have lower corporate purpose

across all job levels except for senior executives. Second and strikingly, the magnitude of the

coefficient increases monotonically as one goes down the organizational hierarchy. Executives in

public firms hold the same beliefs about corporate purpose as their peers in private firms but this

changes for middle management, even more so for professional staff and then even more for hourly

workers. This is true even when adjusting for standard deviations by job level: the point estimates

for executives (Column 1) represent 6% of a standard deviation and are statistically insignificant,

25

while the point estimates for middle managers, professional and hourly workers represent 17%,

24% and 32% of a standard deviation for purpose within each of these job levels, respectively, and

are all statistically significant at conventional levels.

We find a similar effect for private firms that are publicly owned. The trend is similar with

the estimated coefficient insignificant for senior executives (4% of a standard deviation in purpose)

and the most negative for hourly workers (29% of a standard deviation in purpose).

We can also think of these results in terms of “purpose inequality”: senior executives of

public firms experience a greater sense of purpose than their employees, and that inequality of

purpose is exacerbated the deeper one goes within the organization. This is not the case for private

companies. We show this explicitly in Appendix Table A1 by replacing corporate purpose as our

dependent variable with the delta of corporate purpose between executives and the remaining job

levels.

The final pattern in Table 3 is also interesting. The lower purpose previously reported in

Table 2 within private equity owned firms is driven primarily by executives, followed by middle

managers. The coefficients for professional staff and hourly workers are insignificant. In other

words, executives of private equity owned firms have a lower sense of corporate purpose relative

to those of privately owned (non-PE, not public owned) (p=0.013) or public firms (p=0.048), more

so than the remainder of the employees.

<<< Insert Table 3 here >>>

Ownership Concentration

So far, we have decomposed private firms to three different types, and kept public firms in

a single category. We now decompose public firms according to their level of ownership

concentration. Firms in the below median group of ownership concentration have 20% of the

26

shares held by top 5 investors while firms in the above median group have 34% of the shares held

by top 5 investors.

Figure 2 shows the histogram distributions of corporate purpose within public firms by

each of these four quartiles, overlaid with the distribution of corporate purpose within private firms

(the red line) for comparison purposes. The top left panel shows that public firms with the most

dispersed owners actually have higher purpose relative to private firms. This purpose progressively

falls as concentration increases, with the above median having notably lower purpose than private

firms.

<<< Insert Figure 2 and Table 4 here >>>

The multivariate analysis confirms these results. In Table 4 Panel A, we reproduce Table

2, but replace the Public indicator variable with two ownership concentration indicator variables.

Purpose is lower among firms with higher ownership concentration. Public firms in the low

concentration group exhibit no different purpose than private firms. In contrast, public firms in the

high concentration group exhibit the largest negative difference compared to private firms. Given

that firms with concentrated ownership might be firms where the founding family has a major

stake, we are interested to understand if the concentrated ownership effect is driven by institutional

investors or by family ownership. We construct an indicator variable taking the value of one for

all public firms where a family has more than 1% of the shares. Column 4 includes this indicator

variable and the estimated coefficient on it is positive but not significant. Interestingly, although

these firms tend to have concentrated ownership, if anything, corporate purpose is at least as high

as in private firms. The coefficients on the concentrated ownership indicators become even more

negative after we control for whether a public firm is a family firm. Altogether, the results in Table

4 show that corporate purpose decreases with concentrated ownership.

