Embed Size (px)

Citation preview

Coworking &Flexible Workspace in Vietnam2020-2021A Market Insight Report by Acclime Vietnam, supported by Cushman & Wakefield

2

Flexible workspace in Vietnam.Where opportunity meets growth.

The outlook.

Marketplace analysis and the underpinning for the future of work.

Insights into operators and market entry ramifications.

The power of users.Value and perception of occupiers.

Future of work and the key role of flexible workspace.

References & Engagement team.

pg. 3

pg. 9

pg. 14

pg. 19

pg. 31

pg. 34

pg. 36

CONTENTS.

1

2

4

5

6

3

Flexible workspace in Vietnam.Where opportunity meets growth.

1

3

4

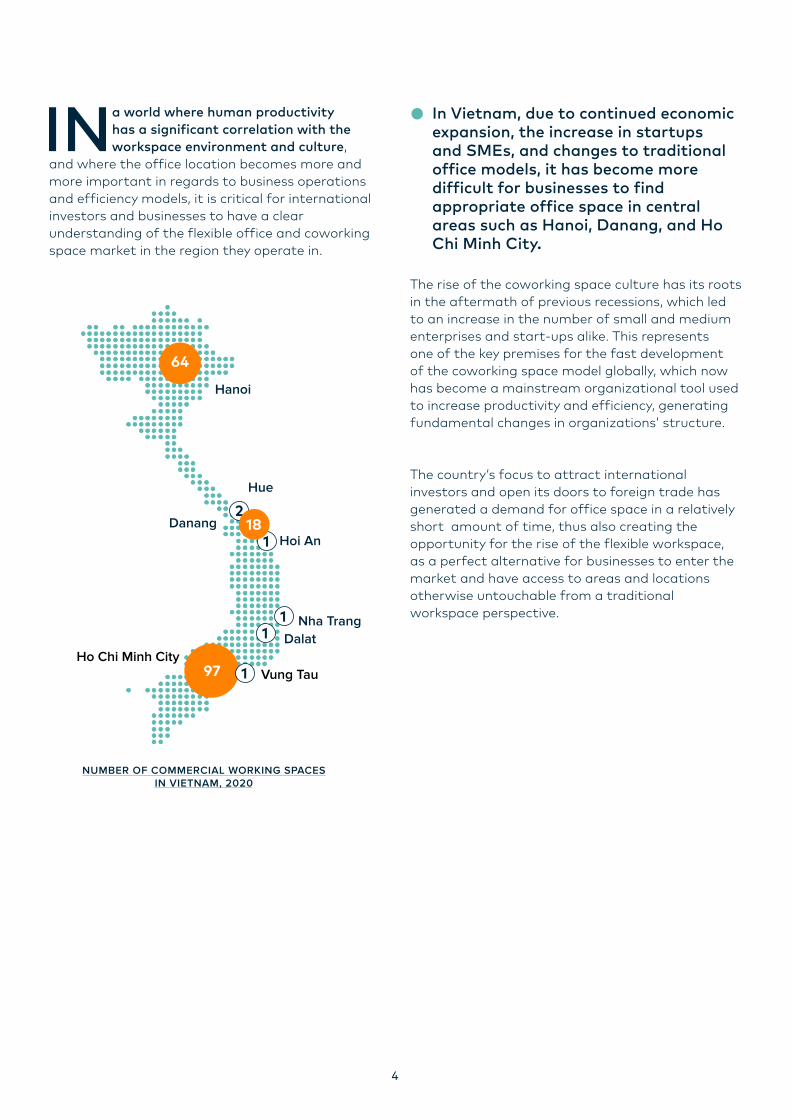

IN a world where human productivity has a significant correlation with the workspace environment and culture,

and where the office location becomes more and more important in regards to business operations and efficiency models, it is critical for international investors and businesses to have a clear understanding of the flexible office and coworking space market in the region they operate in.

Hanoi

Ho Chi Minh CityVung Tau

Danang

Hue

Hoi An

Nha TrangDalat

The rise of the coworking space culture has its roots in the aftermath of previous recessions, which led to an increase in the number of small and medium enterprises and start-ups alike. This represents one of the key premises for the fast development of the coworking space model globally, which now has become a mainstream organizational tool used to increase productivity and efficiency, generating fundamental changes in organizations’ structure.

The country’s focus to attract international investors and open its doors to foreign trade has generated a demand for office space in a relatively short amount of time, thus also creating the opportunity for the rise of the flexible workspace, as a perfect alternative for businesses to enter the market and have access to areas and locations otherwise untouchable from a traditional workspace perspective.

In Vietnam, due to continued economic expansion, the increase in startups and SMEs, and changes to traditional office models, it has become more difficult for businesses to find appropriate office space in central areas such as Hanoi, Danang, and Ho Chi Minh City.

NUMBER OF COMMERCIAL WORKING SPACESIN VIETNAM, 2020

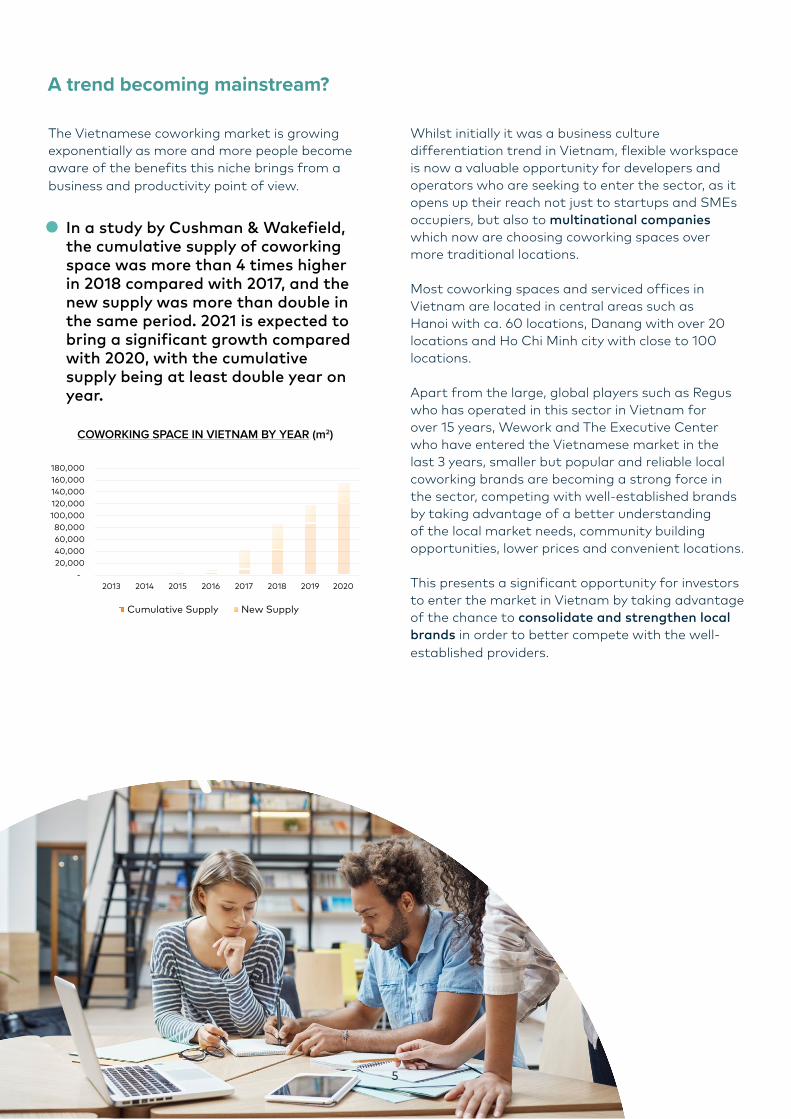

The Vietnamese coworking market is growing exponentially as more and more people become aware of the benefits this niche brings from a business and productivity point of view.

Whilst initially it was a business culture differentiation trend in Vietnam, flexible workspace is now a valuable opportunity for developers and operators who are seeking to enter the sector, as it opens up their reach not just to startups and SMEs occupiers, but also to multinational companies which now are choosing coworking spaces over more traditional locations.

Most coworking spaces and serviced offices in Vietnam are located in central areas such as Hanoi with ca. 60 locations, Danang with over 20 locations and Ho Chi Minh city with close to 100 locations.

Apart from the large, global players such as Regus who has operated in this sector in Vietnam for over 15 years, Wework and The Executive Center who have entered the Vietnamese market in the last 3 years, smaller but popular and reliable local coworking brands are becoming a strong force in the sector, competing with well-established brands by taking advantage of a better understanding of the local market needs, community building opportunities, lower prices and convenient locations.

This presents a significant opportunity for investors to enter the market in Vietnam by taking advantage of the chance to consolidate and strengthen local brands in order to better compete with the well-established providers.

A trend becoming mainstream?

COWORKING SPACE IN VIETNAM BY YEAR (m2)

(Source: Cushman & Wakefield - Research)

In a study by Cushman & Wakefield, the cumulative supply of coworking space was more than 4 times higher in 2018 compared with 2017, and the new supply was more than double in the same period. 2021 is expected to bring a significant growth compared with 2020, with the cumulative supply being at least double year on year.