27

<<< Insert Table 4 here >>>

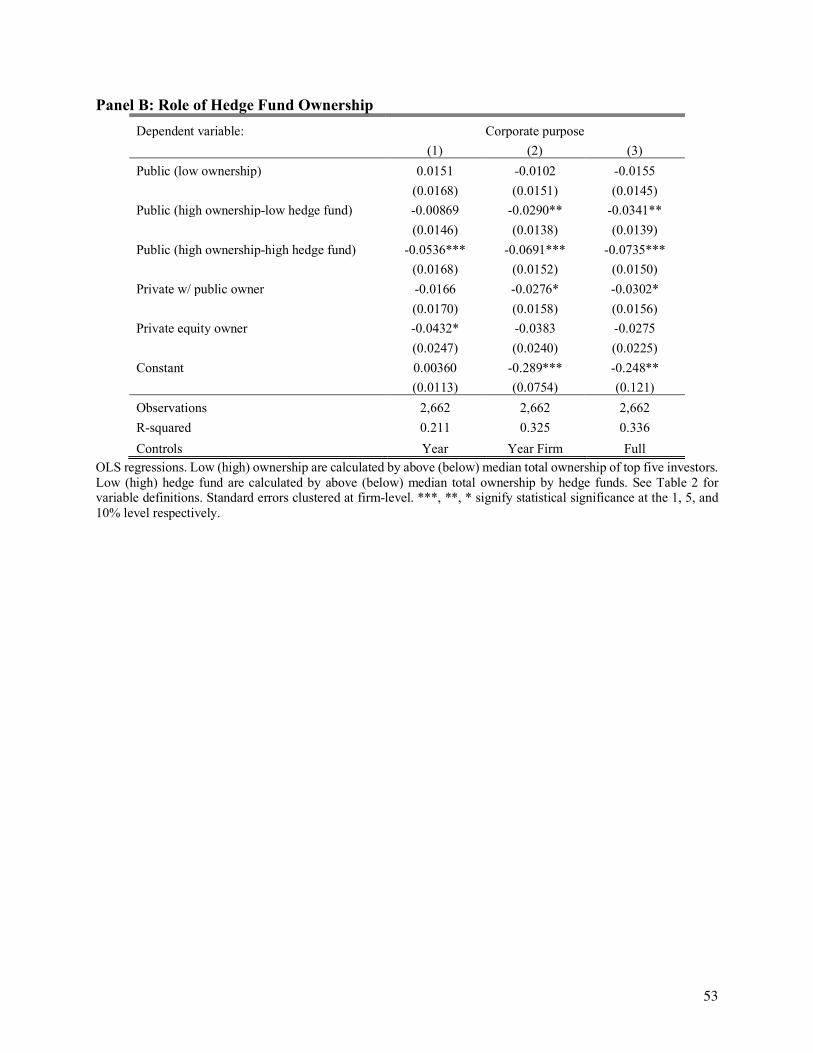

Table 4 Panel B further decomposes the high concentration variable based on whether there

is low or high hedge fund share ownership. We are interested in further understanding the

relationship between ownership concentration and purpose. The type of investors seems a primary

candidate in providing further evidence on the nature of this relationship. Specifically, we expect

for firms with concentrated ownership and high levels of hedge fund ownership the negative

relationship with corporate purpose to be stronger. This is because hedge funds are among the

most active investors when it comes to influencing management and governance processes.

Therefore, we decompose the indicator variable for high concentration to two indicators: one for

low and one for high hedge fund ownership. We find that the coefficient on the high hedge fund

ownership group is both larger in magnitude (i.e. more than double) and more statistically

significant. It is worth noting, that the coefficient on the indicator for high concentration but low

hedge fund ownership is also significant, suggesting that other types of investors are also driving

the previously documented relationship between ownership concentration and purpose.

Sorting or treatment effect?

Our findings are consistent with two distinct, although related, interpretations. The first

interpretation is that different types of owners choose different types of companies, and hence we

are reporting a sorting effect in the market for corporate control. The second interpretation is that

owners have a direct impact on the employees of their companies, and so our patterns capture the

treatment effect of companies under different types of corporate owners. We consider each of these

now.

28

Under the first interpretation, the patterns that we report reflect companies with higher

purpose choosing to remain private. Our findings would also suggest that, among public firms,

shareholders that take large positions in companies choose to invest in lower purpose companies.

This assortment may arise either because these companies have other attributes that attracts

powerful investors, or that investors – for whatever hard to identify reason – find lower purpose

an attractive attribute on its own. Under this interpretation, investors have no direct influence on

purpose of the company, and the differences strictly reflect a selection effect. Under the second

interpretation, owners have a direct impact on purpose. This effect could manifest as the impact of

these investors on the choices and culture of the company that directly influences the strength of

purpose felt by the employees. For example, if investors change the investment priorities of the

company, or the identity or focus of the management team, these changes could meaningfully

affect the employees.

Absent a convincing exogenous change to company ownership, it is impossible to

definitively separate these two effects. Moreover, from a theoretical perspective, it is implausible

to us that only one is present in our setting: it is much more likely that owners match to different

types of companies, and then influence the sense of purpose within those companies in different

ways. While we cannot separate these two interpretations, Table 4 Panel C shows our best attempt

to isolate a treatment effect in our setting. In this table, we replace the ownership categories with

lagged ownership and forward ownership throughout all specifications (hence our sample drops

by nearly half in this test). If a sorting effect is present, we expect purpose to lead ownership. If a

treatment effect is present, we expect ownership to lead purpose. Columns 1-3 show the results for

low and high concentration and columns 4-6 decompose the high concentration further into low

and high hedge fund ownership. Throughout all columns we find the that association between lag

29

ownership and purpose is stronger and statistically significant. Overall, the results in Panel C are

more consistent with a treatment effect being present in our setting.

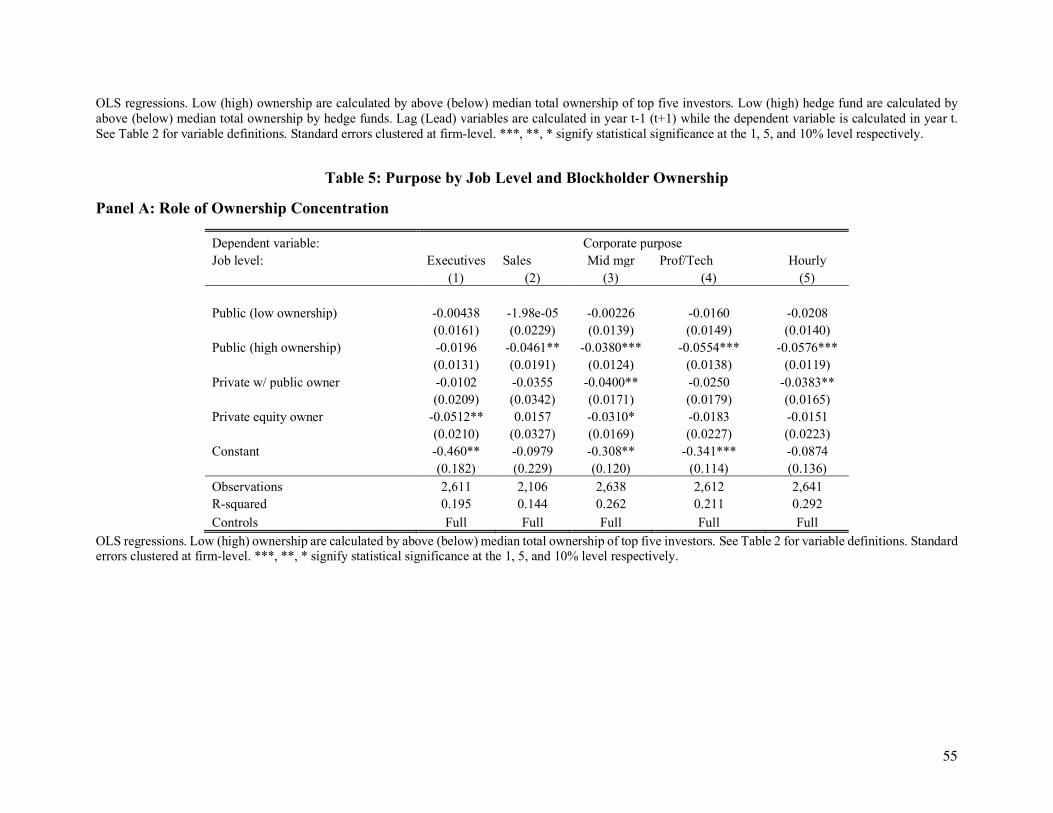

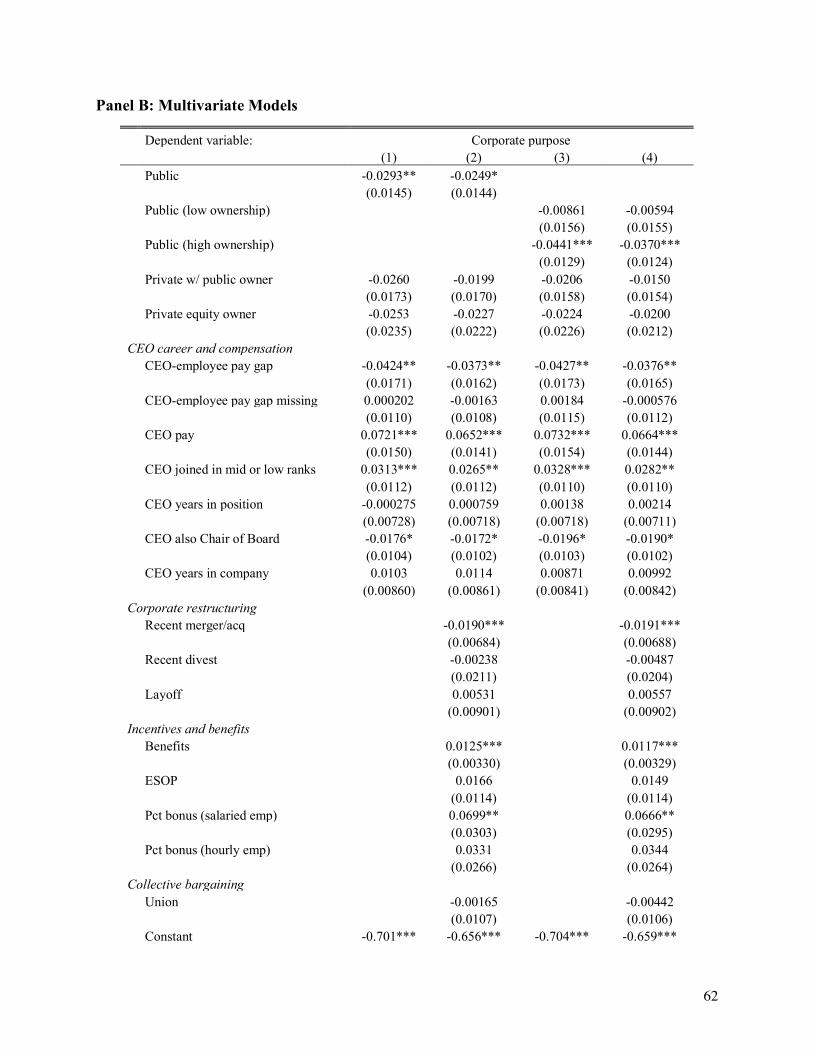

Table 5, Panel A now examines the effect of blockholder concentration on corporate

purpose by job level. Overall, the results suggest that the decline in purpose with more

concentrated ownership reported in the prior table is not driven by senior executives, but instead

by their subordinates. Furthermore, the fall in purpose down the organization hierarchy noted in

Table 3 is driven by blockholder concentration. In other words, the “purpose inequality” of public

companies between senior and lower levels is most pronounced within firms with the most

concentrated shareholders. In fact, public firms with low blockholder concentration exhibit none

of the “purpose inequality” evident in the firms with concentrated shareholders, and are

indistinguishable from private firms. This result is inconsistent with the prediction that as public

ownership becomes more concentrated corporate purpose becomes more similar to the one found

in private firms. In fact, we find the opposite suggesting that public investors might be

systematically making different choices and influencing companies in different ways than private

investors when it comes to CEO characteristics and incentives and the choices that managers might

be making. Appendix Table A1 provides these inequality results directly.