- 20,000 40,000 60,000 80,000

100,000 120,000 140,000 160,000 180,000

2013 2014 2015 2016 2017 2018 2019 2020

Coworking space in Vietnam by year

Cumulative Supply New Supply

5

6

Telephones and accessories Computer electronic products & components

Textiles Machinery, equipment, tools and spare parts

Footware Wood & wooden products

Means of transport and equipment Sea food

Iron & steel

Others

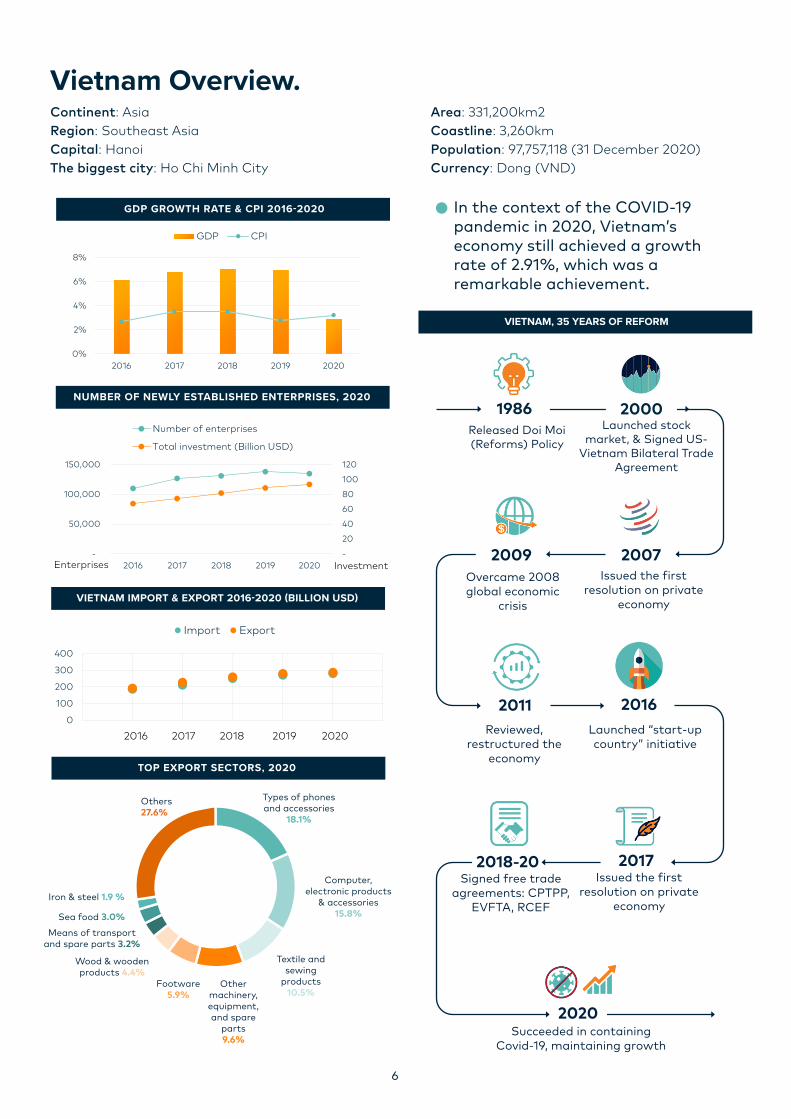

Vietnam Overview.Continent: AsiaRegion: Southeast AsiaCapital: HanoiThe biggest city: Ho Chi Minh City

Area: 331,200km2Coastline: 3,260kmPopulation: 97,757,118 (31 December 2020)Currency: Dong (VND)

NUMBER OF NEWLY ESTABLISHED ENTERPRISES, 2020

VIETNAM IMPORT & EXPORT 2016-2020 (BILLION USD)

GDP GROWTH RATE & CPI 2016-2020

TOP EXPORT SECTORS, 2020

Types of phones and accessories

18.1%

Computer, electronic products

& accessories15.8%

Textile and sewing

products 10.5%

Other machinery, equipment, and spare

parts9.6%

Footware5.9%

Wood & wooden products 4.4%

Means of transport and spare parts 3.2%

Sea food 3.0%

Iron & steel 1.9 %

Others 27.6%

VIETNAM, 35 YEARS OF REFORM

2020

20172018-20

20162011

20072009

2000Launched stock

market, & Signed US-Vietnam Bilateral Trade

Agreement

Succeeded in containing Covid-19, maintaining growth

Signed free trade agreements: CPTPP,

EVFTA, RCEF

Issued the first resolution on private

economy

Issued the first resolution on private

economy

Launched “start-up country” initiative

Reviewed, restructured the

economy

Overcame 2008 global economic

crisis

In the context of the COVID-19 pandemic in 2020, Vietnam’s economy still achieved a growth rate of 2.91%, which was a remarkable achievement.

Enterprises Investment

2016 2017 2018 2019 2020

1986Released Doi Moi (Reforms) Policy

-

20

40

60

80

100

120

-

50,000

100,000

150,000

2016 2017 2018 2019 2020

Number of new established enterprises

Number of enterprises

Total investment (Billion USD)

0%

2%

4%

6%

8%

2016 2017 2018 2019 2020

GPI Growth rate & CPI, 2016-2020

GDP CPI

0

100

200

300

400

0 1 2 3 4 5 6

Vietnam export and import 2016-2020

Import Export

7

Vietnam’s Resilient Strategy - Prospects and Reform

Under Covid-19, Vietnam earned a valuable market position in 2020 by being among one of the few economies across the globe that managed to maintain a positive economic growth, cumulated with attracting foreign investments and keeping the number of virus infections to a minimum.

Over the last decade, Vietnam has experienced significant development, due to economic and political reforms that drove the country’s growth to new heights, transforming it into a medium-income country with exceptional prospects.

Recent changes and economic reforms, combined with political stability and the government’s drive to engage Vietnam in multiple favourable agreements and treaties, have created an extraordinary opportunity for international investors to take advantage of the regional growth prospective and focus their attention on Vietnam.

In 2020, due to the Covid-19 pandemic, the country’s economy expanded only 2.91%, and from October to December 2020 the economy grew with 4.48%, signaling a strong recovery supported by continuous investments in the private sector, in conjunction with the successful actions of the local authorities to mitigate and contain the health crises.

In 2019, Vietnam’s GDP grew by 7.02%. At the same time, imports and exports of goods and services increased with 13% and 14.3% compared with previous year. The top export destinations in 2019 were South Korea, Japan, ASEAN, China, EU and United States. The US was the biggest export destination with circa 58 billion USD, and in 2020 the export destinations maintained their positioning.

According to World Bank analysts, Vietnam’s growth is explained by three main factors: Trade Liberalisation, Domestic Reforms combined with lowering the cost of doing business, and Investments in Education and Human Capital development.

Vietnam has continued its commitment to internationalise its economy by being a part of multiple Trade Agreements which offer investors commercial incentives and tariff reductions. Vietnam joined the ASEAN free trade area in 1995 and signed a free trade agreement with the US in 2000.

In January 2007, it participated in the World Trade Organisation (WTO) and is concluding several free trade agreements in 2015-2019 such as EU – Vietnam Free Trade Agreement (EVFTA) and the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP), and more recently the Vietnam-UK Free Trade Agreement.

15.2

35.9 35.538.0

28.5

15.8 17.5 19.1 20.4 20.0

05

10152025303540

2016 2017 2018 2019 2020

Vietnam foreign direct investment (Billion USD)

Registered Disbursed

Internationalisationand Trade Openness is Key.

The country has signed a historical treaty with European Union on the 30th of June 2019, boosting trade and investment on both sides, and helping Vietnam to further integrate into the global economy and the international community.

In the EVFTA, Vietnam has increased its offered benefits compared with the WTO in terms of market access granted to EU service providers, where additional sectors will be opened up for EU investors. The EU has described the free trade deal as “the most ambitious free trade deal ever concluded with a developing country.”

Foreign direct investment into Vietnam rose 6.7% percent in 2019 from USD 19.1 billion in 2018.

The manufacturing and processing industry to receive the largest amount of investment (64.6% of total pledges) followed by real estate (10.2%). Based on the projected growth of the real estate sector, opportunities for developers to take advantage of the momentum become more and more attractive.

Data released by the General Statistics Office in Vietnam shows that FDI disbursement dropped only 3.2% yoy in September 2020, compared with the previous year and Foreign Direct Investments dropped 18.9% compared with previous year. In perspective, compared with the region and the EU, US economies, Vietnam has overall managed to maintain a positive economic growth and enabled investors to take advantage of the market’s opportunities, even in the Covid-19 conditions.

Within this complex, country-wide development mechanism, enabled by sustained foreign direct investment in most of the major business sectors in Vietnam, flexible office spaces present an attractive segment, not just from the operators’ vantage point, but also considering the standpoint of developers entering the sector and creating a healthy competition with the traditional office models.

TOP 10 FOREIGN INVESTORS BY COUNTRY, LIFETIME, 2020

70.6 60.3 56.6

33.7 25.7 22.3 18.5 12.9 12.9 10.4

Top 10 Foreign Investors by Country, Lifetime, 2020

Total registered capital (USD billion)

KoreaRep. of

Japan Singapore Taiwan MalaysiaChina. PR

NetherlandsThailandHong Kong SAR

(China)

British Virgin

Islands

VIETNAM FOREIGN DIRECT INVESTMENT 2016-2020 (BILLION USD)

8

Total registered capital (billion USD)

The outlook.

2

9

10

Flexible workspace has turned into a global industry, enabling a fundamental shift in the way companies interact and do business

around the world. According to Statista’s coworking space worldwide data, there are currently over 18,700 coworking spaces around the globe.

A research publication by Cushman & Wakefield found that coworking spaces are rapidly expanding in Southeast Asia due to the region’s fast-growing economies and tech-savvy population. The high internet penetration in Southeast Asia along with the rapid development of e-commerce are key drivers which explain the exponential and sustained rise of flexible workspace.

Globally, the Asia Pacific region accounted for 35% of all coworking spaces.

Based on an analysis from Statista, Singapore is currently home to the largest start-up ecosystem in the ASEAN region, followed by Malaysia, Philippines, Thailand, Vietnam and Indonesia.

With a continuous flow of direct foreign investments and mergers & acquisitions – Southeast Asia region aggregates cutting-edge technological innovation with infrastructure development and state driven digital initiatives, thus laying the underpinning for the rise of flexible workspace demand.

Flexible vs Traditional.Cross-functional competition?

Ho Chi Minh City, Vietnam is one of the most attractive destination for investors due to its fast-growing economy. The city is also considered the biggest market of flexible workspace in Vietnam. Along with CBRE’s report in July of 2019, as of Q2 2019, the total market supply reached 46,266 sq. m. GFA, increased by 101% from the same period last year. This figure is projected to have a twofold increase in 2020, lifting the rate of flexible workspace from total available office locations up from 2% to 5%.

Due to the China-US trade war, the manufacturing and logistics industries were a key driver for industrial and traditional office space market in Ho Chi Minh City, with major companies exploring opportunities laid out by the shift in production from China to Vietnam.

Under the current global situation of the Covid-19 pandemic, where both traditional and flexible office space markets are going through a temporary downturn, it is a high probability that in the coming aftermath, the move towards flexible workspaces will be reinvented by a sustained drive of the digital economy and a more agile approach from international enterprises.

Coworking Resources states, following the regional growth, that Vietnam is in the top 50 countries worldwide by coworking growth per capita. The country secured 0.1 new spaces annually for every 1,000,000 inhabitants. Compared with Singapore, which has almost 5 new spaces per million inhabitants, Vietnam has a long way ahead. This is actually good news for investors entering the market, as sustained development and internationalisation are the underlying foundation for the sector’s growth.

Furthermore, Ho Chi Minh City ranked 41 of top 50 cities worldwide in 2019/2020, where every 47.5 days a new coworking space was established.

The entry of international operators in the Vietnamese market is expected to further the scalability of the industry, by engaging providers in competitive strategies, partnership agreements or business consolidation models.

From the user’s perspective, these are all beneficial outcomes as market diversity and healthy rivalry creates more added value and flexibility, bringing down the overall office prices as well.

Understanding Growth and Leveraging Opportunities.

COWORKING GROWTH PER CAPITA

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

COWORKING GROWTH PER CAPITA

11

12

Which trends stand out?

Increase in foreign operators entering the market

The flexible workspace market in Vietnam has experienced significant expansion, especially in central hubs such as Ho Chi Minh City and Hanoi. This development has made the sector highly attractive to international providers across the world, which view Vietnam as a fecund business market, expecting high returns with relatively low risk.

Between 2019 and 2021, large flexible workspace brands such as WeWork, The Executive Center, and Regus have been expanding their coverage in Ho Chi Minh City and Hanoi, challenging local providers in active, consistent competition. However, due to Covid-19 and its impact on the market, some of the providers have paused their expansion or downsized, adopting a more risk-averse strategy.

This trend is seen to increase further in 2021 due to the high market growth rate, demand drivers and also because of the structural mindset shift started by the covid-19 pandemic, which pushed companies not just towards swift digital transformation adoption, but also made them view employee engagement and flexible work communication as key productivity assets.

Large enterprises are key demand driver

In 2021, aside from freelancers and SMEs who already represent a considerable percentage of the occupiers in flexible workspace locations across Vietnam, the demand of large enterprises are growing as they push towards digital transformation and adopt a lean approach towards employee engagement and work benefits. As vacancy rates drop annually and coworking operators continue to develop their signature product sets and scale new solutions to improve

their occupiers’ working condition, we will see more large enterprises turning towards flexible workspace operators, solving this way one of their major problems: the relatively high price and limited availability in the traditional workspace sector.

Innovation & Value-add

Enabled by technology, flexible office spaces are now being built in premium buildings, using unique architectural design models created to facilitate engagement, using modern communication facilities.

Operators are re-thinking coworking spaces using agile and lean working methodologies, thus empowering down the line the tenants to further expand on this communication transformation and start using the same innovative technologies themselves.

Transformation in facilities such as interior gardens and modern studios bring a high satisfaction to customers seeking something different than traditional offices. Other operators are adding extra amenities including food and beverage outlets(F&B), art galleries, game rooms, and bed & breakfast to stand out from the crowd.

The biggest value-adds for both large and small companies consider flexible workspace lies inthe flexibility to scale up and down, not having to invest significant Capex, and having theiroffices in a more vibrant environment that aligns more with the mindset and needs of youngemployees. It also gives companies access to the communities that operators build andmaintain, connecting everyone together through business matching, events, workshops andsocial engagements.

The Value In Numbers Key Operators and Scalable Locations

According to Cushman & Wakefield, flexible Vietnamese office space industry in 2020 occupies approximately 160,000m2 of space in A and B grade buildings across the two office hub cities, less than 4% of total A and B grade inventory.

As market growth rate of flexible workspace develops sustainably, numerous providers have emerged in the sector and have expanded rapidly. Alongside well established local providers such as Dreamplex and Toong whom already managed to aggregate their brand with local communities, foreign brands Regus, The Executive Center, Wework, UPGen, and Circo account for an increasing proportion in the market, with several locations in central areas like Ho Chi Minh City and Hanoi and future expansion plans on the table.

In addition, global providers The Hive, and Compass offices are believed to expand their locations in Vietnam during the next few years, seeking valuable consolidation opportunities and partnerships.

These market movements make the Vietnamese flexible workspace sector become extremely competitive, but also innovative, thus facilitating new technological adoptions and high-quality customer service delivery.

In 2020 and 2021, the number of coworking and serviced offices in Vietnam is set to break through the 160,000 square meters (m2).

According to the CBRE Global Research on Flexible Workspace, HCMC market is ranking in top 5 developing markets with the CAGR of more than 80% per year, where 91% of coworking space members are millennials under the age of 35.

75,000sq.mof space ingrade A&B buildings

HO CHI MINH CITY FLEXIBLE MARKET

TOP

5developing market

COWORKING SPACE MEMBERS

TOTAL FLEXIBLE MARKET SUPPLY

2020

under 35

160,000sq.m

91%

13

14

3Marketplace

analysisandthe

underpinningfor

the futureof work.

14

15

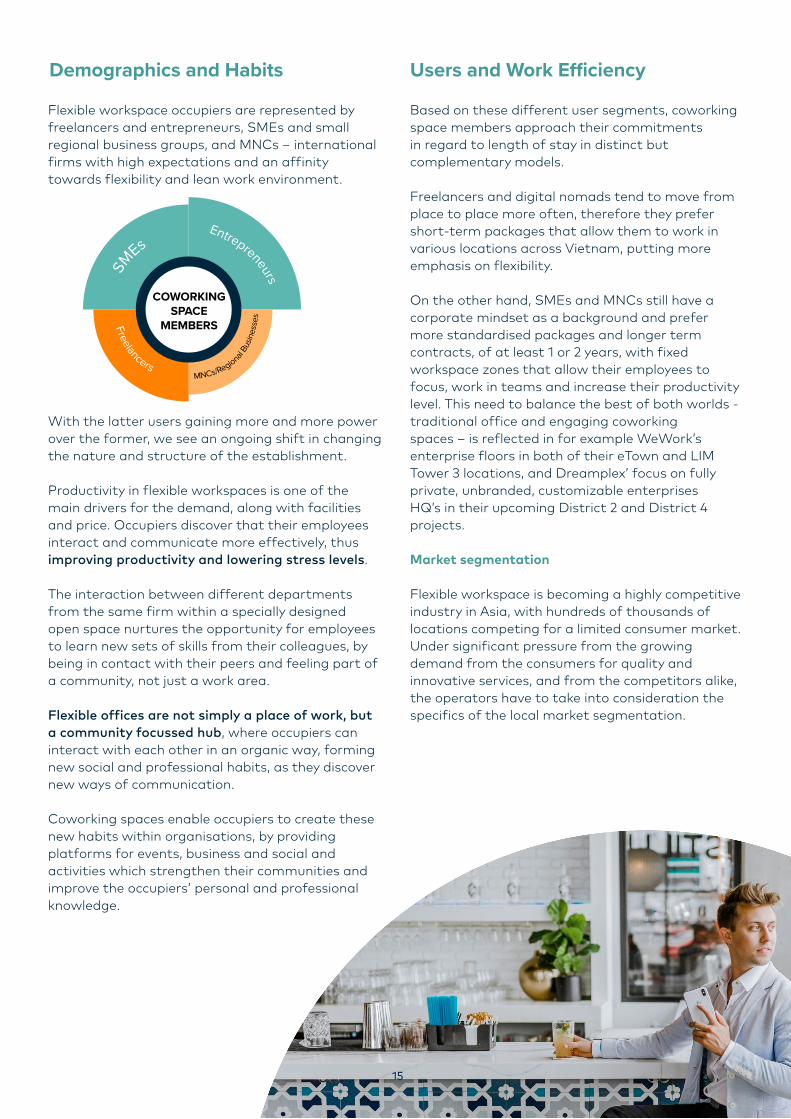

Demographics and Habits

Flexible workspace occupiers are represented by freelancers and entrepreneurs, SMEs and small regional business groups, and MNCs – international firms with high expectations and an affinity towards flexibility and lean work environment.