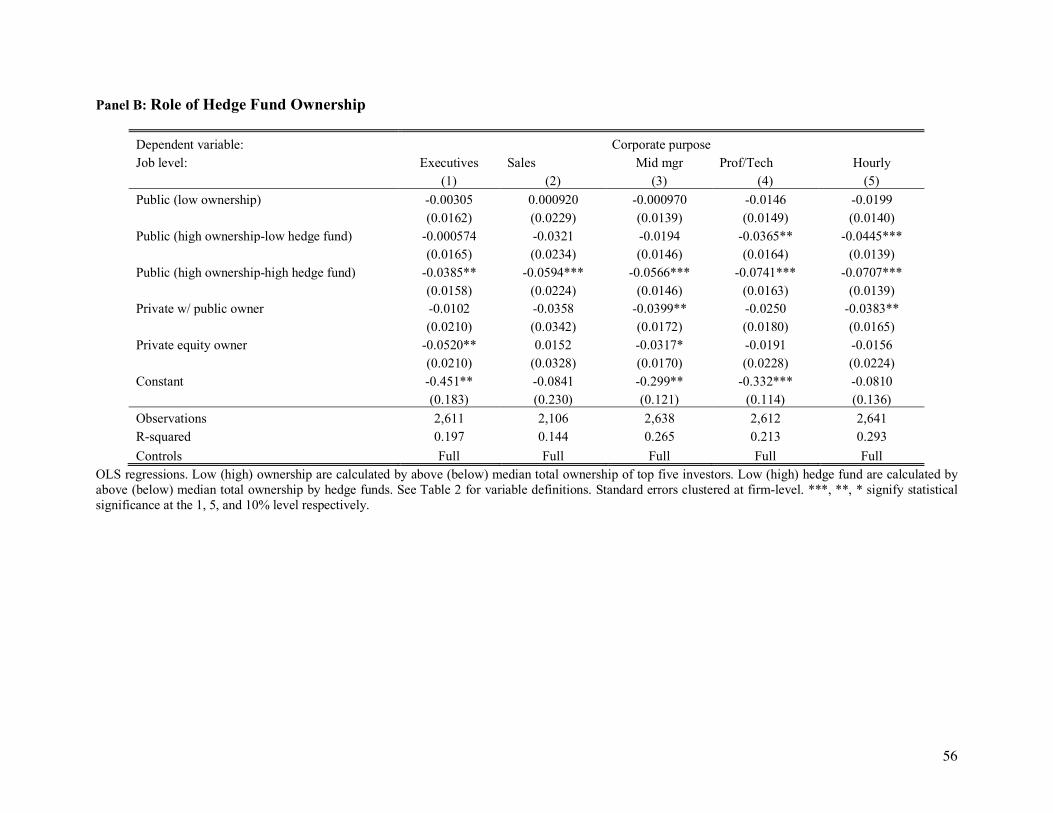

Table 5 Panel B illustrates a more nuanced picture where within the firm group with high

ownership concentration having high hedge fund ownership is associated with lower purpose

across all levels in the organization, including executives. Table 5 Panel C replicates the lead/lag

analysis of Table 4 Panel C by job level. As with the prior analysis, we find that our results are

primarily driven by lagged ownership, rather than forward ownership. This pattern is consistent

with a treatment effect of ownership on corporate purpose.

<<< Insert Table 5 here >>>

30

Another potential explanation is that the results we document are driven by differences in

financial performance in those companies. For example, if some investors take concentrated

positions in badly performing companies and these companies have a low sense of purpose partly

due to frustration with bad financial performance, then financial performance operates as a

correlated omitted variable. This alternative explanation would also suggest that private firms in

our sample have better financial performance than public firms. We fail to find evidence consistent

with this alternative explanation in our data. Including return-on-sales (ROS), the only financial

performance variable include in the GPTW data, does not change our key results. However, the

financial performance explanation could also affect our results within public firms if for example,

hedge funds might choose to invest in struggling companies. To address this concern, we match

across types of ownership within industry and year based on financial performance as measured

by three periods of lagged return on assets and three periods of lagged revenue growth.

In Table 6 we estimate average treatment effects after applying inverse probability

weighted regression adjustment (IPWRA) matching that is often applied in studies of public health

to estimate treatment effects in populations. One advantage of the method compared to propensity

score matching is that it allows for multiple treatments (in our case, high and low ownership, and

hedge fund ownership), rather than a single dichotomous treatment variable.

The results of Table 6 show that our results are robust to IPWRA matching on prior

performance. Public firms with highly concentrated ownership continue to have lower purpose

compared to private firms, matching on past performance. This effect is magnified for firms with

high hedge fund ownership.

The results of the prior analysis provide the following insights. First, corporate purpose is

lower in public firms relative to their private counterparts, particularly private firms that are not

31

owned by either a private equity firm or public parent. Second, this result is driven by employees

below the top of the organization—middle managers, professional and hourly workers—and not

executives. Lastly, among public firms, purpose is progressively lower among firms with higher

shareholder concentration. This pattern is also driven by employees below the top of the

organization and not executives.

Role of CEO Characteristics

What might explain these patterns? In this section, we examine whether differences in corporate

leadership, in particular CEO characteristics, across private and public firms can account for the

difference in purpose among these firms. We focus on two categories of characteristics. First, we

explore compensation structure and in particular the gap between a CEO and average

compensation of employees inside the firm. Second, we examine the background of the CEO,

including whether he or she rose in the company through its low or mid-level ranks, and how long

the CEO has been at the company and in the role itself.

Table 6 Panel A provides summary statistics for the variables of interest. We note that we

have CEO-employee pay gap and CEO pay only for a subset of public firms and for none of the

private firms. Both measures decline as ownership concentration increases although the decline is

not monotonic. We note that because firm size also declines, these relations could be obscured by

firm size. Therefore, in the models we always control for firm size to ensure that our results are

not confounded by absence of appropriate controls for size.12

We find a large difference in whether the CEO was externally hired in C-suite vs internally

promoted from lower level of the organizations across private and public firms. Within public

12 To keep the sample constant in the multivariate analysis, we impute missing values of compensation at the mean, and include an indicate variable whether the data is imputed. These imputed values are not included in our panels of descriptive statistics.