With the latter users gaining more and more power over the former, we see an ongoing shift in changing the nature and structure of the establishment.

Productivity in flexible workspaces is one of the main drivers for the demand, along with facilities and price. Occupiers discover that their employees interact and communicate more effectively, thus improving productivity and lowering stress levels.

The interaction between different departments from the same firm within a specially designed open space nurtures the opportunity for employees to learn new sets of skills from their colleagues, by being in contact with their peers and feeling part of a community, not just a work area.

Flexible offices are not simply a place of work, but a community focussed hub, where occupiers can interact with each other in an organic way, forming new social and professional habits, as they discover new ways of communication.

Coworking spaces enable occupiers to create these new habits within organisations, by providing platforms for events, business and social and activities which strengthen their communities and improve the occupiers’ personal and professional knowledge.

Users and Work Efficiency

Based on these different user segments, coworking space members approach their commitments in regard to length of stay in distinct but complementary models.

Freelancers and digital nomads tend to move from place to place more often, therefore they prefer short-term packages that allow them to work in various locations across Vietnam, putting more emphasis on flexibility.

On the other hand, SMEs and MNCs still have a corporate mindset as a background and prefer more standardised packages and longer term contracts, of at least 1 or 2 years, with fixed workspace zones that allow their employees to focus, work in teams and increase their productivity level. This need to balance the best of both worlds - traditional office and engaging coworkingspaces – is reflected in for example WeWork’s enterprise floors in both of their eTown and LIMTower 3 locations, and Dreamplex’ focus on fully private, unbranded, customizable enterprisesHQ’s in their upcoming District 2 and District 4 projects.

Market segmentation

Flexible workspace is becoming a highly competitive industry in Asia, with hundreds of thousands of locations competing for a limited consumer market. Under significant pressure from the growing demand from the consumers for quality and innovative services, and from the competitors alike, the operators have to take into consideration the specifics of the local market segmentation.

COWORKING SPACE

MEMBERS

Entrepreneurs

SM

Es

MNCs/Regional B

usin

esse

s Freelancers

15

16

91%

COWORKING SPACE MEMBERS

Under age 35 Others

As the demand curve elevates, the market will see competition heating up, challenging operators to provide an even more innovative workplace to get ahead of their competitors and win market share. A large percentage of the flexible workspace user market share is represented by small businesses with relatively young workforce, who are seeking access to a new type of workspace. A new community spirit connects them together under a similar growth culture and set of values, where entrepreneurs and young businesses can compete togethear and thrive together, in a modern, open work environment.

A study by CBRE Research Vietnam found that 91% of co-working space members are millennials, i.e. under the age of 35.

The young workforce - Generation Z and millennials are eager to work in creative environments, surrounded by like-minded change-makers, enabling them to leverage opportunities to discover, connect, collaborate in new ways. With the smaller businesses catered to, operators focus extensively on supporting the MNCs growing expansion.

The old ‘status-quo’, where coworking spaces were dedicated and created to serve freelancers, part time workers and small businesses that cannot afford a traditional office, is not just challenged, but completely overhauled from the ground up. Large corporations are moving their traditional workspace to take advantage of the robust market which holds record low vacancy rates across A & B grade stock. Regional and global flexible workspace operators have an opportunity to enter the market, fuelled by increased demand from multinational companies and supported as well by low vacancy rates in traditional workspace.

In 2020 Vietnam achieved a 2.91% growth, and has become one of the most sought out investment locations in Asia and throughout the world. Though undertaking foreign investment in Vietnam, MNCs continue to grow aggressively and face difficulties in finding space for their workforce and projecting an accurate employee growth count.

Under these structural and social market preconditions, coworking spaces become the natural, immediate and most flexible solution for many large investor groups, allowing them to expand their business and workforce count with much more elasticity compared with traditional office space.

9%

17

Availability and Supply in Prime City HubsRelatively new in the office supply market, coworking spaces gradually became a mainstream alternative to traditional offices and developed rapidly due to the high demand from enterprises and supported by the Vietnamese economic growth.

Following the global trend, more and more flexible office spaces are opened in Vietnam, especially in the two central hubs Ho Chi Minh City and Hanoi. The graphs illustrating the coworking space market A & B supply from Cushman & Wakefield express the remarkable development of flexible workspace market in the two biggest cities in Vietnam: Ho Chi Minh City and Hanoi.

In the end of 2020, Ho Chi Minh City had 74,961 total square meters area supply of coworking spaces in grade A & B building. The city supply has experienced a significant increase since 2017 and is forecasted to keep on expanding to 81,961 square meters area in 2021 – more than 6 times the supply in 2017.

Major Openings and Key Operators

The coworking space market in Vietnam has expanded consistently in recent years and not only major local operators like Toong, UPGen, Circo, and Dreamplex, but the number of small operators with just only one venue like Leopalace21, Vuong Tron Giac, Spiced are also increasing considerably.

Wework is one of the dominant global providers in the market and they are consistently increasing their footprint in Southeast Asian countries like Vietnam, Singapore, Malaysia and Thailand. In 2020 however, Wework took a more careful approach in their expansion in Ho Chi Minh City with opening at Lim Tower and closing Sonatus.

Due to the Covid-19 outbreak, several flexible office operators are deferring their new location opening and are waiting for stabilisation around the region. Along with challenges, opportunities arise as well, enabling the well-established providers to take advantage of the market slowdown and seek to acquire smaller coworking spaces that are under pressure.

However, some operators have focused on growth as their key strategy based on large amounts of customer demand. Dreamplex continues to reinforce their position in the market with a new location in Thao Dien, District 2, Ho Chi Minh City opened at the beginning of 2021. It is expected to open another 3 further locations in late 2021 across District 1, 2, and 4.

020,00040,00060,00080,000

100,000120,000140,000160,000180,000

2017 2018 2019 2020 2021(F)

Coworking Market, A&B Supply (sqm)

HCMC Hanoi

COWORKING MARKET - A&B SUPPLY (TOTAL M2 AREA)

Along with Ho Chi Minh city, coworking space supply in A & B buildings in Hanoi has also grown from 27,896 to 75,686 square meters in the period of 2017 to 2020. In 2021, Hanoi coworking supply is predicted to rise to 82,686 square meters in total area due to the continuing high demands.

17

18

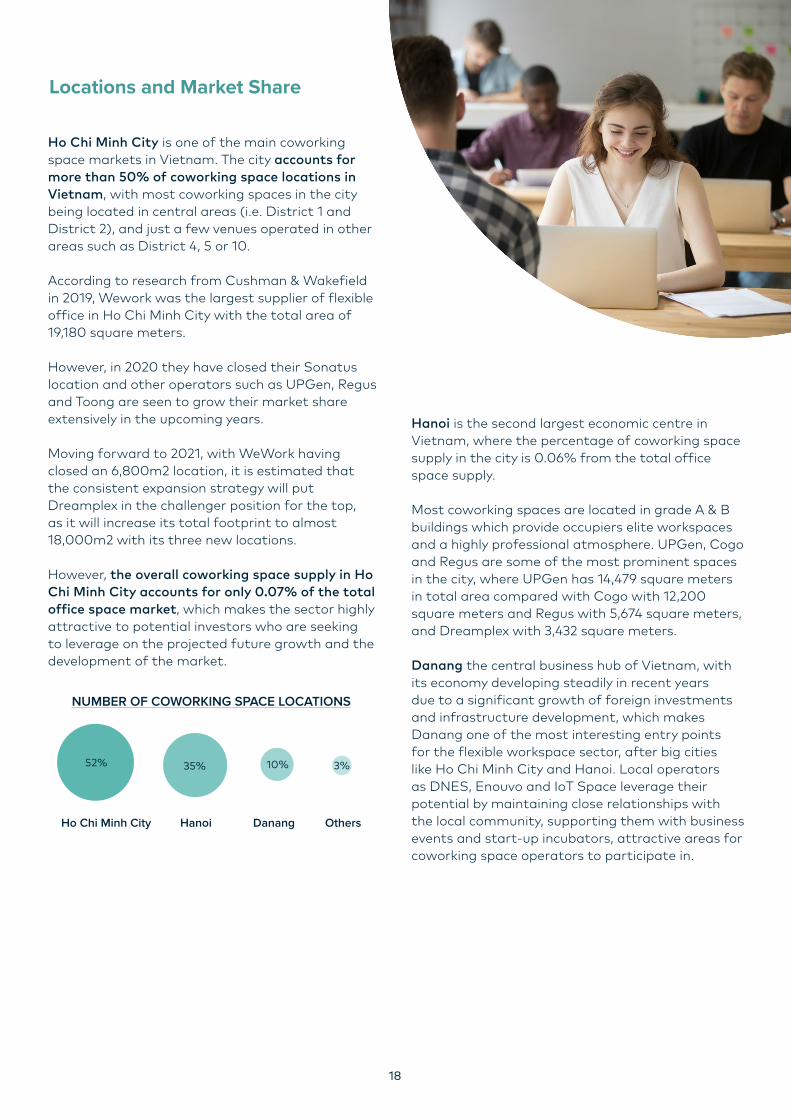

Ho Chi Minh City is one of the main coworking space markets in Vietnam. The city accounts for more than 50% of coworking space locations in Vietnam, with most coworking spaces in the city being located in central areas (i.e. District 1 and District 2), and just a few venues operated in other areas such as District 4, 5 or 10.

According to research from Cushman & Wakefield in 2019, Wework was the largest supplier of flexible office in Ho Chi Minh City with the total area of 19,180 square meters.

However, in 2020 they have closed their Sonatus location and other operators such as UPGen, Regus and Toong are seen to grow their market share extensively in the upcoming years.

Moving forward to 2021, with WeWork having closed an 6,800m2 location, it is estimated thatthe consistent expansion strategy will put Dreamplex in the challenger position for the top, as it will increase its total footprint to almost 18,000m2 with its three new locations.

However, the overall coworking space supply in Ho Chi Minh City accounts for only 0.07% of the total office space market, which makes the sector highly attractive to potential investors who are seeking to leverage on the projected future growth and the development of the market.

Hanoi is the second largest economic centre in Vietnam, where the percentage of coworking space supply in the city is 0.06% from the total office space supply.

Most coworking spaces are located in grade A & B buildings which provide occupiers elite workspaces and a highly professional atmosphere. UPGen, Cogo and Regus are some of the most prominent spaces in the city, where UPGen has 14,479 square meters in total area compared with Cogo with 12,200 square meters and Regus with 5,674 square meters, and Dreamplex with 3,432 square meters.

Danang the central business hub of Vietnam, with its economy developing steadily in recent years due to a significant growth of foreign investments and infrastructure development, which makes Danang one of the most interesting entry points for the flexible workspace sector, after big cities like Ho Chi Minh City and Hanoi. Local operators as DNES, Enouvo and IoT Space leverage their potential by maintaining close relationships with the local community, supporting them with business events and start-up incubators, attractive areas for coworking space operators to participate in.

Locations and Market Share

NUMBER OF COWORKING SPACE LOCATIONS

35% 10%52% 3%

Ho Chi Minh City Hanoi Danang Others

19

4Insightsintooperatorsandmarketentryramifications.

19

20

Cheaper Rent and Lower maintenance fees

One of the essential factors that make coworking spaces an ideal choice for many enterprises is the lower price compared with traditional workspaces. The coworking space operators negotiate long term deals with landlords and design their space using advanced analytics and fit-out planning to optimize the square meter rental yield to the maximum.

Furthermore, enterprises and individuals working in flexible offices do not have to deal with setting up amenities, furniture and office supplies such as printers and lunch areas. Operators undertake these for their occupiers as an added value and offer additional services such as mail services, administrative tasks, office accessories supplies, internet fees and sometimes business processing support.

Demand customization

One of the key benefits of flexible workspaces is the ability to allow a wide range of space customization models, relating directly to the needs of their occupiers. For instance, start-ups and freelance project teams will be satisfied with just small office as they may need more privacy to focus on their work.

IN a market where the competition between traditional and flexible workspace is becoming more and more severe, it is

paramount to understand and further differentiate the core attributes that define coworking spaces.

Where are the strengths in contrast with traditional offices?

When their team will grow, they can expand seamlessly withing the coworking space and take over additional area according to their exact needs. In addition, for freelancers or long-distance employees who don’t work in one permanent place, coworking spaces with a wide regional coverage have created packages to allow their member to access all of their locations under the same contract.

Collaborative environment and community engagement

Within the highly innovative and growing shared-space work model, members can easily find new collaboration opportunities or build new relationships with their peers. Most of the coworking spaces in Vietnam are highly active and organize various community activities and events such as panel discussions, seminars and workshops, leveraging on industry experts and their extensive network to share valuable insights for their occupiers.

Wework was globally one of the forefront promoters of more causal activities which are slowlybecoming a norm, such as Friday after work meet-ups, weekly happy hours, communitylunches and networking activities. Over the past year, these activities have been halted per global WeWork guidelines and events are no longer permitted in the WeWork spaces.

21

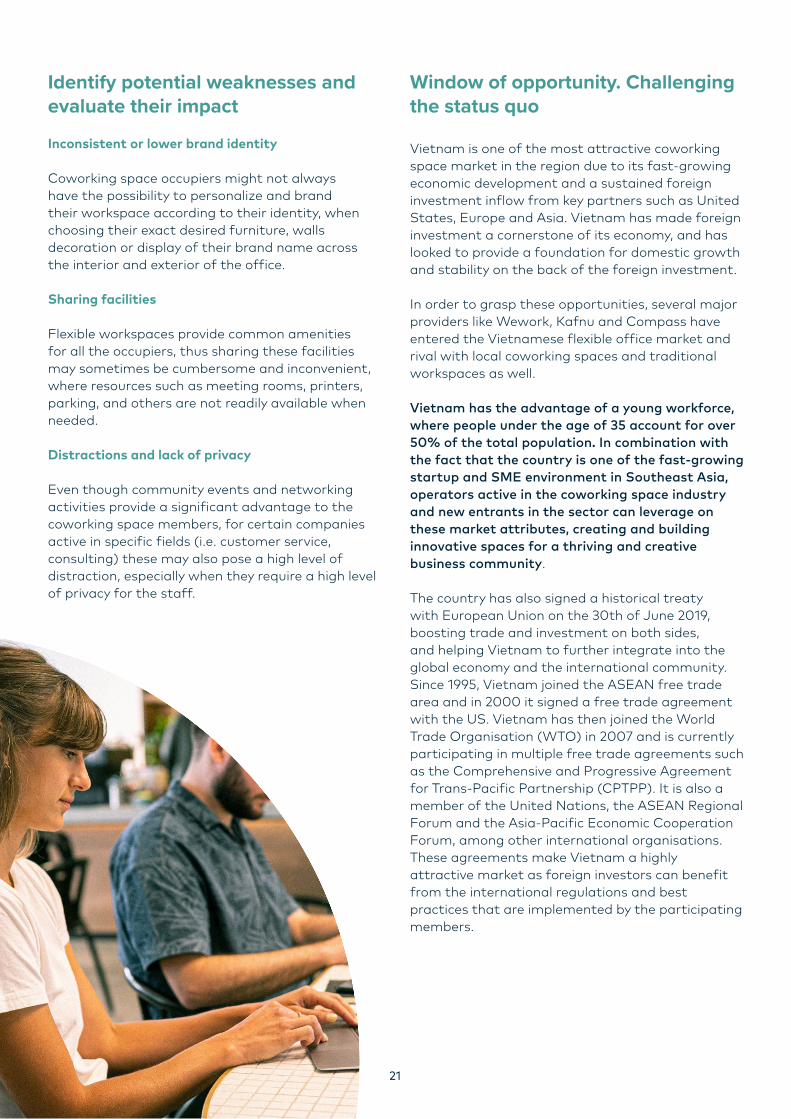

Inconsistent or lower brand identity Coworking space occupiers might not always have the possibility to personalize and brand their workspace according to their identity, when choosing their exact desired furniture, walls decoration or display of their brand name across the interior and exterior of the office.

Sharing facilities

Flexible workspaces provide common amenities for all the occupiers, thus sharing these facilities may sometimes be cumbersome and inconvenient, where resources such as meeting rooms, printers, parking, and others are not readily available when needed.

Distractions and lack of privacy

Even though community events and networking activities provide a significant advantage to the coworking space members, for certain companies active in specific fields (i.e. customer service, consulting) these may also pose a high level of distraction, especially when they require a high level of privacy for the staff.

Vietnam is one of the most attractive coworking space market in the region due to its fast-growing economic development and a sustained foreign investment inflow from key partners such as United States, Europe and Asia. Vietnam has made foreign investment a cornerstone of its economy, and has looked to provide a foundation for domestic growth and stability on the back of the foreign investment.