32

firms, 34% of CEOs are internally promoted and started in middle management or lower levels.

Within private firms, in contrast, 54% of CEOs are internally promoted. Within public firms the

percentage declines as ownership concentration increases. The rate for the bottom portfolio is 39%

while the rate for the top is 28%. Within private firms, both firms owned by public companies and

PE-owned firms have much lower percentages at 27 and 28% respectively. In contrast, the

percentage is 65% for all other private firms.

Notably, these differences do not reflect differences in the number of years the CEO has

been in that position. Within public firms, the average CEO tenure is 9.6 years, a value that does

not decrease monotonically across the ownership concentration quartiles. Within private firms,

average CEO tenure is longer for PE-owned companies at 13.2 years. Similarly, we find no

differences in terms of CEO power, as reflected by whether the CEO is also the Chair of the Board.

Although, the percentage of holding both positions is much higher in public rather than in private

firms, it does not follow a meaningful patterns across types of public or private firms. In contrast,

average number of years in the organization is related to where the CEO started. The highest CEO

tenure as an employee is for purely private firms at 26.4 years and the lowest for private firms

owned by public companies at 18 years and declines with shareholder power, consistent with

internal promotion statistics.

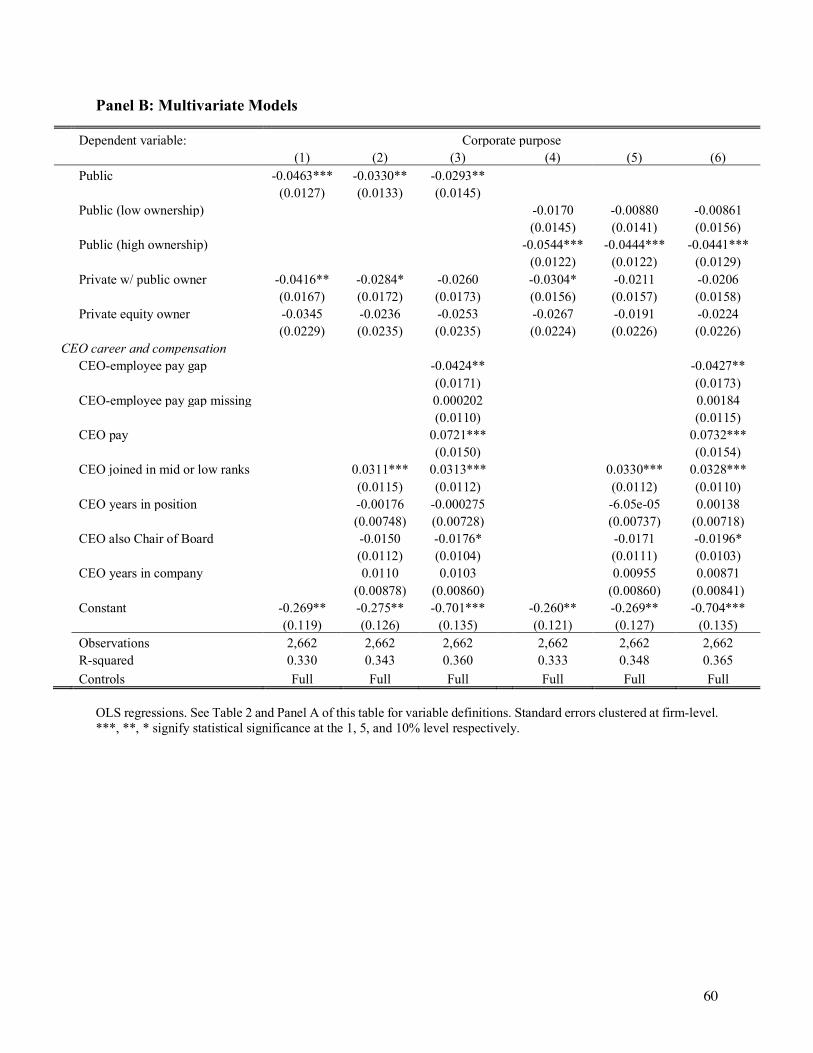

Panel B includes these variables in the models to understand a) how those factors might be

related to corporate purpose and b) whether including them in the model mediates the effect of the

ownership variables. Columns 1-3 include the public indicator variable while Columns 4-6 include

the four ownership concentration indicators for public firms. Columns 1 and 4 are the baseline

reproducing the existing results from the previous tables and are presented for comparison

purposes. Columns 2 and 5 include the CEO position variables. Columns 3 and 6 add the CEO pay

33

and pay gap variables. The coefficient on whether the CEO has joined from mid or low-level ranks

is positive and significant at the 1% level across all models. Moreover, including it reduces the

magnitude of the coefficient on the public indicator variable by close to 30%. It also reduces the

magnitude of the coefficients on the ownership concentration variables by close to 20%. Adding

the CEO pay gap and pay variables further decreases the magnitude of the Public firm coefficient

although not by as much. These variables also load significantly in the models. Firms with higher

CEO to average employee pay gap have lower sense of purpose after controlling for average CEO

pay level (which is significantly and positively correlated with purpose). These results provide

support to the idea that in organizations where the CEO is higher paid employees are not

dissatisfied as long as they are also rewarded with proportionally higher pay.

The two variables that together explain substantial differences in purpose across

organizational owners are CEO-employee pay gap and whether the CEO joined at a middle or

lower organizational rank. In Panel A, however, these two variables do not appear to differ

substantially by the type of owner. One challenge in interpreting the descriptive statistics in Panel

A, however, is that each blockholder ownership group can represent companies that are very

different sizes, which we control for in our multivariate analysis in Panel B. To account for these

between-group differences, we create size-adjusted blockholder groups sorting firms first in size

quartiles and then within quartiles firms into the top and bottom ownership concentration. We find

that the CEO-employee pay gap does in fact increase with ownership concentration, and insider

CEOs decline, as we would expect.

<<< Insert Table 6 here >>>

Figures 3-5 provide graphical depictions of this result. Figure 3 provides a bin-scatter plot

of corporate purpose versus CEO-employee pay gap, and shows that purpose exhibits a strong

34

decline as the pay gap increases. We can also consider this result in terms of “purpose inequality”.

Figure 4 shows the relation between CEO-employee pay gap and purpose inequality: there is a

strong, positive relation between the two, suggesting that the firms which pay CEOs are more

relative to employees also have the largest gap in purpose between executives and their

subordinates. Figure 5 shows the difference in purpose between public firms with CEOs joining at

low or middle ranks, and those with outsider CEOs. This figure visually confirms the multivariate

results showing that firms with internally promoted CEOs have a stronger sense of purpose.

<<< Insert Figures 3, 4, and 5 here >>>

Overall, we conclude that CEO starting position and CEO-employee pay gap are likely

important determinants of purpose, mediating the relation between purpose and ownership. The

inclusion of CEO starting position and compensation together explains approximately 35% of the

difference in purpose between public and private firms.

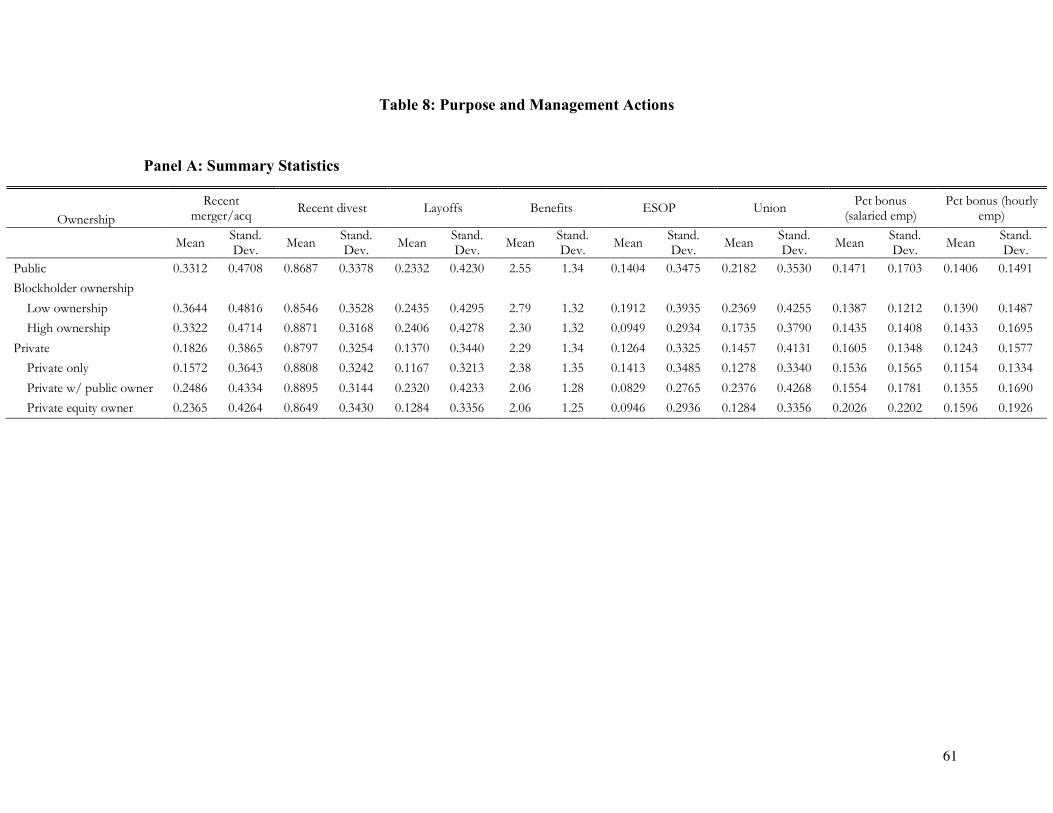

The Role of Management Actions

We next explore whether critical actions taken by the management team can account for our

observed differences in purpose. These actions fall into two categories: restructuring activities

(mergers, divestitures, and layoffs) and compensation structure and benefits granted to employees.

In particular, we construct an index that sums five indicator variables for whether the firm offers

schedule benefits or family benefits. The schedule benefits index is composed of three variables:

option for compressed work week offered, flexible schedule program offers and telecommute

option offered. The family benefits index is composed of two variables: onsite childcare offered

and offsite childcare subsidized. We can think of the second category both as the incentives

35

provided to employees and also as a heuristic about how management considers splitting its surplus

between employees and owners.

Table 7 Panel A shows summary statistics for these variables. A few interesting

observations are worth highlighting. The percentage of firms that had a merger, layoff, and unions

is much higher at public rather than private firms. Within public firms and across ownership

concentration quartiles, the benefits index and the percentage of firms with ESOPs and unions

declines, although these relations could be driven by size differences. Within private firms, firms

that are not owned by public firms or PE funds exhibit significantly lower percentage of mergers,

layoffs, higher benefits index, and higher percentage of ESOPs. PE owned firms exhibit higher

variable compensation pay for both salaried and hourly workers consistent with PE funds

introducing stronger pay for performance incentive contracts.