In order to grasp these opportunities, several major providers like Wework, Kafnu and Compass have entered the Vietnamese flexible office market and rival with local coworking spaces and traditional workspaces as well.

Vietnam has the advantage of a young workforce, where people under the age of 35 account for over 50% of the total population. In combination with the fact that the country is one of the fast-growing startup and SME environment in Southeast Asia, operators active in the coworking space industry and new entrants in the sector can leverage on these market attributes, creating and building innovative spaces for a thriving and creative business community.

The country has also signed a historical treaty with European Union on the 30th of June 2019, boosting trade and investment on both sides, and helping Vietnam to further integrate into the global economy and the international community. Since 1995, Vietnam joined the ASEAN free trade area and in 2000 it signed a free trade agreement with the US. Vietnam has then joined the World Trade Organisation (WTO) in 2007 and is currently participating in multiple free trade agreements such as the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP). It is also a member of the United Nations, the ASEAN Regional Forum and the Asia-Pacific Economic Cooperation Forum, among other international organisations.These agreements make Vietnam a highly attractive market as foreign investors can benefit from the international regulations and best practices that are implemented by the participating members.

Identify potential weaknesses and evaluate their impact

Window of opportunity. Challenging the status quo

22

Alongside opportunities, investors should be aware of the macro-economic and socio-cultural challenges that govern the business environment in Vietnam and the flexible workspace sector.

Investment and legal challenges

Apart from the commercial aspect, operators and especially foreign investors, should be aware of the compliance and regulatory conditions specific to the real estate sector, and make sure they are in line with the authorities expectations in respect to licensing requirements and corporate governance.• The process to establish a foreign enterprise in

Vietnam can be somewhat different to other jurisdictions, with the terms used and specific requirements often confusing or difficult to interpret.

• Prior to the end of 2020, operators were required to commit a minimum charter capital of VND20 billion (equivalent to USD 805,702) which needed to be identified based on the contributed capital on the Investment Registration Certificate, and charter capital on the Enterprise Registration Certificate; However, under the provisions of the new Law of Investment, investors in real estate are not restricted by this minimum capital requirements, which has been removed to further promote market growth;

• Operators must implement a project plan and submit it with the authorities for approval. This condition may be more lenient for local investors, however foreign investor are required to undertake a project assessment plan at the initial stage of the incorporation and market entry process; and

• Requirements in terms of premises and location conditions

At the end of this chapter we will delineate and emphasize the provisions and regulatory requirements for foreign investors seeking to enter the coworking space sector in Vietnam.

Macro Implications and Barriers to Entry

The relative political and economic stability, together with legislative processes to encourage foreign investment (whilst still protecting domestic and state enterprises), have enabled foreign investment to grow across a broad range of sectors and locations. Vietnam has also benefited from political and economic instability of other economies in Asia in recent years, with Vietnam continuing to provide a credible investment destination.

Vietnam is in top 50 countries worldwide by ‘coworking space growth per capita’, however the number of coworking spaces in the market is still considerably lower compared with top countries like Singapore, Hong Kong, Malaysia. This situation means that Vietnamese coworking space market still has plentiful spaces to grow Under these preconditions, the are obvious business considerations for investors to look into and consider the coworking space market in Vietnam, where there are clear signs for rising demand, low supply and growth opportunities.

joined the ASEAN free trade area

joined the World Trade Organisation (WTO)

1995

2000

2007

2018

2020

2019

signed a free trade agreement with the US

signed to world’s largest commercial treaty: RCEP

signed the CPTPP(Comprehensive and Progressive Agreement for Trans-Pacific Partnership)

signed a treaty with European Union

KEY AGREEMENTS / ORGANISATIONS THAT VIETNAM HAS SIGNED / JOINED TO FACILITATE

FOREIGN INVESTMENT

23

0

8

16

24

32

40

0

500

1000

1500

2000

2500

2016 2017 2018 2019 2020

HCMC Office Market

Leased Vacant Gross rent

Economic environment and sectorial limitations

In the current Vietnamese real estate market environment, the vacancy rate in central hubs like Ho Chi Minh City and Hanoi is limited, which makes it difficult for coworking space operators to find appropriate, available locations when deciding to enter the market.

(thousand m2)

(thousand m2)

(USD/m2)

(USD/m2)

HO CHI MINH CITY OFFICE MARKET

HANOI OFFICE MARKET

The above charts with data on occupancy illustrate the small percentage of available space compared with leased space in Ho Chi Minh City and Hanoi, thus consequentially finding a suitable location is one of the substantive challenges for operators setting up coworking spaces in Vietnam.

In addition, the Covid-19 epidemic has affected the Vietnamese economy and the coworking space sector, which had a setback when the authorities advised businesses to adopt the work from home model and social distancing provisions in April 2020.

With many employees working from home, coworking space operators faced a dilemma: continue their expansion and focus on growth, to meet the projected demand of the market in the upcoming years, or take a moment to rethink their strategy, pause the growth cycle and focus on improving the interior and design areas, to make the more attractive to the current customers.

Social and cultural environment

As the coworking space industry is viewed as a new, growing trend in Vietnam, even though the demand is increasing consistently, the number of spaces per capita in the country is still significantly lower compared with regional peers Singapore, Hong Kong, Malaysia etc. Consequently, the consumer awareness of the concept is still moderate, as the majority of young Vietnamese citizens are culturally habitual to use coffee shops as their work and study venues, which makes it difficult for coworking spaces to attract new occupiers in the short term.

0

8

16

24

32

40

0

500

1000

1500

2000

2500

2016 2017 2018 2019 2020

Hanoi Office Market

Leased Vacant Gross rent

24

Direct and indirect competition

Global operators such as Kafnu and Compass have increased competition in Vietnam, with massive investments in grade A locations in Ho Chi Minh City and Hanoi, and with expansion plans ready to take off as soon as the pandemic signs of recovery are in sight. Due to the limited availability in major hubs, flexible workspace owners have to find solutions that will enable them to continue their expansion and development, and in the same time create an efficient market strategy to compete for the available locations.

Vietnamese coworking space market is one of the most dynamic and innovative industries, with a significant growth potential and profitability.To leverage on this growing trend, coworking space operators have to find and express their unique value proposition, ensuring they stand out from the norm and are ahead of their competitors.

The vast majority of the Vietnamese working class are used to work in traditional corporate offices, coffee shops, universities and public libraries. The cultural and historical characteristics of the labour capital in Vietnam echoes in the flexible workspace market, where operators have to compete not just with traditional offices but also with a variety of indirect, unconventional providers.

Where authenticity and innovation play a cornerstone role in today’s extremely dynamic market, operators have to create their own specific competitive strategies to set themselves and their occupiers apart from apart from other types of workspaces.

Competing Against Each Other or Thriving Together?

For Dreamplex,

Dreamplex believes they will compete with traditional office spaces by bringing them into “abetter office building”.

There’s a reason why companies like traditional offices. They provide a professional look, give full privacy, and are a place to bring the company brand and culture to life. What we are doing with our new locations is to combine those qualities with the attractiveness of a coworking space: a vibrant environment, well-designed spaces, lots of choice to fit every personality and working style, and a rich program of employee experience activities. Your private office then just happens to be within this lively, exciting campus that your employees love going to.

Different is better?

Mirroring their client’s personas, needs and values, coworking spaces in Vietnam shape their environment, culture and services to match their direct audience.

The layout and decoration is one of the essential elements, however it is not the benchmark for constructing a successful market positioning and brand. Most operators agree that the coworking space is beyond the workspace itself, which only provides for its members a physical location, coffee and Wi-Fi. What is more important is the specific culture of the environment, which becomes the cornerstone of each unique value proposition.

As a result, operators leverage on their own, particular competitive advantage to attract occupiers in their physical space and community network. Their focus is not only to increase the number of occupiers but also to enhance the service quality and the additional benefits for the members, so that the client retention value is consistent, based on genuine loyalty.

“The biggest reason why companies still pay for an office is because when done right, it can bea strategy tool to attract, engage, and retain the best talent. We design and deliver engagingworkplaces that create ‘a Better Day at Work’ for the employees of medium and largecompanies in Vietnam.” explains Dreamplex. They differentiate their “outsourced workplaceexperience” service through 3 core pillars:

(i) “Private, Branded Offices: starting in 2021, Dreamplex locations are very lightly branded.Instead, the occupier’s logo and brand are central. For guests visiting those companies, there are little cues the company is housed in a flexible office – other than from the vibrant ground floor that oozes energy and excitement. Gone too are the long corridors of glass walls that provide no privacy. Instead, offices are as private as in traditional office buildings, while they’re designed for each company’s specifications, needs, and culture.

(ii) Hospitality-Level Care: as ‘serviced offices’ have become a commodity, Dreamplex elevated its offerings to 5-star care. Their dedicated Member Experience team is trained in hospitality and understands that now more than ever, it’s the human touch which makes the biggest difference. Companies can bring their (large) teams, and leave the daily care to these hospitality experts. This is especially attractive for international companies who don’t have strong local leadership or HR teams present.