Panel B presents the estimated models now including these variables. Columns and 1 and

3 present the baseline specifications for comparison purposes from Table 6. Columns 1-2 include

the public indicator variable while Columns 3-4 include instead the two ownership concentration

indicator variables. Including these additional variables further decreases the magnitude of the

coefficients on the ownership variables. However, they are still significant. Firms with recent

mergers exhibit significantly lower purpose while firms with higher benefits index and higher

variable pay exhibit stronger purpose. The rest of the variables, such as past layoffs, offering

ESOPs or presence of union are not correlated with purpose. As before, we conclude that including

management actions mediate the relation between purpose and ownership but they do not fully

explain that relation as the ownership variables are still significant in the models.

<<< Insert Table 7 here >>>

36

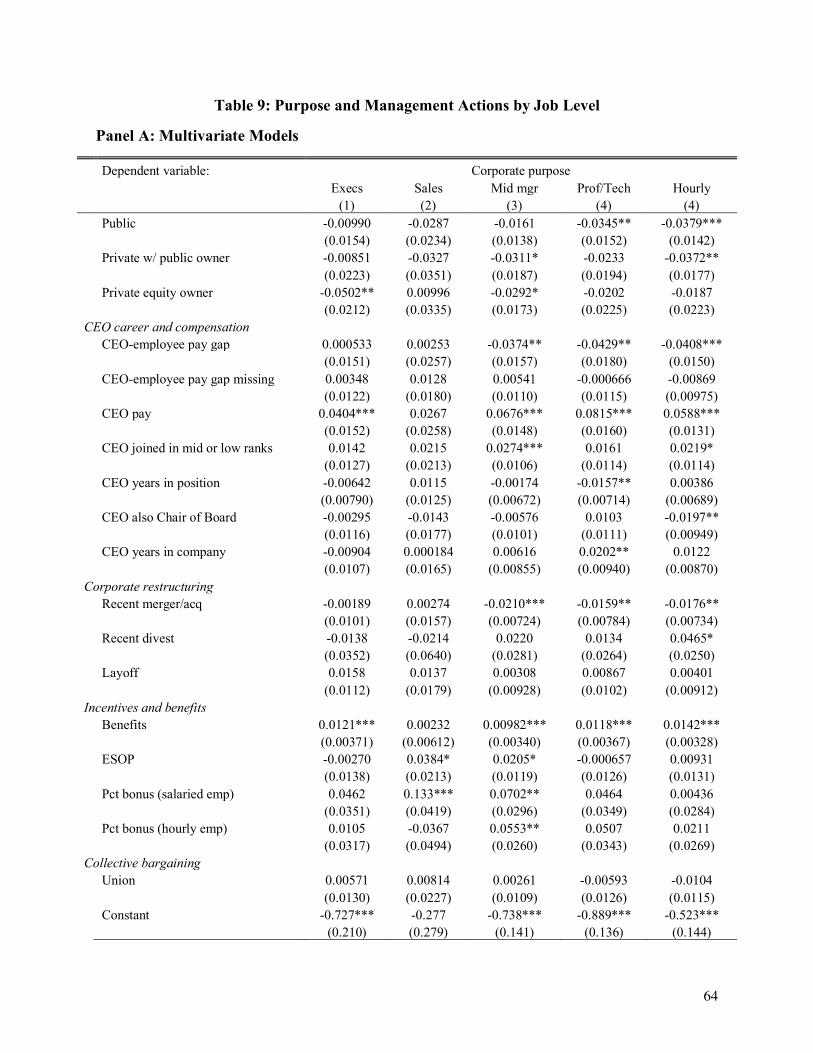

For our final analysis of this section, we disaggregate the analysis of Table 7 by job level.

Table 8 Panel A provides the results with all public firms together, and Panel B splits public firms

by blockholder concentration quartile. This table shows that the inclusion of management

restructuring and benefits almost completely explains purpose for middle managers, and explains

a substantial additional portion for the other job levels below the executive level.

<<< Insert Table 8 here >>>

In summary, the second half of our analysis provides the following insights. First, the CEO-

employee pay gap and background of the CEO collectively explain approximately 30% of the

difference between public and private firms. Second, the addition of management restructuring

actions and benefits explain an additional 5%, and more so for middle managers. We now turn to

a discussion of these results.

Discussion

In the first half of our analysis, we report markedly lower purpose in public firms, particularly

those with concentrated blockholders. These patterns are driven by subordinate employees within

the hierarchy, rather than executives and senior managers. In the second half of our analysis, we

show that these patterns can be substantially explained by the following differences among these

companies: first, companies with lower purpose are also those that bring in the CEOs from outside

the organization and pay them more relative to their employees. Second, companies with lower

purpose are those that recently underwent fundamental restructuring activities, such as mergers

and layoffs, and also offer their lower-level employees lower benefits and incentives.

In this we consider both the interpretation of our results, as well as their robustness.

37

Interpretation of our results

What might explain these results? In our view, much of these patterns are consistent with

the need for equity in organizations. As a recent article in Harvard Business Review contended, a

strong sense of purpose among employees and CEO-employee pay inequality are mutually

exclusive: “to avoid a corporate-purpose exercise being viewed by employees as a cynical joke

there are certain pre-conditions that must be met. The major ones are addressing excessive CEO

and senior executive pay, and treating employees and other stakeholders fairly.”13 According to

equity theory (e.g., Adams, 1963; Akerlof and Yellen, 1990), the perception of fairness,

particularly a consistent and understandable allocation of rewards to inputs, is a critical workplace

attribute, and that employees withdraw their effort in the face of perceived inequity.

A related question arises. If purpose leads to higher performance, as shown by Gartenberg,

Prat and Serafeim (2018), why would profit-motivated investors pursue actions associated with

lower purpose? Given our large sample research design, we cannot observe the specific intent of

these investors. However, these are several plausible reasons in our view why they might do so.

First, these investors may simply not be aware of the link between their actions and corporate

purpose. As we discussed, research studying how investors influence firms has found a wide

variety of outcomes from very positive to very negative ones. Purpose is hard to observe,

particularly among employees below the executive ranks, and investors may not be focused on

how their actions impact employees. Second and related to ease of observability, multitasking

challenges may lead investors to focus on more readily observable outcomes than purpose. For

example, if shareholders succeed in attracting an external CEO or pushing for a new acquisition,

13 https://hbr.org/2018/08/your-corporate-purpose-will-ring-hollow-if-the-companys-actions-dont-back-it-up

38

these acts are both easier to observe and communicate to their own constituents than the impact on

corporate purpose that may arise from these actions.

Alternatives and robustness

Several questions arise regarding the robustness of our analysis, to which we now turn.

Purpose Measure

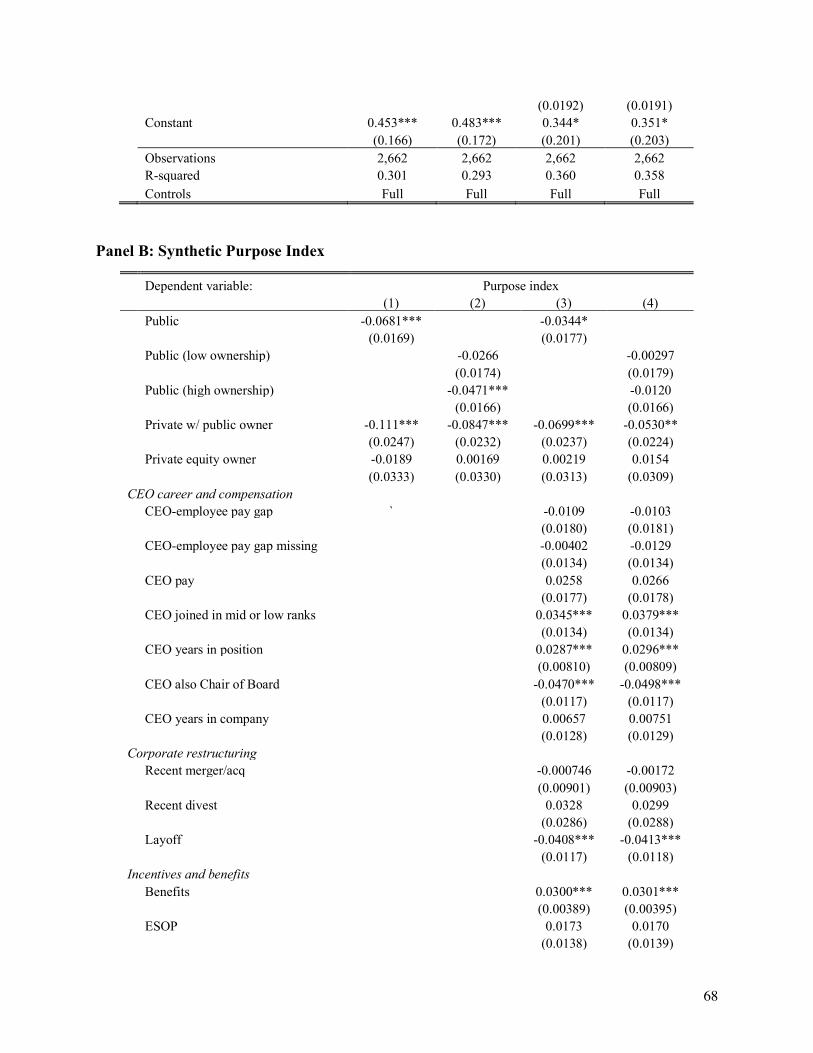

So far we have focused our analysis using a purpose metric that measures employee beliefs both

about the purpose and meaning of the work but also about the clarity provided by management

towards that purpose, a measure identified by Gartenberg, Prat and Serafeim (2019) as one of two

purpose-related factors in an exploratory factor analysis and labeled Purpose-Clarity. We focused

on this measure because it strongly predicts firm performance, and varies substantially across

firms. For robustness, however, we look here at two alternative approaches to capturing purpose.

One alternative measure of purpose is what Gartenberg, Prat and Serafeim (2019) call

Purpose-Camaraderie, the second of two factors they identified in a factor analysis that concern

purpose. This measure includes the four purpose questions, listed in the introduction section,

together with questions on the degree of camaraderie between employees in the workplace. The

two items with the highest loadings on this question are i) whether employees have fun at work

and ii) whether they believe that there is a familial atmosphere among employees at work. The

other questions included in this factor similarly focus on workplace collegiality. Table 10 Panel A

presents the results. Columns 1 and 2 do not include the CEO characteristics and management

choice variables. These are included in Columns 3 and 4. Columns 1 and 3 include the public firm

indicator variable while Columns 2 and 4 include the four indicators for ownership concentration.

39