(iii) Employee Experience: the office and the great care are just the starting points. Dreamplex has built an Employee Experience team that works directly with large customers like Tiki, Topica, and others to deliver a world-class Employee Experience without any additional HR resources, budget, or time. This includes social events for team-building, creative workshops, training & development, wellbeing programs, and more.

25

26

Market-Share and Expansion Prospects. Timing is critical

Pricing and Forecast

Covid-19 outbreak impacted the real estate market in a significant way, and coworking spaces are seeing the aftereffects of the crisis in their occupancy rates and demand. Many operators’ expansion plans have been put on hold for the moment, as they are concentrating on customer retention, support for affected businesses and improvements in their service offerings.

However, flexible workspaces are considered a cornerstone trend in the real estate industry and the demand will have a consistent growth trajectory, in line with the systemic changes in the way companies and their employees embrace digitalization, innovative work models and a more lean, versatile approach to labour.

In the aftermath of the outbreak, it is expected that many global coworking spaces will enter the Vietnamese market, expand or consolidate their current operations, especially in key locations like Ho Chi Minh City and Hanoi. In the same time, prime local coworking spaces like Toong and Dreamplex will grow their brand with new locations and new services to meet their occupiers’ demands and establish an efficient strategy in line with the growing competition.

As SMEs and multinational companies will continue to shift their attention towards flexible offices, to improve their culture and enhance their staff’s working conditions, operators have to prepare in advance and ready their resources to be able to leverage the demand boost post-Covid-19 and align themselves with the occupiers needs in a timely way.

In Vietnam, flexible workspaces rental fees are overall much lower when compared with Asia Pacific neighboring countries.

Location is one of the key pricing drivers in the market, where flexible offices located in grade A buildings have higher fees than those in grade B, grade C, and obviously the customer segmentation plays a big role as well.

Furthermore, the fees are higher in the main city hubs, with Ho Chi Minh City leading the trend with the highest rental fees in Vietnam. The price varies from VND 1.8million to 9.3million monthly for a desk, with the average price at ca. VND 3million per month for a desk located in a coworking space. Second in line is Hanoi, where the average rental fees per month fluctuates around VND 2million.

In comparison with the two largest cities in Vietnam, the price of flexible workspaces in Danang is more affordable, creating a valuable opportunity for freelancers, start-ups and small entrepreneurs to set up their operations in the coastal city, which has become one of the most sought out hubs for technology related start-ups and digital nomads. A typical high-end price for a desk in a coworking space is VND 2.4million per month and in most cases, the average rental fees are under VND 2million per month.

COWORKING RENTAL FEES FOR A DESK(million VND/month)

1.2 1.21.82 23

2.4

6.5

9.3

0

2

4

6

8

10

Danang Hanoi HCMC

Coworking rental fees

Lowest fee Average fee Highest fee

25

27

The new work culture has lead enterprises to look for new solutions to enhance their staff efficiency and coworking spaces is one of the primary solutions for this approach. The industry has offered several services, customization options and cheaper costs that helps the enterprises to improve their business performance and save their time and money. They have successfully transformed a fixed workplace hierarchy to a more flexibility workspace. It is no denying that coworking space will have a lucrative growth in the workspace industry in the next few years despite the hindrance of the industry due to Covid-19 in 2020.

As Wework explains, “The situation is calling for a refresh in how we rethink and reimagine spaces amidst a changing future of work landscape, and companies need to think about having a holistic approach towards their real estate portfolio. As we navigate the future of the workplace, there is no doubt that the re-entry back to the workplace will require offerings that make us prepared for a post COVID-19 environment. Along with greater emphasis and pressure for professional distancing post COVID-19 and given our presence and close proximity, we have the ability to create a dispersed workspace campus for enterprises and are able to provide alternative and business ready space for business continuity.

Future Growth and Innovation

Given the volatility in the economy and uncertainty regarding business and headcount projections, this is where we see opportunities for enterprises to be more proactive about reassessing their long-term real estate needs. The co-working sector will continue as a relevant partner to the more real estate industry, and such spaces will continue to be in demand as companies rethink their flexible real estate portfolio.

As such, co-working spaces will continue to be an additional resource for companies as we foresee them taking into consideration factors such as resource efficiency, lease flexibility, and mobilization of their workforce in preparation for future unprecedented scenarios.”

Furthermore, Wework states:

As the economic confidence and interest continues to grow in Vietnam, co-working space needs will also evolve to reflect more of what large enterprises want as well. Apart from the agility and flexibility when it comes to leases and operations, they will also focus on cultivating an environment to keep their employees engaged and interested. The physical workspace will be a key element in this and the coworking industry in Vietnam will see a stronger emphasis in design and experiences to support employee engagements and interactions.

27

28

The industry will develop more and more into Workplace Experience as a Service, where companies get more than just the bare office basics. At its heart, this really is a service industry and any offering needs to provide real, differentiated value. Similar to consumers having the choice to end their Netflix or Spotify membership when they repeatedly feel there isn’t much use in it due to lack of new content, in WXaaS customer will come to expect us to deliver them true, continuous, value beyond just the flexible office space. It will therefore be not only a question of scale and price, but a true understanding of SMBs and Enterprise needs – especially in how to use their office as a strategic tool to recruit, engage, and retain talent.

In Dreamplex’s vision,

Coworking spaces will also integrate their technology systems to keep up with the demand of the modern working trends and bring the most flexible environment to their members. The technology in coworking spaces will go beyond performant computers and traditional office utilities like printers, copiers, embracing digital transformation at all levels.

29

Regulatory Requirements and How to Open a Coworking Space in Vietnam

From a legal and compliance perspective, to enter the Vietnamese flexible workspace market, investors need to be aware of certain provisions and requirements. Although there are various restrictions that need to be carefully considered, if the processes are followed through in a compliant manner, operators are able to leverage on the market’s opportunities, start and develop their business successfully.

Under the WTO Commitments, Vietnam did not commit to open the market for foreign investors in real estate trading. However, as stated in Article 3.1 of Law on Real Estate, although the law does not specify leasing flexible office/coworking space as a real estate trading activity, upon the official definition of real estate trading, it is commonly understood that leasing or subleasing coworking space is a type of real estate trading activity.

In addition, Article 11 of Law on Real Estate Trading state the scope of real estate trading conducted by Vietnamese organizations, individuals, overseas Vietnamese or foreign-invested enterprises as below:A Vietnamese organization or individual may conduct real estate trading under following forms:a) Purchase of buildings for sale, for lease, or for

lease purchase.b) Rent buildings for sublease.

Based on these prerequisites, the Vietnamese law allows local and foreign investors to invest in real estate trading sectors, however the scope of permitted real estate trading activities differ case by case.

Business lines

According Decision 27/2018/QD-TTg dated 6 Jul 2018, the appropriate business line for the activity of leasing coworking space/service offices is:

Business lines VSIC CPCTrading of own or rented property and land use rights

6810

What are the conditions?

Apart from the commercial aspect, prior to the end of 2020 investors should also meet certain legal conditions, which may present some entry barriers for new market entrants.

Aside from the requirement to have a formal commercial entity in Vietnam, as described in Article 10.1 of Law on Real Estate Trading, and Article 3.1 and Article 4 of Decree 76/2015/ND-CP, prior to 1 January 2021, investors were required to have a minimum charter capital of VND20 billion, equivalent to USD805,702, which has to be identified in the Investment Registration Certificate(“IRC”) and the Enterprise Registration Certificate (“ERC”). However, under the new Law of Investment, from 2021 the VND20 billion minimum capital requirement is removed, enabling investors to take advantage of the market’s opportunities with much more ease and less restrictions.

Foreign investors are also required to present for approval a “project” at the initial stage of the establishment process, as the licensing authority usually requires the project documentation as a key first step.

Lastly, there are specific provisions regarding the premise of the real estate project. As per Article 9.1 of Law on Real Estate Trading, a building part of the real estate trading market should satisfy the following requirements:• The ownership of the building on land must be

registered in the Certificate of land use right, referred to as Certificate of land.

30

30

• There is no dispute about the land and ownership of the building on land.

• The building is not distrained.

Steps to Register a Foreign Owned Real Estate Trading Company in Vietnam

Assuming the preceding conditions are met, foreign investors are required to conduct two steps in order to obtain their real estate trading business license for renting/subleasing a serviced office space or coworking space in Vietnam. The first step is to register an “investment project”, with this project becoming the initial purpose of the foreign investor’s company. The resulting Investment

Registration Certificate permits the foreign investor to commence the establishment of their company in Vietnam. The IRC is akin to the concept of “Foreign Investment Approval” in other jurisdictions.

The second step refers to the application for the Enterprise Registration Certificate, which shows the business registration information of a company established in Vietnam. This document is akin to the “Certificate of Incorporation” in other jurisdictions.

After receiving the ERC, foreign investors must remit the registered charter capital within 90 days from the date of the ERC issuance.

Each foreign owned company in Vietnam must appoint at least 1 Legal Representative. A Legal Representative of an enterprise is an individual who can exercise the rights and obligations for and on behalf of that enterprise. Generally, only a Legal Representative can sign contracts for the company with other parties, although Power of Attorney’s can be issued to delegate certain powers to others in the organisation.

Step 1 Step 2Application for an

Investment Registration Certificate (the “IRC”)

Application for an Enterprise Registration Certificate (the “ERC”)

IRC ERC

30

31

5Powerof users.Valueandperceptionof occupiers.

31

32

Coworking spaces have become an instrument that businesses leverage on to improve productivity, grow their corporate culture

and create a more inclusive environment for their employees. The concept of being part of a business community, aligning oneself to a common work culture has enabled the workspace transformation to take off, reaching out through a horizontal growth model most of the core, strategic management departments in a business.

Coworking spaces are now suitable not just for freelancers and digital nomads, but due to limitations in office space availability and the competitive real estate market, the demand has shifted to enterprises, especially SMEs and multinationals.

In Wework’s view, the notable trends that play a significant role in the occupier’s decision-making process are:

“Near-term: Business continuity for occupiers• The emphasis on business continuity brought

about by COVID-19 has generated interest from members and non-members on how space-as-a-service plays into their business continuity strategy.

• For occupiers, it’s all about having the scalability and flexibility to address their needs – both operational and regulatory in a timely fashion

• Conversations have also elevated to the discussion of a longer-term and more comprehensive future-proofing business strategy as opposed to just a one-off reaction to the COVID-19 situation

• COVID-19’s impact on the economy also indicates the need for organizations to take on a more conservative approach when it comes to operational needs such as lease flexibility and saving as well as being able to outsource services to drive cost impact and resource efficiency.

Long-term: Shifts in perceptions of a new occupier future• As companies recognize the growing

importance of having flexible workplace arrangements, conversations have also elevated to the discussion of a longer-term and more comprehensive future-proofing business strategy as opposed to reactive measures to the current situation.

• More than ever, there will be a greater emphasis on operational and resource efficiency. Flexible workspaces are proving to be crucial for larger enterprises, given the ability to scale the amount of space needed.

• For many companies, it will be about having the space to scale and mobilise their workforce in situations as such - it is about the ease and convenience for their employees to plug and work.

• As such, large enterprises future-proof operational efficiencies by innovating their global real estate strategy and forging strong partnerships with flexible workspaces”.

32

33

The occupiers play an essential role along with developers and operators in the flexible workspace industry, where their user personas generate different demands and expectations that end up shaping the market as a whole.

The coworking occupiers are divided into two main groups: individuals (i.e. freelancers, digital nomads) and enterprises (i.e. startups, SMEs, and MNCs). The individual occupiers have high price sensitivity and seek to work in a dynamic and collaborate environment so that they can connect and build their relationships with other potential partners or clients.

On the other hand, the enterprise occupiers mostly focus on their privacy and professional environment in which they can boost their staff’s work efficiency and improve their public image. Therefore, although shared - workspace is a trend developing around the world, to adapt and shift from the traditional workspace to a flexible one, most of the enterprises choose serviced offices as the first step.

This approach is confirmed by Toong as well:

Serviced office space rental is still the most profitable service for Toong. The demand in the market is still high, and as our spaces are well designed for customer to establish or expand their business, we are receiving consistent inquiries for serviced studios.

According to Dreamplex:

The demand for a different kind of workplace is now undeniable for SMEs and Enterprises. Millennials and especially Gen Z workers don’t settle any more for the old style of hierarchical, cookie-cutter workplaces. They want a place that offers tons of flexibility. A workplace that they can either spend a morning working from a lounge over a fresh cup of coffee or spend time deeply focusing on their work in their own office. This, alongside phone booths, cozy nooks in sunny spots, bookable meeting rooms, and a range of regular desks, moveable desks and standing desks. There always needs to be something new, which is why having a dynamic environment in which no day is the same is exactly what a new generation of workers’ demands.

Toong demonstrates the growing trend of enterprises shifting towards flexible workspace: “More and more SMEs and MNCs establish their presence in Toong’s spaces; if in the past the number of start-ups used to account for 50% of the premises, today this number is around 30%, while the rest of the occupiers are multinational companies 30%, 10% representative offices, SMEs 20% and 10% freelancers”.

In addition, a new business model emerges according to Toong, where corporations are considering to expand only a part of their office to Toong as an emergency office or complementary space.

The above metrics are in line with the overall industry movements. Within the sector, we can see a moving trend that clearly shows the multinational companies competing for space with startups and SMEs.

The startups and multinational companies recently accounted for more than a half of flexible workspace occupiers in Vietnam, with 30% for each segment and it is expected that the trend will continue to move upwards, fueled by the continuous rise of foreign investments in Vietnam. The data further solidifies the optimistic prospects of the coworking space industry in Vietnam and its potential for growth in the future.

Power of occupiers User segmentation

*based on data from Cushman & Wakefield and specific info from WeWork, Dreamplex, Toong, and Compass.

34

Startups30%

Multinational companies

30%

SMEs20%

Representative Offices20%

FLEXIBLE WORK SPACE OCCUPIERS

34

Marketplace Analysis and the Underpinning for the Future of Work.

6Future

of workand

the keyrole

of flexibleworkspace.

34

Over the next years, the digitalization and automatization of work will continue to expand, becoming a key part in changing

the status quo of work models, culture and workplaces alike.It is expected that not only the demand for technological skills will grow, but the need for emotional, cultural, social intelligence skills will flourish, bridging the gap between technology and social interaction.

Within this framework, the flexible workspace and coworking industry plays a cornerstone part, enabling technology, digitalisation and social engagement to coexist and complement each other in a common, efficient multi-functional space.

Traditional workspaces are in a process of redefining their identity, where the main change drivers are digital transformation, remote and lean work models. Employees demand flexibility, social engagement and community benefits, and years from now flexible workspaces will become the norm.

Supported by a consistent foreign investment flow, a young, agile workforce and a booming economic development, Vietnam is one of the most attractive markets in the region for international investors and operators looking at the flexible office space sector.

The growth potential is further confirmed by the relatively low market penetration of the coworking spaces versus traditional offices, enabling international providers to consolidate their positions and solidify their presence in Vietnam.

Under the impact of Covid-19 on the market, according to Wework, “given the volatility in the economy and uncertainty regarding business and headcount projections, this is where we see opportunities for enterprises to be more proactive about reassessing their long-term real estate needs. The co-working sector will continue as a relevant partner to the real estate industry, and such spaces will continue to be in demand as companies rethink their flexible real estate portfolio”.

Post Covid-19, the real estate market in Vietnam is expected to speed up its transformation and create the underpinning for the flexible workspace to become an industry standard alongside traditional offices, with a significant pivot on wellness, mobility and community engagement.

Vietnam’s Market Positioning

35

ResearchReference

&Engagement

Team.

36

Data and metrics were corroborated in partnership with Cushman & Wakefield, a global real estate company focused on guiding our clients with strategic insights and innovative solutions.

Research References

In addition, Wework, Dreamplex and Toong also have provided valuable information and specifics.

Additional research references below:• The World Bank• Coworking Resources• Statista• General Statistics Office of Vietnam• Vietnam Investment Review

37

Engagement Team

VLAD SAVINHead of Business Development | Acclime Vietnam

Vlad is a business development and marketing professional, who has resided in South East Asia for the last 7 years. He has wide experience in personal finance and corporate servicing, working with investment firms in Malaysia and Vietnam, while having a strong background in marketing, client service and events with international exposure. Vlad has been developing Acclime’s business strategy and growth, organizing and creating seminars and workshops for the foreign and local investor community in Vietnam, while assisting with client relationships and the overall brand positioning of the firm. Vlad graduated from Spiru Haret University in 2006 with a Bachelor of Marketing and International Relationships.

Email: [email protected]

MATTHEW LOUREYManaging Partner | Acclime Vietnam

Matthew is a qualified accountant who has resided in Vietnam for over 16 years. He has extensive experience working in Australia for Big 4 accounting firms and investment funds, and since Matthew relocated to Vietnam he has spent much of his time advising foreign investors on successfully undertaking business in Vietnam, corporate investment transactions, market entry and corporate finance. He also currently sits on a number of boards in Vietnam, advising as an independent non-executive director.

Matthew graduated from Monash University in 1994 with a Bachelor of Commerce and qualified as a Chartered Accountant in Australia in 1997.

Email: [email protected]

If you have any questions regarding this study, please don’t hesitate to contact us

38

ACCLIME VIETNAM

Ho Chi Minh City: Level 9, Lim Tower 329A Nguyen Dinh Chieu, District 1

Hanoi: Level 13, Hanoi Tower49 Hai Ba Trung, Hoan Kiem District

Level 9, A Chau Building24 Linh Lang, Ba Dinh District

Danang: Level 3, Indochina Riverside Tower74 Bach Dang, Hai Chau District t. +84 (0)28 3535 8200 e. [email protected]

vietnam.acclime.com

![[FR] [Coworking] Sonorisez vos espaces de coworking avec Tracktl](https://img.pdfslide.net/doc/110x75/55b3ad8fbb61ebd7568b4690/fr-coworking-sonorisez-vos-espaces-de-coworking-avec-tracktl.jpg)